Abstract

Saudi Arabia's Vision 2030 and the National Health Insurance Scheme (NHIS) aim for a more equitable healthcare system. Public participation and health insurance literacy (HIL) are vital for its success, yet underserved areas like Al-Jouf lack research on these factors. This cross-sectional observational study was conducted with 408 adult Saudi citizens from public health clinics in Al-Jouf. A structured questionnaire assessed demographics, HIL, confidence in choosing (CCI), comparing (CCP), utilizing insurance (CUI), proactive behavior (PBS), and willingness to enroll in NHIS. Correlational analyses were performed using Spearman's correlation and multinomial logistic regression. Among participants, predominantly men (82.11%) aged 41 to 50 (21.81%), only 15.93% were enrolled in health insurance. Social media was the primary information source, and HIL scores were low to moderate. Significant correlations were observed between income and PBS (p = 0.015) and CCI (p = 0.021). Higher HIL and confidence positively influenced willingness to participate. The study underscores the gap between awareness and enrollment in NHIS, emphasizing the need for tailored interventions, particularly for low-income and unemployed individuals.

Keywords

Introduction

Modern healthcare policy relies on health insurance systems to ensure financial protection, equitable access, and sustainable service delivery.1,2 The World Health Organization (WHO) recommends achieving universal health coverage in high- and middle-income countries through national health insurance programs (WHO, 2025). In Saudi Arabia, the National Health Insurance Scheme (NHIS), introduced under Vision 2030, represents a strategic shift toward a more efficient, contributory healthcare system.3–6 This initiative aims to enhance quality, efficiency, and long-term sustainability by replacing the predominantly state-funded model.7,8 However, successful implementation depends heavily on public awareness, understanding, and willingness to engage.8,9 An important but frequently overlooked factor in insurance use is health insurance literacy (HIL).10,11 It includes the capacity to acquire, process, and comprehend insurance-related data to make well-informed choices.10,12 Individuals with low HIL are more likely to make poor choices, misunderstand benefits, delay care, and disengage from the system. 13 These risks are amplified in countries introducing new insurance models, especially where citizens lack experience with formal insurance systems. 14 In Saudi Arabia, the free public healthcare tradition may reduce appreciation for insurance and resistance to cost-sharing.6,15–17 In Al-Jouf, a primarily rural and semi-urban region, sociodemographic factors, limited information access, and past care-seeking behaviors may further impact HIL.18,19 Despite its inclusion in national reform efforts, little empirical research has assessed insurance literacy or willingness to participate in NHIS in this region. This study addresses that gap by examining HIL, willingness to participate, and related behavioral constructs—confidence in choosing (CCI), comparing (CCP), and using (CUI) insurance. It also considers proactive behaviors like researching networks and understanding coverage limits. By analyzing demographic and psychosocial predictors, this study aims to inform policy through a multivariable model and support NHIS implementation via targeted tools, subsidies, and awareness campaigns.

Methods

Study Design and Setting

A cross-sectional observational study was conducted in Al-Jouf, a northern region of Saudi Arabia with over 500,000 residents in both urban and rural areas. The region is served by more than 60 primary healthcare centers and several public hospitals. The study aimed to assess the HIL and willingness to enroll in the proposed NHIS among adult Saudi citizens.

Population, Sampling Method, and Sample Size Calculation

The target population included Saudi nationals aged 18 and above residing in Al-Jouf. Non-Saudis, minors, and individuals outside the region were excluded. A convenient, nonrandom sampling method was used, which may limit generalizability. The minimum required sample size was determined based on a total population of 508,475, using Raosoft's online sample size calculator. Based on a 50% response distribution, 5% margin of error, and 95% confidence level, the minimum sample size was calculated to be 384. A total of 408 valid responses were collected and analyzed.

Data Collection

This cross-sectional study accessed the target sample by recruiting individuals who visited various healthcare facilities in the Al-Jouf region. Data were collected using a structured questionnaire via Google Forms, to which participation was voluntary. The survey link was shared across 17 outpatient clinics at Prince Mutab bin Abdulaziz Hospital, King Abdulaziz Specialist Hospital, Jouf University clinics, blood donation centers, and primary healthcare centers in Sakaka. The instrument, adapted from a previous validated study titled “Measurement of Health Insurance Literacy and Willingness to Participate in the National Health Insurance Scheme among Saudis,” included 7 sections: 11 demographic items, 5 items each on willingness to participate in NHIS and pay, 5 on HIL, 5 on CCI, 6 on CCP, 5 on CUI, and 4 on proactive behavior (PBS). Responses were scored on a 5-point Likert scale, and composite scores were computed. Validity was confirmed through exploratory analysis and item-total correlation (P < .01), and self-validity was high (coefficient = 0.945).

Ethical Considerations

Ethical approval for the study was obtained from the Institutional Review Board (IRB) at King Khalid University Hospital, under approval number KSU-HE-25-098. Additionally, written informed consent was secured from all participants, with materials provided in Arabic to ensure comprehension and compliance.

Statistical Analysis

SPSS version 26 was used. Categorical data were summarized with frequencies and percentages; continuous data with mean ± SD or median interquartile range (IQR). Normality was checked using the Shapiro-Wilk test. Analysis of variance (ANOVA)/Kruskal-Wallis and t-test/Mann-Whitney U were used for group comparisons. Spearman's correlation examined relationships between HIL, CUI, and PBS. Chi-square tested categorical associations. Multinomial and ordinal regressions identified predictors of NHIS participation and contribution willingness. Significance was set at P < .05.

Reliability Analysis

Cronbach's alpha values ranged from 0.858 to 0.919 for all subscales. Specifically, the HIL yielded a value of 0.862, CCP was 0.919, PBS was 0.863, CCI was 0.874, and CUI was 0.858. With a total reliability coefficient of 0.913, indicating strong internal consistency. These findings confirm that the instrument is both reliable and appropriate for assessing the constructions in this study.

Results

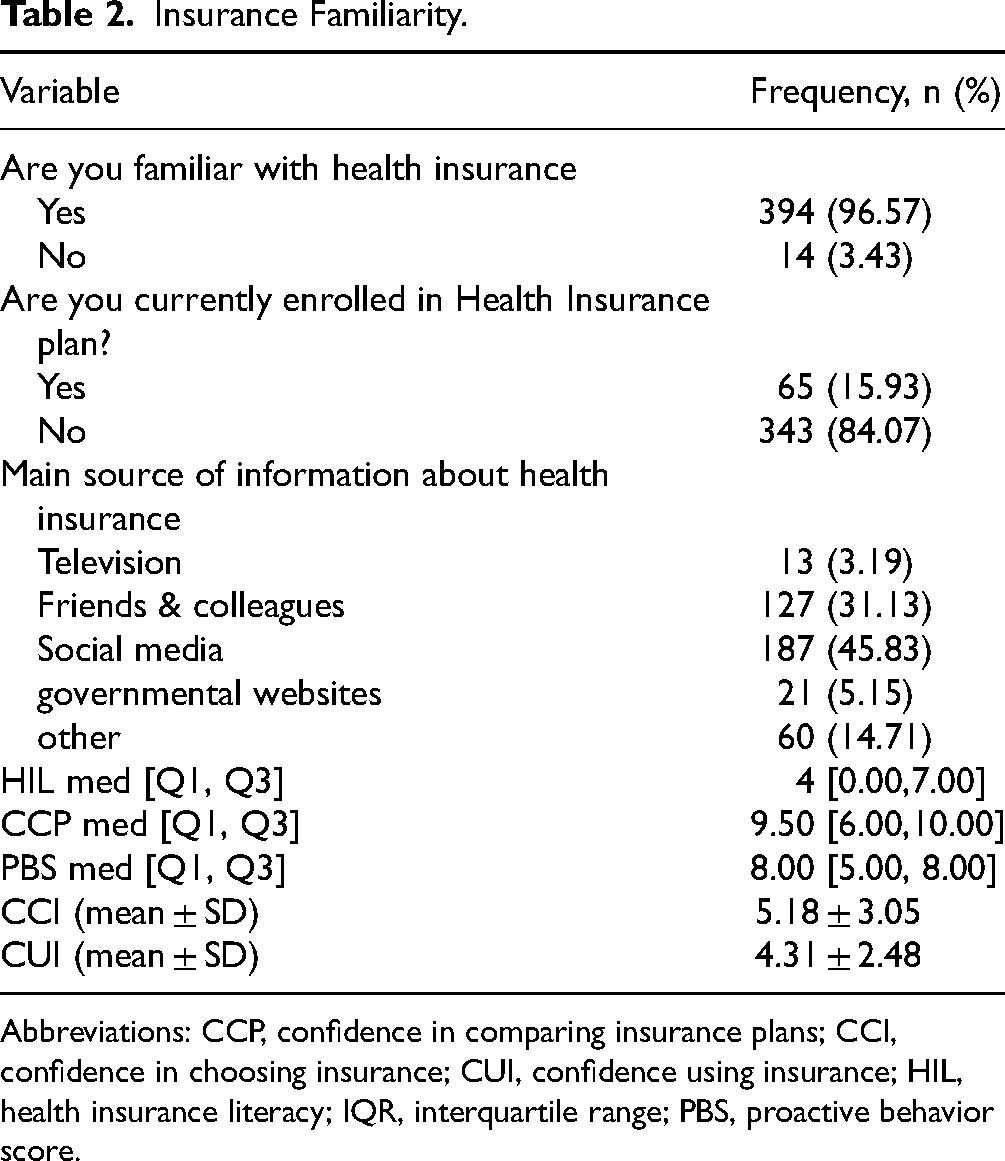

The majority of participants were males (82.11%), with the largest age group being 41 to 50 years (21.81%), and most were married (75.98%). Government employment was most common (40.93%), followed by retirees (27.21%). Over half (56.37%) held a bachelor's degree. Income distribution showed 35.54% earned ≥15,000 Saudi riyal (SR), while 23.53% earned ≤5000 SR (Table 1). Although 96.57% were familiar with health insurance, only 15.93% were enrolled. Social media was the primary information source (45.83%), followed by friends and colleagues (31.13%). The HIL score had a median of 4 (IQR: 0.00-7.00), the CCP median was 9.5 (IQR: 6.00-10.00), and the PBS median was 8 (IQR: 5.00-8.00). CCI had a mean of 5.18 ± 3.05, and CUI a mean of 4.31 ± 2.48 (Table 2). Significant differences in CCI (P = .021) and PBS (P = .015) were found across income groups. Post hoc analysis showed those earning ≤5000 SR had higher CCI than those earning 11,001 to 15,000 SR (P = .011). PBS differences were noted between income brackets: ≤ 5000 SR and 5001 to 7900 SR (P = .013), 5001 to 7900 SR versus 7901 to 11,000 SR (P = .011), and 5001 to 7900 SR versus 11,001 to 15,000 SR (P = .009). Marital status influenced CCI (P = .048), though post hoc tests showed no group differences (Table 3). No significant gender, age, employment, or education differences were found (Supplemental Table S1).

Demographic Characteristics of the Participants (n = 408).

Insurance Familiarity.

Abbreviations: CCP, confidence in comparing insurance plans; CCI, confidence in choosing insurance; CUI, confidence using insurance; HIL, health insurance literacy; IQR, interquartile range; PBS, proactive behavior score.

Association Between Health Insurance-Related Scores and Demographic Characteristics of Participants.

Anova test; €Kruskal-Wallis test; ¶Mann-Whitneys u test; *P < .05(significant).

The bold numbers represent statistically significant results (P < 0.05).

Abbreviations: CCI, confidence in choosing insurance; CCP, confidence in comparing insurance plans; CUI, confidence using insurance; HIL, health insurance literacy; IQR, interquartile range; PBS, proactive behavior score.

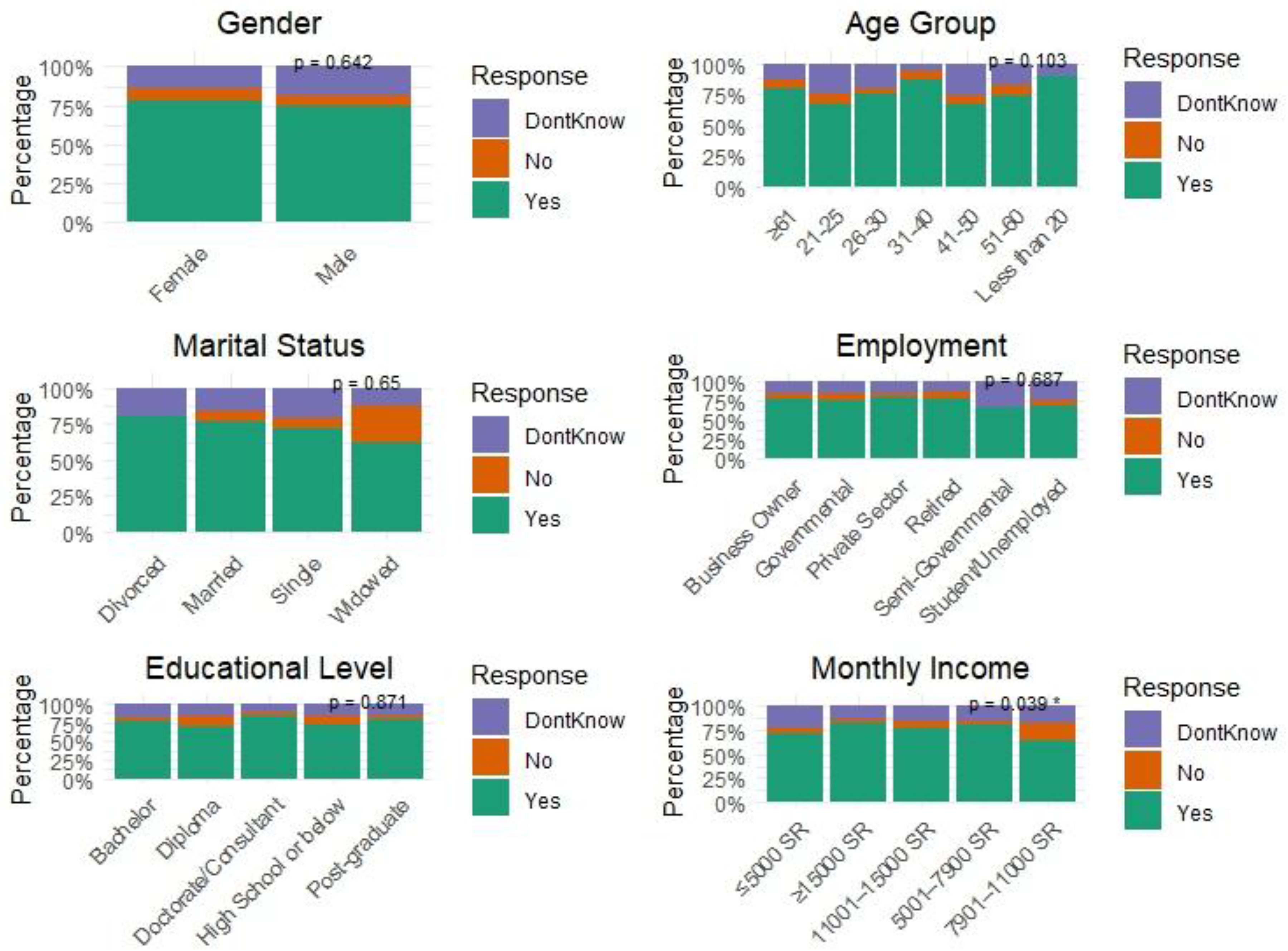

The findings indicate that a statistically significant association was observed only between monthly income and willingness to participate in NHIS (P = .039). Participants with a monthly income of ≥15,000 SR had the highest willingness to participate (38.44%). In contrast, those earning between 7901 and 11,000 SR showed a higher refusal rate (36.77%). Uncertainty about participation was most common among individuals with a lower income (≤5000 SR, 31.99%). Other demographic variables, such as gender (P = .642), age (P = .103), marital status (P = .650), employment (P = .687), and educational level (P = .871), are not significantly associated with willingness to participate in the National Health Insurance Program (NHIP), as their P values are >.05 (Figure 1; detailed table is provided in Supplemental Table S2).

Willingness to participate in National Health Insurance Plan by demographic variables.

A moderate positive correlation was found between HIL and CCI (ρ = 0.522, P < .001), indicating that higher health insurance literacy is associated with greater confidence in choosing insurance. A weak to moderate positive correlation was observed between HIL and PBS (ρ = 0.384, P < .001), suggesting that individuals with higher health insurance literacy are more likely to engage in proactive behaviors regarding insurance decisions. A weak to moderate positive correlation was also found between CCI and PBS (ρ = 0.398, P < .001), implying that individuals with higher confidence in selecting insurance tend to exhibit more proactive behaviors (Table 4).

Relationship Between HIL, CCI, and PBS.

Abbreviations: CCI, confidence in choosing insurance score; HIL, health insurance literacy score; PBS, proactive behavior score.

The findings reveal significant associations between various confidence-related factors and willingness to participate in the NHIS. Specifically, a higher proportion of individuals with low CCI, low CCP, low CUI, low PBS, and low HIL were unwilling or uncertain about participating in NHIS. In contrast, individuals with high levels of these factors were more likely to express a willingness to participate. For instance, individuals with low CCI were more likely to be unwilling (83.33%), while those with high CCI showed a higher willingness (30.62%). Similarly, those with high CCP (76.55%), high PBS (69.06%), high CUI (25.41%), and high HIL (29.64%) were more likely to show willingness to participate. These findings underscore the importance of confidence in insurance-related decisions and proactive behaviors in influencing participation in the NHIS, with all variables showing statistically significant associations (P < .05) (Table 5).

Association Between Confidence in Insurance-Related Decisions and Willingness to Participate in NHIP.

*P value < .05(significant).

Abbreviations: CCI, confidence in choosing insurance; CCP, confidence in comparing insurance plans; CUI, confidence using insurance; HIL, health insurance literacy; NHIP, National Health Insurance Plan; PBS: proactive behavior.

Figure 2 summarizes the results of the multinomial logistic regression analysis conducted to identify predictors of participants’ willingness to participate in the NHIP. Only the significant predictors are presented in Figure 2, while the detailed regression results are provided in Supplemental Table S3. Factors significantly predicting willingness to participate (“Yes”) include PBS, HIL, and employment status. Participants with low PBS and HIL were significantly less likely to express willingness to participate (odds ratio [OR] = 0.222, P = .001, and OR = 0.317, P = .026, respectively). Additionally, unemployed participants were less likely to participate (OR = 0.173, P = .049). Age also played a role, with participants aged 31 to 40 being more likely to participate (OR = 8.490, P = .020). Conversely, no factors were significantly associated with predicting unwillingness to participate (“No”). Notably, none of the factors had a significant effect on participants’ likelihood of answering “No” regarding participation (Figure 2).

Significant predictors of willingness to participate in National Health Insurance Plan.

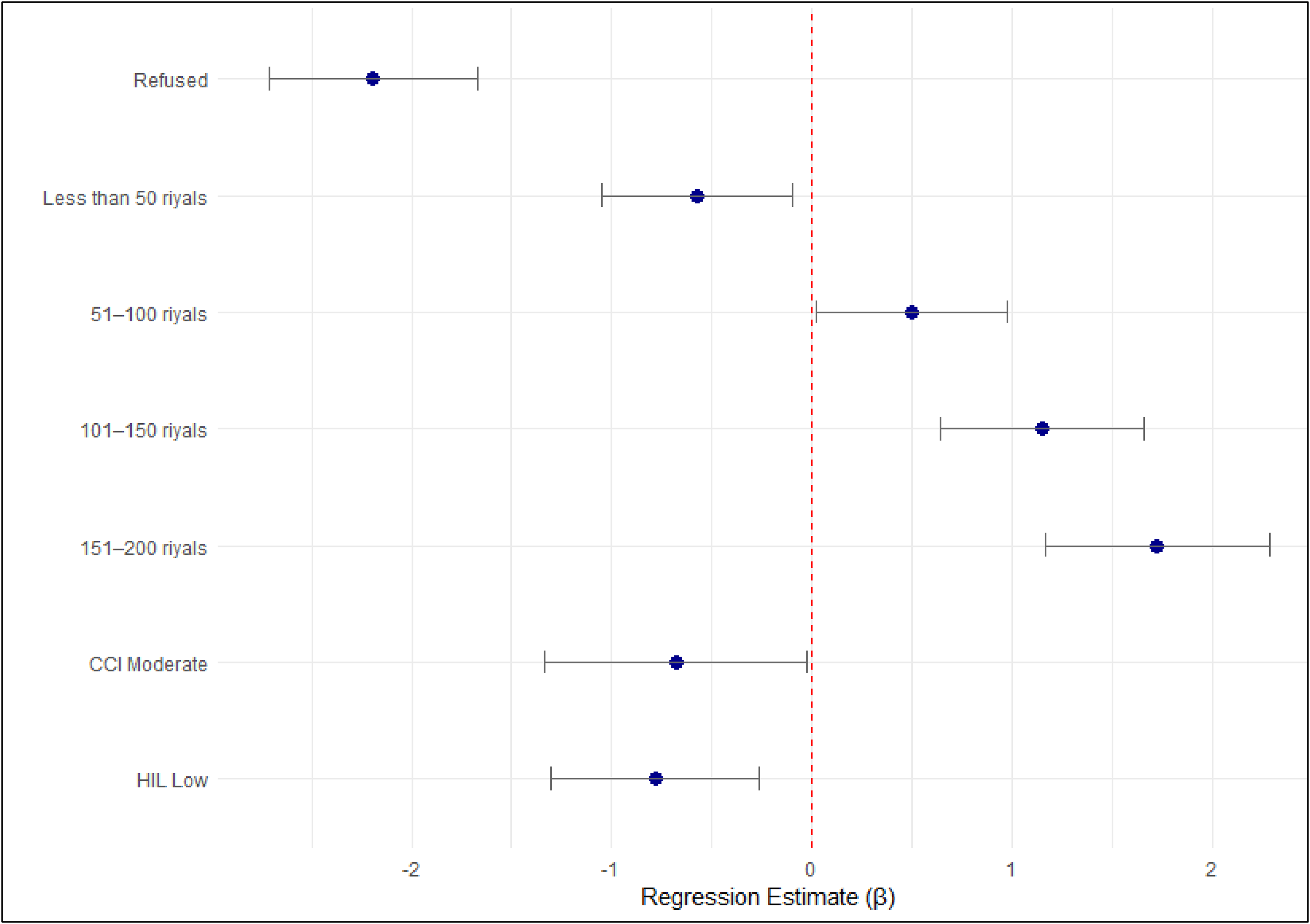

Figure 3 presents the results of an ordinal logistic regression analysis predicting participants’ amount of willingness to contribute to the NHIP. The analysis highlights significant associations between various factors and the willingness to contribute higher amounts. Participants who refused to contribute or chose lower amounts (less than 50 riyals) were significantly less likely to contribute compared to those willing to contribute between 202 and 250 riyals. A stronger likelihood of contributing was observed by those willing to contribute between 101 and 200 riyals. Participants with moderate confidence in CCI were significantly less likely to contribute higher amounts compared to those with high CCI (estimate = −0.680, 95% confidence interval [CI]: −1.335, −0.025, P = .042). Similarly, those with low HIL were significantly less likely to contribute higher amounts (estimate = −0.784, 95% CI: −1.304, −0.264, P = .003). However, no significant associations were found for CCP and CUI with the willingness to contribute (Figure 3). Only the significant predictors are presented in Figure 3, while the detailed regression results are provided in Supplemental Table S4.

Significant predictors to contribute to National Health Insurance Plan.

Discussion

Among Saudi citizens in the Al-Jouf region, the current cross-sectional study sought to assess the degree of HIL and its correlation with several demographic factors, as well as proactive behaviors, confidence levels in selecting and utilizing health insurance, and willingness to take part in a proposed NHIS. This inquiry coincides with the Kingdom of Saudi Arabia's Vision 2030 plan, which calls for significant advancements in healthcare reform. 20 Determining the health insurance literacy of the populace is essential to guaranteeing the fair and effective execution of national insurance programs. 21

One of the study's most important findings is that the population surveyed had a limited comprehension of key health insurance concepts, as evidenced by the overall low to moderate HIL scores (median score = 4). This is consistent with a study carried out in various nations and areas, which discovered that many Saudi nationals are not well-versed in the fundamentals of health insurance. 22 Interestingly, although most participants (96.57%) had heard of health insurance, only a small percentage (15.93%) were enrolled in any insurance plan. This shows that awareness alone doesn’t always equate to participation. This result is consistent with a study that showed that enrollment is discouraged by ignorance of the use and advantages of health insurance, even in populations with high awareness. 23

Subsequent research showed that PBS (P = .015) and CCI (P = .021) were statistically significantly associated with income level. In particular, people making ≤5000 SR showed more proactive behaviors and greater confidence when choosing insurance than people in higher income brackets. Lower-income people might be more motivated by necessity-driven motivation, which makes them more likely to research their options carefully to guarantee affordability and coverage. 24 This phenomenon aligns with the idea that high perceived personal benefits render economically disadvantaged groups greatly participate in decision making. 25 In contrast, a study found that persons with low-income levels skip health insurance as they worry about the affordability, especially adults who are near retirement. 26

Although post hoc tests were unable to identify the precise differences between marital groups, marital status also demonstrated a significant relationship with CCI (P = .048). This suggests family responsibilities are significantly associated with perceptions of health insurance necessity and confidence in plan selection, aligning with research showing marital status and family size predict Saudis’ likelihood to purchase insurance. 27

The findings also contrast with what has been stated by the WHO, that there is an association between educational attainment and health literacy. Higher educational attainment is positively correlated with a better comprehension of insurance concepts, as demonstrated here. 28 Context-specific factors like consistency in educational curricula or general misunderstanding of insurance-specific terminology, irrespective of educational background, could be the reason why this relationship was not found in the current study. 29 Findings from this study about the variables affecting people's willingness to contribute to and participate in the NHIS were statistically significant. Individuals who demonstrated greater confidence in insurance-related decisions, specifically in CCI, CCP, and CUI, as well as PBS and higher levels of HIL, were significantly more likely to support and participate in the NHIS (P < .001). These findings suggest a statistically significant association between policy engagement and psychological and educational readiness. 30 However, no significant differences in HIL, CCP, CUI, or PBS were observed across gender, age, employment, or education, contrasting with an international study that links education level strongly with health literacy. 31

Despite the moderate to low overall literacy score, the examination of mean and median scores for different constructs revealed moderate levels of confidence and proactive behaviors. For instance, the median CCP score was 9.5, and the median PBS score was 8 (out of 10). These comparatively higher scores indicate that even though participants might not have technical knowledge, they are still actively trying to learn about insurance options. Some studies highlighted that formal literacy and comprehension can occasionally come after behavioral willingness to interact with insurance options. 32

Participants who had low HIL (OR = 0.317, P = .026) and low PBS (OR = 0.222, P = .001) were substantially less likely to indicate a desire to participate in the NHIS. Additionally, unemployment was significantly linked to lower willingness (OR = 0.173, P = .049), which agrees with the systematic review conducted by Bayked et al. 33 Moreover, individuals with low HIL (estimate = −0.784, P = .003) and moderate CCI (estimate = -0- 680, P = .042) were significantly less likely to make larger financial contributions to the NHIS. These findings imply that focused interventions that improve literacy and proactive participation, particularly among lower-income or unemployed populations, could greatly increase NHIS acceptance. 34

The practical implications of insurance literacy and decision-making confidence in influencing the public's willingness to make financial investments in national healthcare programs are highlighted by these statistically significant associations. These results align with existing research, which found that insurance engagement and informed health plan selection are positively correlated with health insurance literacy.35,36 It further agrees with a study that highlighted that enrollment decisions are heavily influenced by insurance confidence; however, another study pointed out that willingness to pay is driven by perceived value rather than just affordability. 37 Age-related trends that have been observed are consistent with the study, which discovered that middle-aged adults were more likely to support health funds and policies. 38 Our findings also indicate more specific awareness campaigns that, in addition to creating familiarity, are associated with increased actionable knowledge as well as self-efficacy. 39 This cross-sectional study showed that good awareness of the social health insurance program encouraged approximately 91.9% of the participants to renew their health insurance in the future. 31

The study's key strength is its focus on the under-researched Al-Jouf region, unlike most Saudi studies centered on Riyadh and Jeddah. It fills a vital data gap and adds value by expanding to a more rural, potentially underserved area. The study used a wide range of measures, such as PBS, HIL, and multiple confidence dimensions (CCI, CCP, and CUI). Unlike similar studies treating HIL as 1-dimensional, this approach offers a nuanced understanding. Nonparametric variables were analyzed with appropriate tests like Mann-Whitney U and Kruskal-Wallis for thorough analysis.

Limitations

Despite its strengths, this study has limitations. The use of nonrandom, convenience sampling and a male-dominated sample (82.11%) may limit generalizability. Participants were recruited from healthcare settings only, which may result in bias. Additionally, self-reported data may introduce bias, and the absence of objective HIL testing affects accuracy. The cross-sectional design prevents causal inference. Additionally, important psychosocial factors, such as trust in healthcare providers or negative past insurance experiences, were not examined, which could influence confidence and willingness to participate.

Future Recommendations

Future policies should include educational initiatives using visual aids, simplified language, and social media to enhance health insurance literacy. Community-based programs, especially for low-income and rural groups, are essential. Future research should adopt gender-inclusive approaches, use longitudinal designs, and incorporate objective literacy tests. Policymakers must tailor NHIS enrollment to varied literacy levels and explore psychosocial factors like perceived fairness and trust in the healthcare system to improve participation.

Conclusion

The study identifies a gap between awareness and actual use of health insurance among Saudi citizens in Al-Jouf. While most people understood health insurance, enrollment rates were low due to limited HIL. Higher HIL was linked to greater confidence in selecting, evaluating, and using insurance, and increased willingness to participate in and contribute to the NHIS. Socioeconomic factors like age, employment, and income influenced engagement, with middle-aged and employed individuals more interested. These findings highlight the need for targeted education and policy efforts to improve HIL, especially among unemployed and low-income groups, supporting Vision 2030's healthcare reform goals.

Supplemental Material

sj-docx-1-jpx-10.1177_23743735251406357 - Supplemental material for Measurement of Health Insurance Literacy and Willingness to Participate in the National Health Insurance Scheme Among Saudis, in Al-Jouf Region: A Cross-Sectional Study

Supplemental material, sj-docx-1-jpx-10.1177_23743735251406357 for Measurement of Health Insurance Literacy and Willingness to Participate in the National Health Insurance Scheme Among Saudis, in Al-Jouf Region: A Cross-Sectional Study by Abdulelah Fayadh Alrashed and Asma Alyaemni in Journal of Patient Experience

Footnotes

Acknowledgements

The author extends appreciation to the Ongoing Research Funding program (ORF-2025-870), King Saud University, Riyadh, Saudi Arabia.

Author Contributions

Both authors contributed equally to the study's conceptualization, methodology, data collection, data analysis, interpretation of results, drafting of the original manuscript, and critical revision of the final manuscript. Both authors approved the final version and agree to be accountable for all aspects of the work.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Ethical Approval

Ethical approval for the study was obtained from the Institutional Review Board (IRB) at King Saud University, under approval number KSU-HE-25-098.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the King Saud University (grant number (ORF-2025-870)).

Informed Consent

Written informed consent was secured from all participants, with materials provided in Arabic to ensure comprehension and compliance.

Statement of Human and Animal Rights

This cross-sectional study involved human participants only, and no animal subjects were involved. All procedures were conducted in accordance with the ethical standards of the institutional research committee and the 1964 Helsinki Declaration and its later and edit.

Supplemental Material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.