Abstract

Purpose

Cryptocurrency’s novelty and volatility—combined with the absence of standardized reporting prior to 2023—created an opaque information environment. This study explores whether such conditions enabled assertive impression management in corporate reporting. We examine how firms not only varied the volume of cryptocurrency disclosures over time, but also strategically manipulated their readability. Additionally, we use this context to demonstrate the utility of machine learning and natural language processing tools for consistent analysis of complex financial narratives.

Study design

We analyze full-text annual reports, MD&A sections, and proxy statements from five publicly traded U.S. firms with diverse cryptocurrency involvements. Our methodology includes machine learning-based topic modeling, readability assessment using standardized indices, and visualization tools.

Findings

(i) Information Demand: Google search trends for target firms are strongly associated with Bitcoin price movements, reflecting external attention cycles. (ii) Impression Management: Firms increase both the frequency and readability of crypto disclosures in favorable markets and reduce or obscure them in downturns, consistent with strategic impression management. (iii) Readability: Crypto-related disclosures are significantly more readable than non-crypto sections from the same reports suggesting deliberate simplification.

Contributions

This study advances the limited literature on cryptocurrency disclosure by offering a textual and behavioral lens on corporate impression management. A key contribution is the integration of readability metrics, public attention signals, and NLP tools into disclosure analysis. We highlight how firms use both narrative framing and readability engineering as tools to influence perception—especially in periods of regulatory uncertainty.

Implications

Our findings have direct implications for policy and practice: (i) Policymakers should consider not only disclosure quantity but also its linguistic clarity and comparability, especially for volatile assets. (ii) Investors and analysts can use automated text analysis to detect subtle impression management tactics and to interpret the strategic use of clarity in disclosure narratives.

Keywords

Introduction

The use of cryptocurrency by public companies and related disclosures has been shrouded in complexity. Prior to the issuance of FASB ASU 2023-8, Accounting for and Disclosure of Crypto Assets, on Dec 15, 2023 (effective for fiscal years beginning after Dec 15, 2024), there was little guidance on corporate cryptocurrency reporting. The novelty, proliferation, and price volatility of digital assets created strong demand for clearer disclosures, with 85% of respondents in the FASB’s (2021) Invitation to Comment emphasizing the need for standards on digital assets accounting.

The strong demand for accounting guidance stemmed from the opacity of voluntary cryptocurrency disclosures. Luo and Yu (2022) and Anderson et al. (2024) highlight that firms employed varied and inconsistently applied accounting treatments for cryptocurrency activities, complicating financial statement analysis. This inconsistency increased stakeholder reliance on narrative disclosures in financial reports. Accordingly, this study examines both financial and non-financial cryptocurrency disclosures in the opaque pre-2023 environment.

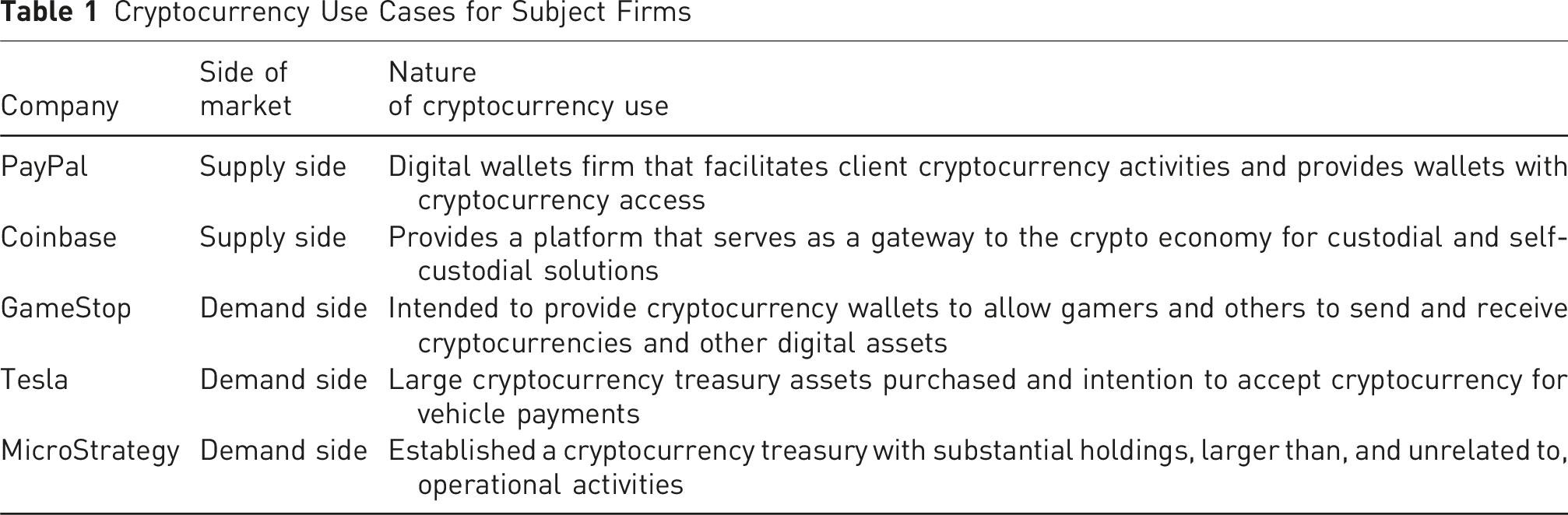

Corporate cryptocurrency involvement was minimal before 2018 but saw significant growth around 2020, as noted by Anderson et al. (2024). Firms adopted cryptocurrencies as a medium of exchange and a store of value, driven by diverse motivations. On the demand side, some held cryptocurrency as treasury assets or used them for payments to meet customer demand, to be competitive with other firms accepting cryptocurrency payments, or to reduce transaction costs. Others incorporated cryptocurrency into their operations, such as for gaming platform prizes, where cryptocurrency holdings functioned as a sort of operational inventory.

On the supply side, organizations provided financial services, operated exchanges and offered investment advisory and account management services. Some also supplied or mined cryptocurrencies by solving complex algorithms. To capture this diversity, we analyze the 2018–2022 disclosures of five publicly traded U.S. firms with diverse cryptocurrency involvements: PayPal and Coinbase (on the supply side) and MicroStrategy, Tesla, and GameStop (on the demand side).

Our analysis of corporate cryptocurrency disclosures extends beyond financial statements and notes to include related textual disclosures in SEC regulatory filings. While formal accounting and disclosure rules are critical, such “storytelling” often provides deeper insights into the potential impact of cryptocurrency involvement on future corporate earnings and cash flows. 1

Corporate storytelling occurs through various mediums. For example, Stratopoulos et al. (2022) examined blockchain adoption using diverse corporate disclosures and indicators, including google trends, book titles, news articles and public companies regulatory fillings (S-1, 10-K, and 8-K). Similarly, we employ Google Trends analysis to assess the demand for, and supply of, crypto-related information by our subject firms, complementing our analysis of their regulatory filings.

To assess the complexity and communicative intent of regulatory disclosures by our representative firms, we apply established readability indices that are particularly relevant for analyzing highly intricate or strategically crafted texts. Following Gunning (1952), Coleman and Liau (1975), Mc Laughlin (1969), Flesch (1948), and Kincaid (1975), we use the Gunning Fog Index, Coleman-Liau Index, SMOG Index, Flesch Reading Ease Index, and Flesch-Kincaid Grade Level Index. These measures indicate that overall disclosures are consistently complex, requiring university or graduate-level reading skills. However, a key contribution of this study is our paired-sample readability analysis, which reveals that, on average, cryptocurrency-related sections are significantly more readable than non-crypto sections within the same reports.

Yet, this readability advantage is not consistent across time. Our longitudinal analysis reveals an opportunistic pattern: firms tend to emphasize cryptocurrency involvement—and do so using simpler, more readable language—when market conditions are favorable. During downturns, however, crypto disclosures are often reduced or omitted, and the language becomes notably more complex. This suggests that firms may strategically adjust both the presence and tone of crypto disclosures, using readability as a tool to project transparency in optimistic periods and obscure risk when sentiment sours.

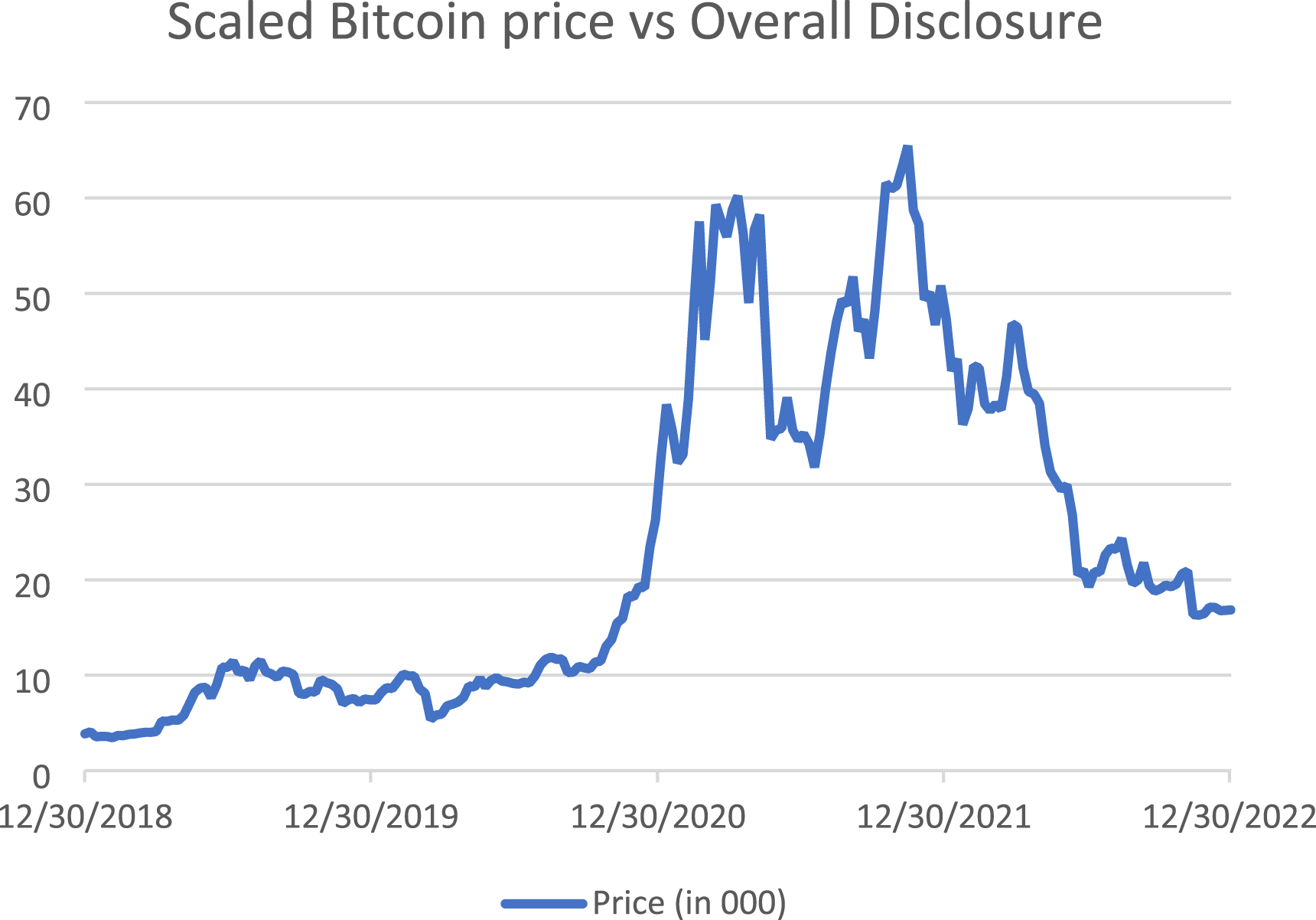

Our sample period is marked by extreme cryptocurrency market price volatility. As illustrated in Figure 1, Bitcoin’s price surged to nearly $70,000 in November 2021, only to plummet below $17,000 by November 2022, a dramatic downturn commonly referred to as the “crypto winter”. Companies that had expanded their cryptocurrency activities before this market crisis faced intense value fluctuations and substantial, often unrealized, losses on their cryptocurrency holdings. Bitcoin Prices 2018–2022 Sample Period

This environment provides a compelling opportunity to explore assertive impression management in corporate reporting (Albuquerque et al., 2023). During turbulent times, companies may engage in strategies to enhance their public image and reassure shareholders. While such practices have been studied in other contexts, such as the global financial crisis (e.g., Yang & Liu, 2017), they remain underexplored in the context of cryptocurrency market volatility.

Existing literature on cryptocurrency disclosures is limited, focusing on adoption, accounting practices, and auditing. We contribute by applying machine learning and data visualization methods to corporate regulatory filings, efficiently identifying key text priorities (Luo, 2021; Sanchez-Pi et al., 2014). Our data-intensive approach allows a detailed examination of specific companies, though the analysis is limited to a small number of representative firms.

We examine how companies’ disclosures evolve as both their cryptocurrency activities and cryptocurrency market conditions change over time. When cryptocurrency was novel and prices were rising, firms disclosing cryptocurrency involvement in their 8-Ks experienced positive abnormal stock price effects—similar to those experienced by technology companies in the dot-com era—according to Cheng et al. (2019). This gave firms strong incentives to disclose crypto involvement under favorable market conditions. In contrast, as market conditions worsened, firms deemphasized their involvement, sometimes obscuring disclosures (Powell, 2021), aligning with impression management via minimum narrative disclosure (Leung et al., 2015). Based on assertive impression management strategies (Cooper & Slack, 2015), we argue that firms strategically modulate both the presence and the readability of their cryptocurrency disclosures to influence investor perception.

This study contributes to the emerging literature on corporate cryptocurrency disclosures by examining how firms adjust their disclosure practices in response to evolving market conditions and corporate involvement. While our paired-sample readability analysis shows that, on average, cryptocurrency-related sections are more readable than non-crypto disclosures, our longitudinal analysis reveals that this readability advantage is not constant. Instead, an opportunistic pattern emerges: firms tend to emphasize cryptocurrency involvement—and do so in more readable language—when market conditions are favorable, while obscuring or reducing such disclosures during downturns, often using more complex language. These behaviors align with established theories of impression management, where narrative disclosures are selectively crafted to enhance public image and mitigate stakeholder concern. We situate this analysis within the broader literature on disclosure strategy during periods of financial uncertainty and regulatory ambiguity.

In doing so, we also demonstrate the value of underutilized machine learning-based textual analysis and data visualization tools for the study of complex financial and non-financial disclosures. These methods allow us to uncover patterns and shifts in narrative content that would be difficult to detect through traditional qualitative or manual approaches. Together, these methodological tools and theoretical insights enable us to address two key research questions: (1) How do public companies’ cryptocurrency disclosures evolve in response to changes in market conditions and corporate involvement? (2) How can readability metrics and machine learning–based textual analysis reveal new forms of impression management in financial disclosures?

A Primer on Cryptocurrency Development and Common Uses

Cryptocurrencies such as Bitcoin are digital currencies verified through a decentralized cryptography system. Early attempts at digital currencies, as described by Haber and Stornetta (1991), only succeeded with the advent of Blockchain technology (BCT), originally designed for document time stamping. While BCT has many corporate applications beyond cryptocurrency, such as production and internal accounting, it underpins cryptocurrency by enabling consensus mechanisms and immutable transaction records (e.g., proof of work). BCT also facilitates “smart” contracts to execute actions based on predefined conditions.

Bitcoin, the most popular cryptocurrency, was first mined in 2009 (Grant & Hogan, 2015). Unlike fiat currencies, cryptocurrencies function without government or central bank involvement, relying only on market acceptance. In some cases, such as in El Salvador, they have even been declared legal tender. Cryptocurrency challenges traditional financial intermediaries’ roles.

We focus on cryptocurrency as a transaction mechanism, though other types exist, including utility and security tokens (Hardle et al., 2020). The rise of cryptocurrencies and Decentralized Finance (DeFi) is driven by their ability to solve inefficiencies and flaws in traditional finance, such as opacity and centralized control (Harvey et al., 2021). Cryptocurrencies can offer faster transactions and lower costs, exemplified by Bitcoin’s reduced foreign exchange transfer fees (Foley et al., 2019; Kim, 2017).

Cryptocurrency values are highly volatile, often described as “bubble like” (Enoksen et al., 2020). Bouri et al. (2018) argue that this volatility hinders the potential for cryptocurrencies to serve as a stable payment medium. Cryptocurrencies are also traded on exchanges, with derivatives and ETFs emerging as investment options (Akyildirim et al., 2020; Alexander et al., 2022; Ali et al., 2020). Bitcoin Futures began trading in December 2017 on the Chicago Mercantile Exchange (CME) and on the Chicago Board Options Exchange (CBOE) (Winkel & Hardle, 2023).

Cryptocurrency Risks

While cryptocurrencies present opportunities, they also carry significant risks and costs for corporate users. Liu et al. (2022); Liu & Tsyvinski (2021) link cryptocurrency price volatility to investor overreaction, attention-driven momentum, and bad actors engaging in schemes like “pump and dump”, exposing users to significant risks and manipulations. 2 Beyond price stability issues, corporate cryptocurrency users face technological vulnerabilities such as hacks, thefts and data breaches (Castonguay & Stein Smith, 2020; Lewis et al., 2017), as well as internal control challenges. 3 Grant and Hogan (2015) suggest mitigating these risks by immediately converting accepted cryptocurrency into traditional currency to avoid direct holdings. Many firms accepting cryptocurrency use intermediaries, such as apps (e.g., SPEDN), gift cards (e.g., CoinCard) or PayPal, to minimize disclosure and reduce the risk of exposure to possible illicit client activities like money laundering or tax evasion.

Auditing cryptocurrency also involves complexities, such as verifying asset existence, ownership, and valuation, resulting in higher audit fees, increased auditor turnover, and frequent accounting restatements (Cheng et al., 2023; Vincent & Wilkins, 2020).

Background and Context

Corporate engagement with cryptocurrency has increased markedly over the past decade, introducing new challenges for financial reporting and stakeholder interpretation. Initially used by a limited number of tech-focused firms, cryptocurrencies have evolved into both a speculative investment vehicle and an operational asset for diverse sectors. Firms have held cryptocurrencies as treasury assets, used them in transactions, integrated them into customer incentives, or provided crypto-related financial services such as trading platforms, advisory services, and mining operations. This distinction between financial (e.g., treasury holdings) and operational (e.g., transactional or platform-based) uses may influence how—and why—firms choose to disclose cryptocurrency involvement.

This growing involvement has unfolded in an environment of regulatory ambiguity. Until the issuance of the FASB’s Accounting Standards Update (ASU) 2023-08, there was little authoritative guidance on the accounting and disclosure of crypto assets. In its 2021 Invitation to Comment, the FASB noted that 85% of respondents supported clearer standards for digital assets—highlighting widespread concern over inconsistent and opaque disclosure practices.

The lack of formal rules has resulted in significant variation across firms in how cryptocurrency activities are reported. Disclosures have often been voluntary, narrative-based, and embedded within broader filings such as 10-Ks, 8-Ks, and MD&A sections. This narrative form increases reliance on textual disclosures, which are susceptible to impression management and subjective framing. At the same time, the cryptocurrency market has exhibited extreme volatility. For instance, Bitcoin rose to nearly $70,000 in November 2021 before plummeting below $17,000 by November 2022. Such fluctuations create further incentives for firms to manage investor perceptions through strategic disclosures.

This study is situated within this complex and evolving landscape. We analyze how firms disclose their cryptocurrency activities in the absence of mandatory standards, particularly during periods of high market volatility. Our focus is not only on what is disclosed, but also how—examining patterns in volume, tone, and complexity over time using machine learning and text analysis tools.

Methodology

In this section, we first describe the nature of cryptocurrency involvement for the subject companies, including PayPal, Coinbase, MicroStrategy, Tesla and GameStop, based on their reported financial data. Given that corporate cryptocurrency involvement varies over time, we conduct analyses over multiple years. As more firms entered the cryptocurrency space, related disclosures increased. Anderson et al. (2024) identify 2020 as a key year when institutional and corporate investors began allocating portions of their portfolios to cryptocurrency assets, whereas prior to 2020, most firms had only limited cryptocurrency involvement.

A detailed, step-by-step description of our text analysis and visualization procedures—including preprocessing, topic modeling, and readability assessments—is provided in Online Appendix – Part I.

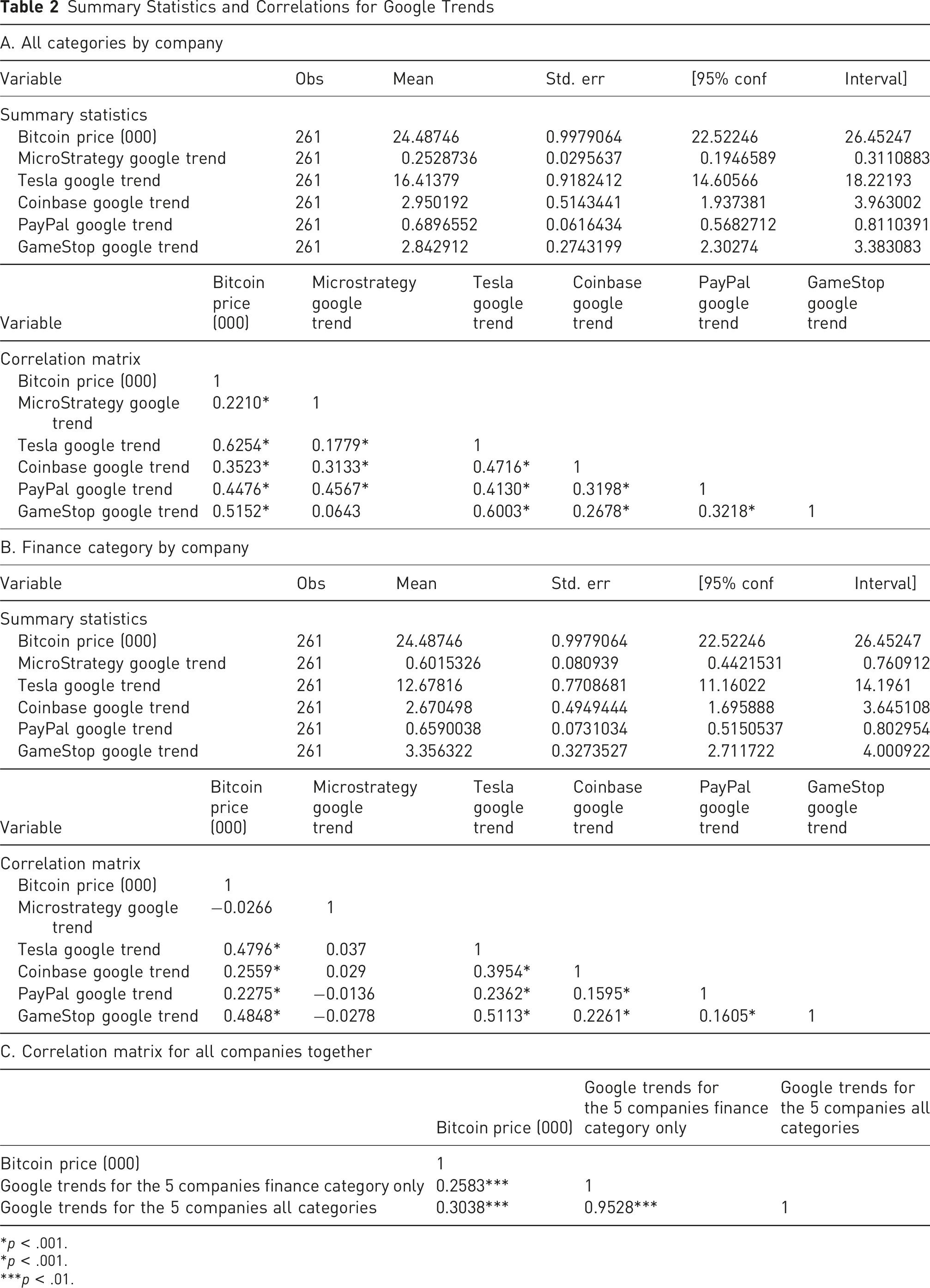

We begin by assessing the demand for information about these firms over 2018-2022, finding that it is positively influenced by cryptocurrency market conditions. To do this, we use Google Trends analysis, similar to prior studies that employed this technique to gauge public interest in cryptocurrency-related assets (e.g., Aslanidis et al., 2021; Raza et al., 2022). We relate Google search volumes for our subject companies (Coinbase, MicroStrategy, GameStop, PayPal and Tesla) with Bitcoin prices as a proxy for cryptocurrency market conditions (see Figure 1 for Bitcoin pricing during our sample period).

We analyze Google searches in the US for these companies combined with the term “cryptocurrency”, from December 30, 2018, to December 31, 2022 (four years in total). We retrieved Bitcoin prices in dollars from Yahoo!Finance (N.D) for the same period. We then charted the Google search volumes for each company combined with cryptocurrency and Bitcoin price (in $000).

Following this, we conduct univariate and correlation analyses for all variables, and perform panel data regression models to examine the relationship between Bitcoin prices and the combined search volume for all companies and cryptocurrencies from December 30, 2018, to December 31, 2022 (see Online Appendix – Part II for variable definitions). The regression models included firm fixed effects to control for unobservable firm-specific factors.

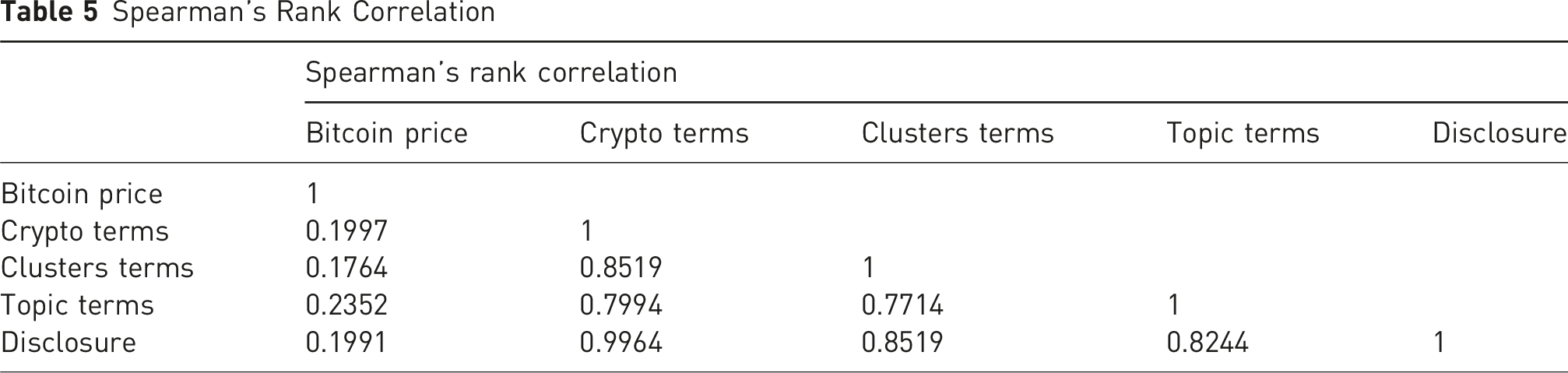

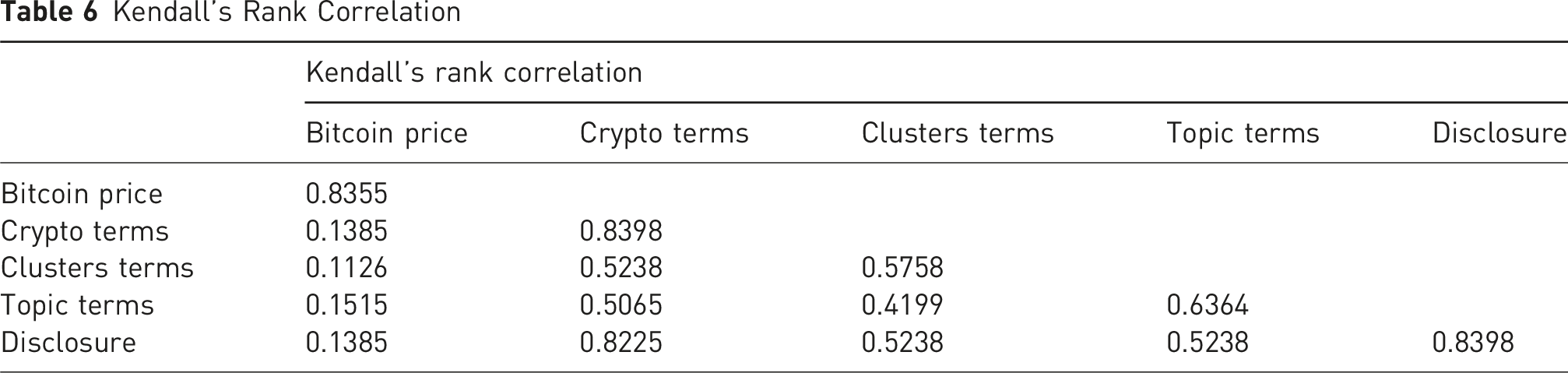

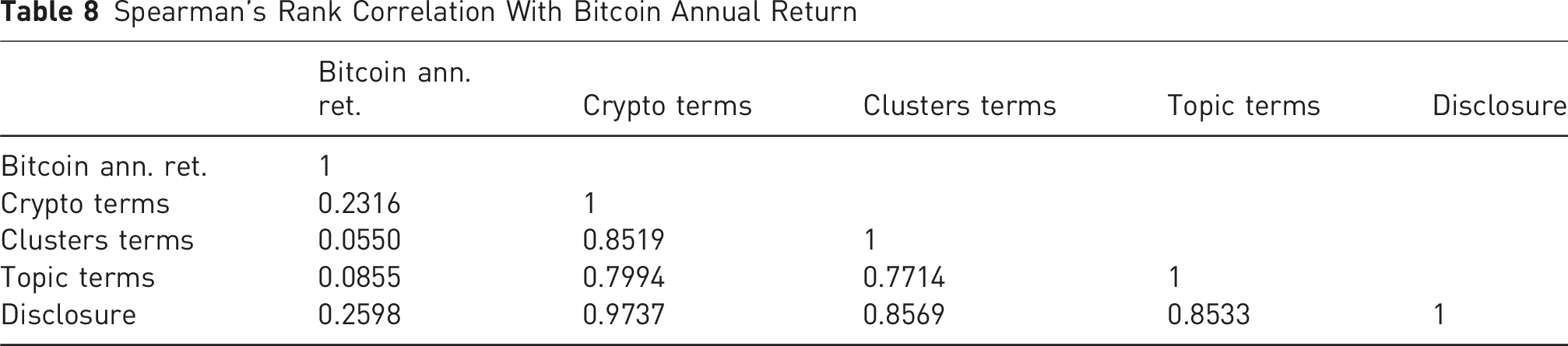

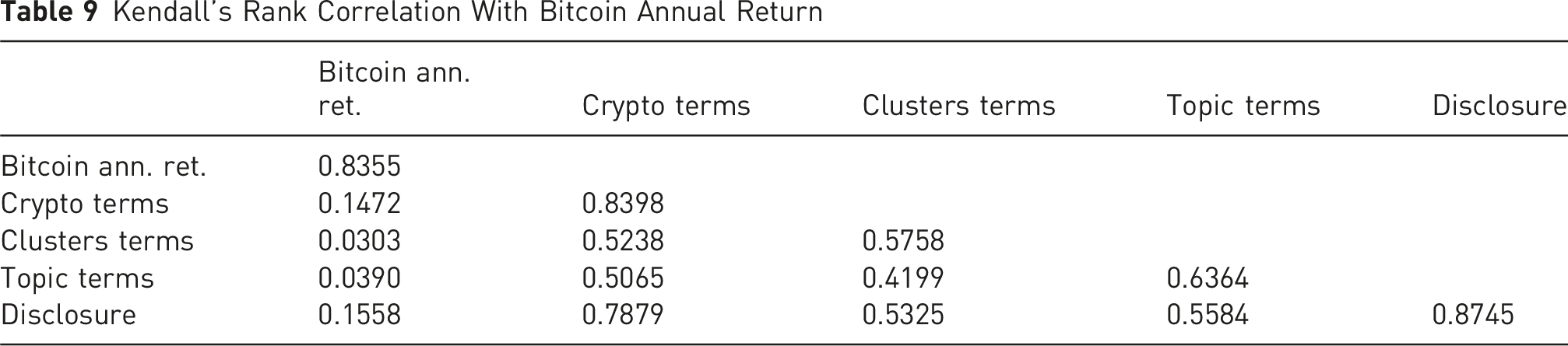

In addition, to relate narrative disclosure metrics with annual Bitcoin returns, we conducted the following analyses: (1) We graphed all disclosure metrics used in this study (described in more detail below) against Bitcoin returns. The disclosure metrics examined included crypto terms, cluster terms, topic terms and overall disclosure, as defined in Online Appendix – Part II: Glossary and Variable definitions. (2) We performed nonparametric rank correlation analysis, including Spearman’s Rank Correlation and Kendall’s Rank Correlation, to assess relationships between the disclosure metrics and Bitcoin returns.

4

(3) We conducted robustness tests to ensure the reliability and consistency of our findings.

Text Analysis Methods

After analyzing Google trends, we next examine the readability of the corporate reports of our subject firms. We then apply machine learning and data visualization techniques to analyze corporate cryptocurrency disclosures in the 2018–2022 period. This approach allows us to gain deeper insights into the textual content and patterns in the firms’ disclosures over time.

Readability Analysis

To assess whether firms strategically adjust the clarity of their cryptocurrency disclosures, we apply five widely used readability indices: the Gunning Fog Index (Gunning, 1952), Coleman-Liau Index (Coleman & Liau, 1975), SMOG Index (Gunning, 1969; Mc Laughlin, 1969), Flesch Reading Ease Index (Flesch, 1948), and Flesch-Kincaid Grade Level Index (Kincaid, 1975). These indices offer established measures of textual complexity and required reading level and are frequently used in research across accounting, finance, and entrepreneurship. All scores were calculated using the Online-Utility.org platform. A detailed explanation of each metric is provided in Online Appendix – Part III.

We go beyond conventional readability assessments by conducting a paired-sample analysis, comparing cryptocurrency-related passages to non-crypto passages from the same annual reports across all five firms and years. This within-document design isolates the variation in language attributable to topic (crypto vs. non-crypto), controlling for firm- and year-level reporting norms.

These readability indices have been validated in prior studies. e.g., Chen et al. (2023) find that low readability in annual reports impairs information assimilation and is associated with equity mispricing. Lo et al. (2017) show that managers can deliberately modulate text complexity to obscure or highlight key information—often in conjunction with earnings management. In the entrepreneurship literature, readability has been shown to affect perceptions of legitimacy, trustworthiness, and investment likelihood (e.g., Chan et al., 2020; Costello & Lee, 2022).

In our setting, readability is treated not only as a proxy for cognitive burden but as a potential instrument of impression management. Firms may simplify disclosures to frame speculative or volatile activities—such as cryptocurrency involvement—as more transparent, stable, or low-risk. To test this, we perform both parametric (paired-sample t-tests) and nonparametric (Wilcoxon signed-rank tests) across all readability indices. We also compute Cohen’s d to assess effect sizes and practical significance.

This approach enables a novel contribution: revealing that cryptocurrency sections are consistently and significantly more readable than other sections in the same reports, suggesting that readability itself is being strategically modulated. These findings support our broader thesis that readability engineering is a subtle but powerful form of narrative impression management.

Machine Learning Text Analysis

Following our assessment of disclosure readability, we applied machine learning and data visualization methods to financial statement and related textual disclosures from 2018 to 2022, capturing variations across different market conditions. Our focus was on trends in cryptocurrency involvement and disclosures to determine whether firms employed assertive impression management for self-promotion.

We used JMP® Pro 17.2.0 (hereafter referred to as JMP®) for text analysis of annual reports (including management discussion and analysis) and proxy statements. Heuristic methods provided initial insights, while machine learning methods delivered structured, actionable information. This allowed us to quantitatively assess the emphasis on specific terms and their prioritization within corporate disclosure (Luo, 2021; Sanchez-Pi et al., 2014).

The Text Explorer platform in JMP® facilitates the analysis of unstructured text, offering tools to combine similar terms, recode incorrectly specified terms, and uncover underlying patterns in textual data, thereby enhancing our understanding of corporate disclosure practices. First, the platform employed the Bag-of-Words model (Harris, 1954; Ko, 2012; Sivic & Zisserman, 2008; Weinberger et al., 2009) to represent text as word collections, preserving word frequencies while disregarding grammar and order. Our analysis included the proliferation of cryptocurrencies, focusing on Bitcoin but also incorporating broader terms like “cryptocurrency” to capture diverse datasets. The output of the Text Explorer platform includes a count of the individual terms and phrases, where a phrase is defined as a short collection of terms (see Online Appendix – Part II for glossary and variable definitions).

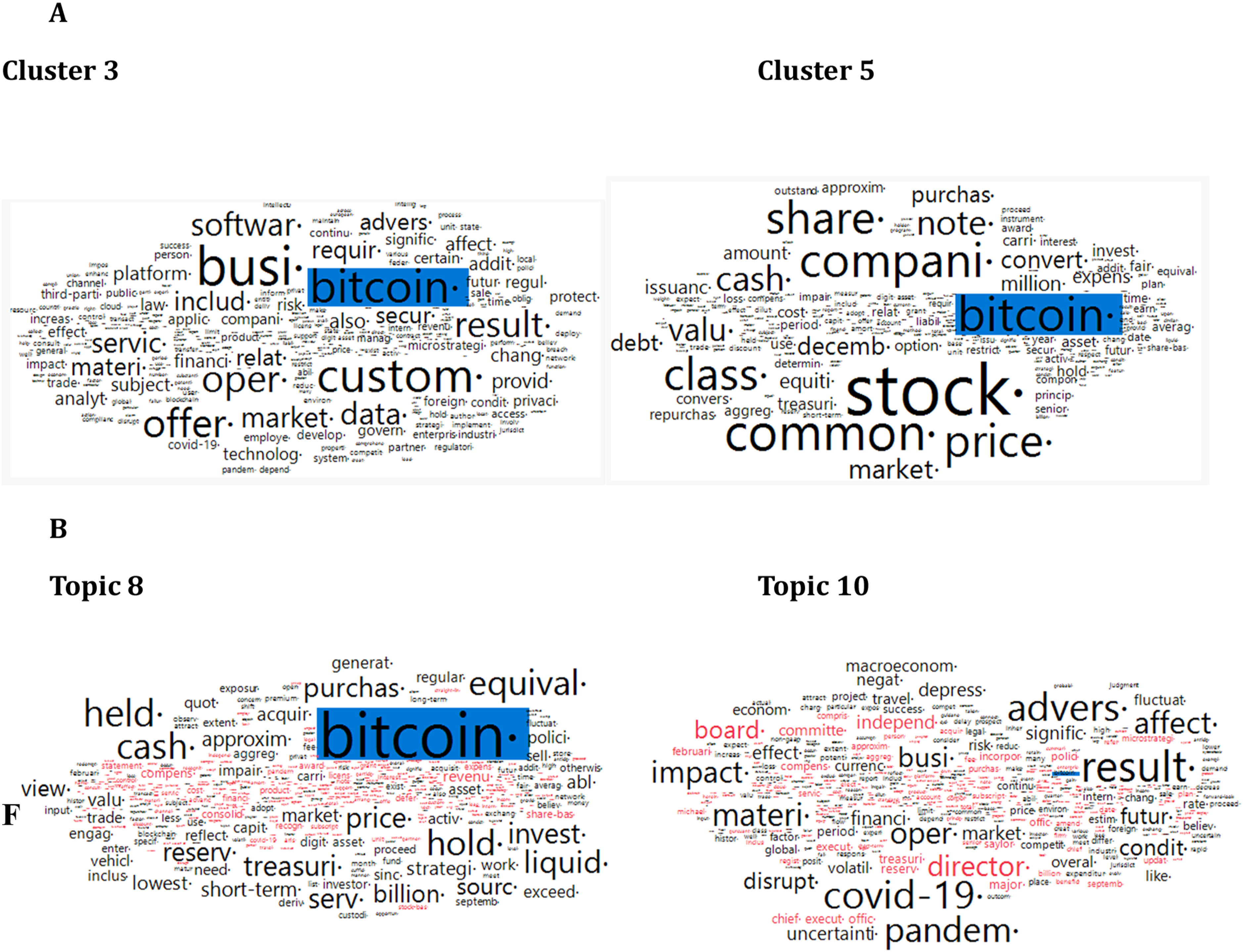

Next, we employed the Latent Class Analysis (LCA), using five Clusters (Goodman, 1974; Karnowski, 2017; Lazarsfeld & Henry, 1968; Weller et al., 2020) to uncover hidden (latent) structures in the data. LCA, a structural equation modeling technique, identified latent clusters in corporate disclosures based on probabilistic patterns, offering interpretability and robustness compared to purely algorithmic methods like k-means clustering. Outputs included cluster membership probabilities, term importance, and Multi-Dimensional Scaling (MDS) plots, which visualized text similarities and relationships. 5

We generated a word cloud for each cluster to visualize term frequency, with larger terms indicating higher frequencies. This tool efficiently highlighted priorities in corporate disclosures and their evolution over time, helping to detect impression management. It also allowed us to examine correlations between disclosure trends and cryptocurrency popularity and pricing. An example of the word clouds for MicroStrategy in 2020 is provided in Figure 2 Panel A. MicroStrategy Word Clouds 2020. (A) For Clusters. (B) For Topics

We applied Latent Semantic Analysis (LSA) (Evangelopoulos et al., 2012; Wolfe & Goldman, 2003), a natural language processing method. LSA is a computational approach that examines relationships between text and terms by grouping documents and terms with similar meanings into shared vector spaces, even when different words are used, making it more effective than relying on superficial matches. Another advantage of LSA is its ability to reduce noise by filtering out infrequent or irrelevant terms through Singular Value Decomposition (SVD). This dimensionality reduction process enhances analysis quality by focusing on significant terms and relationships, improving the reliability of subsequent clustering or classification.

JMP® Pro employs partial singular value decomposition (SVD) for LSA, reducing text data to manageable dimensions, 6 similar to principal components analysis (Miner et al., 2012, Chapter 11). 7 This computationally efficient method extracts significant semantic structures and captures indirect connections between terms with related meanings. For instance, SVD links terms appearing with a common third term, even if they never co-occur directly, and maps related documents to similar vectors. We used SVD for topic analysis, identifying terms with the highest loadings in each topic and visualizing them with word clouds. An example of a word cloud for MicroStrategy in 2020 for topics is shown in Figure 2 Panel B.

Comparison of LCA and SVD

The key distinction between these complementary analyses lies in their approach. LCA uses structural equation modelling to group similar sets of words (documents) while SVD reduces the document-term matrices (DTM) into smaller text matrices with fewer dimensions. In LCA, clustering identifies terms that frequently co-occur in the same document, while in rotated SVD, topic analysis groups terms based on their correlations, highlighting conceptual relationships.

Sample Firms and Their Apparent Cryptocurrency Involvement

We began by identifying firms representative of diverse types of corporate cryptocurrency involvement. This was done by searching all corporate regulatory filings of annual reports (including Management Discussion and Analysis) and proxy statements on Edgar. 8 Surprisingly, even though regulators have prioritized this area (e.g., Edwards et al., 2019, and the FASB Invitation to Comment on the FASB agenda, 2021), we found minimal meaningful disclosure of cryptocurrency involvement in these filings. 9

Cryptocurrency Use Cases for Subject Firms

Corporate Use Cases

As described above, there are several reasons for corporate involvement with cryptocurrencies, and usage has increased over time. On the demand side of the market, firms use cryptocurrency as a means of exchange, as an aspect of their operations, or as a store of value. Firms on the supply side of the cryptocurrency market provide a variety of financial services for businesses and individuals exchanging or holding cryptocurrency assets.

Our selected firms on the supply-side of the cryptocurrency market include PayPal and Coinbase. Demand-side firms include MicroStrategy, Tesla and GameStop. These companies vary widely in both their cryptocurrency involvements and in their related disclosures, as explained below.

Supply Side Firms: PayPal and Coinbase Cryptocurrency Involvements and Disclosures

PayPal

PayPal demonstrates a significant mismatch between its limited financial disclosures and the strategic importance of cryptocurrency to the company and its customers. As a digital wallet and payments firm, PayPal’s 2021 Combined Proxy Statement and Annual Report emphasizes its goal to “Become the World’s Leading Digital Wallet”, highlighting services such as consumer financial tools, bill pay, and cryptocurrency access. Cryptocurrency initiatives are included in performance highlights and play a role in executive compensation. For example, in 2021, CEO Daniel H. Schulman expanded Venmo’s crypto capabilities, while Jonathan Auerbach oversaw the launch of products like Checkout with Crypto and UK cryptocurrency services.

Despite this strategic focus, PayPal’s financial disclosures on cryptocurrency remain minimal. The company facilitates client cryptocurrency activities via a third-party custodian, with related disclosures limited to safeguarding asset and liabilities- $605 million dollars at year-end 2022 compared to total assets of almost 79 billion dollars. This discrepancy arises because PayPal does not own cryptocurrency directly. Instead, its cryptocurrency emphasis is revealed in textual disclosures, which we analyze using data visualization and machine learning techniques to assess their evolution over time and to examine their apparent response to changing market conditions.

Coinbase

In its 2022 10-K, Coinbase states that it offers “a safe, trusted, easy-to-use platform that serves as a gateway to the crypto economy for our three customer groups via both custodial and self-custodial solutions: consumers, institutions and developers”. The company highlights its role as an agent in customer transactions, earning fees for facilitating these activities. Unlike PayPal, Coinbase provides extensive financial disclosures on its cryptocurrency activities, including numerous cryptocurrency-related accounts and detailed discussions of associated risks and opportunities.

Most of Coinbase’s narrative focuses on risks, such as price volatility and potential regulatory or legislative changes. The regulatory classification of cryptocurrencies as securities is flagged as a significant threat to its business model, as this would require registration of all related transactions with regulators, complicating trading, clearing, and custody operations.

In 2022 Coinbase reported nearly $90 billion in total assets, up from $21 billion in 2021, driven largely by the recognition of over $75 billion in customer crypto assets and liabilities. Previously, only corporate crypto assets and borrowings were reported, which are comparatively minor. The valuation bases for different crypto items vary. Unhedged corporate crypto assets are categorized as intangible assets and are measured at acquisition cost (subject to impairment losses). In contrast, crypto loan receivables are valued at fair market value. Corporate crypto holdings declined from $988 million in 2021 to $424 million in 2022, while crypto borrowings dropped from $427 million to $152 million.

While both PayPal and Coinbase have extensive cryptocurrency involvement, Coinbase’s financial and narrative disclosures are far more detailed, whereas PayPal’s focus is primarily on textual disclosures.

Demand Side Firms: GameStop, Tesla and MicroStrategy

GameStop

GameStop is unique among our demand-side firms in that its cryptocurrency holdings were directly related to corporate operations and were not intended primarily as a treasury asset. During our sample period, there was a major strategic shift at the company regarding its cryptocurrency activities. In 2022, GameStop announced, and then retracted, the provision of cryptocurrency wallets that would allow gamers and others to send and receive cryptocurrencies and other digital assets.

Like Coinbase, the GameStop disclosures present a lengthy description of risks related to cryptocurrency activities. Regulatory risks are also a significant concern. Another major issue is whether GameStop’s customers comply with anti-fraud and anti-financial crime laws. They state that “we require third parties using our digital products or services to confirm that their digital asset activities will comply with all applicable laws and regulations in connection with their use of our digital assets or services, but there can be no assurance that these parties will do so”.

The company reports cryptocurrency holdings in its financial statements as Intangible Assets 10 (similar to MicroStrategy and Tesla). Under this accounting treatment, all three of our demand-side firms report impairment losses associated with their cryptocurrency holdings during poor market conditions. However, prior to the new FASB (2023) guidelines, they were unable to recognize any associated revaluations. GameStop reported a realized gain on sale of digital assets of $7.2 million in 2022, alongside digital asset impairments of $34 million.

We now turn to the cryptocurrency involvements and disclosures of Tesla and MicroStrategy. The disclosures of MicroStrategy and Tesla are similar, with MicroStrategy having much more cryptocurrency involvement, and more sustained involvement than Tesla.

Tesla

In early 2021, Tesla purchased $1.5 billion in Bitcoin, representing between 2 and 3% of total assets ($62.1 billion at year end). Soon after, in March, Elon Musk announced (by tweet) that Tesla would allow customers to purchase cars with Bitcoin, secured with the equivalent of $100 in Bitcoin. This arrangement was retracted 10 months later, in early 2022, citing climate related concerns. The Bitcoin holdings were a treasury asset that was unrelated to operating activities, since the prospect of accepting crypto in payment would not require this level of holdings.

An interesting aspect of Tesla’s involvement with cryptocurrency is that the size of their trades, and the high-profile nature of the company, influenced market movements (Ante, 2023; Patnaik et al., 2021). Gerken (2023) reports that Elon Musk has been among the most high-profile champions of cryptocurrency, with his pronouncements on social media often driving significant trading activity. Tesla’s 2021 Bitcoin purchase caused the cryptocurrency to rise in price by more than 25% to $48,000 – a record high at the time. It rose again in March 2021 when Musk tweeted that Tesla would allow customers to make their car purchases using Bitcoin and then it fell by more than 10% two months later when the firm retreated on its plan, citing climate change concerns. The price of Bitcoin also fell when the firm sold most of its holdings.

Tesla had no reported purchases or sales of digital assets until 2021. In that year, the company purchased $1.5 billion and sold $272 million of cryptocurrencies, reporting a $27 million gain on those sales. In 2022, there were no purchases, but the company sold $936 million in cryptocurrencies and recorded a loss of $140 million.

Tesla describes its cryptocurrency holdings as follows: “We have ownership and control over our digital assets, and we may use third-part custodial services to secure it. The digital assets are initially recorded at cost and are subsequently remeasured on the consolidated balance sheet at cost, net of any impairment losses incurred since acquisition” in accordance with ASC 350. The company discloses its impairment losses on cryptocurrencies in the financial statement item “Restructuring and other” in the consolidated statement of operations, in the period when the impairment is identified. This arguably offers an opaque treatment of cryptocurrency-related losses, given that there is no clear connection between the operations of the company and its cryptocurrency investments.

MicroStrategy

MicroStrategy is a software analytics company providing business intelligence solutions across sectors such as financial services, retail, healthcare, and technology. It was the first publicly traded firm to adopt Bitcoin as a capital allocation strategy (Khatri, 2020), announcing an initial $250 million Bitcoin purchase in August 2020. This decision, spearheaded by then-CEO Michael Saylor, was framed as a hedge against inflation and a visionary step toward modernizing corporate treasury practices. Saylor described Bitcoin as “a dependable store of value and an attractive investment asset with more long-term appreciation potential than holding cash.”

MicroStrategy’s cryptocurrency acquisitions were primarily funded through a mix of excess cash, debt issuance, and equity offerings. Consequently, investors gained indirect exposure to Bitcoin, even though these holdings were unrelated to the company’s core business operations. Starting in 2022, the firm began referencing initiatives tied to the Bitcoin Lightning Network, signaling a potential operational integration of crypto technologies. However, these projects do not justify the scale of Bitcoin accumulation, reinforcing the interpretation of the holdings as part of a financial—not operational—strategy.

Until the issuance of ASU 2023-08, U.S. GAAP required Bitcoin to be classified as an Intangible Asset and reported at the lower of cost or market. This approach resulted in significant impairment charges, which MicroStrategy presented as part of its operating results. As of December 31, 2022, the carrying value of its digital assets was $1.84 billion—after recognizing cumulative impairments totaling $2.15 billion—on total assets of $2.41 billion. In other words, nearly 89% of the company’s asset base was in cryptocurrency.

Supplementary financial disclosures are presented in the Online Appendix (Tables A-1 and A-2) to contextualize the materiality and accounting treatment of these holdings. As shown in Table A-1 of the Online Appendix, digital asset impairment losses made up a substantial portion of reported net losses. In 2022 alone, the company recorded $1.3 billion in impairment charges, equivalent to 325% of its gross profit of $396 million. After adjusting for these impairments, the company’s operating profit after all other expenses was only $10.5 million, underscoring the dominance of crypto-related accounting in shaping reported results.

Because positive price movements in Bitcoin were not recognized under historical cost rules, reported asset values and earnings systematically understated recoveries. Table A-2 in the Online Appendix compares reported carrying values with year-end market values, illustrating substantial valuation gaps. For example, at year-end 2021, MicroStrategy reported $2.85 billion in digital assets, while their market value exceeded $5.7 billion. These discrepancies reveal how historical cost treatment distorted both balance sheets and earnings—volatility that will likely increase under forthcoming fair value accounting rules.

As with Tesla, MicroStrategy’s crypto holdings far exceed what would be justified by operational use cases, suggesting a financial, not functional, motive. Yet, the firm’s classification of associated impairments as operating expenses raises important questions about how such exposures should be portrayed in the financial statements.

Understanding these actors—and the financial reporting implications of their cryptocurrency strategies—is a critical precursor to our text-based analysis. To further contextualize firms’ disclosure behavior, we integrate Google Trends data as a proxy for public attention to cryptocurrency-related topics. This allows us to examine whether firms time or shape their disclosures to align with peaks in external interest—potentially amplifying favorable sentiment or downplaying involvement during downturns. In this way, we connect market-facing impression management to broader cycles of information demand and supply.

Results

To examine impression management in cryptocurrency disclosures, we apply a multi-layered analysis combining external information demand (Google Trends, 2023), disclosure complexity (readability metrics), and content evolution (machine learning–based text analysis). We begin by assessing investor interest in our subject firms using Google Trends as a proxy for public attention. This helps determine whether firms are disclosing more during periods of heightened visibility. Next, we analyze the readability of disclosures, using five established indices to measure linguistic complexity and track changes over time. We then present results from text analysis, including topic modeling and word cloud visualizations, to uncover the timing and emphasis of cryptocurrency-related language across firms. Finally, we conduct a detailed case analysis of MicroStrategy to illustrate how firm-specific disclosures align with market cycles and signal management strategy.

Cryptocurrency Market Conditions and Google Trends Analysis Results

Given our interest in impression management through cryptocurrency-related disclosures, we first investigated investor awareness of these firms’ cryptocurrency involvement. To do so, we examined whether interest in firm-related information correlated with Bitcoin price movements during the volatile period from 2018 to 2022. As shown in Figure 1, Bitcoin prices remained relatively stable until 2020, surged to nearly $70,000 in November 2021, and then plummeted to under $17,000 in November 2022 amid a crisis of confidence.

Kerner (2023) and Salvucci (2023) highlight key events that undermined crypto investor enthusiasm including the crash of the TerrUSD and Luna stablecoins, FTX’s bankruptcy, mass layoffs at crypto companies, and fears over stricter regulation. Rising interest rates and inflation concerns further strained the macroeconomic environment. The sharp market declines of 2022, often called a “crypto winter”, saw lower prices, reduced trading volumes, and layoffs at major exchanges. This period was followed by dramatic price recovery in 2023 that could not have been anticipated in late 2022.

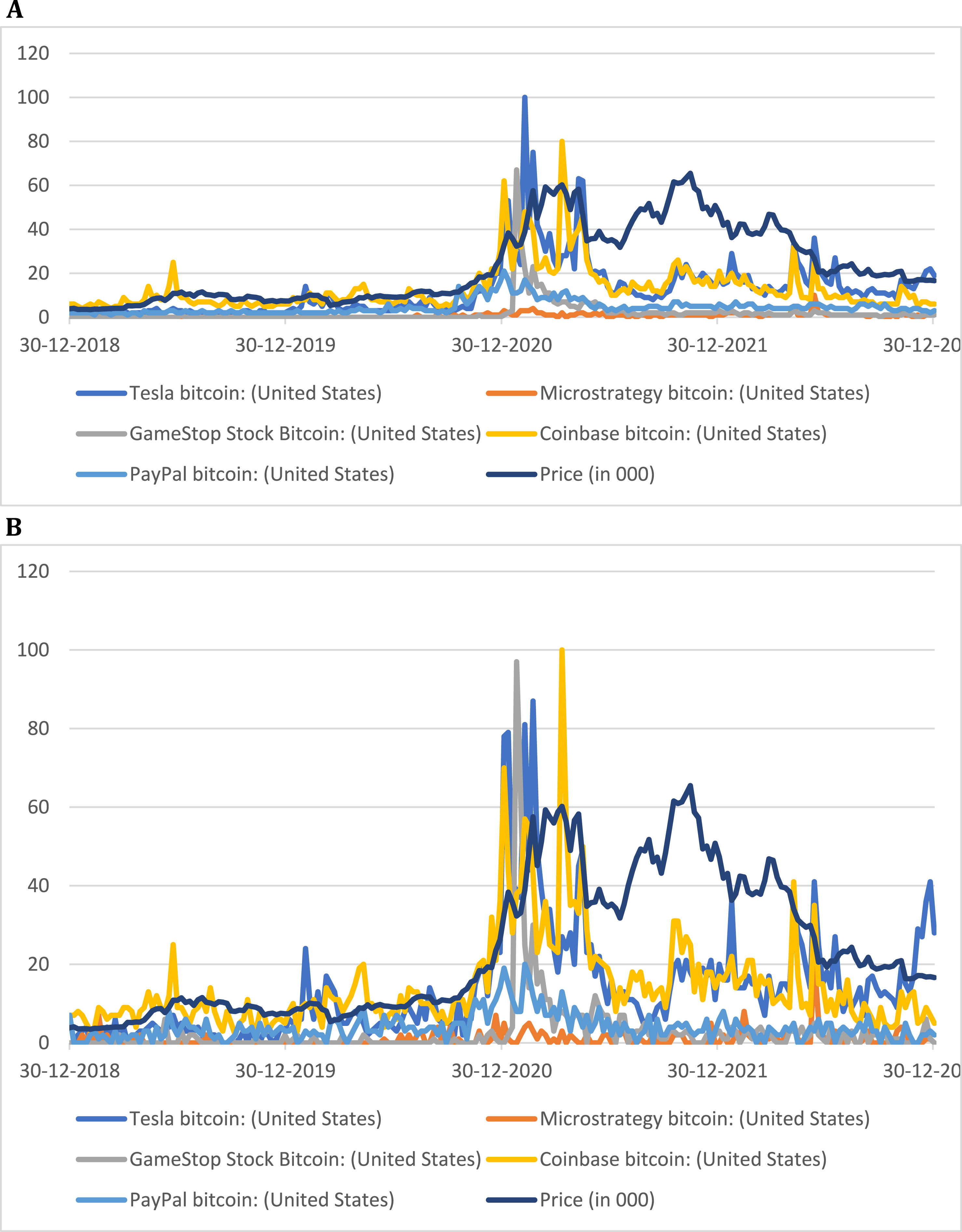

Next, we assess the demand for information about selected firms from 2018 to 2022 using Google Trends and examine its relationship with Bitcoin price movements. Figure 3A and B display the Google Trends data for US Web searches related to our five subject firms, encompassing overall Google searches, and Google Finance-specific searches, respectively. Bitcoin prices (in thousands of $) are overlaid to represent cryptocurrency market conditions. Both figures reveal a clear relationship between interest in these firms and cryptocurrency market trends. Notably, interest in the firms surged during 2020 as Bitcoin prices increased, but this interest waned as the cryptocurrency market declined. (A) – Google Trends by Company and Bitcoin Price All Google Categories. (B) - Google Trends by Company and Bitcoin Price for Google Finance Category

Summary Statistics and Correlations for Google Trends

*p < .001.

*p < .001.

***p < .01.

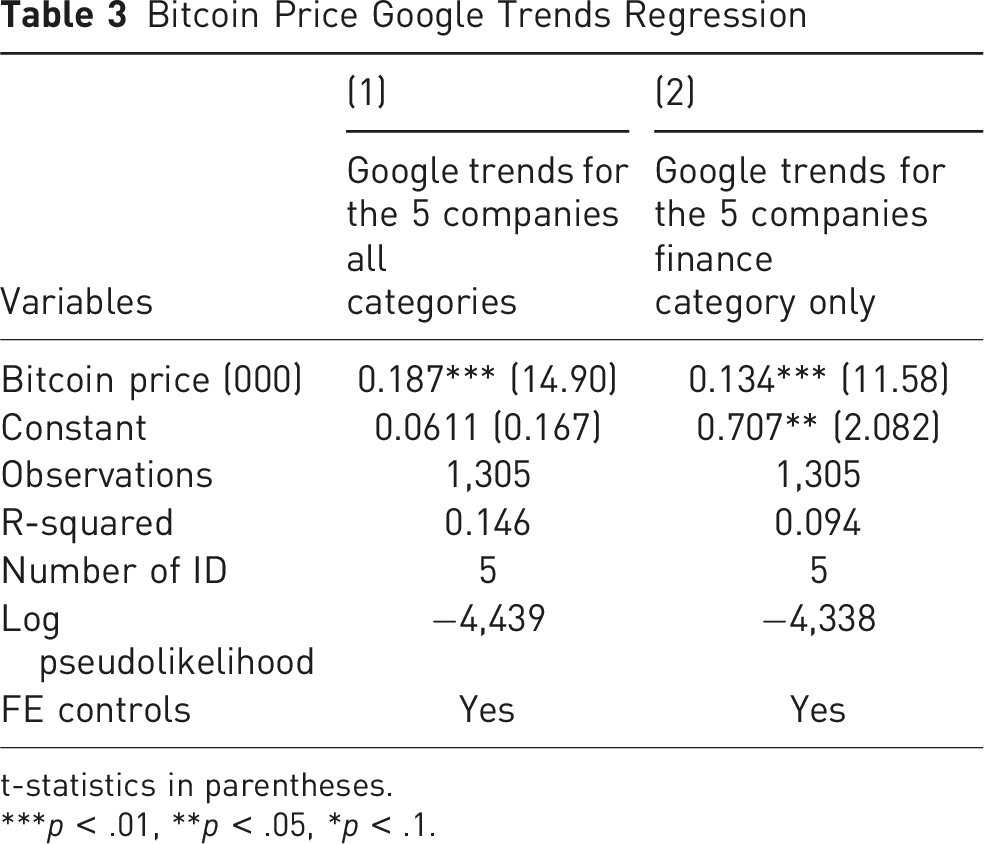

Bitcoin Price Google Trends Regression

t-statistics in parentheses.

***p < .01, **p < .05, *p < .1.

In summary, Google Trends data for our representative firms reveals that information demand closely aligns with cryptocurrency market conditions, as indicated by Bitcoin prices. Specifically, Google searches for these firms increase when Bitcoin prices rise and decline with Bitcoin prices fall, highlighting a clear link between information demand and market dynamics. This suggests that search activity reflects public awareness of these firms’ involvement in the cryptocurrency space.

Next, we analyze the readability of cryptocurrency-related disclosures in annual report and proxy statements by the subject firms, followed by text analysis and data visualization. These analyses highlight how corporations assertively manage investors and analysts perceptions of their cryptocurrency involvement beyond their financial disclosures.

Readability Analysis

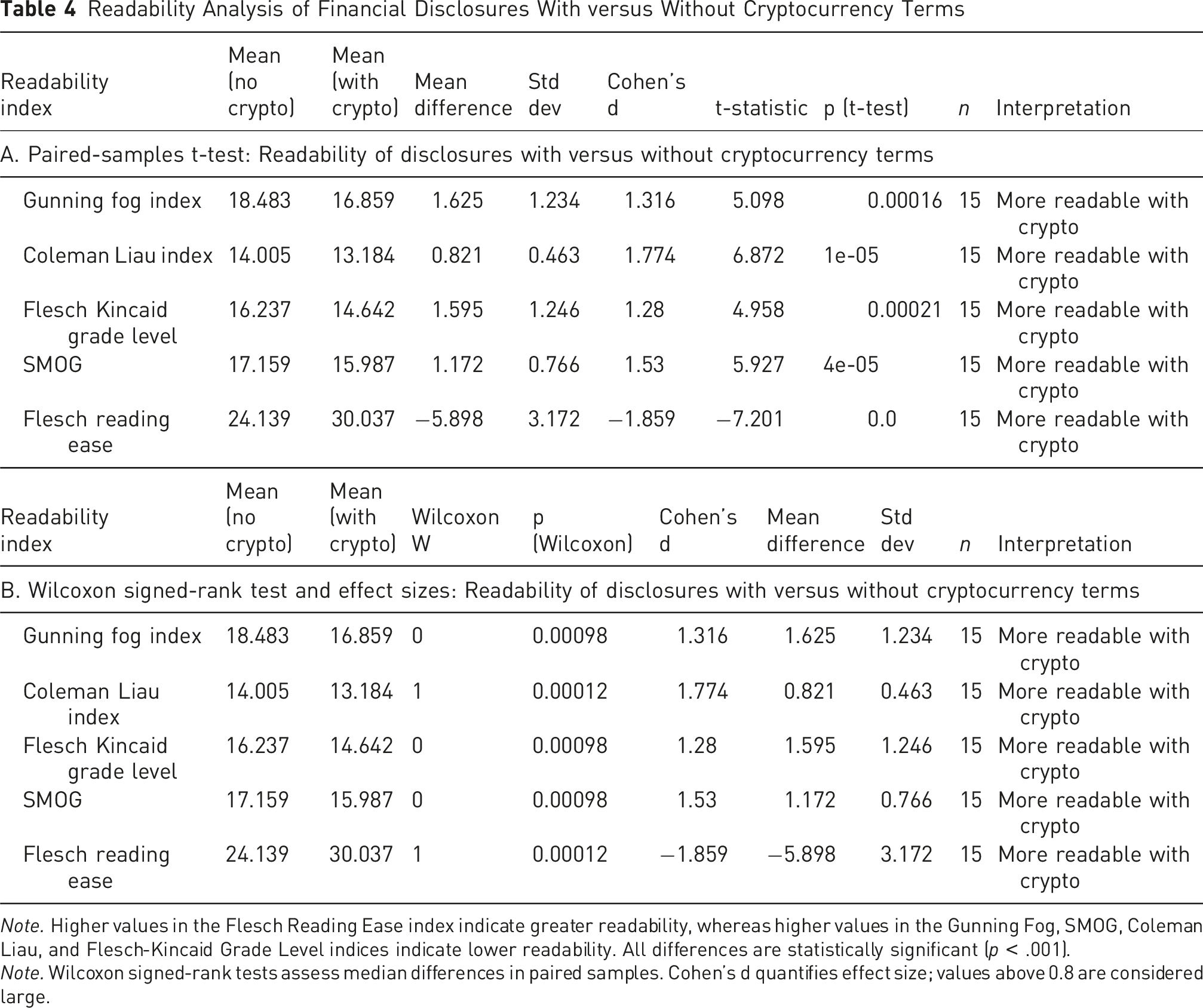

To evaluate whether cryptocurrency-related disclosures differ in complexity from other parts of financial reports, we conducted a paired-sample readability analysis comparing full annual filings (including all cryptocurrency references) with versions in which all crypto-related terms (e.g., “bitcoin”) were removed. This within-document comparison offers a precise reference point for assessing readability differences.

Readability Analysis of Financial Disclosures With versus Without Cryptocurrency Terms

Note. Higher values in the Flesch Reading Ease index indicate greater readability, whereas higher values in the Gunning Fog, SMOG, Coleman Liau, and Flesch-Kincaid Grade Level indices indicate lower readability. All differences are statistically significant (p < .001).

Note. Wilcoxon signed-rank tests assess median differences in paired samples. Cohen’s d quantifies effect size; values above 0.8 are considered large.

For example, the Gunning Fog Index for crypto-related disclosures was on average 1.63 points lower, implying that less formal education is needed to understand the content. The Flesch-Kincaid Grade Level was 1.60 points lower, and the Flesch Reading Ease score was 5.90 points higher, indicating increased textual accessibility. Four out of five readability indices showed large effect sizes (Cohen’s d > 1.3), suggesting not just statistical significance but substantial practical impact.

These findings suggest that firms strategically simplify their cryptocurrency disclosures relative to the rest of their financial reports. In contrast to the broader complexity of corporate reporting, the readability of crypto-related sections appears designed to maximize accessibility and reduce investor skepticism. This pattern aligns with theories of impression management, whereby firms craft disclosures to influence stakeholder perceptions. Given the volatility and reputational sensitivity surrounding cryptocurrency activities, enhancing readability may serve as a deliberate tactic to frame such involvement as transparent, accessible, and low-risk.

Machine Learning Text Analysis

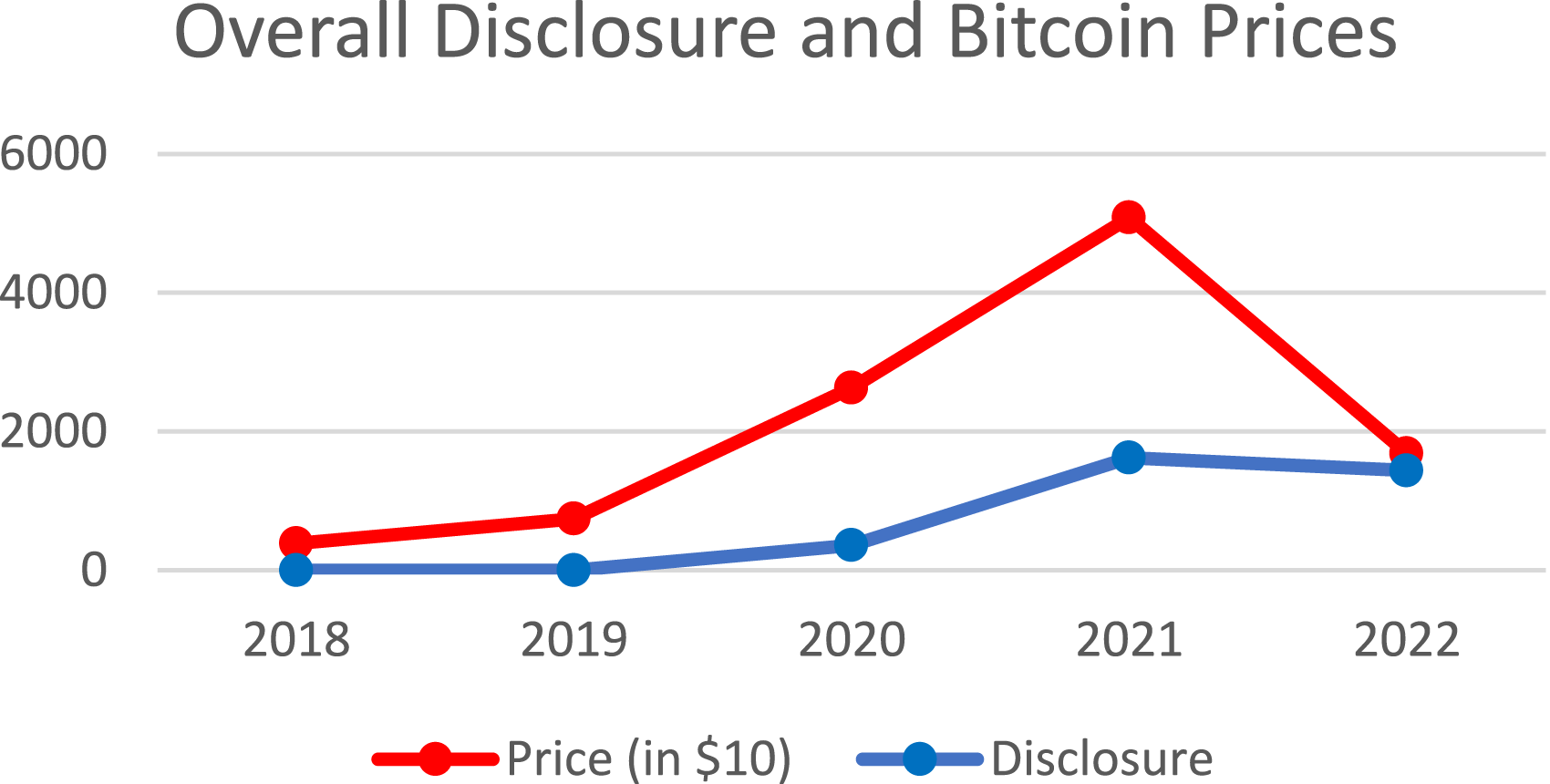

Figure 4 presents the text analysis of cryptocurrency disclosures across all subject firms, showing that the overall Disclosure metric closely tracks Bitcoin prices over time. Both peak in 2021 and decline in 2022, suggesting that firms’ crypto disclosures were opportunistic and aligned with market conditions. Disclosure Metrics for All Companies. Note. Disclosure is Defined in Appendix 1, as Follows:

Spearman’s Rank Correlation

Kendall’s Rank Correlation

Overall, consistent with the notion of assertive impression management, both the demand for information on the subject companies, as revealed earlier through Google Trends, and its supply, are found to be correlated with cryptocurrency market movements.

Robustness Tests

Correlation Matrix

Spearman’s Rank Correlation With Bitcoin Annual Return

Kendall’s Rank Correlation With Bitcoin Annual Return

To illustrate the usefulness of our approach, we provide a detailed analysis of MicroStrategy data in the Online Appendix – Part V.

Discussion

Contribution to the Literature

This study contributes to and extends the growing body of research on cryptocurrency disclosures and impression management. Consistent with Luo and Yu (2022) and Anderson et al. (2024), we confirm that firms adopt varied approaches to disclosing their crypto-related activities. However, our results go further by revealing how firms strategically adjust both the volume and complexity of these disclosures in response to market conditions—highlighting the dynamic use of narrative framing.

Most notably, our paired-sample readability analysis reveals that crypto-related disclosures are consistently more readable than non-crypto sections from the same reports. This finding challenges the assumption that crypto disclosures are inherently more complex and suggests instead that firms may deliberately simplify crypto narratives to maximize accessibility and reduce investor skepticism—particularly when public attention is high. This insight aligns with theories of impression management through linguistic framing, where firms seek to influence stakeholders by adjusting disclosure tone, visibility, and understandability.

In contrast to Cheng et al. (2019), who found positive investor reactions to crypto-related announcements in bullish markets, we show that firms increase both the frequency and readability of crypto disclosures during favorable conditions and either obscure or reduce them during downturns. This complements Cheng et al. (2023), who explored the costs of crypto adoption, by illuminating the evolving communication strategies that accompany those risks.

Our work thus extends the literature on impression management. While prior studies (e.g., Leung et al., 2015; Lo et al., 2017) focused on tone or selective omission, we document a more subtle mechanism: strategic clarity. Firms may use readability itself—not just complexity—as a signaling tool. In boom periods, simplifying crypto disclosures helps frame innovation as accessible, legitimate, and low-risk; during downturns, firms withdraw or complicate these narratives. This adds new nuance to the impression management literature and introduces readability engineering as a corporate communication strategy.

An additional insight from our sample concerns the distinction between firms that hold cryptocurrency for financial versus operational purposes. Financial holders—such as those using crypto for treasury or speculative investment—are more exposed to valuation swings and reputational scrutiny, which may increase the incentive to obscure or downplay such disclosures during downturns. By contrast, operational users—firms that embed crypto within platforms or services—may disclose more consistently and transparently, given the centrality of crypto to their business models. This distinction may help explain observed differences in disclosure timing, clarity, and tone. While not the central empirical focus of our study, it offers a promising theoretical lens for future research on impression management in crypto reporting.

Methodologically, our integration of machine learning topic modeling, readability indices, and Google Trends data offers a scalable approach to analyzing disclosure strategy. By triangulating textual features with public attention patterns, we uncover how firms align disclosure choices with investor sentiment. While Stratopoulos et al. (2022) applied Google Trends to blockchain adoption, our framing emphasizes temporal and strategic alignment between public interest and narrative design.

Practical Implications

Our findings carry several practical implications. For regulators and standard-setters, the observed strategic use of readability suggests that crypto disclosures are not only selectively timed but also linguistically engineered. This underscores the need to go beyond mandating disclosure and begin specifying clarity and comparability standards for crypto-related narratives.

Investors and analysts should be aware that increased readability—rather than complexity—may itself be a form of impression management, used to frame volatile or speculative activities as more transparent or legitimate than they are.

For preparers, understanding how disclosure tone, structure, and readability are interpreted by markets can inform more consistent and credible reporting practices.

Finally, our results highlight the value of text analysis tools—such as NLP-based readability testing and temporal framing detection—for identifying subtle forms of impression management in narrative disclosures.

Theoretical Implications

The findings from our five case firms suggest emerging patterns that may inform theory on disclosure behavior in early-stage financial innovation. While exploratory, these regularities point to the following propositions for future validation in larger, cross-industry samples. First, we propose: P1 (Readability): Crypto-related disclosures are more readable than non-crypto sections in companies’ financial reports. Second, the results indicate strategic variation in narrative complexity consistent with impression management. P2a (Boom Periods): Firms simplify narratives in crypto sections of financial reports during boom periods; P2b (Downturns): Firms complicate narratives in crypto sections of financial reports during downturn periods; and P2c (Strategic Omission): Firms remove narratives of crypto sections in financial reports during downturn periods.

These propositions offer a foundation for future research into how firms modulate disclosure readability and presence in response to shifting market conditions.

Limitations and Future Research

The main limitation of this study is its relatively small sample of five representative firms, which may constrain generalizability. Future research could extend our analysis to a larger and more diverse sample, including international disclosures, and assess the impact of ASU 2023-08 once fully implemented.

Another important limitation is that the observed correlation between Bitcoin prices and firm-level information demand may be explained by other market variables, as the current analysis does not include controls for macroeconomic, sectoral, or firm-specific factors. Without accounting for such potential confounders, the relationship we document should be interpreted as descriptive rather than causal. Future research could address this by incorporating control variables or applying causal inference techniques to better isolate the effect of cryptocurrency exposure on information demand.

A promising avenue for future work is to explore whether firms strategically simplify some disclosures while complicating others, using text complexity as a communicative lever. More fine-grained analyses could test whether simplified crypto narratives are more likely to appear in shareholder letters or MD&A sections, and whether they differ across operational versus investment-based crypto involvement.

Additional research could also investigate investor reactions to readability shifts, testing whether more readable crypto disclosures lead to different market outcomes.

Finally, researchers could explore selective non-disclosure—comparing media-documented crypto-involved firms with those disclosing such involvement in filings—to examine concealment strategies and further illuminate the role of impression management in early-stage financial innovation

Summary and Conclusions

This study contributes to the emerging literature on cryptocurrency disclosures by analyzing full-text regulatory filings from five U.S. firms with diverse forms of crypto involvement. Contrary to prior assumptions that such disclosures are inherently complex, our paired-sample readability analysis reveals that crypto-related sections are significantly more readable than other parts of the same reports. This finding highlights readability as a strategic tool, suggesting that firms may simplify these disclosures to influence stakeholder perception during periods of heightened public interest.

A central contribution of this study is methodological: we integrate machine learning, readability metrics, and Google Trends data to examine how crypto narratives evolve in both tone and prominence. Beyond financial statement data, we account for the type of corporate involvement (e.g., treasury holdings, operational use, service provision) and map how disclosure practices shift with cryptocurrency market conditions—particularly during the “crypto winter” of 2022.

Our findings support the view that firms use narrative design—including both selective emphasis and linguistic clarity—to manage impressions. During bullish periods, firms increase both the volume and readability of crypto disclosures to frame their involvement as transparent and accessible. During downturns, disclosures tend to become less frequent, and in some cases, less clear. This dynamic reflects a broader pattern of strategic narrative management under uncertainty.

While the 2023 ASU may reduce reporting discretion for crypto assets, narrative disclosures will remain a key site for impression management. Our results demonstrate how firms adapt disclosure strategies in response to market signals and reputational pressures, and how emerging technologies such as NLP and topic modeling can uncover these shifts.

Ultimately, this study offers both theoretical and practical contributions. Theoretically, it extends impression management literature by identifying readability engineering as a subtle but potent disclosure tactic. Practically, it underscores the need for investors, analysts, and regulators to interpret narrative clarity not just as transparency—but as a strategic corporate choice in volatile and underregulated environments.

Supplemental Material

Supplemental Material - Text Analysis of Corporate Cryptocurrency Disclosures in Varying Market Conditions

Supplemental Material for Text Analysis of Corporate Cryptocurrency Disclosures in Varying Market Conditions by Ramy Elitzur, and Wendy Rotenberg in Journal of Alternative Finance

Footnotes

Authors’ Note

During the preparation of this article, the authors used ChatGPT (OpenAI) to assist with phrasing refinement and clarity improvements. Following the use of this tool, the authors critically reviewed and edited the content to ensure accuracy and accept full responsibility for the final version of the manuscript.

Acknowledgements

The authors would like to thank the participants of the 3rd International Conference for Alternative Finance Research, held in Krems, Austria in June 2024, as well as the anonymous reviewers and the editor for their valuable comments and suggestions.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.