Abstract

This study examines how the integration of corporate social responsibility (CSR) criteria in executive compensation can improve green innovation performance in European countries. Using agency theory and stakeholder theory, and a database of 5,603 firm-year observations from European companies in the period 2012–2021, we find that CSR aligns the interests of senior executives with the company’s green innovation goals through green compensation contracts. We also explore the indirect effect in this relationship and reveal that the implementation of green practices mediates the impact of CSR contracting on green innovation performance. These findings indicate that CSR contracting as an effective governance mechanism could be strengthened by green practices, such as reducing resource use, water efficiency, energy reuse, emission reduction and pollution prevention. This study offers valuable insights for senior executives and policymakers who wish to manage CSR initiatives and green practices to improve their green innovation performance.

Keywords

Introduction

Concern about the impact of human activities on the environment has been growing among enterprises and society over the last two decades. To demonstrate their commitment to environmental and social responsibility, many companies are currently incorporating corporate social responsibility (CSR) criteria in their strategies. Moreover, many companies are now integrating CSR criteria intro executive compensation. This practice is gaining importance because it can motivate senior executives to align environmental concerns with business goals (Flammer et al., 2019; Singh et al., 2022; Yuan & Cao, 2022). This helps companies to build competitive advantages and enhance their corporate images (Flammer et al., 2019; Focke, 2022; Peng, 2020; Radu & Smaili, 2022; Tsang et al., 2021). For instance, BP, the British multinational oil and gas company, has incorporated staff diversity and health and safety into their director’s remuneration. Similarly, food group Nestlé has linked 15% of the annual bonuses of the CEO, CFO, and other members of the executive board to environmental, social, and governance (ESG) objectives. Meanwhile, Schneider Electric has included climate change and energy usage into its bonus plan. In 2020, one-fifth of the total incentive salary of Jean-Pascal Tricoire, Schneider Electric’s Chairman and CEO, was due to his efforts to hit ESG targets. These are only some examples of an increasing number of companies who have introduced similar compensation structures.

The literature has pointed out that CSR contracting mainly promotes the long-term development of a firm through two mechanisms. First, incorporating CSR contracting can reduce agency problems between executives and shareholders. CSR contracting promotes managers to make long-term investments that benefit the shareholders’ interests (Cavaco et al., 2020; Focke, 2022; Tsang et al., 2021). Second, CSR executive compensation is a governance tool that encourages managers to manage with the needs and expectations of different stakeholders in mind (e.g., customers, employees, governments, and communities), which ensures that companies will improve their social and environmental performance to create long-term value (Flammer et al., 2019; Flammer & Kacperczyk, 2016; Singh et al., 2022).

A few studies have explored the impact of integrating CSR goals into executive compensation (hereinafter referred to as CSR contracting) on corporate performance. Flammer and Luo (2017) found that CSR incentives at the employee level promote a more engaged and productive workforce, while Flammer et al. (2019) found that CSR criteria in executive compensation produces positive effects on long-term orientation, social and environmental initiatives, and green innovations.

This article aims to analyze the impact of CSR contracting on green innovation performance. To do so, it builds upon the research of Flammer et al. (2019) and Flammer and Luo (2017) by analyzing the mediating effect of green practices on the relationship between CSR contracting and green innovation performance. By adopting green initiatives that aim to reduce resources use and emissions, companies can take an intermediate step toward enhancing their green innovation performance and advance the broader goal of promoting corporate sustainability.

Green innovation performance refers to the ability of an organization or industry to develop and implement new technologies, processes and products that are environmentally sustainable and which contribute to the reduction of negative environmental impacts (Nadeem et al., 2020; Shahzad et al., 2021). However, investing in green innovation activities is associated with high levels of uncertainty because it often takes a long time until its outcomes realize their full value (Berrone & Gomez-Mejia, 2009). Research has shown that incorporating CSR criteria into executive compensation can help motivate executives to focus more on long-term values and sustainability goals, which can positively influence green innovation performance (Flammer et al., 2017; Focke, 2022; Tsang et al., 2021). This approach can align the interests of executives with those of shareholders and other stakeholders, which leads to a stronger commitment to sustainability and environmental performance. Moreover, companies that prioritize green innovation and environmental sustainability can benefit from increased operational efficiency, cost savings and a stronger reputation for responsible business practices (Chiou et al., 2011; Schiederig et al., 2012). Nevertheless, despite the potential benefits of green innovation performance, the specific practices that executive can use to achieve better green innovation performance are not yet widely demonstrated in the literature (Cherrafi et al., 2018; Shahzad et al., 2021; Su et al., 2020).

From the theoretical perspective, using both agency theory and stakeholder theory, we propose that CSR contracting has both direct and indirect effects on green innovation performance, with green practices playing the role of mediator in the relationship. Empirically, we construct a longitudinal database from Thomson Reuters’ Refinitiv Eikon (formerly Asset 4), which consists of 5,603 firm-year observations from 28 European countries in the period of 2012–2021. Although recent studies have employed output-oriented measures, such as patents, to assess green innovation performance (Flammer et al., 2019 and Tsang et al., 2021), in this study, green innovation is a complex and multifaceted concept that involves a range of economic, environmental, and social considerations. To address this challenge, we employ a holistic green innovation metric that covers both input-oriented and output-oriented indicators (e.g., green innovation targets, green innovation initiatives, green innovation products, green innovation process, and green innovation assets), which provides a comprehensive view of the economic, environmental, and social impact of a company’s green innovation activities.

Using a Tobit model, our empirical findings confirm that CSR contracting has a positive impact on green innovation performance. Our multiple mediator analysis also demonstrates that green practices, as measured by resource use practices and emissions practices, mediate the impact of CSR contracting on green innovation performance. These findings support our theoretical arguments that CSR contracting enhances green innovation performance by incentivizing managers to adopt long-term horizons and engage in green practices.

This study contributes to the literature in several ways. First, we used a large sample of small-, medium-, and large-sized companies operating in different European Union (EU) countries. Although the EU remains the largest economic bloc and the most polluting economy in the world, the existing studies have mostly focused on the United States (Derchi et al., 2021; Flammer et al., 2019), India (Suganthi, 2019), and China (Waheed & Zhang, 2022; Yuan & Cao, 2022). Furthermore, European countries play a critical role in supporting the implementation of the United Nations (UN) 2030 Agenda in its member states through policy coordination, funding, and technical assistance. Previous studies have focused solely on large companies, such as those in the SandP 500 (Flammer et al., 2019; Qin & Yang, 2022). Moreover, our sample covers the period from 2012 to 2021, which provides a more current and robust analysis of the CSR contracting–green innovation performance relationship.

Second, this study contributes by introducing CSR contracting as a critical antecedent of green innovation performance. Despite the growing importance of green innovation, there remains a lack of research on the antecedents of green innovation at the executive level (Karimi Takalo et al., 2021). This study provides valuable insights into the factors that drive green innovation performance at the executive level. It also introduces a new construct for CSR contracting that defines the extent of CSR criteria in relation to executive compensation as a continuum. This approach acknowledges that different levels of CSR-contingent executive compensation may lead to varying degrees of green innovation outcomes, which is in contrast to previous studies that treat CSR contracting as a binary construct (e.g., Abdelmotaal & Abdel-Kader, 2016; Flammer et al., 2019; Focke, 2022).

Third, this study sheds light on the mechanisms through which CSR contracting can lead to better green innovation performance. While there is a clear trend toward including CSR components in executive compensation (Focke, 2022; Haque & Ntim, 2020), little is known about the practices through which these executives can achieve green innovation goals. By examining the mediating role of green practices, specifically resource use practices and emissions practices, our findings emphasize the need for organizations to adopt sustainable and eco-friendly business practices. This adds to the highly relevant literature on the relationship between CSR contracting and green innovation performance.

Finally, this study employs Tobit post-estimation techniques to obtain the marginal effect of independent variables on the observed dependent variable. This provides more accurate estimates regarding the effect of CSR contracting on green innovation performance. Furthermore, most previous studies that have investigated the mediation effect have relied on cross-sectional designs (Aguinis et al., 2017; Radu & Smaili, 2022). However, some scholars have suggested that mediator models with panel data can produce more unbiased estimates than cross-sectional data because they involve the passage of time (Maxwell & Cole, 2007).

The remainder of this article proceeds as follows. Section “Theoretical framework and hypotheses development” outlines the theory and hypotheses development. Section “Data and methodology” presents the data and methodology. Section “Supplementary analyses and robustness test” describes the supplementary analyses and robustness tests. Finally, the discussion and conclusion are provided in section “Discussion and conclusion.”

Theoretical framework and hypotheses development

CSR contracting and green innovation performance

Unlike traditional executive compensation, which primarily focuses on financial goals and perquisites (Murphy, 1999), CSR contracting provides a holistic understanding of executive compensation by linking executive compensation to environmental and social performance (Flammer et al., 2017; Hong et al., 2016; Tsang et al., 2021). It contends that executive compensation should contribute not only to the achievement of economic goals but also to the long-term interests and sustainability of the company (Cavaco et al., 2020; Flammer et al., 2019; Focke, 2022). In addition, due to the separation of ownership and management, the interests of shareholders may differ from those of a company’s senior executives, who may be inclined to prioritize short-term profits over long-term shareholder value. Furthermore, the integration of CSR criteria into executive compensation can align the interests of companies and their managers (Adu et al., 2022; Flammer, 2013; Focke, 2022). CSR contracting can also raise environmental and social awareness and can promote senior executive responsiveness to a wide range of stakeholders, thereby establishing legitimacy and corporate reputation (Flammer et al., 2019; Singh et al., 2022). In this sense, executive performance should be assessed based on both financial and non-financial performance criteria, such as CSR metrics.

Green innovation refers to a set of measures that aim to mitigate the negative impact of production and operations on the environment. These measures can take the form of improvements in technologies, products, services, organizational structures or management models and are crucial for gaining a competitive advantage and achieving long-term growth (Asadi et al., 2020; Karimi Takalo et al., 2021; Nadeem et al., 2020). As a relatively new area of research within the field of corporate innovation, green innovation performance has attracted increasing research interest (Kraus et al., 2020; Phung et al., 2023; Rehman et al., 2021). For instance, scholars have analyzed how environmental strategies (Song & Yu, 2018), dynamic capabilities (Yousaf, 2021; Yuan & Cao, 2022) or stakeholder pressure (Singh et al., 2022) affect green innovation. However, a few researchers have explored how a green incentive can affect green innovation performance. Therefore, the main objective of this research is to examine and analyze the relationship between CSR contracting and green innovation performance.

Previous research on the relationship between executive compensation and corporate performance has been firmly rooted in agency theory (Jensen & Meckling, 1976) and stakeholder theory (Freeman, 1984). According to agency theory, CSR contracting is expected to mitigate agency conflicts between shareholders and executives related to social and environmental issues. In other words, green innovation is characterized by high capital investment, long profitability cycles, high risk, and uncertainty, all of which may discourage managers from undertaking this activity due to their risk-averse nature and preference for short-term interests over long-term benefits (Flammer et al., 2017). However, shareholders are generally considered to be risk neutral because they can avoid risk by diversifying investments and they fear that executives may prioritize risks reduction over the company’s long-term benefit (Mehran, 1995). Therefore, a well-structured executive compensation contract that integrates CSR criteria can shift the managers’ attention toward a long-run orientation and improve the firm’s profitability by adopting innovative production methods and efficient use of resources (Derchi et al., 2021; Nadeem et al., 2020; Phung et al., 2023).

Stakeholder theory suggest that companies have a responsibility to meet the needs of their stakeholders and CSR contracting can motivate senior executives to be responsive to a broad range of stakeholders, which is crucial for long-term success (Waheed et al., 2020; Waheed & Zhang, 2022). Increasingly, customers are becoming more environmentally and socially conscious. They also tend to prefer eco-friendly products, even if they are more expensive (Costa & Menichini, 2013; Kumar et al., 2017). By investing in green innovation, firms that integrate CSR into executive compensation can attract and retain customers, enhance their corporate image and brand loyalty, and ultimately improve profitability (Derchi et al., 2021; Flammer & Kacperczyk, 2016).

Government regulations on environmental issues are growing, and companies must comply with existing regulations while also anticipating new trends and changes in regulations that may affect their corporate strategies and actions (Shao et al., 2020; Wu et al., 2020). Environmental and local community pressures are also directing companies to focus on sustainability and long-term development, which may be less salient but financially significant to firm outcomes in the long term (Flammer et al., 2019).

CSR can also be used as a governance tool for employees, which promotes their involvement in eco-friendly activities and reduces adverse behavior in the workplace (Flammer & Luo, 2017; Guerci et al., 2015). When a company is perceived to be committed to CSR engagement, it can attract and retain good employees and promote their job satisfaction, thereby increasing success in green innovation (Suganthi, 2019; Tan & Zhu, 2022; Tsang et al., 2021). Therefore, we argue that integrating CSR criteria into executive compensation incentivizes senior executives to adopt a long-term orientation and generates better green innovation performance for the company. Accordingly, we propose that:

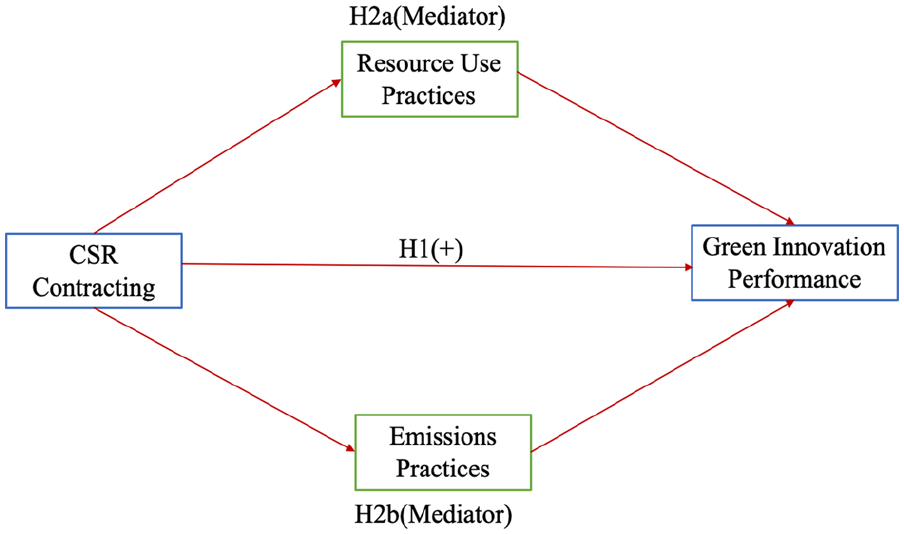

Hypothesis 1. CSR contracting has a positive effect on green innovation performance.

The indirect effect between CSR contracting and green innovation performance

The remunerative consumption of natural resources and release of harmful emissions resulting from economic development place an enormous and growing burden on the climate and environment (Suganthi, 2019; United Nations, 2018; Yousaf, 2021). To address this challenge, green innovation has gained significant attention in recent years. However, organizations still face a significant challenge in achieving green innovation goals due to a lack of implementation of green practices (Cherrafi et al., 2018; Shahzad et al., 2021).

Green practice refers to the actions and strategies that organizations undertake to reduce their environmental impact (Ryoo & Koo, 2013). In addition, the importance of senior executives in setting and implementing green practices has been widely recognized in the literature. Studies by Adu et al. (2022), Phung et al. (2023), and Tsang et al. (2021) have shown that the concerns and engagements of senior executives are positively related to the speed and scope of their firm’s environmental responses. As leaders of their organizations, senior executives hold the power to allocate resources, set priorities and motivate employees, as well as influence stakeholders and partners to adopt sustainable practices (Sharma & Henriques, 2005). Through the adoption of CSR contracting, senior executives can foster a culture of environmental responsibility within their organizations. This can lead to increased employee engagement and motivation to embrace green practices, which ultimately drives progress toward corporate sustainability (Flammer & Luo, 2017). In addition, senior executives can leverage their influence to encourage partners and the other stakeholders to adopt sustainable practices, which leads to a ripple effect throughout their industries (Ho et al., 2022; Sharma, 2000).

Previous studies suggest that organizations that prioritize CSR and adopt green practices tend to be more effective in creating and sustaining innovative behaviors, for the following reasons. First, green practices such as energy efficiency, resource reduction, and sustainable sourcing can help companies save costs and improve their bottom line, which can free up resources for investment in green innovation (Yousaf, 2021; Yuan & Cao, 2022). Second, companies that prioritize green practices tend to have a culture that values sustainability and environmental responsibility, which can foster creativity and innovation in this area (Ghisetti & Rennings, 2014). Third, consumers and other stakeholders are increasingly demanding environmentally sustainable products and services, which can create a market incentive for companies to innovate in this area (Waheed et al., 2020). Finally, government policies and regulations that aim to reduce environmental impact can also encourage green innovation by providing incentives and support for companies that invest in sustainable practices (Wu et al., 2020).

In summary, we contend that CSR contracting is an important motivator for senior executives to engage in green practices and achieve greater green innovation performance. Therefore, the following hypothesis is proposed:

Hypothesis 2. CSR contracting improves green innovation performance through the adoption of green practices (resource use practices and emissions practices).

Based on the hypotheses, the theoretical model for this study is shown in Figure 1.

Conceptual research framework.

Data and methodology

Sample and data collection

We constructed our sample using the information from Thomson Reuters’s Refinitiv Eikon (formerly Asset 4), which offers one of the most comprehensive ESG databases in the industry and covers over 80% of the global market cap across more than 450 different ESG metrics. Refinitiv has ESG data coverage for more than 10,000 global companies across 76 countries, and it spans major global and regional indices. ESG Scores from Refinitiv are designed to transparently and objectively measure the relative ESG performance, commitment, and effectiveness of a company across 10 main themes (e.g., resource use, emissions, environmental product innovation, human rights, and shareholders) based on publicly reported data. This database identifies companies that demonstrate an active and positive contribution to sustainable development, and it has been widely used in previous studies (Bassetti et al., 2021; Orazalin & Baydauletov, 2020; Papagiannakis et al., 2019).

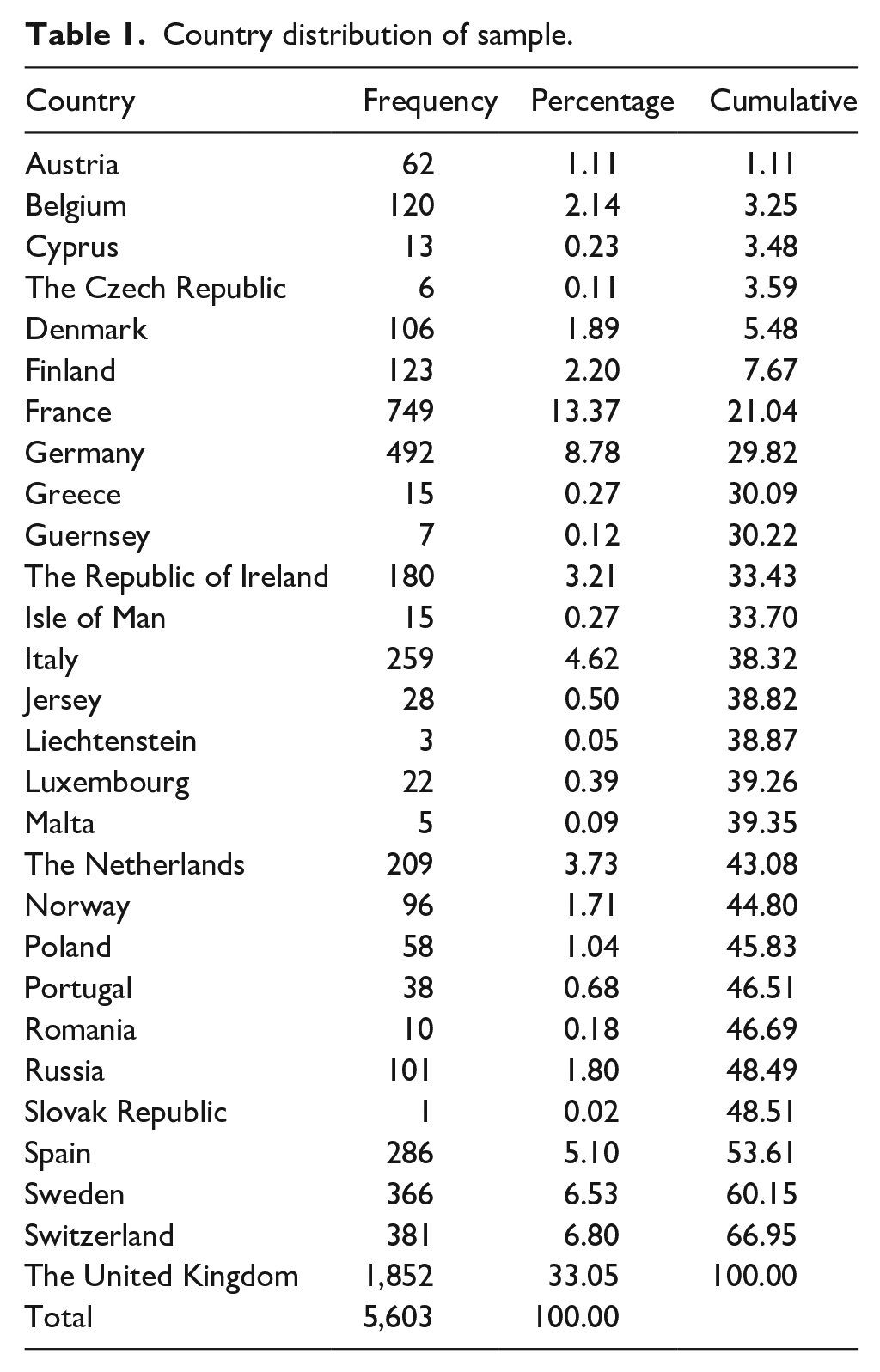

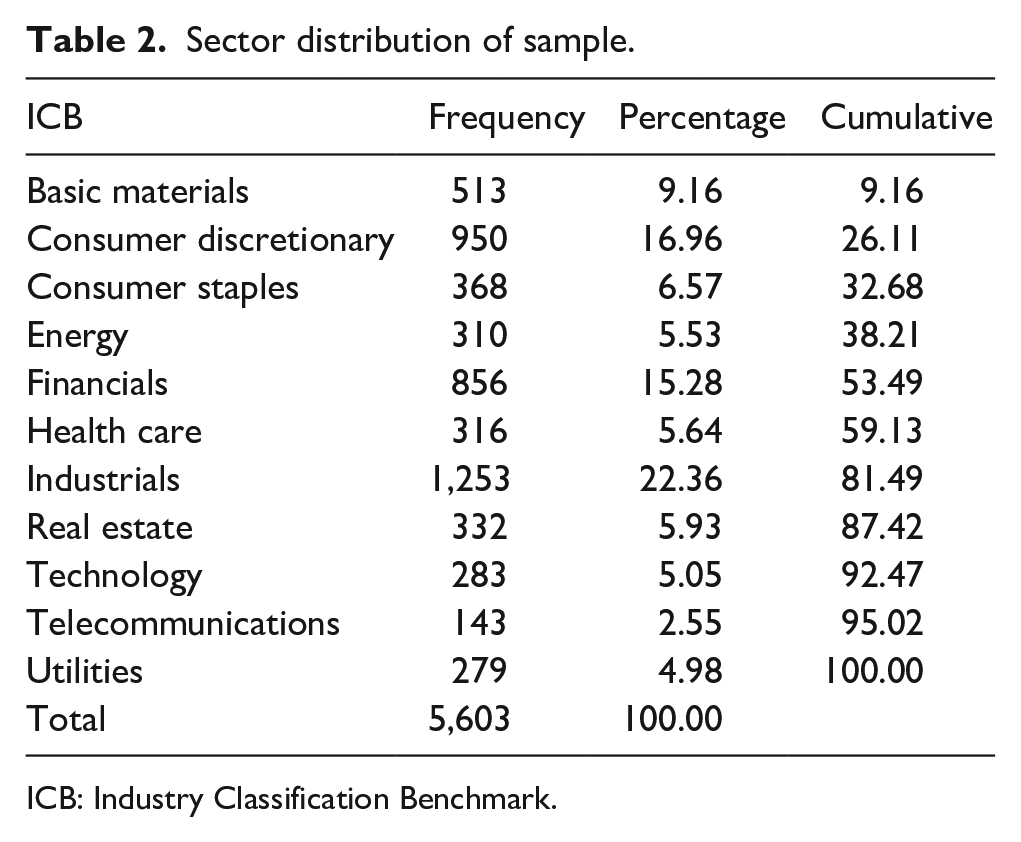

Our initial sample consisted of 963 firms from 28 European countries. After considering missing data required for model design, we constructed a panel of 909 firms from Europe. The final sample for hypotheses testing consisted of 5,603 firm-year observations of firms operating in 11 different industries in 28 European countries from 2012 to 2021. Table 1 shows the distribution of the companies in the sample among countries. The United Kingdom (33%) had the most observations, followed by France (13%), Germany (9%), and Switzerland (7%). In addition, the sample consisted of companies from 11 different sectors that primarily belong to the following industries: (1) industrials, (2) consumer discretionary, (3) financials, (4) basic materials, and (5) consumer staples. Table 2 shows the distribution of the sample by sector type.

Country distribution of sample.

Sector distribution of sample.

ICB: Industry Classification Benchmark.

Variable measurement

Dependent variable

Green innovation performance (GIPer)

Data on green innovation performance were extracted from the Refinitiv Eikon database, which provides a reliable and comprehensive measure of a company’s environmental innovation performance. The variable “environmental innovation score,” which is widely adopted in previous studies, is a crucial indicator of a company’s green innovation performance (Nadeem et al., 2020; Phung et al., 2023). It ranges from 0 to 100 and reflects a company’s ability to develop and implement new technologies, processes, and products that are environmentally sustainable and contribute to the reduction of negative environmental impacts. This score is essential in evaluating a company’s commitment to sustainability, which is increasingly becoming a critical consideration for investors, customers, and other stakeholders.

Independent variables

CSR contracting

Consistent with previous research (Abdelmotaal & Abdel-Kader, 2016; Baraibar-Diez et al., 2019; Derchi et al., 2021; Focke, 2022), we employed the “Sustainability Compensation Incentive” from the Refinitiv Eikon database that reflects the integration of CSR criteria into senior executive compensation packages. A continuous variable is used to capture the presence of executive compensation associated with CSR criteria, which measures the extent to which senior executive compensation is linked to CSR and sustainability goals. It ranges from 0 to 100, with higher scores representing higher levels of implementation of CSR contracting. To assess a firm’s green practices, we utilized two subdimensional scales: resource use practices and emissions practices.

Resource use practices (RUPra)

It measures a firm’s implementation of green practices to reduce their consumption of materials, energy, and water, while seeking more sustainable solutions through better supply chain management. This index is determined by six key practices: resource reduction, water efficiency, energy efficiency, environmental supply chain, environmental material sourcing, and environmental management criteria. Each firm is assigned a score of 1 if they have engaged in each resource use practice during the given year and is 0 otherwise. The range of scores for resource use practices is 0–6, with higher scores indicating a higher level of adoption of green practices related to resource use.

Emissions practices (EPra)

It measures a firm’s implementation of green practices to reduce environmental emissions during production and operations. This index is calculated by adding scores for six items: emission reduction, climate change opportunities, waste reduction, environmental restoration, ISO 14000, and environmental investment initiative. A firm’s absolute score for emissions practices can range from 0 (poor adoption of emissions practices) to 6 (good adoption of emissions practices).

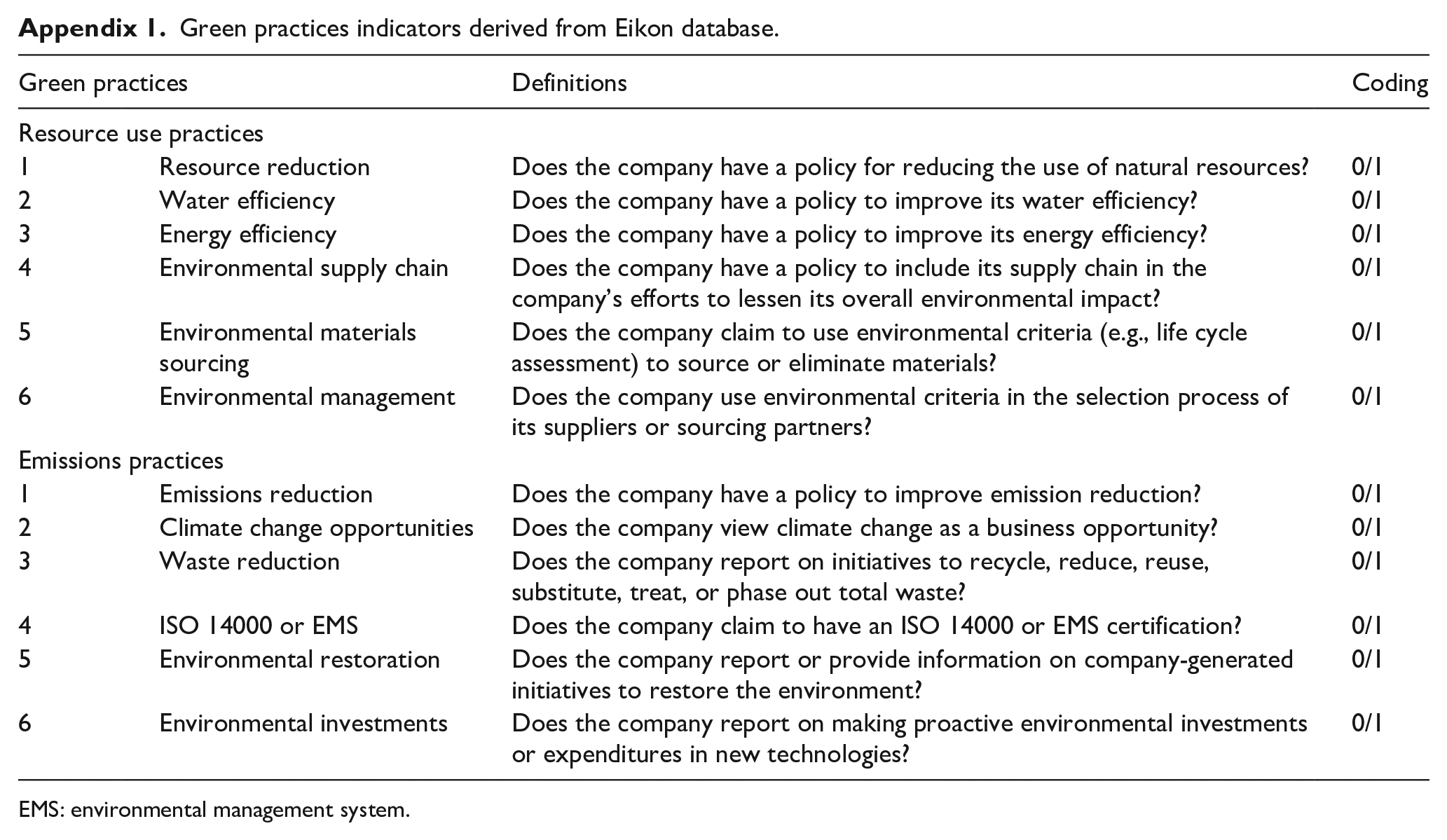

We calculated the Cronbach’s alpha to ensure the validity of the resource use practices and emissions practices construct. The alpha values for each subdimension were found to be 0.789 and 0.665, respectively. These values indicate that the items within each subdimension are consistent with each other, which suggests that the measure is reliable. Appendix 1 provides further details about each item for resource use practices and emissions practices.

Control variables

In accordance with previous studies, we introduced several firm characteristics that are known to be associated with CSR contracting and the dependent variable of interest (Flammer et al., 2019; Focke, 2022; Shahzad et al., 2021).

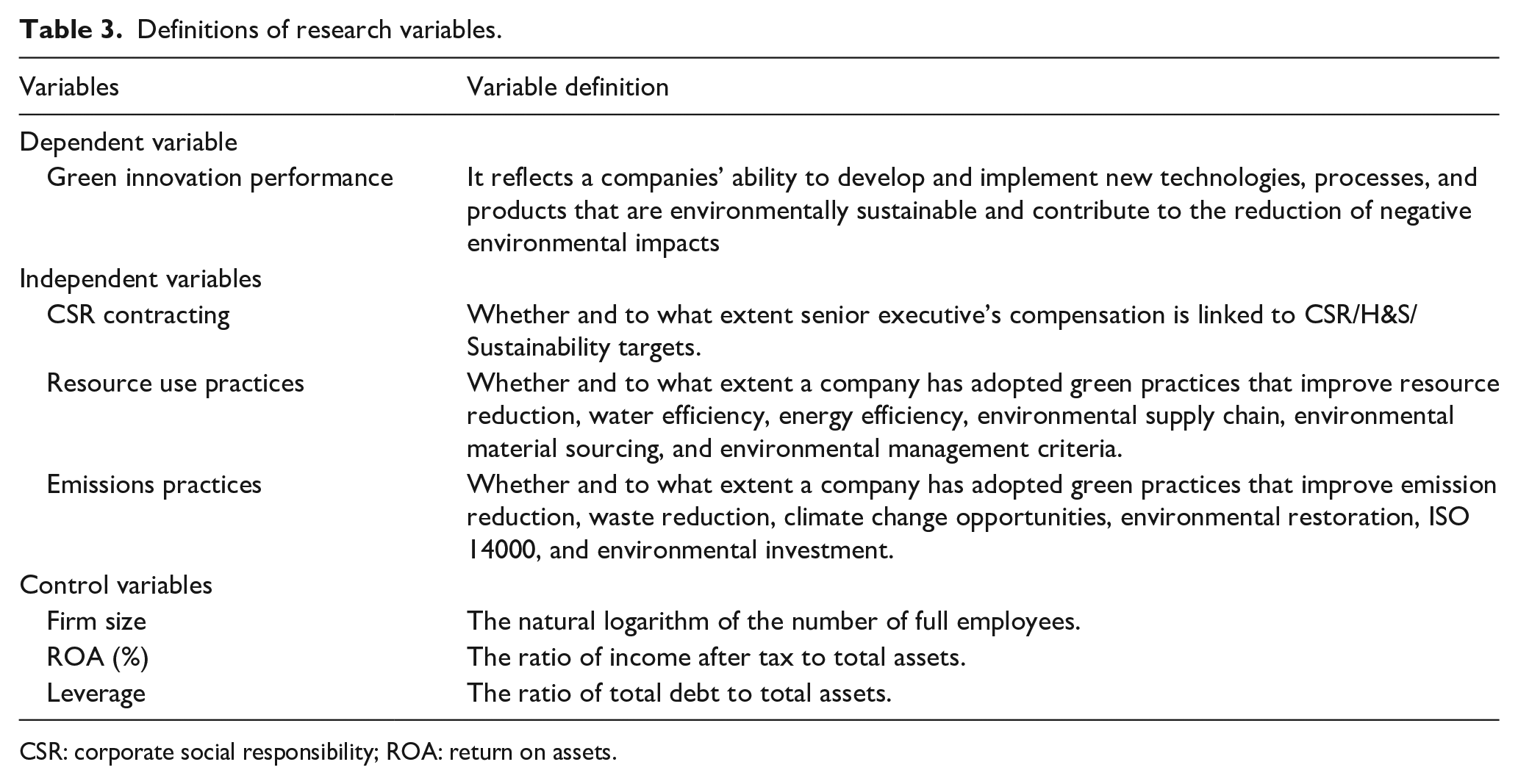

First, we included firm size as our control variable, which was measured by the natural logarithm of the total number of full-time employees. Previous studies have proved that larger firms face more pressure from stakeholders and have more resource availability to develop sustainability (Orazalin & Baydauletov, 2020; Papagiannakis et al., 2019). Second, we included financial profitability as a control variable because a company’s financial capacity is directly proportional to its environmental investments, which are fundamental to improving green innovation performance (Flammer et al., 2019; Focke, 2022; Peng, 2020; Radu & Smaili, 2022; Tsang et al., 2021). We used return on assets (ROA) as a financial profitability indicator and calculated it by dividing income after taxes by average total assets, expressed as a percentage (Maas, 2018; Phung et al., 2023). Third, we controlled the financial leverage (Leverage) to capture the ability of a company to make proactive environmental investments and increase environmental engagement. Following previous studies (Aslam et al., 2021; Flammer et al., 2019), we measured leverage as the ratio of total debt to total assets (Tsang et al., 2021). To mitigate the impact of outliers, all of the ratios are winsorized at 5th and 95th percentiles of their empirical distribution. Finally, we included year fixed effects in the model because there are differences in the implementation of sustainable development strategies and practices across time (Flammer et al., 2019; Tsang et al., 2021). Table 3 summarizes the definitions of key research variables.

Definitions of research variables.

CSR: corporate social responsibility; ROA: return on assets.

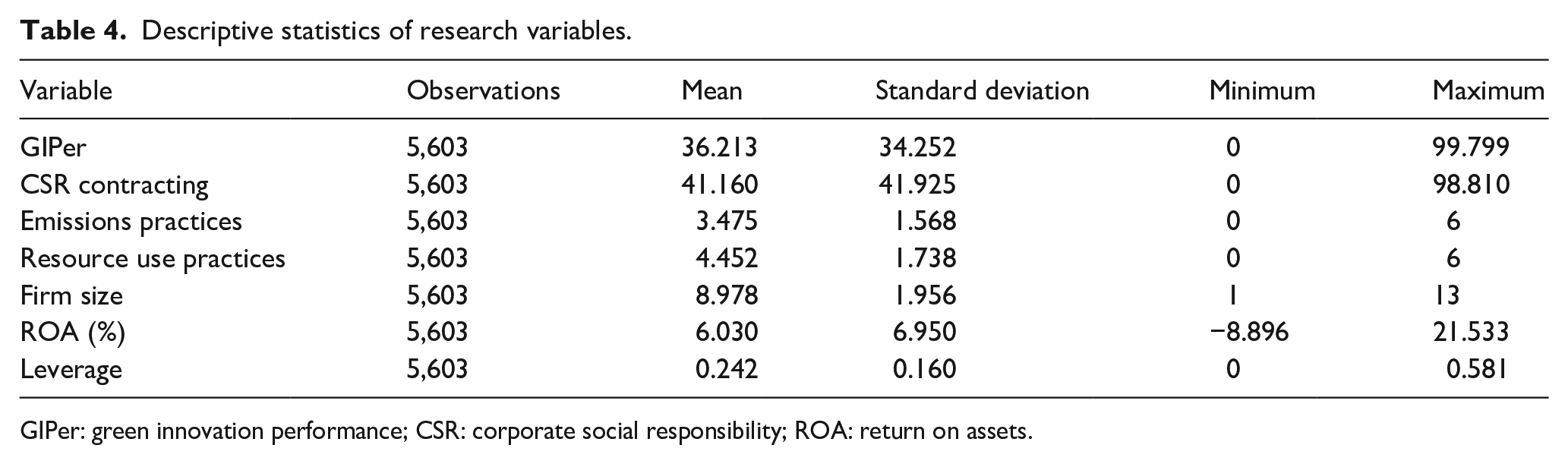

Descriptive statistics and correlations

Table 4 presents the descriptive statistics for the studied variables. The sample companies achieved an average score of 36 out of 100 for green innovation performance, which indicates that there is significant potential for improvement. Although the companies scored slightly better in developing CSR-related executive compensation, with an average score of 41, there is still significant room for improvement here. On average, the companies implemented four resource use practices and three green emissions practices, which underscore the need to adopt more sustainable practices to enhance their environmental performance.

Descriptive statistics of research variables.

GIPer: green innovation performance; CSR: corporate social responsibility; ROA: return on assets.

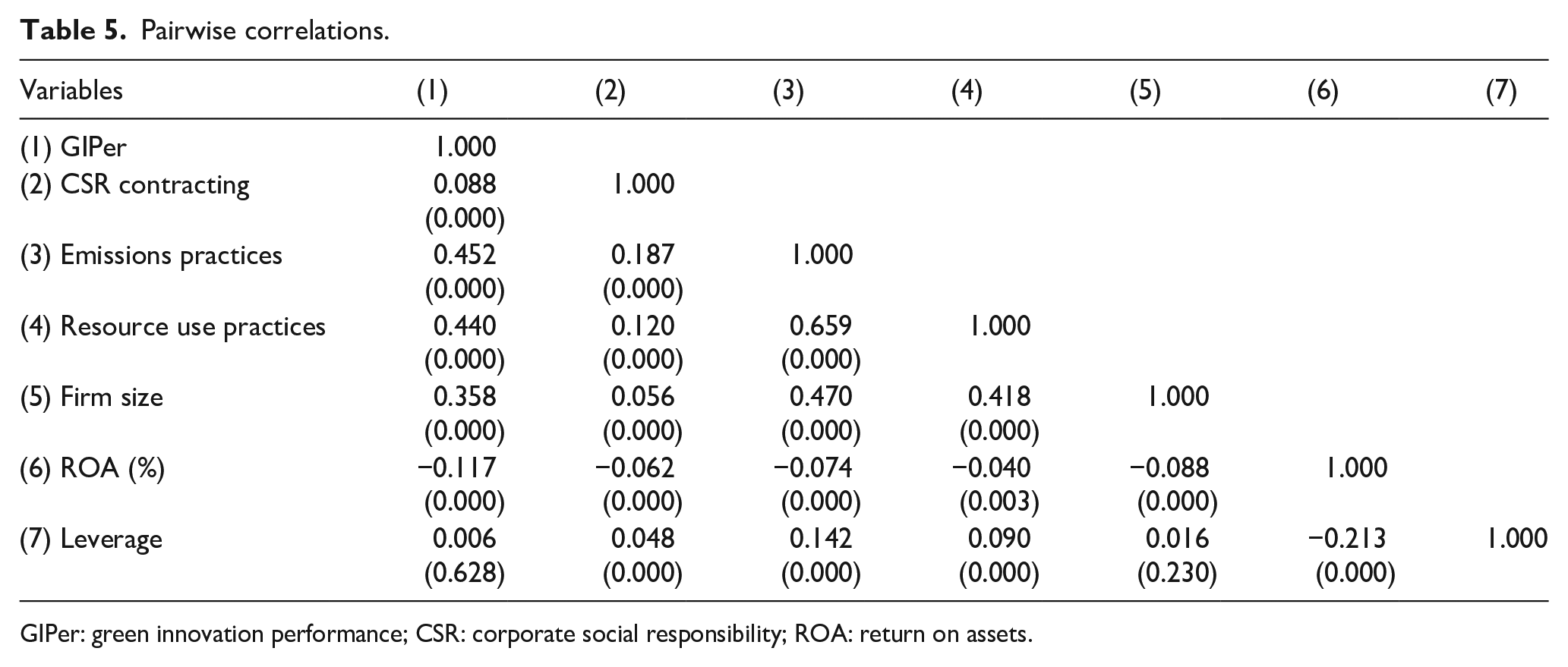

Table 5 provides the correlation results of the research variables. The results show that CSR contracting is positively correlated with green practices (resource use practices and emissions practices) and green innovation performance at a 1% significance level. Similarly, green practices (resource use practices and emissions practices) are positively correlated with green innovation performance at a 1% significance level. These results are consistent with our hypotheses. In addition, all of the correlation coefficients are less than 0.7 and the average variance inflation factor (VIF) for all cases is well below 10 at around 1.37. This means that our regression model does not suffer from multicollinearity.

Pairwise correlations.

GIPer: green innovation performance; CSR: corporate social responsibility; ROA: return on assets.

Empirical model

The Tobit model is a well-established econometric tool that is particularly appropriate for analyzing limited dependent variables characterized by bounded or specific ranges. In this study, the dependent variables of interest, namely, Green Innovation Performance is constrained within the range of 0–100. However, a large proportion (38%) of firms reporting zero commitment to Green Innovation Performance, leading to a sharp lower bound in the distribution at the minimum possible value. Similarly, for mediation analysis with Resource Use Practices and Emissions Practices, both variables are subject to an upper bound constraint of 6. These bounded distributions deviate from the assumptions of normality and continuity that underlie traditional regression models, making the Tobit model an appropriate alternative.

The Tobit model addresses these limitations by assuming that there is an unobserved latent variable that generates the observed data. It models the relationship between this latent variable and the observed variable, considering the censoring or truncation mechanism. However, it is important to note that the regression coefficients in a Tobit analysis are linear and additive with respect to the latent response continuum but not the observed variables. This means that the coefficients reflect the relationship between the underlying latent variable and the predictors, rather than the relationship between the observed variable and the predictors. Therefore, we adopt the post-estimation procedure to estimate the marginal effect of the censored expected value and describe how the observed variable changes with respect to the regressors. This involves estimating the partial derivative of the expected value of the censored variable with respect to each of the regressors, while holding all of the other variables constant.

We used a regression-based approach to test our hypotheses. First, we constructed a Tobit regression model to test the effect of CSR contracting on green innovation performance (H1). Regarding the indirect effect, the causal steps approach or four-step mediation model established by Baron and Kenny (1986) is the most extensively used method to examine the mediation effect. However, it has been heavily criticized due to its low power (Aguinis et al., 2017; Hayes, 2017; Radu & Smaili, 2022). Therefore, we adopted the method proposed by Hayes (2017) to examine the indirect mediation effect. Considering that there are two potential mediators in this study (i.e., resource use practices and emissions practices), we followed Hayes (2017) and used parallel multiple mediator models to test the mediating effect of green practices (resource use practices and emissions practices) between CSR contracting and green innovation performance (H2). The following Tobit regression models are used for the empirical analysis:

In Model (1), for firm i and year t, GIPerit represents the green innovation performance, CSR Contractingit reflects the adoption of CSR contracting, and Controls represents all of the control variables. This regression is aimed to predict the positive effect of CSR contracting on green innovation performance (H1).

Three Tobit panel regressions were used to test the mediation effect (H2). Models (2) and (3) test the relationship between CSR contracting and the mediator: green practices (resource use practices and emissions practices, respectively). Model (4) tests the effect of CSR contracting on green innovation performance when controlling for green practices (resource use practices and emissions practices). It also tests the effect of green practices (resource use practices and emissions practices) on green innovation performance when CSR contracting is controlled.

According to Hayes (2017), coefficient c in equation (1) captures the total effect of CSR contracting on green innovation performance. In equations (2) and (3), coefficients a1 and a2 qualify the differences in resource use practices and emissions practices, respectively, due to one-unit change in CSR contracting. In equation (4), b1 estimates the amount by which two cases differ by one unit on resource use practices differ on green innovation performance, while holding all others constant. Similarly, b2 estimates the difference in green innovation performance caused by changes in the emissions practices of a unit, while controlling for other variables. Finally, c′ examines the difference in green innovation performance caused by the unit change in CSR contracting, while holding resource use practices and emissions practices constant.

In the parallel multiple mediator models, the direct effect of CSR contracting on green innovation performance is estimated without passing through green practices (resource use practices and emissions practices), that is, coefficient c′, as previously stated. The indirect effects refer to two specific indirect effects: the first through resource use practice, estimated as the product of a1b1, and the second through emissions practices, estimated as the product of a2b2. When added together, the specific indirect effects yield the total indirect effect of CSR contracting through green practices. The total effect of CSR contracting on green innovation performance is the sum of the direct and indirect effects, as shown in equation (5).

Regression results

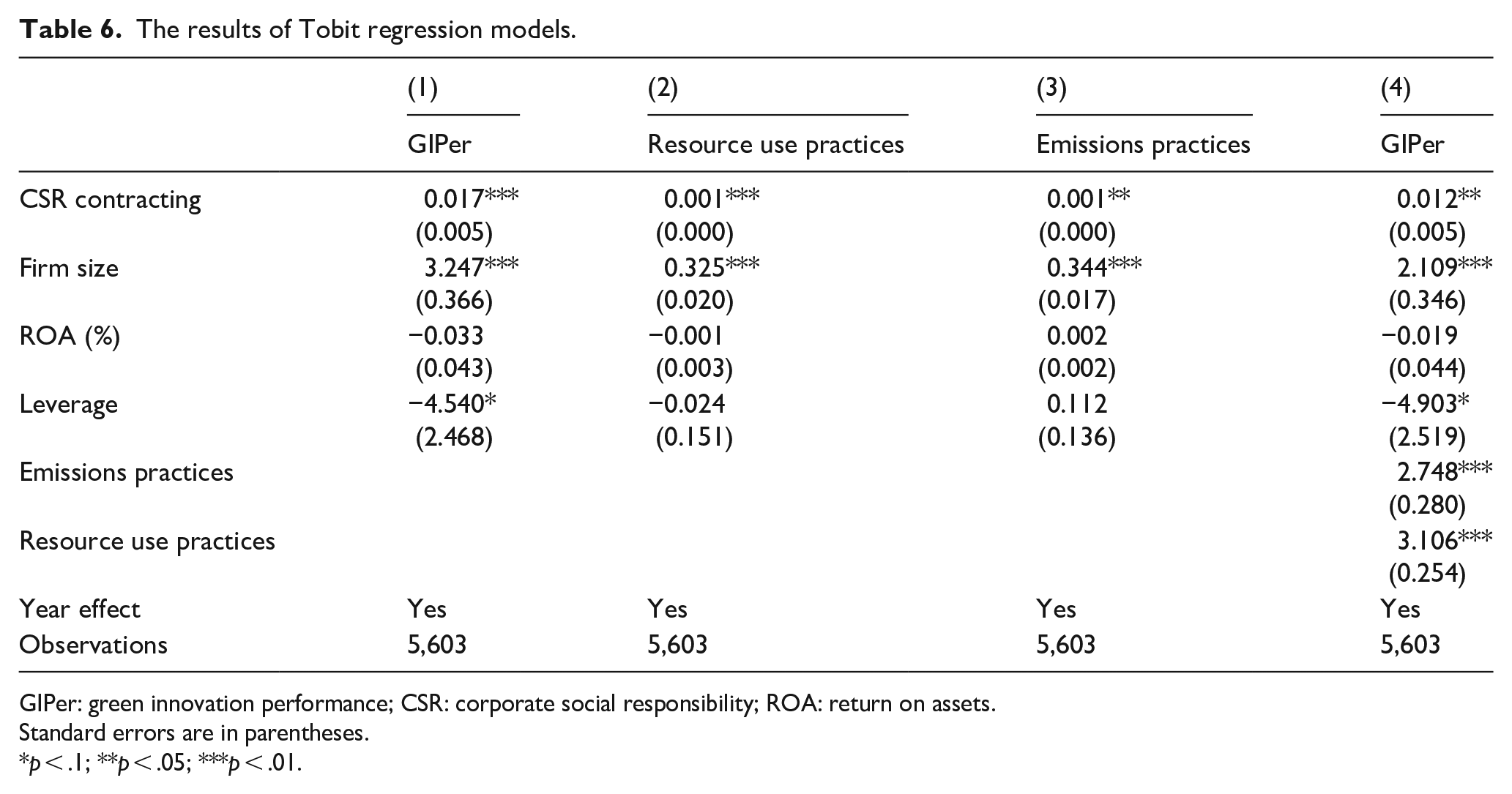

Table 6 reports the results of the Tobit model that we used to test our hypothesis. Note that all of the coefficients are marginal effects obtained by the posterior estimation procedure of the Tobit regression. Column (1) predicts the total effect of CSR contracting on green innovation performance. CSR contracting is significantly and positively related to green innovation performance (β = 0.017, p < .01), which implies that a one-unit increase in CSR contracting will increase the green innovation performance score by 0.017. Thus, our H1 is supported. Columns (2), (3), and (4) examine the indirect effect of CSR contracting on green innovation performance through resource use practices and emissions practices. The CSR contracting coefficient in Column (2) provides evidence of a positive and significant relationship between CSR contracting and resource use practices (β = 0.001, p < .01). In Column (3), there is also a very strong and positive relationship between CSR contracting and emissions practices (β = 0.001, p < .05). The results in Column (4) show a strong relationship between CSR contracting and green innovation performance. Although the CSR contracting coefficient (β = 0.012) is lower than the coefficient (β = 0.017) in Column (1), it is still positive and significant. These results suggest that CSR contracting affects green innovation performance through both resource use practices and emissions practices, thereby supporting H2.

The results of Tobit regression models.

GIPer: green innovation performance; CSR: corporate social responsibility; ROA: return on assets.

Standard errors are in parentheses.

p < .1; **p < .05; ***p < .01.

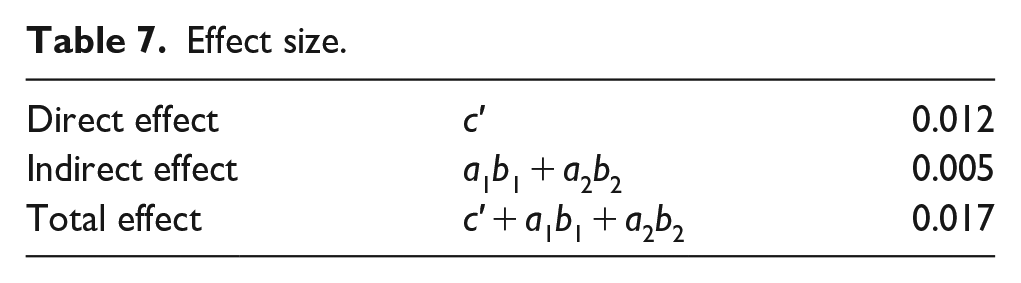

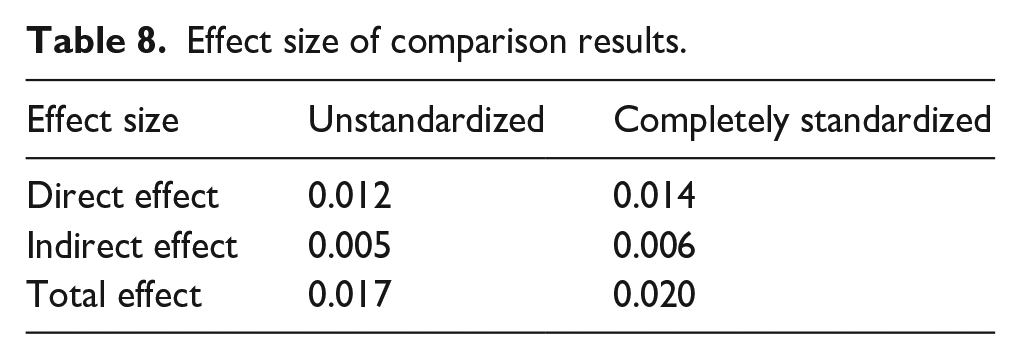

The total positive effect of CSR contracting on green innovation performance is 0.017 (p < .01), consisting of a direct effect of 0.012 (p < .05) and two specific indirect effects. One specific indirect effect of CSR contracting on green innovation performance is through resource use practices, which is the product of a1b1 (0.003 = 0.0011 × 3.106, both coefficients are significant at a 1% level). Another specific indirect effect is through emissions practices, which is the product of a2b2 (0.002 = 0.0007 × 2.748, significant at the 5% and 1% level, respectively). These two indirect effects are summed to obtain the total indirect effect (0.005 = 0.003 × 0.002). As a result, the total effect of CSR contracting on green innovation performance is the sum of the direct effect (0.012) and indirect effect (0.005), that is, 0.017. The results are shown in Table 7.

Effect size.

Completely standardized effect size

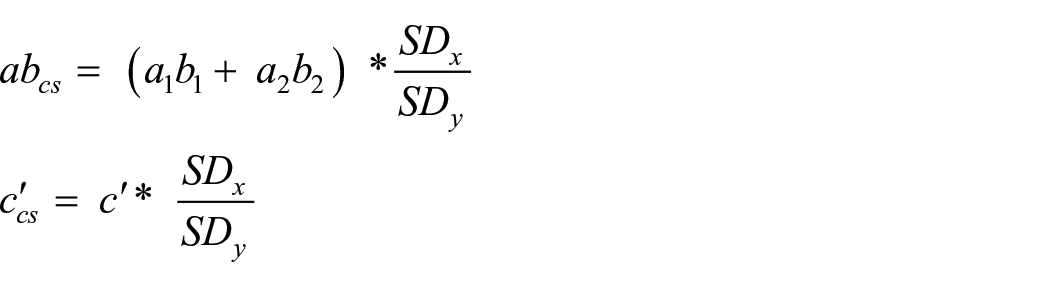

The most common method to express effect sizes is to interpret the estimated coefficients of the sample as the estimated coefficients of the population. However, the drawback of using the estimated coefficients of sample as a measure of effect size is that it is not robust to changes in size, which limits its usefulness in meta-analysis. We followed Hayes (2017) and conducted a completely standardized indirect effect measure. The indexes are shown as follows

where a1, b1, a2, and b2 are the raw coefficients from the regression model, and SDx and SDy are the standard deviation of the independent variable and dependent variable, respectively.

This completely standardized effect rescales ab and c′ to the standard deviation of both the dependent and the independent variable and captures the difference in standard deviation in Y between the two cases that differ by one standard deviation in X. Appling this to our case, the completely standardized direct effect size of CSR contracting on green innovation performance is 0.014 = 0.012 × 41.160/36.213. Similarly, the completely standardized indirect effect size of CSR contracting on green innovation performance through green practices is 0.006 = (0.003 + 0.002) × 41.160/36.213. Table 8 summarizes the unstandardized effect size (from the original regression model) and completely standardized effect size.

Effect size of comparison results.

Supplementary analyses and robustness test

Mitigating large sample bias

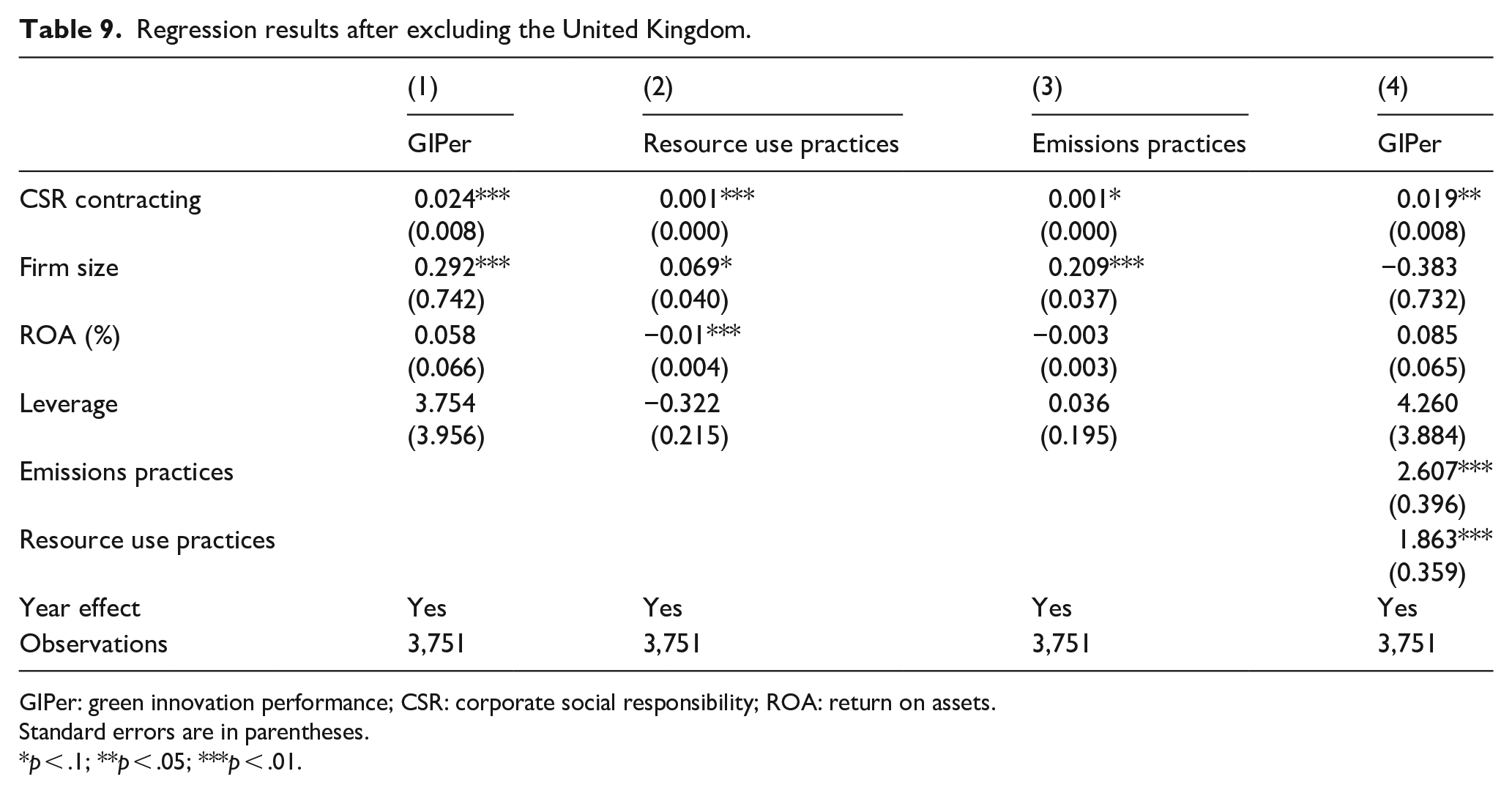

Table 1 shows that the majority of our sample consists of UK firms, who accounted for approximately 33% of the sample. As large sample bias can be a concern when a significant proportion of firms are from a single country. Consequently, we conducted a robustness check by excluding UK firms from the sample and re-estimating the main regression. The results of this robustness test are presented in Table 9.

Regression results after excluding the United Kingdom.

GIPer: green innovation performance; CSR: corporate social responsibility; ROA: return on assets.

Standard errors are in parentheses.

p < .1; **p < .05; ***p < .01.

Consistent with our main findings, we find that the effect of CSR contracting on green innovation performance remains positive and significant (β = 0.024, p < .01 for the total effect; β = 0.019, p < .05 for the direct effect model), even after excluding UK firms from the sample. Furthermore, we conducted an additional analysis to estimate the mediation effect of green practices on the relationship between CSR contracting and green innovation performance. The results indicate that resource use practices and emissions practices mediate the relationship between CSR contracting and green innovation performance. This highlights the importance of green practices in driving corporate sustainability outcomes.

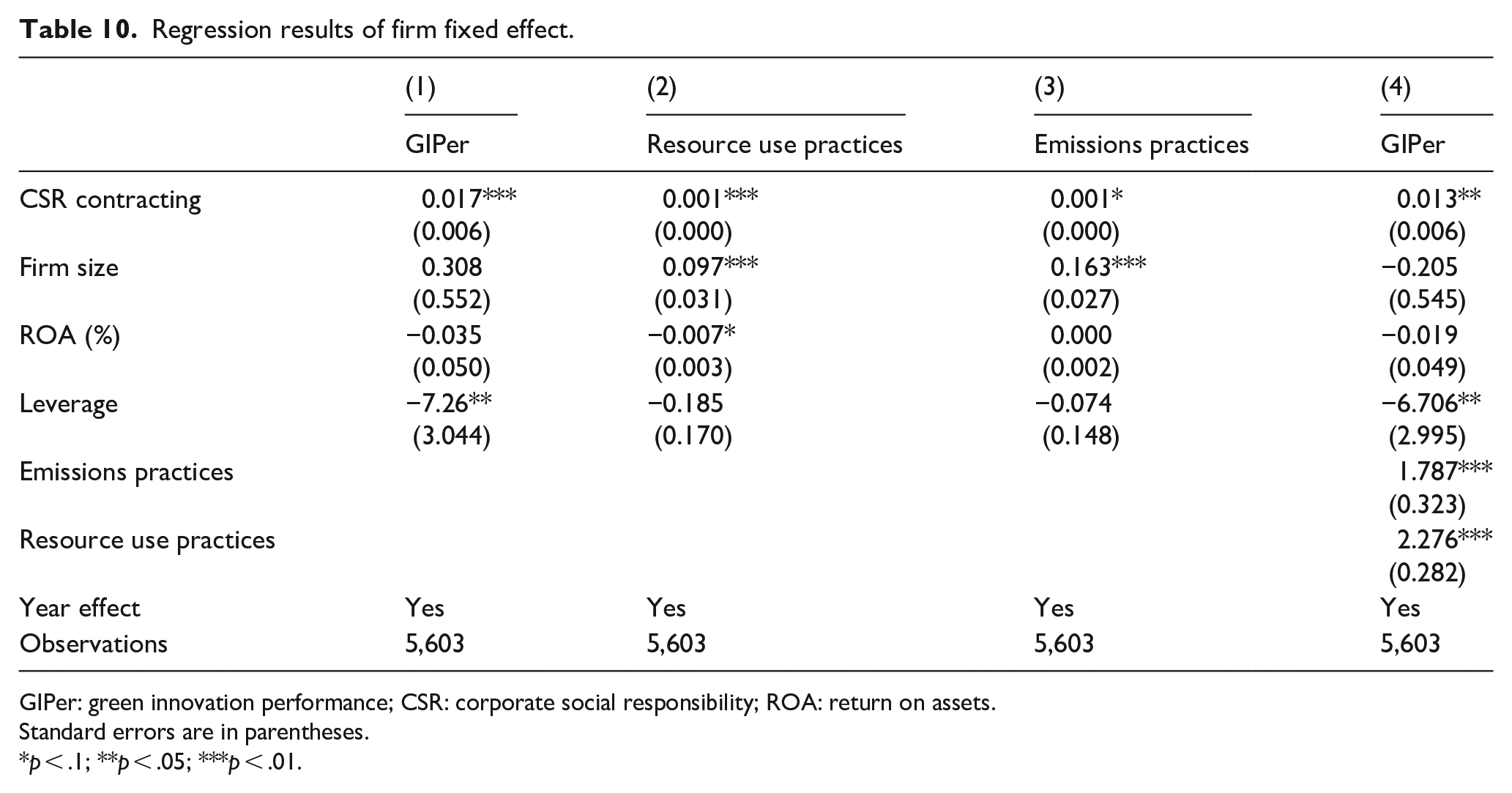

Controlling for firm fixed effect

To address concerns about omitted variables, we conducted additional analyses by re-estimating equations (1)–(5) using the full sample and including firm fixed effects in the panel regressions. Firm fixed effects capture time-invariant unobservable firm characteristics that are correlated with both CSR contracting and green innovation performance. If these characteristics are constant over time, then controlling for firm fixed effects will address concerns about omitted variables. The results of the regressions that include firm fixed effects are reported in Table 10.

Regression results of firm fixed effect.

GIPer: green innovation performance; CSR: corporate social responsibility; ROA: return on assets.

Standard errors are in parentheses.

p < .1; **p < .05; ***p < .01.

Consistent with our main findings, we find that the coefficients on CSR contracting remain significantly positive (β = 0.017, p < .01 for the total effect model; β = 0.013, p < .01 for the direct effect model) when controlling for firm fixed effects. Moreover, our analysis indicates that the indirect effects of resource use practices and emissions practices provide support for our main findings. Specifically, these practices serve as important mediators in the relationship between CSR contracting and green innovation performance. This further underscores the effectiveness of CSR contracting in promoting green practices and fostering green innovation performance. Overall, these additional analyses strengthen the robustness of our results and provide additional support for the effectiveness of CSR contracting in promoting green innovation in corporations.

Addressing potential endogeneity

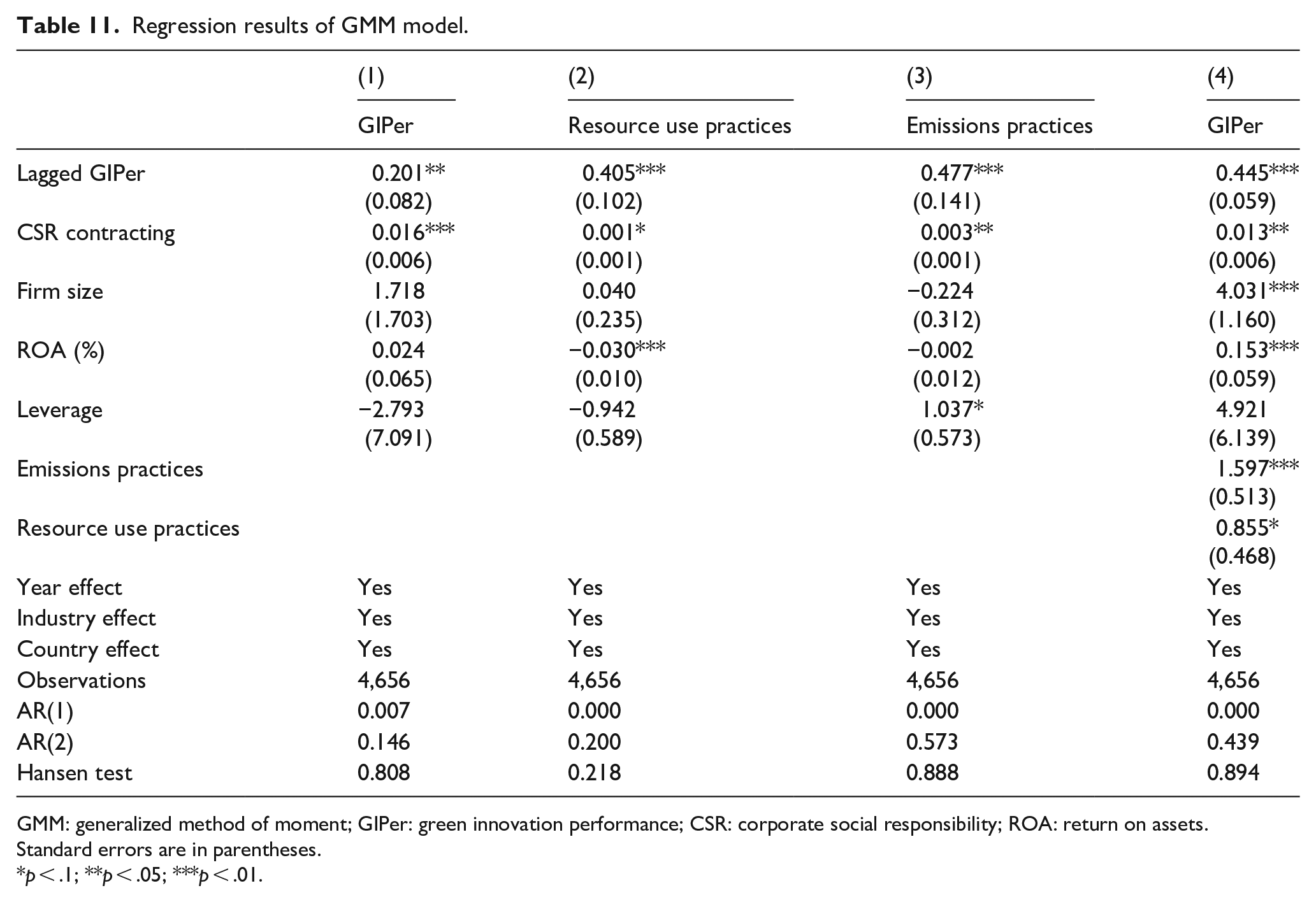

To address potential issues of endogeneity and reverse causality among CSR contracting, green practices, and green innovation performance, we utilized a dynamic two-step system generalized method of moment (GMM) approach, which was proposed by Blundell and Bond (1998). This method is effective at mitigating endogeneity through the internal transformation of data and the use of lagged values of the dependent variable (i.e., green innovation performance t − 1). To ensure robustness, we also incorporated year, industry, and country dummies in all of our models to control for year, industry, and country-level fixed effects. In line with previous research, we used the lags of all explanatory variables as instruments in all model specifications (Phung et al., 2023; Radu & Smaili, 2022; Ullah & Wu, 2023). We present our results of GMM models in Table 11.

Regression results of GMM model.

GMM: generalized method of moment; GIPer: green innovation performance; CSR: corporate social responsibility; ROA: return on assets.

Standard errors are in parentheses.

p < .1; **p < .05; ***p < .01.

To test the validity of our instruments, we employed the Arellano–Bond test for the absence of serial autocorrelation and the Hansen test for over-identifying restrictions. We found that our main findings remained relatively unchanged in all of our GMM models, and Arellano-Bond test and Hansen tests indicated that all model specifications passed the autocorrelation test for the validity of the instruments. Therefore, we conclude that after controlling for dynamic endogeneity, our results are robustly grounded.

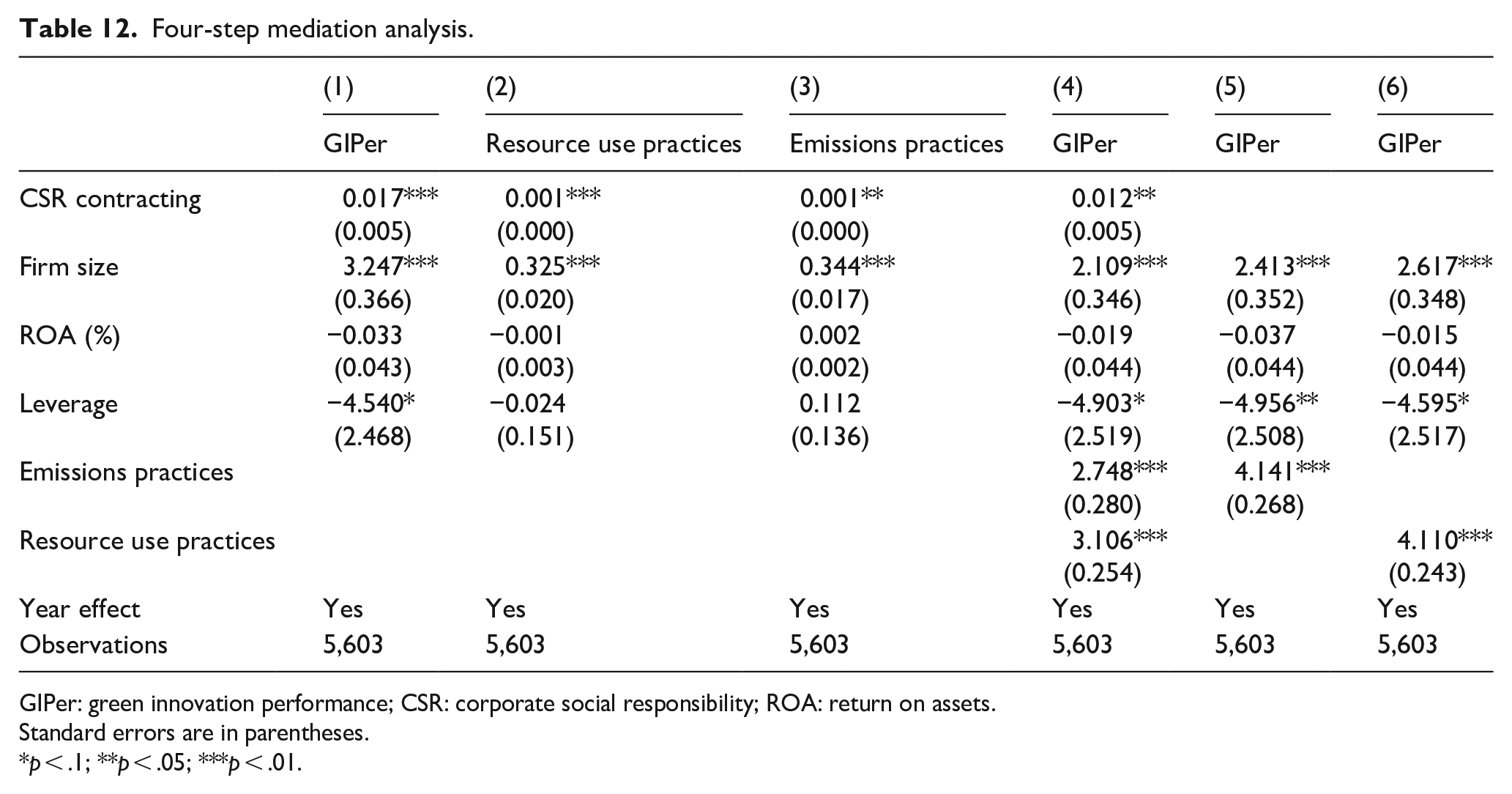

Four steps mediation effect analysis

To ensure the robustness of our mediation analysis, we followed Baron and Kenny’s four-step approach (Baron & Kenny, 1986). First, we tested the total effect of CSR contracting on green innovation performance and estimated the coefficient c for the total effect. Second, we tested the relationship between CSR contracting and the mediator green practices (including resource use practices and emissions practices separately) and estimated the coefficients a1 and a2. Third, we tested the effect of green practices on green innovation performance, while controlling for the effect of CSR contracting and estimated the coefficients b1 and b2. Finally, we tested the direct effect of CSR contracting on green innovation performance, while controlling for the effect of resource use practices and emissions practices and estimated the coefficient c′. As shown in Table 12, the results of our mediation test on green practices using Baron and Kenny’s four-step approach were similar to those presented in Table 6, which further supports our main findings.

Four-step mediation analysis.

GIPer: green innovation performance; CSR: corporate social responsibility; ROA: return on assets.

Standard errors are in parentheses.

p < .1; **p < .05; ***p < .01.

Discussion and conclusion

The objective of this study was to investigate the relationship between CSR contracting and green innovation performance in European firms from 2012 to 2021. Our findings suggest that the adoption of CSR contracting contributes to the promotion of green innovation performance. This study builds on previous research that emphasizes the importance of aligning executive compensation with CSR goals to promote sustainable development for various stakeholders, including shareholders, employees, customers, and the environment (Aguinis et al., 2017; Flammer et al., 2019; Focke, 2022; Phung et al., 2023). This study highlights the critical importance of incorporating CSR criteria into executive compensation plans to promote eco-friendly practices and green innovation performance. By aligning the senior executives’ interests with the company’s long-term goals, CSR contracting can increase the effectiveness of incentivizing executives to prioritize green innovation performance, which ultimately contributes to the company’s broader sustainability objectives.

This study has explored the indirect effect between CSR contracting and green innovation performance and found that green practices—specifically resource use and emissions practices—play a crucial role in strengthening the link between CSR contracting and green innovation performance. This is a significant finding because it highlights opportunities for top managers to engage in practices that ultimately promote green innovation performance. The findings demonstrate the need to develop effective green practices. They also identify two specific paths toward green innovation performance. First, resource use practices such as resource reduction water efficiency, energy efficiency, and environmental material sourcing were found to be effective in reducing operating costs and provide better sustainable solutions to environmental issues. Second, this study found that green practices that focus on emissions reduction and pollution prevention contribute significantly to the benefits of CSR contracting for a firm’s green innovation performance. This may be attributed to the fact that emissions practices often involve new technologies, products, and processes, which are fundamental to achieving green innovation performance.

Our findings provide valuable insights for managers and policymakers on how CSR contracting can be leveraged to promote green innovation development, which is especially important in EU countries as the largest economic block. First, implementing CSR-contingent compensation may lead to the achievement of corporate sustainability goals and the alignment with the United Nation (UN) 2030 agenda for sustainable development. We stress the significance of CSR in executive compensation and find that a firm’s green innovation performance is driven by the effectiveness of CSR contracting, which encourages senior executives to engage in a green agenda while continuing to recognize their contribution. Importantly, integrating CSR criteria into executive compensation can benefit the firm because it holds senior managers explicitly accountable for the firm’s CSR issues. Therefore, well-structured executive compensation can align the interests between senior executives and companies regarding green innovation development.

Second, this research finds that encouraging senior executives to engage in green practices can help a firm to achieve greater green innovation performance. In this study, we analyzed two types of green practices: efficient resource use and emissions reductions. Our findings provide a novel perspective on promoting green practices among executives and leveraging them to achieve better green innovation performance. The results indicate that companies can encourage executives to adopt eco-friendly practices by optimizing resource utilization and increasing operational efficiency and profitability. Moreover, companies can enhance their public image and reputation by reducing their environmental footprint, which can further motivate executives to prioritize sustainability. These findings underscore the significance of integrating sustainability into corporate strategy and incentivizing executives to align their actions with long-term environmental goals. By integrating green practices into the decision-making process and incentivizing executives to prioritize sustainability, companies can improve their overall performance and contribute to a more sustainable future.

For the academy, this study adopts the theoretical frameworks of agency theory and stakeholder theory to explore how CSR compensation—an additional tool among the existing governance mechanisms used by board of directors—can be used to incentivize the managers to take actions that increase green innovation performance over their risk-averse nature. Environmental innovation is crucial for long-term survival in today’s business environment and can even improve a firm’s profitability by adopting innovative production methods and efficient use of resource. In addition, by examining the mediating effects of green practices, we gain a better understanding of the mechanisms at play. To obtain more precise estimates of the impact of CSR contracting on green innovation performance, we employ Tobit post-estimation techniques. Furthermore, this study includes detailed robustness checks, which enhance the reliability of our empirical evidence.

This study has also observed some limitations that may be addressed by further research. First, we believe that CSR contracting is a driving factor for green practices and green innovation performance, but employee-level compensation incentives may also play an important role. Therefore, further studies may examine the relationship between CSR and green innovation from the perspective of the employees. Second, our findings may not apply to companies in other regions because our data only cover companies in European countries; thus, a more international and comprehensive result is needed. Finally, this study explores two types of green practices (i.e., resource use practices and emissions practices), and therefore, other types of green practices could be included in future research.

Footnotes

Appendix

Green practices indicators derived from Eikon database.

| Green practices | Definitions | Coding | |

|---|---|---|---|

| Resource use practices | |||

| 1 | Resource reduction | Does the company have a policy for reducing the use of natural resources? | 0/1 |

| 2 | Water efficiency | Does the company have a policy to improve its water efficiency? | 0/1 |

| 3 | Energy efficiency | Does the company have a policy to improve its energy efficiency? | 0/1 |

| 4 | Environmental supply chain | Does the company have a policy to include its supply chain in the company’s efforts to lessen its overall environmental impact? | 0/1 |

| 5 | Environmental materials sourcing | Does the company claim to use environmental criteria (e.g., life cycle assessment) to source or eliminate materials? | 0/1 |

| 6 | Environmental management | Does the company use environmental criteria in the selection process of its suppliers or sourcing partners? | 0/1 |

| Emissions practices | |||

| 1 | Emissions reduction | Does the company have a policy to improve emission reduction? | 0/1 |

| 2 | Climate change opportunities | Does the company view climate change as a business opportunity? | 0/1 |

| 3 | Waste reduction | Does the company report on initiatives to recycle, reduce, reuse, substitute, treat, or phase out total waste? | 0/1 |

| 4 | ISO 14000 or EMS | Does the company claim to have an ISO 14000 or EMS certification? | 0/1 |

| 5 | Environmental restoration | Does the company report or provide information on company-generated initiatives to restore the environment? | 0/1 |

| 6 | Environmental investments | Does the company report on making proactive environmental investments or expenditures in new technologies? | 0/1 |

EMS: environmental management system.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors gratefully acknowledge the funding received through the PID2020-115018RB-C31 and PID2019-105001GB-I00 (AEI/FEDER, UE) research projects financed by the Spanish Ministry of Science, Innovation and Universities and the European Regional Development Funds.