Abstract

This article investigates the relationship between Inter-Korean geopolitical risk (IKGPR) and South Korean firms’ risk-taking in the context of highly political tensions in the Korean peninsula. Using a recently developed news-based index of geopolitical risk, our empirical analysis shows an inverse U-shaped relationship between IKGPR and firm risk-taking in South Korea, implying that South Korean firms’ risk-taking increases with IKGPR when IKGPR is low but becomes prudent when IKGPR is high. Such an effect of IKGPR on firm risk-taking is weaker for firms that survive wartime (1900–1969) and is stronger for firms that were established after the Second Korean War (1966–1969), suggesting the role of corporate resilience to geopolitical risk in motivating differences in corporate behaviors. Further analyses indicate that South Korean firms tend to take less risk when the nuclear risk is higher and when they are more technology-oriented.

Keywords

Introduction

How does corporate risk-taking react to increasing geopolitical risk and threats of war? Previous studies show that corporate risk-taking is sensitive to changes in the macroeconomic and political institutions (Boubakri et al., 2013; Tran, 2019). However, little is known about how geopolitical risk affects corporate risk-taking behavior. As uncertainty in geopolitics leads to changes in the business environment and affects corporate operations (Julio & Yook, 2012; Le & Tran, 2021), firms may have to consider undertaking fewer risky operations if the political risk is high.

Using a sample of South Korean firms that operate under a high degree of geopolitical risk, this study seeks to reveal how Inter-Korean geopolitical risk influences corporate risk-taking. The unique geopolitical context of the Korean Peninsula presents an interesting setting to study the impact of geopolitical risk on corporate risk-taking. In principle, North Korea and South Korea have been at war since 1950. The two parts of Korea only preserve a so-called “peace” by an armistice in 1953, which only served the purpose until the Second Korean War 1966–1969. Since the 1990s, there have been increasing concerns from South Korea and the international community as North Korea has been developing nuclear weapons. From 2006 to date, there have been six observed nuclear tests conducted in North Korea’s territory, leading to heightened geopolitical tensions in the peninsula and the Asia-Pacific region. As the threats of war and nuclear risk become more visible, it is a compelling context to study how corporates behave under extreme uncertainty.

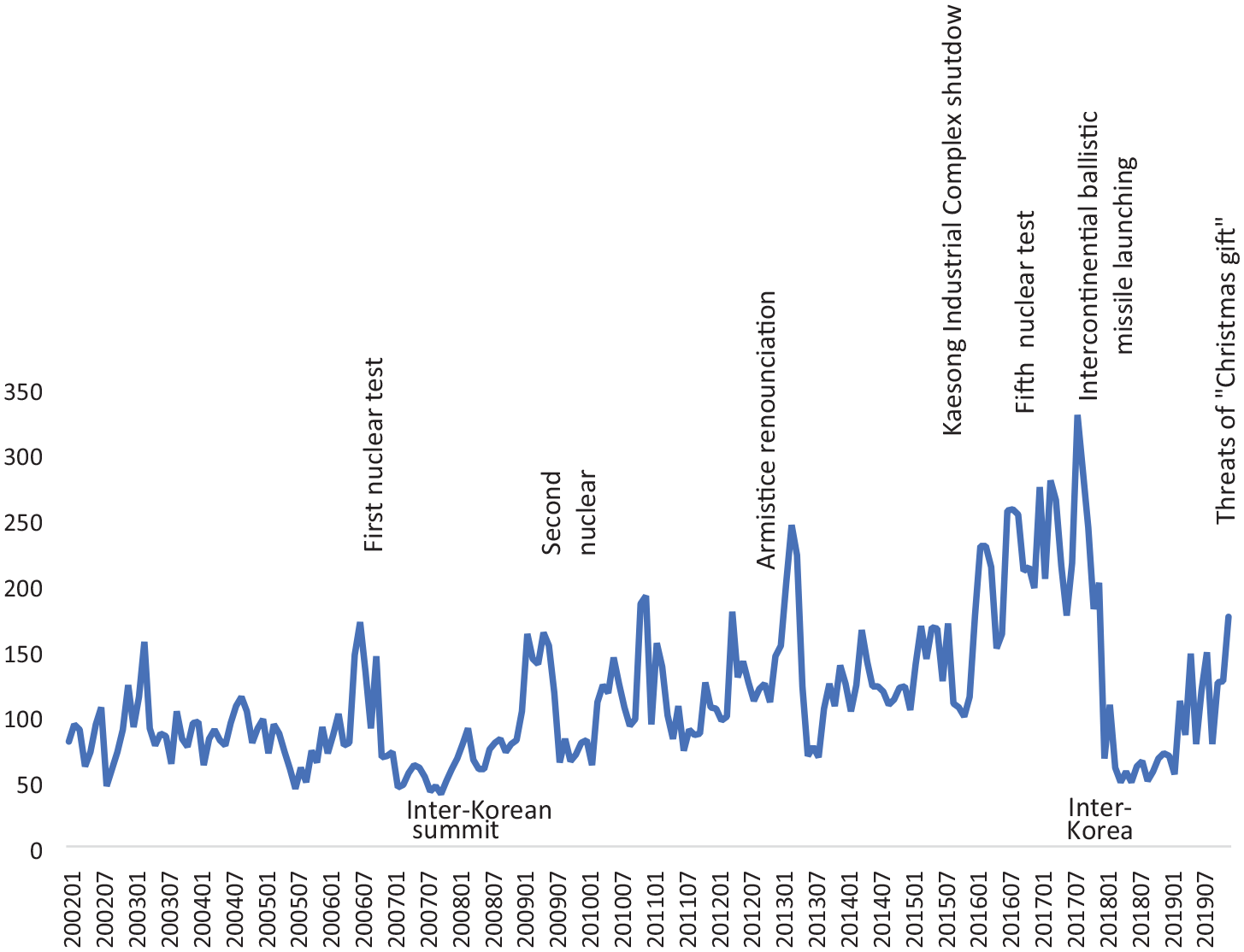

We follow Jung et al. (2021) to measure Inter-Korean geopolitical risk using a news-based approach. Because geopolitical risk is unobservable and cannot be quantified in conventional ways, Jung et al. (2021) measure this factor by counting the frequency of news articles with keyword combinations representing Inter-Korean geopolitical tensions and military events, that is, the risk associated with geopolitics between North and South Korea. Figure 1 shows the main developments of Inter-Korean geopolitics and the movement of the Geopolitical Risk Index proposed by Jung et al. (2021).

Developments in Inter-Korean geopolitics and the IKGPR index during the 2002–2019 period.

Using a multiple fixed effect model and intensive controls for firm-level, industry-level, and macro-level confounding factors during the 2002–2019 period, we find that, in general, South Korean firms’ risk-taking increases with Inter-Korean geopolitical risk when Inter-Korean geopolitical risk is low; however, this relationship reverses to form a U-shaped curve when Inter-Korean geopolitical risk is high. The empirical finding remains qualitatively unchanged after a battery of sensitivity tests. Interestingly, analysis shows that such an effect is more pronounced in firms established after the Second Korean War (1966–1969) while remaining weaker in their counterparts. Further analyses demonstrate the variations of the impact during North Korea’s nuclear test events and among firm groups of different technology intensities and chaebols. The findings are novel and not documented elsewhere in the literature.

Our study contributes to the literature in several ways. First, we show a nonlinear relationship between Inter-Korean geopolitical risk and South Korean firms’ risk-taking, indicating the asymmetry in corporate behavior across different levels of geopolitical risk. Our finding well supports the notion that firms rationally take risk and can distinguish between taking risk and gambling (March & Shapira, 1987). Therefore, despite firms taking risk when the risk is low, they become prudent when the level of geopolitical risk exceeds a certain threshold. From there, we indicate that the differences in the research designs (linear vs nonlinear model setting) may eventually lead to contradictory findings on the relationship between geopolitical risk and corporate risk-taking. This is an important remark that provides implications for future studies in this field.

Second, we suggest the role of corporate resilience to geopolitical risk in motivating differences in corporate behaviors under uncertainty. In the context of the Korean Peninsula, firms that survive wartime may develop a certain degree of resilience to the political tension between the South and the North. In contrast, firms established after the Second Korean War (e.g., firms with less resilience to political tension) exhibit stronger negative reactions to unfavorable developments in Inter-Korean politics. This finding is intuitive as South Korean firms established and survived the Inter-Korean war periods (1950–1953 and 1966–1969) have experience dealing with extreme uncertainty during the war, thus having better corporate resilience to such extraneous shocks. As a result, negative developments in Inter-Korean geopolitical tensions do not affect their behavior as much as firms that did not experience war.

Third, we provide additional evidence of how the impact varies in the cross-sections and the time dimension, thus adding new understandings of the newfound relationship. The finding suggests the role of research and development (R&D) intensity in corporate operations under extreme geopolitical risk, where technologically intensive firms take less risk than their counterparts when the threats from the North draw near. As investments in R&D activities are usually regarded as risky operations (Xu et al., 2019), firms with more R&D intensity may have less incentive to take more risk in their operations under increased geopolitical risk relative to less R&D-intensive firms. The finding provides important implications for the decision-making of R&D-intensive firms under extreme-risk situations.

The rest of the article proceeds as follows. Section “Literature background and hypothesis development” reviews related literature and develops hypotheses. Section “Methodology and data” presents the research methodology and data used in this study. Section “Empirical results and discussion” reports and discusses empirical results. Section “Conclusion, limitations, and future research” concludes this article.

Literature background and hypothesis development

Some particular areas are more complicated than others due to their historical events that motivate an intense atmosphere in the areas. One of the most unpredictable regions is the Korean Peninsula, where two countries of North Korea and South Korea co-exist. The tension in the Inter-Korea relationship, as elaborated by Jung et al. (2021, p. 7), is due to their “international sanctions against North Korea, bilateral and multilateral talks to seek reconciliation, and, finally, economic cooperation between South and North Korea.” The tightening economic and financial sanctions from the international organizations and the United States threaten North Korea’s economy and at some points trigger aggressive reactions from North Korea, which, in turn, elevate tension on the geopolitical landscape of the Korean Peninsula. Although the relationship between North and South Korea has improved recently, marked by the historical handshake of President Kim Jong Un and President Moon Jae In at the shared border of the two countries, their strain is still there to solve.

Different from commonly used proxies for uncertainty such as (economic) policy uncertainty and political uncertainty, geopolitical risk is overlooked in firm-level research. The scarcity of research on Inter-Korean geopolitical risk is probably partly because of a lack of proper measurements for this term alongside the complexity of the bilateral relationship. To effectively grasp the idea of geopolitical risk, it is important to understand that risk is associated with a known outcome, while uncertainty refers to the shortage of reliable information to come up with an effective prediction of the outcome (Kobrin, 1979). March and Shapira (1987, p.1404) make a point that managers “make a sharp distinction between taking risks and gambling.” According to Pratt (1964) and other early treatments, if an individual stands between two options with similar expected values, in which one’s outcome is known for certain and the other is a gamble, the person will lean toward the former option. If firms may consider trading off risks for potential future profits when the outcome is known, they tend to be more prudent with business decisions when they cannot anticipate the consequence. Hence, firms’ reactions to risk and uncertainty may not be identical. Despite that risk and uncertainty differ in nature, the antagonistic history of North and South Korea implies that geopolitical risk may bring forth geopolitical uncertainty (i.e., an increasing probability of an armed conflict leading to unpredictable business prospects) when politically risky events incessantly take place. Therefore, rising Inter-Korean geopolitical risk also heightens uncertainty threats in this specific context.

Despite corporate responses to Inter-Korean geopolitical swings being under-studied, several papers on stock performance in the face of Inter-Korean geopolitical fluctuations have yielded dissimilar results. Jung et al. (2021) use their self-constructed Inter-Korean geopolitical risk index, based on machine learning techniques, to reveal an inverse association between geopolitical risk and stock returns of South Korean firms. In contrast, Pyo (2021) points out that the market reacts favorably when the geopolitical situation in the Peninsula turns milder; however, the market shows limited attention to negative Inter-Korea events. Moreover, how this type of risk impacts South Korea’s macroeconomic indicators also remains inconclusive due to contradictory empirical findings (Ha et al., 2022; Pyo, 2021). The divergence in empirical findings may stem from different measurement constructions; however, another possible scenario is the empirical conflicts could be an indication of variations in the impact of Inter-Korean geopolitical risk at different risk levels, which has not been tapped into by existing studies.

Given the looming risk of geopolitics and war in the Korean Peninsula for almost a century, the latter explanation is not irrational. Although this inherent risk may somehow alter the business practice of South Korean firms, it is well noted that most currently operating firms were established after the Second World War; therefore, they are probably born with a tolerance of Inter-Korean geopolitical swing. In other words, South Korean firms may not strongly react to minor fluctuations in geopolitical risk unless when it considerably elevates. In that light, South Korean firms likely pursue some risky projects until the risk level reaches a threshold. Theoretically, Kahneman and Tversky (1979) indicate that when an agent’s utility is based on gains or losses rather than final income levels, there is a tendency toward risk-seeking behavior in the domain of minor losses. Adding to that, French and Sichel (1993) suggest that because heightened uncertainty is often a result of negative shocks, the adverse effect of uncertainty tends to dominate when uncertainty is high. Conversely, there is room for a positive effect when uncertainty is low. These theoretical viewpoints imply that the association between corporate risk-taking and geopolitical risk is not necessarily linear.

Whereas no prior research directly delves into the linkage between corporate risk-taking and Inter-Korean geopolitical risk, current studies provide some hints at a nonlinear impact of uncertainty from the investment and cash-holding channels. Given that Inter-Korean geopolitical risk serves as a source of uncertainty in the Korean Peninsula, it is logical to associate Inter-Korean geopolitical risk with uncertainty when studying Korean firms’ risk-taking. The term risk-taking is highly linked with investment, referring to a firm’s investment decision to trade off anticipated cash flows for uncertain risks (Acharya et al., 2011). Sarkar (2000), although agrees with the validity of the real options theory, also points out that uncertainty does not always increase the value of the option to wait. Instead, higher uncertainty may also bring up the probability of investment; however, this positive effect seems to be restricted only within a low-uncertainty domain and reverses when uncertainty exceeds a certain threshold. Therefore, according to Sarkar (2000), the relationship between investment and uncertainty should follow an inverted U curve. The nonlinear effect of uncertainty on investment is also shown in Bo and Lensin (2005), an empirical study on a sample of Dutch non-financial firms. Particularly, they find that when the uncertainty is low (high), an increase in uncertainty leads to higher (lower) investments. From the cash-holding perspective, Su et al. (2020) reveal that when uncertainty emerges, firms tend to trade off their cash holdings to seize new investment opportunities to boost their earnings. However, once uncertainty is clearly present, a risk-aversion attitude prevails as continuously heightened uncertainty makes it challenging for corporate managers to assess the company’s ability to handle the risks, leading to a more conservative investment approach and an increase in the amount of cash kept for precautionary reasons (Kotcharin & Maneenop, 2020; Lee & Wang, 2021). These findings inform that firms lean toward risky decisions when uncertainty rises as long as it has not reached a certain threshold.

Firms’ ability to take risks during escalated uncertainty is also restrained by the capital market. As uncertainty heightens, banks will be more prudent in lending decisions, leading to a shortage of cash supply limiting firms’ available funds for investment (De Nicolò et al., 2010; Hu & Gong, 2018). In that context, banks’ precautionary policies when geopolitical uncertainty turns visible constrain firms’ financing options (Brogaard & Detzel, 2015; Zhang et al., 2015). The increasing risk of financing gradually decimates the expected benefit from investments, making investment options unjustifiable and encouraging managers to adopt a more conservative approach (Bernanke, 1983; Gormley & Matsa, 2016; Gulen & Ion, 2016; Shapira, 1995). This exogenous impact incentivizes firms to minimize their exposure to uncertainty in the fear of the unanticipated adverse effect caused by growing uncertainty. Corporate risk-taking, hence, decreases if uncertainty is continuously magnified as a result of geopolitical swing. Firms’ risk-taking, however, may increase in the short run because the benefit gained from investment still outweighs its cost and banks do not necessarily adopt stringent measures against unnoticeable uncertainty.

The different corporate risk-taking behavior during different periods of uncertainty indicates that the relationship between firms’ risk-taking and uncertainty is likely to be nonlinear. Since Inter-Korean geopolitical risk acts as a form of uncertainty imposed on the South Korean economy, we conjecture that South Korean firms demonstrate different risk-taking attitudes across escalating geopolitical tension and calm periods. Following this conjecture, we propose the research hypothesis as follows:

Hypothesis 1: The relationship between Inter-Korean geopolitical risk and firm risk-taking is inverted U-shaped.

Methodology and data

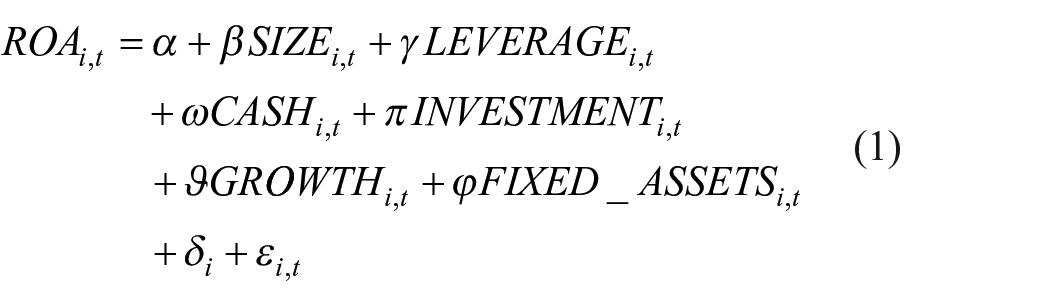

Variable measurements

Inter-Korean geopolitical risk

We use the Inter-Korean geopolitical risk index proposed by Jung et al. (2021) as our variable of interest in this study. According to Jung et al. (2021), the geopolitical risk involves four key drivers that link to each other and create a geopolitical background for the Korean Peninsula. The drivers include the conflict between the South and North Korean military, international embargoes on North Korea, bilateral and multilateral conversations to reconcile, and cooperation between South and North Korea’s economies. Jung et al. (2021) construct the Inter-Korean geopolitical risk index based on the news articles of 18 broadcasters and newspapers of BigKinds, a news-analyzing firm formed by the Korea Press Foundation. The topics of the news focus on economics, international relationships, and politics. Then, a list of keywords on headlines or contents is determined.

From the search for keywords, Jung et al. (2021) calculate the news frequency in each category (military issues, sanctions, conversation of reconciliation, and economic cooperation) and divide it into two groups: positive and negative news. Positive and negative news indicate the news that reports the tension decrease and increase between South and North Korea, respectively. Let

Jung et al. (2021) then transform

For each media source, Jung et al. (2021) standardize

Finally,

The higher the value of IKGPR, the higher the geopolitical risk between North and South Korea is.

Corporate risk-taking

Following the commonly accepted practice in the previous literature (Kim et al., 1993; Wright et al., 2007; Yung & Chen, 2018), we use the rolling standard deviation of return-on-assets ratio (SDROA) as a measurement of corporate risk-taking. SDROA is calculated over a rolling window of three continuous years. For robustness check, we compute an alternative measure of risk-taking: the three-year rolling standard deviation of return-on-common equity ratio (SDROE). The higher the value of SDROA and SDROE, the riskier projects the firm takes on and the more volatile its income is.

Using an alternative approach to measure firm risk-taking (Martins, 2020), we proxy firm risk-taking by the absolute deviation from expected performance for each year. Martins (2020) models the expected firm performance using the following equation

where

Control variables

Based on the previous literature (Tran, 2019; Yung & Chen, 2018), we adopt country-level, industry-level, firm-level, and corporate governance controls to capture the specific characteristics of each firm in each year of our sample. Regarding country-level controls, we employ South Korea’s Economic Policy Uncertainty Index (Baker et al., 2016) and the gross domestic product (GDP) growth rate (in percentage) of South Korea. The country-level controls indicate the military issue, economic, and political background of South Korea. In terms of industry-level controls, the standard deviation of total sales of firms in the same industry and the standard deviation of ROA of firms in the same industry are included. For the firm-level controls, we select popular-used control variables in the literature, including firm size, firm age, leverage, sales growth, cash ratio, fixed assets ratio, cash flow, Z-score, market-to-book ratio, and annual stock returns following Yung and Chen (2018), Tran (2019), and Koirala et al. (2020).

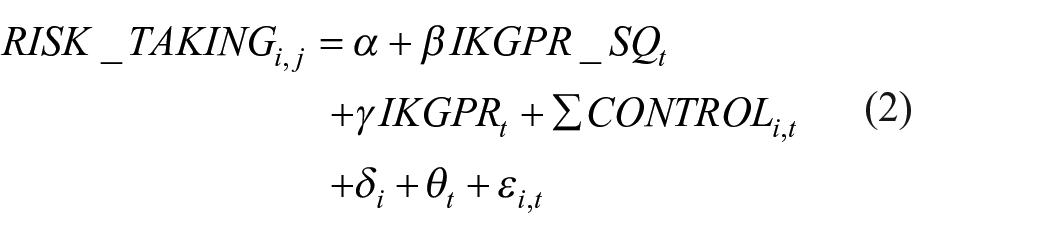

Empirical model

We use the following empirical model to investigate the impact of Inter-Korean geopolitical risk on firm risk-taking

where

Following the hypotheses development, we expect the coefficient

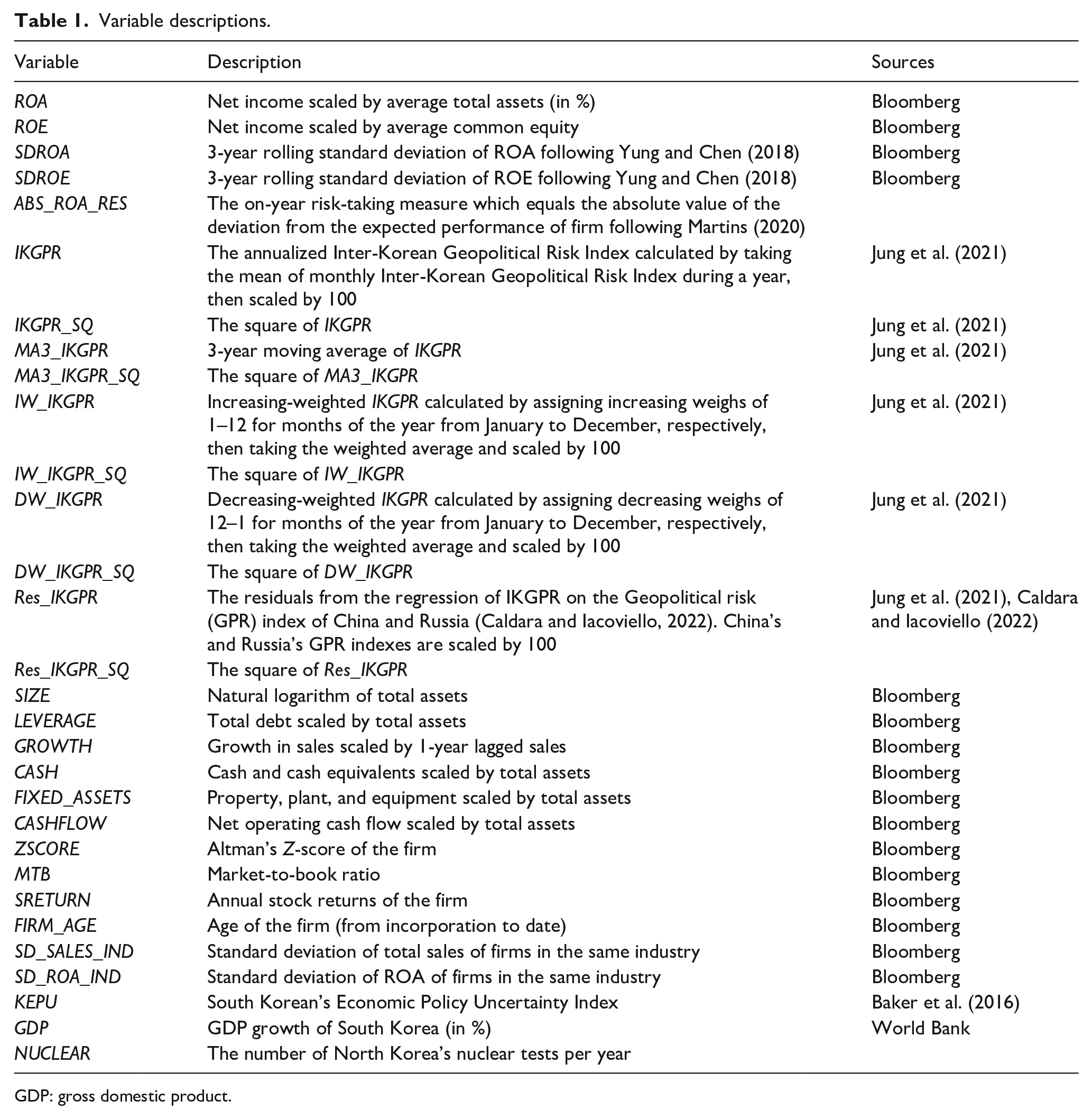

Variable descriptions.

GDP: gross domestic product.

Data and sample

We collect data from several sources. Financial data of South Korean firms are from the Bloomberg database. We retrieve macroeconomic data from World Bank open database; the economic policy uncertainty index of South Korea (Baker et al., 2016) is from the website www.policyuncertainty.com. For independent variable, we adopt the Inter-Korean Geopolitical Risk Index proposed by Jung et al. (2021). Our initial sample includes all firms listed on Korea Stock Exchange from 2002 to 2019. We screen the sample and exclude all financial and utility firms because the risk-taking nature is different from that of non-financial firms. After excluding missing data, the final sample consists of 1,668 South Korean firms with a total of 15,412 firm-year observations. All continuous variables are winsorized at the 1st and the 99th percentiles to alleviate the potential impacts of outliers on the outcomes of data analysis.

Empirical results and discussion

Descriptive statistics

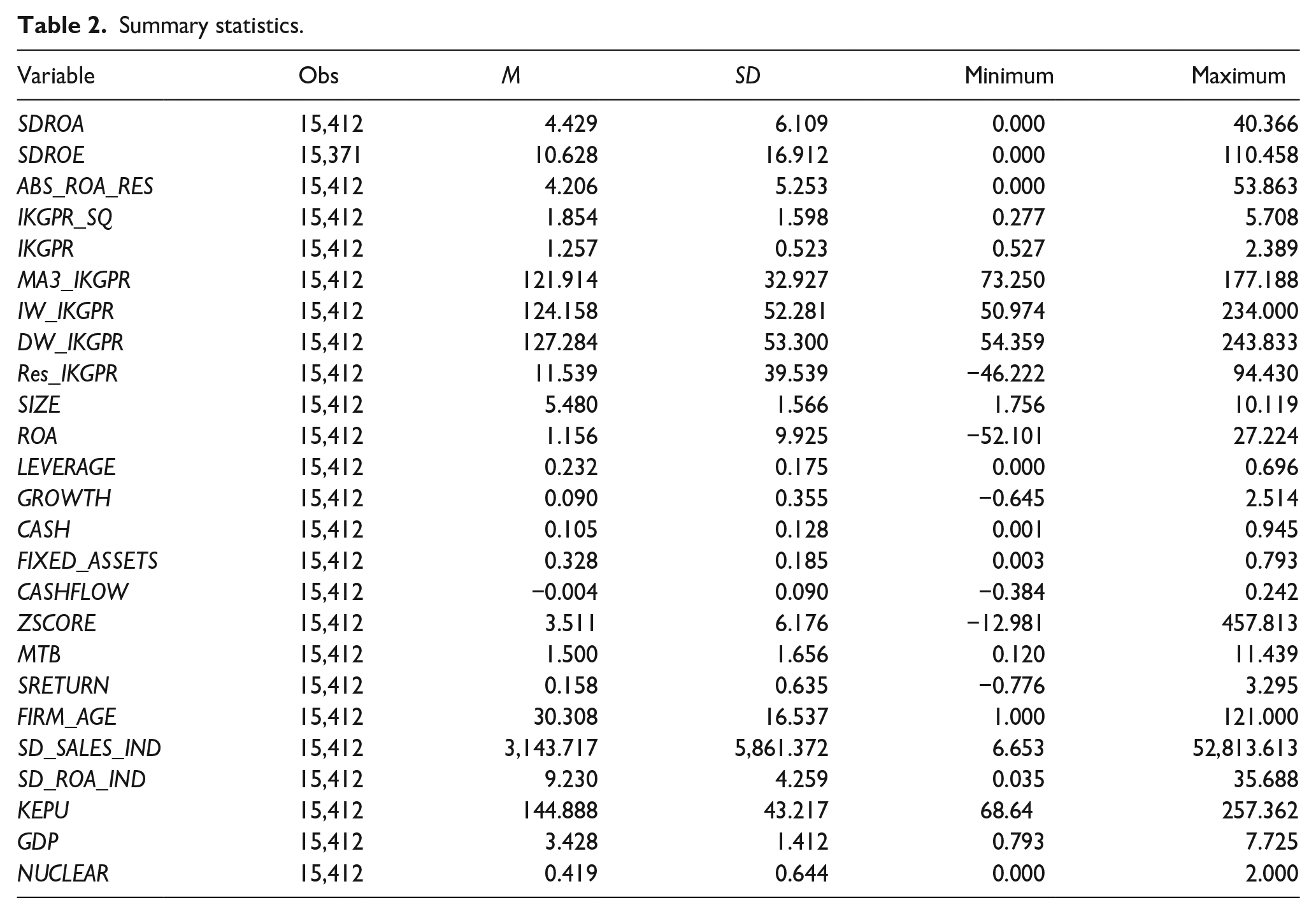

The variables’ descriptive statistics are displayed in Table 2. The average corporate risk-taking level (SDROA) of the listed Korean firms is 4.429, with a standard deviation of 6.109. The variable IKGPR during the sample period ranges from 0.527 to 2.389, with a mean of 1.257. Figure 1 shows that the Inter-Korean geopolitical risk index reaches new peaks at the announcement of important negative news, such as the first and second nuclear tests, the Yeonpyeong Island attack. The index drops to low level when positive news, for example, Inter-Korean summit and Inter-Korean and North Korea-United States summits, are informed.

Summary statistics.

Regarding the control variables, an average Korean-listed firm has leverage and sales growth of 23.2% and 9%, respectively. The average fixed assets ratio and cash ratio are 32.8% and 10.5%, correspondingly. There are both young firms and mature firms in the sample, with an average firm age (FIRM_AGE) of 30.3 years, where the youngest firms are only 1 year old and the oldest firms are 121 years old. In terms of market performance, Korean-listed firms’ market-to-book ratio and annual stock returns are averaged at 1.5% and 15.8%, respectively. For the corporate governance factor, the statistics show that a majority (81.5%) of the Chief Executive Officer is also the chair of Korean firms’ board of directors. Besides, as shown in Table 2, during the study period (2002–2019), the average GDP growth of Korea is 3.428%. The average number of North Korea’s nuclear tests is 0.419 times per year.

Table 8 in the Appendix shows the pairwise correlation matrix of our regression model’s variables. Since all correlation values are smaller than 0.5, there are no notable correlations among independent variables in the regression model.

Baseline results and discussion

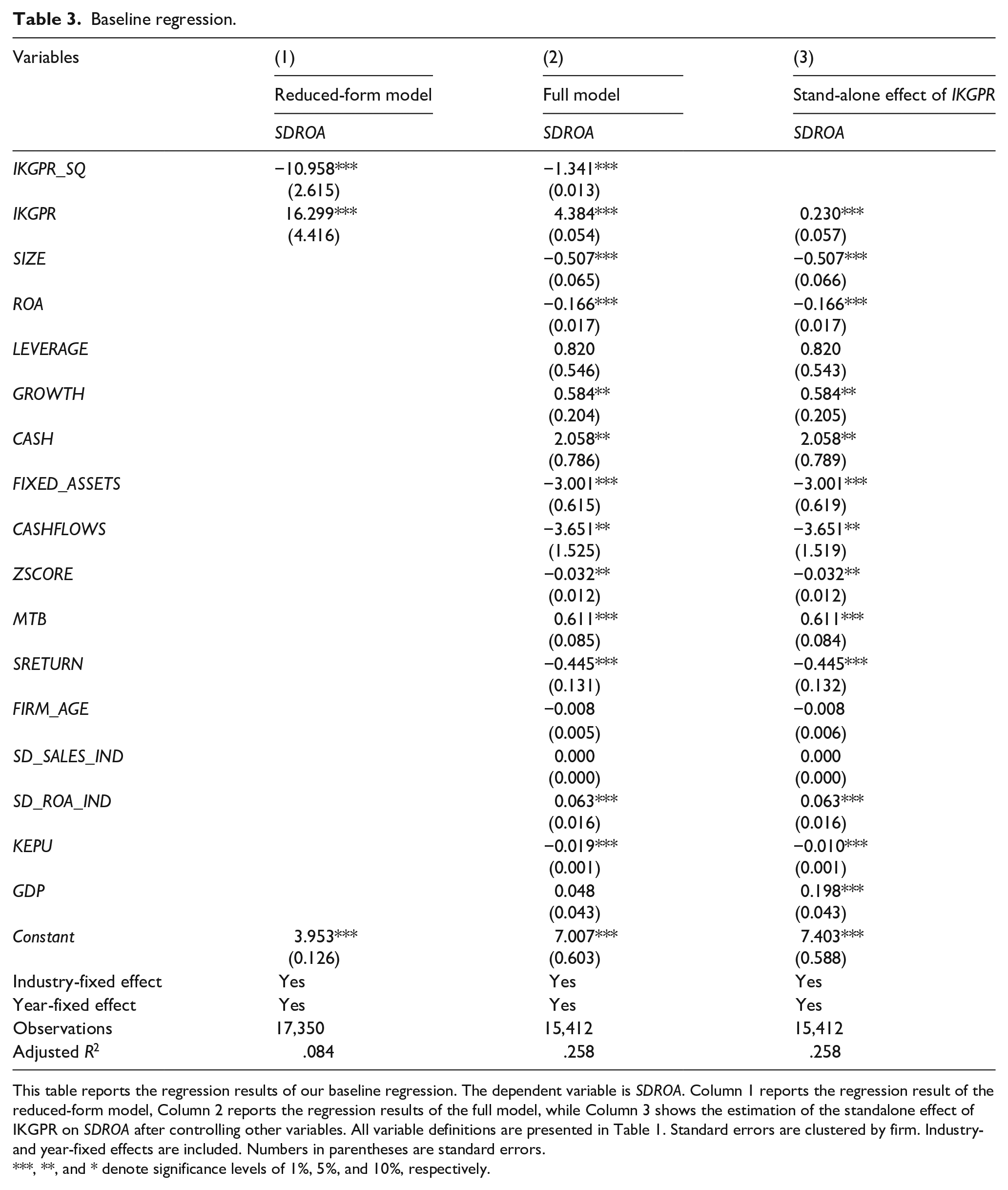

The baseline regression results of Model 2 are presented in Table 3. As shown in Table 3, the coefficient of IKGPR is positively and significantly associated with corporate risk-taking at 1% level in all three regression analyses (reduced-form, full model, and stand-alone effect of IKGPR). This result suggests that corporate risk-taking of Korean-listed firms generally increases with Inter-Korean geopolitical risk. However, the risk-taking attitude could be reverted when the geopolitical risk elevates to a certain level as documented by Bo and Lensin (2005).

Baseline regression.

This table reports the regression results of our baseline regression. The dependent variable is SDROA. Column 1 reports the regression result of the reduced-form model, Column 2 reports the regression results of the full model, while Column 3 shows the estimation of the standalone effect of IKGPR on SDROA after controlling other variables. All variable definitions are presented in Table 1. Standard errors are clustered by firm. Industry- and year-fixed effects are included. Numbers in parentheses are standard errors.

, **, and * denote significance levels of 1%, 5%, and 10%, respectively.

Furthermore, the results show that the coefficient of IKGPR_SQ is negatively and significantly related to corporate risk-taking at 1% level during the sample period. This finding reveals an inverted U-shape relationship between Inter-Korean geopolitical risk and corporate risk-taking, indicating that at a low level of Inter-Korean geopolitical risk, corporate risk-taking is positively associated with Inter-Korean geopolitical risk. However, when Inter-Korean geopolitical risk is high, corporate risk-taking reacts negatively to Inter-Korean geopolitical risk. This inverted U-shape nexus between corporate risk-taking and Inter-Korean geopolitical risk is in line with the suggestions of the previous literature (French & Sichel, 1993; Kahneman & Tversky, 1979) that firms tend to reduce risk-taking by investing less and holding more cash under extreme uncertainty. The underlying reason for the reaction of managers during high geography risk periods is possibly due to the risk-averse characteristic that discourages the undertaking of risky projects and additional financial leverage during high volatility periods (Gormley & Matsa, 2016; Zhang et al., 2015).

Overall, the findings of the baseline regression model support our hypothesis that the relationship between Inter-Korean geopolitical risk and firm risk-taking is non-linear. Particularly, when the geopolitical risk is low, corporate risk-taking increases with the geopolitical risk. However, when the geopolitical risk is considerably high, firms take less risky operations.

Robustness checks

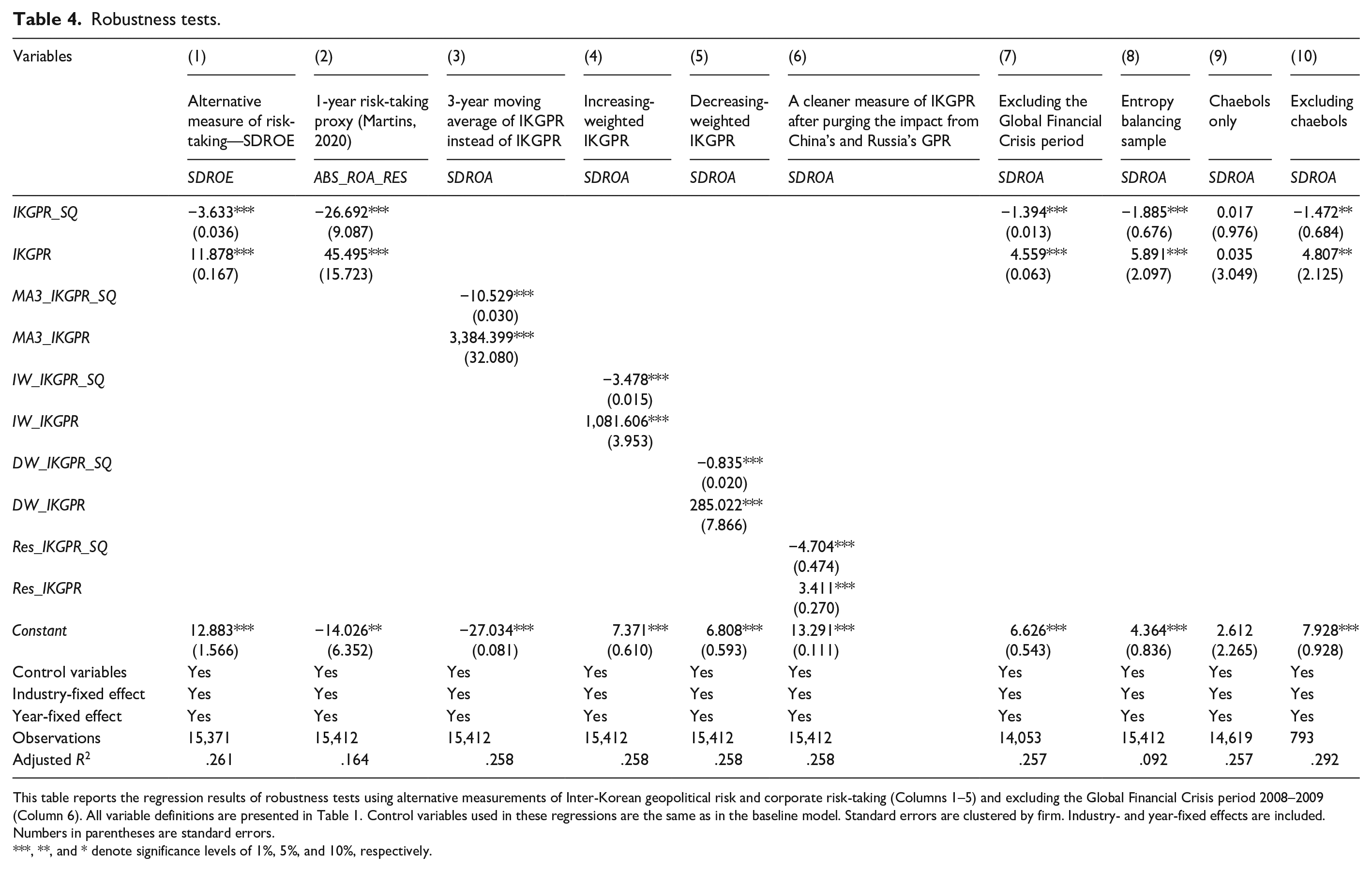

To check the robustness of baseline findings, we use different measurements of IKGPR and corporate risk-taking as presented in Table 4. In the first column of Table 4, the standard deviation of ROE (SDROE) is used as an alternative measure of risk-taking. The effects of IKGPR and IKGPR_SQ on SDROE are consistent with our previous findings that there is a U-shape relationship between Inter-Korean risks and Korean firms’ risk-taking. Column 2 reports the regression results of the baseline model using the 1-year deviation from expected performance (ABS_ROA_RES) as another alternative measure of risk-taking to revisit the empirical finding.

Robustness tests.

This table reports the regression results of robustness tests using alternative measurements of Inter-Korean geopolitical risk and corporate risk-taking (Columns 1–5) and excluding the Global Financial Crisis period 2008–2009 (Column 6). All variable definitions are presented in Table 1. Control variables used in these regressions are the same as in the baseline model. Standard errors are clustered by firm. Industry- and year-fixed effects are included. Numbers in parentheses are standard errors.

, **, and * denote significance levels of 1%, 5%, and 10%, respectively.

In Columns 3–6 of Table 4, different measures of IKGPR are adopted to test the impacts of Inter-Korean geopolitical risk on corporate risk-taking. The alternative measures of Inter-Korean geopolitical risk include 3-year moving average of IKGPR (MA3_IKGPR and MA3_IKGPR_SQ), increasing-weighted IKGPR (IW_IKGPR and IW_IKGPR_SQ), decreasing-weighted IKGPR (DW_IKGPR and DW_IKGPR_SQ), and a cleaner measure of IKGPR after purging the impact from China’s and Russia’s geopolitical risk (Res_IKGPR and Res_IKGPR_SQ). The intuition is that the news-based Inter-Korean geopolitical risk index may accidentally capture other news that reflects other sources of geopolitical risk originated from other countries or territories than North Korea, for instance, China, Russia, or Japan. To exclude those sources of geopolitical risk, we regress IKGPR on the geopolitical risk indices of China and Russia (Caldara & Iacoviello, 2022), then take the residuals of the regression as the cleaner measure of IKGPR. We cannot include Japan’s geopolitical risk in this regression as such data are not available. As such, Res_IKGPR reflects the component of Inter-Korean geopolitical risk after removing the potential impacts from China and Russia. In the seventh column, we exclude the 2008 Global Financial Crisis (GFC) period from the sample.

To confirm the baseline findings under the Ceteris Paribus assumption, we employ the entropy balancing approach (Hainmueller, 2012; Tübbicke, 2022) to mitigate the potential confounding factors and pairwise correlation between variables in our model. As entropy balancing approach can be applied for continuous treatment (Tübbicke, 2022), we match the sample by all the firm-level and industry-level control variables in the baseline model while setting IKGPR as the treatment variable. Hainmueller (2012) and Zhao and Percival (2017) indicate that entropy balancing has more advantage over propensity score matching in terms of re-weighting sample to eliminate the impact of confounding factors and even Pearson correlation at different orders. After re-weighting the sample, we use the entropy balancing weight to re-perform the baseline regression. The regression results are reported in Column 8, Table 4.

There is a special feature of South Korea’s economy: the chaebols. Chaebols are large, family-owned conglomerates that dominate the South Korean economy. They are typically owned and managed by a single family and have enormous influence over the economy. They are known for their large size, diversified business portfolios, and close ties to the government, thus may be more resilient to external risk, including geopolitical risk. Based on this understanding, we conduct further sensitivity tests to see whether the baseline effect of IKGPR on firm risk-taking persists in the case of chaebols. We use the 2020 Forbes List of 50 largest South Korean–listed corporations to identify the group of chaebols in our sample. Next, we, respectively, re-estimate the baseline model using the chaebols-only subsample and the full sample excluding chaebols to see how the impact differs with and without chaebols in our sample. Columns 9 and 10 present the regression results.

In general, the regression results of the robustness tests confirm the baseline findings. In other words, our baseline findings hold with different variable measurements, model specifications, an entropy balancing approach, and sample selection. An interesting finding is that we do not find a statistically significant impact of IKGPR on the risk-taking of chaebols (see Column 9), while the impact remains consistent for other firms. This corroborates our conjecture about the resilience of chaebols under increased geopolitical risk in the Korean Peninsula.

In summary, the impact of Inter-Korean risk on South Korean firms’ risk-taking remains intact after numerous sensitivity tests using various measures of Inter-Korean geopolitical risk and excluding the 2008 GFC period. The sensitivity tests’ results, hence, suggest the robustness of our findings.

Further analyses

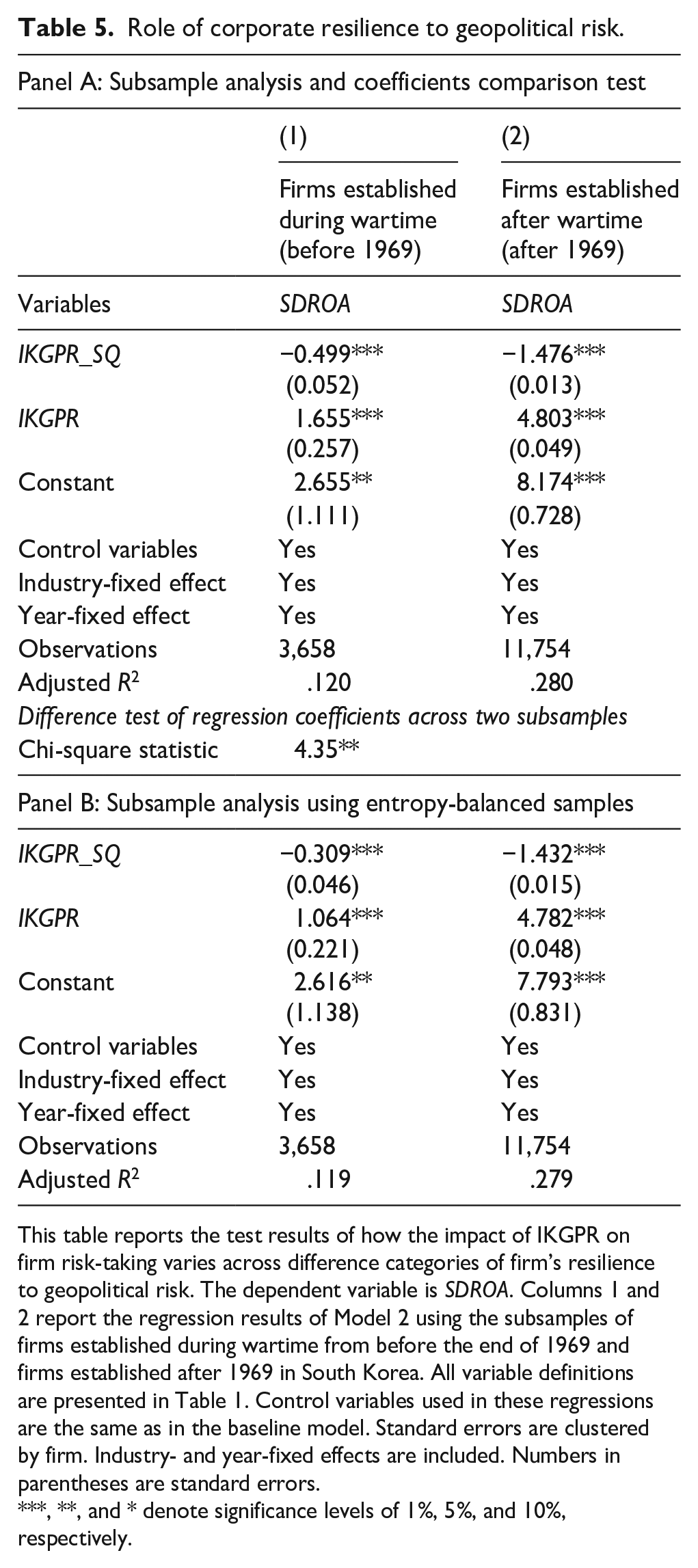

In this section, we take further steps to unveil how the relationship between IKGPR and firm risk-taking works. We follow the discussion in the work by Yeoh and Hooy (2022) that war experience may affect corporate risk-taking behavior and argue that firms that experienced the Korean wars may withstand the later upheaval in Inter-Korean geopolitics better than those did not. To verify this argument, we divide the sample into two subsamples: South Korean firms that experienced war (i.e., firms established before the end of the Second Korean War 1966–1969) and South Korean firms that have never experienced war (i.e., firms established after the Second Korean War). We re-perform the baseline regression on each of the subsamples. Next, we apply the seemingly unrelated regression (SUR) and a Hausman specification chi-square test to test the difference between the two coefficients of IKGPR_SQ in the two regressions. This procedure is to see whether those two groups react differently to heightened geopolitical risk. In addition, firms from the subsamples may not be comparable, thus being subject to selection bias concern. To alleviate this potential bias, we use the entropy balancing weights in the subsample regressions as an adjustment to eliminate the impact of confounding factors and even Pearson correlation at different orders of variables in the baseline model. Panels A and B of Table 5 report the regression results.

Role of corporate resilience to geopolitical risk.

This table reports the test results of how the impact of IKGPR on firm risk-taking varies across difference categories of firm’s resilience to geopolitical risk. The dependent variable is SDROA. Columns 1 and 2 report the regression results of Model 2 using the subsamples of firms established during wartime from before the end of 1969 and firms established after 1969 in South Korea. All variable definitions are presented in Table 1. Control variables used in these regressions are the same as in the baseline model. Standard errors are clustered by firm. Industry- and year-fixed effects are included. Numbers in parentheses are standard errors.

, **, and * denote significance levels of 1%, 5%, and 10%, respectively.

In both regressions in Panel A of Table 5, the coefficients of IKGPR_SQ are negative and statistically significant, thus consistent with the baseline results. Interestingly, the coefficient of IKGPR_SQ in the regression using a subsample of firms surviving wartime (−0.499) is less negative than that in the regression using a subsample of firms established after the Second Korea War (−1.476), and the difference between the two coefficients is statistically significant (chi-square = 4.35). We obtain similar results in Panel B where we use entropy balancing weights in the regressions to mitigate the selection bias concern. Specifically, the coefficient of IKGPR_SQ in Column 1, Panel B, is −0.309, while it is −1.432 in Column 2 of the same panel; both are statistically significant at 1% significance level. These empirical findings suggest that firms that experienced heightened geopolitical risk and war are more familiar with volatility and political upheaval, thus those firms have more resilience to geopolitical risk compared to their counterparts. Therefore, their risk-taking is less affected by the extreme level of Inter-Korean geopolitical risk. Our finding is in line with that of Yeoh and Hooy (2022) that wartime experience exerts certain influences on firm risk-taking.

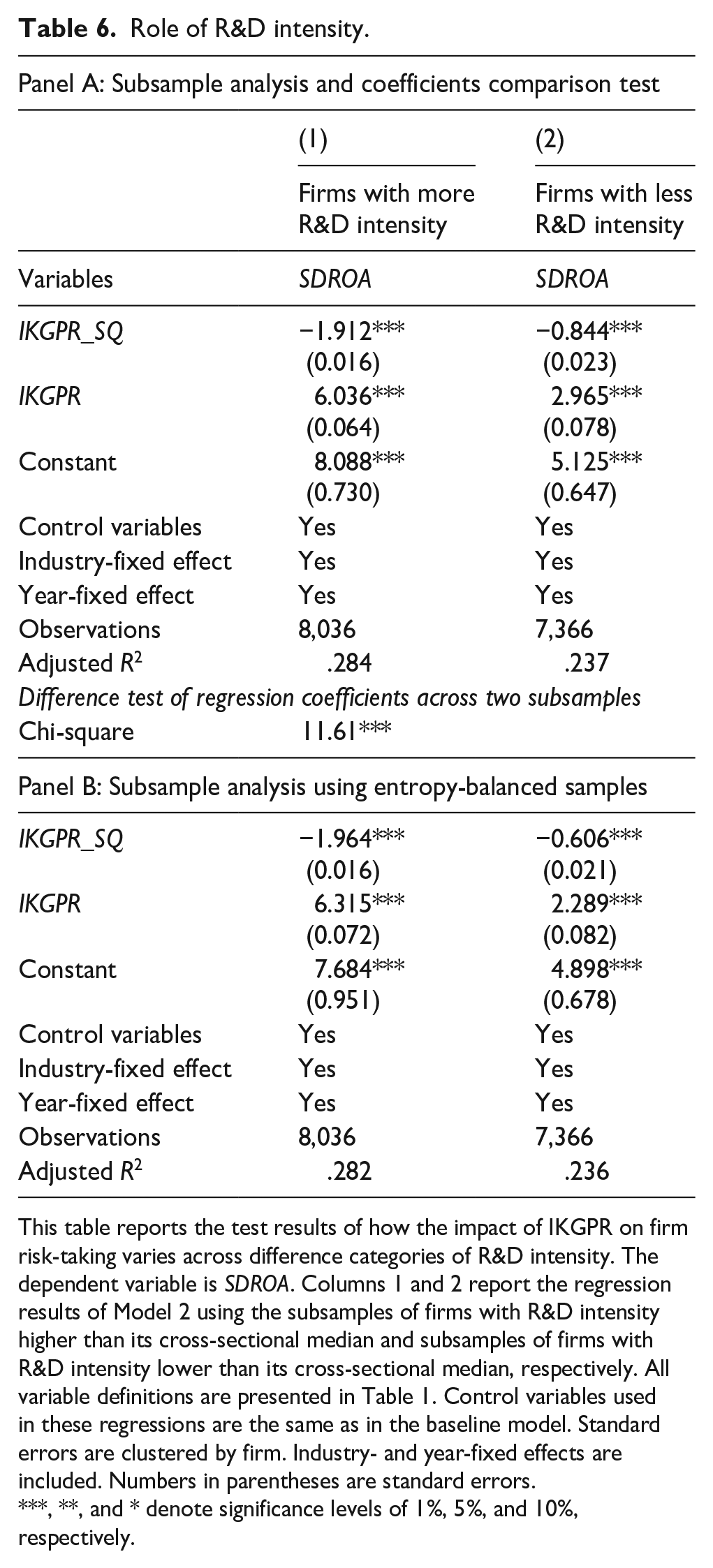

Some argue that firms with more R&D orientation generally have different degrees of risk compared to other firms (Hsu et al., 2015; Jia, 2018). Therefore, firms may react differently to macro-level risk and uncertainty in regard to their current degree of R&D intensity (Czarnitzki & Toole, 2011; Hoang et al., 2022; Vo & Le, 2017). In this vein, we test whether the risk-taking pattern differs across different categories of corporate R&D intensity. We sort firms by R&D intensity (i.e., the R&D expenditure to net sales ratio) and define firms with R&D intensity higher than its cross-sectional median as firms with more R&D intensity, and vice versa. We then re-perform the baseline regression on the subsamples of firms with higher and lower R&D intensity and compare the coefficients of IKGPR_SQ in the two regressions. As a caution, we again use the entropy balancing weights to check the robustness of the empirical results. Table 6 reports the regression results. In general, we find the coefficients of IKGPR_SQ in all regression specifications negative and significant at 1% level, however, with different magnitudes. Specifically, in Panel A of Table 6, where we do subsample analysis without the entropy balancing weights, the size of the negative effect of Inter-Korean geopolitical risk seems to be larger in the group of firms with higher R&D intensity compared to the group of firms with less R&D intensity (−1.912 compared to −0.844, respectively). The test of coefficient difference indicates the difference in the coefficients of IKGPR_SQ is statistically significant with a chi-square of 11.61 (p < 0.01). We document similar findings with subsample analysis using entropy balancing weights in Panel B of Table 6. The results show the heterogeneity in the responses of South Korean firms to geopolitical risk across different categories of corporate R&D intensity. Our finding corroborates the view of previous literature that technology intensity associates with less volatile future performance (Pandit et al., 2011).

Role of R&D intensity.

This table reports the test results of how the impact of IKGPR on firm risk-taking varies across difference categories of R&D intensity. The dependent variable is SDROA. Columns 1 and 2 report the regression results of Model 2 using the subsamples of firms with R&D intensity higher than its cross-sectional median and subsamples of firms with R&D intensity lower than its cross-sectional median, respectively. All variable definitions are presented in Table 1. Control variables used in these regressions are the same as in the baseline model. Standard errors are clustered by firm. Industry- and year-fixed effects are included. Numbers in parentheses are standard errors.

, **, and * denote significance levels of 1%, 5%, and 10%, respectively.

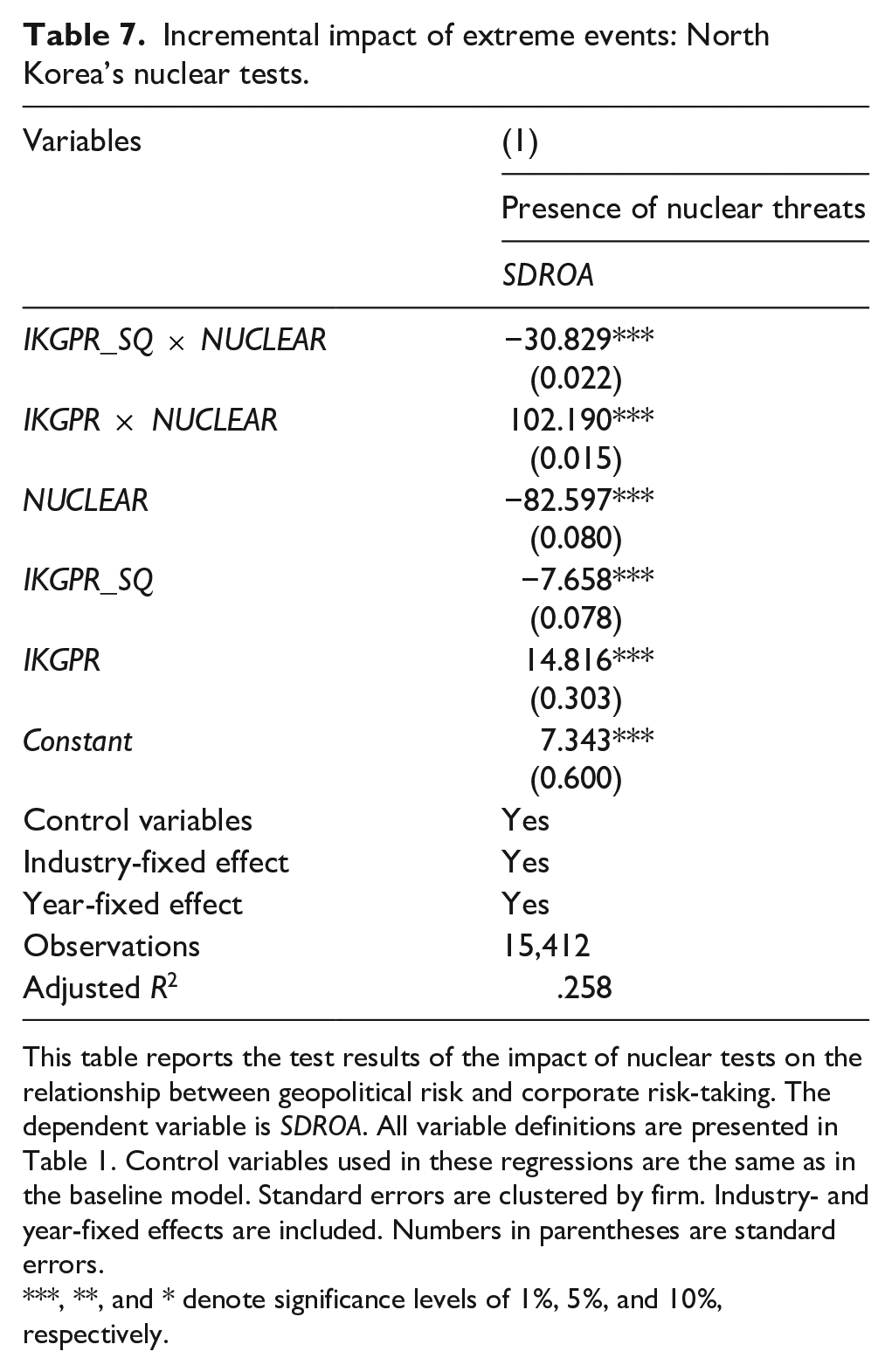

Given the fact that the nuclear threat from North Korea is visible to South Korea, it is compelling to examine how South Korean firms react to the nuclear tests on the other side of their northern border. We use the number of North Korea’s nuclear tests per year (NUCLEAR) as a measure of the nuclear threat to South Korean firms. To date, there has been a total of six observable nuclear tests within North Korea’s border. The year 2016 witnessed a record of two consecutive nuclear tests in North Korea, thus raising serious concerns about the nuclear risk in the Asia-Pacific region. To see how such events influence corporate risk-taking of South Korean firms, we interact NUCLEAR with IKGPR_SQ and IKGPR in Model 2, then perform the regression. The estimation results are in Table 7. The results show that the coefficient of the interaction term between NUCLEAR and IKGPR_SQ is negative and significant at 1% level, suggesting that the presence of nuclear threats magnifies the impacts of Inter-Korean geopolitical risk on corporate risk-taking.

Incremental impact of extreme events: North Korea’s nuclear tests.

This table reports the test results of the impact of nuclear tests on the relationship between geopolitical risk and corporate risk-taking. The dependent variable is SDROA. All variable definitions are presented in Table 1. Control variables used in these regressions are the same as in the baseline model. Standard errors are clustered by firm. Industry- and year-fixed effects are included. Numbers in parentheses are standard errors.

, **, and * denote significance levels of 1%, 5%, and 10%, respectively.

In summary, our further analyses demonstrate the variations of the impact of Inter-Korean geopolitical risk on firm risk-taking in the cross-section and in extreme events. We show that firms experienced Inter-Korean wars are less affected by increased geopolitical risk because they have survived even harsher situations. Furthermore, we indicate how the extreme nuclear test events and R&D intensity influence South Korean firms’ risk-taking behavior.

Conclusion, limitations, and future research

This article is the first study that discloses how exogenous geopolitical risk affects corporate risk-taking behavior in the unique context of South Korea. The empirical results show an inverse U-shaped relationship between Inter-Korean geopolitical risk and corporate risk-taking, suggesting that South Korean firms take risk only when geopolitical risk is low and refrain from doing so when the risk is high. Our findings survive a wide range of robustness tests, including different model specifications, alternative sample choices, alternative variable measurements, and the entropy balancing approach. This asymmetric risk-taking pattern suggests that South Korean firms rationally distinguish between taking risk and gambling, thus reacting differently to different degrees of external they have to bear. Our study contributes to the extant literature by investigating the relationship between geopolitical risk and corporate risk-taking in a modern civil war setting.

We acknowledge several limitations of this study that should be addressed in future research. First, we cannot examine North Korean firms’ risk-taking behavior in response to Inter-Korean geopolitical risk due to a lack of data. As business data from North Korea have never been available to the public, we can only use South Korean firms’ data to study this topic. This limitation prevents us from looking at the relationship from both sides (e.g., the North and the South of Korea). As firm reactions to heightened geopolitical risk might be different from the North to the South of Korea, it is compelling for future research to study this matter further when the North Korean economy integrates into the world economy and more data become available. Second, although we employ intensive control for potential confounding factors in our empirical model and a robustness test purging the effects of China and Russia politics on Inter-Korean geopolitical risk, we cannot control for the other potential impacts of foreign interventions (e.g., the interventions from the US government and the United Nations) as factors that constrain the geopolitical tensions in the Korea Peninsula. Foreign interventions are arguably unobservable and also may not have a linear effect, if any, on the geopolitics of the peninsula. Therefore, instead of incorporating overly complicated factors without a good method to quantify them, we rather keep the analysis concise and concentrated. We leave this matter to future research when a relevant methodology is available to do so. Besides, our study only observes the nexus between Inter-Korean geopolitical risk and firm risk-taking before the COVID-19 pandemic due to data availability. The global impact of COVID-19 from 2020 to 2022 may result in significant changes in Inter-Korean geopolitical risk and firm risk-taking relationship. Hence, future related studies may include the influence of the worldwide pandemic on the investigation. In addition to the above suggestions, the prospective research may explore other aspects of corporate behavior under extreme geopolitical risk in the context of the Korea Peninsula or similar contexts to provide more comprehensive perspectives and directions for business management and decision-making.

Footnotes

Appendix 1

Correlation matrix.

| Variables | (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) | (11) | (12) | (13) | (14) | (15) | (16) | (17) | (18) | (19) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (1) SDROA | 1.000 | ||||||||||||||||||

| (2) SDROE |

|

1.000 | |||||||||||||||||

| (3) IKGPR_SQ |

|

|

1.000 | ||||||||||||||||

| (4) IKGPR |

|

|

|

1.000 | |||||||||||||||

| (5) MA3_IKGPR |

|

0.002 |

|

|

1.000 | ||||||||||||||

| (6) IW_IKGPR |

|

|

|

|

|

1.000 | |||||||||||||

| (7) DW_IKGPR |

|

|

|

|

|

|

1.000 | ||||||||||||

| (8) RES_IKGPR |

|

0.013 |

|

|

|

|

|

1.000 | |||||||||||

| (9) SIZE |

|

|

|

|

|

|

|

|

1.000 | ||||||||||

| (10) ROA |

|

|

|

|

|

−0.012 |

|

−0.011 |

|

1.000 | |||||||||

| (11) LEVERAGE |

|

|

|

|

|

|

|

|

|

|

1.000 | ||||||||

| (12) GROWTH |

|

0.004 |

|

|

|

|

|

|

|

|

−0.011 | 1.000 | |||||||

| (13) CASH |

|

0.011 |

|

|

|

|

|

|

|

|

|

|

1.000 | ||||||

| (14) FIXED_ASSETS |

|

|

|

|

|

|

|

|

|

|

|

|

|

1.000 | |||||

| (15) CASHFLOW |

|

|

0.011 |

|

|

|

|

0.004 |

|

|

|

0.010 |

|

|

1.000 | ||||

| (16) ZSCORE | −0.003 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1.000 | |||

| (17) MTB |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1.000 | ||

| (18) SRETURN |

|

|

|

−0.012 |

|

|

0.002 |

|

|

|

|

|

|

0.006 |

|

|

|

1.000 | |

| (19) FIRM_AGE |

|

|

|

|

|

|

|

−0.012 |

|

|

|

|

|

|

|

|

|

−0.003 | 1.000 |

This table reports the pairwise correlation matrix of Inter-Korean geopolitical risk measures and firm-level variables used in the baseline model. Bold numbers represent the correlation coefficients that are significant at 10% level or stronger.

Acknowledgements

We thank both referees for suggesting additional robustness tests. We thank Referee 2 for suggesting this analysis. This research is partly funded by University of Economics Ho Chi Minh City (UEH), Vietnam.

Authors’ note

Khanh Hoang is also affiliated to Lincoln University, Lincoln, New Zealand.

Author contributions

K.H. analyzed and interpreted the data. H.V.H. provided the literature review for the manuscript. D.L.T.A. wrote the introduction, conclusion, and implication for this study. All authors read and approved the final manuscript. All authors read and approved the final manuscript.

Availability of data and materials

The data that support the findings of this study are available from different open sources (as stated in the study) and Bloomberg but restrictions apply to the availability of these data, which were used under license for the current study, and so are not publicly available. Data are, however, available from the authors upon reasonable request and with permission of Bloomberg.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research is partly funded by University of Economics Ho Chi Minh City, Vietnam.