Abstract

Study Design

A multi-disciplinary review.

Objectives

To provide a roadmap for implementing time-driven activity-based costing (TDABC) for spine surgery. This is achieved by organizing and scrutinizing publications in the spine, neurosurgical, and orthopedic literature which utilize TDABC and related methodologies.

Methods

PubMed and Google Scholar were searched for relevant articles. The articles were selected by two independent researchers. After article selection, data was extracted and summarized into research domains. Preferred reporting items for systematic reviews and meta-analyses (PRISMA) systematic review process was followed.

Results

Of the 524 articles screened, thirty-five articles met the inclusion criteria. Each included article was examined and reviewed to define the primary research question and objective. Comparing different procedures was the most common primary objective. Direct observation along with one other strategy (surveys, interviews, surgical database, or EMR) was most commonly employed during process map development. Across all surgical subspecialties (spine, neurologic, and orthopedic surgery), costs were divided into direct cost, indirect cost, cost to patient, and total costs. The most commonly calculated direct costs included personnel and supply costs. Facility costs, hospital overhead costs, and utilities were the most commonly calculated indirect costs. Transportation costs and parental lost wages were considered when calculating cost to patient. The total cost was a sum of direct costs, indirect costs, and costs to the patient.

Conclusion

TDABC provides a common platform to accurately estimate costs of care delivery. Institutions embarking on TDABC for spine surgery should consider the breadth of methodologies highlighted in this review to determine which type of calculations are appropriate for their practice.

Keywords

Introduction

The cost of health care in the United States is unsustainable, and has consistently outpaced inflation year after year. Unfortunately, this level of spending is not consistently associated with superior outcomes.1,2 Experts point to the traditional “fee-for-service” reimbursement model as a major cause of this problem – providers are paid based on the volume and complexity of their care, rather than the outcomes of that care. This has prompted a shift towards “value-based reimbursement”, where value is defined as the outcomes achieved per healthcare dollar spent.3,4 Examples of value-based reimbursement are bundled payment programs and direct-to-employer purchasing, which can promote efficiency and optimal resource allocation. 5

A fundamental prerequisite for the viability of any such reimbursement model, however, is an accurate understanding of the costs of care. What matters most, in this context, is the total cost to the hospital or practice for a given patient’s episode of care. This is because value-based payments are organized around care episodes. By prospectively tracking patient-level costs in this manner, one can determine reimbursements that benefit provider groups while also creating efficiencies. Surprisingly, institutions do not routinely track this information. The gold-standard approach for doing so, which is applied widely in other industries, is time-driven activity-based costing (TDABC). In TDABC, cost units are created for each material and personnel resource utilized for a patient, which are then multiplied by the amount of time spent at each step of a care episode. 6 A less granular approach is activity-based costing (ABC), which assigns broad costs to specific activities but does not account for the times associated with those activities.7,8 What institutions often resort to is a methodology called “cost-to-charge ratios” (CCR), wherein the costs are assigned in proportion to charges for individual services.9-11 This is a crude and inaccurate approach because it is well-known that hospital charges for individual items and services are generally unrelated to their true costs.

The paradigm shift to value-based reimbursement is currently underway, and institutions will succeed or struggle based on their ability utilize strategies such as TDABC. 12 This is particularly true in the context of spine surgery, which is a high-dollar and high-volume service line throughout the country. What is lacking is a practical roadmap for implementation, which accounts for the complexity of coding and heterogeneity of procedures inherent to spine surgery.13,14 The aim of this review is to provide such a roadmap by organizing and scrutinizing publications in the spine, neurosurgical, and general orthopedic literature which utilize TDABC, ABC, or CCR.

Methods

Study Design

After establishing the research domain, inclusion and exclusion criteria were developed to identify and select relevant articles. Information from the shortlisted studies were extracted, organized, summarized, and charted accordingly. The results were analyzed and reported. The primary research question guiding this review is: “Which strategies are being utilized to appropriately quantify cost in surgical fields such as neurosurgery, spine surgery, and orthopaedic surgery?”

Search Strategies

PubMed or Medical Literature Analysis and Retrieval System Online (Medline), and Google Scholar, were reviewed for relevant articles. Medical subject headings were searched using the Boolean operators “OR/AND”. The search terms were: (“costing strategies” OR “costing” OR “TDABC” OR “TDABC” or “ABC” OR “ABC” OR “CCR” OR “CCR”) AND (“neurosurgery” OR “spine surgery” OR “spine” OR “orthopaedic surgery”).

Inclusion and Exclusion Criteria

Studies were included which described strategies to quantify cost in the aforementioned surgical specialties. Studies not describing details of costing methodologies were excluded, as were non-English articles.

Identification and Selection of Studies

The studies were selected after two stages of screening. Two researchers (DMA and AS) independently extracted information from the studies. In stage 1, the article titles and abstracts were individually reviewed and those which matched the inclusion and exclusion criteria were selected for full text review. In the final stage, we reviewed full texts of the articles and determined their inclusion in the review. Any conflicts between researchers during the article screening process was resolved by the senior author (AS). Data was organized using a database in Microsoft Excel. Figure 1 presents a Preferred Reporting Items for Systematic Reviews and Meta-Analyses (PRISMA) flow diagram showing the process of searching and selecting the research articles. Preferred reporting items for systematic reviews and meta-analyses (PRISMA) flow diagram for database search of studies.

Data Extraction From Included Studies

After article selection, information was extracted and reviewed in a data extraction form in a spreadsheet. The domains in the data extraction form were: study title, name of author, surgical subspecialty, costing strategy utilized, and details of cost calculated.

Summarizing the Findings

We summarized our findings into the following research domains: type of research question answered, details of costing methodology, process mapping strategy, cost determination, and capacity calculation.

Assessing Level of Evidence

To assess the level of evidence, each study was assigned an Oxford Center for Evidence Based Medicine (OCEBM) score based on its design.

Definition of Terms

Definitions of Common Terminologies Employed for Cost Determination.

Results

Study Characteristics

A total of 524 articles were retrieved from PubMed and Google Scholar. Two hundred and seventy-one duplicate articles were excluded. Out of the remaining 253 articles, 218 articles were either not describing the type of research question answered, did not provide costing methodology details, had no process mapping strategy outlined, did not describe source of cost determination or capacity calculation, or were written in a language other than English (and no English translation was available) and therefore were excluded. Thirty-five articles were reviewed and included in this study.

Research Domains

Summarized Findings of Included Research Articles Describing Different Costing Strategies.

Surgical Subspecialty and Type of Research Question

Primary Research Question Driving Cost Analysis Within Each Surgical Subspecialty.

Surgical Subspecialty Process Mapping Methodologies

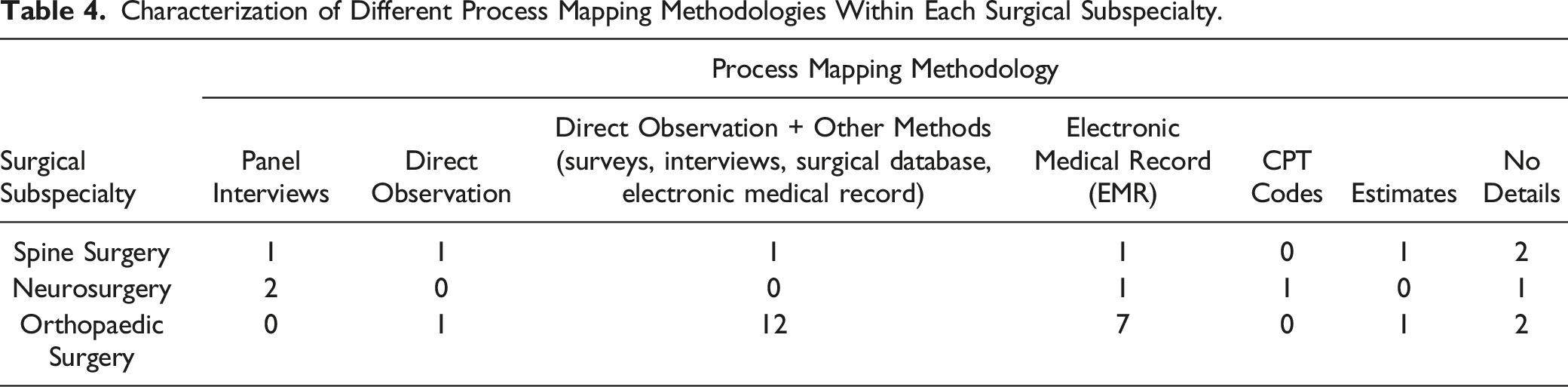

Characterization of Different Process Mapping Methodologies Within Each Surgical Subspecialty.

Surgical Subspecialty and Type of Costs

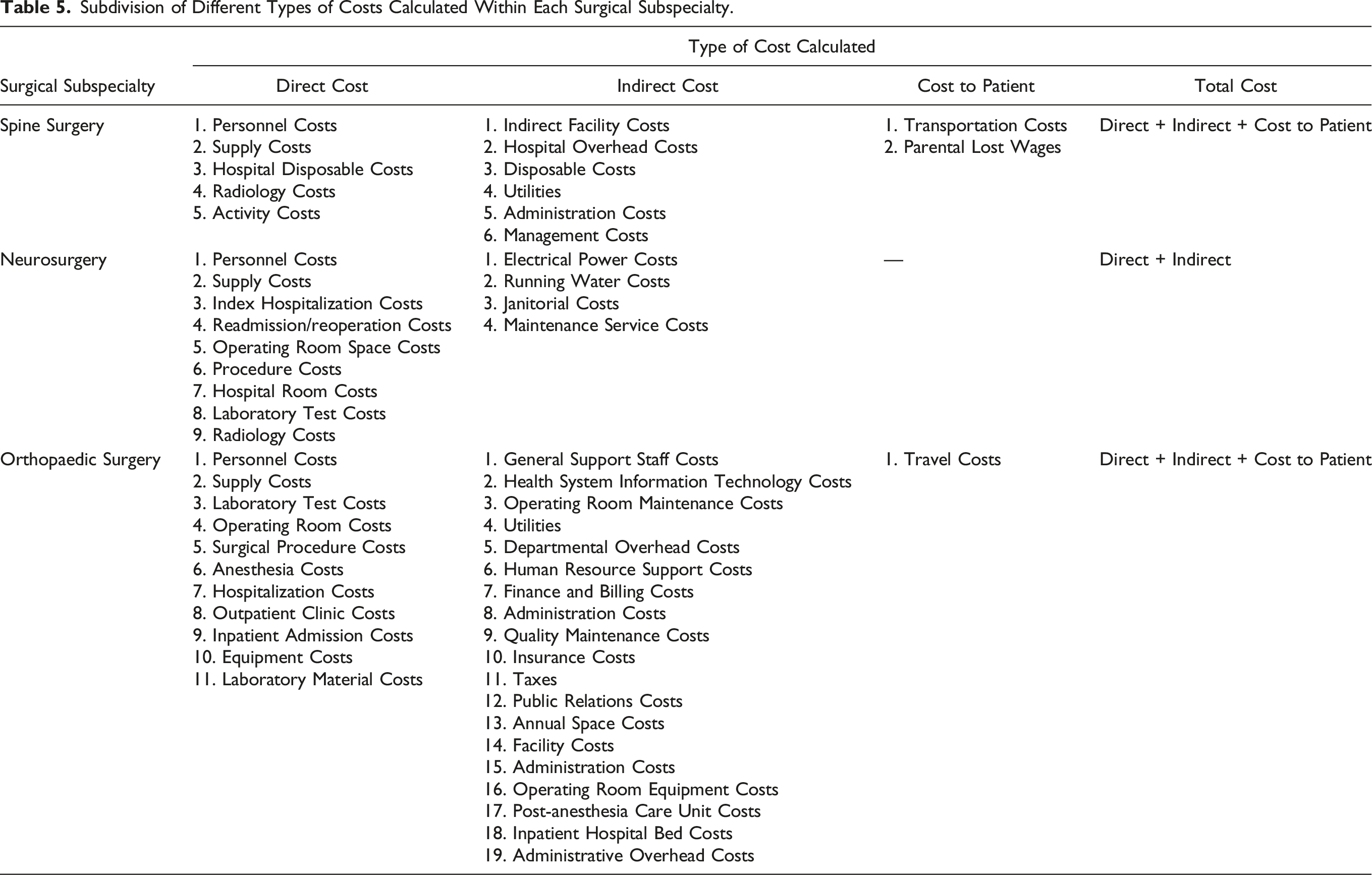

Subdivision of Different Types of Costs Calculated Within Each Surgical Subspecialty.

Cost Determination and Capacity Calculation

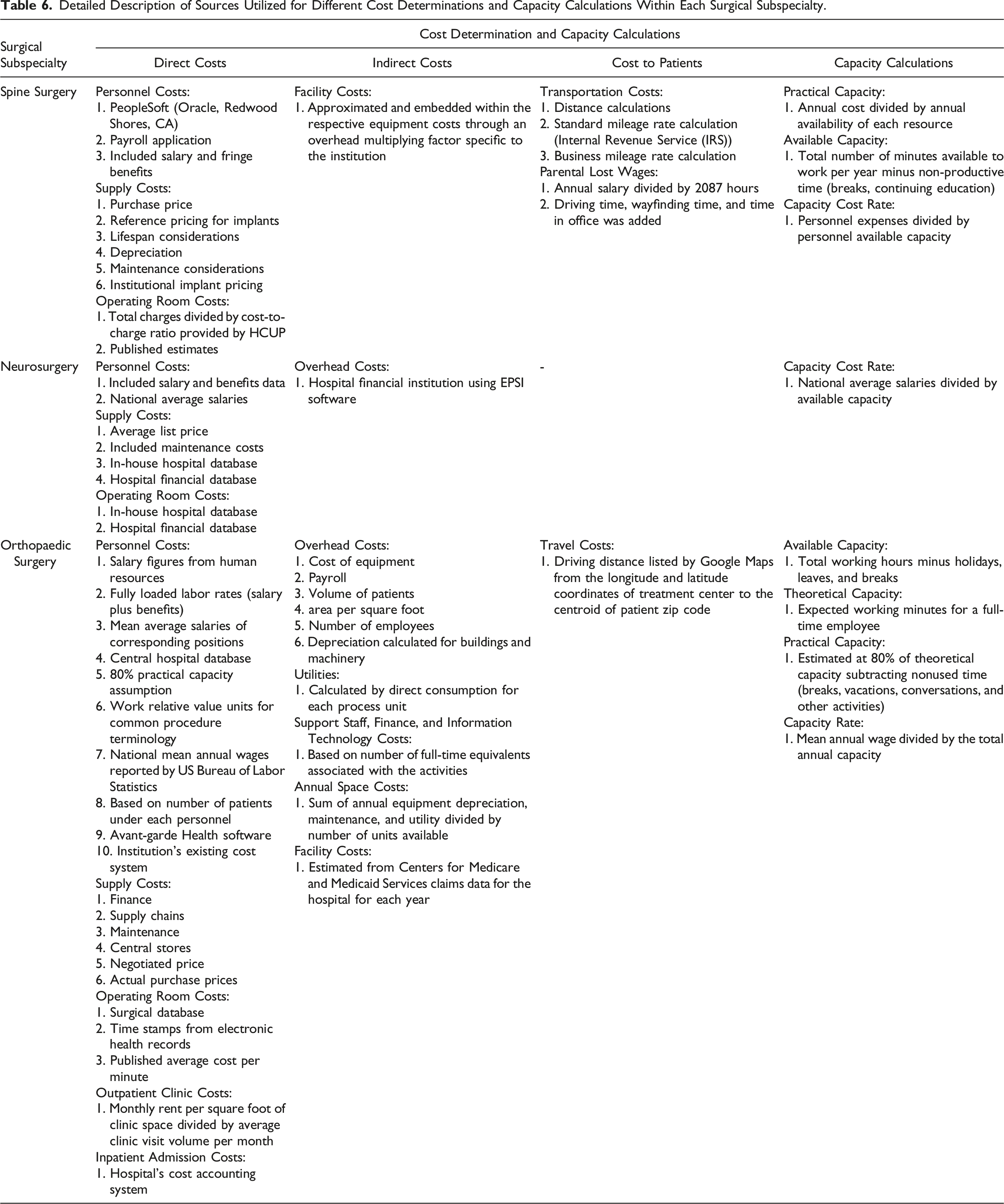

Various sources were used to determine the aforementioned costs accurately. To calculate personnel costs, fully loaded labor rates (salary plus fringe benefits) were used. PeopleSoft (Oracle, Redwood Shores, CA), payroll applications, and national average salaries were some of the common sources. To determine the exact cost of supplies, purchase price, reference pricing, lifespan, depreciation, maintenance, and institutional pricing were some of the determining factors. Overhead and facility costs were calculated by evaluating cost of equipment, volume of patients, area per square foot, number of employees, payroll, and building and machinery depreciation. Utilities - a major component of indirect cost - were determined by calculating direct consumption for each process unit.

Detailed Description of Sources Utilized for Different Cost Determinations and Capacity Calculations Within Each Surgical Subspecialty.

Discussion

The problem of cost in healthcare is one of the most important, yet one of the least defined, issues facing the industry today. At all levels of the healthcare industry, from the individual private practice or hospital to large health systems, there is poor understanding of how to estimate real costs and allocate resources accordingly. Currently, costs within an institution are often aggregated at a department or specialty level, which can allow individual providers who provide great value to go unnoticed while not incentivizing inefficient providers to change their practices. Additionally, resources are often shifted to those with the highest reimbursement, which are often inaccurate measures of the care provided and value delivered. Getting more value out of healthcare means reducing costs and improving outcomes, and to do so we must be able to accurately measure both cost and outcomes. Much work has been done in the way of measuring outcomes, but accurate cost measurement often receives significantly less attention. In this review we organized and scrutinized efforts to measure costs in spine, neurosurgery, and general orthopedic surgery, in an attempt to delineate differing methodologies for strategies such as TDABC. The motivation was to provide a practical roadmap for TDABC that could be standardized and applied widely for spine surgery.

Kaplan and Anderson advocate for the use of the patient as the individual cost unit, following the patient through the system as they navigate care for a particular condition. 6 This addresses many of the aforementioned drawbacks of estimating aggregate cost at a department, specialty, or hospital level. As seen in our review, multiple groups in spine, orthopedics, and neurosurgery have attempted to do this for a multitude of conditions using TDABC. One of the difficulties with TDABC is that there are many different types of resources utilized, these resources are often a part of distinct and independent departments or specialties throughout the hospital, and process mapping can therefore be cumbersome. Moreover, while describing the TDABC processes, the majority of the studies mention a software called Avant-garde Health (Boston, MA). However, the authors do not provide granular details of the software’s methodologies, which makes reproducibility a challenge in the absence of that software. Table 5 lists the cost categorization, and Table 4 lists the methods authors used for process mapping. These costs can mostly be split into direct or indirect costs, with some estimating ancillary costs such as costs to the patient, which may include items such as transportation costs or missed wages.

Direct Costs

Direct cost includes the cost of the surgeon and procedure-specific staff, along with the supplies required for that procedure. Given the complexity and variability of staff involved, many publications separated out personnel costs in their analyses. Table 2 lists the exact personnel considered in each paper’s analysis. To calculate personnel costs, some used national salary data, while others used their specific institutional data. Some groups used average salary for each personnel’s position based on that data, while others used the specific salaries for staff that were obtained from interviews and included the costs of fringe benefits as well. These costs are estimated by performing the CCR calculation mentioned earlier, which estimates the cost per unit time each person spent with the patient. This is then multiplied by the time spent with the patient, which is calculated as part of process mapping.

In addition to staff, direct costs included the costs of supplies: medications, lab tests, non-medication supplies such as drapes and surgical tools, implants, equipment, and imaging studies. The list of each direct cost considered for each paper can be seen in Table 2. The cost for each unit used was usually calculated using purchase price from the hospital database. Khan et al also included support costs in that calculation, which not only includes the purchasing price but also the costs of receiving, storing, sterilizing, and delivering those supplies. 15 This was less common amongst other calculations. In the case of reusable equipment, Kaplan and Anderson advocate for including depreciation or leasing costs of equipment. 6 This varied among cost estimations- Schroeder et al 12 used annual maintenance costs for reusable equipment such as the C-arm, while others did not include this in their calculation. Calculating those support costs and depreciation of equipment require more intensive calculations and are not likely immediately available from a hospital database. This can make estimations of true direct costs difficult to attain, and their omission creates variability among cost calculations.

Indirect Costs

Indirect costs are those associated with general support staff, information technology, insurance, taxes, floor space, facility, and administration. This was most often calculated as a factor of the total hospital or department overhead which could not be assigned to a specific patient activity. For some groups that was a general calculation determined by dividing the total overhead costs by the patient volume.7,8,12,16 Some used this general calculation for costs such as administration and insurance, but space and electricity were calculated based on specific consumption for each process. 15 Akhavan et al calculated these indirect costs based on their consumption for each activity, estimating how many full-time equivalent employees were associated with each activity (from human resources, finance, and IT). 3

The majority of indirect costs in these studies were calculated as a fraction of the general overhead found in most hospital databases. This is what Kaplan et al 6 refer to as the “peanut butter method,” which can be misleading and falsely equalizes these costs among departments and care episodes with significantly different usage rates. While this may not be ideal, these costs are often the most difficult to estimate, as they require personnel from other departments such as finance, human resources, and IT to estimate accurately. This is one of the biggest hurdles in obtaining an accurate cost measurement, but is pivotal for accurate TDABC.

Cost to Patient

One of the less prioritized aspects of total cost was the costs incurred by the patient. This does not refer to a patient’s out of pocket cost for services charged by the hospital, but ancillary costs associated with their episode of care. In our review, only two studies addressed these costs. Meirick et al 17 focused heavily on these costs, both investigating transportation and lost parental wages associated with the treatment of adolescent idiopathic scoliosis. Ganske et al 18 included the cost of travel for parents in the delivery of infant orthopedic care. Both studies that included these costs came from the pediatric literature. These calculations are largely omitted from the literature regarding TDABC and are not mentioned in the original paper by Kaplan et al 6 as they do not directly apply to physicians, practices, or institutions. Though these costs are less important at an institutional level, they become more relevant in determining the true cost to the patient and their family, and may be important when making national policy decisions.

Conclusion

Time-driven activity-based costing has given hospitals and practices a common platform with which to accurately estimate costs of care delivery. These calculations present a multitude of challenges: many different types of resources are often utilized, care is fragmented across silos that are often part of different departments or even organizations, and the delivery of care for one condition is highly variable, taking different paths through a system. Multiple groups have attempted TDABC calculations in spine, orthopedic, and neurosurgery, but there remains variability in how costs are calculated. These calculations can be resource-intensive and time-consuming, making them inaccessible to many institutions. On the other hand, even simplified calculations detailed in this review provide some valuable information. We recommend that institutions embarking on TDABC for spine surgery consider the breadth of methodologies highlighted in this review, to determine which type of calculations are appropriate for their practice and the questions they are attempting to answer.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.