Abstract

Based on the institutional perspective, this article examines whether institutional pressures in home and host countries affect multinational enterprise (MNE) subsidiaries’ corporate social responsibility (CSR) practices and whether the institutional distance between home and host countries moderates these relationships. We collect data from 185 Chinese MNEs’ 349 foreign subsidiaries operating in 27 host countries and conduct a cross-classified multilevel model analysis of the data. The findings indicate that institutional pressures in home and host countries significantly affect the CSR practices of the MNE subsidiaries operating in host countries. Also, we find that the formal and informal institutional distances between the home and host countries exert different interaction effects on these CSR practices. The findings from this study offer useful implications for MNEs’ social strategies for sustainability.

Keywords

Introduction

When multinational enterprises (MNEs) internationalize (Villar et al., 2020), they face various institutional environments (e.g., local culture, ethical values, government regulations, and laws). For an MNE subsidiary to survive and succeed in the host country, it must cope with local environments that differ from those in the home country. Market strategies that concentrate simply on costs and benefits may be insufficient for MNE subsidiaries to adapt to diverse and complex environments. In the same vein, the importance of nonmarket strategies focusing on the role and performance of firms in institutional and social contexts has recently increased (Frynas et al., 2017). Considering the social aspects of corporate strategies (Mellahi et al., 2016), corporate social responsibility (CSR) is a critical axis of nonmarket strategy that represents firms’ duty to pursue their own interests while promoting and protecting social welfare beyond compliance (McWilliams & Siegel, 2001; Rodriguez et al., 2006). However, an MNE forms complex business networks worldwide through internationalization, and thus its subsidiaries experience different institutional backgrounds. The unique institutional setting in each host country may therefore lead to varying corporate social behaviors among subsidiaries. These explanations clearly indicate that the relationship between institutional environments and MNEs’ strategic responses to them should be studied from a social perspective. Hence, the key argument of this study is that institutions constrain MNEs’ CSR behaviors and thus produce varied social outcomes.

Prior studies on the relationships between institutional pressures under social environments and the CSR of MNEs have adopted institutional theory as the theoretical foundation (e.g., Beddewela & Fairbrass, 2016; Khan et al., 2015; Reimann et al., 2015). However, there are still two main research gaps in terms of MNEs’ CSR based on institutional theory. First, although some previous studies on MNE CSR deal with institutional pressures (Beddewela & Fairbrass, 2016), very few empirical studies consider both home- and host-country institutions altogether, and these are mainly concerned with how institutional voids influence MNE CSR (Kim et al., 2018). In this vein, this study analyzes how the institutional pressures from MNEs’ home and host countries affect their CSR strategies.

Second, the institutional distance between home and host countries may also influence an MNE’s ability to adapt to the local environment. Despite the considerable prior research on institutional distance in the MNE context (e.g., Brouthers & Brouthers, 2001; Xu & Shenkar, 2002), research explaining the extent to which cross-national distance influences MNE subsidiaries’ CSR behaviors is still in its infancy (Reimann et al., 2015). The extant literature on institutional distance between MNEs’ home and host countries investigates the impacts of such a distance, including cultural (e.g., Dikova et al., 2010), political (e.g., Rodgers et al., 2019), economic (e.g., Campa & Guillén, 1999), psychological (e.g., Ellis, 2008), and geographic (e.g., Li & Vashchilko, 2010) distances. However, with a few exceptions (e.g., Campbell et al., 2012), studies examining the relationship between institutional distance and CSR adopt only one institutional pressure at a time (e.g., Reddy & Hamann, 2018; Reimann et al., 2015). In contrast, we assume institutional pressures at both formal and informal levels, using institutionalism to explore the impact of institutional distance on CSR practices. Thus, our research questions are as follows:

To what extent do institutional pressures in home and host countries affect MNE subsidiaries’ CSR practices?

Does the institutional distance between home and host countries moderate the relationship between institutional pressures in both home and host countries and MNE subsidiaries’ CSR practices?

This study contributes to the CSR literature in two ways. First, it brings the institutional perspective on MNEs into conceptualization to account for how the demands of the social environment shape the local CSR activities of MNE subsidiaries. Thus, the study deepens the institutional perspective as a theoretical foundation to explain MNE subsidiaries’ CSR by examining both home and host country institutional pressures on them. Our findings demonstrate that through interactions with governments and nongovernmental organizations (NGO) overseas, MNEs comply with institutional pressures, thereby producing social outcomes. Second, this research identifies the influence of cross-national institutional distances on the relationship between local social pressures and the CSR decision-making process of MNEs. Our findings illustrate how the differences in institutional and social characteristics between the home and host countries are related to the CSR practices of MNE subsidiaries. In summary, this study demonstrates that MNEs’ CSR can be socially strategized.

Theory and hypotheses

Formal and informal institutional pressures toward CSR

MNEs’ CSR practices differ remarkably across countries and organizations because they meet local institutions in foreign markets (Yang & Rivers, 2009). MNE subsidiaries may adopt CSR practices that seem particularly appropriate to their overseas environment to overcome the uncertainty of local business activities and acquire legitimacy (Reimann et al., 2012). In institutional theory, institutions have a substantial influence on the behavior of individuals and organizations in society. According to North (1991), institutions provide interaction and trade among organizations with a stable structure by reducing rampant uncertainty in society. Formal institutions, such as government regulations and laws, shape the frame of activities through rules, regulations, and legislation that coerce firms into compliance (DiMaggio & Powell, 1983; North, 1991; Peng et al., 2008; Scott, 2007). Meanwhile, informal institutions depend on normative and cognitive elements, such as norms, values, and culture, to mold organizations’ behavior (North, 1991; Scott, 2007). These institutions serve as the “rules of the game” in business activities (North, 1991). Organizations are under constant pressure to adapt to a particular structure or a mechanism and go through institutional isomorphism, in which actions are repeated and become routine over time (DiMaggio & Powell, 1983; Jackson & Deeg, 2008; Khan et al., 2015). Following predominant norms and traditions in a social context, firms tend to have commonality among firms in their structure and activities, and this isomorphism can be explained by the actions taken by the firm as a result of its attempts to gain legitimacy (DiMaggio & Powell, 1983).

Legitimacy is defined as “a generalized perception or assumption that the actions of an entity are desirable, proper, or appropriate within some socially constructed system of norms, values, beliefs, and definitions” (Suchman, 1995, p. 574). By obtaining legitimacy, MNEs alleviate uncertainty and discrimination risks in local society, thus securing competitiveness and a stable local operation (Kuznetsov & Kuznetsova, 2012). Thus, suitable CSR approaches are based on local institutions, such as shared values and behavioral norms among members of local society. Conforming to institutional pressures enables MNEs to succeed in obtaining support and legitimacy from the society in which they operate (Khan et al., 2015; Oliver, 1991). An MNE that adheres to local laws (formal institutions) or accepts cultures (informal institutions) may be recognized as a member of the society and is likely to sustain its business in an overseas market. Tan and Wang (2011) suggest that the ethical expectations and pressures of the host country can be different from those of the home countries and can thus shape MNE subsidiaries’ CSR approach. That is, a proper CSR approach is based on institutional environments, including laws and rules, shared values, and codes of conduct among community members (Beddewela & Fairbrass, 2016; Campbell, 2007; Campbell et al., 2012; Park et al., 2014).

Institutional theorists have a commonality in that they illuminate the forces and methods that compel firms to meet the demands of society to obtain social support and legitimacy (Beddewela & Fairbrass, 2016; Campbell, 2007; Park et al., 2014; Yang & Rivers, 2009). Institutional agents infuse local institutional pressures into MNEs, thereby substantially affecting their CSR activities. Institutional mechanisms, especially in the case of informal normative and cognitive institutions, typically possess invisible and intangible characteristics, which complicates the process of determining CSR strategies in host countries. In order for changed institutions to be transferred to the firm (i.e., institutional isomorphism), the social actors first need to directly interpret these institutions for the firm. For instance, even when environmental legislation is enacted or cultural perceptions change, MNEs may show passive responses if there is a lack of contact and dialogue with institutions. From an institutional perspective, Beddewela and Fairbrass (2016) find regulatory and normative isomorphic pressures from institutional actors, such as governments or NGOs. MNE subsidiaries not only have to mimic and conform to the institutional environment of their home country but must also be concerned with the demands of key agents who channel and emphasize institutions. Thus, taking the institutional perspective on MNE subsidiaries can be a useful conceptual foundation for their CSR behaviors.

Based on the literature, governments and NGOs as influential agents form formal and informal institutions and exercise pressures on subsidiaries in host countries. Local governments urge and enforce regulations and legal systems, and NGOs require MNEs to share the values and norms of the local society. Thus, they are salient influencers and exercisers involved in the business environment or institutions that affect operations in overseas markets (Reimann et al., 2012; Yang & Rivers, 2009). If MNEs pass over the institutional pressures from host country governments and NGOs, 1 they may delay acquiring legitimacy or face operational risk. In addition, subsidiaries should take into account not only the institutional environment of the host country but also the institutional pressures from the home country. The institutional characteristics of the political environment in the home country are likely to determine whether and how MNEs pursue CSR (Detomasi, 2008). The political system and legal characteristics of the home country affect the MNE subsidiaries’ CSR decision-making. Therefore, the home-country institutional pressures perceived by MNEs may perform an important role in shaping their CSR practices in the host country. Moreover, government regulation and laws in home and host countries are generally codified and published, meaning they are classified as formal institutions (DiMaggio & Powell, 1983; North, 1991; Scott, 2007). MNEs’ managers may easily grasp and address the formal pressures and thus are likely to effectively show their perceptions. In contrast, the informal pressures from NGOs cover a variety of social issues reflecting the norms, values, and culture of the countries (North, 1991; Scott, 2007), which is difficult for managers to precisely recognize.

Home institutional pressures and CSR practices of MNE subsidiaries

Based on institutional theory, home-country governments may influence MNE subsidiaries’ CSR practices abroad by exerting specific formal laws or regulations. Particularly, governments in many emerging markets have been argued to control the critical resources that are needed for foreign direct investment (FDI) by providing knowledge and financial incentives and assisting MNEs through the institutional support and local legitimacy required for FDI (Wang et al., 2012). Similar to other emerging market firms, Chinese MNEs are highly dependent on the home-country government to obtain critical strategic assets necessary for FDI; such MNE subsidiaries that highly rely on home-country government to acquire critical strategic resources are likely to perceive high institutional pressures. Even the home-country government can influence MNE subsidiaries’ CSR practices abroad by regulating their FDI through examination and approval implementation. Such formal systems are particularly useful in limiting FDI projects that are illegitimate or not in line with the government’s FDI policies.

The effect of home institutional pressures is unlikely to be perceived equally by different MNE subsidiaries as it is likely to vary depending on the degree of resource and institutional dependence on the home-country government. As a result, such perceived institutional pressures exerted by the same home-country government may shape MNE subsidiaries’ CSR practices differently. For example, home-country governments in emerging markets like China are likely to exert important institutional pressures on MNE foreign subsidiaries’ CSR practices when going abroad by providing these firms with governmental support. However, such institutional and financial resource dependencies may not be experienced equally by all MNE subsidiaries originating from the same country. A firm that is more dependent on the home-country government for increased access to competitive strategic resources abroad is likely to perceive a greater effect of such institutional pressures (Cui & Jiang, 2012; Xiao et al., 2013).

It is expected that the home-country government may influence the decision-making process or social strategic choices of MNE subsidiaries through institutional support or restrictions. More specifically, when investing abroad, MNE subsidiaries’ nonmarket strategies for managing social responses to local conditions in the host country may be motivated not solely by their self-interests but also by the interests of the home-country institutions (Estrin et al., 2015; Lu et al., 2014). The perceived institutional pressures exerted by the home-country government on the MNE subsidiaries may encourage the willingness of these firms’ social responses to engage in CSR in the host market. Accordingly, MNEs that are experienced in managing external institutions, such as the home-country government, may face less difficulty than inexperienced ones, making them more likely to conform to the requirements by adopting CSR practices to obtain institutional legitimacy in a host market.

H1. Home institutional pressures for CSR positively influence the CSR practices of subsidiaries in a host country.

Host institutional pressures and CSR practices of MNE subsidiaries

It has been reported that host governments can exert powerful pressure on firms’ engagement in social issues by introducing mandatory reporting requirements or measures related to CSR (Han et al., 2008). Governmental CSR regulations represent both a tangible inducement to increase social investment toward local society and a set of penalties applied to MNEs’ malpractices (Yang & Rivers, 2009). Unilateral and punitive actions inflicted by host governments constitute a menace to the business activities of MNE subsidiaries that must comply with the government’s CSR policy (Khan et al., 2015). Subsidiaries’ deficient responses to the social demands from governments may represent a risk for internal managers in the form of the non-fulfillment of short-term financial performance. Therefore, in host countries where CSR rules and laws are well established, MNE subsidiaries should reject selfish and exploitative business practices and comply with CSR policies to meet public interests. Moreover, governmental actions with respect to CSR arouse a social expectation of corporate social obligation and develop the belief that firms should participate in solving social problems (Aguilera et al., 2007; Arya & Zhang, 2009). For example, governments promote the social commitment of MNE subsidiaries by deducting social contributions from corporate income taxes. These governmental policies form a social consensus that firms’ CSR practices are desirable and positive actions for social well-being, not merely profitless spending, thereby encouraging voluntary CSR participation from firms. Ultimately, governments may improve the socially responsible behaviors of the subsidiaries.

NGOs put pressure on MNEs to adapt to local CSR practices by leaning on social norms. Although NGOs cannot directly handle or control firms’ resources, they influence socially responsible operations by possessing institutional legitimacy and normative authority (Lee, 2011). NGOs’ pressure can encourage MNEs to adopt socially responsive nonmarket strategies, such as sustainability norms and standards, which are less explicit than government regulation (Doh & Teegen, 2002; Teegen et al., 2004). This is because NGOs not only tend to receive high levels of trust in society, but can also play a role in changing public opinion and reputation regarding MNEs by raising awareness of and generating conflict with unethical firms (Villo et al., 2020). In other words, MNEs that ignore the social demands from NGOs may provoke criticism from the public because NGOs are typically regarded as desirable inspectors in host countries. Because failing to comply with demands increases the managerial uncertainty in foreign markets, MNEs should consider NGOs as key institutional actors for their local business.

NGOs exercise their force on firms’ management and structure in various respects (Guay et al., 2004; Jonker & Nijhof, 2006). They also transmit intangible informal institutions (e.g., belief and value systems of foreign markets) into MNE subsidiaries through tangible activities that are more available for MNE subsidiaries than invisible institutional pressures. Local NGOs can help MNEs understand social norms, beliefs and cognitive structures, and expectations for appropriate business behavior (Marano & Tashman, 2012). For this reason, the subsidiaries may conform to the social pressure embodied by NGOs, which provides a direction for social actions, such as charitable contributions. In turn, NGOs and MNEs develop mutually supportive cooperation with respect to CSR (Jonker & Nijhof, 2006; Liu et al., 2020; Marano & Tashman, 2012). According to Liu et al. (2020), MNE partnerships with NGOs provide resources of ethical knowledge for the suppliers or competitors and increase the trust, credibility, and reputation of the MNEs, especially in terms of social legitimacy. The subsidiaries can take useful advice on social obligation from NGOs and thus acquire social support and institutional legitimacy in host countries. In sum, the social pressures from NGOs as well as the regulatory pressures from the host-country government may affect the social activities of the subsidiaries.

H2. Host institutional pressures for CSR from the local government and NGOs positively influence CSR practices of the subsidiaries in a host country.

Formal and informal institutional distances

Institutional distance means the difference in the institutional environment between countries (Kostova, 1999). MNEs operate within formal and informal institutions of home and other countries, which are considered important factors determining the strategy and business activities of firms (Konara & Shirodkar, 2018). For example, a number of studies examine the relationship between institutional distance and various MNE practices, such as corporate performance (Konara & Shirodkar, 2018), ownership strategy (Xu & Shenkar, 2002), and entry method (Brouthers & Brouthers, 2001). To formulate a CSR strategy, MNEs should be concerned about the institutional differences between the home and host countries because appropriate and socially responsible behaviors depend on the social context of each country.

Shorter institutional distance is supposed to enable easy adjustment to the legitimacy requirements of host countries as their institutions are similar to those of the home country (Kostova & Zaheer, 1999; Xu & Shenkar, 2002). In contrast, greater institutional distance may lead to a greater risk of facing distrust from actors in local markets in a way that prevents the MNE from obtaining legitimacy (Lee, 2011; Yang & Rivers, 2009). It is also supposed that imitating local companies and complying with local business rules and practices may accelerate the social legitimacy buildup of MNEs working in institutionally distant markets. In the same context, Yang and Rivers (2009) claim that MNE subsidiaries adapt to local CSR practices for legitimacy when they are operating in host countries with institutional environments that are different from those of their home countries.

Prior studies suggest that longer institutional distance reduces MNEs’ local CSR capabilities (Campbell et al., 2012; Reddy & Hamann, 2018; Reimann et al., 2015). Studies on the liabilities of foreignness (LOF) and institutional distance assume that the larger the institutional distance, the more it induces uncertainty for MNE subsidiaries in the environment of the host country, and the more it costs the firms to learn about and accustom themselves to the institutions (Campbell et al., 2012; Konara & Shirodkar, 2018; Zaheer, 1995). As such, LOF is shown through the discrepancies among the institutions of countries (Ghemawat, 2001; Kostova & Zaheer, 1999), which may hinder firms from participating in CSR practices. Campbell et al. (2012) find that institutional, cultural, administrative, geographical, and economic distances are negatively correlated with CSR engagement. According to their findings, MNE subsidiaries located institutionally distant from their home country have trouble addressing uncertainties in local societies, resulting in LOF and additional adaptation costs of the unfamiliar business environment so that their local CSR capabilities diminish. Similarly, Reimann et al. (2015) argue that MNE subsidiaries are less likely to rely on a strategic commitment to CSR when administrative distance is high in emerging market contexts.

In the meantime, institutional distance is not a single dimension but rather a multidimensional construct that includes several types of distance between countries (Berry et al., 2010; Ghemawat, 2001). For example, Berry et al. (2010) conceptualize cross-national distance based on national systems of business, governance, and innovation. This cross-national distance includes economic, financial, political, administrative, cultural, demographic, knowledge, connectedness, and geographic dimensions. Institutional studies insist that formal and informal institutional factors should be considered together to deal with institutions and institutional distance (North, 1991; Scott, 2007). However, most previous CSR studies mainly focus on formal institutional distance, such as administrative distance (Reimann et al., 2015) and regulatory distance (Reddy & Hamann, 2018).

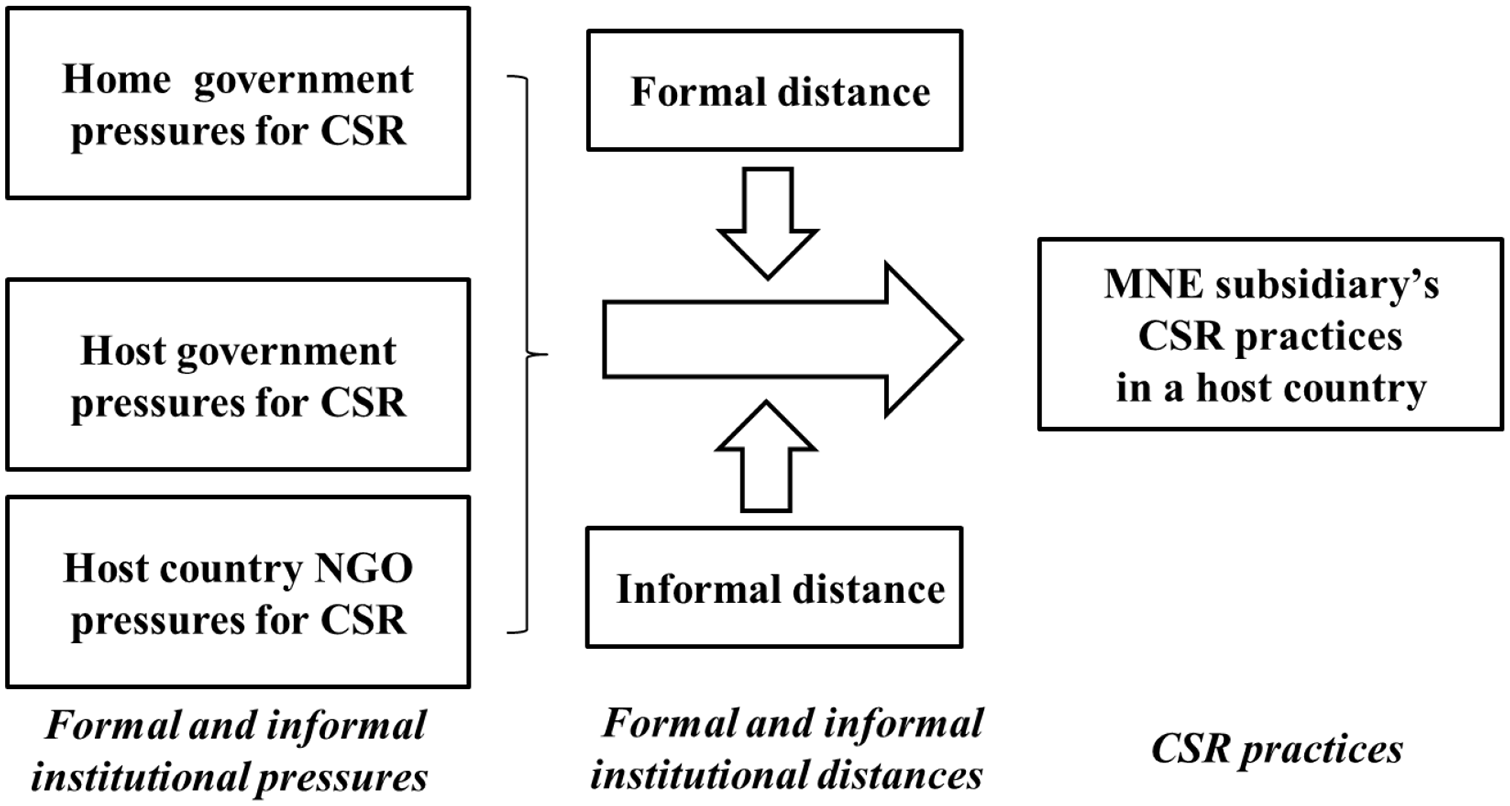

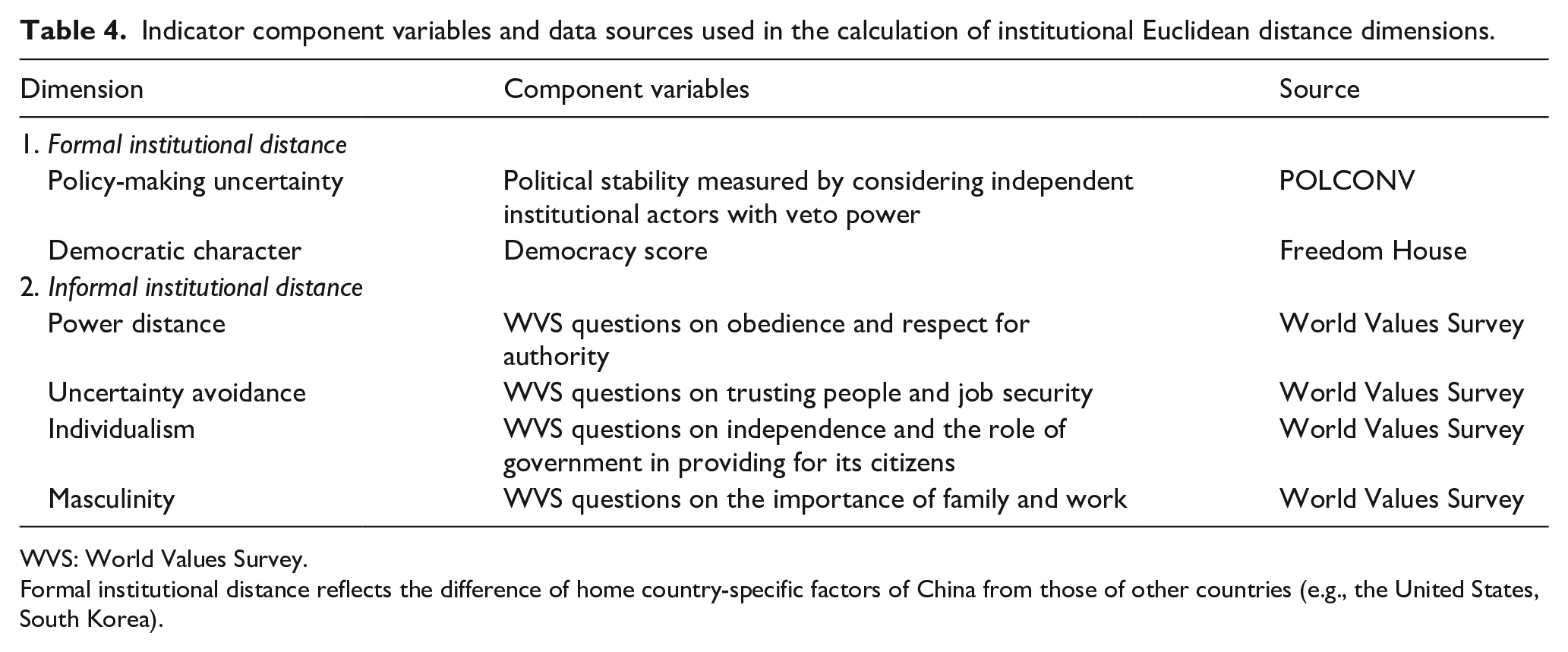

To simplify the framework, we attempt to classify and analyze institutional distance as something that can represent formal and informal institutional elements (Garrido et al., 2014). Formal institutional distance is related to codified or explicit national systems that refer to national differences in a formal institutional environment. Formal institutional distance includes the political distance between the home and host countries. Meanwhile, informal institutional distance involves implicit cultural conditions, which often lend uncertainty to the business activities of MNE subsidiaries. Cultural distance is classified as an informal institutional distance. Figure 1 summarizes the conceptual framework of the study.

Conceptual model.

Moderating effects of institutional distance

This section further expands the previous CSR literature by incorporating the role of institutional distance between the home and host countries in influencing the effects of both the home and host institutional pressures on MNE subsidiaries’ CSR practices. Institutional distance has been viewed as one of the most salient factors to take into account when exploring MNEs’ behaviors (Verbeke et al., 2018). Despite a substantial body of MNE literature on the influence of institutional distance on firms’ strategic choices and practices, such studies often neglect incorporating institutional distance into firms’ social behaviors abroad (Reimann et al., 2015). As explained in the previous sections, given our arguments that home and host institutions, such as the government and NGOs, may apply either or even both formal and informal rules to foreign investing firms to encourage them to engage in CSR practices, MNE subsidiaries are subject to various home and host institutional pressures. Drawing on Hypotheses 1 and 2, we expect that both formal and informal institutional distances may moderate the effects of home and host institutional pressures on MNE subsidiaries’ CSR practices in the host country (see Figure 1).

While both home and host institutional pressures are likely to influence MNE subsidiaries’ social responses to CSR in the host market, these institutional effects can conflict with a foreign subsidiary’s internal need and strategic motivation to engage in CSR to cope with and lower its LOF, which leads to varied responses from these MNE subsidiaries. Therefore, we argue that formal and informal institutional distances between home and host countries play an important role in the responses of MNE subsidiaries to home or host institutional pressures regarding their CSR practices; this is because these distances determine an MNE subsidiary’s need to reduce its LOF, and thus its need to gain legitimacy by engaging in CSR practices in the host market. The extant literature has focused on how foreign entrants such as MNE subsidiaries can overcome LOF (Barnard, 2010; Bell et al., 2012).

As a crucial factor moderating home and host institutional pressures, we argue that when facing larger differences between home and host countries’ formal institutions, MNE subsidiaries will be more compliant to the home and host institutional pressures. Formal institutional distance, by definition, represents the dissimilarity in political and regulative systems between the MNE subsidiary’s home and host countries (North, 1991; Scott, 2007). When operating in a formally distant host market, MNE subsidiaries may be more willing to conform to home institutional pressures, because in this situation they may require more home-country government support to overcome the LOF experienced in the host market, especially for MNE subsidiaries originating in emerging markets (Luo et al., 2010; Wang et al., 2012; Xiao et al., 2013). By conforming to home institutional pressures, those subsidiaries can be better positioned for both increased support for internationalization efforts and increased access to valuable and privileged financial and diplomatic resources abroad, which enables them to overcome their LOF in an institutionally distant host market (Cui & Jiang, 2012; Luo et al., 2010; Wang et al., 2012). Home-country government support can be an important source for emerging market MNE subsidiaries to mitigate their resource deficiencies and scarce knowledge of foreign markets. Thus, the subsidiaries would be more likely to conform to the home institutional pressures on them to engage in CSR practices in the host market, especially when investing and operating in a more formally distant host market.

A similar logic can also be applied to predict the moderating effect of formal institutional distance on the contribution of host institutional pressures to MNE subsidiaries’ CSR. When investing in a host country that is more institutionally distant from the home country, MNE subsidiaries may have a stronger need to mitigate their LOF by establishing institutional and social legitimacy in the host market (Campbell et al., 2012; Kostova & Zaheer, 1999). When the strategic motivation to maintain or gain institutional and social legitimacy in the host market is greater, MNE subsidiaries are more likely to conform to host institutional pressures and thus host institutions’ expectations of engaging in CSR practices.

Taken together, this line of reasoning indicates that, in comparison to less institutionally distant MNE subsidiaries, which have a weaker strategic motivation to cope with LOF in the host market, more institutionally distant ones are likely to suffer from LOF and have a need to reduce it because their business behaviors are supposed to be regulated by the variation in formal institutional rules between the MNE subsidiary’s home and host countries. Therefore, in response to such institutional pressures, the subsidiaries are inclined to be willing to invest and engage in CSR activities in host countries that are formally institutionally dissimilar to their home countries.

H3a. Formal institutional distance between home and host countries positively moderates the effects of home institutional pressures on an MNE subsidiary’s CSR practices in a host country.

H3b. Formal institutional distance between home and host countries positively moderates the effects of host institutional pressures on an MNE subsidiary’s CSR practices in a host country.

Meanwhile, the form of informal institutional distance (operationalized as cultural distance) is more involved in the dissimilarity in implicit social values, beliefs, cognitions, and norms of doing business between the MNE subsidiaries’ home and host countries (Dikova et al., 2010; North, 1990). In particular, these informal institutional conditions constitute the critical facades of the intended CSR activities of MNE subsidiaries from a culture that is similar to that of the host country (Demirbag et al., 2017). For instance, when MNE subsidiaries invest and operate in a culturally distant host country, the cultural values and norms between the MNE subsidiaries’ home and host countries complement each other, and, as a result, these firms’ CSR activities are highly contextual (Demirbag et al., 2017; Rodgers et al., 2019).

Indeed, Laurent (1983) offered evidence that MNE managers tend to retain many of their original national values when forming their management strategies and styles, suggesting that management practices may be largely culturally determined. However, unlike the moderating effect of formal institutional distance, we expect that informal institutional distance may shape the willingness of MNE subsidiaries to comply with home and host institutional pressures on CSR practices differently. MNE subsidiaries are expected to comply with home (regulative) institutional pressures on foreign CSR practices when operating abroad in a formally dissimilar institutional environment because such institutional conformity may offer substantial resource and institutional support to reduce their formal institutional distance-based LOF (Cui & Jiang, 2012); however, this logic may not hold for MNE subsidiaries that suffer from informal institutional distance-based LOF (DiMaggio & Powell, 1983). Therefore, when investing and operating in host countries that are informally distant from their home country, MNE subsidiaries might be less dependent on home institutions that exert institutional pressures on them to engage in CSR practices abroad. In this vein, we can expect that MNE subsidiaries are less likely to conform to, or may even resist, home institutional pressures (Oliver, 1991).

A similar logic can also be applied to the responses of MNE subsidiaries to host country institutional pressures (either regulative pressures from the host government or normative ones from other stakeholders like NGOs). When investing and operating in host countries that are more culturally distant from their home country, MNE subsidiaries may perceive local constituents in the host country as different from themselves because there will be a paucity of shared norms, values, and social principles between the MNE subsidiaries and host-country constituents. This implies that informal institutional distance between the home and host countries may become one of the main barriers to compliance with host institutional pressures. In addition, we also acknowledge that it could be possible for MNE subsidiaries to reduce their LOF and attain legitimacy in the informal dimension, but, unlike the formal one, such informal legitimacy may be rather challenging for MNE subsidiaries to acquire (Kostova & Zaheer, 1999) by simply conforming to the host country’s instructional pressures for CSR practices. Indeed, MNE subsidiaries may find it more efficient and effective to attain legitimacy by offering something distinctive to their host countries that is valued and appreciated by their host constituents rather than attempt to comply with the host institutional pressures.

To sum up, while MNE subsidiaries can be subject to both home and host institutional pressures to engage in CSR practices in the host market, they may be less willing to comply with such pressures when they invest in informally distant host countries. The underlying logic is that the LOF stemming from informal dissimilarities between the MNE subsidiaries’ home and host countries may not be easily rectified through compliance with the home or host institutional pressures imposed on them to engage in CSR practices. Therefore, MNE subsidiaries may be less receptive to home and host institutional pressures regarding CSR practices when there is a greater informal institutional distance between the home and host countries because such informal institutional distance may psychologically hamper MNE subsidiaries’ willingness to engage in more CSR practices (Campbell et al., 2012). Conversely, MNE subsidiaries may be more likely to conform to such home and host institutional pressures on CSR practices and can also benefit more from their nonmarket experiences in similar informal institutional settings due to their shared cultural principles with the local constituents in the host country. Thus, the shorter the informal institutional distance between the home and host countries, the stronger the positive effect of home- and host-country institutions on MNE subsidiaries’ CSR practices in the host country.

H4a. Informal institutional distance between home and host countries negatively moderates the effects of home institutional pressures on an MNE subsidiary’s CSR practices in a host country.

H4b. Informal institutional distance between home and host countries negatively moderates the effects of host institutional pressures on an MNE subsidiary’s CSR practices in a host country.

Methods

Research setting

The Chinese context provides a crucial research setting for the study. China has quickly risen to become the second largest investing economy in the world and has been recognized as the most promising source of FDI in recent years (The United Nations Conference on Trade and Development [UNCTAD], 2017). For example, according to the latest 2020 rankings released by Fortune Magazine, Chinese MNEs’ share on the Fortune Global 500 list expanded from zero in 1990 to more than 130 in 2020, overtaking the number of US MNEs for the first time since the annual ranking implemented in 1990. While significant research attention has been given to the role of host country governments, the role of home country governments in shaping MNEs’ outward FDI has been largely ignored in the literature (Peng, 2012). In this sense, prior research suggests the home-country governments in many emerging markets have played an important role in driving emerging market MNEs’ outward FDI by providing both incentives and institutional support (Luo et al., 2010; Luo & Tung, 2007; Peng, 2012). The Chinese government has been increasingly exerting great institutional pressures on Chinese firms by implementing various policies and incentives to encourage them to undertake more CSR practices and upgrade their CSR strategies. Clearly, China is an ideal setting to observe the importance of various institutional pressures in shaping MNE subsidiaries’ CSR practices abroad because it represents one of the major largest emerging markets in the world. Furthermore, the ongoing economic and institutional reforms have not only facilitated many Chinese firms to undertake outward FDI, but have also created various institutional pressures to encourage the firms to engage in more CSR practices.

Data collection and sample

Data were collected from two-wave surveys with a time gap, whereby the first survey was conducted from the first to third quarters of 2016, and the second survey was conducted from the second to fourth quarters of 2017. Our sampling frame was identified from the database of the Ministry of Commerce of the People’s Republic of China (MOFCOM), which includes information on Chinese MNEs, including names of parent firms and foreign subsidiaries, investment locations, and capital investment (Chung et al., 2016). In addition, the database of the National Bureau of Statistics of China (NBSC) was used. This all-inclusive firm-level dataset is compiled by the Chinese statistical agency and is directly under the State Council of the People’s Republic of China. It is charged with the collection and publication of statistics in relation to the economy, population, and society of the People’s Republic of China. This database includes information on manufacturing firms’ tangible assets, number of employees, sales, exports, and so on. From this group of Chinese manufacturing firms, an initial sample of 1,037 firms was collected. After excluding firms with missing values, the final sample provided 912 manufacturing firms that have undertaken outward FDI.

The survey questionnaire was cross-checked by three professors who have expertise in institutions and CSR from China and the United States and tested for instrument validity by 15 senior managers. Then, we revised imprecise and unsuitable questionnaire items based on the reviewers’ feedback. We hired a leading survey institute in China with substantial experience in conducting comprehensive field surveys for Chinese MNEs over the years. To enhance the response rate for the first round of surveys, we conducted a three-step survey process. First, 17 professional researchers conducted pre-screening over the telephone to identify one or two potential senior manager(s) from each MNE who are charged with overseas operations. Second, a series of field interviews was conducted to obtain insights into our theme and provide a link to one or two senior manager(s) who is(are) (a) top decision-maker(s) at the firm’s foreign subsidiary(-ies). Finally, with the consent of the interviewees, a qualified sample of 478 foreign subsidiaries, affiliated with 236 MNE parent firms, was selected for the first questionnaire survey. The aforementioned research team conducted the survey process. As a result of the first survey, we received 392 usable questionnaires via email, fax, and mail. We excluded nine responses due to unclear or omitted answers on a number of questions. In sum, we reached a response rate of 82%.

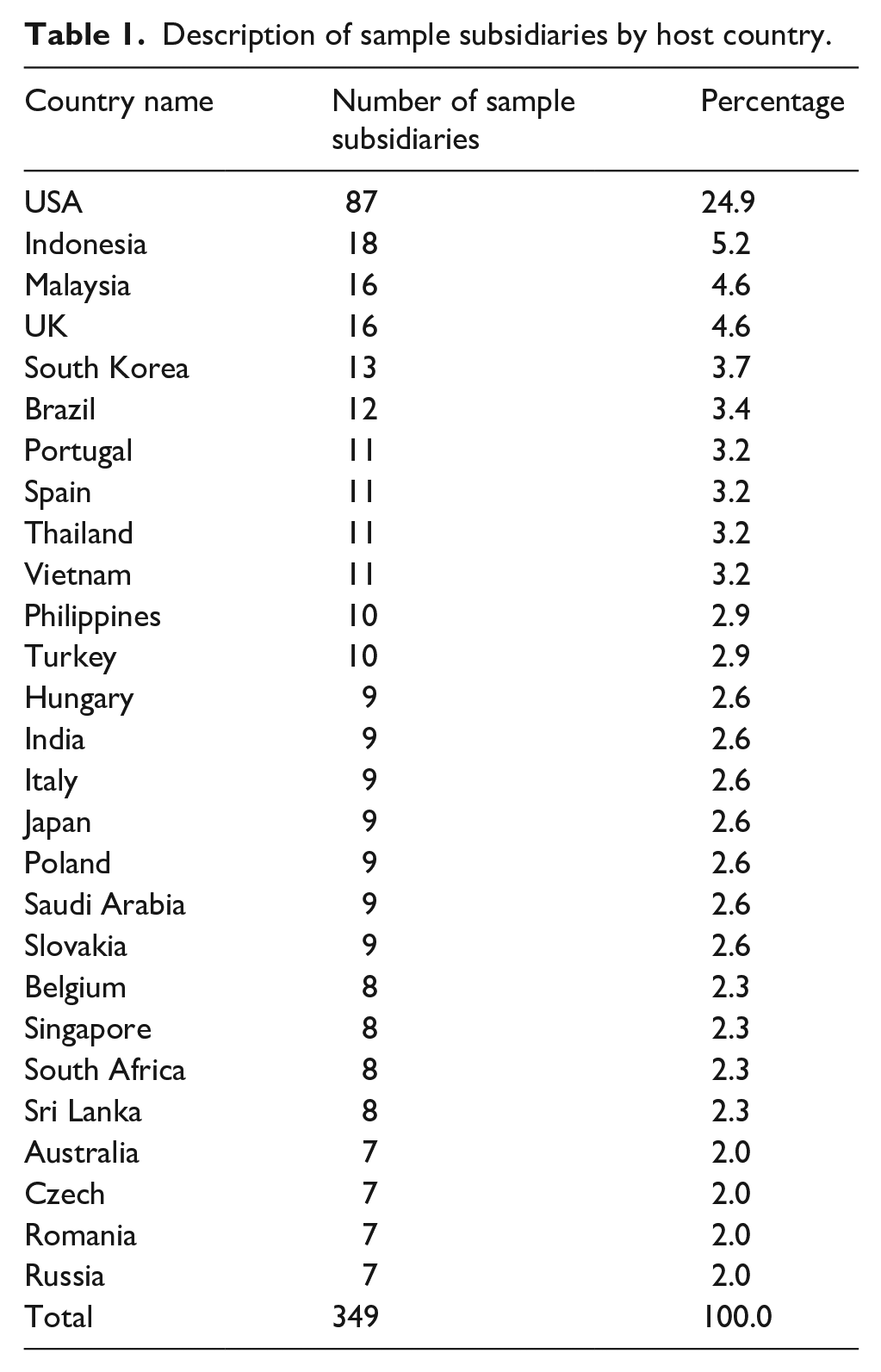

To minimize the problem of causal confusion and common method bias, we used the first survey data to measure two independent variables (i.e., home- and host-government pressures for CSR), whereas we used the second survey data to measure the dependent variable (i.e., CSR practices) with a time gap of at least 6 months. The hired research team conducted one more survey by targeting the final respondents of the 392 usable questionnaires in the first survey. As a result of the second-round survey, we received 349 usable questionnaires via email, fax, and mail by excluding seven responses due to unclear or omitted answers for certain questions. Hence, we achieved a final response rate of 73%. The 349 foreign manufacturing subsidiaries operate in 27 host countries and are affiliated with 185 Chinese MNEs in the manufacturing industry. Table 1 summarizes the description of the sample subsidiaries by host country.

Description of sample subsidiaries by host country.

We checked the final sample for non-response bias. Based on the MOFCOM and NBSC databases, we compared non-respondents with respondents according to size and age of the firm and industry to detect potential self-selection bias. We did not find any significant results in mean comparison t-tests (p > .05).

Measures

CSR practices

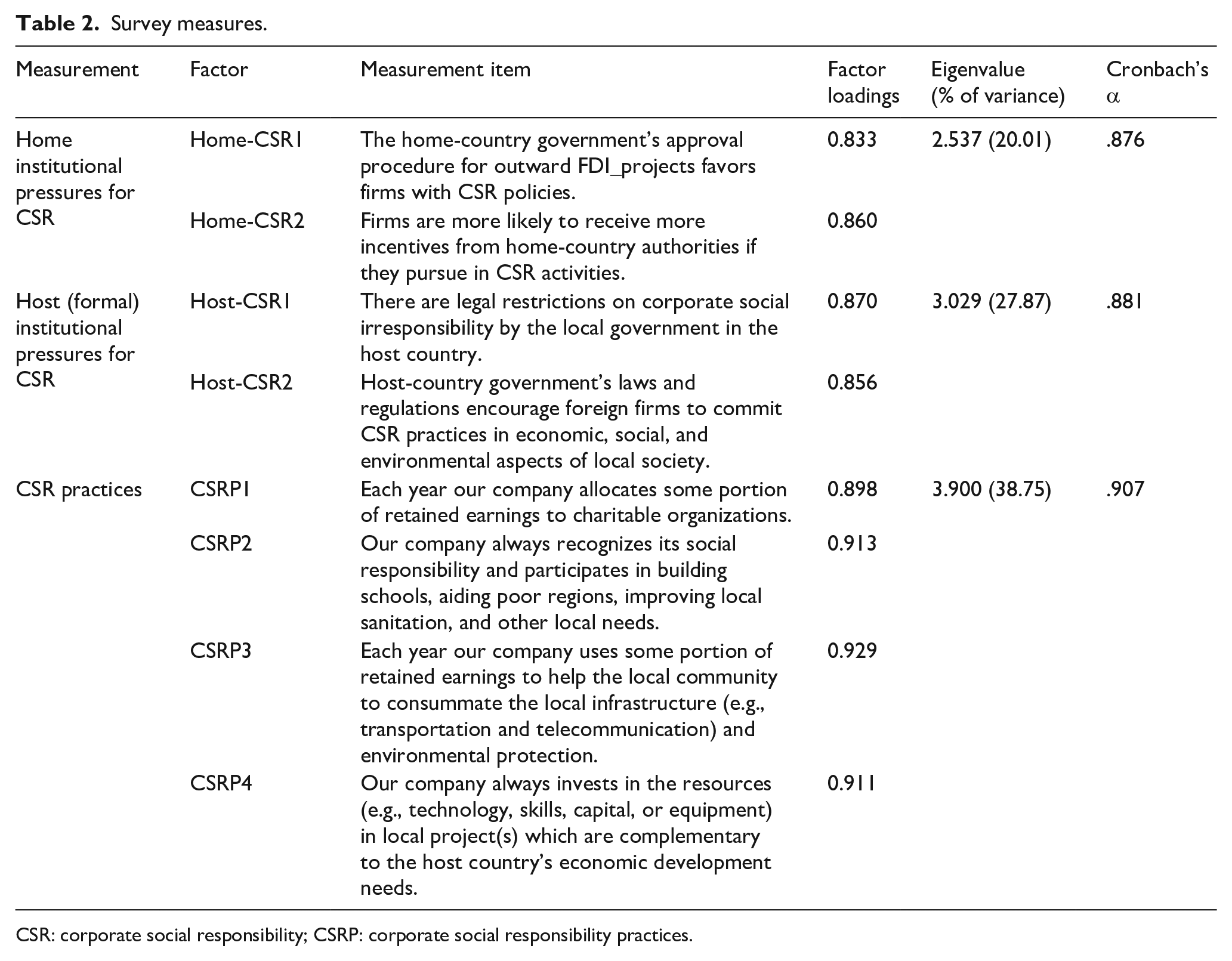

We define CSR practices as the MNEs’ voluntary philanthropic commitments and contributions to the development of the local community and host countries. Following previous literature (Luo, 2006), we employ four items that reflect the perceptions in this research using a 7-point Likert-type scale. 2 Developing this measure of CSR practices, Luo (2006) stated the following: Even though he could not find any direct reference to measuring CSR practices in the vein of “philanthropic contribution,” Logan et al.’s (1997) discussions “on philanthropic commitment provided the insights into the content of this commitment” to CSR practices, which he referred to (see Luo, 2006, p. 756) as one of “the main building blocks of global CSR improvement” (see Luo, 2006, p. 750).

Formal and informal institutional pressures

Previous bodies of research use two types of measurements for the variables of institutional pressures, namely secondary index measures (Meyer et al., 2009) and survey-based perceptual measures (Chung et al., 2016; Cui & Jiang, 2012). In this study, we adopt the psychometrics for the two variables of formal institutional pressures (i.e., home- and host-country government pressures for CSR). Furthermore, we develop a secondary data-based measure for informal institutional pressures (i.e., host-country NGO pressures for CSR) for two reasons.

First, prior studies (e.g., Kostova & Roth, 2002) propose that formal institutional pressures are classified as a domain in the home- or host-country contexts. Thus, the measures for the variables of institutional pressures should be categorized into the specific organizational implementation between institutions and organizations. The specific domain is the formal institutional pressures for CSR. However, an archival index to measure these variables, particularly for formal institutional pressures for CSR at the subsidiary level, is lacking. Therefore, our survey-based measures for the previously mentioned formal institutional pressures fit this context.

Second, informal institutional pressures, such as NGO pressures for CSR, transmit the intangible informal institutions of foreign markets, such as belief and value systems (Guay et al., 2004). The NGO pressures for CSR can be interpreted as “implicit CSR,” referring to socially responsible organizations’ roles within broad informal institutions for the interests and concerns of the local society in relation to its values, norms, and legitimacies (Matten & Moon, 2008). Compared to “explicit CSR,” that is, affected by rather coercive formal institutional pressures, implicit CSR is hard to capture by surveys because it is elusive. For example, managers of an organization cannot easily answer precise perceptions. Therefore, our archival public disclosure of CSR/CSI (corporate social irresponsibility) is appropriate for the measurement of NGO pressures for CSR.

Home (formal) institutional pressures for CSR is measured via the impact of the institutional pressures exerted by the home government for CSR. We use a two-item scale rating of the extent of such pressures over the last 5 years by defining home-country institutional pressures as the home government’s favoring of Chinese firms that have CSR policies in place and the incentives it offers for Chinese firms pursuing CSR. We adopt this rating system from prior studies (Chung et al., 2016; Cui & Jiang, 2012; Luo et al., 2010; Matten & Moon, 2008) and use a 7-point Likert-type scale.

Host (formal) institutional pressures for CSR is measured by the effect of the institutional pressures exerted by host-country governments for CSR. We use a two-item scale rating of the extent of such pressures over the last 5 years by defining host government pressures as laws and regulations established by the host government for the purpose of restricting CSI and encouraging foreign firms to commit to CSR practices in the local society. We adopt this rating system from previous studies (Brouthers, 2002; Cui & Jiang, 2012; Matten & Moon, 2008) and use a 7-point Likert-type scale.

Third, the database of RepRisk AG—a Zurich-based data provider on social and environmental controversies or incidents—provides information from more than 80,000 media, institutional, and third-party sources, such as print and online media from NGOs, government organizations, think tanks, social media, and other online sources in 16 languages (RepRisk, 2018). Host (informal) institutional pressures for CSR (independent variable) is measured via the public disclosure of NGOs’ pressures against CSI incidents based on the count of media reports of NGOs’ pressures against or interferences in CSI incidents in the host country during 2010–2016, weighted by the severity and reach of the CSI incidents.

In addition to identifying news items, the RepRisk database provides an evaluation of the reach of the source for each news item as well as the severity of the criticism (RepRisk, 2018). The reach of CSI coverage depicts the potential audience that a given media article could reach based on the reporting medium’s circulation and geographic range at the local, national, and international levels. Articles are categorized in terms of their reach into three levels of reach, namely, high, medium, and low. High reach involves news outlets with a robust global media presence. Medium reach involves print media of national or regional importance with a circulation of approximately 150,000. Low reach involves local newspapers with a circulation of less than 150,000 (Kölbel et al., 2017). Similarly, articles are categorized into three levels according to the severity of the criticism, namely, high, medium, and low severity (Kölbel et al., 2017).

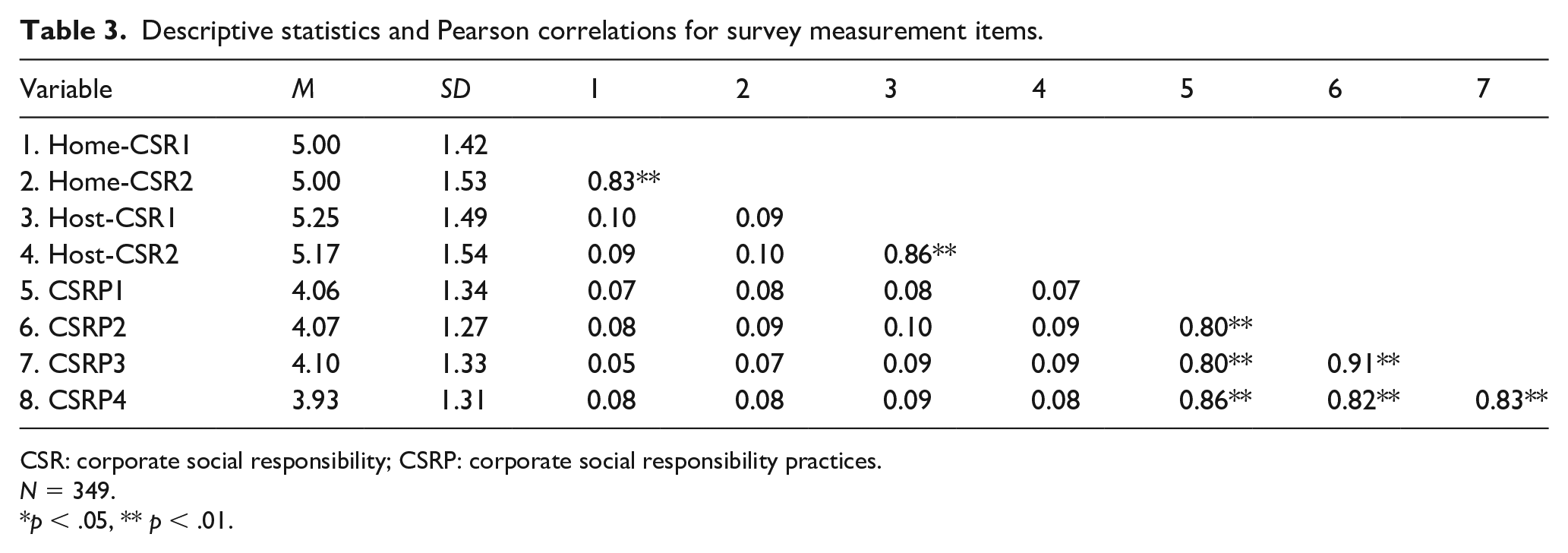

Consistent with prior research (Kölbel et al., 2017; Wang & Li, 2019), a weighted count of CSI incidents is computed based on severity and reach. Two sets of weights are applied (high = 3, medium = 2, and low = 1 and high = 10, medium = 5, and low = 1 (Wang & Li, 2019). Table 2 summarizes the measurement items used in this research model, and Table 3 reports the summary statistics and the correlation matrix for the different measurement items.

Survey measures.

CSR: corporate social responsibility; CSRP: corporate social responsibility practices.

Descriptive statistics and Pearson correlations for survey measurement items.

CSR: corporate social responsibility; CSRP: corporate social responsibility practices.

N = 349.

p < .05, ** p < .01.

Formal and informal institutional distances

MNE subsidiaries have to engage in the dissimilar formal and informal institutional environments of the home and host countries. Thus, the formal and informal institutional distances (i.e., moderating variables) between the home and host countries influence an organization’s adaptive behaviors in deploying its CSR strategies to survive in local institutional environments. We view regulatory political distance as a formal institutional distance (Jiménez et al., 2018; Tsang & Yip, 2007), whereas we categorize normative cultural distance as informal institutional distance (Dikova et al., 2010; Lee et al., 2008).

We calculate the institutional distance based on prior studies (Berry et al., 2010; Kang et al., 2017; Slangen & Beugelsdijk, 2010). We use these measures in our study to explain the moderating effects of formal and informal institutional distances on the relationship between CSR pressures from the home and the host-country governments and NGOs and CSR practices.

To calculate the previously mentioned dimension, we collected data from various sources. Table 4 summarizes each of the three dimensions, including the component variables and data sources adapted from prior studies (Berry et al., 2010; Kang et al., 2017; Slangen & Beugelsdijk, 2010). We use the Euclidean distance calculation method to calculate the cross-national distance between China and the 27 host countries. Euclidean distance is the most popular measure for cross-national distance in the international business literature, and it is the geometrically shortest possible distance between two points (Mimmack et al., 2001; Seber, 1984). The traditional Euclidean distance measure meets all five desirable characteristics, namely symmetry (dij = dji for all i and j), non-negativity (dij ⩾ 0 for all i and j), identification (dii = 0 for all i), definiteness (dii = 0, only if xi = xj), and triangle inequality (dij ⩽ dik + djk for all i, j, and k).

Indicator component variables and data sources used in the calculation of institutional Euclidean distance dimensions.

WVS: World Values Survey.

Formal institutional distance reflects the difference of home country-specific factors of China from those of other countries (e.g., the United States, South Korea).

We use different sources to collect the data measuring the direct effect of institutional pressures (formal and informal) than when calculating the institutional distances (formal and informal) between home and host countries. This is because for the direct effect we are analyzing the institutional pressures toward CSR, while for the moderating effect we are analyzing more general formal and informal institutional environments (not specific pressures to invest in CSR).

Control variables

We control for subsidiary size and age. Subsidiary size is measured by the natural logarithm of total sales, whereas subsidiary age is measured by the natural logarithm of the length of operations (i.e., number of months in the host country). According to the previous literature (Reimann et al., 2015, pp. 845–846), “the larger the size of a subsidiary (as a proxy for a local subsidiary’s available resources)” and “the longer a subsidiary’s experience in the host country (as a proxy for accumulated knowledge and awareness of the local situation),” “the more the MNE subsidiaries strategically commit to CSR” practices. We also include parent firm-, industry-, and country-fixed effects to take into account the potential impacts of unobserved differences in organizational, industrial, and host-country characteristics that are associated with institutional pressures or competitions on the MNEs’ CSR practices.

Common method bias

We minimize common method bias by (1) conducting two-round surveys with a time gap in-between; the first survey data were used to measure the two independent variables, whereas the second survey data were used to measure the dependent variable. Furthermore, (2) we combine these survey data with secondary data for other objective-independent, moderating, and control variables with lagged periods. In addition, we conduct Harman’s single-factor test, which is a widely used method to investigate the existence of common method bias. If the test result is applicable to one of the following cases—(1) a single factor emerges from the factor analysis or (2) one general factor accounts for the majority of the covariance among the measures—then common method bias may exist. Conventionally, in a number of studies that employ Harman’s single-factor test, all variables in the model are loaded into the exploratory factor analysis (EFA) (Eiadat et al., 2008; Luo, 2006; Tang & Tang, 2012). Three factors with eigenvalues more than 1 are extracted by employing varimax rotation in this research. The first factor accounts for 38.75% of the total variance (86.63%). The results suggest that the items are banded together in affiliated variables and the latent constructs are stable.

Results

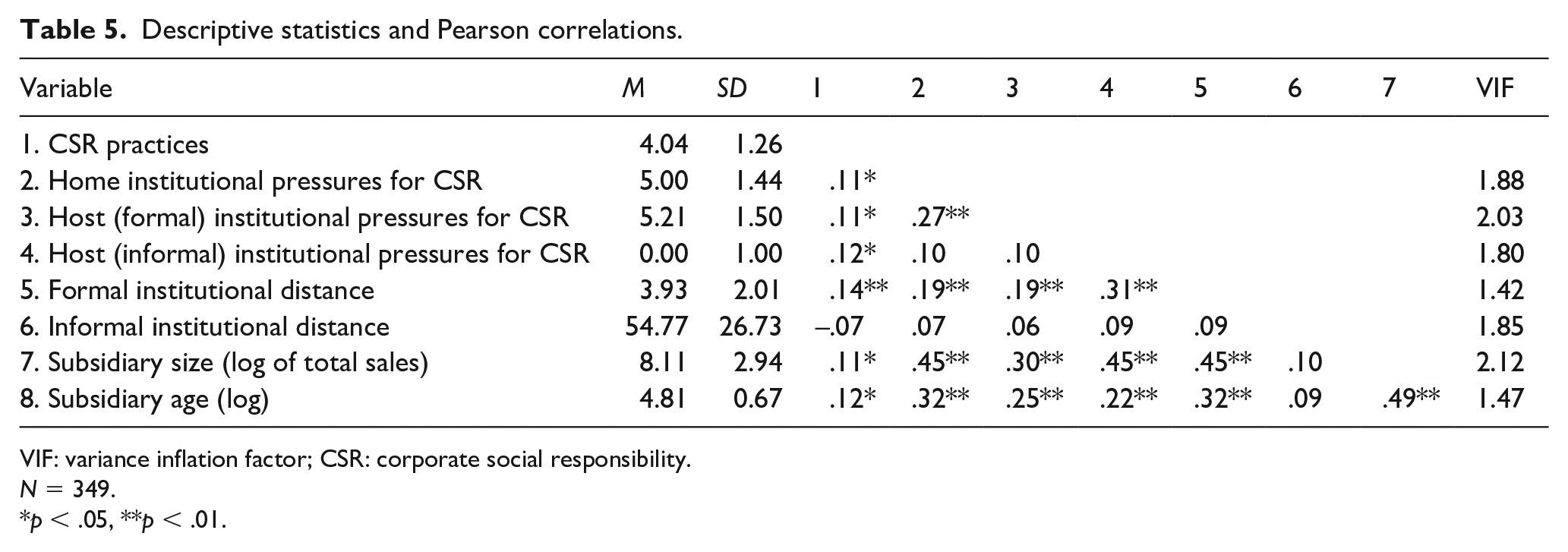

Descriptive analysis and multicollinearity diagnosis

Table 5 shows the descriptive statistics and Pearson correlations for the variables as well as the variance inflation factors (VIFs). We have confirmed that there is less concern of multicollinearity affecting the sample because all the correlations are comparatively low and all VIFs are under the recommended threshold of 10 (or the stricter threshold of 5.30), used here as the rule of thumb to diagnose multicollinearity based on the literature (Kennedy, 1992; Studenmund, 1992). Also, each of the scales for home institutional pressures for CSR, host formal institutional pressures for CSR, host informal institutional pressures for CSR, and formal institutional distance is positively and significantly related to CSR practices. These results are consistent with our hypotheses.

Descriptive statistics and Pearson correlations.

VIF: variance inflation factor; CSR: corporate social responsibility.

N = 349.

p < .05, **p < .01.

Reliability and validity analyses

As shown in Table 2, we conduct an EFA to check the unidimensionality of the measures. Each item used in the main surveys is grouped as intended. When we apply an eigenvalue greater than 1, three-dimensional factors are deducted. The survey structure is tested and modified to confirm only one common factor in each area. All loading factors are greater than 0.8, which satisfies the recommended cut-off of 0.4 (Nunnally & Bernstein, 1994). To verify internal consistency, we also calculate Cronbach’s alpha coefficients and confirm that all the main constructs demonstrate coefficients over .6. The variance for all measures is more than 50% of the variance (Bagozzi & Yi, 1988).

Confirmatory factor analysis (CFA) is conducted to investigate the construct distinctiveness of the main constructs in this study. The measurement model shows a χ2 value of 135.497 (df = 68, p = .000), an above-threshold 0.9 for four goodness-of-fit indices (comparative fit index [CFI] = 0.953, normed fit index [NFI] = 0.924, Tucker–Lewis index [TLI] = 0.941, goodness-of-fit index [GFI] = 0.921), and a below-threshold 0.7 for root mean square error of approximation (RMSEA = 0.051), indicating an appropriate fit (Malhotra, 2010).

Cronbach’s alpha denotes the internal consistency among the items, and in the item reliability analysis, all display values over 0.7; thus, the items are reliable. Convergent validity is positively related to the correlations among items in a certain construct is estimated by standardized factor loadings, composite reliability (CR), and average variance extracted (AVE). The standardized factor loadings by CFA are over 0.6, CR is more than 0.8, and AVE is over 0.5, meaning they are suitable for the standard and denote validity (Hair et al., 2011).

Discriminant validity is assessed by examining whether the AVE of each construct is larger than the construct’s highest squared correlation with any other construct (Fornell & Larker, 1981; Hair et al., 2011). The square root of the AVE of each construct (home-CSRSQRT = 0.843; host-CSRSQRT = 0.847; CSRPSQRT = 0.825) is greater than the correlations with other constructs in the corresponding rows and columns, indicating that discriminant validity is evident for all constructs. However, there has been some criticism of this criterion of Fornell-Lacker, so a more appropriate measure for discriminant validity is the heterotrait-monotrait (HTMT) ratio of correlation. Henseler et al. (2015) suggested “the superior performance of this criterion by means of Monte Carlo simulation study” and confirmed that HTMT can attain “higher specificity and sensitivity rates (97%–99%) compared to the cross-loadings criterion (0.00%) and Fornell-Lacker (20.82%)” (see Hamid et al., 2017, p. 3). Employing the HTMT means comparing it to a predefined threshold, and a lack of discriminant validity is confirmed if the value of the HTMT is above a threshold of 0.85 (Kline, 2011) or 0.90 (Gold et al., 2001) under the condition that HTMT values near to 1 suggest a lack of discriminant validity. We confirm that our HTMT values are below these thresholds (HTMTHome-CSR vs Host-CSR = 0.11; HTMTHome-CSR vs CSRP = 0.09; HTMTHost-CSR vs CSRP = 0.10).

Statistical estimation

We perform the analysis using the multi-level regression approach, and thus, our explanatory variables operate at differential levels. Certain data structures such as ours do not have a complete hierarchical structure, thus cross-classified multilevel (crossed random effects) model analysis is more appropriate (Gooty & Yammarino, 2016; Hillman & Wan, 2005). An MNE subsidiary’s CSR practices may be influenced by both the parent firm to which the subsidiary is affiliated and the host country into which its parent firm enters. A single parent firm may have subsidiaries in more than one host country. Thus, parent firms are not nested within the host country, and host countries are not nested within parent firms. Hence, this study’s data structure follows a cross-classified multilevel data structure. Even if our data have a multilevel structure at three levels (level 3: parent firm level, level 2: host country level, and level 1: subsidiary level), it is not a complete three-level hierarchical structure. The respective lower-level unit (level 1) in our sample is cross-classified by other higher-level units. Accordingly, we use the “xtmixed” command in STATA 15 to assess the cross-classified multilevel regression in this research. We also perform a robustness test using ordinary least squares (OLS) regression and find consistent results.

Hypothesis testing

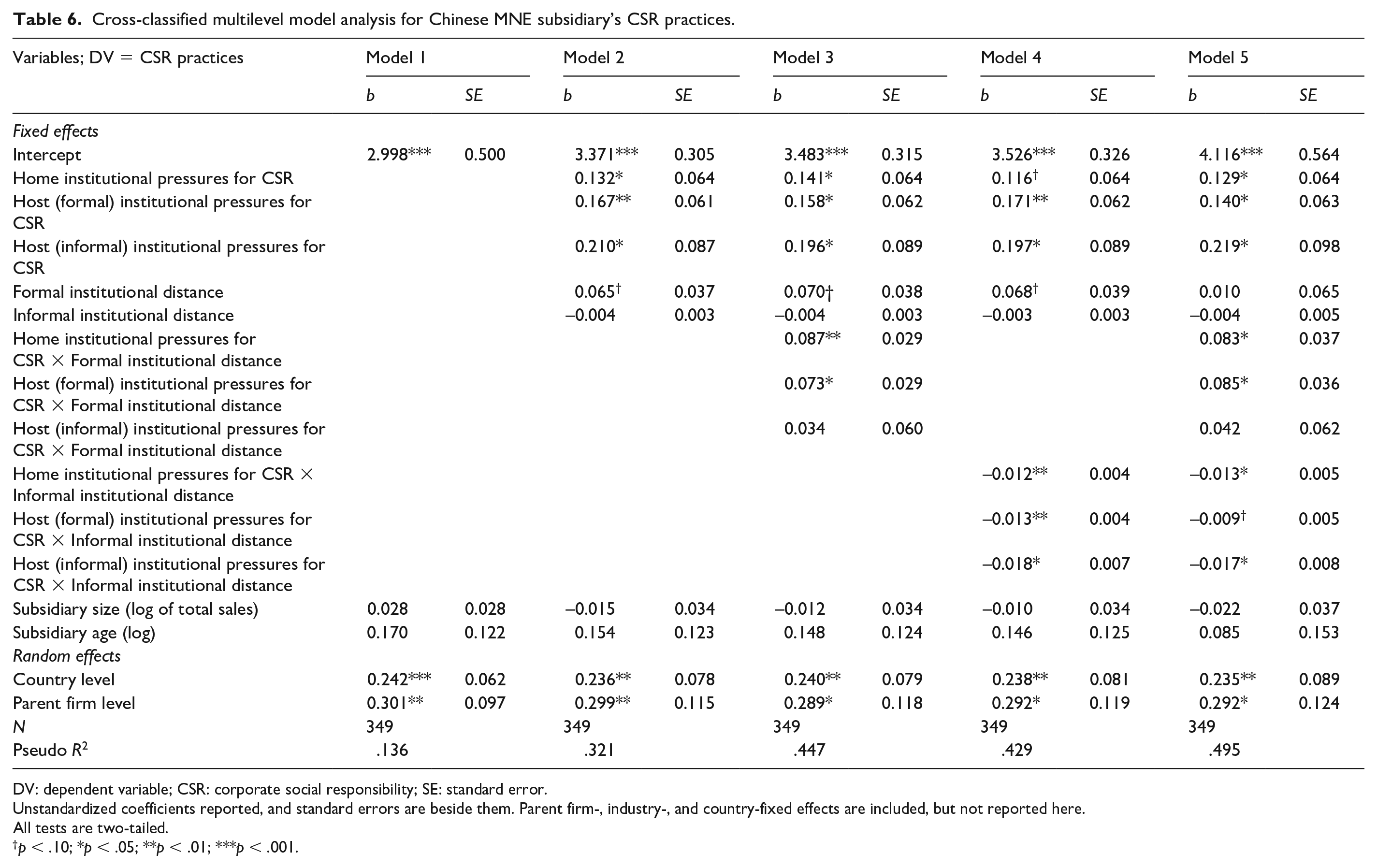

Table 6 exhibits the results of the cross-classified multilevel model analyses. In Model 1, we include only the control variables. Both subsidiary size and age are positively but insignificantly associated with CSR practices.

Cross-classified multilevel model analysis for Chinese MNE subsidiary’s CSR practices.

DV: dependent variable; CSR: corporate social responsibility; SE: standard error.

Unstandardized coefficients reported, and standard errors are beside them. Parent firm-, industry-, and country-fixed effects are included, but not reported here.

All tests are two-tailed.

p < .10; *p < .05; **p < .01; ***p < .001.

In Model 2, we add the independent and moderating variables. All three independent variables (i.e., home institutional pressures, and host [formal] institutional pressures, and host [informal] pressures for CSR) are positively and significantly associated with CSR practices (bHome-CSR = 0.132, p < .05; bHost-CSR = 0.167, p < .01; bHost-NGO = 0.210, p < .05); hence, Hypotheses 1 and 2 are supported. The direct effects of two moderating variables (i.e., formal and informal institutional distances) show mixed results, although their signs are opposite (bFD = 0.065, p < .10; bID = −0.004, p > .10).

In Model 3, we add the three interaction terms of home and host institutional pressures for CSR and formal institutional distance. As predicted, the interaction term between home institutional pressures for CSR and formal institutional distance and the interaction term between host (formal) institutional pressures for CSR and formal institutional distance are positively and significantly associated with CSR practices (βHome-CSRxFD = 0.087, p < .01; βHost-CSRxFD = 0.073, p < .05). Meanwhile, the interaction term between host (informal) institutional pressures for CSR and formal institutional distance is positively but non-significantly associated with CSR practices (βHost-NGOxFD = 0.034, p > .10). Hence, these results for these interaction terms support Hypothesis 3a fully but Hypothesis 3b only partially. These results are consistent in Model 5 as well.

In Model 4, we add the three interaction terms of home and host institutional pressures for CSR and informal institutional distance. As we assumed, the interaction term between home institutional pressures and informal institutional distance and the interaction terms between host (formal and informal) institutional pressures for CSR and informal institutional distance are all negatively and significantly associated with CSR practices (βHome-CSRxID = −0.012, p < .01; βHost-CSRxID = −0.013, p < .01; βHost-NGOxID = −0.018, p < .05). Thus, the results for these interaction terms support Hypotheses 4a and 4b. These results, too, are consistently supported in Model 5.

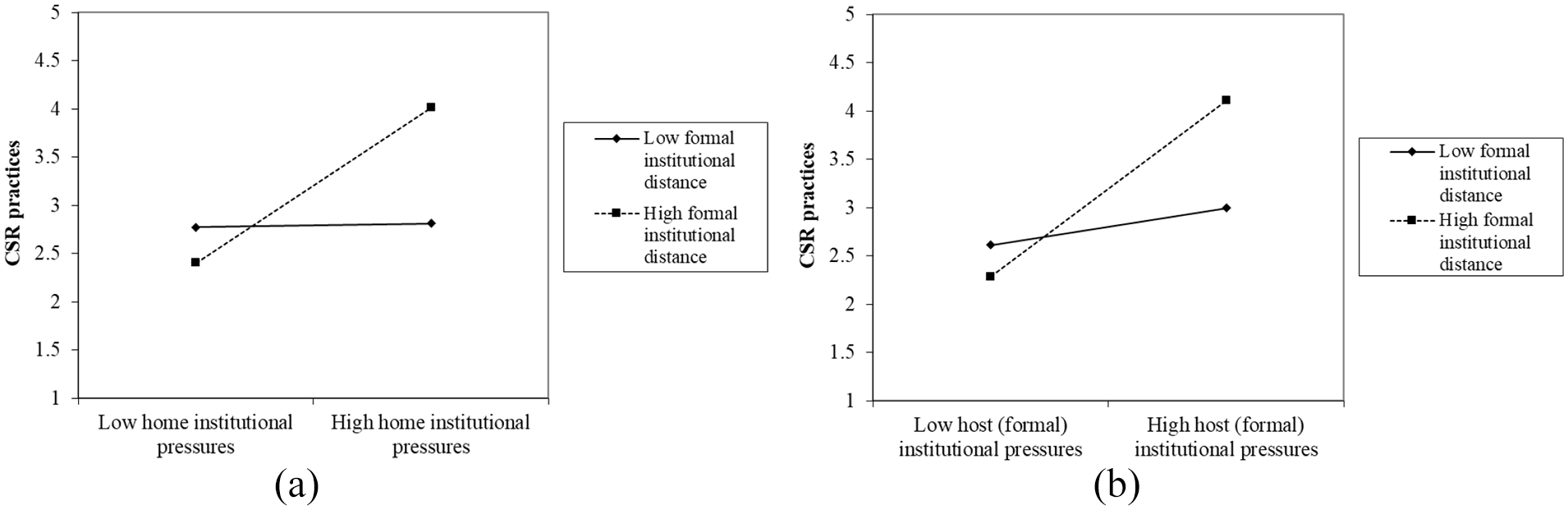

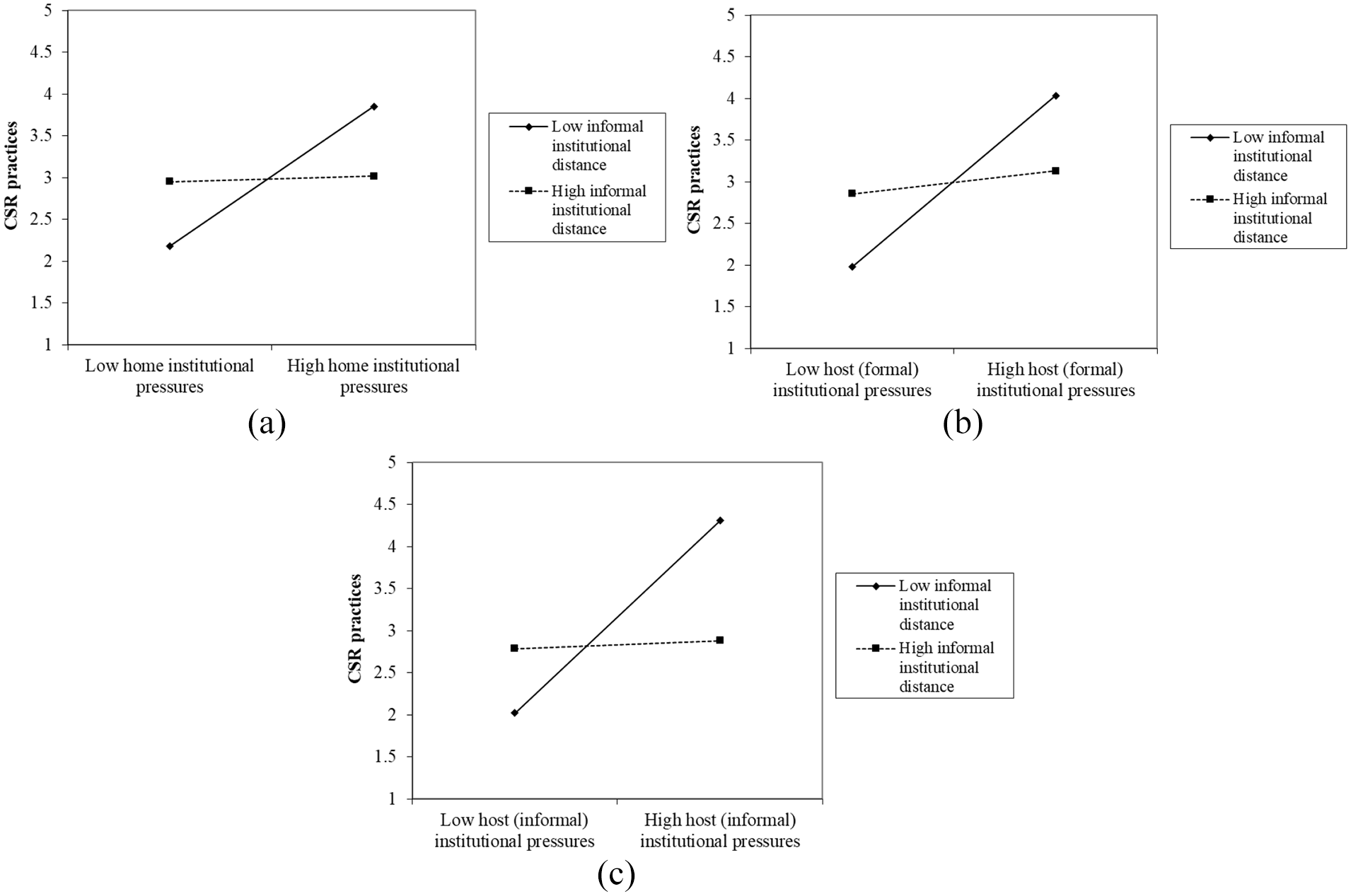

We plot all these interaction effects except for one insignificant interaction term (host [informal] institutional pressures for CSR × formal institutional distance) in Figures 2(a) and (b) and 3(a) to (c) and find consistencies with the results, thus, supporting Hypotheses 3a, 4a, and 4b fully but Hypothesis 3b partially. Finally, Model 5 is a full model, so in this model we include all the variables and interaction terms, showing consistent findings, as mentioned previously.

(a) The interaction effect between home institutional pressures for CSR and formal institutional distance. (b) The interaction effect between host (formal) institutional pressures for CSR and informal institutional distance.

(a) The interaction effect between home institutional pressures for CSR and informal institutional distance. (b) The interaction effect between host (formal) institutional pressures for CSR and informal institutional distance. (c) The interaction effect between host (informal) institutional pressures for CSR and informal institutional distance.

Discussions and conclusion

In this study, we find that the home-country government significantly affects MNE subsidiaries’ CSR practices through institutional support or restrictions. Also, the findings show that the CSR of MNE subsidiaries is closely related to the institutional environment of the host country. Formal and informal pressures from institutions in the host country motivate the MNE subsidiaries to foster CSR commitment and practices. MNE subsidiaries’ CSR activities are socially constructed and context-specific (Ringov & Zollo, 2007). In addition, local governments and NGOs demonstrate their significant roles as key agents in transmitting the institutional contexts of host countries to the subsidiaries. MNEs, through dialogues with local governments and NGOs, can interpret the institutional context and identify the responsibility demanded by the local society for the firms (Aguilera et al., 2007; Arya & Zhang, 2009).

To gain a further nuanced understanding of institutions and the institutional effect on MNE subsidiaries’ CSR behaviors, investigating the role of various institutional forces in the host and home countries as well as the interplay among these forces is critical. To overcome the limitations of prior studies on institutions and MNEs’ CSR activities, this study employed two categories of moderating variables (i.e., formal institutional distance for Hypotheses 3a and 3b and informal institutional distance for Hypotheses 4a and 4b) in the conceptual model. Our results show that home and host institutional pressures for CSR have a positive effect on CSR practices. Formal institutional distance enhances these positive effects while informal institutional distance mitigates these positive effects.

Importantly, our findings provide a perspective that is different from the prevailing view, namely regarding the roles of the direct effects of institutional forces in the home and host countries and the effects of the institutional distance between home and host countries in explaining MNEs’ strategic choices or behaviors (Cui & Jiang, 2012; Wang et al., 2012). Apart from the independent main effects of formal and informal institutional forces in host countries, the interaction effects of formal and informal institutional forces and differences in institutions between the home and host countries explain a significant amount of variation in the intended nonmarket strategies of MNE subsidiaries to engage in CSR activities abroad, which in turn significantly shapes MNEs’ CSR practices.

Theoretical implications

Our study contributes to the literature on MNE subsidiaries’ CSR in international business. First, it adds to institutional theory by identifying critical elements facilitating CSR practice and informing prime movers, which expedite organizational triumph in the global context. Both international business scholars and practitioners conventionally tend to regard CSR as an unnecessary cost that does not help to overcome LOF in host markets. Such perception has often played a pivotal role in causing MNE failure in public relations. For the same reason, empirical experiments examining MNE CSR practices remain in their infancy (Park & Ghauri, 2015). Our model suggests that the effects of home- and host-country governments and host-country NGOs, as key institutional constituents, influencers, and exercisers surrounding local business environments, can be crucial to institutional settings and act as a trigger in significantly changing MNE subsidiaries’ CSR practices.

Second, the findings extend the research on MNEs’ CSR strategies and institutionalism. This study has clarified how different institutional environments influence the social activities of MNE subsidiaries (e.g., Lee, 2011; Mellahi et al., 2016; Reimann et al., 2012; Yang & Rivers, 2009). These subsidiaries operate under institutional diversity, requiring the consideration of the dynamic and intricate institutions in both the home and host countries. Thus, explaining MNEs’ business environment from the “thin” view of institutions of previous studies (Jackson & Deeg, 2008), in which institutions were described using summary indicators or unidimensional parameters, is insufficient. By applying an institutional perspective to the large MNE boundaries through the inclusion of home- and host-country institutions, this research depicts MNEs’ institutional environments in a rich and stereoscopic manner. Therefore, the study identifies the path upon which MNEs approach institutional systems and establish nonmarket strategies to obtain legitimacy in the host country.

Our third contribution is a conceptualization of institutions that considers the host- and home-country institutions in the model. The validated model demonstrates both home and host (formal) institutional pressures for CSR as well as formal and informal institutional distances between the home and host countries that moderate the effects of host institutional pressures on MNE subsidiaries’ CSR practices. Using social strategies helps MNEs resolve institutional ambiguity overseas, thereby legitimizing their business activities within uncertain institutional environments. By looking beyond the independent main institutional effects (Berry et al., 2010), our study paves the way for the exploration of the dynamic and complex interactions and influences of diverse institutions on CSR.

Finally, the study extends the literature on emerging market MNEs’ nonmarket strategies by showing the interconnected yet varied institutional forces that shape their international strategic choices. Although the literature has made substantial progress in enriching our understanding of the strategic behaviors of MNEs from emerging economies, the paucity of research that empirically tests established theories in the context of various institutions remains large (Mellahi et al., 2016; Puck et al., 2018; Xiao et al., 2013). As such, our work extends and refines the institutional logic by examining the extent to which home market institutional pillars and the institutional distance between the home and host countries influence emerging economy MNEs’ social strategies abroad, above and beyond market and political strategies (see Banerjee & Venaik, 2018; White et al., 2018).

Practical implications

Our results provide valuable and practical guidelines for local policymakers and practitioners. The laws, rules, and public policies imposed by host governments are commonly the essential principles with which MNE subsidiaries operate in host countries and are generally applied to the business activities within their boundaries. As most governmental regulations institutionalize and codify the moral values of a society, meaning that MNEs are noticeably both violating laws and engaging in unethical behavior, MNEs may be subject to legal sanctions as well as criticism from members of local society. This explanation clearly indicates that local policymakers need to pay particular attention to the design of the legal environment and institutional measures to push MNE subsidiaries to good citizenship in host economies.

In addition, the increased activities of NGOs often trigger changes in institutional environments, to which MNEs need to adapt, thereby potentially creating a causal link between the unethical behaviors of particular MNE subsidiaries and undesirable social outcomes stemming from those actions; these function as formidable pressures on MNEs to change their policies and schemes. This means that NGOs play a primary change agent role in altering corporate behaviors and the subsequent strategies. In particular, MNEs are continuously faced with a series of international agreements and codes of conduct that are aimed at supervising their behavior, many of which are enforced by NGOs. In other words, NGO activism is the main element driving ethical justice in corporate management activities. In this vein, considering MNE CSR in host countries, policymakers should try to nurture local NGOs so that these can more thoroughly campaign against MNE subsidiaries to kickstart them into improving their CSR in local markets.

Taken together, our study provides valuable managerial implications for managers of MNE subsidiaries. It also suggests that MNE subsidiaries should take their host- and home-country institutions into account when formulating CSR strategies. To reiterate, instead of viewing institutions as backgrounds and firms as independent from their institutional surroundings, host institutional pressures in particular positively influence the intended CSR of MNE subsidiaries, causing them to consider and engage in CSR in the host country. However, whether MNE subsidiaries abroad will be willing, and therefore conform to, such host institutional pressures remains unclear because firms’ strategic responses are often frequently motivated by self-interest. In such situations, home-country institutions play an important role in encouraging the key efforts of MNE subsidiaries in the host country, such that MNEs will consider and engage in CSR.

Furthermore, managers of MNE subsidiaries should take the institutional distance between the home and host countries into account when formulating their CSR strategies abroad. Managers in these MNE subsidiaries should recognize the importance of formal and informal institutional distances in influencing firms’ CSR responses to local institutional pressures in the host country. By considering and bridging the institutional differences between the home and host countries, managers of MNE subsidiaries will be further prepared to decide how to successfully incorporate the effects of external institutional environments into their CSR decision-making processes. Therefore, for managers of MNE subsidiaries, a clear understanding and comprehensive assessment of the institutional differences between the home and host countries is critical for a full grasp of the challenges and opportunities of overseas operations.

Limitations and future research

This study attempted to clarify the influence of institutional pressures from home and host countries on the CSR practices of MNE subsidiaries; however, there are several limitations. First, this study may have a limitation in that it did not develop more sophisticated items to properly measure institutional pressures and CSR practices. It could be argued that the number of items used in this study is small, making it difficult to sufficiently reflect complex multidimensional institutional pressures and CSR practices. However, previous studies dealing with institutional pressures in home and/or host countries (e.g., Chung et al., 2016; Cui & Jiang, 2012) used only two or three measurement items for these variables. Also, our measurement items of CSR practices were based on previous studies (e.g., Luo, 2006) in the vein of the philanthropic contribution of CSR, which originally captured this construct using only three items. However, this issue still has some limitations, and thus, further research is needed to develop more detailed measurement items for these variables to improve the depictions of institutional pressures and CSR practices.

Second, this study’s focus on Chinese MNE subsidiaries may raise concerns regarding generalizability. Using this sample of Chinese MNE subsidiaries, the validated model shows that institutions do matter. However, a reasonable question arising from this finding is whether the implications are specific to Chinese foreign investing firms. The Chinese government has significantly reformed and improved home institutions and social policy instruments in comparison with other emerging economies. However, we also believe that the theoretical arguments developed in this study may be applicable to several other large emerging economies, such as the other BRICS countries (Brazil, Russia, India, and South Africa). This is because the home-country government may also play an important role in shaping MNE subsidiaries’ nonmarket strategic practices and choices abroad by encouraging or restricting the outward FDI of these firms. Nevertheless, this issue may offer a valuable opportunity for future researchers to select other samples of foreign investing firms and explore whether the findings of this study can be generalized beyond the context of MNE subsidiaries originating from China, the largest emerging economy in the world.

Finally, additional limitations may reside in the fact that our study did not consider subsidiary size. However, the influences of home- and host-country institutions experienced by MNE subsidiaries may vary according to organizational size. Thus, subdivisions of the sample into large, small, and medium-sized MNEs could be a future research avenue. Another weakness of this work could stem from the fact that the different dimensions (e.g., ethics codes, organizational credibility, and philanthropic contribution) of CSR practices were not considered, although factors promoting CSR activities may depend on such CSR characteristics. This issue also indicates that further consideration, including the innate attributes of CSR practices, will extend our understanding and can lead to additional attention-grabbing future research.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study was funded by Hankuk University of Foreign Studies Research Fund.