Abstract

The literature on corporate governance has highlighted the importance of board characteristics related to firm innovation. However, empirical findings have not been totally conclusive, and some seem contradictory. Adopting a new perspective, we have tried to help resolve the puzzle using a meta-analysis that integrates findings from 96 previous studies to analyze the relationship between board attributes, grouped by their relation to structural or demographic diversity, and firm innovation for the period 1988–2018. The results suggest that certain aspects of boards, such as meeting frequency and the proportions of independent directors and outsiders, show the most significant correlations with firm innovation, but the levels of association vary depending on whether innovation is measured as inputs or outputs and depending on the sample considered and the methodology employed. Finally, general guidelines are suggested regarding practical implications and future research.

Introduction

Firm innovation is an important element inside organizations for maintaining their position or expanding into new markets (Brown & Eisenhardt, 1997). Innovation is the implementation of a new or significantly improved product (good or service), or process, a new marketing method, or a new organizational method in business practices, workplace organization, or external relations (OECD/Eurostat, 2005). It involves making long-term risk decisions that must be carefully addressed and planned to ensure success (Aghion et al., 2013). The function of the board of directors is important not only as a monitoring and control mechanism, but also as a source of support and assistance in decision-making (Adams & Ferreira, 2007). Consequently, over recent years, increasing interest has become apparent in the literature in the role played by the board of directors and in the board characteristics that are most desirable for promoting firm innovation. Additionally, the empirical evidence is not conclusive, and the results are sometimes contradictory. The representativeness of samples or the context analyzed are some aspects that might determine such results, making it impossible to reach conclusions that can be generalized. Sometimes, prior studies focus on a single variable relating to the board, variables are defined in different ways or innovation is not considered in its two dimensions, namely inputs and outputs. Inputs are related to efforts in terms of investment in resources and incentives to support innovation and are generally represented by R&D activities (Balsmeier et al., 2014; Buchwald & Thorwarth, 2015; Ghosh, 2016) or R&D intensity (Deutsch, 2007; Kor, 2006; Lacetera, 2001). Outputs refer to the results obtained and the productivity of research in the form of new products (Chen et al., 2016; Kim & Kim, 2015; Wu, 2008a) or processes within the organization (Balsmeier et al., 2017) including, among others, patents and patent citations (Ahuja et al., 2008). When studying innovation, the emphasis must be placed on measuring all inputs and innovation activities and/or on measuring innovation outputs (Cirera & Muzi, 2020, p. 2). 1 In consequence, it is necessary to analyze the relationship between the board of directors and firm innovation from another perspective which can group, summarize, and analyze large amounts of information using quantitative data. Meta-analysis is a methodology for the statistical analysis of previously reported results that provide evidence regarding a research question. Since its birth in the fields of psychology and education (Glass, 1976), meta-analysis has become increasingly important in research but it did not reach all disciplines at once. It was widely adopted first in the social sciences and health sciences in the 90s (Sánchez-Meca & Botella, 2010; Shelby & Vaske, 2008) and arrived a little later in economics. Since then, it has become consolidated as a methodological tool. Within economics, some fields began to develop meta-analysis before others. For example, in management and marketing, it was introduced earlier than in finance research, where its opportunities for application have only recently begun to be widely identified. Geyer-Klingeberg et al. (2020) review 61 meta-analyses published in finance and state that the median for the year of publication is 2017, which indicates that in the last 4 years, there has been an authentic explosion of meta-analysis in this area.

Considering that innovation is one of the key strategic decisions for firms and for the economy as a whole, the main goal of our research is to explore the determinants of firm innovation and, in particular, to clarify the role played by the board of directors. We aim to unify criteria and determine both whether board characteristics are closely associated with firm innovation (measured in inputs and outputs) and the sign (positive or negative) of the relationship. We also distinguish between board structural and demographic diversity. Corporate governance codes around the world as well as research on corporate governance tend to recommend increasing board diversity (e.g., Baker et al., 2020; Ben-Amar et al., 2013) to enhance information resources and broaden the cognitive and behavioral range of the board (Fernández-Gago et al., 2018; Harjoto et al., 2018). Board diversity may also generate environments of creativity and discussion for decision-making (Brunninge et al., 2007) and reduce the information asymmetry associated with new projects (Wang, 2011). To achieve the above research goal, we perform a meta-analysis of 96 prior studies on 19 countries from Africa, Asia, Europe, North America, and Australia.

On analysis of the literature, we found a systematic review of non-exhaustive literature on corporate governance (ownership structure and board of directors) and firm innovation (Gonzales-Bustos & Hernández-Lara, 2016) as well as a theoretical review on the topic (Asensio-López et al., 2019). However, as far as we know, there are no prior studies on the specific association between the board and firm innovation using the meta-analysis technique. 2 Thus, although the qualitative contributions of systematic and theoretical reviews are important, our research takes a step further with the quantitative analysis that meta-analysis allows by including statistical techniques. In addition, given the variety of innovation measures and the inconclusive results of previous research when analyzed together, we delve into each of the most used board features related to firm innovation distinguishing between inputs and outputs.

Thus, our research offers several contributions regarding the relationship between boards of directors and firm innovation. First, we use a meta-analysis methodology to gain a broader perspective in order to add additional evidence to previous literature that has not always been conclusive regarding the relationship between the board of directors and firm innovation. Unlike the previous reviews and the two previous meta-analyses which tangentially consider the link between a few board attributes and innovation (Deutsch, 2005; Van Essen et al., 2012), our research also includes a comprehensive review of this specific relationship in the previous literature. For this purpose, we consider several board characteristics that have been widely analyzed by previous literature, and we group them by their relation to structural or demographic diversity. Although previous research (Hafsi & Turgut, 2013; Hoang et al., 2017) highlights the importance of including both dimensions of board diversity when explaining firm decisions, this approach has not yet been considered in the innovation literature. Thus, by considering both the group characteristics of the board (structural diversity) and the individual characteristics of each director (demographic diversity), combined with the meta-analysis methodology, we can analyze their role as determinants of innovation from a different and more complete perspective. In addition, more papers are analyzed in this document (96) than in the aforementioned previous meta-analyses, making our findings more representative.

Second, there is a distinction between the efforts and results of innovation, so it is necessary to analyze whether the relationship between the board of directors and firm innovation differs when inputs and outputs are considered. Previous empirical results are not conclusive, so the use of homogeneous measures in each of the relationships studied is important when performing a meta-analysis.

Third, our findings highlight the presence of other factors that may moderate the relationship (board and firm innovation). Previous meta-analyses have already considered the location or region in which the study was conducted as a possible moderator variable (Hancock et al., 2013; Marín-Idárraga et al., 2020). In addition, since findings differ if studies are conducted in one country (Balsmeier et al., 2014; Kim & Kim, 2015) or across multiple countries (Bobillo et al., 2018; Harjoto et al., 2018), it can be inferred that the fact that a study is carried out in one specific country or in a sample of countries may affect the relationship between the board and firm innovation. In addition, another moderating variable that stands out in previous meta-analyses is the methodology employed (Junni et al., 2013; Kohli & Devaraj, 2003; Stam et al., 2014). Results can differ if the sample data are cross-sectional (Barnhart & Rosenstein, 1998; Barroso-Castro et al., 2016) or longitudinal (Chen et al., 2016; Guldiken & Darendeli, 2016). As firm innovation requires short-term investment expenditure but has long-term results (Hoskisson et al., 2002), research with cross-sectional data may not be sufficient to visualize the effects of the board on firm innovation as a whole. In contrast, longitudinal analyses allow for a deeper understanding over time, as well as the inclusion of other variables such as lags or firm-specific effects. Therefore, considering these aspects (country and methodology) may be important for new research in this field.

The results suggest that board structural diversity (board size, composition, duality, and meeting frequency) is positively associated with innovation outputs (except for director equity when the association is negative). Regarding the relationship between board structural diversity and innovation measured as inputs, two associations stand out: a negative association with board size and a positive association with duality. Regarding board demographic diversity, a positive association is found between the percentage of women and social capital with innovation inputs. There is also a positive association of directors’ tenure with innovation outputs. In addition, our results show that some moderator variables, like country or methodology, may affect the board–innovation relationship.

The article is structured as follows: the second section presents the literature review on the board of directors and innovation and the hypotheses to be tested. Section “Methodology” describes the methodology used for the meta-analysis regarding compilation of the literature, operationalisation of the variables, and the statistical techniques used. Section “Results” describes the results obtained for each of the variables proposed, and section “Discussion and conclusion” gives the general conclusions of the study, its implications, and future lines for research.

The board of directors and firm innovation: theoretical background and hypotheses

The literature on the board of directors as a determinant of firm innovation has studied this relationship from different viewpoints. The first studies that related the board with firm innovation were focused on board equity and the proportion of inside and outside directors (Baysinger et al., 1991; Hill & Snell, 1988). Subsequently, other board characteristics started to be considered, such as size, independent directors, or duality. More recent studies not only include the traditional variables mentioned above but also analyze other characteristics related to boards such as gender, knowledge and professional diversity, or connections outside the firm, among others (Hernández-Lara & Gonzales-Bustos, 2019; Mukarram et al., 2018; Whitler et al., 2018).

Regarding the theories used to study the relationship between firm innovation and the board of directors, since the first article in 1988, most of them have been mainly based on agency theory (Jensen & Meckling, 1976). This theory assumes that there is likely to be opportunistic behavior by managers acting for their own benefit rather than for the firm, and in consequence, shareholders should adopt measures to prevent such managerial behavior (Hill & Snell, 1988). This theory emphasizes the importance of aligning interests between shareholders as principals and managers as agents through incentive mechanisms or through monitoring and control by the board of directors to promote the pursuit of innovation (Zahra, 1996). Subsequently, authors such as Kor (2006) began to use other theories to give another perspective to the board characteristics–innovation relationship. Thus, the resource dependency theory (Pfeffer & Salancik, 1978) started to be used. This theory proposes that firms need to obtain resources from the environment, since they cannot generate resources on their own. The board of directors thus becomes a tool that allows the firm to access these external resources and minimize the risk involved in making decisions related to innovation (Chen, 2012; Kor, 2006). In addition, the resource-based theory (Barney, 1991) argues that each firm has its own unique set of resources and capabilities. When these resources and capabilities are properly developed, they may be transformed into dynamic competencies such as innovation (Ferreira et al., 2020; Teece et al., 1997). An example of such resources is board diversity, which can enrich the decision-making process related to innovation (Wang, 2011). Another frequently used theory is stewardship theory (Donaldson & Davis, 1991), which assumes that managers and directors will do a good job because doing so will bring them greater utility and prestige than opportunistic and individualistic behavior. Consequently, it may be beneficial for strategic decision-making such as innovation for the board of directors to consist mostly of inside directors who have greater knowledge of the firm (Hernández et al., 2010).

Other less commonly used theories are the board capital theory (Haynes & Hillman, 2010; Hillman & Dalziel, 2003), which proposes that boards use their human capital (educational level and experience) and social capital (interconnections with other firms) to provide monitoring and advice on major strategic actions like firm innovation. Stakeholder theory (Freeman, 1984; Freeman & Evan, 1990) states that not only are the interests of shareholders important, but also the interests of other actors such as customers, suppliers, employees and society in general. Consequently, the board of directors needs to look after the interests of all of them. Critical mass theory (Kanter, 1977) has also been used. It argues that when a minority group, such as women directors on boards, reaches a certain threshold or critical mass, there is a qualitative change in the nature of the group’s interactions and organizational changes which allows innovation to begin (Torchia et al., 2011). In addition, the friendly board theory (Adams & Ferreira, 2007) has been used, suggesting that a close relationship between directors and the CEO can be beneficial by creating an environment of cooperation, confidence, and exchange of information that enables improved decision-making in different aspects like innovation (Kang et al., 2018). Another theory used is the upper-echelon theory (Hambrick & Mason, 1984), which assumes that the psychological and observable characteristics of managers and directors, such as age, gender, experience, tenure, and educational and functional background, are determinants of strategic decisions such as firm innovation (Wincent et al., 2012).

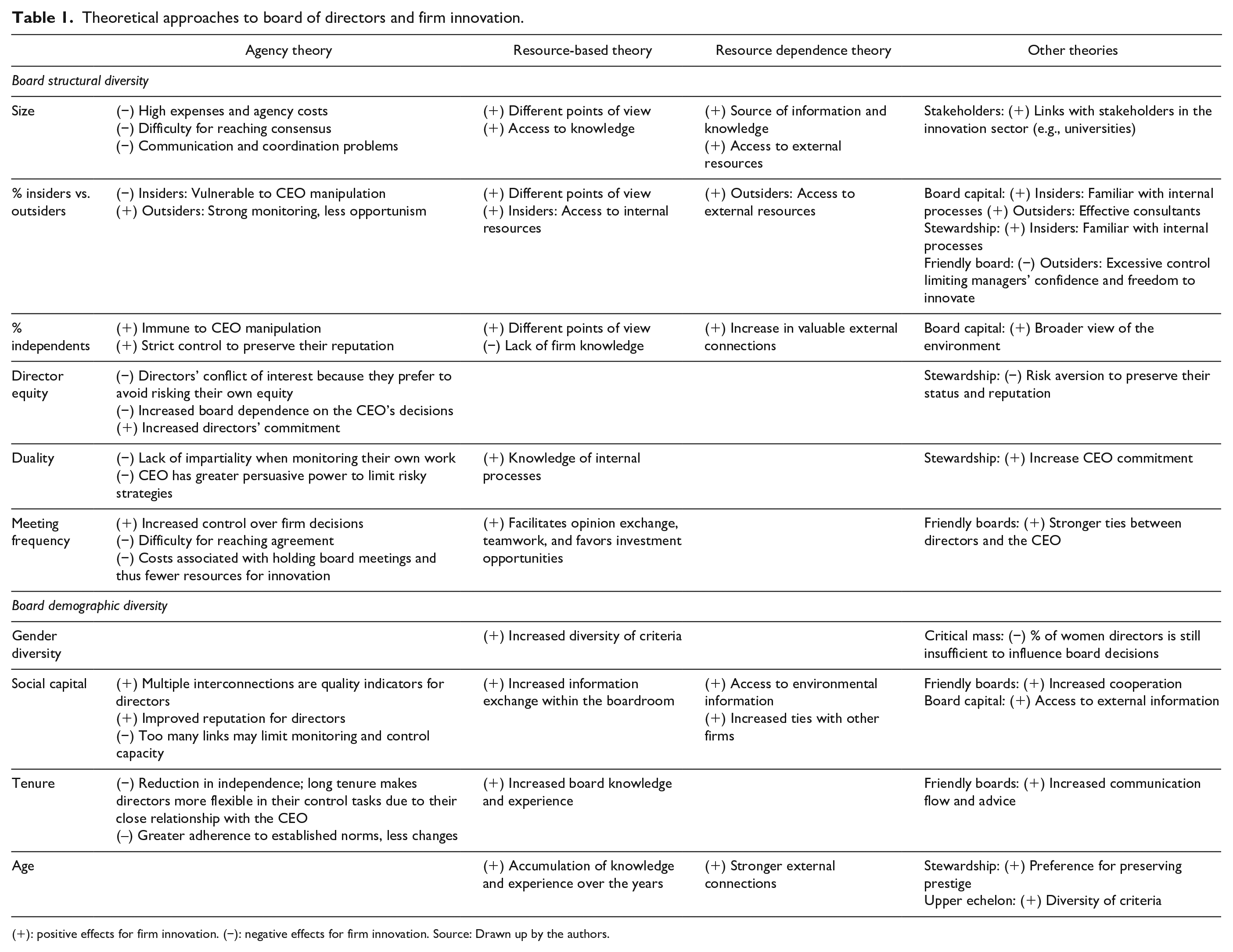

As stated above, this research considers most of the board characteristics that have already been analyzed and, especially in order to perform the meta-analysis, those that can be compared because they use the same proxies and those for which it is feasible to obtain individualized data for each type of association with firm innovation (inputs and outputs). Previous research suggests that board of directors’ characteristics may be grouped in two main categories depending on whether they relate to structural diversity or demographic diversity (Ararat et al., 2015; Hafsi & Turgut, 2013; Hoang et al., 2017; Johnson et al., 2013). Structural diversity includes those group attributes of the board that differ from one board to another, while demographic diversity refers to the set of individual attributes inherent to each board member within the board. Therefore, in order to analyze the relationship between firm innovation and the selected board characteristics, we grouped the latter into these two categories: structural diversity, which includes board size, composition (percentage of insiders, outsiders, and independent board members), board equity, board seat accumulation (duality), and board meeting frequency; and demographic diversity, which refers to the rest of the variables studied (presence of women directors, board social capital, directors’ tenure, and directors’ age). Table 1 shows an overview of the main theories presented above to explain the relationship between each board variable and firm innovation. Next, we explain how board structural and demographic diversity influence firm innovation, and we propose several hypotheses related to that influence.

Theoretical approaches to board of directors and firm innovation.

(+): positive effects for firm innovation. (−): negative effects for firm innovation. Source: Drawn up by the authors.

Board structural diversity and firm innovation

Board size and firm innovation

Board size is one of the most widely used determinants in empirical studies on the board and firm innovation relationship, and there are both positive and negative arguments for explaining such a relationship. Previous research has not yet reached a consensus on the right size of the board to stimulate firm innovation. Several theories have been used. According to the theory of resources and capabilities (Barney, 1991; Grant, 1991; Mahoney & Pandian, 1992), a larger number of directors can contribute different points of view to improve decision-making, and this may be positive for achieving a stable financial performance over the long term (Cheng, 2008). Moreover, the more complex the strategic decisions to be taken, as in innovation, the more likely it is that the situation will need to be analyzed in detail in order to reduce the risk involved. This means that the larger the board, the more probable it is that the organization will have access to resources, knowledge, and sources of information to make better decisions in line with both the theory of resources and capabilities and resource dependency theory (Chouaibi & Jarboui, 2012; Wang, 2011). These arguments are also consistent with stakeholder theory (Freeman, 1984; Freeman & Evan, 1990), which suggests that a firm’s connection with research institutions (e.g., universities) might benefit the generation of new projects. A larger board of directors may accommodate more stakeholders in innovation, such as key scientists, whose influence may lead to more innovation efforts due to their research background and distintive capabilities (Lacetera, 2001; Shapiro et al., 2015). Thus, there is empirical evidence in some papers that board size has a positive effect on innovation, such as Chen et al. (2015), De Cleyn & Braet (2012), and Wincent et al. (2012).

On the contrary, based on agency theory (Fama, 1980; Fama & Jensen, 1983; Jensen & Meckling, 1976) a large board may incur high costs in terms of expenses and may increase agency costs (Jensen, 1993). Similarly, Goodstein et al. (1994) suggest that, depending on the complexity of tasks and the ambiguity of decisions (as in investment in R&D), larger boards may prolong the decision-making process by presenting very divided positions and even personal interests, thus damaging the firm’s goals in the long term. Also, due to the communication and coordination problems that a large board size may create and the resulting lack of cohesion and divided criteria, directors are also likely to be more susceptible to CEO manipulation (Cheng, 2008). Several empirical studies support these negative arguments (Blibech & Berraies, 2018; Chen, 2012; Lin & Chang, 2012; Rossi & Cebula, 2015; Sharma et al., 2018). However, other empirical evidence suggests that board size does not have a significant effect on innovation (Bianchi et al., 2012; Chouaibi & Jarboui, 2012; Shapiro et al., 2015; Valencia, 2018) and that it is difficult to establish an optimal board size because this depends on each organization’s needs and size.

Board composition and firm innovation

Board composition is generally defined by two types of director: inside directors and outside directors. Inside directors are directly linked to the firm through a contract or employment. These inside directors are also often employed in executive positions inside the firm reporting directly to the CEO (Dalton et al., 1999). By contrast, outside directors do not have a position in the firm and their income does not mainly depend on it (Hermalin & Weisbach, 1988). Outside directors may be affiliated or independent (Dalton et al., 1999). Affiliated directors are typically key suppliers to the firm, consultants, equity owners, or representatives of equity owners, and other individuals who may have significant links to the firm in addition to serving on the board of directors (Hernández et al., 2010; Kang et al., 2017). Independent directors have no direct, contractual relationship with the firm apart from their place on the board (Fama & Jensen, 1983; Williamson, 1983). Thus, independent directors are neither employees of the firm nor affiliated with the firm or its group of companies (Ashwin et al., 2016; Blibech & Berraies, 2018).

The agency theory perspective (Fama, 1980; Fama & Jensen, 1983; Jensen & Meckling, 1976) considers inside directors to be more vulnerable to CEO manipulation. Moreover, according to the theory of resources and capabilities (Barney, 1991; Grant, 1991; Mahoney & Pandian, 1992) and resource dependency theory (Pfeffer & Salancik, 1978), inside and outside directors are considered to provide different points of view in board decisions like firm innovation. Given their direct relationship with the firm, insiders are part of the firm’s own resources and capabilities. Outsiders, since they do not belong to the firm, provide the firm with access to resources and capabilities from the environment (Hoskisson et al., 2002). This diversity of views enhances discernment capabilities when making risky strategic decisions such as innovation. The board capital theory (Hillman & Dalziel, 2003) and stewardship theory (Donaldson & Davis, 1991) offer similar arguments, namely, that inside directors know the organization, have access to privileged information and are familiar with internal processes (Chouaibi & Jarboui, 2012), and outside members provide other perspectives and may become effective consultants for the board regarding innovation. The empirical evidence obtained by Hill & Snell (1988), suggests that firms with more outside directors tend to diversify their strategies, while firms with inside directors tend to innovate more. This result is in line with other empirical studies that find that the effect of inside directors is positive for innovation (Chouaibi & Jarboui, 2012; Hoskisson et al., 2002; Takahiro, 2015b). However, Epstein et al. (2017), Hill & Snell (1988), and Lacetera (2001) do not find that the presence of internal directors has a significant effect on innovation.

Regarding the presence of outside directors on the board, some studies find a negative effect (Bobillo et al., 2018; Buchwald & Thorwarth, 2015; Deutsch, 2007; Tribbitt & Yang, 2017; Yoo & Sung, 2015; Zahra, 1996). One explanation may be that the existence of excessive control by the board of directors might have negative effects on the behavior of managers. Managers stop seeing board members as providers of advice and start to distrust them. Thus, according to friendly board theory, managers may abstain from sharing information with outsiders or limit investment in high-risk projects such as innovation to prevent putting their jobs at risk (Guldiken & Darendeli, 2016). Hoskisson et al. (2002) find evidence that the percentage of inside directors is important for promoting internal innovation, while the percentage of outside directors is important for generating more external innovation. Conversely, other authors argue that the presence of outside directors exerts greater oversight over managers’ opportunistic behavior (Fama, 1980). From a resource dependency perspective, outsiders offer the organization the possibility of accessing knowledge and external resources (Chouaibi & Jarboui, 2012), which might reduce the environmental information asymmetry and increase the firm’s intentions to invest in new projects. Some empirical studies support this positive relationship (Balsmeier et al., 2014; Hernández et al., 2010; Kor, 2006; Lu & Wang, 2015). Other studies even suggest that the effect of the proportion of outside directors on firm innovation may be positive or negative, depending on board size (Zona et al., 2013).

Related to the influence of independent directors on innovation, the agency theory perspective (Fama, 1980; Fama & Jensen, 1983; Jensen & Meckling, 1976) suggests that it is important for directors to be independent in order to guarantee that the board can exercise effective oversight over managers and prevent opportunistic behavior that might damage the firm. Given the fact that independent directors are not under the influence of the CEO, they are more free to propose new projects or question the CEO’s decisions in the boardroom than inside or affiliated directors (Kor, 2006). Moreover, as they are usually well-known professionals, they are likely to be more inclined to exercise strict control in order to preserve their own reputation (Gu & Zhang, 2016). In addition, in accordance with the board capital theory (Hillman & Dalziel, 2003) and the theory of resources and capabilities (Barney, 1991; Mahoney & Pandian, 1992), there are several reasons, most of them positive, for arguing that innovation will increase thanks to the different points of view that such independent directors can provide because they come from other environments and have a broader vision (Chen & Hsu, 2009; Dong & Gou, 2010; Shapiro et al., 2015; Wincent et al., 2012). The inclusion of independent directors, such as bankers, venture capitalists, and politicians, may facilitate access to financial resources or valuable connections outside the firm based on resource dependence theory (Shapiro et al., 2015). Thus, some studies also find a positive relationship between director independence and innovation (Berezinets et al., 2018; Chen et al., 2016; Sena et al., 2018; Sharma et al., 2018), pointing out that the presence of independent directors can also help the board to be more assertive when taking decisions on innovation (Ashwin et al., 2016). Conversely, the studies by Jermias (2007) and by Blibech & Berraies (2018) find a negative effect. They argue that this is because independent directors lack knowledge on the firm’s specific needs, which might hinder innovation. These ideas are in line with the resources and capabilities theory, which highlights the importance of the firm’s internal know-how in decision-making process (Barney, 1991; Mahoney & Pandian, 1992). In addition, other authors do not find that board independence has a significant effect on innovation (Takahiro, 2015b; Valencia, 2018).

Director equity and firm innovation

Stock options as an incentive for directors seek to empower and encourage them to participate in the firm’s long-term decisions, to ensure that these are in line with the shareholders’ interests (Deutsch, 2005). However, according to agency theory (Jensen & Meckling, 1976), when a part of the ownership is in the hands of directors, there might be conflicts of interest in making decisions, leading to opportunistic behavior. There may also be power conflicts in the boardroom between directors with a large percentage of equity (more power) and directors with less or none (less power) (Hernández et al., 2010). Directors with more power might be especially reluctant to participate in decisions on risky investments in innovation, preferring short-term investments that might lead to more stock options for themselves (Jensen & Meckling, 1976). In addition, the oversight function performed by the board and its independence might be affected because, if the directors’ focus is on gaining a larger stake in the firm, they may be obliged to support the CEO’s decisions even if these are not the most appropriate for innovating (Zahra, 1996). These arguments are also in line with stewardship theory, which suggests that directors are reluctant to assume more risk as their equity increases because, if such investments fail, their reputation and even their jobs will be at risk (Hernández et al., 2010). This is demonstrated in empirical evidence obtained by Herrmann et al. (2010), Cebula & Rossi (2015), and Rossi & Cebula (2015) that offers negative results for this relationship. Conversely, Hoskisson et al. (2002) find that incentives for board members in the form of stock options are positively related to internal innovation in a firm with regard to product generation. Deutsch (2007) analyses the effect on firms’ R&D intensity of compensation in the form of stock for external directors, finding that including a stake in directors’ remuneration increases firms’ R&D activity. They argue as a possible explanation that equity incentives for the board may encourage their active participation in R&D investment decisions (Deutsch, 2007; Hoskisson et al., 2002). That is, when directors risk their own capital, they increase their efforts and their commitment to the success of their investments. Similar results are obtained by Guldiken & Darendeli (2016). Other authors, however, do not find that directors’ stock ownership has a significant effect on innovation (Epstein et al., 2017; Kim & Kim, 2015).

Board duality and firm innovation

Duality is the term used when more than one position in the firm is held by a single person, as when the CEO is also a Chairperson of the Board and may lead to possible agency problems (Fama & Jensen, 1983). Since the limits of each role in the organization are not clear, there may be opportunistic behavior on the part of a CEO who also holds the position of Chairperson of the board and who does not objectively assess their own work (Jensen & Meckling, 1976). In addition, the duality of positions may increase the CEO’s persuasive power over the boardroom to limit long-term or risky strategies such as innovation (Kor, 2006). For these reasons, it is recommended that such power should be limited by appointing a different person to the position of Chairperson in order to facilitate oversight and keep shareholders informed of movements in the firm (Fama & Jensen, 1983). From the point of view of agency theory (Fama & Jensen, 1983), separating the positions of the CEO as decision-maker and of Chairperson of the board as overseer of decisions taken might be positive for the organization, especially in firms that decide to invest in risky, long-term projects involving innovation (Hill & Snell, 1988). This is confirmed by empirical evidence found by Kor (2006) and by Lu & Wang (2015). There are also other studies indicating that duality on the board may be negative for investments in innovation (Blibech & Berraies, 2018; Herrmann et al., 2010; Jermias, 2007).

Conversely, Driver & Guedes (2012) found no significant effect on innovation for the separation of CEO powers. Other studies show that separating positions might be negative for innovation (Chen & Hsu, 2009; Sharma et al., 2018; Takahiro, 2015c; Valencia, 2018). This argument is in line with stewardship theory, which offers a different approach (Davis et al., 1997; Donaldson & Davis, 1991), whereby the CEO is not an agent motivated by opportunism but an efficient professional who displays ethical values and is keen to work to benefit the firm and its collaborators. Thus, duality would increase the CEO’s commitment to the firm. Chouaibi & Jarboui (2012) suggest that the duality of roles allows for better strategic vision on the part of the CEO-Chairperson to make decisions. This deeper knowledge of the internal processes and constraints of the company could help the firm to take better advantage of opportunities related to new projects and developments in accordance with the theory of resources and capabilities.

Board meetings and firm innovation

From the agency theory perspective, a larger number of meetings will allow the board to exercise greater control over managers’ activities to ensure the implementation of strategies and new projects (Bianchi et al., 2012). The theory of resources and capabilities (Barney, 1991) suggests that key strategies in an organization are developed when there is joint work between the managers and the resources of an organization. In this way, the board of directors becomes a source of consultation, and board meetings may be the space in which new ideas for innovation may be generated. In addition, changes in market conditions may force organizations to explore new business opportunities (Dustin et al., 2014), and thus organizations need to generate frequent meetings for discussion and to be in the front line of new technologies and new products coming onto the market (Vafeas, 1999). Teamwork can improve when there is greater interaction among the members of a group, so it can be expected that the more meetings are held, the more likely it will be that important investment opportunities will be taken up, such as innovation (Lipton & Lorsch, 1992). According to this same criterion, board meetings are for sharing not only technical but also personal information, that is, they may help the directors to build a more consolidated team, giving them the “friendly” characteristic that furthers teamwork with CEOs, in line with the friendly boards theory (Adams & Ferreira, 2007). However, a high number of meetings could mean difficulties for directors to reach agreements on strategic decisions such as innovation and increase the costs associated with holding board meetings, such as directors’ travel expenses, directors’ meeting fees, and even managerial time (Vafeas, 1999), having the firm less resources for innovative activities. Empirical evidence is not conclusive. For example, Bianchi et al. (2012) and Sharma et al. (2018) find that board or strategy committee meeting frequency, respectively, has a positive effect on innovation. Chen (2012), however, does not find that board meeting frequency has a significant effect on R&D investments.

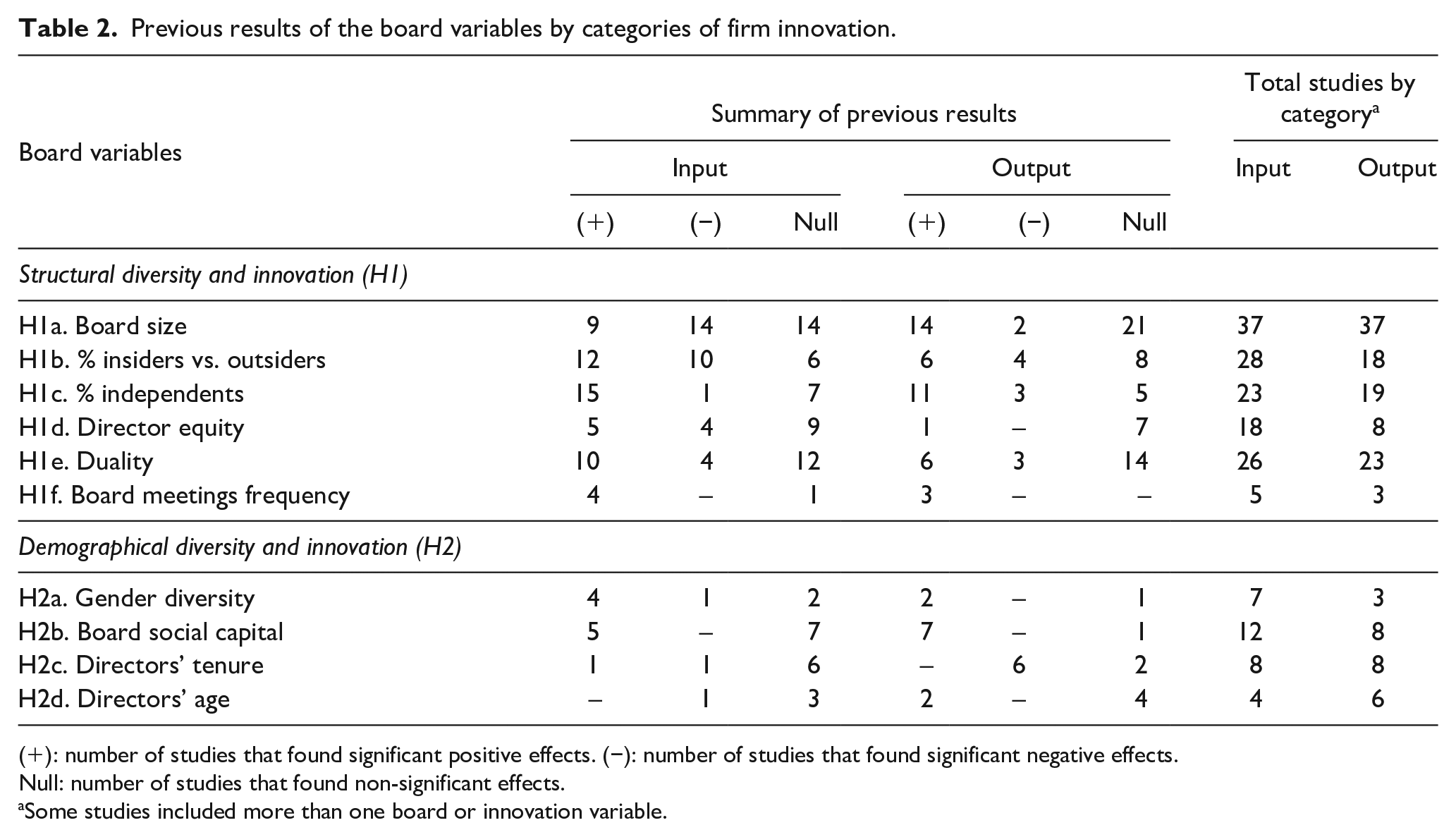

Therefore, given the existence of contradictory theoretical arguments and that empirical evidence linking board structural diversity (size, composition, board equity, duality, and meetings) to firm innovation is not conclusive (see Table 2), the following hypothesis and sub-hypotheses are put forward:

Hypothesis 1: Board structural diversity affects firm innovation.

H1a: Board size affects firm innovation.

H1b: Percentage of outside directors affects firm innovation.

H1c: Percentage of independent directors affects firm innovation.

H1d: Directors’ equity affects firm innovation.

H1e: CEO duality affects firm innovation.

H1f: Board meeting frequency affects firm innovation.

Previous results of the board variables by categories of firm innovation.

(+): number of studies that found significant positive effects. (−): number of studies that found significant negative effects.

Null: number of studies that found non-significant effects.

Some studies included more than one board or innovation variable.

Board demographic diversity and firm innovation

Presence of women directors and firm innovation

Increasing empowerment of women in various areas of society has led to a larger percentage of women in the business world (Triana et al., 2019). In accordance with the theory of resources and capabilities (Barney, 1991) more diverse criteria in an organization enriches the way in which assertive decisions can be taken. One of the questions to ask is whether women tolerate financial risk more than men (Brooks et al., 2019). Another concern is whether there is a minimum number of women for generating a sufficiently strong critical mass for influencing strategic decisions (Torchia et al., 2011), as suggested by the critical mass theory (Kanter, 1977). In any case, the specific experiences and perspectives of women directors are considered to enrich board criteria. For example, given their affinity with market needs and consumer behavior, their presence may benefit the development of new ideas (Galia et al., 2015). Regarding the empirical evidence, Miller & Triana (2009) were the first to find a positive relationship between gender diversity on the board and expenditure on innovation. They are in line with Del Brío & Del Brío (2009) and with Mukarram et al. (2018) who also find a positive effect on firm innovation. However, in their research, Galia & Zenou (2012) conclude that there is a positive relationship between gender diversity and marketing innovation but a negative relation between gender diversity and product innovation. Other authors, however, do not find a significant relation between the presence of women on the board and innovation (Bianchi et al., 2012; Jiraporn et al., 2017; Whitler et al., 2018) and others like Rossi & Cebula (2015) find a negative relation. This suggests that it is likely that the number of women in boardrooms is not yet sufficient to influence board decisions, in line with the critical mass theory (Torchia et al., 2011).

Board social capital and firm innovation

Board social capital refers to the sum of actual and potential resources derived from directors’ relationship networks (Haynes & Hillman, 2010). Such resources come to the fore when directors also serve as board members or managers in other firms, generating interconnections between the firms that share board members (Chen et al., 2013). Such links are considered to allow firms to gain access to information on the environment, to know what the trends in the industry are, to find funding, and to negotiate agreements for cooperation with other firms in order to invest in R&D projects (Chen, 2014; Wincent et al., 2010), in line with resource dependence theory (Pfeffer & Salancik, 1978). This sharing of information plays an important role in the behavior and results of operations based on insider information (Goergen et al., 2019), especially in the case of key strategic decisions such as the level of investment in innovation for which the board is responsible (Helmers et al., 2017).

The resource-based theory (Barney, 1991) provides arguments relating to firms’ social capital when it mentions that synergies among the members of a team promote the development of new strategies in firms (Grant, 1991). For this reason, firms often hire outside directors on the basis of the resources and background they could bring to the firm. For example, they select business experts, scientists, bankers, and others who subsequently become links to other organizations and therefore with more resources (Ashwin et al., 2016). Similarly, Adams & Ferreira (2007) propose the friendly boards theory, whereby the promotion of information sharing by both directors who become “friendly” and the CEO can generate an optimum working environment of mutual cooperation. Fama & Jensen (1983) suggest that an indicator of the quality and reputation of directors as expert decision-makers are their links with multiple firms. Since these interconnected directors are more focused on looking after their own reputation, they are less susceptible to CEO manipulation. As a consequence, agency problems are reduced. Conversely, too many commitments may make board members too busy to supervise or advise effectively because of their time and energy limitations (Gu & Zhang, 2016).

Regarding the empirical evidence, several studies indicate that directors’ links with other firms may be an effective channel for knowledge and experience and may also promote partnerships with other organizations for joint innovation (Wincent et al., 2010, 2012). Previous studies also agree with these findings (Ashwin et al., 2016; Chen, 2014; De Cleyn & Braet, 2012; Helmers et al., 2017; Kang et al., 2018; Swift, 2018; Takahiro, 2015c). 3 Hernández-Lara & Gonzales-Bustos (2019) perform a detailed analysis to identify the effect of trading links (both inside and outside the industry) and social links (with women directors, outside, independent, and international directors) finding a positive effect on innovation for directors’ interconnections outside the industry and for independent directors. On the contrary, the effects of directors’ interconnections within the industry and of women directors are negative, and they found no significant effects for the interconnections of outside and international directors.

Directors’ tenure and firm innovation

Director tenure is another characteristic that prior literature relates to firm innovation. It can be considered that the longer a director remains on the board, the more likely they are to acquire more experience and knowledge on the firm’s performance (Lu et al., 2017). So, a long-standing member of the board may acquire the “friendly” characteristic described in the friendly boards theory (Adams & Ferreira, 2007), facilitating the fluid communication and advice that are needed for new projects. According to the theory of resources and capabilities (Barney, 1991; Grant, 1991; Mahoney & Pandian, 1992), the future of an organization may depend, among other things, on specific knowledge of the firm, its environment and its management, and such knowledge accumulates over the years and with the time spent on the board (Patro et al., 2018). The empirical evidence found by Wincent et al. (2009) concludes that board tenure is an important tool for managing R&D in firms that cooperate as it facilitates the management of investments in innovation, in accordance with the resource dependence theory.

However, from the point of view of agency theory (Fama, 1980), a long stay in the same organization will not necessarily improve knowledge of its reality (Somech & Drach-Zahavy, 2013). When directors spend a long time in an organization, they may lose their independence because they establish a close relationship with the CEO, become less effective when overseeing the alignment of managers’ and shareholders’ interests and encourage CEO entrenchment (Lu et al., 2017). In addition, long tenure may be associated with greater adherence to established norms and therefore directors may be more reluctant to change. This rigidity might be negative for R&D strategies (Bravo & Reguera-Alvarado, 2017). Along these lines, Jia (2016) and Héroux & Fortin (2016) find that firms with a larger proportion of outside directors who have been in their positions for a long time produce significantly fewer patents, and that such patents receive fewer citations.

Directors’ age and firm innovation

According to the theory of resources and capabilities (Barney, 1991; Grant, 1991; Mahoney & Pandian, 1992), directors’ age can be considered indicative of accumulated experience and knowledge. Older directors are likely to have added to their skills over the years and may also be able to create more lasting, sounder interconnections with other firms in the same environment than younger ones (Xu et al., 2018), in accordance with the resource dependence theory. Along the same lines, according to stewardship theory (Donaldson & Davis, 1991), older directors can be described as individuals who seek to be more efficient, ethical and reliable because this brings them greater utility and prestige for their careers than opportunistic behavior. Moreover, the upper-echelon theory proposes that observable, psychological characteristics such as age may be important determinants in directors’ strategic decisions, such as those on innovation and that a range of directors of different ages might provide different points of view. Older directors can offer the experience and knowledge they have acquired over the years, while younger ones can contribute creativity and less risk aversion (Hambrick & Mason, 1984).

Regarding empirical evidence, Galia & Zenou (2012) conclude that age diversity shows a positive relationship with product innovation and a negative one with organizational innovation. Subsequently, in another study, these same authors find similar results (Galia et al., 2015). It is likely that these negative effects are due to the lack of time available to older directors due to the accumulation of professional commitments (Gu & Zhang, 2016). However, other authors find no significant results when analyzing the influence of directors’ age on firm innovation (Bravo & Reguera-Alvarado, 2017; Faleye et al., 2017; Jia, 2016; Shaikh et al., 2018).

Given that the above arguments and previous empirical evidence (see Table 2) are inconclusive regarding the relationship of board demographic diversity (presence of women directors, board social capital, directors’ tenure, and directors’ age) with firm innovation, the following hypothesis and sub-hypotheses are proposed:

Hypothesis 2: Board demographic diversity affects firm innovation.

H2a: Presence of women directors affects firm innovation.

H2b: Board social capital affects firm innovation.

H2c: Directors’ tenure affects firm innovation.

H2d: Directors’ age affects firm innovation.

Methodology

Compilation of prior studies and criteria for inclusion

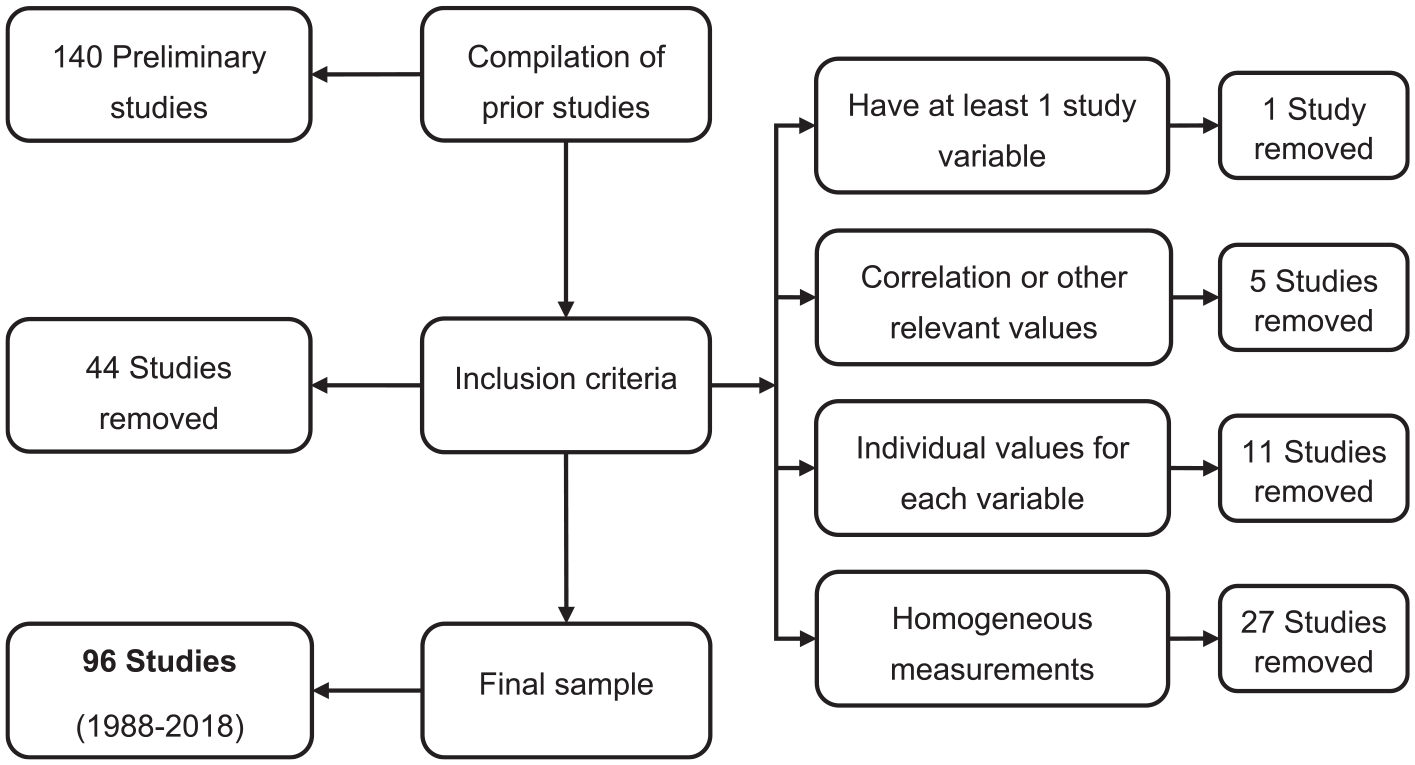

In order to compile the largest possible number of studies on the relation between board of directors and innovation, four strategies were adopted. First, articles covering prior reviews of the literature on governance and innovation were consulted (Asensio-López et al., 2019; Gonzales-Bustos & Hernández-Lara, 2016). Second, a search was made for related articles in five data bases, namely (1) ABI Inform, (2) ISI Web of Knowledge, (3) EBSCI, (4) ScienceDirect, and (5) Scopus, using the terms: “boards of directors,” “directors,” “corporate governance,” “innovation,” “R&D,” “new products,” “patents,” “citations,” “research,” “development,” “risk investments,” “firm performance” and possible combinations among them. Third, a manual search was performed in each issue of 17 of the most important journals on business management, corporate governance and innovation; most of them are included in JCR (Journal Citation Reports) to ensure that all the studies included meet the same quality standards. 4 Fourth, to avoid omitting important articles from other journals, the bibliographies of each of the articles found were explored in detail. The result was 140 initial documents that relate the board of directors with firm innovation.

After identifying the studies, the next step was to analyze them all to exclude any which did not contain the statistical information needed to estimate the effect size (Hedges & Olkin, 1985). This research includes most of the board characteristics considered in the corporate governance literature, specifically when explaining firm innovation, which can be comparable and for which it is feasible to obtain individualized data for each type of association with firm innovation (inputs and outputs). The following criteria were applied. First, the study had to contain at least one board of directors’ variable related to at least one innovation variable (1 study excluded). Second, the study had to include a correlation value or other relevant value (such as a non-standard regression coefficient) so that the necessary statistical calculations could be done (5 studies excluded). Third, the study had to show separately individual values for each board and innovation variables. Therefore, studies with values stemming from constructs, indices, or groups of variables were removed (11 studies excluded). Fourth, the study had to use homogeneous measurements for both their board and innovation variables so that they would be comparable, as described below regarding coding (27 studies excluded) (Figure 1).

Flow chart of the selection process.

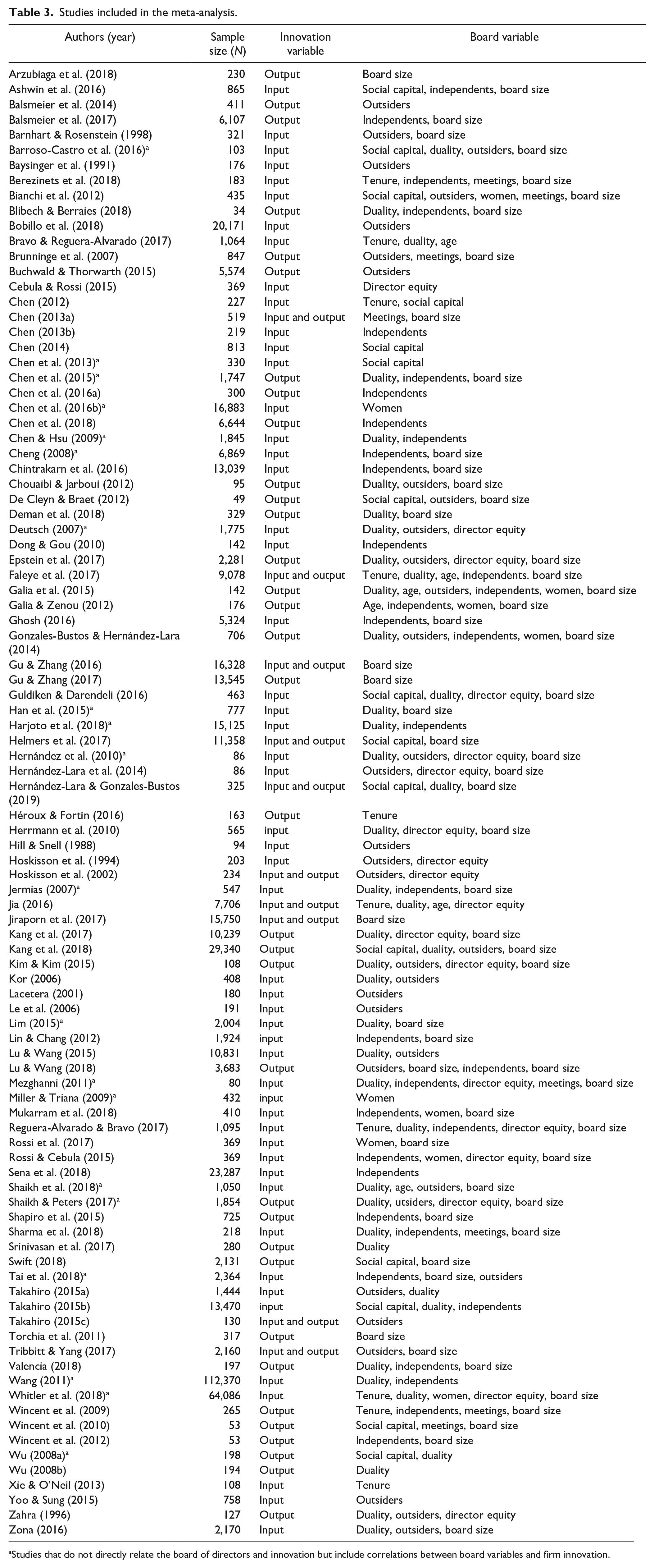

Summarizing, after applying the inclusion criteria to the 140 documents initially identified, 44 studies were ruled out because they did not satisfy the established inclusion criteria, giving us a final sample of 96 studies over a long period, 1988–2018, as shown in Table 3. We chose to start our period of study in 1988, when the first paper about board of directors and firm innovation by Hill & Snell (1988) was published in the Strategic Management Journal, and 30 years seemed to be a reasonable and sufficiently long period of time for the aim of our article.

Studies included in the meta-analysis.

Studies that do not directly relate the board of directors and innovation but include correlations between board variables and firm innovation.

Coding the studies and measuring the variables

The studies were coded according to how they measure each variable, trying to make them as homogeneous as possible to allow for comparison and to avoid losing robustness (Stone & Rosopa, 2017). As a result, in some cases, in addition to the main variables, moderating variables are included to distinguish between the different ways in which the variable in question is measured. So, for example, innovation measures were coded in two main categories. On the one hand, INPUTS is classified as any investment or expenditure made by the firm in R&D (Ashwin et al., 2016; Balsmeier et al., 2017) measured as a ratio or logarithm. On the other, OUTPUTS and its moderating variable OUTPUT_MEASURE are used to distinguish between the ways in which they are measured: TYPE_1 for the number of new products, TYPE_2 for patents, and TYPE_3 for patent citations (Balsmeier et al., 2017; Valencia, 2018).

Regarding board variables, to ensure homogeneity of measurements, only studies that were consistent with the following measurement schemes were included. SIZE measures the total number of directors (Ghosh, 2016; Jiraporn et al., 2017). For board composition, we consider, on one hand, the percentage of outside versus inside directors (OUTSIDERS) (Shaikh et al., 2018; Yoo & Sung, 2015), and on the other hand, the percentage of INDEPENDENTS, that is, the number of directors whose only link with the firm is as members of the board (Berezinets et al., 2018; Bravo & Reguera-Alvarado, 2017). DIRECTOR_EQUITY measures the number of shares held (equity) by the directors (Guldiken & Darendeli, 2016; Rossi & Cebula, 2015) and, in line with information in prior studies, SUBGR_EQUITY is considered as the moderating measurement variable for three groups: TYPE_1, where all directors hold shares, TYPE_2, only inside directors hold shares, and TYPE_3, only outside directors hold shares. DUALITY is a dummy variable, measured as 1 where there is duality and 0 otherwise (Kim & Kim, 2015; Kor, 2006). MEETINGS is the number of board meetings held in 1 year (Bianchi et al., 2012; Sharma et al., 2018). WOMEN measures the percentage of women directors (Miller & Triana, 2009; Rossi & Cebula, 2015). SOCIAL_CAPITAL is the number of positions that directors (interlocks) have on other boards (Ashwin et al., 2016; Swift, 2018). TENURE is the average number of years directors have been on the firm’s board (Bravo & Reguera-Alvarado, 2017; Whitler et al., 2018). AGE is the average age of directors (Faleye et al., 2017; Shaikh et al., 2018).

In addition, another two moderating variables for the results of the initial board-innovation relationship are considered. On one hand, the COUNTRY variable distinguishes between studies that focus on a single country (TYPE_1) and those in which the sample is from several countries (TYPE_2). On the other hand, the METHODOLOGY variable differentiates between studies using a cross-sectional (TYPE_1) or panel data methodology and, within the latter, whether the data are checked for possible endogeneity or not (TYPE_2 and TYPE_3, respectively).

Statistical method

The statistical methods used are the linear weighted models of the frame work of Hedges & Olkin (1985). The effect size index is Pearson’s correlation coefficient r, as in most primary studies relating to board characteristics and firm innovation, are reported as correlations. It is also the recommended index for the association between two quantitative variables (Borenstein, 2009; Botella & Sánchez-Meca, 2015; Rosnow et al., 2000; Sánchez-Meca et al., 2011). The inverse variance weighting has been chosen because under general conditions, as in this study, it provides an estimate of optimal efficiency or minimum variance (Stanley & Doucouliagos, 2012). In addition, Fisher’s transformation is used to normalize the distribution. The SPSS macros devised by Lipsey & Wilson (2001) are the program employed for most of the analyses. The funnel plots are obtained through the R package METAFOR (Viechtbauer, 2010).

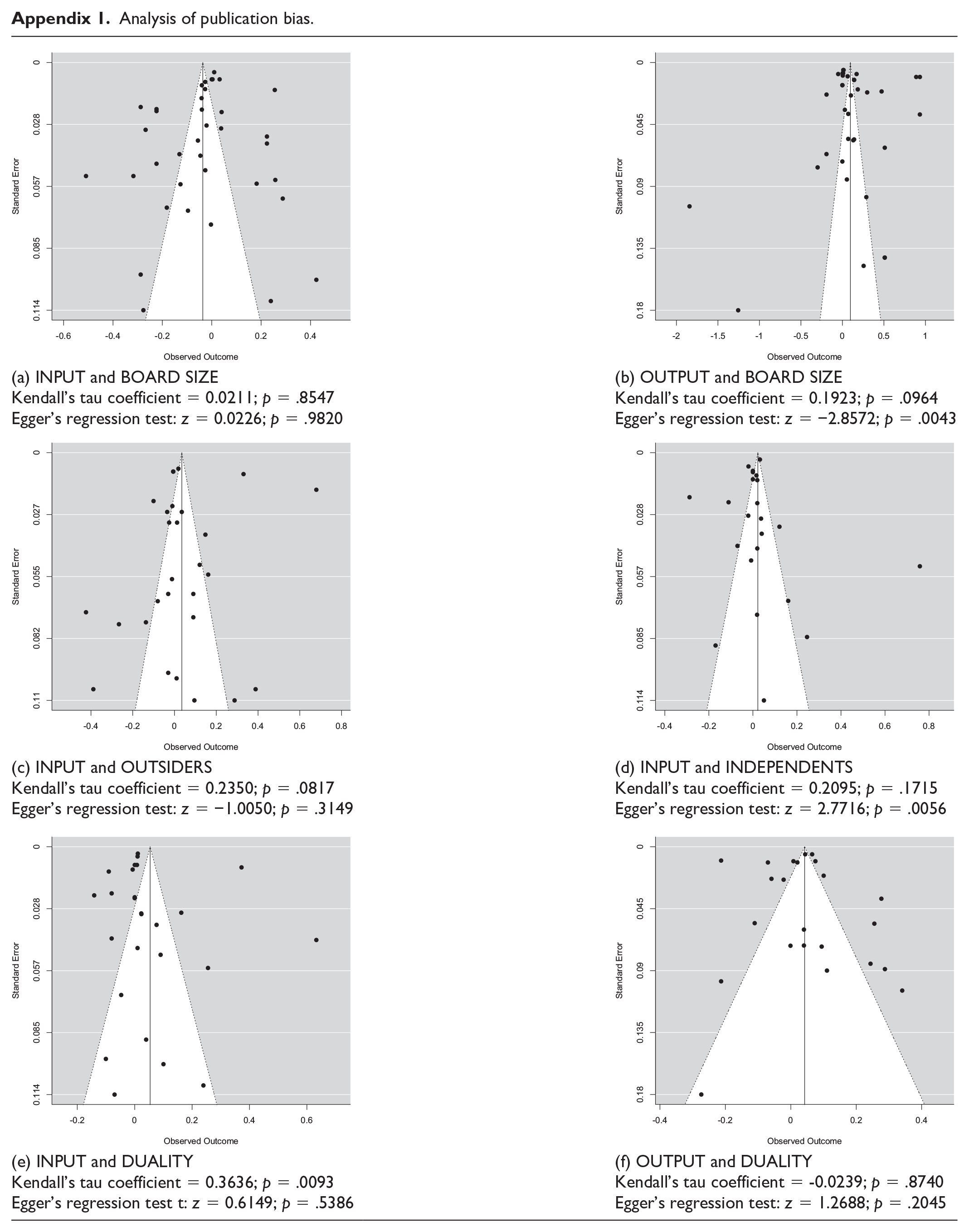

Random effect models are adjusted because they are more conservative than fixed-effect models and allow the results to be generalized beyond the specific set of studies analyzed (Borenstein et al., 2010). The heterogeneity of estimations of effect size is assessed using the Q statistic (Huedo-Medina et al., 2006). The association of moderating variables is analyzed following the steps suggested by Hedges & Olkin (1985). To check for possible publication bias, the R METAFOR package (Viechtbauer, 2010) is used. We do not calculate any failsafe N, as the steps are only used to conjecture whether it is credible for censorship to be so great that the effect sizes found to be significant would cease to be significant if the unpublished studies were recovered. They do not provide evidence of the presence of publication bias, so are not recommended for diagnosing it (e.g., Vevea et al., 2019). Therefore, the threat of publication bias is analyzed using several tests such as the Egger’s regression (Egger et al., 1997) and the Kendall’s correlation coefficient (Begg & Mazumdar, 1994), neither of which reveal significant asymmetry. The same can be deduced from visual inspection of the funnel plots (Egger et al., 1997; Sousa & Ribeiro, 2009) (Appendix 1, which only gives the funnel plots for variables in which k > 20, because in samples covering a small number of studies, visual inspection is very low). It can be concluded that the results of this meta-analysis are not threatened by publication bias. Although there are some significant results, the number is small, and they are often related to small groups of studies in which the tests are unstable.

Results

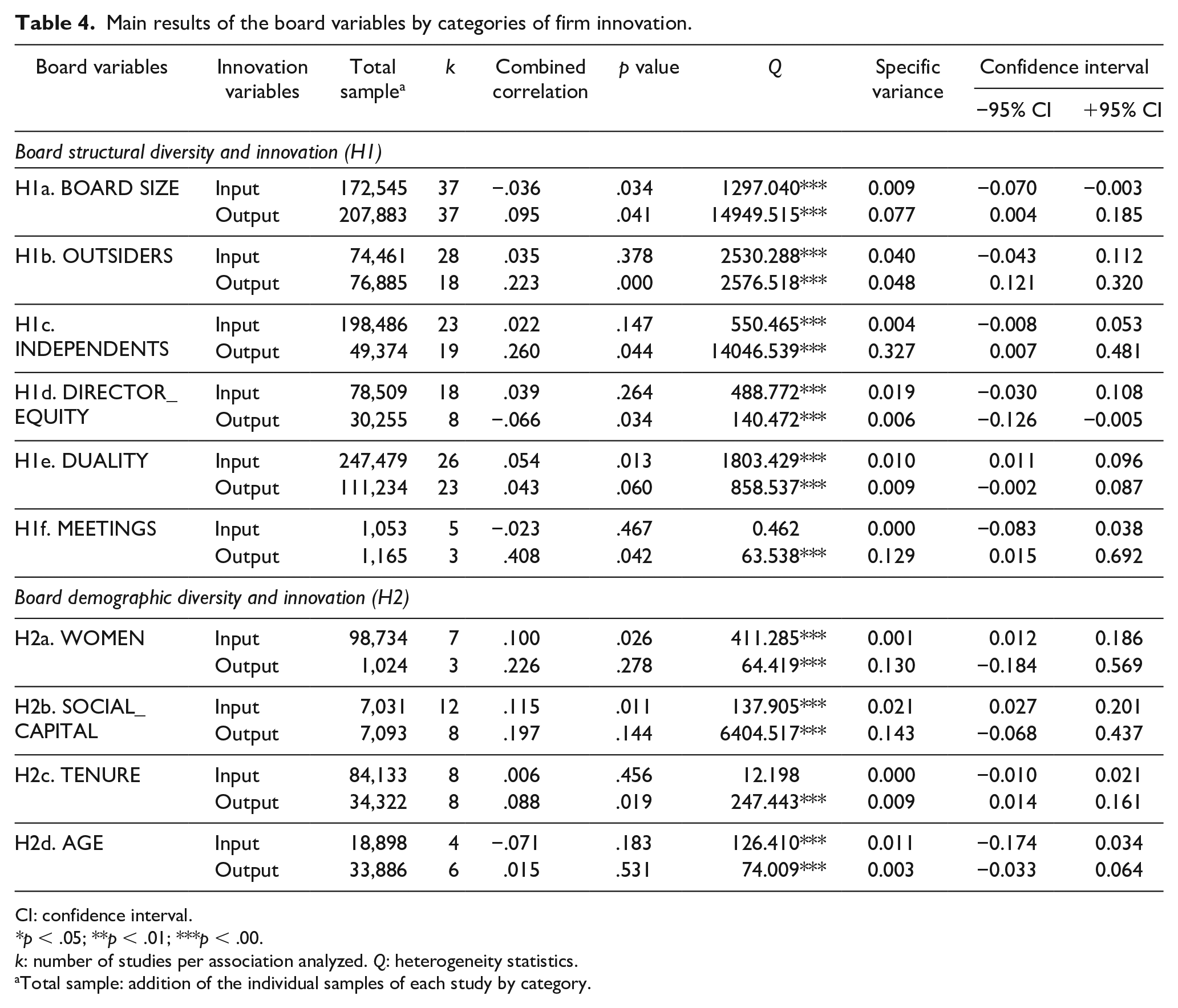

Table 4 shows the main results of the combined estimation of the size of the effect, r, for the two categories of board characteristics, separated by the way in which innovation (input or output) is measured, the Q heterogeneity statistic and the estimation of specific variance. Some of the variables show a statistically significant association with innovation, although the correlations are generally small. In some cases, moreover, the results must be interpreted with caution because of the small number of preliminary studies considered for each association.

Main results of the board variables by categories of firm innovation.

CI: confidence interval.

p < .05; **p < .01; ***p < .00.

k: number of studies per association analyzed. Q: heterogeneity statistics.

Total sample: addition of the individual samples of each study by category.

The results for board structural diversity and firm innovation are as follows: the combined estimation of the association between board SIZE and innovation (INPUT) is negative and significant (–.036; p = .034; k = 37), while the combined estimation of the association between board size and innovation (OUTPUT) is positive and significant (0.095; p = .041; k = 37). These results are in line with hypothesis 1a, which suggests an association between board size and innovation. The coefficient for the association between INPUT and OUTSIDERS is not significant, but the combined estimation for the association between the percentage of outside directors (OUTSIDERS) and innovation (OUTPUT) (0.223; p = .000; k = 18) is significant, partially supporting hypothesis 1b. Similarly, for the association between INPUT and INDEPENDENTS, the coefficient is not significant, but the combined estimation of the association between the presence of independent directors (INDEPENDENTS) and innovation (OUTPUT) is positive and significant (0.260; p = .044; k = 19), as suggested by hypothesis 1c. The results also show that there is a significant association between director equity (DIRECTOR_EQUITY) and innovation measured as OUTPUT (–0.066; p = .034; k = 8), but not when measured as inputs. This partly confirms hypothesis 1d. The combined estimation of the association between the presence of board duality (DUALITY) and innovation is positive and significant whether the latter is measured as INPUT (0.054; p = .013; k = 26) or as OUTPUT (0.043; p = .060; k = 23). This suggests that the presence of duality on the board is positively correlated with innovation (inputs and outputs), in line with hypothesis 1e. Finally, the combined estimation between the number of board meetings (MEETINGS) and innovation is only significant if the latter is measured as OUTPUT, when the result is positive and significant (0.408; p = .042; k = 3), thus partially supporting hypothesis 1f.

Based on the results obtained, it can be said that the board’s structural diversity is associated with firm innovation, supporting hyphothesis 1. In most cases, this association is positive for innovation outputs, except for directors’ equity ownership which has a negative association. As for innovation inputs, only duality is positively associated while board size is negatively associated. The disparate association of board size with inputs (negative) and outputs (positive) can possibly be explained by the fact that once the decision to invest in R&D has been taken, large board size may hinder both the contribution of new ideas for product creation and patents (outputs) and agreement on R&D investments (inputs). In addition, a large board may incur high expenses and agency costs, which may reduce the resources available for investments.

The results regarding board demographic diversity and firm innovation, are as follows: the combined estimation for the association between the presence of women on the board (WOMEN) and innovation (INPUT) is positive and significant (0.100; p = .026; k = 7), indicating that the presence of women directors is positively correlated with innovation (INPUT), but with OUTPUT it is not significant. So, hypothesis 2a is partially supported. The combined estimation for the association between directors’ SOCIAL_CAPITAL and innovation (INPUT) is positive and significant (0.115; p = .011; k = 12), but not for OUTPUT. So, hypothesis 2b is also partially supported. The combined estimation of the association between directors’ tenure (TENURE) and innovation (OUTPUT) is positive and significant (0.088; p = .019; k = 8), but this is not the case for inputs. So, hypothesis 2c is partly supported. Finally, the combined estimation of the association between directors’ AGE and innovation (INPUT and OUTPUT), no significant values are found, which goes against hypothesis 2d. Thus, although both the number of variables considered for board demographic diversity and the number of studies are smaller, the results seem to suggest a positive association between this type of board diversity and innovation inputs (percentage of women directors and board social capital). Conversely, directors’ tenure seems to be positively associated with outputs. Therefore, it can be stated that board demographic diversity is also associated with firm innovation, in accordance with hyphothesis 2.

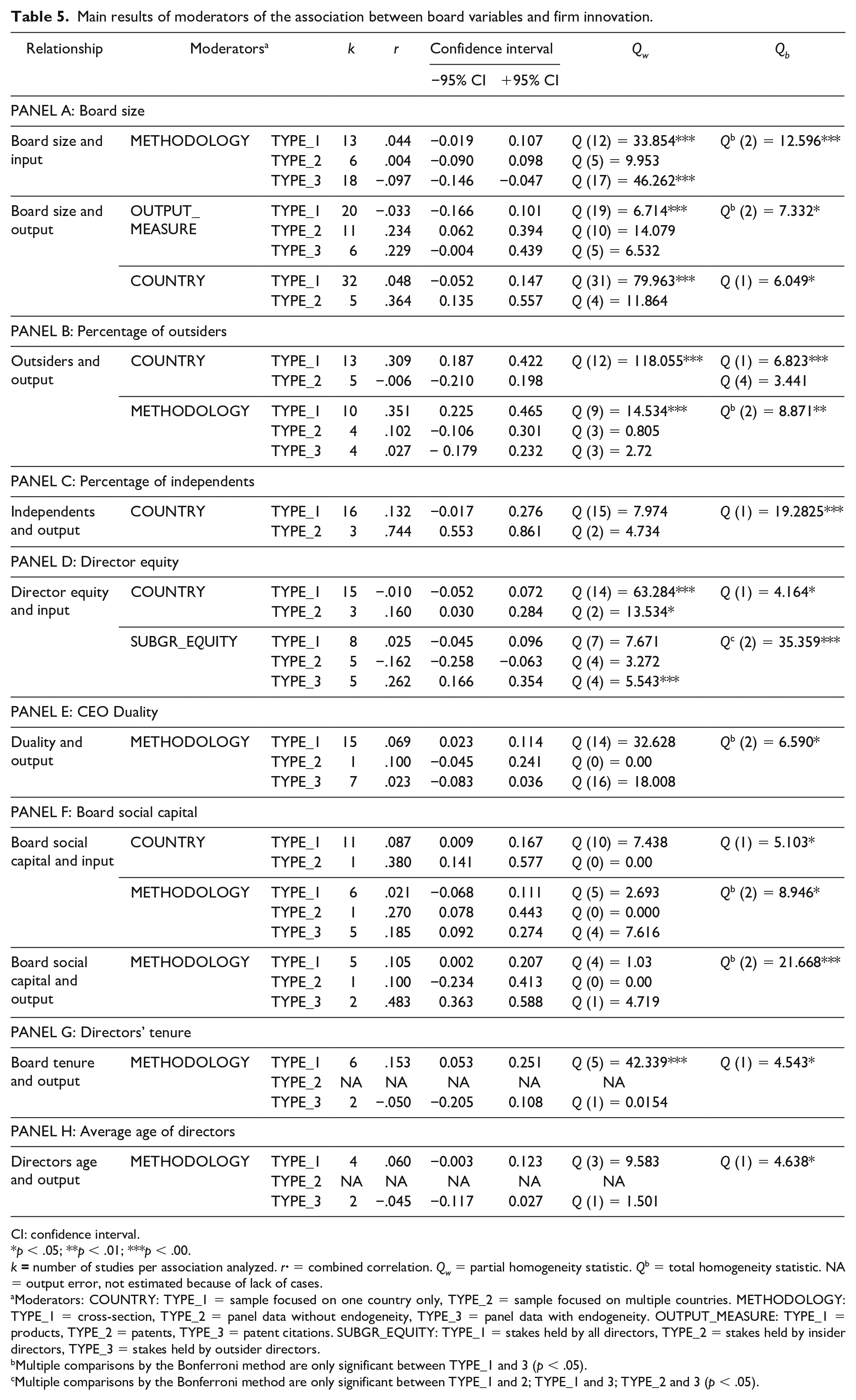

In summary, the results suggest that board variables are associated with firm innovation in different ways, most of them positive, depending on whether innovation is measured as inputs or outputs. In addition, Table 5 gives the most relevant and significant results of the analyses of the moderating variables, helping to explain these differences in each of the associations considered in the hypotheses between boards and innovation, separated by board features. These moderating variables correspond to COUNTRY (single country vs. several countries), METHODOLOGY (cross-sectional analysis, panel data methodology with or without endogenity), OUTPUT_MEASURE (new products, patents, and patent citations), and SUBGR_EQUITY (stakes held by all directors, insiders and outsiders, respectively). The main results are as follows: the moderating variable COUNTRY TYPE_1 (sample focusing on a single country) has a positive and significant effect in analysis of the association between OUTSIDERS and OUTPUT (Panel B). The COUNTRY TYPE_2 (multi-country sample), on the contrary, has a positive and significant effect for associations between both SIZE (Panel A) and INDEPENDENTS and OUTPUT (Panel C) and between DIRECTOR_EQUITY (Panel D) and SOCIAL_CAPITAL and INPUT (Panel F).

Main results of moderators of the association between board variables and firm innovation.

CI: confidence interval.

p < .05; **p < .01; ***p < .00.

k

Moderators: COUNTRY: TYPE_1 = sample focused on one country only, TYPE_2 = sample focused on multiple countries. METHODOLOGY: TYPE_1 = cross-section, TYPE_2 = panel data without endogeneity, TYPE_3 = panel data with endogeneity. OUTPUT_MEASURE: TYPE_1 = products, TYPE_2 = patents, TYPE_3 = patent citations. SUBGR_EQUITY: TYPE_1 = stakes held by all directors, TYPE_2 = stakes held by insider directors, TYPE_3 = stakes held by outsider directors.

Multiple comparisons by the Bonferroni method are only significant between TYPE_1 and 3 (p < .05).

Multiple comparisons by the Bonferroni method are only significant between TYPE_1 and 2; TYPE_1 and 3; TYPE_2 and 3 (p < .05).

For the METHODOLOGY moderating variable, TYPE_1 (cross-sectional) is positive and significant for the percentage of outside directors (OUTSIDERS) (Panel B), and directors’ TENURE (Panel G) and AGE when associated with OUTPUT (Panel H). The TYPE_2 METHODOLOGY variable (panel data without correction for endogeneity) is positive and significant for the association between SOCIAL_CAPITAL and INPUT (Panel F) and DUALITY and OUTPUT (Panel E). The TYPE_3 METHODOLOGY variable (panel data corrected for endogeneity) is negative and significant for board size (SIZE) and INPUT (Panel A) but positive for SOCIAL_CAPITAL and OUTPUT (Panel F). Moreover, a positive, significant moderation is found for OUTPUT_MEASURE TYPE_2 (patents) for SIZE (Panel A). Finally, regarding the SUBGR_EQUITY moderating variable of TYPE_3 (shares owned by outside directors), this is only positive and significant for the association between DIRECTOR_EQUITY and INPUT (Panel D).

So, related to moderators, the results suggest that they may affect the main associations. Whether the sample focuses on one or several countries may be relevant for associations between inputs and social capital and director equity, and for outputs and board size, percentage of outside and independent directors. In addition, the methodology employed (cross-sectional or panel data analysis) should be carefully chosen because this is another element that may affect the results (when inputs are associated with board size and social capital and outputs with proportion of outsiders, social capital, duality, tenure, and directors’ age). Finally, how the output dimension is measured seems to be less important as a moderator as it only affects one board-innovation association (board size).

Discussion and conclusion

The literature on corporate governance has considered the role of the board in firm innovation in several studies that analyze this link from several different points of view, but no consensus has yet been reached. Based on a novel methodology for this strand of research, we integrate previous research results into a meta-analytical study that covers a large number of board characteristics and firm innovation. In addition, board characteristics were divided into two categories according to their group or individual nature to better understand the role of the board in firm innovation. As expected, the findings of this meta-analysis suggest that firm innovation is associated with board structural diversity (board size, composition, director equity, duality, and board meeting frequency) and with board demographic diversity (percentage of women directors, board social capital, and directors’ tenure) but also that such effects vary depending on whether innovation is measured as inputs or outputs.

First, regarding board structural diversity, the results suggest that board size is positively associated with innovation outputs, especially patent generation, in accordance with the results found by Chen et al. (2015), De Cleyn & Braet (2012), and Wincent et al. (2012). These authors argue that a large board size might assist in reaching better decisions regarding new projects. This association is greater in samples with firms from different countries. However, board size is negatively associated with innovation efforts. This divergent association might be explained according to the resource based theory by the fact that a large board of directors may be a source of new ideas for product creation and patents (outputs) (De Cleyn & Braet, 2012) but may have difficulties in agreeing on what type of R&D investments to make (inputs) in line with agency theory (Blibech & Berraies, 2018; Sharma et al., 2018).

Regarding board composition, a positive association was found between the percentages of outsiders and of independent directors with innovation outputs. Although previous literature was not unanimous, this result is in line with those of other prior studies (Balsmeier et al., 2017; Jia, 2016; Lu & Wang, 2018; Sharma et al., 2018), which suggest that outside and independent directors may benefit innovation because their extensive knowledge of the environment enriches the board’s human capital. However, it is necessary to highlight other factors that may influence this association, such as the country of study. In the case of outside directors associated with outputs, this positive association is greater in single-country studies. But in the case of independent directors associated with outputs, this positive association is greater in studies of several countries.

However, inclusion of shares as compensation for directors seems to be negatively associated with innovation outputs, in line with Hoskisson et al. (2002). Participation in ownership of the firm’s shares may produce risk aversion in directors and cause them to limit their support for new ideas. Thus, according to our results, a negative association between directors’ equity and firm innovation seems to prevail. In addition, although previous literature was not conclusive regarding the existence of a significant relationship, our findings also indicate that duality is positive for innovation (inputs and outputs), in line with some previous studies (Chouaibi & Jarboui, 2012; Driver & Guedes, 2012; Sharma et al., 2018; Valencia, 2018). Hence, it is likely that thanks to knowledge of the company’s internal processes, the CEO-President will be able to manage decision-making better, especially decisions related to innovation, both to increase investments and to translate ideas into new products and patents. In addition, it is important to highlight that board meeting frequency has the highest level of positive correlation with innovation outputs, in line with most previous empirical findings, probably because meetings can be seen as a space where the exchange of ideas helps to generate new products and patents, in accordance with Brick & Chidambaran (2010).

Second, in what concerns to board demographic diversity, the presence of women on boards is likely to generate a greater level of diversity in boardrooms and thus to encourage investment in firm innovation. This result favors a positive effect of the presence of women directors on innovation, in line with the majority previous literature. Therefore, heterogeneity within groups can greatly increase information for the generation of new innovative projects (Miller & Triana, 2009). Similarly, directors’ social capital shows a positive association with inputs, especially when samples are based on several countries and panel data without controlling for endogeneity is the methodology used. This positive effect of social capital is aligned with most previous research which states that the diversity of directors’ ties can increase the firm’s opportunities to access financing or to participate in joint projects with other organizations (Ashwin et al., 2016; Chen, 2014; Swift, 2018).

The association between firm innovation and board tenure is only positive with outputs. Probably, long tenure in the same firm may increase directors’ experience and knowledge on the firm’s performance (Lu et al., 2017) and perhaps strengthens communication ties with the other members of the board. Although these findings differ from the predominant negative relationship found in previous research, the type of methodology employed may explain the divergences. The positive association between board tenure and outputs is stronger in cross-sectional studies. Finally, no significant associations are found between directors’ age and innovation. A possible explanation for this non-significant result could be the measurement of the age variable. Measuring age as an average maybe does not reflect the age diversity of directors but rather the age homogeneity within the board. A homogeneous board (in terms of age) is made up of individuals who shared similar values when they grew up and who are influenced by historical events during their formative years (Mahadeo et al., 2012), so is a group with common points of view. Therefore, if there is no measurement of age diversity, there is unlikely to be an association between age and firm innovation. It is, however, possible that the characteristics associated with each age group may offer support when making decisions (Kim & Lim, 2010). Thus, older board members might contribute with experiences, connections and financial resources, middle-aged board members with management skills and younger board members with new ideas (Mahadeo et al., 2012). Consequently, the synergy between this diversity of skills and knowledge may provide a beneficial environment for firm innovation (Kim & Lim, 2010; Xu et al., 2018).

As a whole, the results obtained in this study show that a positive association exists between the different board variables and firm innovation (inputs/outputs), except for board size and board equity. Therefore, the concept of the board as a governance body that fulfills an advisory and resourcing function seems to predominate. So, the innovation-related decision-making process may be enhanced because the board is composed of a diverse set of individuals with different backgrounds and capabilities. This diversity of board attributes (structural and demographic) may affect both R&D investment and innovation outputs. Our findings thus are in line with the theoretical approach of a positive nature that emphasizes the importance of creating efficient work teams with human talent with a range of characteristics, skills, and abilities that benefit the firm. From this perspective, based on several theories that can be considered complementary such as the resources and capabilities theory (Barney, 1991), the resource dependence theory (Pfeffer & Salancik, 1978), the board capital theory (Hillman & Dalziel, 2003) or the friendly board theory (Adams & Ferreira, 2007), the board’s role is to complement and improve the decision-making process. In addition, in line with another theoretical approach, of a negative nature, based on agency theory (Jensen & Meckling, 1976) the board’s role is to control and monitor, with the aim of minimizing possible managerial opportunistic behavior. This guarantees the effectiveness of strategies such as innovation. Our results suggest that these theoretical arguments are closely related to board size associated with inputs and directors’ equity with outputs.

This research makes several contributions from a new perspective. First, unlike the qualitative analysis of previous theoretical and systematic reviews, our research goes a step further by using meta-analysis to integrate the previous results in a quantitative way based on statistical techniques. As far as we know, it is the first meta-analysis to study in greater depth the specific relationship between the board of directors and firm innovation with a broad review of the literature in a single study. For this purpose, we delved into each of the most studied board characteristics, grouping them in two categories (board structural and demographic diversity), adopting different approaches and considering different theories. We made comparisons with previous empirical evidence to provide a broader perspective on the board’s role in firm innovation.

Second, we point out the importance of dimensions of innovation (inputs and outputs) for future research because in some cases, results differ depending on the measure of innovation used. Findings suggest that the key to this divergence depends on the nature and requirements of the inputs and outputs of innovation. R&D investments (inputs) require in-depth knowledge of the firm, access to financial resources, risk tolerance, a conciliatory attitude, and the possibility of alliances with other firms (Liang et al., 2013). For new products and patents (outputs), market knowledge, project management, creativity, new ideas are required as well as access to knowledge about new technologies, new production techniques that favor knowledge creation, and so on (Hernández-Lara & Gonzales-Bustos, 2019). Third, we show that the relationship between the board and innovation is moderated by the presence of other factors, such as the context of the sample analyzed, and the methodology employed. These aspects should therefore be considered in future research in this field.

In addition, our results have important practical implications, offering several guidelines to firms for acting on aspects related to this internal control mechanism; for example, firms should be aware that the board of directors is a determinant of their innovation activities. Thus, selecting the most suitable directors or determining the characteristics of the board should be seen to be important if the firm’s aim is to promote innovation. Several board characteristics are more positively associated with innovation, but the firm must decide if what it wishes is to promote R&D strategies or to generate new products and patents. Firms should consider that the presence of outside and independent directors may expand the board’s vision, generating new ideas for the development of new products and patents according to market requirements. Along the same line, they should be aware that the frequency of board meetings can enhance the development of new products, patents, and patent citations. Therefore, it is important for managers to promote dialogue and information exchanges that will allow the identification of new market needs that can be satisfied with innovative solutions. Related to innovation inputs, both the directors’ social capital and the presence of female directors can encourage investment in innovation. However, managers must consider that a large board size may be detrimental to investment in innovation. In general, innovation can benefit from a sufficiently diverse, balanced board including women and external and independent members who can exert effective oversight, provide social capital to generate links inside and outside firms and share their criteria and knowledge in board meetings in order to generate new ideas and encourage innovation. Our findings suggest that a firm is most innovative when it finds the right balance between monitoring and consulting inside the boardroom. Finally, as a research implication of this paper, it can be stated that studies focusing on innovation management should include variables related to board characteristics, especially if they use output measures of innovation.

Regarding the limitations of this study, although meta-analysis is a useful methodology among new researchers, unfortunately it does not allow the inclusion of previous qualitative research, such as case studies that could enrich our understanding of the board role. Concerning the results obtained in the analysis, even if they are statistically significant, they should be considered with caution because in some cases, the number of preliminary studies is limited. In addition, the inclusion criteria used to analyze variables relating to board characteristics and innovation may well omit important conclusions from other similar prior studies (44 articles were excluded during the selection process), mainly because the heterogeneous definitions and measures of the variables used by their authors make it impossible to carry out quantitative comparisons in a meta-analysis. For example, board’s human capital is often used as a variable for analyzing directors’ specific characteristics such as their educational level or profession, among others, and process innovation is another important aspect of firm innovation. But there is no single criterion for measuring these variables, so it is difficult to analyze them and establish comparisons through meta-analysis. Something similar occurs with board diversity, which is sometimes measured as an index and does not present individual values for comparison. These variables were therefore not included in this study but could be included in future research.