Abstract

Introduction

The increasing cost of long-term care is an issue faced by older care recipients and their families. The financial burden of long-term care for older adults may reduce the well-being of family caregivers. However, it remains unclear how family caregivers experiencing financial strain adapt to both caregiving and daily life.

Objective

This cross-sectional study examined the caregiver characteristics and financial burden associated with the cost of utilizing long-term care services for an older relative among 427 family caregivers.

Methods

Potential influencing factors were compared among three categories of financial burden and their impact on the lives of family caregivers. The chi-square test was used for categorical data (e.g., sex, marital status, employment status), and the Kruskal–Wallis test for continuous or ordinal data (e.g., age, self-rated health, annual household income).

Results

The proportion of family caregivers experiencing financial burden was statistically significantly higher among those living with an older relative compared with those whose older relative was in a care facility (68.2% vs. 57.3%, respectively; p = .049). Among 198 family caregivers living with an older relative, a greater severity of functional disability in an older relative was statistically significantly associated with financial burden and its impact on their lives (p = .004). On the other hand, among 229 family caregivers of an older relative utilizing institutional care, those bearing the costs of long-term care were statistically significantly more likely to experience financial burden and its impact on their lives (p < .001).

Conclusion

A financial shortage among older relatives was found to have a negative impact on the work, private life, and care choices of family caregivers. These findings may inform the development of support measures tailored to caregivers with a limited household income.

Introduction

Japan is experiencing a more rapidly aging population than other Organisation for Economic Co-operation and Development countries (Organisation for Economic Co-operation and Development, 2023). In 2022, 29.0% of the population of Japan, or 36.24 million persons, were aged ≥65 years (Cabinet Office, 2025). Among these older adults, 18.8% (6.81 million persons) required assistance with activities of daily living (ADL) and other forms of personal support because of functional disabilities and were receiving long-term care services (Cabinet Office, 2025). The long-term care insurance system in Japan was implemented in 2000 (Houde et al., 2007). The purpose of this system is to promote independence among older persons with functional disabilities and reduce the care burden for households by covering the costs of home-based, community-based, and institutional care (Ikegami, 2019).

In 2019, long-term care costs accounted for approximately 2% of Japan's gross domestic product (GDP) (Organisation for Economic Co-operation and Development, 2021). However, Japanese government spending on long-term care could more than double, reaching even 4.4% of GDP by 2050 (Organisation for Economic Co-operation and Development & European Commission, 2013). Rapidly increasing long-term care costs is an issue faced by not only the Japanese government, but also older long-term care recipients and their family caregivers. A long-term care policy to address the problem of how the caregiving costs and financial burden of older care recipients can be shared equitably across society via risk-pooling among all users is needed (Organisation for Economic Co-operation and Development & European Commission, 2013). However, in 2019, the financial burden associated with long-term care services actually fell directly on older persons and their family caregivers, with out-of-pocket payments accounting for as high as 12% of annual household income (average: 2.6%) (Organisation for Economic Co-operation and Development, 2021).

Regarding household financial hardship among older care recipients and their family caregivers, the estimated average annual household income in 2021 was 5.5 million JPY (equivalent to 50,000 USD), and more than half of all households (53.1%) experienced financial hardship. However, the estimated average annual income of households consisting of an older couple was only 3.2 million JPY (equivalent to 29,091 USD), with half of these households experiencing financial hardship and depending on income from public pension (Ministry of Health, Labour and Welfare, 2023). Families with an older care recipient experiencing financial hardship often provide financial support, with employed family caregivers bearing more out-of-pocket caregiving costs than retired and unemployed caregivers (Keita Fakeye et al., 2022).

Review of Literature

Financial Impact on Family Caregivers

The impact of financial hardship on family caregivers differs by household income status and/or amount of out-of-pocket payments. Chovatiya et al. (2022) reported that households that have lower annual income (≤24,999 USD) and higher out-of-pocket payments (>1,000 USD) face significantly greater financial impacts compared with those that do not. These costs do not include indirect costs (e.g., loss of productivity, diminished quality of life), but rather, are based on estimated direct care costs (e.g., out-of-pocket payments). Conceivably, the financial impact on family caregivers may differ by whether the costs and benefits of formal care services are balanced, including caregiver burden and diminished social activity. Skaria (2022) reported that dependence on informal unpaid care provided by family caregivers increases the financial and social burdens of care provision for an older relative.

Family caregivers living with an older care recipient have been reported to experience a greater caregiver burden and poorer health compared with family caregivers with older relatives in a care facility (Metzelthin et al., 2017). In particular, given the limited utilization of community care services during the COVID-19 pandemic, the degree of emotional and instrumental support that was met decreased, and the amount of physical and psychological burden increased among family caregivers (Chiu et al., 2022; Tsapanou et al., 2021). Previous studies have shown that intensive caregiving also has strong and direct impacts on poor health, employment, and financial difficulties (Chiu et al., 2022; Organisation for Economic Co-operation and Development, 2021). Furthermore, experiencing financial hardship is known to contribute to low life satisfaction (Bakkeli, 2021). Therefore, the authors considered that family caregivers who experience financial hardship may limit their utilization of long-term care services to save on out-of-pocket costs. However, little remains known about how family caregivers experiencing financial hardship adapt to care and life, or whether financial hardship caused by care provision is a predictive factor contributing to alternative in-family care. To reduce the caregiver burden for family caregivers who experience financial hardship, it is crucial to gain a comprehensive understanding of the financial impact of caregiving on their life. The findings of the present study may provide strategies for long-term care policy that not only provide support for family caregivers experiencing financial hardship, but also improve the quality of community-based family care.

Long-Term Care Services and Participants’ Payments in Japan

There are three major types of long-term care services in Japan: (a) home-based care services (e.g., home helper, visiting nurse); (b) community-based care services (e.g., adult day services, adult day care with rehabilitation); and (c) institutional care services (e.g., nursing homes, chronic-care hospitals). Participants utilizing home- and community-based care services bear 10% of the service costs, while the remaining 90% is funded through insurance premiums and taxes. Payments for institutional care vary depending on the income of the participant and their household. In this study, participants are defined as family caregivers of older relatives utilizing the above-mentioned long-term care services.

Definitions of Financial Burden and Its Impact in This Study

Financial burden, as defined with reference to Skaria (2022), was assumed to influence the degree of impact of care costs. In this study, financial burden is defined as the financial strain caused by the costs of utilizing with long-term care services among family caregivers. Its impact on family caregivers’ lives is defined as resulting from both the financial burden and indirect costs of care, such as informal unpaid care and loss of productivity.

Aims of the Present Study

This study aimed to examine the caregiver characteristics and financial burden associated with the cost of utilizing long-term care services for an older relative among family caregivers. In particular, this study examined whether experiencing financial burden was related to poorer health and greater caregiver burden, along with a lower annual household income and bearing the long-term care costs among family caregivers.

Methods

Design

This cross-sectional study conforms to the STrengthening the Reporting of Observational studies in Epidemiology (STROBE) guidelines (Von Elm et al., 2008). Quantitative data were collected through surveys conducted from February to September 2021.

All responses (N = 427) were categorized into two groups: an institutional care group and a community care services group (including home- and community-based care). First, a quantitative analysis was conducted to examine differences in characteristics between the two groups of family caregivers. Next, descriptive statistics were used to examine the financial burden and its impact on the lives of the family caregivers in each group.

Sample

The study participants were 427 family caregivers who were utilizing long-term care services for an older relative. In this study, an older relative was defined as someone who required support for daily living (e.g., assistance with basic ADL, laundry, shopping, household management, financial support) and was utilizing long-term care services. The family caregiver's relationship to the older relative was that of a parent, parent-in-law, partner, or grandparent. A family caregiver was defined as someone who provided care for their older relative, including assistance with basic ADL, laundry, shopping, household management, financial support, responding to calls from the care facility, communicating with care managers and care professionals regarding the older relative, and carrying out the necessary administrative procedures to access long-term care services.

Inclusion and Exclusion Criteria

Participants were included in the study if they were (1) aged≥18 years, (2) providing care for an older relative, and (3) utilizing long-term care services for those relatives. Participants (1) whose age or sex was missing or (2) who did not answer the question about living arrangement or financial burden were excluded.

Data Collection

For this study, a convenience sampling technique was adopted. The questionnaire survey was distributed and collected from February to September 2021. Before recruiting the family caregivers, permission to conduct the survey was obtained from the directors of long-term care service offices. In a cover letter attached to the questionnaire, an explanation of the study purpose and protocol, as well as various ethical considerations, was provided, and voluntary participation was requested (see Supplementary Material). Next, self-administered questionnaires were distributed to 896 family caregivers, who were asked to complete and return them by postal mail (Figure 1). Of these, 488 responses were received, for a response rate of 54.5%, nine of which were excluded from the analysis because the respondent indicated a refusal to participate or the survey had missing demographic information. After excluding the questionnaires with missing data on age, sex, living arrangement, or financial status from the remaining 479 responses, a total of 427 family caregivers constituted the final sample.

Sample Selection.

Ethical Considerations

The Institutional Ethics Committee of St. Mary's College reviewed and approved this study (No. R02-008; January 14, 2021), which was conducted in accordance with the Japanese Ethical Guidelines for Medical and Biological Research Involving Human Subjects and the guidelines laid down by the Declaration of Helsinki. In this study, returning a completed questionnaire by postal mail was considered to indicate voluntary consent to participate.

Measurements

Outcome Variables

Financial burden and its impact on family caregivers’ lives. In this study, the participants were asked to indicate their financial burden and its impact on their lives by responding to the following question: “Do you experience financial burden associated with the cost of utilizing long-term care services for your older relative?” Then, the respondents were categorized as follows: Group A (Family caregivers did not experience financial burden), Group B (Family caregivers experienced financial burden, but it did not significantly impact their lives), and Group C (Family caregivers experienced financial burden, which significantly impacted their lives).

Primary Independent Variables and Covariates

The primary independent variables were the two caregiver characteristics of sex (0 = male or 1 = female) and employment status (1 = employed or 0 = unemployed) and five caregiving contexts (described below). The caregivers’ other demographic characteristics, including age, self-rated health, and marital status, were included as covariates. Self-rated health was assessed as follows based on the participants’ own self-ratings: poor (1), fairly poor (2), intermediate (3), fairly good (4), and very good (5). The five caregiving contexts are as follows.

Psychological distress. Psychological distress was assessed using the 10-item Kessler scale (K10) (Kessler et al., 2002). Participants were asked to indicate how frequently they had experienced psychological distress or negative feelings during the past month using a 5-point Likert-type scale, from none of the time (0) to all of the time (4). The total score was calculated as the sum of all responses (range = 0–40). A score of ≥15 on the K10 scale indicates an increased risk of psychological distress (Schmitz et al., 2009), with higher scores reflecting more severe psychological distress (Cronbach's alpha = .93) (Donker et al., 2010). The screening performance of the Japanese version of the K10 scale is essentially equivalent to that of the original English version (Cronbach's alpha = .94) (Furukawa et al., 2008), and Cronbach's alpha for the present survey was .92.

Number of caregiver burdens. Caregiver burden was assessed using a total of eight dichotomous items (1 = presence or 0 = absence; Cronbach's alpha = .65), excluding financial burden. These eight items were classified into four indices as follows: psychological burden, which consists of difficulty communicating with the care recipient, psychological distress, and a lack of free time due to caregiving (three items); distress related to social support, which consists of insufficient information on care services and a lack of a place for consulting others about caregiving (two items); physical burden, which consists of fatigue and physical pain, such as back, knee, or shoulder pain (two items); and social restrictions, which are related to whether the caregiver can leave the home (one item). This scale has been validated in a prior study (Honda et al., 2024). Among the caregiver burdens examined, the mean number was 2.0 (SD = 1.8; range = 0–8), with a higher number reflecting greater stress due to care provision for an older care recipient.

Annual household income. Annual household income, converted from Japanese JPY to USD based on the exchange rate at the time, was categorized as follows according to the income tax brackets applicable in Japan: 1 (<1,300,000 JPY, equivalent to <11,818 USD); 2 (1,300,000 to <2,000,000 JPY, equivalent to 11,818 to <18,181 USD); 3 (2,000,000 to <2,500,000 JPY, equivalent to 18,181 to <22,727 USD); 4 (2,500,000 to <3,000,000 JPY, equivalent to 22,727 to <27,272 USD); 5 (3,000,000 to <3,500,000 JPY, equivalent to 27,272 to <31,818 USD); 6 (3,500,000 to <4,000,000 JPY, equivalent to 31,818 to <36,363 USD); 7 (4,000,000 to <5,000,000 JPY, equivalent to 36,363 to <45,454 USD); 8 (5,000,000 to <6,000,000 JPY, equivalent to 45,454 to <54,545 USD); and 9 (≥6,000,000 JPY, equivalent to ≥54,545 USD).

Out-of-pocket costs. Out-of-pocket costs borne by the participant and/or their family member were defined as a private payment source (Skaria, 2022). The participants were asked to indicate who paid the costs of utilized care services for the older care recipient, and the responses were categorized as follows: 0 (the older care recipient) or 1 (the family caregiver only, or shared payment by the family caregiver and older care recipient).

Japanese Government-Certified Disability Index (GCDI) of the older care recipient. The Ministry of Health, Labour and Welfare of Japan developed the GCDI under the long-term care insurance program. The GCDI has been applied to assess the severity of dementia and the level of functional disability among care recipients as follows: normal, mild disability 1 (very mild), mild disability 2 (mild), level 1 (low level 1), level 2 (low level 2), level 3 (moderate), level 4 (severe), and level 5 (very severe/bedridden with decreased level of consciousness). Care services are allocated based on the GCDI; older people with disabilities are entitled to decide both the kind and amount of services they wish to use within the parameters allowed by the GCDI (Arai et al., 2003; Tsutsui & Muramatsu, 2007).

Statistical Analysis

The potential influencing factors were compared among the three categories of financial burden and their impact on family caregivers’ lives. The chi-square test was used for categorical data—that is, sex, marital status, employment status, and responsibility for care costs, while the Kruskal–Wallis test was used for continuous or ordinal data—that is, age, K10 score, self-rated health, number of caregiver burdens, annual household income, and GCDI of the older care recipient. Subsequently, post hoc comparisons were conducted with the Bonferroni correction. SPSS Statistics 24 (IBM, Tokyo, Japan) was used for all analyses.

Results

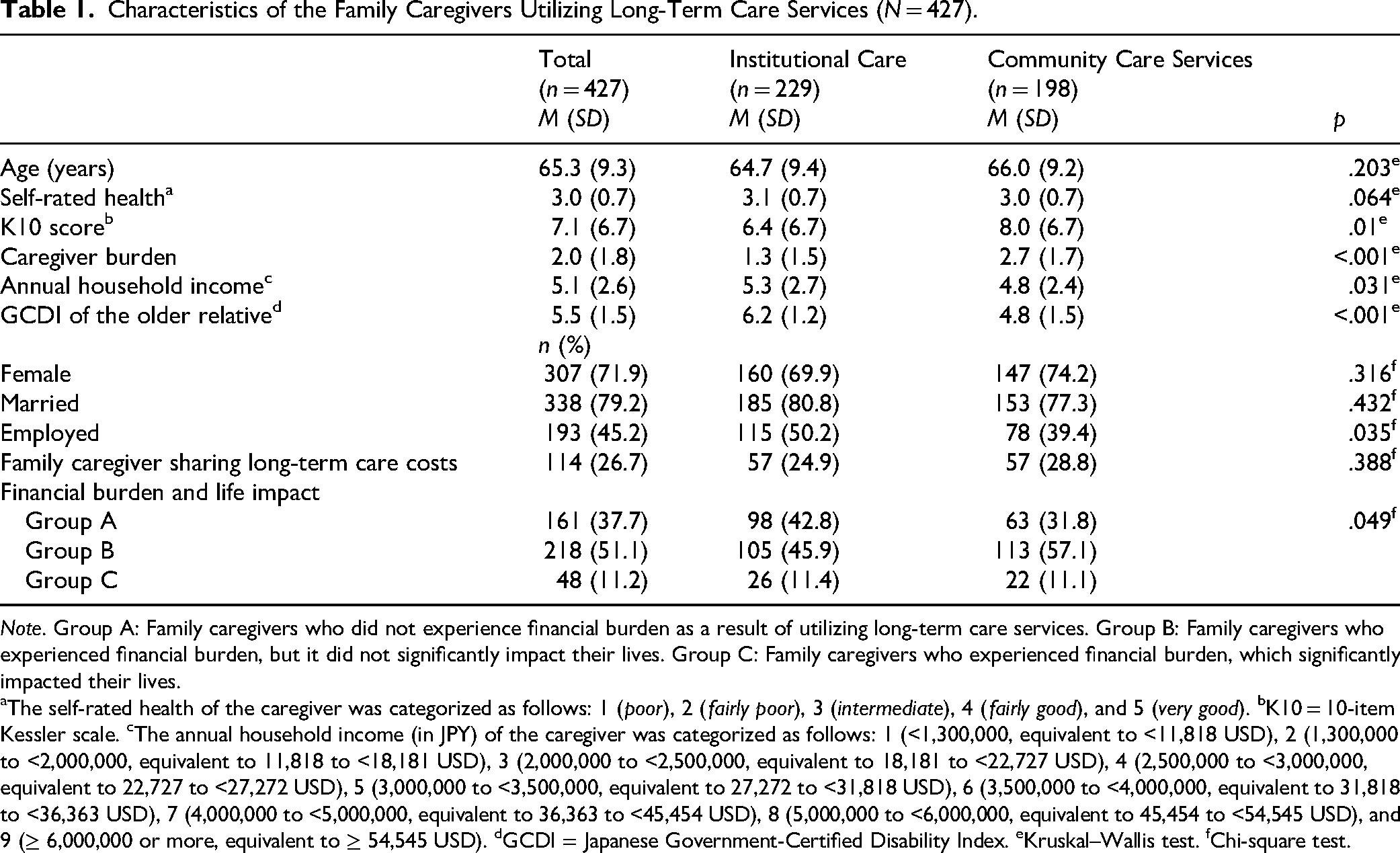

As shown in Table 1, the M ± SD age of the family caregivers (72% female) who participated in this study was 65.3 ± 9.3 years. Compared with family caregivers with older relatives in a care facility, those who were living with an older care recipient reported experiencing a significantly greater caregiver burden (p < .001) and more psychological distress (p = .01). In addition, the family caregivers living with an older care recipient were significantly less likely to be employed (39.4%, p = .035) and to have a lower annual household income (p = .031) compared with those with older relatives in a care facility. Although the proportion of participants who reported bearing the costs of long-term care did not differ, 131 (57.3%) family caregivers with an older relative in a care facility and 135 (68.2%) family caregivers living with an older care recipient (i.e., Groups B and C) experienced financial burden as a result of utilizing long-term care services (p = .049).

Characteristics of the Family Caregivers Utilizing Long-Term Care Services (N = 427).

Note. Group A: Family caregivers who did not experience financial burden as a result of utilizing long-term care services. Group B: Family caregivers who experienced financial burden, but it did not significantly impact their lives. Group C: Family caregivers who experienced financial burden, which significantly impacted their lives.

aThe self-rated health of the caregiver was categorized as follows: 1 (poor), 2 (fairly poor), 3 (intermediate), 4 (fairly good), and 5 (very good). bK10 = 10-item Kessler scale. cThe annual household income (in JPY) of the caregiver was categorized as follows: 1 (<1,300,000, equivalent to <11,818 USD), 2 (1,300,000 to <2,000,000, equivalent to 11,818 to <18,181 USD), 3 (2,000,000 to <2,500,000, equivalent to 18,181 to <22,727 USD), 4 (2,500,000 to <3,000,000, equivalent to 22,727 to <27,272 USD), 5 (3,000,000 to <3,500,000, equivalent to 27,272 to <31,818 USD), 6 (3,500,000 to <4,000,000, equivalent to 31,818 to <36,363 USD), 7 (4,000,000 to <5,000,000, equivalent to 36,363 to <45,454 USD), 8 (5,000,000 to <6,000,000, equivalent to 45,454 to <54,545 USD), and 9 (≥ 6,000,000 or more, equivalent to ≥ 54,545 USD). dGCDI = Japanese Government-Certified Disability Index. eKruskal–Wallis test. fChi-square test.

Table 2 presents the descriptive statistics on financial burden and its impact on the lives of 198 family caregivers with an older care recipient utilizing community care services. Compared with family caregivers who did not experience financial burden (i.e., Group A), those who experienced financial burden and its impact on their lives (i.e., Group C) had a significantly lower annual household income and were bearing the costs of long-term care for an older care recipient (p = .033 and p < .001, respectively); however, we found no significant difference in annual household income between Groups A and B or between Groups B and C. In addition, family caregivers who experienced financial burden and its impact on their lives (i.e., Group C) had significantly worse self-rated health and psychological distress compared with those who did not experience financial burden (i.e., Group A) (both ps < .001). Furthermore, family caregivers who reported a greater caregiver burden and who had an older care recipient with a more severe GCDI level were significantly more likely to experience financial burden and its impact on their lives (i.e., Group C) (p < .001 and p = .004, respectively). Moreover, no significant differences in age, sex, marital status, or employment status were found among the three groups.

Descriptive Statistics for Financial Burden and Its Impact on the Lives of 198 Family Caregivers Utilizing Community Care Services.

Note. Group A: Family caregivers who did not experience financial burden as a result of utilizing long-term care services. Group B: Family caregivers who experienced financial burden, but it did not significantly impact their lives. Group C: Family caregivers who experienced financial burden, which significantly impacted their lives.

aThe self-rated health of the caregiver was categorized as follows: 1 (poor), 2 (fairly poor), 3 (intermediate), 4 (fairly good), and 5 (very good). bK10 = 10-item Kessler scale. cThe annual household income (in JPY) of the caregiver was categorized as follows: 1 (<1,300,000, equivalent to <11,818 USD), 2 (1,300,000 to <2,000,000, equivalent to 11,818 to <18,181 USD), 3 (2,000,000 to <2,500,000, equivalent to 18,181 to <22,727 USD), 4 (2,500,000 to <3,000,000, equivalent to 22,727 to <27,272 USD), 5 (3,000,000 to <3,500,000, equivalent to 27,272 to <31,818 USD), 6 (3,500,000 to <4,000,000, equivalent to 31,818 to <36,363 USD), 7 (4,000,000 to <5,000,000, equivalent to 36,363 to <45,454 USD), 8 (5,000,000 to <6,000,000, equivalent to 45,454 to <54,545 USD), and 9 (≥6,000,000 or more, equivalent to ≥54,545 USD). dGCDI = Japanese Government-Certified Disability Index. ns = not significant.

Table 3 presents the descriptive statistics on financial burden and its impact on the lives of 229 family caregivers with an older care recipient utilizing institutional care. Compared with family caregivers who did not experience financial burden (i.e., Group A), those who experienced financial burden and its impact on their lives were significantly more likely to have a lower annual household income (i.e., Group C) (p = .05); however, no significant differences were found between Groups A and B or between Groups B and C. Moreover, participants who reported bearing the costs of long-term care for an older care recipient were significantly more likely to belong to Group C (p < .001), meaning that those bearing such costs were more likely to experience financial burden and its impact on their lives; this difference was significant across all three groups. Similar to the family caregivers living with an older care recipient at home, a significantly higher proportion of family caregivers who experienced financial burden and its impact on their lives (i.e., Group C) reported poor self-rated health and caregiver burden compared with Groups A and B (p = .005 and p < .001, respectively). The three groups did not differ with respect to age, sex, marital status, employment status, psychological distress, or the GCDI severity level of the older care recipient.

Descriptive Statistics of Financial Burden and Its Impact on the Lives of 229 Family Caregivers Utilizing Institutional Care.

Note. Group A: Family caregivers who did not experience financial burden as a result of utilizing long-term care services. Group B: Family caregivers who experienced financial burden, but it did not significantly impact their lives. Group C: Family caregivers who experienced financial burden, which significantly impacted their lives.

aThe self-rated health of the caregiver was categorized as follows: 1 (poor), 2 (fairly poor), 3 (intermediate), 4 (fairly good), and 5 (very good). bK10 = 10-item Kessler scale. cThe annual household income (in JPY) of the caregiver was categorized as follows: 1 (<1,300,000, equivalent to <11,818 USD), 2 (1,300,000 to <2,000,000, equivalent to 11,818 to <18,181 USD), 3 (2,000,000 to <2,500,000, equivalent to 18,181 to <22,727 USD), 4 (2,500,000 to <3,000,000, equivalent to 22,727 to <27,272 USD), 5 (3,000,000 to <3,500,000, equivalent to 27,272 to <31,818 USD), 6 (3,500,000 to <4,000,000, equivalent to 31,818 to <36,363 USD), 7 (4,000,000 to <5,000,000, equivalent to 36,363 to <45,454 USD), 8 (5,000,000 to <6,000,000, equivalent to 45,454 to <54,545 USD), and 9 (≥ 6,000,000 or more, equivalent to ≥54,545 USD). dGCDI = Japanese Government-Certified Disability Index. ns = not significant.

These results, which are summarized in Tables 2 and 3, indicate that experiencing financial burden and its impact is related to poorer health and a greater caregiver burden among family caregivers, along with a lower annual household income and bearing the cost of long-term care.

Discussion

Among family caregivers with an older care recipient living at home, care recipients with a higher GCDI level due to physical and/or cognitive disabilities require more support, which leads to more frequent use of long-term care services and higher associated costs. Family caregivers must bear the long-term care costs when the care recipients are unable to cover these expenses themselves. By contrast, older relatives with a lower GCDI level require less care, incur lower costs, and are able to cover these expenses independently. As shown in Table 2, financial burden is associated not only with lower annual household income and bearing the costs of long-term care, but also with the GCDI level of an older relative. Family members may take on more caregiving responsibilities and devote more time to caregiving tasks in an effort to reduce care-related expenses. However, this situation may increase their financial strain indirectly as a result of a decline in physical and mental health, reduced employment opportunities, and decreased disposable income.

For family caregivers whose older relatives are receiving institutional care, the financial burden is associated with bearing the long-term care costs, similar to that of caregivers living with an older relative at home. In general, the cost of institutional care is higher than that of home- and community-based care services (Ikegami, 2019). Therefore, the financial burden of long-term care may be greater for family caregivers whose older relatives are in institutional care than for those using community-based services. Financial burden has also been associated with greater caregiver burden in both institutional and community-based care settings. However, caregiving tasks differ between family caregivers with an older relative in institutional care and those using community-based services. Family caregivers with institutionalized older relatives are more involved in indirect tasks (e.g., communicating with care staff, handling administrative procedures, responding to facility calls), whereas family caregivers using community-based services are more engaged in direct care, such as assisting with ADL and instrumental ADL. Therefore, the approaches to reducing caregiver burden and coping with caregiving-related stress differ between these two groups of family caregivers. For instance, to cope with direct care stress, it may be effective to introduce flexible formal support that provides personal care, such as a free home helper service for family caregivers with a lower annual household income. By contrast, to cope with indirect care stress, it may be effective to distribute caregiving responsibilities among several family members and/or care management personnel, rather than placing the burden intensively on a single family member.

The present study aimed to examine caregiver characteristics and associations with financial burden, especially whether experiencing financial burden was related to poorer health and greater caregiver burden among family caregivers. The results suggest that financial burden is related to caregiver burden, worse health, and bearing the caregiving costs. Especially, family caregivers who had experienced financial burden and its impact on their lives and were living with an older care recipient tended to provide care for older care recipients with a higher severity of functional disabilities and to bear the costs of care. Consistent with previous studies (DiGiacomo et al., 2020; Kang et al., 2007), the present study found that financial burden among family caregivers increased as their care recipients’ limitations in ADL and long-term care costs increased. Many family caregivers living with an older care recipient have fixed employment schedules and utilize community care services, although the out-of-pocket costs involve some trade-off. However, family caregivers who cannot fully utilize community care services as a result of financial hardship are unable to juggle the requirements of family caregiving, employment, and private life (Connell et al., 2001). Therefore, family caregivers who have limited coping strategies are considered more likely to experience both a greater caregiver burden and worse health. Given this background, family caregivers who experienced financial burden and its impact on their lives may have limited their utilization of long-term care services. As a result of the rapidly increasing costs of long-term care in Japan, the government has been accelerating the transition from institutional to community-based care. However, accelerating this transition may be problematic for those who have caregiving issues.

Strengths and Limitations

This study has several limitations. First, the sample size was small, and thus caution is warranted when generalizing the results to the general Japanese population. Second, in this study, the authors did not perform a detailed examination of the caregiving situations, and as a result, were unable to conduct nuanced analyses of the associations between financial hardship and detailed caregiving contexts. Thus, the impact of key predictive factors on financial hardship across caregiving contexts needs to be investigated in a future study. Finally, as this study utilized a cross-sectional design, causal relationships between predictors and financial burden could not be inferred. Despite these limitations, the present findings suggest that family caregivers who experience financial burden and its impact on their lives tend to live with their older care recipient and have a higher proportion of out-of-pocket payments compared with other family caregivers.

Implications for Community-Based Family Support

The findings of the present study indicate that a lack of financial resources among older care recipients has a negative impact on their family caregivers’ work and private lives, as well as their choices with respect to care services. It is difficult for older individuals and their family caregivers who lack financial resources to continue to receive the long-term care services they need without any social safeguards. Under the current public long-term care insurance policy in Japan, family caregivers are not provided with caregiving-related allowances or compensation. Conceivably, the provision of caregiving-related allowances or compensation for the livelihoods of family caregivers may need to be incorporated into the public long-term care insurance policy, especially for those who lack financial resources or care for older relatives with a GCDI level above a certain threshold. Community-based care is a social care activity that contributes to human well-being among not only older long-term care recipients, but also their family caregivers. Therefore, community-based family care should attempt to solve the issues (e.g., caregiving burden, no time for daily life for family caregivers) that interfere with well-being among family caregivers with financial hardship. For instance, family caregivers with an older care recipient can receive multilayered care support by utilizing various home- and community-based care services. However, if they cannot continue to utilize these care services because of a limited household care budget, it can become difficult to maintain the same level of care support. In response, promoting volunteer-based, nonprofit, and community-oriented long-term care services may help reduce the financial strain on family caregivers who face difficulties in continuing care because of limited resources.

Implications for Practice

For family caregivers with limited care budgets, merely receiving long-term care services is not sufficient to alleviate caregiver burden and stress. In nursing practice, it is essential to provide family-centred care in daily long-term caregiving in order to reduce caregiver burden and deliver value that exceeds the cost of care services borne by family caregivers. To achieve this, nursing staff need to continuously assess family caregivers’ personal and caregiving needs and adjust their support accordingly.

Conclusion

The findings of the present study suggest that financial hardship is related to caregiver burden, worse health, and bearing the caregiving costs. Financial hardship also has a negative impact on family caregivers’ work and private lives, as well as their choices with respect to care services. These challenges are partly driven by insufficient social safeguards. Current community-based care services do not adequately support the caregiving responsibilities of those with limited financial resources. Future community-based family care models should take into account the financial burdens experienced by family caregivers and implement strategies to alleviate them.

Supplemental Material

sj-docx-1-son-10.1177_23779608251383386 - Supplemental material for Impact of Financial Burden on Family Caregivers of Older Adults Using Long-Term Care Insurance Services

Supplemental material, sj-docx-1-son-10.1177_23779608251383386 for Impact of Financial Burden on Family Caregivers of Older Adults Using Long-Term Care Insurance Services by Ayumi Honda, PhD, Takahiro Nishida, RN, Mayo Ono, PhD, Tatsuya Tsukigi and Sumihisa Honda, PhD in SAGE Open Nursing

Footnotes

Acknowledgments

The authors are grateful to all the study participants for their valuable contributions.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was supported by JSPS KAKENHI [grant number 20K10959].

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.