Abstract

This study examines how the co-location of firms within the same industry enhances their information environments. We hypothesize that benefits arise from two effects: the industry peer effect, involving intra-industry information spillovers, and the geographic peer effect, related to shared local economic conditions with nearby non-industry peers. Our analysis evaluates how these effects, both separately and jointly, impact analysts’ forecast properties and stock price informativeness regarding future earnings. We find that the industry peer effect is negatively related to forecast dispersion and positively related to forecast accuracy, while the geographic peer effect shows no significant correlation. In addition, stock price informativeness about future earnings is positively associated with the industry peer effect but not with the geographic peer effect. We also find that greater proximity to industry or local peers enables analysts to incorporate more private (relative to public) information into their earnings forecasts, thereby enhancing the firm’s information environment.

Introduction

A substantial body of research across the disciplines of accounting, economics, and finance has extensively explored the positive externalities associated with the co-location of peer firms, commonly referred to as “agglomeration” or “geographic clustering” effects (Ellison et al., 2010; Engelberg et al., 2018; Jennings et al., 2017). Theoretically, the impact of industry co-location can be conceptualized as a combination of the “industry peer effect” and the “geographical peer effect,” where the benefits derived from business similarity and geographic proximity manifest simultaneously (Matsumoto et al., 2022). As a result of these dual benefits, co-located industry peers frequently share similar economic fundamentals due to common industry-level and geography-specific factors. This similarity in operational factors facilitates isomorphic financial reporting practices through dense formal and informal networks, thereby enhancing the uniformity of reporting behaviors (De Franco et al., 2019; Diaz et al., 2017; Francis et al., 2024).

In terms of the informational benefits of industry co-location, Jennings et al. (2017) focus on the information environment of financial analysts, arguing that a firm’s proximity to its industry peers reduces the costs of information acquisition and processing for individual analysts. Supporting this argument, Jennings et al. (2017) present evidence of a positive relationship between geographic proximity and the quality of an analyst’s information environment. Specifically, they find that the average geographic distance between the firms in an analyst’s coverage portfolio and other industry peers (i.e., an inverse measure of proximity) is negatively correlated with both the number of firms in the portfolio and the accuracy of the analyst’s earnings forecasts. However, it remains unclear whether these documented informational benefits are driven by intra-industry information transfer facilitated by geographic proximity (i.e., the industry peer effect) or by shared local fundamentals among co-located firms, regardless of whether they belong to the same industry (i.e., the geographic peer effect). This article aims to disentangle the industry and geographic peer effects in the context of these documented informational benefits to analysts’ information environments by separately considering the influence of co-located firms from different industries as opposed to co-located industry peers.

In addition, this article seeks to extend the work of Jennings et al. (2017) by investigating whether the informational benefits are driven by more efficient processing of public information or by enhanced acquisition of private information. Given that capital market regulations frequently emphasize the public disclosure of material information by firms, a significant body of literature has examined the relative importance of public versus private information for various stakeholders (e.g., Chen & Jiang, 2006; Frankel & Li, 2004; Vega, 2006). In particular, the distribution of public and private information among financial information users is considered a crucial aspect of a firm’s overall information environment (Barron et al., 1998; Easley & O’Hara, 2004). However, Jennings et al. (2017) do not address this issue. This article aims to fill that gap by employing the analytical framework proposed by Barron et al. (1998) to represent an analyst’s information environment.

To empirically investigate these issues, we develop a measure of the industry (geographic) peer effect based on the number of peer firms in the same (different) industry located within a 100-mile radius of a firm’s headquarters. We first examine the association between our measure of the industry peer effect (Proximity_Numi,t) and the properties of aggregate analyst forecasts that signal the quality of a firm’s information environment. After controlling for several factors that may influence the properties of analyst forecasts, we find that our proxy for the industry peer effect is positively associated with the accuracy of consensus analyst forecasts and negatively associated with the dispersion of individual analysts’ forecasts, consistent with the findings of Jennings et al. (2017). However, we do not find any significant association between our proxy for the geographic peer effect (Proximity_Num_Diffi,t) and the properties of analyst forecasts, despite well-documented geographic peer effects from non-industry peer firms in the vicinity on a firm’s financial policies, such as dividend payouts (Cave & Lancheros, 2024), corporate social responsibility (CSR) engagements (C. Li & Wang, 2022), and voluntary disclosure of management earnings forecasts (Matsumoto et al., 2022). Furthermore, we find that our proxy for the industry peer effect remains positively associated with forecast accuracy and negatively associated with forecast dispersion, even after controlling for the proxy for geographic peer effect. Collectively, these results suggest that geographic proximity among industry peers, rather than the mere agglomeration of local peers from different industries, is the primary source of information benefits accrued to financial analysts.

As further evidence of industry and geographic peer effects on the corporate information environment, we examine whether both co-location measures are positively associated with the informativeness of stock prices with respect to future earnings, measured by the future earnings response coefficient (FERC). To the extent that a firm’s information environment influences how value-relevant information about the firm’s prospects is reflected in stock prices (Ayers & Freeman, 2003; Collins et al., 1987; Lundholm & Myers, 2002), we hypothesize that a firm’s stock prices will be more informative about future earnings when the information benefits from either the industry peer effect or the geographic peer effect contribute to an improved information environment. Consistent with our analyst forecast test results, we find that a firm’s FERC increases incrementally with our proxy for the industry peer effect, even after controlling for the geographic peer effect.

Next, we extend our analysis to consider the relative importance of common versus private information in explaining the information benefits of industry co-location. Financial analysts typically gather and analyze both public information (such as conference calls and regulatory filings with the Securities and Exchange Commission [SEC], including 10-Qs and 10-Ks) and private information (obtained through their own research and site visits) to formulate their earnings forecasts. Although the use of common and private information by analysts is not directly observable, Barron et al. (1998) analytically demonstrate that the accuracy of consensus forecasts primarily reflects errors in public information, while forecast dispersion is driven by idiosyncratic (private) information. Moreover, Barron et al. (1998) propose that the relative importance of common versus private information embedded in consensus forecasts can be measured by the ratio of the covariance of analysts’ beliefs to the overall uncertainty across analysts. Therefore, we re-estimate our empirical models using this ratio (denoted as ρi, t) as the dependent variable and find that both co-location measures are negatively associated with ρi, t. This result indicates that greater proximity to industry or local peers enables analysts to incorporate more private (relative to public) information into their earnings forecasts, leading to an improvement in the firm’s information environment.

This study builds on the work of Jennings et al. (2017) and aims to contribute to the literature on peer effects in the information environment. From the perspective of an individual analyst, Jennings et al. (2017) demonstrate that the co-location of industry peer firms affects analysts’ information acquisition costs for the firms in their coverage portfolios. However, Leary and Roberts (2014) note that identifying peer effects is empirically challenging due to the reflection problem (Manski, 1993). In the context of the influence of industry co-location on a firm’s information environment, the confluence of industry and geographic peer effects may exacerbate the reflection problem. While Jennings et al. (2017) do not explicitly address this issue, our study attempts to disentangle the two peer effects by employing separate measures for industry and geographic peer effects.

Furthermore, this study seeks to identify how the informational benefits derived from industry co-location can enhance a firm’s information environment. Prior research indicates that consensus analyst forecasts may reflect common information shared by the financial analyst community, but the collective opinion of analysts may “overweight the information common to all analysts, thereby failing to fully exploit their private information” (Kim et al., 2001, pp. 329–330). However, Jennings et al. (2017) do not address whether the informational benefits from industry co-location result from the acquisition of more private information or the more efficient processing of public information. To address this gap, our study examines how the information benefits from industry co-location affect the relative importance of public versus private information in enhancing a firm’s information environment.

This study also provides new insights into the findings of Shroff et al. (2017). While Shroff et al. (2017) argue that the information environment of industry peers affects the cost of capital for other firms within the same industry, they do not explicitly consider the effect of geographic proximity among industry peers. Our findings suggest that not only the presence of industry peers but also their geographic proximity can create information benefits that enhance a firm’s information environment. A concurrent study by Matsumoto et al. (2022) also focuses on the impact of geographic peers on a firm’s management forecast decisions, which is a form of voluntary disclosure. While Matsumoto et al. (2022) examine how a firm internalizes the effects of co-location by altering its disclosure behavior, our study focuses on the information externalities from industry co-location that accrue to external users of the firm’s financial information.

This study also complements and extends the existing literature on the information advantages provided by geographic proximity between corporations and users of their financial information, such as analysts and investors (e.g., Coval & Moskowitz, 1999; El Ghoul et al., 2013; Malloy, 2005; O’Brien & Tan, 2015). While prior research typically focuses on the benefits derived from proximity to a single firm—often referred to as the “distance effect”—our study shifts the focus to proximity to a cluster of industry peers. Specifically, we examine the informational spillover effects resulting from the co-location of firms within the same industry, an effect commonly described as “agglomeration.”

Moreover, this study contributes to the broader literature on Marshallian spatial externalities, which investigate the spillover effects generated by the geographic clustering of industry peers. While existing studies often focus on how geographic clustering influences a firm’s strategic decisions—such as location choices (Alcácer & Chung, 2014), acquisition strategies (McCann et al., 2016), and the formation and management of R&D alliances (Ryu et al., 2018)—we provide evidence that industry co-location also generates significant informational spillovers. These spillovers benefit external users of firms’ financial information, including analysts and equity investors, by enhancing the overall information environment.

The remainder of this article is organized as follows: section “Related literature and hypotheses development” reviews the related literature on the effects of industry and geographic peers and develops our hypotheses. Section “Variable measurements and research design” outlines the methodology employed to test these hypotheses. In section “Results,” we present the results of our hypothesis testing. Finally, section “Conclusion” offers our conclusions and discusses the implications of our findings.

Related literature and hypotheses development

Spillover effects of industry and geographic peer information

The spatial co-location of firms within the same industry has long been recognized as a source of competitive advantage, reducing transaction costs and fostering innovation through the exchange of ideas (Marshall, 1920). When firms within the same industry are geographically clustered, their supply chains often become more efficient, labor markets for specialized skills more accessible, and knowledge spillovers more likely, enhancing the overall economic environment of the cluster (Dougal et al., 2015; Ellison et al., 2010). Consequently, the co-location of industry peers is expected to facilitate information spillovers, thereby influencing the behavior of firms through shared industry connections and local market conditions.

Existing research has documented the influence of industry peer information on various firm behaviors, such as investment decisions (Beatty et al., 2013; Durnev & Mangen, 2009; V. Li, 2016), financial policy (Leary & Roberts, 2014), voluntary disclosure (Lin et al., 2018; Seo, 2021), and earnings management (Kedia et al., 2015). For instance, Shroff et al. (2017) argue that peer information can enhance a firm’s information environment, particularly when firm-specific information is limited. Firms in the same industry often face similar economic conditions related to demand, input costs, supply chains, and regulations, which can lead to mimicking or benchmarking behaviors. As more firms within an industry publicly disclose information, the collective understanding of the industry-wide economic outlook improves, thereby enhancing investment efficiency (Badertscher, Shroff, and White, 2013).

In contrast, another body of literature explores the influence of geographic peers on firm behaviors. Geographic proximity, even among firms from different industries, can lead to co-movements in stock returns due to shared exposure to local economic shocks (Pirinsky & Wang, 2006). In addition, firms in close geographic proximity often exhibit similarities in their financial reporting practices influenced by local norms and practices (De Franco et al., 2019). Geographic peer effects have been shown to affect investment decisions (Dougal et al., 2015), stock option compensation (Kedia & Rajgopal, 2009), and voluntary disclosure practices (Matsumoto et al., 2022).

Despite these findings, it remains unclear whether the spillover effects of industry or geographic peer information are more influential in shaping a firm’s broader information environment, particularly in relation to analysts’ forecasts and stock price informativeness.

Industry peer effects

Industry peer effects arise from the commonalities that firms within the same industry share, such as similar demand patterns, regulatory environments, and risk profiles. These shared characteristics can lead to information spillovers, where the actions or disclosures of one firm provide valuable insights into the economic conditions or future prospects of other firms within the same industry.

Previous research has established that industry peer effects influence a wide range of corporate decisions. For instance, firms are more likely to make similar investment decisions when they observe their industry peers doing so, a phenomenon often attributed to social learning or isomorphic pressures (Beatty et al., 2013; Durnev & Mangen, 2009). Industry peer information can also impact financial policies, such as capital structure decisions and payout policies (Leary & Roberts, 2014). Moreover, firms often align their voluntary disclosure practices with those of their industry peers, potentially to mitigate information asymmetry or avoid standing out negatively (Lin et al., 2018; Seo, 2021).

One of the key mechanisms through which industry peer effects influence firm behavior is the enhancement of the information environment. When firms in an industry disclose more information, it reduces uncertainty and improves the accuracy of forecasts made by financial analysts. Badertscher et al. (2013) argue that the presence of multiple firms disclosing information within the same industry leads to a more complete understanding of industry-wide conditions, thereby increasing investment efficiency.

Geographic peer effects

Geographic peer effects, by contrast, arise from the spatial co-location of firms, which can lead to shared exposure to local economic conditions, regulatory environments, and labor markets. Geographic proximity can create externalities that benefit all firms within the region, such as access to a skilled labor force, improved supply chain logistics, and the exchange of tacit knowledge through informal networks.

The impact of geographic peer effects on firm behavior has been well-documented in the literature. For example, Kedia and Rajgopal (2009) find that firms are more likely to adopt broad-based stock option compensation when other firms in the same metropolitan statistical area (MSA) do so. Similarly, Dougal et al. (2015) show that firms’ investment decisions are sensitive to those of their geographic peers, even when these peers operate in different industries. Geographic peer effects also influence accounting practices, as evidenced by the higher financial statement comparability among co-located firms (De Franco et al., 2019). Matsumoto et al. (2022) further demonstrate that a firm’s voluntary disclosure practices are affected by the disclosure behavior of its local peers.

Hypotheses development

Information environment and analyst forecasts

A firm’s information environment encompasses the production and dissemination of both public and private information about its current and future prospects. This information is generated by various stakeholders, including related firms, investors, and information intermediaries such as financial analysts. The co-location of industry peer firms can influence analysts’ information environments in two primary ways: (1) by lowering the cost of information acquisition and facilitating the processing of firm-specific information, and (2) by leveraging information spillover from both industry-specific and geography-specific factors.

Prior research has shown that a firm’s public disclosure, such as earnings announcements, can trigger information spillover effects on other economically connected firms within the same industry (Foster, 1981; J. Han & Wild, 1990). These spillover effects are not limited to explicit disclosures but can also arise from the mere presence of industry peers, which can increase the coverage of financial analysts and improve the dissemination of value-relevant information (Badertscher et al., 2013). In addition, co-located firms are more likely to share the same local economic fundamentals, which can lead to geographic information transfer and improve the information environment of the region as a whole (Dougal et al., 2015; Parsons et al., 2020).

Given the potential for both industry and geographic peer effects to influence a firm’s information environment, it is crucial to examine which effect has a stronger impact on analysts’ forecasts. Analysts often face cognitive burdens when deciphering industry-specific and firm-specific information. However, greater exposure to common industry-wide and geographic economic conditions among co-located industry peers may reduce biases and dissipate idiosyncratic factors in forming analyst forecasts (Hui et al., 2016). In light of this, we propose the following competing hypotheses:

Hypothesis 1a (H1a). A firm’s industry peer effect is negatively associated with the dispersion of analysts’ earnings forecasts.

Hypothesis 1b (H1b). A firm’s geographic peer effect is negatively associated with the dispersion of analysts’ earnings forecasts.

Hypothesis 2a (H2a). A firm’s industry peer effect is positively associated with the accuracy of analysts’ earnings forecasts.

Hypothesis 2b (H2b). A firm’s geographic peer effect is positively associated with the accuracy of analysts’ earnings forecasts.

Stock price informativeness and FERC

When the information environment is enhanced, value-relevant information about a firm’s prospects is more effectively disseminated to investors, allowing the stock price to incorporate more information about future earnings (Collins et al., 1994; Kothari & Sloan, 1992). The FERC measures the extent to which current stock prices reflect future earnings information.

J.-H. Choi et al. (2019) examine the effect of financial statement comparability on stock price informativeness and find that when firms’ accounting practices are more comparable to those of their peers, it becomes easier for financial statement users to evaluate economic performance, leading to higher FERC. Engelberg et al. (2018) show that industry-wide factors are more rapidly incorporated into stock prices when firms are co-located with their industry peers.

To the extent that a firm’s information environment is improved due to its industry co-location, prior empirical findings suggest that the spatial concentration of industry peers should lead to a higher FERC. Thus, we extend our competing hypotheses to test the influence of industry and geographic peer effects on FERC:

Hypothesis 3a (H3a). A firm’s industry peer effect is positively associated with its FERC.

Hypothesis 3b (H3b). A firm’s geographic peer effect is positively associated with its FERC.

Public versus private information

The spatial concentration of firms within the same industry can reduce the costs associated with acquiring and processing public and private information about a firm’s current and future prospects (Jennings et al., 2017). Financial analysts, who specialize in particular industries, rely on both public information (e.g., financial disclosures, industry reports) and private information (e.g., insights gained from direct communication with management or site visits) (Bradshaw et al., 2017). The co-location of industry peers can influence the relative importance of these two types of information in a firm’s information environment.

On one hand, the concentration of industry peers in a specific geographic area can lead to a higher volume of publicly available information, as firms may align their disclosure practices with those of their peers to meet market expectations or regulatory requirements. This increased availability of public information can reduce the uncertainty faced by analysts, leading to more accurate forecasts and potentially diminishing the need for reliance on private information.

When analysts cover firms that are co-located, shared industry connections and local market conditions can reduce information heterogeneity across firms, thereby lowering the cognitive burden of processing available public information. If this is the case, the role of public information in firm valuation may increase due to industry co-location.

On the other hand, geographic proximity might also facilitate the acquisition of private information. Analysts covering firms in the same location can more easily access management, conduct site visits, and build local networks. This could lead to an increased reliance on private, “soft” information, particularly in settings where public information is less informative or where analysts can gain a competitive edge through their private insights.

Given these dynamics, it is theoretically ambiguous whether industry or geographic co-location increases the reliance on public or private information. Acknowledging the complexity and potential countervailing forces at play, we propose Hypothesis 4 in the null form to allow for an empirical investigation:

Hypothesis 4 (H4). The relative importance of public versus private information in improving a firm’s information environment is not significantly affected by the presence of industry or geographic peer effects.

Variable measurements and research design

Measures of co-location: industry peer effect and geographic peer effect

Prior studies on the role of geographic proximity often assume a firm’s headquarters as the source of financial information and measure the distance between the headquarters and the location of financial information users such as analysts, fund managers, and investors as a proxy for the proximity (e.g., Coval & Moskowitz, 1999; Jennings et al., 2017; O’Brien & Tan, 2015). Distinct from these studies focusing on the dyadic relationship between a firm and its financial information users, we are interested in the information effect of the geographic clustering of industry peers. Therefore, to capture the density of the co-location of industry peers, we first estimate the distance from a firm’s headquarters to all other firms in the same industry as defined by the Global Industry Classification Standard (GICS) code. 1 Then, we count the number of firms in the same industry located within 100 miles of the firm i’s headquarter location (by ZIP code) in year t as a proxy for industry peer effect, which we label Proximity_Numi,t. As industry peer firms are more clustered within 100 miles, we consider that the firm is more closely located to its industry peers.

To develop a new measure of geographic peer effect, we also count the number of non-industry peer firms (from different industries) located within 100 miles of the firm i’s headquarter location in year t, which we label Proximity_Num_Diffi,t. Considering that the effect of industry co-location can be confounded with the geographic peer effect affecting a firm’s financial reporting behavior (Matsumoto et al., 2022), we include both Proximity_Numi,t and Proximity_Num_Diffi,t in the models separately and jointly to compare the influence of industry peer effect and geographic peer effect. After estimating these industry co-location measures, we standardize them to take values between .01 and 1 by ranking them into percentiles and dividing the ranks by 100: R_Proximity_Num and R_Proximity_Num_Diff. Standardization further helps interpret the coefficients, diminishes outliers’ influence, and decreases the effects of skewness in the proximity variables.

Regression models

Model for the (industry/geographic) peer effects on analysts’ forecast properties

In the first part of this study, we examine how firms’ industry co-location influences the properties of financial analyst forecasts as a group, such as forecast dispersion and consensus forecast accuracy. We predict that analysts’ earnings forecast dispersion (accuracy) is negatively (positively) associated with either industry peer effect or geographic peer effect.

To examine our prediction on the relationship between analysts’ forecast quality and the industry co-location, we estimate the following regression model (Subscripts i and t, which represent the firm and fiscal year, respectively)

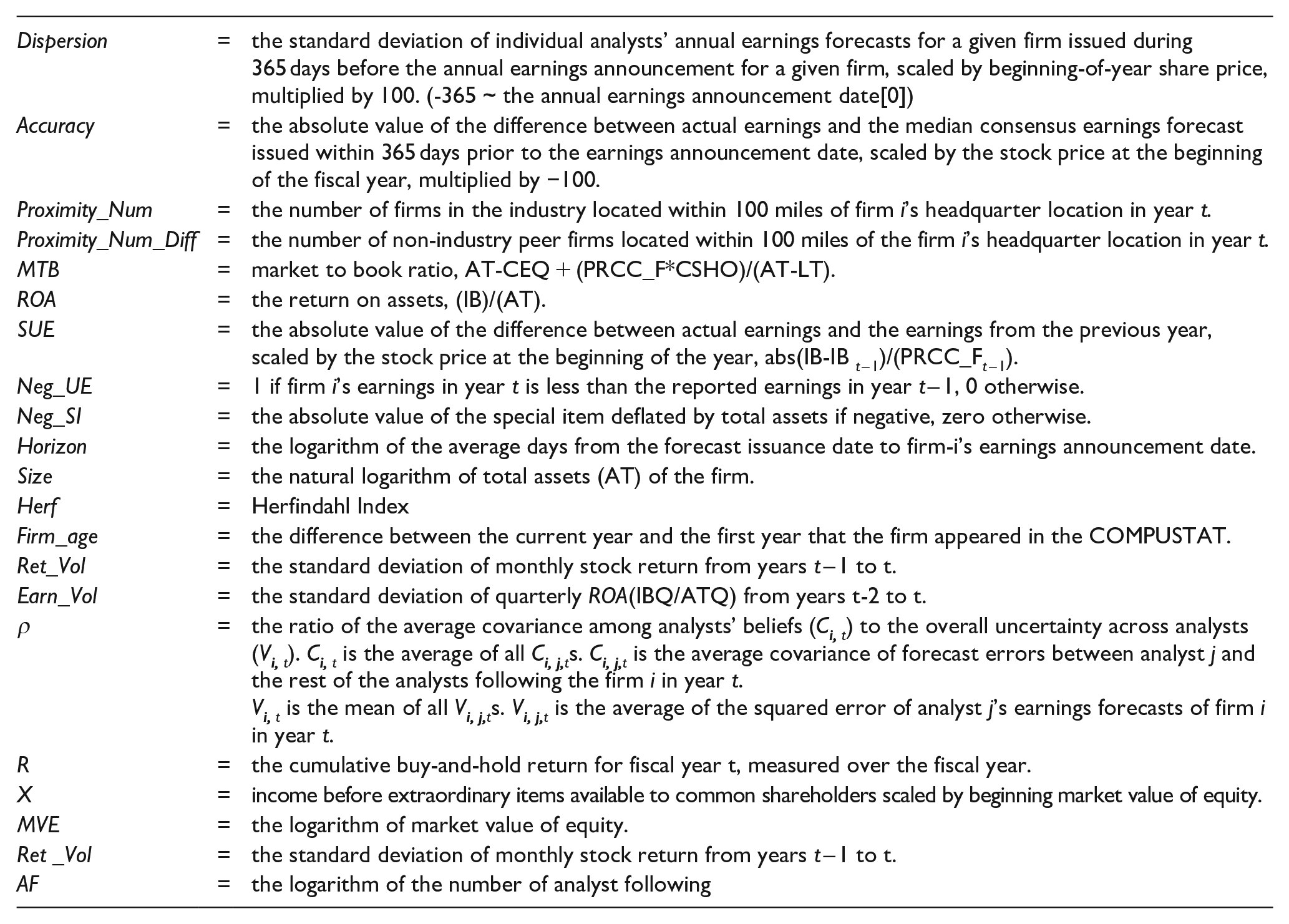

In equation (1), the dependent variable is either analysts’ forecast dispersion (Dispersion) or analysts’ consensus forecast accuracy (Accuracy) of firm i in year t. We measure the dispersion of analysts’ forecasts as the standard deviation of individual analysts’ annual earnings forecasts for a given firm issued 365 days before the annual earnings announcement for a given firm, scaled by beginning-of-year share price, multiplied by 100. To assess analyst consensus forecast accuracy, we use the absolute value of the difference between actual earnings and the median consensus earnings forecast issued within 365 days prior to the earnings announcement date, scaled by the stock price at the beginning of the fiscal year, multiplied by −100. As the absolute forecast error is multiplied by −100, higher values of Accuracy imply more accurate forecasts. Following Payne and Thomas (2003), we use I/B/E/S unadjusted files to avoid rounding errors in adjusted earnings forecasts to obtain analyst forecast dispersion (Dispersion) and forecast accuracy (Accuracy).

In equation (1), our main variable of interest is Proximity. Proximity represents the number of industry peer firms within 100 miles (Proximity_Numi, t) and the number of non-industry peer firms within 100 miles (Proximity_Num_Diffi,t). In estimating the equation, we use the rank of Proximity variables, R_Proximity_Numi,t, and R_Proximity_Num_Diffi,t. We expect the coefficient of R_Proximity_Numi,t to be negative (positive) because we predict that a firm’s closeness to industry peer firms is negatively (positively) associated with analysts’ forecast dispersion (accuracy). Likewise, we expect that the coefficient of R_Proximity_Num_Diffi,t is negatively (positively) associated with analysts’ forecast dispersion (accuracy) to the extent that geographic peer effect operates independently from industry peer effect to improve a firm’s information environment.

We include several control variables that could be associated with analysts’ forecast metrics following prior literature. We include the absolute value of firm i’s unexpected earnings in year t, the difference between actual earnings and the earnings from the previous year, scaled by the stock price at the beginning of the year (SUE). Firms with greater variability are more difficult to forecast (e.g., Kross et al., 1990; Lang & Lundholm, 1996). Earnings with more transitory components should also be more difficult to forecast (Heflin et al., 2003). Neg UE equals one if firm i’s earnings in year t are less than the reported earnings in year t − 1, zero otherwise. Neg_SI equals the absolute value of the special item deflated by total assets if negative, zero otherwise. Horizon is calculated as the logarithm of the average days from the forecast issuance date to firm-i’s earnings announcement date to control for differences in the information available to analysts at the time of their forecasts. The literature shows that the forecast horizon strongly affects accuracy (Brown & Mohd, 2003; Clement, 1999; Sinha et al., 1997).

Furthermore, we augment our empirical model by controlling for firm-specific variables, including (1) firm size (Size) to control for the information; (2) return on assets (ROA) to control for firm profitability; (3) market to book (MTB) to capture growth opportunities; (4) return volatility (Ret_Vol) and earnings volatility (Earn_Vol) to control for the difficulty in the forecasting environment; (5) firm age (Firm_Age) to control for differences in the difficulty of forecasting early-stage versus mature firms; and (6) the Herfindahl Index (HERF) to control for the effect of industry competition.

Also, we include industry-fixed effects to control for variation in geographical clustering across industries and year-fixed effects to control for unidentified time-variant fluctuations. Finally, we cluster the standard errors at the firm levels. The detailed definitions of the control variables used in this study are provided in Appendix 1.

Model for the (industry/geographic) peer effects on the informativeness of stock prices about future earnings

As another dimension of a firm’s overall information environment, we employ an investor’s perspective and examine whether industry co-location affects the informativeness of stock prices about future earnings. The corporate information environment affects the way average investors obtain and process information about the future earnings of a firm, and in turn, the degree to which stock prices impound the information about future earnings (Collins et al., 1987). Extending the view, we expect investors to predict future earnings better for firms geographically closer to industry peer firms and that these improved predictions will result in more information about future earnings reflected in the current stock price.

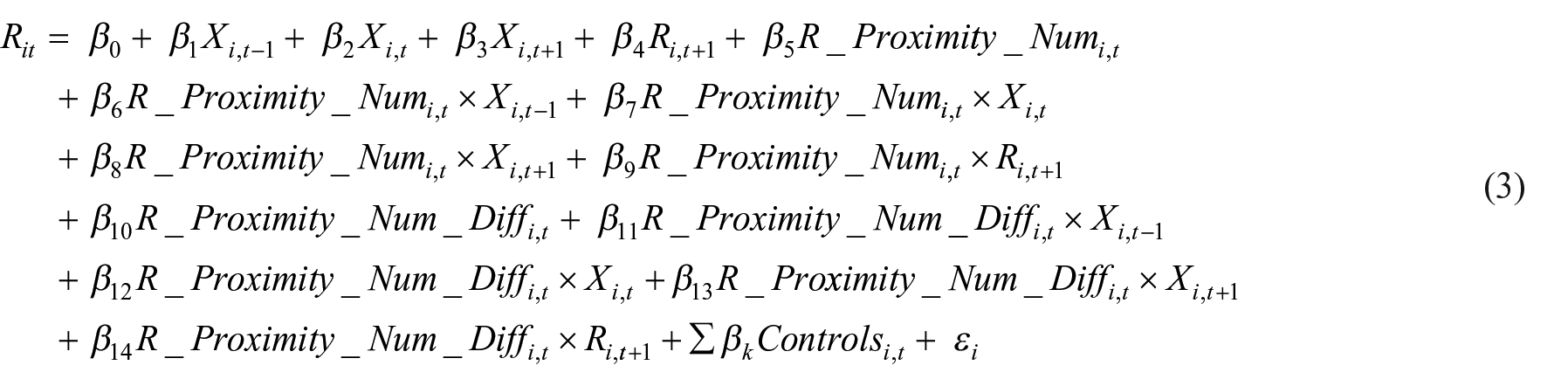

To examine whether industry peer effect or geographic peer effect increases the informativeness of stock price, we first estimate current period stock returns’ ability to reflect investors’ current period change in expectations about future earnings. Specifically, we measure the informativeness of stock price using the future earnings response coefficient (or FERC) that relates current stock returns (in year t) to future earnings (in year t + 1) (Ayers & Freeman, 2003; Piotroski & Roulstone, 2004). To estimate the capability of stock returns to reflect future earnings, we use the following baseline model

where, for firm i in year t, Rit is the cumulative buy-and-hold return for fiscal year t, measured over the fiscal year, and Xit is the income before extraordinary items available to common shareholders scaled by the beginning market value of equity.

The FERC model’s basic intuition is that unexpected earnings in the period, changes in expectations about future earnings, and random noise determine current returns. We include the levels of past earnings (Xit−1) and current earnings (Xit), respectively, because unexpected earnings are unobservable (Lundholm & Myers, 2002). This allows us to avoid assuming whether the earnings process follows a random walk versus a white noise process. We follow J.-H. Choi et al. (2019) and use the level of realized future earnings (Xit + 1) and future returns (Rit + 1) as the proxy of changes in future earnings expectations. 2 We add Rit + 1 to control for future events that affect Xit + 1 but could not be predicted at the end of year t (Collins et al., 1994; Lundholm & Myers, 2002). We isolate the expected component of future earnings by incorporating both Xit + 1 and Rit + 1 in the model. Following prior studies, we expect β2 (i.e., the ERC) and β3 (i.e., the FERC) to be positive.

To test our third hypotheses (H3a and H3b), we extend equation (2) as follows

If industry peer effect enhances the market’s ability to forecast future earnings, the coefficient on the interaction term, R_Proximity_Numi,t×Xi, t + 1, in equation (3), will be positive.

Similarly, if geographic peer effect stimulates greater incorporation future earnings in current stock price, the coefficient on the interaction term, R_Proximity_Num_Diffi, t×Xi, t + 1 will be positive.

To address concerns that ERCs and FERCs are affected by several firm characteristics, we also include analyst coverage (AF), firm size (MVE), market-to-book ratio (MTB), and return volatility (Ret_Vol12), along with their respective interactions with Xit−1, Xit, Xit + 1, and Rit + 1. Finally, we include industry- and year-fixed effects to control for unobservable, time-invariant industry-wide confounding factors and time-specific undue influence on the corporate information environment. In all tests on FERC, we use robust standard errors clustered by firm.

Sample and descriptive statistics

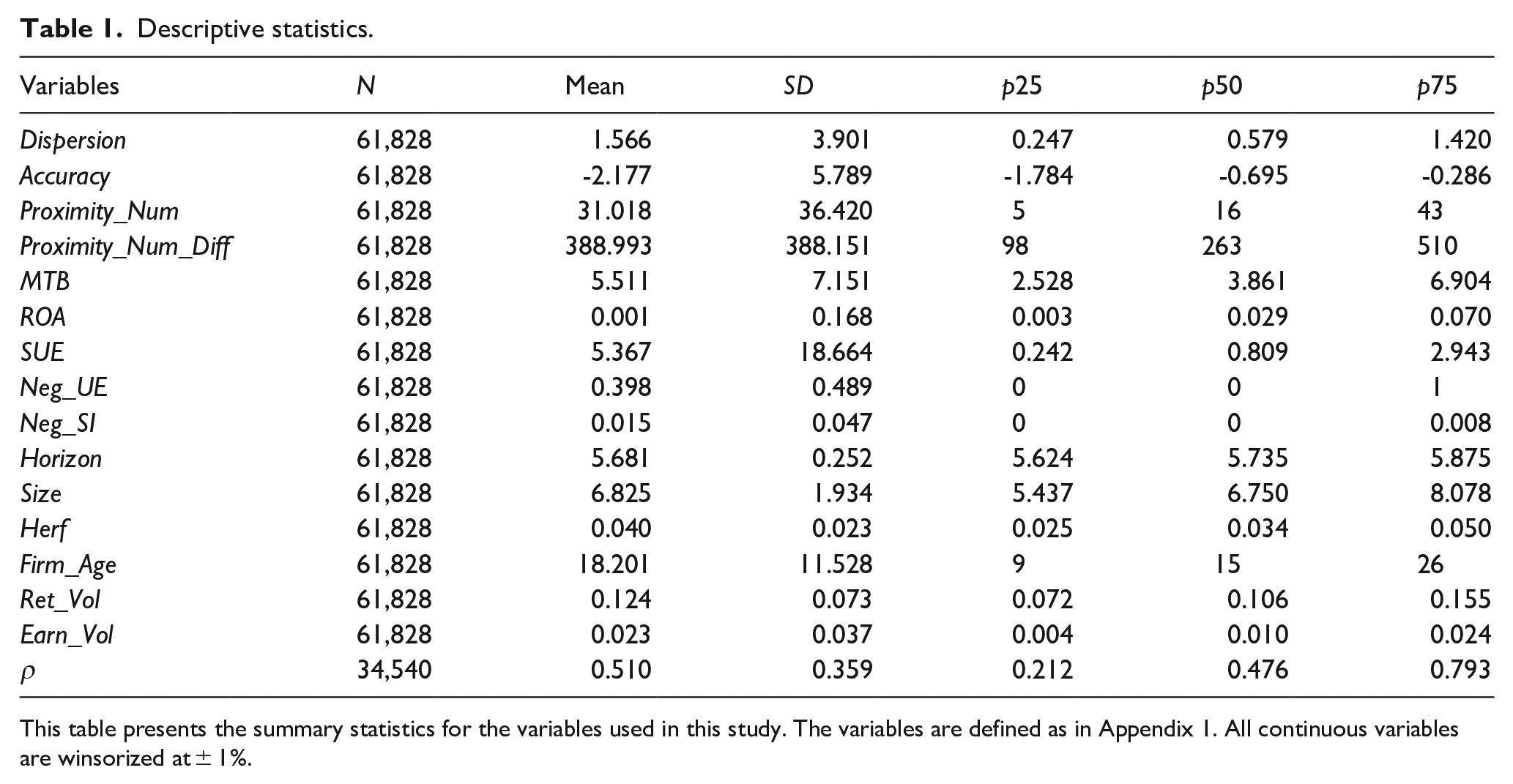

The sample includes all required data from COMPUSTAT, I/B/E/S, and CRSP from 1994 to 2018. After requiring the variables of interest and relevant control variables, the final sample includes 61,828 firm-year observations. 3 We require at least 20 observations per year for each Global Industry Classification Standard (GICS) code to ensure that firms have the opportunity to locate near other firms in the same industry. 4 Our sample for FERC test includes 54,025 firm-year observations after matching financial data with stock market data. Table 1 presents descriptive statistics for the primary sample.

Descriptive statistics.

This table presents the summary statistics for the variables used in this study. The variables are defined as in Appendix 1. All continuous variables are winsorized at ± 1%.

The average number of local industry peers within 100 miles is about 31 firms (median of 16 firms), whereas the average number of neighborhood firms not in the same industry is about 389 (median of 263 firms). The mean values for analyst forecast dispersion and forecast accuracy are 1.566 and −2.177, respectively. (As discussed in section “The effect of co-location on the informativeness of stock price on future earnings,” the original dispersion and accuracy estimates are multiplied by 100.) For ease of interpretation in the regression analysis, we rank the raw value of the industry co-location measures to take values between .01 and 1 by placing them in percentiles and dividing the percentile ranks by 100.

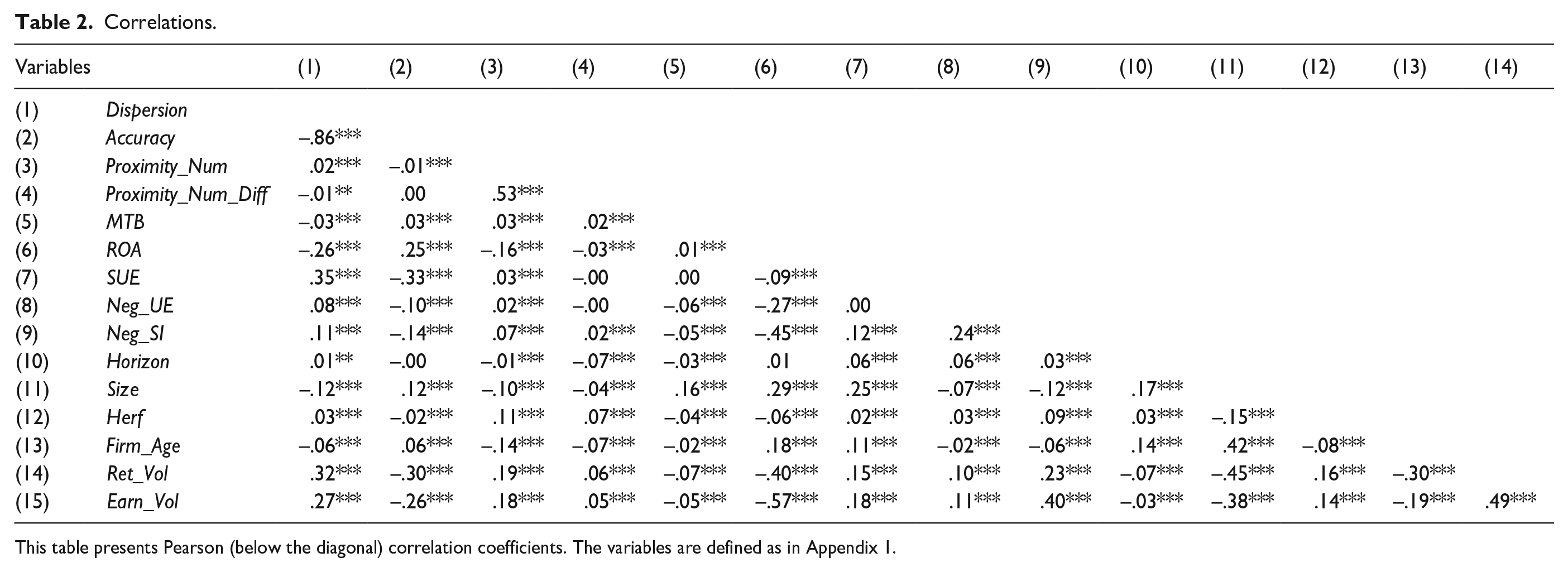

Table 2 presents Pearson correlation coefficients among the variables used in this study. Proximity measures, Proximity_Num and Proximity_Num_Diff, are positively and significantly correlated with each other. None of the other explanatory variables exhibit correlations sufficiently large to raise concerns over multicollinearity.

Correlations.

This table presents Pearson (below the diagonal) correlation coefficients. The variables are defined as in Appendix 1.

Results

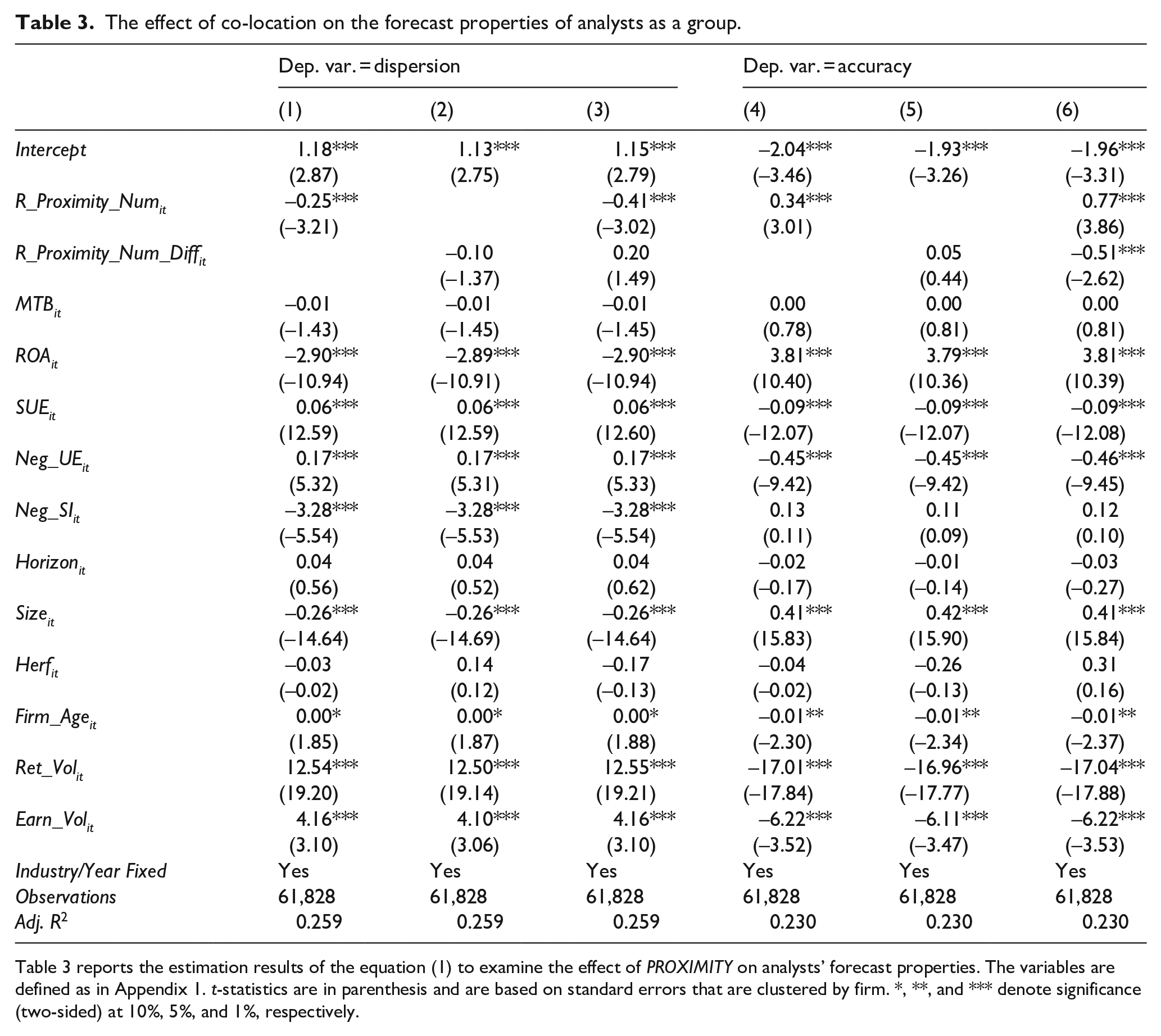

The effect of co-location on the forecast properties of analysts as a group

The first three columns of Table 3 present the results from estimating equation (1) when the dependent variable is analysts’ forecast dispersion, Dispersion. In column (1), a ranked Proximity variable, R_Proximity_Numit shows a negative and significant coefficient (β1 = −0.25, t-statistics = −3.21), suggesting that moving from the least to the greatest percentile of geographic proximity of industry peers reduces forecast dispersion by 0.25 or about 39% of the sample mean value. By contrast, when R_Proximity_Num_Diffit is used in column (2), we find that the statistical significance of the coefficient disappears, suggesting that the mere clustering of economically disconnected neighborhood firms may not create information benefits, thereby showing no meaningful reduction in analysts’ forecast dispersion. Importantly, when we include both R_Proximity_Numit and R_Proximity_Num_Diffit in column (3), we find the coefficient for our measure of industry co-location is negative and statistically significant, while the coefficient for the geographic peer effect proxy is insignificant. This suggests that the information benefits associated with industry co-location, as documented by Jennings et al. (2017), are driven more by a firm’s proximity to industry peers rather than by the simple clustering of firms from different industries.

The effect of co-location on the forecast properties of analysts as a group.

Table 3 reports the estimation results of the equation (1) to examine the effect of PROXIMITY on analysts’ forecast properties. The variables are defined as in Appendix 1. t-statistics are in parenthesis and are based on standard errors that are clustered by firm. *, **, and *** denote significance (two-sided) at 10%, 5%, and 1%, respectively.

The last three columns in Table 3 report the results from estimating equation (1) using analysts’ forecast accuracy, Accuracy, as the dependent variable. In column (4), a ranked Proximity variable, R_Proximity_Numit, shows a positive and significant coefficient (β1 = 0.34, t-statistic = 3.01), suggesting that about 15% of the sample mean of forecast accuracy may be increased when the geographic proximity of industry peers is changed from the least to the greatest percentile. Meanwhile, the coefficient of R_Proximity_Num_Diffit in column (5) remains insignificant, consistent with our result from using Dispersion as the dependent variable.

Interestingly, when we include both R_Proximity_Numit and R_Proximity_Num_Diffit in column (6), we find that the coefficient for our measure of industry co-location remains positive and statistically significant (β1 = 0.77, t-statistic = 3.86), while the coefficient for R_Proximity_Num_Diffit becomes negative and statistically significant (β2 = −0.51, t-statistic = −2.62). This indicates that a firm’s information environment may suffer when too many firms from different industries are clustered in a specific area, as this may impede the industry-specific information spillovers in the neighborhood.

Overall, the results in Table 3 indicate that industry co-location reduces forecast dispersion and increases forecast accuracy for the financial analysts as a group, supporting hypotheses H1a and H2a. These findings suggest that a firm’s information environment benefits from information spillovers associated with proximity to industry peers but not necessarily from the simple clustering of firms from different industries.

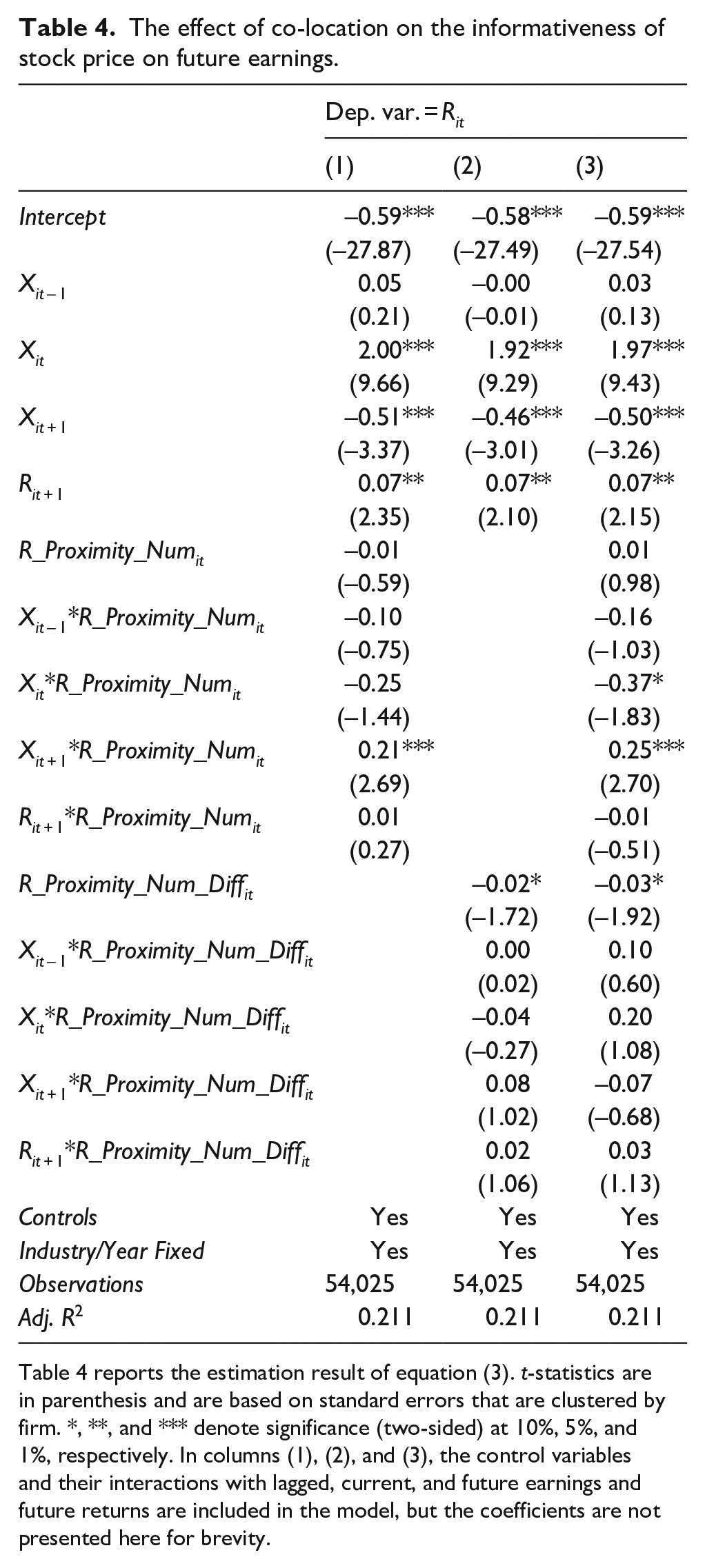

The effect of co-location on the informativeness of stock price on future earnings

The information benefits from industry co-location may influence how average investors acquire value-relevant information about a firm’s future performance and incorporate it into current stock prices (J.-H. Choi et al., 2019; Collins et al., 1994). To test this conjecture, we estimate equation (3) and present the results in Table 4. Column (1) shows the results from estimating equation (3) using R_Proximity_Numit as the sole proximity measure. As expected, the coefficient on X it (i.e., ERC) is positive and statistically significant (β2 = 2.00, t-statistic = 9.66). However, the coefficient on Xit + 1 (i.e., FERC) is negative and statistically significant (β3 = −0.51, t-statistic = −3.37). Although this result for FERC is inconsistent with Collins et al. (1994) and Lundholm and Myers (2002), we interpret it as indicating that the incorporation of future earnings into current stock price is conditional upon the efficient flow of value-relevant information, which partly depends on the informational benefits of industry co-location. Consistent with this view, the coefficient on the interaction term Xit + 1*R_Proximity_Numit, which represents the effect of industry co-location on a firm’s FERC, is positive and significant at the 1% level (β8 = 0.21, t-statistic = 2.69).

The effect of co-location on the informativeness of stock price on future earnings.

Table 4 reports the estimation result of equation (3). t-statistics are in parenthesis and are based on standard errors that are clustered by firm. *, **, and *** denote significance (two-sided) at 10%, 5%, and 1%, respectively. In columns (1), (2), and (3), the control variables and their interactions with lagged, current, and future earnings and future returns are included in the model, but the coefficients are not presented here for brevity.

Column (2) of Table 4 presents the results from estimating equation (3), using the proxy for geographic peer effects instead of industry co-location measure, to assess the impact of geographic proximity on a firm’s information environment as reflected by FERC. In this column, when the rank variable of geographic proximity, R_Proximity_Num_Diffit, is used, we find that the interaction term with future earnings, Xit + 1*R_Proximity_Num_Diffit is positive but statistically insignificant. This suggests that the incorporation of future earnings into stock prices does not benefit from the mere presence of a larger number of geographically proximate firms that do not share the same industry profile.

The results from considering both industry co-location effect and geographical peer effect are presented in column (3). When including both R_Proximity_Numit and R_Proximity_Num_Diffit in equation (3), we find that the coefficient for Xit + 1*R_Proximity_Numit is positive and statistically significant coefficient, while the coefficient for Xit + 1*R_Proximity_Num_Diffit remains insignificant. Overall, these results, as shown in Table 4, support our findings from the analyst forecast tests and suggest that industry co-location enhances investors’ ability to interpret financial statement information and better anticipate future firm performance, thereby improving the corporate information environment.

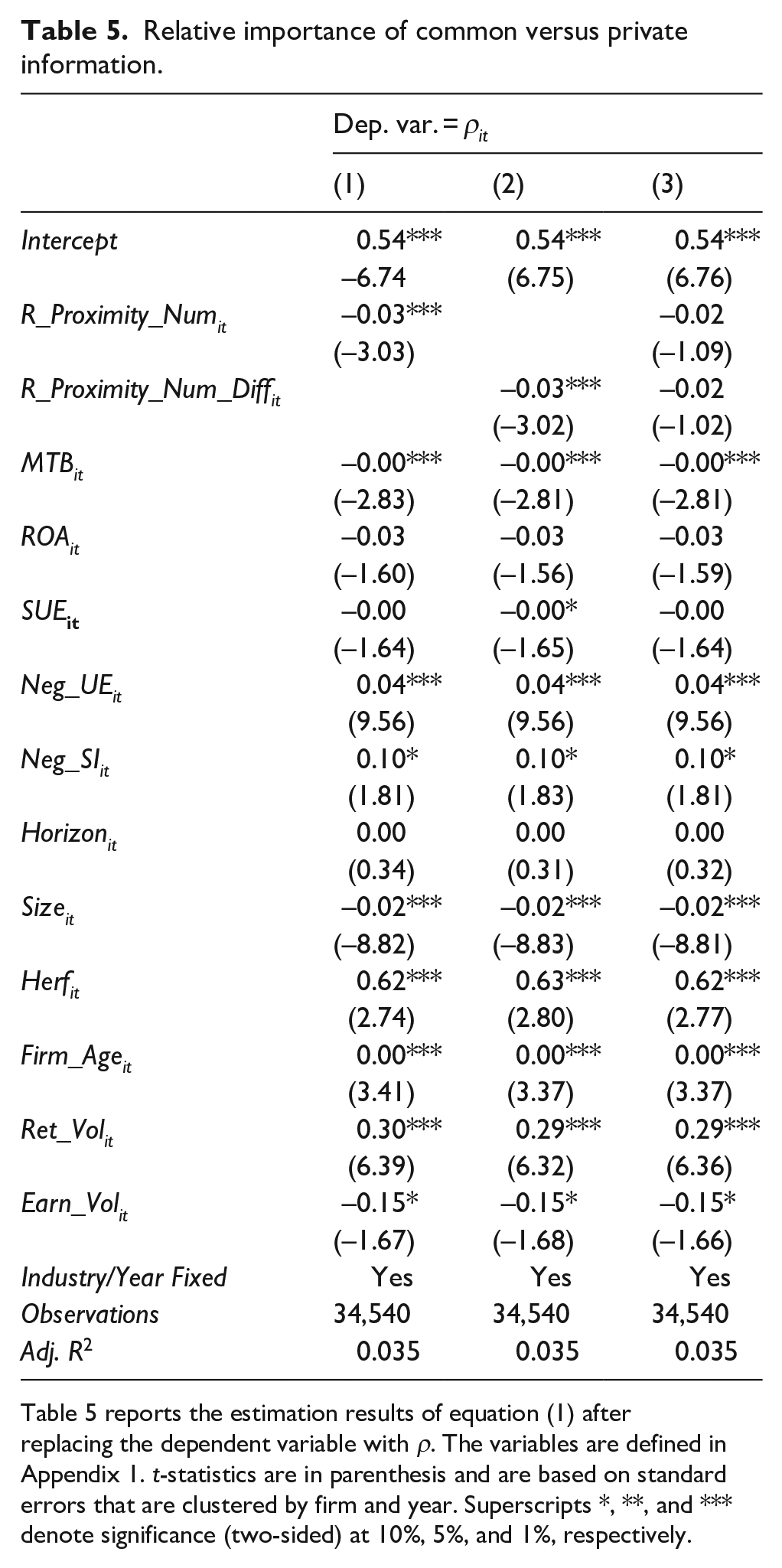

Relative importance of common versus private information

After showing that the information benefits accrued by individual analysts can be generalized to the broader corporate information environment—reflected in the forecast properties of analysts as a group and investors collectively—we proceed to investigate the source of these information benefits. Specifically, we examine the relative importance of common versus private information in explaining how geographic proximity of industry peers influences a firm’s information environment. Although Jennings et al. (2017, p. 124) suggest that “the co-location of firms within an industry affects analysts’ cost of gathering and processing information,” it remains unclear whether these informational benefits are primarily driven by more efficient processing of public information facilitated by information spillovers, or by cost savings in acquiring private information about firms located near their industry peers.

Prior studies also suggest that sharing of common information (such as insights into local economic fundamentals) among analysts may lead to less (not more) accurate earnings forecasts, indicating poor information environment (Kim et al., 2001; Kirk et al., 2014). Even if the shared information about co-located industry peers is informative, its widespread use may cause analysts to repeatedly rely on the same common information, leading to an information cascading problem (Anderson & Holt, 1997; Hung & Plott, 2001). Similarly, financial analysts who follow firms co-located with their industry peers might overweight common public information about these peers and underweight their own private insights in their earnings forecasts. Consequently, it is unclear whether the information benefits from industry co-location are driven by an “information spillover effect,” which facilitates the processing of industry-wide common information, or by an “information cost effect,” which enables more efficient acquisition of private information about a firm.

Therefore, we explore the relative importance of common versus private information in explaining the information benefits of industry co-location. To do this, we use a measure of relative precision of common versus private information embedded in consensus forecasts, denoted as ρi, t, developed by Barron et al. (1998).

Following Barron et al. (1998), we estimate ρi, t by first calculating Ci, j,t, the average covariance of forecast errors between analyst j and the rest of the analysts following the firm i in year t. We then use the average of all C i,j,t values as the firm-year observation of C i,t . The overall uncertainty across analysts (Vi, t) is measured as the average of all Vi, j,t values, where Vi, j,t represents the mean of the squared error of analyst j’s earnings forecasts for firm i in year t. In estimating ρi, t, we require that analyst forecasts be made within 120 days of earning announcement and within 90 days of the fiscal year-end. In addition, analysts must issue their forecasts for each of the four quarters in the fiscal year. After estimating ρi,t, we re-estimate equation (1) using ρi,t as the dependent variable.

Table 5 presents the results of estimating equation (1) using ρi, t as the dependent variable. In column (1), the coefficient on R_Proximity_Numit is negative (β1 = −0.03) and statistically significant (t-statistics = −3.03), suggesting that the ρ decreases by 0.03, approximately 6% of the sample mean, when geographic proximity increases from the lowest to the highest percentile. In column (2), the proxy for geographic peer effect, R_Proximity_Num_Diffit, also shows a negative and statistically significant coefficient, indicating that analysts’ earnings forecasts incorporate more private information as a firm’s geographic proximity to both local and industry peers increases, after controlling for the factors affecting the properties of analysts’ forecasts. However, when both proximity measures are included in column (3), the coefficients for both R_Proximity_Numit and R_Proximity_Num_Diffit become insignificant, implying that the combined effects of industry co-location and geographic peer effects may obscure the relative importance of private information by creating information overload.

Relative importance of common versus private information.

Table 5 reports the estimation results of equation (1) after replacing the dependent variable with ρ. The variables are defined in Appendix 1. t-statistics are in parenthesis and are based on standard errors that are clustered by firm and year. Superscripts *, **, and *** denote significance (two-sided) at 10%, 5%, and 1%, respectively.

Conclusion

In this study, we explored the effects of the geographic clustering of firms within the same industry on their corporate information environment. Our findings show that industry co-location not only enhances the accuracy and reduces the dispersion of analysts’ earnings forecasts but also positively impacts the FERC. This suggests that industry co-location facilitates better incorporation of future earnings information into current stock prices.

In contrast, the geographic clustering of firms from different industries does not provide similar benefits and may even lead to information overload. Our study also investigates the source of these informational benefits by examining the relative importance of common versus private information. We find that geographic proximity among industry peers reduces the role of common public information and increases the importance of private information in forming a firm’s overall information environment. This is evidenced by the decreased role of common information and the increased significance of private information in consensus forecasts, as measured by Barron et al.’s (1998) precision measure.

Overall, our findings complement prior research on information spillovers by demonstrating that while geographic clustering of industry peers facilitates information spillovers and improves the information environment, the clustering of firms from different industries does not offer similar advantages and may complicate the information landscape. This underscores the unique value of industry co-location in enhancing both analysts’ forecast accuracy and stock price informativeness regarding future earnings.

Footnotes

Appendix 1. Definition of variables.

| Dispersion | = | the standard deviation of individual analysts’ annual earnings forecasts for a given firm issued during 365 days before the annual earnings announcement for a given firm, scaled by beginning-of-year share price, multiplied by 100. (-365 ~ the annual earnings announcement date[0]) |

| Accuracy | = | the absolute value of the difference between actual earnings and the median consensus earnings forecast issued within 365 days prior to the earnings announcement date, scaled by the stock price at the beginning of the fiscal year, multiplied by −100. |

| Proximity_Num | = | the number of firms in the industry located within 100 miles of firm i’s headquarter location in year t. |

| Proximity_Num_Diff | = | the number of non-industry peer firms located within 100 miles of the firm i’s headquarter location in year t. |

| MTB | = | market to book ratio, AT-CEQ + (PRCC_F*CSHO)/(AT-LT). |

| ROA | = | the return on assets, (IB)/(AT). |

| SUE | = | the absolute value of the difference between actual earnings and the earnings from the previous year, scaled by the stock price at the beginning of the year, abs(IB-IB t – 1)/(PRCC_Ft – 1). |

| Neg_UE | = | 1 if firm i’s earnings in year t is less than the reported earnings in year t – 1, 0 otherwise. |

| Neg_SI | = | the absolute value of the special item deflated by total assets if negative, zero otherwise. |

| Horizon | = | the logarithm of the average days from the forecast issuance date to firm-i’s earnings announcement date. |

| Size | = | the natural logarithm of total assets (AT) of the firm. |

| Herf | = | Herfindahl Index |

| Firm_age | = | the difference between the current year and the first year that the firm appeared in the COMPUSTAT. |

| Ret_Vol | = | the standard deviation of monthly stock return from years t – 1 to t. |

| Earn_Vol | = | the standard deviation of quarterly ROA(IBQ/ATQ) from years t-2 to t. |

| ρ | = | the ratio of the average covariance among analysts’ beliefs (Ci, t) to the overall uncertainty across analysts (Vi, t). Ci, t is the average of all Ci, j,ts. Ci, j,t is the average covariance of forecast errors between analyst j and the rest of the analysts following the firm i in year t. Vi, t is the mean of all Vi, j,ts. Vi, j,t is the average of the squared error of analyst j’s earnings forecasts of firm i in year t. |

| R | = | the cumulative buy-and-hold return for fiscal year t, measured over the fiscal year. |

| X | = | income before extraordinary items available to common shareholders scaled by beginning market value of equity. |

| MVE | = | the logarithm of market value of equity. |

| Ret _Vol | = | the standard deviation of monthly stock return from years t – 1 to t. |

| AF | = | the logarithm of the number of analyst following |

Appendix 2

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.