Abstract

Due to external pressures organizations are confronted with the need to increase pay transparency and communication. However, there is limited research that has looked at when organizations are more likely to open up about pay. This study explores whether organizations report different levels of pay transparency depending on the characteristics of their variable pay systems. Using data from HR professionals at 400 organizations collected in a multi-country study, we investigated how proportion of variable pay, existence of group-level variable pay and use of objective and absolute performance criteria are associated with procedural variable pay transparency (i.e., transparency about how pay is determined), distributive variable pay transparency (i.e., transparency about actual pay levels) and variable pay communication restriction (i.e., discouraging employees from discussing pay among themselves). Overall, our results point to both external factors (i.e., country) and internal factors (i.e., variable pay system characteristics) that are associated with variable pay transparency.

Keywords

Introduction

Organizational pay transparency—defined as the extent to which an organization voluntarily discloses pay information to its non-executive employees and allows employees to discuss pay-related information with others inside the organization (Marasi & Bennett, 2016)—is a topic widely discussed among scholars, professionals, employees, politicians and the broader public (Heisler, 2021). Due to efforts to reduce the gender pay gap and other societal inequities related to pay and income (Castilla, 2015; Kim, 2015), pressure to increase transparency is growing, and several countries (e.g., the United States, the United Kingdom, Iceland, Germany, Switzerland) have introduced new employment laws to increase pay transparency in recent years (European Commission, 2017). Compounding this trend are increasing expectations among employees for more information about pay (Smit & Montag-Smit, 2018). Consequently, organizations are often confronted with the necessity of communicating more openly about their pay system and of providing more individual pay information.

In spite of such interest among different stakeholders, scholars know relatively little about organizational practices around pay transparency. Specifically, little is known about when organizations are more likely to open up about pay. Research thus far has explored either contextual external (macro-level, e.g., social norms or legislation) factors determining when organizations introduce pay transparency (Brown et al., 2022; Scott et al., 2020) or focused on the employee perspective and investigated consequences of pay transparency for individuals (Bamberger & Belogolovsky, 2017; Belogolovsky & Bamberger, 2014, 2015; Day, 2012; Scheller & Harrison, 2018; Scott et al., 2020; Shaw & Gupta, 2007). However, recent conceptual reviews also indicate within-organizational level factors, such as pay system characteristics, that constitute an important motive for higher or lower levels of pay transparency in organizations (Avdul et al., 2023; Brown et al., 2022; Stofberg et al., 2022). For example, it has been suggested that pay system characteristics likely play an important role in pay transparency decisions given that under some pay system conditions (e.g., lower pay dispersion) pay transparency may be less risky for managers (e.g., fewer potential conflicts, negotiations; Brown et al., 2022; Wong et al., 2023).

However, little organizational research has explicitly addressed the internal conditions (i.e., pay practices) under which organizations make pay-related issues transparent to their employees (Fulmer & Chen, 2014). The strategic Human Resource Management (HRM) literature postulates the importance of internal alignment of different HRM policies, practices and processes for achieving sustainable competitive advantage (Banks & Kepes, 2015; Delery, 1998; Delery & Shaw, 2001; Jackson et al., 2014; Kepes & Delery, 2007). Internally aligned HRM practices may lead to positive synergetic effects (Banks & Kepes, 2015; Becker et al., 1997). In contrast, misaligned HRM practices result in negative synergistic effects exist and consequently harm organizational performance (Banks & Kepes, 2015; Becker & Huselid, 1998). Thus, in addition to pay transparency practices that vary across countries and industries due to different cultural values, norms and traditions as well as legal requirements (Arnold, Fulmer, Sender, Allen, Staffelbach et al., 2018; CIPD, 2019; Schuler & Rogovsky, 1998; Scott et al., 2020), the strategic HRM literature would suggest that certain pay transparency dimensions and pay system characteristics would also be likely to coexist.

Importantly, there are good reasons for both higher level of pay transparency (e.g., pay transparency may help employees understand their contributions and rewards and send signals to current and future employees; Brown et al., 2022; Cullen & Perez-Truglia, 2022; Scheller & Harrison, 2018; Sharkey et al., 2022) and low level of pay transparency (e.g., pay transparency may induce envy, conflict and collide with employees’ privacy preferences; Brown et al., 2022; Král & Kubišová, 2021; LaViers, 2019; Marasi & Bennett, 2016; Schnaufer et al., 2022). These arguments for and against pay transparency in the literature are derived from different theoretical perspectives but reflect well organizations’ reality in balancing pros and cons of pay transparency and deciding what to reveal and to whom (Tse, 2022). Consequently, organizations’ pay transparency decisions are characterized by tensions and more research is needed to understand how organizations tend to resolve these tensions (Avdul et al., 2023; Heisler, 2021).

These tensions are specifically salient for variable pay (Wong et al., 2023), defined as pay that varies with some measure of individual or organizational performance (Milkovich et al., 2013). The basic logic behind the use of pay for performance is that such incentive plans pursue two major goals: incentivizing and sorting (Cadsby et al., 2007; Gerhart et al., 2009; Rynes et al., 2005). The incentive effect refers to the impact a variable pay plan has on performance by motivating employees toward needed role behaviors (Schuler & Jackson, 1987). Sorting effects increase performance through changes in the composition of the workforce that increase the proportion of workers willing and able to enact the needed role behaviors. Although organizations that implement variable pay may wish to provide higher level of transparency to motivate employees toward needed role behaviors (Schuler & Jackson, 1987), simultaneously they may want to limit variable pay transparency to avoid generating unfairness perceptions and negative effects on performance (Trevor et al., 2012; Wong et al., 2023). Specifically, employees’ reaction to pay level depends on how much they make in comparison to relevant others (Pfeffer & Langton, 1993) and whether they perceive their pay as fair (SimanTov-Nachlieli & Bamberger, 2021). For example, when variable pay is a significant component of pay which results in larger pay differences between individuals, or when variable pay decisions are based on subjective criteria, organizations may prefer to adopt less variable pay transparency to prevent employees from becoming demotivated by learning about large pay differentials that could be perceived as unfair (Fahn & Zanarone, 2021).

In this study we take strategic HRM literature as overarching theoretical lens and adopt a descriptive, explorative approach to investigate the relationship between variable pay transparency and variable pay characteristics. We explore whether organizations are more likely to implement certain variable pay transparency practices depending on their variable pay system characteristics, namely: (1) the proportion of variable pay in the overall pay package, (2) whether an organization offers group-level variable pay, (3) the extent to which organizations use objective performance criteria to evaluate performance and (4) the extent to which pay is determined using criteria relative to other employees (vs. absolute criteria). In the early stages of investigation in an under-researched area, scholars have recommended the utilization of exploratory approaches examining covariance between variables (i.e. pay transparency and pay system characteristics; Spector, 2019). Consequently, given the nascent state of the academic literature, we use a cross-sectional design and a relatively descriptive approach to shed light on the underexplored relationships between pay transparency and pay system characteristics.

We contribute to the literature in three ways. First, we provide insights into organizational motives (Brown et al., 2022) related to pay characteristics for pay transparency in organizations. Specifically, we explore the relationships between different variable pay components and distinguish among different pay transparency types (Arnold & Fulmer, 2018). In line with recent developments in the literature postulating that pay transparency is a complex construct (Arnold & Fulmer, 2018; Heisler, 2021), we differentiate between procedural variable pay transparency (i.e., transparency in how variable pay is determined), distributive variable pay transparency (i.e., transparency in actual variable pay outcomes) and variable pay communication restriction (i.e., the extent to which organizations discourage employees from discussing individual variable pay information). This differentiation is important as research indicates that the effects of pay transparency vary based on what transparency actually reveals (Gutierrez et al., 2022).

Second, in contrast to previous studies focusing on external factors determining pay transparency level in organizations (e.g., Scott et al., 2020), and in line with recent calls in the literature (Stofberg et al., 2022) we explore whether there is evidence for the link between pay transparency practices and organizational factors (i.e., pay system). From the strategic HRM perspective, appropriate communication—such as the correct degree of transparency about pay—may be crucial in order to permit realization of competitive advantage (Jackson et al., 2014; Piening et al., 2014); however, organizational research has not explicitly addressed the internal conditions (i.e., pay practices) under which organizations are more likely to make pay-related issues transparent to their employees (Fulmer & Chen, 2014) or, alternatively, restrict employees from discussing pay (Rosenfeld, 2017). Our third contribution is of a practical nature. In view of the growing imperative for greater pay transparency, this research provides some of the earliest multi-organizational, multi-country information about what organizations are actually doing with respect to their variable pay transparency practices and how those are associated with various dimensions of their pay systems.

Pay Transparency and Variable Pay

Arnold and Fulmer (2018) developed their pay transparency typology by distinguishing among three different dimensions of pay transparency: (1) procedural pay transparency, (2) distributive pay transparency and (3) pay communication restriction. Whereas procedural pay transparency refers to the extent to which organizations provide information about how pay is determined (e.g., which criteria are considered for a pay rise or bonus), distributive pay transparency refers to how much actual pay information the organization discloses to its employees, which they can use to compare their actual pay to others’ pay. Pay communication restriction reflects the degree to which employees are formally or informally discouraged from exchanging and discussing individual pay information. Our study uses Arnold and Fulmer’s (2018) approach and distinguishes among three different dimensions of variable pay transparency: (1) procedural variable pay transparency, (2) distributive variable pay transparency and (3) variable pay communication restriction.

In general, organizations may have good reasons to be more or less transparent about pay. As recent review of the literature indicates (Brown et al., 2022) organizations may wish to provide a lower level of pay transparency to avoid conflict among employees, ensure employee privacy or maintain competitive advantage. In contrast, organizations may strive for higher pay transparency to foster internal labor markets or improve employer branding (Avdul et al., 2023; Brown et al., 2022; Sharkey et al., 2022). These arguments for and against pay transparency in the literature are derived from different theoretical perspectives, but often ignore one important consideration—the nature of the underlying pay system itself. In line with strategic HRM literature, HRM policies, practices and processes should work in concert and build a coherent HRM system (Kepes & Delery, 2007). Intra-HRM activity area alignment refers to alignment among HRM activities within a certain HRM area (Banks & Kepes, 2015; Kepes & Delery, 2007), and, we argue, extends to alignment among variable pay transparency and variable pay system characteristics. Empirical findings (Pfeffer & Davis-Blake, 1992; Shaw & Gupta, 2007) and strategic HRM literature (Jackson et al., 2014) indicate that pay transparency is an important element of organizations’ compensation practices and should be internally aligned with pay system characteristics. In the following we discuss theoretical and empirical research which may point to different relations between variable pay transparency and variable pay system characteristics.

When designing their variable pay components within the context of the broader pay system, organizations have different options to consider. First, the proportion of variable pay in the overall pay package is a tradeoff—greater variable pay may have a motivating aspect and thereby foster organizational performance (Shaw & Gupta, 2015), but it may also have negative consequences for employees in the form of reduced income security (Eisenhardt, 1989). Second, organizations that provide variable pay can either provide variable pay on an individual level, group level (e.g., team or organization), or both. Under individual performance pay systems, employees are compensated for their own individual performance, whereas under group performance pay systems, their pay is based on the performance of the whole group (e.g., group bonus, gain-sharing, profit-sharing; Gerhart et al., 2009). Because group-level variable pay may reinforce collective effort and may be suitable for jobs with higher task interdependence (Shaw et al., 2001; Wageman, 1995), organizations may choose to offer group-level variable pay in addition to individual-level variable pay.

Third, organizations that provide variable pay can base compensation on subjective or objective performance measures, or a combination of the two. Objective measures of performance rely on measurable results such as productivity, sales volume or profitability, whereas subjective performance measures rely on evaluations (e.g., by supervisors or peers) of employees’ behaviors such as perceived effort (Gerhart et al., 2009). Fourth, organizations can choose how performance is translated into actual pay. Organizations with absolute pay determination criteria evaluate performance in accordance with predetermined performance standards that are independent of the performance of other employees, teams or organizations. Relative pay determination criteria, in contrast, consider performance relative to that of other employees, teams or organizations (Belogolovsky & Bamberger, 2014). Consequently, we focus on four characteristics of variable pay and how they are likely to co-occur with particular variable pay transparency practices. The pay characteristics we consider include: (1) proportion of variable pay in the overall pay package, (2) existence of group-level variable pay, (3) existence of objective versus subjective criteria and (4) whether organizations use relative (vs. absolute) pay determination criteria.

In general, we argue that variable pay practices that increase the magnitude of pay differences between individuals will be associated with a tendency to be more transparent about procedures, but less transparent about outcomes and with greater restrictions on pay communication. We also argue that variable pay practices that take the focus off of competition between individuals (i.e., group-level variable pay; absolute performance criteria) or that are less subjective (i.e., objective criteria) will be associated with a general tendency toward greater transparency in terms of procedures, outcomes and communication restrictions. In the following, we provide arguments for each variable pay system characteristic.

Proportion of Variable Pay in the Overall Pay Package

Variable pay can be a powerful tool for aligning the interests of stakeholders and managers and other employee groups (Jackson et al., 2014; Shaw & Gupta, 2015). However, for a variable pay plan to be an effective motivator, employees need to know what they must do to achieve the desired pay outcome (Vroom, 1964). Thus, organizations that provide sufficient information about the criteria and processes by which variable pay is determined signal the value of certain criteria and thus induce needed role behaviors in line with strategic goals (Schuler & Jackson, 1987). This is even more important in organizations where the proportion of the variable pay within the overall pay package is higher, because it draws more attention to that specific pay component. Thus, from an organizational perspective, greater communication regarding pay determination criteria and the use of variable pay can establish a powerful connection within the HRM practice of compensation. From an employee’s perspective, increasing the proportion of variable pay in the total compensation package puts their overall compensation at risk (Eisenhardt, 1989; Stroh et al., 1996); therefore, employees will want to know what they must do to secure their desired pay outcome. Consequently, we argue that organizations are more likely to have higher procedural variable pay transparency when they offer a higher proportion of variable pay.

Although increased procedural transparency in the condition of higher proportion of variable pay may be beneficial to the organization, we argue that in organizations with higher proportion of variable pay, the distributive variable pay transparency is likely to be lower and communication restriction greater. Specifically, although being open about pay determination criteria may bring strategic benefits to organizations, transparency regarding actual bonus amounts being paid to individual employees may pose risks to organizations. First, research has confirmed that greater pay transparency leads to reduced pay dispersion (Lam et al., 2022; Wong et al., 2023) which may be problematic for organizations embracing pay for performance, as use of pay for performance tends to increase dispersion. Second, because individuals perceive their own performance more favorably compared to their supervisors, peers or other external raters (Heisler, 2021; Murphy, 2020), when more information on others’ pay is available—especially when that information conflicts with self-perceptions—individuals who perceive such pay information may feel that they are being treated unfairly (Adams, 1965; Greenberg, 1990b; SimanTov-Nachlieli & Bamberger, 2021). Transparency increases salience of pay information to employees (Göbel et al., 2020), and research suggests that perceptions of unfairness can lead to negative employee reactions such as lower job performance (Bretz & Thomas, 1992) or higher theft rates (Greenberg, 1990a). This effect may be even stronger in organizations where variable pay makes up a higher proportion of the overall pay package, as a larger part of employees’ income depends on the amount of variable pay. Large actual differences in pay that are induced by higher levels of variable pay may constitute a challenge to supervisors who might be concerned about how differences will be perceived and reacted to, as other employees learn about them; under conditions of transparency, such supervisors may be reluctant to differentiate as much on performance, resulting in greater pay compression. Thus, although some research suggests that disclosing pay levels may serve to encourage employees to apply greater effort to climb an internal career ladder (Connelly et al., 2014), because of these potential negative effects, we argue that organizations whose pay structures comprise a higher proportion of variable pay will be reluctant to provide detailed information about actual variable pay outcomes and will be more likely to restrict their employees from discussing variable pay.

Higher proportion of variable pay in overall pay package is associated with (a) higher procedural variable pay transparency, (b) lower distributive variable pay transparency and (c) greater variable pay communication restrictions.

Use of Group-Level Variable Pay

Group-level reward systems promote shared goals for the whole team (Gerhart et al., 2009) and are assumed to be suitable for certain organizations, such as those following innovation-focused strategies (Schuler & Jackson, 1987). Thus, from an organizational perspective, offering group-level variable pay may be of strategic importance. Consequently, to foster behaviors in line with the group goals, organizations with group-level variable pay will be more likely to have higher levels of procedural variable pay transparency, thus profiting from internal alignment of the variable pay system with variable pay transparency. In addition, because goals for group-level reward systems are more likely to be objective and based on historical standards, thereby facilitating employees’ goal acceptance (Case, 1998), openness about pay determination criteria and actual level of pay poses limited risks to organizations. Furthermore, from an employee perspective, group reward systems bear lower psychological costs (i.e., less individual ego threat) than individual reward systems in terms of fairness perception (Larkin et al., 2012), and employees are more likely to discuss group-level variable pay with one another. Therefore, organizations that offer group level variable pay are more likely to have greater distributive variable pay transparency than those organizations that offer only individual-level variable pay. Similarly, they will also be less likely to restrict their employees from discussing variable pay.

Organizations offering group-level variable pay, compared to those that do not, have (a) higher procedural variable pay transparency, (b) higher distributive variable pay transparency and (c) lower variable pay communication restrictions.

Use of Objective Performance Criteria

Although subjective performance measures are widespread especially for managerial and professional jobs (Fahn & Zanarone, 2021), we expect that organizations with a stronger focus on results-based (objective) measures find it more efficient and effective to be more transparent about how variable pay is determined and also about actual variable pay outcomes, compared to organizations with a stronger focus on behavior-based (subjective) measures. First, from the strategic HRM perspective, objective performance criteria constitute a clear signal to the workforce regarding needed role behaviors (e.g., reductions in the failure rate in quality enhancement strategy; Schuler & Jackson, 1987), and transparency about pay determination criteria would be consistent with and enhance strategy implementation. However, the use of objective criteria also poses fewer risks for organizations in terms of transparency. Specifically, compared to results-based (objective) performance measures, behavior-based (subjective) performance measures are “noisier” (i.e., more error-prone). Meta-analytic research of Viswesvaran et al. (1996) shows that the mean inter-rater reliability for supervisor performance ratings was only .52. Thus, organizations may have difficulty justifying differences in variable pay based on subjective performance measures, whereas organizations that use more objective performance measures can more plausibly justify differences in variable pay and, therefore, their employees may be less likely to complain about pay differences (Bamberger & Belogolovsky, 2017; Heisler, 2021). Thus, for organizations using more objective performance criteria, it may be more efficient (in terms of worker reactions and managerial time) to offer greater procedural and distributive variable pay transparency. Furthermore, organizations that base their variable pay decisions on more objective measures will be less inclined to restrict employees from talking about pay compared to organizations with a stronger focus on subjective measures. This argumentation is in line with the Futrell and Jenkins’ (1978) proposition from over 40 years ago, which posits that the ability to objectively measure performance is critical to the success of an open pay system.

A greater use of objective (versus subjective) performance criteria is associated with (a) higher procedural variable pay transparency, (b) higher distributive variable pay transparency and (c) lower variable pay communication restrictions.

Use of Relative Performance Criteria

From the strategic HRM perspective, the use of relative performance criteria (i.e., in relation to other employees) may be suitable because of its potential to reduce instances of employees being penalized or rewarded for factors beyond their control (Farmer et al., 2013). However, use of relative performance criteria may be less well-suited to the use of variable pay transparency. In organizations that use absolute performance criteria, employees are able to precisely forecast their variable pay outcome based on their own performance, and have less need to compare their performance and pay to others. In contrast, in organizations using more relative performance criteria, variable pay is less predictable because pay decisions are based not only on how well employees themselves are performing, but also on how well others are performing. Thus, relative pay determination criteria will likely lead to more inter-employee comparisons. Furthermore, relative pay determination criteria signal that performance standards are inconstant and that receiving the desired variable payout may be somewhat unpredictable (Lazear & Oyer, 2013). Thus, relative pay determination criteria may increase employees’ uncertainty regarding their performance outcome and intensify their concerns about the underlying motives of the overall pay system (Belogolovsky & Bamberger, 2014). Consequently, to mitigate these negative outcomes, organizations that have a stronger focus on relative pay determination criteria will be less likely to share variable pay information with their employees compared to organizations that rely more heavily on absolute pay determination criteria.

A greater use of relative (vs. absolute) performance criteria is associated with (a) lower procedural variable pay transparency, (b) lower distributive variable pay transparency and (c) greater variable pay communication restrictions.

Data and Methods

Participants and Procedures

We used data from a multi-country, organization-level survey study that was conducted in the following countries: Croatia, Estonia, Germany, Portugal, Slovakia, Switzerland, Turkey and the United States and is part of a larger data collection effort (Arnold, Fulmer, Sender, Allen & Staffelbach, 2018; Arnold, Fulmer, Sender, Allen, Staffelbach et al., 2018). At the time of the data collection, the countries represented in the study differed in their respective national legislative measures with respect to pay transparency. For example, as of early 2018, Germany required organizations with more than 200 employees to disclose the earnings of their employees on demand by any employee of those organizations (ILO, 2018). In contrast, in some other participating countries (i.e., Croatia, Portugal, Slovakia) the disclosure of other employees’ pay information was not possible without the consent of the individual(s) involved (European Commission, 2017). In Switzerland, a 2010 federal court decision declared that wages are not a trade secret and, therefore, employees are free to discuss their wages. In addition, in 2020 the amended Federal Act on Gender Equality entered into force, obligating organizations with at least 100 employees to conduct gender pay gap analyses every four years and inform employees about their results. In the U.S., federal contractors are prohibited from enforcing pay secrecy policies (Office of Federal Contract Compliance Programs, 2021), and the National Labor Relations Board has stated, in a view reinforced by the U.S. Court of Appeals in 2000, that pay secrecy policies interfere with employees’ protected right to discuss their working conditions (Fulmer & Chen, 2014). In recent years, some U.S. states, such as Colorado, have begun to require companies to disclose target pay ranges for positions in their job postings (Nagele-Piazza, 2021).

In each country (except for the U.S.), we collaborated with an HR professional membership association that provided access to their members. In the U.S., we purchased the email addresses of HR managers from Leadership Directories. Data collection took place between May 2017 and October 2017. Invitations to the online survey were distributed by email. Participants were able to choose between English and one of their countries’ official languages. The questionnaire was translated from English to German, Italian, French, Croatian, Slovakian, Portuguese and Turkish, and the accuracy of each translation was verified by two bilingual interpreters. Participation was voluntary, participants were assured of confidentiality and they did not receive any incentive for completing the questionnaires.

Our final data set consists of data from 601 organizations with surveys being answered by their HR representatives. Although obtaining more raters from each organization may increase reliability, it is more critical to approach knowledgeable respondents than many respondents from the same organization (Farndale et al., 2017; Huselid & Becker, 2000). Because we were interested in information on pay system characteristics and pay transparency, we targeted HR professionals and compensation specialists, who are likely to be more knowledgeable than other employees about these issues. Respondents worked mostly in HR, with 50.5% being heads of HR, 12.5% being compensation specialists and 10.8% working in an HR department, HR business partner or generalist role. Owners and C-level respondents (CEO, CFO or COO) accounted for 8.2% of the sample. Average organizational tenure was 8.4 years (SD = 8.0 years). Because not all 601 organizations had variable pay systems in place, only data from 400 organizations were used for the analysis of the characteristics of the variable pay system. Of the participating 400 organizations, 68.3% were in the private sector. In terms of organizational size, 5.8% of the organizations employed fewer than 10 employees, 10.0% 10 to 49 employees, 26.8% 50 to 249 employees, 23.8% 250 to 999 employees and 33.8% employed 1000 or more employees. In terms of nationality, 64.3% of the participating organizations were from Switzerland, 12.8% from the United States, 6.5% from Portugal, 5.5% from Slovakia, 4.0% from Germany, 3.0% each from Croatia and Turkey and 1.0% from Estonia. Organizations operating in diverse industries were represented in the sample, with manufacturing (19.8%) and financial and insurance activities (15.0%) being most represented.

Measures

Characteristics of Variable Pay System

Following common practice in the literature studying HRM (Lazarova et al., 2008) and compensation practices (Brookes et al., 2011; Schuler & Rogovsky, 1998; Tosi & Greckhamer, 2004) across organizations and countries, characteristics of variable pay were measured, where possible, with factual information to allow for comparability across contexts. In addition, the research team developed several measures for the purpose of this study. The measures were carefully designed on the basis of extant literature (Gerhart et al., 2009; Milkovich et al., 2013) and previous surveys (CIPD, 2019; Montemayor, 1996; WorldatWork, 2020) and were then content validated during discussions with HR and compensation professionals (Hinkin, 1995) from different industries.

Proportion of variable pay

The proportion of variable pay was measured with three formative indicators (Diamantopoulos & Winklhofer, 2001). Participants were asked: “Please indicate the percentage of variable pay of the overall pay package for the following employee groups. If the pay package mix varies significantly within the indicated employee groups, please try to calculate the mean percentages. Your best estimate is sufficient.” Participating organizations indicated the variable-pay percentage of the overall pay package for (1) management, (2) sales employees and (3) other employees. We differentiated between the three groups because research indicates that the proportion of managerial and non-managerial employees covered by performance- and incentive-related performance schemes differs (CIPD, 2015), which was corroborated by feedback from practitioners involved in the development of measures. In addition, special pay structures are often offered to sales employees (Chung, 2015). We calculated the measure of proportion of variable pay as a mean across the three employee groups.

Group-level variable pay

Group-level variable pay was measured with a dummy variable. Participants were asked: “Which of the following forms of team- or organization-based variable pay does your organization offer to at least some of the employees?” The provided list included: (1) incentive plans for teams or small groups, (2) bonus for teams or small groups, (3) gain-sharing plans, (4) profit-sharing plans, (5) risk sharing plan, (6) stock option plans, (7) other (please specify) and (8) the organization does not offer any team- or organization-based variable pay. Group-level variable pay was coded 0 if an organization did not offer any group-level variable pay, and 1 otherwise.

Objective performance criteria

Participants were asked: “Is the individual performance of employees for the following performance-related pay components more likely to be measured with subjective or objective performance criteria?” Four performance-related pay components were indicated: (1) incentives, (2) bonus, (3) merit pay raise and (4) awards for special achievements (CIPD, 2019; Milkovich et al., 2013). Respondents answered on a scale ranging from 1 (mainly subjective performance criteria) to 5 (mainly objective performance criteria). We calculated mean score across pay components. Cronbach’s alpha was .75.

Relative performance criteria

Participants were asked: “Is the individual performance of employees for the following performance-related pay components more likely to be measured with absolute (evaluation against predetermined standards) or relative performance criteria (evaluation relative to that of the employee’s peers)?” for the following performance-related pay components: (1) incentives, (2) bonus, (3) merit pay raises and (4) awards for special achievements (CIPD, 2019; Milkovich et al., 2013). Respondents answered on a scale ranging from 1 (mainly absolute performance criteria) to 5 (mainly relative performance criteria). We calculated mean score across pay components. Cronbach’s alpha was .88.

Pay Transparency Measures

For the broader data collection of which this study is a part, we created scales integrating multiple aspects of pay transparency (see Arnold, Fulmer, Sender, Allen & Staffelbach, 2018; Arnold, Fulmer, Sender, Allen, Staffelbach et al., 2018). The measures were designed on the basis of extant literature (Gerhart et al., 2009; Milkovich et al., 2013; WorldatWork, 2020), and on previous surveys (CIPD, 2019; Montemayor, 1996; WorldatWork, 2020) and then content validated in discussions with eight HR and compensation professionals (Hinkin, 1995) from different industries. Specifically, the questions were reviewed for wording, completeness and understanding by four compensation specialists and compensation consultants working in both local and multinational organizations in Switzerland. In addition, four HR specialists working in international organizations reviewed the questionnaire in the US. Importantly, the broader pay transparency measures used in this project have been subsequently validated by other researchers and in other contexts (i.e., in China; Wong et al., 2023).

Procedural variable pay transparency Participants were asked: “Please indicate how transparent this organization is about how the following pay components are determined” and provided separate responses for individual-level variable pay and group-level variable pay. Responses were made on a scale that ranged from 1 (not at all) to 5 (completely). We calculated mean score across pay components. Cronbach’s alpha was .85.

Distributive variable pay transparency

Distributive variable pay transparency was measured with two items developed by the research team. Participants were asked: “Please indicate how much actual pay information your organization voluntarily discloses to employees for each of the following pay components,” providing separate responses for individual-level variable pay and group-level variable pay. Responses were made on the following five-point scale: (1) no or minimal information, (2) aggregated information (e.g., mean bonus) for reference group (e.g., same pay grade or job), (3) aggregated information (e.g., mean bonus) for all employees, (4) exact individual information for reference group (e.g., same pay grade or job) and (5) exact individual information for all employees. We calculated mean score across pay components. Cronbach’s alpha was .87.

Variable pay communication restriction

Variable pay communication restriction was measured with two items developed by the research team. Participants were asked: “Please indicate to what extent your organization discourages employees from disclosing pay-related information to other employees inside the organization,” providing separate responses for individual-level variable pay and group-level variable pay. Responses were made on the following six-point scale: (1) formal obligation that would be punished in case of noncompliance, (2) formal obligation (e.g., employment clauses), (3) formal discouragement (e.g., written statements or codes of conduct), (4) informal discouragement at several times (e.g., verbally transmitted by supervisor), (5) informal discouragement at the beginning of employment (e.g., verbally transmitted at job interview, employee orientation) and (6) no communication restriction. Lower numbers indicate less restriction. We calculated mean score across pay components. Cronbach’s alpha was .94.

Controls

Because pay transparency practices may differ due to external factors such as national legislation and sector (Jackson et al., 2014; Scott et al., 2020), we controlled for country (the U.S. was used as the baseline country), and whether the respondent comes from a private-sector organization (1 = private sector, 0 = not private sector). Given that HRM practices, including compensation, differ across industries (Jackson et al., 2014), we controlled for the two most represented industries: manufacturing and financial services (dummy coded, reference group being other industries). In addition, we controlled for organization size (log; 1 = less than 10 employees, 2 = 10–49 employees, 3 = 50–249 employees, 4 = 250–499 employees, 5 = 500–999 employees, 6 = 1000–2499 employees, 7 = 2500–4999 employees, 8 = 5000–9999 employees, 9 = 10,000 employees and above). We also controlled for the use of performance evaluation because we expect that organizations with more employees undergoing formal performance evaluation are more likely to be transparent in terms of that component. Specifically, respondents indicated the approximate percentage of employees who receive a performance evaluation at least once a year, using a 12-point scale: 1 = 0%, 2 = 1%–10%, 3 = 11–20, 4 = 21%–30%, 5 = 31%–40%, 6 = 41%–50%, 7 = 51%–60%, 8 = 61%–70%, 9 = 71%–80%, 10 = 81%–90%, 11 = over 90%. Furthermore, we controlled for whether there had been a recent change in the pay system (“Were there any major changes in the compensation system in general over the last two years?” Yes = 1, No = 0).

Results

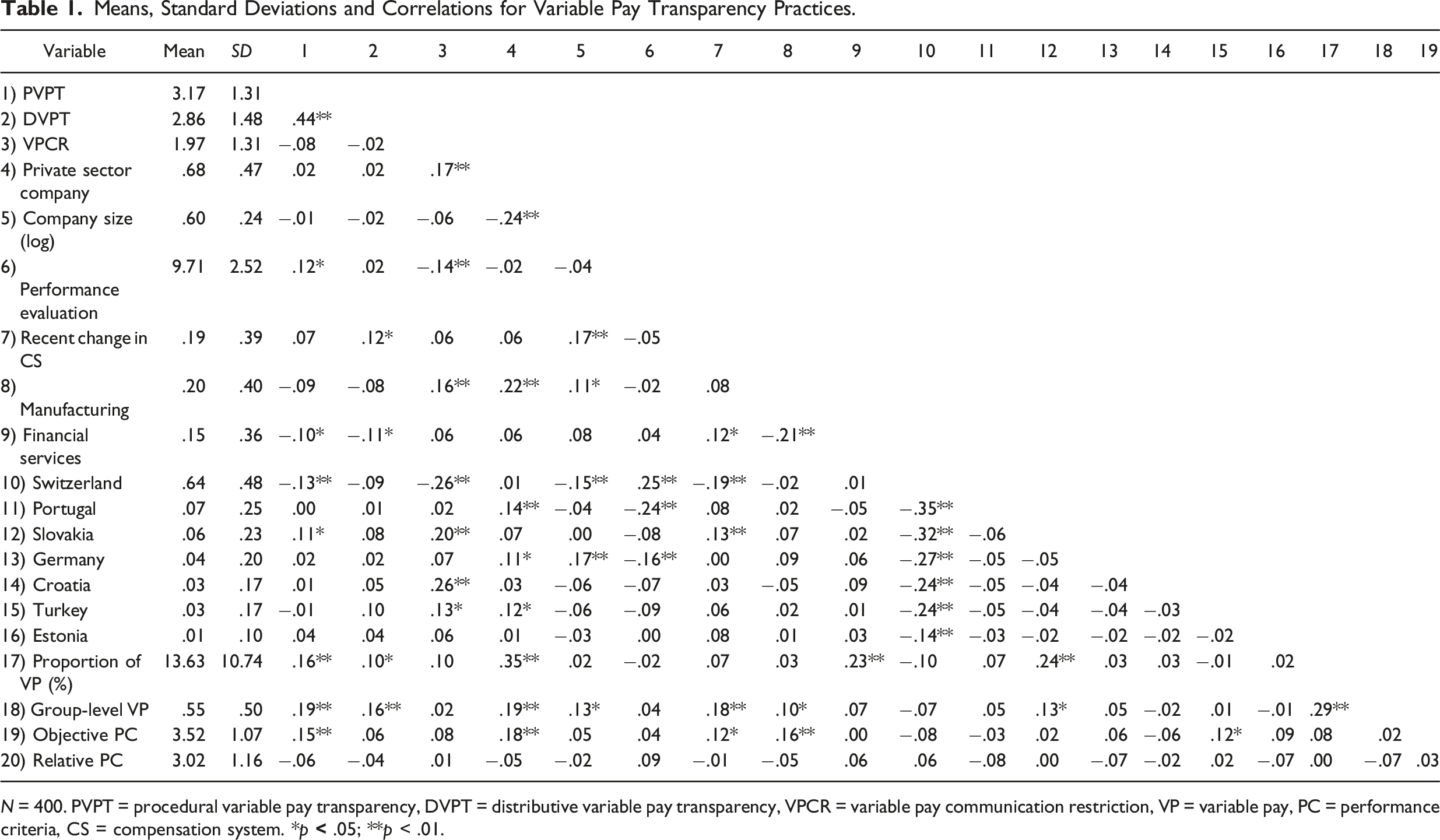

Means, Standard Deviations and Correlations for Variable Pay Transparency Practices.

N = 400. PVPT = procedural variable pay transparency, DVPT = distributive variable pay transparency, VPCR = variable pay communication restriction, VP = variable pay, PC = performance criteria, CS = compensation system. *p

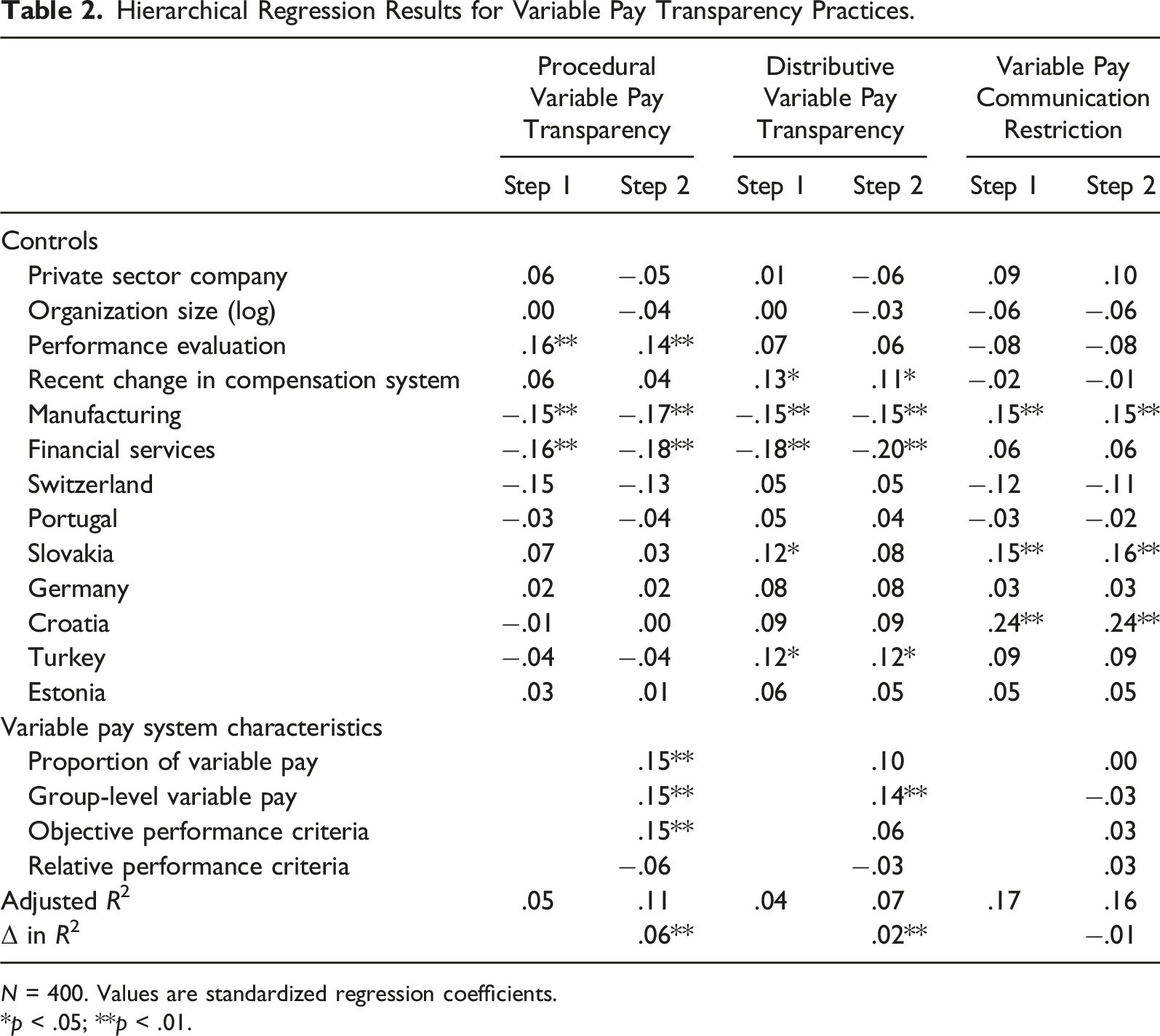

Hierarchical Regression Results for Variable Pay Transparency Practices.

N = 400. Values are standardized regression coefficients.

*p < .05; **p < .01.

Overall, characteristics of the variable pay system explained an additional 6.1 percentage points in the variance of procedural variable pay transparency and 2.5 percentage points in distributive variable pay transparency. However, characteristics of the variable pay system did not explain any variance in variable pay communication restriction.

Discussion

This study investigated the existence of internal alignment among variable pay transparency practices and characteristics of variable pay systems. Controlling for organizational characteristics, country and industry, we found that variable pay system characteristics explain additional variance in procedural and distributive variable pay transparency but not in communication restriction. Our results reveal that variable pay practices that increase the magnitude of pay differences between individuals (i.e., proportion of variable pay) were associated with organizational tendencies to be transparent about procedures. However, the results did not support our hypotheses predicting that in organizations where variable pay constitutes a larger proportion of total pay, distributive pay communication would be reduced and communication restriction would be increased. One potential explanation for this finding is that if employees perceive variable pay criteria to be fair and based on productivity-relevant inputs, such that increased distributive variable pay transparency and lower restrictions regarding communication bring benefits to the organization (Shaw, 2015) and, in line with tournament theory (Connelly et al., 2014), foster improved organizational performance. In other words, inequality in income does not necessarily translate to perceived inequity when pay differences are perceived to depend on productivity-relevant inputs (Trevor et al., 2012). This would suggest that additional factors beyond the focus of our analysis, such as fairness perceptions, may serve as moderators in the relationship between proportion of variable pay and distributive variable pay transparency. Our non-significant findings open up opportunities for future research into this and other moderating factors in the relationship between pay transparency and pay system characteristics.

In organizations using variable pay system characteristics that take the focus off of competition among individuals (i.e., group-level variable pay), we observed greater procedural and distributive variable pay transparency. Additionally, objective performance criteria were associated with higher procedural pay transparency but not with higher distributive variable pay transparency or reduced communication restriction. Notably, and contrary to our hypotheses, the use of relative performance criteria does not relate to any dimension of variable pay transparency.

According to the strategic HRM perspective, organizations’ HRM policies, practices and processes are, ideally, internally aligned with each other (Banks & Kepes, 2015; Kepes & Delery, 2007). However, we found only partial support for our expectations regarding alignment of variable pay transparency and variable pay system characteristics. Thus, although it was predicted that organizations would be strategically aligning variable pay transparency and variable pay system characteristics, our evidence does not definitively indicate that they are doing so. We encourage future research to explore how different configurations of pay transparency dimensions and pay system characteristics, beyond those we examined here, may influence the effectiveness of variable pay in fostering individual and organizational performance.

Our research makes several contributions to the literature. First, this study enriches the literature on pay transparency by providing evidence on the differences among factors shaping various dimensions of variable pay transparency. Overall, it appears that variable pay system characteristics were less strongly related to distributive variable pay transparency and variable pay communication restriction than to procedural variable pay transparency. Thus, the effects between pay system characteristics and pay transparency practices are not equal among all three dimensions of pay transparency identified by Arnold and Fulmer (2018). Organizations may have greater freedom of action to dictate their own procedural pay transparency policies, in contrast to more stringently regulated dimensions of pay transparency such as distributive pay transparency or pay communication restrictions. Future research using cross-country samples may further explore how different legislative regimes governing pay transparency may shape organizations’ pay systems and decisions regarding distributive pay transparency and communication restrictions. Overall, these findings call for future studies that adopt a more nuanced view in investigating the antecedents of pay transparency.

Second, by using a finer-grained approach to variable pay transparency, our study enriches strategic HRM literature by considering pay transparency as an important element when conceptualizing pay systems. Specifically, we advance the literature on strategic alignment by offering pay system-centric explanations for why some companies are more likely than others to implement greater variable pay transparency. Our empirical results suggest that external as well as internal factors (pay practices themselves) play a role in explaining the level of different dimensions of variable pay transparency across organizations.

Given that existing research has yielded mixed findings on the beneficial effects of pay transparency (Day, 2012; Fossum, 1976; Futrell, 1978; Futrell & Jenkins, 1978; Mahoney & Weitzel, 1978; Ockenfels et al., 2015; Scott et al., 2020), we also provide insight into potential reasons for organizations’ reticence to open up about pay by demonstrating that certain pay system characteristics and pay transparency dimensions are more likely than others to coexist. Recent research indicating that organizational pay transparency practices vary widely not only among countries, but also within the same legal and cultural contexts (e.g., Arnold & Fulmer, 2018; CIPD, 2019; Scott et al., 2020), supports this claim and suggests that organizations may strategically choose different pay transparency practices (within the scope of the legal requirements) in order to leverage the benefits and limit the disadvantages of pay transparency. An interesting area for future research would be to explore how organizations adapt their pay systems in response to exogenous changes in legislation as well as how such legislative changes indirectly influence organizational and employee outcomes.

Limitations and Future Research

This study has several limitations that may constitute opportunities for future research. First, we focused exclusively on variable pay system characteristics as drivers of organizational variable pay transparency decisions, and thus did not consider other potentially significant drivers of pay transparency, such as national or regional cultural differences in terms of norms and traditions or organizational culture characteristics. Considering the low level of variance explained, especially in the case of distributive variable pay transparency, we call for more research to explore factors other than pay system characteristics in predicting pay transparency.

Second, our theoretical approach leads us to believe that variable pay system design is an important driver of organizational variable pay transparency, and our empirical results appear to corroborate this assumption. However, our cross-sectional research design cannot eliminate the possibility of reverse causality. It is possible that changes in transparency may be implemented in concert with changes in the pay system, or that changes in variable pay transparency driven by internal (i.e., employees), and external (i.e., legislation) pressures may actually influence pay system characteristics. A field experiment following the disclosure of the salaries of all state employees at the University of California indicated that employees are more likely to seek out pay information when their employer increases pay transparency (Card et al., 2012). Anticipating employee reactions to such information, organizations may in fact change certain aspects of the pay system in order to reduce complaints and inquiries. However, we believe that at this relatively early stage in the development of research into organizations’ pay transparency practices, evidence of significant associations between pay practices and transparency practices is a meaningful advancement.

Third, there are limitations related to the measures used in our study. For example, we used only two items to measure the different dimensions of variable pay transparency. This would appear sufficient for a first attempt at analyzing the relationships between pay system characteristics and pay transparency, and considering that we used mostly fact-based measures (e.g., distributive pay transparency and communication restriction). However, we acknowledge this limitation on the measures and encourage future research to improve on this aspect. Fourth, although we sought to address the common method bias concern by assuring the participants of anonymity and separating the predictor and outcome variables in the questionnaire (Podsakoff et al., 2012), the use of single respondents and vulnerability to the common method bias is a substantial limitation of our research. However, the great majority of respondents worked in HR department; we approached informants who were able to provide accurate information on compensation practices in their respective organizations (Farndale et al., 2017; Huselid & Becker, 2000). In addition, we collected mostly fact-based data from participants, which—compared to opinions elicited in an effort to access attitudinal constructs—are less likely to be influenced by potential perceptual differences. Future research could address these shortcomings, such as by using both publicly available data on compensation systems as well as survey data on pay transparency practices over time. As noted in a recent review of the pay for performance literature (Fulmer et al., 2023), because experimental research on compensation in organizations can be challenging, more quasi-experimental intervention studies would be useful. Specifically, quasi-experiments in pay transparency research would be fruitful for further exploration of which configurations of pay system characteristics and pay transparency dimensions may be more effective for organizations.

Practical Implications

In light of growing internal and external pressures to increase pay transparency, organizations are confronting the need to open up about pay (Heisler, 2021). Strategic HRM and pay transparency literature posits that organizations benefit from aligning certain HRM practices such as pay system characteristics and pay transparency (Avdul et al., 2023; Jackson et al., 2014). Consequently, in line with our argumentation, not all organizations decide to be transparent about pay-related issues or to allow employees to discuss pay, presumably for what they perceive as good reasons related to the characteristics of their pay system. Our research confirms what has been postulated in the literature that organizations approach the goal of moving toward greater transparency with caution (Heisler, 2021; Schnaufer et al., 2022) and, at least partially, in a strategic way (Avdul et al., 2023). Specifically, our research provides some of the first indications of which pay system characteristics relate to pay transparency dimensions and thus may constitute a basis for revising variable pay systems to fit the intended transparency level. As more and more organizations are compelled (i.e., by increasing legal and industry pressures from competitors and employees) to open up about pay, these pressures constitute an invitation to thoroughly rethink the overall pay system and to evaluate how the existing pay system characteristics align with any newly adopted transparency. In addition, the demonstrated link between distributive pay transparency and pay system characteristics indicates that organizations may need time to adapt their variable pay systems (e.g., simplify them; Bryant et al., 2020) in response to new legal distributive pay transparency regimes.

Conclusions

Using data from organizations operating in different industries and countries, this study examined the relationship between variable pay system characteristics and three dimensions of variable pay transparency in organizations. Findings indicate that variable pay system characteristics explain additional variance in procedural and distributive variable pay transparency, but variable pay system characteristics did not predict variable pay communication restriction, with the variance mostly explained by industry and country differences. This study complements the existing knowledge about existence of internal alignment of pay transparency and pay system and supports the notion of differentiating between pay transparency dimensions. We encourage future research to expand on the foundation we have laid with the present study.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.