Abstract

A sound investment selection is even more crucial since substantial information asymmetries enable managers to act advantageously after the investment is made. Crowdfunding has become one of the main ways that entrepreneurs may raise money in recent years. As a result of the growth of Internet platforms, business owners may now communicate directly with possible investors and avoid using conventional fundraising methods. But there are obstacles to overcome and no assurances of success while navigating the world of crowdfunding. In light of this, an increasing amount of research has been done to identify the elements of effective crowdfunding campaigns. The influence of an enterprise’s ethical and environmental emphasis on its performance on crowdfunding platforms is one area that has drawn more attention. To shed light on this subject, this research compares the performance of businesses that emphasize social and environmental issues against those that do not. Through an analysis of the decision-making processes and venture attributes of these endeavours, researchers aim to pinpoint the critical elements that lead to prosperous crowdsourcing campaigns. The study’s conclusions have significant ramifications for investors, crowdfunding platforms and business owners. They also provide insightful information on how to maximize participation in this expanding sector. Notwithstanding the significance of this expanding phenomenon, little is known about the mechanics of profitable lending-based prosocial crowdfunding and its consequences for the literature on business ethics. The results also have applications for other stakeholders in the realm of entrepreneurship funding. Only predictive entrepreneurs should collaborate with investors who are aiming for exceptionally robust growth.

Keywords

Introduction

Academics studying entrepreneurship, finance, management and economics are becoming more and more interested in the pertinent topic of venture valuation. Furthermore, according to some academics, entrepreneurship has a significant influence on the kinds of futures that can and cannot materialize (Bertoni et al., 2022). According to the resource-based approach, businesses with a greater variety of distinctive resources are, on the whole, more valued (Colombo et al., 2022). Scholars concur that a lemon premium is created by the frequently significant knowledge asymmetries that exist between venture insiders and outside investors (Wesemann & Antretter, 2022). Intangible assets make up the majority of an entrepreneurial venture’s assets, its operations are very unpredictable and its track record is frequently short (Dinh & Wehner, 2022). However, as worldwide angel investing platforms have grown in prominence, business angels’ (BAs’) decision-making process has evolved in recent years. These platforms make it easier for members to make both local and foreign investments, which broadens the scope of their investment strategies (Tajvarpour, 2023). Because it falls between traditional investment and charitable giving, crowdlending for sustainable new companies draws in non-professional investors with a variety of incentives. But our present knowledge of these many reasons for making judgements about crowdlending is incomplete (Cervantes-Zacarés et al., 2023). Because crowdfunding allows for the pooling of funds from a wide number of individuals whose investment decisions may not be driven just by projected financial rewards, it has become a viable alternative form of financing for entrepreneurs. Previous studies have demonstrated how crowdsourcing might help social network variables address the current financial gap (Rugina & Ahl, 2023).

The landscape of the entrepreneurial finance industry has been changing due to technological advancements and the emergence of social media, which has brought in new players, financial intermediaries and a range of growing market sectors (Hernández-Gracia & Duana-Avila, 2022). However, up until now, the majority of the viewpoint in the literature on entrepreneurial finance has been business- oriented, concentrating microscopically on the many sources of funding that entrepreneurs may use to obtain the capital they want for expansion and start-up (Lundmark et al., 2022). A macro perspective of the general dynamics between supply as well as demand in all of these market segments reveals fundamentally and qualitatively comparable traits, even though each entrepreneurial finance market sector does display its particularity at the micro level (Lam et al., 2022). Entrepreneurs seeking to secure seed capital for their projects must constantly go to sources with surplus cash, regardless of how the funding cycle is conceptualized (Lo & Rhee, 2022). From the perspective of the global economy, the global demand for entrepreneurial finance is made up of all the individuals searching for such money for their entrepreneurial activities, and the global supply of entrepreneurial finance is made up of all the various financing sources combined (Niemi et al., 2022). The future is ‘articulated, projected and made present’ through conversation. For example, it demonstrates how rhetoric in Dutch policymaking has given rise to five alternative futures (Peters, 2022). However, there is still much to learn about the discursive creation of the future through food entrepreneurship (Järvensivu & von Bonsdorff, 2022). Research indicates that entrepreneurship discursively creates futures via employing language and storytelling to convince prospective customers of the sustainability of the commodities, services or products their businesses offer (Cervantes-Zacarés et al., 2023). As a result, the study examines how entrepreneurs’ discourse affects the outcome of their loan campaigns and highlights some noteworthy value-added initiatives carried out by venture capital (VC) companies with operations in India.

Literature Survey

Berjani et al.’s (2023) examination of entrepreneurship policy documents in Kosovo and The Netherlands combines discourse and content analysis. By highlighting the variations between social settings and establishing a connection between policymaking and a contextual perspective on entrepreneurship, these findings contribute to a more nuanced understanding of the relationships among discourses, ideology, entrepreneurship and policymaking. By identifying the logic of justification they employ, which is typically characterized as orders of worth, Varas et al. (2023) looked into that question. This study offers novel insights into how, depending on the characteristics of a venture, start-ups may use particular linguistic patterns to explain advances.

The study by Sanda et al. (2023) sheds light on emotions in the decision-making processes of creative entrepreneurs and how their thought processes influence such decisions. The study’s conclusions provide comprehensive knowledge of the dynamics of creative entrepreneurs’ decision-making processes and how emotions function as a mediating component in those processes. With this knowledge, creative entrepreneurs may more effectively develop practices and skills for improved entrepreneurial decision-making. The link between effectuation logic, causation logic and company performance was investigated by Zhang et al. (2023). The findings indicate that there is a positive relationship between the two decision-making styles (DSs) and business performance, with the effectuation DS having a somewhat greater impact.

Estelami and Nejad’s (2023) investigation sought to ascertain the influence of managers’ cognitive and demographic traits on their choices to discontinue goods. The results show that cognitive style and academic profile have a major influence on how definitive product elimination judgements are. According to Botti & Monda (2023), using big data and a data-driven strategy might be especially beneficial for sustainable tourism (ST). The findings highlight the advantages of a data-driven strategy for tourism and entrepreneurship, highlighting the new directions that data usage opens up for decision-making in ST and HumEnt. A fundamental query that unofficial venture capitalists have been battling for decades is examined by Skalicka et al. (2023).

Our research indicates that there may be early indicators of an existential crisis for the project. BAs’ inclination for foreign investments and the part that investment and entrepreneurial experience play were studied by Croce et al. (2023). Consistent with the expectations derived from the local bias hypothesis, the internationalization of BAs’ investments is supported by both individual investment and entrepreneurial experience. Based on a sample of 78 angel investors, Vejmělková (2023) examined the investment and demographic features of BAs active in the Czech Republic. The results show that there are two different types of angel investors. On a crowd investment platform, Skare et al. (2023) created a thorough decision-support model for funding start-up ventures with VC money. For this reason, a model for aggregating data and determining the degree of decision-making about start-up finance was created. The current study looks at the various environmental orientations (EOs) and social orientations (SOs) of enterprises and how such orientations affect their performance in investment-based crowdfunding.

Research Problem Definition and Motivation

The study of entrepreneurship has produced a wealth of research that links the development rates of nascent businesses to certain cognitive and motivational traits of the entrepreneur, such as their desire for growth and the information and abilities they have acquired via education and experience. New businesses have several difficulties with their internal operations and organizational structure as they expand. These difficulties are especially noticeable in small, entrepreneurial businesses, which frequently go to outside investors for money to support their expansion due to their lack of resources and underdeveloped competencies. This work uses institutional theory, specifically institutional logic, to investigate how different investors manage human resources in small, entrepreneurial businesses. By contrasting a hyper-growth venture with a moderate-growth venture, we demonstrate how crucial it is for the founders to be able to make use of the financial and intellectual resources provided by BAs and VCs in a continuous process of interaction. To create a variety of growth routes, it is crucial to dynamically match the DSs of various investors and entrepreneurs as they interact.

Growth is a dynamic process that requires the entrepreneur to constantly communicate with different players in their ecosystem, particularly VCs and BAs in the case of start-up tech companies. Through a comparison between a hyper-growth venture and a moderate-growth venture, we highlight the criticality of the founders’ ability to leverage the financial and intellectual capital of VCs and BAs in an ongoing exchange of ideas. Even though studies have been looking into venture success for decades, empirical studies using archive data are still uncommon. As a result, this dissertation adds to the body of knowledge by providing fresh perspectives on how entrepreneurs and investors make decisions. These perspectives are based on previously unheard-of real-world data, such as thousands of actual, recorded deal screenings and evaluations—data that academics are typically not allowed to access. The dynamic matching of distinct DSs by investors and entrepreneurs is crucial to generating a variety of development routes during their interactions.

Research Gap

There is a big knowledge vacuum regarding how financing for entrepreneurship interacts with financial intermediation in diverse contexts, although the body of current research offers deep insights into several facets of entrepreneurship, such as policy analysis, decision-making procedures and investment behaviours. Research such as those conducted by Varas et al. (2023) and Berjani et al. (2023) emphasize the significance of reasoning and discourse in entrepreneurship, whereas Sanda et al. (2023) and Zhang et al. (2023) focus on decision-making and how it affects business performance. Nevertheless, little study has been done to combine these many components to investigate how financial intermediation processes help or impede entrepreneurial endeavours, especially in different socioeconomic contexts. This discrepancy emphasizes the necessity of thorough studies that relate funding strategies to the performance of entrepreneurs while taking intermediation dynamics and contextual factors into consideration to improve practice and policy.

Hypothesis Formation

According to the warm glow idea, people derive positive value from their contributions to worthy causes as well as from the tangible results of their activities. According to Allison et al. in 2013 and Cecere et al. in 2017, this theory has been effectively used to explain financing behaviour in reward-based crowdfunding as well as donation-based microlending for prosocial initiatives. Its application to investment-based crowdfunding, where financial and altruistic motivations coexist, has not yet been investigated.

Hypotheses on EO and SO

Hypothesis: a project’s EO as well as SO has a beneficial effect on its fundraising success in investment-based crowdfunding, even after controlling for other factors. This expands on the warm glow hypothesis and the knowledge that funding these initiatives can have two benefits (possible financial return and the fulfilment of making a difference in the community or environment.

H1a: An environmental focus greatly increases the likelihood that a crowdsourcing initiative will successfully raise funds.

H1b: A crowdfunding project’s social emphasis significantly increases the likelihood that it will successfully raise funds.

Number of Funders as a Mediator

The amount spent by each fundraiser and the total number of funders might influence the success of crowdfunding. We propose that the number of funders acts as a mediator in the relationship between a project’s environmental/social direction and its effectiveness in obtaining funds. According to Allison et al. (2013), initiatives with a larger potential for a warm glow effect will draw in more investors based on the warm glow idea. In a similar vein, Vismara in 2019 discovered that on equity crowdfunding (EC) platforms, initiatives with a focus on sustainability drew greater investor interest.

H2a: A project’s environmental emphasis positively affects how many donors choose to sponsor it.

H2b: A project’s SO positively affects how many donors choose to sponsor it.

H2a and H2b as mediators: The quantity of funders drawn to the project (H2a and H2b) acts as a partial mediating factor in the favourable impact of EO/SO on financing success (FS; H1a and H1b). Put differently, the positive perception attached to initiatives that focus on the environment or society attracts more donors, which in turn leads to increased financial success.

Proposed Research Methodology

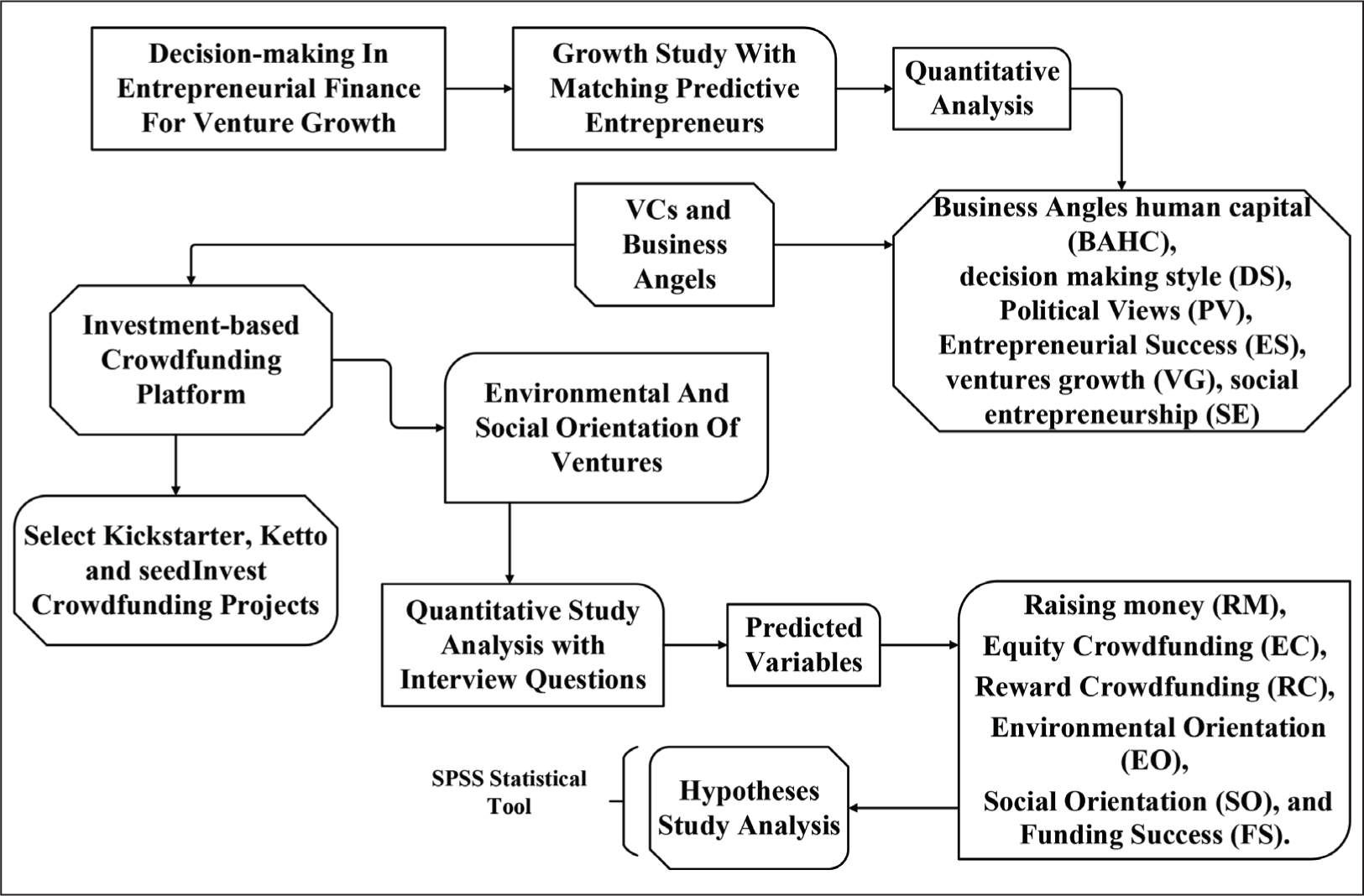

The market for funding entrepreneurs has evolved dramatically during the past few decades. There are currently several choices available to entrepreneurs seeking money to grow their innovative, start-up technology companies. These possibilities include formal VC, unofficial VC provided by different BAs and, more recently, EC. Strong financial literacy and decision-making skills enable people to evaluate their options, choose when and how to save and spend, shop around for the best deals before making big purchases and make long-term plans like retirement savings. Figure 1 displays the block diagram for the recommended work.

Conceptual Research Framework.

By connecting astute entrepreneurs with astute venture investors and BAs, more attempts are made to study the rise of VC. In this study, 100 entrepreneurs were able to secure funding. Both of these types of entrepreneurs can be considered representative within their respective categories, even though the sample is not typical of the population as a whole and undersamples entrepreneurs without capital. Since we gathered our data from two different institutional contexts, our results on that dimension have more external validity. Strong venture development is facilitated by predictive decision-making shared by crowdlending entrepreneurs, venture investors and business analysts. Thus, the research explores the DS in entrepreneurial funding and growth studies to encourage venture development by pairing predictive entrepreneurs with predictive venture capitalists and BAs. As a result, the current study examines how different EO and SO of firms impact their chances of success in investment-based crowdfunding.

Entrepreneurial DS in the Investment Process

The idea of effectuation—a method of decision-making for business owners in ambiguous situations—is explained in this section. According to Sarasvathy in 2001, entrepreneurs can adopt two primary styles—predictive and control- oriented—to effectively handle uncertainty.

Based on causality theory, predictive decision-making aims to forecast future events and make plans appropriately. By producing precise forecasts, this method is predicated on the idea that people may influence the future. In unpredictable situations when forecasts might not come true, this approach is constrained. Contrarily, control- oriented decision-making is concerned with influencing the future by acting and choosing in a way that is under one’s control. With this strategy, entrepreneurs focus on adopting controllable activities and adjusting to changing conditions, acknowledging that they cannot foretell the future with precision. Entrepreneurs who use this approach might feel more in control and empowered in unpredictable circumstances.

Matching Predictive Entrepreneurs

The application of matching theory to the situation of entrepreneurs looking for investors is covered in this section. Matching theory holds that individuals like to connect with others who have similar traits. This is especially significant for businesses looking to raise capital. Investment selections are often made based mostly on an investor’s expertise as an entrepreneur and their company strategy. Nonetheless, this study implies that investors could potentially take an entrepreneur’s gender and physical appeal into account. The study investigates how success and attitudes might be impacted by matching investors and entrepreneurs based on pre-existing variables, such as demographics. The study suggests that task-specific trait matching, as opposed to general demographic matching, may be more strongly correlated with entrepreneurial achievement. According to the assumptions, entrepreneurial success (ES) may be favourably impacted by matching investors and entrepreneurs based on pertinent characteristics, especially for high-growth enterprises. Furthermore, the biggest development may be achieved if all stakeholders have the same ‘highly predictive DS’. The text also highlights how important it is for investors to consider human capital and DS when making investments. Overall, the study emphasizes how matching theory plays a crucial role in comprehending the interactions between investors and entrepreneurs and raises the possibility that the matching process may be influenced by both conventional and unconventional elements.

H3: Other than the establishment and success of businesses, a wide range of ES outcomes are predicted by the social impact attributes.

H4: Strong growth and a wide variety of ES outcomes are favourably predicted when investors and entrepreneurs are matched.

The greatest growth may result from formal VCs and specific kinds of BAs making simultaneous co-investments. However, a highly predictive DS that all of the characters share seems to be a necessary need for this to happen. It is crucial since it makes it easier to communicate while creating a rigorous growth route and enhances investors’ opinions of a founder’s motivation and capacity to do so. The study’s analysis aligns with one of the possible investors, which is demonstrated to affect the likelihood of drawing investors as well as the viability and longevity of the entrepreneurs’ connection with them.

With an emphasis on the influence of human capital (HC) on the decision-making process of individual angels, Mitteness et al. in 2012 distinguish between angels based on their industry experience, operating experience from start-ups or established businesses, entrepreneurial background and prior investment experience, while Bonini et al. in 2018 separate HC by differentiating between managerial and entrepreneurial experience. The human capital, DS, political beliefs, entrepreneurial performance and venture growth (VG) of BAs are the factors used in this study.

Growth of Ventures

The relationship dynamics of raising equity financing to sustain robust growth in a technological start-up with co-investment from BAs and VCs are examined in this article. The goal is to determine which of the two theoretical frameworks—the cognitive approach to entrepreneurial finance or agency theory—best predicts how investors and entrepreneurs will interact. The study carried out a prospective case study, the analysis of which not only provides general support for both methods but also shows that the significance of agency-related and cognitive concerns varies according to investor type and process stage. From the initial interviews with the company’s two co-founders, the following descriptive data were obtained. Obtaining an overview of the whole dynamics of the business, from the first concept to the initial encounters with the different investors, was the aim of the semi-structured interviews. The co-founders revealed the identities of the three VC companies and the four BAs, and they located thorough investor profiles for the majority of them online.

Reward-based Crowdfunding

Equity-based models, such as reward crowdsourcing and EC, deal with investments made by people or institutions in unlisted shares or debt-based instruments by a company, usually a small to medium-sized enterprise. Here, business owners post an open call on the Internet to sell a certain quantity of stock or shares that resemble bonds in the hopes of drawing in a sizable investor base. Beyond VC, a wider range of uses has been made possible by the advancement of equity-based models. In this context, variants of the model such as real estate as well as property-based crowdfunding have thrived, enabling investors to obtain property ownership through the purchase of property shares. The cooperative model, also referred to as community shares, is an intriguing take on the equity idea. Funders’ contributions are gathered in this way to help a community initiative. Furthermore, most funders are more driven to participate in their local community than in financial rewards, even if certain revenue-generating community initiatives may be able to reimburse backers who desire to cash in their shares. A relatively modern addition to crowdfunding methods is invoice trading. According to Dorfeitner et al. in 2017, it is a ‘quick and simple method for small and medium-sized enterprises (SMEs) to raise short-term debt by refinancing their outstanding invoices through individual or institutional investors’. These short-term financing alternatives help SMEs by alleviating their cash-flow issues. They enable firms to sell their accounts receivable at a discount in exchange for rapid cash. Therefore, in contrast to other types of crowdfunding, this particular model focuses more on cash-flow management that is funded by community contributions than it does on fundraising.

Initiatives that focus on the environment and society have a lot of potential to support sustainable development. Many believe that by giving these businesses access to capital, crowdfunding will possess the ability to fully realize their potential. Therefore, the current study looks at how enterprises’ varying degrees of EO and SO affect their ability to succeed in investment-based crowdfunding. Crowdfunding with an investment focus offers a novel financial instrument to assist in the establishment, maintenance and expansion of Main Street enterprises. Through online platforms, equity-based crowdfunding provides a variety of methods for people and institutions to participate in start-ups and SMEs.

This covers EC, in which business owners sell shares; real estate crowdfunding, in which investors purchase real estate shares; community shares, emphasizing social effect; and invoice trading, in which SMEs finance loans by selling unpaid bills at a discount.

H5: Factors that increase the success probability of a crowdfunding project.

H6: Investment-based crowdfunding can be a viable source of entrepreneurial finance.

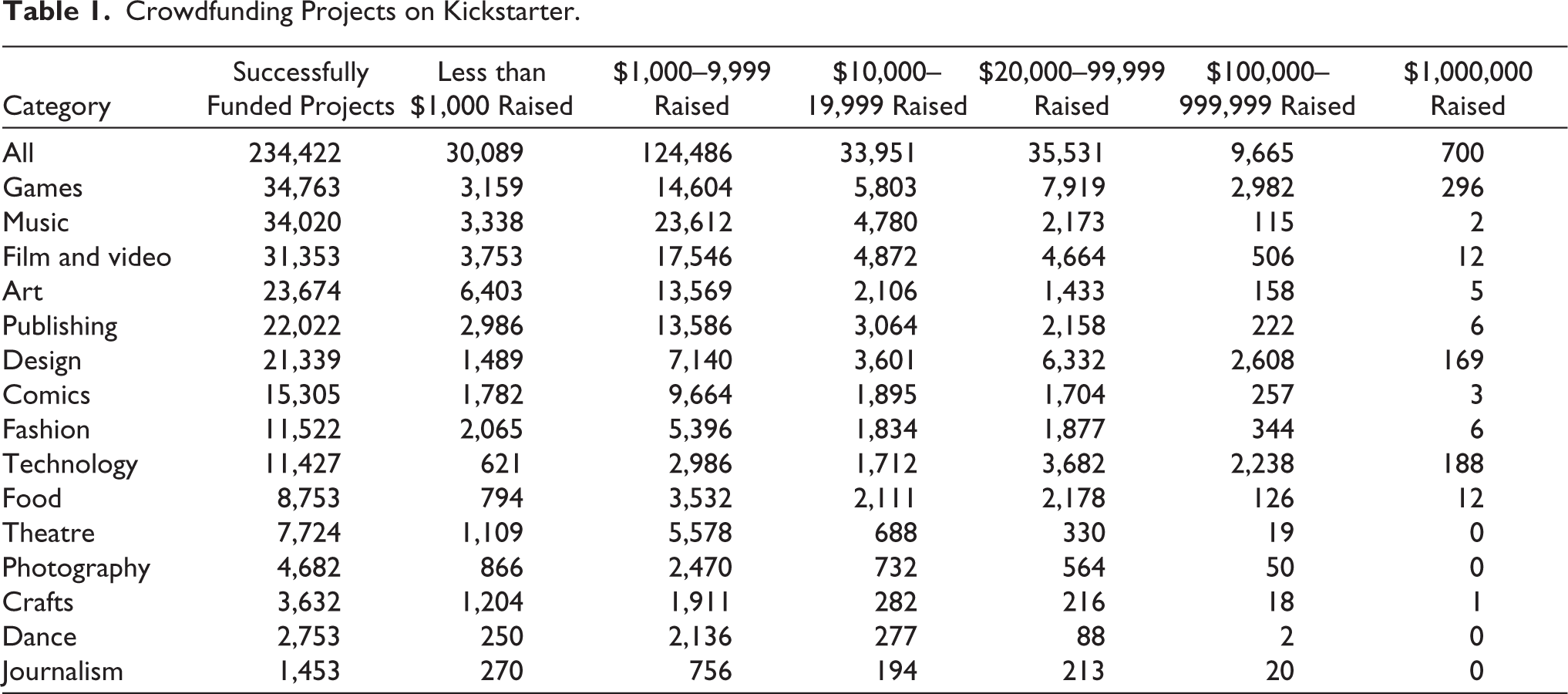

This study’s empirical component is derived from a thorough literature analysis, 30 in-person interviews and the answers to 20 BA and 44 VC questionnaires. A brief postal questionnaire was created using the results of the interview as a reference, and it was thoroughly pilot-tested with investors the author knew. For sustainable businesses that frequently struggle to obtain loans from conventional finance sources, crowdfunding offers enormous promise. Researchers are interested in these endeavours because they can address urgent environmental and societal challenges, and recent research has already found elements that boost the success of these kinds of projects through crowdsourcing. The potential of sustainable crowdfunding to support sustainable development and the differences between crowdfunding initiatives with an environmental, social or sustainability focus and those with a traditional orientation are still unexplored. The investment-based crowdfunding projects on Kickstarter, Ketto and SeedInvest were categorized using the entrepreneurship typology proposed by Thompson and associates, based on a quantitative dataset.

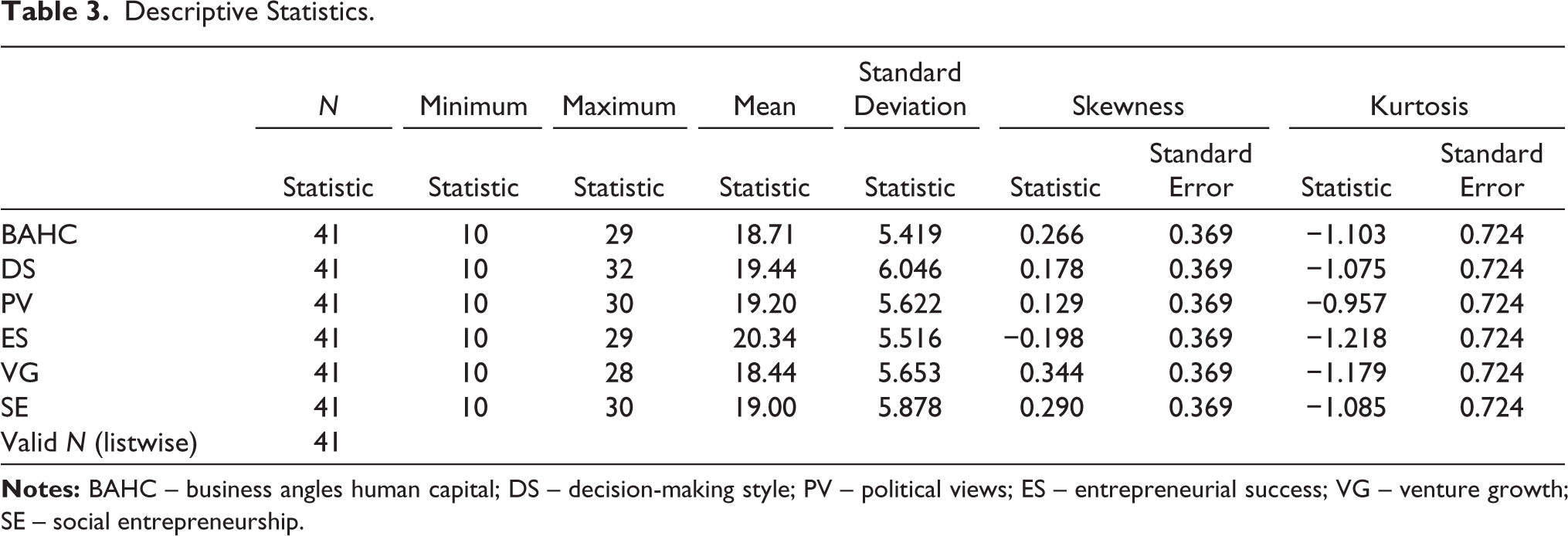

Table 1 lists Kickstarter users according to their creation and project support actions. The following two user groups were identified by the article: (a) all-time creators (AT creators), who only developed projects and did not support other projects; and (ii) active users, who supported other projects in addition to their own. Table 3 presents descriptive statistics for six variables (BAHC, DS, PV, ES, VG, and SE) based on a sample size of 41. For each variable, the table reports the minimum and maximum values, mean, standard deviation, skewness, and kurtosis. The mean scores range from 18.44 (VG) to 20.34 (ES), with standard deviations indicating variability in responses. Skewness values close to zero suggest a symmetrical distribution, with most variables showing slight positive skewness, while ES exhibits negative skewness, indicating a leftward tail. Kurtosis values, all negative, suggest distributions that are flatter than normal. Overall, these statistics provide insights into the central tendency and distribution characteristics of the measured variables. There are 71,319 (53.9%) current users and 60,967 (46.1%) AT producers, as indicated in Table 3. On average, each AT creator produced 1.12 projects. These artists sought funding with the sole intent of completing their ideas. It is interesting to note that these inventors only produced one or two projects, according to the average amount of projects made per AT creator. On average, though, each of the 71,319 active users supported 6.45 projects and developed 1.25 projects. Even though they funded a great deal of other projects, these active users developed a few more projects than AT creators.

Crowdfunding Projects on Kickstarter.

Inter-reliability Analysis.

aType C intraclass correlation coefficients using a consistency definition. The between-measure variance is excluded from the denominator variance.

bThe estimator is the same, whether the interaction effect is present or not.

cSince the interaction impact is not estimable otherwise, this estimate is calculated on the assumption that it does not exist.

Descriptive Statistics.

Crowdfunding Platforms

Today, Kickstarter stands among the most widely used crowdfunding sites globally. By avoiding conventional fundraising channels and expanding the market for specialized productions, the website helps creators raise money for their ideas. Every project has an end date, and no money is taken in if the predetermined financing target is not reached. The website only accepted projects with a US base until October 2012; in September 2013, it opened to the UK and then Canada. Backers of the project do not need to be US citizens. To analyse the social and environmental endeavours, this study used data from 15 Kickstarter projects. Ketto is a crowdfunding website with an array of campaigns available, situated in Mumbai. There are campaigns for personal care, sports, healthcare, education and animal welfare. Additionally, it offers backers tax incentives and has a section devoted to initiatives that require immediate funding. Additionally, Ketto provides a cash collection service. Apart from its plethora of advantages, Ketto is among the several crowdfunding platforms available in India. SeedInvest is an additional choice for Indian companies. While the services on both sites are comparable, the amount of fees each site charges to receive your gift varies. Republic charges a modest platform fee, while SeedInvest is free to use. Republic charges 2–5% of the money invested, and this cost is around 3% of the total amount generated. Depending on the platform, the fee might be as much as 8% of the entire amount. These platforms were selected because of their thematic openness, which allows crowdfunding campaigns to be launched by conventional companies as well as those with an environmental and social focus.

Data Collection

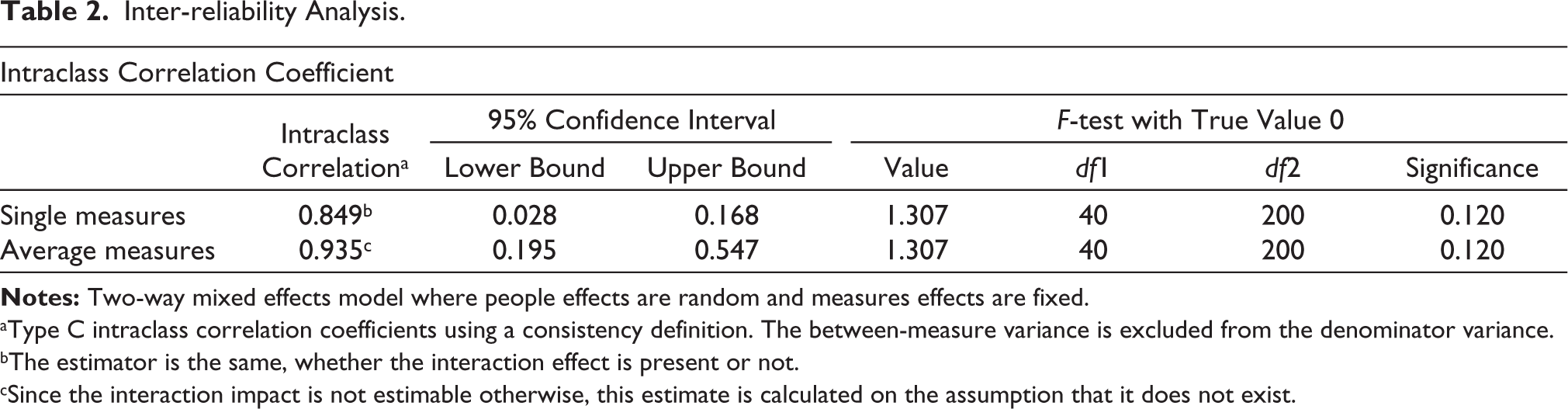

To investigate the effect of SO and EO on fundraising success, this article outlines the techniques utilized to gather and measure data from crowdfunding projects in India. Four well-known crowdfunding sites for investments that provide investors with financial benefits were the sources of data that the researchers gathered. Two independent coders were given training and comprehensive instructions, and they used a manual coding procedure to assess a project’s environmental and social focus. The degree of EO and SO was measured by the researchers using a 7-point scoring system, which went from ‘−3: strong negative environmental/social effects’ to ‘+3: strong positive environmental/social effects’. This method transcends basic yes/no measurements and enables a more nuanced evaluation of the impact of a project. By determining Krippendorff’s alpha values, the study confirmed the coding technique’s dependability. The results demonstrated a high degree of agreement amongst the coders (0.849 for environmental and 0.935 for social). The use of quantitative techniques to differentiate between different degrees of effect inside projects is made easier by the manual coding methodology, which also permits the investigation of complex variables such as the impact of SO and EO on FS.

Using a pre-planned coding scheme, a full-text analysis of each crowdfunding campaign’s project site was performed in April 2018 to manually gather the data. The dataset contained all 320 projects that were finished on these platforms from the platforms’ debut and 19 April 2018. As a result, the dataset includes both successfully funded initiatives and those that fell short of their financing goal. All models that are run rely on the complete dataset, which includes both successful and unsuccessful projects. With the exclusion of two projects from the dataset (explained below), the final sample comprises 318 projects.

Experimentation and Results Discussion

The descriptive statistics (means [M] and standard deviations [SD]) and correlations between all the variables in the analysis are shown in Table 1. All correlations, as shown in Table 1, are well below the 0.8 threshold, indicating that the variables under consideration for the study each reflect a distinct concept. The table presents data on successfully funded projects across various categories, detailing the number of projects that raised different funding amounts. Overall, there are 234,422 projects, with 30,089 raising less than $1,000 and 700 achieving $1 million or more. Categories like Games and Music have the highest numbers, with 34,763 and 34,020 projects, respectively. Notably, the Games category had 5,803 projects raising between $10,000 and $19,999. In contrast, Journalism shows the lowest activity, with only 1,453 projects. The table highlights the diversity in crowdfunding success across different sectors.

Table 2 presents the results of an inter-reliability analysis using the Intraclass Correlation Coefficient (ICC) for both single measures and average measures. The ICC for single measures is .849, indicating good reliability, while average measures show a higher ICC of .935, reflecting even stronger reliability. The 95% confidence intervals for both measures range from .028 to 1.307, suggesting some uncertainty in the estimates. The F-test results, with a significance value of .120, indicate that the reliability is not statistically significant at the traditional level, but the high ICC values suggest that the measurements are consistent.

The ideas of zero-order correlations, SD and descriptive statistics are presented in Table 3. A descriptive statistic calculates the normality and distribution. It may be calculated by utilizing kurtosis and skewness. The kurtosis value is closer to zero for business angles human capital (BAHC), DS, political views (PV), ES, VG and social entrepreneurship (SE), suggesting that the data are more consistently distributed. The following descriptive statistics show that all variables are almost huge negatives, which suggests that the distribution is highly platykurtic (flat) or symmetrical. The researcher computed correlation analysis, full regression models and coefficient of determination from the average means calculated in the descriptive statistics to determine the true relationship between the dependent variables PV, ES, VG and SE and the independent variables BAHC and DS.

Multiple Regression Analysis of Variables

SPSS Statistics provides a lot of output tables for linear regression. Three primary tables in this section are necessary to comprehend the outcomes of the multiple regression process, assuming that no assumptions were broken. To ascertain the relationship between variables and the automobile industry’s output quality, the researcher employed a multivariate regression analysis. In this test, the proportion of the dependent variable’s total variance that the independent variable explains is calculated.

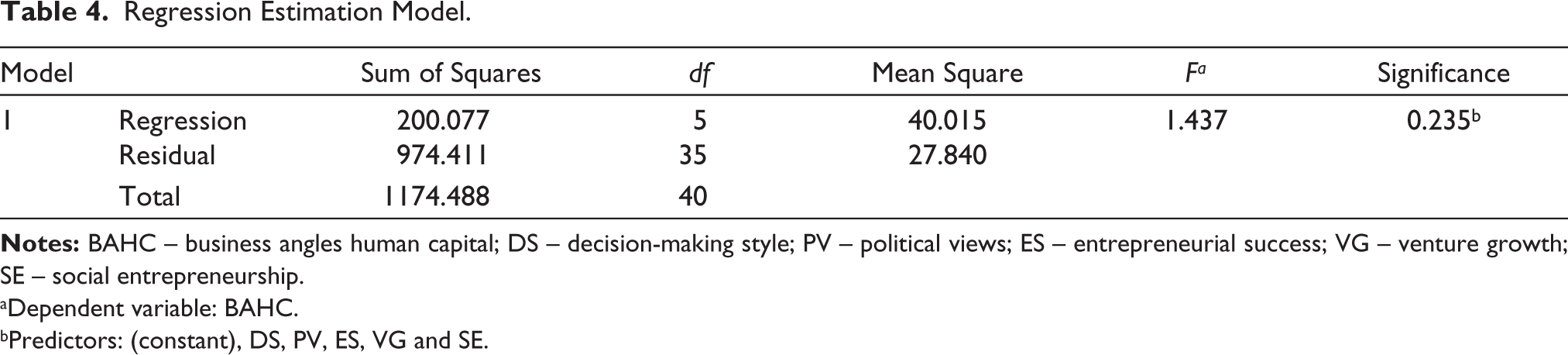

The F-ratio in ANOVA (Table 4) assesses how well the entire regression model fits the data, with BAHC as the dependent variable (footnote a) and the predictors including DS, PV, ES, VG, and SE (footnote b). Given that the table shows the independent components statistically significantly predict the dependent variable, the regression model appears to be a good match for the data. The null hypothesis, which posits that the population R in the whole regression model is zero, is tested. Meanwhile, this null hypothesis is excluded from the data if p < 0.05.

Regression Estimation Model.

aDependent variable: BAHC.

bPredictors: (constant), DS, PV, ES, VG and SE.

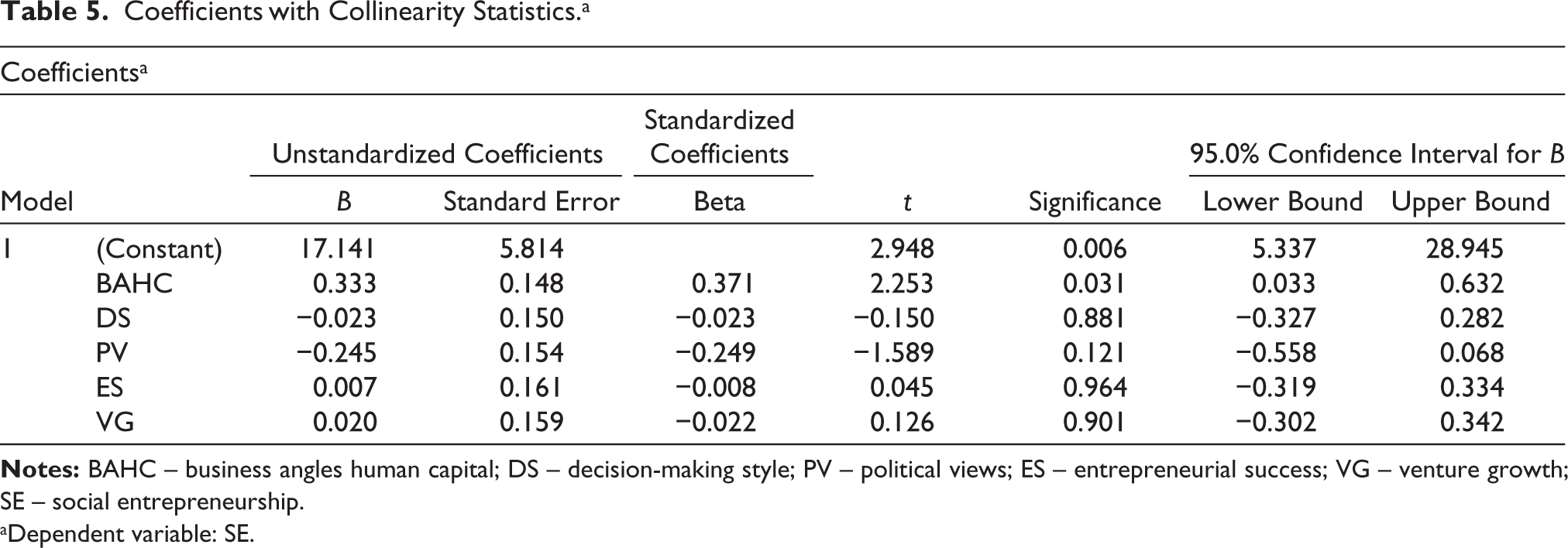

Table 5 illustrates the use of unstandardized coefficients to determine the relationship between the dependent variable, SE, and the independent variables while maintaining all other independent variables constant. This approach assesses whether the population’s unstandardized (or standardized) coefficients equal 0 (zero). The t-value and corresponding p-value are provided in the ‘t’ and ‘Sig’. columns, respectively. The managerial hubris coefficients are not statistically significant, with a p-value greater than .05. Additionally, when examining the multiple regression model for multicollinearity, the tolerance values were found to be less than 0.1, with corresponding values of 0.006, 0.031 and 0.121, indicating potential multicollinearity issues among the independent variables.

Coefficients with Collinearity Statistics.a

aDependent variable: SE.

Correlation Analysis of Predictive Entrepreneurs

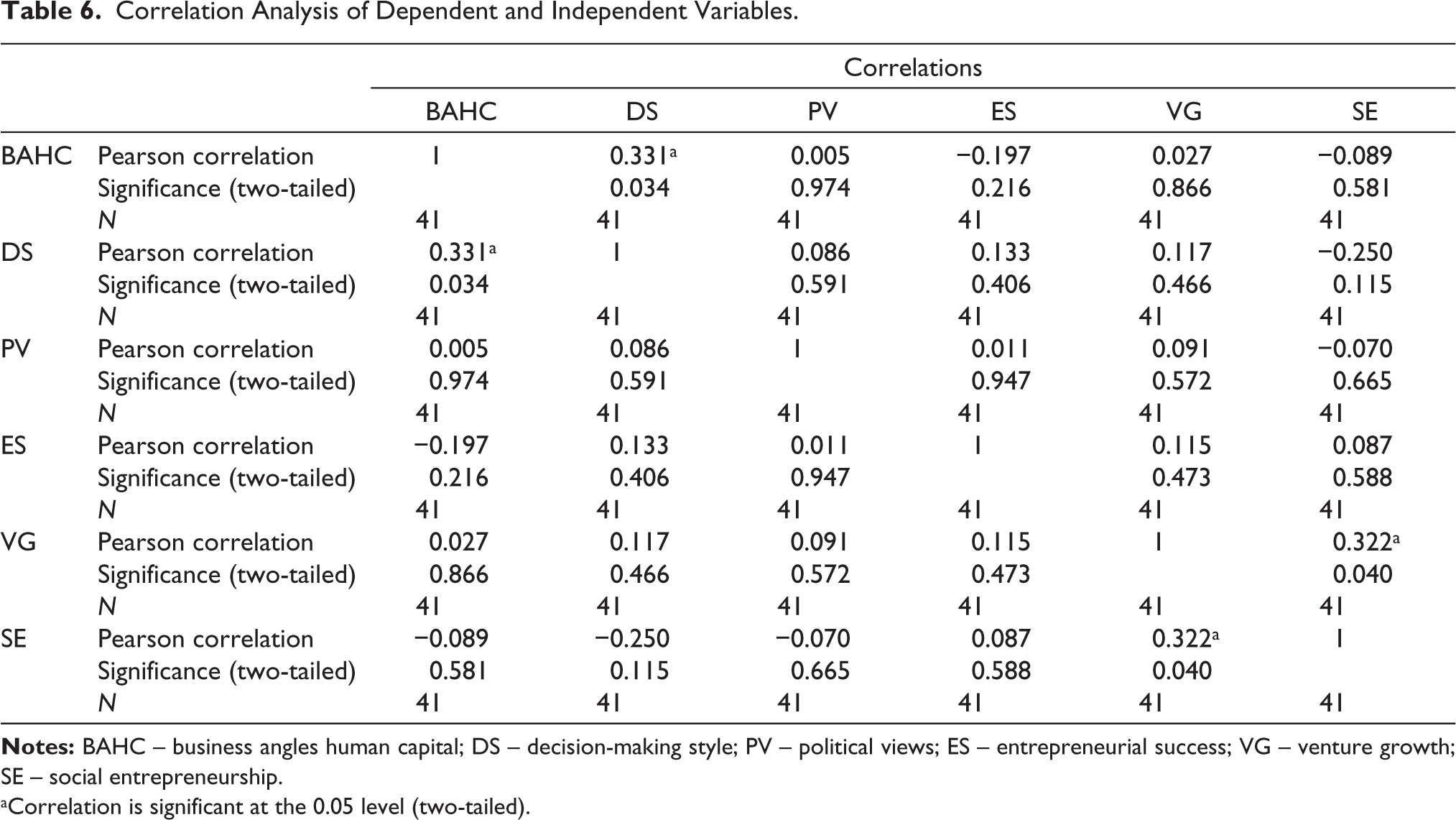

To determine whether there was any association between the independent and dependent variables, the Pearson product-moment correlation analysis was used in this study. The range of correlation coefficients is 1.0 plus or minus one. A change in the independent item will not affect the dependent object when using a coefficient of zero technique since there may be no relationship between the two things. Table 8 displays the association table.

Table 6 shows that BAHC has a substantial positive correlation (r = 0.331) with VC, indicating a favourable link, whereas other components have a negative correlation with the variables. Additionally, DS and BA show a strong association, indicating DS’s great significance. For DS and ES, there was a substantial positive link with a correlation coefficient of r = 0.133. Although VG and project evaluation might have a positive connection of r = 0.027, it is not statistically significant. For the dependent variable, investment motivation (IM), the correlation coefficients reveal the following IM has a strong positive correlation with BAHC (r = 0.275) and a moderate positive correlation with DS (r = 0.215). However, the only element that was not significant was SE. Examining the Pearson correlation with both the dependent and independent variables reveals that flexibility only exhibited a negative link (r = –0.150) and was insignificant in most situations.

Correlation Analysis of Dependent and Independent Variables.

aCorrelation is significant at the 0.05 level (two-tailed).

Investor-based Crowdfunding Platform

The following two datasets are used in the study: the Backer Location dataset and the Kickstarter Project dataset. All of the Kickstarter projects that were started between 2009 and 2020 are covered in detail by the Kickstarter Project dataset. Project title, category and subcategory; location (city, state or nation for US-based projects); financing target (in US dollars as well as original dollars); pledged amount (in dollars); number of supporters for each project; and more are included in this. The Kickstarter Project dataset contains the 506,199 funded projects, both successful and unsuccessful. The overall amount committed for each geographic region, the Backer region dataset, contains information about the supporters’ nation and state. The following are the elements that were considered: funding success (FS), SO, EO, EC, reward crowdfunding (RC) and raising money (RM).

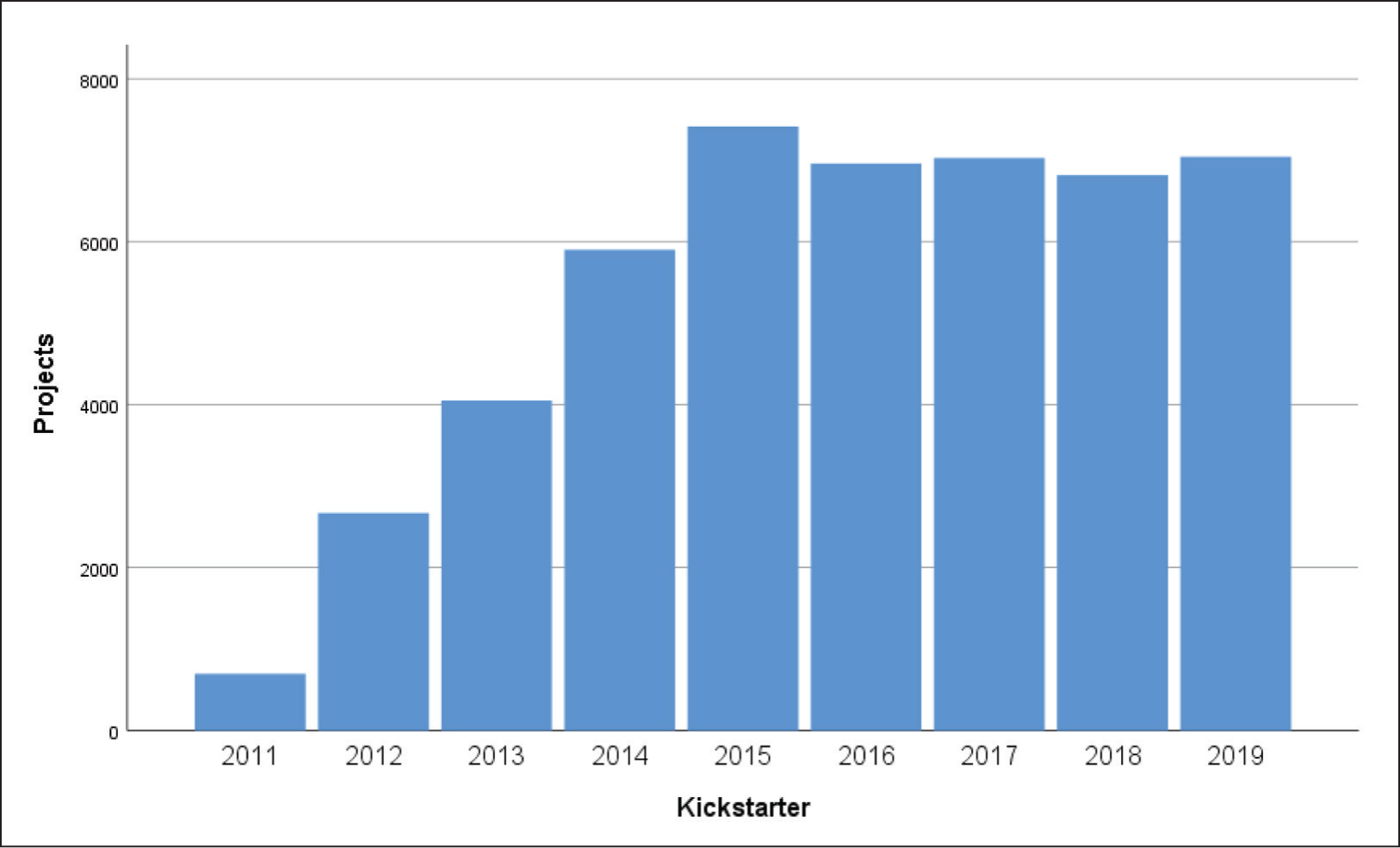

With a colour split based on project status, the bar charts independently display the number of Kickstarter projects by category and the number of supporters by category. The aim is to gain an understanding of many categories and the degree of ease with which initiatives in disparate businesses may be completed successfully. The ‘Project by Category’ bar chart shows investors and Kickstarter organizations which category is most popular. ‘Film’ is the most popular category. Regarding the projects by tiers, the total number of projects raising between $100,000 and $5000,000 decreased from 25 in 2018 to 19 in 2019, while there was almost the same number of projects totalling $500,000 or more as in 2018 (six projects in 2019 for five in 2018). All of the projects that raised $100,000 or less were responsible for the (modest) rise observed in the video games category (Figure 2).

Kickstarter Total Number of Projects.

Regression Analysis

Since every dependent variable is a metric, linear regression analyses were used. Each model that is executed is derived from the complete dataset, encompassing both unsuccessful and prosperous endeavours. Moreover, all the models are statistically significant and explain relevant amounts of the variance in the dependent variable. All of the variance inflation factors are much below the crucial threshold of 10, suggesting that there are no issues with multicollinearity in any of the models.

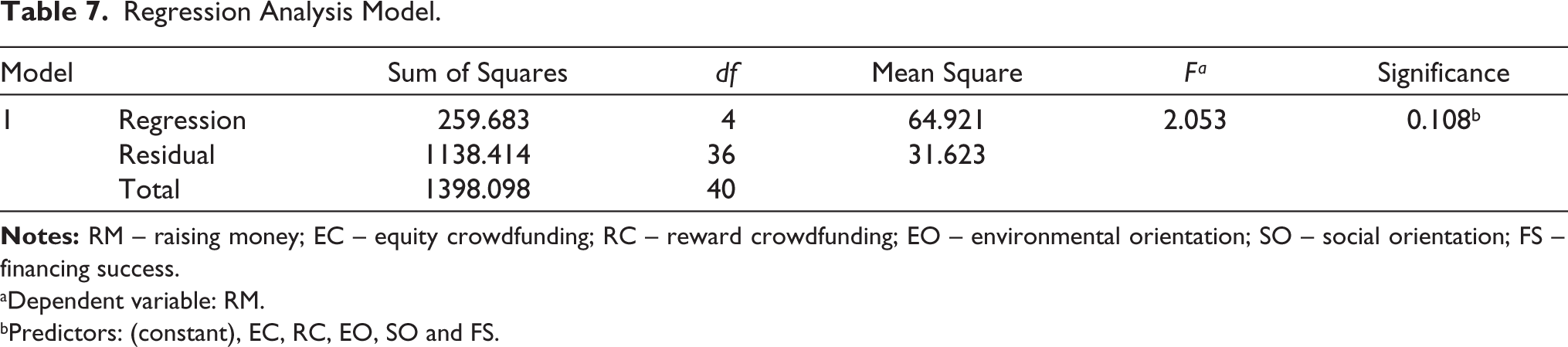

The overall regression model’s ability to fit the data properly is tested by the F-ratio in the ANOVA (Table 7). The dependent variable in this analysis is RM (footnote a), while the predictors include EC, RC, EO, SO, and FS (footnote b). Given that the independent components statistically significantly predict the dependent variable, Table 7 demonstrates how well the regression model fits the data. It assesses the null hypothesis, according to which the population R of the whole regression model is zero. Meanwhile, the results reject this null hypothesis when p < 0.05.

Regression Analysis Model.

aDependent variable: RM.

bPredictors: (constant), EC, RC, EO, SO and FS.

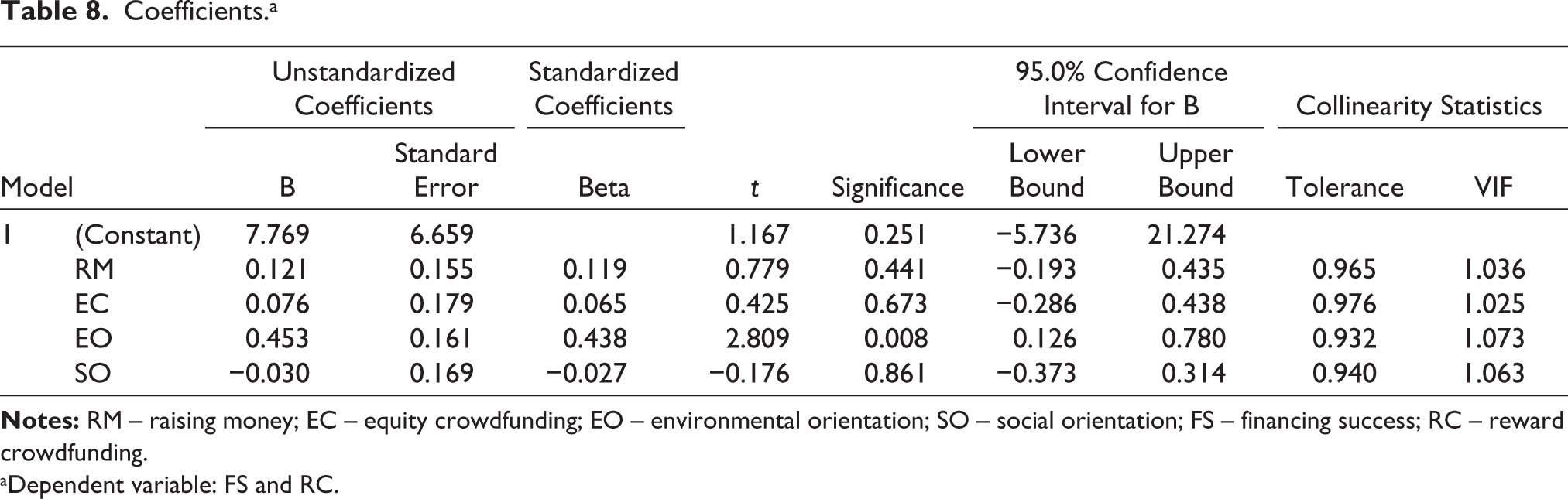

The unstandardized coefficients in Table 8 show the coefficient table’s variation between the dependent and independent variables while all other variables are held constant. This establishes if the unstandardized or standardized coefficients of the population equal 0 (zero). The ‘t’ and ‘Significance’ columns provide the t-value and related p-value, respectively. The coefficients are not statistically significant in this case since the p-value is more than .05. Upon examining the multiple regression model with tolerance for multicollinearity, the following values were obtained: 0.499, 0.014, 0.010 and 0.017. In general, the tolerance value was less than 0.1, meaning that this requirement was met.

Coefficients.a

aDependent variable: FS and RC.

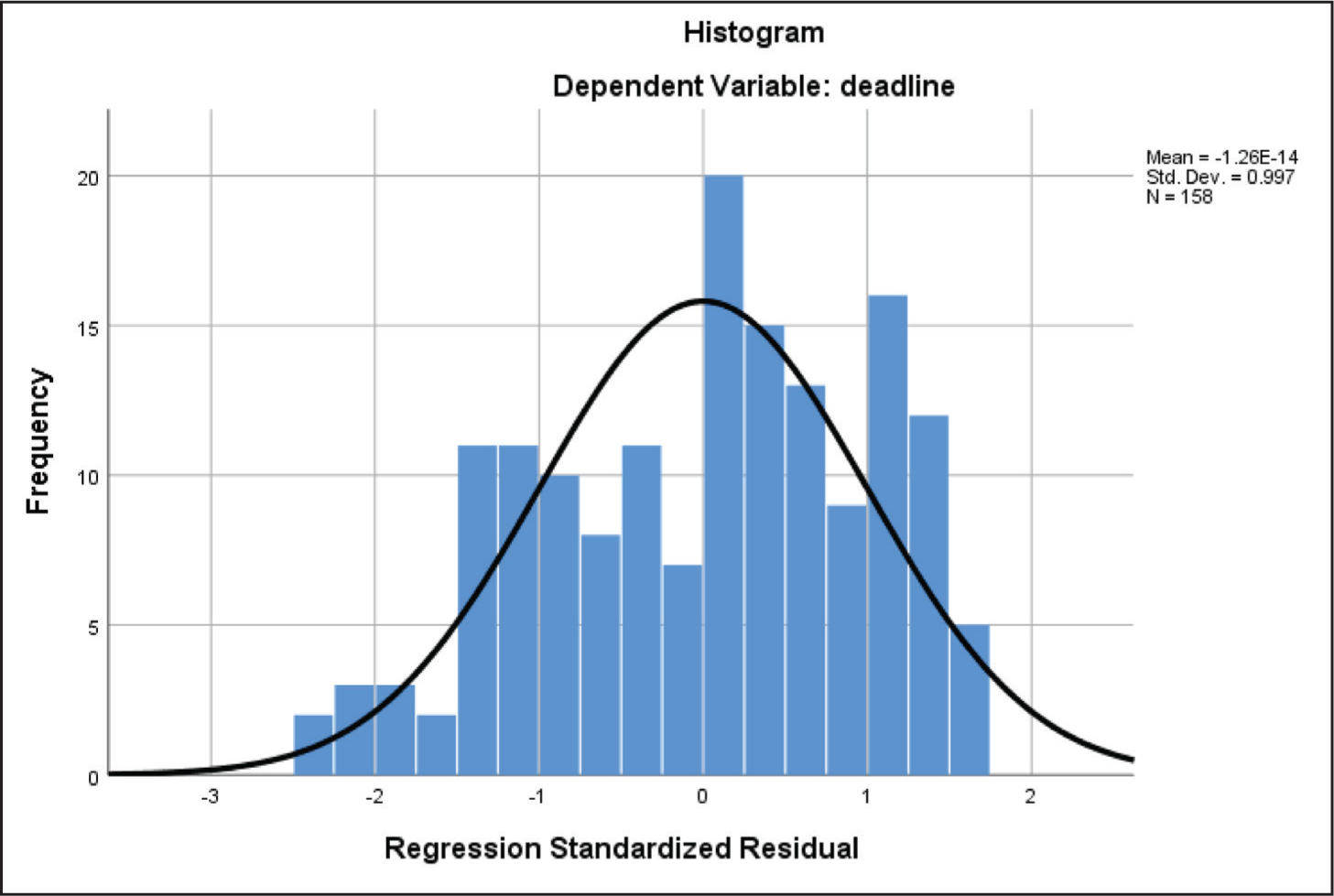

Histogram-normality Test for Deadline.

The normality test histogram chart for the dependent variable deadline in crowdfunding projects is shown in Figure 3. The consequence of the performance reveals that the histogram line produces a bell. This data value is often varied, making it transmitted naturally.

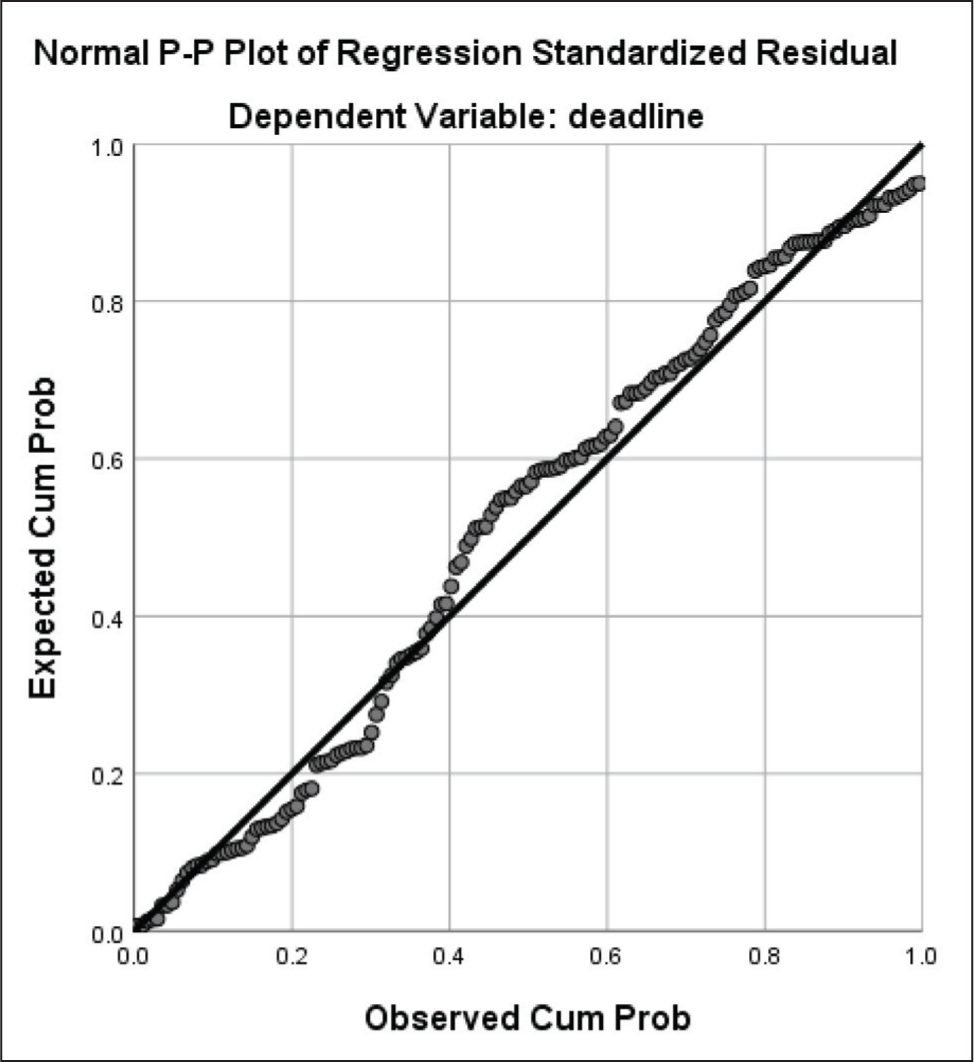

Figure 4 depicts the normal P–P plot of the normality test for deadlines in Kickstarter projects with the expected cumulative probability and the observed cumulative probability. The P–P plot chart demonstrates that the point cluster is tightly along the diagonal line. This implies the respondents filled out the circulated poll or questionnaires normally distributed. Therefore, it can be concluded that the information about the regression model meets the assumption of normality.

Normal P–P Plot of Kickstarter Project Deadlines.

Figure 5 depicts the histogram chart of the normality test for the dependent variable launched in Kickstarter projects with regression standardized residual in terms of frequency. The performance result indicates that the histogram line is bell-shaped. Similarly, this data value is also variated, which makes it normally distributed.

Histogram-normality Test for Launched Projects.

Normal P–P Plot Analysis of Crowdfunding Data.

Figure 6 depicts the normal P–P plot of the normality test for launched projects with RC with the expected cumulative probability and the observed cumulative probability. The P–P plot chart demonstrates that the point cluster is tightly along the diagonal line. This implies the respondents filled out the circulated poll or questionnaires normally distributed. Therefore, it can be concluded that the information about the regression model meets the assumption of normality.

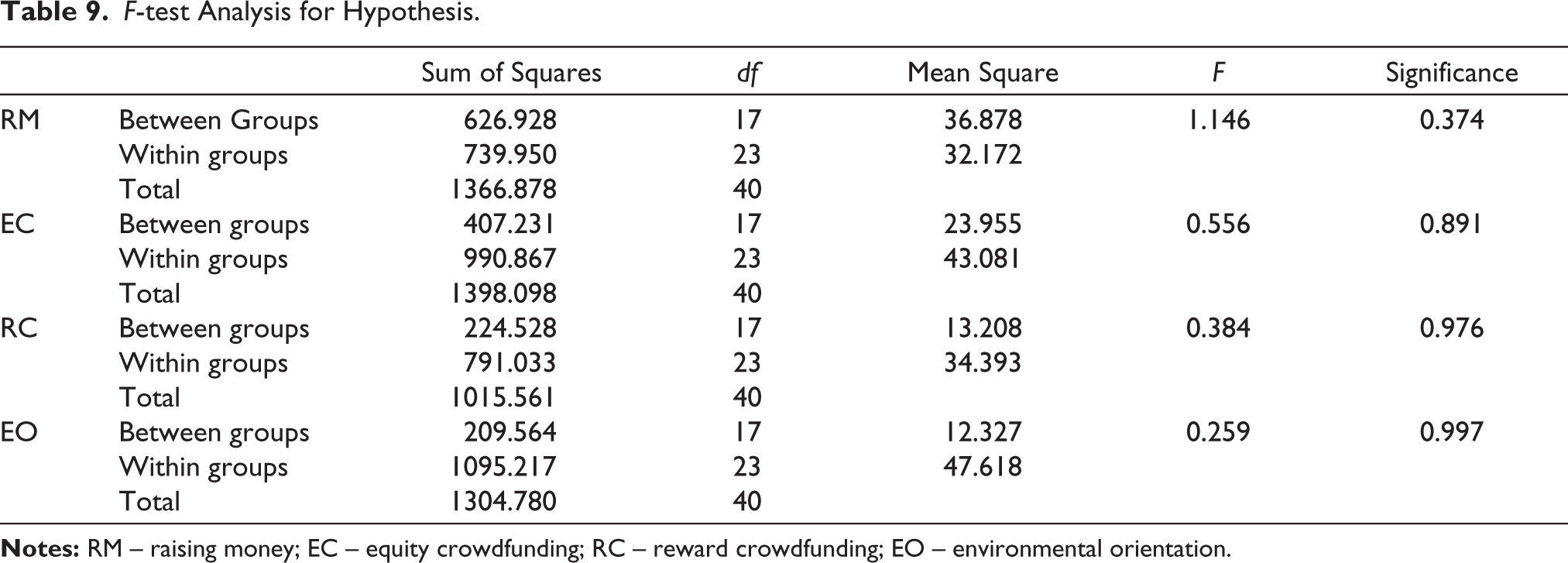

F-test Analysis

The statistical F-test has been considered to determine whether a group of attributes or its subsets are jointly significant for the primary attribute. An F-test is any statistical test in which the test statistic has an F-distribution under the null hypothesis. For this study, the Granger causality test’s null hypothesis is as follows. It is a variation of the Granger causality theory itself. Another way to visualize this hypothesis is as a vector with all of the coefficients set to zero.

Based on these findings, the research focuses on the F-statistic provided in ANOVA (Table 9) together with its p-value, which is shown in the table as significance F. This selects 0.05 as the level of significance. The research obtained the values 374, 891,976 and 0.997 because the t-test of significance for each predictor variable only establishes whether each predictor variable is individually significant, while the F-test of overall significance establishes whether all of the predictor variables are jointly significant. This suggests that crowdsourcing with an investment focus may be a good way to support new ventures.

F-test Analysis for Hypothesis.

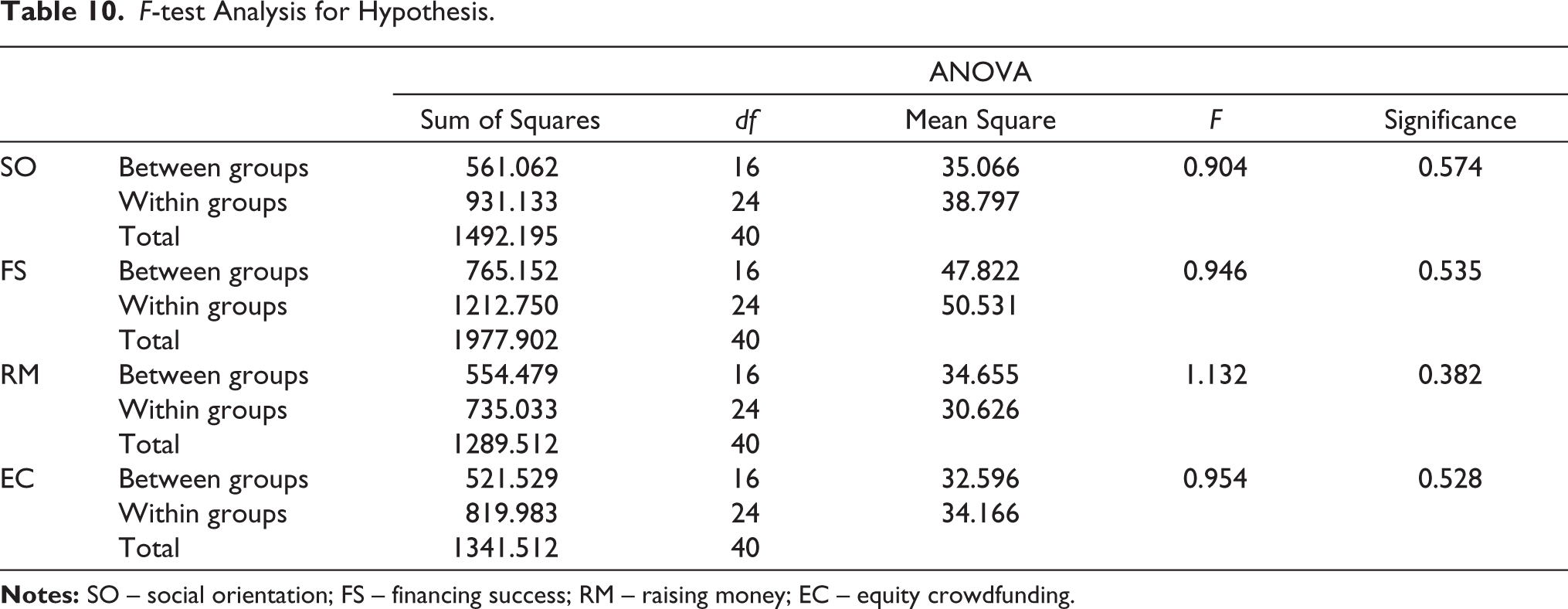

The combined impacts of dependent variables on crowdfunding projects, such as RM, EC, RC, SO, EO and FS, are examined in Table 10. This suggests that there is considerable value in both the independent and dependent variables. As a result, it has a positive correlation with the factors’ combined impact. Consequently, it confirms that talent acquisition benefits the company, which supports H4. In this sense, the results add to our understanding of the relationships between the variables that raise the likelihood that a crowdsourcing project would succeed.

F-test Analysis for Hypothesis.

According to this investigation, EO has a beneficial impact on investment-based crowdfunding initiatives’ ability to raise funds. Thus, it adds credence to the often-expressed belief that crowdfunding may promote sustainable development by funding initiatives that improve environmental conservation. The study’s findings are consistent with those of Calic and Mosakowski in 2016, who discovered that EO positively impacted FS in the context of reward-based crowdfunding in the United States. However, our examination of investment-based crowdfunding success in Germany and the USA shows no evidence of a beneficial influence of SO, which runs counter to their findings and to further analyses on donation-based microlending.

As a result, several distinctions between donation-based microlending and reward-based crowdfunding have been noted. The association between a project’s financial success and EO is adversely mediated by the average funding amount of the initiative. Furthermore, the association between a project’s SO and its effectiveness in raising funds through RC is favourably mediated by the average financing amount of the project. The influence of agile information update and communication, two distinct strategic activities that founders might do during fundraising campaigns, on crowdfunding success was examined by Eunjun Jung et al. in 2022. The findings corroborate the theories and demonstrate that while two-sided communication stimulates investors, information updates from company founders have non-linear quadratic connections with fundraising performance.

Research Conclusion

In an entrepreneurial context, making decisions may be difficult due to a variety of unknowns that need contextual intelligence understanding and a dynamic business environment. These challenges are made even more acute in developing countries due to regulatory instability and change. One of the primary challenges is the uncertainty and dynamic nature of the business environment, especially in emerging economies with regulatory flux. Crowdfunding provides entrepreneurs with an alternate form of capital, particularly EC and crowdlending for sustainable ventures. The study identifies different investor segments with varying preferences and motivations, with human values playing a significant role in shaping these segments. The research provides recommendations for entrepreneurs, crowdfunding platforms and policymakers to capitalize on the growth of crowdfunding for sustainable ventures. The study uses SPSS software for data analysis and finds that environmental as well as social crowdfunding projects tend to use marketing more than conventional projects. Social projects tend to be smaller in scale with lower funding targets, while conventional projects use crowdfunding for service and organizational innovation. The study also finds a positive correlation between EO, SO and FS on investment-based crowdfunding platforms. Future research opportunities include exploring new crowdfunding models like royalty-based crowdfunding and comparing crowdfunding with other financing options like business incubators and VC. All things considered, the framework emphasizes how critical it is to comprehend investor motives and customize methods for various players in the crowdfunding ecosystem. It highlights the increasing importance of crowdsourcing, especially for projects that have an environmental or social focus, and advises entrepreneurs to make their project’s environmental or social objective obvious to draw in a larger pool of investors.

Footnotes

Data Availability Statement

Data sharing is not applicable to this article as no datasets were generated or analysed during the current study.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.