Abstract

The Women’s Economic Stability Initiative developed and evaluated a new model to help low-income, single women with children make progress toward economic stability through vocational training/educational attainment (particularly in fields traditionally dominated by men), financial assistance for reliable childcare, transportation, and housing, and life coaching/case management using an empowerment approach. During the first 3 years of the initiative, participants made progress in attaining academic degrees, maintaining employment, experiencing modest increases in income, some success in building assets, and paying down/eliminating credit card debt. The initiative provided the support needed to help women gain greater stability for themselves and their children.

Policies and programs to help single women with children achieve financial self-sufficiency have been a major focus of public attention and debate in the years both preceding and following the era of welfare reform 1 (O’Campo & Rojas-Smith, 1998). As low-income families hit 5-year limits on public cash assistance provided under Temporary Assistance to Needy Families (TANF), new approaches for reducing poverty have not kept pace with the need (Pavetti, Finch, & Schott, 2013). Indeed, since the onset of the “Great Recession” and during the continuing economic downturn in the United States, more families are living in poverty than ever before (Danzinger, Chavez, & Cumberworth, 2012).

Beginning in 2004, the Women’s Economic Stability (WES) initiative was developed through a multistage process by the Trio Foundation of St Louis, a private family foundation, to test a new approach to increasing the economic stability of single mothers with children. The new initiative was implemented in collaboration with the YWCA of Metro St Louis, whose mission and core expertise were consistent with those of the initiative. The purpose of this article is to present the program model along with preliminary results of the WES during its first 3 years of operation (Phase 1).

Literature Review

The plight of low-income, single mothers in raising children has been the subject of numerous studies and initiatives (Bullock & Limbert, 2003; Dominguez & Watkins, 2003; Edin & Lein, 1997; Green, 2013). Single mothers not only carry considerable family responsibilities, they also face tenacious challenges to self-sufficiency, including (a) limited education and lack of marketable skills, (b) difficulty in paying for daily expenses like housing, health care, and other necessities, (c) difficulty in finding quality, affordable childcare, and (d) a lack of the financial reserves needed for coping with emergencies (Bowie & Dopwell, 2013; Fields & Casper, 2001; McLanahan & Kelly, 1999; Nichols-Casebolt & Krysik, 1997). Single mothers, when compared to married men, married women, and single women, are the group most likely to be unemployed. In 2009, their unemployment rate was 12%, nearly twice as high as the unemployment rate for married women as well as married men (English, Hartmann, & Hegewisch, 2009). In 2005, among employed single mothers, 40% had household incomes in the lowest quartile of all U.S. workers, with 77% in the bottom 40% of working households (Employment Policy Foundation, 2005). Women have fared more poorly than men during the recession: From October 2009 to March 2010, women lost 22,000 jobs while men gained 260,000 (Joint Economic Committee, 2010).

Low incomes of single mothers are related to low educational attainment: 74% of single women household heads have no more than a high school diploma. They also face income penalties associated with their gender. In 2010, women who worked full time and year-round continued to earn only 77 cents for every dollar earned by men (Hegewisch & Williams, 2011). Education, employment, and income deficits are compounded by other challenges. Low-income women who are interested in postsecondary education are hampered not only by the costs but also by a lack of confidence that they can meet the bureaucratic requirements needed to access that education; single mothers face difficulties in finding adequate study time, keeping up with financial obligations, and spending adequate time with children (Institute for Women’s Policy Research, 2003). In addition, low-income mothers often contend with discrimination in the workplace and in daily living, inadequate access to health care (Ambert, 1998), and the inflexibility and instability of low-income jobs (Miranda & Green, 1999).

Mental health issues are frequently identified among single mothers living in poverty. One study on homeless mothers found that 82% had experienced physical or sexual assaults at some point in their lives, with 63% experiencing assaults from a male partner (Bassuk, Browne, & Buckner, 1996). As Graber and Wolfe (2004) point out “…uncertainty and instability results in single women and their children living an unpredictable life” (p. 62). Not surprisingly, depression is common (Broussard, Joseph, & Thompson, 2012; Hobfoll, Ritter, Lavin, Hulszier, & Cameron, 1995).

Efforts to support the self-sufficiency of female-headed households have fallen well short of their goals. For example, a study of transitional housing programs found that approximately 78% of the participants still demonstrated medium to high levels of welfare dependence, and 33% accrued additional financial debt (Trask, 2009). A report released in 2003 by the Institute for Women’s Policy Reform recommends that job training programs be more accessible to low-income women. The expansion of education and training is necessary to increase skills and the potential for increasing earnings to a more family-sustaining level (Kahne, 2004). Training that prepares women for careers traditionally dominated by men are desirable because these jobs typically pay more than traditional jobs for women. For example, male-dominated work in areas like automotive engineering and construction pay median hourly wages of US$18.04, while traditionally female fields (like childcare, cosmetology, and other service jobs) pay about US$13.80 (National Alliance of Partnerships in Equity, 2006). Studies of vocational training programs for low-income adults have documented increased earnings of 10–156% beyond what similar job seekers were able to gain without training or with job search services only (Rynell, Terpstra, Carrow, & Mobley, 2011). Skills training can also improve access to jobs with benefits. For example, 89% of those who received vocational training through the Annie E. Casey Foundation Jobs Initiative found jobs that provided employer-sponsored benefits (Annie E. Casey Foundation, 2000). Thus, programs that assist low-income mothers with childcare, living expenses, personal support, and vocational training in fields traditionally held by men may be successful in helping increase economic stability.

The WES Initiative: Establishing the Framework

In 2004, the Trio Foundation’s Board of Directors identified “services to increase women’s economic empowerment” as the focus of their first targeted giving initiative. 2 Foundation principals reviewed research, contacted other organizations working for women’s empowerment, and held a series of community meetings with nonprofit and postsecondary educational leaders to gather input. Feedback from community organizations confirmed the need in the St Louis region for a new initiative to support low-income women with children; forum participants noted that “women in the middle,” who were not dealing with severe financial and personal crises but still in need of significant support in building economic security were underserved by current programs and services. 3 Foundation principles utilized concepts from Wider Opportunities for Women (WOW), a national nonprofit organization based in Washington, DC, that provides programs, advocacy, research, and training related to Family Economic Security, Women and Work, Economic Security for Survivors, and Elder Economic Security. WOW’s Economic Security Institute “supports progressive research and advocacy agendas by promoting the discussion, definition, measurement and advocacy of economic security” helping “advocates, policy makers, researchers, practitioners and others employ an economic security framework in their efforts to help workers, families and elders build better lives.” 4 As part of their Family Economic Security Project, WOW defined the following strategies as vital to financial empowerment for low-income women: (a) promoting economic security as defined by a Self-Sufficiency Standard, 5 (b) targeting higher wage and nontraditional employment, and (c) promoting Individual Development Accounts (IDAs). Foundation principals also contacted the Eleanor Foundation, a research-oriented grant maker in Chicago that not only provides financial support to programs that help working women who head their own households but also collaborates in providing career education and access to affordable housing, dependable childcare, and financial coaching. 6 Discussions with this foundation yielded additional recommendations, including (a) targeting women with the potential to achieve economic stability within a relatively short time; (b) identifying a lead agency, with expertise in job training and placement, to administer the initiative; and (c) employing a case manager who fills the role of a “mentor” or “coach” in working with participants. Following this planning period, the Trio Foundation set three directives. Due to the amount of funding available, the initiative would target a smaller group of women (10) rather than attempting to reach a large number. Direct service would be a central element of the initiative. The administrating organization would use “empowerment” approaches in working with participants, making specific decisions about how to provide assistance and services within a general program framework provided by the foundation. Women in the initiative would be (a) educated for higher wage jobs, primarily in nontraditional fields; (b) earning incomes that provided economic stability at the end of 3–5 years; (c) supported while pursuing vocational education with reliable and safe housing and childcare, health benefits, and reliable transportation; and (d) participating in a savings or asset development program.

Theoretical Perspectives

These directives are in alignment with social justice and feminist theoretical perspectives by recognizing that individual struggles are often rooted in oppressive social, political, and cultural environments, and that, in the face of these oppressive systems, individuals must be empowered in order to make progress (Atkinson, Thompson, & Grant, 1993; Morrow & Hawxhurst, 1998). In this case, the oppressive systems included (a) a job market that did not reward women with positions that paid enough to support a family and that judged “women’s work” to be less valuable than “men’s work”; (b) a punitive and rigid public welfare system; and (c) an educational system that was inaccessible to low-income single women who were also raising children. As Parsons, East, and Boesen (1994) noted “welfare reform” programs in the United States typically focus on job training and financial assistance without taking into account the effects of oppression and disempowerment experienced by low-income, single heads of households. Addressing women’s oppression includes reducing the power differentials between men and women (Trautner & Smith, 2006), which the initiative sought to accomplish through empowerment and education within the existing power structure. Social work models based on empowerment are vital when working with women who are disempowered by constraints at both the individual and societal levels, including women in poverty and victims or survivors of domestic violence (Mills, 1996; Parsons, 2001; Parsons, East, & Boesen, 1994; Prigoff, 1992). Further, the education of women has long been recognized as an empowerment strategy for addressing the power differential between men and women (Stromquist, 2002). The initiative approach was also based on a human capital perspective, positing that education would increase productivity and economic growth, in part by improving individual decision making and systematic thinking (Denison, 1962; Wozniak, 1984). The initiative also incorporated an asset development approach with the belief that accumulating assets is vital in achieving economic stability in the United States, hypothesizing that, when individuals develop assets, they are better able to focus their efforts, take reasonable risks, maintain a future orientation, and further develop their human capital (Sherraden, 1991). Research has supported this premise, finding that the ownership of assets is associated with benefits like self-efficacy (Moore et al., 2001), higher self-esteem (Rohe & Stegman, 1994), and higher educational attainment of children (Zhan, 2006). Finally, savings and financial assets are associated with greater economic security among female-headed households (Rocha, 1997; Sanders & Porterfield, 2010) and are an important consideration in helping women who are victims of domestic violence achieve financial independence from their abusive partners (Sanders & Schnabel, 2006; Sanders, Weaver, & Schnabel, 2007).

Service Model

Through a competitive proposal process, the Trio Foundation selected the YWCA of Metro St Louis as the administering organization because (a) its mission and core expertise were consistent with those of the initiative, (b) the YWCA had demonstrated past success with the target population, (c) the agency’s case management philosophy was empowerment based, and (d) personnel to staff the initiative were already in place. The final initiative service model included (a) the provision of financial assistance over 3–5 years to cover tuition and books plus help with housing, childcare, transportation, and health care costs, (b) one-on-one life coach/case management sessions to set goals, provide intensive support, and monitor progress, (c) financial counseling and support in opening bank accounts and building other assets, 7 and (d) group meetings, seminars, and mentoring from women in the community. The fulfillment of the planning process began with the selection of the first class of participants in the fall of 2007.

Method

During the initiative planning phase, Trio principals contracted with an external evaluator 8 to assist with community forums and develop a simple logic model to articulate program activities along with short- and long-term targeted outcomes. The evaluator, in collaboration with initiative staff, developed a questionnaire and rating scale that was used in the participant selection process. This instrument addressed needs and areas of stability (strengths) with rating scales in education, employment, income, debt, housing, childcare, health care, mental health, and transportation. After participants were selected, progress in each of these areas was documented by the Life Coach/Case Manager (LCCM) using forms created by the evaluator to track school enrollment, grade point averages (GPAs), and degrees completed; employment positions, number of hours worked, and hourly rates of pay; levels of credit card and other kinds of debt; balances in bank accounts and IDAs; appropriateness of housing situations for family stability; quality and stability of childcare services; follow through with mental health and other needed services; and other indicators of progress. This information, along with detailed case notes, was collected/kept by the LCCM during monthly check-ins with participants and submitted without the use of any participant identifying information to evaluators, who entered all quantitative data into Statistical Package for the Social Sciences for analysis. The LCCM also submitted monthly reports on the number of hours she devoted to each participant, the nature of their contact, and the amount of financial assistance each woman received and for what purpose. An evaluator conducted twice yearly participant interviews to verify overall outputs and outcomes and to gather qualitative data on other life changes. 9 Reports of evaluation results were provided to Trio principles, YWCA staff, and other stakeholders on a twice yearly basis so that results were used in program improvement.

Initiative Participants

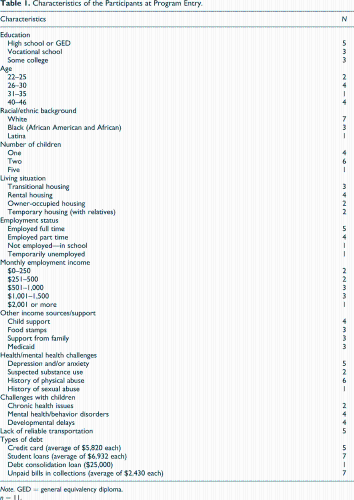

The WES Initiative served 11 women from November 2007 until the end of Phase 1 in June 2010. Forty-five women were referred from area educational institutions and human service providers. An intensive application and interviewing process with the aforementioned ratings of prospects’ levels of needs and strengths helped staff select participants who were mostly stable in terms of mental health, substance use, and basic needs, and who were also either currently enrolled in an educational program or interested in enrolling to pursue jobs that paid living wages including through male-dominated occupations. These considerations led to the selection of 8 women from the original applicant pool of 45 in November 2007. In May 2008, another two women were accepted. Later in 2008, one woman dropped out of the initiative to start her own business, so another participant was accepted to take her place, bringing the total number served to 11. 10 As Table 1 shows, women faced significant challenges when they began participation that included the lack of permanent housing histories of domestic violence, the lack of child support payments from fathers, mental health needs, and the special needs of their children. Most of the women were also carrying high levels of debt while half reported a lack of reliable transportation. Although they needed additional support to maintain functioning and make ends meet, these women were also perceived to be stable and resourceful enough to make significant progress.

Characteristics of the Participants at Program Entry.

Note. GED = general equivalency diploma.

n = 11.

Initiative Services

Financial Assistance

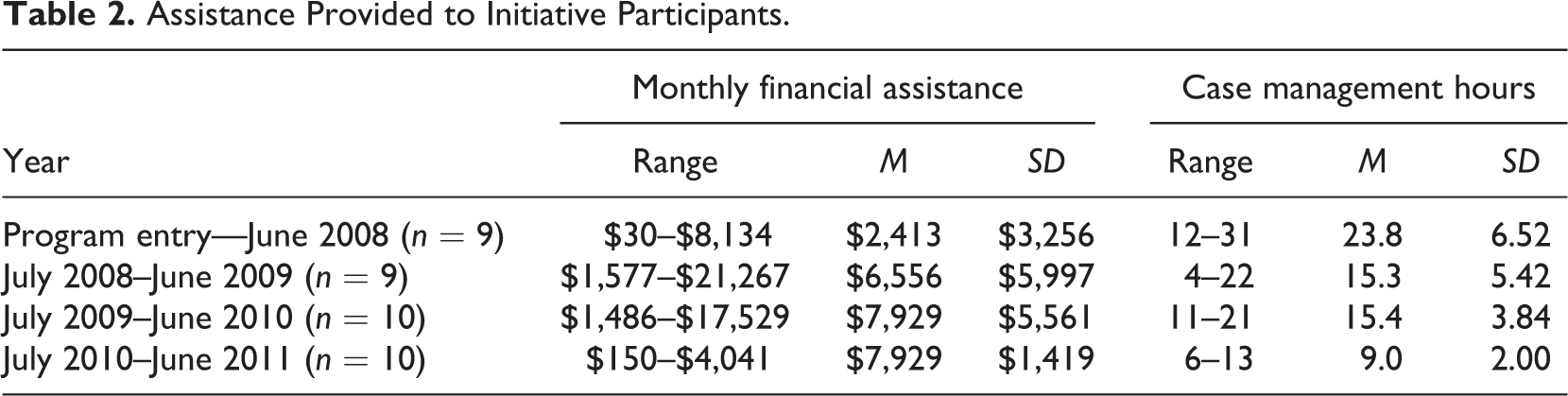

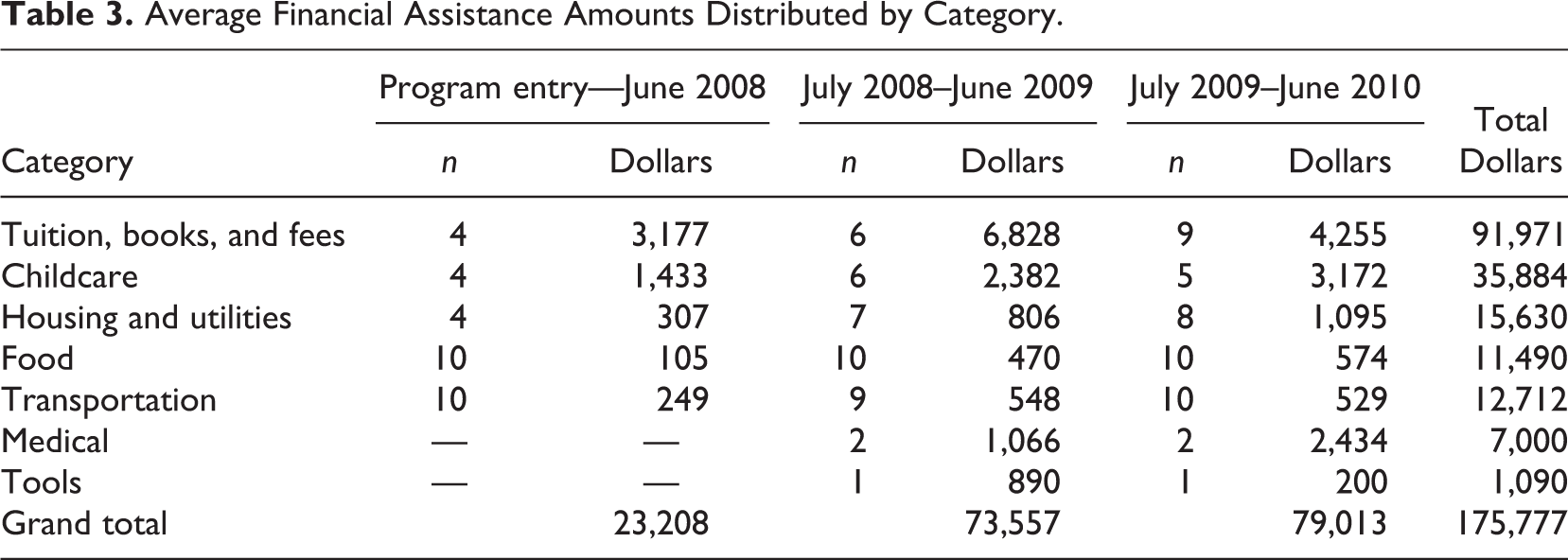

A cornerstone of the initiative was the provision of financial assistance as participants pursued their educational and employment goals. Individual assistance levels were flexible, based on need and ongoing discussions between the women and the initiative LCCM, a social worker involved with the women’s transitional housing program at the YWCA. Altogether, more than US$175,000 11 was distributed over the first 3 years of the initiative with individual levels ranging from US$1,474 to US$26,238 per calendar year (see Table 2 for details of monthly financial assistance levels by program year). Participants had varying needs for assistance, which tended to change over time (see Table 3). The largest category of assistance provided covered tuition, books, and fees, followed by funds for childcare, housing and utilities, and transportation. Smaller amounts were provided for food assistance, medical costs, and tools or special supplies needed for new occupations.

Assistance Provided to Initiative Participants.

Average Financial Assistance Amounts Distributed by Category.

Life Coaching/Case Management

The LCCM delivered a total of 479 hr of one-on-one coaching to address participants’ immediate and longer term needs during Phase 1. These services were provided from an empowerment perspective in which the LCCM interacted with participants as more of a coach and facilitator than a traditional case manager. Sessions included reviewing budgets and helping women access more stable and adequate services. Primary topics addressed during these sessions (in order of frequency) include school, employment, debt reduction, medical needs, 12 housing needs, and childcare. The LCCM coached participants in applying for school, choosing majors, selecting classes, creating or revising resumes, locating employment opportunities, applying for positions, interviewing for jobs, following up with prospective employers, and negotiating, when needed, with educational institutions and employers to address individual difficulties in maintaining stable and productive experiences. As with financial assistance, the hours of direct service provided varied widely depending on the needs of individual women, which changed over time. The number of hours provided on an annual basis ranged from 11 to 31 per person (see Table 2). Several women experienced declines over time in the amount of time needed, while others remained relatively stable. A number required services from other organizations, including programs for women who had experienced domestic violence. Although financial assistance and coaching were the keystones of the initiative, the program was also designed to include workshops to help women further develop life skills; peer groups for social support; and mentoring with women in the community who could provide guidance in helping participants realize their career goals. However, these components did not develop as originally envisioned due to logistical issues and concerns that group meetings or mentor appointments would put additional strain on women’s already overburdened schedules.

As a result of the financial assistance (which gave women some relief from financial stress) plus the LCCM’s support, the women in the Economic Stability Initiative experienced a number of social/psychological benefits that were a vital link between services and the preliminary outcomes described in the next section. These benefits include an increased motivation to change and improved coping skills. 13 During interviews with evaluators 9 months following the initial start-up phase, participants were overwhelmingly positive about the support they received from the LCCM. 14 Even after a relatively short time in the initiative, nearly all the women believed they were able to manage daily challenges more effectively.

Initiative Results

The services described in the previous section were designed to help participants make progress in achieving economic stability. Interim outcomes that support this overall goal include enrollment into and graduation from postsecondary educational programs, job attainment, increases in income, decreases in debt and increases in savings, and more stability in the areas of transportation, housing, and childcare. 15

Educational Outcomes

All WES participants enrolled in, or, if they were enrolled at the time they entered the initiative, continued in an educational program leading to an associate’s or bachelor’s degree. Five enrolled in a private technical college, three in community colleges, and two in public universities. All of these programs were accredited and provided degree programs suited to the goals of both the initiative and the women themselves. Enrollment levels rose from program entry with all women in school at the end of 2008 and through most of 2009. By 2010, two women were no longer in school because they had completed their programs, and another two women were facing difficulties that required them to take a break from their educations. 16 Overall, during the first phase of the initiative, 8 of the 10 women were successful in maintaining enrollment in programs leading to bachelor’s or associate’s degrees.

In addition to maintaining enrollment, all women maintained GPAs of 2.7 or above, meaning they were making satisfactory progress toward their degrees. As of June 2010, five women were maintaining GPAs of 3.0 or above, signifying that their progress was well above average. Furthermore, six women graduated in the first 3 years of the initiative, with five attaining 2-year degrees and one earning a bachelor’s degree. Three of those who earned associate’s degrees went on in school to earn 4-year degrees, while the woman who earned the bachelor’s degree enrolled in graduate school. Degrees earned were in the following fields: electrical systems design technology, automotive maintenance technology, automotive collision repair technology, architectural technology, engineering science, and construction management. True to the original intent of the initiative, the degrees earned by participants in the first 3 years were in fields that did not traditionally involve women. 17

Employment and Income Outcomes

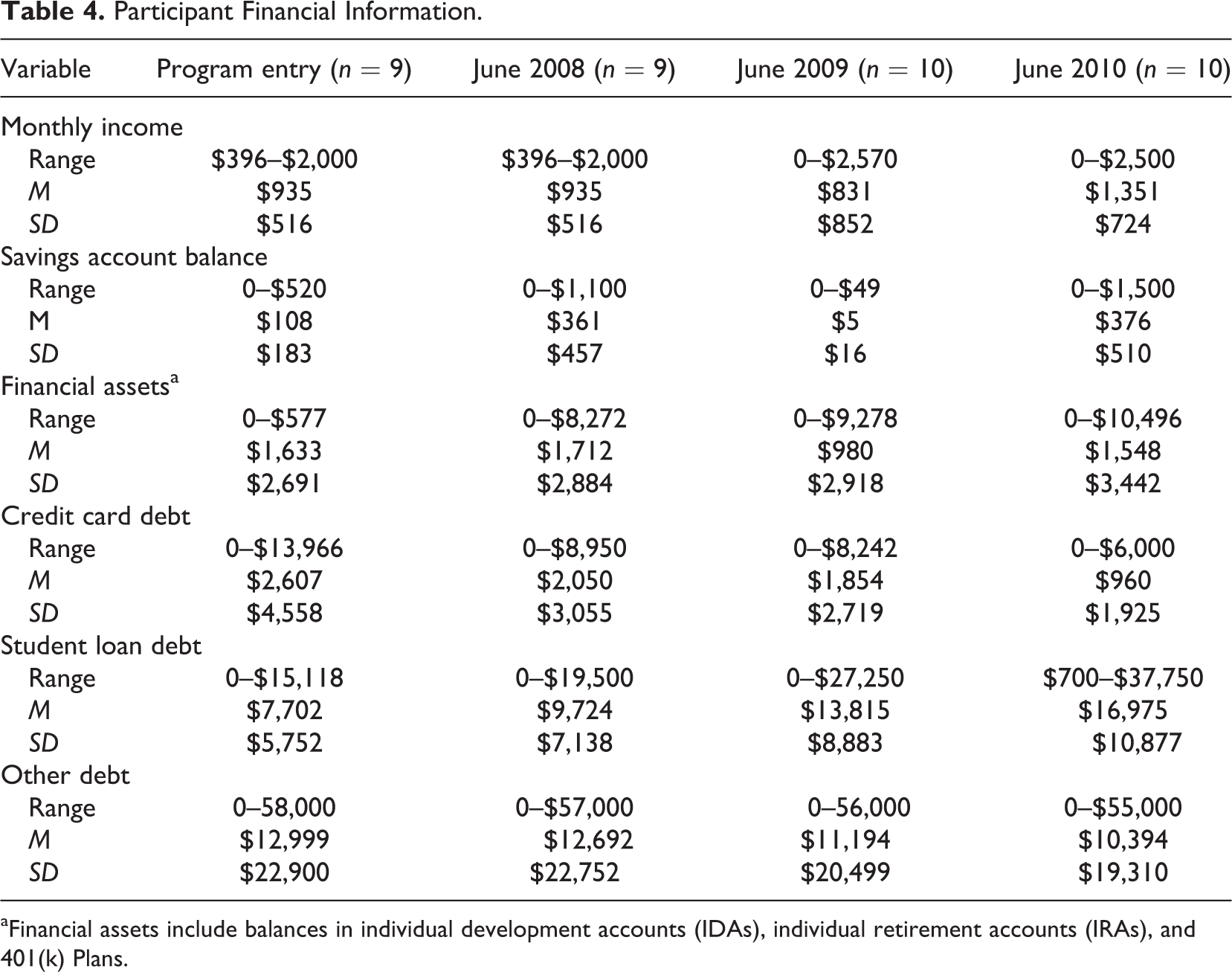

Three women graduated and found jobs in their new fields. For example, in October 2008, one woman completed the requirements for an associate’s degree in automotive maintenance technology, quit her pizza delivery job, and obtained a job with benefits with an automotive company paying US$10 an hour. She began working 20 hr per week in 2009 with hours increasing to full time in 2010. Most of the women were able to maintain either part-time or full-time employment throughout Phase 1. At various points, some participants (typically, one or two per year) experienced times of unemployment or underemployment due to layoffs. However, success in maintaining some level of employment is particularly noteworthy because all of them (except for two in the last year of Phase 1) were also in school and making satisfactory progress toward their degrees, while also caring for children. The time frame for Phase 1 coincides with what the National Bureau of Economic Research refers to as the Great Recession which began in December 2007 (Hurd & Rohwedder, 2010). During this time period, more than half (55%) of the adults in the U.S. labor force experienced some type of work-related hardship, including spells of unemployment, cuts in wages, and reductions in hours (Pew Research Center, 2010). Thus, in spite of high demands on their time and the impacts of the recession, participants were relatively stable in terms of employment. As a result, a number of them experienced increases in earned income. As Table 4 shows, the average income at program entry in 2007 was US$935 per month; by June 2010, it had increased to US$1,351, a 44% increase.

Participant Financial Information.

aFinancial assets include balances in individual development accounts (IDAs), individual retirement accounts (IRAs), and 401(k) Plans.

Although participants were able to maintain employment while completing degrees and achieving modest increases in income, personal academic goals affected their abilities to earn higher incomes. The initiative’s original intent was to help women earn 2-year degrees and then enter the workforce full time in their new fields. However, several women, after experiencing success at school, decided to pursue bachelor’s degrees, which meant a higher probability of earning living wages after graduation, but also meant that they chose to delay earning more during the first phase of the initiative.

Asset Development

One of the initiative objectives was to coach and support women in building savings or asset accounts to give them a firmer foundation for long-term security. This approach was successful to some extent. One woman made steady progress in building her savings. When she entered the initiative, her account had a balance of US$200; by June 2010, the balance had increased to US$1,000. Three women saved for and bought automobiles for more reliable transportation, with two of them using IDA accounts 18 toward their purchases. One of these women increased the balance in her IDA from US$120 at the time she entered to the initiative to US$4,500 in June 2010, a striking increase, while another woman experienced steady increases in her individual retirement account (IRA) balance, beginning at US$7,577 at program entry to US$10,496 by June 2010. Altogether, 6 of the 10 women in the Economic Stability Initiative made progress toward increasing their financial assets during Phase 1. This outcome is noteworthy at a time when average household wealth (assets) in the United States fell about 20% from 2007 to 2009 (Pew Research Center, 2010).

Debt Reduction

Most participants were carrying significant levels of debt when they entered the initiative. Six women carried credit debt ranging from US$900 to nearly US$14,000, and many were making ends meet by putting every day expenses on credit cards without paying off their balances. By the end of Phase 1, women were no longer charging everyday expenses, and altogether, had paid off more than US$20,000 in debt. At program entry, the average level of credit card debt was US$2,600 per person; by the end of Phase 1, the average balance had declined by 68%, to an average of US$960 per person, with 7 of the 10 ongoing participants carrying no credit card debt at all. These results indicate success for a number of reasons. First, a number of women had used credit cards for daily expenses without paying off their balances and were in a cycle of debt accumulation when they entered the program; however, this behavior stopped with the assistance they received from the initiative. During the same time period, average debt in American households increased while credit card interest rates and late payment amounts also increased. 19

Regarding other debt, women added significantly to student loan balances during participation. At program entry, they carried an average student loan debt of US$7,700 each; as of June 2010, this amount had increased to nearly US$17,000. 20 Although women received degrees in return for their investments, this represents significant debt for individuals who were still low income. Nonetheless, the terms of and interest rates on these loans were much more favorable than for credit cards. Women made additional progress paying down other kinds of debt, like mortgages, unpaid utility bills, medical bills, and bank/credit union loans. At program entry, each woman carried an average of US$13,000 in debt other than credit card and student loan debt. By June 2010, this amount had decreased by 26% to an average of approximately US$10,400.

In addition to the progress of women in education, employment, income, and reduced debt, initiative participants experienced other positive changes. Three women were able to move into better housing situations. Other women gained more stable and better quality childcare for their children. These supports made it possible for women to continue their progress toward education and employment goals while providing a better foundation for their families’ futures.

The Future of the Initiative

The 10 women who participated throughout Phase 1 of the WES Initiative continued receiving a reduced level of financial and case management/life coaching support during a second phase of the program from 2011 through 2012. Each woman completed a “continuation agreement” with initiative staff that outlined the types and amounts of assistance they would continue to receive. In return, the women agreed to participate in monthly sessions with the LCCM, seminars and group sessions, and continued progress in school (for those who had not yet graduated). In addition, the YWCA received funding from the Trio Foundation and other sources to begin a new cohort of the initiative in 2013.

Discussion

The results of the first phase of the WES Initiative provide evidence that the program was successful in retaining participants who experienced numerous benefits from the financial assistance and life coaching services provided. These benefits include positive improvements in family stability; significant educational accomplishments, including academic success in 2- and 4-year programs in a number of fields traditionally reserved for men, and the completion of degrees by six women; success in gaining and maintaining employment on either a part-time or full-time basis; modest increases in monthly income, with three women gaining employment in their new fields and two others gaining positions in related areas; progress toward increasing financial assets (balances in IDAs, IRAs, and 401(k) Plans); and progress in paying down credit card balances and other kinds of personal debt (other than student loans). These single mothers made progress in building human capital while greatly reducing their dependence on credit cards and increasing both tangible and intangible assets, laying the foundation for their ability to earn living wages in the future. The opportunity to participate in setting and achieving life goals with the extensive support provided by the LCCM, and the ability to request and receive financial assistance according to their individualized needs, helped empower these women. By completing degree programs and attaining work in male-dominated fields, they succeeded in overcoming some of the barriers that hinder women from achieving economic parity with men.

Recommendations

For future adaptations, it is possible that more progress in the areas of employment and income could have occurred if the peer support and mentoring components of the initiative had been fully developed and implemented. 21 Networking may have given the women the additional contacts, information, and the impetus to find additional opportunities in their traditionally male-dominated fields. Having a stronger support network outside initiative staff may have helped some women move on to employment in their new fields rather than choosing to go on in school. The decisions to stay in school contributed to growing dependence on student loans, resulting in high balances that may place additional burdens on mothers after initiative completion. Nonetheless, the results of Phase 1 of the WES Initiative suggest that this model has shown a level of effectiveness that makes it worthy of future replications and refinements, along with more comprehensive research studies involving control or comparison groups to further evaluate outcomes on a long-term basis.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Our work was funded by a private family foundation, the Trio Foundation, located in St. Louis, Missouri. They also funded the initiative that is the subject of this article.