Abstract

This article contributes to the literature by indicating how certain monetary policies impact the compensation incentives of US managers to adopt riskier business policies. Specifically, based on the agency problems between shareholders and managers and between shareholders and creditors, a research framework is developed to identify the influence of low interest rates on managers’ risk-taking incentives proxied by the sensitivity of executive compensation to stock return volatility (Vega). We examine 1,293 firms in the United States between 2000 and 2016, and the results indicate that low interest rates increase the managers’ short-term risk-taking incentives and that those incentives contribute to the risk effectively taken by the firm. Our results are robust to the use of alternative monetary proxies and to the presence of passive versus active institutional shareholders.

Keywords

Introduction

Monetary policy transmission has changed in the United States in recent decades. Furthermore, after the burst of the housing market bubbles in the United States and Europe (Boivin et al., 2010; Gambacorta & Marques-Ibane, 2011) the banking sector has high leverage, and interest rates have decreased substantially to incentivize borrowing. Interest rates are at historically low levels, and consequently, there is an increase in credit availability due to an expansive macroeconomic policy (Maddaloni & Peydró, 2011). The short-term nominal interest policy (nearly zero) was implemented after the financial crisis of 2007 by the US Federal Reserve, causing a zero lower bound (ZLB) policy. Consequently, the credit supply increased, affecting the relationships between creditors and managers.

However, managerial compensation has grown dramatically since the 1980s. During this time, there have been significant changes in the form of compensation for executives. Stocks and options have become essential incentives for CEOs. However, in spite of the plethora of literature studying the determinants and effects of managerial compensation, the influence of macroeconomic policies on the risk-taking incentives of executives is still unknown. Our objective is to fill this void and study how the managers’ risk-taking incentives change due to low-interest-rate monetary policies.

Following Brockman et al. (2010), Coles et al. (2006), Fich et al. (2014), and Liu and Mauer (2011), among others, we focus on the compensation of CEOs due to their role in managing the business strategies of the firm. Previous literature (Cohen et al., 2000; Coles et al., 2006; Dong et al., 2010; Gormley et al., 2013; Guay, 1999) finds that managers with high Vega (sensitivity of executive compensation to stock return volatility) tend to engage in higher risk-taking behavior since their compensation increases when the business is more volatile. In this way, the firms’ boards can use CEOs equity compensation to align shareholders’ and managers’ interests to solve this agency conflict. In fact, empirical evidence has demonstrated quick adjustment of CEO compensation in response to external shocks (Bakke et al., 2016; Gormley et al., 2013; Hayes et al., 2012; Hong, 2019) and subsequent modification of business policies to take or cut business risks (Saunders & Song, 2018).

In this article, the external factor under study with potential effects on risk-taking compensation incentives is a low-interest-rate monetary policy. Given that interest rates are the main components of the firm’s cost of capital, which is a basic element of the managers’ decision-making concerning both the financing and investing policies of the firm, that interest rates are the main drivers of the investors’ expected return, and that interest rates are the fundamental macroeconomic variables behind credit, a relevant effect can be expected from a new risk-return setting for shareholders, managers, and creditors induced by changes in interest rate policies.

Specifically, low interest rates have been found to encourage investors’ risk-taking through psychological mechanisms such as reference dependence 1 and salience 2 (Lian et al., 2019). Therefore, as investors searching for yield, shareholders would be induced by low interest rates to encourage managers to take more risks. In addition, a low-interest-rate policy has been found to reduce the perception of credit risk and increase the risk tolerance of banks as credit suppliers through different channels (Bernanke & Gertler, 1995; Borio & Zhu, 2012; Paligorova & Santos, 2017). Therefore, we can expect that the relevant monitoring role of creditors in controlling the mangers’ risk-taking incentives (Balsam et al., 2018; Saunders & Song, 2018) could be offset or weakened by the creditors’ risk-taking channel. In this way, the agency conflict between shareholders and creditors would be attenuated in a low-interest setting by the alignment of shareholders’ and creditors’ interests to obtain higher returns. Managers’ risk-taking incentives would be increased by the board to improve business returns and by a relaxation of the bank monitoring of excess risks. The manager channel means that managers offered risk-taking incentives would use their discretion in making financing and investing decisions to adopt riskier policies in line with the shareholders’ interests. As these riskier policies aggravate the creditor–shareholder agency conflict, creditors would use their monitoring ability to limit both the managerial risk-taking incentives and the firms’ riskier policies. In our research context, the creditor channel means that CEO risk-taking incentives are higher and that riskier policies are undertaken by managers only when creditors themselves are searching for yield at the expense of higher risk. Our empirical work builds on this theoretical framework to check if the subsequent business policies and overall firm risk indicates the predominance of the manager channel versus the creditor channel in solving the creditor–shareholder agency conflict (Hong, 2019; Saunders & Song, 2018).

Taking into account the study by Edmans et al. (2012), where it is suggested that contract sensitivity is affected by the temporal horizon, we have computed a comprehensive Vega for each CEO and then distinguished between vested and unvested Vega to separately analyze the short-term and long-term horizons. Therefore, as a more specific objective, we can assess whether the monetary policy has differential effects on managers’ compensation incentives depending on the compensation horizon.

In summary, this article combines three strands of literature on monetary policies, CEO pay incentives, and risk-taking business policies and uses a panel database of 1,293 US firms (9,252 firm-year observations) over the 2000–2016 period to examine whether low-interest-rate monetary policies increase short-term risk-taking incentives of managers (proxied by Vega), and whether these incentives exacerbate the influence of those monetary policies on the firms’ risk-taking. Our results are robust to the use of alternative proxies for monetary policy and to the presence of institutional investors. To our knowledge, this study is the first work in which the effects of monetary policies on CEO compensation incentives have been analyzed.

The main contribution of this article is in the research stream on managers’ risk-taking incentives proxied by Vega. Our research extends the previous evidence by showing that low-interest-rate policies affect CEOs’ short-term risk-taking incentives with an effect on the risk effectively taken by the firms. We identify an external factor derived from the monetary policy, and our results suggest an alignment of interests between creditors and shareholders and between shareholders and managers concerning the firms’ risk-taking. Specifically, managers’ higher risk-taking incentives in a short-term low-interest setting are consistent with both the shareholders’ and creditors’ interest in higher returns, as both groups of stakeholders may influence managers’ compensation incentives. Furthermore, the contribution of the short-term risk-taking incentives to the riskier policies adopted by the firms under analysis is only seen in a low-interest setting, which is consistent with the creditor channel. That is, the creditors tend to extend credit in softer conditions, which works with the shareholders’ incentive to obtain higher profitability in the short run. Consequently, both interests would be aligned to encourage (or not avoid) undertaking riskier projects by firms’ managers.

The rest of the article is organized as follows. Section “Theoretical background and hypotheses” presents a discussion of the arguments that link managerial risk-taking incentives and firms’ risk-taking to low-interest-rate monetary policy. In section “Data overview and variable measurement,” we describe our data, the measurement of key variables, and the models used. Section “Empirical results ” shows the empirical results, and section “Conclusion” presents the article’s conclusions.

Theoretical background and hypotheses

Monetary policy and risk-taking

The monetary transmission mechanism has evolved both in theory and modeling over time in the United States, producing changes in policy behavior as well as in the effects that the policy interest rates have on the economy (Boivin et al., 2010). In addition, credit provision regulations have significantly changed. Gambacorta and Marques-Ibane (2011) argue that the changes in banks’ business models and market funding patterns were the factors behind the modification of the monetary transmission mechanism in the United States and Europe before the 2007 crisis, finding that the structural changes deepened during the crisis.

There are several ways in which monetary policy influences the economy. According to the interest rate channel, the borrowers’ demand for credit increases as the price (interest rate) decreases (Paligorova & Santos, 2017). The strongest effect occurs on short-term interest rates, whereas the impact on long-term rates is relatively weaker (Bernanke & Gertler, 1995). The credit channel theory explains that the effect of interest rates is amplified by the changes in the external finance premium (difference in cost between external and internal funds). Through the balance sheet channel, the amplifying effect comes from the impact of the monetary policy on the borrowers’ financial position 3 (Bernanke & Gertler, 1995; Paligorova & Santos, 2017), whereas through the bank lending channel, 4 the amplifying effects come from the impact of the monetary policy on the supply of loans by banks (Bernanke & Gertler, 1995; Brissimis & Delis, 2009; Kishan & Opiela, 2000).

Some authors (Den Haan et al., 2007) find a differential “balance-sheet effect” for consumers and firms. This effect is either attributed to the larger fraction that higher interest rates take of consumer expenditures, or to the decreasing effect of growing interest rates on property prices. The additional consumer risk detected by banks would explain the reduction of consumer and real estate loans parallel to the increase in firm loans.

From the borrowers’ perspective, through the credit channel, a reduction in interest rates modifies the target rates of return. Since the effect is stronger for larger gaps between market and target rates, they are powerful when nominal rates are close to zero, such as with the ZLB interest rates (Borio & Zhu, 2012). Thus, investors search for yield, turning to riskier assets due to their previously stablished reference returns and the salience of those higher returns from risky assets (Lian et al., 2019). Finally, in addition to the reduced risk perception and the increased risk tolerance derived from the higher value of assets, cash flows, and profits when interest rates go down (balance sheet channel), we highlight the interconnection between liquidity and risk-taking in periods of weaker constraints, which act as a multiplier effect in monetary policy transmission allowing the counterparts to engage in riskier projects (Borio & Zhu, 2012).

From the creditors’ perspective, a further step in the bank lending channel research stream concerns the monetary policy effects on credit risk-taking, which are labeled the “risk-taking channel.” 5 It has been empirically detected in the euro-area and the United States that low short-term interest rates are linked to a softening of the standards for household and corporate loans. Securitization and weak supervision for bank capital are found to amplify the softening factor, contributing to a prolonged effect. In contrast, low long-term interest rates do not soften lending standards (Maddaloni & Peydró, 2011). Similar results are found by Jiménez et al. (2014) with an exhaustive credit register of Spanish loan applications and contracts.

Concerning the interest rate risk, previous studies (Baker et al., 2016; Creal & Wu, 2014) propose different measures for the policy uncertainty, highlighting the importance of capturing the macroeconomic fluctuations. According to Creal and Wu (2014), a highly uncertain market could accelerate the ZLB adoption for the short-term interest rate.

Risk-taking by managers and executive compensation

According to the previous literature, the sensitivity of the managers’ wealth is one of the main effects of equity-based compensation related to the risk-taking behavior of CEOs. Specifically, the sensitivity of executive compensation to stock-return volatility, or the Vega effect, encourages managers to take more risks caused by the convex remuneration structure of options. Therefore, a higher sensitivity of executive compensation to stock return volatility or a higher Vega might lead to riskier business choices by managers since they can obtain a higher compensation when the business is more volatile, as suggested by Cohen et al. (2000), Coles et al. (2006), and Guay (1999).

In the literature, firms’ boards have been found to quickly adjust compensation incentives to external shocks and new settings for firm risk. Thus, for example, after the implementation of the FAS 123R (accounting regulation), firms significantly reduced option-based compensations (Bakke et al., 2016; Mao & Zhang, 2018; Hayes et al., 2012; Hong, 2019). Another example of quick adjustment of incentives by boards considering increased risk from an exogenous cause was studied by Gormley et al. (2013), who focused on the discovery of a carcinogen in a chemical used by the firm. However, the reaction of compensation incentives to changes in interest rates has not been previously analyzed. We try to fill this void by considering that interest rate changes have relevant consequences on both the financial and investment policies of the firm. Therefore, the firms’ boards would be encouraged to modify incentives due to interest rate changes. Furthermore, the boards (shareholders) themselves, as investors, would be pushed to search for yield in the presence of low interest rates.

Another research stream has evidenced that the CEO compensation incentives are significantly induced by bank monitoring (Balsam et al., 2018; Saunders & Song, 2018). Due to it, we incorporate the risk-taking channel derived from the monetary policy to reason about the potential effect of the interest rates on CEO compensation incentives.

Regarding the relationship between CEO risk-taking incentives and the risk effectively taken by the firm, previous literature has confirmed a positive effect on comprehensive measures of uncertainty (Gormley et al., 2013; K. Kim et al., 2017; Serfling, 2014) but also on riskier financing policies and investing policies (Gormley et al., 2013; Hayes et al., 2012). Specifically, a higher Vega is found to be associated with greater leverage 6 (Coles et al., 2006; Gormley et al., 2013), more R&D expenditures (Gormley et al., 2013), fewer investments in fixed assets (Coles et al., 2006), less hedging with derivative securities (Bakke et al., 2016; Knopf et al., 2002), and less cash reserves (Gormley et al., 2013). Therefore, a higher Vega would increase the agency cost between managers and creditors, as well as between managers and shareholders.

In the case of creditors, some monitoring instruments can be used to control for managers’ risk-taking behaviors. Thus, Liu and Mauer (2011) indicate that CEOs with a high Vega are required to hold additional cash balances to reduce bondholder risk. Brockman et al. (2010) indicate that an increase in Vega is related to a shorter maturity of the debt structure. Specifically, they and other authors (e.g., Barnea et al., 1980; Leland & Toft, 1996) show that short-term debt could reduce managerial incentives to increase risk and act as a powerful monitoring tool for creditors.

However, how the CEO’s pay contract is designed is even more important than the incentive amounts (Jensen & Murphy, 1990). The horizon in which the incentives are exercised is a relevant aspect in the design of executive compensation packages. According to Edmans et al. (2012), CEOs prefer shorter incentive horizons since they can obtain higher future rewards by saving privately than by obtaining payments planned in contracts. The previous literature has debated on the optimal duration of executive compensation. For instance, Bebchuk and Fried (2010), among others, indicate that pay contracts are focused excessively on short-term performance, which could lead to self-interested and frequently myopic managerial behavior. However, some authors (Bolton et al., 2006; Gopalan et al., 2014) show that optimal compensation contracts might highlight short-term stock performance in line with the perspective of the firm’s existing shareholders. These incentives will make it attractive for managers to select projects that boost short-term performance, which is aligned with managerial interests such as early reputation enhancement (Thakor, 1990). Thus, CEOs with short-term incentives could engage in myopic managerial behavior, as they may make decisions with short-term effects that amplify risks.

Hypotheses

As discussed in the previous sections, the influence of monetary policy on managers’ risk-taking incentives and the risks effectively taken by managers is the question, not yet studied, for which this work attempts to offer a first approach. According to the literature on monetary transmission mechanisms, on the firms’ part, as borrowers, lower interest rates mean cheaper loans (interest rate channel), which induces managers to obtain more funds to be invested in the firms’ projects (Paligorova & Santos, 2017). In the case of firms as investors, a low short-term interest rate makes riskless assets less attractive for them. Hence, boards (shareholders) may be encouraged to look for higher yields by investing in riskier projects (Jiménez et al., 2014). After a decrease in interest rates, boards’ and managers’ “search for yield” would be addressed by psychological mechanisms, such as reference dependence and salience (Lian et al., 2019). Therefore, we can expect an alignment of interests: boards would adjust managers’ incentives to increase Vega, and managers would choose riskier investments to improve the business returns and their resulting rewards.

On the creditors’ part, the monetary transmission mechanisms work through the risk-taking channel (derived from the lending channel and the balance sheet channel), by which changes in policy rates modify risk perceptions and risk tolerance by banks. Lower interest rates encourage banks to soften lending standards (Jiménez et al., 2014; Maddaloni & Peydró, 2011). Specifically, Borio and Zhu (2012) and Paligorova and Santos (2017) point to subsequent changes in the degree of risk in banks’ portfolios, their pricing of assets, and the price and non-price terms of the funding. Therefore, the monitoring role of creditors on the managers’ risk-taking incentives would be relaxed since lenders are expected to provide more funds to invest in risky projects. Furthermore, a long period of ZLB would cause both a decrease in risk aversion by lenders and a deepened search for yield by boards and managers.

From the perspective of the potential agency conflicts between creditors and borrowers, two opposite forces are triggered by the decrease in interest rates. On one hand, lower interest rates could increase the use of bank assets since the debt repayment is less severe for firms, whereas boosted asset valuations, cash flows, and profits improve collateral and incomes (Borio & Zhu, 2012), and the risk-taking channel softens the creditors’ conditions. On the other hand, lower interest rates could increase agency problems between managers and creditors since CEOs might look for different choices of investing to obtain high yields, increasing moral hazard. According to Hong (2019) and Saunders and Song (2018), external shocks on the creditor–shareholder agency conflict are solved by the creditor channel with preference over the manager channel. In the case under study, the creditor channel would imply a relaxation of monitoring in line with the risk-taking channel of the creditor.

In sum, considering the board’s ability to adjust the CEO compensation incentives in the presence of external changes (Bakke et al., 2016; Gormley et al., 2013; Hayes et al., 2012; Hong, 2019; Mao & Zhang, 2018), we expect a change in Vega in response to interest rate modifications. As investors, the boards will be encouraged by interest rate cuts to promote higher risks to reach previous benchmarks for investment returns. Therefore, we expect an increase in Vega because of the yield-searching behavior of the boards. Furthermore, we expect that increase in Vega to be intensified (or not offset) by monitoring by creditors who are in parallel affected by their own risk-taking channel derived from the low-interest-rate monetary policy:

H1a. Low interest rates increase the sensitivity of a CEO’s compensation to stock return volatility.

In line with the finding that softening lending standards in the United States is linked to low short-term interest rates but not to low long-term interest rates (Jiménez et al., 2014; Maddaloni & Peydró, 2011), we tested whether the low-interest-rate monetary policy, addressed by short-term horizons have a preeminent effect on short-term compensation incentives, and we formulate a more specific hypothesis:

H1b. A low interest rate increases the sensitivity of a CEO’s short-term compensation to stock return volatility.

As a second step, we argue that the managers’ risk-taking incentives exacerbate the effects of the low-interest-rate monetary policy on the firms’ policy actions. First, following Gormley et al. (2013), Serfling (2014), Cain and McKeon (2016), K. Kim et al. (2017), and Ferris et al. (2017), aggregate risk-taking is measured through market return volatility. We predict that lower interest rates induce managers to choose riskier policies, which increases the volatility of the firm’s returns. This comprehensive effect would result from the manager’s preference for riskier investment and financial policies. Therefore, we use leverage as a proxy for the financial policies (like in Cain & McKeon, 2016; Ferris et al., 2017; Karpavicius & Yu, 2019) and capital expenditures as a proxy for the investment policies of the firm (like in Andreou et al., 2017; Hayes et al., 2012).

Low interest rates would induce managers to look for previous (higher) return benchmarks, turning to riskier investment alternatives (with salient interest spread) (Lian et al., 2019). The agency problem driven by career concerns and lack of diversification that pushes managers to less risky (suboptimal) policies than those preferred by shareholders (Demsetz & Lehn, 1985; Ferris et al., 2017) would be offset by the low-interest monetary policy, resulting in aligned interests between shareholders and managers. Therefore, a positive relation is expected between risk-taking incentives and the risk effectively taken by the firm’s managers, first proxied by the mentioned aggregate risk-taking measure, return volatility, and then by leverage and capital expenditure as proxies of the financial and the investment policies of the firm, respectively:

H2a. Low interest rates induce the sensitivity of a CEO’s compensation to stock return volatility to have a stronger positive effect on the risk taken by the firm.

We considered that the time horizon of pay incentives can influence managerial behavior, as some authors have demonstrated (Cadman & Sunder, 2014; Edmans et al., 2015). Specifically, Gopalan et al. (2014) showed how CEOs might seek business choices that amplify the risk for the firm when managers have short-term incentives. Therefore, in the context of our analysis, risk-taking incentives in the short-term horizon could be influenced by macroeconomic policies that reduce investment returns (low interest rates and monetary policy stability). In accordance with the above argument, we formulate a more specific hypothesis:

H2b. Low interest rates induce the sensitivity of a CEO’s short-term compensation to stock return volatility to have a stronger positive effect on the risk taken by the firm.

Data overview and variable measurement

Data sources and sample selection

We use data from a variety of sources: ExecuComp, 7 Compustat, Thomson Reuters, and the Federal Reserve. We collect data for the period from 2000 to 2016. Following previous studies, we remove financial firms (SIC codes from 6000 to 6999) from the list of selected firms. We use ExecuComp to collect executive compensation data, and then we merge the resulting database with firm-level characteristics extracted from Compustat and institutional ownership data from Thomson Reuters. Finally, we use data on macroeconomic policies in United States from the Federal Reserve and merge them with the characteristics of the CEOs, firms, and ownership. Observations with missing or zero values for total assets, and firm-years with market or book leverage outside the unit interval were excluded. The final sample is made up of a panel database of 1,293 industrial firms in the United States.

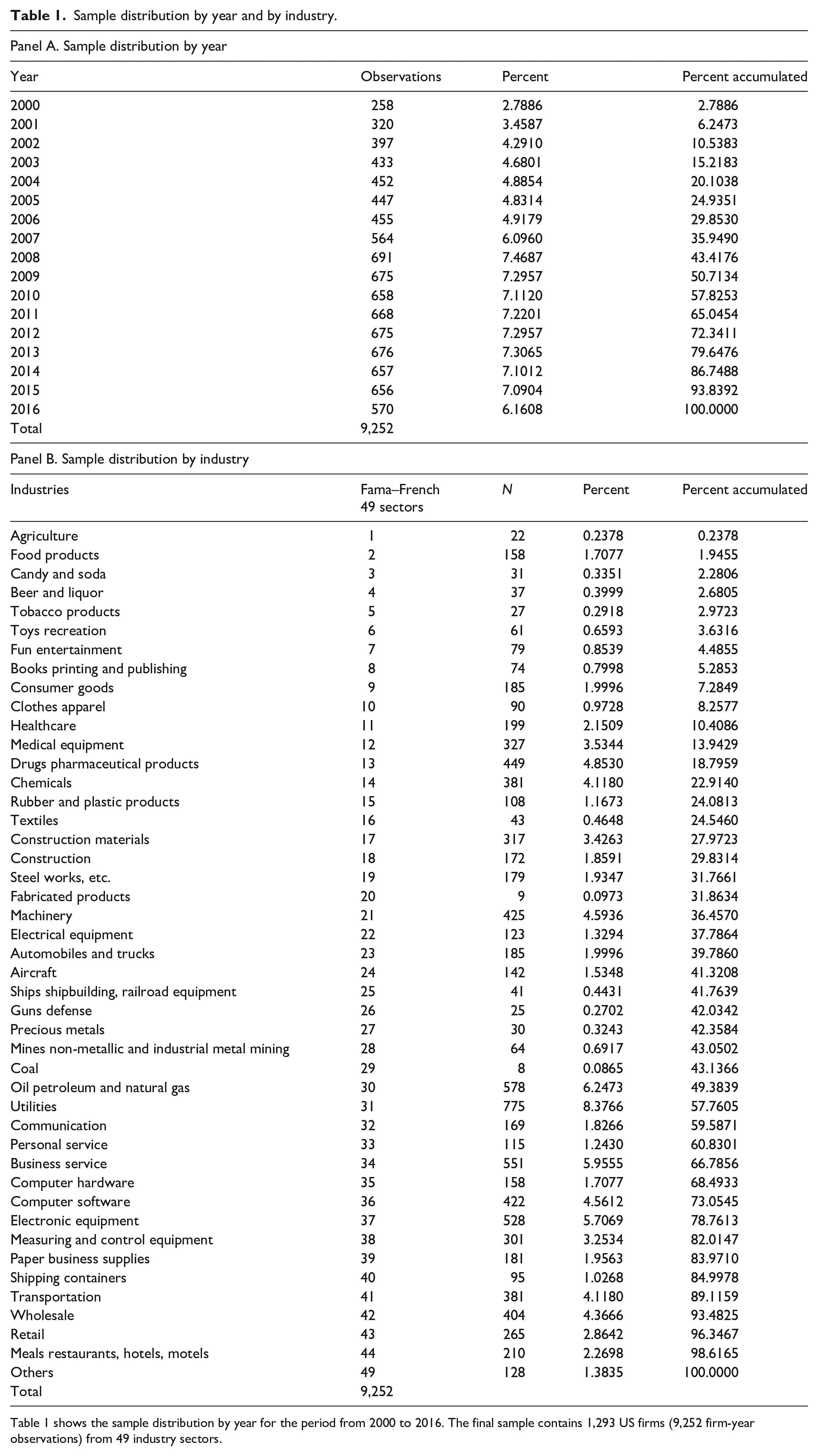

In Panel A of Table 1, we report the sample distribution by year. Our final sample contains 9,252 firm-year observations for 1,293 unique firms. The number of firms ranges from a minimum of 258 in year 2000 to a maximum of 691 in year 2008. In Panel B of Table 1, we report the sample distribution by industry breakdown based on the Fama and French industry classification. Overall, we observe that the “Utilities” and “Oil Petroleum and Natural Gas” sectors present the highest number of observations.

Sample distribution by year and by industry.

Table 1 shows the sample distribution by year for the period from 2000 to 2016. The final sample contains 1,293 US firms (9,252 firm-year observations) from 49 industry sectors.

Variables

Equity-based incentives

We measure the sensitivity of the CEO’s stock and option portfolio to stock return volatility or Vega (VegaCEO). It measures the change in the value of the CEO’s option portfolio due to a 1% increase in the standard deviation of firm stock returns. Vega is a conventional measure of risk-taking incentives in executive pay widely employed in the literature (see Brockman et al., 2010; Coles et al., 2006; Core & Guay, 2002; among others). We compute Vega following the methodology proposed by Coles et al. (2006) and Core and Guay (2002), which is based on the Black and Scholes (1973) option-pricing model adjusted for dividends by Merton (1973) (Appendix 1). Therefore, Vega should capture the incentives for CEOs to undertake investments that increase firm risk.

However, for different executives with the same Vega, benefits in the short run from an increase in firm volatility may differ depending on when their options can be exercised. To consider the horizon of incentives, we observe the vesting periods of the portfolio of options held by each CEO (Cadman & Sunder, 2014).

We decompose the Vega measure into both vested and unvested pay incentives. Vested Vega is defined as the value sensitivity to stock return volatility of all exercisable options which are the existing vested options. However, unvested Vega is the value sensitivity to stock return volatility of all unexercisable options, including those of newly granted options and existing unvested options. Consequently, a higher vested Vega might give prominent benefits to the CEO from stock return volatility in the short run.

Estimation method and control variables

To estimate how monetary conditions impact risk-taking incentives in executive compensation, we initially employ an econometric approach based on managers with high and low risks. As estimation method, we use the generalized method of moments—specifically, the system GMM—to partially solve the endogeneity (Arellano, 2003; Baltagi, 2005). Using panel data in our analyses, the biased results caused by unobservable heterogeneity can be alleviated. Blundell and Bond (1998) and Arellano and Bover (1995) support the efficiency of GMM because this estimator controls for the correlations among errors over time and the heteroscedasticity across firms. Specifically, following Munjal et al. (2018), the instruments we use in the estimation process are the lags from t − 2 to t − 5 of all explanatory variables and the lag of the dependent variable. In addition, system GMM reduces the collinearity among different explanatory variables, and is more efficient when the underlying economic process itself could be dynamic, as in our case

VegaCEOit is a measure based on the CEO’s option portfolio that indicates the risk-taking incentives of managers. Macroeconomic_conditionst are the variables under study. The measures we have used in this study as proxies for macroeconomic policy are ZLB, growth of interest rates, and the difference between long-term and short-term interest rates. First, to study the effect of interest rate policies, we use the zero lower bound (ZLB), a dummy equal to one if the year is between 2008 and 2012, when the short-term nominal interest rate was nearly zero in the United States. In the robustness analyses, we use the growth of the bank prime loan rate (G_INT) variable and the difference in the 10-year and the 6-month treasury constant maturity rates (Diff_10y_6m).

The control variables used concern CEO and board characteristics, the firm’s economic and financial situation, and the macroeconomic setting. Although the evidence found in the previous literature with respect to the effect of those variables on the risk-taking incentives of managers and the risk-taking policies of the firms is scarce and heterogeneous in general, we followed several works as references. For CEO and board characteristics, two control variables are selected considering their potential influence on corporate hedging (Bakke et al., 2016): the logarithm of the total cash compensation received by the CEO (BonusCEO) and the logarithm of CEO age (AgeCEO). The percentage of a company’s shares owned by the CEO (OwnCEO) is expected to behave similarly to a reduction in options and to have a potential effect on both compensation contracts and risk-taking (Gormley et al., 2013; K. Kim et al., 2017). Two other variables are selected as proxies of the CEO’s power: a dummy variable equal to one if the CEO is the Chairman of the Board (DualityCEO) and the number of executive officers on the board (Board_size) since powerful managers have discretionary authority and can engage in opportunistic investments according to their risk preferences (Andreou et al., 2017). We highlight the negative influence expected from AgeCEO as a proxy for risk aversion in line with the evidence found by Shen and Zhang (2013) and Serfling (2014).

For the firms’ economic and financial situation, we extend our models with some variables that plausibly affect the firms’ risk. The book-to-market ratio (BookMarket), the growth of sales (G_Sales), size (Size), firm profitability (Profitability), and the degree of asset tangibility (Tangibility) are widely recognized determinants of leverage (Cain & McKeon, 2016; Rajan & Zingales, 1995). The value of R&D expenses divided by total assets (R&D) 8 and the logarithm of the number of years since appearing in the Compustat database (Firm_age) are required to control for investment opportunities (Cain & McKeon, 2016). Furthermore, R&D, jointly with BookMarket and G_Sales, has been found to provide CEOs with risk-taking incentives (Ferris et al., 2017; Hayes et al., 2012). Book leverage (Leverage) can affect corporate hedging (Bakke et al., 2016), and has been identified as a mediating factor between risk-taking incentives and the risk effectively taken by firms (K. Kim et al., 2017). Finally, abnormal returns (Abnearn) is added to some of the previous variables to explain the firm’s debt maturity (Brockman et al., 2010; Hong, 2019). As already mentioned, except in the case of AgeCEO, previous evidence shows contentious or not significant effects on Vega for the other variables. Considering the macroeconomic nature or origin of our monetary proxies, used as drivers of interest, we have added the growth of US Gross Domestic Product (G_GDP) to control for the macroeconomic setting. We provide more detailed definitions of all variables in Appendix 2. β0 is the constant term and the other βs are the coefficients of the explanatory variables, Sk is the set of industry dummies, Yt is a set of time dummy variables, and ε it is the error term. All variables are winsorized at 1% and 99% to remove possible bias due to the presence of outliers.

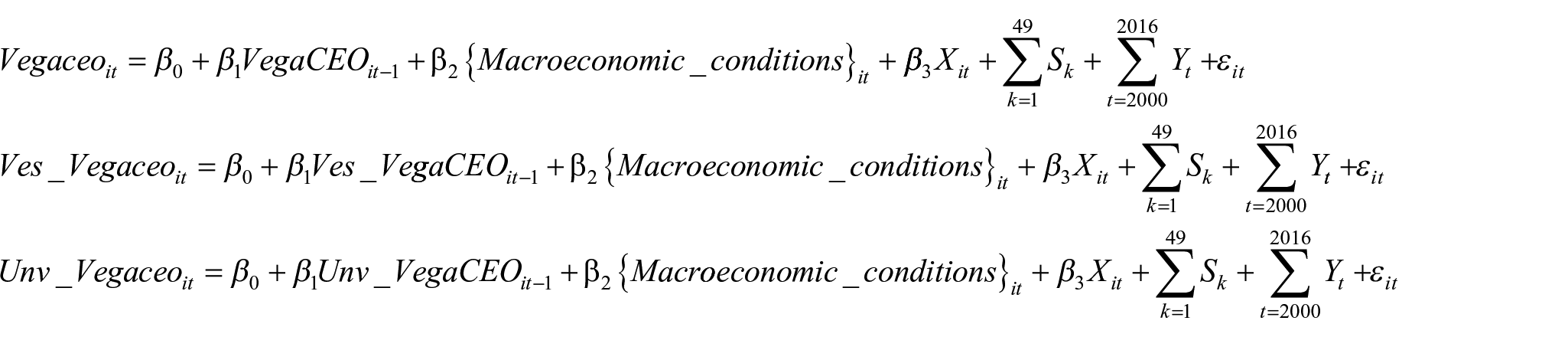

To observe the effect of macroeconomic conditions on the optimal duration of executive compensation, we split up the dependent variable into incentives with short-term maturities (Ves_VegaCEO) and those with long-term maturities (Unv_VegaCEO), studying the Model 1 in both cases.

To test our second hypothesis, Model 2 pays attention to the firms’ risk as an explained factor and examines how the effect of low-interest-rate monetary policy on corporate risk policies could change considering the risk taken by executives based on their compensation incentives. The dependent variable is corporate risk policies (CRP) proxied by three different variables: leverage, investment, and stock return standard deviation (STD_RET). In all cases, the main coefficient of interest is the interaction between the monetary policy proxy and VegaCEO

In an additional robustness analysis, whether macroeconomic conditions could alter the influence on CEO risk-taking incentives due to the institutional ownership structure is examined. To test for institutional ownership effects, we examine if the reaction of the managers’ risk-taking incentives in the presence of changes in the monetary policy varies for different types of institutional investors. Therefore, we classify institutional investors into two groups according to their interests and monitoring over management. We follow Almazan et al. (2005), who classify the proportion of shares owned by banks, insurance companies, and others as potentially passive monitors (Passive) and the proportion of shares owned by investors of other categories, such as investment companies and advisors, as potentially active monitors (Active).

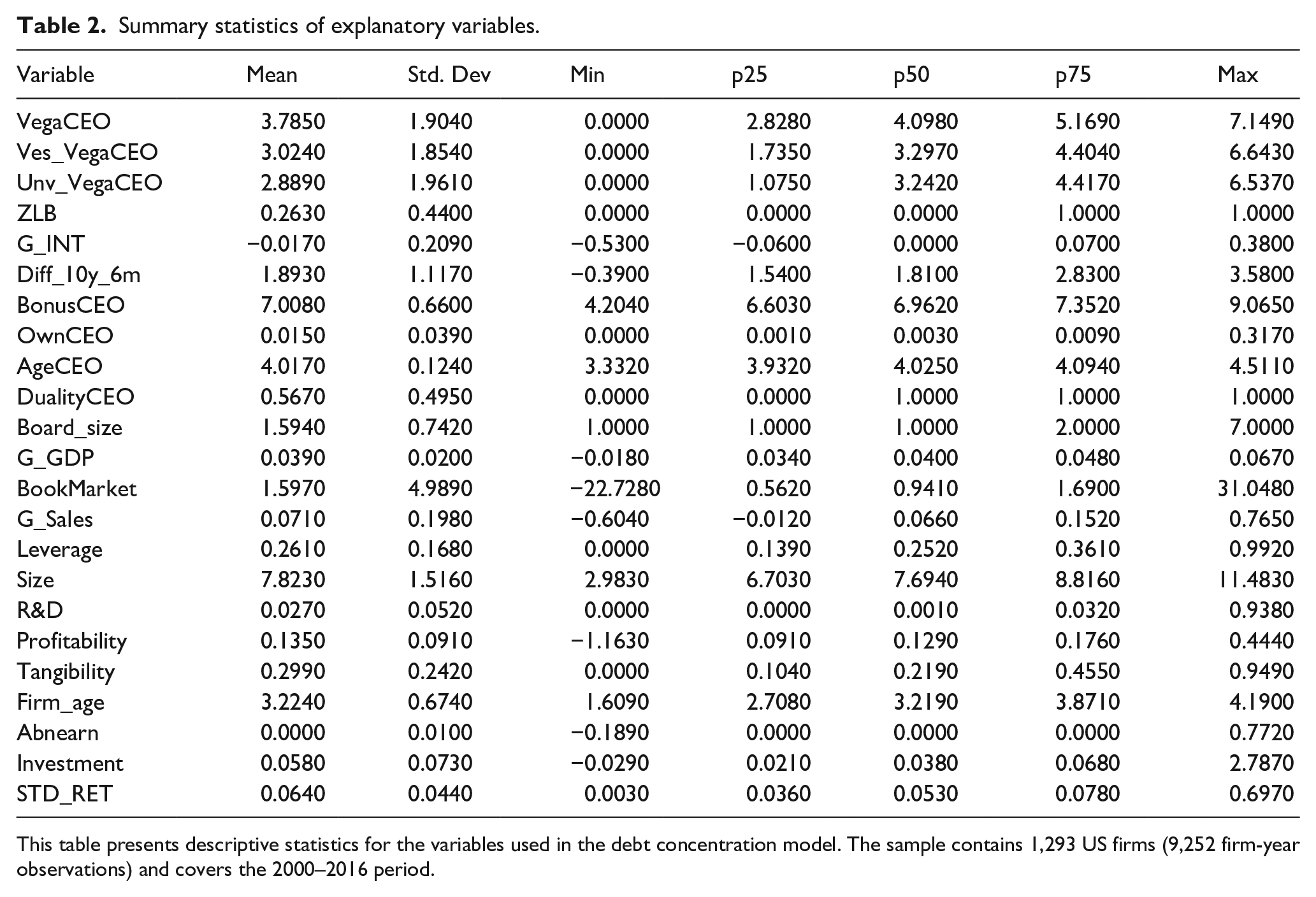

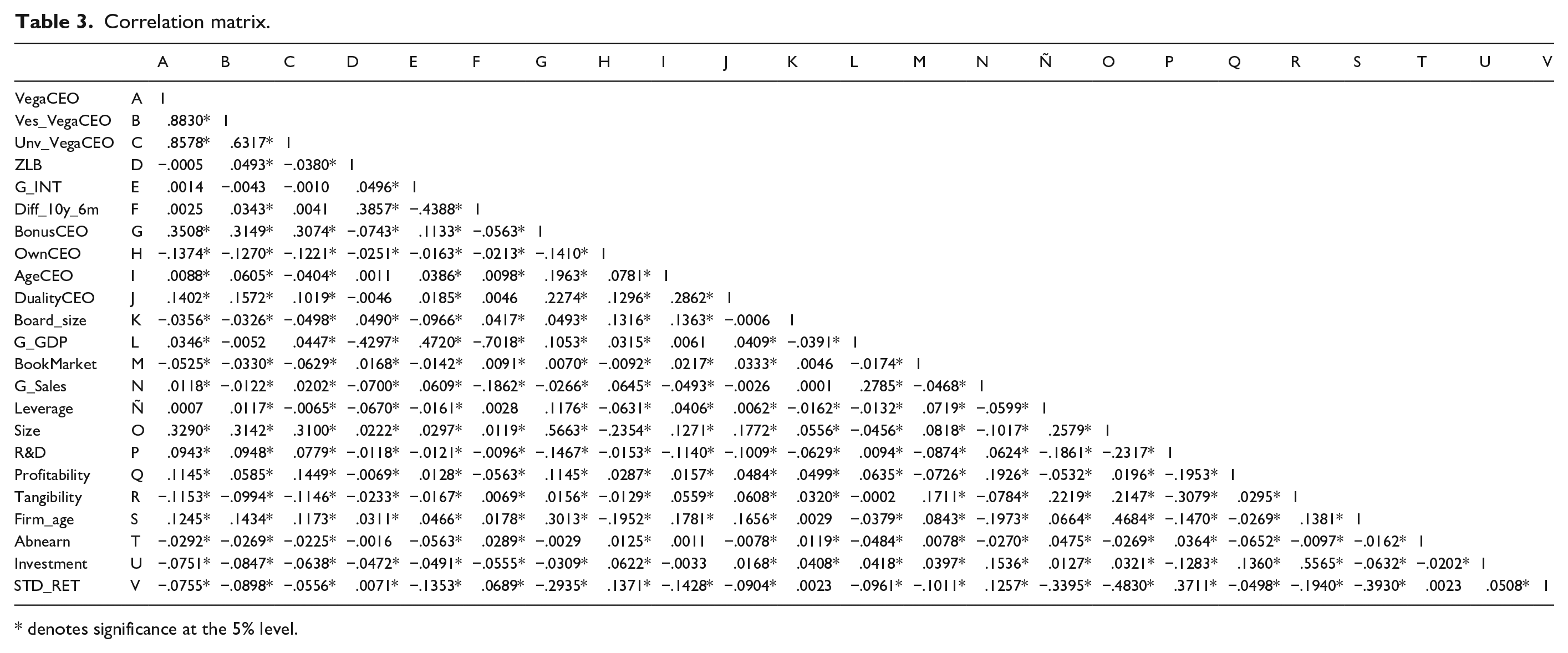

The summary statistics for our control variables, reported in Table 2, are, in general, consistent with those reported in previous literature (Balsam et al., 2018; Billett et al., 2007; Brockman et al., 2010; K. Kim et al., 2017 and Hong, 2019, among others). The correlation matrix for all the explanatory variables, reported in Table 3, indicates that the selected variables are, in general, far from being highly correlated.

Summary statistics of explanatory variables.

This table presents descriptive statistics for the variables used in the debt concentration model. The sample contains 1,293 US firms (9,252 firm-year observations) and covers the 2000–2016 period.

Correlation matrix.

denotes significance at the 5% level.

To reduce the skewness of the distribution of the measures of equity pay incentives, we follow J. B. Kim et al. (2011) and employ the log transformation of Vega (VegaCEO), unvested Vega (Unv_VegaCEO), and vested Vega (Ves_VegaCEO) instead of the raw measures in the empirical tests. The summary statistics of these variables and the other dependent variables used in our models show similar values to those in the previous literature (i.e., Hayes et al. (2012), Serfling (2014), and Andreou et al. (2017), for leverage; Hayes et al. (2012), K. Kim et al. (2017), and Saunders and Song (2018), for Investment; and Hong (2019) for STD_RET).

Empirical results

Impact of interest rates on CEO risk-taking incentives

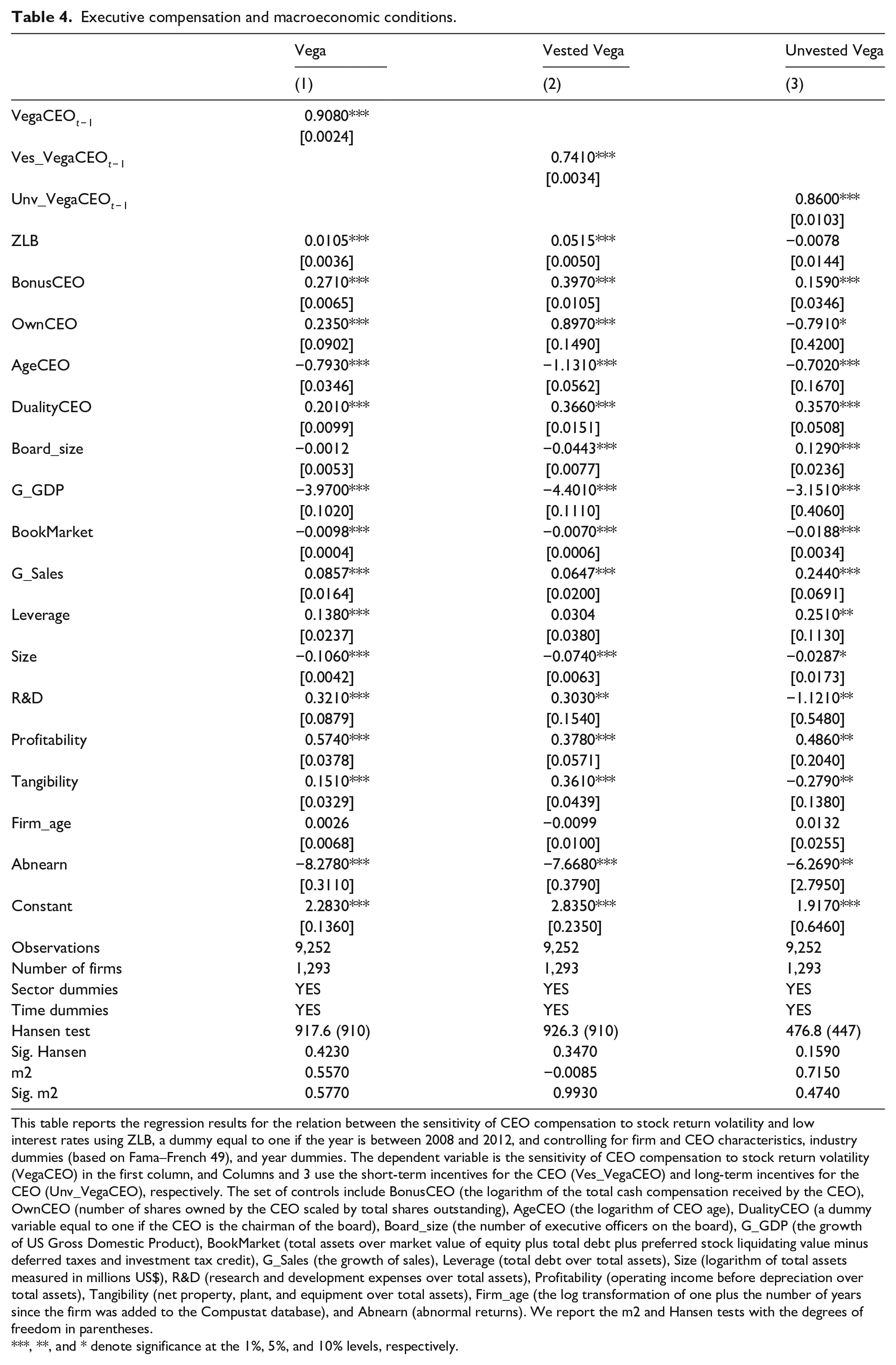

In Table 4, we report the empirical results from the GMM panel data model where the CEO risk-taking incentives are modeled as a function of the low-interest-rate monetary policy. The variable under study is ZLB (interest rates close to zero or lower). ZLB is an extreme low-interest setting in which the lenders’ incentive to soften lending conditions and relaxed monitoring of firms’ credit would be stressed. On the boards and managers part, in the presence of ZLB, they would receive stronger risk-taking incentives to obtain higher business returns, and managers would be more urged to improve personal wealth via incentives.

Executive compensation and macroeconomic conditions.

This table reports the regression results for the relation between the sensitivity of CEO compensation to stock return volatility and low interest rates using ZLB, a dummy equal to one if the year is between 2008 and 2012, and controlling for firm and CEO characteristics, industry dummies (based on Fama–French 49), and year dummies. The dependent variable is the sensitivity of CEO compensation to stock return volatility (VegaCEO) in the first column, and Columns and 3 use the short-term incentives for the CEO (Ves_VegaCEO) and long-term incentives for the CEO (Unv_VegaCEO), respectively. The set of controls include BonusCEO (the logarithm of the total cash compensation received by the CEO), OwnCEO (number of shares owned by the CEO scaled by total shares outstanding), AgeCEO (the logarithm of CEO age), DualityCEO (a dummy variable equal to one if the CEO is the chairman of the board), Board_size (the number of executive officers on the board), G_GDP (the growth of US Gross Domestic Product), BookMarket (total assets over market value of equity plus total debt plus preferred stock liquidating value minus deferred taxes and investment tax credit), G_Sales (the growth of sales), Leverage (total debt over total assets), Size (logarithm of total assets measured in millions US$), R&D (research and development expenses over total assets), Profitability (operating income before depreciation over total assets), Tangibility (net property, plant, and equipment over total assets), Firm_age (the log transformation of one plus the number of years since the firm was added to the Compustat database), and Abnearn (abnormal returns). We report the m2 and Hansen tests with the degrees of freedom in parentheses.

, **, and * denote significance at the 1%, 5%, and 10% levels, respectively.

We find that close-to-zero interest rates increase the risk-taking incentives in the form of a higher sensitivity of CEO pay to stock return volatility (higher values of VegaCEO). The coefficient assigned to our proxy for low interest rates is in line with our first hypothesis. This result supports the view that low interest rates induce the board to adjust the CEO’s risk-taking incentives to obtain higher returns. Furthermore, consistent with the creditor channel in the creditor–shareholder agency conflicts, a relaxation of creditor monitoring would allow an increase in CEOs’ risk-taking incentives. Theoretically, we reason that the effect is expected from both parts of the agency relationship, what would mean an alignment of interests between shareholders and creditors. However, our first model cannot distinguish the origin of the effect. Therefore, this alignment is expected to be confirmed by our subsequent tests. As an extension of Model 1, we report here the three versions applied to obtain the results displayed in Table 4. Note that Xit is a vector gathering all firm, CEO, and macroeconomic control variables

In terms of control variables, Column 1, reporting the general model, shows that the estimated coefficients of BonusCeo, OwnCEO, DualityCEO, G_Sales, Leverage, R&D, Profitability, and Tangibility are positive and statistically significant at customary levels, whereas the coefficients of AgeCEO, Board_size, G_GDP, BookMarket, Size, and Abnearn show a negative and significant effect on the managers’ risk incentives. 9 Our results for AgeCEO are consistent with the homogeneous previous evidence (Serfling, 2014; Shen & Zhang, 2013).

To test our hypothesis H1b, we explore how the horizons of CEO compensation resulting from pay incentive contracts are associated with monetary policy. Our baseline model is extended by decomposing the dependent variable into vested and unvested Vega, as explained in section “Data overview and variable measurement.” We find a positive and significant coefficient for the influence of low interest rates (ZLB) on vested Vega (Column 2). In contrast, the results for unvested Vega (Unv_VegaCEO) are not significant at customary levels. Overall, in line with hypothesis H1b, we find that when the horizon of the pay incentives is short (vested Vega), the low-interest monetary policies produce a significant effect as risk-taking determinants, implying that the significant effects of monetary policy on VegaCEO reported in Column 1 are driven by horizons. This finding is consistent with the fact that the risk-taking channel of creditors is especially present under low short-term interest rates, hence the creditor channel in the creditor–shareholder agency conflict would mean a relaxation of monitoring of short-term horizon incentives.

The impact of executive compensation on the effect of monetary policies on corporate risk policies

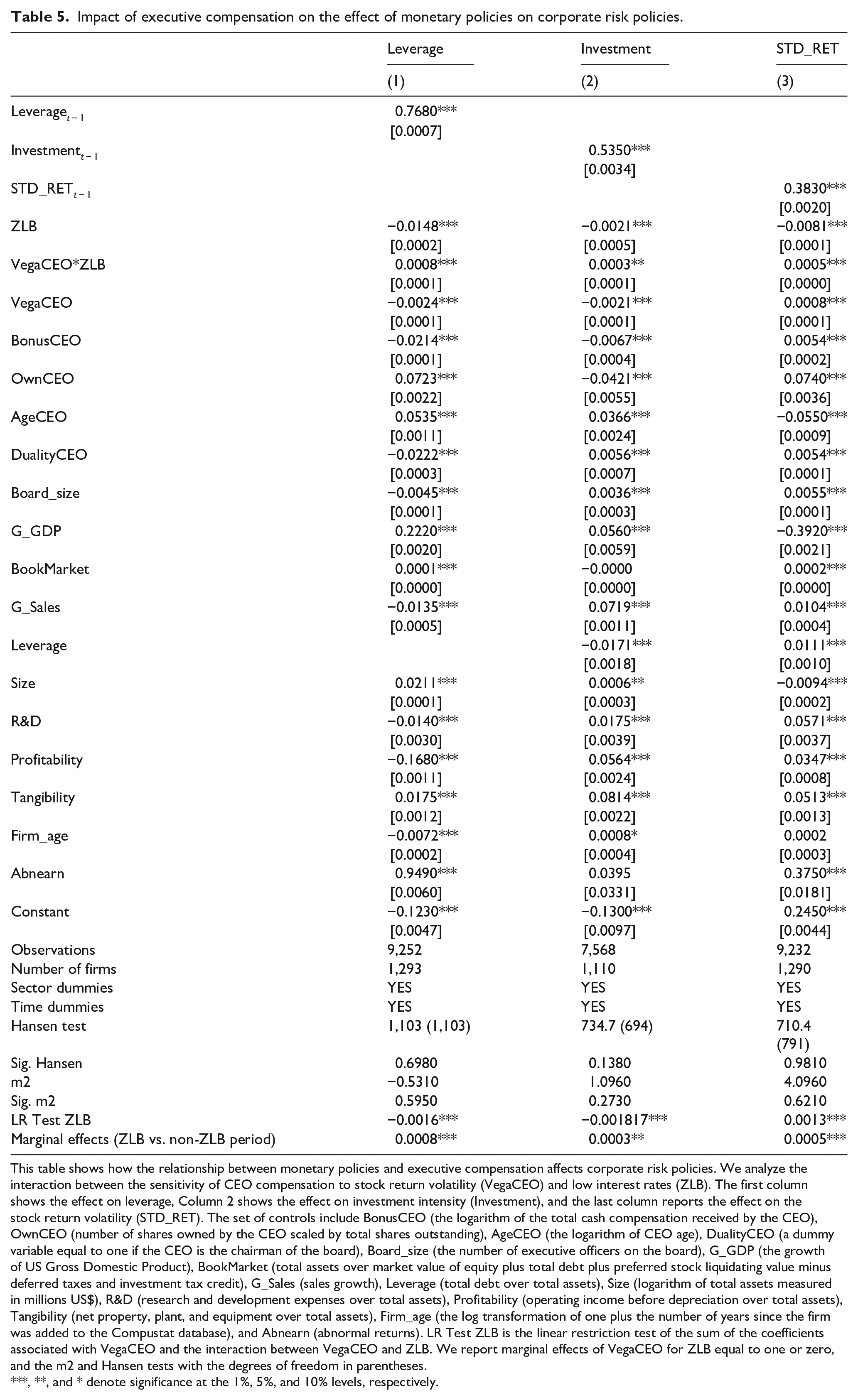

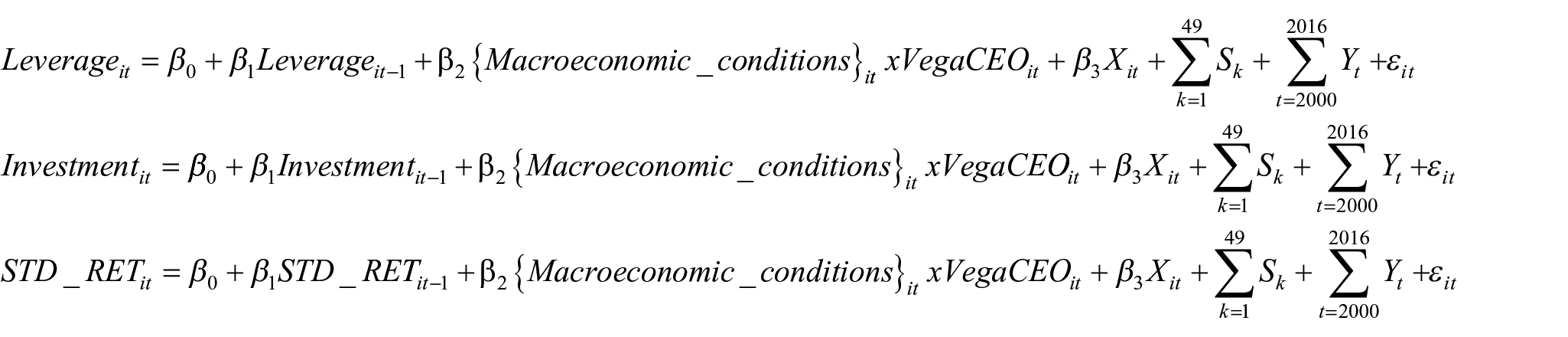

To capture the specific effect of the managers’ risk-taking incentives on the financing and investing policies of the firms and on the global risk of the firm in the presence of low interest rates, we modeled the interaction of our monetary policy proxy with VegaCEO. We report the three specifications of Model 2 used to obtain the results displayed in Table 5. Leverage, investment, and stock return standard deviation are the proxies for corporate risk policies (CRP), and Xit is a vector gathering all firm, CEO, and macroeconomic control variables

Impact of executive compensation on the effect of monetary policies on corporate risk policies.

This table shows how the relationship between monetary policies and executive compensation affects corporate risk policies. We analyze the interaction between the sensitivity of CEO compensation to stock return volatility (VegaCEO) and low interest rates (ZLB). The first column shows the effect on leverage, Column 2 shows the effect on investment intensity (Investment), and the last column reports the effect on the stock return volatility (STD_RET). The set of controls include BonusCEO (the logarithm of the total cash compensation received by the CEO), OwnCEO (number of shares owned by the CEO scaled by total shares outstanding), AgeCEO (the logarithm of CEO age), DualityCEO (a dummy variable equal to one if the CEO is the chairman of the board), Board_size (the number of executive officers on the board), G_GDP (the growth of US Gross Domestic Product), BookMarket (total assets over market value of equity plus total debt plus preferred stock liquidating value minus deferred taxes and investment tax credit), G_Sales (sales growth), Leverage (total debt over total assets), Size (logarithm of total assets measured in millions US$), R&D (research and development expenses over total assets), Profitability (operating income before depreciation over total assets), Tangibility (net property, plant, and equipment over total assets), Firm_age (the log transformation of one plus the number of years since the firm was added to the Compustat database), and Abnearn (abnormal returns). LR Test ZLB is the linear restriction test of the sum of the coefficients associated with VegaCEO and the interaction between VegaCEO and ZLB. We report marginal effects of VegaCEO for ZLB equal to one or zero, and the m2 and Hansen tests with the degrees of freedom in parentheses.

, **, and * denote significance at the 1%, 5%, and 10% levels, respectively.

Table 5 shows the positive and significant coefficients obtained for the VegaCEO*ZLB interaction explaining leverage (Column 1), investment (Column 2), and market return volatility (Column 3). Therefore, the effect of CEO risk-taking incentives on corporate risk policies when interest rates are close to zero (ZLB = 1) are significantly different from the effect when they are not (ZLB = 0). Thus, the negative effect of VegaCEO on leverage (Column 1) and investment (Column 2) is mitigated in a ZLB scenario, as captured by the positive estimated coefficient for the VegaCEO*ZLB interaction term. As for stock return volatility (Column 3), the positive effect of VegaCEO on STD_RET is intensified in a ZLB scenario, as the positive coefficient of VegaCEO*ZLB indicates. Following Cantero-Sáiz et al. (2017), we carry out linear restriction tests of the sum of the coefficients associated with VegaCEO and the coefficients associated with the interaction between VegaCEO and ZLB (reported in Table 5 by LR_Test_ZLB). The tests confirm these significant effects in all cases. In Columns 1 and 2, the LR_Test_ZLB coefficients mitigate the negative effect of VegaCEO on leverage and investment being less negative, and in Column 3, the LR_Test_ZLB coefficient emphasizes the positive effect of VegaCEO on stock return volatility. Following Berger and Bouwman (2013), we computed the coefficient of the marginal effects of the difference in the effect of stock return volatility (Vega) between ZLB and non-ZLB periods. These magnitudes of marginal effects explain how the observed variable (leverage, investment or STD_RET) changes with respect to variations in managerial risk-taking incentives (VegaCEO) for ZLB versus non-ZLB periods. As reported at the end of Table 5, we find that the magnitudes of the marginal effects of Vega are positive and significantly different between ZLB and non-ZLB periods for the three proxies of the corporate risk policies.

Our results are consistent with the alignment of interests between shareholders and managers due to close-to-zero interest rates because part of the riskier financing and investing policies of the firm and their overall risk is related to risk-taking incentives. VegaCEO measures the effect of managers’ risk-taking incentives on the firms’ financing and investing policies when the interest rates are different from zero (ZLB = 0), as there are negative coefficients for leverage and investment and a positive coefficient for stock return standard deviation. This finding implies that the CEO’s risk-taking incentives result in riskier leverage and investment policies only in the presence of low interest rates, in line with the creditors’ “search for yield” that induces the risk-taking channel of creditors and softer lending standards (creditor channel). Therefore, those results support the alignment of the creditors’ interests with those of the managers and the shareholders.

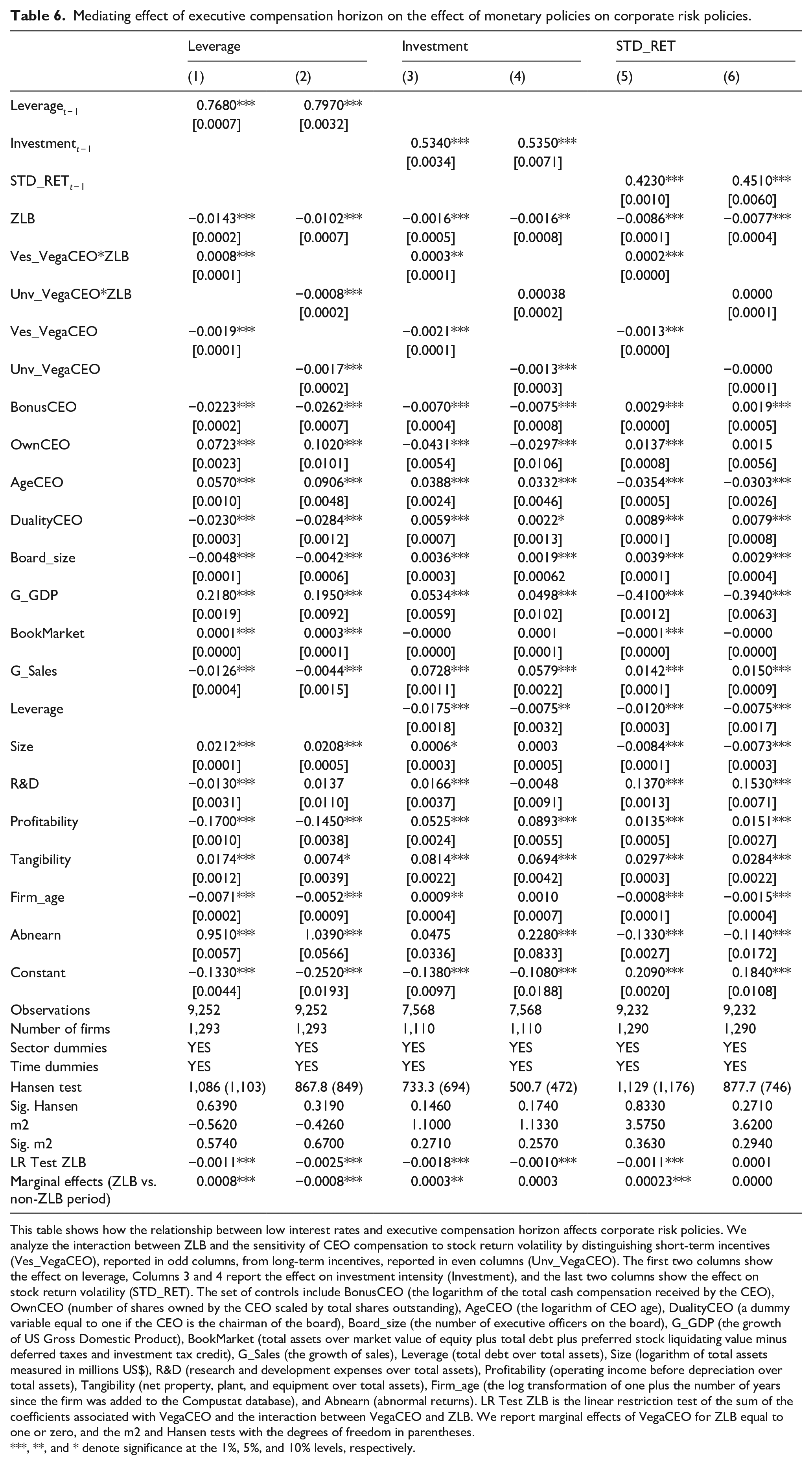

In Table 6, we incorporated the horizon of executive compensation. In Columns 1 and 2, relative to leverage as the explained factor, it can be observed that the interaction of vested Vega with ZLB has a significant positive coefficient, whereas the interaction of unvested Vega with ZLB shows a significant negative coefficient. In Columns 3 and 4, relative to investment as the explained variable, only the effect of vested Vega is significant. These results indicate that the positive effect of CEO compensation on the firm’s financing and investing policies in the presence of low interest rates is addressed by the compensation horizon, and the short-term horizon is the horizon of interest. In Columns 5 and 6, the same pattern is observed to explain the market return volatility as a proxy for the global risk of the firm. Only the interaction between vested Vega and ZLB has a significant positive coefficient, indicating the relevant role of compensation horizons for risk-taking behavior induced by compensation incentives in low-interest settings. The increase in leverage and the other riskier corporate policies is induced only by vested Vega in the presence of ZLB policies, which is again consistent with an active role of creditors in controlling managerial risk-taking except in the scenario under study with interest rates close to zero and a short-term horizon. Thus, the results suggest an alignment of interests with managers and shareholders to chase higher returns at the expense of higher risk.

Mediating effect of executive compensation horizon on the effect of monetary policies on corporate risk policies.

This table shows how the relationship between low interest rates and executive compensation horizon affects corporate risk policies. We analyze the interaction between ZLB and the sensitivity of CEO compensation to stock return volatility by distinguishing short-term incentives (Ves_VegaCEO), reported in odd columns, from long-term incentives, reported in even columns (Unv_VegaCEO). The first two columns show the effect on leverage, Columns 3 and 4 report the effect on investment intensity (Investment), and the last two columns show the effect on stock return volatility (STD_RET). The set of controls include BonusCEO (the logarithm of the total cash compensation received by the CEO), OwnCEO (number of shares owned by the CEO scaled by total shares outstanding), AgeCEO (the logarithm of CEO age), DualityCEO (a dummy variable equal to one if the CEO is the chairman of the board), Board_size (the number of executive officers on the board), G_GDP (the growth of US Gross Domestic Product), BookMarket (total assets over market value of equity plus total debt plus preferred stock liquidating value minus deferred taxes and investment tax credit), G_Sales (the growth of sales), Leverage (total debt over total assets), Size (logarithm of total assets measured in millions US$), R&D (research and development expenses over total assets), Profitability (operating income before depreciation over total assets), Tangibility (net property, plant, and equipment over total assets), Firm_age (the log transformation of one plus the number of years since the firm was added to the Compustat database), and Abnearn (abnormal returns). LR Test ZLB is the linear restriction test of the sum of the coefficients associated with VegaCEO and the interaction between VegaCEO and ZLB. We report marginal effects of VegaCEO for ZLB equal to one or zero, and the m2 and Hansen tests with the degrees of freedom in parentheses.

, **, and * denote significance at the 1%, 5%, and 10% levels, respectively.

As in the previous table, we perform the linear restriction test LR_Test_ZLB and find significant coefficients with the same sign as vested and unvested Vega. These results support the different influences of vested versus unvested Vega on the analyzed corporate policies when interest rates are near zero, confirming that the previous results obtained for Vega (reported in Table 5) are driven by vested Vega.

We also compute the marginal effects of the ZLB and non-ZLB periods for the three proxies of corporate risk policies for both vested and unvested Vega. The coefficient of the marginal effect for vested Vega is significant and positive in all cases (Columns 1, 3, and 5), supporting the results, and the coefficient for unvested Vega is negative (Column 2) or nonsignificant (Columns 4 and 6).

Robustness tests

Alternative measures of low-interest-rate monetary policies

To check the robustness of our results, we use alternative measures of the low-interest-rate monetary policy. First, we use the growth of interest rates, proxied by the growth of the bank prime loan rate, and then the uncertainty in the interest rate market, proxied by the difference between long-term and short-term interest rates. As the second monetary proxy is defined in terms of growth, the expected sign is opposite to that of ZLB, with negative or lower growth of interest rates producing greater CEO risk-taking incentives.

Our third monetary proxy is the difference between two interest rates with different time horizons, which is a powerful indicator of monetary market stability. During periods of stability, long-term interest rates are higher than short-term ones. However, during unstable periods, short-term interest rates increase quickly while long-term interest rates remain more stable, resulting in a smaller difference between them. Overall, a greater difference between the 10-year interest rate and the 6-month interest rate indicates better stability in the monetary market. However, a smaller difference between the two interest rates indicates greater instability in the market since the short-term interest rates may dramatically increase. In Columns 1 and 2 of Table 7, we can see that the significant coefficients support the previous results, meaning a significant increase in risk-taking incentives, measured as the sensitivity of CEO pay to stock return volatility (higher values of Vega) in low-interest-rate settings. As expected, the negative and significant coefficient for the growth of interest rates and the positive and significant coefficient of the difference between long-term and short-term rates support the results obtained with the ZLB.

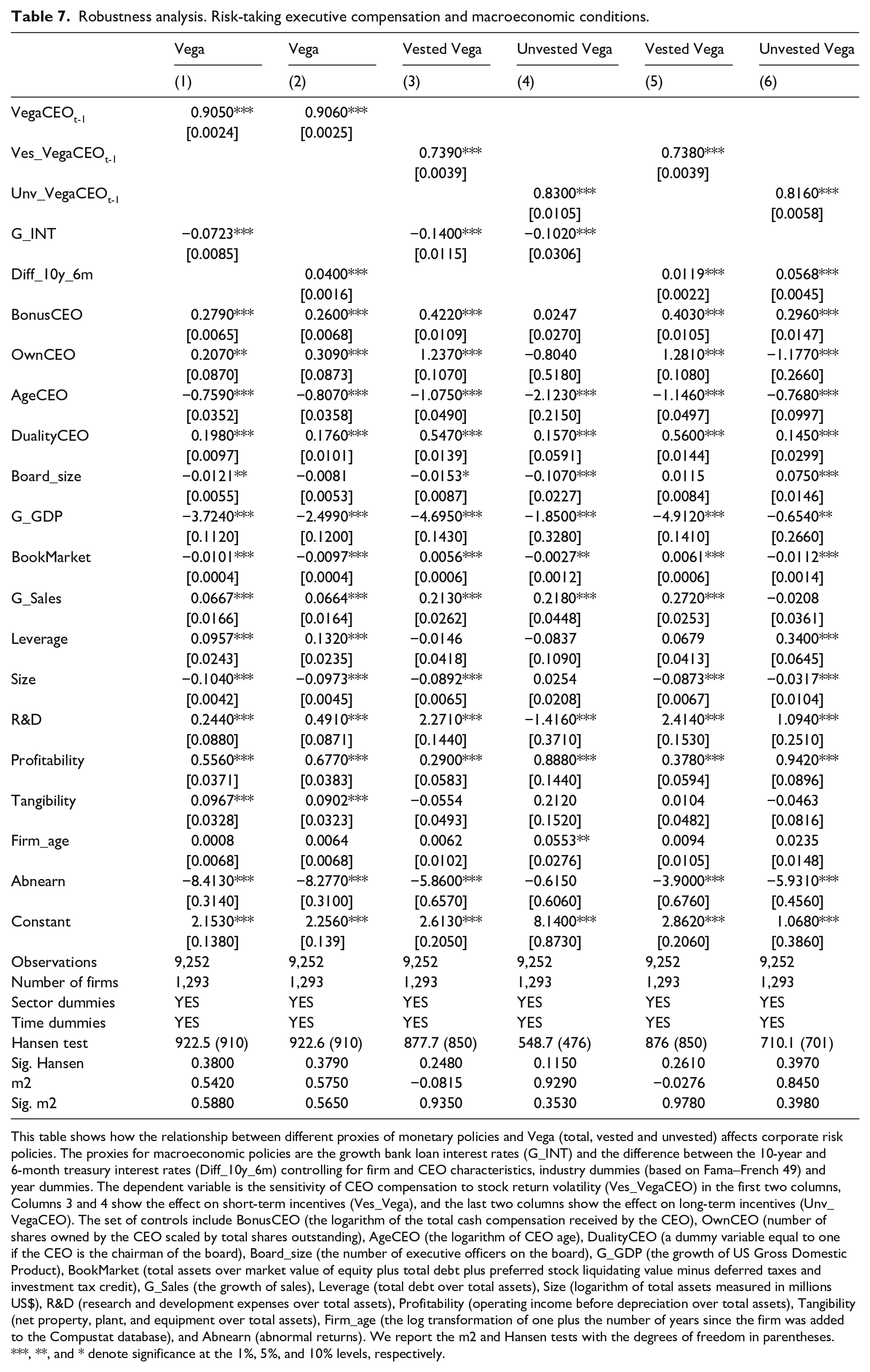

Robustness analysis. Risk-taking executive compensation and macroeconomic conditions.

This table shows how the relationship between different proxies of monetary policies and Vega (total, vested and unvested) affects corporate risk policies. The proxies for macroeconomic policies are the growth bank loan interest rates (G_INT) and the difference between the 10-year and 6-month treasury interest rates (Diff_10y_6m) controlling for firm and CEO characteristics, industry dummies (based on Fama–French 49) and year dummies. The dependent variable is the sensitivity of CEO compensation to stock return volatility (Ves_VegaCEO) in the first two columns, Columns 3 and 4 show the effect on short-term incentives (Ves_Vega), and the last two columns show the effect on long-term incentives (Unv_VegaCEO). The set of controls include BonusCEO (the logarithm of the total cash compensation received by the CEO), OwnCEO (number of shares owned by the CEO scaled by total shares outstanding), AgeCEO (the logarithm of CEO age), DualityCEO (a dummy variable equal to one if the CEO is the chairman of the board), Board_size (the number of executive officers on the board), G_GDP (the growth of US Gross Domestic Product), BookMarket (total assets over market value of equity plus total debt plus preferred stock liquidating value minus deferred taxes and investment tax credit), G_Sales (the growth of sales), Leverage (total debt over total assets), Size (logarithm of total assets measured in millions US$), R&D (research and development expenses over total assets), Profitability (operating income before depreciation over total assets), Tangibility (net property, plant, and equipment over total assets), Firm_age (the log transformation of one plus the number of years since the firm was added to the Compustat database), and Abnearn (abnormal returns). We report the m2 and Hansen tests with the degrees of freedom in parentheses.

, **, and * denote significance at the 1%, 5%, and 10% levels, respectively.

In addition, we find significant coefficients for vested Vega (Ves_VegaCEO) explained by the growth of interest rates (with the expected negative sign) and by the difference between the 10-year and 6-month interest rates (with the expected positive sign) in Columns 3 and 5, respectively. Similar results are found for unvested Vega, but in the case of the third monetary proxy, the significant, positive effect is even stronger, as shown in Column 6. This result is consistent with the psychological salience effect (Lian et al., 2019) of wider differences between long-term and short-term interest rates inducing the horizon of risk-taking incentives. Therefore, during periods of monetary market stability, marked differences in long-term interest rates over short-term interest rates would induce shareholders to extend the compensation horizon to induce the managers’ risk-taking to those more profitable horizons.

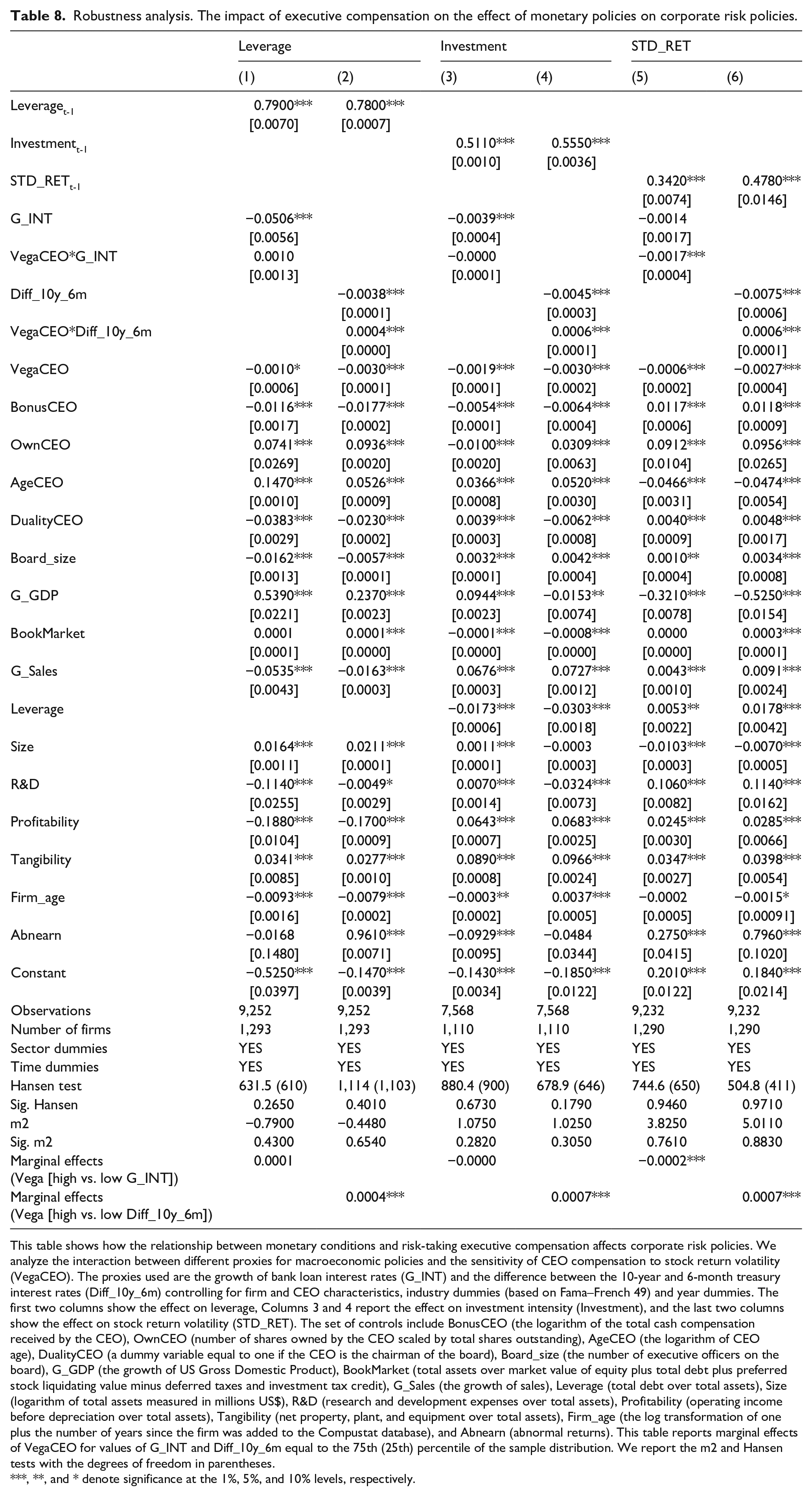

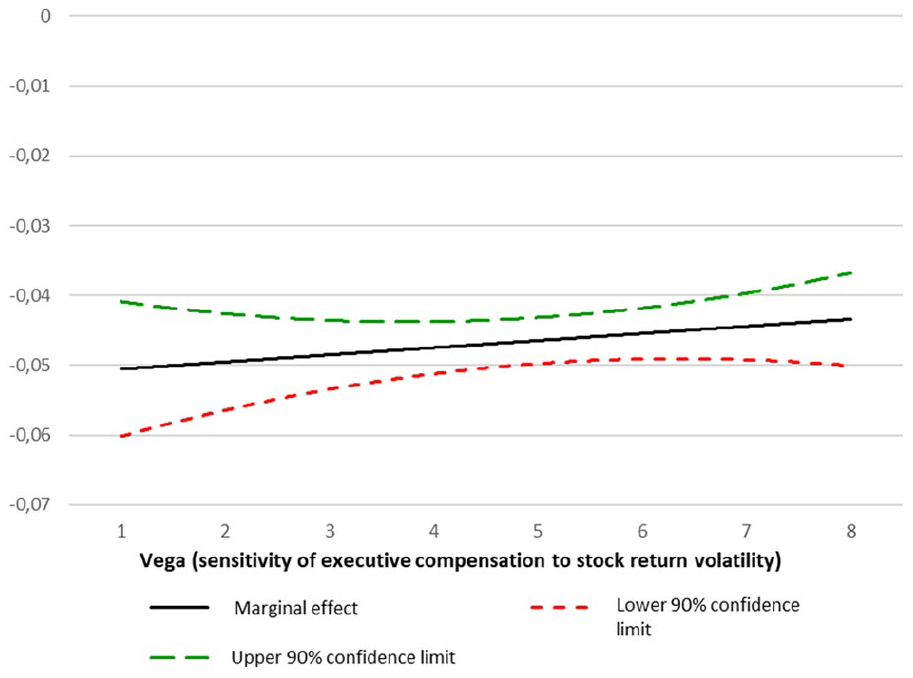

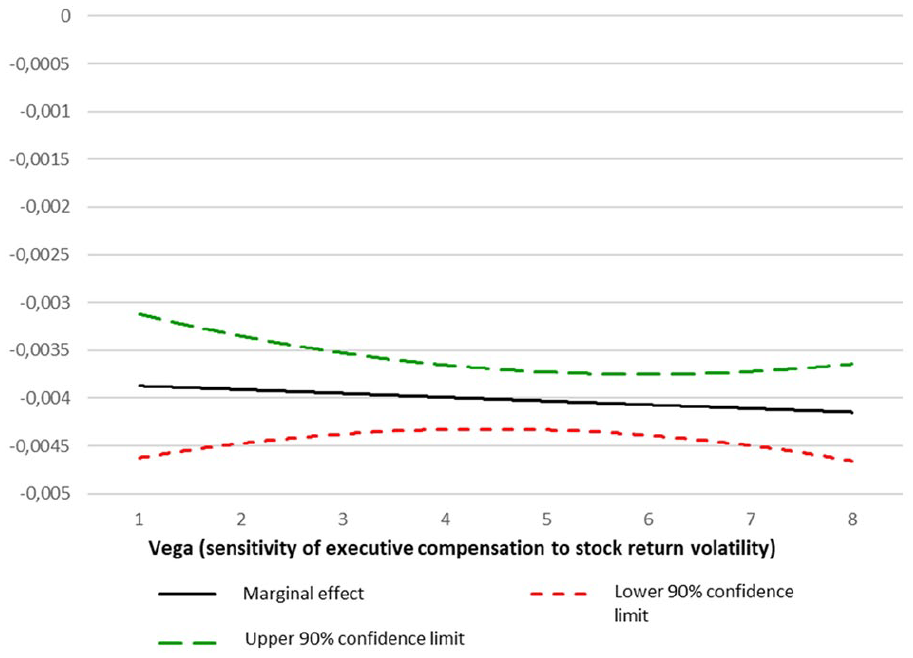

In Table 8, the impact of Vega is tested on the effect of the alternative monetary proxies on corporate risk policies. When the growth of interest rates is used as the second proxy for the monetary policy, we observe that the monetary policy alone is a stronger factor than the interaction with VegaCEO to affect financing (Column 1) and investing (Column 3) policies. Lower interest rates would induce increases in leverage and capital expenditures, which is consistent with riskier financing and investing policies. Notwithstanding, for the aggregate business risk, proxied by market return volatility (Column 5), the interaction shows the expected negative coefficient to indicate that lower interest rates provide CEOs with risk-taking incentives to adopt riskier policies. For the third monetary proxy (Columns 2, 4, and 6), the coefficients obtained for the interaction with VegaCEO are similar to those obtained for the interaction with ZLB, indicating that with higher differences between long-term and short-term interest rates, managers with risk-taking incentives tend to adopt riskier financing and investing policies resulting in higher global risk. However, VegaCEO is a continuous variable and can have infinite values. Therefore, to overcome this limitation, we follow Cantero-Sáiz et al. (2018) to analyze how the marginal effect of VegaCEO on the different dependent variables varies with the macroeconomic policies. Figures 1 to 6 report the marginal effects of macroeconomic policies on the level of leverage (Figures 1 and 4), investment (Figures 2 and 5), and stock return volatility (Figures 3 and 6) when there is an increase in the growth of bank loan interest rates (Figures 1 to 3) and in the difference between the 10 year and 6 month treasury interest rates and (Figures 4 to 6). We can determine the conditions under which the macroeconomic policies have a statistically significant effect on corporate risk policies using the 90% confidence interval (dotted lines). Supporting the results in Table 8, Figures 4 to 6 show how an increase in the difference between the 10-year and the 6-month treasury interest rates leads to an increase in the financing and investing policies when managers have risk-taking incentives. However, Figures 1 and 2 show a less clear trend due to the nonsignificant coefficients found for the interactions. Finally, Figure 3 indicates how an increase in the bank loan interest rate leads to a decrease in stock return volatility when managers have risk-taking incentives supported by the negative and significant interaction reported in Column 5 of Table 8. We compute the marginal effects of VegaCEO on the different dependent variables with the magnitudes of the three proxies for monetary policies. Specifically, we compute the difference in the marginal effect of managers’ risk-taking incentives (VegaCEO) computed for low (proxy equal to the 25th percentile of the sample distribution) and high growth of bank loan interest rates and the difference between the 10-year and the 6-month treasury interest rates (proxy equal to the 75th percentile of the sample distribution). The results shown in Table 8 support the coefficients of the interactions terms.

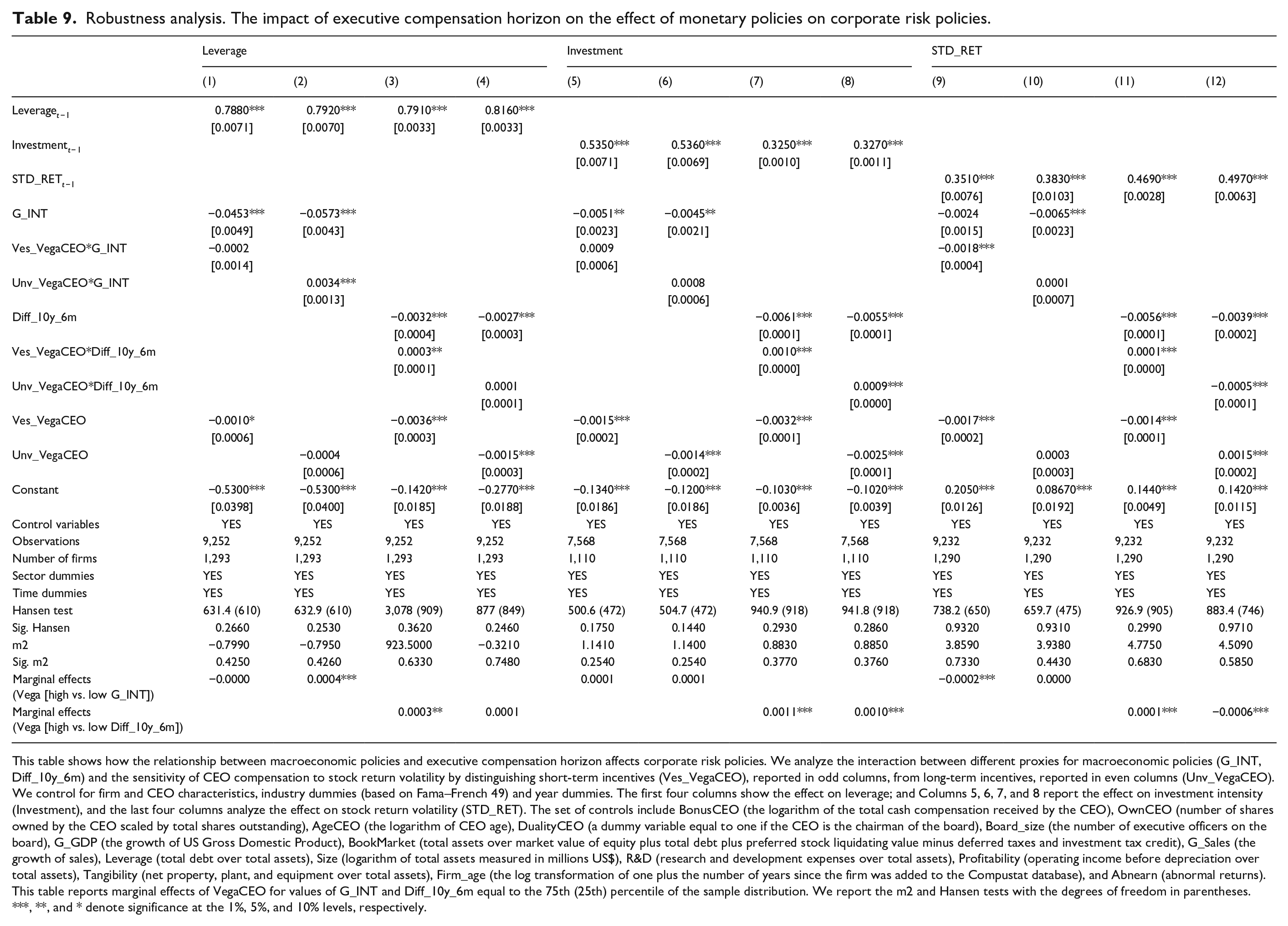

Robustness analysis. The impact of executive compensation on the effect of monetary policies on corporate risk policies.

This table shows how the relationship between monetary conditions and risk-taking executive compensation affects corporate risk policies. We analyze the interaction between different proxies for macroeconomic policies and the sensitivity of CEO compensation to stock return volatility (VegaCEO). The proxies used are the growth of bank loan interest rates (G_INT) and the difference between the 10-year and 6-month treasury interest rates (Diff_10y_6m) controlling for firm and CEO characteristics, industry dummies (based on Fama–French 49) and year dummies. The first two columns show the effect on leverage, Columns 3 and 4 report the effect on investment intensity (Investment), and the last two columns show the effect on stock return volatility (STD_RET). The set of controls include BonusCEO (the logarithm of the total cash compensation received by the CEO), OwnCEO (number of shares owned by the CEO scaled by total shares outstanding), AgeCEO (the logarithm of CEO age), DualityCEO (a dummy variable equal to one if the CEO is the chairman of the board), Board_size (the number of executive officers on the board), G_GDP (the growth of US Gross Domestic Product), BookMarket (total assets over market value of equity plus total debt plus preferred stock liquidating value minus deferred taxes and investment tax credit), G_Sales (the growth of sales), Leverage (total debt over total assets), Size (logarithm of total assets measured in millions US$), R&D (research and development expenses over total assets), Profitability (operating income before depreciation over total assets), Tangibility (net property, plant, and equipment over total assets), Firm_age (the log transformation of one plus the number of years since the firm was added to the Compustat database), and Abnearn (abnormal returns). This table reports marginal effects of VegaCEO for values of G_INT and Diff_10y_6m equal to the 75th (25th) percentile of the sample distribution. We report the m2 and Hansen tests with the degrees of freedom in parentheses.

, **, and * denote significance at the 1%, 5%, and 10% levels, respectively.

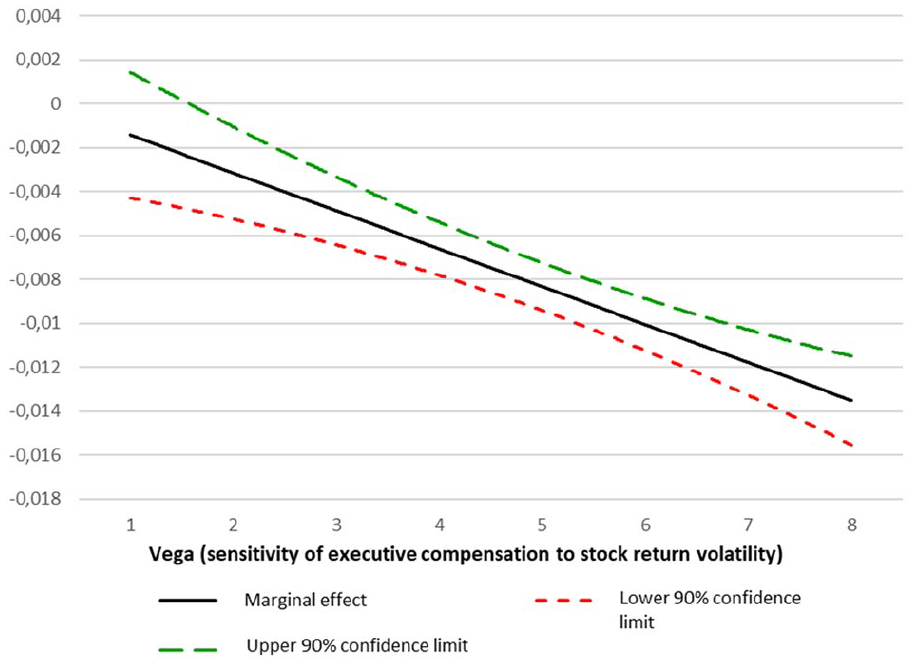

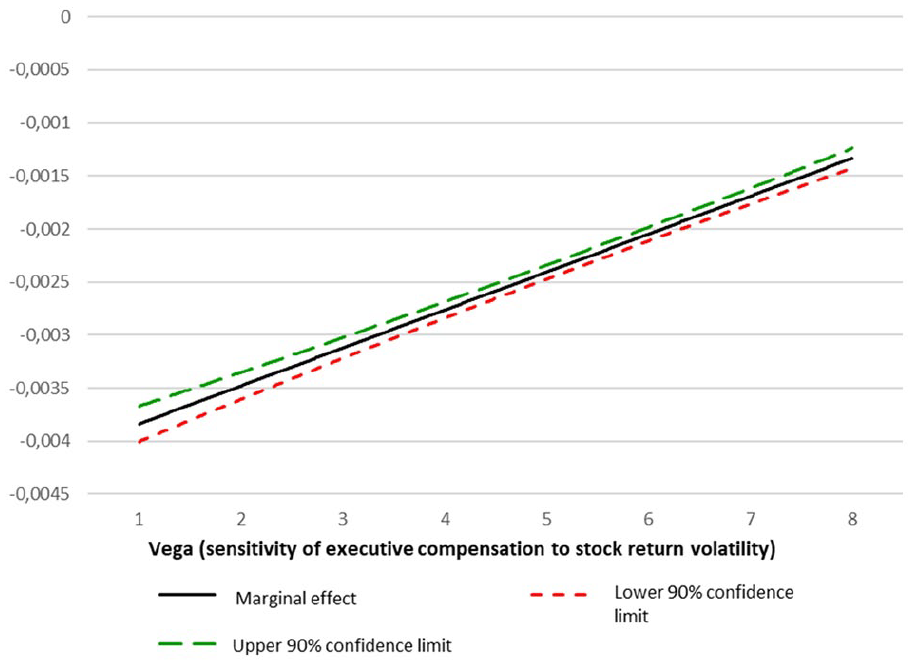

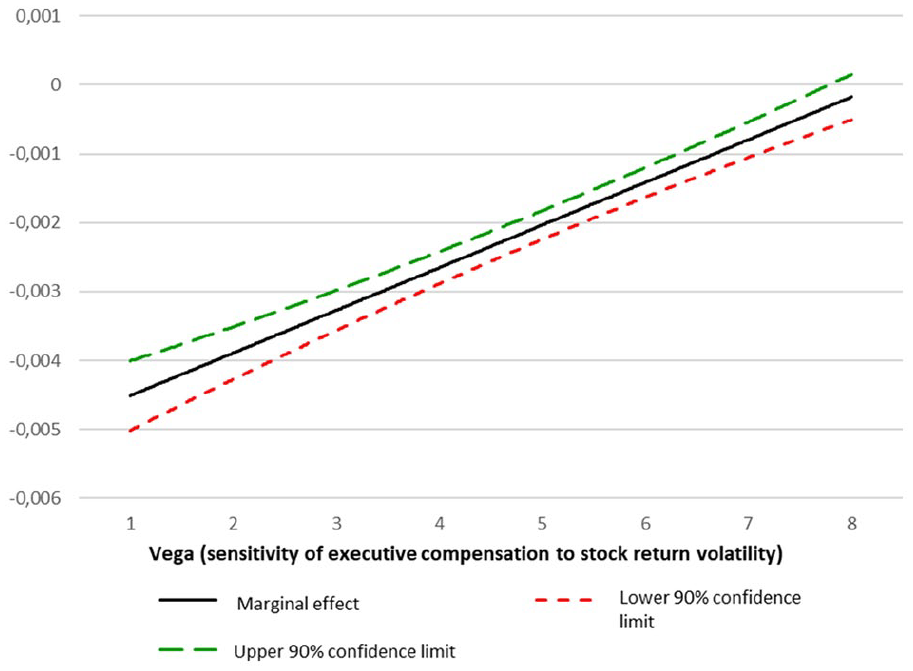

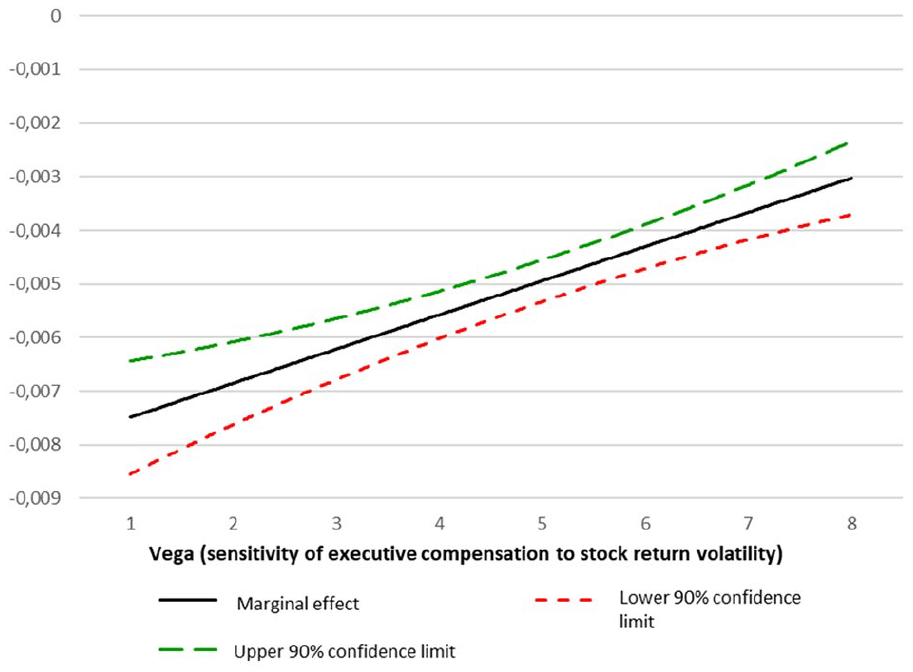

Marginal effect of macroeconomic policies on Leverage in relation to Vega when the growth of interest rates increases.

Marginal effect of macroeconomic policies on Investment in relation to Vega when the growth of interest rates increases.

Marginal effect of macroeconomic policies on stock return volatility in relation to Vega when the growth of interest rates increases.

Marginal effect of macroeconomic policies on Leverage in relation to Vega when the difference between the 10-year and the 6-month treasury interest rates increases.

Marginal effect of macroeconomic policies on Investment in relation to Vega when the difference between the 10-year and the 6-month treasury interest rates increases.

Marginal effect of macroeconomic policies on stock return volatility in relation to Vega when the difference between the 10-year and the 6-month treasury interest rates increases.

Table 9 shows the results obtained when the disaggregation into vested and unvested Vega is used. The second monetary proxy, growth of interest rates, shows clearly different behavior when interacted with vested Vega and unvested Vega to explain leverage. The expected negative coefficient is not significant for vested Vega, but an opposite significant coefficient is found for unvested Vega. However, the interactions are not significant to influence the investment policies. As previously explained, when the growth of interest rates is used, the monetary policy itself seems to be a better determinant of the increase in leverage and investment than the interaction with VegaCEO. In Columns 3 and 4, 7 and 8, and 11 and 12, the results for the third monetary proxy are shown. Again, we can appreciate that when the difference between long-term and short-term interest rates is used, the results are more similar to those obtained with ZLB, supporting the adoption of riskier financing and investing policies by managers with short-term risk-taking incentives. Concerning the aggregate risk of the firm, proxied by market return volatility (Columns 9 to 12), our results with the second monetary proxy (growth of interest rates) and with the third monetary proxy (difference between long-term and short-term interest rates) obtain the expected negative sign and positive sign, respectively, and support the results obtained with ZLB, confirming that the short-term horizon of incentives is a factor in addressing the effect induced by the interactions. By contrast, with higher differences between long-term and short-term interest rates, the long-term compensation incentives are related to a reduction in the firm’s risk. As in Table 8, we compute the marginal effects of vested and unvested Vega on the different dependent variables with different magnitudes of the proxies for monetary policies. Specifically, we report the difference in the marginal effect of managers’ risk-taking incentives computed for low (proxy equal to the 25th percentile of the sample distribution) and high growth of bank loan interest rates and the difference between the 10-year and 6-month treasury interest rates (proxy equal to the 75th percentile of the sample distribution). In this case, we distinguish the short-term incentives (vested VegaCEO) from the long-term incentives (unvested VegaCEO). The results reported in Table 9 support the coefficients found for the interaction terms. 10

Robustness analysis. The impact of executive compensation horizon on the effect of monetary policies on corporate risk policies.

This table shows how the relationship between macroeconomic policies and executive compensation horizon affects corporate risk policies. We analyze the interaction between different proxies for macroeconomic policies (G_INT, Diff_10y_6m) and the sensitivity of CEO compensation to stock return volatility by distinguishing short-term incentives (Ves_VegaCEO), reported in odd columns, from long-term incentives, reported in even columns (Unv_VegaCEO). We control for firm and CEO characteristics, industry dummies (based on Fama–French 49) and year dummies. The first four columns show the effect on leverage; and Columns 5, 6, 7, and 8 report the effect on investment intensity (Investment), and the last four columns analyze the effect on stock return volatility (STD_RET). The set of controls include BonusCEO (the logarithm of the total cash compensation received by the CEO), OwnCEO (number of shares owned by the CEO scaled by total shares outstanding), AgeCEO (the logarithm of CEO age), DualityCEO (a dummy variable equal to one if the CEO is the chairman of the board), Board_size (the number of executive officers on the board), G_GDP (the growth of US Gross Domestic Product), BookMarket (total assets over market value of equity plus total debt plus preferred stock liquidating value minus deferred taxes and investment tax credit), G_Sales (the growth of sales), Leverage (total debt over total assets), Size (logarithm of total assets measured in millions US$), R&D (research and development expenses over total assets), Profitability (operating income before depreciation over total assets), Tangibility (net property, plant, and equipment over total assets), Firm_age (the log transformation of one plus the number of years since the firm was added to the Compustat database), and Abnearn (abnormal returns). This table reports marginal effects of VegaCEO for values of G_INT and Diff_10y_6m equal to the 75th (25th) percentile of the sample distribution. We report the m2 and Hansen tests with the degrees of freedom in parentheses.

, **, and * denote significance at the 1%, 5%, and 10% levels, respectively.

Institutional investors and risk-taking incentives

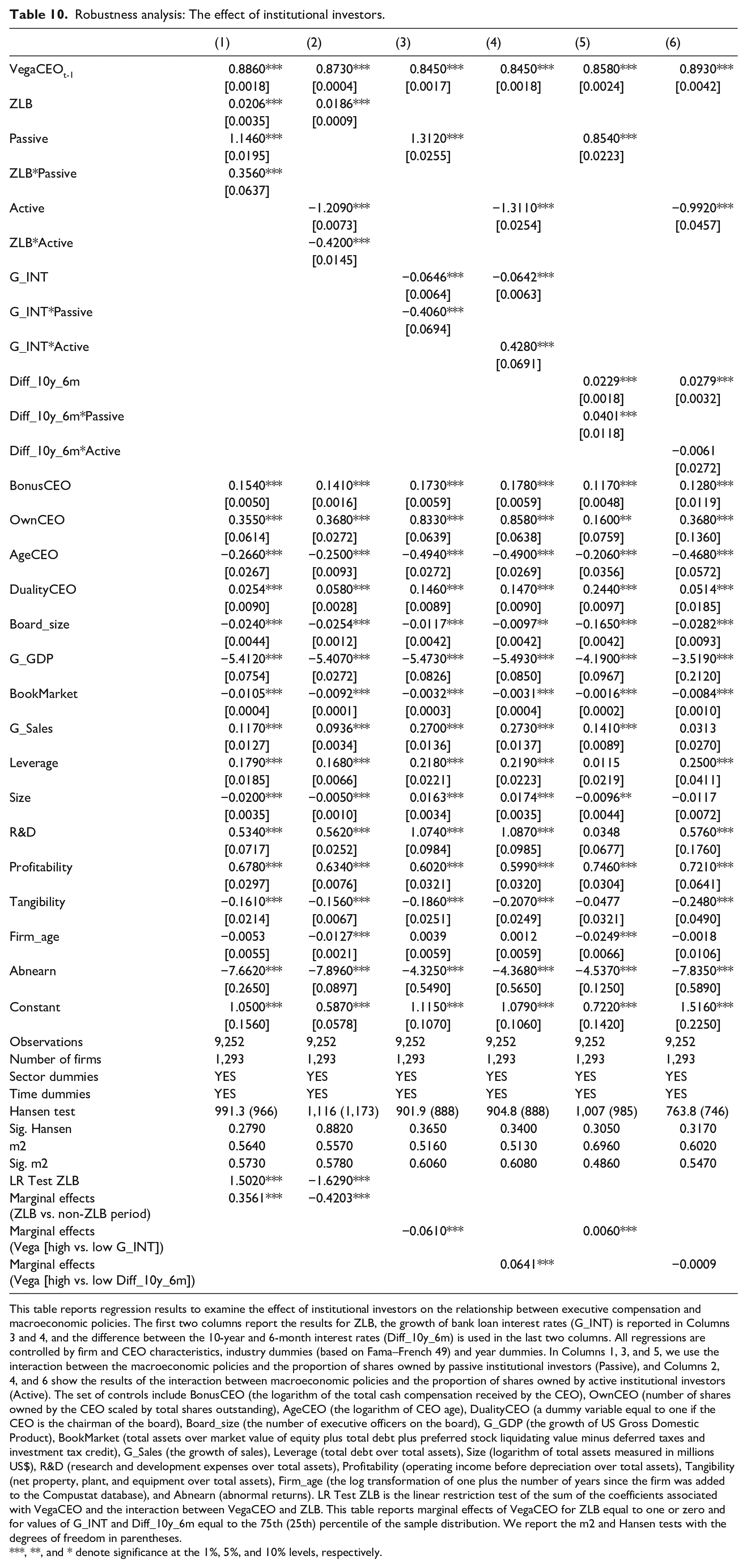

To ensure the robustness of our results, we conduct additional tests to study the effect of the presence of intuitional investors. Specifically, we analyze whether the effects of low-interest-rate monetary policies on CEO risk-taking incentives vary depending on the institutional investor category (passive vs. active). We are especially interested in passive investors as banks take part in this group. In this way, we can assess how low interest rates affect their monitoring role as investors.

Aggregate institutional ownership (banks, investment companies, insurance companies, investment advisors, etc.) has significantly grown in recent decades, and these groups have been identified as distinctive and better monitors because they have an information advantage (Grinstein & Michaely, 2005). Regarding the influence of institutional ownership on managers’ risk-taking, Hartzell and Starks (2003) find a positive relationship between the institutional ownership concentration and the pay performance sensitivity of managerial incentives, and a negative relationship with the level of executive compensation. Concerning the influence of institutional investors on the risk-taking behavior of the managers, Chan et al. (2013) show a positive relationship between the number of banks and earnings volatility, as well as the deviation in monthly equity returns.

Institutional investors do not form a homogeneous group (Webb et al., 2003). Pressure-insensitive, foreign and large institutional shareholders have a stronger positive relationship with firm performance than pressure-sensitive, domestic, and small institutional investors (Lin & Fu, 2017). Some studies suggest two different institutional investor views, depending on their category. Almazan et al. (2005) classify them into active monitoring and passive monitoring. Investment companies and advisors are potentially active monitors. Meanwhile, shareholders, banks, insurance companies, and others would potentially act as passive monitors.

Passive monitors might not intervene in management decisions as they are not interested in improving corporate governance and firm performance (Lin & Fu, 2017). According to Elyasiani and Jia (2010), these institutional shareholders may be short-term investors since they act as traders without participating in the corporate governance. Therefore, a positive relationship should be expected between passive monitoring and CEO risk-taking incentives since they have aligned their interests in search of short-term performance.

However, active monitors can reduce information asymmetries and agency problems between managers and shareholders. Furthermore, they may try to maximize shareholder value by improving corporate governance policies. Lin and Fu (2017) explain that if institutional investors act as active monitors, they can influence business decisions. Active monitors could boost the firm performance by applying their knowledge and developed management skills to influence executives to enhance firm efficiency and, consequently, corporate governance policy. Therefore, we might expect no relationship or a negative relationship between active monitoring and CEO risk-taking incentives since active institutional shareholders can mitigate some of the risky managers’ decisions, decreasing the information asymmetry and agency problems.

Therefore, we expect passive institutional investors to address the CEOs’ incentives to increase their risk-taking in the presence of low-interest-rate monetary policies. Estimations in Table 10 include, sequentially, interaction terms between different proxies of monetary policy and the variables for the role played by institutional investors. We expand Model 1 by considering the interaction between macroeconomic conditions (monetary policies) and the passive or active institutional investors as explanatory variables. Note that Xit is a vector gathering all firm, CEO, and macroeconomic control variables

Robustness analysis: The effect of institutional investors.

This table reports regression results to examine the effect of institutional investors on the relationship between executive compensation and macroeconomic policies. The first two columns report the results for ZLB, the growth of bank loan interest rates (G_INT) is reported in Columns 3 and 4, and the difference between the 10-year and 6-month interest rates (Diff_10y_6m) is used in the last two columns. All regressions are controlled by firm and CEO characteristics, industry dummies (based on Fama–French 49) and year dummies. In Columns 1, 3, and 5, we use the interaction between the macroeconomic policies and the proportion of shares owned by passive institutional investors (Passive), and Columns 2, 4, and 6 show the results of the interaction between macroeconomic policies and the proportion of shares owned by active institutional investors (Active). The set of controls include BonusCEO (the logarithm of the total cash compensation received by the CEO), OwnCEO (number of shares owned by the CEO scaled by total shares outstanding), AgeCEO (the logarithm of CEO age), DualityCEO (a dummy variable equal to one if the CEO is the chairman of the board), Board_size (the number of executive officers on the board), G_GDP (the growth of US Gross Domestic Product), BookMarket (total assets over market value of equity plus total debt plus preferred stock liquidating value minus deferred taxes and investment tax credit), G_Sales (the growth of sales), Leverage (total debt over total assets), Size (logarithm of total assets measured in millions US$), R&D (research and development expenses over total assets), Profitability (operating income before depreciation over total assets), Tangibility (net property, plant, and equipment over total assets), Firm_age (the log transformation of one plus the number of years since the firm was added to the Compustat database), and Abnearn (abnormal returns). LR Test ZLB is the linear restriction test of the sum of the coefficients associated with VegaCEO and the interaction between VegaCEO and ZLB. This table reports marginal effects of VegaCEO for ZLB equal to one or zero and for values of G_INT and Diff_10y_6m equal to the 75th (25th) percentile of the sample distribution. We report the m2 and Hansen tests with the degrees of freedom in parentheses.

, **, and * denote significance at the 1%, 5%, and 10% levels, respectively.

Columns 1, 3, and 5 show significant coefficients in all cases, indicating that the effect of lower interest rates on the CEOs’ risk-taking incentives is intensified to obtain even higher levels in the presence of passive monitors. This result is obtained for interest rates close to zero or ZLB (Column 1) but also for growth of interest rates (Column 3) and for wider differences between long-term and short-term interest rates (Column 5). Consequently, passive investors would be encouraging managers to take more risks to improve their performance. By contrast, we found opposite or nonsignificant coefficients for the interaction of the presence of active institutional investors and the monetary proxies. Notwithstanding, we highlight that the coefficients for the three monetary proxies maintain their sign and significance when both active and passive institutional shareholders are present as owners, thus supporting our first hypothesis. In the untabulated results (available upon request), we obtained evidence that the rest of results found in this work are maintained when active versus passive institutional investors are present. Furthermore, in all cases, we find that the presence of passive institutional investors intensifies the effect of low interest rates on Vega and the effect of Vega on the risk-taking policies of the firm. Consistent with the strong influence of low interest rates on banking businesses both as creditors and investors, we find stressed effects when the analysis is made isolating banks as passive institutional investors.

To provide more robustness to our results, we compute linear restriction tests and marginal effects. In Columns 1 and 2, the linear restriction tests (LR_Test_ZLB) are positive and negative, respectively, supporting the results obtained for interaction terms. In addition, we show the coefficient of the marginal effects of the difference between the effect of passive and active institutional investors in ZLB and non-ZLB periods on VegaCEO. These magnitudes of the marginal effects explain how the sensitivity of CEO compensation to stock return volatility changes with respect to the variations in shares owned by institutional investors during ZLB versus non-ZLB periods. We compute the marginal effects of passive and active institutional investors on VegaCEO with different magnitudes of the proxies of monetary policies. Specifically, we report the difference in the marginal effect of passive and active institutional investors, computed for low (proxy equal to the 25th percentile of the sample distribution) and high growth of bank loan interest rates and the difference between the 10-year and the 6-month treasury interest rates (proxy equal to the 75th percentile of the sample distribution). The results reported in Columns 3 to 6 of Table 10 confirm the sign and significance of the interactions terms. 11

Conclusion

The current empirical study shows that during the period from 2000 to 2016, in the United States, the sensitivity of executive compensation to stock return volatility (Vega effect) increases in the presence of interest rates close to zero (ZLB). Specifically, the increase is found with vested Vega but not with unvested Vega, indicating that the positive impact of the low-interest-rate monetary policy on managerial risk-taking incentives is specifically driven by short-term horizons. This finding is consistent with an alignment of interests between shareholders and creditors and with the preeminence of the creditor channel to solve the agency conflict between them. As the risk-taking effect for creditors works only when the monetary policy reduces short-term interest rates (instead of when long-term interest rates are reduced), our results suggest that creditors’ monitoring of risk-taking incentives would be relaxed with short-term horizons. Therefore, with low short-term interest rates, banks tend to give more loans in softer conditions and join with the shareholders’ incentives to obtain higher profitability in the short run. Consequently, both interests would be aligned to encourage (or not avoid) the firms’ managers to undertake riskier projects.