Abstract

This study considers the impact of the COVID-19 pandemic on sub-national housing markets in Wales, focusing on the contribution of environmental and productivity attributes on house price change. Using a hybrid hedonic/repeat sales framework, we examine trends before, during, and after the pandemic. Initially, higher-quality environmental and productivity attributes were associated with a positive premium in price growth, while lower quality attributes were associated with a negative premium. However, during the pandemic’s second phase, these effects reversed but positive premiums for higher-quality attributes did not fully unwind during the transition to less acute phases of the pandemic. When we disaggregate the analysis for the urban-rural gradient, we find that both contexts placed a premium on high quality environmental housing, but lower quality productivity attributes negatively affected urban areas. The contribution of the study lies in revealing the complex, evolving and unequal relationship between the COVID-19 pandemic, housing preferences, and prices that, in our study context, have been subject to much conjecture but with little empirical investigation.

Introduction: COVID-19 and changing residential locational preferences

It is widely recognised that globally the COVID-19 pandemic led to significant changes to mobility, sociability, and employment. A growing body of literature has explored impacts on housing systems and behaviours with the pandemic acting as a natural experiment to assess the changes to the meaning and functions of our homes (Ahrend et al., 2022; Gallent and Madeddu, 2021; Huang et al., 2022; Parsell and Pawson, 2023; Pawson et al., 2022). With the implementation of ‘stay at home’ orders, housing assumed a newly critical role in safeguarding against virus transmission, while also serving multiple and diverse functions for different household members (Nanda et al., 2021; Preece et al., 2023).

Here the pandemic made visible, and in some cases intensified, a range of inequalities in individual housing outcomes, whether relating to amenity, space, conditions and quality, and locational effects (Parsell and Pawson, 2023; Preece et al., 2021, 2023). This recognition has prompted debate about the extent to which our homes met household needs and preferences during the pandemic and post-pandemic periods (Parsell and Pawson, 2023). This reflective process also created knock-on effects, such that ‘…the pandemic appears to have brought about a major change in tastes, with significant ramifications for house prices’ (Pawson et al., 2022: 88).

The severity and length of ‘stay at home’ orders (or ‘lockdowns’) varied among countries and even within cities. Countries like the UK and Italy were heavily affected early on, while others like Australia, New Zealand, and Japan experienced lighter impacts initially. Over time, the lockdown restrictions and conditions fluctuated with waves of infection, new variants, and vaccination efforts. The changes in daily life caused by the pandemic were expected to have lasting effects on housing preferences, particularly in terms of work organisation, impacting both commercial and residential property markets (Guglielminetti et al., 2021: 7).

Here some have predicted ‘…a radical and structural change in housing demand’ in the future (De Toro et al., 2021: 2) based on ‘the new utility of housing’ (Gallent and Madeddu, 2021). Indeed, housing markets internationally underwent considerable and rapid changes during the pandemic. Initially there were predictions of substantial decreases in house prices, but emergency income support measures and stimulatory monetary policies were implemented to varying extents in Europe, North America, and the Asia Pacific regions. As a result, house prices experienced a significant boom globally, with several complex housing market patterns emerging. People moved from city centres to suburbs or rural areas, and neighbourhood centres adapted to accommodate increased leisure and consumption demands due to widespread remote working for some groups. Additionally, there was a notable return of overseas workers and international students to their home countries, leading to repercussions in housing markets and different sectors within them. Later stages of the pandemic witnessed increased demand for properties and markets suitable for remote work, escaping lockdowns, and lifestyle preferences (Bank of England, 2021; Office for National Statistics, 2021a; Pawson et al., 2022; Savills, 2020).

Set against this context, it is well known that house prices are conditioned by certain structural features of the property and the quality and accessibility of locational amenities (Leishman, 2009). While overall the pandemic may have heightened the significance of these positive externalities (Savills, 2020), impacts are likely to vary across different countries, regions, and housing markets. For example, policy interventions are understood to have contributed to increased housing market activity and prices in some areas (Gallent and Madeddu, 2021), with the UK stamp duty holiday, for instance, benefiting ‘second-steppers’ moving to larger homes (Judge and Pacitti, 2021).

The severity of ‘stay at home’ orders and pandemic restrictions also likely influenced demand. In countries and cities heavily affected by restrictions, it is speculated that the pandemic intensified the desirability of features like residential location outside urban centres, proximity to green or open spaces, private green spaces, walkable neighbourhoods, home study or workspace, and digital connectivity (Ahrend et al., 2022; Batty, 2020; Pawson et al., 2022; Savills, 2020). Despite the potential for significant impacts, there has been limited empirical evidence of the behavioural and structural shifts in specific markets over time, or of how COVID potentially impacted housing systems unevenly in terms of urban-rural or regional context.

At the same time, during the initial pandemic period, there was debate over whether COVID signalled ‘the end of cities’ (Brail, 2021) or at least a profound transformation in prevailing urban behaviours (Florida et al., 2021). The concentration of urban life and its economic functions became perceived as a public health risk, leading to residential movement away from city centres (Brail, 2021). Initial housing market trends in the UK and internationally provide some support for this shift. The UK witnessed increasing average prices in rural areas compared to other locations and increasing demand for houses relative to flats (Office for National Statistics, 2021a). Analysis across multiple countries also provided evidence for faster price growth for detached properties, and rural or suburban locations, compared to urban areas (Pawson et al., 2022).

Although the evidence for changing locational preferences is varied, it seems clear that the pandemic disrupted the importance of proximity to employment in housing location choices (Gallent, 2022; Parsell and Pawson, 2023), with consideration of internal space and multi-functionality, access to outdoor space and residential amenities having taken on increasing prominence in household locational decision-making (Lohmus et al., 2021; London Assembly, 2021; Office for National Statistics, 2021b). Here it is recognised that positive health and wellbeing is connected to access to outdoor space (Lohmus et al., 2021; Poortinga et al., 2021). However, it was also the case that differential access held the potential for those who can afford to relocate and work from home, potentially displacing low-wage earners from areas with positive environmental attributes and contributing to a residualisation of urban populations unable to move (House of Lords, 2021a).

The pandemic also increased the importance of overall space in housing preferences (London Assembly, 2021), with suggestions of higher demand for larger homes and those with multi-functional, modular spaces (Alves and San Juan, 2021; Bank of England, 2021; De Toro et al., 2021). The demand for more flexible, multi-use homes has in some cases led to a ‘demand doughnut’ effect, with increased demand for family homes in suburban areas and decreased demand for smaller flats (Gallent and Madeddu, 2021). Although more difficult to measure empirically than house size, a range of other dwelling attributes may have taken on increased importance because of higher rates of home-working, including energy efficiency and access to natural light (Cuerdo-Vilches et al., 2021; Nanda et al., 2021). Digital infrastructure and the connectivity of dwellings also assumed a new significance with the growth in home-working (House of Lords, 2021b). Fast internet connections already influenced property values before the pandemic (Ahlfeldt et al., 2017), but experiences of remote working and learning during the pandemic exposed existing geographical and socioeconomic inequalities in access to high-speed internet (Nanda et al., 2021).

These changing preferences for housing attributes have implications for house prices, with increasing costs for those aligned with shifting priorities, and potentially decreased costs in urban centres (Ahrend et al., 2022; Huang et al., 2022). Later trends in the pandemic period suggest a decline in the drivers of decentralisation from urban areas (Gallent, 2022, Gallent et al., 2022), with the possibility that increased affordability in city centres renewed their attractiveness over time, wiping out initial patterns of decentralisation (Gallent and Madeddu, 2021). Indeed, some analyses have shown little change in house prices related to shifting housing preferences, with urban house price growth remaining stronger than that in rural areas (Reusens et al., 2022).

What is clear here is that the SARS-CoV2 pandemic was a complex period with implications that varied across national and sub-national contexts, reflecting already existing home-work practices, residential and workplace preferences, perceived risks of the pandemic, and social distancing requirements (Preece et al., 2023). Effects differed between urban, suburban, and rural housing markets, as well as among income and generational groups. It is recognised that the pandemic induced economic impacts that were distinct from more typical recessionary periods, where the disruption had the potential to produce persistent economic effects (Blundell et al., 2022: 609), necessitating a deeper understanding of COVID impacts on local housing markets.

Against this backdrop, Colomb and Gallent’s (2022: 634) call for in-depth studies on the local housing market impacts of COVID provides a valuable framing for this study. In this paper, we consider the theoretical implications of the pandemic shock followed by restrictive impacts on freedom of movement. Based on a review of the literature and synthesis of a range of early studies published during the pandemic, we set out expectations for implications on housing market choices, behaviours, and outcomes. We build hypotheses that physical and environmental housing and neighbourhood attributes conducive to productive ‘working from home’ will have led to the establishment of price premia during the pandemic and set out a strategy for defining and measuring such attributes. Finally, we set out an empirical strategy for testing for house price effects specific to dwellings that possess attributes that are conducive to working from home.

Study context and methodology

This study focuses on Wales, one of the four constituent nations of the UK. Since political devolution in 1999, Wales has implemented various progressive housing policies that diverge from other parts of the UK (Smith and Mackie, 2021), including a focus on increasing affordability, innovative design, addressing homelessness, and improving the quality of existing housing stock (Welsh Government, 2019). The COVID-19 pandemic raised questions over housing choice, quality, and affordability, amidst concerns of widening wealth inequalities (Blundell et al., 2022; Smith and Mackie, 2021). Framed within discussions surrounding local government finance reform and the future of council tax (Welsh Government, 2021), Wales provided an opportunity to employ an empirical strategy for analysing changing price effects that reflect shifts in housing and locational preferences throughout different phases of the pandemic.

Against this context, Wales boasts a housing stock of over 1.4 million dwellings, comprising 0.990 million owner-occupied, 0.203 million privately rented, and 0.226 million social rented dwellings (Hincks and Leishman, 2021). Using AddressBase, 1 an initial dataset was constructed by linking 29 million Royal Mail postal addresses to unique property reference numbers (UPRN). This approach enabled the creation of a modelling framework to estimate price changes for individual properties over time, leveraging Land Registry data, 2 while accounting for the discrete effects of neighbourhood and locational attributes. The initial dataset included 463,271 housing unit observations; however, missing data for some observations covering the potential environmental variables and/or productivity indicators reduced the final dataset to 335,577 observations.

The Hincks and Leishman (2021) study adopted the long-established hedonic price modelling approach to estimate up-to-date values for every dwelling in Wales. Significantly for this particular article, the UPRN’s also facilitated the linking of chains of repeat sales over time to neighbourhood and locational attributes, which were then incorporated into an econometric modelling framework.

The repeat sales modelling approach can be seen as a variant of the hedonic method. The essential assumption is that if a dwelling remains physically unaltered between observed pairs of transactions over time, the price differential between sales can be seen as indicative of market trends. Yet, the hedonic and repeat sales methods can also be combined to form the hybrid hedonic/repeat sales modelling approach. We explain this in more detail in the methods section, but the important aspect to note is that the method combines the fact that most dwelling attributes remain the same at two observed sales, and the fact that there may be one or more new or altered attributes. This can also take the form of new information or an external event. We examine the interplay between different stages of the pandemic and indicators of environmental productivity attributes in this particular application.

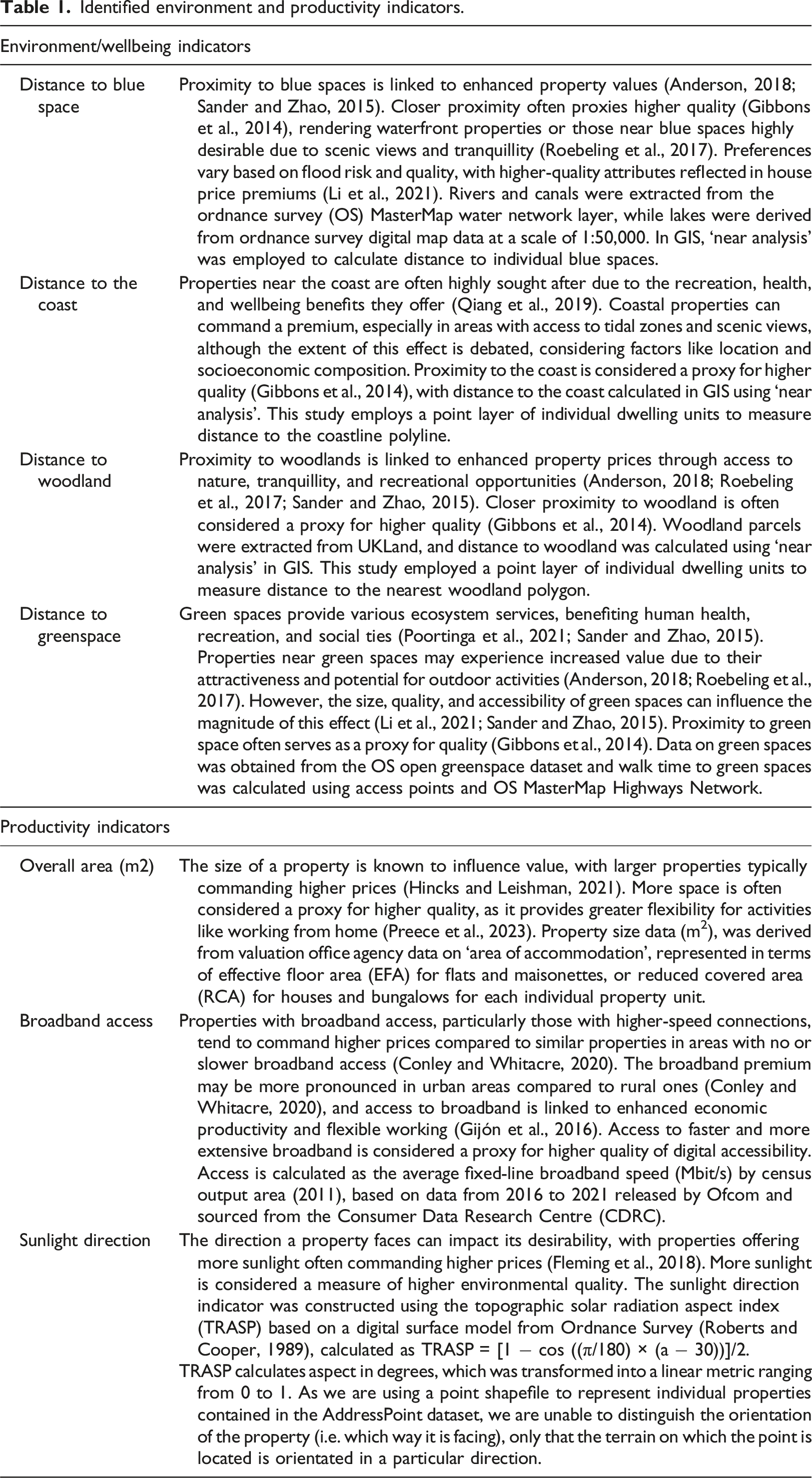

Developing indicators of environmental and productivity attributes

Identified environment and productivity indicators.

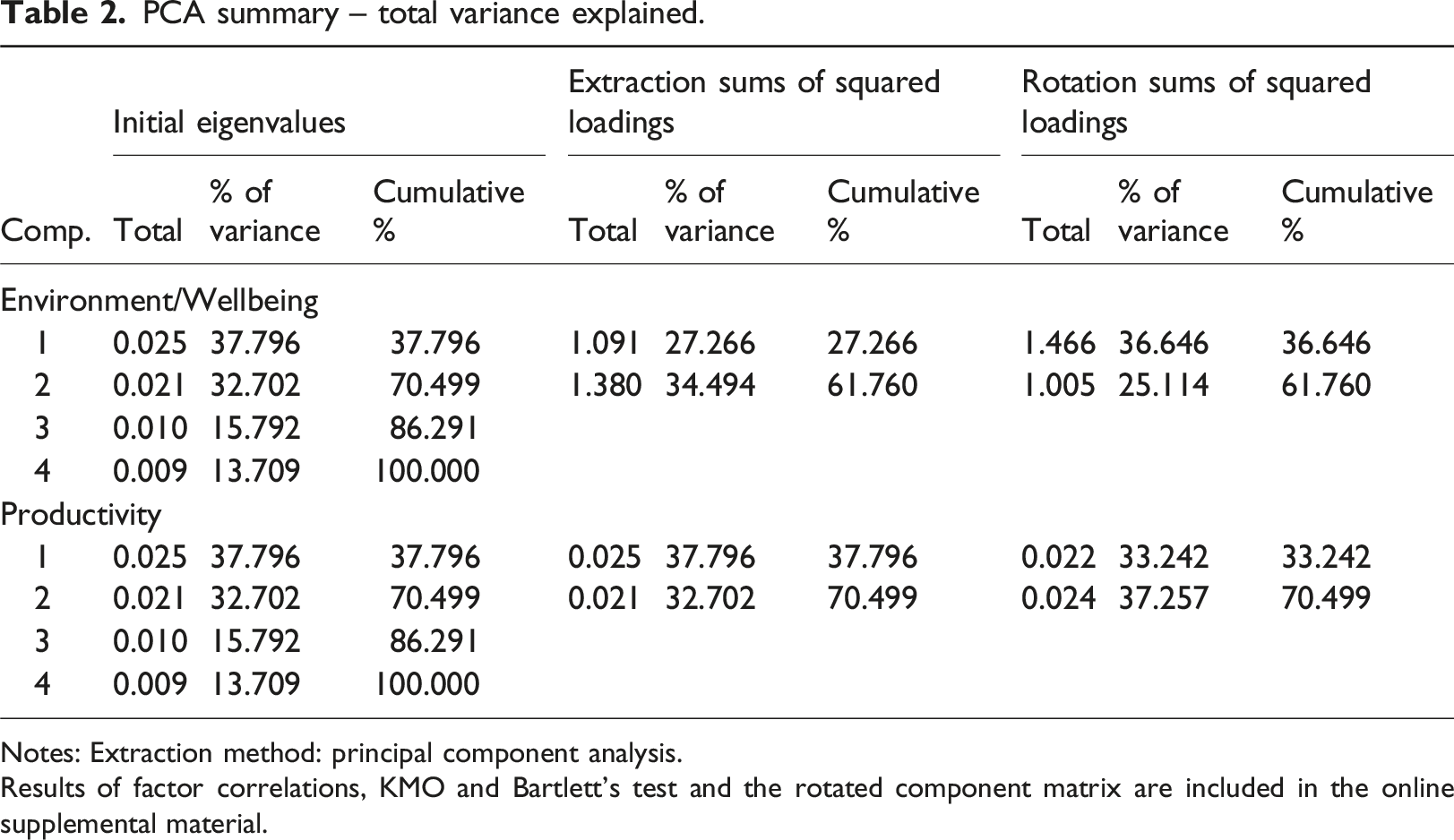

Exploratory analysis revealed high and statistically significant correlation between the environment/wellbeing and productivity variables (>0.7), highlighting potential problems with multicollinearity. Principal Component Analysis (PCA) was adopted to reduce the original environment/wellbeing and productivity indicators. Four normalisation approaches were tested: Log, Box–Cox, Inverse Hyperbolic Sine, and fractional ranking with inverse distribution function. Two standardisation processes were tested: Z-score and range standardisation (Hincks et al., 2018). Fractional ranking with inverse distribution function and range standardisation was adopted based on the performance of this combination in minimising skewness and kurtosis measures. 3

PCA summary – total variance explained.

Notes: Extraction method: principal component analysis.

Results of factor correlations, KMO and Bartlett’s test and the rotated component matrix are included in the online supplemental material.

The hybrid hedonic repeat sales modelling framework

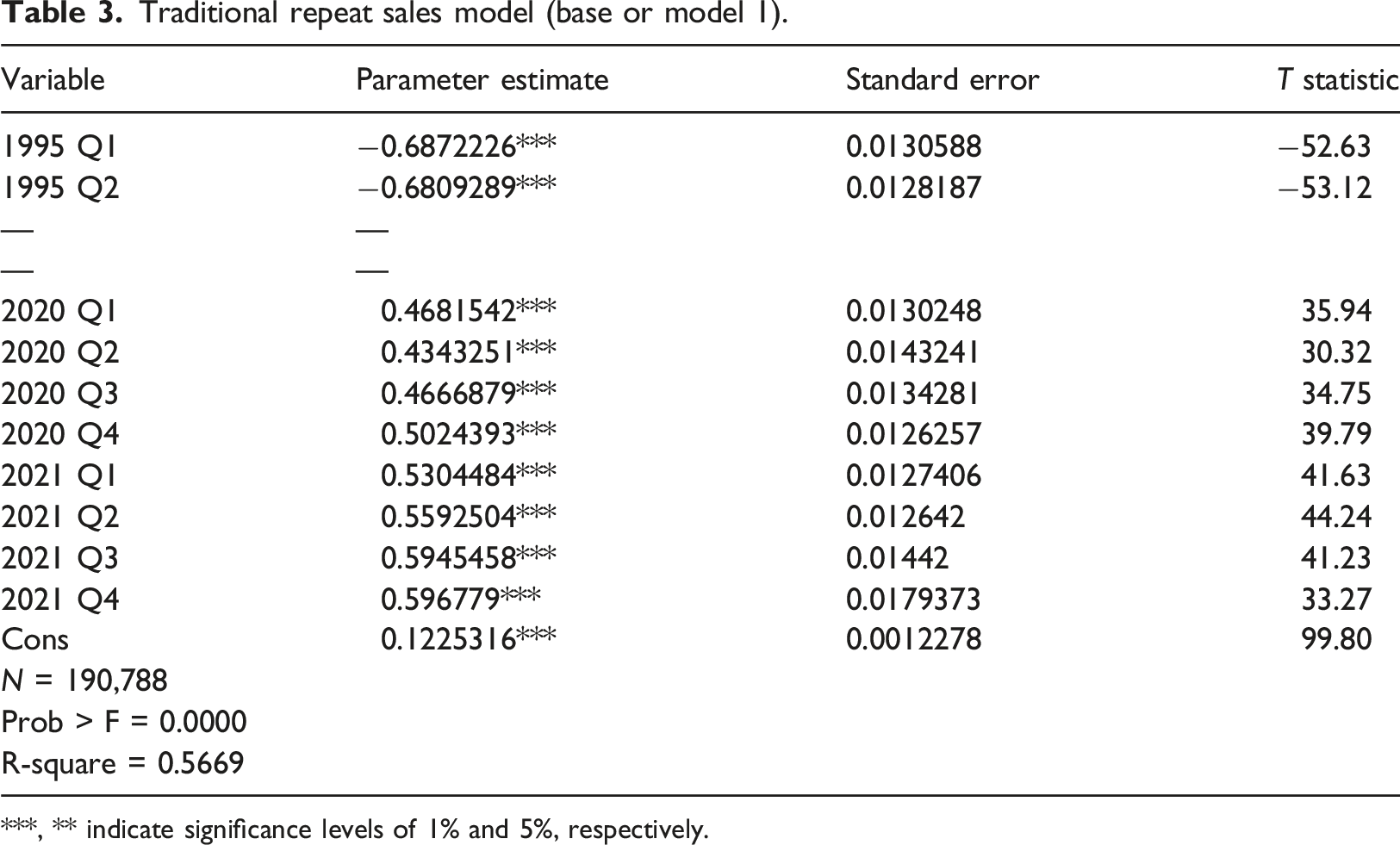

Having defined a set of variables designed to capture environmental factors and conditions conducive to home-working, we are now able to set out our empirical strategy. We begin by examining the traditional repeat sales regression (RSS) model which is shown below as equation (1):

A hedonic attribute, which is present in both time periods of a repeated transaction of the same property, offers no information that can be used to infer the movement of prices between those time periods. As Case et al. (2006) put it, the attribute effects in the two different time periods effectively cancel each other out. However, an attribute that appears in only one time period of a matched repeat sale can be used to infer information. This fact gives rise to the possibility of a hybrid hedonic/repeat sales model in which the presence of a changed physical attribute at the second transaction can be measured using an interaction with a time function as shown in equation (2):

The application of this model reported by Case et al. (2006) involved a housing market in which dwellings were found to have been constructed on contaminated land. Discovery of this news could be related to a specific date, and so the repeat sales model made use of transaction pairs straddling the shock date to determine the impact of the shock on price change.

In the context of this study, we suggest the use of the hybrid repeat sales/hedonic model of housing prices first proposed by (Shiller, 1993) and subsequently used in other applications designed to cover the impact, and sometimes the later unwinding, of housing market shocks. The main housing market trends over time are captured through the coefficients of the traditional repeat sales model. Hedonic attributes measured at the point of one sale, but not another, in each pair of matched repeat sales capture the effect of shocks. In our application, the arrival of the SARS-CoV2 pandemic is treated as an initial shock, or a date which may have altered the relative importance of high environmental and home-working amenities. Additional model estimations are then used to test whether the pandemic shocks were permanent or transitory, as explained in more detail in the next section.

Modelling the impacts of environment and productivity attributes on housing prices

Traditional repeat sales model (base or model 1).

***, ** indicate significance levels of 1% and 5%, respectively.

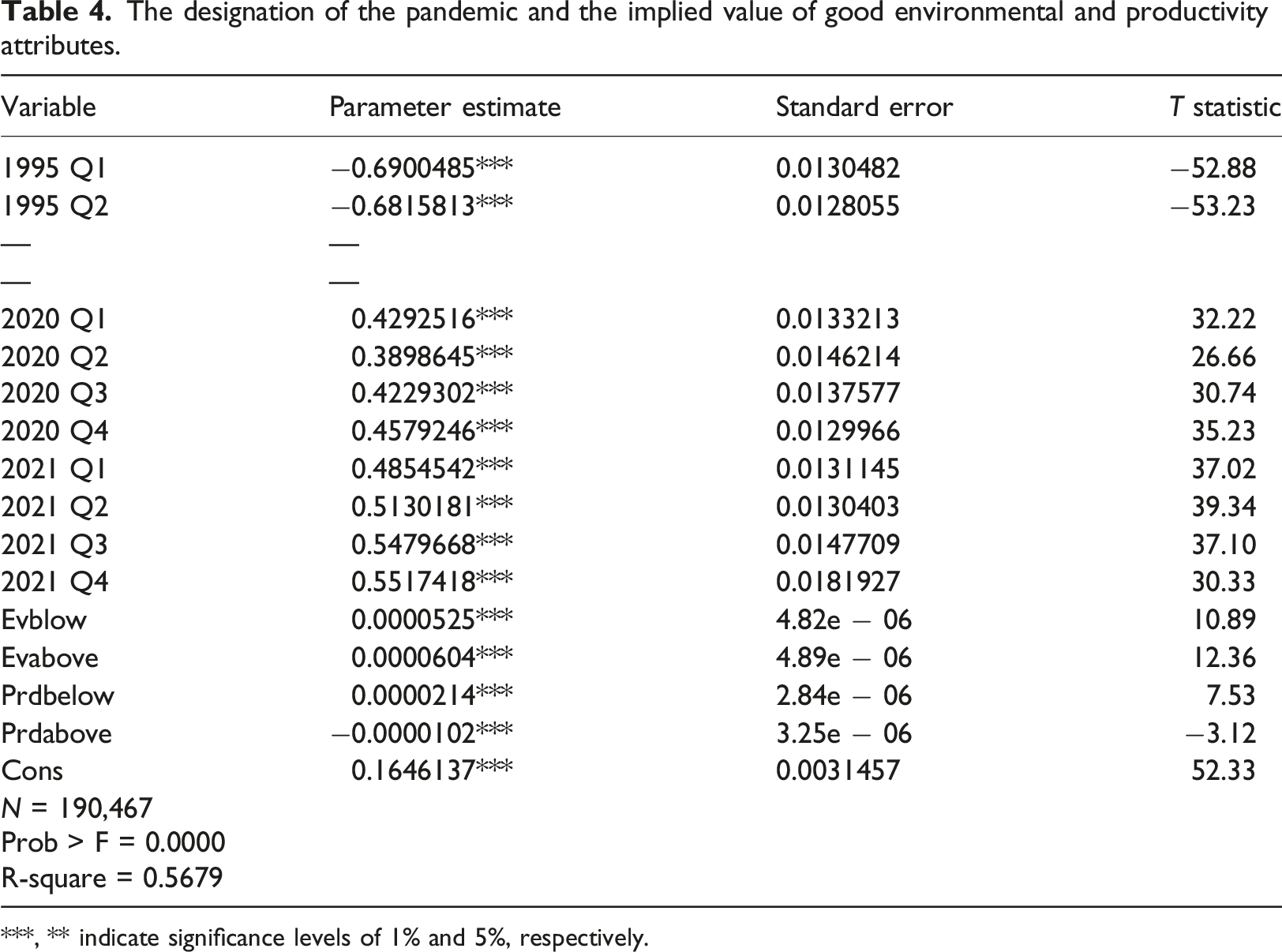

We now introduce a series of hybrid repeat sales/hedonic models designed to test for the combined impacts of the pandemic and the presence of desirable environmental attributes and/or dwelling attributes conducive to enhanced productivity while working from home. As mentioned above, the hybrid RSH model requires the presence of an attribute at one point in time of a pair of observed transactions – but not the other. However, given temporally distributed nature of repeat sales transaction pairs, this is insufficient to extract a parameter estimate. In other words, it is too imprecise to assume that the magnitude of a coefficient 12 months after a ‘shock’ would be the same as the magnitude, for instance, 2 months after the shock. To increase the precision of the measurement of the effect it is necessary to interact the dummy variable denoting the shock or event with a time trend. This can be defined as either a linear variable or some other formulation (e.g. a polynomial). In this study, and partly reflecting the relatively short time span of the pandemic, we have opted for a linear, continuous time trend. March 20th 2020, is chosen as the shock date. This was the date of the official designation by the World Health Organisation of the SARS-CoV2 pandemic.

The designation of the pandemic and the implied value of good environmental and productivity attributes.

***, ** indicate significance levels of 1% and 5%, respectively.

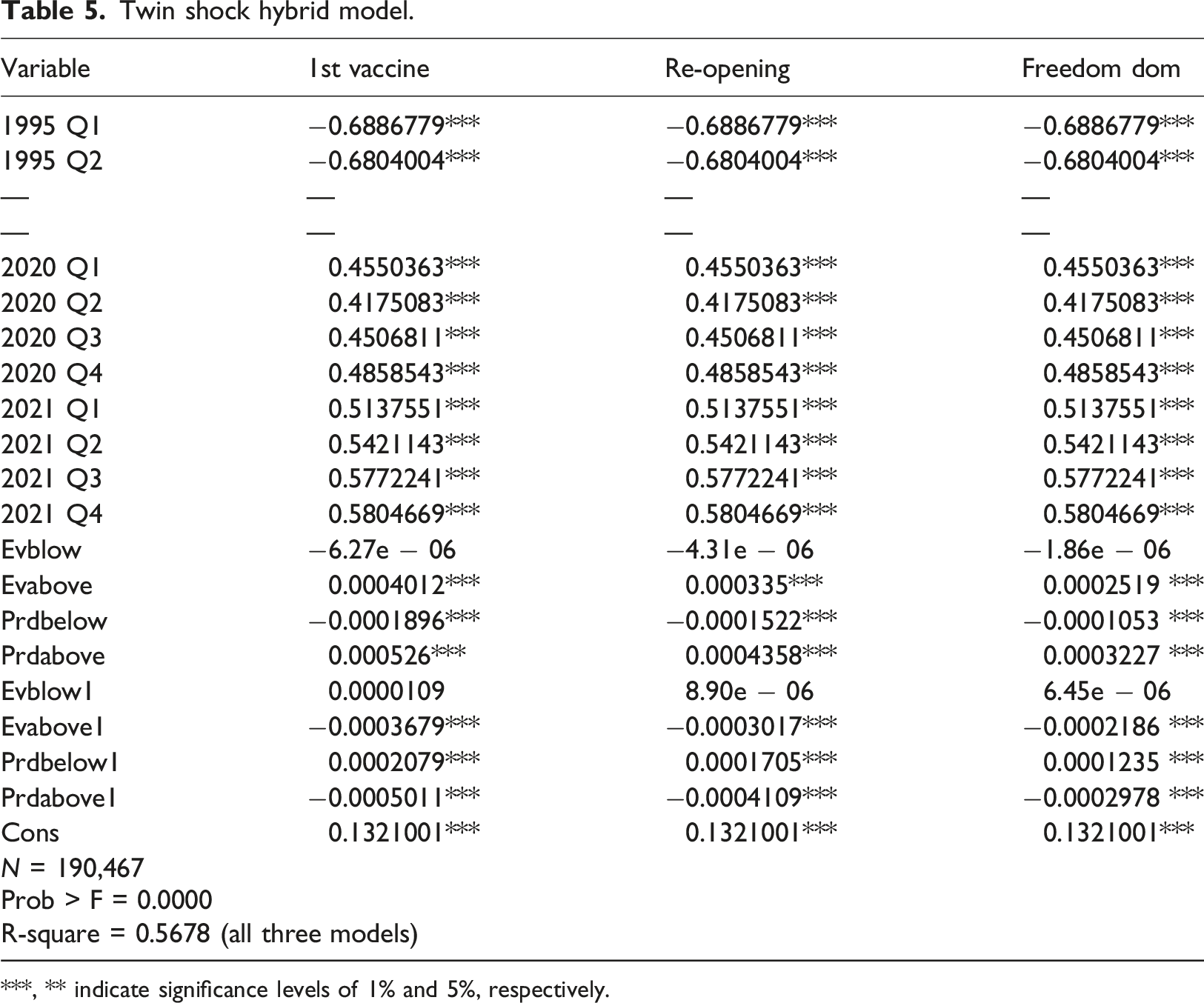

Twin shock hybrid model.

***, ** indicate significance levels of 1% and 5%, respectively.

The results of all three twin shock hybrid RSH models are very similar. The standard time dummy coefficients are almost identical across estimations, and the adjusted R 2 are almost precisely the same. The parameter estimates for the shock interacted with environment/productivity variables differ between the estimations, but the signs and levels of statistical significance are consistent. Taken together, the results clearly show a positive premium for high quality environment and productivity attributes after the announcement of the pandemic. There is also a negative premium associated with low quality dwelling productivity attributes (but not low quality environment) after the announcement of the pandemic on 20th March 2020.

Environment, productivity and house price effects across the urban-rural gradient

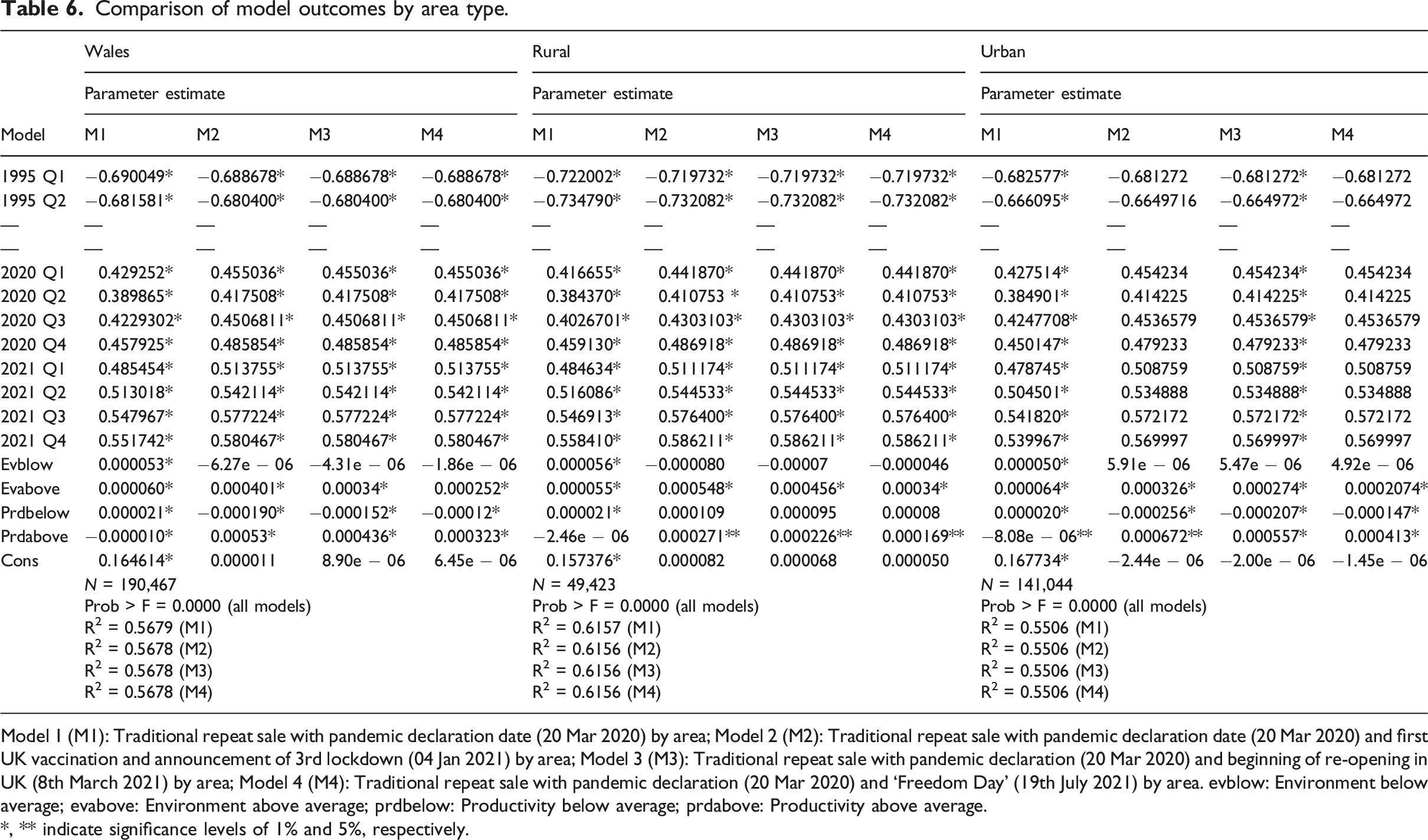

Comparison of model outcomes by area type.

Model 1 (M1): Traditional repeat sale with pandemic declaration date (20 Mar 2020) by area; Model 2 (M2): Traditional repeat sale with pandemic declaration date (20 Mar 2020) and first UK vaccination and announcement of 3rd lockdown (04 Jan 2021) by area; Model 3 (M3): Traditional repeat sale with pandemic declaration (20 Mar 2020) and beginning of re-opening in UK (8th March 2021) by area; Model 4 (M4): Traditional repeat sale with pandemic declaration (20 Mar 2020) and ‘Freedom Day’ (19th July 2021) by area. evblow: Environment below average; evabove: Environment above average; prdbelow: Productivity below average; prdabove: Productivity above average.

*, ** indicate significance levels of 1% and 5%, respectively.

The results also show very consistently that the premia effects reversed sharply after the pandemic entered a less acute, emergency phase. Whichever way the date of the second (positive) shock is defined, the presence of high quality environmental and productivity attributes began to detract from price growth and the presence of low quality features added to price growth during the second phase of the pandemic. It is also noticeable that the magnitudes of the coefficients in the second phase are consistently slightly less than those in the initial phase of the pandemic. This might be interpreted to mean that the positive price premia associated with better quality environmental and productivity attributes did not fully unwind as housing markets transitioned from the emergency to less acute phases of the pandemic.

It is fair to say that the differences between coefficient sizes are very small. It is also worth noting, of course, that the number of observations differs between these contexts (∼50,000 for the rural model and ∼140,000 for the urban context). Nevertheless, as the columns labelled ‘model 2, 3, 4’ demonstrate, the results are not only stable, irrespective of the choice of second shock date definition, but the urban/rural differences are also stable. The implication here is that high quality environmental housing attributes are associated with a premium for both urban and rural settings after the pandemic designation. However, the reverse premium associated with lower quality productivity attributes exclusively affect urban settings.

Discussion and conclusion

The contribution of this study lies in its examination of the trends and implications of COVID-19 on the housing market in Wales, using a hybrid repeat sales approach. The study was framed around two core questions. The first asked to what extent environmental and productivity attributes during the initial phase of the COVID-19 pandemic impacted house price growth differently from what might have been expected. The second considered how the housing market responded during the transition from the initial phase of the pandemic to a more ‘stable’ state, and what were the effects of high versus low environmental and productivity attributes on housing price appreciation? In establishing this framework, we sought to respond to recent calls for in-depth studies on the housing market impacts of COVID that reflect local contexts, amenities, and housing attributes (Colomb and Gallent, 2022).

In answering these questions, we employed a hybrid/hedonic repeat sales approach, drawing on HM Land Registry Price Paid data from 1995 to 2021, to explore how housing and locational attributes – including environment quality, productivity dimensions, and digital connectivity – contributed to changing trends in house prices across Wales before, during and in the post-pandemic period. From the perspective of the first question, we developed a base model alongside hybrid hedonic repeat sales models to examine the impact of environmental and productivity attributes on housing price change. We found that both high and low quality environmental attributes, as well as higher and lower productivity attributes, were associated with higher price growth compared to the average. The coefficients representing the impact of these attributes on price growth were small but nevertheless statistically significant. This trend ran counter to our prior expectations, where we anticipated that price growth would be associated with positive externalities of higher-quality environments and productivity potential (Alves and San Juan, 2021; London Assembly, 2021; Office for National Statistics, 2021a). The subsequent hybrid model considered the time trend and revealed that the effects of environmental and productivity attributes on price growth changed over time, with the effects diminishing slightly as the pandemic transitioned from the emergency to the less acute phases as anticipated by others (Gallent, 2022; Gallent and Madeddu, 2021), albeit with differences in coefficient sizes that were minimal.

Turning to the second question, we went on to consider the combined impacts of the pandemic and the environment and productivity attributes on housing price change during different phases of the pandemic. Three alternative dates were considered to represent the transition from the emergency phase to a more ‘stable’ market context. The results from all three twin shock hybrid RSH models were consistent. After the announcement of the pandemic, there was a positive premium associated with high quality environmental and productivity attributes, and a negative premium associated with low quality dwelling productivity attributes (excluding low quality environment). However, during the second phase of the pandemic, the effects reversed sharply. High quality environmental and productivity features began to detract from price growth, and the presence of lower quality attributes added to price growth. Notably, the magnitudes of the coefficients in the second phase were slightly smaller than those in the initial phase, suggesting that the positive price premiums associated with better attributes did not fully unwind during the transition to the less acute phases of the pandemic.

Perhaps one of the more interesting insights from the empirical analysis, and worthy of further investigation, is the idea that accessibility to a high quality environment affected dwellings in both urban and rural settings. A priori it could be argued that the reverse might have been expected given the anticipation that dwellings in rural locations have readier access to higher quality and more desirable environmental attributes (Bank of England, 2021; Office for National Statistics, 2021a; Pawson et al., 2022; Savills, 2020). At the same time, the premium associated with higher productivity housing attributes appears to be an urban phenomenon, perhaps reflecting an urban productivity dividend identified elsewhere (Bosworth and Venhorst, 2018). Yet we also acknowledge that the findings could indicate some form of sample selection bias. For example, presumably urban dwellers have already made a housing and neighbourhood choice that emphasises productivity over living environment. It follows, then, that the importance of productivity-enhancing dwelling or neighbourhood attributes is more highly valued for them than by their rural living counterparts. These suggestions are, of course, speculative and require in-depth study to unravel further the housing market dynamics revealed through our empirical analysis.

Supplemental Material

Supplemental Material - Valuing the ‘new normal’? Housing markets under COVID-19: Insights from a hybrid hedonic repeat sales model

Supplemental Material for Valuing the ‘new normal’? Housing markets under COVID-19: Insights from a hybrid hedonic repeat sales model by Stephen Hincks, Chris Leishman, Hung Pham and Jenny Preece in Journal of Environment and Planning B: Urban Analytics and City Science.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: UK Collaborative Centre for Housing Research (CaCHE).

Data availability statement

Data sharing not applicable to this article as no datasets were generated or analysed during the current study.

Supplemental Material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.