Abstract

Technology-driven change has generated new, even revolutionary business models, characterized by high levels of user participation. In the finance field, business models based on crowdfunding have seen significant growth and entered use as an alternative means of extending access and gaining financing for various types of projects. Nonetheless, current crowdfunding practices have been subject to criticism for issues such as information asymmetry, lack of trust and transaction costs, spurring discussion of how to develop and improve these practices. One way of speaking to the criticism has been a suggestion that platforms could be owned by the ones who use them. While the associated way of thinking, referred to as platform co-operativism, has seen some inroads in practice, its novel and practical nature means that a clear knowledge gap remains with regard to its potential for dealing with challenges of platform economy. Consequently, the aim of this study is to examine the relevance and potential of the co-operative company form for crowdfunding arrangements. Our conceptual study utilizes existing research on co-operatives and considers features of crowdfunding from three different perspectives: asymmetry of information and of trust, interaction frequency and homogeneity of interests. As a result, we provide three taxonomies for outlining future research on co-operative platforms.

Introduction

In the past few years, technology-driven change has provided new tools for revolutionary business models. Examples of this development, characterized by extensive user participation and by business value often being created by the users, are open collaboration—Airbnb, Uber and YouTube (e.g., Adler, Kwon, & Heckscher, 2008; Faraj, Jarvenpaa, & Majchrzak, 2011; Levine & Prietula, 2014; Kane & Ransbotham, 2016; Majchrzak & Malhotra, 2013). Consequently, scholars have begun turning their eyes to the increasing role of non-traditional stakeholders and a perspective focused on co-operation in designing organizations and envisioning their future (e.g., Alberts, 2012; Baldwin, 2012; Galbraith, 2012; Obel & Snow, 2012, 2016). It has been suggested that the associated disruption of business models is precisely the piece needed to complete the puzzle of how to tap the productivity–gain potential of the new technology (Brynjolfsson & McAfee, 2014).

Recently, work with new business models has opened an alternative way to access and provide financing for projects of numerous types, in a novel approach called crowdfunding. The term implies raising money from a host of capital providers, termed ‘the crowd’ (see Belleflamme, Lambert, & Schwienbacher, 2014). An entire industry based on crowdfunding has sprouted and experienced remarkable growth in recent years, reaching a total value of US$33 billion in 2017 with peer-to-peer lending being the most popular form (Statista.com, 2019). Still, criticism has been levelled at current crowdfunding practices: issues such as asymmetric information, lack of trust and transaction costs have prompted debate on how to develop and improve these practices, and parallels have emerged with widespread discussion connected with new sharing-economy-related business models (cf. Hainz, 2018; Hildebrand, Puri, & Rocholl, 2016; Rey-Martí, Mohedano-Suanes, & Simón-Moya, 2019).

One way of speaking to the criticism has been a suggestion that platforms could be owned by the ones who use them (e.g., Cherry, 2016). The idea is to remove conflict of interests between the owners and users of the platform by merging these two roles. While the associated way of thinking, referred to as platform co-operativism, has seen some inroads in practice, its novel and practical nature (cf. Scholz, 2014, 2016) means that a clear knowledge gap remains with regard to its potential for dealing with challenges of platform economy (e.g., Sandoval, 2019). For example, in what ways user-ownership changes the way platforms are organized and used, and what are co-operative form’s limitations and challenges in particular. In other words, earlier discussion falls short in critically considering the possibilities and potential of cooperative form in crowdfunding. Thus far, scientific research on crowdfunding has concentrated more on the various features of the principals (those seeking and granting funding) than on the structure of the platform for the activity itself. Moritz and Block (2016) are among those noting that studies focused on the role of platforms and their optimal business models remain scarce.

Consequently, the aim of this study is to examine the relevance and potential of the co–operative company form for crowdfunding arrangements. Our critical view recognizes that co-operative form may not be as suitable in every situation as the practical discussion presumes. Our conceptual study utilizes existing research on co-operatives and considers features of crowdfunding from three different perspectives that are representative themes of cooperation between individuals and organizations. These perspectives are asymmetry of information and of trust, interaction frequency and homogeneity of interests. As a result, we provide three taxonomies for outlining future research on co-operative platforms. In addition, they aid practitioners to evaluate the development of user-owned platforms. The article builds on early scientific forays by Talonen, Kulmala and Ruuskanen (2016) and advances more in-depth discussion of the non-economic features of crowdfunding.

We begin our discussion with an adequate literature review by introducing crowdfunding phenomenon and earlier research on the topic as well as defining the fundamental principles of user-ownership and cooperative company form. This grounding is followed by discussion of three non-monetary relationship-based taxonomies within and between the two sets of parties involved, whom we refer to as the applicants (for people who request funds) and funders (for those providing resources), on account of these terms’ independence of platform type. Finally, our conclusions summarize the results, identify areas for future research and delineate policy implications.

Literature

Crowdfunding as a Research Context

The concept of crowdfunding has evolved from the broader idea of crowdsourcing, which refers to decentralized problem-solving and a production model wherein the online ‘crowd’ is a source for services, ideas, feedback and solutions that contribute to developing corporate activities (Bayus, 2013; Belleflamme, Lambert, & Schwienbacher, 2014; Howe, 2008; Kleemann, Voß, & Rieder, 2008). In the case of crowdfunding, the objective is to obtain financing for a project or other venture without standard financial intermediaries, via each member of the online community participating with a small contribution towards the amount needed (Belleflamme et al., 2014; Schwienbacher & Larralde, 2010). In the business model of crowdfunding, online platforms act as an intermediary between the fundraisers and funders to create opportunities for novice entrepreneurs and creative projects, to democratize financial decisions or to make profit for themselves. Lately, even traditional financial intermediaries have experimented with crowdfunding with varying results (one example is crowdfunding.nordea.fi).

Before the term ‘crowdfunding’ entered the literature, about a decade ago, scientific articles on its lending-based form referred to ‘social lending’ and ‘peer-to-peer-lending’ (e.g., Freedman & Jin, 2008; Hulme & Wright, 2006; Klafft, 2008). While the first academic papers to use the newer term were oriented towards the legal issues, Belleflamme et al. (2010) soon established discussion of venture financing that involves crowdfunding. Since then, the amount of discussion and the number of scientific contributions has mushroomed.

As a novel and still evolving phenomena, there is a need for researchers to conceptualize and categorize different aspects of crowdfunding. These activities produce useful taxonomies that help to understand the main features in the domain of the inquiry. By building different taxonomies and typologies, it becomes possible to structure the features into meaningful areas of analysis (DeVellis, 2012). Moreover, the projection of different features into categorization scheme can reveal missing elements and caps for future research.

Scoping studies have provided a useful paradigm for building taxonomies based on literature reviews. These enable to map different contributions into various characteristics to be used when constructing a meaningful taxonomy. (Arksey & O’Mally, 2007) One of the purposes of scoping studies is to find missing elements and to illustrate domains that lack content Pham et al., 2014).

The commonly used classification divides crowdfunding into donation-based, support-based, lending-oriented and equity-based models (e.g., Bradford, 2012; Massolution, 2015). The funders engaging with donation- and support-based platforms do not receive financial return on their investment; instead, supporters may be rewarded with small benefits of nominal value. In contrast to donation- and support-based crowdfunding, equity and lending models usually offer a financial return on funders’ investment. The equity model resembles traditional capital funding, wherein funders receive a share of the profit or other return of what they are funding. Lending-based crowdfunding can be subdivided into peer-to-peer lending and peer-to-business lending. As for lending models, one can also identify social lending and traditional lending; the former does not offer any financial or material return on investment, whereas the platforms using the latter model promise financial return as a form of interest for the funders. (Bradford, 2012; Massolution, 2015).

There are also other classifications of crowdfunding, and Haas, Blohm, and Leimeister (2019) introduce a classification acknowledging the financial intermediation as core function of crowdfunding. They develop a system theory of crowdfunding intermediation and identify three archetypes of crowdfunding intermediation—philanthropic, hedonistic and profit-oriented. The first enables raising funds for charitable projects without direct compensation, whereas the second enables the funding of innovative and creative projects and offers nonmonetary rewards as compensation. Finally, the third focuses on gaining profit by funding of start-ups or giving loans for private consumption.

Academic research concerning crowdfunding can be categorized in accordance with the main actors involved: its fundraisers (i.e., founders, applicants or project creators), funders (i.e., crowdfunders, backers or investors) and intermediaries (i.e., platforms). Prior research has mainly focused on the motivations for crowdfunding, the determinants of success and the legal restrictions. There are also some literature reviews addressing the work done. For instance, Bachmann et al. (2011) introduce the peer-to-peer lending market in their review of 43 scientific articles; Feller, Gleasure, and Treacy (2013) identify the characteristics shared by different types of platforms through metatriangulation of 109 peer-reviewed research papers; and Moritz and Block (2016) offer a comprehensive overview of economics literature on crowdfunding.

Various scholars have studied the motives behind the choice of crowdfunding. These studies underline the non-financial motives, such as visibility of the product/service, garnering greater press coverage, forming relationships and networks, and receiving feedback (Belleflamme et al., 2014; Burtch, Ghose, & Wattal, 2013; Gerber, Hui, & Kuo, 2012; Mollick & Kuppuswamy, 2014). For the funders, a desire to interact in social networks, interest in using the product or service, a desire to support the project or applicant and a hunger for self-affirmation or fun can drive potential crowdfunders to action (e.g., Gerber et al., 2012; Hemer, 2011). However, crowdfunding is also used by fundraisers as a ‘last resort’, when they need funds and lack additional debt capacity (Walthoff-Borm, Schwienbacher, & Vanacker, 2018).

In addition to motives, there are also several studies focusing on the backing behaviour of the crowdfunders during a campaign (e.g., Block, Hornuf, & Moritz, 2018; Lukkarinen et al., 2016; Kuppuswamy & Bayus, 2017, 2018; Hornuf & Schwienbacher 2018). These studies do not only enhance the understanding about the crowdfunders’ behavior but also produce practical implications for the project creators. Studies have found that the determining factors for successful crowdfunding include a large social network, the presence of a product video, positive updates during a campaign and close proximity between the parties (Block et al., 2018; Giudici, Guerini, & Rossi Lamastra, 2013; Hekman & Brussee, 2013; Mollick, 2014; Mollick & Kuppuswamy, 2014; Petitjean, 2018).

So far, majority of the research has concerned itself with the applicants and funders, while only few have focused on intermediary, despite its key role in crowdfunding success (see, e.g., Moritz & Block, 2016). That said, some topics associated with the platforms have received attention, among them the various business models, the regulatory environment and the asymmetric information problems faced by crowdfunding intermediaries (e.g., Belleflamme, Omrani, & Peitz, 2015; Chen, Ghosh, & Lambert, 2014; Courtney, Dutta, & Li, 2016; Doshi, 2014; Rey-Martí et al., 2019; Wash & Solomon, 2014). These studies provide a vital basis for our research design, since we explore the co-operative ownership’s potential to deal with challenges of platform economy.

Intermediaries generate revenue mainly from three sources: a transaction fee, the interest on the money dedicated to a given campaign and the additional pre-launch, ongoing and post-launch services such as payment-handling charges or periodical updates (Belleflamme et al., 2015; Rossi & Vismara, 2018). Several scholars have focused on finding the best suitable practices and models for crowdfunding platforms. According to these studies, platforms should be designed to perceive useful and easy to use, attract the highly successful performers, rely on the all-or-nothing principle and offer number of post-launch services, in order to increase total transaction volume and the number of successful campaigns (Doshi, 2014; Lacan & Desmet, 2017; Wash & Salomon, 2014).

One key challenge faced by crowdfunding platforms is the information asymmetry between fundraisers and funders. The asymmetric information is due to the fact that the fundraisers have more knowledge of the product or service quality and the capital and credibility of the venture, whereas the funder has to settle for the limited information shared on the platform (Belleflamme et al., 2015). Lack of trust is seen as one of the main disadvantages of crowdfunding compared to other forms of financing (e.g., Rey-Martí et al., 2019), and critics, regulators and academics have been concerned about the crowdfunding markets, allowing unscrupulous project originators or sophisticated investors to take advantage of inexperienced investors. According to Cumming, Hornuf, Karami, and Schweizer (2020), the fraud rate is still low in the crowdfunding market, but it may be simply due to low incentives to detect fraud (Hainz, 2018). Some scholars (e.g., Hildebrand, Puri, & Rocholl, 2016) have also provided evidence of perverse incentives in crowdfunding that are not fully recognized by the market. Nevertheless, the legal enforcements by third parties are very small, which put the pressure on the crowdfunding platforms (Cumming et al., 2020).

Literature highlights that the key factors for succession within crowdfunding industry are trust, reputation and legitimacy (Cumming et al., 2020). This applies for the crowdfunding platforms acting as intermediaries as well as the individuals or start-ups seeking crowdfunding. Thus, intermediaries have a strong incentive for self-regulation to mitigate asymmetries, build trust and protect themselves from all risks that might harm their reputation in the eyes of potential campaign creators and funders, and several scholars have studied the ways to tackle problems and risks caused mainly by asymmetric information in the crowdfunding platforms (Belavina, Marinesi, & Tsoukalas, 2018; Courtney et al., 2016; Cumming et al., 2019, 2020; Greiner & Wang, 2010; Hainz, 2018; Mäschle, 2012; Rey-Martí et al., 2019).

Studies show that with the goal of reducing negative effects of information asymmetries on funders; platforms should apply due diligence, use third-party endorsements; give profound information on the campaigns; publish comprehensive information about each applicant’s business, finances and management; and share all the details of the risks that potential funders expose to (Courtney et al., 2016; Cumming et al., 2019; Mäschle, 2012; Rey-Martí et al., 2019). More technical efforts include stopping the campaign once the target is achieved and escrowing any funds raised in excess of the goal for funders as insurance (Belavina et al., 2018). Finally, Cumming et al. (2020) present some proposals, such as heavier private or public regulation with the dynamically adapting fraud detection models to reduce fraudulent action in this new, developing market.

While studies have identified platforms’ important role in reducing asymmetries; providing a standardized process for funding; acting as an information, communication and execution portal; and building trust in crowdfunding markets (Agrawal, Catalini, & Goldfarb, 2013; Belleflamme et al., 2014; Greiner & Wang, 2010; Haas, Blohm, & Leimeister, 2014), the work on models reveals little about which business models are optimal if the platforms are to facilitate such positive results for the market participants, as Moritz and Block (2016) have noted. Research has been devoted to investigating platforms’ current practice, without attention being paid to the significance of the platform’s company form.

The Co-operative as an Ownership Innovation

The co-operative is a company form dating all the way back to the mid-nineteenth century. Today, co-operatives are prominent actors in many distinct fields, such as retail, banking, insurance and agriculture, and the 300 biggest co-operatives together generate more than US$1,500 billion in annual income (ICA, 2016). Notwithstanding their significant role and long history, co-operatives of whatever sort have started to spur interest among scholars only recently (e.g., Talonen, 2016). It has been suggested that one reason for this may have been paradigmatic dominance of economics textbooks and mainstream theories by the stock-based company and a shareholder perspective for most of the twentieth century (e.g., Kalmi, 2007).

The absence of co-operatives from mainstream discussion is rather interesting, in that the fundamental differences between company forms could have considerable implications for how a given company is organized and value created. The end purpose of an investor-owned company is to produce maximal economic value for its shareholders in the form of dividends and increases in share value (e.g., Hansmann, 1996). This is rooted in the shareholders’ interest in the highest possible return on the capital. In co-operatives, in contrast, the purpose of the company is expected to move towards creating benefits and value for the ones use its' services. In other words, this form is its member–owners’ mechanism for ‘protecting their interests and meeting their needs in the market’ (Byrne, Heinonen, & Jussila, 2015). Accordingly, co-operatives should identify and invest in those business operations reflecting what is most needed by the member–owners instead of seeking the greatest opportunities to make money (Mazzarol, Limnios, & Reboud, 2011).

As the member–owners’ own tool, the co-operative is a participatory mechanism that facilitates co-operation among them in pursuit of their common goals. Scholars have posited on this basis that members have an active role in the value-creation processes at two levels (Talonen, Jussila, Saarijärvi, & Rintamäki, 2016). First, their consumption behaviour can influence perceptions of value. This mechanism is supported by built-in features such as co-operatives granting rewards commensurate with the member–owner’s contribution to the co-operation. Second, as owners, a member can be active in steering the co-operative in such a direction that the members gain maximized value in the future as well. Consequently, a co-operative can be a highly agile player in the markets on a normative level, and one could argue, further, that its performance is best measured in terms of not only end-of-period profit but also user satisfaction and the perceived value of the services (e.g., Jussila, Tuominen, & Saksa, 2008; Peterson & Anderson, 1996). In this thinking, the owners of the co-operative should be understood as users rather than investors (Borgen, 2004). The following section discusses implications for the crowdfunding domain.

The Role of Non-monetary Factors for Crowdfunding Platforms

Research has shown that financial motivation is not necessarily the key factor in crowdfunding—for applicants and funders alike, there are multiple other incentives to take part (e.g., Agrawal et al., 2013; Belleflamme et al., 2014; Gerber et al., 2012). Accordingly, crowdfunding sites have been identified as in many cases providing their users with a number of additional services alongside economic benefits. For example, Beaulieu, Sarker and Sarker (2015) noted that these sites represent a wide spectrum of operations beyond just transferring funding between two sides of the market. The sites have a role to play in the discovery, communication and contribution stages of the process.

Researchers such as Hagedorn and Pinkwart (2016) have shed further light on the motivations by considering each stage in the process in turn. For equity-type crowdfunding, they found that platforms support additional value elements sought by users in all seven stages identified—application, screening, contracting, the ‘roadshow’, subscription, holding and exit. Whether the system is arranged in co-operative or stock-owning form can, hence, have a profound effect on the ease of ensuring the various associated incentives and avoiding disincentives. These are mediated by the psychological constructs and tangible ownership structures specific to particular forms of an organization. Here, we focus on these, especially with regard to asymmetry of information/trust, interaction frequency and the level of homogeneity of the patrons.

Asymmetries in Information and Trust

While removing financial intermediaries from the picture has given market players new means of providing and seeking funding via direct co-operation with each other, it has also created new challenges. One of these is connected with how funders and applicants can trust each other when there are no traditional financial intermediaries facilitating the exchange. The other main question is how to lessen the information disparity between the principals. Especially in equity-based funding, in which the funder must assess the viability and the prospects of the entire business entity involved, informational problems are rife.

Agrawal and colleagues (2013) have highlighted three means by which the asymmetric nature of the information can be addressed between crowdfunding applicants and funders: reputation, regulation and platform rules. Furthermore, their report points to reputation as built in three ways. Quality signals can be provided through brand-reputation or patent instruments, feedback systems can be incorporated into a site and third-party intermediaries may certify or validate the offering.

The trust component can be cultivated through ready communication between the two sides of the market. In light of this, Beaulieu et al. (2015) investigated the variety of tools offered by crowdfunding sites, which depend largely on the funding model utilized. In a large-scale survey of crowdfunding sites, they found that sites applying an equity-based model provide the most extensive facilities for communication between the participants. However, unequal footing is still evident, in that the party in search of funding often has discretion with regard to which potential funding sources to contact. Lending-based platforms are particularly strong in providing tools to estimate the creditworthiness of each prospective funder. The researchers found support-based systems to offer tools for close contact between funders and applicants. Also, social media are used extensively to highlight the project. In contrast, donation-based funding provides room for describing one’s project, but social media are not prominent.

It has been argued that excessively high costs of market contracting result in opting for a co-operative structure (Hansmann, 1999). This arises from the possibility that exploiting merging of the two parties through ownership (e.g., customer–owners) will reduce information asymmetry and related transaction costs. Furthermore, it may influence the behaviour of the member–owners, in that service-users who are also owners of the company have an incentive to behave and act for the good of the company. As both users and owners, they bear the risks of the company and know that its success hinges on their own behaviour. Such ideas have been put forward particularly in discussion of mutual insurance companies, where this company form has been seen as a tool against moral hazard and adverse selection (e.g., Adams, Andersson, Jia, & Lindmark, 2011; Ligon & Thistle, 2005; Smith & Stutzer, 1995).

Moreover, while co-operatives’ first and only mission should be to provide the member–owners with maximum benefits and value, that comes about via individuals choosing this tool for pooling their resources and joining together to reap these benefits. In other words, they all are dependent on each other for gaining individual-level benefits. The collective-level interdependency coheres in a particular social tool and engenders incentives for these individuals to act in pursuit of the co-operative’s success; cf. the notion of social capital (e.g., Nilsson, Svendsen, & Svendsen, 2012; Tuominen, Tuominen, Tuominen, & Jussila, 2013).

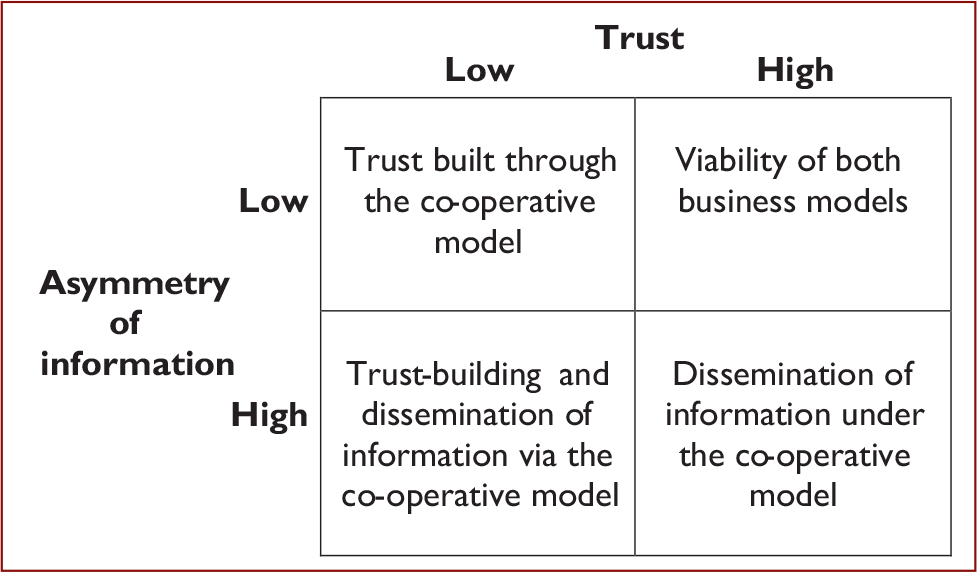

We argue, therefore, that using the co-operative company form could anchor trust within a given crowdfunding platform, and those platforms whose approach (e.g., applying the keep-it-all principle or entailing more challenging estimations of applicants’ prospects) demands additional mechanisms to reduce asymmetry of information would benefit the most from this form of organization. Figure 1 illustrates the potential by dividing the space into high- and low-trust environments and between situations wherein the level of information asymmetry is low and high.

Frequency of Interaction

One important determinant of the trust that can be cultivated for a platform is a function of the frequency of the interaction between partners. Three interaction scenarios are typical in a crowdfunding context. In the first, the party on each side of the market interacts only once with the platform and then exits. In the second case, one party performs a single interaction only, but the other engages in repeated participation. The final scenario manifests multiple engagements on both sides.

Some facets of relationships can be characterized in line with the platform type. Support-based platforms facilitate a limited, transactional arrangement between applicant and funder. Funds here are raised only for a particular project, with a set goal that may eventually be reached, at which point the applicant should produce something. Once the project is over and the rewards are delivered, the relationship between the project initiator and platform usually ends.

Funders’ relationships with a support-based crowdfunding platform display slightly more variety. Recent studies have revealed that most funders using support-based platforms back only one project (Inbar & Barzilay, 2014; Marom & Sade, 2013). Although these one-time funders, who usually have a personal attachment to a specific project, are in the vast majority, repeat funders play a significant part for the platform. In the case of Kickstarter, they account for 30 per cent of all funders and produce 72 per cent of the pledges on the platform (Inbar & Barzilay, 2014). Applying a finer-grained typology, Hahn and Lee (2013) identified five classes of backers in support-based crowdfunding, of which four back projects relatively frequently. Some funders, ‘category backers’, focus on a specific sort of project, and others divide their support across all categories on the relevant platform (‘site backers’), with some Kickstarter users supporting 20+ projects, in a variety of funding categories, per month (Hahn & Lee, 2013).

Similar funder-side behaviour is visible with donation-based platforms. On the applicant side, however, a longer-term relationship with the platform may unfold in cases of a not-for-profit organization. This is only natural, in that not-for-profits’ very existence is often contingent on donations. With funders, in contrast, recent studies attest that donation-based platforms’ donor retention rates are rather low, although repeated actions, similar to those in the support-based class, can be seen too (Althoff & Leskovec, 2015; Sargeant, 2008; Song, Lee, Ko, & Lee, 2015). It could be argued that funders with highly altruistic motivation establish a longer-term relationship for reason of willingness to be involved with several charitable causes fairly often.

The lending- and investment-based forms of crowdfunding, in contrast, are designed mainly for financing of extended-duration ventures. Generally, the applicants seek money for a specific one-time cause and so do not necessarily launch new campaigns frequently, but repaying a loan or managing the investments may take years, and a longer-term relationship with the platform follows. The associated administration strengthens the funders’ ties to the lending- and investment-based platform, in addition to which those funders motivated by a desire for profits and diversified investments from crowdfunding may engage in repeated interaction with it.

According to social exchange theory, exchange between parties can take either of two forms—negotiated or generalized exchange. Negotiated exchange, with openly agreed terms of exchange, is favoured by parties responding to self-interest (Cropanzano & Mitchell, 2005). This form brings with it a risk of opportunism. Generalized exchange, involving benefits that are produced and received on a longer time horizon, has reciprocity at its core and is characterized by trust and a collectivist orientation. The group members taking part in generalized exchange elevate their common interests above short-term individualistic ones.

Both aspects are vital. In a co-operative context, it is important for individuals to perceive short-term benefits and thus understand the immediate gains, yet a co-operative’s success requires the members to understand and be committed to a more distant future, such that they can unite to achieve benefits further down the line. Because this entails member–owners’ commitment, participation and close long-term relationship with the co-operative, it is evident that successful co-operative manifest both short-term and long-term benefits, and a balance between the two needs to be found. According to Jussila, Goel, and Tuominen (2012), emphasis on the short-term benefits encourages opportunistic actions and undermines longer-term benefits. At the same time, dominance of the long-term thinking pays insufficient attention to the short-term benefits for the member, rendering it hard for them to justify their participation. In other words, immediate terms are negotiated, while there is room for later alteration/completion.

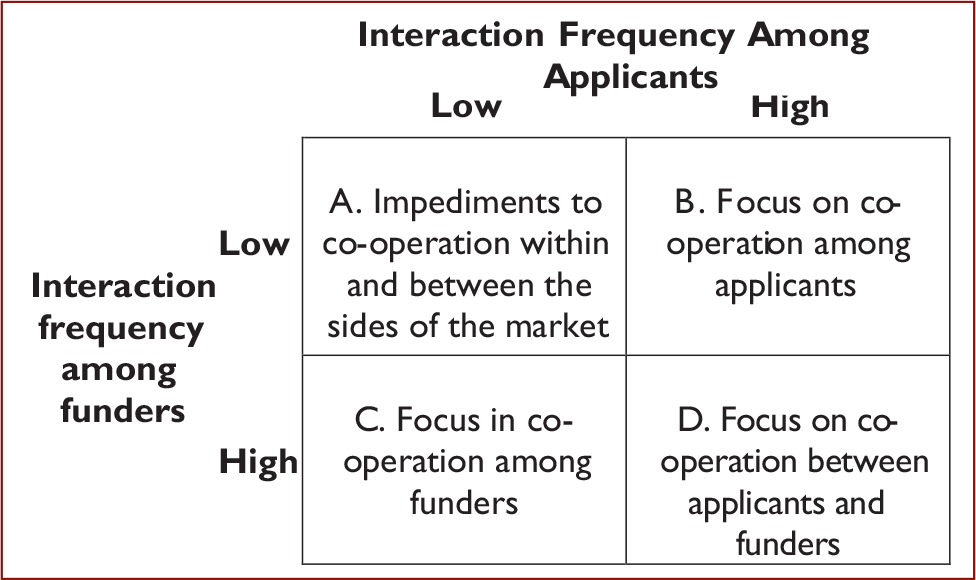

In that, a co-operative acts as a tool by which individuals pool resources to reap individual-level benefits—that is, they are dependent on each other for achieving these benefits (e.g., Puusa, Hokkila, & Varis, 2016)—it is the co-operation and the unity of individuals that matter. Since this entails extensive collective interdependency on a longer time horizon than found with investor-owned firms, we posit that the potential this business form represents for a platform is dependent on the market parties’ frequency of interaction, as illustrated in Figure 2.

When both funder-platform and applicant-platform interaction are infrequent (depicted in cell A), it becomes challenging to arrange co-operation oriented towards a longer time horizon and aimed at producing benefits within a longer time frame. When applicants’ frequency of interaction is high but funders’ is low (cell B), focus should be shifted towards emphasizing co-operation between applicants. We suggest that in the opposite scenario (cell C), it becomes more rational to attend to optimizing co-operation among funders. Finally, when frequent interaction is visible on both sides of the market (cell D), focus should be placed on developing the co-operation in a manner that takes both groups—funders and applicants—into account. In other words, great effort should be put into developing the co-operative such that it can facilitate multi-stakeholder co-operation. For a good outcome in such a situation, however, it is vital that the interests within (but not necessarily between) the two groups be rather homogeneous. This is what we consider next.

Platform-internal Decision-making

Internet-based commerce is claimed to exhibit hyper-specialization, wherein platforms diverge to serve various niche market segments. One can also point to a tendency for some sites to serve considerably wider swaths of the market, to reap economies of scale and scope (as with Amazon and eBay). Both types of business logic appear to be at play on the Internet.

Crowdfunding sites display the same polarization. There are those that strive for volume and those that specialize in a niche market. The trust factor may play an important role in the scope of a site’s activities: the wider the net is cast, the higher the volume and the more credible the operation may seem. In an important development, one also finds hybrid sites, which encompass multiple funding mechanisms. Most studies have focused on large-scale platforms of this nature, such as Kickstarter, where the variety of project categories and rewards is huge (e.g., Hahn & Lee, 2013; Inbar & Barzilay, 2014; Kuppuswamy & Bayus, 2015; Lin, Boh, & Goh, 2014; Marom & Sade, 2013; Mollick, 2014). One might expect the funders and applicants involved with these platforms to be quite heterogeneous in their motivations and, therefore, not representative of the entire crowdfunding landscape. The variety of motives might not be as wide with other platform types.

As noted earlier, motivations of funders differ between platform types. Participation by funders who act as donors or supporters usually is underpinned by altruistic or normative reasons, and the outcome of the project or the feeling of belonging to a community is stressed. On the contrary, funders under lending or investment models are driven by a desire for future profit. That said, studies have revealed that even funders using the same crowdfunding platform are heterogeneous in their motivations, strategies and behaviours (e.g., Hahn & Lee, 2014; Lin et al., 2014).

Emphasizing the common interests of the platform users, the past few years have witnessed proliferation of niche platforms that focus on specific industries, regions or demographic groups. These platforms, exemplified by the fan-targeted ArtistShare, creative arts–targeted Patreon, donations-based GoFundMe and technology-focused SeedInvest, serve as umbrellas for a common interest that their users share, so their membership tends to be more homogeneous and exclusive.

If the platform is organized in a co-operative manner and its ownership is thereby distributed among numerous member–owners, the efficiency of the decision-making hinges on the member–owners’ homogeneity. According to Hansmann (1999), the costs of collective decision-making are low when ‘all transact with the firm under similar circumstances for similar quantities of a single homogenous commodity’. Accordingly, if the members’ interests diverge considerably, it may be challenging to reach collective, democratic decisions, and the costs of decision-making rise.

Furthermore, even when the decision-making process functions well, it may be that the decisions prove inefficient. This is due to the democratic voting process considering all the various interests—by ‘averaging’, it fails to maximize the benefits for individual patrons. Moreover, a broad member–owner base with divergent interests may tend to break into coalitions or sub-groups that seek to exploit other factions and steer the co-operative’s collective decisions in the direction that serves their personal interests (e.g., Hansmann, 1999; Jussila et al., 2012). In the same time, managerial incentive problems have been identified as growing as a co-operative gets larger and less connected with specific member–owner groups. Accordingly, co-operatives should focus on serving more concentrated markets than investor-owned firms attend to (Mayers & Smith, 1988). Therefore, spatial and non-spatial proximity between the co-operative and its members can be seen as important value-creating factors (Byrne et al., 2015).

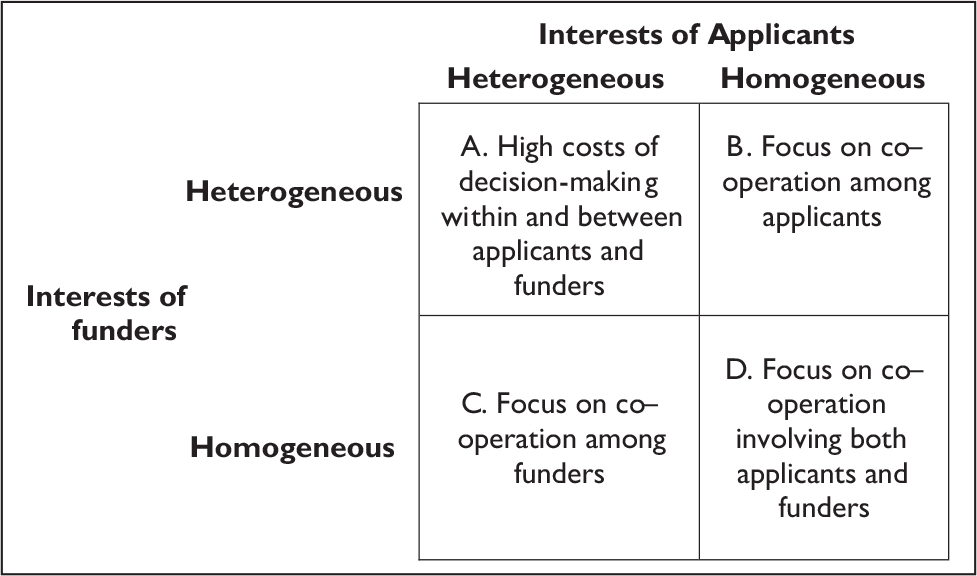

Proceeding from the foregoing discussion, we suggest that the potential of the co-operative form in organization of a crowdfunding platform depends on the level of homogeneity of the market parties’ interests. This is illustrated in Figure 3. When interests differ greatly within and between the funder and applicant sides (cell A), arranging co-operation becomes more challenging. Where the interests of applicants are largely convergent, while those among funders differ (cell B), the organizers should emphasize co-operation between applicants. For the opposite scenario (cell C), we suggest that it becomes more rational to direct attention towards optimizing co-operation among funders. Finally, if interests are quite coherent among both groups (cell D), there is potential to direct operations towards cultivating co-operation wherein funders and applicants alike can be readily taken into account. In a parallel with frequency of interaction, the co-operative’s reward mechanisms should be developed so as to support multi-stakeholder co-operation. This potential could be harnessed by identifying and concentrating on fostering interests that bring unity across stakeholder-group boundaries.

Conclusions

With crowdfunding sites being predominantly investor-owned, this conceptual article has contributed to understanding by illustrating the potential of the co-operative company form in the development of crowdfunding platforms. This contribution has entailed analysing certain key non-monetary factors that have implications for how this company form can be implemented successfully: the asymmetric nature of information and of trust, frequency of interaction and the decision-making internal to the platform in question.

The problems connected with information asymmetry and lack of trust can be reduced by utilizing a co-operative structure and philosophy. Drawing together the role of owner and that of user signals commitment, by which the co-operative entity builds trust among the potential market participants. This form also enables wider dissemination of information, thereby bringing the market participants onto a level playing field with regard to the amount of information they possess.

Co-operatives’ success is rooted in their members’ mutual relationship and their commitment to co-operation with each other in pursuit of the desired benefits. Consequently, the potential of user-owned platforms is conditioned on ongoing frequent interaction with the platform. We propose, in light of this, that the co-operative is a form better suited to those platforms characterized by long-term relationships between the platform and its users.

In addition to relationships extending over time, successful co-operation hinges on a certain level of homogeneity of interests among the users. This is connected with member–owners’ ability to make decisions and steer the co-operative in such a manner that it benefits all of the members. Therefore, we argue that the co-operative form is more suitable for platforms whose patrons constitute a homogeneous group with relatively uniform interests.

Because this article is, to the best of the authors’ knowledge, the first journal article to address the question of company form in the context of establishing and maintaining a peer-to-peer platform, it serves as an entry point for discussion of the associated issues. The taxonomies presented pave a new avenue for academic research into developing models and mechanisms that offer potential to capture the overall value created by today’s new Internet-based business models.

Future Research

As a conceptual piece, this article has focused on bringing together existing constructs (cf. Yadav, 2010, 2014)—namely crowdfunding and user-ownership in light of the co-operative company form. The conclusions crystallize a need to complement and widen the body of knowledge in this area by means of empirical research. With the concept of applying the co-operative form in the field of crowdfunding being quite new, valid data answering this call remain scarce. In the meantime, complementary conceptual studies can still enhance understanding of the issue and provide important and managerially relevant taxonomies for actors entering this field—players whose operations could, in turn, generate such data.

Moreover, while we have offered some initial scientific discussions related to the role and implications of the co-operative company form with regard to crowdfunding, research questions encompassing several issues must be addressed. First, researchers should consider more extensively how existing knowledge of co-operatives could be applied in crowdfunding and crowdsourcing practices. Also, addressing such matters as the role of co-operative principles (e.g., Novkovic, 2008), the sense of psychological ownership (e.g., Jussila & Tuominen, 2010), implications of social capital (e.g., Tuominen et al., 2013) and creating member value (e.g., Suter & Gmür, 2013; Talonen et al., 2016) could yield important insight into the relationship between a co-operative platform and its member–owners.

In addition, it would be interesting to advance understanding of the ways in which Internet-based co-operative platforms can be managed and co-operation among their members arranged efficiently. The importance of this question is only amplified by the fact that research into co-operatives has traditionally been focused on geographically restricted entities and local impact (cf. Jussila, Kotonen, & Tuominen, 2007). Consequently, research on the management of digitized and globally owned co-operatives could contribute greatly to knowledge in this domain. Furthermore, we should stress that as the discussion takes its first strides, stepping into empirical research too is crucial. Again, although there are no co–operative platforms involved in crowdfunding at the moment, data from existing platforms could be used to deepen understanding of the challenges the industry faces.

Second, discussion of co-operative platforms could benefit from multidisciplinary research. Many opportunities exist in this regard for such disciplines as sociology, law, economics, marketing and management, alongside general co-operative research. Hence, we encourage scholars to engage in this discussion across boundaries between scientific disciplines.

Third, it should be noted that platform-based business models in the digital age are often defined in terms of two-sided markets. This issue, beyond the scope of our study, adds to the complexity of considering which people or which group of platform users should own a given site. We encourage academics to direct efforts in this direction (for a review of two-sided markets, see Rochet and Tirole, 2006; on specific models, see Rochet and Tirole, 2003; Weyl, 2010). Overall, the question of two-sided markets is not limited to co-operatives, so should be considered more broadly in scholarship, developing the understanding of the expanding roles of consumers and platform users.

In addition, the crowdfunding industry is rather diverse, with numerous models in play (manifested, e.g., by support, equity, donation and lending platforms). Research could benefit from in-depth articles that examine particular models of crowdfunding in terms of corresponding company forms, since the models exhibit fundamentally different features and relationships with their users.

Finally, we have provided a solid foundation for research not only in a crowdfunding context but also with regard to crowdsourcing and Internet-based business models in general. There appear to be many similarities in fundamental principles across peer-to-peer platforms. These should be addressed. In addition, there is certainly a need to evaluate the differences between these related fields and, accordingly, conduct context-specific research.

Policy Implications

One clear policy implication is connected with most markets’ lack of comprehensive legislation and regulation dealing with crowdfunding platforms. The shape of future regulation of crowdfunding sites is going to affect the magnitude of the risks taken by these sites and their users, influencing, in turn, such factors as the amount of trust these sites generate. What may emerge is unclear—for instance, with the crowdfunding industry being young, not many cases of default have yet been recorded. The regulatory landscape can also affect the attractiveness of specific organizational arrangements. Proactive assurance could have considerable influence in this respect and guide towards balanced and healthy development.

Again, this article represents the first exploratory look at the emerging crowdfunding industry. Several questions remain to be studied further, and more will become apparent as the industry matures. It serves as only a starting point for contemplating the alternative ownership structures that could emerge in that space. As in other industries, diversity of ownership usually grows as novel practices and solutions get implemented and face their market test.

Footnotes

Acknowledgements

Author Antti Talonen gratefully acknowledges the support of the Foundation for Economic Education for writing of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article