Abstract

This study investigates the effect of government pay policy for chief executive officer’s (CEO’s) compensation on corporate innovation (CI). Furthermore, it explores the role of the CEO’s career horizon and shareholding in this nexus. Utilizing the difference-in-differences method to analyze Chinese-listed state-owned enterprises from 2010 to 2020, the baseline findings indicate that government pay policies have had a negative impact on CI. In addition, CEOs with shorter career horizons and higher shareholding demonstrate an enhanced ability to counteract the adverse effects of pay policy, thereby sustaining high levels of innovation. Our findings indicate a necessity for regulatory bodies to re-evaluate mandated constraints on CEO compensation. These restrictions lead to a decline in firm innovation, ultimately affecting shareholder interests. Importantly, the study conclusions remain robust even after rigorous analysis using parallel trend assumptions, propensity score matching, alternative pay policy and innovation metrics, and placebo tests.

Keywords

Introduction

The excessive compensation of chief executive officers (CEOs) relative to common workers has been a topic of intense debate. According to a report by the economic policy institute, CEO pay rose by an astonishing 1,460% between 1978 and 2021, while the wages of average workers increased at a much slower pace. By 2021, CEOs were compensated 399 times more in the United States than the average worker, a sharp contrast to the 20:1 ratio observed in the 1970s (Bivens & Kandra, 2021). Proponents assert that CEO compensation is crucial for attracting and retaining top talent, aligning executive interests with shareholders, and driving decisions that enhance long-term company value and profitability in a competitive market (Jia et al., 2016; Kweh et al., 2022; Q. Li et al., 2024). However, critics argue that the vast sums paid to CEO are often unjustified and need to be aligned with the company’s overall performance (Srivastava et al., 2024). In addition, there is concern that CEO pay packages are grossly exorbitant, further contributing to income inequality (Weng & Yang, 2024).

The ongoing debate surrounding CEO compensation has spurred global initiatives to cap executive salaries, exemplified by legislation such as the CEO Pay Act in both Australia and the United States (Atif et al., 2020; Burns & Minnick, 2013). China has also implemented a government-led policy regulating CEO pay in state-owned enterprises (SOEs), known as government say-on-pay (SOP; policy), which was introduced in 2004 and revised in 2009 before being strictly enforced in 2014. The 2014 version of policy places specific limits on executive compensation, capping CEO base salaries at twice the prior year’s average employee salary, restricting bonuses to twice the base salary, and setting a cap on CEO incentives at 30% of total annual compensation. As a result, SOEs executive total pay is generally limited to around 7–8 times that of the average employee. Recent research has increasingly spotlighted the far-reaching effects of policy, particularly how regulations on CEO pay influence various aspects of organizational performance. Bai et al. (2019) found that such regulations increase stock price crash risk, suggesting a higher likelihood of sudden price declines in regulated firms. Jiang and Zhang (2018) observed that CEO pay regulation reduces firm profitability, while Su et al. (2020) noted a decline in CEO’s willingness to take strategic risks, potentially limiting higher returns. In addition, Jiang et al. (2021), Maqsood et al. (2023), and Q. Li et al. (2024) showed that these policies negatively impact financial performance, social responsibility, and green innovation, highlighting how regulatory constraints can hinder socially responsible and sustainable practices.

Building on existing literature, this study investigates how government regulation of CEO pay affects corporate innovation (CI), using tournament theory (Lazear & Rosen, 1981) as its theoretical foundation. As a primary source of value creation, CI enables firms to adapt to market changes, improve operational efficiencies, and develop groundbreaking products or services that ensure relevance in dynamic business environments. In this context, tournament theory posits that hierarchical pay structures, where substantial gaps exist between ranks, incentivize executives to compete for higher compensation, thereby driving higher performance, particularly in areas like CI (Cai et al., 2021). The rationale for this study stems from the dual role of compensation as both a motivator and a potential constraint. While tournament theory suggests that a larger pay gap motivates CEO to pursue ambitious innovation projects, government-imposed limits on CEO compensation may inadvertently suppress these incentives. By restricting the financial rewards for CEO, government pay policies could reduce their motivation to achieve exceptional performance (Xu et al., 2017), thereby affecting CI outcomes. Moreover, the reduction in executive motivation under regulated pay structures may ultimately undermine firm value and shareholder interests, as decreased commitment to innovation could lead to lower returns on CI efforts (Hirshleifer et al., 2012; Tang et al., 2015).

Prior research on CEO pay structures and innovation presents mixed findings, with studies highlighting three core dimensions of pay disparity: (a) the pay gap between executives and employees, (b) disparities among different executive levels, and (c) variations in compensation between CEOs, other top executives, and employees. Each dimension offers unique insights into how compensation disparities impact CI. For instance, Firth et al. (2015) and Salinas-Jiménez et al. (2010) found that widening the pay gap between executives and employees can harm firm innovation by fostering employee discontent and reducing motivation, ultimately lowering morale and commitment to the organization. Conversely, Lazear and Rosen (1981) and Jia et al. (2016) argue that a broader pay gap among executives can promote CI by motivating CEOs to undertake high-quality innovation projects, improve productivity, and reduce excessive board intervention. Despite these findings, the effect of government-imposed restrictions on CEO compensation and its impact on CI remains underexplored, especially within regulated environments where personal interests may be compromised. This study begins by exploring the following central research question: how does government regulation of CEO pay influence CI? The primary inquiry delves into how regulated pay structures might limit CEO motivation while reshaping the competitive dynamics that typically drive innovation. As pay restrictions are imposed, the balance between the CEO’s financial incentives and their commitment to long-term organizational goals is altered. This dynamic leads to the subsequent inquiry: how do factors such as CEO’s career horizon and CEO’s shareholding moderate this relationship between pay regulation and CI?

The first factor, CEO’s career horizon, is particularly important when considering the strategic choices of CEO near the end of their careers. From the perspective of agency theory, CEO compensation is designed to align the interests of the CEO with those of the shareholders (Jensen & Meckling, 1976). However, this alignment becomes more tenuous as the CEO’s time horizon diminishes. As CEOs approach retirement, their career horizon shortens. This influences their decision-making priorities. This shorter career horizon incentivizes immediate rewards and legacy-building rather than long-term value creation. Upper echelons theory further deepens this understanding by suggesting that the characteristics, experiences, and cognitive biases of executives significantly influence their decision-making and organizational outcomes (Hambrick & Mason, 1984). Career horizon prioritizes short-term goals in CEO cognitive frames, possibly favoring immediate financial gains or strategies that boost short-term performance over investments that foster long-term innovation (Cheng, 2004). These theories highlight how a shortened career horizon can influence CEO behavior, making them more risk-seeking or focused on immediate results, potentially at the expense of long-term innovation such as R&D investments (Matta & Beamish, 2008). This shift is particularly relevant when examining how government-imposed CEO pay regulation may exacerbate this tendency, as the regulation could reinforce the short-term focus of CEOs with limited time left in their careers.

The second moderating factor, CEO’s shareholding, has been identified as an important factor in understanding how pay regulation affects CI. When CEOs hold significant shares in the company, their financial interests are more closely aligned with those of shareholders. Thus, agency theory suggests that this ownership can drive CEOs to make decisions that enhance shareholder wealth, including investments in long-term projects such as innovation (Jensen & Meckling, 1976). Furthermore, stewardship theory posits that CEOs with substantial ownership are more likely to adopt a stewardship-oriented mind-set, viewing their role as responsible stewards of the organization’s resources and prioritizing the long-term success of the company (Davis et al., 2018). In this context, CEO’s shareholding may mitigate the negative effects of government-imposed pay regulations by ensuring that CEOs are still motivated to pursue long-term strategic objectives, including innovation, despite regulatory constraints. Therefore, the moderating role of CEO’s shareholding is essential to understand in this nexus, as it may enable CEOs to continue pursuing innovative strategies, even in the face of restrictive compensation policies.

To empirically investigate the research questions, this study uses a sample of Chinese SOEs spanning the period from 2010 to 2020. The approach to measure innovation variables is followed by Cai et al. (2021) and Maqsood et al. (2023). CI is measured as the count of patent applications (reflecting innovation quality) and research and development (R&D) expenditure (reflecting innovation intensity). Innovation quality is used in baseline models, while innovation intensity serves as an alternative measure for robustness tests. To capture government CEO pay regulation, a “policy” variable is introduced which equals 1 for the years 2014 and onward; otherwise, it is 0. Moreover, for robustness, a multifaceted variable “government pay restrictions” is incorporated with three distinct indicators, derived from the studies of Q. Li et al. (2024) and Jiang et al. (2021). Applying the difference-in-differences (DiD) methodology alongside an alternative fixed-effect regression model, which ensures robust treatment effect estimation. The study’s initial results suggest a negative association between policy and CI in regulation-targeted firms, and these results hold true when using the parallel trend assumption, propensity score matching (PSM), placebo tests, and alternative measures of government pay restrictions and CI. Furthermore, moderation analysis reveals that the negative impact of policy on CI is positively moderated by the CEO’s career horizon and shareholding. In addition, heterogeneity analysis indicates a more pronounced negative impact for local SOEs than for central SOEs. In sum, this study not only fills a critical gap in research but also offers a methodologically and empirically grounded exploration of the intricate relationships among government regulations, CI, and moderating factors in the Chinese business context.

This study makes a groundbreaking contribution by examining the intersection of government regulation for CEO compensation and CI, with a focus on Chinese firms. Unlike previous research, which has primarily analyzed the direct link between CEO pay and innovation (Cai et al., 2021; Shahzad et al., 2022; Xu et al., 2017), this study uniquely explores how government regulations shape CEO compensation structures, thereby influencing innovation. By differentiating the effects of government-regulated pay policies from shareholder-driven mechanisms like SOP, this research introduces a new perspective on how external regulatory pressures align executive incentives with long-term innovation goals. This novel framework is adaptable to other global regulatory contexts, such as those in the United States and Australia, where the interplay between government intervention and corporate governance is increasingly under scrutiny.

From an empirical standpoint, this study enriches the understanding of how government regulation of CEO compensation can drive CI on a global scale. Through the unique case of China, where government oversight in corporate governance is particularly strong, the findings offer broader relevance to regulatory environments in other regions, such as South Korea and Russia, where government influence also plays a significant role. In addition, the study emphasizes the moderating roles of CEO’s shareholdings and career horizon in the CEO pay policy-innovation relationship. These factors, often overlooked in traditional studies, emerge here as critical determinants of corporate behavior, underscoring that regulatory changes do not affect all executives uniformly. Specifically, CEO’s shareholdings play an essential role by aligning executive incentives with corporate goals, while long-term career horizons significantly enhance CEO’s engagement with innovation. The study’s theoretical contributions are also significant, as it broadens the literature on executive pay disparity by moving beyond team-level inequalities (Berri & Jewell, 2004) to encompass disparities among senior executives and their impact on innovation. CEOs play a central role in shaping corporate strategy, and by examining how their compensation structures influence innovation outcomes, this research provides a deeper understanding of regulating executive compensation’s far-reaching implications on corporate behavior and strategic goals. Furthermore, by treating government intervention in CEO compensation as an external shock, this study extends the theoretical literature on regulatory impacts on wealth inequality and corporate outcomes. This approach aligns with the foundational work of scholars like Murphy and Jensen (2018), while advancing discussions around government SOP policies and their environmental, social, and financial consequences (Bai et al., 2019; Jiang et al., 2021; Q. Li, et al., 2024; Maqsood et al., 2023; Su et al., 2020). This framework offers an enriched theoretical lens to understand the implications of government-led regulation, particularly in fostering or challenging CI through regulating executive compensation.

The remainder of this paper is organized as follows. The Background and literature review section provides a background of government pay restriction and a literature review. The Hypothesis development section demonstrates the hypothesis development. The Data source, variable measurement and research methods section details the dataset, variable measurements, and the regression model. The Empirical findings section provides the empirical results and a series of robustness tests, followed by the Conclusion section.

Background and literature review

Chinese government restriction of CEO pay

The optimal control of excessive executive compensation is best achieved through two different mechanisms: rational shareholder and market forces intervention (Obermann & Velte, 2018). The first mechanism, the shareholder control approach, ensures that compensation packages are aligned with performance metrics and shareholder interests, discouraging unjustified rewards that may not be warranted by company performance (Dittmann et al., 2011). The second mechanism is government regulation of CEO compensation, which has gained significant attention globally, with measures such as the CEO Pay Act in Australia and the United States (Atif et al., 2020; Burns & Minnick, 2013). Specifically, in China, the government has taken substantial steps to promote pay equality, particularly by limiting CEO compensation. In 2004, China introduced its first executive compensation laws and guidelines for all SOEs. These regulations specify a formula for determining the maximum compensation of top executives, including the CEO, deputy CEO, and CFO. The formula incorporates factors such as total assets, major operational revenues, net assets, and net profit. In addition, it considers the average employee wages across all SOEs nationwide, within the same geographic area, and within the same industry to establish senior executives’ pay levels. Later, this policy was updated to include executives’ retirement benefits and insurance as part of the concept of executive compensation, overseen by the Ministry of Finance, the State-Owned Assets Supervision and Administration Commission, the Ministry of Human Resources and Social Security, and the Organization Department of the Communist Party of China. In 2014, China strengthened its policy on executive compensation by imposing stricter limits. Senior executives’ base salaries were capped at no more than double the average salary of regular employees. In addition, any bonuses from share-based incentives were restricted to a maximum of twice the executive’s base salary. Although stock-based compensation is infrequently utilized in Chinese SOEs, the 2014 legislation stipulated that share-based incentives for top executives could not exceed 30% of their total annual compensation. This regulation also introduced swift consequences for policy violations or organizational delays in enforcement. Therefore, the 2014 regulations provide a comprehensive basis for conducting a regulatory impact assessment.

Related literature

CEOs are pivotal figures in a firm, holding substantial influence over its strategic direction and overall performance. As the primary decision-makers, their compensation and behavior are crucial factors that shape a company’s outcomes, particularly in areas like CI. A significant body of research has explored how CEO compensation impacts a firm’s behavior and performance, highlighting both positive and negative effects. For instance, Firth et al. (2015) observed that an increasing pay gap between executives and employees can negatively affect a firm’s innovation and productivity. This observation is further supported by Salinas-Jiménez et al. (2010) and Sommet et al. (2019), who found that a wider pay disparity tends to foster employee discontent, reducing their motivation and ultimately undermining organizational performance. When employees perceive unfair compensation disparities, their morale and commitment to the organization diminish, ultimately impacting their capacity to contribute to innovation. Building on these findings, Xu et al. (2017) demonstrated that unfair compensation reduces motivation and that discontent among employees directly impedes a firm’s innovation. Conversely, Lazear and Rosen (1981) argue that a pay gap among executives incentivizes high-quality innovation projects and improves efficiency and productivity. Furthermore, Jia et al. (2016) found that a higher pay gap between CEOs and other executives can promote innovation by attracting talent and reducing board intervention. In addition, Xu et al. (2017) reveal that while a pay gap among executives positively impacts CI, a pay gap between executives and employees harms CI.

The corporate governance literature focusing on CEO compensation draws increasing scrutiny and is sparking debate about the optimum structures and regulations for executive pay (Murphy & Jensen, 2018). This attention underscores the importance of examining how regulating CEO compensation impacts a firm’s performance and innovation, highlighting the need for frameworks that align pay structures with company goals and stakeholders’ expectations. Two primary approaches for regulating executive compensation have emerged in the literature: internal SOP and external SOP mechanisms (Banker et al., 2016; Obermann & Velte, 2018). Internal SOP involves shareholder or board approval of CEO compensation during annual meetings, allowing for internal oversight and accountability. Here, boards of directors design pay structures, and shareholders approve them to reward performance while managing potential risks of excessive payouts (Dittmann et al., 2011). In contrast, external SOP involves government or policy interventions that require firms to submit compensation plans to mandatory shareholder votes at annual meetings, aiming to set uniform standards and bring greater transparency to CEO pay practices. Together, these frameworks are essential tools for addressing discrepancies in pay structure and ensuring that executive compensation aligns with long-term corporate objectives. Research on the shareholder SOP framework has gained traction over time. Some studies suggest that an increasing role for shareholders in monitoring executive pay can enhance a firm’s performance (Balsam et al., 2016; Cai & Walkling, 2011), while others present contrasting evidence, suggesting that greater shareholder involvement may not always benefit a firm’s performance (Knutt, 2005). Further evidence indicates that implementing a shareholder SOP framework can help companies struggling with inefficient executive compensation practices. However, the impact of this framework may vary for firms facing labor-sponsored proposals. Typically driven by activists, these proposals often target larger companies grappling with issues such as excessive CEO pay, poor governance, or underperformance (Cai & Walkling, 2011).

Despite extensive research on shareholder SOP mechanisms, literature on government-led executive pay regulation remains limited, with minimal evidence on its effects on corporate outcomes. Previous studies have examined the influence of executive pay regulation on various corporate elements, finding that government regulation may reduce stock price crash risks (Bai et al., 2019), lower CEO’s risk-taking capabilities (Su et al., 2020), decrease a firm’s efficiency (W. Li et al., 2024), and diminish green innovation (Q. Li et al., 2024). Some studies even indicate that such regulations can prompt talented CEOs to leave (Nanda et al., 2024), potentially eroding leadership stability and firms’ performance. However, the impact of government-imposed pay regulation on CI has been largely overlooked, leaving a critical gap in understanding the comparative effects of government-imposed regulations versus market-driven compensation frameworks on CI. Our study addresses this gap by examining the implications of government regulation on CEO pay within Chinese SOEs. This study contributes to a nuanced understanding of how external regulatory intervention shapes CI and informs future policy decisions on executive compensation.

Hypothesis development

Government pay restriction and CI

Government regulation of CEO compensation, while aimed at ensuring accountability and curbing excessive pay, may have unintended consequences. By imposing strict limitations on CEO compensation or tying pay to rigid, non-performance metrics, regulatory frameworks can inadvertently create an environment where CEOs are less incentivized to take the risks necessary for groundbreaking innovation. This issue is particularly relevant in the context of Chinese SOEs, where government influence is pervasive, and compensation structures are closely monitored. Innovation is often fueled by incentives that promote risk-taking (Giaccone & Magnusson, 2022), the ability to attract top executive talent (Chemmanur et al., 2019), and a rapid response to market changes. Therefore, restrictions on CEO compensation could hinder these key drivers, potentially stifling long-term innovation within organizations.

Scholars have empirically examined these drivers and provided evidence on how they influence CI. Risk-taking is essential for CI as it enables firms to explore untested areas, often leading to breakthroughs that strengthen competitive advantage (Giaccone & Magnusson, 2022). Likewise, aligning CEO incentives with innovation goals encourages leaders to prioritize and invest in innovative activities, directly linking their compensation to the firm’s innovation outcomes (Cai et al., 2021). Furthermore, skilled talent management is crucial in driving innovation, as ensuring top talent is directed toward creative, high-impact projects is key (Chemmanur et al., 2019). In addition, crisis conditions can spur innovation by forcing firms to adapt rapidly, prompting them to seek novel solutions (Dahlke et al., 2021). In regulated environments, particularly under government intervention, these dynamics become even more complex. CEO pay regulation reduces the incentive for risk-taking (Su et al., 2020). Innovation often requires bold, uncertain investments, and without substantial personal rewards tied to success, CEOs may be discouraged from pursuing high-risk initiatives. When compensation is capped or overly restricted by regulations, the potential for personal financial gain diminishes, leading CEOs to avoid ventures that, although risky, could be highly innovative and transformative for the company (Giaccone & Magnusson, 2022). Moreover, the regulatory environment may also pose challenges in attracting and retaining top talent (Nanda et al., 2024). Competitive executive compensation is essential for attracting visionary CEOs, particularly in industries where innovation is crucial (Chemmanur et al., 2019). In highly regulated environments, where CEO pay is limited, firms may struggle to recruit leaders with the entrepreneurial spirit and experience needed to drive innovative projects. Consequently, talented CEOs may prefer roles in less-regulated sectors where their compensation is more directly tied to their performance, diminishing the innovative potential of regulated firms. Furthermore, pay regulatory oversight often introduces compliance requirements that can slow down decision-making (W. Li et al., 2024), reducing a firm’s efficiency in responding to market dynamics. CEOs in highly regulated firms may find themselves prioritizing regulatory adherence over the agile execution of innovative strategies, causing the firm to lag in adapting to rapidly evolving market demands.

The focus of the current study is to examine the impact of regulatory intervention, specifically government SOP policies, on CI. This study distinguishes itself from existing literature on shareholder SOP frameworks by focusing on tournament theory, which utilizes pyramid compensation structures to inspire and reward superior performance among CEOs (Lazear & Rosen, 1981). According to tournament theory, a wider pay gap can incentivize CEOs to exert greater effort, potentially leading to higher-quality innovation projects and improved efficiency and productivity (Cai et al., 2021). Conversely, restricting or reducing CEO compensation may lower motivation and discourage CEOs from demonstrating superior performance. When personal interests are not adequately fulfilled due to compensation restrictions, it can undermine value creation, ultimately impacting shareholder interests within the firm. In the Chinese context, Jia et al. (2016) propose that a wider pay gap between CEOs and other executives can stimulate innovation by attracting talent and reducing board intervention. In contrast, Xu et al. (2017) found that a substantial pay gap between executives and ordinary employees can have a detrimental effect on CI. Drawing on tournament theory, which posits that fostering competition encourages innovation, regulatory constraints on CEO pay imposed by the government might deter CEOs from engaging in high-quality innovation initiatives. Therefore, it is hypothesized that:

Moderating role of CEO’s career horizon

As CEOs approach retirement, their career horizon typically shortens, which can influence their decision-making processes and risk-taking behavior (Kang, 2016). This shift in strategic priorities and behaviors is key to understanding the relationship between pay regulation and CI, and how it is moderated by CEO’s career horizons.

The concept of the CEO’s career horizon is deeply embedded in the broader understanding of executive decision-making, particularly in relation to the temporal context within which CEOs operate. As CEOs approach the end of their careers, their decision-making horizon typically shortens, which has significant implications for their strategic choices. From a theoretical standpoint, the shift in focus due to a shortened career horizon can influence both the nature of corporate decisions and the long-term direction of the firm. Agency theory serves as a foundational framework for understanding the role of compensation in aligning CEO interests with those of the firm (Jensen & Meckling, 1976). The core idea is that executive pay structures should incentivize CEOs to act in the best interest of the shareholders. However, as CEOs approach retirement, their temporal horizon for decision-making narrows, which can lead to a shift in priorities. CEOs with short career horizon are less concerned with the long-term health of the organization and more focused on securing immediate, personal gains (Cho & Kim, 2017). This shift is particularly relevant in the context of executive compensation, where CEOs nearing retirement may prioritize strategies that offer short-term financial benefits, such as cost-cutting measures or acquisitions, over investments in long-term innovation. In addition, upper echelons theory, which argues that executives’ experiences, values, and cognitive frames shape organizational outcomes (Hambrick & Mason, 1984), provides further insights into how a CEO’s career horizon influences their decision-making. As the end of a CEO’s tenure draws near, their cognitive frames may increasingly prioritize short-term tangible achievements over long-term strategic planning. This can manifest in decision-making that favors actions that provide immediate financial results or enhance the CEO’s legacy, such as aggressive stock buybacks, pursuing high-risk, high-reward ventures, or even focusing on market share expansion at the expense of innovation and R&D investments (Cheng, 2004). CEOs in their final years may also feel a stronger sense of urgency to demonstrate their leadership effectiveness, leading to an inclination toward decisions that produce immediate visible outcomes rather than those that will have a delayed effect.

Empirical studies support these theoretical perspectives. For instance, Xu and Yan (2014) suggest that CEOs with short career horizons tend to pursue strategies with immediate payoffs, like acquisitions or high-return projects. On the other hand, Matta and Beamish (2008) find that CEOs with short career horizons are more likely to pursue international acquisitions, indicating a preference for strategic growth and innovation over short-term financial rewards. The risk-seeking behavior of CEOs nearing retirement, particularly those with substantial equity holdings or unexercised stock options, may further skew decisions toward quick returns, often sidelining long-term innovation efforts essential for sustained competitiveness. In line with the findings of Su et al. (2020), which suggest that CEO pay regulation reduces the tendency for CEOs to engage in risky behavior, it is likely that such regulation also influences how CEOs with short career horizons approach CI. CEOs nearing retirement may be more inclined to pursue risky initiatives that benefit their personal and professional interests in the short term, potentially detracting from long-term investments in innovation. Building on these theoretical insights, the following hypothesis H2 is proposed:

Moderating the role of CEO’s shareholding

The relationship between CEO’s shareholding and CI has attracted increasing attention within academic and policy circles, particularly in the context of external regulatory frameworks such as government-imposed pay restrictions. This connection holds critical implications for understanding how corporate executives, when holding substantial stakes in their organizations, may navigate the complexities of external constraints and still pursue innovation-driven growth (Flath & Knoeber, 1985). This question becomes particularly relevant when we consider how ownership interests could potentially reshape the dynamics of decision-making, particularly in environments where government regulations impose limitations on CEO compensation.

To approach this inquiry, we can draw on agency theory (Jensen & Meckling, 1976), which offers a foundational framework for understanding the alignment of interests between CEOs and shareholders. In the context of CEO’s shareholding, agency theory suggests that executives with a significant ownership stake in the firm are incentivized to make decisions that directly contribute to the financial success of the organization. By linking personal financial outcomes to the firm’s performance, these CEOs may be better positioned to counteract the potential downsides of regulatory pay restrictions, which could otherwise discourage risk-taking and long-term strategic investments, such as those needed for innovation. In this regard, CEO ownership can serve as a moderating factor, fostering an environment where innovation remains a priority despite the limitations imposed by external forces. Building on this, stewardship theory by Davis et al. (2018) offers an alternative, yet complementary perspective, which emphasizes a CEO’s intrinsic motivations to act in the best interest of the firm, particularly when their personal stake in the organization is substantial. Rather than focusing solely on self-interested behavior, stewardship theory suggests that CEOs with significant ownership are more likely to adopt a long-term, sustainable vision for the company. This perspective underscores the idea that ownership can foster a stewardship orientation, where the CEO sees themselves as a guardian of the firm’s resources, driven by a sense of responsibility to ensure its continued growth and innovation. In this light, pay restrictions may not dampen the CEO’s drive for innovation, but rather, ownership creates a deeper sense of commitment to the firm’s long-term success.

This dual theoretical lens provides a richer understanding of how CEO’s shareholding may influence CI, especially when pay policies are in play. Research has shown that when CEOs hold a significant equity stake in their companies, they are more likely to engage in innovative activities, as their personal wealth is closely tied to the firm’s performance. Kamoto (2017) argues that management buyouts, which often involve CEOs acquiring significant shares in their firms, lead to increased innovation intensity, as these CEOs are more motivated to drive a firm’s performance. Similarly, studies by Lin et al. (2021) and others have highlighted a positive relationship between CEO’s shareholding and CI, suggesting that higher ownership levels foster a greater commitment to innovation and long-term value creation. Moreover, the findings by Su et al. (2020) and Maqsood et al. (2023) support the notion that CEO’s shareholding can serve as a counterbalance to the potentially adverse effects of external pay restrictions. In this context, CEOs with substantial ownership can better navigate the challenges posed by these policy constraints, maintaining their focus on innovation and strategic risk-taking despite the regulatory environment. Their ownership stake ensures that their personal financial interests are aligned with the firm’s long-term performance, which may mitigate any tendency to limit risk-taking behaviors in the face of pay regulations. Based on the theoretical perspectives of agency theory and stewardship theory, as well as the empirical evidence on CEO’s shareholding, the current study proposes the following hypothesis:

Data source, variable measurement, and research methods

Data sample and source

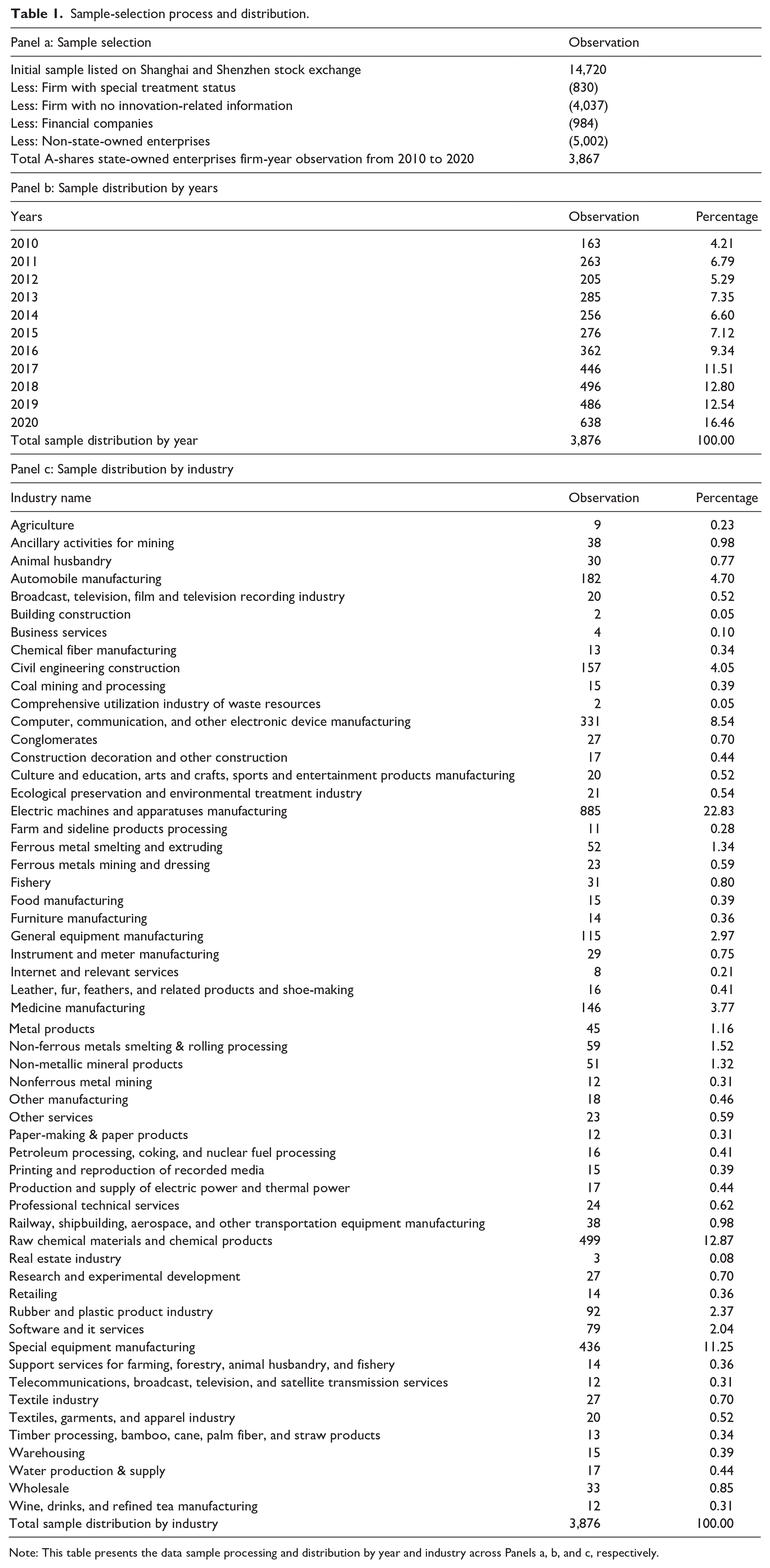

The data used for this study were sourced from the CSMAR (China Stock Market & Accounting Research) database, covering the period from 2010 to 2020. The sample selection focused on SOEs listed on the Shanghai and Shenzhen stock exchanges. To ensure data quality, specific exclusions were made; financial firms, firms with special treatment, and firms with missing values were excluded from the analysis. After applying the selection criteria, 3,876 firm-year observations were included in the final dataset. The government’s pay policy targeting only SOEs motivated the decision to examine SOEs specifically. By concentrating on SOEs, the analysis aims to gain insights into the unique characteristics and dynamics of these government-controlled entities, particularly concerning executive compensation and ownership structure. Table 1 provides a detailed explanation of the sample-selection process and the distribution of data by year and industry, respectively.

Sample-selection process and distribution.

Note: This table presents the data sample processing and distribution by year and industry across Panels a, b, and c, respectively.

Dependent variable measurement

Existing studies have examined the CI index using various metrics. These include input innovation measures, such as R&D expenditure, which indicate the intensity of innovation, and output innovation measures, such as patent applications, grants, and citations, which reflect innovation outcomes. Among these metrics, patent applications are noted for their rapid and accurate portrayal of innovation output compared to R&D investment (Cai et al., 2021; Kong et al., 2017). Therefore, in our baseline regression, we quantify innovation output using the natural logarithm of one plus the number of patent applications. Moreover, the generation of high-quality patents is important for economic progress (Zhang et al., 2018). Patent quality is often assessed by the number of citations they receive. However, our evaluation of patent quality is limited to the categories outlined in Chinese Patent Law, specifically patents for inventions, utility models, and designs, which vary in quality. Consequently, we use the count of invention patents as an indicator of technological innovation given the Chinese government’s stringent standards on the uniqueness and quality of inventions (Kong et al., 2017). In contrast, utility models and designs undergo less-rigorous evaluation; for instance, utility model assessments primarily ensure the adherence of application materials to specific format and fee requirements (Zhang et al., 2018). This distinction leads us to consider invention patents to be the most innovative and original, thus reflecting superior innovation quality. Innovation quality is measured using the natural logarithm of one plus the count of invention patent applications.

In addition, to enhance the robustness of the baseline regression model and ensure comprehensive findings, this study includes input innovation ratios, such as R&D to total assets and R&D to total sales, as alternative proxies for the CI index in supplementary regression models.

Independent variable measurement

Following prior studies on government CEO pay regulation and their impact on corporate performance, such as those by Maqsood et al. (2023), Su et al. (2020), and W. Li et al. (2024), this study measures government pay regulation as a binary policy variable, reflecting the implementation of CEO pay-regulation reforms. These reforms, which act as an external shock, specifically target SOEs and are expected to influence CI. The policy variable is coded as 1 if the CEO pay regulation reform was implemented in or after 2014, and 0 otherwise. This approach aligns with existing research that considers regulatory changes as significant external shocks affecting a firm’s behavior. In addition, to isolate the effect within SOEs, an interaction term is created by multiplying the policy-2014 indicator (Policy) with an SOE indicator (1 for SOEs and 0 for non-SOEs). This interaction term, SOEs × Policy, captures the differential impact of the government pay regulation on SOEs, allowing for a clear assessment of its effect on CI specifically within these firms.

Control and moderating variables measurement

Drawing from studies on CI and CEO pay regulation (Cai et al., 2021; Q. Li et al., 2024; Maqsood et al., 2023; Su et al., 2020), we incorporate various firm-level and board-level variables into our analysis.

Firm-level variables include leverage (Leverage), represented by the ratio of total liabilities to total assets; property plant and equipment (PPE), calculated as the natural logarithm of net property, plant, and equipment divided by the number of employees; firm age (age), measured as the natural logarithm of the number of years since listing; and the operating cash flow (OCF) ratio, calculated as OCF divided by total assets. In addition, we account for market concentration using the Herfindahl-Hirschman Index (HHI), which is calculated by taking the market share of each firm in the selected industry (the details of these industries are presented in Table 1, Panel c). At the board level, we include CEO duality (Duality), where a dummy variable equals 1 if the CEO also serves as the board’s chairman; board size (BS), defined as the natural logarithm of the number of directors on the board; and independent directors (IND), represented by the percentage of INDs on the board.

For the moderating analysis, we introduce two variables: CEO’s career horizon (CEO_HRZ) and CEO’s shareholding (CEO_SH). The CEO_HRZ variable captures the length of a CEO’s remaining career based on the assumption that the retirement age is 70. It is calculated by subtracting the CEO’s current age from 70, indicating that younger CEO possess a longer potential career horizon. This longer horizon suggests a greater likelihood of making decisions with long-term impacts, as they are more likely to remain in the role and experience the outcomes of their choices (Matta & Beamish, 2008). In contrast, shorter career horizons may prompt CEOs closer to retirement to prioritize immediate gains over long-term goals. On the other hand, CEO_SH is assigned a value of 1 if the CEO’s shareholding is above the median, and 0 otherwise, based on the study by Maqsood et al. (2023). Table 2 provides detailed definitions of all variables used in the study.

Variable definition.

Note: This table presents the definitions and sources of calculation for all variables used in this study.

Research methodology

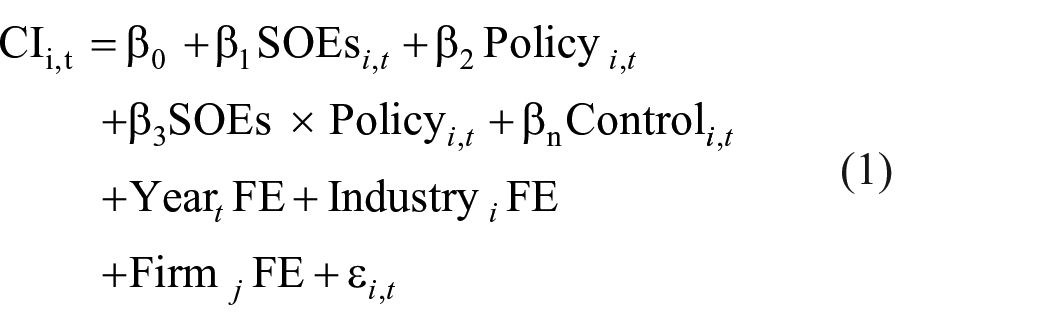

To empirically examine how government regulations on CEO pay affect CI, our analysis begins by employing the DiD model. We use Equation (1) as the baseline regression model.

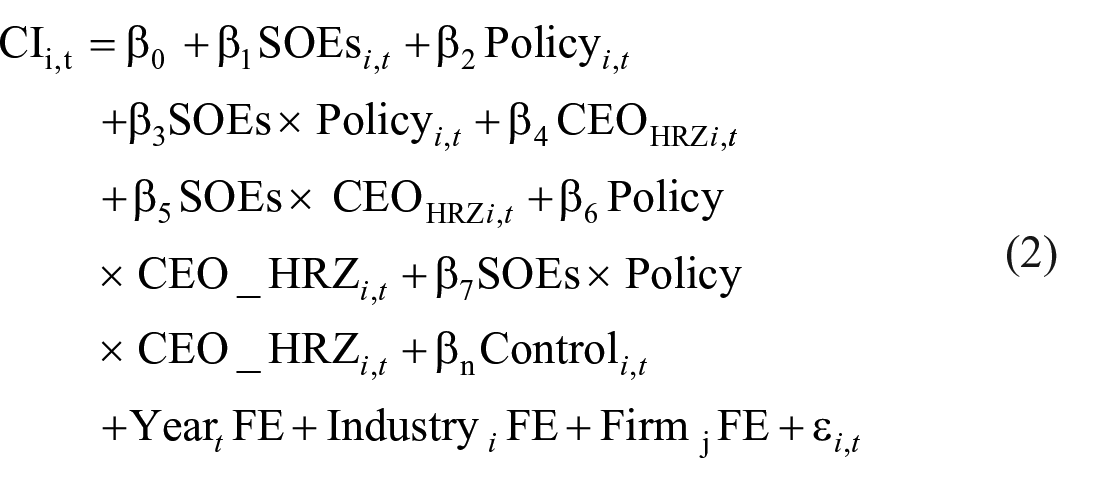

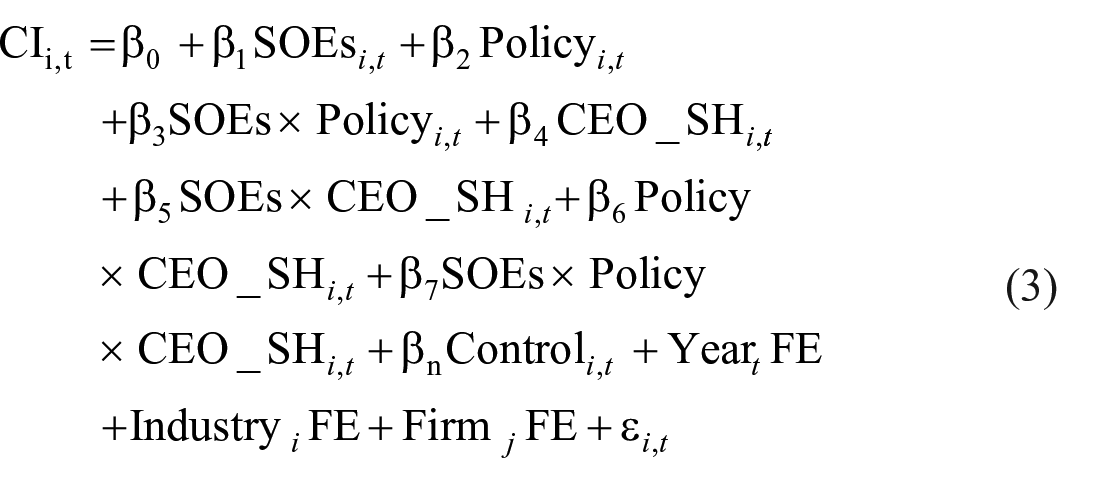

Furthermore, we apply Equations (2) and (3), which are modifications of Model (1), to evaluate our H2 and H3.

In all models, the dependent variable is CI, which represents two proxies for innovation, namely patents and inventions. The variable of interest in Equation (1) is the interaction term between SOEs (the treated group) and Policy (which signifies whether the observation occurs during or after 2014). The second model, Equation (2), examines the interaction between CEO’s career horizon (CEO_HRZ), Policy, and the treated group, while the third model, Equation (3), explores the interaction between CEO’s shareholding (CEO_SH), Policy, and the treated group. All three models (1, 2, and 3) incorporate the control variables outlined in the Independent variable measurement section. In addition, year, industry, and firm fixed effects are included to account for industry-firm-specific and time variations. Moreover, if the value of β7 in Equations (3) and (4) are significant, this indicates that the effect of government policy on CI is moderated by the selected moderator in this study. The random error terms are denoted by ε.

Empirical findings

Descriptive statistics

Table 3 presents the descriptive statistics for the variables employed in this research. Specifically, the mean values for the CI proxies are 3.159 for utility and 1.866 for invention. Discrepancies in the averages among the CI may stem from differences in innovation nature, resource allocation, or industry variation. In addition, the variable “Policy” has a mean of 0.441, which accounts for approximately 44.1% of the potential impact of CEO pay regulation within our dataset. These mean values for CI and “Policy” closely align with findings reported in previous studies (Cai et al., 2021; Maqsood et al., 2023; Shahzad et al., 2022).

Descriptive statistics.

Note: This table provides the descriptive statistics of all variables. The first three columns show the mean, standard deviation, and median, while the last two columns show the 25th percentile (P25) and 75th percentile (P75). The total number of observations N = 3,876. SOE: state-owned enterprise; OCF: operating cash flow; HHI: Herfindahl-Hirschman Index.

The alternative variables 1 representing government pay policy exhibit specific characteristics. To begin with GovSOP1, a mean value of 7.709 indicates that the wage disparity between SOEs and non-SOEs is eight times larger for SOEs. A higher value (a less negative number) in GovSOP1 signifies a higher degree of pay disparity. To aid comprehension, the raw values of GovSOP2 and GovSOP3 are multiplied by −1. Considering GovSOP2, which has an average value of −5.742%, it suggests that salaries of SOE executives are around six times greater than those of regular employees. Meanwhile, the average value of GovSOP3 is −15.267, indicating that the top three executives in SOEs earn 15.267 times more than other executives on average.

Main result

Government pay restriction and CI: a DiD analysis

The baseline results shown in Table 4 highlight several key findings related to the effects of the CEO pay regulation policy. First, the SOE variable shows a positive and statistically significant coefficient of 0.123 in Column 1 and 0.317 in Column 2, suggesting that prior to the policy implementation, SOEs were more innovative than non-SOEs. Next, the Policy variable, which measures the overall effect of the CEO pay regulation on CI, shows negative coefficients of −0.065 and −0.023 in Columns 1 and 2, respectively. However, these coefficients are not statistically significant, indicating that the policy alone does not have a significant effect on innovation. This lack of significance suggests that the pay restriction, when applied universally, does not directly influence innovation outcomes.

Impact of government pay restriction on corporate innovation: difference-in-difference estimation at different specifications.

Note: This table presents the baseline impact of government pay regulation on CI. The term SOEs × Policy represents the interaction between the variables SOEs and pay policy. Definitions for all other variables are provided in Table 2. Standard errors are shown in parentheses. SOE: state-owned enterprise; OCF: operating cash flow; HHI: Herfindahl-Hirschman Index.

Statistical significance levels are indicated as follows: ***p < .01, **p < .05, *p < .1.

The main variable of interest, however, is the SOEs × Policy interaction term, which examines the differential effect of the CEO pay regulation on SOEs compared to non-SOEs. The interaction term shows negative coefficients of −0.216 and −0.036 in Columns 1 and 2, both of which are statistically significant at the 5% and 1% levels, respectively. The negative sign suggests that, while SOEs were more innovative before the policy, the introduction of the pay restriction resulted in a decrease in innovation levels for SOEs relative to non-SOEs. This highlights the unintended consequence of the policy: although it was intended to regulate executive compensation, it may have inadvertently reduced innovation in the very firms it targeted. Furthermore, when firm and year fixed effects are added (Columns 3 and 4), the coefficient for the SOEs × Policy interaction term remains negative, although its magnitude decreases to −0.024 and −0.174, with the latter being statistically significant at the 10% level. This suggests that even after controlling for additional firm-level and temporal factors, the negative effect of the policy on innovation in SOEs persists, although it is somewhat diminished. These findings are not only statistically significant but also economically meaningful. For example, based on the standard deviation of the policy (0.497) and the mean of patent (3.159), using the reported coefficient of SOEs × Policy in Column 1 of Table 5, we calculate that each standard deviation increase in regulation leads to a 3.39% [(0.216) × (0.497)/3.159] decrease in CI.

Government pay restriction and corporate innovation: moderating role of CEO’s career horizon.

Note: This table presents the results of the moderating role of CEO’s career horizon (CEO_HRZ) in the relationship between pay policy and CI nexus. Standard errors in all columns are reported in parentheses, and significance levels are denoted as ***p < .01, **p < .05, and *p < .1. Definitions of all variables can be found in Table 2, and the estimated coefficients are obtained using Equation (2).

Moreover, our findings contribute to the discourse by demonstrating a negative impact of pay policy on CI, which aligns with the unintended consequences discussed by Murphy and Jensen (2018) and the hindrance to firms’ green innovation and ESG performance (Q. Li et al., 2024; Maqsood et al., 2023). This comprehensive viewpoint reinforces the case for thoughtful deliberation in CEO pay regulation to prevent unintended adverse effects on different facets of corporate performance.

Government pay restriction and CI: moderating role of CEO’s career horizon

We expand our analysis by introducing the CEO’s career horizon (CEO_HRZ) as a moderating variable to explore its influence on CI within the context of government-imposed CEO pay restrictions. This model assesses the interaction between CEO’s career horizon, SOEs, and the pay-regulation policy, offering insights into how CEO’s career horizon shapes innovation outcomes under the policy.

The findings presented in Table 5 indicate that the CEO_HRZ variable itself is not statistically significant across any of the columns, with coefficients ranging from −0.017 to −0.009. This suggests that, in isolation, the CEO’s career horizon does not have a direct effect on patent or invention. Therefore, CEO’s career horizon does not independently drive innovation in this context. However, the interaction between SOEs × CEO_HRZ shows significant results. In Column 1, the coefficient is 0.034, and in Column 2, the coefficient is 0.018. These results indicate that the CEO_HRZ moderates the relationship between being an SOE and innovation, with long-term-oriented CEOs (those with a longer career horizon) more likely to foster innovation within SOEs. The positive coefficients suggest that CEOs with a longer career horizon can offset the negative impact of being an SOE on innovation, particularly in patenting activities. The interaction between the Policy × CEO_HRZ also yields significant results. In Column 1, the coefficient is −0.021, and in Column 2, it is −0.016. This suggests that CEOs with longer career horizons exacerbate the negative effects of the pay restriction policy on innovation, reinforcing the overall negative relationship. However, this also implies that long-term-oriented CEOs may be better equipped to adjust their firms’ strategies in response to pay regulations, even though the policy’s overall impact on innovation remains detrimental

Finally, the three-way interaction between SOEs × Policy × CEO_HRZ is significant across all columns. In Column 1, the coefficient is 0.048 (significant at the 5% level), and in Column 2, it is 0.027 (significant at the 5% level). In Columns 3 and 4, the coefficients are 0.032 and 0.021, respectively, significant at the 1% and 10% levels. This three-way interaction suggests that the negative impact of the CEO pay restriction policy on innovation in SOEs can be partially mitigated by CEO’s career horizon. Specifically, CEOs with longer career horizons help alleviate some of the adverse effects of the pay regulation on innovation outcomes. The positive coefficients indicate that long-term-oriented CEOs can counterbalance the policy’s negative impact, likely due to their ability to make strategic decisions that prioritize long-term firm growth despite regulatory constraints. This finding aligns with previous studies by Cho and Kim (2017) and Xu and Yan (2014), which highlight that CEOs with shorter time horizons tend to de-prioritize innovation.

Government pay restriction and CI: moderating the role of CEO’s shareholding

We further examine the moderating role of CEO’s shareholding (CEO_SH) on the relationship between SOEs, the policy, and CI, while accounting for industry and year fixed effects in Columns 1 and 2, and firm and year fixed effects in Columns 3 and 4. The results from Table 6 show that the influence of CEO_SH on innovation outcomes varies based on the fixed effects specification and the innovation measures being analyzed.

Government pay restriction and corporate innovation: moderating the role of CEOs’ shareholding.

Note: This table displays the outcomes of how CEO’s shareholding (CEO_SH) moderates the relationship between pay policy and CI nexus. Standard errors are shown in parentheses. Definitions for all variables can be referenced in Table 2, and the estimated coefficients are derived from Equation (3).

Significance levels are indicated as ***p < .01, **p < .05, and *p < .1.

In Columns 1 and 2, where industry and year fixed effects are applied, the coefficient for CEO_SH is positive and significant, with values of 0.192 in Column 1, and 0.226 in Column 2. These findings suggest that CEO’s shareholding positively impacts both patent and invention innovation, particularly within industry contexts. However, in Columns 3 and 4, which use firm and year fixed effects, the results diverge. In Column 3, the coefficient is negative (−0.172), and in Column 4, it is slightly positive (0.057), but neither are statistically significant. This variation indicates that the effect of CEO’s shareholding on innovation may be more nuanced when considering firm-specific characteristics in addition to industry trends. The interaction term SOEs × CEO_SH also varies by the type of fixed effects used. In Columns 1 and 2, where industry and year fixed effects are accounted for, the coefficient for SOEs × CEO_SH is −1.115 in Column 1, indicating a negative effect on patent innovation, and 0.621 in Column 2, suggesting a positive effect on invention innovation. In contrast, the results for firm and year fixed effects (Columns 3 and 4) show a less-pronounced effect, with coefficients of −0.293 and 0.397, respectively, both of which are not statistically significant. This suggests that the impact of CEO’s shareholding within SOEs may differ depending on whether industry-specific factors or firm-level controls are emphasized in the analysis. When we turn to the interaction between the policy and Policy × CEO_SH, the coefficients are not significant in any of the models, regardless of the fixed effects used. The coefficients range from 0.121 to 0.16 in Columns 1 and 2, and from −0.107 to 0.113 in Columns 3 and 4, indicating that CEO’s shareholding does not strongly moderate the relationship between the policy and innovation outcomes. This suggests that the CEO’s ownership stake does not substantially influence how the pay restriction policy impacts innovation. Finally, the three-way interaction SOEs × Policy × CEO_SH is significant across all models. In Columns 1 and 2, where industry and year fixed effects are included, the coefficient is 1.374 in Column 1, and 0.452 in Column 2. In Columns 3 and 4, where firm and year fixed effects are included, the coefficients are 0.345 and 0.72, respectively. These results suggest that CEO’s shareholding moderates the negative effects of the CEO pay-restriction policy on innovation in SOEs. Specifically, CEOs with larger ownership stakes are better able to mitigate the adverse effects of the policy on innovation outcomes, especially in terms of patenting and invention. This moderating role of CEO’s shareholding is consistent across both industry-level and firm-level analyses, highlighting its importance in shaping innovation strategies within regulatory constraints. This outcome is consistent with earlier studies of Kamoto (2017) and Lin et al. (2021), suggesting that CEO’s shareholding encourages a connection between CI and personal wealth growth, thereby motivating CEOs to invest in innovative initiatives. These results support our H3, indicating that CEO share ownership helps align CEO interests with those of other stakeholders, thus offsetting the potentially discouraging impact of compensation restrictions on a firm’s innovation.

Robustness test

Three alternative measures of government pay restriction

To strengthen the robustness and validity of our findings, we have incorporated three additional measures of government pay policy (the independent variable) into our analysis, following the methodology outlined by Q. Li et al. (2024) and Jiang et al. (2021) and integrating them into Equation (4).

where GovSOP encompasses three measures of government regulation. The GovSOP1 compares the pay gap between top executives in SOEs and the average pay gap of top executives in non-SOEs within the same industry or sector. The calculation subtracts the SOEs pay gap (average cash compensation of the top three CEOs to other employees’ pays) from the average pay gap of non-SOEs in the corresponding industry and year. A higher value of GovSOP1 indicates greater regulation and restriction on executive compensation in SOEs than in non-SOEs. Furthermore, GovSOP2 compares the average cash compensation of the top three CEOs in SOEs and the average salary of all employees within the same firm. GovSOP2 is calculated by dividing the average cash compensation of the top three CEOs by the average salary of all employees. The resulting value of GovSOP2 reflects the level of government restrictions on executive pay relative to the average employee salary. GovSOP3 measures the pay gap between the top three CEOs and other CEOs within SOEs. GovSOP3 is calculated as the disparity between the average cash compensation of the top three CEOs and that of other CEOs. It is worth noting that the resulting value of GovSOP2 and GovSOP3 are multiplied by −1. Higher levels of GovSOP2 and GovSOP3 indicate more stringent restrictions on CEO compensation within SOEs.

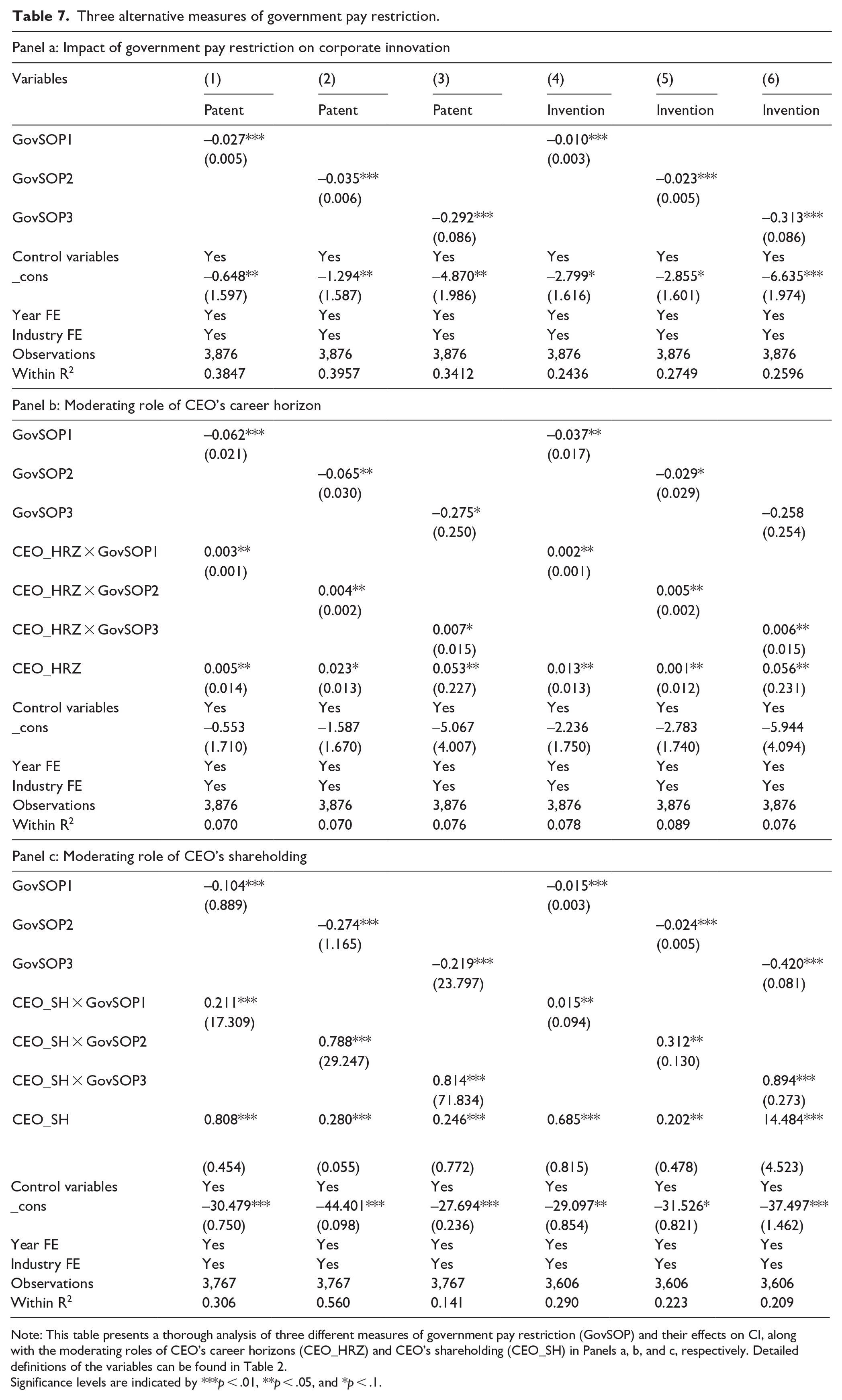

After measuring the three indicators of government regulation of CEO pay, we incorporated these measures into our analysis to test all three hypotheses. The findings are presented in Table 7. Panel a shows a significant negative relationship between the regulatory measures (GovSOP1, GovSOP2, GovSOP3) and CI, with coefficients of −0.027, −0.035, and −0.292 for patients, and −0.010, −0.023, and −0.313 for inventions, respectively. Panel b reveals the moderating effect of CEO_HRZ on this relationship. The interaction terms indicate that CEO’s career horizon reduces the effect of CEO pay restrictions on CI, with significant coefficients of 0.003, 0.004, and 0.007, respectively, suggesting that the effect of pay restrictions on CI is less pronounced as CEO_HRZ increases. Panel c highlights the moderating role of CEO_SH. The interaction terms show that CEO’s shareholding also reduces the impact of CEO pay restrictions on CI, with coefficients of 0.211, 0.788, and 0.814, all significant at the 1% level. These findings suggest that both CEO_HRZ and CEO_SH serve as moderating variables that reduce the impact of CEO pay restrictions on CI. Thus, it confirms our baseline model findings.

Three alternative measures of government pay restriction.

Note: This table presents a thorough analysis of three different measures of government pay restriction (GovSOP) and their effects on CI, along with the moderating roles of CEO’s career horizons (CEO_HRZ) and CEO’s shareholding (CEO_SH) in Panels a, b, and c, respectively. Detailed definitions of the variables can be found in Table 2.

Significance levels are indicated by ***p < .01, **p < .05, and *p < .1.

Government pay restriction and CI: types of SOEs

The reported findings in Table 7 may be subject to heterogeneity and potential bias. This raises concerns about the reliability and generalizability of the results. One significant source of this endogeneity could stem from the diversity within the sample, particularly in terms of the types of SOEs analyzed (Q. Li et al., 2024; Zahid et al., 2023). To address this issue, we further examined both local and central SOEs separately. These two categories of Chinese SOEs are characterized by distinct methods of CEO selection. In the case of local SOEs, CEOs are typically appointed by local governments, which introduces a different dynamic compared to central SOEs, where CEO selection processes may vary.

Research by Chen et al. (2005) discovered that political promotion provides CEOs with power, rewards, and advantages. Notably, central SOE CEOs tend to hold higher political ranks than their local SOE counterparts. CEOs of central SOEs are incentivized to enhance social and environmental performance through non-monetary compensation, as highlighted by Xin et al. (2019). Hence, we examine the influence of GovSOP on CI across various categories of SOEs through a sub-sample analysis. The results presented in both panels of Table 8 substantiate that the effect of GovSOP on CI is more pronounced among local SOEs when contrasted with central SOEs.

Impact of government pay restriction on corporate innovation—types of SOEs.

Note: This table presents the results of heterogeneity analysis conducted by categorizing SOEs into local and central types. Panel a displays the findings for local SOEs, while Panel b presents the results for central SOEs. The definitions of all variables used in the analysis are provided in Table 2. Standard errors are reported in parentheses. The values of control variables are not reported due to brevity.

Statistical significance levels are denoted as follows: ***p < .01, **p < .05, *p < .1.

Alternative measures of CI

Our dependent variable, CI, is undoubtedly a well-researched area within business literature, yet the measurement of this innovation remains a critical point of concern. In our initial model, we have primarily relied on patenting and invention metrics to capture the outcomes of firm innovation. While these metrics offer valuable insights into innovation outcomes, it is conceivable that they may not fully encompass the broader spectrum of innovation inputs. Recognizing this limitation, we have expanded our investigation by incorporating alternative measures that consider innovation inputs alongside outcomes. Specifically, we have employed alternative measures of CI, such as R&D expenditure relative to total assets and R&D expenditure relative to total sales. The results of this analysis, presented in Table 9, consistently highlight the significant negative impact of GovSOP on these alternative CI measures. This additional analysis serves to complement and strengthen the findings observed in Table 4, reaffirming the adverse influence of GovSOP on CI across multiple dimensions.

Alternative measure of corporate innovation.

Note: This table presents a robustness analysis where the main dependent variable is replaced with alternative innovation variables. GovSOP1, GovSOP2, and GovSOP3, which measure government restrictions. Standard errors are reported in parentheses. Definitions of all variables can be found in Table 2, and the estimated coefficients are obtained using Equation (4).

Significance levels are denoted as ***p < .01, **p < .05, and *p < .1.

Test of endogeneity

Parallel trend assumption

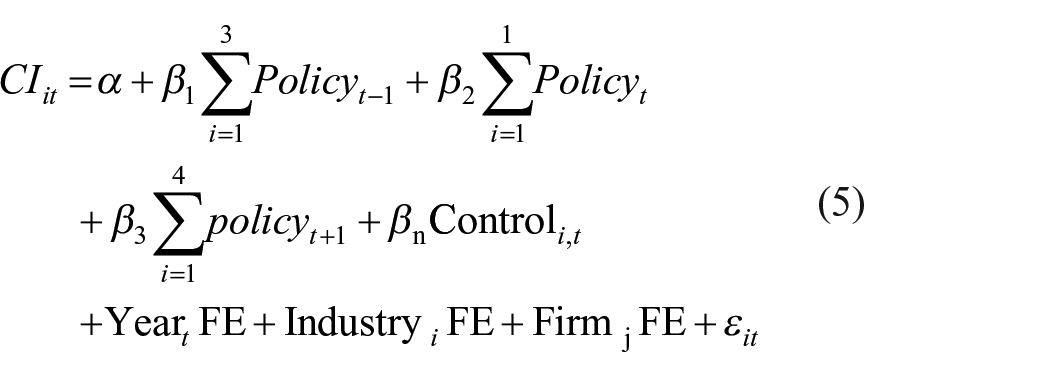

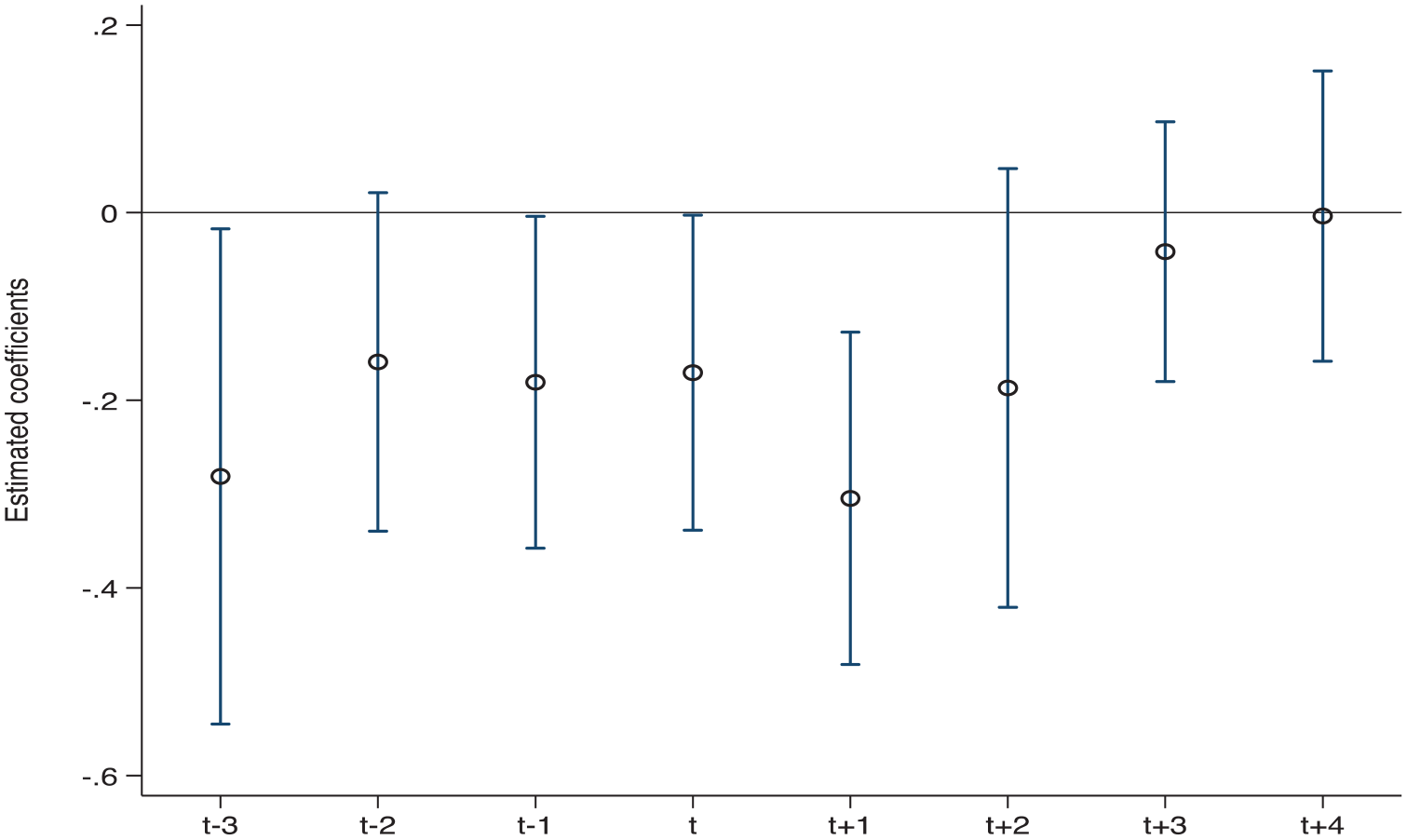

To validate the DiD model (1) estimation, we performed a parallel trend analysis as outlined in Equation (5). We defined specific periods as indicators to examine trends before and after the introduction of the CEO pay policy. For the pre-policy periods, we assigned a value of 1 to the indicators

The results of the parallel trends test, shown in Table 10 and Figures 1 and 2, confirmed the presence of parallel trends. We found that the impact of the CEO pay policy shock was most significant in the first year (Policyt − 3), although statistically insignificant. However, the effect of the policy gradually diminished over time. Notably, we observed a significant and marked reduction in CI following the CEO pay policy, particularly among firms affected by stricter pay regulations implemented after 2014. These findings support the validity of the DiD estimation and are consistent with the results presented in Table 4.

Government pay restriction and corporate innovation: parallel trend test.

Note: This table shows the result of the parallel trend assumption. All other variables are defined in Table 2. Standard errors are in parentheses.

p < .01, **p < .05, *p < .1.

Parallel trend assumption using patents as a proxy.

Parallel trend assumption using invention as a proxy.

Propensity score matching

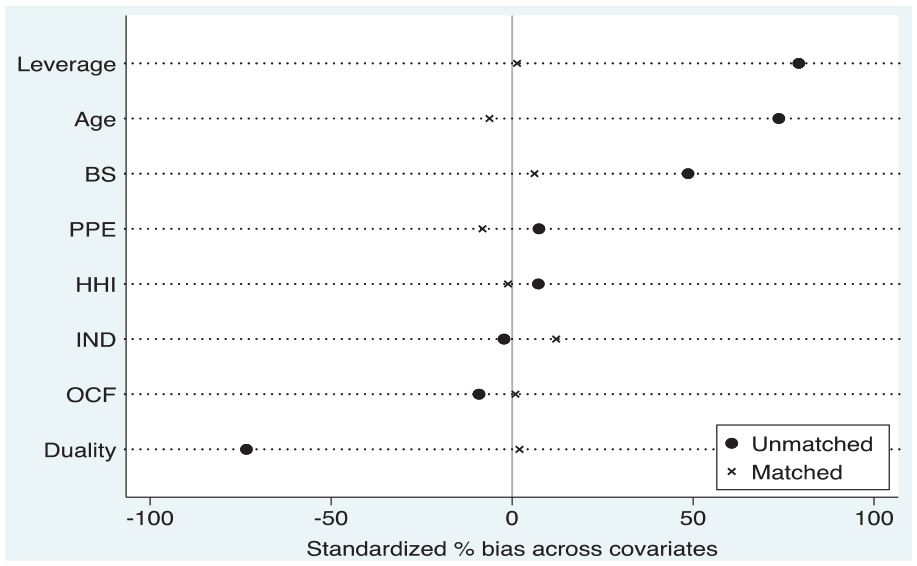

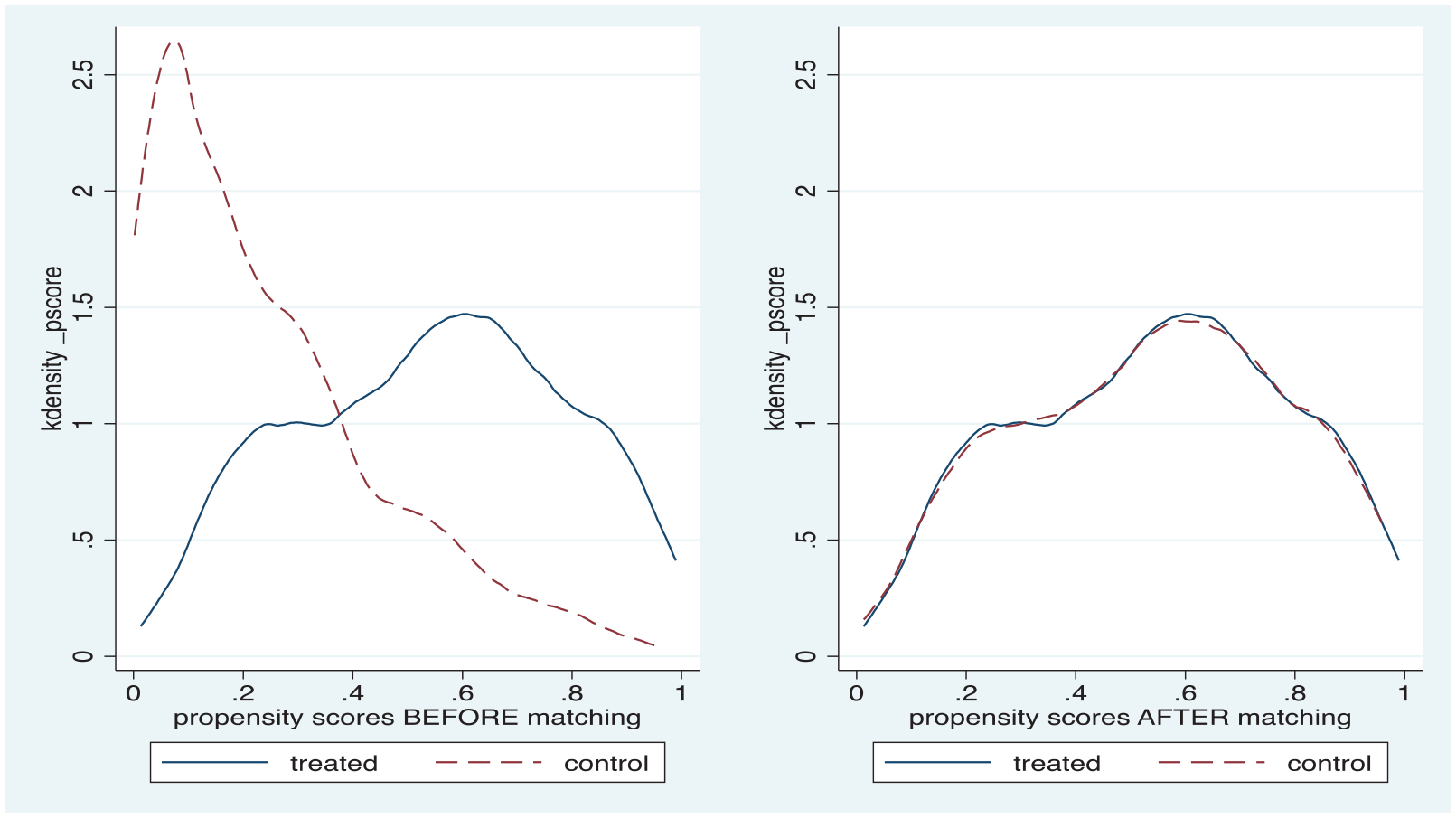

To reduce bias, create comparable groups, and enhance the validity of causal inferences in our current scenario, we conducted a PSM analysis. This method helps to validate and strengthen the initial findings of our study and ensures a more dependable assessment of the causal impact of pay restrictions on CI. To evaluate the balance of covariates before and after implementing the treatment, we used Figure 3, which illustrates the distribution of the covariate of interest. This visual representation allows us to observe any differences in covariate distribution before and after treatment. Moreover, in Figure 4, we utilized kernel matching, a technique that estimates the probability density of covariates in each group using a kernel function. This ensures that the groups are very similar in characteristics, thus reducing bias in our results.

PSM balance covariates.

PSM matching.

Once we established the validity of our matched sample, we conducted a regression analysis on the matched data, using CI proxies as our variables of interest. The results of this analysis are presented in Table 11. In Panel a of Table 11, the PSM balance test results are displayed. These tests assess whether the treatment and control groups in a study are well-matched after applying the PSM technique. This assessment aims to determine if the groups are comparable in terms of their baseline characteristics, ensuring that any observed differences in outcomes can be attributed to the treatment rather than initial group imbalances. Panel b of the same table presents the results of the PSM regression, likely supporting the primary findings of the study presented in Table 11.

Propensity score matching test.

Note: This table presents the results of a PSM test. Panel a displays the balance test between matched and unmatched firms before and after matching, while Panel b presents the regression results with industry, firm, and year fixed effects. Standard errors are reported in parentheses. Definitions of all variables can be found in Table 2. OCF: operating cash flow; HHI: Herfindahl-Hirschman Index.

Significance levels are denoted as ***p < .01, **p < .05, *p < .1.

Placebo test

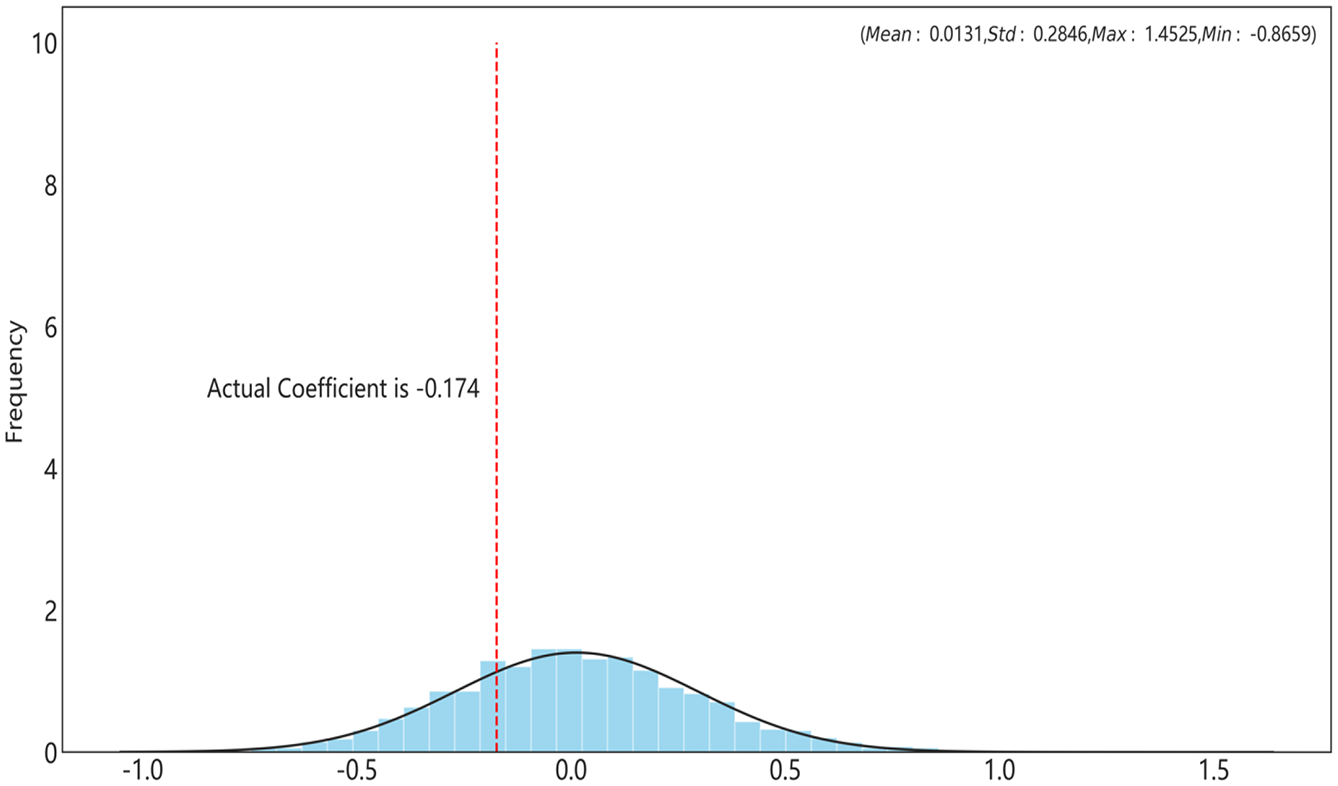

To address concerns about omitted variables, we implemented a robust testing approach. Specifically, we conducted placebo tests by randomly assigning pseudo-treated firms and running 2,000 simulations. For each simulation, we estimated the baseline model, as shown in Table 5, using the simulated data. These tests allowed us to generate a distribution of the coefficients for the interaction term SOEs × Policy, which is depicted in Figure 5.

Placebo test.

This methodology is commonly employed in the literature to address omitted variable concerns, as demonstrated in studies by Wang et al. (2023) and Maqsood et al. (2023). The placebo test results showed that the actual coefficient for SOEs × Policy, presented in Column (4) of Table 4, differs significantly from the simulated coefficients. By comparing the actual coefficient (−0.174) with the simulated mean (0.0131) and dividing it by the simulated standard deviation (0.2846), we obtained a value of approximately 0.5653. This value is notably to the right of the placebo distribution, supporting the conclusion that government CEO pay regulation has a significant effect on reducing CI within SOEs.

Conclusion

Leveraging the framework of SOP regulations within a governmental context, this study examines the impact of government restrictions for CEO pay on CI. Utilizing data from Chinese SOEs spanning from 2010 to 2020 and employing the DiD model, the findings indicate that firms subject to pay-restriction policies experience a decline in CI. This decline is likely attributed to reduced CEO effort or risk aversion, which ultimately leads to a decrease in CI. Moreover, the study proposes that CEO’s career horizons and shareholding moderate the negative impact of these policies on CI. This implies that CEOs increase their efforts to improve a firm’s performance to achieve personal gains, given their ownership stake in the firms.

The study’s findings underscore the unintended consequences of government regulations on CEO pay structures, offering significant implications for both practitioners and regulatory bodies. While government regulations aimed at controlling CEO compensation are often intended to curb income inequality by setting limits or guidelines on executive pay, this study reveals that these regulations can lead to unintended outcomes that affect businesses in various ways. One key consequence highlighted by this study is the need for practitioners and regulatory bodies to reconsider the design of CEO compensation packages. This recommendation arises from the realization that certain regulations (i.e., pay regulation), while addressing social inequality, can inadvertently hinder a firm’s competitiveness or financial health. For practitioners involved in corporate governance or executive compensation, the study also suggests a critical review of how CEO pay structures are designed. This includes considering the balance between competitive compensation and compliance with regulatory requirements to ensure that firms can attract and retain top talent while adhering to legal frameworks.

While this study focuses on Chinese SOEs, its findings have global relevance. Countries with similar CEO pay regulations, such as the United States, Russia, Australia, and South Korea, may experience similar unintended effects, such as reduced CEO effort or innovation. As the study’s objectives are met, it is important to acknowledge certain limitations that could inform future research. This study specifically examines the financial consequences of government pay regulation on CEO compensation and its impact on CI. Moving forward, future research could make a valuable contribution by exploring R&D manipulation as a means of understanding CEO ethical behavior following the introduction of pay policies. Furthermore, the findings of this study are confined to the year 2020 and do not account for the disruptive impact of the COVID-19 pandemic. Future studies could expand the dataset to include post-COVID data, providing insights into how government policy impacts a firm’s operations in the presence of pay regulation during and after a major shock like COVID-19.

Footnotes

Acknowledgements

This study is part of the first author’s Ph.D. research at the School of Economics and Finance, Xi’an Jiaotong University.

Author’s contribution

Umer Sahil Maqsood: Writing initial draft and revision, Data collection, analysis, and research validation. Qian Li: Supervision. R. M. Ammar Zahid: Reviewing, editing, and assistance in addressing the suggestions of the two anonymous reviewers and associate editor. Shihao Wang: Reviewing and providing assistance in conducting the analysis part.

Data availability statement

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.