Abstract

Fragmentation of ownership has long been a recognised constraint to UK city centre development, a complexity that is growing in significance as centres try to manage the decline in physical retailing and transform obsolete retail units. Yet, our understanding of the structure of ownership and how that might be facilitating or inhibiting urban change remains weak. In this paper, the objective is to address this gap by examining the structure and diversity of land ownership in five retailing centres - Edinburgh, Glasgow, Hull, Liverpool, and Nottingham – between 2000–2017 using original databases created by linking administrative and commercial property data sets. Overall, the analysis finds property ownership to be spatially complex with ownership richness and diversity generally rising over the study period. The study also reveals that ownership structure has been shifting away from financial institutions towards overseas investors, private individuals and unlisted property companies, implying greater fragmentation of ownership. While the greater diversity in ownership should stimulate competition and innovation in property market practices, the shift in balance from equity-rich larger investors towards smaller and sometimes unknown investors makes urban centre management harder to manage. This suggests policymakers need to rethink the urban governance model to find a better way to galvanise the actions of this increasing disparate group of stakeholders if their visions of more resilient, mixed use city centres are to be realised.

Introduction

There is a growing body of literature documenting the struggles faced by retailers in town and city centres across the UK. The literature highlights online retailing as the cause of their distress, but operational costs are also contributing to rising vacancies, uncertainty and instability, a situation exacerbated since the start of the Covid-19 pandemic (CBRE, 2018; Mumford et al., 2021; ONS, 2021). The challenge these structural changes raise for urban centre management has focused attention on land use change and the creation of more diverse, vibrant places (for example, Carmona, 2021; Hubbard, 2017; Portas, 2011). Whilst this is not a particularly new response, it is one that has regained vigour in recognition of the growing surplus of retail space that needs to be repurposed (Grimsey, 2018; Savills, 2020).

At the centre of the ongoing struggle are landowners and investors, with serious ramifications arising from the crisis experienced by retailers. The interests and aspirations of these stakeholders are multiple and complex, may be complementary or in conflict, and are often misunderstood. Their actions and relationships, operating within regulatory, institutional, technological and social boundaries, underpin the adaptation of the built environment, but often in ways that are not recognised, understood or, importantly, explored. Their response to shocks, however, are often manifested in the physical form and heterogeneity of town and city centres, areas that are core to economic stability and growth but increasingly polarised in their fortunes.

For those centres that are experiencing significant decline, efforts to repurpose redundant retail space and recreate vibrant and attractive destinations depend on well-functioning property markets, and policies that adequately support necessary land use changes, and motivate developers and investors (Jackson and Watkins, 2005). The Levelling-Up and Regeneration Bill (2022) is one attempt to target landowners through proposed Compulsory Rental Auctions. Yet, understanding of landowners is limited, frequently distilled down into the generic groupings of ‘developer’ and ‘investor’, based on the preconception that property owners are all the same. Jackson and Watkins (2011) highlight, by reference to a case study presented in Campbell et al. (2009), the failure of policymakers to fully understand the motivations and behaviours of different landowners which frustrates their efforts to guide market processes. Furthermore, Urban Task Force (1999) identify complex land ownership patterns in urban centres as development constraints, and Adair et al. (1998) argue that multiple tenurial rights deter private investment in urban regeneration projects, while Adams et al. (2002a) specifically identify it as a primary barrier to retail development. Understanding of the workings of the commercial property market is further obscured by the lack of data on the ownership structure of urban retailing centres (Dixon, 2009). These information barriers to understanding are amplified by the London-centric focus of research (e.g. Lizieri et al., 2011), further exacerbating market imperfections.

Drawing on evidence from property stock databases in five northern UK city centres, this quantitative method study seeks to contribute to the bridging of this knowledge gap by answering two questions: (1) how has the structure of ownership evolved? (2) what are the consequences of these changes for the management and adaptation of city centres? The theoretical underpinnings are rooted in complex systems theory, which adopts an evolutionary perspective to study how stakeholders are responding to the structural changes experienced by retailers through innovation, re-organisation and adaptation.

The study is novel in that the first stage of the analysis links diverse administrative and commercial datasets in a manner not previously undertaken, to enable investigation into the heterogeneity of ownership. The second stage of the analysis maps diversity metrics, developed using the databases developed in stage 1, to examine spatial changes in ownership. Diversity indices have been employed previously to examine land use (for example, Ritsema van Eck and Koomen (2008); Velázquez et al. (2018)) but not ownership patterns. The exploratory methods developed should inform international research agendas into urban ownership, while the choice of case studies seeks to contribute to the UK levelling-up debate by identifying potential barriers that imped the creation and management of more resilient urban retailing centres.

The paper is organised into five further sections. The next section examines adaptive capacity and sets out the key role played by the retail property market in resilience, forming the conceptual framework for the study. The third section begins with a brief review of land and property ownership, to inform the later empirical decisions. It then introduces some motivations of owners investing in retail property and broad ownership patterns. The research methods are detailed in the fourth section of the paper. In particular, it provides information on the data linking processes employed and the creation of diversity metrics. In the second last section, the focus is on the empirical results, while the final section of the paper sets out the conclusions and examines the implications for city centre management and adaptation.

Resilience in urban retailing centres

Retail markets are spatial economic systems, consisting of organisations, institutions, and individuals, that can reorganise their form and function to adapt to external and internal destabilising shocks. Wrigley and Dolega (2011) conceptualise urban retailing centres as dynamic systems that exhibit ‘adaptive resilience’ (Martin, 2012), as they evolve, grow and adapt in a continuous process of anticipatory or reactive change and are unlikely to ever be in an equilibrium state. Innovation and urban development are products of these shocks, as multiple organisations, institutions and individuals, whether occupiers, landowners and other stakeholders, adapt alongside each other to endogenous and exogenous disruptions, resulting in unpredictable system effects and variation.

The property market provides the fundamental context for retailing system changes, and can be defined as interconnected sub-systems of mechanisms and stakeholders that create, transfer, manage, finance, use and adapt the built environment. An adaptive cycle can be seen, as demand and supply fluctuations, which Barras (1994) associated with short-term, property production and longer urban development cycles, affect the system. Rising demand from reorganising and growing occupiers characterises periods of ‘growth’ and high resilience in the cycle (Dolega and Celinska-Janowicz, 2015). In turn, this triggers increasing investment returns and development viability, attracting investors and developers. Investment in the form of new retail development, and the refurbishment and adjustment of existing space takes place. Eventually growth in the local economy and property values slow, and the system enters a ‘consolidation’ phase with occupiers and owners less responsiveness to change, and the resilience of the system starts to drop (Dolega and Celinska-Janowicz, 2015).

The system remains in this slow but stable growth phase until a severe external shock triggers the demise of unproductive and dated retailers and other organisations, the ‘release’ phase of the cycle. The closure and/or relocation of occupiers and rise in vacancy rates, result in a surge in uncertainty as the centre’s vitality diminishes, causing development activity to halt (Dixon and Marston, 2002).

Emerging from the disruption and instability are new brands, organisations, land uses and opportunities as innovation and creativity are reinvigorated. These processes give rise to new occupiers, properties changing use, and the creation of new retailing forms as the retailing centre enters a ‘reorientation’ phase. Innovations, possibly nurtured by public-sector support for recovery, draw footfall which stimulates growth, further innovation and development activity as the centre re-enters a phase of growth and urban renewal. The timing and duration of each phase of the adaptive cycle is centre-specific and, perhaps more importantly, spatially uneven within a centre (Dolega and Celińska-Janowicz, 2015; Orr et al., 2021; Wrigley and Dolega, 2011).

This concept of adaptive resilience, at least in part, complements evolutionary theory, which is concerned with processes, diversity, connections, variety, interactions, knowledge, institutions, and capabilities. However, the evolutionary economics perspective sees transformational change in a complex system primarily as a product of evolution (Dopfer et al., 2004), rather than the ‘reactive anticipatory’ or ‘rational intent’ that underpins the adaptive processes in urban centres. Furthermore, while evolutionary mechanisms, such as selection, variation, replication and self-organisation are important, offering some explanation of internal adaptation mechanisms, Dolega and Celińska-Janowicz (2015), highlight gaps in understanding of the internal mechanisms that determine the capacity of retailing centres to change.

Illustrating the evolutionary mechanisms, selection is evident when disruptions occur, usually triggering the release phase, and landlords who cannot adjust to the contraction in occupation demand may leave the market, or have their assets repossessed as banks foreclose on distressed loans, while occupiers who fail to adapt to the change in competitive pressures do not survive. The context to the current study is that through the structural changes, retailer distress and consequent vacancies, there is increasing pressure for land use change. This suggests that markets are on the cusp of the shift from the release phase to the reorientation phase, with demand for multi-functionality and greater variation in retail centres. Innovation is a driver of this greater variation and examples include the development of new retail configurations (Hughes and Jackson, 2015; Jones and Livingstone, 2017), such as drive-thru coffee shops, competitive socialising leisure activities as new forms of land use, and the rise of ‘experience’ retailing (Carmona, 2021). Such innovations can trigger replication within those parts of the retailing and leisure sectors able to respond quickly and with dynamism. Turning to self-organisation, while Guy (1999) identifies vacancies as a symptom of decline, Findlay and Sparks (2010) argue that they are essential in the self-organisation process and enable retailers and service providers to adjust store formats and relocate in response to shifting consumer tastes and demand.

Moving through the reorientation phase, and increasing the resilience of city centres, is about more than rebalancing the retailer/service provider, it is about changing to alternative uses. Responding to Dolega and Celińska-Janowicz (2015), it is here that greater understanding is needed of the pivotal role played by owners in the internal mechanisms that determine the capacity of retailing centres to change. Architecture, building formats and condition and unit sizes are all factors influenced by land and property owners, alongside walkability, street layout and public realm space, that create connectivity and sense of place. This (re)organisation of form and function underpin adaptive capacity and resilience.

Ownership within the retailing system

Classifying ownership

Surprisingly, little is understood about the nature and behaviour of land and property owners in towns and city centres, largely due to a historic lack of data that shrouds the subject in a veil of secrecy (Dixon, 2009). When urban landownership is discussed in the literature, it is usually from the perspective of the development process and the barrier that land assembly presents as UK settlements “are notorious for their patchwork of existing ownerships” (Adams et al., 2002a, p. 144).

Landownership can generally be divided into private- and public-sectors (Adams et al., 2002b). Kivell (1993) starts from this position but then, using a classification that originates in Massey and Catalano (1978), divides private landownership into former “landed” ownership where land and buildings are held by the Church, Crown Estate and other landed aristocracy; industrial land ownership which is held for occupation by businesses; and financial land ownership held by investors for a range of purposes. McNamara (1983) divides the different forms of financial ownership into four broad groupings, based on their business model:

Engagement with the development process is central to the distinctions made by McNamara (1983) but many owners are not motivated by the profitability of development activities. An alternative classification, by organisation type, is adopted by Lizieri et al. (2011) in their examination of the ownership structure of the City of London office market, as well as by organisations such as CoStar and the Investment Property Forum (IPF) (see, for example, Key et al., 2018). While there are slight differences in the taxonomy they use, they tend to split property investors into financial institutions, unlisted/collective specialist real estate funds, property companies, individual private investors, traditional owners (Kivell’s ‘landed’ owners), and ‘other’ which includes public-sector owners and owner-occupiers.

This brief review reveals the complexities of ‘ownership’, illustrating historical characteristics that are still evident, different operational models and types. Overall, it is clear that, in order to explore ownership, a classification is needed, but one which is balanced between enabling meaningful, yet manageable analysis.

Owners as investors

Traditionally, investment in city centre retail property was seen as attractive, providing a secure and stable cashflow. Jackson and Watkins (2005) in the UK and Newell and Hsu (2006) in Australia explain that restrictive planning policies historically protected city centre investment properties from competition, providing investors with good returns and relatively low risk as income voids were rare Jones, (2010). Furthermore, the location of prime shops shielded assets from physical obsolescence inherent in other property types, while Jones (2010) sets out that tenants accepted repair liabilities to control their brand, together providing owners with a passive investment vehicle.

Planning policy purposively sought to maximize the attractiveness of town centres to institutional investors because their cash-rich nature enhanced the vitality and viability of town centres Jackson, (2006). Furthermore, local authorities were previously encouraged by central government policy to assemble sites for developers to overcome the obstacle of fragmented ownership and encourage new investment. This, and high investment returns, saw retail used as a regeneration tool in the 1990s and 2000s with many major UK financial institutions targeting prime in-town assets either as developer/investors or acquiring assets from developer/traders (McGreal and Kupke, 2014).

However, the threat of economic obsolescence for units outside the prime pitch due to shifting pedestrian flows (Hughes and Jones, 2015) and the shift in planning policy from 1996 to allow decentralisation of provision increased investment risk. The number of standard High Street shop units held by risk averse financial institutions fell by more than half between 1995 and 2006, while their out-of-town retail warehousing portfolio weighting rose from 17% to 37% (Jones, 2010). Byrne and Lee (2009) identified 2000 to 2003 as the period of the greatest net disinvestment by institutions when they reduced their holdings in standard shops, department stores, supermarkets and minor shopping developments.

Patterns of ownership are available at an aggregate level. Exploring the estimated £509 billion of non-domestic UK investment stock, while UK financial institutions (specifically insurance and pension funds) historically dominated, they have been replaced by overseas investors, estimated to hold 29.9% of commercial property, typically biased towards offices in London and the south-east of England (Key and Law, 2005; Key et al., 2018). Consequent diversity of ownership of UK property is clear, with UK financial institutions estimated as holding 17%, unlisted & collective schemes 16.3%, listed companies and REITs 14.3%; private companies 11.4% and private investors 2.8%. These smaller investors are more likely to hold small lot sizes (Byrne and Lee, 2009). Importantly, understanding of these ownership changes tends to be limited to the aggregated level. The sparsity of academic studies into ownership within towns and cities means the fine grain operation of the property market remains opaque, with little known about how ownership impacts on the retailing market and its adaptability. Rare exceptions to this are Child (2019), who examines shop ownership at a single snapshot in time on 22 UK High Streets and, in the office sector, Lizieri et al. (2011) who trace office ownership in the City of London. This study seeks to address this clear gap by examining the changing temporal and spatial structure of ownership in five regional urban retailing centres over the last two decades.

Data and research methods

The research approach

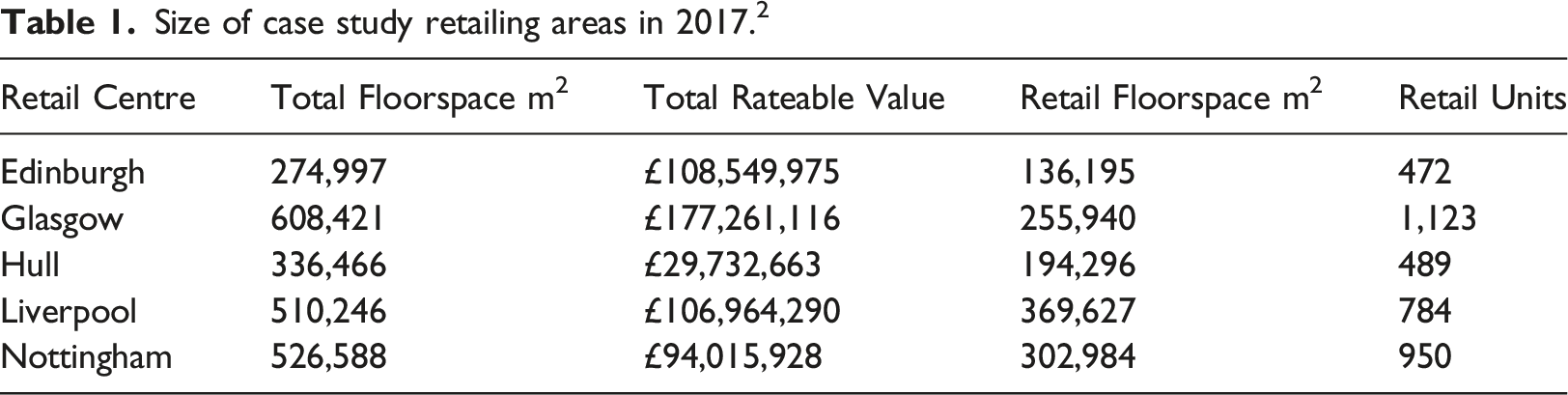

This study forms part of a larger mixed methods project designed to explore the adaptability of UK city centres, through five ‘northern’ case studies: Edinburgh, Glasgow, Hull, Liverpool and Nottingham. Typically cities, despite their economic and cultural importance, have been neglected in the ongoing High Street debate, with attention focused on town centres. This study uses quantitative methods to investigate changes in the structure and diversity of property ownership over a period of almost two decades, 2000–2017. The purpose is to look at how ownership within the core retailing area has changed, and explore the consequences on the management and adaptation of city centres. Focusing on the core retailing areas 1 within these large cities reflects the pre-dominant focus of private-sector ownership and investor activity, while the sample provides insights into retailing centre resilience from a northern perspective.

Size of case study retailing areas in 2017. 2

Developing ownership databases

Ownership and land use data are collected for all the properties within the study areas, effectively linking a number of existing disparate administrative and commercial datasets. This provides a new temporal and spatial stock database for each centre. Details of the existing datasets and the exhaustive steps taken to link them are set out in the Supplementary File.

Classifying property ownership

Drawing on the review of existing classifications above in section 3, it is clear that a balance is needed between manageability and meaningfulness for the stock databases created here. The data must also exist, and specific operational business models are often not stated. Thus, the system selected is a modified version of that used by PropertyData.Com, based on type of investor and is shown in Supplemental Table 1. The main difference is that the sub-types do not differentiate individual financial institutions as this level of detail is not needed here and would hinder meaningful analysis. The identified owner is the holder of the title with “economic use” of the property rights. In Scotland this is typically the heritable interest holder. In England it is the freeholder, unless a long leasehold exists, which is then recorded as the owner. 3 This classification system is similar to that used by CoStar, Lizieri et al. (2011) and Key and Law (2005) although unlisted collective vehicles and UK institutional investors, and traditional and private investors are grouped together as separation is not always possible.

Measuring ownership patterns and diversity

Ownership patterns tend to be represented by the percentage of properties held by different types of owners within an area. Sometimes this percentage holding is based on the area of land held, or the value of properties, or number of properties within each category. Key and Law (2005) for example, base their estimates of the total value of investable commercial property in the UK on investor type, although the values rest on aggregated estimates derived from Office for National Statistics (ONS) and National Accounts, and values from VOA records and Real Capital Analytics transaction database (similar data providers to CoStar and PropertyData), with no way to validate the figures employed.

Ownership can be further analysed using richness and diversity metrics. Ownership richness (R) is simply the total number of different ownership categories within a study area. This can be extended to take into account their relative abundance using the Gini-Simpson Index of Diversity (Jost, 2006). If the Gini-Simpson Index (GSI) is adapted to measure ownership in a retailing system, it can be measured as:

To apply ownership Richness and the GSI diversity measure to the new databases, the entries are imported into ArcGIS, along with those in a buffer zone. 4 The indices are initially calculated at the aggregated (PSA/PRA) level, and then disaggregated to a micro-level. A 100 m by 100 m fishnet grid is created, spanning the study area and buffer zone in each city, with every individual property unit assigned to a square cell within the grid. 5 This technique, also used by Greenhalgh et al. (2020) to examine property floorspace and value changes in York, typically divides the areas into around 50–75 cells, or part cells. Count analyses are used to count the presence of different categories of known owners (allowing for main and sub-type groupings but ignoring units where ownership could not be confirmed) within each grid cell which, in turn, are converted into diversity indices for each cell as well as for the overall study area.

Ownership analysis

Using the newly created database for each of the five study areas, and the indices of ownership and diversity, the following sections set out temporal and spatial characteristics and changes in ownership. This, then, provides for new insights into the adaptive capacity of retailing centres and how they may be enabled, or frustrated, to move into and through reorientation and thus increasing resilience, as set out in the final section.

Ownership structure in the case study areas

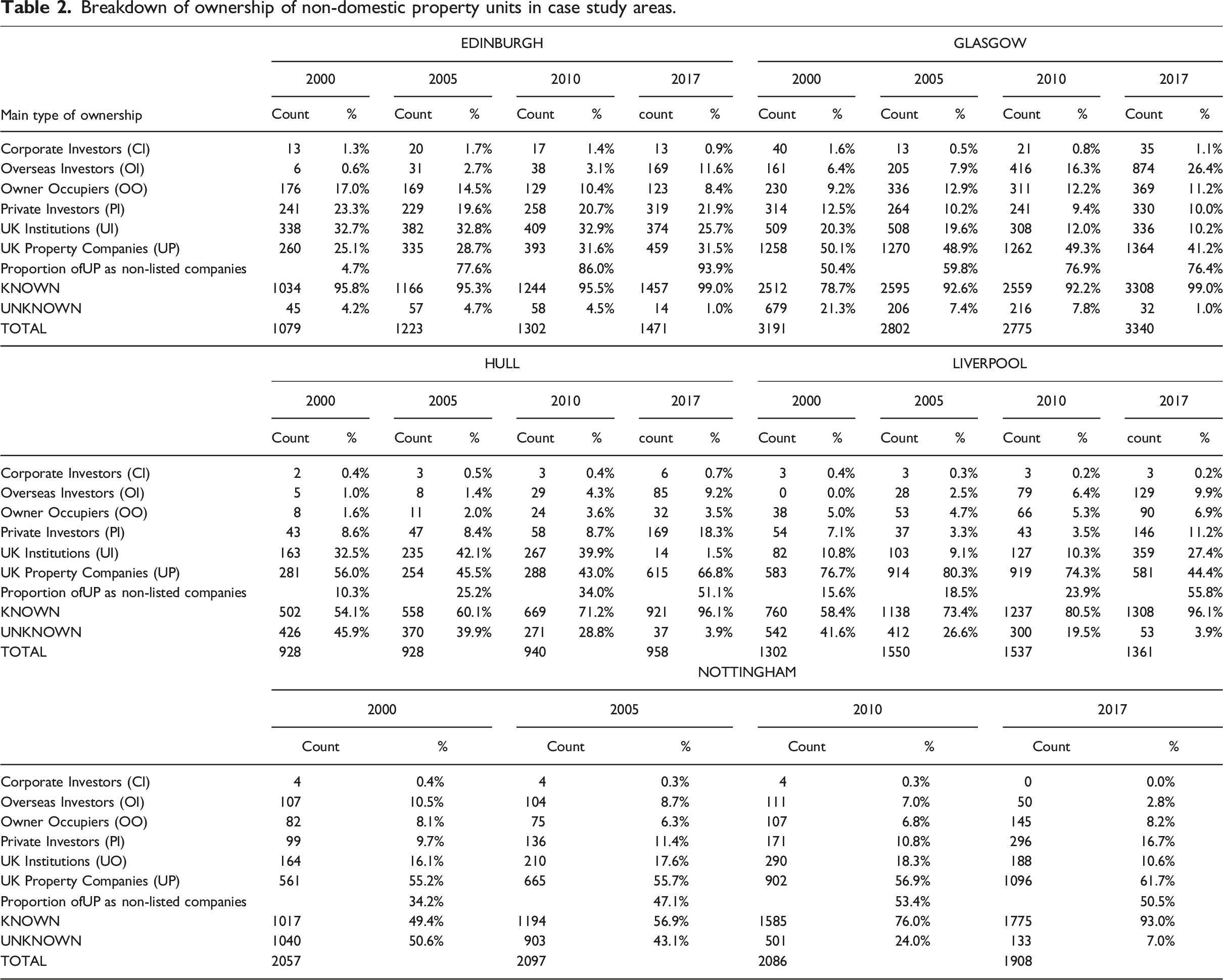

Breakdown of ownership of non-domestic property units in case study areas.

Listed and unlisted UK property companies (UP) stand out as the dominant retail and commercial property owners in all retailing centres, across the whole study period, for all centres other than Edinburgh. In Edinburgh, UK financial institutional investors (UI) held the greatest proportion of commercial stock up to 2010, perhaps reflecting its status as a capital city. However, this then fell in favour of overseas investors (OI), which increased ownership almost four-fold over 2010–17, allowing listed and unlisted UK property companies (UP) to become the dominant owner by 2017. Mirroring Edinburgh, in Glasgow there has been a large increase in overseas investors, over four-fold in the period 2000–17. Child (2019), one of the few studies to examine the ownership of retail units on the High Street, presents similar results in his study of 22 UK cities. He found overseas investors dominate the retail market in Edinburgh (24.24%), but their preference for retail is revealed, as here they have a lower presence of 11.6% across all non-domestic properties in 2017. This trend provides additional detail to the findings of Key et al.’s (2018) IPF study which, while revealing the increase in overseas investors to become dominant at the UK level, found that the holdings tend to be concentrated in offices in the south-east of England. Increases in overseas investors, are also shown in Hull and Liverpool, albeit less marked. These overseas investors can be a consortium, high net worth individuals, sovereign funds and offshore companies and vehicles. However, this group of investors appears to have shrunk in Nottingham.

Other marked ownership patterns revealed in Table 2 include that UK institutions had a large presence in Hull – 42.1% of known investors in 2005 – but this had plummeted to 1.5% by 2017. This is also revealed in the MSCI index of institutional ownership (MSCI, 2021). Ownership by UK financial institutions also contracted in Nottingham between 2010 and 2017, albeit from a lower starting point, with only Liverpool experiencing a rise in institutional ownership. Jackson (2006) previously highlighted that investment in the High Street and town centres in general is dominated by institutional investors and, therefore, she argued that this form of investment is a vital factor in the sustainability and vitality of town centres and high streets. The findings in Table 2 suggest that their influence is decreasing, confirming the findings of Key et al. (2018). Instead, as highlighted above, listed property companies now tend to be dominant owners, with multiple holdings, including shopping malls. Subsequently, they are able to influence and effectively manage tenant mix and are better placed “to deliver a point of difference that will attract the ever more discerning customer” (Knight Frank, 2017, p. 5) but on the whole there has been an increase in smaller, typically local or regional, unlisted property company holdings (shown as a percentage of UK property companies in Table 2).

The cyclical nature of the commercial property market offers some explanation for the withdrawal of UK financial institutions. Investment total returns post-Global Financial Crisis (GFC) for standard retail in the case study centres, while historically volatile, are systematically lower than in previous cycles (revealed in MSCI, 2021). The negative returns for 2008 and 2009 recorded in the MSCI index also marked the start of high profile national retailers failing (such as Woolworths in 2008). Dixon and Marston (2002) predicted the impact of online retailing on physical retailer margins and fall in demand for retail space, although they did not foresee the compounding effects of rising operational costs, such as business rates and labour costs. Financial institutions tend to be risk averse, so the lower yet volatile returns, accompanied by rising business failures, and retailers and leisure operators using Company Voluntary Arrangements (CVAs), explain, at least in part, their dis-investment from the sector. Regarding the converse rise in property company ownership, Collet et al. (2003) argue that the increasing need to actively manage retail units, particularly in weak markets, might explain the increasing attraction to property companies that tend to be more opportunistic in their investment behaviour.

Private Investors (PI) is a group of owners that can be difficult to track and unpick. While there are notable proportions shown in Table 2, this difficulty means that it is likely that they also make up a good proportion of the ‘unknown’ category. Private investors are associated with more fragmented ownership as they tend to hold smaller property lots, and also tend to have different risk and return objectives. Spatial and temporal patterns are almost impossible to chart, as data on specific owners are often not publicly available. These difficulties and characteristics are important as ownership by this group is significant, as shown in Table 2, peaking in 2017 for Edinburgh (21.9%), Hull (18.3%) and Nottingham (16.7%).

Diversity of ownership

Changing non-domestic ownership richness and diversity in case study areas.

The figures in Table 3 reveal that richness is higher in the Scottish cities of Edinburgh and Glasgow in all periods. It also rose overall from 2000 to 2017 in all cities, except Nottingham, with consistent growth in Glasgow and Liverpool, and variation in Edinburgh and Hull. In terms of diversity of ownership as revealed through the GSI, at an aggregate level most cities saw diversity fall, then rise again, during the study period, although the timing varies a little. Nottingham and Liverpool perhaps appear a little distinct from other cities, with the number of different types of owners (richness) towards the lower range of the sample, yet diversity is generally highest in Nottingham while lowest in Liverpool and consistently increasing over the study period.

As highlighted in the review of the literature, the timing and duration of each new phase of the adaptive cycle is spatially uneven within a centre (Dolega and Celińska-Janowicz, 2015; Orr et al., 2021). It is important, therefore, to explore these metrics at a micro-level. Mapping has been undertaken and is available for each measure, for each city, for each period (See Supplemental Figures S1–S10). These reveal that both ownership richness and diversity are spatial uneven in each city centre in each time period. The maps show that richness in ownership in all five cities increased between 2000 and 2017. Ownership diversity in Liverpool, Nottingham and Hull also appears to have increased over the period but is more complex in Edinburgh and Glasgow. In Edinburgh diversity dipped in 2010 whereas in Glasgow it has fallen since 2005.

Typically the primary retail frontages (depicted by the dotted lines in Supplemental Figures S1, S3, S5, S7 and S9) display higher ownership richness (6 or more different types of owners within a 100m by 100m block) and diversity (a GIS index of above 0.600) although, unsurprisingly, this tends to be lowest where shopping malls are located. Orr and Stewart (2022) employ these ownership metrics in panel rent models and confirm the statistically positive relationship between rents and ownership richness. Thus, areas of the retailing centre with clusters of ownership types, such as exists for shopping malls, tend to command higher rents. By contrast, they find a negative relationship between ownership diversity and rents in 2005, 2010 and 2017, implying that greater evenness in the spread of ownership types results in lower values.

Discussion and conclusions

The context for this study is the ongoing challenge faced by the UK’s northern city centres. To achieve the widespread aspiration of the creation of more diverse, vibrant places, many commentators have set out that land use change, and the repurposing of property, is needed. These examples of innovation and change are key to increasing the resilience of centres during the reorientation phase of the adaptive cycle. It is argued that, to effectively facilitate such a change, key stakeholders with a role in managing urban centres must be able to have a fuller understanding of ownership within urban retailing centres, given the pivotal importance of ownership in change. Exploring these issues has been the focus of the discussion and the large-scale datasets developed open the door to improving understanding of city centre ownership. Here the discussion answers the question of how the structure of ownership has changed and, crucially, this then leads onto the second question by reflecting on the consequences for the management and adaptation of city centres.

The key change is that there has been a rise in ownership diversity in most of the case study areas. This reflects the steady decrease in institutional ownership, and a rise in ownership by overseas investors, smaller unlisted property companies and private owners. These findings align with the contraction of institutional property ownership identified by Key et al. (2018) at the national level. Liverpool is the only city where institutional ownership increased but this seems to have been due to a rise in investment confidence following the city being European Capital of Culture in 2008. The increase in the number of types of owners means that ownership has become more fragmented.

While greater variety in ownership may increase competition which can lower markets rents and benefit occupiers, fragmentation of ownership has been a long-standing issue in the redevelopment of city centres. The richness and diversity metrics show fragmentation has increased unevenly and, importantly, is especially marked in the traditional retail frontages. This heightens the barrier to the repurposing of the ‘High Street’. Higher ownership diversity does not seem to inhibit land use diversity (Orr et al., 2021), but where these are smaller private individual investors and small property companies, they are more likely to rely on debt to fund their activities than financial institutions, and so are unlikely to always have the resources to do more than adopt a passive approach to managing their assets, the traditional attraction of such property. Their management activities are also subject to the strict requirements of lenders, who have been increasingly restricting retail investment lending. The withdrawal of institutional investment capital in northern retailing centres could impede the outcome of future levelling-up initiatives.

Furthermore, fragmented ownership represents a barrier to the co-ordinated management and overarching stewardship of town and city centres. Unlike shopping malls, which are tightly controlled environments usually in single ownership, multiple ownership prevents control of the tenant mix to ensure tenants benefit from neighbouring land uses and many owners do not have the scale and flexibility to transform vacant space into different sized units or new uses (Carter, 2009). Existing city centre retail associations, Business Improvement Districts (BIDs) and other urban partnership initiatives tend to focus on pulling together large stakeholders, such as the recently created City Centre Partnership in Nottingham, but the findings suggest the growing significance of smaller-scale investors is not reflected in such city centre management strategies.

This should be of concern to planners and for town centre management policy. Change and the stewardship of such change need to be enabled. At the very least, every city centre should have an up-to-date master plan to create a shared vision and guide High Street change. The Use Classes Order 2020 in England, which was revised to promote flexibility within the High Street by permitting more types of use change without the need for planning permission, has the potential to create unintended spatial impacts on established uses. For instance, individual permitted changes of use that, collectively, negatively impact on the overall experience of the shopper, or tourist, or uses that create dead frontages which dissect the flow of a street would reduce the vibrancy of an area. A master plan would help deal with these changes and minimise negative spatial externalities.

Urban governance is another central issue. In the UK the BID model has been used to effectively promote and manage defined urban areas, provide general public realm improvements, and deliver services of benefit to occupiers. Following the recommendation in the Portas Review (2011), Property Owner BIDs, where property owners are charged a levy to have services provided for their benefit, were introduced in London but has not been extended to other areas of the country. 7 This is needed for a more long term strategic approach to place-making as the remit of the original BID arrangement tends to be occupier focused. More recently the BID model has been extended in Scotland into Community Investment Districts with the purpose of facilitating community participation in the transformation of neighbourhood centres. This pilot initiative might provide the opportunity to engage small landowners but as yet remains unproven.

Property owner associations, common in the US, are known to be effective in managing the multiple ownership of residential and commercial developments or communities. Mandatory city centre property owner associations may offer an alternative mechanism that specifically helps support and co-ordinate owners in the proactive management of their assets. The remit of an association would be dictated by its governing documents that are tailored to the challenges faced by a particular area. This might include a defined role in shaping the policy framework during the master-planning for the centre, the monitoring of the impact of land use changes and providing both a voice and a stimulus for all owners in the delivery of a local vision.

The aim of this study has been to unravel the changing structure of ownership and explore the consequences of these changes on the management and adaptation of city centres. The findings suggest that greater fragmentation of ownership and, indeed, increase in smaller-scale owners, are inter-linked with the release and reorientation phases of the adaptive cycle, and goes some way to address the gap in understanding the internal mechanisms pertaining to ownership. This is important as they determine the capacity of retailing centres to change.

The study also highlighted the complexity of the evolutionary mechanisms in adaptation. On one hand, these changes make city centre management harder and the discussion has stressed the importance of better understanding and integrating diverse property owners into the place-making process. On the other hand, the rise in ownership heterogeneity facilitates successful innovation and replication within city centres. These are essential elements of the reorientation phase, necessary to increase the resilience of core city areas (Dolega and Celińska-Janowicz, 2015), and additional study by Orr et al. (2021) reveal that the rise in ownership variety has been accompanied by property use innovation and an increase in use heterogeneity. French et al. (2021) and Orr et al. (2022) found that this has occurred in parallel with greater flexibility and innovation in the leasing process.

The connections between type of ownership and capital-intensive forms of innovation, such as new and flexible building forms, remain unexplored in this study and is an area for further research into the mechanisms within the adaptive cycle. Additionally, the new property use, ownership and value datasets developed represent an opportunity for further analysis. For example, they could be linked using the fishnet grid technique to housing developments to examine the practicality of 20 min neighbourhoods or to footfall and environmental quality data to examine the impact of public realm improvements and other public-sector interventions on the evolution of retailing centres.

Supplemental Material

Supplemental Material - Ownership diversity and fragmentation: A barrier to urban centre resilience

Supplemental Material for Ownership diversity and fragmentation: A barrier to urban centre resilience by Allison M Orr, Joanna L Stewart, Cath Jackson, and James T White in Environment and Planning B: Urban Analytics and City Science

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Economic and Social Research Council [grant number ES/R005117/1].

Supplemental material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.