Abstract

Microenterprise development has been lauded for its capacity to empower socially marginalised women and alleviate poverty. However, the high cost of microcredit due to the relatively high-interest rate charged by institutions poses a debt trap to microenterprises. The study presents a successful case of a private sector-non-governmental organisation partnership to provide interest-free microcredit embedded in a flexible training and mentoring program by Women of Will. The study uses quantitative and qualitative methods to measure the impact of such microcredit and mentoring models on women’s empowerment and entrepreneurial growth, analysing what works and why. The growing importance of environmental, social and governance (ESG) suggests that corporate support for these initiatives has become increasingly sustainable, challenging neoliberal assumptions concerning the inevitable cost of microcredit. The case study draws on a realist approach to inform evidence-based policy by shedding light on the interactions and processes that influence the outcomes.

Keywords

Introduction

The global market for microcredit has grown significantly over time and was valued at approximately USD 145–160 billion in 2021, with projections that it will reach USD 400 billion by 2027 (OECD & European Commission, 2021). The initial model of microcredit that underpinned its popularity as a means of alleviating poverty was based on the Grameen Bank which provided low-cost microcredit through subsidies. Macchiavello (2018) explains that the definition of microcredit varies across countries, and there is a lack of a universal definition of the term. Despite these variations, the core objective of microcredit programs remains consistent. According to Khandker (1998), one of the main objectives of microcredit programs is to provide ‘small amounts of credit to the poor to generate self-employment in income-earning activities’ (p. 3). There are different types of microcredit financing models, including the group-lending model popularised by Grameen Bank, which relies on peer pressure to ensure the repayments of loans (Schurmann & Johnston, 2009).

The provision of small loans is posited to provide borrowers with the means to generate a better income, often premised on microenterprise development (Bateman & Chang, 2012; Cooke & Amuakwa-Mensah, 2022). In the context of poverty alleviation initiatives, ‘microenterprises’ refer to small businesses owned and operated by individuals, at times with family members or several other people, who engage in small-scale vending or services (Midgley, 2008). Underprivileged women are often over-represented among microentrepreneurs who struggle to obtain mainstream finance due to the lack of collateral and insecure income. At the same time, microenterprises are an important source of empowerment for women at the base of the pyramid, providing women the flexibility to earn an income while juggling caring responsibilities. Low-cost microcredit programs empower them through access to credit which would otherwise not be available, enabling microenterprise development and the benefits of enhanced income.

Increased household income is expected to have flow-on effects on women’s standing in their families and society, to engender improved outcomes for their families’ education, nutrition and health (Yunus, 1987), and to help lift their communities out of poverty. The World Economic Forum highlights the value of women as agents of change and the importance of microcredit in enhancing their ‘capacity to address social problems in their communities and influence social norms’ (World Economic Forum, 2013).

Our article contributes to the literature in two ways. First, our research investigates a less-studied, alternative not-for-profit model funded and supported through collaboration with corporations. The Women of Will (WoW) model is unique in that the non-governmental organisation (NGO) not only provides interest-free microcredit loans but socially and economically empowers women microentrepreneurs through training and mentoring sessions. The WoW model, initially adapted from the Grameen Bank model, diverges by integrating three phases of development: microfinancing combined with entrepreneurship development (Phase 1), leadership development (Phase 2) and community resources (Phase 3). While traditional group lending models, like Grameen Bank, primarily focus on financial services aimed at financial inclusion and poverty alleviation, WoW emphasises a more holistic approach. This includes comprehensive support through skills training, business coaching and community empowerment, fostering sustainable transformation beyond financial assistance.

The case study examines how such collaboration has successfully empowered marginalised women and identifies practices and interactions that influence the outcomes (Hewitt et al., 2012). NGO-private collaboration also enables an expansion of markets for the participants’ goods and services, answering the call for a more nuanced understanding of specific aspects of microcredit models that have a genuine impact on poverty reduction and women’s empowerment (Chliova et al., 2015; Mayoux, 1998). As such, in terms of the practical implication of our study, the WoW model can be a case example of what works and why.

In terms of theoretical contribution, we draw upon a realist approach and employ both quantitative and qualitative methods. A multi-method approach allows us to evaluate the impact of WoW’s microcredit program on poverty alleviation and women’s empowerment and produce rich descriptions that illuminate the drivers of change (Pomeranz, 2014). We argue that the neoliberal rationale for passing the cost of lending to borrowers is ostensibly less compelling in today’s increasing demand for better corporate environmental, social and governance (ESG). Corporate support for WoW’s microcredit and mentoring has become increasingly sustainable as ESG has gained traction among corporations, regulators, investors and the broader community.

The article is structured in five sections. The first part introduces the study, including a literature review and the context of the case study followed by an examination of the rationale behind the prevalence of the microcredit lending model to alleviate poverty and promote empowerment and the objectives. The second section describes the research methods used in the study. Key findings are presented in the third section and discussed, including their implications in the fourth section. The fifth section concludes.

Literature Review

Microcredit-enabled entrepreneurship has been promoted by leading transnational organisations as a means of addressing poverty, bridging the gender gap and empowering women in the Global South (Bhuiyan & Ivlevs, 2019; Chatterjee et al., 2022; Khan et al., 2021). Microcredit is thought to facilitate economic empowerment for low-income women who experience higher levels of exclusion from mainstream finance (Bhuyan & Islam, 2020). The underlying rationale is that access to credit enables women to grow their microenterprises and increase their incomes, with benefits that flow onto their families.

A possible drawback of the microcredit lending program is the issue of high indebtedness among borrowers, leading to increased financial vulnerability. At the same time, reports have raised concerns over harmful consequences that further entrench marginalised women in poverty and exacerbate their hardship (Parmar, 2003). These unintended consequences include men controlling the use of money while the burden of repayment remains with women (Goetz & Gupta, 1996). Household tensions have been known to increase as a result of pressure to make repayments and at times reports of domestic violence have emerged. The burden of repaying loans also leads some to compromise on health, nutrition or their children’s education (Khan & Khan, 2016). Some women resort to taking out other loans to meet repayment obligations, leading to increasing levels of indebtedness (Green & Estes, 2019; Rahman, 1999). At times, relationships within the wider community are adversely affected, particularly where group loans are involved or others provide collateral or act as guarantors (Gobezie, 2010; Khan & Khan, 2016). Parmar (2003) recounts situations of women being humiliated and dealt with aggressively by other women following failure to pay their instalments on time, with devastating consequences such as suicide ensuing in some situations.

Notably, many of these adverse consequences are linked to the burden of debt repayment arising from the loans. Critics argue that commercialisation of microcredit with its high interest rates underpins the problem of unmanageable debt and its related consequences (Brickell et al., 2018). Bateman and Chang (2012) highlight the risk of for-profit microcredit institutions constituting a ‘poverty trap’ for many low-income earners but posit that the business model remains the ‘international development community’s preferred economic and societal model based on self-help and individual entrepreneurship’ (p. 30).

Hudon and Sandberg (2013) argue that the central question for the various microcredit initiatives is whether they have proven beneficial effects on people with low incomes. Tavanti (2013) posits that social engagement, entrepreneurial skills and capacity building are central to achieving sustainable livelihoods in addition to economic gains. Broader social impacts should include women’s empowerment, leadership, skills such as micro-enterprise management, and community development. For instance, in their evaluation of microcredit programs, Che and Mbah (2021) posit that microcredit loans help rural communities to be self-reliant through a social solidarity economy model vis-à-vis village-centric development.

Microcredit and Mentoring Model

WoW provides microcredit to low-income women who run home-based microenterprises, who are the breadwinners for their families, and who are single mothers or have other dependents who are unable to work. WoW provides a range of support to empower women, including interest-free microcredit, skills training to develop their microenterprises and individual coaching tailored to their specific needs. Participation is typically for 18 months, but a small proportion of women extend their involvement through advanced training or leadership development. 1 The core belief underpinning the training and coaching offered is reflected in their guiding principle of ‘Teaching women how to fish, rather than giving them fish’ (Women of Will, n.d.). While helping women realise their desire to improve their financial well-being through enhancing their enterprise is pivotal, WoW’s program takes a holistic approach to empowerment. Its program also enables the participants’ personal development and development of supportive networks amongst women and assists women in further empowering their communities.

One of the key distinguishing features of WoW’s model is its collaboration with corporations. Generous funding from donors enables WoW to run its microcredit, training and mentoring programs. Corporate donors are the primary source of WoW’s funding. Not only does this funding allow WoW to offer women interest-free microcredit, but in situations of financial hardship, such funding also allows for debt waivers to be granted, avoiding the detrimental consequences of unmanageable debt. In practice, however, the need for debt waivers is rare, as many participants have experienced positive outcomes from the program. Women’s increased income has enabled repayments that are channelled towards projects that address specific community needs.

In contrast with many microcredit programs that focus solely or primarily on the provision of capital, microcredit is one of several aspects of WoW’s model. The program adopts targeted measures to empower women through capital contribution towards microenterprise development and through new skills, additional income-generating opportunities and support networks. All women experience training and coaching to assist them in developing their microenterprise. In the area of business and entrepreneurship training, participants undergo education programs that include financial literacy, business and finance management, changing mindsets, and product development and marketing strategies. One newer area of training relates to digital marketing and the use of social media. The support provided by WoW also extends to the participants’ personal development and includes information sessions on health, both physical and mental health, nutrition and personal care. Additionally, each participant is allocated a coach for six months who assists them in developing strategies to grow their microenterprise and overcoming challenges. The suite of training modules and supports included in WOW’s model is developed by WoW administrators in response to regular feedback from participants as well as consultation with focus groups of community leaders to assess its relevancy and utility as well as the efficacy of WoW’s training methods.

Participants can also acquire new knowledge and skills in textiles, sewing, food preparation and cooking while earning additional income in dedicated centres run by WoW. Through partnerships with corporations, WoW has fostered the development of a market for bespoke products made collectively, alleviating the problem of saturated markets, which Bateman and Chang highlighted (Bateman & Chang, 2012). Bulk corporate orders for products such as festive hampers allow participants to supplement their income through joint efforts to fulfil these orders. The corporate orders also enable participants to upskill as they contribute to creating high-quality products designed by WoW volunteers. The sewing centre, for example, receives orders such as upcycling packaging, which would otherwise be discarded in landfills, into tote bags which the companies then sell to their customers. Family-friendly policies at the sewing centre enable participants to balance caring responsibilities while earning additional income to support their families.

The feedback that WoW has received from participants indicates that many have experienced higher profits from their microenterprises after implementing strategies learned from training and mentoring. Digital access, for example, was found to be especially useful following the COVID-19 outbreak (Rice et al., 2023). Participants also reported positive outcomes beyond their financial well-being, such as having more time to spend with their children and an increase in income.

One of the objectives of WoW’s microcredit program is to enable its participants to empower their communities. Following the successful growth of their respective microenterprises, women have opportunities to participate in leadership training. Some participants have taken on leadership roles, sharing their experiences and successful strategies that they have acquired with newer participants and other women in their housing communities. WoW takes steps to assist them in identifying needs in the community and addressing those needs in collaboration with their peers. Community initiatives include a kompang (Malay drum) band to promote constructive activities among the youth, as well as the development of a community kitchen and community business centre. Their ability to contribute back to their communities was also valued, enhancing their self-confidence and standing in the community. In an interview, one of the leaders remarked that she had benefitted much from being part of WoW and was now a leader supporting other women. Her participation in the leadership network had increased her social circle and given her friends from various parts of the city.

From a neoliberal perspective, the sustainability of a microcredit program that relies primarily on corporate donations is likely to be viewed with scepticism. Nevertheless, the authors’ interviews with WoW’s management indicate that their microcredit program has indeed been sustainable. In 2022, WoW had approximately 700 ongoing participants and had assisted more than 2,000 women over five years. Corporate contributions to the program are incentivised by mandatory sustainability reporting requirements for listed companies (Bursa Malaysia, 2023a, 2023b). 2 Recent regulatory reforms have further increased the momentum towards creating a positive social impact. Companies that are socially responsible are also perceived as being more attractive to a talented, younger workforce (Jones et al., 2014; Story et al., 2016) and consumers (Chernev & Blair, 2015). In tandem with the rise in social consciousness, WoW’s management has found that their funding model, which depends mainly on corporate giving, has become increasingly sustainable in recent years. This financial stability has allowed WoW to focus on assessing and enhancing their programs.

As such, the objective of the case study is to measure the impact of (WoW)’s model of microcredit and mentoring programs on the empowerment and entrepreneurial growth of women microentrepreneurs. This involves analysing the efficacy of these interventions and investigating the factors contributing to their success.

Research Method

Multi-method Approach

Multiple methods facilitate a more nuanced understanding of how this microcredit model functions and its key attributes and impact on participants. The methods are complementary and allow the findings to be triangulated (Mark, 2015). The study employs qualitative methods to contextualise the impact studies, using ethnography and interviews to produce ‘thick descriptions’ and to facilitate a deeper understanding of the underlying drivers of change (Harrison, 2020). Utilising a natural experiment in the context of WoW’s microcredit program can provide valuable insights into the program’s efficacy and its potential impact on women microentrepreneurs.

The quantitative natural experiment approach allows the study to observe the effects of microcredit financing on women’s empowerment. In contrast, qualitative methods allow the quantitative findings to be analysed within their broader context, enabling causal inferences to be drawn. The research draws on perspectives from the women participating in the microcredit program to illuminate the value that WoW’s model offers to women and their communities (Biddle & Schafft, 2015).

Study Design

As part of the natural experiment, we compare the outcomes of two groups of women microentrepreneurs from the bottom 40% of the household income group (B40) in Malaysia (Klang Valley). The treatment group comprises women who were granted microloans through the WoW program during an intervention period from 2016 to 2022. In contrast, the control group consists of female microentrepreneurs who did not receive any loan assistance.

Data were collected using a survey administered to the treatment and control groups. The survey consisted of questions related to the participants’ financial situation, decision-making power and other measures of women’s empowerment. The researchers shared a draft of the questionnaire with two Malaysians who work directly with the women microentrepreneurs in the bottom 40% of the household income group (B40) in order to ensure that the question wording and response categories are appropriate.

After pretesting the questionnaire with 10 female microentrepreneurs from the B40 group, the researchers revised it based on feedback from those involved. Another 10 female microentrepreneurs were used to test the amended version, and the researchers further modified the survey instruments in response to their comments. These adjustments were primarily made in response to respondents’ confusion over the questions that were part of the same construct. For instance, when the respondents did not understand how the questions within the same construct differed from one another, the researchers either reworded or eliminated them.

The survey was sent to the participants via WhatsApp through the WoW, and they were given a link to the Qualtrics form. For participants who required assistance, the researchers provided them with the option of answering the survey questions over the phone. In the nine months that the poll was open—from April to December 2022—201 valid responses were received from the treatment group and 246 from the control group.

Using a life-world analytical ethnographic framework (Honer & Hitzler, 2015), the research was conducted by one of the researchers who participated in the group’s activities as a volunteer, interviewed key leaders and observed participants with their consent. Based on a phenomenological approach, we aimed to capture, at least approximately, the view of participants and make it understandable to others. ‘Life-world’ in this context refers to lived experience or, in other words, to the world as it is subjectively experienced by WoW women. The research took place over approximately four years, during which the researcher kept abreast of WoW’s activities online through the group’s Facebook page, discussions on Zoom, women’s accounts of the impact that WoW’s interventions had on their lives, and face-to-face interactions. Internet-based communications were the predominant means of social interactions during movement restrictions necessitated by the COVID-19 outbreak. Scholars such as Wang and Liu highlight the value of combining online and in-person observation and interviews in an era where social interactions are ‘increasingly mediated by the internet’ (Wang & Liu, 2021). The use of social media sites for ethnography has gained traction in recent years as researchers have discovered the wealth of regular and accessible interactions on web-based platforms, transcending the geographical limitations of face-to-face interactions (Postill & Pink, 2012). Social media plays a vital role in WoW’s interactions with various stakeholders. It enables information on their activities to be widely disseminated to existing and potential donors, in addition to providing a platform for marketing their products to businesses that support them through large orders. When possible, the researcher also attended various locations where WoW’s activities were held, including its community kitchen, sewing and business centres, and Mont Kiara centre. Face-to-face interactions and semi-structured interviews facilitated insights into other aspects of their operations and interactions among group members. The collected data were analysed by using both quantitative and qualitative methods. The authors obtained ethics approval for the research.

Findings

Quantifying the Impact of WoW’s Microcredit and Mentoring Model

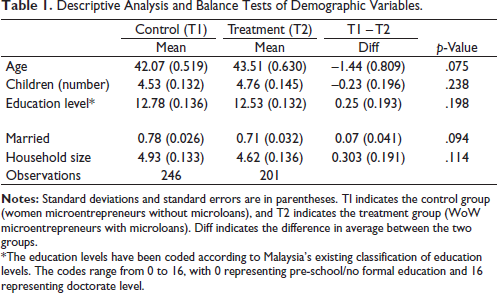

Table 1 presents a comparison between two groups, Control (T1) and Treatment (T2) (the WoW participants), with the following variables: age, number of children, education level, marital status and household size. The means, standard errors (in parentheses), mean differences and p-values are provided for each variable. The comparison between the Control (T1) and Treatment (T2) groups shows no significant differences in age, number of children, education level, marital status or household size at the conventional 5% level. In the context provided, the lack of significant differences in demographics between the Control (T1) and Treatment (T2) groups suggests that any observed differences in outcomes can be attributed to the treatment (e.g., receiving microcredit) rather than demographic factors.

Descriptive Analysis and Balance Tests of Demographic Variables.

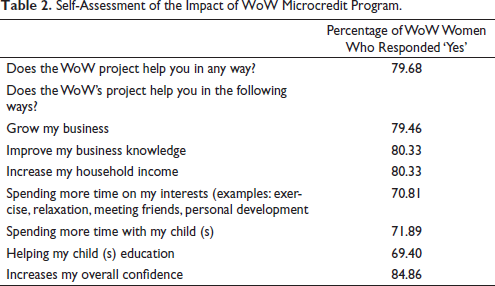

Table 2 provides a summary of the overall impact of WoW microcredit programs on women based on the data collected from the survey. The WoW’s intervention has positively impacted women in various aspects of their lives. A significant majority (79.68%) of the WoW participants responded ‘Yes’ when asked if the project has helped them.

Self-Assessment of the Impact of WoW Microcredit Program.

In particular, the project has successfully supported business growth, with 79.46% of women reporting that it helped them grow their businesses. Additionally, 80.33% of the participants indicated that WoW’s project had improved their business knowledge and increased their household income. The intervention has also positively influenced women’s personal lives, as 70.81% of respondents mentioned that they now have more time to spend on their interests, such as exercise, relaxation, meeting friends and personal development. Moreover, 71.89% reported spending more time with their children, and 69.40% stated that the project has been beneficial in supporting their children’s education. Notably, the WoW microcredit program has substantially impacted the overall confidence of women, with a remarkable 84.86% of clients reporting an increase in their confidence levels. The intervention has successfully fostered business growth and knowledge and improved the personal lives and overall confidence of the women who participated in WoW’s programs.

Women’s Empowerment and Entrepreneurial Skills

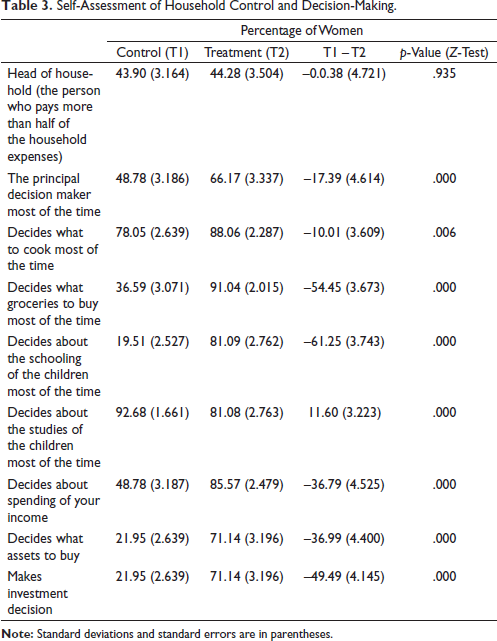

Table 3 presents the results on measures of women’s empowerment within the household. The analysis is based on the percentage of women who said they were the head of the household, the main decision-maker, and in charge of where their children go to school, how to spend money, buy assets and invest money.

Self-Assessment of Household Control and Decision-Making.

The results indicate no significant difference in the percentage of women heads of household between WoW women (T2) and the control groups (T1). However, WoW women (T2) are significantly more likely to report being the principal decision-makers; deciding what to cook and what groceries to buy, deciding about their children’s schooling, deciding about spending their income, deciding what assets to buy, and making investment decisions. These differences (measured by T1 – T2) are large, with all p-values being less than .05, which suggests that the observed differences are unlikely to occur by chance.

These findings suggest that WoW program positively impacts women’s empowerment, particularly in terms of decision-making power. The results are consistent with previous research that indicates that access to financial resources can increase women’s decision-making power and autonomy within the household (Laha & Kuri, 2014).

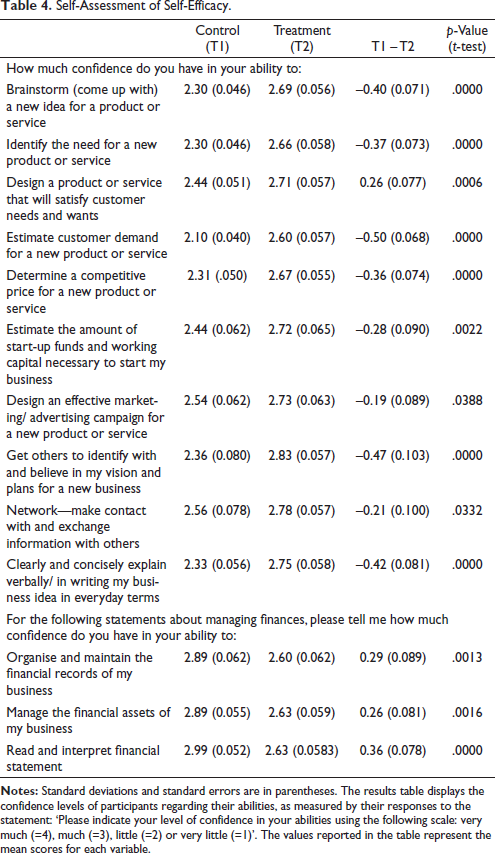

Table 4 shows the mean scores for the women’s confidence levels in various entrepreneurship and financial management aspects. A positive value in the T1 – T2 column indicates that the control group (T1) has higher self-efficacy, while a negative value suggests that the WoW women’s group (T2) has higher self-efficacy. The p-value column provides the statistical significance of these differences.

Self-Assessment of Self-Efficacy.

According to the findings, WoW women (T2) show greater self-efficacy in entrepreneurship-related activities such as brainstorming for new products, recognising a need for and developing new products/services, predicting client demand, pricing, calculating start-up funding, marketing, networking and presenting business ideas. All of these distinctions are statistically significant (p < .05).

However, when it comes to managing finances, WoW women show lower self-efficacy than the control group. Surprisingly, WoW women have lower confidence in organising and maintaining financial records, managing financial assets, and reading and interpreting financial statements. These differences are also statistically significant.

One possible explanation for their lower confidence in managing finances could be the added responsibility and pressure that comes with receiving and managing a microloan. Microloans can introduce a new level of complexity to financial management, as entrepreneurs need to track loan repayment schedules and balance their cash flow while investing in their businesses. This additional burden may lead to lower estimations of self-efficacy in financial management tasks compared to the control group, who do not have to manage loan-related finances (Furrebøe & Nyhus, 2022). Another possible explanation is that WoW women in the treatment group may need more financial education or support to manage their loans effectively, leading to lower confidence in their financial management abilities. Further research could investigate the role of financial education (Chan et al., 2017) and support in improving self-efficacy in financial management among microloan recipients.

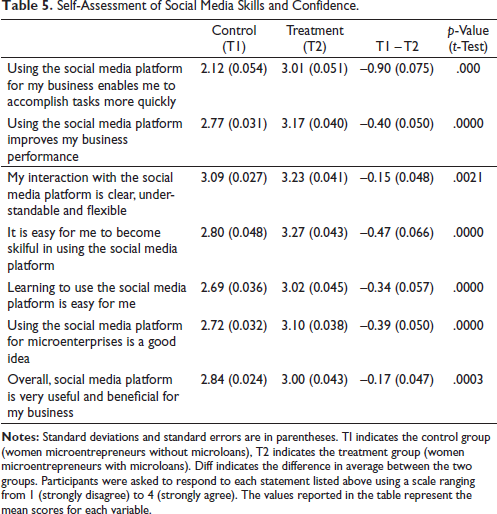

Finally, Table 5 shows that for all statements on the perceived usefulness of social media platforms, the mean scores in the WoW group (T2) were considerably higher than in the control group (p < .001). The findings indicate that WoW women found social media platforms to be more useful and easier to use for their businesses than those who did not. The findings imply that WoW programs may improve women’s perceptions of the usefulness and the ease of use of social media platforms for their businesses. This conclusion is consistent with prior research that has emphasised the relevance of technology for the development and profitability of microenterprises (Lee & Haidir Anuar Bin Zubir, 2022). WoW may assist women to overcome financial hurdles that inhibit women microentrepreneurs from embracing technology to build their businesses by giving microloans.

Self-Assessment of Social Media Skills and Confidence.

Discussion and Implications

The quantitative and qualitative data examined in preliminary discussions consistently reflect the beneficial outcomes of the microcredit, training and mentoring that the women receive through WoW. Results from the natural experiment indicate that WoW’s support helped participants grow their microenterprises, improve their business knowledge and increase their household income. WoW women had better financial capability, well-being and stability than the control group. The positive impacts are also reflected in their personal and family lives. WoW participants reported that they were able to spend more time with their children. This, in turn, had positive flow-on effects on their children’s education. Likewise, their increased empowerment, overall confidence levels and self-efficacy in entrepreneurship are evident. Participants had improved capacity to develop and market new products, predict client demand and network. They also acquired digital skills, which helped them manage the challenges of the COVID-19 pandemic.

Several aspects of WoW’s interventions appear to contribute to favourable outcomes and hold significant implications for research in this area. Importantly, interest-free microcredit enables participants to focus on developing their microenterprise without worrying about escalating debt. In addition, participants are provided practical skills training which enables them to develop their microenterprise, manage their finances, improve their customer service, broaden their customer base, and develop new and innovative products that attract more sales. As each participant is allocated a mentor to support them in developing their microenterprise, the support is individualised to meet specific needs and those of their microenterprise. Participants can opt to join the group initiatives to fulfil corporate orders for festive hampers and other products to earn additional income. This is optional, and some women prefer to focus on their microenterprise and caring for their family members, particularly if they have high needs. Hence, there is flexibility for them to choose what works best for them.

The flexibility and responsiveness of WoW’s program stand in contrast to standard models of microcredit, which emphasise women’s access to credit as a solution to their poverty and a source of their empowerment while neglecting the need for skills training and social support. Banerjee and Jackson (2017) underscore the value of incorporating target communities in co-creating developmental programs and tailoring supports according to the specific needs of such communities. Likewise, McCarthy (2017) emphasises the need to consider the priorities of the women themselves, while Sutter et al. (2019) highlight the importance of local knowledge and input. Prioritising the voices of target communities avoids the unintended consequences that may result when aims and priorities are determined by external institutions that are removed from the lived realities of poverty. Given the diversity of women’s lived experiences of poverty and the multidimensional contributors to their experience, it follows that there is no one or predictable pathway to empowerment (Krenz et al., 2014; McCarthy, 2017). Instead, there is a need for responsive microcredit lending. The practice adopted by WoW of designing its program in consultation with community leaders, as well as feedback from participants, is therefore notable. Women participating in WoW’s program are provided with many opportunities to suggest topics for training and information sessions that are relevant to them or to provide feedback to inform improvements to existing training and supports offered. Their feedback is also sought on matters such as scheduling of training and choice of trainers. Together with the flexibilities embedded in the program for each participant, the women are not simply passive participants; rather, they have an active voice in defining their priorities and needs.

In terms of practical implications, community support and social networks that participants acquire through WoW ostensibly contribute to their empowerment. Supportive leaders and peers share with the newer recruits the strategies that they have learned to help them overcome similar challenges and thrive. These informal supports are not limited to entrepreneurial skills. As they interact during training sessions and work together to fulfil corporate bulk orders, the women share strategies that have helped them manage life better and encourage each other as they navigate the day-to-day challenges of single motherhood and caring responsibilities. The significance of community resonates with Haldar and Stiglitz’s observations on the centrality of community networks, social embeddedness and trust to the success of the early Grameen model (Haldar & Stiglitz, 2016). According to them, ‘it is social capital—broadly interpreted in terms of human altruism and reciprocity—that was the main factor’ that accounted for its accomplishments (Haldar & Stiglitz, 2016). They posit that a reversion to the not-for-profit model and the careful cultivation of social capital is essential to avoid reducing microcredit, which was originally intended to alleviate poverty, to ‘mere moneylending’ (Haldar & Stiglitz, 2016).

A microfinance model that relies on subsidies from third parties to provide interest-free credit raises concerns primarily on the grounds of sustainability. Nonetheless, WoW’s experience indicates that its microcredit funding model, based mainly on corporate donations, is sustainable and has seen an increase in corporate funding in recent years. WoW’s model offers insights into a constructive way in which corporations can contribute to the meaningful empowerment of vulnerable women in collaboration with not-for-profit organisations. As the demand for authentic social impact gains traction internationally, microfinance models that eschew the risks of further entrenching impoverished women at a disadvantage and have targeted support to help women build sustainable microenterprises provide a valuable alternative to the dominant microfinance model.

Conclusion and Future Research

The study indicates that the microcredit, training and mentoring offered by WoW has positively impacted participants across a range of criteria intended to capture the multidimensional concept of empowerment and the transformations experienced by the participating women. Approximately 80% of WoW participants acknowledged the positive effects of WoW on their personal, business and financial well-being. Of particular note is the extent to which these women reported that their engagements with WoW had improved their levels of overall confidence and quality of life. Also of note, while roughly the same proportion of women from both the control group and WoW group identified themselves as head of household, the extent to which women from the WoW group felt in control household decisions, from daily decisions over groceries to household purchases and even long-term investment decisions over family assets is markedly greater than in the control group.

Interest-free loans provided by WoW allow women to focus on growing their microenterprises, while practical training programs enable them to gain new skills. They are further supported through individualised mentoring and being part of a community of women who inspire them to overcome adversity through lived experiences. WoW’s assistance also goes beyond providing women with opportunities to improve their financial well-being; it provides women with the opportunities to develop their leadership skills and develop and lead projects that will benefit their communities collectively. In contrast to standard models, WoW’s microcredit, training and support program is reflexive and responsive to the needs of the women the organisation seeks to assist.

Having acknowledged the importance of the responsive and flexible character of WoW’s model, we do not propose it as a one-size-fits-all solution for micro-credit and enterprises. Rather, WoW’s model and its impact on participants suggest an alternative to the dominant model of microcredit underpinned by assumptions that it is necessary to recoup the cost of lending from borrowers. WoW’s experience reflects the viability of interest-free microcredit and the value of considering an alternative to the more commercialised microcredit model. It suggests that training and mentoring play a critical role in enabling women microentrepreneurs to realise their aspirations of growing their businesses, their own empowerment and contributing to their communities. The analysis emphasises the importance of social embeddedness and corporate support for not-for-profit microcredit and mentoring. At the same time, the study suggests that the leadership of the not-for-profit organisation, its commitment to fostering the well-being of participants, and key leaders’ capacity for building networks with corporate sponsors, play a significant role in the success of WoW’s program. The study was conducted during the tail end of the COVID-19 pandemic in 2022. However, our analysis accounts for these external factors to ensure that the findings reflect the effects of microcredit and mentoring interventions on women microentrepreneurs. Future research could consider longitudinal studies to further validate our findings.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors received financial support only for the original research from the Faculty of Business and Economics Australia–Malaysia 2021–2022 Research Collaboration Development Scheme, but no financial support for the authorship and/or publication of this article.