Abstract

Continued greenhouse gas emissions will lead to a rise in temperatures, accompanied by rising sea levels threatening low-lying coastal cities. This vulnerability is especially acute in developing countries’ cities. This study reviews whether Bangkok, Manila, and Jakarta, less prepared emerging urban centers of developing countries, are investing in adaptation projects for resilience against sea-level rise and urban flooding. Sea-level rise and urban flooding resilience projects were identified in the selected cities through secondary research methods, data on multilateral climate funds, and other aggregated funding databases such as Aid Atlas, Cities Adaptation Action, and City Risk Index. Our findings show that even though these cities do have some adaptation projects to address coastal flooding and rising sea-level threats, the funding has been disparate and dispersed due to a lack of continuous, sizeable, and diverse financing options and does not come close to the requirement, given the risks, of covering potential disaster-related losses. Our findings further highlight the need to expand financing beyond multilateral funds and bilateral funding agreements and to include financial mechanisms that incentivize potential stakeholders to invest in projects that ordinarily are considered nonrevenue generating.

Introduction

Climate change is happening faster than previously estimated. While in 2009, only five of 16 Earth system’s climatic tipping points were active, by 2019, that had increased to nine (Lenton et al., 2008, 2019). Bamber et al. (2019) estimated that if carbon dioxide levels follow current trends, the future average sea level could increase by two meters until 2100. Approximately 300 million people are at risk of being severely affected by coastal flooding caused by sea-level rise (Kulp and Strauss, 2019). As the average temperature rises alongside the average sea level, this will create fertile ground for more devastating storms and increasing rainfall rates. The effects of sea-level rise and urban flooding-related destruction will severely impact already vulnerable populations that do not have the economic capabilities to recover.

Cities are at the center of modern economic growth. Urban centers generate 80% of global gross domestic product (GDP) and consume above 70% of all energy produced on the planet (C40 Cities Climate Leadership Group, 2016). The United Nations predicts that by 2050, 68% of the global population will live in cities, primarily concentrated in Asia and Africa (United Nations, 2018) with East Asia Summit countries city dwellers projected to grow from 500 million to 900 million between now and 2030. Given that nearly 75% of cities are located in coastal areas directly exposed to the risk of any future increase in the sea level (C40 Cities Climate Leadership Group, Siemens and Citi, 2016), they are at the forefront of climate changes negative consequences. McGranahan et al. (2007) suggest that larger urban settlements are more concentrated in low-elevation coastal zones and that around 65% of cities with populations greater than five million are located in these zones. Hallegatte et al. (2013) studied future flood losses in the 136 largest coastal cities across the world and estimated that average global flood losses would increase from US$6 billion in 2005 to US$52 billion in 2050. A recent report by the Global Commission on Adaptation and World Resources Institute (2019) stated that temperature above 2°C could cause annual urban flood damage losses of US$11.7 trillion.

Rising seas and cities in Southeast Asia

With sea-level rise, many Association of Southeast Asian Nations (ASEAN) cities are already sinking. As coastal cities, Bangkok, Jakarta, and Manila face the risk of sinking and rising sea levels. The sinking is mostly driven by the sheer weight of the built-up urbanization and uncontrolled groundwater extraction. Simultaneously, climate change is increasing sea level, and storms (e.g., typhoons and monsoons) are becoming more assertive. The 2007 Jakarta flood resulted in the flooding of 70,000 homes and displaced 500,000 people costing US$400 million in damages. As a response to this unfortunate event, Indonesian and Dutch governments joined forces to develop and execute the National Capital Integrated Coastal Development master plan, relying on Dutch expertise and knowledge to help Indonesians save Jakarta from urban flooding and sea-level rise. The massive Giant Sea Wall Jakarta (US$40 billion) coastal development project consists of networks of artificial islands and dykes carrying an airport, harbor, toll road, residential area, industrial area, and parks (Sherwell, 2016). The project will be jointly financed by the national government, local government, and private investors.

In 2009, Tropical Storm Ondoy caused US$1 billion in damages across the Philippines, mostly affecting Manila (Yarina, 2018). The Philippines soon intensified their cooperation with multilateral organizations to obtain financing and develop solutions to prevent future calamities. The Metro Manila Flood Management Master Plan, approved in 2012, aims to mitigate this risk through physical strategies such as dams, dikes, canal-dredging, new pumping stations, and the resettlement of slums which block waterways. The World Bank and Asian Infrastructure Investment Bank have provided expertise and financial help to implement the city’s master plan. In the case of Manila, multilateral institutions provided sovereign loans that will cover US$415 million of the total US$500 million cost (World Bank Group, 2017a). The government of the Philippines will provide the remaining amount.

Bangkok experienced devastating floods in 2011, costing billions of dollars, which led the government to develop plans to harden defensive infrastructures in industrial areas to discourage investors from fleeing the country (Yarina, 2018). Since the city occupies a flood plain, rapid urbanization exacerbated the flood risk. The government decided to invest domestic budgetary funds in the Chao Phraya for All project -- a system of pumps and 57 kilometers (km) of floodwall upon an already existing 80 km of floodwalls on the Chao Phraya’s riverbank (Reed, 2019).

In all three cities, donors and politicians like to fund technical solutions that can be achieved quickly or at the very least with a high degree of visibility, as they are looking at ways to showcase achievements under their administrations. Additionally, many of the proposed projects in ASEAN’s megacities (e.g., dams, walls, and pumps) have been successfully implemented in developed countries (e.g., the Netherlands and Japan). The added benefit of replicating developed countries’ projects lies in demonstrating the rapid development of a developed country even when it is unrepresentative of its overall development. Also, donors who help countries develop these projects see the idea of exporting expensive anti-flooding large-scale solutions as a reliable business opportunity (Yarina, 2018).

Nevertheless, it is essential to mention that urban mitigation rather than urban adaptation dominates the political economy of strategic planning, project selection, and the size of funding (Macomber, 2011). This fact is due to the ease with which public, private, and even multilateral investors can measure the effectiveness of mitigation investments, usually by looking at cost per ton of abated greenhouse gas emissions. Adaptation climate finance remains an unclear investment choice because costs potentially remain with the investor, whereas benefits are often public (Pauw, 2015). Furthermore, benefits from adaptation projects might not always be easy to quantify and do not become apparent in the short term. Therefore, the return rate on climate adaptation can pose market barriers for investors, whether private, public, or multilateral. For example, investment from multilateral development banks focused around 20% of finance on adaptation while mitigation comprised the remaining 80%; similarly, only about 25% of public funds flowing from developed to developing countries are for adaptation funding (Yeo, 2016).

Building and investing in urban adaptation infrastructure will be crucial for megacities to better prepare for the future increase in global sea levels. The capacity of megacities to build resilience, protect economic assets, and manage the impact of future sea-level rise will depend on their ability to achieve macroscale solutions for mobilizing investment in climate-resilient urban infrastructure by utilizing urban adaptation climate finance.

The challenge of financing urban resilience

In 2017, the Organisation for Economic Co-operation and Development (2017) estimated that US$600 billion infrastructure investment per year would be needed in the period 2016--2030 to meet climate goals outlined in the Paris Agreement. Bhattacharya et al. (2015) predicted that until 2030, around US$62 trillion of investments would be needed to finance exclusively urban low-emission and climate-resilient infrastructure. There has not been enough finance channeled to support sustainable development. The World Economic Forum (2013) estimated that the annual global climate finance gap, encompassing both mitigation and adaptation, surpassed US$500 billion.

Furthermore, mitigation finance dominates adaptation finance. On the global scale, mitigation climate finance flows are almost five times greater than adaptation funding (United Nations Framework Convention on Climate Change, 2018). In their examination of urban climate finance investments from 1994 to 2014 by five major multilateral climate funds across developing countries, Causevic and Selvakkumaran (2018) concluded that from an aggregate value of almost US$1.8 billion, 90% was invested in urban mitigation and only 10% to urban adaptation and resilience-building projects. Mitigation projects dominated the climate finance sphere because mitigation can be commoditized and traded on the local and global markets, while adaptation and resilience projects’ positive externalities cannot be easily monetized. To address climate change, humanity will need to provide support for adaptation and mitigation efforts simultaneously. Mitigation must limit the global average temperature increase, and adaptation must reduce cities’ vulnerability.

Aim of the study

Earlier studies by Hunt and Watkiss (2011) show that only a small number of cities, mainly in developed countries, have conducted quantitative estimates of the costs of climate change risks. Their work also suggests that such analyses are still in their early stages, especially at the policy level. In order to adapt to a world that is more susceptible to coastal and storm flooding, it is essential to understand how prominent cities in Southeast Asia are currently preparing to adapt to the inevitable threats of climate change. Therefore, this study’s central research question is: Are the leading coastal megacities in developing ASEAN countries investing in resilience against sea-level rise? The analysis also considered two supplementary questions: What type of investments is in focus and under what financing structures? Which adaptation climate finance mechanisms can ASEAN countries use to mobilize necessary sea-level rise-related urban climate finance? In particular, focusing on ASEAN’s megacities is of interest considering their economic potential, rapid urban infrastructure development, population growth, and vulnerability to natural disasters.

Methodology and scope

This research will focus on data and policy framework analysis of urban sea-level rise resilience initiatives among leading coastal megacities in ASEAN. This study is concerned with how the financing of climate-related impacts in an urban context is limited and how cities can promote adaptation plans and ways to finance adaptation efforts. It mainly investigates the linkages between the ASEAN cities’ adaptation and resilience actions and their financing to understand the broader trends and challenges.

To this effect, the analysis was conducted using secondary materials (i.e., academic and gray literature), internet searches’ findings, and examination of the data acquired from several the urban risk index and urban adaptation actions databases. The first step was to identify the leading coastal urban agglomerations in ASEAN. These were the cities that act as important focal points within a national context and global economic systems; parameters such as GDP share, population size, estimated future GDP increase, and political significance were considered. Cities such as Singapore were determined to have enough domestic financial resources to finance urban resilience; hence, they do not face aggressive population growth and urban climate finance gaps in the same magnitude as rapidly rising coastal megacities in developing countries (Chin, 2019). Cities such as Bangkok, Jakarta, and Manila are both the center of their respective countries’ political hierarchy and economic life while struggling with developing urban and climate resilience, unlike Singapore. Jakarta represents 23% of Indonesia’s, Bangkok 40% of Thailand’s, and Manila 42% of the Philippines’ GDPs (Lloyd’s, 2018). As a result, the research focused on urban resilience financing, emphasizing sea-level rise and urban flooding in these emerging ASEAN cities. 1

The second step utilized global forecasting analysis and quantitative data on population growth, information about increases in income and consumer spending, and GDP at risk due to sea-level rise metrics from Oxford Economics (2014), Cambridge Centre for Risk Studies (2015), and several leading multilateral climate funds (Climate Funds Update, 2019). Data from Brookings Institution (2018) and PriceWaterhouseCoopers (2016) were studied to acquire information on the most significant ASEAN metropolitan economies and high-performing metro areas with a focus on GDP per capita growth.

The third step followed this, a review of current literature about or produced by the identified cities concerning their plans to adapt and prepare for flood-related disasters. Additionally, online searches identified adaptation, mitigation, and their respective financing projects on the sub-national levels (e.g., state, municipality, and city) to gain insights on city- or state-financed projects. The authors interchangeably used several keywords searches (i.e., “city name,” “sea-level rise,” “urban flooding,” “storm flooding,” “adaptation,” “resilience,” “plan,” “project,” “finance”) in two separate phases. This step helped identify the type of sea-level rise urban resilience projects, and to identify distinctions between hard infrastructure and nature-based solutions (NBS) 2 . The first phase encompassed the English language keyword search on Google’s home and scholar pages. The second phase imitated the first phase’s methodological logic but performed the search in the country’s respective official languages in which selected cities are located (i.e., Bahasa Indonesian and Thai). In Manila’s case, the search was conducted only in English since it is one of the Philippines’ official languages. The second step expanded access to information available on the internet in multiple languages. The English language covered international information, and respective official national languages covered domestic climate finance and sea-level rise information flows.

The fourth step was to examine the Stockholm Environment Institute (SEI) Aid Atlas, Carbon Disclosure Project (CDP) Cities Adaptation Action, and Centre for Risk Studies (CRS) databases for urban sea-level rise and urban flooding project-linked climate finance. The research also examined project-specific databases from the Pilot Program for Climate Resilience (PPCR) and Special Climate Change Fund (SCCF), classified as significant multilateral climate funds, financing urban adaptation efforts. In the case of Aid Atlas, the research has examined all climate adaptation financial flows, focusing on identifying adaptation projects in the focus cities in 2002--2017. CDPs had the shortest time scale covering only 2017--2019, but it was taken into analysis due to its importance. CRS database analysis covered risk scenarios modeling 2015--2025. PPCR analyzed projects covering 2010--2018 and, in the case of SCCF, examined the 2006--2018 period.

The fifth step evaluated the results gathered in the two previous steps to inform an open discussion on sea-level rise adaptation projects’ financial mechanisms, risk to parties involved, and funding costs in three ASEAN megacities. Furthermore, the discussion scrutinizes how other coastal megacities in developing countries are mobilizing financial mechanisms to address sea-level rise. When evaluating adaptation financing, it is essential to acknowledge that there is no universally accepted definition for what qualifies as adaptation financing. Therefore, the CRS and CDP data have been analyzed considering the Climate Policy Initiative (CPI) categories. The CPI categories include Water and Wastewater Management, Agriculture/Resource/Land Use, Disaster Risk Management, Infrastructure/Built Environment, Policy/Budget/Capacity Building, Coastal Protection, and Industry/Extractive/Trade—listed in the largest share of projects to smallest.

Findings

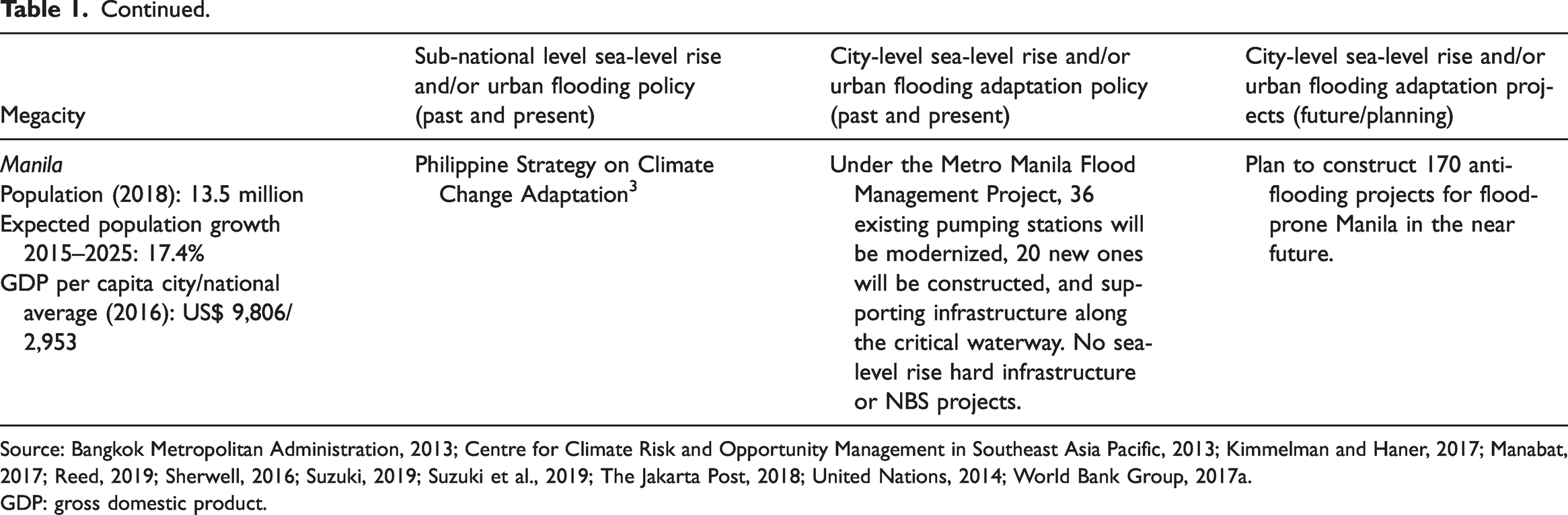

When it comes to planned projects on adaptation to sea-level rise, Jakarta was the leader. Jakarta already started building an estimated US$40 billion Giant Sea Wall Jakarta project, including the construction of a sea wall along the coast, building a water reservoir, and the reclamation of land (Kimmelman and Haner, 2017; Van Dijk, 2016). City planners in Bangkok are considering building a green belt barrier, super water levees, and an 88 km long watergate (Reed, 2019). Bangkok has a running project to build 14 km long Chao Phraya Promenade and urban resilience infrastructure to reduce flooding at an estimated cost of US$463 million (Rujivanarom, 2018).

Manila did not have any current projects or plans to build a sea-level rise defense (Manabat, 2017). Nonetheless, for years, the city has been working to build hard infrastructure and community preparedness to address storm-linked flood surges’ acute issues. The World Bank has been a crucial actor helping Manila to build urban flooding resilience (World Bank Group, 2017b). In 2017, the World Bank, alongside the Asian Development Bank (ADB) approved US$415 million for the Metro Manila Flood Management Project. This project aims to modernize drainage infrastructure, minimize the amount of solid waste in waterways, and execute the resettlement of selected poor communities severely affected by urban flooding (World Bank Group, 2017a). The plans for each of these cities are highlighted in Table 1.

Three ASEAN coastal megacities adaptation to sea-level rise and urban flooding policy documents and projects.

Source: Bangkok Metropolitan Administration, 2013; Centre for Climate Risk and Opportunity Management in Southeast Asia Pacific, 2013; Kimmelman and Haner, 2017; Manabat, 2017; Reed, 2019; Sherwell, 2016; Suzuki, 2019; Suzuki et al., 2019; The Jakarta Post, 2018; United Nations, 2014; World Bank Group, 2017a.

GDP: gross domestic product.

City-level adaptation preparation across evaluated databases is limited. The CPI, which tracks the flows of mitigation and adaptation finance on a global basis, estimated that in the 2017--2019 evaluation period there was a global total of US$579 billion dedicated to climate financing. Of this total amount, the East Asia and Pacific region served as an action point in attracting both public and private financing, totaling in the amount of US$238 billion (Climate Policy Initiative, 2018). The Climate Policy Initiative (2015, 2018) also found that only 5%, US$30 billion, of globally tracked data related to climate finance was oriented toward adaptation initiatives, an increase from 2015/2016 levels but extremely small, and almost all originating from public sector actors, further illustrating the persistent gap in needs versus current actions.

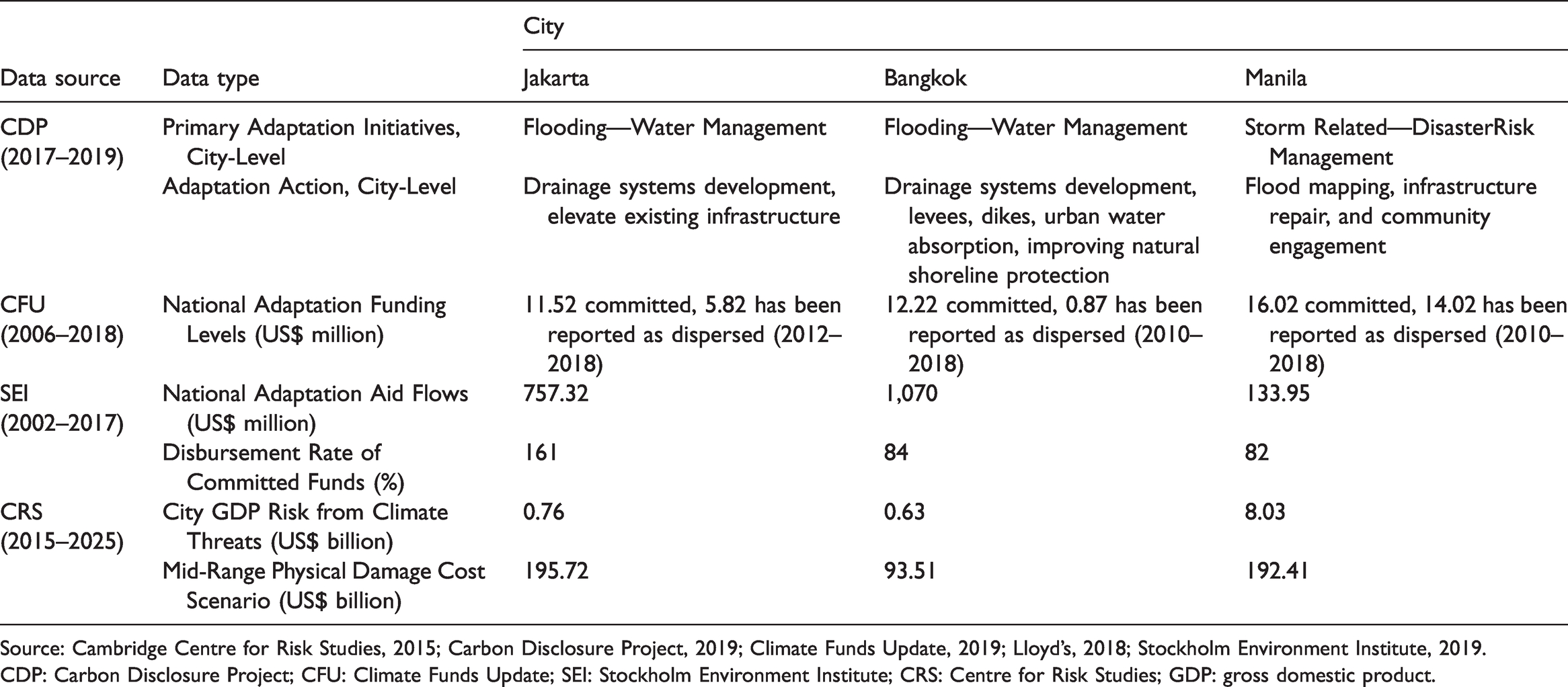

As outlined in Table 2, considering the CDP data (2019) from 2017 to 2019, Jakarta has enacted three major adaptation initiatives focusing on Flooding—Water management. These projects aim to improve urban drainage systems and to elevate existing infrastructure. In Bangkok, eight projects were reported. Six focused on Flooding—Water Management and two projects focused on heat, which can be considered Policy/Budget/Capacity Building projects.

Climate adaptation actions and quantitative risks.

Source: Cambridge Centre for Risk Studies, 2015; Carbon Disclosure Project, 2019; Climate Funds Update, 2019; Lloyd’s, 2018; Stockholm Environment Institute, 2019.

CDP: Carbon Disclosure Project; CFU: Climate Funds Update; SEI: Stockholm Environment Institute; CRS: Centre for Risk Studies; GDP: gross domestic product.

Similar to Jakarta, Bangkok’s flooding-related projects focused on drainage systems development. However, Bangkok further emphasizes levees, dikes, urban water absorption, and improving natural shoreline protection. The projects concerning heat emphasize planning and research required to reduce carbon emissions, including ideas focusing on green buildings. The remaining plans emphasized an effort to inform the public about fire safety and plan how buildings create fire safety regulations.

In Manila, there were a total of 69 listed projects. A majority of these projects focused on Storm-Related Disaster Risk Management, a total of 21 projects, or Flooding—Water Management, Water-Borne Disease—Water Management, and Drought—Water Management totaling at 20, five, and three projects, respectively. Like Jakarta and Bangkok, these projects focus on flood mapping, infrastructure repair, and community engagement. The remaining projects focus on issues of Land Use and Policy/Budget/Capacity Building.

Despite the limited number of reported projects within the CDP database, the Climate Funds Update (CFU) database (2019) has some insights into the national level funding available to Indonesia, Thailand, and the Philippines. Unfortunately, the amount contributed by these funds is also minimal and further speaks to the need for advancements in climate adaptation funding. In Indonesia, between 2012 and 2018, 21 adaptation funds provided only US$11.52 million, of which only US$5.82 million has been reported as dispersed. Thailand fairs worse as its three multilateral adaptation focused climate funds formed between 2010 and 2018 have granted US$12.22 million, of which US$0.87 million has been reported as dispersed. In the Philippines, four multilateral funds have granted US$16.02 million within the 2008 to 2012 period and have dispersed US$14.02 million of their funds.

Evaluations of adaptation finance through bilateral donations provide a more optimistic picture of adaptation finance’s current state; expectations still fall short of needs. Stockholm Environment Institute (2019) collected data on aid flows for adaptation purposes in their Aid Atlas project. By evaluating this data throughout 2002–2017, Indonesia, Thailand, and the Philippines received a total of US$2.22 billion in successfully distributed financing, about US$148 million per year, which is still below global goals but shows continuous financial flows (see Table 2). A positive takeaway from this data is that the disbursement rate of committed funds for Indonesia is over 100%, meaning more was disbursed than committed, and that the Philippines and Thailand have rates of 84% and 82%, which is near the global average of 86%. Nevertheless, the analysis could not locate any sea-level rise or urban flooding climate finance for Bangkok, Jakarta, and Manila projects.

CRS and Lloyd’s data (2019) considers how these limited adaptation developments, led by the public sector, leave room for substantial GDP risks and can be costly for these urban centers. Of the identified risks in the CRS data, five were determined to be climate change-related risks that could be avoided or limited with adequate adaptation financing: flood, drought, plant epidemic, power outage, and temperate/tropical windstorm in the period 2015--2025. In Jakarta, in a typical scenario, these risks are driven in large part by flood and drought and can affect the GDP of the city by US$0.76 billion with potential damages reaching a cost of US$195.72 billion. In Bangkok, with flooding and plant epidemics being the driving forces, city GDP can be affected by US$0.63 billion, with US$93.51 billion in damages at risk. Finally, in the Philippines, US$8.03 billion in GDP is at risk, driven primarily by the threat of tropical storms. Total damages in a typical scenario for all disaster risks can amount to US$192.41 billion, with the most significant causes of damagers being tropical storms and floods.

The CDP, CRS, and Aid Atlas databases provided us with valuable insights to better understand the type of urban adaptation infrastructure being developed. Jakarta and Bangkok have flooding-related projects focused on drainage systems development. Manila’s project portfolio was orientated toward addressing disaster risk management through efficient water management. Aid Atlas provided a general picture of aid flows for adaptation purposes; nonetheless, the database did not offer detailed insights into sea-level rise and urban flooding adaptation projects. CRS data helped quantify the average scenario for all disaster risks that can amount to US$481.64 billion in damages amongst the three examined cities, with the most significant causes of damages being tropical storms and floods.

There was no publicly available information to identify the financial mechanism that Thailand plans to use to finance Chao Phraya Promenade or green belt barrier, super water levees, and watergate projects. In the past, these types of projects in Bangkok were financed from budgetary funds and loans to governments by multilateral financial institutions, which is Manila’s strategy. This is very common in many developing countries that rely on foreign development aid. Nevertheless, these undermine borrower country ownership and restrict policy space and hurt poor communities located on the project (Yarina, 2018).

The Indonesian mangrove planting projects in the north of Jakarta are community-run and are nonprofit sector financed but are limited in scale, thus requiring less capital than most projects. The larger Giant Sea Wall Jakarta project is expected to mobilize both private and public funds. However, the government expects that the private sector will provide the capital for a significant share of the US$40 billion bill, despite a previous desire for it to be majority government funded. Since this is a massive project, and the financing details are still not defined, there are several possibilities in which the private sector can participate (Van Dijk, 2016).

First, private investors can be attracted via public-private partnership (PPP) schemes through which the private sector works together with the government to deliver goods or services to the public (Koppenjan and Enserink, 2009). PPP joint partnerships reduce the overall risk of large-scale public projects by shifting operational and project execution risks from the government to the private sector. Second, project developers can obtain a concession (e.g., build-operate-transfer) for their investment, granting them a right to develop and operate a specific business or property for a specific time and under specified conditions (Van Dijk, 2016). When a country lacks knowledge and capital, outsourcing the development or operation of specific infrastructure projects can fill that vacuum. Third, the government can decide to issue bonds, a debt instrument to raise funds from the capital markets for mitigation and adaptation projects (Tuhkanen, 2020). In the case of sea-level rise and flooding projects, issuing green adaptation bonds is also possible. Green bonds are a type of fixed-income instrument that is specifically earmarked to raise money for climate and environmental projects. They are usually asset-linked and backed by the issuing entity’s balance sheet. This financing instrument can be utilized to fill the private market-driven adaptation finance gap (Tuhkanen, 2020). If issued in a local currency, green bonds might carry a serious currency risk that investors are unwilling to accept. Adaptation green bonds can often bring low yields; hence, investors are willing to invest in mitigation-tailored green bonds instead.

While projects like Chao Phraya for All and the Giant Sea Wall Jakarta will place pressure on governments’ technical, financial, and logistical capabilities, it is guaranteed that these large adaptation projects must have a commercial component attached to them. For example, dike and watergate projects can be transformed into toll road like systems, anti-sea-level rise artificial islands can host residential and business areas, and NBS can generate earnings through tourism and recreation initiatives.

Discussion

The results demonstrate that Jakarta and Bangkok are building resilience against sea-level rise, but all three cities have better addressed urban flooding than the sea-level rise. Jakarta has started constructing the first phase of its Giant Sea Wall. Bangkok’s projects are in the planning phase, in which the city will decide whether it will build just one or all three options under consideration (e.g., green belt barrier, water levies, and 88 km watergate). While the Chao Phraya Promenade project is underway, as of 2019, the project is still waiting for approval to initiate e-bidding for contractors. Unfortunately, Manila is not actively planning adaptation initiatives but instead operates via one-off instances.

When it comes to urban flooding, both Manila and Jakarta rely on the World Bank to acquire financial loans and technical expertise. In Manila’s case, the World Bank supports the Metro Manila Flood Management Project, which is simultaneously developing new pumping stations and early warning systems. The World Bank also works with Indonesian authorities on the Jakarta Urban Flood Mitigation Project that, similar to Manila’s project, encompasses synchronized work on constructing anti-flood hard infrastructure, capacity building of institutions responsible for flood mitigation, and developing flood management information systems. Bangkok has already built an extensive network of drainage canals, underground containers, pumping stations, retention areas, and floodwalls. However, those defenses are not enough to protect its growing population and rapidly developing infrastructure. Thus, the Chao Phraya Promenade project will help the city to improve its capacity to deal with flooding.

As results demonstrated, Manila and Bangkok preferred hard infrastructure solutions rather than NBS to address sea-level rise threats. Unfortunately, nationally and in their capitals, Indonesia, the Philippines, and Thailand have experienced a significant loss of mangroves. Jakarta had one project, which included planting 10,000 mangroves in the northern part of the city, providing many additional benefits for both people and nature (Cohen-Shacham et al., 2016). Additionally, since sea-level rise can lead to coastal erosion, NBS contribute to mitigating coastal erosion (Van Maanen et al., 2015) and provide additional benefits, such as providing nursery habitats for various economically important marine species, improving coastal water quality, and providing adequate carbon storage (Moberg and Rönnbäck, 2003; Murdiyarso et al., 2015; Taylor et al., 2018).

Currently, about two-thirds of low-carbon projects in Asia’s developing countries receive some form of government support. Compared to developed Asian countries, such as Japan, where private sector resources account for roughly two-thirds of financing through debt or equity for low-carbon infrastructure. Incumbent industries have an advantage with investors as knowledge of these existing industries has been developed. The lack of knowledge of the financing mechanisms in these emerging sustainability-based markets, combined with uncertainty in regulation, slows the influx of capital (Anbumozhi et al., 2018). Even after a project’s commercialization, lack of access to risk capital, project scale, and business skills gaps remain significant barriers to investment for widespread deployment (Anbumozhi et al., 2020).

Bridging existing disconnects between capital borrowers and lenders using regulatory reform is vital to attracting private investment outside of government and international institution grants and loans. Borrowers rely on government support to maintain projects’ viability, while lenders indicated that government and international organizations are the primary sources to share risks. Those involved in project financing have advocated for expanding financial tools like green bonds and the expansion of loss guarantee programs. These same stakeholders showed limited interest in tax breaks or subsidies to support their sustainability initiatives (Anbumozhi et al., 2020). The ability to successfully replicate these initiatives depends on local governments’ ability to provide regulatory clarity and a willingness to include private stakeholders in projects and creating avenues for stakeholders to generate revenue. Implemented mitigation and adaptation initiatives as standard regulations within new projects will be essential for strengthening the foundation of these financing markets (Pauw, 2015).

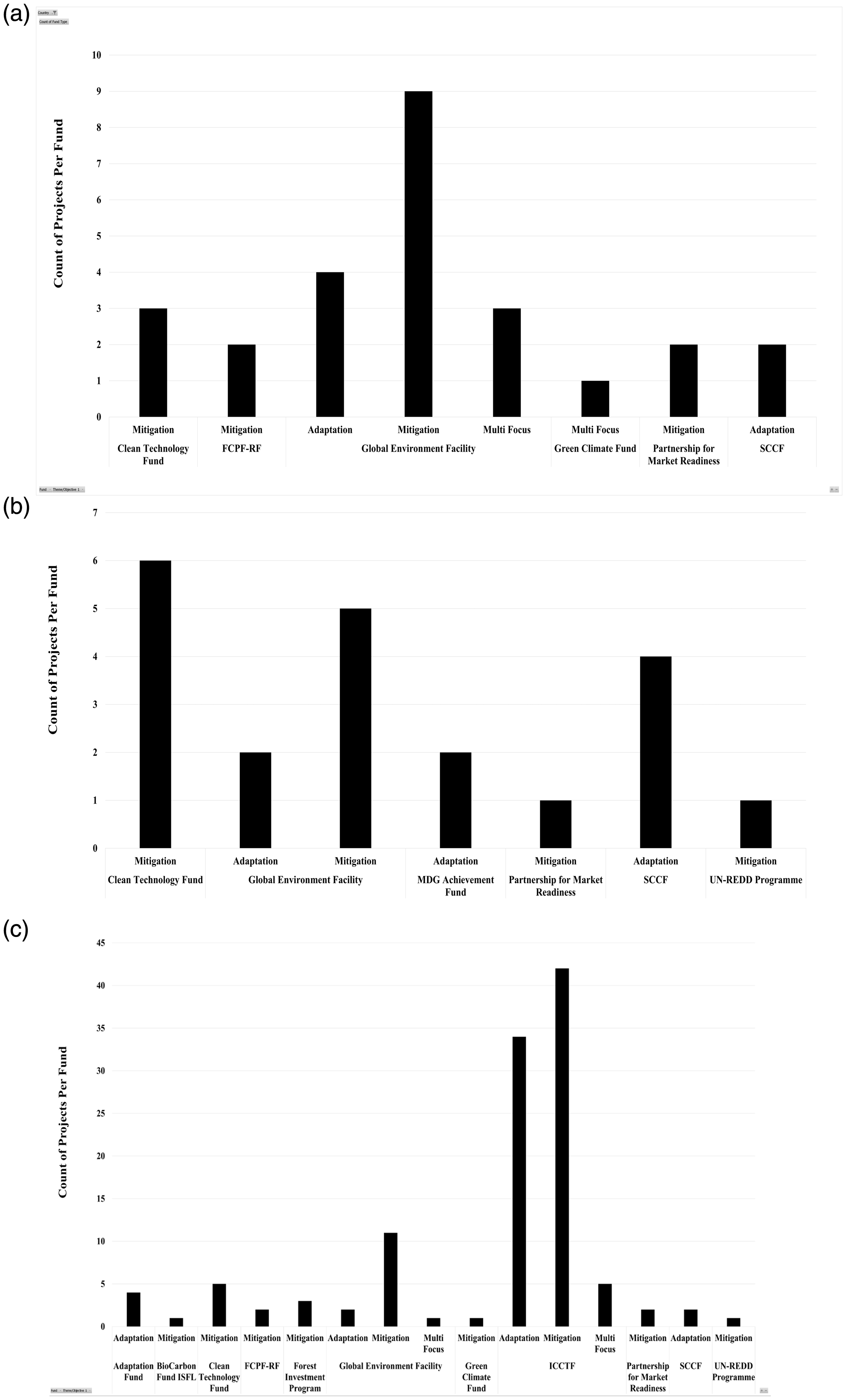

The CFU database’s adaptation and mitigation project financing structure highlights the importance of multilateral and multidonor funds for mitigation and adaptation projects. Many of these projects rely on international support and cooperation and a system of loans and grants to reduce project costs and risks and drive other stakeholders. Funds such as the Global Environmental Facility (GEF) Fund support the most mitigation and adaptation projects across Indonesia, Thailand, and the Philippines using grant funding to encourage co-financing.

However, the multilateral fund with the most projects is the Indonesia Climate Change Trust Fund (ICCTF), which focuses solely on projects across the Indonesian archipelago. ICCTF supports these projects by advancing a business model to increase private sector participation and leverage public and development partner funds to scale-up mitigation and adaptation activities through its grant program. The fund maintains its finances through its inter-sector agreements, placing the fund’s financial assets under the management of an Indonesian bank, Bank Mandiri. Overall, the diversity of multilateral funds is most considerable in Indonesia.

In Thailand and the Philippines, the number of multilateral funds is equal and share significant overlap in operation areas. These two multilateral funding markets have shared operations of four of their six funds. Such overlap of funding and operations possibly further compounds inefficiencies in project operations by involving multiple parties with different projects and objectives that lack communication or coordination. An overview of all funds and the database and their project involvement are outlined in Figure 1 (parts a, b, and c), highlighting the areas of funding overlap within the region and multilateral funds emphasis on mitigation projects.

CDP multilateral/multidonor fund composition: (a) Thailand, (b) Philippines, and (c) Indonesia.

These grants and loan based funds are overwhelmingly overseen by United Nations agencies and affiliates (28% of analyzed CFU projects), followed by World Bank agencies and affiliates (14%). The ADB manages a tiny share of the remaining projects (3%), with the rest being unidentified. The implementing agencies for these funds are government institutions (62%) with the next most significant share being unidentified recipients and only 10% representing private institutions, multilateral institutions, and other public/state-owned organizations.

Cost-effective NBS are already implemented in several emerging Asian cities. Shanghai is in the process of constructing Sponge Park, designed to absorb passively, and clean excess runoff water (Shanghai Urban Planning and Land Resource Administration Bureau, 2018). Mumbai embarked on replanting mangrove trees on beaches surrounding the city (Larsson, 2019). These solutions are cheaper than hard infrastructure and improve resource efficiency.

Regulatory and capital market/banking reforms will likely face high barriers across Southeast Asia. Such reforms would have to curb corruption and develop frameworks to avoid illegal and unsavory actives concerning business and human rights. Unfortunately, steps have been taken to weaken regulatory oversight, most recently in Indonesia (The Jakarta Post, 2019). Regulatory and anti-corruption reductions will likely cause project delays and cost overruns, as has been Malaysia’s case (Zhang et al., 2020).

Even if corruption and regulatory issues are resolved, issues concerning technical capacity remain. Reports have shown that several ASEAN infrastructure projects have failed to reach full operational status due to construction interruption from payment delays and financing shortfalls. Contractor (i.e., material shortages, improper/ineffective planning, poor site management and supervision, and equipment shortage and failure) and owner-related causes (i.e., financial/payment issue and design change/variation order) have also been found to contribute to these delays (Wuala and Rarasati, 2020). Many projects that failed to elevate above the conceptual and planning stages promptly were slowed down due to inadequate project preparation and planning processes as implementing agencies’ lack technical capacity to prepare pre-investment or feasibility studies (Fujisawa et al., 2019).

Low-income and most middle-income nations have what might be considered an advantage because of more of their ongoing urbanization. Since urbanization has not entirely taken place, it can be planned and managed in more effective ways that accommodate the increased risks that climate change is likely to bring. Many cities do not have or may not be able to plan or expect how their cities expand and manage resources to account for growth. With much of the physical growth and economic expansion in the cities of low-middle-income nations taking place outside any official plan and outside official rules and regulations, a large amount of opportunity exists to prepare (Bicknell et al., 2009). An important factor is the adaptation adjustments that cities must make concerning climate change, independent of the often considerable deficiencies in necessary infrastructure that these cities lack, such as storm and surface drains and underground canals.

Recommendations

Cities in developing countries experience financing barriers such as lack of creditworthiness and high default risk. Also, financial institutions that are less risk-averse (i.e., venture capital) are also turned away by the low-reward potential of adaptation investments. These circumstances make it difficult to access more abundant, privately issued climate finance (Causevic and Selvakkumaran, 2018). Therefore, in conjunction with multilateral climate finance funds, international financial institutions will continue to play an essential role as urban adaptation finance providers. However, in Bangkok, Jakarta, and Manila, the major adaptation multilateral climate funds PPCR and SCCF did not provide any sea-level rise and urban flooding adaptation climate finance. In Jakarta and Manila’s case, the World Bank provided big loans for two urban flood management projects. Jakarta’s Giant Sea Wall and Bangkok’s Chao Phraya Promenade are financed from respective governments’ budgets.

When financing hard infrastructure, the issue becomes more complex because the costs are higher. For example, Hong Kong invested US$25 billion in the city’s flood prevention infrastructure between 1989 and 2017 (Environment Bureau of Hong Kong, 2017). Singapore currently invests US$400 million in increasing drainage capacity and an additional US$10 million on a research program that only focuses on sea-level rise and flooding impacts (Goh and Ai-Lien, 2019). In 2006, Tokyo paid US$2 billion for the Metropolitan Area Outer Underground Discharge Channel anti-flood system (Tabuchi, 2017). These high-income Asian cities’ solutions are useful; however, their price tags could be something that middle-income developing cities such as Bangkok, Jakarta, and Manila cannot afford.

The availability of urban adaptation climate finance will determine the expediency and extent of cities like Bangkok, Jakarta, and Manila to build necessary resilience-linked infrastructure. ASEAN cities could work through ASEAN with an international financial institution to establish a climate fund or a sustainable finance bank that would unlock finance exclusively for cities at scale (Alexander et al., 2019). The novelty of this approach would be the establishment of the institution that lends directly to cities. While the ASEAN Infrastructure Fund operated by the ADB exists for ASEAN member states, there is no regional fund or financing mechanisms such as a city-level adaptation tax that can fund building urban resilience.

Megacities in developing countries cannot rely solely on multilateral institutions for funding. Private investments are a crucial resource that can potentially help cities to overcome climate finance gaps. Private sector involvement in adaptation initiatives will draw-in more massive investment and technologies while reducing climate change and vulnerability risks, especially in developing countries where many urban infrastructures are yet to be built. Cities can obtain government guarantees for minimum payments to the private sector to design PPP concessions so that investors primarily face sovereign repayment risk on these minimum payments (Goldman Sachs, 2019).

Bangkok, Jakarta, and Manila can design and issue green bonds for water management projects incorporating sea-level rise and urban flooding themes. These schemes can attract funding from investors (i.e., impact funds). Another strategy to increase private climate finance would be to use land-value capture strategies to collect funding to finance urban adaptation projects. In this case, cities can sell ownership or development rights to fund infrastructure projects or access some of the value of land appreciation by using taxes, transfer taxes, or capital gains taxes (Goldman Sachs, 2019).

Private, public, and nongovernmental organizations stakeholders can work together to develop new climate finance platforms for collaboration. Recently launched Ocean Risk and Resilience Action Alliance platform plans to pilot pioneering climate finance and insurance products that unlock investment in coastal resilience (AXA, 2019). For cities, the application of new insurance products like catastrophic bonds (cat bonds) opens opportunities for sector-specific climate resilience activities. Cat bonds are different from green bonds, which are debt asset-linked products backed by the issuer’s balance sheet. Investors prefer cat bonds because they are treated as insurance products, where their premium proceeds are held in an investment account for the entire bond term; however, if there is no catastrophic event, investors receive their money back at maturity (World Bank Group, 2018).

Cities would need to look into financing more cost-effective NBS, such as the rehabilitation of coastal mangroves, which could be seen as an effective and cheaper resilience-building strategy to better address urban context-specific sea-level rise and flooding threats. Increasing the mangrove area through natural recolonization is a good option instead of more expensive coastal habitat rehabilitation/creation options. The costs to successfully restore both the vegetative cover and ecological functions of a mangrove forest, without counting the land’s cost, have been reported to range from US$225/hectare to US$216,000/hectare, depending on how extensive measures that are needed (Lewis, 2001). Lastly, cities could use ecological fiscal transfers (EFT) to increase access to adaptation finance. EFT programs have been successfully used in Brazil, China, India, South Africa, and the United States since the 1990s and consider biodiversity conservation and ecosystem services-orientated cash transfers from a national government to a local or regional government (World Bank Group, 2018). In these programs, cities receive financial compensation for protecting themselves from sea-level rise and urban flooding at the same time.

Conclusion

Rapid urbanization will continue to occur in low-lying ASEAN cities, increasing their communities’ and infrastructures’ vulnerabilities, compounded by the risks of climate-related disasters such as flooding and storms. Megacities such as Jakarta, Bangkok, and Manila will put them at significant risk with their limited adaption actions, finance, and projects implemented. Our findings show that all three cities studied have existing projects which are addressing urban flooding adaptation projects. Nevertheless, none of the cities have projects which specifically address sea-level rise. On the other hand, Jakarta has plans to continue constructing the Giant Sea Wall as an adaptation measure against sea-level rise.

Our findings also show that public financing for adaptation projects directly addressing sea-level rise is minimal. Our findings lead us to conclude that all three cities’ focus is on urban flood management, primarily through international public financing. All three cities have not attracted key PPPs or focused on NBS for adaptation measures, instead preferring hard infrastructure solutions. This lack of private capital in the adaptation measures against sea-level rise in the three megacities studied here is in stark contrast to other developed Asian cities such as Hong Kong or Singapore. This lack of private funding participation for city-level adaptation measures in developing country cities is compounded by the generally low level of funding cities are attracting for adaptation projects compared to mitigation projects.

Given the varied state of adaptation and mitigation projects in developing cities, an NBS approach can serve as a potential path to diversify financing streams, supplementing the high cost of hard infrastructure projects. Current mitigation and adaptation projects in Jakarta, Bangkok, and Manila are driven by hard infrastructure investments with direct funding from government or multilateral institutions. The development and the usage of new financing tools can help to uplift adaptation and mitigation projects in developing cities. With the growing pressure and frequency of flood-based and sea-level rise-related disasters, implementing financing solutions to support adaptation projects is essential.

Footnotes

Acknowledgements

The authors would like to thank Fumi Harahap, KTH Royal Institute of Technology, whose help was crucial in overcoming linguistic barriers and strengthening overall policy analysis of non-English language city-level documents.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.