Abstract

Studies of financialization have highlighted how politics, particularly through the state, drives the increasing entanglement of financial actors and rationales in the production of urban space. This article shifts the angle to consider the challenges that uncertain politics pose for such entanglement. Looking beyond techno-calculative practices, it explores how finance works politically to sustain value extraction within fragmented regulatory landscapes. It does so through historical and ethnographic analysis of financial investment in urban water and sanitation provision in Brazil, drawing on fieldwork, interviews, and a new dataset on public-private contracts to interrogate how private water companies navigate politico-regulatory relations under financial investors like private equity. It shows that while these providers were quite engaged in local politics under their original owners (construction groups), under financial investors they sought to “escape” it by curbing ties to public officials, reducing the autonomy of local subsidiaries, and successfully lobbying for national standards on regulatory norms. It argues these centralizing efforts constituted forms of centripetal politics meant to enhance asset monitoring, increase regulatory legibility, and reduce political uncertainty. The findings illuminate how financial investors work across political scales to navigate political risk and sustain financial value, thus problematizing the conventional analytical focus on how finance capitalizes on local forms of entrepreneurial politics. Crucially, they reveal the need to treat institutional environments not simply as filters for financial investment but as objects of political contestation by financial actors. This allows for blurring the boundaries between finance and politics, and for politicizing finance.

Introduction

“The hairs of the Canadians stand on end at some of the things that happen,” the manager from BRK Ambiental said with a chuckle as we discussed the firm’s shareholders. 1 We were meeting at BRK’s headquarters, in a high-end commercial tower in a high-priced neighborhood in São Paulo. BRK is one the largest private providers of urban water and sewage services in Brazil. The “Canadians” in question were the private equity firm Brookfield Business Partners, which had acquired a majority stake in BRK 2 years prior, in 2017. Among the “things” that alarmed the new shareholders were local governments unwilling to approve tariff adjustments or pay contractual guarantees. Such political challenges also haunted other private water companies that were owned by or had substantial equity participation from financial investors. In 2019, these companies managed concessions and public-private partnerships in more than 200 Brazilian cities. Across their operations, they confronted the problem of how to navigate uncertain local political relations which could jeopardize the stable returns their investors expected.

Such “political risks,” in investor-speak, are neither new nor unique. Private investors have long felt uneasy about regulatory instability or potential contractual breaches arising from political dynamics. In the water sector, private investment has been the subject of various “political troubles,” ranging from organized protests to everyday efforts by local politicians to intervene in private provision—doing precisely the kinds of “things” that horrified Brookfield, like halting tariff increases due to electoral concerns (Herrera and Post, 2014). Apprehension about political risks may curb enthusiasm around the predictable, long-term returns promised by infrastructures like water and sanitation (Leyshon and Thrift, 2007) and complicate efforts to finance water for all. Indeed, the search for “safe” regulatory environments has often informed the spatially selective investment strategies of global financial actors and inspired calls for strengthening institutional capacity and reducing political interference, particularly in the global South (Serebrisky et al., 2015).

Nevertheless, politics is often not a barrier but a conduit for financial investment. Urban studies scholars have illuminated the active role of states, especially local ones, in supporting financial deepening within cities (Aalbers, 2020). This can occur through various means: from facilitating real estate speculation through the privatization of public land to financing infrastructure and urban development through debt instruments and public-private partnerships. States may be cornered into pursuing these strategies due to sluggish growth and fiscal constraints (Peck and Whiteside, 2016), or act as “go-getters,” constructing attractive instruments that channel financial capital into particular areas (Weber, 2010) or engaging financial capital to advance their own interests (Robinson and Attuyer, 2021; Shatkin, 2022). Beyond states, scholars have highlighted the political work of various intermediaries in mitigating risk and “landing” financial capital in urban space. From standard-setting organizations (Hilbrandt and Grubbauer, 2020) to relational (Torrance, 2008a) and transcalar territorial networks (Halbert and Rouanet, 2014), such intermediaries circulate financial knowledge and practices, reduce information constraints, and mediate relations with the state.

These studies illuminate how politics drives the “financialization” of urban development. However, they tend to position financial investors as the (un)intended beneficiaries of the political efforts of other actors, making them appear removed from the everyday politics of financialization. In contrast, this study seeks to spotlight the political agency of finance. I examine the regulatory relations and political tensions which emerge after investors have “landed” and as they seek to extract stable returns within uncertain political contexts. I explore these issues through historical and ethnographic analysis of private investment in water provision in Brazil. Specifically, I examine shifts to what I call financialized ownership, meaning the acquisition of ownership stakes in water providers by financial investors like private equity groups. Existing studies of financialized ownership in the water sector have emphasized its techno-calculative implications, showing how it encourages utilities to pursue financial engineering techniques (i.e., debt-loading and securitization) or enact extractive calculative practices that privilege the interests of shareholders (Allen and Pryke, 2013; Bayliss et al., 2022; Klink et al., 2019; Loftus et al., 2019; Pryke and Allen, 2022).

What my analysis reveals is that securing stable returns also entails political re-engineering. I show that while private water companies in Brazil engaged closely in local politics under their original owners (construction business groups), the emergence of financialized ownership propelled efforts to “escape” it. Companies sought to formalize ties to local public officials and reduce subsidiary autonomy by centralizing decision-making. They also mobilized politically for national standards on regulatory norms, contributing to a broad reform of the sector enacted in 2020 (Law n° 14,026). I describe these organizational and regulatory efforts as forms of centripetal politics, that is, attempts to move toward more centralized scales of decision-making and regulation. 2 In this case, these attempts aimed at enhancing asset monitoring, increasing regulatory legibility for investors, and stabilizing returns across local operations. At the same time, centripetal politics induced tensions like judicial conflicts with local officials and the deceleration of operational decisions, challenging portrayals of financial investors as paragons of efficiency.

I highlight three insights from this analysis. First, that financial engagement is not simply an extension or deepening of privatization; rather, it may entail shifts in the very political logic of private investment. This signals a need to consider more carefully heterogeneity among investors and their contextual interpretations and spatializations of risk, especially “political risk.” Second, the findings problematize a common analytical focus within urban studies scholarship on how financial investors capitalize on evolving forms of “entrepreneurial” local politics. My discussion of centripetal politics indicates that the political work of securing financial returns from the local sphere might require moving across governance scales—and shifting upward not downward. Finally, the analysis suggests a need to move away from treating existing institutional environments as static filters for financial investment across geographies and instead approach them as objects of political contestation and struggle. This allows for illuminating the blurry boundaries between finance and politics, and, crucially, for politicizing finance.

The politics of finance in politically uncertain worlds

“Financialization” is both a contested concept and multifaceted process. It has become shorthand for describing the growing entanglement of financial actors, instruments, and rationales across various realms, reshaping the workings of households, firms, cities, states, and the global economy (Aalbers, 2019). Some have cautioned, with reason, that speaking of “financialization” risks obscuring the workings of finance itself (Christophers, 2015) or masking “other processes at work” (Robinson and Attuyer, 2021: 7) that involve but cannot be reduced to finance. In this study, I approach financialization not as a taken-for-granted phenomenon but as a set of deeply contextual, albeit interrelated, “problem-spaces.” Hardin (2017: 8) speaks of “problem-spaces of finance”—such as the “securitization of household payments, or proliferating forms of insurance”—as spaces in which we might ask political questions of finance without assuming frameworks a priori. I draw from this suggestion to treat financialized ownership as a problem-space of finance and for finance. It is a problem-space of finance to the extent that it involves financial actors directly in the activities of utilities. It is also a problem-space for finance because, while it presents opportunities for value extraction, the realization of this value is neither automatic nor necessarily stable.

Here, I build on various works which share a sensibility around understanding how financial value is constructed and maintained. Scholarship on “assetization” has underscored that things such as infrastructures do not inherently exist as assets—that is, as sources of durable revenue streams—but must be constructed so (Birch and Muniesa, 2020). This entails rendering assets knowable and liquid through standardization or market-making practices (Carruthers and Stinchcombe, 1999). It may also require the moral “legitimation” of their financial worth (Ouma, 2020). To the extent that financialization processes involve assetization, there are problems that finance—and its willing or chance allies—needs to confront in order to construct revenue-yielding assets that match investors’ risk-return expectations. Chiapello (2020) captures this when noting that “financializing” an activity, policy domain, or organization requires “work,” including framing issues as problems of investment (“problematization”) or operationalizing value through “financial structuring.”

This “work” is arguably continuous. Financial assets “concern obligations that extend over time” (Carruthers and Stinchcombe, 1999: 355), meaning their financial value needs to be sustained in the face of uncertainty. Calculative or evaluative practices can, for example, “embed futurity” in urban governance by assuring the future value of properties (Weber, 2021) or facilitate day-to-day value extraction from infrastructure assets in the South by investors in the North (Allen and Pryke, 2022). But these practices are also intertwined with power relations (Adisson and Halbert, 2022) and may require not only “background work” but “political upkeep” to survive across political cycles (Hilbrandt and Grubbauer, 2020). My concern is precisely with the challenges that uncertain politics pose for the extraction of financial returns over time, and with the kind of political work those challenges engender within particular problem-spaces of and for finance. In essence, I am interested in how finance secures the political conditions for its own temporal reproduction.

Urban studies scholars have attended to the politics of finance and the political consequences of financial deepening in different ways. Some have focused on what financialization means for the state, particularly as state actors internalize financial rationales and come to rely on financial instruments (Adisson and Halbert, 2022). Others have highlighted how financialization undermines politics through “postdemocratic” modes of “technocratic management” (Peck and Whiteside, 2016). In the water sector, financial investors and practices have been shown to evade regulatory scrutiny (Allen and Pryke, 2013; Bayliss et al., 2022) and constrain the space for “shared governance” (Klink et al., 2019). These perspectives make clear the political nature of financial processes and the challenges they pose for democratic governance; what they often lack is more explicit engagement with the political workings of finance itself. While one approach privileges the analysis of politics from the standpoint of the state, the other concentrates on finance’s depoliticizing effects. Financial actors, however, are active political actors—from shaping financial policy and regulation (Pagliari and Young, 2020) to acting as “urban policy-makers” (Sanfelici and Halbert, 2019).

This brings to the fore the question of how private actors behave politically. To understand the politics of finance in Brazil’s water sector, I place the lens on firms. Scholarship on business politics suggests that firms’ economic and political activities cannot be separated and depend both on organizational characteristics—such as ownership structures—and on the politico-institutional contexts in which they operate (Puente and Schneider, 2020; Walker and Rea, 2014). In Argentina, Socoloff (2020) finds that political action by developers enabled housing financialisation within an unstable macroeconomic context, while Post (2014) shows that domestic business groups with diversified holdings and close ties to public officials negotiated water concession contracts and withstood economic and political instability more effectively than foreign multinationals. In Brazil, close state-business relations have historically been a hallmark of urban development and infrastructure projects (Campos, 2012; Rolnik, 2019). Building on these insights, I examine how changes in business ownership influence the way private service providers approach relations with the state. I propose that business politics is driven to manage uncertainty and sustain value. This lens requires treating concessions and public-private partnerships as long-running political relations (Cruxên, 2022a), rather than simply as relatively localized instruments of financialization (Peck and Whiteside, 2016). Put differently, we need to look at the actors behind the instruments. This allows for understanding investors’ situated relationships to states, while exploring heterogeneity among investors themselves—thus considering not only variegated forms of capitalism but “varieties of capital” (Lee, 2017).

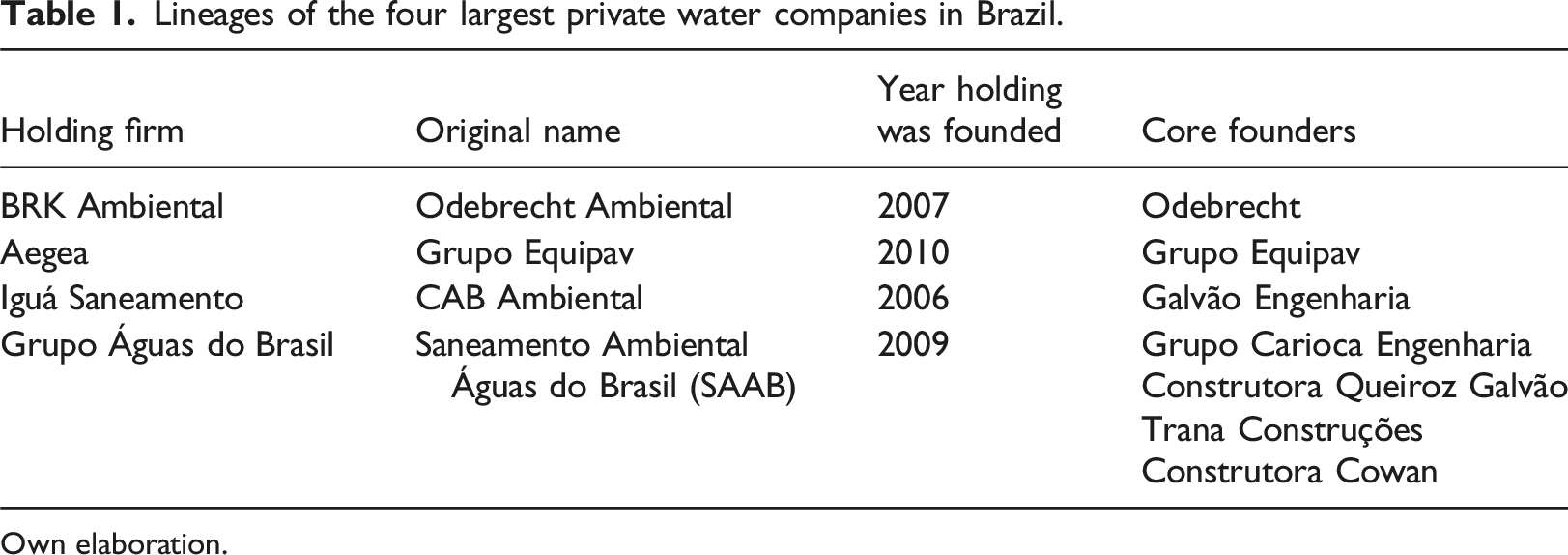

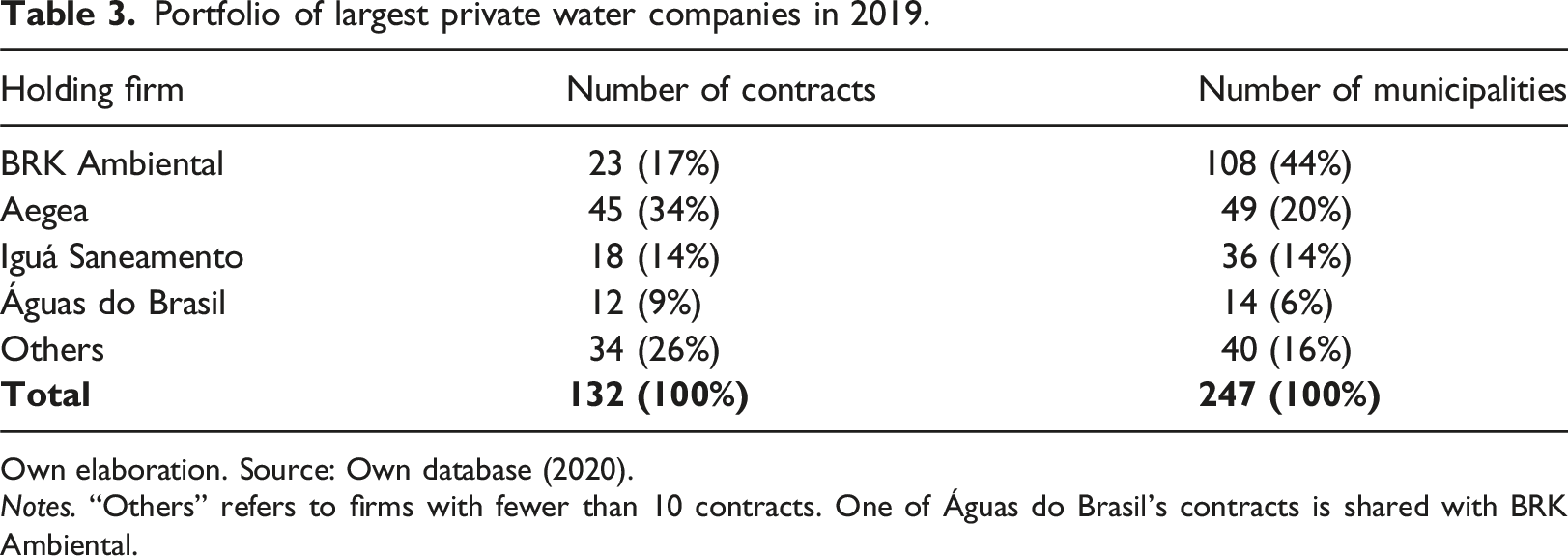

In this vein, I pursue a comparative lens that contrasts financialized ownership to prior ownership models in Brazil’s water sector. I focus on four private firms: BRK Ambiental, Aegea, Iguá Saneamento, and Águas do Brasil. Together they held nearly 75% of public-private contracts in the sector in 2019. As discussed further, the majority were municipal contracts, making local politics particularly salient for the analysis. Through within- and cross-case comparison (George and Bennett, 2005), I trace firm trajectories from their constitution in the mid-2000s until 2020, when a new legal and regulatory framework for the sector was enacted (Law n° 14,026). While those four firms used to share a common DNA—ownership and control by family-owned construction groups—financial investors came to either own or have substantial equity participation in all but Águas do Brasil during the period analyzed. Although business practices may diffuse across companies, including Águas do Brasil allowed for parsing out the implications of financialized ownership among the other firms.

I draw on multi-method research conducted between 2019 and 2021, including document analysis, 85 interviews with 77 individuals, and a dataset I compiled on public-private water and sewage contracts in Brazil from 1994 to 2019. Interviewees included managers and CEOs of private and public water companies, financial actors, consultants, public officials and regulators, specialized lawyers, and leaders of business and civil society associations. 3 My participant observation during a research internship at a private consultancy firm in São Paulo (July–August 2019) facilitated access to business actors. I triangulate across sources to “zoom out,” situating the political-economic processes that shaped private investment over time, and to “zoom in,” examining organizational practices and business politics under different ownership models.

Castles made of sand: How finance gained ground

For investors like private equity groups, “distressed assets” are often unique opportunities to ‘buy cheap, sell high.’ ‘Distressed’ was an appropriate adjective for some of Brazil’s largest private water companies in the second half of 2015. “Multiple bankruptcies could dramatically change the ownership structure of the water concessions market,” announced Global Water Intelligence (GWI), which covers the private water industry (GWI, 2015). The turmoil concerned the repercussions of a broad-scale investigation known as “Lava Jato” (Operation Car Wash), which implicated several Brazilian business groups in overpriced contractual schemes and illicit payments to politicians of all stripes. The deals under scrutiny primarily involved Brazil’s state-owned oil company, Petrobrás, but encompassed other infrastructure sectors (Pupo, 2016). Among the firms affected by the probe were large, family-owned construction groups with diversified holdings like Odebrecht and Galvão Engenharia. These conglomerates were well-established figures in infrastructure development in Brazil and beyond (Campos, 2012). They also had sizeable footprints in the water concessions market. Opportunities for financial investors to take over emerged just as the castles built by construction groups disintegrated into sand.

Construction firms had played a fundamental role in the gradual expansion of private water and sewage services in Brazil since the 1990s. Gradual because of the sector’s complex institutional configuration. Dating back to the 1960s, services have predominantly been provided by publicly owned, state-level companies known as Companhias Estaduais de Saneamento Básico (CESBs), which contract with municipalities. Meanwhile, funding traditionally came primarily from federal funds or public financing from national banks. In the mid-1990s, following a broader privatization agenda, President Cardoso (1995–2002) introduced the 1995 Concessions Law (n° 8987) with the hope of spurring private engagement in public service provision. Yet, confronting the market power of state companies proved difficult (Cruxên, 2022b). Fully private service provision developed largely through sparse municipal concessions, mostly led by Brazilian construction firms. 4

Beginning in the mid-2000s, private water provision underwent a process of consolidation. A few large, family-owned construction groups sought to gain scale by consolidating disparate local operations into holding companies. Favorable macroeconomic conditions driven by the commodity boom together with vigorous public spending and access to cheap federal financing enabled those groups to expand their infrastructure activities (Rufino, 2021). In parallel, regulatory developments and an “ambiguous” (Britto and Rezende, 2017) sectoral policy under President Lula (2003–2010) spurred private interest in water and sanitation. The 2004 Public-Private Partnerships Law (n° 11,079) introduced PPPs as a new investment modality alongside concessions, 5 while the 2007 Sanitation Law (n° 11,445) 6 mandated the creation of independent regulatory agencies to monitor utilities and regulate prices. The promise of greater regulatory clarity provided further stimulus for large construction groups to invest in the sector (Aragão, 2008).

Lineages of the four largest private water companies in Brazil.

Own elaboration.

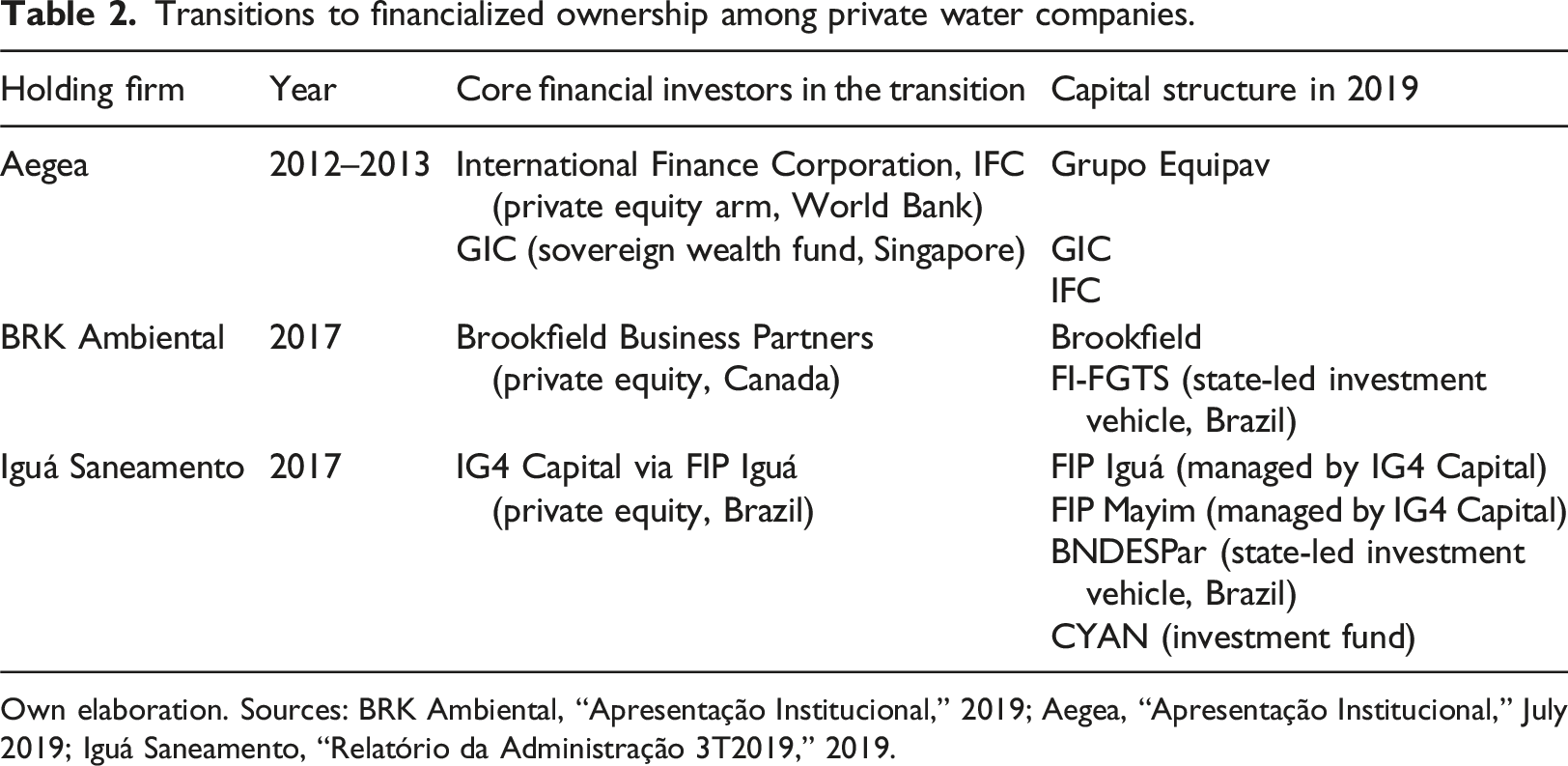

The Lava Jato investigation inadvertently shook up these mini “water empires.” Alongside Brazil’s deepening economic crisis, the corruption scandal eroded the finances and reputations of construction groups like Odebrecht and Galvão Engenharia, pushing them to relinquish assets (Laporta, 2017). As construction groups stepped out, private equity investors were eager to step in (Marcelino, 2019). Between 2004 and 2010, private equity activity in Brazil flourished and diversified, stimulated by consistent growth, a strong currency, and declining interest rates during Lula’s administration (Leeds and Satyamurthy, 2015). Although economic conditions deteriorated beginning in 2011, leading the industry to experience a downturn, prospects brightened again around 2015–2016. Globally, relatively low interest rates facilitated private capital mobilization for infrastructure investments. Domestically, tighter public spending amid growing fiscal austerity—especially under President Temer (2016–2018)—and the restructuring of infrastructure markets following Lava Jato created opportunities for financial investors to cash in (Wehba and Rufino, 2023; Finance_02).

Transitions to financialized ownership among private water companies.

Own elaboration. Sources: BRK Ambiental, “Apresentação Institucional,” 2019; Aegea, “Apresentação Institucional,” July 2019; Iguá Saneamento, “Relatório da Administração 3T2019,” 2019.

Portfolio of largest private water companies in 2019.

Own elaboration. Source: Own database (2020).

Notes. “Others” refers to firms with fewer than 10 contracts. One of Águas do Brasil’s contracts is shared with BRK Ambiental.

Construction groups, of course, did not operate “outside of finance.” As Aegea’s case illustrates, they often spearheaded the integration of “old” business logics with “new” financial strategies (Rufino, 2021). Odebrecht and Galvão Engenharia also sought strategic—albeit passive—partners in state-led investment vehicles such as FI-FGTS and BNDESPar. This illuminates how the federal state—long a key source of sectoral funding—worked as a conduit for financial deepening. Both state funds remained minority shareholders in BRK Ambiental and Iguá Saneamento, respectively, after private equity investors took over. But the fact that construction groups were entangled with finance did not mean that, as shareholders, they approached investments the same way. A reoccurring theme in my interviews and fieldwork was precisely how distinct their approaches were.

Shifting logics of return extraction: Shedding the construction DNA

Since the mid-1990s, large construction groups had approached investments in the sector from a “holistic” perspective: concessions and PPPs were diversification strategies and opportunities to build infrastructure (Parlatore, 2000). Discussing the acquisition of Odebrecht Ambiental, Brookfield’s Managing Partner and South America Head, Marcos Almeida, had noted: “For construction companies, the investment return was not necessarily linked or only linked to the project itself, but to how much money they could make building it” (Marcelino, 2019). This perception of a “construction bias” was generalized among actors in the sector, even if a few company managers from the period tried to downplay it.

By comparison, financialized ownership required firms to shed their construction and engineering DNA. At Aegea, one manager reported their biggest challenge was “running a company of engineers” (Manager_E), while another related the following when asked what they had learned in their career at the firm: Another challenge for me was to understand the financial market itself. (…) The way we looked at the business, from the point of view of profitability, of project evaluation, was one. I think before we looked at it very much from a technical point of view, “engineering-esque” (engenheirístico), you know? (…) With the entry of [financial shareholders], you need to look at it from the point of view of profitability to the shareholder. (Manager_B)

In practice, this lens entailed a greater focus on operational issues with direct bearing on revenue streams. This echoes the well-known tendency for non-financial firms to circumscribe their activities—by outsourcing or curtailing long-term investments—as their fortunes become more entangled with financial markets. “When we came in,” a manager from Iguá Saneamento recounted, “our restructuring plan was to forget investment programs, conceptions, and focus very heavily on operational efficiency (…) The [former company] had a statement of operational focus but we didn’t see that” (Manager_D). For Iguá, this produced quick results. Within a year of being acquired by IG4 Capital, the company went from registering losses of R$ 74.5 million across its operations to earning a profit of R$ 28.1 million (Rocha, 2018).

Politically, this operational focus translated into heightened anxiety around how unpredictable local politics might jeopardize companies’ ability to obtain predictable returns from each operation. While private water provision had become concentrated around a few firms, 88% of the 132 contracts I documented in 2019 were with a single municipality. Despite the regulatory improvements introduced by the 2007 Sanitation Law, regulatory capacity remained patchy: nearly 60% of municipalities lacked a defined regulator of service provision in 2019 (FGV CERI, 2019). Municipal politics, especially relations with mayors, thus played an important role in day-to-day contract regulation and operational activities that rely on state planning, like land use and zoning norms. These activities were often steeped in personalistic and informal relationships that have long characterized local politics in Brazil (Diniz, 1982). While such relationships may lead to rent-seeking or patronage, they may also smooth out day-to-day operations (PrivateProvider_15). Construction groups understood this well. Fragmented and personalistic political environments were “waters they knew how to navigate” (Consultant_05).

For financial investors, however, fragmentation caused greater concern. When asked how changes to financialized ownership mattered for contractual relations, one lawyer observed: “you have more urgency to generate results. (…) There is no longer the possibility of explaining to [shareholders] that you won’t question the mayor’s order to not readjust [tariffs] because it’s an election year” (Lawyer_05). Moreover, regulatory fragmentation was perceived as a source of higher “transaction costs.” Brookfield’s Managing Partner complained, for example, about a labyrinth of “conflicting regulations,” arguing that when regulation is local, “I have to go one by one to explain my case,” meaning that “the risks of municipal regulations are greater than state ones, and the state ones are bigger than the federal ones” (Marcelino, 2019). Political relations in a fragmented context, thus, represented a problem space for finance.

Such anxieties extended beyond concerns from direct financial shareholders. They involved the expectations of financial market actors broadly and of potential future investors and creditors therein. To the extent that uncertain politics can affect future revenue streams, it may compromise firms’ ability to distribute dividends or repay debt. This was particularly important within a context of constrained public financing and greater interest in raising funds via capital markets. According to the Brazilian Ministry for Regional Development (MDR), capital raised for water and sanitation projects through “incentivized debentures”—which exempt individual investors from income tax—increased from R$ 494 million in 2018 to R$ 2.7 billion in 2021 (Rittner, 2022). BRK Ambiental, Iguá Saneamento, and Aegea played an important part in this movement. BRK Ambiental organized three debenture issuances in 2020 alone, while Iguá became the first to issue “green debentures” designed to promote both social and environmental goals. Equity capital also became more fluid. Between 2017 and 2021, Iguá Saneamento’s ownership structure evolved from one to two investment funds: FIP Iguá and FIP Mayim. Both were managed by IG4 Capital, but their core investors were two Canadian pension funds: AIMCo (since late 2018) and CPP Investment Board (since early 2021). As for Aegea, the IFC sold its stake in the company in 2019, while Itaúsa, a Brazilian investment holding company, acquired a minority stake in 2021.

This coming and going of capital, through debt and equity, both immerses firms more deeply in global financial flows and places their reputations under greater market scrutiny. Credibility is crucial for raising capital or potentially going public, a common exit strategy for private equity. Iguá Saneamento, for example, attempted three initial public offerings (IPOs), without success (Alves, 2020). Explaining the difficulty of going public, the head of one private equity group noted: Equity investors… they are still very afraid of exposing themselves to a highly fragmented market, with regulation that is still, as I mentioned, very dependent on municipalities, on mayors, on municipal regulatory agencies (…) They say: ‘Well, Brazil is problematic, chaotic, from a political and institutional point of view, what if there are any issues? Are there any controls? (Finance_05).

A fund manager from a firm specialized in equity securities concurred: “I think the biggest fear the private sector has is this whole issue of having to negotiate mayor-to-mayor (…). The biggest risk in an investment such as this, for those of us who are not inside the company, is to know whether there is nothing there that has effectively collapsed” (Finance_03).

Centripetal politics

Such fear of negotiating “mayor-to-mayor” contrasted starkly with the ethos construction groups had cultivated. One interviewee anonymously observed that companies never expected municipal stability when pursuing infrastructure projects; rather, they sought to “control the follies of the mayors” through campaign contributions. 7 These political strategies built on ingrained relational norms. Founder Norberto Odebrecht wrote in Odebrecht’s rulebook, “‘whatever the client desires or needs (…) that is decisive.’ He made it clear that the client was the elected authority (governante), not the state” (Gaspar, 2020: 45). Former managers of private water companies echoed this perspective. “The service is local. How can I not talk to the mayor? The mayor is my client,” exclaimed one manager from CAB Ambiental when asked how approaches to business risk compared then and now, adding: “You have to create the adequate instruments for dealing with this reality, not try to change that reality” (Manager_A). But financialized water companies were not content to play the same old game. Instead, they began to engage in centripetal politics.

Centripetal politics began with efforts to exert greater control over local operational activities, contributing to the formalization of political relations. This occurred in two main ways. First, companies adopted internal compliance programs to detect and fend off legal or ethical infractions. The “Lava Jato effect” was relevant here. The scandal led to a boom in compliance consulting among Brazilian businesses (Melo and Alvarenga, 2017). Between 2017 and 2018, all major private water companies—including Águas do Brasil—developed codes of conduct, anti-corruption policies, and hotlines for reporting suspicious activities. But compliance changes among the holdings controlled by financial shareholders were reportedly the most stringent (PrivateProvider_01; Lawyer_01; Consultant_03). One consultant remarked that “Brookfield implemented a compliance so strong, many thought it would kill the company” (Consultant_07). “Kill” because strict compliance norms risked stiffening relations with local officials. One manager from Iguá Saneamento recounted leaving a meeting with a mayor and a local public prosecutor after only 5 minutes when they “tried to induce a certain conversation” (Manager_D). For some old-timers, like a former manager from CAB Ambiental, this behavior was excessive: What is happening is that when the mayor approaches the person and says, ‘there is someone who is a cousin of whomever that needs a job, can you see to it?’, the person stands up and says, ‘mayor, this issue I cannot discuss,’ and leaves. So, this causes an unnecessary lack of connection (falta de liga). (…) You could listen to them (…). ‘Look, mayor, I’ll see if I have a job opening and if the person’s profile fits, we can do an interview, a selection process.’ You didn’t commit a crime (…). If the person doesn’t get [the job], you say ‘mayor, they didn’t meet our requirements,’ end of story. (Manager_L)

A second way in which holding companies sought to exert greater local control was through centralizing decision-making. Under construction groups, local subsidiaries tended to have greater decision-making autonomy, which facilitated relationship-building with officials and enabled local managers to address context-specific or emergent issues with greater agility. Odebrecht Ambiental was perhaps the main exponent of a decentralized organizational culture. Local teams and regional managers were responsible for strategic investment and operational decisions and reportedly had complete freedom to talk to officials and close deals (Ribeiro, 2019; Manager_K). The practice was not exclusive to private water companies. São Paulo’s state company, Sabesp, followed a similar logic: “it is much more efficient for Sabesp to have a manager that knows the mayor, especially up-country, [a manager] that goes to the same social club and so on” (StateCompany_04). In contrast, financialized private providers sought to standardize operational processes and centralize, to varying degrees, their relations to subsidiaries. Holdings began to play a greater role in the day-to-day activities of local providers, from commercial strategies to deciding how to repair a broken pump. One manager who experienced this transition at BRK Ambiental observed: In the last 2 years the company has undergone a very big transformation both in terms of culture and of governance. It stopped being a family business (…) that, to me, was one of the best companies I’ve ever worked for because it had a characteristic of granting you autonomy to get results, there was a relationship of trust. And today the culture is more centralized, more professional. (Manager_F)

At Iguá, managers also noted IG4 Capital’s active participation in everyday management and closer oversight of local operations (Manager_I; Manager_D). In comparison, Águas do Brasil had centralized decisions concerning hiring and commercial processes but left operational decisions in the hands of local subsidiaries (Manager_M), with its non-financial shareholders and administration board reportedly maintaining a “hands-off” approach (Manager_J).

Centralization facilitated control over local assets. The point is not that companies neglected local contextual realities but that their subsidiaries had less flexibility for independently handling those realities. The search for greater control reflected concerns with performance—meaning the capacity of subsidiaries to produce expected results (PrivateProvider_16)—but also with legibility and credibility. During a field visit to an operation controlled by one of the financialized holdings, local professionals introduced me to a program designed to standardize procedures and use smart data technologies to better monitor local infrastructure assets. The effort was presented as a means for increasing transparency for creditors and shareholders, but also for managing risks from political turnover. Data could be used to fend off potential opposition from future elected officials and show how subsidiaries were fulfilling contracts. The initiative was not without resistance. Local employees complained about loss of autonomy over their work: “no one likes to be controlled,” observed one professional heading the program.

Beyond organizational changes, centripetal politics entailed strong business mobilization for regulatory changes at the national level. Private water companies hoped that more uniform norms across the country would alleviate investor concerns with regulatory fragmentation and, as I heard often, increase “predictability.” The association of private water providers (ABCON) planted the idea for regulatory standardization in 2016, during consultations with the administration of President Temer. At the time, distressed construction groups were struggling to sell their water companies (Alonso and Pupo, 2015). As financial market actors set their sights on growth opportunities in the sector, regulatory uniformity turned from a hope to an imperative (Finance_01; Finance_02). In a 2017 report, BTG Pactual, one of Brazil’s largest investment banks, explicitly advocated for a federal regulatory body for water and sanitation provision (BTG Pactual, 2017). One of the bank’s founders, Paulo Guedes, would become Minister for the Economy 2 years later, under President Jair Bolsonaro.

The quest for regulatory standardization came to fruition with the enactment of a wide-ranging regulatory reform of the sector (Law n° 14,026) in July 2020. The legislation expanded the mandate of the National Water Agency (ANA)—which previously regulated only water resources management—to include the “harmonization” of regulatory norms and practices for water and sanitation provision. Although ANA would not regulate services directly, the legislation effectively created a new national regulatory layer. Subnational agencies and governments were encouraged—or forced—to comply with ANA’s norms as a condition for accessing federal funds. Beyond such constraints, private companies expected moral enforcement to support norm compliance: “whoever doesn’t follow [the norms],” argued a manager from Aegea, “will be sending sort of mixed signals to the market” (Manager G).

Beyond regulatory standardization, the legislation introduced important changes meant to confront the market power of state companies and amplify opportunities for private provision at regional scales, thus creating additional institutional pathways for the upward rescaling of private water investment. I discuss the political struggles around these changes more deeply elsewhere (Cruxên, 2022b). Suffice to say that ABCON and private providers worked hard to marshal political support for them. They leveraged ties to policymakers to craft iterations of reform bills; they contributed the numbers and language that political allies used to advocate for reform—in the media and on the Congress floor. Financial investors were also not idle bystanders. ABCON’s financial and coordination capacity owed much to membership from large financialized companies like BRK Ambiental, Iguá, and Aegea—all of whom participated actively in reform negotiations. Moreover, sensing broader financial market interest in the sector, the association worked to build a pro-reform alliance with stock traders and large investment banks. One lobbyist recounted: “At the end of the day, the guys who really supported us were the guys who played on the stock exchange. They went to Brasília [the capital], promoted newspaper articles, crowded vans to go door-to-door to speak with legislators” (BusinessAssociation_01).

These rescaling efforts, however, remain partial. One interviewee equated efforts to change relations with public officials to a “civilizing process” (Finance_05), implicitly positioning finance as a modernizing force. But “modernization” projects are often filled with tensions, marked by resistance, and thus never totalizing (Mitchell, 2002). Frictions were already appearing. For example, one of the financialized holdings sought a readjustment of the service tariff at one of its local operations after a discount previously negotiated with the municipal government expired. Seeking to avoid the electoral burden of a tariff increase, the mayor reportedly asked to delay the readjustment. Despite initially holding back, the company eventually adjusted the tariff per the contract, without consulting the mayor. The decision went poorly, and legal battles ensued. The mayor attempted to take over the subsidiary, forcing the holding to adjust its relational approach: “We had to change the relationships at the bottom (embaixo), re-nurture them, and move things forward” (Manager_D).

While conflicts between public and private partners have always existed, specialized lawyers observed a tendency towards greater litigation after financial investors gained prominence (Lawyer_01; Lawyer_04; Lawyer_05). One noted that firms like BRK Ambiental and Iguá Saneamento were struggling to “keep mayors in line,” while another remarked that perhaps what was lacking, among financial investors, was a sensibility towards the fact that stable returns are not inherent to an asset but are also politically constructed: “I think the investor that bought these assets or became a shareholder saw in them a stable cash flow. But in reality, you need a lot of energy to realize this cash flow. A lot of energy and a lot of convincing. It’s the day-to-day work there with the public partner [poder concedente], legitimate but tough” (Lawyer_04).

Such tensions revealed important challenges. Litigation can take years, meaning that taking conflicts to court (judicialization) can curtail investments as private firms await juridical decisions. Moreover, organizational centralization can lead to more rigid and sluggish decision-making. When asked how relationships between the regulatory agency and private subsidiaries changed as financial investors took over, one regulator highlighted delays: “In other times, the operations director (…) in the municipality would have resolved [an issue] in 10 minutes but this process of communicating with São Paulo [the holding], waiting for them to assess, and getting back to us took a week” (RegulatoryAgengy_02). Forms of centripetal politics thus risked offsetting finance’s very quest for efficiency.

Conclusion

Scholarship on the entanglement of finance in urban development and infrastructure provision has done much to show that financialization has political roots. This study demonstrates that it also has political ramifications. Examining business organization and political activity among the largest private water and sanitation providers in Brazil, it shows that shifts towards financialized ownership prompted private water companies to see local “political risks” in a new light: once viewed as navigable waters, they became turbulent seas that needed avoiding. Private providers sought to curb ties to municipal officials and formalize political relations, centralize organizational decision-making to better monitor relationships as well as assets, and mobilize for greater regulatory standardization at the federal level. These movements towards more centralized forms of governance, which I describe as centripetal politics, were understood as necessary strategies for attenuating political instability in a fragmented regulatory environment, while enhancing asset legibility and predictability for investors. At heart, they aimed to reconfigure the politico-regulatory terrain that supports the continuous extraction of returns from urban service delivery.

Three insights from this study are worth highlighting and reflecting on. The first is that the “work of financializing” (Chiapello, 2020) and securing stable returns may require not just financial but political re-engineering. Scholars have illuminated the technical and calculative practices that support the conversion of infrastructures into financial assets. Private equity investors like the ones who gained prominence in Brazil’s water sector have earned a special reputation as debt-loaders and financial engineers (Allen and Pryke, 2013; Appelbaum and Batt, 2014). But this model requires the ability to forecast returns so that debts can be repaid or more debt can be contracted. My research shows that such an ability requires as much politics as it does financial techniques. Moreover, it underscores the need for deeper exploration of how different types of private investors understand political and regulatory risks within particular sectors and political-economic landscapes.

A second insight is that understanding this political work requires treating existing market institutions not simply as filters for investment but as objects of contestation by financial actors. As Klink et al. (2019: 3) note, urban political economy scholarship on financialization has tended to “[take] markets relatively for granted.” Stable regulatory institutions are often considered pre-existing conditions for financial interest. While this may be true in terms of how investors “scan” the globe for profitable geographies, it does not mean that market institutions are fixed. While financial investors may benefit from the institution-building and de-risking efforts of others—such as the state—they may also, as my research indicates, challenge the existing “rules of the game.” Studies of financial regulation have shown that “financialization may create the conditions for its own deepening by conditioning the regulatory environment in which it is situated” (Pagliari and Young, 2020: 113). My analysis extends our understanding of this phenomenon by highlighting how business politics can be a vehicle for finance to exercise political agency and shape regulatory environments in problem-spaces for finance other than financial policy proper.

The third insight is to show that political re-engineering may involve moving across scales of governance (and up rather than down). This problematizes a conventional analytical emphasis on particular cities or projects as privileged sites for the extraction of financial returns from urban space. This privileging of the local often reflects the tracing of financial dynamics to variegated processes of state restructuring that elevated the role of cities and metropolitan regions as sites of institutional experimentation and entrepreneurial governance since the 1970s, particularly in North-Atlantic contexts (Brenner, 2009). In Brazil, however, centripetal politics involved searching for regulatory stability at the national scale as a refuge from local uncertainties. This search is somewhat puzzling because it occurred in relation to a deteriorating fiscal context, wherein we might expect entrepreneurial local government fixes to thrive. However, it is less perplexing when we consider that regulatory standardization may constrain political intervention in local service provision and reduce the need for investors to understand varying subnational regulations. Such changes could mitigate political risks for investors and support the generalization of knowledge about assets (Carruthers and Stinchcombe, 1999), particularly as private water companies looked to capital markets for funds. This observation resonates with scholarship on the subordinated character of financialization in emerging economies, which suggests that standardized regulatory structures make it easier for investors to “see” and invest in assets in these economies (Alami et al., 2023). However, this is not simply a story of global financial forces acting from above. The forms of centripetal politics I have described cannot be divorced from domestic market structures and shifting state-business relations amid the downfall of construction groups post-Lava Jato. Moreover, the search for refuge in upper scales of governance need not be particular to “riskier” Southern markets. Torrance (2008b) uncovers a similar dynamic in the case of a toll road concession in Toronto, Canada. Future comparative research can probe the conditions under which financial actors move—and work politically—across scales of governance, and with what repercussions for urban development and infrastructure provision.

These insights raise questions about the practical implications of centripetal politics. Regarding state-business relations, we may ask, on the one hand, whether this is a more “sanitized” form of business politics given histories of close—and sometimes corrupt—public-private relations; on the other, we may question the extent to which it can be disruptive or lasting because of such histories. Within a transitional context, any answers are tentative. I would caution against reading the potential formalization of local political relations as a form of sanitization. It is hard to ascertain what happens on the political backstage. The creation of a national-level regulatory body could simply shift the costs of regulatory capture away from the local. Once created, standardized reference norms were also not guaranteed to safeguard financial interests or be uncontested. Given the sector’s multi-scalar architecture, political dynamics from local to state and regional levels were likely to remain relevant. Additionally, as noted, efforts to reconfigure politico-regulatory terrains may create friction and require adaptation. Emerging tensions between financialized providers and local officials already signaled the contradictions of seeking efficiency through rigidity or political security through political distancing.

Finally, a related question concerns the extent to which financialized ownership and centripetal politics undermine local accountability in urban service provision. Regulatory centralization could reduce the room for local political processes to shape regulation. It could also prove challenging for the new national regulatory body to reconcile different local contexts and mediate among competing political claims. Here, I share concerns from many scholars around the potentially “depoliticizing” effects of financialization and the loss of socio-political control over policies or services. I am also wary, however, of how the language of “depoliticization” may inadvertently create a separation between finance and politics, and thus constrain our sense of political possibility. Reflecting on urban struggles around financialization, Fields (2017: 6–7) observes that “representing finance as so complex and abstract (…) serves to obfuscate it and shield from contestation.” Similarly, concentrating on finance’s depoliticizing effects risks obscuring the ways in which politics still matters. To the extent that the extraction of financial returns over time requires political effort, as this study suggests, by moving towards a language of politicizing finance or financialization, we might keep in sight the political pathways that allow financial interests and practices to be reproduced. To the extent that these pathways exist, they can be politically disputed.

Footnotes

Acknowledgements

I am grateful to the editors and anonymous reviewers for their helpful comments. I also thank Gabriella Carolini, Ben Schneider, and Jason Jackson for their guidance, and Asmaa Elgamal, Emilia Simison, Catherine D’Ignazio, and Helena Suárez Val for comments on earlier drafts. I am thankful to my colleagues at Queen Mary University of London for their insightful support. My deepest gratitude is to those who agreed to participate and contribute to this research.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by Harold Horowitz Student Research Fund, School of Architecture and Planning, MIT (2020), Summer Study Grant, Center for International Studies, MIT (2019), MIT Brazil Research Grant, MISTI Science and Technology Initiative (2019), and William Emerson Travel Grant, Department of Urban Studies and Planning, MIT (2019).