Abstract

This study aims to examine the role of gender in lending operations and specific features performed in a loan-based crowdfunding (CF) platform oriented to funding sustainable projects.

Using a quantitative approach, the research exploits a database of information on past CF campaigns carried out in a specific Portuguese platform—GoParity.

The results of the study show that gender is able to influence the way CF is used to finance sustainable development projects. The characteristics of the CF operations are shaped by the presence of women in the shareholder structure, and especially by the gender composition of the project team. This specific characteristic affects the design of the CF campaign in terms of the amount of the pledging goal, the maturity of the loan and the guarantee offered.

Introduction

In recent years, the importance of entrepreneurship and new business development has been increasingly recognised in the literature, particularly for its contribution to economic development, job creation, the provision of new products and services to society, and even the enhancement of social and environmental well-being (Neumann, 2021; Ordeñana et al., 2024; Toxirovna & Boyir qizi, 2023). This importance is acknowledged around the world and across countries with varying levels of economic and social development (Munyo & Veiga, 2024; Neumann, 2021; Tahir & Burki, 2023).

The body of research on the importance of entrepreneurial behaviour has grown substantially, encompassing both broad conceptualisations (Neumann, 2021) and specific subtypes of entrepreneurship associated with low levels of entrepreneurial activity (Gouvea et al., 2022; Staples, 2016; Zulkefly et al., 2022). This is the case for female entrepreneurship (Al-Qahtani et al., 2022; Gabarret & D’Andria, 2021; Gaies et al., 2023; Gawel & Glodowska, 2021; Marchesani & Masciarelli, 2024; Salim & Anis, 2021). Indeed, despite the observed increase in the number of female entrepreneurs in recent years, the rate of male entrepreneurship remains higher in most of the countries, including those with high levels of economic development and considered egalitarian (GEM, 2023).

Several barriers have been identified to entrepreneurship (Akkaya et al., 2024; Khanin et al., 2022; Shahid, 2023) and, specifically, to female entrepreneurship (Abd El Basset et al., 2022; Chiplunkar & Goldberg, 2024; Naguib, 2024; Strawser et al., 2021). These barriers include a lack of information, the complexities of starting a business, bureaucratic hurdles, the low confidence of entrepreneurs in pursuing new ventures, and the challenges of managing personal and professional life responsibilities (Góis, 2022). Fear of failure, which is acknowledged to be higher among women, is another important factor (Naguib, 2024; Rodrigues, 2022), as well as the nature of women’s social networks and the greater lack of role models (Abd El Basset et al., 2022).

Moreover, funding was identified as one of the most important obstacles to the development of new ventures, with a greater impact on female entrepreneurs (Abd El Basset et al., 2022; Gafni et al., 2021; Rodrigues, 2022). Women entrepreneurs face specific difficulties in accessing finance, enhanced by sociocultural constraints, and limited access to supportive institutions (Abd El Basset et al., 2022). More recently, the difficulty of obtaining funding has also been identified for projects that focus on sustainable value creation, due to a weaker focus on financial performance, which could have an impact on the ability to attract traditional sources of funding (Maehle, 2020).

Despite the gender gap in entrepreneurship, the literature indicates that women are more inclined to develop entrepreneurial activities aimed at creating new ventures with a social purpose (Bosma et al., 2020; Reichert et al., 2021; Yamini et al., 2022). This tendency is attributed to women’s stronger prosocial attitudes (Yamini et al., 2022) and a heightened sense of mission, as opposed to goals centred on profitability and financial gain (Pines et al., 2012; Reichert et al., 2021). In addition, women who are more empathetic and emotional are more likely to become the leaders of companies devoted to social causes (Rosca et al., 2020).

The integration of digital technologies into entrepreneurial activities has facilitated the growth of women-led businesses by enhancing effectiveness, confidence and inspiration among female entrepreneurs (McAdam et al., 2019; Mora-Rodríguez et al., 2020; Ughetto et al., 2020; Yang et al., 2022). Digital tools have also introduced new financing methods, such as crowdfunding (CF), which leverages the digital environment to connect entrepreneurs seeking funding for their projects (crowdfunders) with potential investors (crowdfundees).

The growth of CF in recent years has led to the emergence of platforms specialising in financing projects tailored to specific target audiences and types of CF (Böckel et al., 2021). These specialised platforms aim to facilitate connections between entrepreneurs and investors who have common interests and objectives.

Given the significance of the topic, there has been substantial growth in research activity in recent years. Many of these studies have focused on the determinants of successful CF campaigns, the motivations behind the use of CF, and the application of signalling theory to CF (Moritz & Block, 2016; Shneor et al., 2020).

Even so, as highlighted in the literature, there remain significant research gaps to be addressed in future studies (Shneor et al., 2020). Research on the intersection of gender and sustainability in the domain of CF is notably scarce (Gafni et al., 2021), particularly with regard to the dynamics of lending in CF. Furthermore, as Böckel et al. (2021) observed in a systematic literature review, although CF lending represents the largest volume of activity among CF modalities, it receives only a small share of academic attention. Studies on CF have predominantly focused on the analysis of the communication strategies employed, rather than exploring the design of the structural terms of the CF operation.

The literature also highlights the potential for extending CF research to different countries. Most existing studies focus on countries with more developed entrepreneurial ecosystems, neglecting countries that remain largely underexplored despite the potential of CF (Böckel et al., 2021).

In view of the gaps identified, this research aims to understand the extent to which gender can influence the use of CF as a source of funding for sustainable projects and the characteristics of the operations carried out, taking as a reference the Portuguese CF campaigns performed on a Portuguese platform specialised in sustainable development.

In Portugal, since 2009, several CF platforms have started to operate, offering entrepreneurs the possibility to raise funds from an undefined group of online investors, who are seeking investment opportunities and/or causes to support.

The legal framework for collaborative financing in Portugal was established in the 2015 legislative act (Law N.º 102 of 24 August 2015). The legislation stipulates the modalities of CF, access to activities, platforms and their ownership, as well as supervision and the membership regime for beneficiaries and investors. Subsequently, in 2018, the legal framework established a system of penalties and the sanctioning regime applicable to the development of CF activity (Law N.º 3 of 9 February 2018). In the context of the regulatory framework, CF platforms using an investment model, which include loan-based CF, are required to obtain registration with the Portuguese Securities and Exchange Commission (Bernardino et al., 2021). Conversely, non-investment platforms are subject to registration with the Directorate-General for Economic Activities (DGEA). Despite the considerable increase in CF activity observed in the country in recent years, there remains a significant gap in terms of development compared to other European countries (Ziegler et al., 2020).

Given the purpose of the research, the remainder of the article is structured as follows. The theoretical background for the article is developed in the ‘Literature Review’ section. ‘Methodology’ section presents the methodology of the study. ‘Analysis of the Results’ section presents the results obtained. This is followed by a discussion of the results and, finally, the conclusions of the study.

Literature Review

CF and the Lending CF Model

The concept of CF originates from the combination of two English terms: ‘crowd’ and ‘funding’ (Beaulieu et al., 2015). As the fusion of these words suggests, CF is a method of financing new ventures that leverages the collective contributions of a large group of individuals (Belleflamme et al., 2014).

The utilisation of CF as a practice has been in existence for a considerable time period. Hemer (2011) provides examples of CF applications from before the 21st century, including concerts and publications of Mozart and Beethoven’s music, which were financed by subscriptions from interested parties. However, the use of the term ‘CF’ is a relatively recent development. The practice of CF, as it is understood today, first appeared in the 1990s, primarily within the creative industries. Since the global financial crisis of 2008, CF has emerged as a noteworthy alternative source of financing, particularly for nascent enterprises and growing companies (Kuti & Madarász, 2014; Stemler, 2013). The significant increase in the use of CF, as related to the number of existing platforms around the world as well as the amount of financing involved (Ziegler et al., 2020), is reinforced by the advent of technology and the internet (Belleflamme et al., 2014).

Entrepreneurs use this internet-based approach to secure funding for their projects by collecting small amounts of money from a large number of people who support or invest in a project with a specific purpose (Ahlers et al., 2015; Belleflamme et al., 2014; Wangchuk, 2021). In this context, a CF platform serves as an intermediary, connecting two different parties: (a) the entrepreneurs seeking capital and (b) investors interested in funding or supporting projects they consider to be worthy (Bernardino & Freitas Santos, 2021a).

There are different models of CF. As highlighted by Shneor et al. (2020), the term ‘CF’ serves as an umbrella term that encompasses a wide range of funding models. In general, four primary CF models are identified, each based on different funding logics (Hommerová, 2020): (a) donation-based CF, (b) loan-based CF, (c) reward-based CF and (d) equity-based CF.

Donation-based CF is a form of CF with no expectation of direct reward, as contributions are made with no idea of repayment or compensation (Hommerová, 2020). As the name suggests, it is a digital donation to a specific project chosen by the investor/donor. In reward-based CF, although there is no repayment of the funds provided, there is an expectation of a small non-monetary reward, either tangible or intangible, offered in return for the support provided (Bouncken et al., 2015; Gutiérrez-Urtiaga & Sáez-Lacave, 2018). This reward can take the form of a thank-you note, a small gift, a discount on the purchase of a future product, or the random distribution of free products to the group of investors/supporters (Shneor, 2020).

Both donation-based and reward-based CF are considered non-investment models because the motivations of crowdfunders are not driven by financial returns (Bernardino & Freitas Santos, 2020). Instead, they often include motivations related to the desire to support the realisation of the project, emotional commitment or personal fulfilment associated with contributing to an area of interest (André et al., 2017).

In contrast, in the case of loan-based CF, the amounts provided by investors are considered as loans (Serrano-Cinca et al., 2015). This means that at the time of the CF operation, there is a commitment by the crowdfunder to repay the borrowed capital on a specific date, along with the payment of an agreed interest rate, defined in the CF agreement (Alsabah & Alibrahim, 2025; Bouncken et al., 2015). The interest rate is determined and negotiated according to the perceived level of risk involved in the transaction (Bernardino & Freitas Santos, 2021b). Typically, the higher the risk, the higher the interest rate charged, which serves as compensation for the risk borne by the investors (Wangchuk, 2021). Equity-based CF is also an investment-oriented CF model. In this type of CF, investors provide funds, expecting to participate in the future profit distribution of the project (Bouncken et al., 2015; Hommerová, 2020).

Globally, the CF modality with the largest volume of transactions is loan-based CF, whose activity has increased significantly in recent years and is the most liquid CF modality (Wangchuk, 2021; Ziegler et al., 2020).

Several benefits have been identified for CF as a fundraising tool for entrepreneurs (Prędkiewicz & Kalinowska-Beszczynska, 2020; Torres et al., 2024; Ziegler et al., 2020), particularly in the absence of conventional start-up financing options. First, and foremost, CF provides a new and alternative source of funding (Prędkiewicz & Kalinowska-Beszczynska, 2020). This is especially beneficial for entrepreneurs who face significant barriers to accessing traditional financing sources or lack a historical track record, which is often required for traditional funding modalities such as bank loans (Ziegler et al., 2020).

The fundraising operation, facilitated by digital platforms, enables access to a larger pool of potential small investors and attracts diverse investor profiles with varied interests—many of whom would otherwise be unreachable (Ziegler et al., 2020). Consequently, one of the key advantages of loan-based CF is its ability to easily and quickly match compatible borrowers and lenders (Ziegler & Shneor, 2020), who are connected through the digital platform, regardless of their physical location.

The low cost at which fundraising could be obtained is also another advantage mentioned in the literature (Prędkiewicz & Kalinowska-Beszczynska, 2020). Other financial advantages include the flexibility of the funding source, the low level of bureaucracy, and the absence of guarantees required for the loans received (Bernardino & Freitas Santos, 2020; Torres et al., 2024).

CF also offers non-financial benefits, such as enhanced reputation and legitimacy, validation of the project’s market potential, feedback from the market for new products/services, and the generation of electronic word-of-mouth (Bernardino & Freitas Santos, 2020; Prędkiewicz & Kalinowska-Beszczynska, 2020; Torres et al., 2024). The ease of use of CF platforms is another advantage, as it simplifies the process for entrepreneurs to create and manage CF campaigns, monitor financing operations, and facilitate the participation of potential investors (Torres et al., 2024).

However, there are limitations to using CF as a funding source. As Maehle (2020) points out, mobilising resources through CF is a hard work activity and often involves more effort than entrepreneurs initially anticipate. This includes planning the entire campaign, preparing communication materials for the campaign, and managing relationships with a large number of investors. Indeed, Maehle’s (2020) study highlights the workload related to CF activities and the effort required for communication, particularly for sustainable projects, which can increase the costs of using CF. Moreover, according to Maehle (2020), experimentation and innovation by entrepreneurs may be constrained due to the dispersion of control and increased public exposure.

Main Features of a Lending CF Operation and Hypotheses Development

When applying to a lending operation, crowdfunders have to submit a proposal for the loan on the CF platform (Emekter et al., 2015). In the application, among other information about the project, the entrepreneurs have to reflect on the desired amount of funding to ask and the intended maturity (Miglo, 2022). Based on the analysis and due diligence procedures, the platform’s technical team decides whether or not to approve the CF operation and suggests the interest rate at which the loan will be launched on the platform, reflecting the perceived level of risk involved and potential guarantees offered (Emekter et al., 2020; Havrylchyk & Verdier, 2018). Under the ‘All or Nothing’ option, the campaign will only succeed, and the crowdfunder will be able to raise the requested funding if the financial goal is attained within the fundraising period; otherwise, the crowdfunder will not receive the funds, and the platform will return all the money raised to the lenders (Tomé, 2022).

Based on this, loan-based CF financing operations are characterised by the following parameters: amount of funding, maturity of the loan, interest rate, duration of the campaign, risk level and guarantees.

The decision on the parameters of CF operation is fundamental and should reflect the characteristics and needs of the crowdfunders. Indeed, existing empirical evidence suggests that the characteristics of funding operations can be shaped by several factors, both related to the fundraiser and to the characteristics of the project (Liu et al., 2023).

The definition of the terms of the CF operation has the capacity to increase or decrease the attractiveness of participation for potential supporters. Investors who provide financial support to projects are exposed to a range of risks, namely credit risk (European Commission, 2015) and liquidity risk.

Since the seminal works of Arrow (1965) and Pratt (1964), risk aversion theory has brought important insights into investors’ decision-making processes. It argues that, in uncertain situations, individuals base their decisions on expected utility and exhibit a preference for avoiding losses rather than gains.

In CF, grounded in risk-aversion theory and from the perspective of a rational, risk-neutral and profit-oriented investor, the financial returns associated with a given operation (loan) must be perceived as compensating for the total amount of risk compared with other existing investment opportunities (Bernardino & Freitas Santos, 2021b; Lenz, 2016; Van Tassel, 2023).

From a behavioural point of view, as outlined in prospect theory (Kahneman & Tversky, 1979; Tversky & Kahneman, 1992), individuals evaluate the anticipated results of their decisions in terms of gains and losses relative to a specific point in time, usually the status quo, rather than merely considering the final outcome in absolute terms. Furthermore, individuals tend to avoid losses more than acquiring equivalent gains. Drawing on the framing effect, prospect theory also posits that the way in which people present information significantly influences their decision-making processes (Jussila et al., 2025).

However, CF operations are conducted in a context characterised by a high level of information asymmetry (Courtney et al., 2017). This is due to the fact that crowdfunders and potential investors do not possess the same information about the risks associated with the project, thereby placing potential investors in a disadvantaged position regarding the effective ability and willingness of the borrower to repay the loan (Serrano-Cinca et al., 2015). The concerns brought by this asymmetric position of the information held by both parties of the CF transaction could raise agency problems and moral hazard (Erjiang et al., 2022; Strausz, 2017) and undermine the ability of entrepreneurs to mobilise financial resources through CF (Courtney et al., 2017).

Based on an examination of CF in the entrepreneurial fundraising context, Steigenberger et al. (2025) posit that signalling theory provides a framework for understanding how high-quality entrepreneurs can successfully address distributed information asymmetrically and mitigate uncertainty among potential investors. In accordance with signalling theory, crowdfunders utilise CF campaign characteristics to provide embedded signals to prospective backers, thereby influencing their propensity to fund CF projects (Moradi et al., 2025). Based on these signals sent to the market, crowdfunders aim to inform potential supporters of the quality and creditworthiness of the project, and convince them to enrol in the CF operation.

In accordance with social role theory, gender can be regarded as a factor capable of engendering differences in social behaviour, given its capacity to influence both societal role expectations and individuals’ own beliefs or skills (Wei et al., 2026).

In the field of CF, current empirical evidence suggests that men are more actively involved in this funding tool, as the number of campaigns initiated by men is twice that of women (Gafni et al., 2021). However, although there is no complete consensus in the literature, women are found to be able to achieve higher success rates than men (Lin & Pursiainen, 2023). The reasons given in the literature include the language used by women in the CF campaign (Gorbatai & Nelson, 2015), as well as the definition of parameters in CF operations (Ullah & Zhou, 2020).

In the following subsections, the primary terms that shape a lending CF operation are analysed and grouped into two main dimensions: (a) financial terms and (b) risk-related factors.

Financial Terms

Although the results obtained are not completely consistent, a large branch of the literature found a negative relationship between the amount of funds requested in the campaign (pledging goal) and the success of the fundraising operation (Liu et al., 2023). As explained by Liu et al. (2023), based on a systematic literature review, a higher funding goal increases the likelihood of not raising all the funds requested within the defined campaign period and, therefore, not being able to complete the fundraising process. Also, since CF is usually funded by individual CF investors or small fund investors, they usually prefer to fund small amounts to avoid large losses (Liu et al., 2023), as well as funding goals defined in a realistic way (Mollick, 2014).

Specifically analysing CF for eco-projects, Prędkiewicz and Kalinowska-Beszczynska (2020) found the same general trends in CF success, meaning that there is also a negative relationship between CF success and the amount of funding requested. Also, the authors add that defining the funding goal according to a fixed goal model is more successful than using a flexible goal mechanism. The former is perceived by investors as the best preparation and recognition of the financing needs by the entrepreneurs, which is particularly important for eco-projects due to the higher intangibility of the results.

There are some gender differences in the amount of funding asked from potential investors. Empirical research suggests that there are gender differences that influence financial decisions. As men are found to be more confident and optimistic than women, male entrepreneurs tend to make more risky decisions, such as higher debt issuance (Lin & Pursiainen, 2023). The same pattern is found in CF operations, where women set lower investment targets than men (Lin & Pursiainen, 2023).

For some authors, the higher success rate of women results from the more realistic definition of the pleading goal (Ullah & Zhou, 2020).

Other authors believe that conducting CF operations in a digital environment reduces the gender gap in traditional sources of funding, as it is conducted in a more anonymous and gender-independent manner compared to traditional financial markets (Barasinska & Schäfer, 2014; Liu et al., 2023). Thus, CF could be understood as being able to reduce the gender gap that exists in funding new ventures, as women are perceived to be more successful than men in raising funds, even though they are less involved and obtain lower amounts of funds than men.

It is worth noting that, according to the study by Lin and Pursiainen (2023), gender differences are blurred with campaign experience and when entrepreneurs (male and female) launch successive campaigns. According to the authors, these results are due to the entrepreneurial experience gained in previous campaigns and learning by doing, which reduces the over-optimism of male entrepreneurs and makes the pledge goals of the next campaigns more realistic.

For the types of CF associated with investment models, the higher success rate of women is more ambiguous. For example, in the case of equity-based CF, Prokop and Wang (2022) found that ventures with female directors were less successful in raising capital in seasoned equity CF campaigns and also asked for higher amounts of funding. Serwaah (2022) also notes that, in the literature, a number of authors have found a reduced ability of female entrepreneurs to raise funds in credit-based CF due to the prevalence of taste-based discrimination.

When analysing the other features of CF campaign promoters, a systematic literature review by Liu et al. (2023) found that the team size of the project has a significant positive impact on CF success, as projects composed of higher team supporting the projects are more able to attract funding from potential backers. In contrast, Prędkiewicz and Kalinowska-Beszczynska (2020) consider that the characteristics of the project and the information provided about the project are more important than the individual or collective entrepreneurial team behind the CF campaign. Here, the presence of a description of the team or person initiating the project in the CF campaign is also recognised as positive for the success of the operation (Prędkiewicz & Kalinowska-Beszczynska, 2020). Serwaah (2022) concludes that the presence of women in an entrepreneurial team has a positive impact on the success of CF campaigns, regardless of the type of CF pursued. According to the author, the presence of these women (in the role of entrepreneur or a member of a team) could be justified on the basis of trust, competence and the use of female-centric messages. These findings could even be fostered by the nature of the CF platform, as funders of platforms that show a social goal prioritise female projects and increase the success of female funding (Moleskis et al., 2019).

Based on previous findings and on the social role theory, the following research hypotheses are proposed:

H1a: The presence of women in the shareholder structure of sustainable development projects is negatively related to the amount of funding to be asked in CF campaigns.

H1b: A higher presence of women in the team of sustainable development projects is negatively related to the amount of funding to be asked in CF campaigns.

The same applies to CF lending models, where crowdfunders must define the maturity of the loan when creating a given campaign. When analysing the characteristics of CF loan campaigns in Portugal, Bernardino and Freitas Santos (2021a) found that CF loans are particularly suitable for medium-term maturities. Conversely, campaigns with very long maturities do not seem to be very attractive, as investors might be reluctant to provide funds in the longer term (Bernardino & Freitas Santos, 2021a).

When analysing the credit market, Beck et al. (2018) found that gender issues can bias the maturity of the loan. The study revealed that loan officers who lacked experience in dealing with borrowers of a different gender tended to provide loans with shorter maturities. As argued by the authors, these patterns emerge as a consequence of shifts in risk perception that are influenced by gender.

In contrast, women characteristically exhibit lower levels of confidence compared to men (Theunissen & Millone, 2024; Ullah & Zhou, 2020), which may result in a preference for the utilisation of shorter maturities in order to mitigate the risk inherent in financing operations. Based on that, and grounded in the prospect and social role theories, we expected that:

H2a: The presence of women in the shareholder structure of sustainable development projects is negatively related to the maturity in CF campaigns.

H2b: A higher presence of women in the team of sustainable development projects is negatively related to the maturity of CF campaigns.

In the context of sustainability-oriented projects, extant evidence indicates that these kinds of projects are confronted with additional challenges in terms of financing costs, which are higher due to the intangibility of sustainable claims and outputs (Maehle, 2020). According to Maehle (2020), this intangibility has a detrimental effect on the ability to convince funders to support the projects, as well as a higher perceived risk, as the projects aim to achieve a balance between economic, social and environmental objectives, which is reflected in higher interest rates for CF operations.

When considering disparities in terms of gender, available research suggests that, irrespective of the quantity of financial resources obtained by entrepreneurs, women tend to obtain higher interest rates in CF campaigns (Serwaah, 2022; Theunissen & Millone, 2022). According to Serwaah (2022), this tendency can be attributed to the fact that women are required to offer lenders a higher rate of return to achieve a successful funding outcome, in comparison to their male counterparts.

Accordingly, combining the double effect caused by gender and the intangibility associated with the sustainability orientation of projects, and building on the risk-aversion theory, the following research hypotheses are proposed:

H3a: The presence of women in the shareholder structure of sustainable development projects is positively related to the interest rate level in CF campaigns.

H3b: A higher presence of women in the team of sustainable development projects is positively related to the interest rate level in CF campaigns.

Based on an extensive literature review, Liu et al. (2023) point out that one of the factors that has been confirmed to influence the success of CF campaigns is the duration. The available evidence found a negative relationship between campaign duration and fundraising success. Out of a total of 31 articles analysed, 21 showed a negative correlation between the two variables (Liu et al., 2023). According to the authors, a longer duration sends a negative signal to investors, which affects the ability to mobilise resources through the CF platform. The same is pointed out by Prędkiewicz and Kalinowska-Beszczynska (2020), for whom long campaigns indicate a lack of confidence on the part of entrepreneurs, while short campaigns signal determination.

Existing research has found that the ability to attract funds over time is U-shaped, as there is typically a high ability to attract funds at the beginning and end of the campaign, with a more stagnant period in between (Tan & Reddy, 2024).

Regarding gender differences, according to Ullah and Zhou (2020), women define shorter campaign durations than men due to their lower confidence levels. According to the authors, this is one of the reasons why women have higher success rates in CF than men. Theunissen and Millone’s (2024) analysis of crowdfunded business loan campaigns revealed that female-led campaigns exhibit a shorter duration of CF campaigns in comparison to those led by males, and this disparity persists across diverse CF platforms. The study findings indicate that the outcomes observed are attributable to two primary factors. First, the definition of parameters from a realistic perspective is predominantly attributed to female participants. Second, a higher herding effect that benefits women is observed. Theunissen and Millone (2024) noted that the gender disparity in the loan application process disappeared when the loans were asked by a couple. In a different approach, Serwaah et al. (2023) suggest that the perception by potential crowdfunders of higher social and economic impact when funding female entrepreneurs leads to a faster completion of the CF campaign by women.

Accordingly, based on the social role, signalling and prospect theories, the following research hypotheses are proposed:

H4a: The presence of women in the shareholder structure of sustainable development projects is negatively related to the duration of the CF campaigns.

H4b: A higher presence of women in the team of sustainable development projects is negatively related to the duration of the CF campaigns.

Risk-related Factors

Therefore, a rational investor will evaluate the risk level of the borrower in order to make their decision to support or not the CF campaign, after analysing the potential risks and returns involved (Bernardino & Freitas Santos, 2021a; Mezei, 2018).

As it is difficult for individuals to accurately assess the credit risk of each loan and decide how to allocate their money within the investment opportunities (Guo et al., 2016), most platforms display a rating level for each project requesting funding, which represents the level of risk assessed by the CF platform staff according to the financial information required from entrepreneurs (Havrylchyk & Verdier, 2018; Theunissen & Millone, 2024). The risk rating that is attached reflects the characteristics of the organisation as well as the specific conditions of the loan operation (Bernardino & Freitas Santos, 2021b). One of the advantages of CF for potential investors is the transparency and due diligence procedures typically created by the managers of the CF platforms (Hommerová, 2020).

Previous research shows that the credit rating provided by the CF platform influences the risk perception of investors and their adherence to a given CF lending campaign (Bernardino & Freitas Santos, 2021b), as well as the interest rate charged (Oliveira, 2019). Nevertheless, the existing research shows some lenient behaviour of investors in lending CF, as they smooth the risk premium charged and penalise less the riskier companies compared to the proposal made by the CF platform, according to the risk profile exhibited. However, as posited by Havrylchyk and Verdier (2018), it is fundamental for loan-based CF platforms to ensure that they are not subject to principal–agent problems if they are to offer efficient and sustainable financial intermediation. As the authors have observed, when the platform’s only revenue source is derived from the application of fees, the platform may incur a financial incentive to reduce the rigour of its loan application screening processes. This, in turn, has the potential to engender a bias in the interest rates assigned to loans listed on the platform. Bernardino and Freitas Santos (2021a) found that CF could be particularly suitable for companies with an intermediate level of risk, since, on the one hand, less risky companies may not be interested in using CF, as they have access to other sources of financing, and, on the other hand, companies with a higher risk profile may not be sufficiently attractive for investors. Nevertheless, it should be noted that besides the rational perspective mentioned, other intrinsic motivators related to emotional connection and support for the project are recognised as important drivers for CF (André et al., 2017).

As research on loan-based CF is relatively unexplored (Böckel et al., 2021) and CF loans are the only type of CF that involves the payment of an interest rate, there is little empirical research on the factors that influence the determination of the interest rate in CF. However, based on the social role theory and given the more conservative behaviour that is typically exhibited by women, and the more realistic pattern definition (Theunissen & Millone, 2024; Ullah & Zhou, 2020) that shapes the loan risk level, the following basic hypotheses are suggested:

H5a: The presence of women in the shareholder structure of sustainable development projects is negatively related to the levels of risk in the CF campaigns.

H5b: A higher presence of women in the team of sustainable development projects is negatively related to the levels of risk in the CF campaigns.

Lending CF can involve a secured or unsecured loan to a consumer or business borrower (Shneor, 2020; Ziegler et al., 2020). The existence of guarantees for the projects gives the investor community greater confidence to invest (Torres et al., 2024). Specific research on the use of guarantees is also very scarce in the study of CF, which only applies to loan-based CF. The limited research available suggests that in the USA, unsecured loan-based CF is a costly form of debt for entrepreneurs due to the high interest rates, compared to the venture capital market, and the information asymmetries involved (Kgoroeadira et al., 2019).

Given the lack of empirical literature on the topic, grounded in the signalling and social role theories, the following basic hypotheses are suggested:

H6a: The presence of women in the shareholder structure of sustainable development projects is positively related to the use of guarantees in the CF campaigns.

H6b: A higher presence of women in the team of sustainable development projects is positively related to the use of guarantees in the CF campaigns.

Methodology

Research Objectives and Methods

The main objective of this study is to understand the extent to which gender can influence the use of CF as a source of funding for sustainable projects, namely in terms of the characteristics of the funding operation. The gender analysis was based on two different and complementary perspectives: first, an analysis of the representation of gender within the project’s property structure, and second, an examination of the composition of the project team.

Considering the defined research objectives, a quantitative approach was used.

To conduct the research, the unit of analysis was projects that obtained resources through the Portuguese platform GoParity. The choice of Portugal as a country of study stems from the literature, which shows a concentration of research in certain countries with greater dynamism in terms of CF operations, while other types of countries remain with scarce research (Baber & Fanea-Ivanovici, 2024; Wenzlaff et al., 2020). The GoParity platform was chosen because it is the only platform in Portugal, specifically dedicated to financing projects that contribute to sustainable development, whether for profit or not. The platform was created in 2017 and has already won several prizes and awards, including Climate Knowledge and Innovation Community (KIC), the Green Project Awards, and the MetLife Foundation, among others.

As part of the research, the authors created a database based on publicly available information on completed CF campaigns whose funding was intended for the development of projects in Portugal. The CF platform website contains a section that provides a detailed description of the projects that have mobilised resources from the platform, their promoters and teams, as well as information about the terms of the CF operation. By consulting the website of the CF Lending platform (

Definition of the Research Variables

The gender dimension has been operationalised through two different variables, as described below:

The presence of women in the shareholder structure: a binary variable, where 1 is used if there are women shareholders and 0 if there are no women in the shareholder structure of the project. The level of feminisation of the team: a continuous variable representing the percentage of women in the total number of team members in the project. A higher percentage corresponds to a higher degree of feminisation of the team.

The characteristics of the CF operation were assessed by the following variables:

Amount, a continuous variable referring to the financial amount in euros mobilised by the CF campaign. Maturity is a continuous variable referring to the maturity of the loan, that is, the period during which the capital requested in the loan operation must be repaid. It is expressed in years, allowing for fractional periods. Interest rate is a continuous variable reflecting the annual gross interest rate at which the CF operation was concluded between the CF provider and the crowdfunders. It is expressed in percentage points. Campaign duration is a continuous variable reflecting the number of days the CF campaign was active on the CF platform until the total amount of funding was raised (target amount), expressed in days. Level of project risk—ordinal categorical variable reflecting the level of project risk as defined by the CF platform. The rating category ranges from A to D, combined with the operators ‘+’ and ‘−’. The rating A+ corresponds to the lowest risk level and D+ to the highest risk level. In addition, the letter R stands for restructured projects, and I for projects more than 90 days overdue. Guarantee—a binary variable where 0 indicates that the loan did not include any type of guarantee and 1 indicates that guarantees were used (such as personal guarantees, overdrafts, pledges or corporate finance).

Analysis of the Results

Sample Profile

The organisations that have used CF started their activities about an average of 17 years ago. In cases where there are women in the shareholder structure, the average age of the organisation is around 20 years. Projects financed through the CF lending platform cover a wide range of sectors, with energy and natural resources (24.4%), food and beverages (12.2%) and aquaculture (11%) standing out. Other relevant sectors include education (7.1%), culture, recreation and leisure (6.7%) and agriculture (5.9%). It should also be noted that 2.4% of projects financed initiatives that were part of more than one sector. Regarding the geographical location of the projects, they are all located on the mainland, with a greater concentration in the Lisbon metropolitan area (28.7%) and the central region (27.6%). In the Autonomous Regions of the Azores and Madeira, no projects with community funding were identified. The profile and characteristics of the projects analysed can be found in Appendix A.

An analysis of the contribution of projects to the different Sustainable Development Goals (SDGs) reveals that most of the projects using CF contribute to SDG7—Affordable and Clean Energy (54.3%), followed by SDG9—Industry, Innovation and Infrastructure (47.2%) and SDG12—Responsible Consumption and Production, which represents 43.7% of cases. There are no projects contributing to Peace, Justice and Strong Institutions (SDG16) and very few cases of projects contributing to SDG17—Partnerships for the Goals (0.4%).

The Presence of Women in Projects Funded by the CF Platform

The examination of the presence of women in the projects financed through the CF platform shows that only 35.4% of the Portuguese projects financed include women in their shareholder structure, which means that there is a predominance of projects in which the capital is held exclusively by men. In terms of team composition, the data show that on average, women represent only 26.75% of the total team members of sustainable projects using CF as a funding source. In addition, 42.4% of the projects have no female team members, while only 5% of the projects have teams made up entirely of women. The average number of women per team is 1.28, compared to 2.88 men per team. A detailed description of the sample according to gender is provided in Appendix A.

The Characteristics of the Operation of CF and Gender

Descriptive Statistics

The data collected (Table 1) show that the average amount of loan obtained in each campaign was around €80,000, although there was a wide range in the value of the operations (the minimum value observed was €5,220, while the maximum was €400,000). It should be noted that the average amount of financing is lower in projects with women in the shareholder structure (average value of €57,871).

The average duration of CF loans is about 4.5 years. In cases where women are included in the shareholder structure of the project, the average repayment period increases to 5.15 years. Considering all operations, the longest maturity is 10 years.

The average annual interest rate contracted in the CF campaigns was 5.3%, ranging from a minimum of 3.5% to a maximum of 7.2%. When analysing only projects with women in the shareholder structure, a similar interest rate is found (5.3%).

Finally, it should be noted that the average time taken to complete a project from the start of the campaign was 15.44 days. This average is very close regardless of gender. Of the projects examined, 2.4% started and ended on the same day. An analysis of the relationship between the characteristics of the financing operation and the degree of feminisation of the teams, both of which are continuous variables, shows that there is a negative statistically significant association in terms of the amount of the loan and the duration of the loan, as indicated by the Pearson correlation coefficient (Table 1).

Lending Characteristics by Gender.

Regardless of gender, projects financed through the platform have a moderate risk profile (Table 2), with a predominance of B, B− and C+ rated projects (22.2%, 41.1% and 26.7%, respectively). Better-rated projects (A+, A and A−) are almost non-existent, with only one A-rated project successfully using the CF platform. The same is observed for higher risk projects (D and D+), which have not completed any operations on the platform.

The results collected show a low percentage of projects that have been restructured (only 3.9%), especially when the projects include women in their shareholder structure (2.2%). In the projects analysed, there were no cases of default for more than 90 days. Finally, only 2% of the projects indicated the need to extend the campaign beyond the originally planned deadline.

Characteristics of the Crowdfunding (CF) Campaign According to Gender.

The majority of projects use some form of guarantee for the CF loan (57.1%). The most common guarantees are pledges (42.5%), followed by personal guarantees from partners (15.4%), company guarantees (11.0%) and guarantees on project receivables (7.1%). The presence of guarantees is also significant in projects with women in the shareholder structure of the company (58.9%), as shown in Table 2.

Bivariate Data Analysis

In order to analyse the extent to which gender can influence the characteristics of the operation, the bivariate data analysis was carried out (Hair et al., 2009). Different statistical inference tests were used to evaluate the different variables relating to project characteristics by gender, according to the two variables previously operationalised.

The statistical inference tests (Table 3) indicate that gender influences certain parameters of the financing operation, either regarding gender representation in the project’s property structure or according to the composition of the teams.

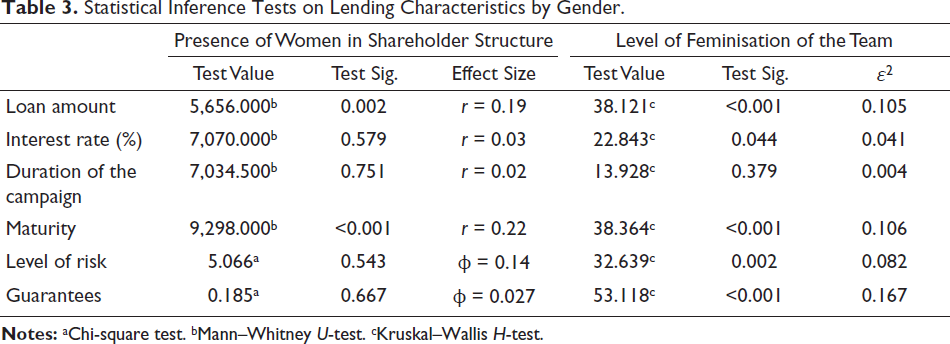

Statistical Inference Tests on Lending Characteristics by Gender.

Still, with respect to the financial terms of the operations, no statistically significant differences were identified in relation to the interest rate charged, as evidenced by both the average values (U = 7,070.000; α = 0.579) and the variability of the interest rates (Moses Extreme Reaction Test: span = 254; U = 254,000; α = 1.000).

Regarding the time-related factors, the results of the study indicate there is no statistical difference between genders in terms of the duration of the campaign (U = 7,034.500, α = 0.751; Moses Extreme Reaction Test: span = 251; U = 249,000; α = 0.287). However, certain differences are observed with respect to the maturity required for the loan. The findings of the Mann–Whitney U-test (U = 9,298.000; α < 0.001) indicate the presence of disparities in the mean maturity of the operations between women and men, despite the small size effect (r = 0.22). Although the punctual estimation of Hodges–Lehmann has suggested that projects whose shareholder structure includes women have CF loans with maturities 1 year shorter than projects only hold by men (∇̃ = −1.00), the confidence level of 95% reveals that the difference found is not statistically significant (CI 95% = [−2.00, 0.00]). The Moses Extreme Reaction Test revealed considerable differences in the variability of interest rates applied to projects held exclusively by men as opposed to projects incorporating women in the shareholder structure (span = 254; U = 248.000; α = 0.009).

Considering risk-related characteristics, the results reveal that the level of risk associated with projects applying to the CF platform and the possible use of guarantees is not significantly associated with the presence of women in the shareholder structure (respectively, χ2(6) = 5.006, p = 0.543 and χ2(1) = 0.185, p = 0.667), with small and insignificant effect sizes (φ = 0.14 and φ = 0.027, respectively).

For the remaining variables, for α = 0.05 significance, the Kruskal–Wallis test demonstrated a significant difference, with a small effect size (ε2) for the interest rate of the loan and a medium effect size for all the remaining variables.

The Jonckheere–Terpstra test revealed a significant monotonic trend of reduction in the amount financed with an increase in the percentage of women in the team (JT = 3,164, Z = −2.06, α = 0.039), with the same significant monotonic trend of reduction observed in relation to the cost of financing charged (JT = 3,164.5, Z = −2.063, α = 0.039).

In relation to the temporal characteristics examined, the Jonckheere–Terpstra test indicated a statistically significant negative trend in maturity (JT = 2,934, Z = −2.965, α = 0.003) for a higher degree of feminisation within the project team. The negative monotonic trend observed in the time required to complete the CF campaign was not deemed to be statistically significant (JT = 3,570.5, Z = −0.264, α = 0.792), which is consistent with prior analyses.

With regard to the utilisation of guarantees (a dichotomous variable) and risk level (a nominal categorical variable), the Jonckheere–Terpstra test is not applicable.

Multivariate Data Analysis

The binary logistic regression was employed, utilising the enter method. The investigation into the linearity of the logit, as derived from the Box–Tidwell method for continuous variables, yielded no compelling evidence to necessitate the transformation of the variables (α > 0.05). Multicollinearity among the variables was analysed using the variance inflation factor (VIF). The outcomes demonstrated that multicollinearity was not a concern, as the outer VIF ranged from 1.2 to 1.7.

The findings of the regression analysis (Table 4) demonstrate that the model is statistically significant and that the variables can significantly enhance the logistic model in comparison to the null model (Omnibus test: χ2 (6) = 17.616, α = 0.007). The model demonstrated an adequate goodness of fit to the data, as evidenced by the Hosmer–Lemeshow test (χ2 (8) = 12.482, α = 0.131). Nevertheless, the explanatory power of the model was found to be modest (Nagelkerke R2 = 0.093).

Of all the factors included in the model, only the amount of the loan was found to be statistically significant. The beta coefficient has been found to exhibit a negative relationship (β = −0.008, Exp B = 0.992), indicating that as the loan amount increases, the probability of the project’s shareholder structure comprising women decreases. Specifically, for each €1.000 increase in the financing operation, the likelihood of women assuming ownership roles is reduced by approximately 8%. As such, hypothesis (H1a) is supported.

The remaining variables in the model (i.e., maturity, interest rate, duration of the campaign, risk and guarantees) are found to be not statistically significant. This suggests that these terms of the CF operation are not constrained by gender issues in the shareholder structure. Consequently, hypotheses H2a, H3a, H4a, H5a and H6a are not supported.

Binary Logistic Regression.

Subsequently, the results were controlled for the characteristics of the project (Model 1b) and for the characteristics of the sustainability of the project—SDG focus (Model 1c).

The outcomes for the control models demonstrate the robustness of the findings attained. It is clear that the statistical significance of the loan amount is consistent across all three submodels. Conversely, the vast majority of the remaining variables exhibited a consistent absence of statistical significance.

It was observed that the characteristics of the project (namely its seniority, location or sector of activity) were not constrained by the gender of the shareholder structure. A number of SDGs were identified as being statistically significant (namely SDG1, 7, 10, 11, 12 and 15), suggesting that female shareholders are underrepresented in certain social domains and prevail in others. It is also evident that the incorporation of the sustainability dimension within the project has the capacity to enhance the explanatory power of the model, with an increase from 9.30% to 27.30%. Moreover, this integration has led to a statistical significance shift in the effect of interest rate (Wald = 4,418, α = 0.036). In such a case, the beta coefficient is found to be positive (β = 0.604, exp B = 1.829), thus indicating that higher interest rates are more likely to be observed in projects whose shareholder structure contains a greater proportion of women. More specifically, for each 1% increase in the interest rate charged, there is an approximately 82.9% increase in the odds that the shareholder structure will contain a greater proportion of women. Accordingly, the findings suggest that the relationship between the interest rate and the presence of women in the shareholder structure is partly explained by the unequal distribution of project areas across gender.

In all the submodels, multicollinearity does not present a problem, as the outer VIF is consistently lower than the maximum value of 5 (with a maximum observed value of 3.4).

Preliminary analysis indicates that the regression model demonstrates a satisfactory global fit, as evidenced by the R2 value of 0.255 and the F-statistic (α < 0.001). The Durbin–Watson value was found to be 1.792, indicating no significant autocorrelation of the residuals. Multicollinearity among the variables was assessed by means of the VIF, which ranged from 1.34 to 1.81, indicating that there was no cause for concern regarding multicollinearity. The analysis of the histograms, Q-Q plots and normality tests demonstrated that the residuals exhibited an approximate normal distribution. The homoscedasticity of the data was confirmed through the examination of the plots of standardised residuals against predicted values.

The analysis of the regression parameters reveals that the amount of funding is statistically significant associated with the gender composition of the teams. The regression demonstrates a negative signal of the relationship (β = −0.181), suggesting that the CF operations having a lower amount of funding are expected to be carried out by teams slightly comprising a higher proportion of women.

According to the findings of the study, for each additional one thousand euros of the CF operation, it is estimated that the degree of feminisation of the team decreases by about 0.181 percentage points. According to that, H2a is supported.

The interest rate at which the CF loans are charged is not statistically significant (α = 0.944). The same is observed with regard to the level of risk of the operations (α = 0.565), which is not conditioned by the gender issues of the team and, therefore, H3b is not supported. In contrast, the guarantees offered were found to be statistically significant (α = 0.027). The negative coefficient of the regression model (β = −12.008) indicates that the absence of guarantees in the CF loan is expected in teams with a higher degree of feminisation, estimated by approximately 12 percentage points. Thus, the result obtained in this study contradicts the initial hypothesis, which posited that women would be more inclined to use guarantees and, consequently, hypothesis H6b is not supported.

With regard to the time-related factors, the regression results indicate that either the maturity of the loan or the time required to complete the CF operations is influenced by the gender composition of the team (α < 0,05), although these factors are influenced in opposite directions. Indeed, short-maturity CF loans are expected to be found in more feminised teams (β = −4.331, α < 0.001). However, CF campaigns are also completed somewhat more slowly (β = 0.528, α = 0.022). In other words, it is estimated that teams with a greater degree of feminisation exhibit a greater propensity to rely on shorter-term loans and to complete the CF operation in more time than teams with a greater degree of masculinisation. Accordingly, the finding suggests that the hypothesis H2a is supported, while H4b is not supported.

Notwithstanding the initial evaluation, which did not reveal any issues pertaining to heteroscedasticity or violations of the assumptions underlying OLS regression, the model was estimated with heteroskedasticity-consistent standard errors (HC3) as a precautionary measure. This approach yielded analogous findings, thereby reinforcing the reliability and robustness of the outcomes.

Ordinary Least Square Regression.

After that, the results were controlled for (a) characteristics of the project; and (b) characteristics of sustainability of the project.

The results of the control models show that the findings obtained are quite stable because the statistically significance for α = 0.05 is maintained for all the variables in the study in both models, with the exception of the existence of guarantees. The latter variable was deemed not to be statistically dependent on the team’s gender composition, as long as the project and sustainability characteristics were incorporated into the analysis. This suggests that, if the context of operations is taken into account, that is, project characteristics and sustainability focus, the initial relevance of gender issues in the guarantee of use becomes negligible.

An examination of the control models reveals that some SDGs have been found to be statistically associated with the gender composition of the team (namely SDG1, 5 and 12), once again suggesting some gender-related area prioritisation. Within the general characteristics of the project, only the region is found to be statistically related to gender, and just if a significance level of 10% is assumed. If the results are corrected by the use of the robust standard error HC3, the region is considered statistically significant at the 0,05 level, whilst the remaining results are corroborated.

Discussion of the Results

The results of the study are schematically summarised as follows (Table 6).

Synthesis of Research Hypotheses.

As suggested in the literature (e.g., Liu et al., 2023), the characteristics of the fundraiser may condition the characteristics of the CF operation. Indeed, a greater presence of women in projects, both in the shareholder structure and mainly in the composition of project teams, is associated with different parameters of the loan.

First, gender differences are found regarding the amount of loans requested, with the impact of women observed irrespective of the role they assume. Indeed, when women are present either in the shareholders’ structure of the project or in the composition of the team, the CF campaign is typically designed with a lower pledging goal. Thus, as other authors have found (Lin & Pursiainen, 2023), the presence of women tends to condition the definition of financing targets in a more conservative way, which translates into the definition of a lower target amount. This can be interpreted in the light of the barriers to accessing funding and women’s lack of confidence, which are strongly supported in the case of female entrepreneurship (Abd El Basset et al., 2022; Gafni et al., 2021).

The definition of less ambitious funding goals on the part of women in CF platforms might be intensified by the intangible nature of sustainability-related projects, as argued by Maehle (2020). Thus, despite the potential that new technologies can offer in mobilising (new) investors (Böckel et al., 2021), the certain ‘anonymity’ of the entrepreneur’s gender through digital platforms (Barasinska & Schäfer, 2014) and the competitive advantage due to the female linguistic patterns (Ullah & Zhou, 2020), there is still a gap for women in accessing CF, which limits the potential amount of funding that can unfold through this funding source.

Interestingly, a different direction is evidenced when gender issues are considered from the perspective of the feminisation of work teams. In this case, although the isolated analysis of the relationship found between gender and the amount of funding shows a negative sign (bivariate analysis of the data), when the multivariate model takes into account the impact of all the variables observed, it becomes evident that the relationship is rather positive, even if it is controlled for the characteristics of the project. This surprising finding underlines the high level of complexity entailed in the conception of CF operations, as well as the interaction between factors that influence the behaviour of both crowdfunders and crowdfundees. The study further emphasises the necessity of employing comprehensive analytical models in research conducted within this domain.

The findings of the study suggest that the characteristics of the CF operation are mainly triggered by gender issues observed on the ground (by the operational teams of the projects), rather than the shareholder structure.

Indeed, in addition to the loan amount previously described, some differences in the maturity, guarantees provided, and time to complete the CF campaign are only explained by the gender composition of the team.

In line with the researchers’ initial expectations, the results show that more feminised teams tend to prioritise the launch of campaigns involving shorter repayment periods (loan maturity). In the context of high information asymmetry that characterises CF, this option in the design of the CF operation parameters signals a lower financial risk hold by investors, as they are exposed to the risk of the project for a shorter and, apparently, more predictable period of time.

This option may be indicative of the higher perceived risk that teams with a more expressive women presence may have about the funding operation (Bernardino & Freitas Santos, 2021a; Koch & Siering, 2015), which is reflected in the attempt to make the CF operation more attractive to potential investors and increase their propensity to support the project.

As previously found in traditional fundraising literature, the results suggest that women are more likely to participate in loan-based CF only if they are confident in their ability to successfully complete the funding process (Khan et al., 2024; Naegels et al., 2018). Accordingly, the result of the study seems to suggest that mixed teams with a higher degree of feminisation tend to incorporate these concerns more extensively in the decision-making process and into the design of the financing operation.

It is also noteworthy that gender was not found to influence the technical risk level perceived by the CF platform managers, and reflected in the risk rating of the projects seeking funding. It appears that teams comprising a higher proportion of women do not tend to engage to a greater extent in riskier projects or rely on the use of such type of financing for projects with a higher risk profile, compared to teams with a more masculine composition. Despite the absence of any substantial disparities in terms of risk level, the presence of women gives rise to an amplified concern with respect to the signalling of risk to the investor, which is made explicit in the definition of the other financing parameters of the loan. In light of the findings presented by Havrylchyk and Verdier (2018), it is recommended that caution be exercised when interpreting the results, as there is a possibility of bias in the risk rating assigned, which could be further explored in subsequent studies. It should also be noted that, contrary to initial expectation, women are less prone to the use of guarantees. In the conventional banking sector, women are often required to provide collateral to a greater extent than men (Theunissen & Millone, 2024). In the context of CF, given the voluntary nature of these guarantees, women may opt to exclude such clauses from loan agreements. Instead, they may seek to manage investors’ risk exposure through alternative parameters, such as the amount and duration of risk, as opposed to a commitment on the part of entrepreneurs due to a failure in their project development.

Concurrently, an examination across the multivariate models reveals that projects comprising a higher proportion of female team members are more likely to be funded somewhat slowly, with a longer timespan until finalisation of the campaign. This pattern contradicts the initial expectation and the Ullah and Zhou (2020) findings. As a corollary of the choices made in other parameters of the financing operation (amount requested and maturity), and as a result of linguistic patterns that could be introduced by a more feminised team (Gorbatai & Nelson, 2015), it would be expected that the time for the completion of the campaign would be lower for women. Nevertheless, an opposite pattern was identified, which merits further investigation in future studies. A more in-depth analysis of signalling theory within the context of the interception of the intangibility of the social dimension and gender issues, which are associated with the limited use of collateral, would be particularly pertinent.

Contrary to the initial expectation, women’s projects do not charge a higher rate of interest than those led by men. Thus, contrary to what Serwaah (2022) suggests, the effort to make loan-based CF more attractive to investors by more feminised teams is not made through the proposed interest rate, but through other characteristics of the financing operation, such as the amount of funding and the maturity of the loan.

This evidence could be interpreted in the light of a greater fear on the part of women to be involved in operations that involve greater financial commitments/sacrifices, and that could threaten the financial viability of the project. Thus, teams with a higher proportion of women seem to prefer to establish the attractiveness of the CF operation based on other characteristics that do not involve a greater commitment to the future financial flows of the project.

Conclusions

CF has been pointed out as a powerful tool for financing entrepreneurial projects, providing an alternative source of finance even for entrepreneurs who typically face difficulties in accessing finance. Indeed, using digital technologies, CF platforms bring together projects from entrepreneurs with potential investors who share common interests.

With a focus on projects with a sustainable purpose, this study aims to analyse the extent to which gender can influence the use of CF as a source of funding and affect the characteristics of the financing operations pursued. Gender issues are analysed from two different perspectives—the shareholder structure and the composition of project teams.

The research conducted highlighted the influence of gender on the design of loan-based CF operations in sustainable development projects. The main differences seem to be driven by the composition of the operational structures rather than the presence/absence of women in the shareholder bodies.

Teams with a higher degree of feminisation tend to design the CF operation in such a manner that it can be perceived as less risky and more attractive to investors. This is achieved by the amount of funding requested in each campaign and the maturity of the loan involved.

The findings show that while there is a certain participation of women in the use of CF to finance sustainable projects, there are also some glass ceilings that limit the ability of more feminised teams to explore all the potential of CF and to achieve the same conditions as their peers, regardless of the gender issue.

From a theoretical perspective, the study contributes to existing knowledge in the field of CF, which is particularly limited at the intersection of gender and sustainability. While most existing research focuses on the signalling embedded in CF campaigns, this study employs a different approach, focusing on the parameters of CF operations. As the research focuses on one type of CF investment model (loan-based CF), the empirical findings also enhance comprehension of fundraising and access to finance in the context of gendered entrepreneurship. Some important practical implications can be derived from the investigation. First, in order to reverse the untapped potential of CF, the knowledge generated could be integrated into the decision-making process of both entrepreneurs and CF platform managers. Second, higher education institution managers could be involved in designing capacity-building programmes and financial literacy strategies for entrepreneurs that take into account the specificities of CF resulting from gender differences. The implementation of empowerment programmes that are designed to enhance women’s entrepreneurial self-confidence is another practical implication that is derived from the study, as the more conservative approach to the definition of the financing parameters damages the ability to take all the potential that CF could offer with respect to the ability to raise funding for sustainable-oriented projects. Third, for entrepreneurs who want to develop sustainability-oriented projects, the research suggests that, in addition to the shareholder structure, the composition of teams is a pivotal factor in the design and implementation of CF campaigns. Therefore, it is vital to ensure that work teams are carefully composed to obtain success. The findings of the study also provide significant practical insights for the design of communication materials and for the information about the risks, which are influenced by gender differences. The explicit communication of the preferred options in the design of the financing operation, which are dependent on gender, could allow entrepreneurs to better reach groups of investors closer to this profile, further enhancing the already recognised gender homophily effect (Serwaah et al., 2024).

From the public policy perspective, governments might enhance the regulation of CF by introducing the obligation to disclose on the platforms the gender of crowdfunders and their teams as a policy for the promotion, analysis, monitoring and support of gender balance. The research was undertaken in the Portuguese context, which is a positive contribution to address a gap in the literature. However, the fact that it focused on a single country could also be seen as a limitation of the research. For future research, it is suggested to develop a comparative study involving platforms from different types of economies and using cross-platform comparisons. It would also be interesting to compare the results between sustainability-oriented platforms and the traditional land-based CF platforms, in order to assess the extent to which the sustainable dimension can or cannot influence the design of CF operations. The utilisation of mixed methods in future research is also recommended, as well as a study on the effects of gender interaction in the use of CF. The integration of additional dimensions, such as entrepreneurial self-efficacy and uncertainty avoidance, in future studies would provide supplementary insights into the topic. A longitudinal study designed to evaluate the integration of the experience effect across both genders is a research avenue that deserves to be analysed in future studies. Furthermore, it would be valuable to integrate the examination of gender issues from the perspectives of entrepreneurs (crowdfunders) and potential investors through qualitative studies (focus groups).

Footnotes

Acknowledgement

FCT - Fundação para a Ciência e Tecnologia, under the project UIDB/05422/2020.

Authors Contribution

All authors have actively contributed to the article.

The main specific contribution of each author could be summarised as follows:

Susana Bernardino: Conceptualisation, formal analysis, methodology, project administration, software, validation, visualisation, writing—original draft, writing—review and editing.

J. Freitas Santos: Conceptualisation, methodology, project administration, supervision, validation, writing—original draft, writing—review and editing.

Leonor Vicente: Data curation, formal analysis, investigation, software, visualisation, writing—original draft.

All authors approve of the content of the manuscript and agree to be held accountable for the work.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest regarding the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.