Abstract

Pay transparency, or the disclosure of pay information to workers, is a topic that is both old and new. The debate over whether pay information should be kept confidential or openly shared can be traced back to the 1960s. During that era, marked by significant social and civil rights movements, issues of discrimination and inequality were prominent topics of discussion. An illustrative example is the United States’ enactment of the Equal Pay Act of 1963, which stipulated that workers should receive equal pay for equal work. To uphold this worker right, it was imperative to enable employees to have information on how others, especially those in similar roles, are paid. Given that decisions regarding workers’ pay were under organizational managers’ discretion (with exceptions like minimum wages and social welfare), it was important to inform managers about possible effects of pay transparency.

In line with this context, management scholars investigated the consequences of pay transparency. For example, Futrell and Jenkins (1978) open their research article by stating that “most sales managers contend that peer pay information should not be disclosed to their salesmen (p. 214)” and after presenting some data, they concluded that “the administration of salesmen’s pay in a more open manner has a positive impact on salesmen’s job performance and their satisfaction with pay, company promotional policies, and work” (p. 218). Other researchers investigated the reason for why pay secrecy leads to low satisfaction and performance (Lawler, 1965, 1967; Milkovich & Anderson, 1972). For example, Lawler (1965, 1967) found that the negative effects stem from managers tending to overestimate their subordinate or peers’ pay levels while underestimating their supervisors’ pay levels. However, research on pay transparency also revealed a nuanced perspective. Schuster and Colletti (1973) surveyed professional employees in a large organization and found that “the respondents divided about equally regarding preferences for pay secrecy” (p. 39).

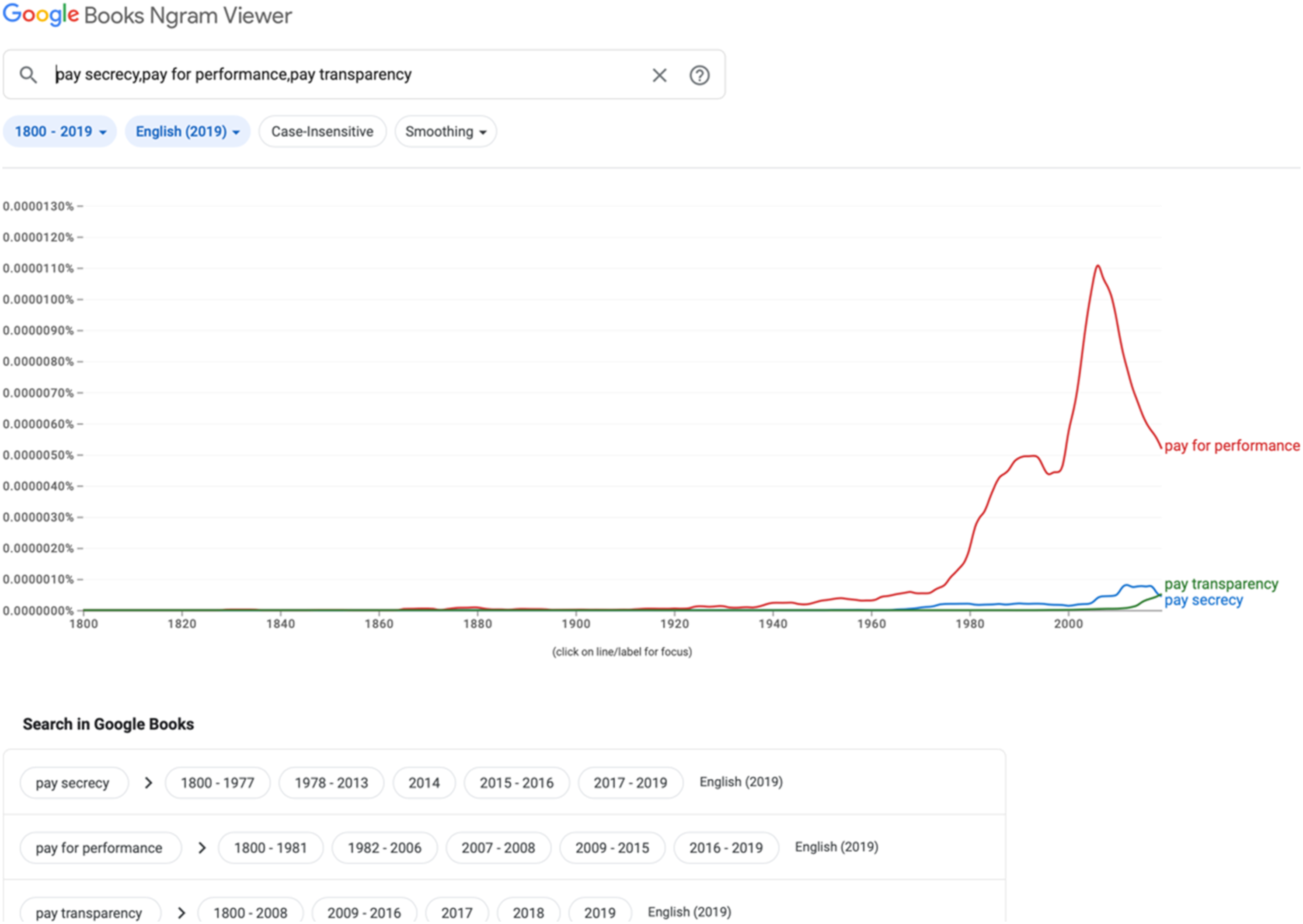

However, the discussions concerning pay transparency did not advance further after the 1980s. Although it is difficult to know exact reasons behind the limited advancement of these discussions, a reasonable guess could attribute it to the rise of pay-for-performance, or incentives practices in workplaces. As shown in Figure 1, the term “pay secrecy” (the blue line) increasingly appeared from the 1960s, but the term’s usage did not increase at all during the 1980s until the 2000s. Instead, the usage of the term pay-for-performance increased dramatically from the 1980s until the 2000s. Interestingly, in the 2000s, the trend reversed to some extent such that the term pay-for-performance became less frequently used, whereas the usage of pay transparency increased during the same time (the green line in Figure 1). “Pay-for-performance” and “pay transparency” term usage from 1800 to today.

What happened in Korean organizations after the 1997 financial crisis also hints at a possible association between increases in pay-for-performance and decreases in pay transparency. In South Korea, like many other Asian regions, worker payments were mainly determined based on their seniority rather than job functions or individual performance. Accordingly, pay information was not secret because employees were able to figure out how much others are paid by referring to the wage table that shows wage rates for levels of seniority. However, when the financial crisis happened in 1997, many Korean organizations made the transition from a seniority-based pay system to a performance-based pay system. This change was partly motivated by their financial budget concerns stemming from the (automatic) wage increases by seniority. In the midst of this transition, organizations also adopted a pay secrecy policy, which required all employees endorsing a salary confidentiality pledge, obligating them not to disclose their salary information to others.

This salary confidentiality pledge case in Korea shows that organizational managers might not be concerned about pay information disclosure itself; rather, their concern could stem from the disclosure combined with pay-for-performance practices. When pay transparency is combined with pay-for-performance, it may intensify the socio-emotional costs of pay comparisons. Notably, pay comparisons are not necessarily bad, as they can enhance employee motivation and retention (or sorting) (Gerhart, Rynes, & Fulmer, 2009; Shaw, 2014). However, managers are equally or even more likely to be concerned about the negative consequences of intense pay comparisons such as envious emotions, reduced cooperation and collaboration, reduced information sharing, and possibly more antisocial behaviors (e.g., victimization). Another reason for why managers were concerned about pay disclosure under pay-for-performance might be that managers can face increased burden of justifying and explaining their decisions on pay and the size of pay differentials. While in some occupations (e.g., sales), giving full explanations about how individual “performance” is defined and measured is relatively straightforward, in most other occupations, it is very difficult to define and measure individual performance. Moreover, even if “performance” can be defined and measured based on objective metrics (e.g., number of publications), it is well known that such a practice tends to cause unintended negative consequences (e.g., Park et al., 2023).

Then, why has the topic of pay transparency re-emerged as a topic for discussions (or controversy) nowadays, even though organizations keep using pay-for-performance practices? One possible reason might be that organizations have gone quite far in differentiating each worker’s pay. During the “talent war” era of 2000s, one of the popular management practices was to attract and retain star workers by paying them whatever their market values are. Despite many benefits, paying solely based on market value is effective and fair, only when labor markets are functioning efficiently, with no information asymmetry and no labor mobility costs. And we know that such conditions are frequently violated. A major concern on inefficient labor market is biases and discriminations toward minority workers. That is, workers are paid lower than otherwise their similar counterparts simply because they are less demanded on the market, for their belonging to a sexually or racially minority group. Relatedly, the issue of social and pay inequality, coupled with discrimination within the labor market, has escalated more, catalyzed by social movements such as the “me-too” movement.

Another possible reason for the re-emergence of pay transparency might be the advancements of technology, which made pay information more public. For example, nowadays it is not difficult to find pay-information-sharing websites, many of which are crowd sourced by workers who self-report their pay and work-related information. Furthermore, government policies have further promoted the discussions on pay transparency. For example, in the United States, many states have already required organizations to disclose their salary range information as part of job postings, and many other states are planning to adopt such approaches.

The dilemma organizations are facing nowadays is about how to promote pay transparency while keeping the pay-for-performance philosophy. The articles in this first of two special issues help address that dilemma. Lori Schumann’s “Pay transparency and pay communication” depicts the regulatory environments regarding pay transparency in the United States and offers suggestions for how organizations can better adapt to the new regulatory environment. In particular, Schumann gives a detailed guideline about how organizations can conduct a pay equity audit, which is very important when preparing for the adoption of a pay transparency policy. She also highlights the importance of managers’ engagement in the process and organizational culture. In their article entitled “Variable pay transparency in organizations: When are organizations more likely to open up about pay?”, authors Alexandra Arnold, Anna Sender, Ingrid Fulmer, and David Allen explore whether variable pay characteristics affect levels of variable pay communication within organizations. They found both internal factors such as variable pay characteristics and external factors such as country do affect variable pay communication. In their article, “Navigating the practical complexities of pay transparency: Implications for employers and public policy”, Peter Bamberger and Valeria Alterman not only make recommendations to organizational managers but also recommend possible pay transparency policies to policymakers. In doing so, they emphasize that pay transparency isn’t a single continuum concept; instead, it involves three different dimensions: pay process transparency, pay communication transparency, and pay outcome transparency. Another important article that should not be missed is the book review of Peter Bamberger’s recent book “Exposing pay: Pay transparency and what it means for employees, employers, and public policy.” Peter Bamberger has probably published the most number of academic research articles in the area of pay transparency, and he made a major achievement in advancing our knowledge on pay transparency in his recent book.

We are very thankful to the authors of this first special issue on pay transparency and communication for their high quality work. We had so many quality submissions on pay transparency and communication that our next issue will also be a special issue on the same topic. We hope you, readers, enjoy reading the articles in this and in our next issue as much as we did.

Footnotes

Correction (October 2023):

This article has been updated with minor affiliation corrections since its original publication.