Abstract

This article introduces the special issue on Pay disclosure: Implications for Human Resource Management in the German Journal of Human Resource Management. Previous research largely assumed employer agency in designing pay disclosure practices. Recent legislation regarding pay disclosure in many countries and an increasing role of employees have to be considered, though. Differences in actors’ attitudes toward pay disclosure and voids in legal rules then lead to multiple perspectives on the nature of pay disclosure. Based on the articles in this special issue, we outline how these themes constitute a challenge for managing actors and an exciting research opportunity.

Keywords

Introduction

In an increasing number of organizations, pay has shed its taboo status and emerged as an important topic of discussion. Driven by ongoing efforts to close the gender pay gap and reduce income-related inequalities, organizations are under increasing pressure to enhance pay transparency. Many countries have introduced regulations requiring companies to share more detailed pay information with employees (Bamberger and Alterman, 2024; Bölingen, 2022; Von Beck and Bölingen, 2024). These regulatory demands are mirrored by internal expectations, as employees increasingly want to understand how pay decisions are made and how their compensation compares to that of others (Smit and Montag-Smit, 2018). In this evolving landscape, HR professionals must carefully manage the growing visibility of pay information—navigating between different stakeholder expectations and the mitigation of potential transparency risks (Bamberger and Alterman, 2024).

Pay disclosure, the sharing of pay-related information (Bamberger, 2023: 2), shapes stakeholders’ understanding of compensation, and influences performance on both individual and organizational levels (Brown et al., 2022). Because pay disclosure contributes to the implementation of compensation policies, it constitutes an important aspect of strategic human resource management (SHRM; Jackson et al., 2014). While sharing pay information used to be more limited, and often employers had control over pay disclosure, we currently recognize major changes: employers are opening up about pay (e.g. Arnold et al., 2018; Arnold and Fulmer, 2018) and their influence on pay communication of employees is decreasing. These trends are “consistent with ethical underpinnings of liberal, humanistic societies” (Bamberger, 2023: 22). Trends toward pay disclosure are accelerated by state interventions such as regulations that seek to combat pay inequity based on gender, most recently from the 2023 European Commission Pay Transparency Directive.

Legal forces reinforced by social expectations create an environment for HRM in which discretion over pay disclosure is no longer solely in the hands of organizations. Considerable research has developed evidence on outcomes of pay disclosure practices for different actors (e.g. Bamberger, 2023; Brown et al., 2022; James and Bryant, 2024; Park and Bryant, 2024). However, what has received less attention is how multiple actors in pay disclosure, such as employees, HR professionals, managers and government representatives, are handling, adapting to and grappling with this changing context and what consequences their responses have—for their own aspirations as well as for those of other stakeholders.

The introduction to this special issue aims to stimulate a debate about research opportunitites that emerge from the decrease in the discretion of employers over pay disclosure, contextual factors and changes to regulations. We present scholarly articles as well as reflections of practitioners that bring attention to themes that are likely to challenge established practices of pay disclosure and call for further investigation. We believe that the articles in this special issue provide inspirations for new and neglected phenomena of studying of pay disclosure.

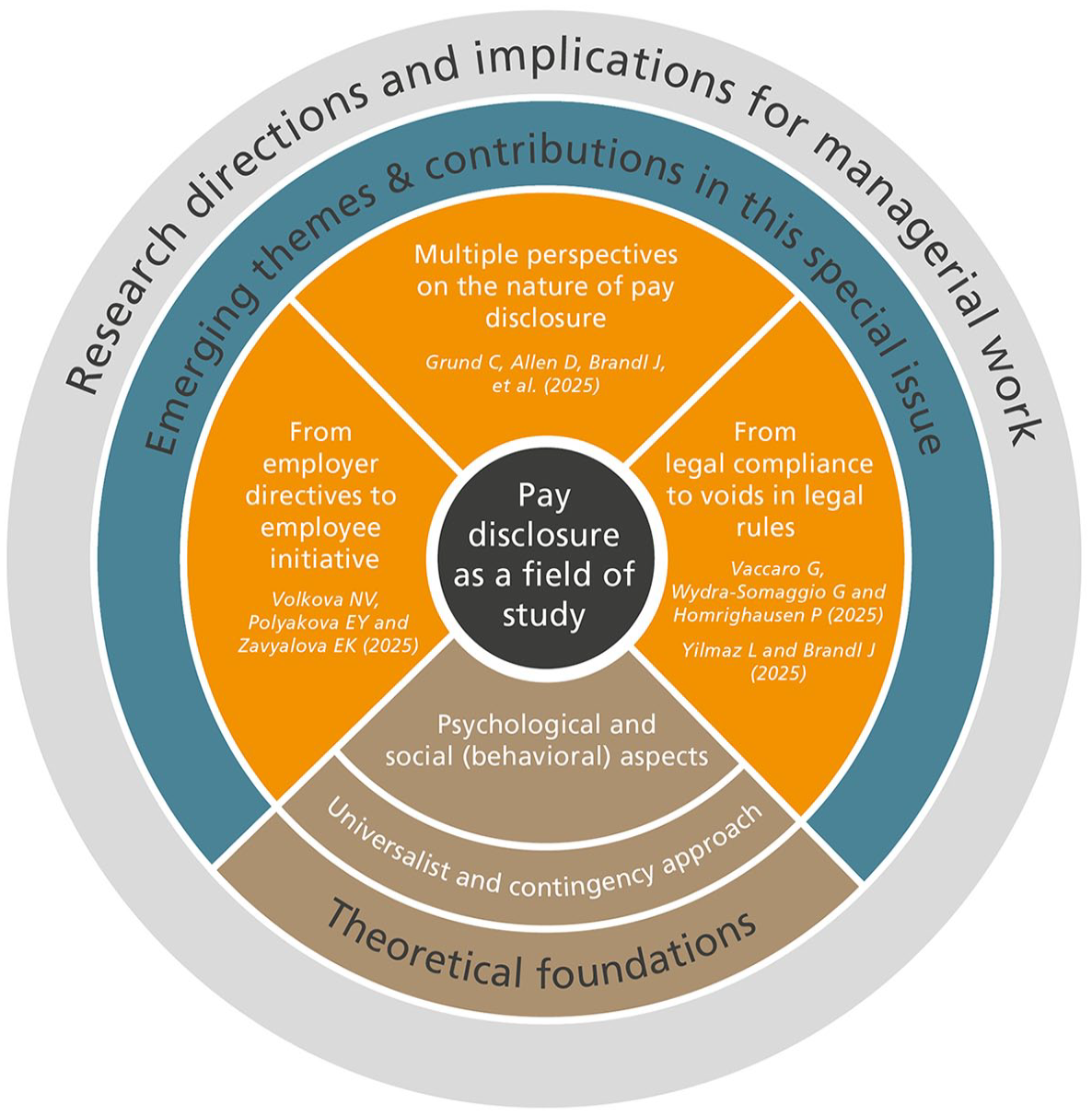

We begin by revisiting current foci for studying pay disclosure for contextualizing our arguments. We note that much current research on pay disclosure has been informed by organizational behavior and applied labor economics traditions, modeling relationships between disclosure practices and employee reactions and sometimes connecting these reactions to employer goals. While we are convinced that there is much more to know about these relationships, we believe that pay disclosure research should make more efforts to go beyond these themes. Since pay disclosure decisions are not made in a vacuum, it is particularly necessary to attend more to the circumstances under which different actors, such as employees, HR professionals, managers and government representatives, position themselves concerning pay disclosure. Recognizing that discretion of employers over pay communication is declining, we identify three inter-related themes that we explore in this special issue: increasing initiative of employees in pay disclosure, multiple perspectives on the nature of pay disclosure, and voids in legal rules. We show how the contributions of the four articles in this special issue contribute to exploring these themes and outline their implications for research as well as for managing actors. We conclude that these themes offer inspirations for empirical phenomena worth studying. These considerations are illustrated and summarized in Figure 1.

Summary of considerations in this article (own source).

Studying pay disclosure

As a field of study, pay disclosure constitutes part of the sets of practices within HRM, the management of labor and employment relations in the firm (Boxall and Purcell, 2000). HRM scholars analyze how practices of managing pay-related information emerge and how they contribute to the development of employment relations. Pay disclosure involves different actors participating in the employment relationship as outlined above. Most scholars agree that the legitimacy of pay disclosure as a field of research is in part also related to the potential to develop knowledge that is useful for practitioners (Aguinis et al., 2022; Banks et al., 2016; Deadrick and Gibson, 2009). Useful knowledge commonly involves definitions what pay disclosure involves and what outcomes specific pay disclosure practices can have. For example, definitions describe what pay elements (e.g. base pay, pay increase, variable pay elements) can be disclosed, what mechanisms for determining pay can be shared and how much freedom employees can have to display their own pay (Arnold et al., 2024). When these elements are combined in ways that facilitate sharing of pay-related information, this can be seen as an indicator for pay transparency (Brown et al., 2022). Studies on pay disclosure can use a universalist theoretical foundation assuming that pay transparency leads to better organizational outcomes or a contingency, context-sensitive foundation, specifying the conditions under which a certain pay disclosure practice is possible and linked to particular outcomes. Importantly, research on pay disclosure often has a normative character: by modeling relationships between pay disclosure and possible outcomes, scholars go beyond description by clearly advocating what pay disclosure practice should exist. The normative character of pay disclosure research becomes visible when scholarly knowledge is turned into guidelines for practitioners.

The above features help to reflect the foci of current pay disclosure research. The management of employment relations as a context of research implies that a variety of fields can be used for theorizing. Contributions come from the field of organizational behavior, strategic management, applied labor economics, industrial relations and critical management, albeit to different degrees. The normative character of pay disclosure scholarship should encourage us to ask who should benefit from this research, and explore how practititoners can become more effective based on this knowledge.

Pay disclosure and employee reactions

Psychological and social behavioral aspects of pay disclosure have received considerable attention in the domain of organizational behavior. Earlier research has explored how employees form their perceptions of pay levels in organizations under the condition of limited pay disclosure. In the 1960s, Lawler (1965) conducted field studies focused on employees’ perceptions of pay and how well they matched “reality”, and demonstrated that while employees tend to overestimate pay of peers they underestimate pay of superiors. Lawler also argued that this distorted perception can have a negative impact on motivation and employee retention. In subsequent years, other studies replicated and expanded Lawler’s research. Milkovich and Anderson (1972) replicated Lawler’s findings and showed that even in organizations with less restrictive pay communication, where employees had access to information about salary ranges and average salaries in their own pay grade, similar perceptual distortions occurred. Subsequently, a study by Futrell and Jenkins (1978) documented work satisfaction and performance increasing effects among salespersons following disclosure of pay. Consequently, this research fueled research advocating for increased pay disclosure.

More nuanced perspectives on the effects of pay disclosure have emerged from more recent research. Although empirical studies have drawn on a range of theories (see Bamberger, 2023: 39–52 for an overview), much of this research builds on equity theory (Adams, 1963), suggesting that responses to pay disclosure are driven by fairness considerations rooted in social comparisons. For example, Colella et al. (2007) argued that in the absence of pay information, employees develop negative perceptions of procedural and informational fairness. These negative perceptions would then become the basis for adverse distributive fairness judgments. Overall, this research seems to suggest that, whereas for some employees pay disclosure may have positive motivational effect (e.g. Belogolovsky and Bamberger, 2014), for others pay disclosure may result in perceptions of unfair treatment in pay and lead to negative reactions such as lower job satisfaction, less helping behavior, lower organizational commitment or higher counterproductive work behaviors (Bamberger and Belogolovsky, 2017; Scheller and Harrison, 2018; SimanTov-Nachlieli and Bamberger, 2021; Stofberg et al., 2022). This can be relevant in particular if the majority of employees considers themselves as top performers (Grund and Soboll, 2024).

The mixed findings on the effects of pay disclosure on employee attitudes and behaviors have stimulated two developments. First, they spurred empirical studies on individual characteristics (e.g. preferences, uncertainty tolerance, position in the compensation hierarchy, gender) which can explain variation in reactions to disclosure practices across employees (Göbel et al., in press; Heisler, in press; Scott et al., 2015; Smit and Montag-Smit, 2018). The introduction of compensation activation theory (CAT; Fulmer and Shaw, 2018) helped to explain person-based differences in reactions. Second, mixed findings led to postulating a multi-dimensional nature of pay disclosure. This research recognizes that pay disclosure practices are not limited to information about actual pay levels, but also involve disclosure of rules underlying compensation-related decisions and the restrictions for employees to communicate their own pay, and thus allows provide a more detailed picture of what pay disclosure options managing actors have (Arnold and Fulmer, 2018; SimanTov-Nachlieli and Bamberger, 2021).

Since studies on employee reactions to pay disclosure commonly use laboratory experiments or student samples, research faces challenges in terms of transferring insights to populations in practice with greater complexity of pay system and pay disclosure. More fundamentally, this research leaves unanswered how practitioners could respond to changing context of pay disclosure and how they can make choices between disclosure options. This means it provides limited guidance for organizations in terms of management of pay disclosure.

Management of pay disclosure

While research on employee reactions to pay disclosure remains dominant in pay disclosure studies, a second line of research addresses more directly questions of pay disclosure in relation to managing actors. The work that we subsume here contributes to the domain of SHRM, which is “concerned with the strategic choices associated with the use of labor in firms and with explaining why some firms manage them more effectively than others” (Boxall and Purcell, 2000: 185). Assuming that managers make decisions on behalf of their organizations, their choices on pay disclosure matter for organizational outcomes as well as for key challenges that HR professionals face in implementing pay disclosure.

Broadly, two main approaches of managing pay disclosure emerge from the literature. Both approaches offer a theoretical foundation for managerial activities on pay disclosure but have different premises about work organizations. The first assumes a unified work organization, where desirable outcomes for both employees and employers can be achieved if communication supports pay disclosure. In contrast, the second assumes that (economic) interests of involved actors can diverge, leading to tactical behavior of actors and, depending on the context, resulting in lower (pay secrecy) or higher (pay transparency) pay disclosure. As SHRM research is often classified into universalist and contingency approaches (Martín-Alcázar et al., 2005), the first may be roughly characterized as a universalist approach, whereas the second has affinities with contingency approaches.

Universalist approach

The universalist approach focuses on how compensation systems, policies and practices can lead to better organizational performance by enhancing pay disclosure. This approach links psychological and social behavioral aspects of pay disclosure and insights from communication of HRM policies for understanding organization-relevant outcomes. The main arguments are that communication quality makes HRM practices visible, understandable to employees, and therefore, closes the gap between intended HRM practices and their perception (Den Hartog et al., 2013; Piening et al., 2014; Sanders et al., 2021). Considering that many organizations design their compensation systems to influence employee behaviors with strategic intent (Jackson et al., 2014), it becomes important that employees understand how compensation works. Thus, it has been argued that greater pay disclosure can help to improve employee understanding of compensation systems, increase their perceptions of fairness, boost motivation, and reduce information asymmetries and misunderstandings (Fulmer and Chen, 2014).

In view of these positive views on increased pay disclosure, research has focused on how change from pay secrecy to pay transparency can be accomplished (Avdul et al., 2024; Bamberger, 2023; Heisler, in press; Trotter et al., 2017). For example, Bamberger (2023) identifies the steps in which organizations with ambitions to increase pay disclosure should communicate particular features of their pay policy. Accordingly, organizations should begin with removing all restrictions of employee rights to disclose (pay communication transparency). Then they should disclose the rules for compensation and how the firm tries to compensate for the job, qualification of the job holder and/or performance (pay process transparency). Finally, organizations should share position-based pay, first in aggregate and later for each job with the job holder (pay outcome transparency). This order of disclosure is more likely to mitigate potentially negative employee reactions to pay outcome transparency, because understanding of the compensation system may result in fairer perception of outcomes (Bamberger, 2023; Brown et al., 2022).

Fulmer and Chen (2014) explore specifically how a communication strategy should look to foster positive employee reactions to pay information. They suggest several features of communication that could lead to desirable employee reactions such as consistency of communication across organizational units, alignment with the organization’s compensation philosophy or availability of two-way communication channels (e.g. discussions with line managers). The crucial role of line managers calls for managerial training on dealing with employee inquiries, ensuring consistent pay decisions, and preventing envy or discord in the workplace. Thereby organizations could address employee concerns before they escalate into dissatisfaction or turnover.

Since the approaches more or less explicitly advocate that organizations will be better off if they disclose pay openly if they implement it in the right way, this begs questions of why we observe a relatively limited diffusion of greater pay disclosure in practice (Arnold et al., 2018). It may be argued that the focus on pay communication in previous research overlooks possible issues within the compensation systems themselves. Compensation systems in practice are often evolving and address ad-hoc challenges (Brandl and Güttel, 2007) rather than resulting from a well-designed compensation strategy, as the universalist approach positions it. Actual pay practices may also include systematic discrimination that requires reviewing the compansation system and its implementation for exemptions and revising it (Avdul et al., 2024; Heisler, in press). Consequently, organizations need to invest in their compensation systems before they move to greater pay disclosure, which seems an often-underestimated challenge. Thus, the underlying costs may cause organizations to abstain from actively striving for pay disclosure.

Contingency approach

The second approach is concerned with alternative strategies toward pay disclosure. It assumes that actors of the employment relationship not only have to bear costs but also benefits from pay secrecy and that there are contingencies which shape their preferences for arrangements in the pay disclosure continuum. The emphasis on benefits-costs assessment and tactical behavior is rooted in liberal models of employment relations associated with labor economics. For example, Brown et al. (2022) propose a theoretical framework based on information asymmetry theory which helps to analyze different arrangements. The assumption is that actors in pay disclosure (e.g. employees, employers) may have a variety of interests with regard to pay disclosure. When employers’ interests diverge from those of employees, this leads to instable situations (called disequilibrium), which spurs efforts from actors to find an arrangement where interests are aligned (equilibrium). This action-reaction scheme explains dynamic shifts from pay secrecy to pay transparency (and the reverse; Brown et al., 2022). Although information asymmetries are modeled with two actors here, the problem of diverging interests could be even more relevant in settings with multiple actors, for example, different employee groups such as women or minorities (Bamberger, 2023).

Assuming that employers typically hold more information about pay processes and actual pay levels than employees, Brown et al. (2022) argue that employers can control what pay-related information is available to employees. This imbalance creates a situation where employees’ interest in fairness is violated, pushing employers to take action toward aligning their interests with employees. Employers can reach alignment by increasing transparency about compensation levels and rules. Doing so can improve employee perceptions of fairness and trust in the employer, potentially leading to higher job satisfaction and retention. Alternatively, employers can use selective disclosure to maintain benefits for themselves that arise from information asymmetries. For example, by withholding certain pay details, they can pursue their interest to prevent internal conflicts or avoid setting expectations that all employees will receive similar pay adjustments. However, as Brown et al. (2022) note, situations with asymmetric information are generally unstable, and sustaining them requires power. Where this power comes from and how it informs dynamics constitute potential for future research.

The disclosure strategy – selective disclosure or transparency - depends on critical contingencies of employers. Selective disclosure can be more important when employers are concerned about competitive advantage—withholding relevant information about compensation levels and rules is believed to protect from turnover and increases in hiring costs. Furthermore, it can prevent conflicts among employees and account for privacy of employees. Transparency can be more important when employers wish to signal to employees their contributions and rewards (as in internal labor markets) and build credibility to outsiders (which can be a costly signal according to Brown et al., 2022). Depending on which of these contingencies becomes salient for employers, different pay disclosure policies (e.g. setting confidentiality regulations in employment contracts, limiting communication to a minimum by, e.g. providing only general information or average pay for positions) can be rational for actors.

The contingency approach is consistent with research that shows the mix of positive and negative findings of pay disclosure. For instance, Montag-Smit and Smit (2021) find that a positive relationship between pay disclosure and trust depends on employees’ sharing preferences and their perceptions of the employer’s motives. The contingency factors can be useful to analyze patterns in the actual variation of pay disclosure policies across organizations and employee groups. Like other contingency approaches, such factors may also be used for guiding decision-making. Understanding management’s critical contingencies in the current situation and managerial priorities for keeping or lowering information asymmetries becomes crucial in such an approach, as well as projecting the downsides that managers need to deal with in a chosen approach.

Why a new look?

As indicated in the previous section, there is a tendency in much current pay disclosure research to assume that employers have substantial discretion to develop approaches for pay disclosure in order to realize their interests, especially for business outcomes. Thus, current approaches fit with a governance model where discretion over managing pay disclosure is concentrated within single work organizations and where managers can unilaterally choose how to design these practices, with a limited attention to the role of employees and that of the state. However, HRM scholars recognize growing limitations of employers’ discretion (Boon et al., 2009; Jackson et al., 2014). Thus, the premise of employers’ discretion over managing pay disclosure becomes questionable when the state takes a proactive role and employees operate independently from employers’ directions.

Governance of pay disclosure has become more complex today and has led to additional empirical phenomena that are worthwhile studying. First, laws for pay equality, cultural change and online platforms increasingly empower employees to decide about their personal pay communication independent from employer rules. For instance, the 2023 European Commission Pay Transparency Directive (EU pay directive 2023/970) requires organizations employing over 100 employees to adopt pay transparency measures by June 2026. These developments are accompanied by the increasing role of salary benchmarking platforms such as Glassdoor (Carter et al., 2023; Cullen, 2024). Second, practitioner insights reveal that there is a plurality of ways for managing pay disclosure that differ not only in directions (i.e. transparency or secrecy), but more fundamentally in the nature of managerial work. Finally, organizations have responded to laws in varied ways, sometimes undermining the interest in promoting equal pay, thereby pointing to voids in legal regulations (Seitz and Sinha, 2023). In the following, we outline these themes, position the four articles in this special issue within these themes, and discuss what the themes imply for management practice and research.

From employer directives to employee initiative

Management’s influence on employee pay communication is increasingly constrained, and disclosure often cannot be requested nor restricted to support management activities. Theoretically, employers could uphold information asymmetry with employees by holding back information about their pay levels and structure, requiring employees to keep their own compensation secret or requesting applicants to open up their personal pay history and expectations. Practically, though, even in pay secrecy contexts, employees can breach pay secrecy rules and share pay information with colleagues (Denice et al., 2025). Thus, managerial challenges related to pay disclosure cannot be solved by mandating pay secrecy as new issues arise from such actions.

Pluralist perspectives of workplace governance postulate that understanding management of the employment relationship requires consideration of employee interests independent from employer interests (Edwards, 2008). Employee behavior is not just a response to managerial policies, but socially embedded. Thus, what pay disclosure means to employees in terms of attitudes and behaviors requires consideration of the broader context. First, social norms around pay disclosure and technological advancements are supporting transparency. For example, Cullen and Pakzad-Hurson (2023) found that younger workers are more comfortable discussing salaries than more senior ones. Where confidentiality regulations in employing organizations prohibit pay communication, online platforms facilitate exchanging pay information anonymously. Online platforms like Glassdoor or Kununu have not only democratized access to pay information but also established mechanisms that encourage employees to share their personal salary information. Brown et al. (2023) argued that willingness to supply personal information can be influenced by the amount and quality of information that online platforms offer to users during the first interaction. A priori information about pay elements helps users to decide about information sharing, because users are able to recognize the usefulness of potentially sharing their personal information. Moreover, online platforms try to attract paying users by emphasizing confidentiality, actuality, quality, and quantity of pay information.

Besides, in many jurisdictions, employers’ rights to demand pay histories from job applicants have been restricted in order to combat the reproduction of pay inequities based on gender and race (Avdul et al., 2024). The EU pay directive 2023/970 states that employers must not ask job applicants about their pay level in current or previous positions with other employers (Art. 5 para. 2). This challenges employers’ ability to gage whether a candidate’s expectations align with the organization’s compensation structure or anticipate the candidate’s productivity. While employers are less and less able to request information on pay from applicants, we note that sometimes applicants voluntarily display their pay expectations to employers. Motives for this behavior can be self-protection and uncertainty reduction (Colella et al., 2007; Lind and van Den Bos, 2002). By sharing their expectations, applicants signal their perceived market value, which can protect them from being underpaid. In addition, applicants may want to signal that they are open and honest and expect the employer to reciprocate, in order to reduce uncertainty and establish fairness in the negotiation process.

Contribution of this special issue

The contribution by Volkova et al. (2025) in this special issue develops this line of research by examining the likelihood that job candidates choose to disclose their expectations regarding pay in their resumes. Volkova et al. draw on signaling theory to study how individual characteristics distinguish job candidates who disclose versus do not disclose pay expectations as well as the salary amounts that are disclosed. Using a unique sample of more than 26,000 resumes posted to an Internet job board operating in the Commonwealth of Independent States, the authors found evidence that applicants who were less educated, less experienced, female, and older were more likely to disclose pay expectations, and speculate that perhaps applicants with traditionally greater labor market power (educated, experienced, younger men) might be more eager to engage in pay negotiation with prospective employers. Those who disclosed expected to be paid above the prevailing average salary; however, those with higher human capital and mobility expected relatively higher pay, whereas those from groups that have experienced more labor market stigma, women and older applicants in this case, expected relatively lower pay. The findings can be interpreted as reduction of uncertainties and protection from underpayment are more common among applicants with lower labor market power.

The restrictions for employers to collect pay information from candidates also has implications for managerial practice. Employers have used pay history as a proxy for the applicant’s skills, experience, and performance in previous roles and often assume that higher past compensation reflects higher productivity or value in the labor market, thus helping them gage whether the applicant is worth a similar or higher wage level in their organization. This helps employers mitigate risks in hiring decisions by aligning compensation offers with perceived productivity based on past earnings (Brown et al., 2022). Limited access to pay history challenges this practice. This is not merely a problem of calculating an appropriate pay level for those candidates where pay history information is not available. Instead, it invites employers to consider the motives of applicants for communicating pay in negotiation processes. This also requires ethical considerations, ensuring that employers do not inadvertently perpetuate inequalities.

Multiple perspectives on the nature of pay disclosure

Scholars have noted that transparency is controversial as a target of managing pay disclosure. The focus on the transparency-secrecy continuum in much research, however, has overlooked that there is a plurality of approaches to managing pay disclosure rather than one single template. For broadening our understanding of the nature of these approaches, we need to take a closer look at the perspectives of practitioners who are involved in managing pay disclosure. We therefore decided to invite practitioners from Germany, Austria, and Switzerland to contribute to this special issue. The task that we gave them was to describe the important challenges for the organization they work for in terms of pay transparency and include personal experiences and reflections.

Contribution of this special issue

In this special issue we curated a Practice Forum (Grund et al., 2025) where we included the contributions from five practitioners. Our (admittedly selective) engagement with practice gives hints that there are several perspectives for managing pay disclosure that make different assumptions about ends, process and activities of actors. For example, Caroline von Kretschmann, managing director of a family-run organization in the hospitality sector, describes her target of pay disclosure as “balancing,” in which she underscores the value of both, secrecy and openness. An important consequence of this perspective for her is to navigate tensions in order to facilitate learning and development. Patrick Mollet, co-owner and director of Great Place to Work Switzerland, indicates pay disclosure requires alignment with the HR strategy, and sees pay transparency as linked to high levels of trust between management and employees, as well as among employees themselves. Therefore, Mollet advocates a link between pay disclosure with employee empowerment and autonomy. In contrast, Ingrid Moritz’ reflection her involvement in developing the Austrian transparency regulation emphasizes conflicting interests between employee and employer representatives. Her account shows how the involved actors mobilize these interests for negotiating a policy. While this regulation was labeled pay transparency law, it did not include her requirements for lowering information asymmetries.

Overall, the accounts from the Practice Forum hint at varied conceptualizations of pay transparency, differing from categories that pay disclosure scholars commonly use. Moreover, disclosure practices are maybe less the outcome of rational processes (and cost-benefit assessments like in the contingency approach) than reflecting power differences and/or worldviews of managing actors (Neyland, 2007).

A fundamental challenge for practitioners who are committed to transparency is that the conceptualization of transparency itself is not fixed but moving. For example, the EU pay directive 2023/970 goes substantially beyond the pay disclosure laws in Austria and Germany in defining compensation structures and rules. It states that pay not only refers to base salary but also includes supplementary and variable components such as bonuses, overtime compensation, travel allowances, housing and meal allowances, training and education allowances, redundancy payments, statutory sick pay, statutory compensation, and occupational pensions. Component specific pay disclosure can then make the origins of possible inequalities such as gender pay gaps more transparent (Grund, 2015). If transparency becomes a moving target, the once defined measures lose legitimacy with time, and managers may face expectations for continuously adapting them. It is important to note that transparency is an ideal. It can never be fully achieved, particularly in complex societies, but may rather be a starting point for reflecting demands to management (Stehr and Wallner, 2010).

From legal compliance to voids in legal rules

The role of the state as a relevant actor for pay disclosure of work organizations is widely acknowledged. The influence has been traditionally conceptualized by the way of legal obligations that employers need to comply with. The focus on compliance remains useful for studying the diffusion of pay disclosure practices. However, since recent work indicates that regulations do not produce the same results wherever they are applied, we suggest paying more attention to voids in legal rules.

According to Reynaud (2002), pay-related regulations from governments are often vague and employers need to interpret them when they adopt these regulations. Their effects therefore depend on the circumstances of the setting in which employers are located. Moreover, legal rules can be implemented without substantially changing the organization’s current pay disclosure practice. Different from the notion of legal compliance, this suggests that no uniform adoption of a particular rule can be expected. Paying attention to such potential voids opens up pay disclosure research questions on explaining variations in handling of regulations and in analyzing the (lack of) effectiveness of regulations. For example, Göbel et al. (in press) investigate how employer inaction in response to the pay disclosure affect employees’ attitudes and behaviors, showing negative effects on organizational citizenship. Other research hints at explanations of variability of effects in the constitution of legal rules. Meta-analysis (Bölingen, 2022; Von Beck and Bölingen, 2024) reveals that, while pay transparency laws weaken gender pay differences, some laws are more effective than others. They are more effective when more specific information is communicated and when more broadcasters are required to communicate pay information.

Contribution of this special issue

Two studies in this special issue contribute to our understanding of the effects of changes of legal environment impact pay disclosure practice. The study by Vaccaro et al. (2025) in this special issue suggests that institutional support is crucial for the effective implementation of laws for reducing pay disparities. The authors study the German case and focus on the potential effects of the implementation of the Pay Transparency Act (Entgelttransparenzgesetz, ETG) on gender pay gaps. The ETG provides for employee rights to information about remuneration paid to peers for organizations with more than 200 employees. Based on an examination of establishment data of the German Institute of Employment (IAB) before and after policy implementation, they highlight the importance of works councils and collective bargaining agreements for advancing pay equity. This fills a gap in existing research, since only a few studies have examined the interaction between pay transparency laws and organizational structures before (see Lyons and Zhang, 2023 for an example).

While the study by Vaccaro et al. points to the relevance of institutional support by local actors for reducing gender pay disparities, Yilmaz and Brandl (2025) investigate how employees adjust their pay expectations depending on the formulation of pay in job announcements, which is mandatory for employers in Austria since 2011. Their experiment shows that expectations about pay rates are contingent on pay communication practices. Yilmaz and Brandl’s study provides evidence that salary ranges are an effective tool for reducing gender differences in pay expectations, while other pay disclosure practices, such as stating starting salary with negotiation options, are less effective. Ironically, the latter is widely diffused in Austria and recommended to firms by the Austrian employer association (WKÖ). This study resonates with research that men are better positioned to deal with ambiguity in pay information than women (e.g. Exley et al., 2020; Leibbrandt and List, 2014) and adds that pay ranges may offer a solution for reducing gender pay disparities.

The studies contribute valuable insights to the ongoing debate about how pay transparency laws can be designed and implemented to address the gender pay gap. Art. 5 of the EU pay directive 2023/970 stipulates that job applicants have the right to receive certain information from the future employer. This information relates to the starting salary or salary range, both of which must be based from the outset on objective and gender-neutral criteria, and, where applicable, the relevant provisions of the collective agreement that the employer applies to the advertised position. This formulation includes considerable space of interpretation and gives leeway to varied practices. Since the effectiveness of the rule for addressing gender pay disparities depends on the adopted practice, national governments should promote the interpretations of the directive that support effective implementation. For HR professionals, this may necessitate a reevaluation of compensation systems and a closer collaboration with work councils or other representative bodies of employees.

Future research avenues

The shift from employer directives to employee initiative for disclosing pay opens up several questions for research. Related to application processes, for instance, how do employers try to overcome information asymmetry in hiring? How do they estimate the worth of candidates when pay history information is not available for some candidates? What other signals do they assess when pay history becomes unavailable? What impact does the pay expectation disclosure have on the likelihood of obtaining jobs and on salary negotiations? More research is also needed regarding the role of online platforms like Glassdoor or Kununu. Research that addresses how platforms engage users and what kinds of exchange relationships they promote as part of their business models is particularly desirable. Research is also needed to understand how online platforms inform pay negotiations between employees and employers.

Another important theme for future research will be to develop a better understanding of the factors that shape the development of pay disclosure practices and their dynamics. To this end, it will be important to explore unique profiles of firms, as illustrated in “Tales from the trenches” (Bamberger, 2023), but also to identify patterns across cases and the evolution of arrangements. To this end, scholars need to see management activities and problems in different ways beyond what universalist and contingency approaches suggest. They may examine varied theoretical perspectives to explore the multiple facets of managing pay disclosure and question basic assumptions. More fundamentally, scholars need to decide whether they see their role in conceptualizing transparency and developing pay transparency measures or whether they want to examine how the understanding of transparency is evolving.

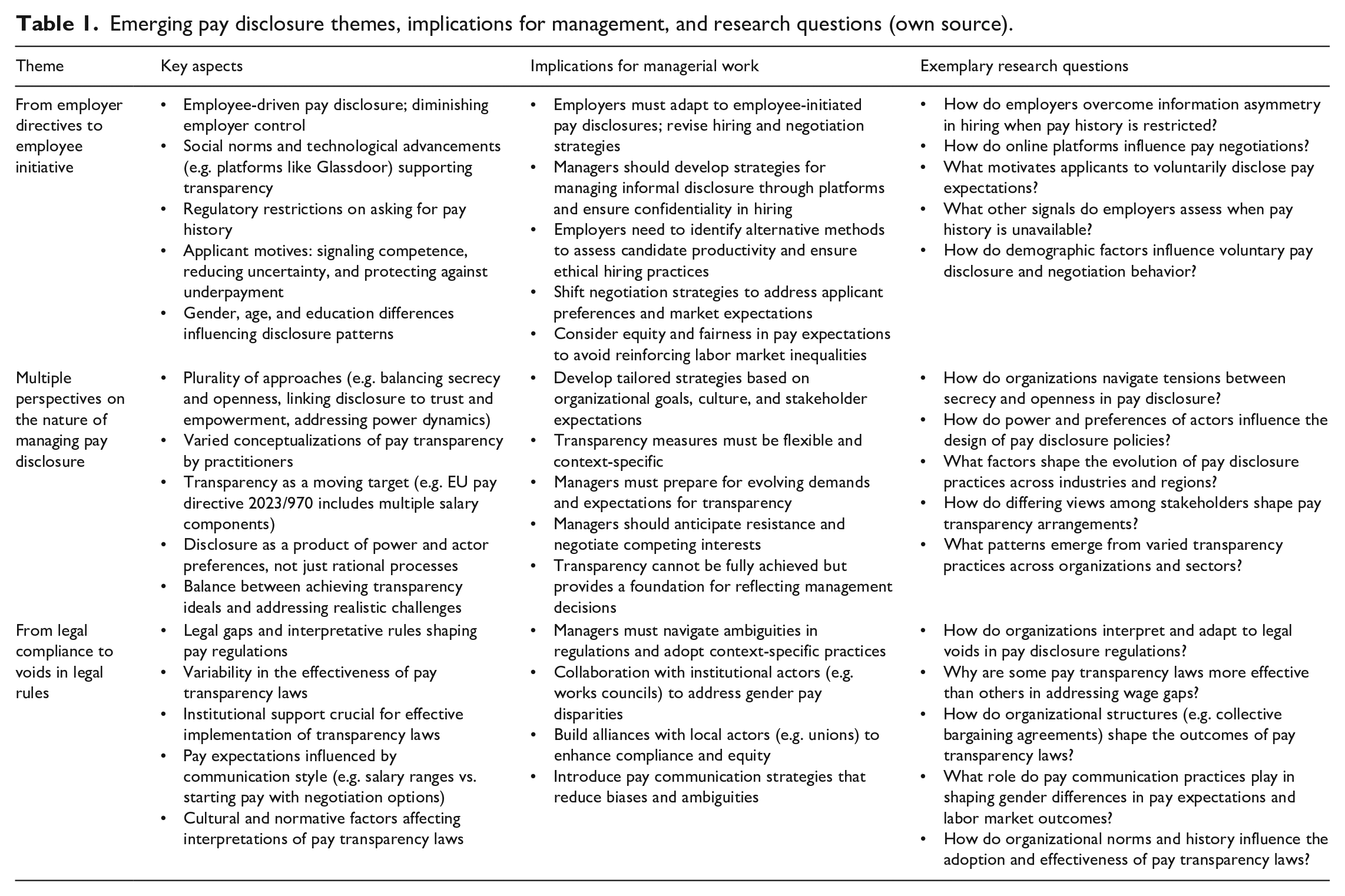

Finally, a promising theme for future research is to expand the study of the factors that contribute to the interpretation of legal rules. In addition to the role of local actors, we see particular value in exploring how norms and history matter for the specific adoption of pay transparency laws in organizations. And it would be interesting to analyze if laws could help to identify weaknesses in compensation systems and lead to changes in these systems. Emerging pay disclosure themes, implications for management and research questions are summarized in Table 1.

Emerging pay disclosure themes, implications for management, and research questions (own source).

Conclusion

The scope of managerial actors for developing pay disclosure practices is very much shaped by socio-political and cultural contexts. Therefore, changing contexts are likely to affect the effectiveness of disclosure practices, stimulate new practices and could lead to evolving dynamics. Much current research on managing pay disclosure assumes a context where organizations (and the managers who are responsible for pay disclosure) are free to design pay disclosure strategies depending on specific business goals and the employee behavior required to achieve these goals. However, pay disclosure is increasingly happening in a different context, where technology, equal-pay regulations, and social norms that promote transparency put considerable pressure on employers, especially when employers want to keep their pay structures and rules secret and attempt to regulate pay communication of employees. As employees become more proactive in communicating their personal pay, as governments impose stricter requirements and perspectives of involved actors diverge, the implications for managing pay disclosure have become profound.

This contribution reflects on the implications of this social context for managing pay disclosure in practice and for doing research. The articles included in this special issue make new ground by investigating phenomena that are linked to self-disclosure of employee, regulatory voids and managing approaches. We emphasize the need for continued research to navigate this complex terrain. To fully look into these themes, the special issue will hopefully inspire scholars to generate further research.