Abstract

In the late 20th century, homeownership became entrenched in a wider societal project that sought to transform the economy and increase social inclusion. This project focused on mortgaged owner-occupation as a means not only to acquire a stable home, but also to realise greater economic security via asset accumulation. The underlying ideology featured an implicit promise that homeownership would be widespread, equalising and secure. Despite transformations in market conditions, such narratives have continued to underscore policy approaches and housing marketisation. This article directly confronts this promise. It first unpacks its key tenets before investigating their currency across three classic ‘homeowner societies’: the US, the UK and Australia. Our empirical findings reveal declining access to homeownership, increasing inequalities in concentrations of housing wealth and intensifying house-price volatility undermining asset security. The article contends that the imperative of homeownership that has sustained housing policy since the 1970s may be increasingly considered a ‘false promise’. Our analyses expose contemporary housing market dynamics that instead appear to enhance inequality and insecurity.

Introduction

In many ways, the second half of the 20th century reflected a ‘golden age’ of increasing homeownership rates. While differing in precise timing and conditions across advanced economies, this period was largely characterised by strong economic and labour conditions supporting a broader middle class, alongside a solid socio-political backing for homeownership (Conley and Gifford, 2006; Forrest and Hirayama, 2009; Kurz and Blossfeld, 2004). Over this period, homeownership not only established itself as the prime aspiration of individual households, but also became entrenched in a wider vision of socioeconomic inclusion (Forrest and Hirayama, 2015).

Past decades of steadily rising homeownership underscored an optimism surrounding mass homeownership, one that perceived owner-occupation as a widespread and democratic means of shelter and wealth accumulation (Forrest, 2018; Forrest and Murie, 1988). Such ideals crystallised in notions of a ‘property owning democracy’, as promulgated in 1980s Britain but also extant in contexts such as the US and Australia (see Richards, 1990; Vale, 2007). The vision presented a society widely reaping the benefits of property ownership – a ‘nation of homeowners’ (Saunders, 1990). Underlying this were sets of associated values promoting the tenure as the natural fulfilment of both societal and individual desires (see Gurney, 1999).

The centrality of homeownership resonated particularly strongly in the economically liberal, English-speaking ‘homeowner societies’ of North America, the British Isles and Australasia – as epitomised in expressions such as the ‘American Dream’, the ‘Australian Dream’ or an ‘Englishman’s home is his castle’ (Ronald, 2008). In an analysis of political manifestos across 19 OECD countries since 1945, Kohl (2018) revealed deeply entrenched support for the potential of mass homeownership. Particularly among this group of English-speaking nations, the widespread benefits of homeownership were argued across the political spectrum (Kohl, 2018). While these contexts typified the ‘homeowner society’, similar ideals were apparent in many countries, whether the southern European ‘culture of homeownership’ (Fuster et al., 2019; García-Lamarca and Kaika, 2016), post-socialist Eastern Europe (Stephens et al., 2015) or East Asia (Doling and Ronald, 2010; Ronald, 2008).

Dissecting entrenched public and policy support for homeownership uncovers an implicit – or often explicit –promise of homeownership. Ostensibly, homeownership is presented as a means of providing everyone not only a stable home, but also the means to accumulate assets and economic security through housing market mechanisms (Groves et al., 2007). Such a promise was no longer individual, but tied to widespread societal and political goals (Forrest and Hirayama, 2015; Ronald, 2008). At its root, this ‘promise’ proffered a model of owner-occupation based on three key tenets: being widespread in access, being equalising in wealth distribution and providing household economic security over the life course.

Arguably, in some contexts and over certain periods, this promise was at least partially borne out, fuelling continued support for marketised owner-occupation and faith in a ‘homeowner society’ model. This was presented as a ‘virtuous congruence’ between secure employment, strong welfare provisions and widespread homeownership (Ford et al., 2001). Such visions, however, were strongly contingent on specific periods of labour and housing market conditions, substantial state subsidies and often one-off transfers of public stock (Forrest and Hirayama, 2009; Mandic, 2008). Crucially, this idealised promise of homeownership stimulated – or enabled – both an ongoing commodification of housing as well as a shift from state welfare provision towards models of privatised asset-based welfare (Doling and Ronald, 2010).

Despite professed ideals of a ‘property owning democracy’, increasing commodification processes shifted focus from the ‘social’ project of homeownership to a neoliberal project where property became embedded in profit making (Forrest and Hirayama, 2015; Ronald and Kadi, 2017). Even given this transformation into an increasingly financialised commodity (see Aalbers, 2016; Rolnik, 2013; Smith, 2008), the notion of homeownership as a widespread means of economic security and stability mostly persisted (Forrest and Hirayama, 2009; Kohl, 2018). Rooted optimism in homeownership’s societal potential arguably mitigated criticisms of inherent inequalities arising under housing, labour and state welfare restructuring (Arundel, 2017), while entrenching policy support for marketised homeownership at the expense of other tenures (Aalbers and Christophers, 2014; Flint, 2003; Kohl, 2018). In other words, the purported benefits of the ‘property owning democracy’ intensified into a ‘property profiting democracy’ without genuine consideration of the inherent contradictions between property commodification and the balance of democratic distribution.

Recent years have seen burgeoning evidence of growing barriers to homeownership and rising housing market inequalities (see Arundel and Doling, 2017; Lennartz et al., 2016; Wind and Hedman, 2018). Among others, Piketty’s (2014) analyses revealed the particularly outsized share of property wealth in increasingly divided capital accumulation, emphasised in further specific work on rising housing wealth concentration (Allegré and Timbeau, 2015; Arundel, 2017). In this article, we contend that the growing evidence of rising housing inequality necessitates a critical confrontation of the underlying tenets that have sustained contemporary models of homeownership. This article takes on this challenge. Its intention is thus two-fold: (a) to unpack the underlying tenets constituting the promise of homeownership and (b) to empirically assess the extent to which these are borne out among contemporary homeowner societies.

The first section unpacks the three key tenets of the promise of homeownership that have presented the tenure as ‘widespread’, ‘equalising’ and ‘secure’. Subsequently, these tenets are evaluated empirically across the classic homeowner societies of the US, the UK and Australia. Our findings point to housing markets that may increasingly function instead as drivers of rising inequality and insecurity, sharply questioning underlying assumptions that have justified ongoing housing commodification, labour market deregulation and welfare retrenchment.

Unpacking the promise of homeownership

While rates of homeownership expanded across developed societies during the later 20th century, drivers of growth vary considerably. Indeed, the highest rates of owner-occupancy in Europe, for example, are concentrated along the Mediterranean rim, with the most rapid gains achieved in Eastern Europe during post-socialist transition. Nonetheless, across economically liberal English-speaking countries, the tenure’s ascendency aligned with a particular economic and political restructuring common to liberal forms of welfare capitalism (Schwartz and Seabrook, 2008). At the very heart of this realignment has been a political sponsorship and intensive state promotion of homeownership grounded in a particular vision of its wider societal promise.

The idealisation of a ‘property owning democracy’ in the UK can be dated back to a speech in 1929 by future Prime Minister Anthony Eden declaring that: the Conservative objective must be to spread the private ownership of property as widely as possible, to enable every worker to become a capitalist … The wider we can spread the basis of national wellbeing, the larger the share of it every worker in the land can enjoy. (cited in Howell, 1984: 14)

Nonetheless, it wasn’t until much later that policy and discourse became more focused on asserting the widespread socioeconomic advantages of homeownership, particularly after 1979 as the Thatcher administration established steps to expand access to – primarily by rolling out the ‘Right to Buy’ for social tenants – and enhance the fiscal basis for owner-occupation. Indeed, by this time, the promise of mass homeownership was expressly clear: There is in this country a deeply ingrained desire for home ownership. The government believes that this spirit should be fostered. It reflects the wishes of the people, ensures a wide spread of wealth through society, encourages personal desire to improve and modernize one’s home, enables people to accrue wealth for their children, and stimulates the attitudes of independence and self-reliance that are the bedrock of a free society. (Michael Heseltine, Secretary of State for the Environment, cited in Hansard, 1980)

In the US, meanwhile, the launch of the propagandist Own-Your-Own-Home campaign, following the First World War, proposed a state-sponsored homeownership expansion (Vale, 2007), bolstered more effectively by the establishment of the Federal Mortgage system in the 1930s that aimed to realise majority homeownership. Between the 1960s and 1980s, homeownership in the US coalesced as the politically favoured and socially aspirational tenure (McCabe, 2016). In the 1990s and 2000s, attention again centred on homeownership expansion – especially among more marginal, non-white households – as a social project, with Bush claiming in 2002, ‘We can put light where there’s darkness, and hope where there’s despondency in this country. And part of it is working together as a nation to encourage folks to own their own home’ (New York Times, 2008). In this context, homeownership was also increasingly promoted as a means to expand access to asset wealth accumulation (Belsky and Retsinas, 2005).

Similar narratives in Australia emphasised the ‘societal benefits’ of homeownership, with governments long being committed to expanding owner-occupation as key to the imaginary of an ‘Australian Dream’ (Troy, 2000). In the 1990s, a more neoliberal vision of homeownership emerged, characterised in Prime Minister Howard’s promotion of a ‘share owning democracy’. Homeownership became explicitly associated with a potential democratisation of wealth. This was intertwined with the idea of the ‘workfare state’, which sold the notion of families building up, and relying on, their own assets rather than public services (Nethercote, 2019).

While comparable political and economic motivations can be found elsewhere (see Doling and Ronald, 2010; Forrest and Hirayama, 2015), support for homeownership across the contexts identified above derives from common assertions in the connections between property ownership, citizenship, social inclusion and economic growth. Critically, the ideology of mass homeownership in these contexts has enjoyed wide political support and increasingly represented a ‘social contract’ between the state and individual households founded on the assumed socioeconomic potential of the tenure. While the ‘promise of homeownership’ is diverse in its manifestation, there are, nonetheless, three key tenets that have – implicitly or explicitly – underscored ideological optimism and expectations of tenure transformation in homeowner societies: that homeownership can be widespread, equalising and secure.

Widespread

The fundamental first premise of a homeowner society is that access is open to the vast majority of households and eventually likely without disproportionate hardship. Forrest and Hirayama (2015: 1010) emphasise that across homeowner societies, ‘homeownership, or at least the promise of access to the tenure, was an important element of the social contract’. Concepts of conventional housing ladders (Kendig et al., 1987), the ‘democratic’ promise of a ‘property owning democracy’ or the ‘nation’ of homeowners (Saunders, 1990) all emphasise the inclusivity – or eventual attainability – of mass homeownership. The political mobilising of such narratives in support of transformations of housing markets (or even labour deregulation and welfare retrenchment) has emphasised a collective benefit in the pursuit of homeownership.

Malpass (2006) argues that at the root of housing market transformations in homeowner societies has been the notion of ‘choice’, underscoring – as in other domains – the political promotion of neoliberal shifts in housing. Malpass (2006: 111) contends, however, that: Choice is a weasel word, a seductive device concealing that what is really afoot in the creation of an ‘opportunity society’ is promotion of the interests of the better-off and toleration of wider social inequality, to the further disadvantage of the poor.

While the debate on choice and state intervention has a long history (see Titmuss and Seldon, 1968), it is in housing that such narratives have seemingly most flourished. While ‘choice’ implies the option of desirable outcomes for all, this masks that the very actions on the housing market of those with a preponderance of ‘choice’ may be intrinsically linked to growing numbers facing diminished opportunities – and the increasing divides between them.

Just as fundamental as a vision of widespread access in homeowner societies has been the assertion that the means to such a goal is through market mechanisms (Aalbers and Christophers, 2014; Flint, 2003; Shlay, 2006). Economically liberal, English-speaking countries pushed for expansion of the tenure through deeper policy interventions and housing finance deregulation. In the US, Bill Clinton championed mortgage deregulation as a means ‘to ensure that families currently underrepresented among homeowners – particularly minority families, young families, and low-income families – can take part in the American dream’ (cited in Ronald, 2008: 148). Gordon Brown’s 2005 UK election campaign – in the run-up to the (Great Financial Crisis (GFC) – centred on the promise of a ‘home-owning, wealth

By consequence, such promises of an asset-owning democracy implied reduced state support for alternative housing options in favour of stimulating the homeownership market. As Malpass (2006) and Hodkinson and Robbins (2013) demonstrate in the British context, political narratives upholding the promise of widespread homeownership have frequently been interwoven with the legitimation of housing market reform. These justifications are mobilised even in enabling the very reforms that saw growing inequality in housing outcomes. Forrest and Hirayama (2009: 1002) attest that, despite declining access in the post-crisis years, the notion of homeownership as a widespread means of economic security persisted with an ideological-political ‘consensus around the superiority of the market and shared commitment to homeownership’.

Equalising

The second ‘promise’ is the implication that housing assets can be a redistributive force in equalising wealth accumulation across society. This notion is clearly tied to the tenet of widespread access, building on the inclusivity of political narratives such as the ‘property owning democracy’, ‘share owning democracy’, ‘nation of homeowners’ and ‘choice’ societies. The implication, however, goes beyond housing market entry in also stressing widespread opportunities for wealth accumulation, as fundamental to the political agenda of homeownership expansion (Forrest, 2018; Forrest et al., 1994). The distributive potential of property wealth is further entangled in the increasing political purchase of asset-based welfare models across homeowner societies (Doling and Ronald, 2010). These have asserted the possibility of widespread private housing assets as an alternative to state redistribution (Forrest, 2018).

Narratives on the equalising potential of housing wealth point to the fact that, in high homeownership countries, housing assets often represent the largest financial holding for most households (Rowlingson and McKay, 2012; Smith, 2008). These ignore, however, the extent that higher shares of homeownership are contingent on past growth during certain periods of favourable labour, housing and state contexts (Arundel and Doling, 2017; Forrest and Hirayama, 2018). Comparisons with the extreme inequality of some other asset classes have often obfuscated critical examination of the housing market’s own role in wealth inequality (Appleyard and Rowlingson, 2010). Such optimism towards the equalising nature of housing wealth appears increasingly unwarranted given burgeoning evidence of growing divergence in both homeownership access and, even among homeowners, differentiations in asset accumulation (Arundel and Lennartz, 2019). Nonetheless, limited research has questioned the purported equalising role of housing through assessing contemporary property wealth distribution.

Secure

The third key tenet has been the notion of homeownership as intrinsically secure. At its root, homeownership has long been associated with ideologies of security (see Dupuis and Thorns, 1998; Duyvendak, 2011). Beyond ontological meanings of security, expectations of tangible economic security through owner-occupation form the foundations for policy promotions of asset-based welfare. Kemeny (1981) and Castles (1998) describe a ‘big trade-off’ where the promotion of property investment enables a supplanting of state welfare provision. Proponents contend that homeownership offers a means for households to build up secure assets which may be relied upon in times of need (Doling and Ronald, 2010; Sherraden and Gilbert, 1990).

These narratives often fed into privileging homeownership at the expense of the security of other options, including retrenchment in social housing, rent-control policies or tenant protection across many countries (Flint, 2003). At the same time, processes of housing financialisation have promoted riskier mortgage practices and exacerbated market volatility (Aalbers, 2008, 2016), undermining the security of owner-occupation itself. This was witnessed most dramatically in large-scale foreclosures in some countries following the GFC (García-Lamarca and Kaika, 2016; Haffner et al., 2017; Pareja-Eastaway and Sánchez-Martínez, 2017). Despite this, the association between homeownership and security remains largely entrenched in societal imaginaries. In the US, 75% of households perceived housing as being a ‘safe bet’ in 2015, similar to pre-crisis levels (Adelino et al., 2018). In the UK, homeownership aspirations have remained consistently high, with the majority listing benefits of ‘financial security’ and only half as many noting concerns over devaluation risks (Pannell, 2016). Even among young adults, arguably most affected by the crisis, a vast majority still state that they have expectations for home-buying in the near future (Forrest, 2018; HSBC, 2017). Alongside other tenets, this entrenched perception of security may help explain both the levels of risk some households are willing to undertake in entering (indebted) homeownership and support for policies that have seen a retrenchment of other dimensions of economic security.

Recent years, since the GFC, have seen a context of diminished credit, rising employment insecurity and new patterns of global real estate investment, resulting in intensified housing affordability stress across many countries. While this is recognised in political and policy responses, governments have, nonetheless, largely continued to reproduce policies and narratives associated with the promise of homeownership. Housing policy across the UK, the US and Australia has retained a strong tenure bias, with a focus on sustaining the flow of first-time buyers. In the UK, there was arguably a doubling down on pro-homeownership market reform in the years following the crisis (Hodkinson and Robbins, 2013), and, although there have been discussions of initiatives that address other tenure options in recent years, there is little evidence of a new policy direction. In Australia, first-time homebuyer grants have been continually extended, with the Morrison government in 2019 arguing that through its market policies it ‘believes that all Australians should be able to aspire to own their own home’ (Liberal Party, 2019). While policy narratives in some contexts have tempered explicit claims on extending homeownership in favour of goals of ‘alleviating’ sector decline and ‘sustaining’ access, the underlying promise of home-ownership has been minimally questioned in mainstream policy narratives.

Empirically evaluating the promise of homeownership

Having outlined the key tenets of the ‘promise of homeownership’, the following empirical analyses attempt to directly evaluate these across three countries, seen as classic homeowner societies: the US, the UK and Australia. Each of the three tenets is examined in relation to relevant macro-level indicators and in terms of recent trends. These analyses remain exploratory in aim, with the objective of spurring ongoing research on how the explicit realities of housing markets may contradict – and increasingly so – entrenched ideologies of homeownership. The operationalisation of each of the three tenets is presented below.

Operationalisation and methodology

In operationalising the extent that home-ownership can be characterised as widespread, the Luxembourg Income Study (LIS) provides large harmonised datasets across the three countries. The LIS includes useable data for the UK from 1986 to 2013, for the US from 1986 to 2016 and for Australia from 1981 to 2010 (LIS, 2018), allowing the examination of trends over nearly three decades. Homeownership attainment is firstly examined for the entire adult population (defined as over 18 years old), for young adults aged 20–39 years old who live independently (defined as not residing with parents) and for individuals aged 55–64 years old. Looking at independent young adults captures the ability of home-leavers to enter the housing market, while 55–64-year-olds represent the oldest working-age group (that thus can be differentiated on working income). This older group constitutes those most likely to have reached the peak of their housing career and most expected to rely on housing wealth in models of asset-based welfare. Secondly, each age group is further divided based on income, with an examination of those in the bottom two quintiles (based on equivalised household income). Across these income and age groups, the analysis focuses on shares and trends of non-homeowners in assessing the extent that the tenure is ‘widespread’ across different sectors of society. For the UK and Australia, it is further possible to distinguish outright and mortgaged homeowners.

The second analysis of the equalising nature of homeownership turns to a partner dataset, the Luxembourg Wealth Survey (LWS), which provides crucial harmonised data on wealth and assets. The LWS is relatively new and unfortunately provides a more limited historical perspective than the LIS. For Australia, the LWS is currently only available for 2010, while for the UK it is possible to measure trends from 2007 to 2011. The US data allow a much longer examination across the period 1995–2016. Despite some limitations (i.e. for Australia), the dataset remains invaluable given the dearth of accurate wealth data. In operationalising the ‘equalising’ nature of housing wealth, the analysis examines distributions of housing equity across households (measured as total housing values minus total outstanding debts for all properties owned). Standardised values are used to measure the difference for each equity decile relative to average equity. Beyond this, a look at housing values (without subtracted debts) provides a proxy for the ‘potential’ achievable assets of properties. Concentration levels of both total equity and housing values evaluate housing wealth inequality with, for the US and the UK, a further assessment of trends over time.

In examining the third tenet of security, the analysis focuses on the key indicator of housing price volatility. Whereas security through property assets relies on a steady increase in housing prices, volatile housing markets may result in insecurity and the potential of equity loss, especially for those less able to wait out downturns and time entry and exit (Allegré and Timbeau, 2015). House-price volatility is further linked to diverging outcomes among homeowners, thus also undermining the associated tenets of widespread and equalising housing markets. The analysis looks at long-term price data, allowing an examination of both the degree of volatility and assumptions that it may have increased in the face of financialisation processes (Aalbers, 2008, 2016; Larsen and Sommervoll, 2004). For the United States, the Case-Shiller Index is used, based on a methodology of repeat sales (Shiller, 2017). The data are inflation-corrected, updated quarterly and available from 1953 until 2017. For the UK, the Nationwide Index provides the longest unbroken data-series, similarly available from 1952 to 2017, using a hedonic regression method to calculate price changes for properties of similar characteristics (Nationwide, 2018). Finally, data for Australia are more historically limited. Combining the available House-Price Index and the Residential Property Price Index (both from the Australian Bureau of Statistics) allows an analysis from 1986 to 2016. Both indices are weighted averages from the eight state capitals (nonetheless comprising about 66% of the national population). The UK and Australian datasets were both also inflation corrected. For all three countries, calculations were made in proportional house-price change considering a hypothetical purchase either two, five or seven years earlier. The approach provides an assessment of changing returns considering short, medium or medium-long term property investments. Subsequently, a calculation of volatility was also made for the house-price indices over five-year intervals using measures of standard deviation. A calculation for the slope of volatility indicates ‘change in volatility’ and its statistical significance.

Results

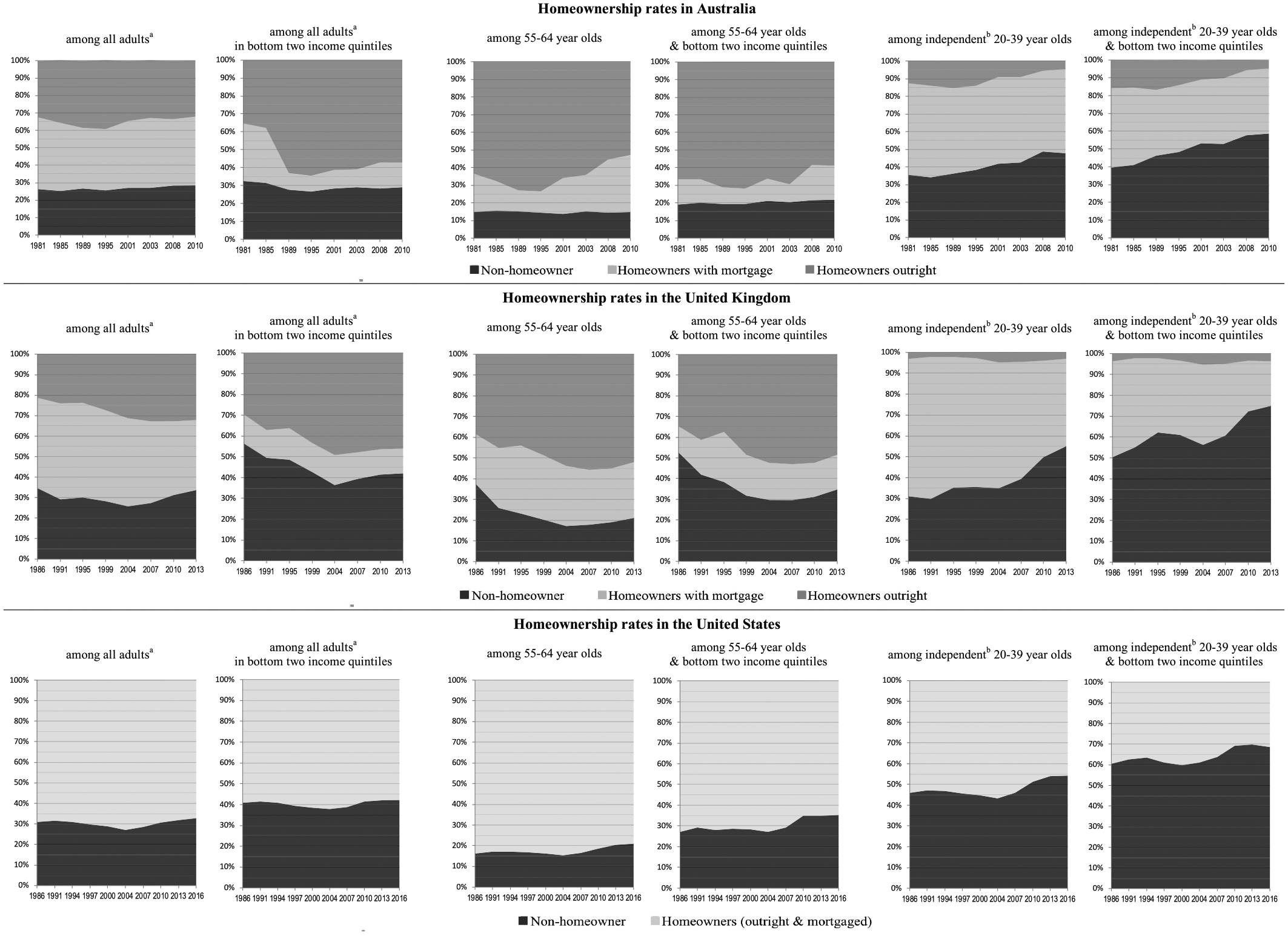

Widespread

The first tenet investigated is the degree to which access to the tenure is widespread. The resulting graphs (Figure 1) present shares of non-homeowners and homeowners over approximately three decades across the countries. For Australia and the UK, it is also possible to differentiate outright and mortgaged owners. In each country, shares are shown for the full adult population, those between 55–64 and independent 20–39-year-olds. For each group, the sub-categories of those in the bottom two income quintiles are further examined.

Homeownership rates.

Looking at the first measure of levels of homeownership attainment among all adults (Figure 1– left-most graphs), we can see that there remains a very significant proportion of households not in homeownership, at around 30%. The data indicate some fluctuation; however, the share of non-homeowners never dips below roughly one quarter of the population in any of the three ‘homeowner societies’. Past trends reveal some reductions in the UK of non-homeowners up until the mid-2000s, with more minimal declines in the US. Some increases in ‘outright homeowners’ are also visible over the same period for the UK and for Australia until the late 1990s. However, recent trends point to a reverse dynamic. Both the UK and the US show clear trends of increasing shares of non-homeowners among all adults since around the financial crisis of 2007 or just before, with the US, where 2016 data are available, stabilising but at a higher level. While for Australia the change in non-homeowners is limited, the trend has been a gradual increase since the mid-1980s and a decline in outright homeowners since the mid-1990s.

Looking at all lower-income households, there is clear evidence of differentiated homeownership entry based on income position, calling into question notions of widespread access across sectors of society. For lower-income individuals, both the UK and the US show recent shares of non-homeowners nearly 10 percentage points higher than for total adult population, with Australia showing a more modest but measurable difference. The Australian and UK data do reveal past growth in lower-income outright homeowners, likely representing increasing shares of older and retired homeowners; however, these increases are limited to a specific period up until about 1990 in Australia and the early 2000s in the UK. This reflects a baby-boomer generation – having experienced more robust labour market conditions – able to pay-off mortgages before entering retirement (Forrest and Hirayama, 2009; Kurz and Blossfeld, 2004). On the other hand, as the data reveal, the contemporary context demonstrates a reversal of this trend, with shares of outright homeowners and homeowners overall declining among lower incomes. This is most evident since the mid-2000s for the UK and the US, while more gradually but over a longer period for Australia. In other words, beyond the fact that significant shares of these populations were always shut out of homeownership (particularly lower-income households), the data reveal worsening access, especially in the post-crisis period in the UK and the US. Together these results support claims of homeownership growth being contingent on specific periods of improved labour market conditions alongside unsustainable growth in credit access (Arundel and Doling, 2017). One-off government transfers of public assets also played a role in some contexts, such as ‘Right To Buy’ sell-offs in the UK which contributed significantly to home-ownership expansion in the 1980s and early 1990s (Jones, 2003).

The subsequent analyses presented in Figure 1 examine homeownership dynamics among older working-age populations. Looking at 55–64-year-olds captures a group ‘nearing retirement’ who, following notions of asset-based welfare, would be most expected to imminently rely on housing assets (Doling and Ronald, 2010). They are also more likely to have reached the ‘top’ of their housing career (Kendig et al., 1987). As anticipated, the results reveal lower shares of non-homeowners among the older age group, representing more favourable past labour, housing and policy contexts (Arundel and Doling, 2017; Buchmann and Kriesi, 2011). While not discounting a still measurable share of non-homeowners, Australia most clearly reflects ideals of higher and stable attainment among this older group. Even given the ‘better case’ of Australia, however, the share of outright homeowners has significantly declined since the mid-1990s. Both the UK and US reveal increasing numbers excluded from home-ownership after the mid-2000s. While the UK saw a period of improving access for this group, the trend has dramatically reversed, and it now exhibits the highest share of older non-homeowners. Looking at 55–64-year-olds with lower incomes reveals similar trends but significantly higher rates of non-homeowners across all three countries. These results reveal both the lack of homeownership attainment as well as significantly worsening conditions for those nearing retirement and on lower incomes, with fundamental implications for the potential for housing assets to supplant public welfare support in old age.

The final graphs in Figure 1 examine how entry to homeownership has changed among independent 20–39-year-olds. Even given the expectation of lower homeownership rates among younger cohorts, the results reveal stark increases in those excluded from homeownership across all three countries. Long-term increases are apparent for both Australia and the UK, and in the period after the mid-2000s for the US. Already high shares of non-homeowners increased further, by roughly 10 percentage points, for both Australia and the US, while the UK saw a near doubling. Similar dynamics are apparent among young adults with lower incomes, but reaching even higher shares at or above 70% non-homeowners in the US and UK and nearly 60% in Australia, with only marginal declines in the most recent US data.

Taken together, the analyses of home-ownership attainment reveal the extent that so-called homeowner societies remain characterised by large population shares excluded from owner-occupation and the extent that this is sharply differentiated by age and income. Most crucially, the data reveal worsening trends in homeownership access across all three countries. While some historically contingent periods encouraged optimism in the potential of widespread access, the longer-term evaluation of homeownership distribution both emphasises the exceptionalism of periods of wider growth (Forrest and Hirayama, 2018) and calls such ideals into question given persistently significant shares of non-homeowners and declining housing market entry.

Equalising

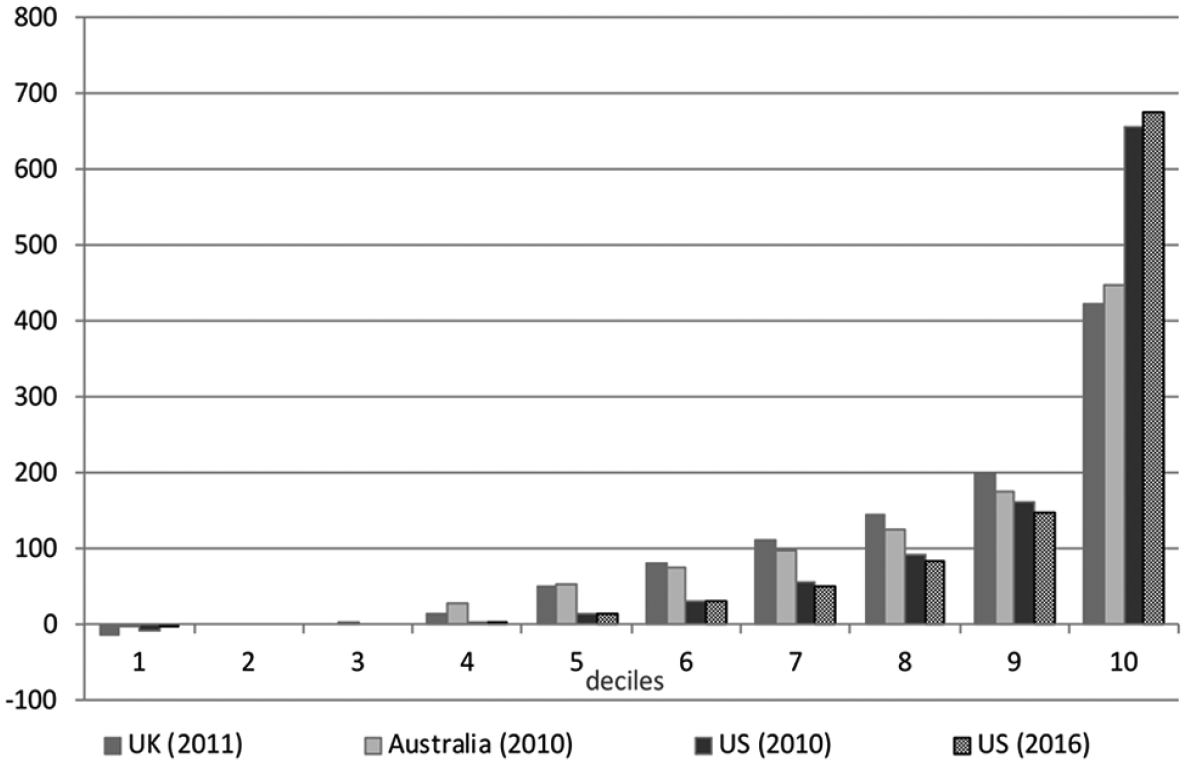

The second empirical investigation tackles the notion of homeownership as an equalising force for wealth distribution across society. As a measure of property wealth, housing equity distribution across all households (total reported values minus total outstanding debts of all properties) is presented for the three countries.

Figure 2 shows the results of standardised housing equity distribution across deciles for the most recent years of the Luxembourg Wealth Study (including 2010 for the US for comparability). The data immediately reveal the starkly uneven distribution of housing wealth across households. The results show especially sharp concentration of housing wealth among the top decile, with none, negligible or even negative equity for the bottom 30% to 50% of households, depending on the country. The US reveals the most uneven equity distribution, where the top decile owns over six and a half times more than the average. While lower, Australia and the UK showed concentrations among the top decile still over four times greater.

Housing equity distribution across deciles. Average household equity = 100.

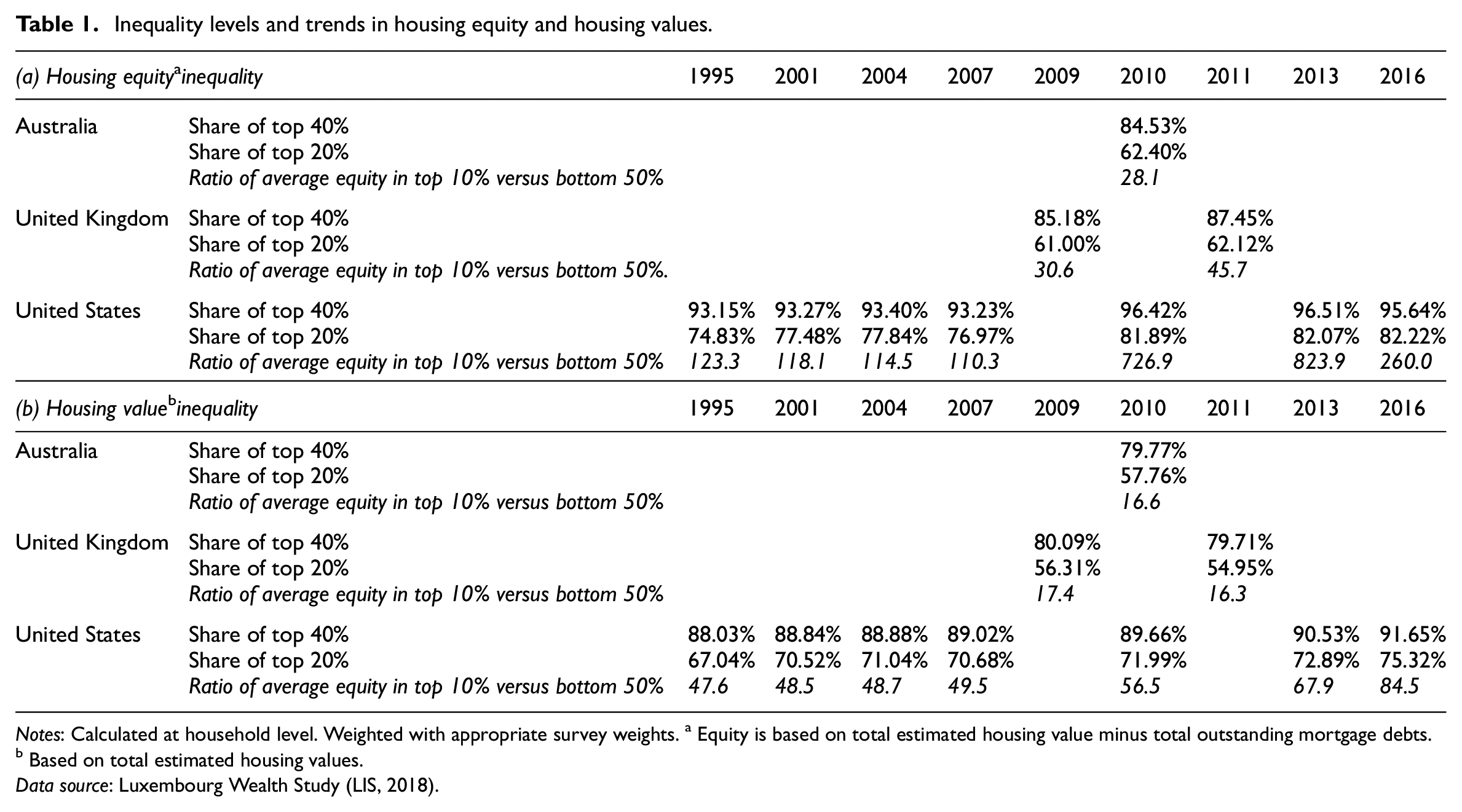

Table 1 presents further measures of property wealth concentration across the three countries over available data years. Table 1(a) reveals that, in both Australia and the UK, the top 20% hold over 60% of equity, with the top 40% having about 85%. These stark concentration levels are surpassed by the US, where the top 40% consistently holds over 93% of all housing equity. Looking at trends for the UK and the US, the data reveal that already high levels of concentration have further increased. While the UK only provides two data points, results are consistent with other research using the national Wealth and Assets Survey, showing increasing equity concentration (Alvaredo et al., 2016; Arundel, 2017; Crawford et al., 2016). The US data reveal that the very high levels of concentration have further increased, especially post-crisis, with only the most recent recovery period seeing a small decline in the top 40% share but further concentration among the top 20%.

Inequality levels and trends in housing equity and housing values.

Notes: Calculated at household level. Weighted with appropriate survey weights. a Equity is based on total estimated housing value minus total outstanding mortgage debts. b Based on total estimated housing values.

Data source: Luxembourg Wealth Study (LIS, 2018).

Considering the ratio of average equity held by the top decile compared with that held by the full bottom half of households reveals increases from already over 100 times pre-crisis (1995–2007), up to peak ratios of more than 800 times in 2013. These stark numbers reflect both increasing housing wealth at the top end as well as growing shares of non-homeowners and precarious owners with negative/negligible equity. The partial recent recovery for the US still displays a dramatic multiple of 260 times more among the top decile. To further take into account the inequality of equity among homeowners and the effect of mortgage repayment cycles, Table 1(b) looks at the reported housing values (not subtracting debt) as a proxy for total potential housing wealth given full loan repayment. While inequality levels are unsurprisingly lower, concentration remains very significant among the top 20% and 40%, with similar rates for Australia and the UK and even higher for the US. The only apparent difference is a slight decrease in inequality for the UK between 2007 and 2011, albeit remaining at high levels. The US shows a pattern of continually increasing inequality up to the most recent data.

Taken together, these results demonstrate the starkly uneven nature of housing wealth, with very high proportions concentrated among a limited number of households. This is especially reflected in the wealth levels of the top 10% being at many multiples greater than those of the entire bottom half of households. These results complement research in the UK that emphasised a concentration of housing wealth, particularly among a subgroup of multiple property owners and landlords (Arundel, 2017; Ronald and Kadi, 2017). The importance of these findings is amplified by the growing dominance of housing wealth in global capital (Piketty, 2014). This assessment of equity concentration fundamentally challenges policy narratives that assert the potential of homeownership as an equalising force of wealth distribution across society.

Secure

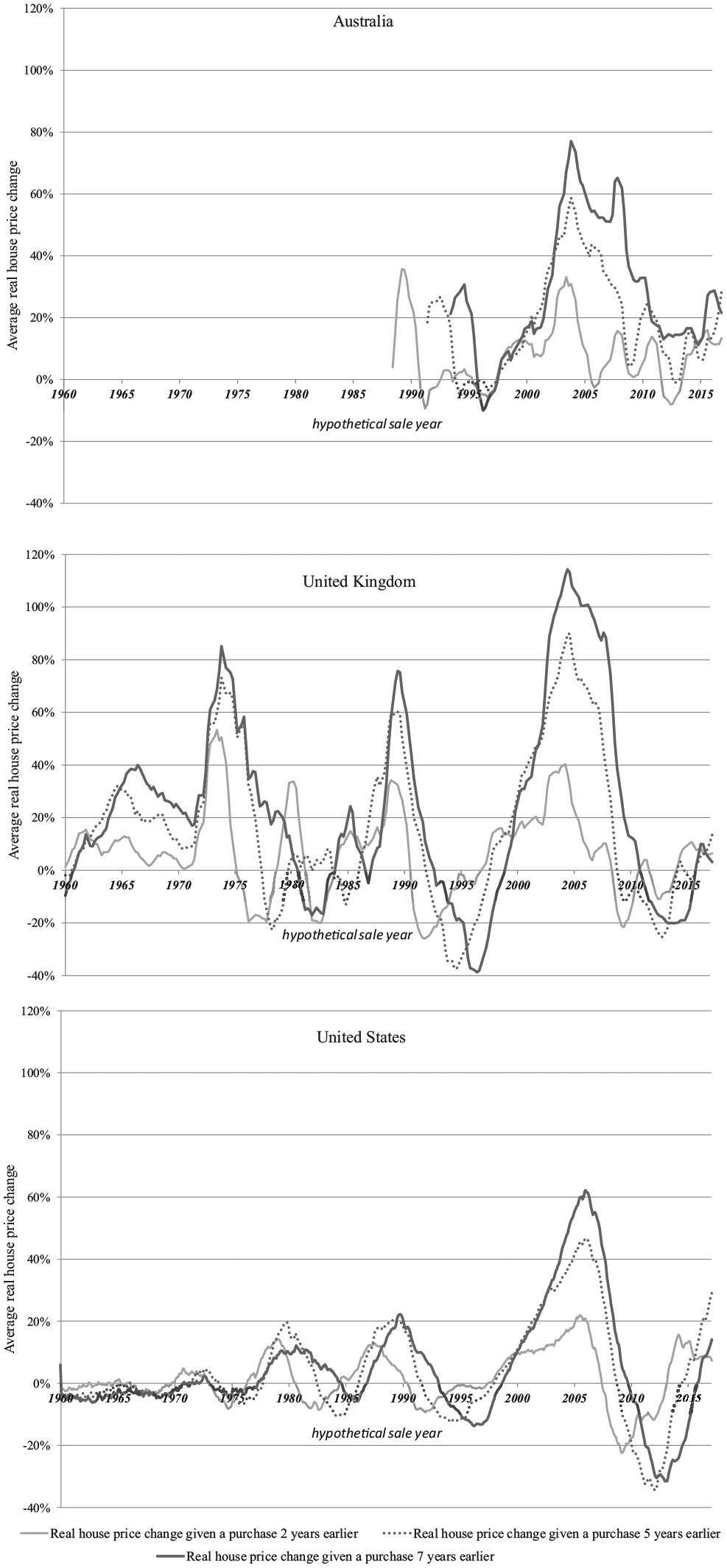

The final analysis examines the promise of economic security through homeownership. While we cannot capture every dimension of housing market precarity, house-price volatility focuses on the crucial aspect of returns on homeownership assets. House-price fluctuations especially impact more precarious households, with those facing immediate economic necessities less able to wait out lower/negative return periods (Doling and Ronald, 2010; Forrest and Hirayama, 2009). Increased volatility therefore has a potential deleterious impact on the ability to reliably deploy housing assets in times of need. On top of this, differentiated impacts on more marginal homeowners would likely increase insider–outsider divisions, thus undermining further ideals of widespread and equalising homeownership.

The results (Figure 3) calculate hypothetical returns for homeowners given a purchase two, five or seven years earlier for each country (on the same scale). While patterns are distinct, the data reflect high levels of fluctuation in housing prices for all three countries, at least in recent decades. Although the time-scope is more limited for Australia, it shows the most consistent positive returns in recent decades. However, volatility during this period remains high, indicating very differentiated (and unpredictable) returns for different purchase and sale periods. Short-term investments – that is, necessitating a sale within two years of purchase – in particular see many periods of limited or even negative returns. The longer-term UK data, on the other hand, reveal the strongest level of house-price volatility, with hypothetical gains reaching close to 120% and losses down to negative 40%. In other words, while many investment periods see positive returns, significant losses are frequently apparent over the period, undercutting longer-term predictability and security. While volatility is apparent throughout the period, the extremes appear highest in recent decades, especially regarding the boom and bust pre- and post-GFC. Lastly, while the US data reveal lower volatility over the long term and a historically extended period of more stability, the pattern reveals clearly increasing volatility since roughly the 1980s.

Housing price volatility.

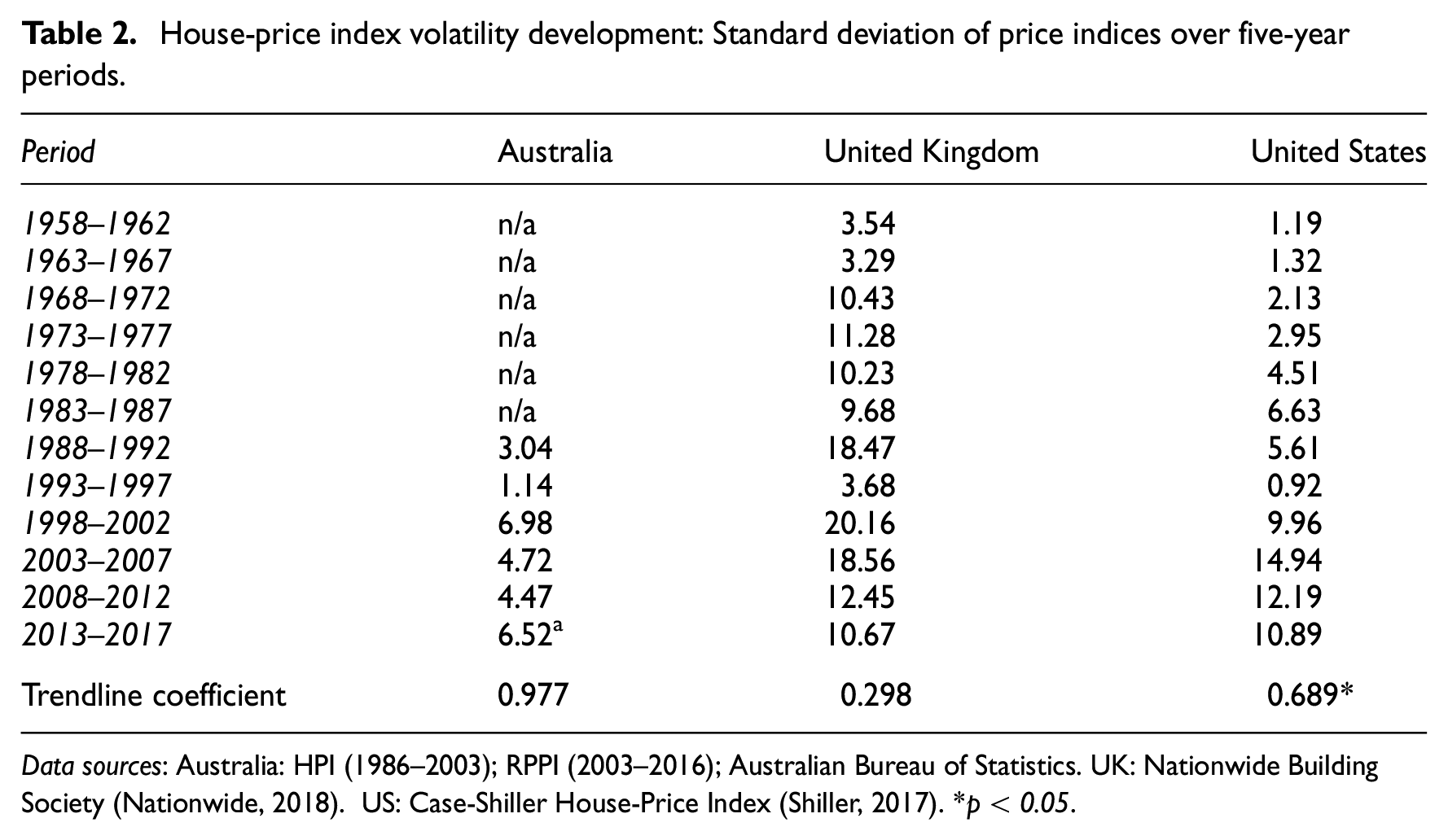

Table 2 provides a further statistical measure of changes in volatility over five-year interval periods. The results confirm a general trend of increasing measures of standard deviation in house-price indices, with positive trendline coefficients. These values are greatest for Australia and the US, with the lower UK value reflecting the higher volatility throughout the period. Only the US value proves to be statistically significant (p < 0.05) – albeit the limited Australian sample makes it difficult to assess significance. Overall, the analyses provide evidence of high volatility levels in recent decades for all three countries, over the long term in the UK, and clearly increasing volatility in the US. There is tentative evidence of growing instability in Australia and the UK. While financial crises may always present cyclical threats to market stability over the long term (see Reinhart and Rogoff, 2008), the data point to growing volatility pre-dating the GFC, and, in recent years, shorter intervals and stronger intensities between cycles. The trends support arguments of growing insecurity associated with increased risks in the face of financialisation, rising speculation and global capital interdependencies in housing (Aalbers, 2008, 2016; Fligstein and Habinek, 2014). Taken together, the evidence of high volatility and worsening trends directly challenges the stability and security of homeownership assets.

House-price index volatility development: Standard deviation of price indices over five-year periods.

Data sources: Australia: HPI (1986–2003); RPPI (2003–2016); Australian Bureau of Statistics. UK: Nationwide Building Society (Nationwide, 2018). US: Case-Shiller House-Price Index (Shiller, 2017). *p < 0.05.

Discussion and conclusion

This article has sought to lay bare the underlying tenets that have driven, either implicitly or explicitly, support for marketised homeownership models (Doling and Ronald, 2010; Forrest, 2018; Kohl, 2018; Ronald, 2008). At its root, an enduring homeownership ideology has presented the tenure as holding a societal ‘promise’ of being widespread in attainment, being equalising in wealth distribution and providing economic security over the life course.

The article presents compelling evidence that, even in so-called ‘homeowner societies’, faith in the promise of homeownership is detached from the reality of contemporary housing market developments. The empirical evidence from the US, the UK and Australia presents, instead, significant shares of non-homeowners and clearly declining access – differentiated across income and age groups – bringing into question the implicit inclusivity of homeownership ideologies. On top of this, far from an equally distributed asset, housing wealth appears strongly concentrated and, where data are available, trends reveal worsening inequalities. Even among homeowners, the security that property assets provide is highly contingent on housing market dynamics, where longitudinal data point to strong and increasing house-price volatility. These results are all the more salient as they have occurred in a context of rising labour market insecurity, growing housing financialisation and retrenched public services (Forrest and Hirayama, 2015; Kurz and Blossfeld, 2004) – circumstances which have only emphasised the importance of housing market position as property assets are increasingly seen as central to household economic security.

Nonetheless, transformations of housing, labour and state welfare contexts have often been sustained with promises of widespread security through access to property assets. Optimistic narratives of the potential of a ‘property owning democracy’ have mostly persisted, and a commitment to homeownership has seemingly gained currency with the spread of increasingly financialised housing markets and shifts towards asset-based welfare policies (Aalbers, 2008, 2016; Forrest and Hirayama, 2015). As states retreat from broader welfare support, the promise of homeownership provides an alternative vision to stability and security. Past periods of more widespread access to homeownership loom large in the political and societal narratives of the democratic promise of homeownership, but may indeed be better represented as periods of historical exceptionalism (Forrest and Hirayama, 2018). The US, the UK and Australia present salient examples where embedded ideologies of the ‘homeowner society’ seem contradicted by increasing divides in access to homeownership, growing housing wealth disparities and insecurity in the face of market volatility. As advanced homeowner societies, they offer lessons for other contexts that have increasingly embraced the societal potential of marketised homeownership (Forrest, 2018) under commonalities in market transformations (Hay, 2004).

As this article argues, it is essential to both uncover and challenge implicit and explicit assumptions promoting ongoing optimism in homeownership models that have prioritised ‘market’ forces over the ‘social project’ of housing (Forrest and Hirayama, 2009, 2015). Through an examination of contemporary housing dynamics, we contend that the purported societal potential of such homeownership models may be increasingly recognised as a ‘false promise’: one that has enabled the ongoing commodification of housing, labour market deregulation and retrenchment of state welfare support (Arundel and Doling, 2017; Doling and Ronald, 2010). Indeed, housing markets in the contemporary era appear increasingly to function as a dimension of growing inequality and insecurity. The implications of rising housing inequalities are far-reaching, from macro-scale economic processes of inequality (Piketty, 2014) to neighbourhood-level socio-spatial dynamics (Hochstenbach and Arundel, 2019; Hochstenbach and Arundel, 2019; Lees et al., 2013). Where Ford, Burrows and Nettleton (2001) initially challenged the ideal of a stable ‘homeownership society’ as a virtuous congruence between secure employment, strong welfare provisions and widespread homeownership, the research presented here raises the spectre of an emerging toxic congruence of employment insecurity, diminished welfare support and restricted homeownership access. The empirical evidence demands a reassessment of the societal potential of marketised homeownership and an outcomes-based consideration of approaches towards economic redistribution and security that ensure an inclusion of those excluded from homeownership.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Australian Research Council under the grant number DP19010118.