Abstract

With the growing global emphasis on agricultural development models and the need to improve efficiency amid tightening resource constraints, enhancing the TFP (total factor productivity) of agricultural enterprises has become crucial. The emergence of patient capital offers new opportunities in this context. This study investigates the impact of patient capital on agricultural enterprises’ TFP using a sample of 104 Chinese A-share listed agricultural companies from 2013 to 2023. The findings reveal a significant positive correlation between patient capital and agricultural enterprises’ TFP, with this positive relationship following the law of diminishing marginal returns. The conclusions remain robust across a series of tests, including instrumental variable estimation, variable substitution, and lagged-variable approaches. Mechanism analysis demonstrates that governance efficiency and uncertainty perception serve as mediating channels between patient capital and agricultural enterprises’ TFP. This research provides empirical evidence on the micro-level mechanisms by which patient capital supports agricultural transformation and offers valuable insights for refining agricultural financial policies.

Introduction

Globally, agricultural development faces mounting challenges from resource constraints. These include shrinking arable land, rising pressures for ecological protection, and increasing water scarcity. In this context, agricultural enterprises must urgently optimize the allocation of production factors. Labor, capital, and land need better management to achieve comprehensive improvements in production efficiency (Korsgaard et al., 2015). TFP is a critical indicator of production efficiency and overall competitiveness for these enterprises. Therefore, research into its enhancement mechanisms is both theoretically valuable and practically significant.

Academic research on TFP has established a relatively systematic theoretical framework. Notably, Young (2003) demonstrates that market-oriented reform measures—such as improving incentive mechanisms, deepening the division of labor, and optimizing resource allocation—can significantly enhance enterprises’ TFP. This result provides a critical theoretical basis for analyzing the relationship between institutional changes and production efficiency. Building upon these findings, Hsieh & Klenow (2009) further reveal that the introduction of talent and reasonable increases in labor costs also positively influence TFP growth, underscoring the essential role of human capital in productivity improvement. Additionally,Recent research findings indicate that digitalization and environmental regulation can significantly enhance TFP (Wen et al., 2022), and the carbon emissions trading system has also been demonstrated to substantially promote TFP growth (Cheng et al., 2023).

In the agricultural sector, TFP research displays unique disciplinary characteristics. Evenson & Fuglie (2010) empirically demonstrated that strengthening R&D(Research and Development) capabilities is crucial for agricultural TFP growth, highlighting technological innovation as central to development. Bagherzadeh (2012) extended this argument, proposing that sharing R&D results and increasing cross-border technology and knowledge flow can boost agricultural efficiency through knowledge spillover. Hicks et al. (2017), in their examination of production factor allocation, showed that better allocation of agricultural labor is a key strategy to increase production efficiency, offering a theoretical basis for labor force restructuring. Emerging research reveals that the integrated development of rural industries plays a pivotal mediating role in the process of digital inclusive finance empowering agricultural TFP (Jin et al., 2024). Furthermore, a 2025 study by Meicui et al. examining the impact of population aging and agricultural infrastructure construction on agricultural GTFP (green total factor productivity) demonstrates that agricultural infrastructure development significantly enhances agricultural GTFP.

China, as a major agricultural country, has seen its agricultural enterprises achieve notable progress in their development. However, significant gaps remain compared to developed nations in terms of production efficiency and management practices. Due to the inherent characteristics of agricultural production—such as long cycles, high risks, and unstable returns—these enterprises face considerable financing challenges and struggle to secure adequate funding from traditional financial institutions. In particular, short-term credit funds are fundamentally mismatched with the long-term cyclical nature of agricultural production. As a result, this capital shortage further constrains their ability to upgrade equipment and adopt technological innovations, ultimately pushing them into a developmental bottleneck.

The concept of “patient capital,” originating in the United States, offers a new perspective for addressing this dilemma. Patient capital is distinguished by its longer investment horizon and stronger risk-bearing capacity, which enables it to weather economic cycles and supply reliable, long-term financial support. This capital form supports economic system repair by providing stability during downturns, encourages sustainable development through consistent investment, and fosters innovation by allowing time for projects to mature (Kaplan, 2021; Knafo & Dutta, 2016). In mature market economies, vehicles such as sovereign wealth funds, university endowment funds (e.g., the Yale University Alumni Fund), social security funds, and pension funds exemplify this long-term investment philosophy (Thatcher & Vlandas, 2016).

Unlike traditional views on “long-term capital,” which focus on liability duration or equity lock-up periods, “patient capital” is a more nuanced idea. It captures not only the length of funding, but more importantly, the patience of investors. These investors accept short-term fluctuations, take part in governance to build long-term value, and tolerate strategic losses or long profitability cycles.

Patient capital, with its long-term investment horizon and higher risk tolerance, suits the long-term and uncertain nature of agricultural enterprise transformation. It offers stable financial support for agricultural projects with long cycles and high risks, and provides new possibilities to overcome developmental bottlenecks. However, existing research mainly examines patient capital’s impact on industrial enterprises or general corporate innovation, while studies on agricultural enterprises—especially mechanisms enhancing their TFP—remain scarce. Most research also emphasizes macro-level analysis and lacks empirical evidence from the micro-perspective of agricultural enterprises to clarify how patient capital affects TFP. This leads to two research questions: (a) Can patient capital enhance the TFP of agricultural enterprises? (b) If so, through what mechanisms does this occur?

Existing research on patient capital primarily explores its dual economic and social value, emphasizing three key contributions in each dimension. Economically, patient capital alleviates financing constraints for long-cycle projects (David et al., 2008), demonstrates higher tolerance for R&D failures (Ge et al., 2021), and supports the commercialization of technological achievements (Chen et al., 2007).These mechanisms enable enterprises to develop cross-cycle strategic perspectives and enhance sustainable competitiveness. Socially, patient capital contributes by promoting improved environmental performance (Kaplan, 2021), refining governance structures and enhancing corporate reputation, and achieving long-term value appreciation through a deep commitment to social responsibility (Lin et al., 2017).

However, significant gaps remain in existing research: Theoretically, current frameworks have rarely established clear connections between patient capital and the TFP of agricultural enterprises, revealing a notable lack of systematic consideration for agricultural firms. Empirically, there is insufficient evidence from micro-level analyses of agricultural enterprise behaviors, particularly regarding how patient capital enhances productivity through specific pathways during their transformation process—a mechanism that has yet to be systematically elucidated. To address these gaps, this study investigates whether and how patient capital improves the TFP of agricultural enterprises, aiming to provide new insights for the transformation and high-quality development of agricultural firms in China and beyond.

This study makes two main contributions. Theoretically, it constructs an endogenous growth model. This model reveals how patient capital—defined by its long-term orientation and risk tolerance—improves the TFP of agricultural enterprises. Empirically, the study identifies two key pathways. Patient capital promotes TFP by enhancing governance efficiency and reducing the perception of uncertainty.

Theoretical Analysis and Research Hypothesis

Theoretical Analysis

According to modern corporate finance theory, a firm’s capital structure and risk preferences are directly influenced by the stability and duration of its capital (Jensen & Meckling, 2019). Patient capital has a long-term return orientation. It requires agricultural enterprises to possess stronger governance capabilities to ensure operational stability and sustainability. Patient capital investors also establish long-term partnerships with agricultural enterprises. They actively participate in business development and strategic planning. By gaining a deep understanding of enterprise needs and providing necessary resources, they help governance improve. This involvement supports better governance in agricultural enterprises and allows investment decisions to be less constrained by financing risks, increasing project success rates. Value-oriented patient capital focuses on long-term development potential and fundamentals, where effective governance is crucial. Higher governance efficiency enhances management, improves resource allocation, boosts product quality, reduces production costs, and promotes TFP (Harrison et al., 2016).

According to managerial risk aversion theory, when external uncertainty is high, managers tend to exhibit greater caution towards high-risk, long-cycle innovation activities, leading to an overall decline in production efficiency (Yu et al., 2021). Similarly, Panousi et al. (2012) demonstrated that when firms face increased uncertainty, their investment expenditures decrease significantly. However, patient capital helps agricultural enterprise managers reduce their sensitivity to external uncertainty, enabling these enterprises to maintain stable strategic direction and long-term development plans, thereby positively impacting TFP. Moreover, patient capital effectively mitigates the inhibitory effect of uncertainty on decision-making and performance in agricultural enterprises, providing crucial support for enhancing their TFP (Arif-Ur-Rahman & Inaba, 2020).

Theoretical Model

To test the above analysis, this study builds a model of how patient capital affects agricultural enterprises’ TFP through governance efficiency and uncertainty perception, and proposes related hypotheses.

Assuming extreme natural conditions are excluded, agricultural enterprises can achieve optimal output by adjusting inputs of patient capital, traditional capital, and labor. In the short term, the effect of technological changes on productivity is considered negligible, and the sum of elasticity coefficients for all input factors in the production function equals 1.

Where: Y represents agricultural enterprise output; Km and Kn denote patient capital and traditional capital, respectively; L stands for labor input; A indicates the TFP of agricultural enterprises; α is the output elasticity coefficient for patient capital; β is the output elasticity coefficient for traditional capital.

To more accurately characterize the cumulative effects and compound growth process, we establish the following Equation 2:

Where: H represents governance efficiency driven by patient capital; I indicates the level of uncertainty perception faced by agricultural enterprises;

The exponential relationship between governance efficiency and patient capital captures the input-output correlation, while the inverse relationship between uncertainty perception and patient capital highlights how patient capital reduces uncertainty for agricultural enterprises. Accordingly, we specify the relationships between governance efficiency, uncertainty perception level, and patient capital through Equations 3 and 4. Specifically, Equation 3 illustrates the “benefit” characteristic of governance efficiency increasing alongside patient capital. The parameter θ is crucial: when 0 < θ < 1, it shows that improvements in governance efficiency follow the law of diminishing marginal returns, reflecting real-world management practices. Equation 4 demonstrates how uncertainty perception decreases as patient capital rises, emphasizing the role of patient capital as a “risk buffer.”

Where: Φ and σ are constant parameters for governance efficiency and uncertainty perception level, respectively; η represents the adjustment coefficient; θ denotes the elasticity coefficient. The final derived relationship between patient capital and TFP is expressed in Equation (5):

To solve for the optimal patient capital input, we apply a logarithmic transformation to the TFP function (Equation 5) and compute its partial derivative with respect to Km.

Taking the natural logarithm of Equation 5 yields:

To simplify the expression, let

To maximize lnA, we take its first-order partial derivative with respect to Km and set it to zero:

For ease of solution, we perform a variable substitution by letting

Solving Formula 6 for z gives:

Substituting back

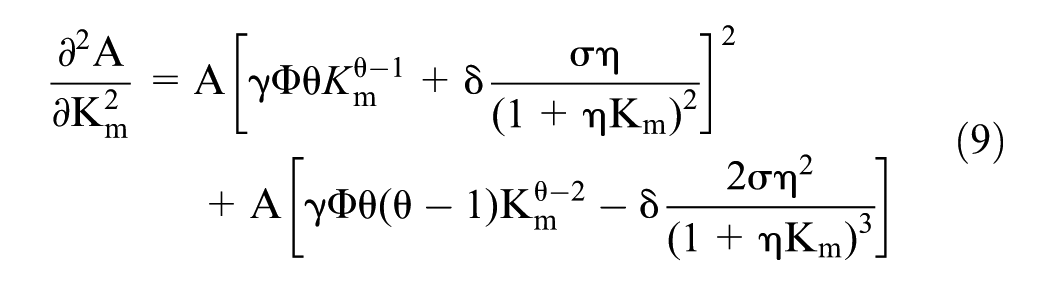

Furthermore, the derivative result of Equation 5 is shown in Formula 8. Based on the economic implications of the parameters, it can be concluded that the

This paper further derives the second-order derivative of

As shown in the first term of Equation 9, this component is always positive. The second term of Equation 9 reveals that its sign critically depends on the governance efficiency elasticity coefficient θ. When 0 < θ < 1,we have

In actual farm business operations, management improvements and better governance are usually limited, and progress typically moves from simple to hard tasks. So, assuming 0 < θ < 1 fits with economic reality and management rules. With this assumption, the negative effect on efficiency (second term) will eventually be stronger than the positive, self-reinforcing effect (first term), resulting in a negative second derivative. Based on the analysis and the model results above, this paper puts forward the following research hypothesis:

Sample and Data Sources

This study examines 104 Chinese agricultural enterprises, utilizing textual data sourced from the annual reports of listed agricultural companies spanning the period 2013 to 2023. Other relevant data were obtained from the Wind database, CSMAR database, and the National Bureau of Statistics. To ensure the reliability of research findings, the sample was processed as follows. First, agricultural enterprises with debt-to-asset ratios exceeding 100% were excluded. Second, specially treated (ST and *ST) samples were removed. A final dataset of 839 observations was obtained. Finally, continuous variables were winsorized at the 1st and 99th percentiles. Additionally, both firm and year fixed effects were controlled for in the regression analyses.

Model Specification

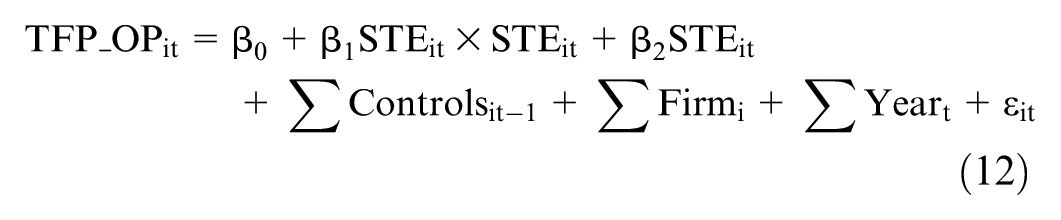

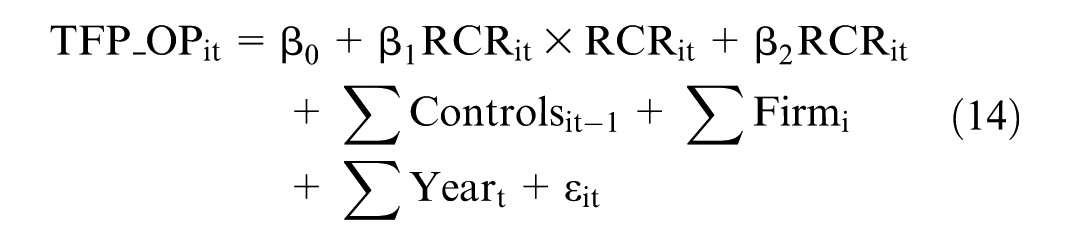

To examine the relationship between patient capital and corporate TFP, we establish Models (11) to (14):

Patient capital consists of stable-type equity (STE) and relationship-based credit rights (RCR). TFP_OPit represents the TFP of agricultural enterprise i in year t, STEit denotes the stable-type equity formed by enterprise i in year t, and RCRit refers to the relationship-based credit rights formed by enterprise i in year t.

Controls represent a set of variables that affect agricultural enterprises’ TFP and vary across i and t. These include return on assets, enterprise growth, board size, CEO-chair duality, largest shareholder ownership ratio, corporate cash flow, and board independence. All control variables were lagged by one period. This lag ensures these variables come before the current period’s TFP, clarifying the direction of causality. It also reflects economic realities, as companies base their investments and decisions on prior financial conditions and governance.

Firm and Year indicate individual fixed effects and time fixed effects, respectively. If the coefficients in Equations 12 and 14 are negative (

Variable Definitions and Measurement

Dependent Variable

Currently, the main approaches for estimating TFP include the OP (Olley-Pakes) method, and the LP (Levinsohn-Petrin) method. This study primarily utilizes the OP algorithm for the following reasons:

Among proxy variable techniques addressing endogeneity, this study selects the OP method over the LP method because the investment variable in the OP approach is typically less reactive to short-term productivity fluctuations than the intermediate inputs (such as raw materials) employed in the LP method. This distinction makes the OP method more consistent with capturing dynamic firm behavior, where investment reflects long-term productivity expectations.

As a robustness check, this study will apply the LP algorithm to cross-validate the main findings and ensure that results are not reliant on a single productivity estimation method.

Independent Variables

The core of stable equity lies in identifying and quantifying equity capital derived from “stable institutional investors” (such as sovereign wealth funds, pension funds, etc.). The essence of relational debt goes beyond the simplistic contractual feature of “long-term borrowing.” It aligns more closely with the concept of “relationship-based financing,” where its “patient” nature is reflected in the creditor’s willingness and capacity to provide sustained support when a company encounters temporary difficulties, fully embodying the principles of “long-term commitment” and “patience.” The investment philosophy, regulatory requirements, and liability structure of these investors inherently drive them toward long-term, stable-value investments, with their “patient” characteristics deeply embedded in their business models.

Therefore, the construction of a patient capital indicator should prioritize metrics within the liabilities and owners’ equity sections that reflect the stability and long-term nature of capital. These metrics help assess whether a company’s funding has characteristics of long-term support. The existing literature also characterizes patient capital using this same logic (Wu et al., 2022). Excluding non-institutional investors, such as individual major shareholders, keeps the concept of measurement valid.

Based on this, the study divides patient capital into stable-type equity and relationship-based credit rights. The exact measurement methods are in Table 1.

Variable Definitions.

Mediating Variables

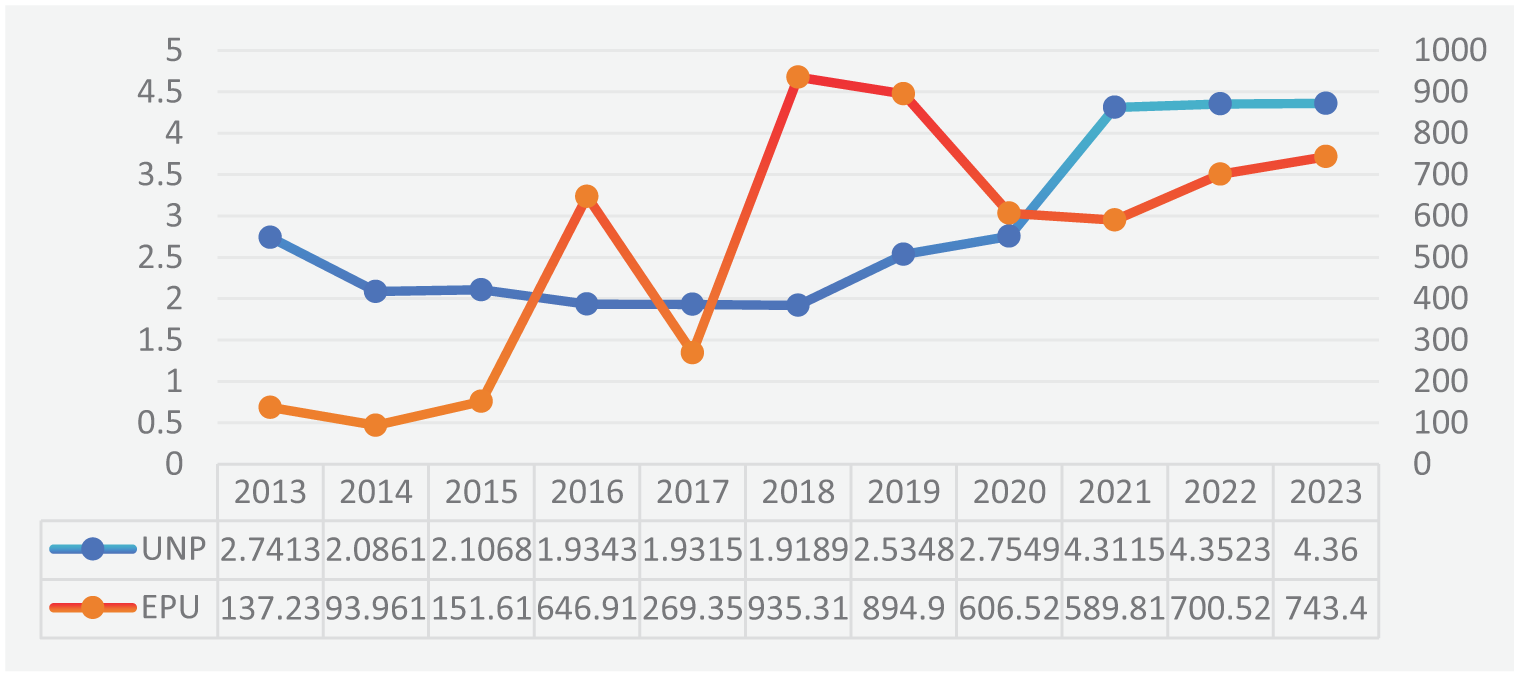

Uncertainty perception (denoted as UNP in this study): While the EPU(Economic Policy Uncertainty) index developed by Baker et al. (2016) has been widely adopted to examine economic policy uncertainty effects, this national-level index provides only a single observation for all firms at any given time point, failing to capture cross-firm heterogeneity in exposure to policy uncertainty. Moreover, applications of the EPU index conventionally assume homogeneous uncertainty perception across firms—an assumption inconsistent with empirical realities.

We follow the methodology of Shen et al. (2012) to measure firm-specific uncertainty (UNP) as follows: (a) For each firm, we compute the standard deviation of its abnormal sales revenue over the previous 5 years. We then divide this value by the firm’s average sales revenue over the same period; this yields the firm’s industry-unadjusted environmental uncertainty. (b) For each year, we calculate the median of the industry-unadjusted uncertainty values among all firms in the same industry, producing an industry-level benchmark. (c) Finally, we calculate the firm’s adjusted uncertainty by dividing its unadjusted uncertainty by the industry median.

We computed annual averages of the UNP indicator and the monthly EPU index for agricultural enterprises and used line charts for visual analysis. As shown in Figure 1, the two measures have a relatively high correlation (correlation coefficient = 0.573), but also significant differences. For example, during 2015 to 2018, the EPU index exhibited fluctuating oscillations, while the UNP indicator showed a gradual downward trend. Then, from 2020 to 2021, the EPU index declined, while the UNP indicator had a substantial upward surge. In subsequent years, the trends of the two measures converged. These findings indicate that external uncertainty shocks and firms’ own perceptions of uncertainty are not fully synchronized. Therefore, it is necessary to incorporate firms’ subjective perceptions when examining the impact of uncertainty on agricultural enterprises, which preliminarily validates the unique value of UNP as an indicator for measuring firm-level uncertainty. Additionally, this study uses the ratio of operating revenue to management expenses to assess the governance efficiency (GOE) of agricultural enterprises.

UNP and EPU.

Benchmark Regression

The regression results in Table 2, columns (1) to (2) and (4) to (5), show that all coefficients of patient capital (STE, RCR) are positive at the 5% significance level. This indicates that patient capital can effectively enhance TFP in agricultural enterprises. When quadratic terms of patient capital (STE, RCR) are introduced in columns (3) and (6), the coefficients of STE2 and RCR2 are negative at the 5% significance level. This shows that the productivity-enhancing effect of patient capital follows diminishing marginal returns, validating Hypothesis 1.

Patient Capital (STE, RCR) and Agricultural Enterprises’ TFP.

Source. Author’s own calculation using STATA – statistical analysis app (Hereinafter the same).

Note. N: Sample Size (applies to all tables). Standard errors in parentheses.

p < .1, **p < .05, ***p < .01 (applies to all tables).

The economic explanation for this finding is that when the investment of patient capital exceeds a firm’s current optimal absorption capacity, it may trigger a series of negative effects, leading to diminishing marginal contributions.

In the early stages of development, funds are preferentially allocated to the most promising core projects, such as improving high-yield farmland, establishing advanced processing lines, or introducing high-quality seed sources. However, once these high-value projects have been sufficiently invested in, additional capital is inevitably directed toward newly cultivated land with limited soil potential, diversification into non-core businesses with longer payback periods (such as agritourism), or scaled expansion that leads to efficiency losses due to an expanded management scope, thereby reducing overall capital efficiency.

Columns (1) to (2) correspond to Model (11), with TFP_OP as the dependent variable and STE as the explanatory variable, with Column (2) including control variables. Column (3) corresponds to Model (12), with STE2 as the explanatory variable. Columns (4) to (5) correspond to Model (13), with RCR as the explanatory variable, with Column (5) including control variables. Column (6) corresponds to Model (14), with RCR2 as the explanatory variable. All regressions use the same set of controls and include two-way fixed effects.

Robustness Tests

Firms in the same industry share characteristics in financing environments, business models, and investor preferences. As a result, a firm’s patient capital level is often correlated with the industry mean or median patient capital. Industry trends are unlikely to link directly to unique, unobserved factors affecting a firm’s TFP, such as managerial abilities or specific technological advances. This study, therefore, uses industry averages and medians of stable-type equity and relationship-based credit rights as instrumental variables, applying two-stage least squares (2SLS) estimation.

Specifically, Columns (1) to (4) in Table 3 present 2SLS results using industry-mean and industry-median STE as IVs. Columns (5) to (8) report 2SLS results using industry-mean and industry-median RCR as IVs. The results demonstrate that patient capital (STE, RCR) maintains statistically significant positive effects on agricultural TFP across varying significance levels, confirming the robustness of baseline findings. Furthermore, F-tests validate the appropriateness of the selected IVs.

Robustness Tests Using Instrumental Variables.

The benchmark regression primarily employed the OP method to measure firms’ TFP, whereas this section utilizes the LP method for measurement. Regression analysis was conducted while maintaining the original model specifications, with results presented in columns (1) and (2) of Table 4. The results indicate that patient capital (STE, RCR) shows positive correlations with agricultural enterprises’ TFP (TFP_LP) across different significance levels, demonstrating the strong robustness of the benchmark regression findings.

Robustness Tests With Variable Replacement and Lagged Variables.

Note. Columns (1) and (2) correspond to Model (11) with TFP_LP as the dependent variable, using TFP measured by the LP method. Column (1) uses STE and column (2) uses RCR as explanatory variables. Columns (3) and (4) correspond to Model (13) with TFP_OP as the dependent variable, with column (3) using L1_STE (one-period lag of STE) and column (4) using L1_RCR (one-period lag of RCR) as explanatory variables. All regressions control for the same set of control variables and include two-way fixed effects.

This study adds one-period lagged patient capital variables (L1_STE and L1_RCR) into the regression. Results in columns (3) and (4) of Table 4 show that these lagged variables have positive correlations with agricultural TFP at the 10% significance level. This suggests patient capital boosts agricultural enterprise productivity in the first year after infusion, further supporting the robustness of the benchmark regression results.

Mechanism Analysis

To examine how patient capital affects the TFP of agricultural enterprises, this study uses the Sobel test for further analysis of the regression results. This approach enhances the rigor and reliability of the mechanism test. The model is shown in Equation 15. M represents the mediating variables, which include governance efficiency and the level of perceived operational uncertainty. PAC stands for patient capital and includes stable-type equity and relationship-based credit rights. The remaining variables are consistent with the baseline model.

The improvement in corporate governance efficiency enables agricultural enterprises to allocate resources more effectively, thereby concentrating limited resources on the most valuable agricultural production activities. Furthermore, enhanced governance efficiency promotes standardized operations, strengthens organizational coordination, and refines management practices, ultimately contributing to the increase in TFP. Meanwhile, patient capital, due to its focus on long-term returns, has a stronger willingness and capacity to engage in corporate governance and provide necessary resource support to agricultural enterprises. The professional management and resource investments from patient capital further reduce agricultural enterprises’ sensitivity to external uncertainties—such as natural disasters and market fluctuations—and internal uncertainties like organizational restructuring, leading to more stable decision-making. These relationships are further illustrated by the empirical results: as shown in Columns (1) and (4) of Table 5, patient capital (STE, RCR) significantly enhances the governance efficiency of agricultural enterprises. In addition, Columns (2) and (5) indicate that improved governance efficiency effectively boosts agricultural enterprises’ TFP, thereby validating Hypothesis 2.

Governance Efficiency (GOE), Patient Capital (STE, RCR), and Total Factor Productivity.

Note. Columns (1) and (4) present Model (15), using STE or RCR, respectively, as the explanatory variable for GOE (mediator). Columns (2) and (5) show Model (16), assessing GOE’s effect on TFP. Columns (3) and (6) display Model (17), where STE and GOE, or RCR and GOE, simultaneously affect TFP. All regressions include the same controls and two-way fixed effects.

Similarly, the results in Columns (1) and (4) of Table 6 demonstrate that patient capital (STE, RCR) significantly mitigates uncertainty perception. Meanwhile, Columns (2) and (5) reveal that uncertainty perception exerts a significantly negative impact on agricultural enterprises’ TFP, thereby validating Hypothesis 3.

Uncertainty Perception (UNP), Patient Capital (STE, RCR), and Total Factor Productivity.

Note. Columns (1) and (4) present Model (15), using STE or RCR, respectively, as the explanatory variable for UNP (mediator). Columns (2) and (5) show Model (16), assessing UNP’s effect on TFP. Columns (3) and (6) display Model (17), where STE and UNP, or RCR and UNP, simultaneously affect TFP. All regressions include the same controls and two-way fixed effects.

Furthermore, the Sobel test results indicate that both governance efficiency and uncertainty perception play partial mediating roles in the relationship between patient capital (STE, RCR) and agricultural enterprises’ TFP. In conclusion, patient capital enhances agricultural enterprises’ TFP not only by improving governance efficiency but also by reducing uncertainty perception, thus confirming Hypotheses H2 and H3.

Conclusion and Discussion

Research Findings

This study uses firm-level data to examine the impact of patient capital on the TFP of Chinese agricultural enterprises. The main findings are:

Core Impact: Patient capital, as a long-term oriented financial resource characterized by its patient nature. It significantly boosts TFP in agricultural enterprises through two main ways: by improving governance efficiency and by reducing operational uncertainty.

Nonlinear Characteristics: The positive effect of patient capital on productivity gets smaller as more capital is added. This means there is an ideal amount of investment. Investing too much can reduce how efficiently resources are used and lower productivity.

Mechanism Validation: The mediation effect model shows that better governance is the main internal mechanism by which patient capital works. Lowering firms’ uncertainty about markets and policies is a key external way.

Theoretical Implications and International Comparability

The findings of this study hold significant theoretical relevance for understanding micro-level mechanisms of financial support in agricultural development. This paper highlights the critical role of capital’s “patient” attributes—namely, investment horizon and risk tolerance. These characteristics help facilitate the transformation and upgrading of agriculture, a sector known for long cycles and high risks. This insight bridges corporate finance theory with agricultural productivity research and deepens our understanding of how heterogeneous capital impacts the real economy.

From an international comparative perspective, China’s agricultural context is rooted in smallholder farming while undergoing modernization. This makes these findings especially relevant for developing countries. Agricultural sectors in developed economies tend to be highly capitalized and technologically advanced. In contrast, the Chinese case shows that in transitional economies, patient capital mainly helps enterprises overcome the “scale threshold” and “risk threshold” in early capital accumulation. It includes facilitating fixed asset investments, such as building standardized breeding facilities and buying large-scale machinery. This finding suggests that developing countries should prioritize the long-term nature and stability of capital when creating agricultural financial policies.

Policy Implications: Specific Recommendations Based on China’s Agricultural Context

Building on the findings above and the key realities of China’s agriculture—large population, small-scale farmers, and a crucial period of scaling up and modernization—this study makes the following policy recommendations:

Recommendations for the Government:

Implement “Tiered” Long-Term Investment Tax Incentives: To counteract diminishing marginal returns on capital, it is recommended to design progressively increasing corporate income tax reductions for long-term equity investment funds or insurance capital directed toward agricultural enterprises, based on their holding period (for example, funds invested for more than 3 years or more than 5 years would receive greater reductions). This approach, moving away from one-size-fits-all universal subsidies, would precisely incentivize capital that is committed for an extended period and can tolerate temporary fluctuations, often referred to as “truly patient capital.”

Establish a National “Agricultural Industry Uncertainty Buffer Fund”: Addressing the uncertainty mechanism identified in the study, a dedicated fund should be established, led by central or provincial finances. This fund would provide premium subsidies for income insurance, which refers to financial products that protect eligible enterprises against income losses due to fluctuations in major agricultural product prices. Additionally, it would create a “Policy-based Medium- and Long-Term Loan Risk Compensation Pool” targeted at agricultural enterprises, directly alleviating concerns for both financial institutions and the enterprises themselves by partially covering possible loan losses.

Recommendations for Financial Institutions:

Develop loans that match farm production cycles. Encourage banks and rural credit unions to design medium- to long-term loans (3–5 years) for specific types of farming, such as pig raising, dairy cows, and growing fruit trees. These loans let farmers repay in line with their full production and sales cycle, helping fix problems with traditional short-term loans.

Create financial products linked to good management. Farms and businesses with clear financial records and strong management, who use digital tools, are offered lower loan interest rates or bigger loans. This targets financial help to those proven to boost productivity.

Recommendations for Agricultural Enterprises:

Enterprises should prioritize capital investments for “Technology-Governance Dual Upgrades.” Long-term capital should focus on two areas. The first is advanced production technology equipment that directly boosts productivity, such as water-saving irrigation facilities and livestock waste recycling systems. The second is internal governance improvements. This includes introducing professional managers and deploying ERP management systems. These steps directly address the two mechanisms validated in this study.

Enterprises should proactively disclose information to build “Trustworthy Assets.” Actively compile and publish Agricultural Corporate Social Responsibility and Sustainable Development Reports. Clearly disclose practices on environmental protection, food safety, and employee welfare. This helps present a long-term, stable, and responsible image in the capital market. It positions the enterprise as an attractive “target” for patient capital.

Research Limitations and Future Outlook

This study offers theoretical and empirical evidence on how patient capital affects agricultural enterprises’ TFP, yet limitations remain. The sample consists solely of A-share listed agricultural firms in China, which means the generalizability to non-listed agricultural enterprises requires further verification. Moreover, contextual factors such as regional disparities and the enterprise life cycle have not been thoroughly examined for their moderating effects.

Future research will aim to build a more comprehensive, multi-dimensional, and dynamic analytical framework for examining the relationship between patient capital and agricultural enterprises’ TFP. Our planned next steps include: expanding the sample scope, leveraging exogenous policy shocks to create natural experiments, and incorporating moderating variables for contextual analysis.

Footnotes

Acknowledgements

The author, Keming Zhou, gratefully acknowledges the support provided by the Key Projects of Humanities and Social Sciences Research of West Anhui University (WXSK202308).

Author Contributions

Writing—original draft, Keming Zhoug; writing—review and editing, Keming Zhou and Qian Huang. All authors have read and agreed to the published version of the manuscript.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Key Projects of Humanities and Social Sciences Research of West Anhui University (Grant No. WXSK202308).

Declaration of Conflicting Interests

The authors declared the following potential conflicts of interest with respect to the research, authorship, and/or publication of this article: This humble work is respectfully dedicated to the hardworking agricultural practitioners across China and World, whose tireless efforts and innovative spirit have been a constant source of inspiration for our research into improving agricultural productivity.

Data Availability Statement

The data supporting this study’s findings are available from the corresponding author* upon reasonable request.