Abstract

Formulating business strategies in times of economic uncertainty can be a challenging exercise because of rapid changes in market assumptions, projections, and conditions. Studies have shown that the repertory of strategic choices that businesses explore, to handle uncertain economic environments, is not highly varied. This article reviews the strategic responses that leading Indian auto manufacturers have adopted in order to handle the dip in demand post COVID-19. Given that the Indian automobile industry has been facing headwinds since 2018, the COVID-19 pandemic could not have hit the sector at a more inopportune time. This article aims to review how firms in the sector ride through an economic slump and also sheds light on strategic decision-making patterns

The article exclusively focuses on leading automobile firms and does not analyze actions taken by comparatively smaller players to stay afloat. Hence, this article does not delve into the actions that suppliers and dealers are exploring. Most importantly, this article contains a comprehensive analysis of the financial performance of a few auto majors. This article seeks to piece together a picture of firm-level strategies on the basis of publicly accessible financial statements and news reports.

Keywords

Introduction

The automobile industry plays a significant role in the Indian economy. While, the continuous domestic growth of the industry at 2.36 percent compound annual growth rate (CAGR) between the fiscal years (FY) 2016 and 2020 (Automobile Industry in India, Indian Automobile Industry, Sector, Trends, Statistics, n.d.) has transformed the sector into the fourth largest automobile market, firms in the sector have also faced periodic slumps. As a matter of fact, the sector has seen a dip in sales, on four different occasions, over the last two decades (Sridhar, n.d.). However, these have been substantially different from the kinds of declines firms in the sector have witnessed since 2018.

Considering the rapid decline in sales volumes since 2019, automobile manufacturers have been bombarded with a plethora of strategic choices. A report by the Boston Consulting Group (Auto Companies Will Outlast COVID-19, n.d.) mentions a wide range of actions actively adopted by various players in the automobile industry, globally. These include revamping the supply chain, driving cost reductions in various areas of operation, and exploring customer-focused makeovers. Another article by The Financial Express (Post Lockdown Recovery for Auto Industry, n.d.) lists India-specific strategies such as adopting virtual vehicle certification, making cosmetic design changes, and ensuring supply chain sustainability.

Since the sector’s fortune is dependent on its wide range of stakeholders and the economic conditions, choosing the optimal set of strategies from the available pool involves a substantial risk. This is why, perhaps, businesses in this sector may pursue an incremental set of strategies rather than those that can be a bold break from the past.

A close reading of the strategies followed by most of the firms in the automobile sector can help establish choice patterns but may still not offer a model to explain why a particular firm walks a specific strategic path. Accordingly, there are various reports and studies that offer details of strategies pursued by automobile firms, in general. But these do not offer a firm-level understanding of why specific companies pursue a particular direction. It is therefore imperative to explore a firm-level analysis of strategic decision-making in order to help businesses understand the promises and limits of both imitating and deviating from generally recommended strategies (what’s good for the geese may not be good for the gander) followed by other players in the sector.

According to the Automotive Component Manufacturers Association (ACMA), Micro, Small and Medium Enterprises (MSMEs) play a big role in the manufacturing of auto components, in that they contribute over 6 percent of the country’s manufacturing GDP (Economic Bailout Package, n.d.). Many of these MSMEs supply automotive parts to large automobile manufacturing firms. Whereas the exact level of dependency on a particular Indian automobile manufacturer is a matter of conjecture, any change in the fortunes of a large manufacturer is generally known to impact MSME suppliers adversely. Consequently, the strategies adopted by any of the automobile majors can significantly influence strategy making at the MSME level.

There are several motivations for undertaking basic research into strategies adopted by specific auto majors in response to the vagaries of the Indian marketplace. Downturns represent a pivotal point in the life of an organization. Major decisions taken during an uncertain economic environment have the potential to create long-lasting impact on the sustainability and growth of an organization. Through an analysis of the strategic responses of Indian auto majors to address the adversity accompanied by the COVID-19 pandemic, a perspective on how they should handle market uncertainties while ensuring business sustainability has been discussed in this research. It also offers insights into how these firms adapt to volatile market conditions by dipping into opportunities that may present themselves during a downturn. Additionally, alternative strategic considerations by the original equipment manufacturers (OEMs) have also been discussed so as to help them recognize the opportunities and thrive through these times. To epitomize, this research addresses the following three major concerns: ‘What are the strategies which the major Indian OEMs have adopted in response to the pandemic?’, ‘What are the limitations of the strategic choices made by them?’, and ‘What other strategies can be considered to make the most out of the opportunities brought by the pandemic in order to sustain the harshly hit Indian auto sector?’

What Is a Business Strategy? Why Is it Essential to Have One?

While business strategy was initially conceived as a form of business policy by 20th-century organizations, its roots can be traced as far back to the dawn of civilization when classical religious texts and epics began to be composed in various cultures. Additionally, ancient treatises on statecraft and military expeditions have also contributed to the present-day understanding of strategy (Edwards, 2014). According to Britannica (Strategy | Military | Britannica, n.d.), the military origins of the term cannot be missed since the word is derived from the Greek word ‘strategos’, which means ‘an elected general’ who ‘combined military and political authority’.

After World War II, during the 1950s and 1960s, strategy found a place in the business world because of the works of management theorists such as Alfred Chandler, Philip Selznick, Igor Ansoff, and Peter Drucker (Business Strategy, n.d.).

Definitions

It is clear from the various definitions that engaging in strategic planning can yield financial as well as non-financial benefits; for instance, the right actions or decisions can help a firm to generate and sustain profitability over a long period of time as well as avoid bankruptcies and unwarranted restructuring. Moreover, since strategic planning relies on robust coordination between different actors inside and outside the firm, the communication of plans across the organization can result in shared understanding of organizational strategies among all stakeholders, as well as an improvement in alignment and commitment within the workforce.

Oddly, while it is common to come across firms that have transformed strategic planning into a regular management ritual, not all have a formal process for discussing and evaluating strategies or even frame long-term strategies. This might be due to lack of formal training in strategic management, limited understanding of the benefits of strategic planning, or negative experience with strategy formulation and implementation processes (Why Some Firms Do Not Do Strategic Planning, n.d.). Since it is not known whether the practice of having a formal strategic planning process offers any specific advantage to firms when compared with firms that do not have formal and informal planning processes, existing studies do point out a clear link between planning processes and firm performance. Hence, it becomes extremely essential for a firm to consider a wide range of strategic choices, especially when pushed to handle the situations caused by economic uncertainty.

What Is an Economic Uncertainty and How Is it Different from a Recession?

Economic uncertainty, referred to as ‘uncertainty’ hereafter, refers to a condition in which businesses find it extremely challenging to predict the future performance of industry and economy. Such situations also lead to apprehensions about the type of economic events that would follow. Accordingly, adverse events are known to accompany periods of economic uncertainty.

Whereas rising economic uncertainty can slow down the growth of economic activity (Uncertainty and the Economy, n.d.), its exact role in producing a recessionary economic climate is not quite clear (Economic Uncertainty and the Great Recession, n.d.). As per a Forbes article (Rodeck, 2020), recession is defined as ‘a significant decline in economic activity that lasts for months or years’. Recession might not always result due to uncertainty. And though such periods of economic decline have been preceded by uncertainty, they do not have the same impact as certain powerful events such as the dot-com bust of the late 1990s, the Great Recession of 2008, and the economic downturn due to the COVID-19 pandemic.

How Do Strategies for Uncertainties Differ from Stable Times?

Research into firm-level decision-making practices, especially during uncertain periods, point out the pervasiveness of cost-cutting measures across industry (Courtney et al., 1997). With the advent of any kind of crisis, it is normative for firms to focus more on survival through cost reductions rather than risky investments. Also, given the kind of uncertain outcomes including that of insolvency, associated with potential decisions, firms may adopt a highly conservative and conventional approach to managing operational costs. One of the most influential pieces of research on types of strategies adopted by firms when facing economic uncertainties also endorses the view that firms utilize a crisis to shed various types of costs (Gulati et al., 2010b). Also, as per a report published in the Business Research Quarterly (Santana et al., 2017), one of the most commonly used cost-cutting strategies is to lay off a section of workforce. Obviously, various cost management measures have certain short-term and long-term implications. A study by McKinsey & Company (How Top Companies Use Resilience Strategy, n.d.), a management consulting firm based in the USA, has pointed out the shortcomings inherent in exclusively focusing on cost control measures alone during a downturn. Hence, it is not uncommon to find companies try out both cost control measures that help contract costs as well as investment measures that lead to cost escalations. Obviously, whether a firm decides to pump capital to fund expansion and/or explore options to shed resources to manage costs, perceptions about current and future uncertainty, as well as likely trade-offs from various strategic choices are bound to influence strategic decision-making.

A firm’s strategic behavior during periods of uncertainty offers interesting insights into how various measures targeting top-line and bottom-line improvements are explored. For firms focusing purely on survival, bottom-line focus is most likely to take precedence over growth-focused top-line maneuvers that may entail additional investments. As survival strategies are implemented and begin to show results in terms of cash flow and bottom-line improvements, firms are likely to change gears and focus on growth enhancing measures. A study by Bain & Company (Beyond the Downturn, 2019), yet another American management consultancy firm, reveals that these changes in priority or focus and strategy during a downturn have been compared to navigating ‘a sharp curve on an auto racetrack - the best place to pass competitors, but requiring more skill than straightaways. The best drivers apply the brakes just ahead of the curve (they take out excess costs), turn hard toward the apex of the curve (identify the short list of projects that will form the next business model), and accelerate hard out of the curve (spend and hire before markets have rebounded)’.

Although uncertainties lead to a substantial surge in stress levels in the market, they are also known to offer a unique set of opportunities; for instance, during uncertain times, as firms with potential cut down on costs and explore divestitures, companies with cash explore acquisition strategies. This unique mix of offensive and defensive strategies during a downturn has interesting long-term consequences for firms in an industry. Accordingly, for firms that are interested in bottom-fishing, economic uncertainties help to acquire resources at bargain prices (The Case for M&A in a Downturn, 2020).

Given that economic uncertainties place constraints on the type of strategies a firm can explore, various notable attempts to classify these strategies have resulted in interesting insights about strategic behavior during a downturn; for example, researchers at Kingston University (Kitching et al., n.d.) classify the business strategies which enterprises tend to adopt in recession conditions into three categories:

The Indian Auto Sector

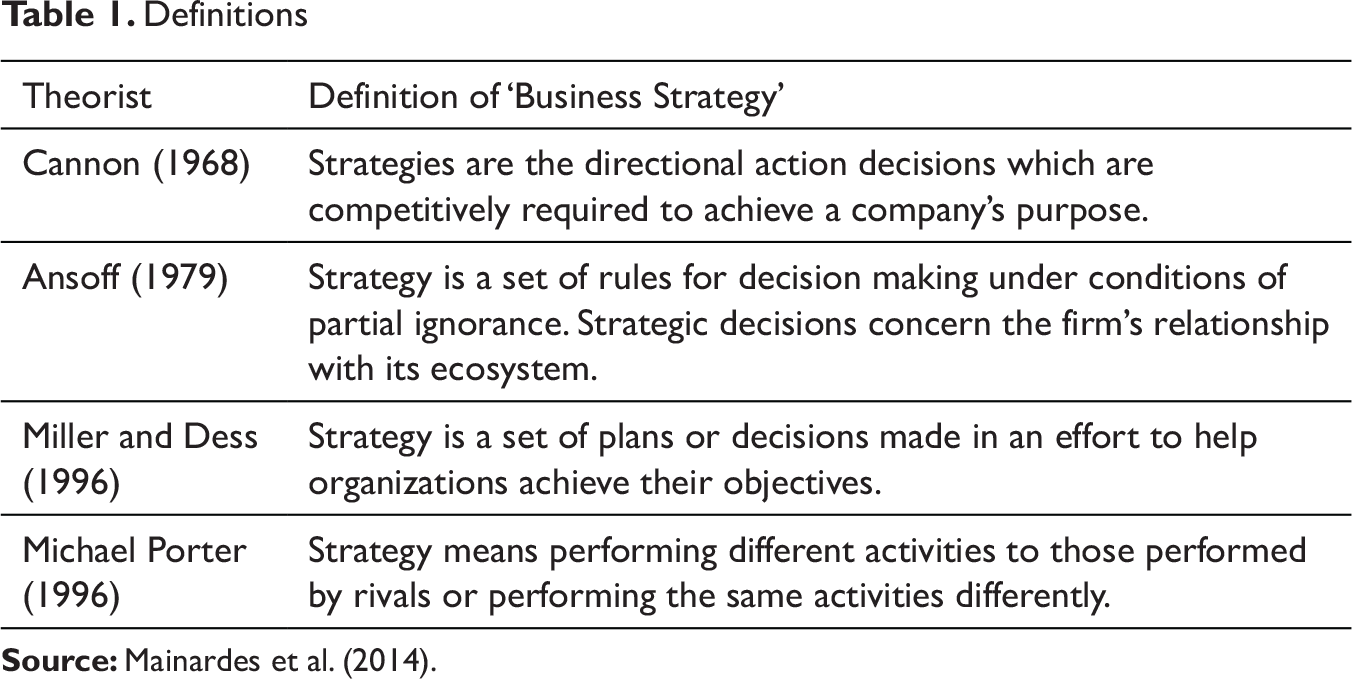

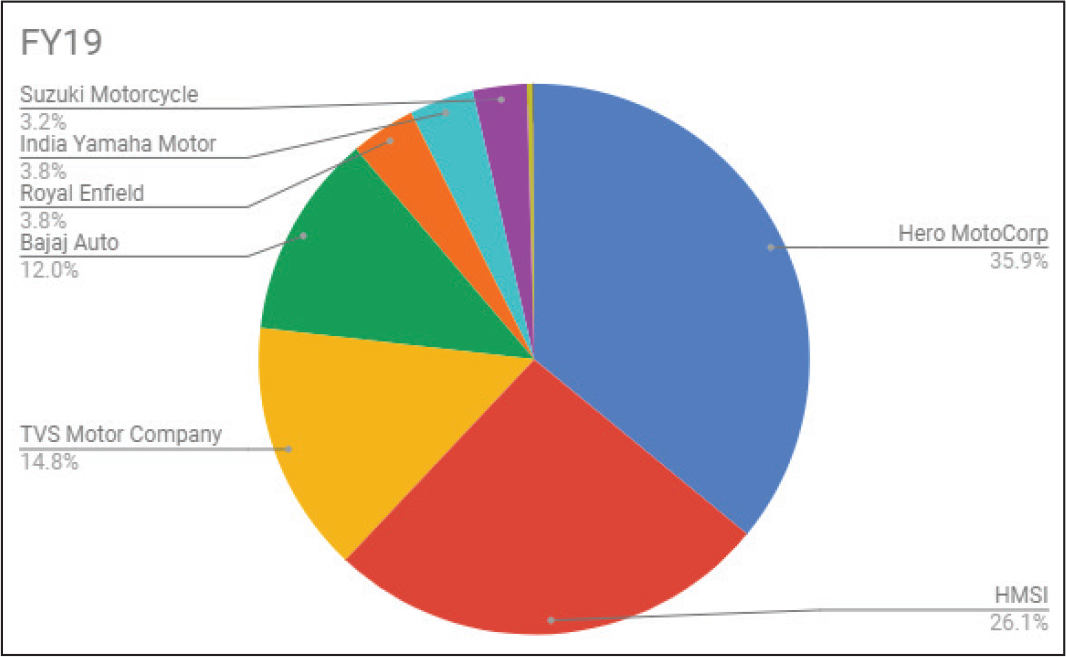

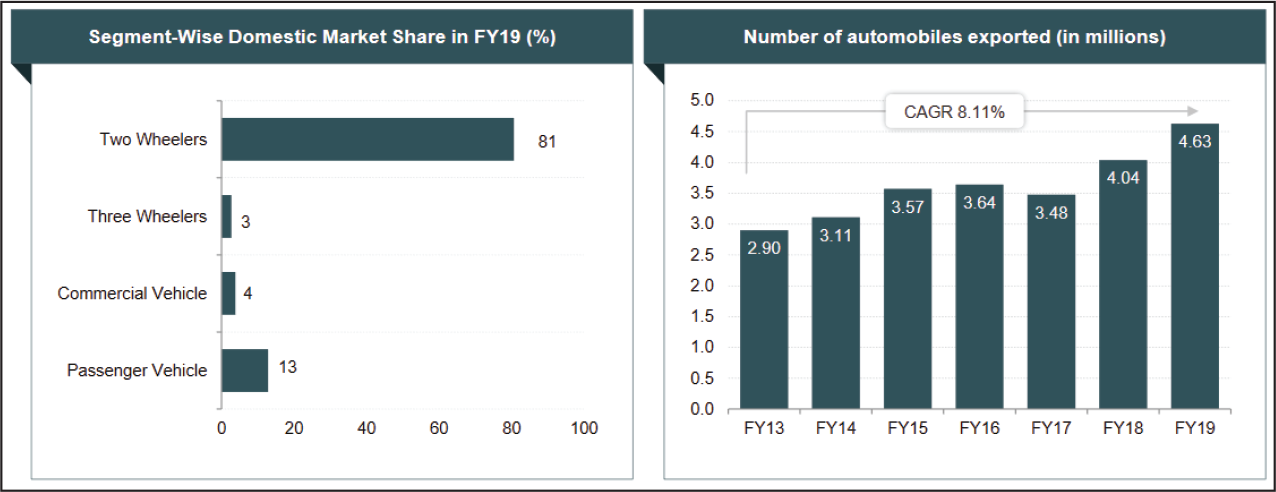

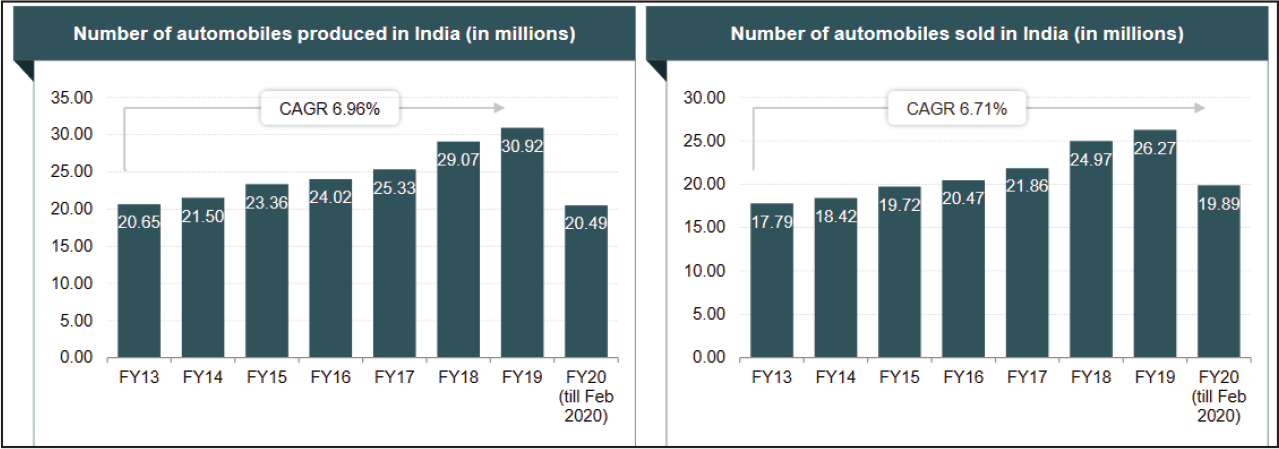

The Indian automobile sector is one of the biggest automobile manufacturing markets across the globe. Various reports (Automobile Industry in India, n.d.) indicate that India is already among the top economies for manufacturing tractors, buses, two-wheelers, three-wheelers, heavy trucks, and cars. As per a report published by Indian Brand Equity Foundation (Automobiles-March-2020.Pdf, n.d.), the Indian automobile market was ranked as the 4th largest in the world in 2018 with an increase in sales by 8.3 percent year-on-year to 3.99 million units. The domestic sales and production of automobiles went as high as 6.71 percent and 6.96 percent of the CAGR, respectively, between FY 2013 and FY 2019. A total of 26.27 million vehicles were sold in FY 2019 out of the 30.92 million manufactured. In the very same FY, automobile exports grew by 14.5 percent year-on-year, with premium motorbike sales leaping to 13,892 units sold and that of luxury cars between 15,000 and 17,000 units in the first half. Commercial and passenger vehicle sales also were as high as 678,486 units. Figures 1 and 2 reveal the market shares of two-wheeler and four-wheeler OEMs, respectively.

While automobiles have been on Indian streets since 1897 (The First Wheels Roll into India, n.d.), the country had no automobile manufacturing facilities till the 1940s, and therefore, depended on imports from other countries. Hindustan Motors set up the very first manufacturing plant in India in 1942, followed by Premier Motors in 1944. However, both were not completely independent and functioned under the mentorship of General Motors & Fiat (Google Books Link, n.d.). In the same decade, Mahindra & Mahindra also initiated the production of utility vehicles (08_chapter 2.Pdf, n.d.).

After Independence, the government tried to boost industry by encouraging automobile manufacturing, locally. The 1950s turned out to be somewhat stagnant for the industry due to trade restrictions imposed on imports. Shortly after, demand hiked up to a nominal extent, mainly in the tractor and commercial vehicle segments. From the 1960s to the 1980s, a highly select set of players like Hindustan Motors dominated the entire industry (The Evolution of the Automobile Industry in India, n.d.).

The entry of Maruti Udyog Limited in the 1980s and its subsequent rise challenged established players like Hindustan Motors and Premier Limited (p. 129). With economic reforms in the 1990s, major global brands such as Hyundai, Honda, Daewoo, Mercedes-Benz, Fiat, General Motors, Ford, Mitsubishi, and Toyota set up shop to expand across India.

The 2000s witnessed expansion of almost all major companies across rural as well as urban pockets in India. Because of the emphasis on local manufacturing and quality, passenger vehicle exports also observed a gradual increase (India Exports, n.d.). As the automobile market began to colonize common modes of transportation, and contribute to pollution levels, government policies dictating mandatory emission standards, first introduced in the 1990s, received increasing attention. Consequently, motivated by European standards to control emission, the Central Pollution Control Board introduced Bharat Stage Emission Standards, based on type of engine (Emission Standards: India, n.d.).

As per a report on the Indian auto industry (India Car Sales, n.d.), India is today home to over a large number of manufacturers who produce passenger vehicles, commercial vehicles, two-wheelers, and three-wheelers.

The presence of several players in various automobile segments has resulted in intense competition for market share and consequently, a plethora of strategies.

Economic Uncertainty and the Indian Auto Sector

Since the 2000s, the Indian automobile sector has witnessed a dip in sales growth on three separate occasions. While the Great Recession of 2008 adversely affected sales across all segments, passenger and commercial vehicles sales nosedived in 2013–2014 (Raj, 2013). More recently, since 2018, sales across all auto segments have been largely heading southwards.

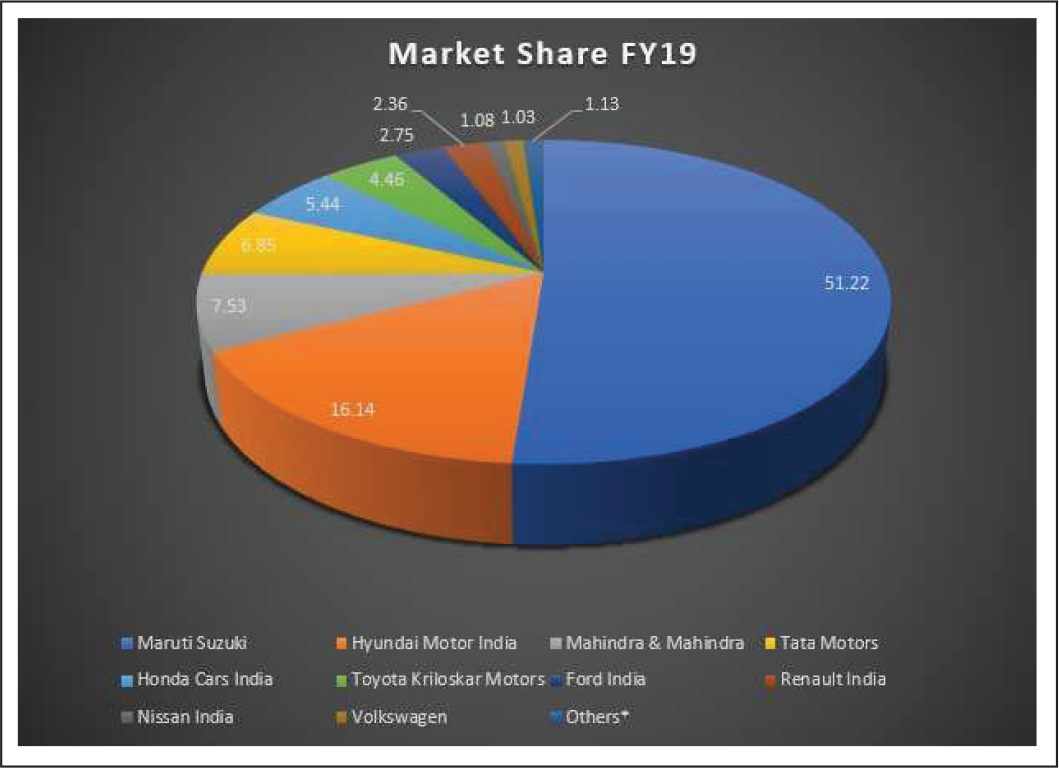

The Indian auto sector has been in a nightmare for two periods for 2 consecutive years in the last two decades—The Great Recession of 2008 and the one started in 2018, which has been endorsed further by the COVID-19 pandemic. Figure 3 shows the car sales in India from 2005 to 2019.

2008 Recession

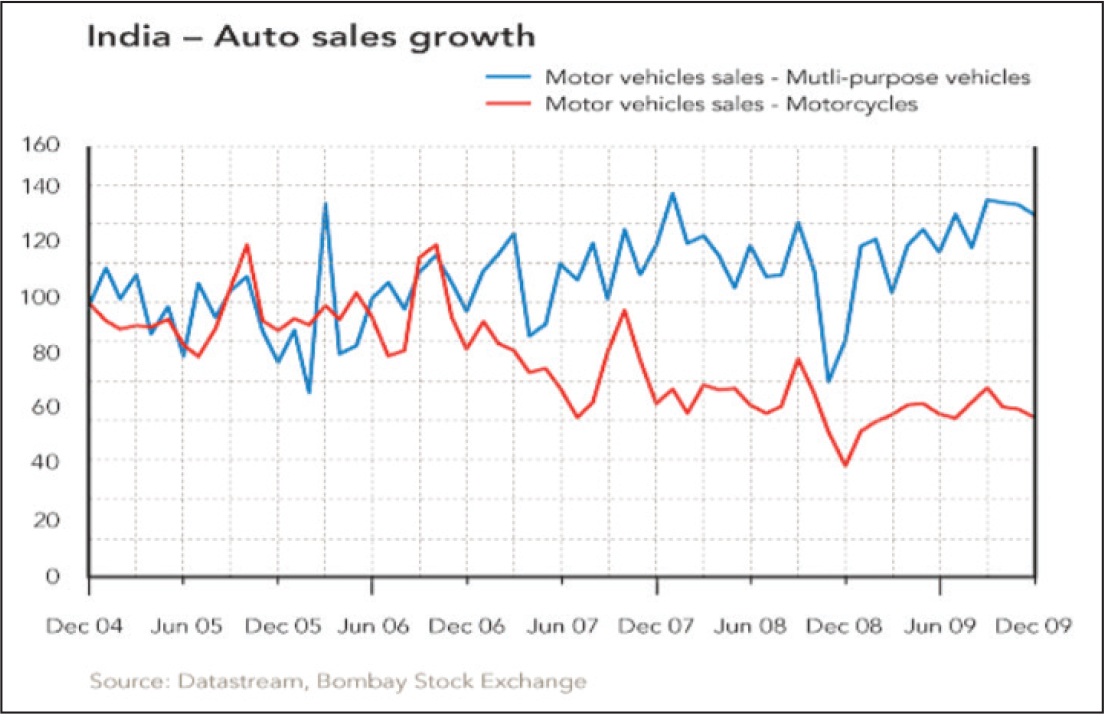

A number of countries faced headwinds when the global financial crisis hit them. Though the recession initially hit USA and Europe, India was moderately impacted as GDP growth rates fell almost by 50 percent (India GDP Growth Rate, n.d.). The auto sector was particularly impacted because of various factors, including a sudden rise in the US dollar against the Indian rupee, an uncertain exchange rate, delayed payments from OEMs, as well as no reduction in alloy and steel prices (Kumar, 2015). Figure 4 shows the trend of automobile sales in India from December 2004 to December 2009.

As per a research by the State University of New York College at Buffalo (Bai, n.d.), in February 2009, the State Bank of India drastically reduced its interest rates on hearing the fall in the production of automobiles. Additionally, Tata Motors launched the Tata Nano in the initial months of the year, describing it as the ‘people’s car’. The motive behind doing so in the recession period was its price, which was reasonably affordable by the growing Indian middle class, which was almost around ₹100,000. State Bank of India significantly reduced the interest rates applied to automotive loans. Tata Motors conducted a widespread marketing campaign in in the starting months of 2009, involving the launch of the automobile Tata Nano. These, along with other similar attempts by the government to back the local manufacturers and customers, resulted in not just the emergence of India from the crisis but also made it robust enough to attract foreign direct investments (FDIs) in spades. However, the good times lasted only until the wave of the 2013–2014 slowdown hit the industry once again.

2013–2014 Slowdown

Various factors including economic slowdown, high interest rates, and increasing fuel prices hit the industry in 2013 (Flashback 2013, n.d.). This phase interestingly witnessed both cutbacks in investment and expansion by established and new players.

2018 Recession

Auto sales in India have dipped drastically since October 2018. Also, the decline in sales has hit firms in the sector, comparatively harder.

According to a Business Standard article (Business Standard News, n.d.), the total sales of vehicles across all the categories, including passenger vehicles, two-wheelers, and commercial vehicles, observed a decline of 13.77 percent in 2019 at 23,073,438 units as against 26,758,787 units in 2018. This was considered to be the worst fall in the auto industry since the monthly and yearly sales data started getting into the books in 1997. Passenger vehicle sales also observed a similar decline of 12.75 percent to 2,962,052 units as compared with 3,394,790 units a year ago. For this particular segment, a decline of 7.49 percent was observed in 2013, making this the worst slump since then. Figure 5 shows the segment-wise domestic market share and export sales.

Two-wheeler sales also went down to 14.19 percent in 2019 to 18,568,280 units as compared with 21,640,033 units in 2018, and so did commercial vehicles with a sales drop of 14.99 percent to 854,759 units as against 1,005,502 units in 2018.

As per a census by the Reuters (Exclusive, 2019), manufacturers, auto ancillary makers, and dealerships had to waive around 350,000 employees in the first quarter of FY 2019.

A recent study by Fitch Ratings (Weak Sentiment to Curb India, n.d.) revealed that the slowdown is a result of the sluggish domestic economic growth rate and will continue due to higher costs incurred by the ownership due to the introduction of BS-VI emission norms since April 1, 2020. Additionally, with a rise in the demand for green energy, a shift in investments has been made by the automakers toward clean energy vehicles and high-tech trends. A consequence of this move would be a tremendous amount of pressure on cash flow and an enhanced focus on profitability by the manufacturers.

In order to tackle this downfall, the Indian government had come up with the measure of encouraging state-run banks to provide loans to potential car dealers as well as buyers.

Gearing up for 2020, discounts, exchange offers, and more accessible finance options were the key strategic plans by OEMs. Companies, including Maruti Suzuki, Hyundai, and MG Hector, were planning for market penetration through launching new models so as to thrive in the anticipated competition (James, n.d.).

Interviews conducted by Mint (Auto Industry Drives into 2020, 2019), an Indian financial daily with some of the renowned names in the Indian auto industry in December 2019 on their prospective views revealed this:

A statement by Society of Indian Automobile Manufacturers (SIAM) president Rajan Wadhera in an interview in December 2019 was as follows:

The Indian economy is expected to revive early next year, which along with the low base of last year and availability of newer models, should support growth in the auto sector.

S. S. Kim, MD and CEO of Hyundai Motor India, was also optimistic enough to state, ‘Probably after the BS-VI implementation, for few months the customer will need time to understand new norms and new situations. So, I would say demand will grow gradually from the second half of the next year’. Similar views were also upheld by Gaku Nakanishi, CEO and President of Honda Cars India.

However, all such predictions were bluntly washed off by the deadly COVID-19 pandemic, which not only affected its victims but also managed to ruin the entire world trade. Whether the Indian auto industry will observe numerous bankruptcy due to lack of hope or will rather see companies showcasing resilience through defensive, intensive, or combination strategies is still questionable.

Future of the Auto Sector: Post-COVID-19 Scenario

The Indian automotive sector was already being haunted by the growth deficit of 18 percent observed in FY 2020 (Automobile Sector Reports, n.d.). The sales, as well as the production of automobiles, had already started facing a decline since February 2020, as shown in Figure 4. And to add fuel to the fire, COVID-19 came up with its own plan of an apocalypse. Besides a nationwide lockdown, BS-VI emission norms, relaxed economic growth, apprehensive consumer sentiment, less utilization of workforce, probabilistic bankruptcies, and liquidity crisis have imposed additional threats. Figure 6 shows domestic automobile production and sales.

With the International Monetary Fund (IMF) anticipating a negative growth rate in FY 2021 across the globe (Coronavirus Crisis, n.d.), the situation of the Indian auto sector will remain vicious due to these three reasons also after FY 2021:

How Should the Indian Auto Sector Approach the Recession

The Indian auto sector has finally come to a stage where the times are demanding serious reforms so as to ensure its growth. The government’s part will not be a focus of this research. Instead, the prospective plans of large OEMs that lead the sector in passenger and commercial vehicle production and the amendments they need will be discussed in detail so as to conquer through this global recession.

An Harvard Business Review (HBR) article (Gulati et al., 2010b)-based research on the performance of 4,700 public companies post 3 years of recession says that during the recessions of 1980, 1990, and 2000, 17 percent of them were either went bankrupt, went private, or were acquired; 80 percent of them could not achieve the prerecession growth rates of sales and profits; and 9 percent of them heavily flourished by outperforming their competitors by at least 10 percent in sales and profits growth.

The prosperous 9 percent neither includes the firms whose immediate action is to cut costs, nor those which lead the investment dashboard during such times compared to their rivals. In fact, the chances that the condition of either minded firms will improve after the recession are 21 percent for the former and 26 percent for the latter, say the researchers. However, the companies adopting a mix of both the kinds of strategies have a probability of 37 percent for overcoming the recessionary blows. They reduce costs by focusing more on operational efficiency than their rivals and investing in new assets, marketing, and R&D.

Prof Rebecca Henderson from Harvard Business School (Henderson, 2018) considers ‘not crashing the company’ as a thumb rule to tackle recessions. This implies not running out of money at such points. As a recession is accompanied by a downfall in sales and low cash to find operations, financial debt management becomes inevitable in a downturn. An exemplary of this claim is Amazon (How Amazon Survived the Dot-Com Bubble, 2018). During the dot-com burst, if money would not have been raised beforehand, Amazon would have indisputably been unable to start the Amazon Marketplace, which opened later that year and operated through a negative cash conversion cycle. Be it an investment in technology, human resources, R&D, marketing, or any other operation, it is the cash a company has on hand that executes them. Hence, optimum use of money has to be taken care of at any period of time, including a downturn.

We have classified companies into three categories based on their response to recession in terms of investments/divestments:

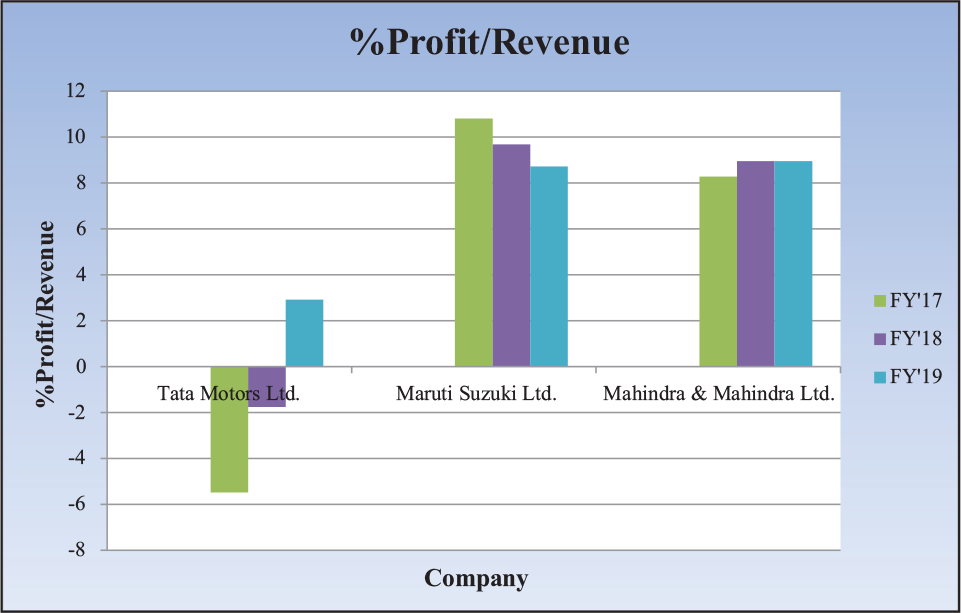

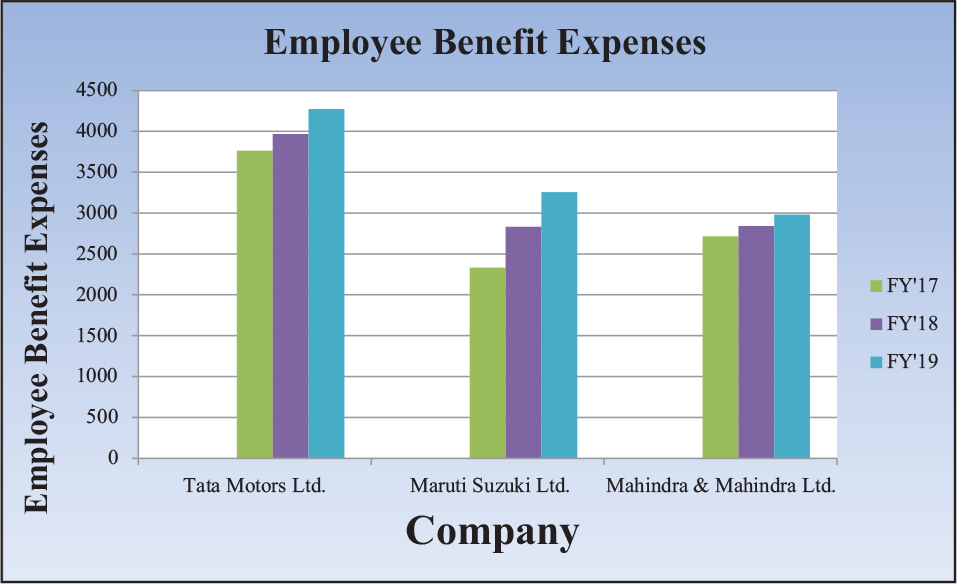

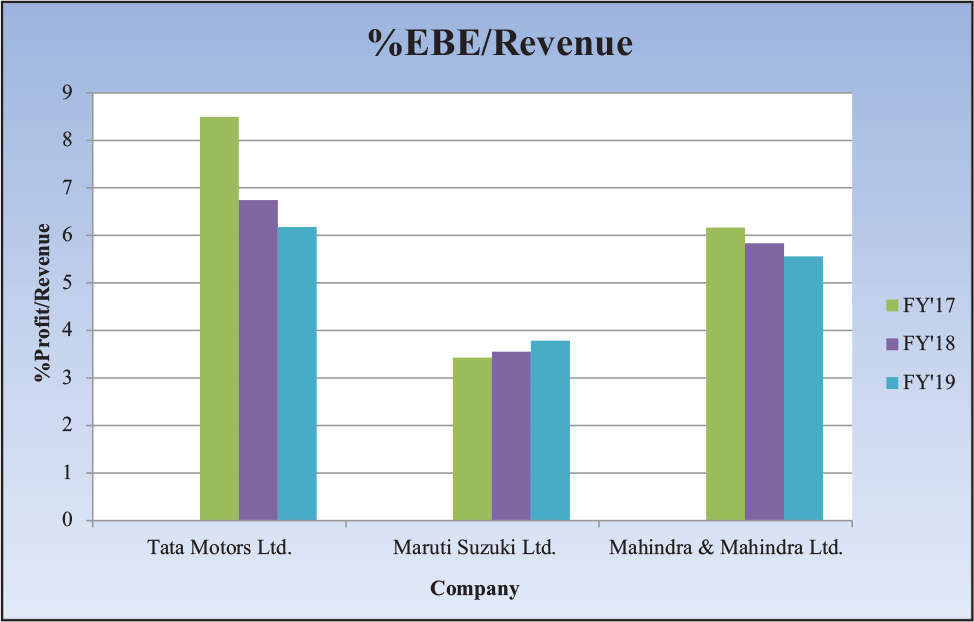

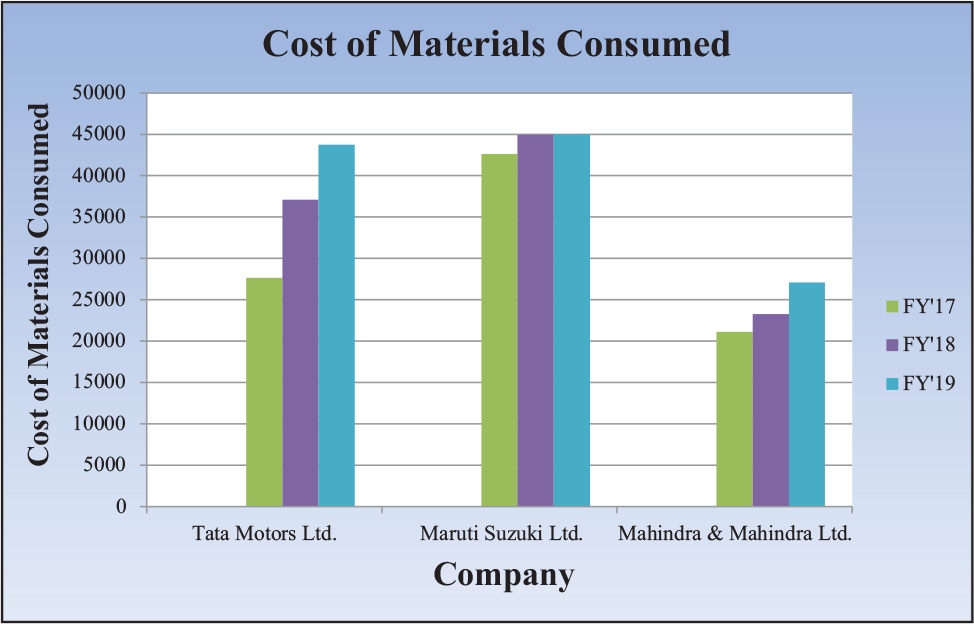

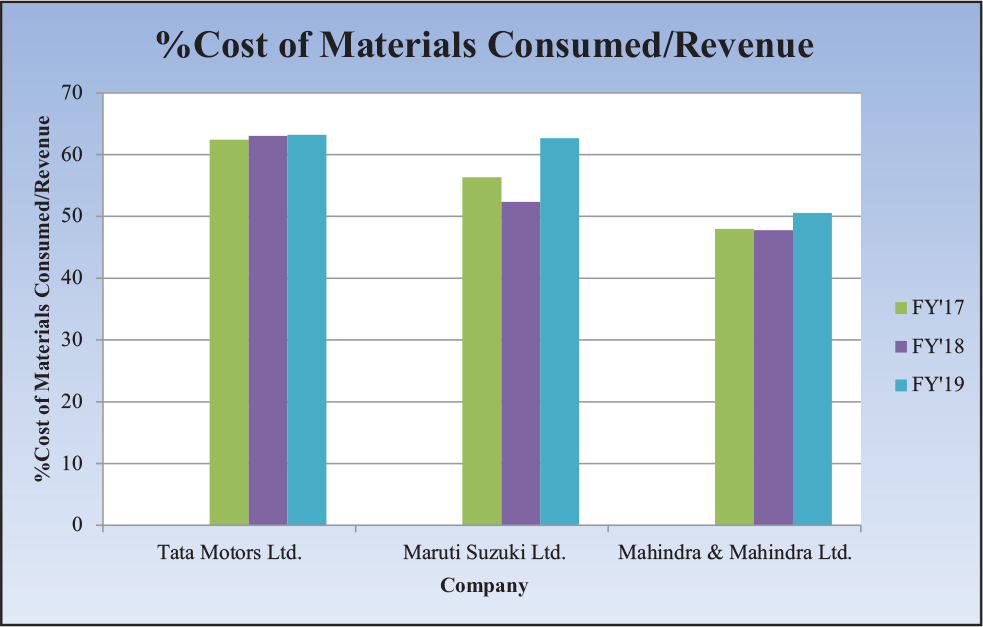

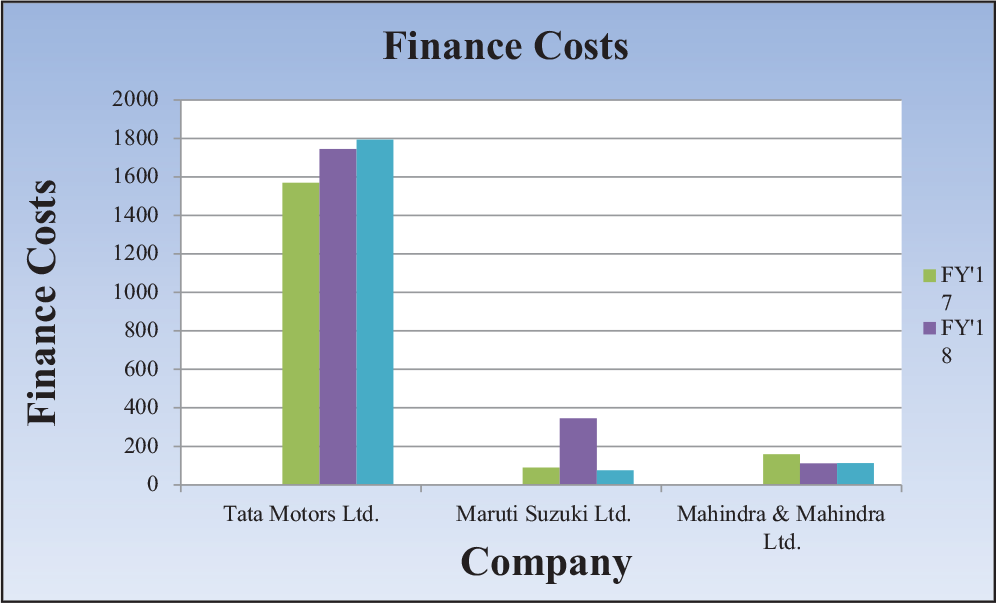

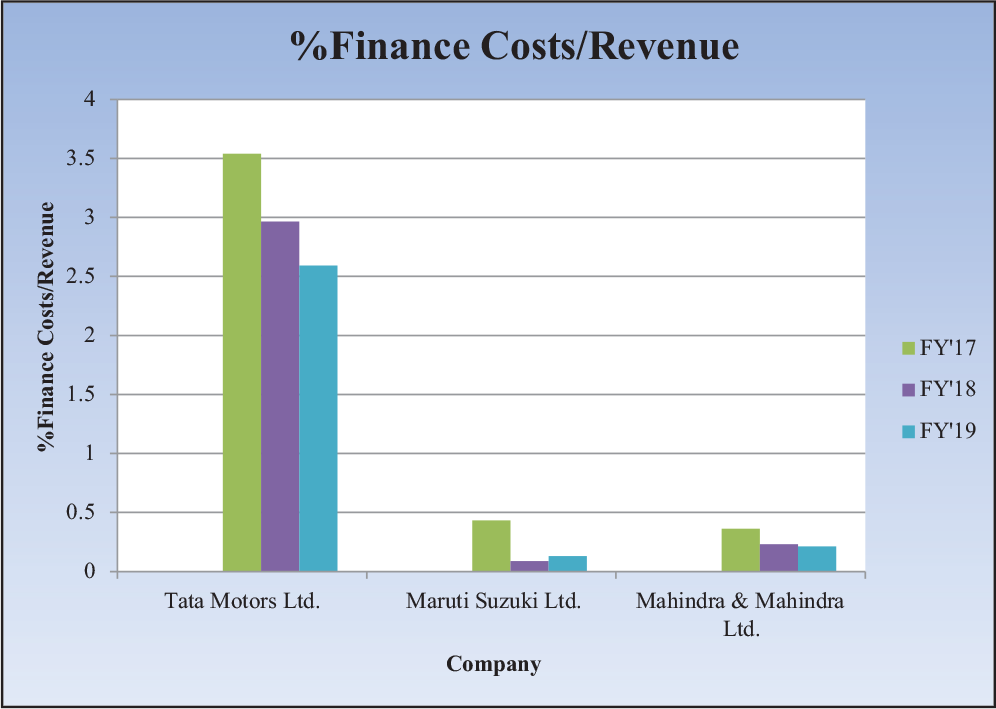

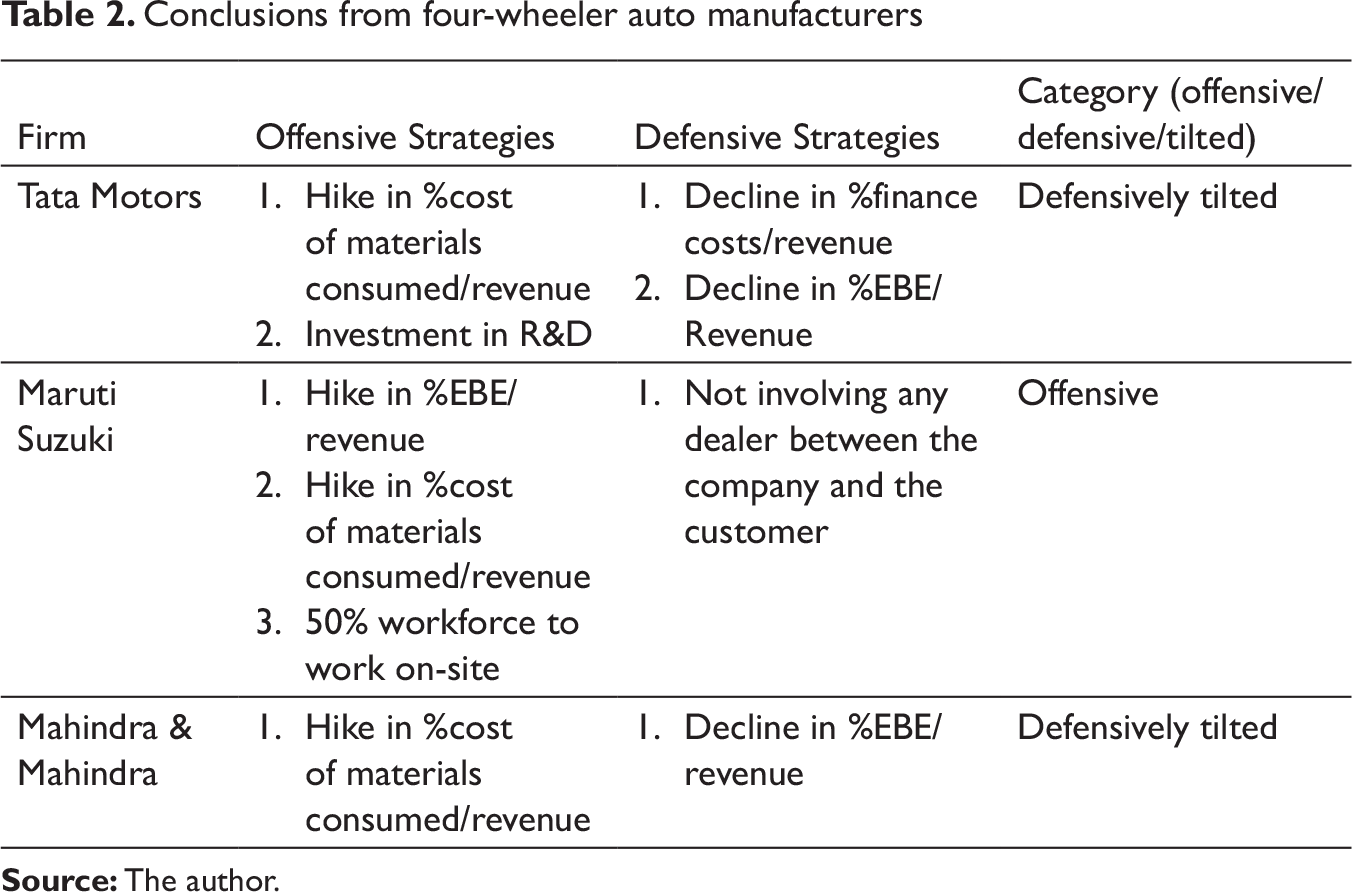

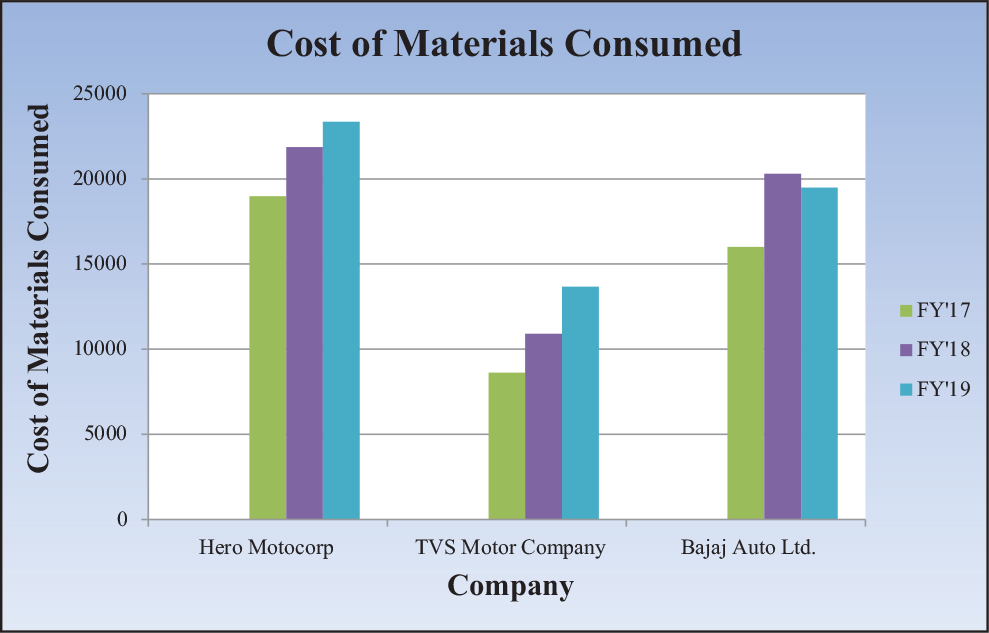

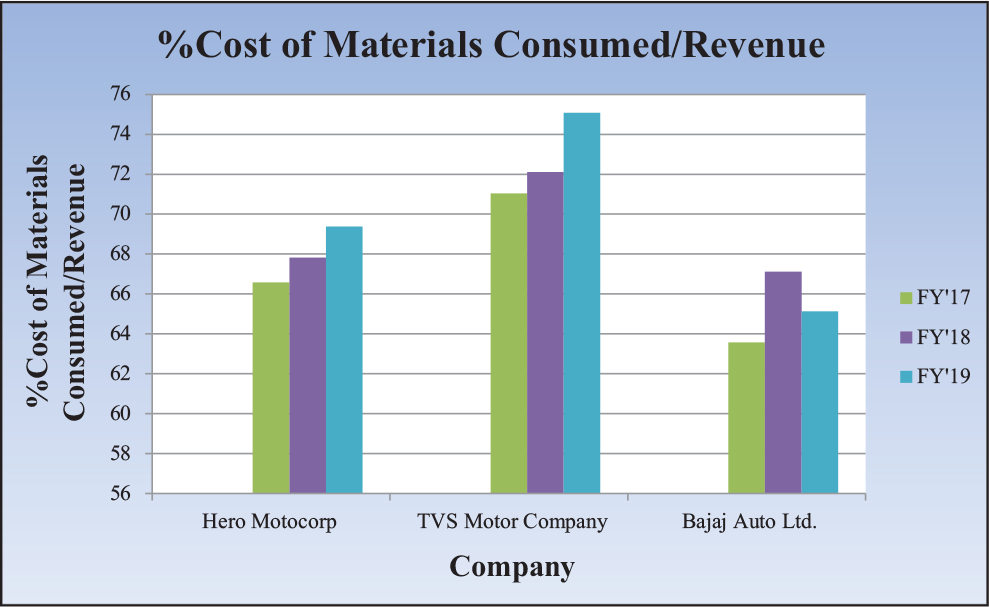

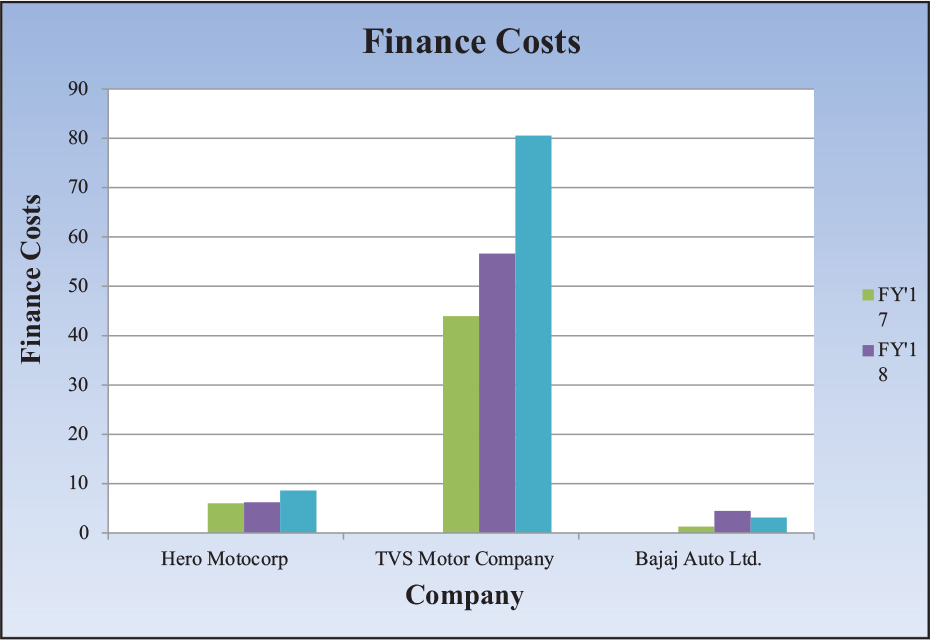

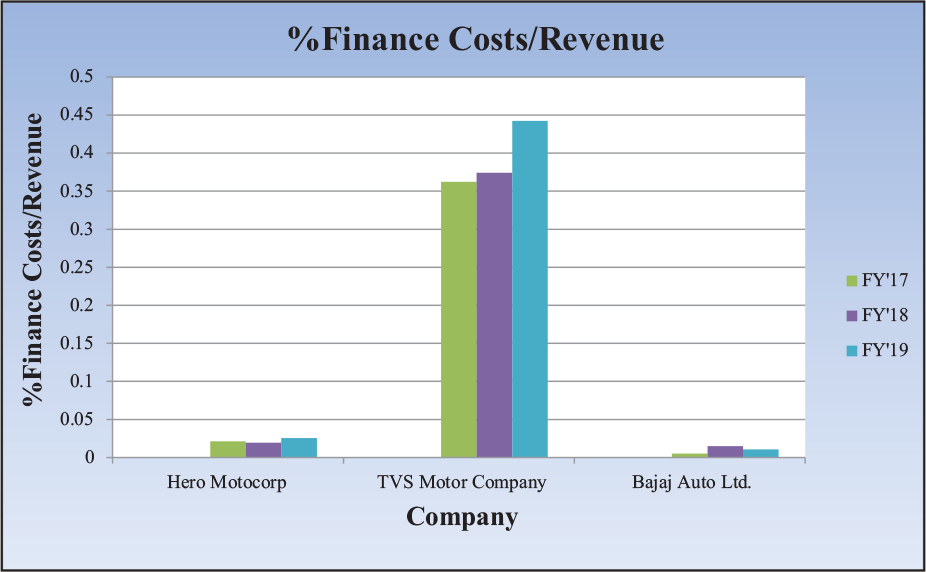

Analysis of the Strategies of Major Four-Wheeler Manufacturers in the Indian Auto Industry (Figures 7–14)

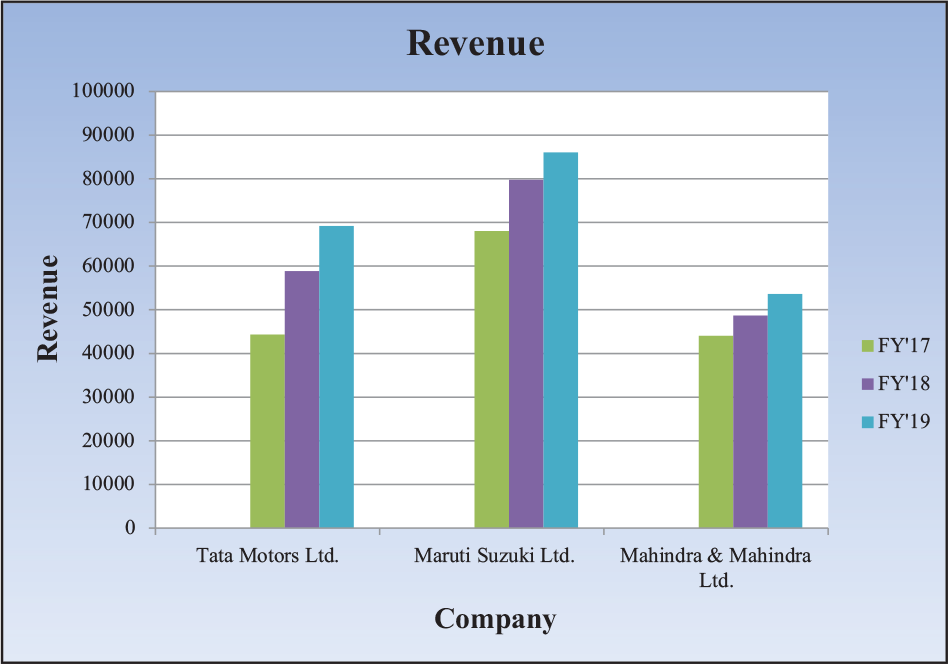

As per an interview by The Economic Times (www.ETAuto.com, n.d.-b), Tata Motors is not much apprehensive about the impact of the virus and is anticipating a reduction in Jaguar Land Rover’s (which contributes to 90 percent of its standalone income) full-year earnings before interest and taxes (EBIT) margin by just about 1 percent. The reason for this level of confidence can be attributed to its rise in profits since the beginning of the recession. It has also started a digital platform named ‘Click to Drive’ (How Coronavirus Has Hit the Global Auto Industry, n.d.), through which the customers can buy a car sitting at their homes with delivery to happen at a later date. This initiative might not compensate for all of their sales-based expectations but will at least attract that set of customers who are aware of the spike in prices after the economy resumes due to a rise in demand.

Like most other firms, delay in the full-fledged working of the plants due to lack of supplies will be a hindrance to Maruti Suzuki as well. The company has announced to work on-site with only 50 percent of the workforce (Maruti Suzuki Prescribes, 2020). This might help the firm have an edge over the competitors in terms of production. However, the employees would not appreciate such a move as most of the rivals of Maruti Suzuki had announced full-time work from home for their entire workforce. Focus for the sake of marketing purposes has been shifted to digital means. Other cost reduction measures are not involving any dealer between the company and the customer, and the deliveries being planned to reach the customer directly from the service center (Maruti Suzuki Readies Strategy, n.d.). Two of these moves are viable and will also satisfy their objective of expenditure reduction.

When every firm’s plants were completely shut down, Mahindra & Mahindra smartly started the production of face shields for two-wheelers at some of its facilities (How Coronavirus Has Hit the Global Auto Industry, n.d.). Their chemical plants were kept busy producing sanitizer. In order to avoid spoiling their terms with customers, they have extended scheduled service deadlines and warranty renewal periods (Coronavirus Pandemic, n.d.). No other strategies have been revealed in public. However, ensuring customer and employee satisfaction, divestitures of unfruitful assets, investments in long-term profits through better R&D projects, or expansion through integration will surely lead to the desired results.

Conclusions from four-wheeler auto manufacturers

Analysis of the Strategies of Two- and Three-Wheeler Manufacturers in the Indian Auto Industry (Figures 15–22)

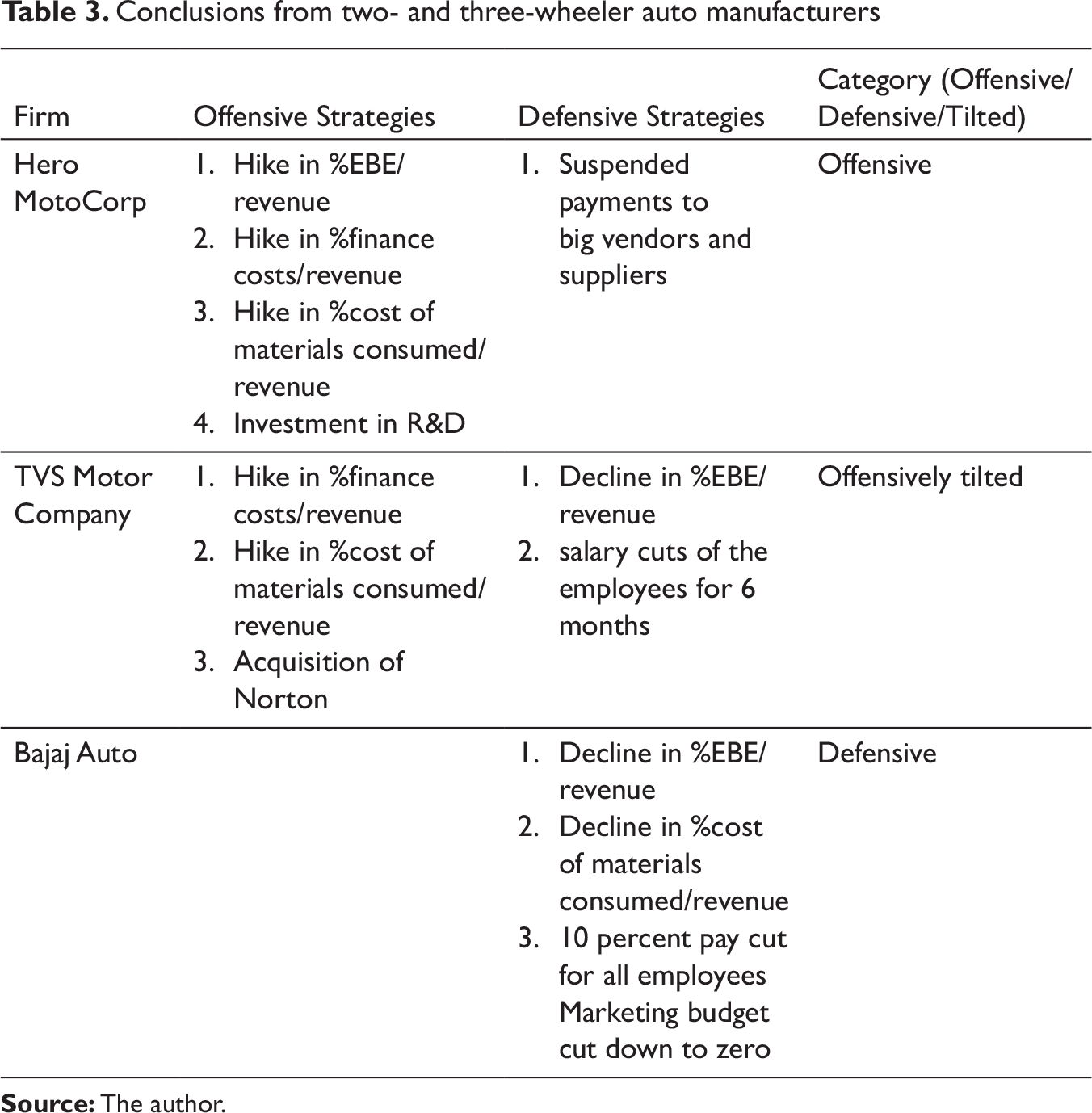

As a combat strategy against the pandemic brought downturn, the firm has suspended payments to big vendors and suppliers. This move might lead to some friction in the supply chain process. However, small vendors, MSMEs, and employees have been paid on time (www.ETCFO.com, n.d.). Prices for all its products and services have been revised, and investment in R&D has also been made with an aim to raise its market share in the upcoming few months (www.ETAuto.com, n.d.-a). These actions might help the firm recover relatively earlier if its main focus is on reducing prices and increasing income.

Unlike Hero MotoCorp, TVS Motors has gone for salary cuts of the employees for 6 months, starting from May 2020 as a cost-reduction strategy (Panday, 2020). This will definitely impact the trust factor among the employees. As there are firms that have not taken such a route, with some even announcing hikes, the employees might consider working for firms other than TVS, given the times. A short delay or a pause to hikes might have been a better option. Keeping good terms with its customers, warranty periods expiring during the pandemic phase have been extended until June 2020 (www.ETAuto.com, n.d.-c). Another big move has been the acquisition of one of the most iconic sporting motorcycle brands of Britain, ‘Norton’, during this period (TVS: TVS Motor Company, n.d.). Both of these actions will undoubtedly bring good to the company in the long run, unless the product/service quality does not exacerbate or the demand in sports bikes sees a downfall.

Their strategies to reduce costs in these times of the deadly pandemic include 10 percent pay cut for all employees, to which the workforce union has agreed, so as to reduce the fixed cost, and the Managing Director of the firm, Rajiv Bajaj himself is going for 100 percent salary loss (Bajaj Auto Workers, 2020). As the cuts have been with the workforce’s consent, the chances of observing a negative impact as a consequence are relatively less. In turn, employees will get a sense of job security as the senior management is ready to bear the losses. Additionally, the marketing budget has been absolutely cut down to zero, which was around 2,000 million before the pandemic (Lockdown Is Not a Long-Term Answer, 2020). A slight reduction in employee payments might not make their stakeholders apprehensive, but such a giant leap in marketing costs can undoubtedly affect their sales as this is the time where people will look for cars as a measure of safety. A good move by them to uphold customer relations is the extension of free service and warranty period of the automobiles owned by their existing customers (Bajaj Extends Warranty, n.d.).

Conclusions from two- and three-wheeler auto manufacturers

Suggestions for Original Equipment Manufacturers of All Scales Which Are a Part of the Indian Auto Sector

Employee Relations

Employees of a company are the ones who put the real efforts behind the scenes, but not all. When it comes to waiving off employees, one has to think smartly to choose which ones to weed off. The 80/20 principle obviously is applicable but following it would drastically impact the reputation of the firm. Rather than 80/20, an approach similar to the 4-4-2 can be implemented with the numbers manipulated based on the needs. Mechanizing selected plants along with relevant skill development programs for the employees will be a perfect blend.

Coming up with incentive programs for employees producing considerable output, ensuring their pay in a trade-off with top-level management, providing them with more company stocks as an additional incentive, and chemistry-enhancement programs should be implemented. If the salary difference between immediate cadres has been substantially high, now is an excellent time to balance so as to gain more trust from the workforce.

Research & Development (R&D) Facilities

Not all the innovation projects lead a firm to thrive in a recession. ‘Managing In A Downturn’, a book authored by renowned academicians as well as professionals (Managing_Downturn_US_Asia.Pdf, n.d.), shares the 4-4-2 approach. This implies cutting on 4, maintaining 4, and doubling-up on 2, out of every 10 projects.

As the word ‘social distancing’ will be in the air for at least around a year, people will prefer cars over two-wheelers as well as carpooling. Recalling the smart move of Tata Nano in 2009, compact and cheap cars will undoubtedly gain a hike in demand. Also, a highlight in the sustainability policies of a firm can be made through more of electric vehicle production. In fact, in May 2019, Nissan Motors received a patent for coming up with wireless charging facilities for electric vehicles in India (Babu, 2019), followed by Tata Motors launching its first electric car in October 2019 (Tata Motors Electric Car, n.d.). As per a Mint article (Global Firms Look to Shift from China to India, n.d.), suppliers across the country can also expect major orders from foreign firms as many of them have plans to shift from China to India. Production of self-sanitizing cars along with accessories that are microbe-resistant will also be in high demand.

M&A

Shaking hands with firms of similar cultural environment for symbiotic relations can reap fruits very much after the recession as well. True for corporations as well as humans, we make lifelong relations with those who illuminate for us in our dark days. Auto manufacturers merging up with food delivery companies to ensure the hygiene of food as well as deliverers, or with vehicle providers on rents can synergize the gain and save costs of both the parties. Almost all transportation-based businesses will look for cheaper and efficient automobiles, hence opening up a plethora of opportunities. Now will be a relatively lenient period for M&As as the government’s goal of achieving a GDP of US$5 trillion and ‘Make in India’ project are tangential to promote them in spades, given the downfall.

Many firms will also announce liquidations, divestitures, and bankruptcies; hence, an eye on acquisitions will also help. Options of acquisition of suppliers, distributors, innovation labs, and transportation businesses will knock many doors, including those of MSMEs. Optimally reducing the supply chain by market penetration or development or by cutting out the evitable intermediaries is yet another alternative.

Customer Relations

Needs of the customers is the governing force toward any business. During a recession like the COVID-19 pandemic, customers will look for safer as well as pocket-friendly options. Leniency in terms of EMI durations, partnering with microfinance institutions (MFIs) for opening up to the urban and rural middle class, as well as providing maintenance services at nominal charges to the existing customers will ensure strong bonds.

With the advent of artificial intelligence and the Internet of Things (IoT), ‘smart cars’ can be developed which detect COVID-19 victims who have been in contact with the car. Such addition of features will attract high-end as well as middle-class customers.

Supply Chain

Intra and international supply chain, which has been disturbed, might take around 6 to 12 months to start working at its fullest. Many suppliers might also announce bankruptcies or closures. Hence, enhancing the network across the industry becomes inevident. Due to increase in demand as well as entry of brand-new products and services in the market, many novel suppliers and distributors will emerge. Given the circumstances, developing relations with the new entrants at the earliest will reap relatively more benefits as the prices will undoubtedly surge up post the recession.

Renewing older contracts with stable suppliers/distributors along with a backup plan will enhance the firm’s adaptability as well as enforce the supply chain to deliver better results due to its adaptable trait. Rather than incurring probable losses by relying on older links, a win-win through new connections is a better option.

Conclusion

Learning from recessions is what distinguishes leading firms from the rest. A recession might seem like a dreadful event with a long-lasting impact, which might or might not be true always, but an unavoidable characteristic of it is that it will keep nudging the economy periodically. Hence, acclimatizing with these dreadful times is the only way to get through. This can be done by firms which are in favor of having strategic plans frequently as well as those which are not. Businesses have to make sure that they have a ready set of strategies on hand so as to tackle any uncertainty whenever it strikes the doors, whether they are in favor of making strategic plans occasionally or not. Not doing so leads to financial shocks which might or might not be bearable and also hindered thinking with an open mind on gaining the most out of the opportunities available for the time being.

Although strategic planning for future adversities is considered beneficial, not always does it make a business flourish. There can be multiple reasons attributable to the same. First, businesses with mainly an ‘offensive’ or a ‘defensive’ mindset have high chances of failure. Second, the inability to predict the trajectory of the downturn will definitely lead to wrong decisions. Third, although everything might have been perfectly planned and analyzed, sudden changes in the economy or any major contributor in business operations can lead to adverse consequences due to a shift in consumer demands. Given these reasons, the best possible option is to stay geared up for an uncertainty without any imitation or replication of previously successful strategies. Imitation of the competitors’ strategic plans might lead to a firm’s success, but that happens only due to good fate. Similarly, blindly re-implementing the strategies which have worked well in the past will also work due to good fortune. And this is how this research differs from most others on the Indian auto sector. Rather than an industry-specific analysis, considering a pool of big players which closely represent the entire industry, and then performing a critical analysis on each of their best practices, reaps better results for them as well as for the rest of the sector (other large companies and MSMEs in this case) and its stakeholders. Apart from the strategies already under consideration by the auto sector majors, other possible strategies have also been discussed based on the opportunities brought by the COVID-19 pandemic.

However, this research can be made more robust by coming up with a quantitative analysis method to evaluate strategic plans. Having a measure for strategic plans makes it easier to understand their impact. Also, a further classification of ‘Tilted’ companies by considering additional segregation criteria can lead to a better understanding of other factors that contribute to the success of a firm during uncertainties. This might lead to more clarity on what might be the perfect blend of offensive and defensive strategies for an Indian automobile business to thrive through future economic uncertainties.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.