Abstract

The disruption of the trade and investment activities of multinational enterprises as a consequence of the Covid-19 pandemic has reinvigorated the debate on the configuration of global value chains (GVCs) as well as the risks and challenges associated with offshoring. This article depicts how the pandemic might affect GVC configuration by driving a trend toward a more regional footprint in industries in which resilience and reliability are critical. Such a shift would create new opportunities for reshoring, and affect both the types of upgrading trajectories and the governance systems in value chains. The article also draws from the intersection of the global-strategy and value-chain fields to propose potential topics and avenues for further research related to these trends.

Keywords

Introduction

Over the past decade, global value chains (GVCs) have entered a period of transformation. The influence of some macro-level trends, such as protectionism, interventionist public policies, sustainability, and the use of digital technologies in manufacturing, suggests a move toward a certain degree of de-globalization (Petricevic & Teece, 2019). De-globalization has been further exacerbated by the Covid-19 pandemic. One of the pandemic’s most visible effects has been its impact on the structure and resilience of GVCs (Organisation for Economic Co-Operation and Development [OECD], 2020). The efficiency of many chains has been disrupted by the wide range of government measures introduced to control the pandemic, which have contributed to the economic slowdown due to the growth in protectionism (Juergensen et al., 2020). In a related development, digital solutions have come to the fore in response to the pandemic as seen, for instance, in online shopping and remote working. These new challenges are also contributing to the reconfiguration of GVCs and, thus, to the adoption of different managerial responses at the firm level.

The debate on the evolving geographical configuration of GVCs predates the pandemic (e.g., Hernández & Pedersen, 2017). Earlier studies on the geographical scope of GVCs indicated that supply chains tend to operate regionally rather than globally (Rugman et al., 2009; Rugman & Verbeke, 2004), and that they are clustered around one of the three main economic hubs of the global economy: Europe, Asia, and the Americas (Baldwin & López-González, 2015). Other studies demonstrated that supply-chain trade appears to be global if the focus is on value-added rather than gross trade flows. These studies suggested that some researchers overestimated internal regional trade in downstream activities (Loss et al., 2015) and disregarded externalized value creation through global networks (Mudambi & Puck, 2016). Nevertheless, there is a widespread perception that supply chains have become more global and increasingly dependent on emerging economies. A salient outcome of this globalization of value chains has been growth in offshoring, which has been widely embraced by firms in developed markets with the aim of reducing costs and improving efficiency (Pla-Barber et al., 2019).

A number of prominent intellectuals (Enderwick & Buckley, 2020; Gereffi, 2020; Shih, 2020; Zhan, 2021) have suggested that the pandemic will result in a more fragmented and regionalized world economy. They argue that such a configuration might address some of the weaknesses of globalization by introducing global supply chains that combine efficiency with resilience and sustainability (Pananond et al., 2020). In fact, a recent survey-based study (McKinsey 2020) reported that 93% of respondents planned to increase the level of resilience across their supply chains using a variety of mechanisms, including reshoring and regionalization.

In light of these developments, we analyze how the Covid-19 pandemic might affect GVC configuration and how firms may adjust their strategies regarding the location of different activities as well as their governance. As a complement to recent work (Hernández & Pedersen, 2017; Kano et al., 2020; Pananond et al., 2020; Pérez et al., 2020), we also highlight several avenues for further research at the intersection of global-strategy and value-chain analysis. By considering the firm’s position within its GVC, we can extend the efficiency-based approach taken in the global-strategy literature to include the dynamics that affect decision-making at the level of the value-chain network. As it draws on the complementarities between the two fields, this article provides a key tool for management scholars interested in applying the GVC framework.

GVC dimensions: governance and upgrading

As organizational systems, GVCs involve a constellation of interconnected companies through a worldwide network of organizational agreements (Giroud & Mirza, 2015). As such, the global economy can be viewed as a “complex and dynamic economic network made up of inter-firm and intra-firm relationship[s]” (Gereffi, 1994, p. 10). Buckley and Ghauri (2004) define GVCs as globally dispersed networks formed by companies with different objectives that jointly develop activities traditionally carried out by a single entity. Such networks have no legal identity, and they are orchestrated or led by a company that controls critical assets, intermediate products, and knowledge flows. In this perspective, the focus shifts from a single company’s value chain to the linkages and relationships that exist among the companies in a GVC (Buckley, 2009). The companies that orchestrate GVCs are usually multinational entreprises (MNEs). They play a prominent role as leaders in the distribution of value among suppliers and customers and in the coordination of activities among different actors across the chain (De Marchi et al., 2014). For a lead firm, ownership of all units in the chain is not a necessary condition for effective coordination and control. In the GVC literature, two influential concepts explain these relationships and their dynamics: the governance of the GVC and the upgrading processes undertaken by various GVC actors. These concepts approach the GVC phenomenon from a top-down and bottom-up perspective, respectively (Gereffi & Fernandez-Stark, 2011).

The governance of a value chain is defined as “both the process by which particular players in the chain exert control over other participants and how these lead firms appropriate or distribute the value that is created along the chain” (Bair, 2009, p. 9). Based on this perspective of relative power across actors, GVCs can be classified into five main categories. At the two extremes, we find the classic governance structures proposed by transaction cost theory (Williamson, 1986): the hierarchy, which emerges when highly complex transactions among actors favors the internalization of activities within the orchestrating firm; and the market, which arises when less complex transactions allow for coordination of activities through the market price. Between these two extremes, we find hybrid forms of GVCs that entail certain degrees of cooperation among companies and involve mechanisms of mutual control: (a) modular chains, which result from transactions that are relatively easy to codify, and in which the suppliers’ investments in specific assets and the exchange costs are low; (b) relational chains, which are characterized by close interactions among actors (i.e., the lead company and its suppliers), as these relationships incorporate complex information that is usually tacit and is not easily transmitted or learned; and (c) captive chains, which often appear when a lead company has significant power over small suppliers that depend on it (De Marchi et al., 2014; Gereffi et al., 2005).

The identification of the nature and governance of the value chain is essential for understanding the second key concept—upgrading. “Upgrading” is defined as the dynamic movement of an actor in the value chain toward activities of greater value and better performance (Humphrey & Schmitz, 2002). A firm can upgrade its competitive position in a GVC by improving processes or products, or by taking on higher functions within the chain. Alternatively, it can move to a new value chain. Generally, upgrading possibilities depend on the GVC’s governance structure (Golini et al., 2018) as well as the internal capabilities of the companies involved in that GVC (Giuliani et al., 2005). Most studies on upgrading have considered the buyer–supplier transaction, with the supplier typically being an independent contractor from a developing country (e.g., Lechner et al., 2020). However, recent research (Ryan et al., 2020), including the upgrading dynamics in intra-MNE GVCs, shows how upgrading accomplished by a subsidiary could become a key determinant of changes in GVC governance.

Effects of the Covid-19 pandemic on GVCs

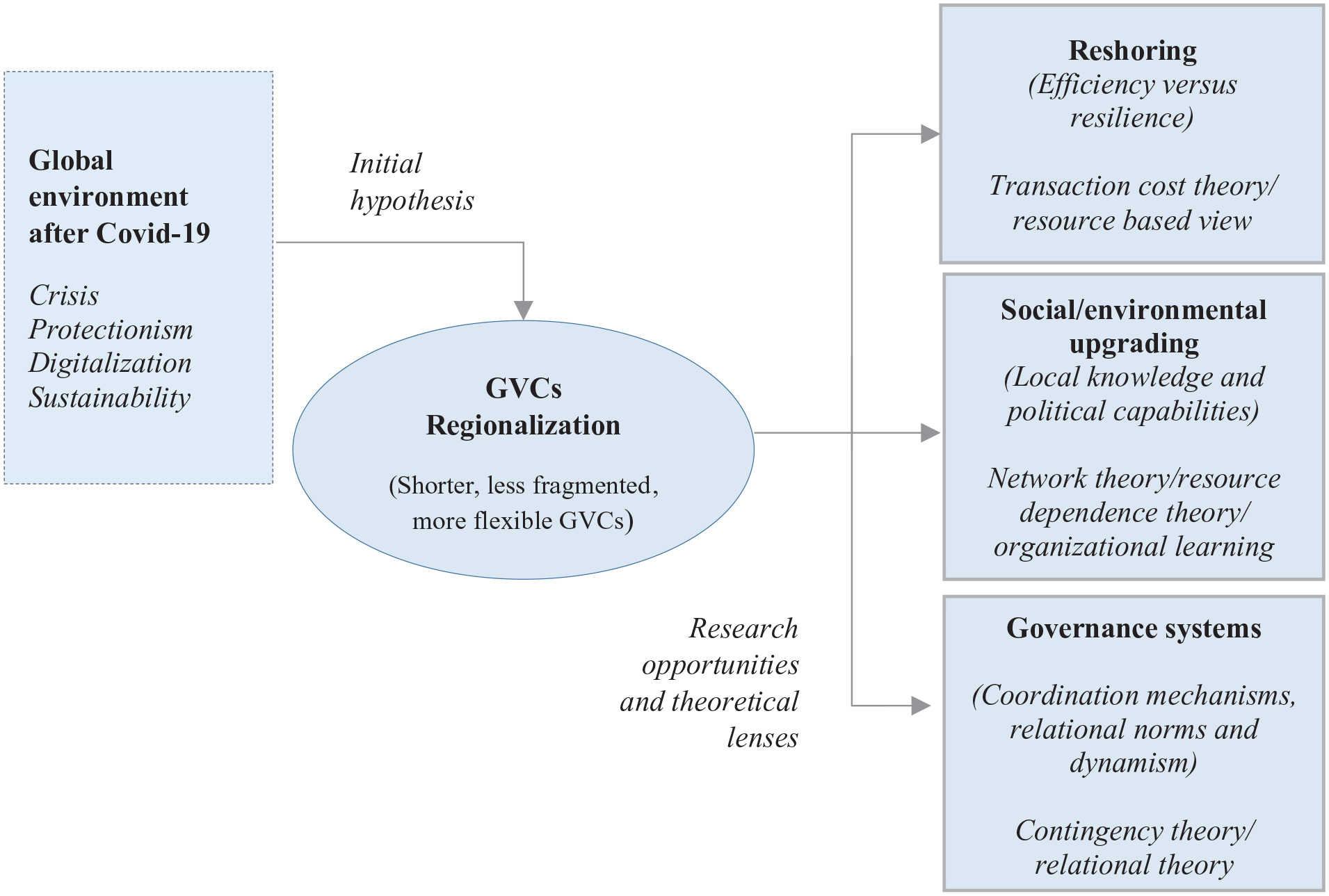

Based on these foundations in the extant literature, we have identified three possible effects that the Covid-19 pandemic may have on the basic dimensions of GVCs, thereby creating new challenges for companies operating in those chains and opening up new avenues for future research. Our initial hypothesis is that, after the pandemic, the new global conditions will trigger a reconfiguration of GVCs, which may evolve toward a more regional footprint in some industries. To a certain extent, this may lead to the return of production previously outsourced to third countries to firms’ home countries, which is known as “reshoring.” This regionalization of the GVCs would also have effects on the types of upgrading trajectories as well as the governance systems in GVCs.

Figure 1 presents the overarching framework that guides the development of our contributions in this article. We highlight not only possible research topics but also the different theoretical lenses that can be applied in attempts to understand these new trends in the global economy.

Framework for research on transformation of GVCs.

The regionalization of GVCs

In the new global context of increasing protectionist policies and pressures for a more sustainable economy, the Covid-19 crisis has strengthened the trend toward GVC reconfiguration (Javorcik, 2020). Disruptions in the supply end of many value chains, shortages of essential products, and volatility in the prices of certain raw materials and final products have revealed the limits of sourcing in distant economies. In the medium to long term, GVCs may be reconfigured to reduce risk by making them more regional or local, reducing the number of linkages, and trading-off productive efficiency for improvements in supply security (Shih, 2020). As such, these reconfigured chains will be organized for collaboration among economies that are geographically close (Gandoy & Díaz-Mora, 2020). Moreover, the leading multinational companies in these chains—both manufacturers and large distributors—are likely to diversify their supplier base by fostering longer-term cooperative relationships on a regional level (McKinsey, 2020). This regionalization could be the result of either a pullback of value-chain configuration from the global to the regional level (with global MNEs replicating value chains at the regional level) or the growth of international production on a regional basis (with MNEs structuring their operations closer to home) (United Nations Conference on Trade and Development [UNCTAD], 2020).

However, the reorganization of GVCs will not be easy. It will be necessary for GVC actors to accept the costs associated with introducing new infrastructure and technologies as well as to seek out new, reliable suppliers. In addition, the destruction of the industrial base in many developed countries has reduced the availability of raw materials and intermediate products, which may increase the risk of shortages in some chains (Gandoy & Díaz-Mora, 2020). Arguably, this shift is unlikely to occur immediately. Nonetheless, we expect companies to reconfigure their GVCs based on the type of chain and the location of final markets, which should drive their choice of production sites (McKinsey, 2020).

We acknowledge that not all value chains will regionalize with the same intensity or to the same extent. Certain economic factors associated with specific supply chains still influence the geography of production. In industries where cost and scale economies are key competitive factors (e.g., textiles and apparel), a more global configuration remains the most efficient way of organizing, especially when distributors keep pushing for low prices and lean inventories (Pérez et al., 2020). Other sectors in which key inputs are location-bound (e.g., industries that rely on extracted natural-resource inputs, such as mining, agriculture, and energy; Narula, 2018) are also likely to be unaffected by regionalization trends. However, some non-economic factors, such as government policies to reinforce national security and competitiveness, are likely to play a prominent role in the re-routing of GVCs. The pandemic has driven home the importance of self-sufficiency in food, pharmaceuticals, and certain medical equipment (McKinsey, 2020). In other cases, some nations will enact industrial policies to safeguard emerging technologies (e.g., artificial intelligence, renewable energy, 5G equipment; Miroudot, 2020).

In general, we expect to see a stronger tendency toward regional configuration of value chains in certain tipping-point industries with medium-high innovation intensity and product differentiation or customization (e.g., machinery and equipment, electronics, and automotive), (UNCTAD, 2020). In this article, we focus on this group of industries. We argue that, for these industries, new trends and research opportunities are arising in three domains: the relocation of production (reshoring); upgrading processes; and governance systems, including mechanisms that support relationships and coordination among actors.

Reshoring

Prior to the Covid-19 pandemic, digitization and the introduction of new manufacturing technologies (e.g., automation, robotics, 3D printing) pointed to the possible return of some production processes (reshoring) from emerging countries to MNEs’ home countries or to a nearby country that belongs to the same region. Digitization allows firms to achieve cost control while reducing the physical distance to the target market. Examples of reshoring driven by new manufacturing technologies have been observed in manufacturing sectors where customization requirements and the speed of response prevail over costs (Ancarani et al., 2019; Strange & Zucchella, 2017). These new manufacturing technologies enable more integrated production methods and reduce transaction and governance costs. At the same time, they allow for the introduction of more effective services (servicification) in the final product (Cirilo & Molero-Zayas, 2019). Both aspects reduce the importance of labor costs and intensify the need for concentrated production to exploit economies of scale. Above all, they enable the company to be closer to the customer by narrowing the spaces between the links in the chain and, therefore, make global fragmentation less attractive (Dachs et al., 2019).

The possible regionalization of some value chains is reinforcing this tendency and moving companies closer to the tipping point for adopting reshoring decisions. Although the macroeconomic figures are still inconclusive, recent empirical evidence supports this hypothesis. For example, Barbieri et al. (2020) highlight several cases of European companies that decided to move production back to Europe. Their decisions were triggered by the new conditions generated by the Covid-19 pandemic and the need to reduce the exposure to risk.

Opportunities for research and theoretical lenses

New opportunities for research in this area are evident on both the theoretical and empirical levels. From a theoretical perspective, transaction cost theory (Williamson, 1986) and the resources and capabilities view (Grant, 1996) are still relevant for explaining reshoring decisions. From a transaction cost perspective, the relocation of industrial activities is explained by the increase in coordination and control costs in the value chain. These additional costs are caused by macro-level institutional trends (e.g., protectionism, volatility) and micro-level cascading effects, such as the unexpected costs associated with managing the complexity of offshoring operations that have emerged during the pandemic. Such costs have been particularly evident in those companies with less experience and a weaker orientation toward organizational design in their offshoring strategy (Larsen et al., 2013). The resource-based view suggests that the reshoring of operations is justified by the growing importance of innovation and quality, which can be enhanced through the location of R&D and production centers closer to the end customer (Pisano & Shih, 2012), and by the need to safeguard intellectual property rights (Tate et al., 2014).

In this new context of shorter, more flexible value chains, it seems pertinent to address questions on the slicing of activities across different locations. At the empirical level, a fruitful path might be to analyze the optimal level of regionalization in each value chain that could trigger the reshoring process and to examine the variables that might have a decisive influence in each of the different chains.

The regionalization trend also raises the discussion of how leading firms can build greater resilience by reshoring GVC activities while maintaining efficiency. Given the wave of severe disruptions, GVCs need to prioritize resilience over efficiency (Gölgeci et al., 2020). In the long run, both efficiency and resilience need to be maintained concurrently in order to avoid a swing back toward offshoring. As such, research focused on determining the most appropriate ways to jointly generate resilience and efficiency after taking the idiosyncrasies of each chain into account could be productive. For example, one way to increase resilience is to diversify sourcing, although doing so could increase costs. In some value chains, long-term purchasing commitments can reduce knowledge asymmetries and give new suppliers an incentive to invest, thereby improving efficiency (Shih, 2020). The orchestrating firms will need to intelligently leverage the full potential of digitization (e.g., AI, robotics, tracking technologies, automation) to monitor and collaborate across regional value chains (Daniels et al., 2021). Alternatively, they can choose to rely on social mechanisms, such as improving the quality of ties and establishing multilateral feedback mechanisms among GVC partners (Gölgeci et al., 2020).

Upgrading trajectories and local linkages

The second line of research arising from the potential regionalization of value chains and the effects of the Covid-19 pandemic revolves around upgrading trajectories and the role that local linkages play in this process. Traditionally, the GVC framework has primarily focused on technological resources as the main trigger of economic upgrading. In parallel, studies in the field of global management have offered some empirical evidence on the improvement of certain subsidiaries as centers of excellence (Holm & Pedersen, 2000), mainly through the acquisition of technical skills (Pananond, 2013). A center of excellence is an important source of value creation, as its capabilities can be leveraged by and disseminated to other parts of the firm (Frost et al., 2002). The formation of these centers is linked to three main factors: the characteristics of the subsidiary’s internal resources, the subsidiary’s relationship with the rest of the MNC, and the subsidiary’s external relationships in the local context (Andersson & Forsgren, 2000). As chains become more regional and flexible, external relationships and local knowledge become critical mechanisms for driving these upgrading processes.

Capabilities other than those associated with product expertise, such as advanced local or regional knowledge (Pla-Barber et al., 2021) or institutional and political links at the local level (Kostova et al., 2016), are likely to be key determinants of competitiveness in regional value chains. In this regard, suppliers in GVCs contribute to knowledge creation and knowledge transfer, as they provide specialized, locally generated information. These interactions among actors in the GVC can increase knowledge connectivity at the regional level, and reduce the hierarchical distance between headquarters and subsidiaries and between lead firms and GVC partners (Cano-Kollmann et al., 2016).

In early GVC research, the idea of upgrading was focused on improvements in economic terms. However, the concept and forms of upgrading have evolved into a much more holistic vision in which social development is prioritized for counteracting the negative impact of globalization. Studies in this field could pay greater attention to the governance regulating the economic activity of companies (generally the lead company) as well as the actions that firms take to meet the expectations and standards of society and institutions (Narula, 2019). In fact, political activity and corporate social responsibility are considered the main “non-market” tools that can be used to improve performance by taking on the social and institutional context (Mellahi et al., 2016). Concepts such as social upgrading (Barrientos et al., 2016) and environmental upgrading (De Marchi et al., 2019) are expected to play a greater role in value-chain configuration in the future.

Opportunities for research and theoretical lenses

The joint analysis of market and non-market strategies offers an interesting avenue for research aimed at providing a holistic view of “integrated strategy” (Lawton et al., 2013). However, although some researchers have highlighted the relevance of complementing both dimensions (Mellahi et al., 2016), at the empirical level, we know little about how companies can take advantage of sustainability and social responsibility strategies to upgrade in a GVC. In this context, we believe that the application of business network theory (see Holm et al., 1999) could offer a much more detailed perspective on power dynamics, especially on how companies can capitalize on those dynamics to gain influence over the rest of the actors in the chain and be recognized by the lead companies.

Another potentially fruitful area of research resulting from the regionalization of GVCs would be to test what type of local knowledge—especially political capabilities—could allow firms to upgrade their positions in the GVC. Such information would be relevant for subsidiaries of MNEs as well as local small and medium entreprises (SMEs) that participate in these chains (Pla-Barber et al., 2020). The most appropriate theoretical approaches to answering this research question are those offering a “micro” vision of these upgrading processes, dynamic capabilities, and organizational learning approaches in an international context (Teece et al., 1997). These frameworks should be complemented with insights from network perspectives and/or resource dependence theory (Pfeffer & Salancik, 1978) to explain how companies can appropriate the value generated by upgrading their position in the GVC. Delving into the distinction between upgrading and the real appropriation of the new value-added created by the actors in GVCs, Dindial et al. (2020) show that suppliers would be able to appropriate more value if other firms (including the lead firms) become dependent on them or the resources they provide, regardless of the scope of their activities. In this sense, an upgrading trajectory can be considered a necessary but insufficient condition for capturing more value-added in a GVC. As such, more research is needed to determine the conditions under which different actors in the GVC are willing to effectively bargain for a share of the value-added derived from upgrading, especially if the new regionalization wave changes the power asymmetries across actors.

Governance systems, mechanisms of coordination, and dynamics

Our third line of research relates to how the wave of post-pandemic regionalization in some value chains will affect relationships and power dynamics in GVCs. The literature on global strategy suggests that the most basic way to control and integrate subsidiaries’ activities is through structural mechanisms of coordination executed by the lead company (Nohria & Ghoshal, 1994). At the same time, the GVC governance literature suggests that governance modes depend on the characteristics of the transaction (Gereffi et al., 2005). As we have discussed, this stream of research proposes five types of governance structures (hierarchy, the market, captive, relational, and modular). Consequently, effective control of relationships with other members of the chain is not executed through ownership but through power. Nevertheless, the GVC literature focuses on the industry level rather than the company level. Beyond identifying the leader in each chain, this field has not delved into the issue of power. The orchestrating firm usually occupies a strategic position within the network (Kano et al., 2020) but the existence of governance relationships does not necessarily explain the dynamics of power, especially when they are implemented outside the hierarchy (e.g., with partners’ suppliers). This is particularly true in developing countries where informal enterprises play a significant role in GVCs (Narula, 2019).

Given our belief in the likely regionalization of value chains, changes can also be expected in the evolution of the forms of governance and in the control mechanisms used by orchestrating companies. In this context, the governance systems established in some chains may not be the most adequate or they may need to evolve in order to better adapt to the new situation.

As such, it seems plausible that regionalization and the relocation of production centers closer to the final markets will allow for greater collaboration among lead companies and other actors in GVCs. In that case, GVCs could adopt more captive or relational types of governance. It is also possible that lead companies will try to control outsourced relationships in the regional value chain using the classical coordination and control mechanisms applied in headquarters–subsidiary relationships. Lead companies could increase their involvement through coordination mechanisms that facilitate higher control, such as the formalization and control of results (Ponte & Sturgeon, 2014), and through mechanisms that favor trust and dependence between partners, such as socialization (Kano, 2018) and the development of common values throughout the network (Ouchi, 1980). These coordination mechanisms might play a critical role in that they can reduce uncertainties regarding the behavior of different units in the chain and ensure the compatibility of objectives between leading companies and their suppliers.

Opportunities for research and theoretical lenses

At the theoretical level, the application of the classical literature on coordination and control mechanisms to non-hierarchical governance systems could lead to interesting contributions. In this regard, contingency theory (Nohria & Ghoshal, 1994) could provide a richer understanding of how relationships across GVCs are organized. Lead firms must consider the different contingencies associated with the context of each governance system and employ an appropriate set of structural elements to manage those contingencies. Analyses of the best combinations of coordination mechanisms for different governance systems would be a promising line of research.

This rationale could be extended with a relational view. The orchestrating firm’s role in the GVC is to improve efficiency and enhance knowledge exchange within the network while reducing the hazards of opportunistic behavior. Indeed, the predictability of partners’ behavior may be the biggest concern not only in equity alliances but also in international partnerships. The need to reduce uncertainties regarding partners within and outside of the value-chain points to the possibility of new avenues of research focused on relational perspectives (Dyer & Singh, 1998). In this sense, the well-established literature on commitment and trust in the field of export marketing relationships (i.e., Morgan & Hunt, 1994) could complement classical approaches in attempts to further explain the role of bilateral norms as quasi-governance mechanisms. Relational governance relies on trust and relational norms to coordinate and achieve long-term objectives, and it uses a self-enforcement approach partly based on social controls, such as reciprocity and goal congruence (Zajac & Olsen, 1993). Furthermore, these mechanisms require fewer resources than formal governance mechanisms, such as monitoring or incentives (Obadia et al., 2017). As such, this seems particularly interesting from the point of view of SMEs within GVCs, which usually lack the resources needed to implement or enforce a proper contract with a lead company.

In times of crises and disruption, governance and coordination mechanisms must be adjusted to the new circumstances not through rational analysis but through incremental learning, creation, and trust-building processes (Vahlne & Johanson, 2021). In this sense, it would be interesting to test whether lead firms develop less complex formal mechanisms and rely more on informal mechanisms, such as relational capital (Kano, 2018) or socialization (Zeng et al., 2018), to facilitate knowledge transfers and reinforce parties’ willingness to contribute to a more socially cohesive regional chain.

Conclusion

In this article, we have attempted to deepen our understanding of how the Covid-19 pandemic will affect the configuration of GVCs, and we have presented three potential avenues for cross-disciplinary research in the GVCs and global management fields. At the theoretical level, potential research questions could be grounded in a wide variety of theories, including classical, efficiency, and resource-based theories (e.g., transaction cost theory, resources and capabilities theory, organizational learning) as well as in more recent approaches that emphasize relationships across actors in the value chain (e.g., network theory, resource dependence theory, the relational view).

In the midst of the pandemic, the momentum toward regionalization of certain GVC categories has been strong. That momentum is likely to increase after the pandemic, especially in industries where maintaining resilient supply-chain flows matters as much as cost and efficiency. These regional GVCs will be shorter and less fragmented. In addition, they are likely to involve more concentrated value-added at each stage (Zhan, 2021). Managers of the leading firms in these regional value chains should work to make them more resilient to the current pandemic and inevitable future shocks. The design of risk-management strategies, such as diversification of the supplier base, the reshoring of some activities, and the establishment of long-term relationships with suppliers, will help companies face new threats. In addition, managers need to introduce risk-monitoring systems and develop business-continuity plans to be used in the event of a disruption. Digitalization, scenario planning, and stress-testing will increasingly play pivotal roles in these processes.

Regionalization is also likely to stimulate the process of local development, thereby allowing for higher participation of local firms in value chains, decreasing firms’ environmental impact, and creating opportunities for value-chain upgrading. Managers of both the leading and the supplier companies must be aware that social and environmental issues will increasingly drive major strategic decisions in firms as well as government policies. Moreover, in contexts characterized by uncertainty, these managers should reinforce trust and relational norms in value-chain relationships with the aim of eliminating the harmful effects of power asymmetries, improving coordination, and shielding their firms against opportunistic behaviors.

Although it falls beyond the scope of our article, these trends will also have some repercussions for public policies. Developing countries have tended to attract supply-chain activities that not only emphasize low costs but are also less strategically important for both MNEs and national security. In such GVCs, we are less likely to see significant reshoring. Where resilience is a significant concern, such as in pharmaceuticals, the possibilities for economic upgrading may be reduced to a certain extent, which could have negative effects on employment. Developing countries may experience significant shortages on this type of products as their customers reshore activities to developed countries. This, in turn, may make it more difficult to access essential products (Miroudot, 2020), which may result in policies aimed at securing strategically important activities and creating barriers to reshoring. At the extreme, governments may implement restrictions on such repatriations. We also expect to see new strategies for attracting and embedding foreign direct investments to make them more locationally “sticky.” Finally, we expect developing countries also implementing similar policies to maintain resilience in key sectors by restricting exports of specific activities (Narula, 2020).

In developed economies, the transformation of GVCs will create new opportunities for governments to attract investors looking to diversify supply bases and build resilience. This may also help strengthen industrial clusters, thereby increasing industrial capacity and the production of final goods. Moreover, digitalization is likely to lead to a change in the dominant model of manufacturing, which is currently focused on large-scale production. Selective reindustrialization will take time and policy makers will have to adjust their policies to ensure that it is properly enforced.

It is certainly challenging to find positive aspects of the disruption caused by the Covid-19 pandemic. However, the crisis offers companies and governments a unique opportunity to rethink their activities and to contribute to a more sustainable future in business.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors are grateful for the financial support received from the Ministry of Economy, Industry and Competitiveness (ECO201785456R).