Abstract

Success in launching new therapies for rare diseases (RDs) implies the ability for the manufacturer to achieve a level of reimbursed price and a level of market access that are commercially viable on the global market. Access to RD therapies is challenging in many countries because the legal and policy frameworks may be absent, funding may be insufficient and/or payers do not see the justification with the prices for these therapies. The industry has, however, a real opportunity to partner with healthcare systems to address these issues, for example, through education towards payers, responsible and evidence-based pricing, and innovative contracting. Such support is particularly needed in middle-income and emerging markets, where it will contribute to growth in RD therapy coverage.

Keywords

Introduction

Rare diseases (RDs) represent an attractive global market for the pharmaceutical industry. 1 For example, a recent report suggests a 11% annual growth of worldwide sales of RD therapies, to reach close to 25% of prescription drug sales by 2024; 2 the same report indicates that, although oncology is a notable area, the RD drug market spans a number of other therapeutic areas, such as blood and central nervous system disorders. It has also been argued that firms with marketing authorization for orphan products are more profitable than those without marketing authorization. 3

Yet, the opportunities go hand in hand with addressing multiple hurdles, particularly when it comes to market access. For example, reimbursement of RD therapies can be limited due to lack of supporting policies and funding, challenges of high prices, lack of specific approaches to evaluating RD drugs in view of limited evidence and payers’ concerns about budget impact. This article focuses on the payer-related aspects of market access for RD therapies, leaving aside upstream, regulatory considerations. The perspectives of middle-income and emerging markets will be included, as these are often less prominent in commentaries dedicated to RDs but, in the author’s opinion, have significant growth potential. The next section highlights the examples of countries where there is a large patient pool that could eventually be accessed (China) or the political environment is conducive to good access (Colombia).

The views expressed in this article are based on both the literature and the author’s long-standing experience with pricing and reimbursement of RD therapies across diverse geographies. Recommendations will be made about ways the pharmaceutical industry can help foster broader and sustainable market access to much needed therapies in the RD space.

Uneven access to RD drugs around the world

Level of access to RD therapies varies greatly across the world. Although it is considered to be adequate in the wealthy countries, patient organisations (especially in Europe) lobby for better and more equal access. 4 Availability of RD therapies to patients is much more challenging in less wealthy parts of the world, for example, in Asia.5–10

Out of the many reasons for variable level of access to RD therapies, let us examine broad categories that directly relate to reimbursement: (1) legal and policy frameworks and (2) funding pathways and practices. To exemplify the variety of situations along these dimensions, we will examine countries representing high, medium and low overall levels of access, respectively: France, Colombia and China (see Table 1).

Examples of variability in RD access policy and practices across the world.

Source: author’s personal experience; Dharssi et al. 5

RD: rare disease; HTA: health technology assessment; CEPS: Comité économique des produits de santé.

France has a been a leader in implementing a national RD plan since 2005, has a clearly supportive policy in RDs and has created a well-coordinated, comprehensive infrastructure to deliver on the policy. 11 Of note, the European regulatory framework incentivising development of RD therapies creates a conducive context. The pricing and reimbursement process is the same for RD therapies and the other therapies. However, the French payer system has been favourable to new RD drugs, for example, through reimbursement of therapies before regulatory approval (Autorisation Temporaire d’Utilisation (ATU)). Colombia is an example of a country where the constitutional right to treatment is explicit and central government has been proactive and efficient in the past few years in driving an RD policy and capabilities; however, policy implementation may be slow. 14 Other countries in Latin America trail, but are working on ways to establish an adequate RD policy that escapes the unsustainable reliance of the judicial route to access. 9 China does not have RD-specific legal framework or incentives, reimbursement policy and coordinated infrastructure;5,8 also, decision makers’ understanding of RDs may be limited 8 (and personal communication). However, a national list of RDs has recently been published, 13 grass-root pressure is rising and the country is slowly moving towards better access to RD drugs.5,8 Given the large Chinese population, low level of access to RD therapies (e.g. 20%–40% of drugs accessed in the US/EU/Japan markets are available in China 8 ) and local signs of greater interest in RDs, it can be hypothesised that a substantial patient pool can be eventually accessed.

An interesting observation when looking across countries, and organisations within, is that the prevalence threshold used to define an RD varies significantly, from 5 to 76/100,000 inhabitants, although a majority fall within the 40–50/100,000 range. 15 This means that more diseases would be classified as ‘rare’, and possibly be treated differently by payers, in jurisdictions where the threshold is higher. Looking at the three countries in Table 1, ‘official’ prevalence thresholds are highest in France (50/100,000), followed by Colombia (20/100,000) and China (0.2/100,000); in contrast, average prevalence thresholds based on surveying the whole range of stakeholders and in particular patient organisations are, respectively, 50, 50 and 76/100,000 in France, Colombia and China, 15 suggesting a substantial RD recognition gap in Colombia and even more China. Definition of RDs by prevalence may, however, not be the most useful – China, for example, has established local and, recently, national lists of RDs 13 even though there is no consensus on a prevalence threshold. Interestingly, emphasis in China is on catering for those treatable RDs that have the greatest total burden on society (being the most prevalent). 13 This contrasts with a position taken in the United Kingdom, where ‘ultra-rare’ diseases (e.g. 0.1 or 2 per 100,000 inhabitants) are singled out and willingness to pay higher for effective therapies. 16 Perhaps, this difference is linked to public health priorities and political sensitivity: focus on extending health care coverage to a huge population in a sustainable way or reflecting local needs (China) versus focus on equitable access for individuals (United Kingdom).

Cross-country comparisons invite to further thoughts. One is that societies and governments in countries outside the group of wealthiest economies may aspire to a fair access to therapies for patients suffering from RDs, but the learning curve to achieving the access goals is long and complex. Another one is that there is a real opportunity for international exchange of thinking and best practice to support health systems along this learning curve; the author’s view on this is based on personal discussions with payers in developing countries, for example, in Colombia and South East Asia, which revealed a keen interest in learning from the European experience.

Budget impact of RD therapies create a real concern for payers

Estimates vary regarding the level of budget impact of RD drugs (Figure 1). Some authors argued that in the foreseeable future, it would remain small (<5% of total pharmaceutical expenditures) in Europe until the 2020 horizon. 17 Others quote somewhat higher (8%–16%) figures for the RD share of drug spend.2,17–20 The discrepancy may result from many reasons, such as what therapies are included in the RD category, what costs are considered (e.g. with or without discounts), what geographies are in scope and what assumptions are made regarding sales growth – a detailed, in-depth analysis would, however, be needed to tease out the reasons for discrepancy.

Although an authoritative and comprehensive meta-analysis of the trends in RD drug budget would be welcome, it is less defendable to claim that this impact is small enough for payers not to ignore it. For example, a 10% share of drug spent in the near future may not ‘break the bank’, but it certainly attracts attention. Of note, US private payers are clearly concerned about the issue 16 and, based on the author’s discussions with payers, similar concerns appear to exist in other parts of the world (Latin America, Asia and Europe). An implication for the pharma industry is that it is time to acknowledge the problem up front, and transparently work with payers to help them manage their legitimate concerns and uncertainty about financial impact.

Increasingly challenging price justification

Whether the price of RD therapies is justified or not is at the centre of many commentaries, some criticising potential abusive strategy to achieve high prices, such as repurposing commonly used drugs towards an RD indication, or artificially dividing a common disease into smaller, biomarker-defined categories.21,22 In the author’s experience, fair price justification is in the minds of most payers around the world. It is, however, a complex question.

The first complication is that estimates of cost per patient vary substantially, for example, the median annual cost per patient was recently quoted at £30K in one report 4 and at US$84K in another one, 2 which represents a twofold difference. Another level of complexity is that there is limited clarity about the factors that justifiably drive price differences between RD therapies. A consistent finding is that the rarer the condition, the higher the price.2,23 Obviously, when the number of patients is extremely small (i.e. for so-called ‘ultra-rare’ conditions), recouping the developer’s investment implies a high price. Also, the argument can be made that the total budget impact is truly modest, hence high willingness to pay bears lower risks.

Another driver for a high price can be the unavailability of any effective treatment for a disabling or life-threatening condition. Arguably, a genuinely high unmet need makes it more acceptable to grant a ‘higher’ price as long as the new therapy offers a patient benefit that is meaningful and not too uncertain. At the same time, lack of price benchmarks makes it difficult for payers to establish a ceiling price.

The third situation to consider is that of therapies that represent breakthrough innovation potentially leading to a cure or at least long-lasting benefits (e.g. gene therapy), some of them falling in the category of RD therapies – in that case, the reasonable expectation of a major clinical benefit and the need to reward innovation can justify a high price.

But other RD therapies do not fall into these extreme categories, making it hard for payers to accept annual cost per patient that are substantially over average. Often-quoted arguments for a higher price for RD therapies include the following: need to recoup large investment from a small number of patients; higher willingness to pay ‘mandated’ by ethical/societal principles (e.g. equity, fair innings, value of hope and rule of rescue); and ‘small’ budget impact allowing ‘flexibility’ in granting premiums. In payers’ views, all three arguments may be either debatable or may not justify a high premium, especially when considering that the clinical evidence for meaningful patient benefits is often thin because it is based on small, short trials using surrogate markers of efficacy.

Perhaps, one of the most important considerations for payers is whether the level of price and access claimed by the manufacturer is sufficiently in line with the relevance and quality of the evidence provided. Payers are well aware of the challenges of generating clinical trial evidence and can accept thinner data packages when the drug is credibly promising in an area of high unmet need. At the same time, payers need to see that an effort has been made during clinical development (and after launch) to use study designs (endpoints, trial size and duration) that can be agreeable to health technology assessment (HTA) bodies and payers, taking into account the clinical trial challenges in the particular disease area, and as can be determined through consultations with key HTA and payer bodies as an early stage of development.

With respect to this, a comparison of two recent cases from Spain is enlightening. One is nusinersen, indicated for the treatment of spinal muscular atrophy, and the other one, ataluren, is a therapy for Duchenne muscular dystrophy. Both were reviewed using the same national HTA process, but the report was more critical of the evidence in the case of ataluren, highlighting evidence limitations and methodological flaws – nusinersen was granted reimbursement in Spain, and ataluren was not.24,25 Since the cases occurred in the same country, within the same time window (10 months), and involved quite similar RDs, this suggests that the determining factor for reimbursement was the quality of the clinical trial evidence.

An implication for developers of RD therapies is that payers now demand reasonable and fair pricing, based on relevant clinical evidence of the drug’s benefits, in the context of a clear unmet need. High prices are acceptable, but only if objectively justified.

Ways forward for better market access to RD therapies

Common principles emerge to guide the way forward, despite the heterogeneity of situations across the world. The overarching concept is that of partnership. In many countries, decision makers and payers would like to improve access to RD therapies but would not be able to make good progress without input from and cooperation with the multiple actors in the RD space. As a key stakeholder, the pharma industry can play an effective role as a partner in three areas related to payers: education and support; funding and pricing; and innovative contracting.

Education and support

A prerequisite for a stable and conducive access policy to RD treatments is that decision makers are aware of, and understand, the high burden that falls on patients affected by RDs, often from birth, and what the lack of effective therapy means to these patients. Patient organisations and clinical specialists have the insight, but politicians and payers are often ignorant to this because they have many competing priorities. In the author’s experience, education of these latter groups is still very much needed, particularly in countries with less knowledge resources. The industry has a role to play in disseminating basic information about RDs, but partnerships need to progress in many geographies, supporting capabilities of healthcare systems in a range of areas (epidemiology, knowledge management, creation of coordinating networks and centres of excellence).

In addition, decision makers and payers need evaluation frameworks that can help them to prioritise the RDs they should focus on, and assess the value of therapies for these diseases. Due to the specifics of rare conditions, the conventional approaches may not work. For example, the shortcomings of applying cost-utility analysis to RD therapies have been widely commented and various ways to adapt the approach proposed. 16 Interestingly, most if not all, US private payers recently surveyed in a study admitted they were unsure of what economic assessment tools to use for RD therapies. 16 In the author’s experience, decision makers and payers in many other countries are looking for methodology appropriate for RDs. The industry has an opportunity to help healthcare systems to devise approaches that are simple enough (e.g. along the lines of multi-criteria decision analysis) and adapted to the local context, keeping in mind that there is no ‘one size fits all’ solution in decision-making.

Funding and pricing

If decision makers are willing to improve market access to RD therapies, they need to find the money and decide what price to grant to new products. These are normally routine questions, but, as highlighted above in this article, they can be particularly challenging for RD therapies. Drug developers can usefully contribute to identifying and coordinating funding sources – in China, for example, the industry co-contributes to funding RD therapies, along with charities, insurance groups and public payers. A range of funding options may be available depending on the country, but not necessarily easy to access for patients and physicians, and the industry can help by identifying and perhaps coordinating funding, within the boundaries of ethics and local regulations.

Funding is half of the problem. One of the most significant challenges for the industry is to have a pricing policy that is reasonable and justifiable to all parties. Payers, patient organisations and even clinicians are now placing boundaries to what a fair price is, especially when the competitive mechanisms to limit prices are not effective. As mentioned before, high prices are readily justifiable in some situations. In many cases, however, it is challenging to align price and demonstrated value for an RD therapy, and an early dialogue is needed between the therapy developer and the health care stakeholders to agree an acceptable evidence generation plan and identify price/budget sensitivity.

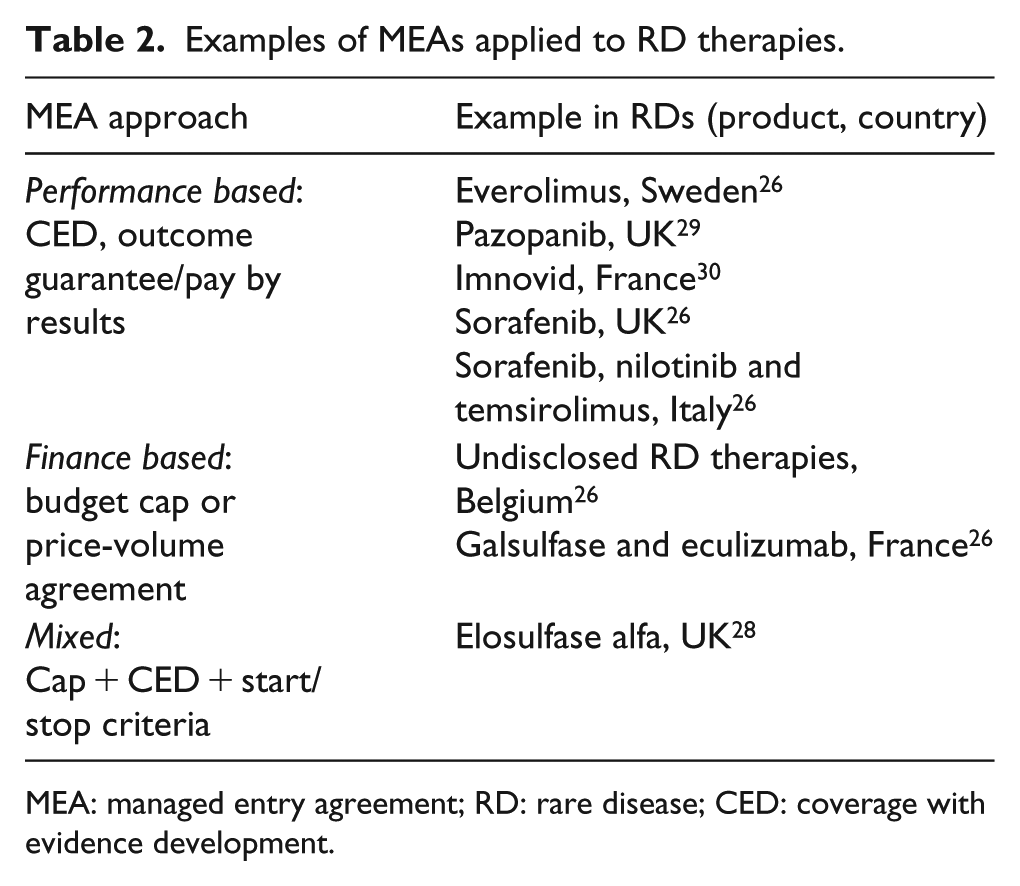

Managed entry agreements

Managed entry agreements (MEAs) struck between drug manufacturers and payers link payments to therapy’s performance observed in the real world (e.g. outcome-guarantee or coverage with evidence development), put in place financial clauses that mitigate the budget impact of the drug (e.g. utilisation cap, price-volume agreement and discounted initiation) or combine performance and financial aspects;26,27 MEAs may also include commitments to evidence generation or criteria to guarantee appropriate use. 28

These approaches are particularly appropriate to support price and reimbursement negotiations in the RD space because they address the high level of uncertainty about the clinical benefits of the therapy or concerns about its budget impact (which may be significant, as discussed previously). Table 2 provides the examples of MEAs that have been put in place for RD therapies.

Examples of MEAs applied to RD therapies.

MEA: managed entry agreement; RD: rare disease; CED: coverage with evidence development.

MEAs should be considered systematically by developers of RD therapies, where they are both fit for purpose and likely to be implementable. Let us take a typical case of a new RD product coming to market with promising but limited clinical data, and targeting patients treated in a few centres of excellence, at an expected substantial cost per patient. Implementation of a performance-based scheme is likely feasible because appropriate response parameters can be easily tracked (and even captured by default) in these centres, and cost of setting up and running the scheme is only a small fraction of the annual cost per patient. But another reason to introduce an MEA is that it can be very useful for the price and reimbursement process itself. Considering our example again, a manufacturer proposing a performance-based MEA sends a strong message that they believe in the clinical value of the product; also, the discussion with health authorities starts with a focus on product’s benefit and ways to deliver the value, instead of focusing narrowly on price from the beginning. In the author’s experience, the MEA proposal can shift the nature of the conversation, demonstrating the manufacturer’s desire to address payers’ concerns and creating a more positive mind-set and a more mutually satisfactory outcome to the negotiation. Importantly, the pre-launch, country-level discussions around MEA approaches do not negate the value for payer/HTA body consultations, at least in a few key markets, at the early stage of development.

Conclusion

There is clear scope to increase the level of access to RD therapies, hence significant commercial opportunity, in many parts of the world and particularly in large, growing economies such as China. The journey to realising the potential is long and success requires the efforts of many stakeholders, and the industry has a welcome role in transparently and honestly partnering with decision makers, payers and third parties to find the appropriate solutions. Table 3 summarises the key recommendations.

Recommendations for the pharma industry.

RD: rare disease; MEA: managed entry agreement.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship and/or publication of this article.