Abstract

Combining strategic balance theory and enterprise behavior theory, this study explores the relationship between the performance expectation gap (i.e., the actual performance of an enterprise is lower than the expected level) and strategic distinctiveness (referring to the degree to which an enterprise’s strategic choices deviate from industry norms). Strategic distinctiveness is a key strategic behavior that reflects an enterprise’s willingness to pursue unique resource allocation and competitive positioning, which may enhance differentiation advantages but also bring legitimacy risks. On the basis of the data of all A-share listed companies in China from 2005 to 2019, the fixed effect model was determined as the benchmark analysis method through the Hausman test. This study reveals that when an enterprise’s actual performance is lower than the historical expected level, to gain competitive advantages and reverse the unfavorable situation, the enterprise tends to increase strategic distinctiveness; however, when the performance gap further expands and threatens the enterprise’s survival, owing to concerns about institutional legitimacy, the enterprise is more inclined to strategic convergence, thus resulting in an inverted U-shaped relationship between the performance expectation gap and strategic distinctiveness. Further analysis reveals that economic policy uncertainty weakens this inverted U-shaped relationship, whereas nonstate-owned enterprises (compared with state-owned enterprises) strengthen this relationship. This study expands the relevant literature on the antecedents of strategic distinctiveness, enriches strategic balance theory and enterprise behavior theory, and provides practical implications for the strategic choices of enterprises in the state of performance expectation gap.

Keywords

Introduction

Under the trend of economic globalization, the external environment is highly complex and volatile, and enterprises face major challenges in strategic choices and even survival. To effectively cope with dynamic changes in the external environment and seize new opportunities, enterprises must balance convergence and divergence: on the one hand, they must follow industry mainstream trends and regulatory rules to obtain institutional legitimacy (Meyer & Rowan, 1977; Tang et al., 2011); on the other hand, they must deviate from industry conventions to build a competitive advantage and mitigate external shocks (Gao et al., 2023). Therefore, how to choose between convergence under legitimacy pressure and differentiation under competitive pressure becomes an important issue faced by enterprises.

Strategic difference is regarded as a strategic behavior in which an organization deviates from established industry standards or practices to gain competitive advantage (Li et al., 2024; Tang et al., 2011), reflecting the degree to which the organization’s strategy and allocation of key strategic resources deviate from the industry average (Geletkanycz & Hambrick, 1997). Existing studies explore mainly the antecedents of strategic difference from perspectives such as the external institutional environment, internal governance structure, and executive characteristics. For example, Audia et al. (2000) reported that strategic inertia after dramatic environmental change leads to performance decline; Chen et al. (2023) reported that past success easily triggers managerial complacency and inhibits strategic change; Pan et al. (2019) reported a nonlinear relationship between the proportion of female executives and strategic difference; and Tang et al. (2011) reported that CEOs with greater power are more inclined to deviate from industry norms. However, few studies have focused on the outcomes of organization’s own behavior, especially the impact of performance feedback on strategic difference.

The theory of firm behavior lays the foundation for in-depth research on the degree of strategic difference among firms, and within it, performance feedback theory emphasizes that firms adjust their behavior and strategy on the basis of the gap between performance and the expected level (Cyert & March, 1963). In practice, decision-makers set a “minimum satisfactory output,” that is, the expected level, as the decision-making benchmark, defining states below this level as “losses” and those above as “gains,” and accordingly adopt different decisions, which is largely consistent with the assumptions of prospect theory (Kahneman et al., 1979). In existing research, many scholars have focused on revealing how performance feedback gaps affect organizational change, particularly innovation-related strategic behaviors that involve typical risk-tradeoff characteristics (Su et al., 2023), but no consensus has been reached, possibly because the relationship between performance feedback and firm behavior is nonlinear. Furthermore, the persistence of performance gaps amplifies pressure and urgency through the time dimension, thereby influencing decision-making (Zhao et al., 2024). Threat-rigidity theory posits that strategic adjustments in times of distress may exacerbate bankruptcy risk (Staw et al., 1981). The inconsistency in existing research findings may stem from the fact that prior studies mostly adopted a single expected target as the reference point. However, as performance gaps continue to widen, enterprises’ decision-making reference points change dynamically. Under different performance gap states dominated by different decision-making reference points, the degree of strategic difference adopted by enterprises may vary.

On this basis, this article integrates the theory of firm behavior and the theory of strategic balance to examine whether enterprises tend to adopt convergent or differentiated strategies under performance gaps. In addition, owing to dramatic changes in the external environment and the heterogeneity of enterprise ownership, enterprises exhibit different strategic choice preferences. This article further explores two important boundary conditions: the impact of economic policy uncertainty and the nature of ownership on the relationship between performance expectation gaps and strategic difference.

The contributions of this article are as follows: First, it integrates the theory of firm behavior and the theory of strategic balance to explain enterprises’ strategic difference behavior, focusing on the driving role of performance expectation gaps in strategic difference, thereby providing an important theoretical perspective for a comprehensive and in-depth understanding of the antecedents of strategic difference. Second, it introduces the aspiration reference point and the survival reference point into the analytical model of the relationship between performance expectation gaps and the degree of strategic difference, revealing the nonlinear variation in strategic difference across different performance gap ranges and offering a basis for decision-making to resolve business dilemmas. Third, grounded in the Chinese context, the degree of strategic difference is largely influenced by the institutional environment and enterprise ownership. This study examines the moderating effects of economic policy uncertainty and ownership, further extending and deepening the analysis of boundary conditions in the relationship between performance expectation gaps and the degree of strategic difference.

Theoretical Analysis and Hypotheses Development

Strategic balance theory holds that there is tension between institutional legitimacy and competitive pressure and that an appropriate level of strategic differentiation can improve enterprise performance more than highly differentiated or highly convergent strategies can (Salimi et al., 2026; Zhang et al., 2025). In general, enterprises tend to adopt conventional strategies that converge with the industry to ensure enterprise performance stability (Lee et al., 2024). However, enterprises may also choose differentiated strategies that deviate from the conventional industry model to enhance their core competitive advantages and prevent competitors from copying or imitating them. How to balance the pressure of institutional legitimacy and competitive pressure and choose an appropriate level of strategic difference is an urgent problem. Additionally, according to the theory of corporate behavior, enterprises use their own performance feedback to promote the development of strategic decisions, which helps them achieve maximum enterprise profit. Therefore, this article combines strategic balance theory with corporate behavior theory to explore how enterprises make strategic choices under performance expectation gaps, thereby achieving a balance between competitive benefits and legitimacy costs.

Performance Below the Aspiration Level and Strategic Deviance

The theory of firm behavior suggests that a firm’s strategic decisions are a response to the gap between actual performance and expected goals. When actual performance falls below the expected level, the firm enters a “problemistic search” state, seeking changes to reverse the unfavorable situation (Kahneman et al., 1979). However, the nature and intensity of this search behavior are not constant; they depend on the severity of the performance gap, or the “threat” level perceived by decision-makers (Staw et al., 1981). This study posits that the impact of the performance expectation gap on strategic diversity is not a simple linear relationship but a dynamic process dominated by different decision-making reference points, thus presenting an inverted U-shaped curve that first increases but then decreases.

First, when actual performance is slightly below the expected level (i.e., when the performance expectation gap is small), decision-makers tend to view this poor performance as caused by temporary or local factors (He et al., 2017). At this point, the firm’s survival is not directly threatened, and decision-makers are more concerned with how to quickly return to the expected level. Following industry conventional strategies is a relatively low-risk choice, as it ensures operational stability and institutional legitimacy, avoiding additional risks from hasty changes. Therefore, in the small performance gap range, firms tend to converge in strategy, with a low degree of strategic diversity.

Second, as the gap in performance expectations increases, the competitive pressure and market threats faced by the firm intensify (Lian et al., 2019). Decision-makers realize that incremental improvements are insufficient to bridge the performance gap and must take more radical measures. In accordance with the logic of “necessity breeds innovation” (He et al., 2017), firms will conduct a broader search for problems, daring to break conventions and implement differentiated strategies that deviate from industry norms to seek breakthroughs and develop new competitive advantages (Alipour et al., 2025). Strategic convergence cannot make them stand out in competition, whereas differentiated strategies may result in excess returns. Therefore, as the gap widens, the motivation and ability of firms to implement strategic diversity increase, indicating a positive correlation.

However, when the performance gap further deteriorates, reaching or threatening the firm’s “survival reference point,” the priority of decision-makers shifts completely from “gain-seeking” to “loss-aversion” (March & Shapira, 1987). In this extreme predicament, any unproven, high-risk differentiated strategy that has not been widely validated by the industry may accelerate the firm’s failure by consuming already scarce resources. At this point, decision-makers exhibit a “threat-rigidity” response, narrowing the range of strategic choices and returning to mainstream industry strategies to obtain the most basic institutional legitimacy and support from stakeholders (such as the government and suppliers) and striving to survive first (Staw et al., 1981). Therefore, in the large performance gap range, to avoid the risk of bankruptcy, firms reduce strategic diversity and turn to strategic convergence.

In summary, there exists a turning point in the impact of the performance expectation gap on strategic distinctiveness: before the turning point (where the expectation reference point is dominant), an increase in the gap prompts enterprises to increase strategic distinctiveness in pursuit of breakthroughs; after the turning point (where the survival reference point is dominant), an increase in the gap compels enterprises to reduce strategic distinctiveness to ensure survival. On this basis, we propose Hypothesis 1:

The Moderating Effect of Economic Policy Uncertainty

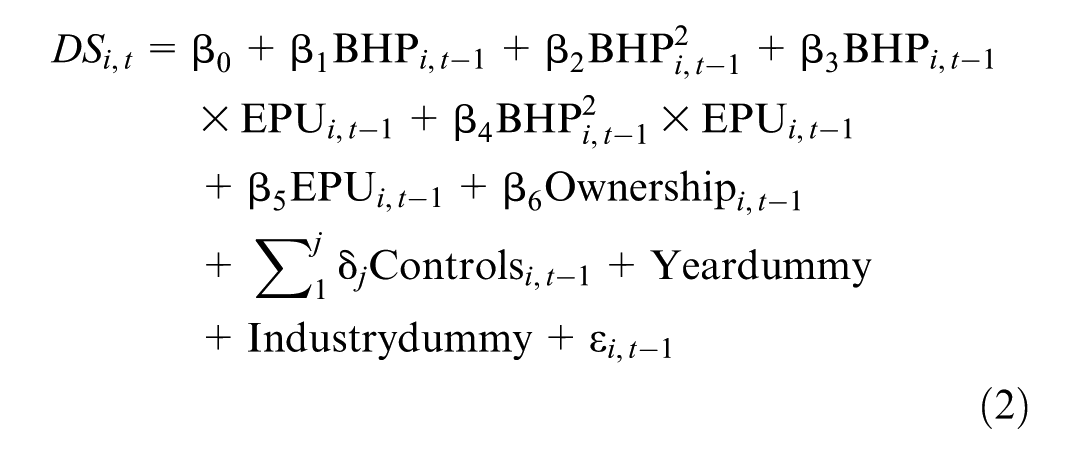

Economic policy uncertainty refers to the inability of economic agents to accurately determine whether, when, and how the government will change its current policies, making it difficult to form stable policy expectations (Ali et al., 2024). As a developing country with a long-term economic transition period, China’s economic policy uncertainty has made the business environment more complex, which in turn has affected the strategic decisions of enterprises to some extent. Although deviations from industry-standard strategies can bring competitive advantages to enterprises, they may also face institutional legitimacy pressure. In particular, when economic policy uncertainty is high and enterprises are experiencing performance expectation gaps, the risk of implementing unconventional strategies is further magnified (Lian et al., 2019). Additionally, under conditions of high economic policy uncertainty, owing to self-reinforcement effects, decision-makers tend to attribute performance gaps to external environmental factors (Blagoeva et al., 2020). Therefore, under conditions of high economic policy uncertainty, the positive correlation between performance below the aspiration level and strategic deviance weakens.

The further expansion of performance gaps increases competitive pressure and survival threats for enterprises. At this point, decision-makers realize that the current performance difficulties may not be caused by external environmental factors but rather by systematic problems within the company (Li et al., 2018), leading enterprises to seek long-term solutions and develop competitive advantages. Seeking strategic differences is an appropriate choice. When facing economic policy uncertainty, decision-makers who hold a positive attitude are more conducive to the long-term development of the company. By gaining insight into the opportunities contained in future uncertainties, companies can actively identify these opportunities and reap benefits from uncertain economic policies (Lahiri et al., 2025). Therefore, when survival reference points are reached, economic policy uncertainty weakens the negative correlation between performance below the aspiration level and strategic deviance.

The Moderating Effect of Property Rights

State-owned enterprises (SOEs) and non-SOEs are two types of enterprises with different natures, and they have different resource endowments (Ge et al., 2020). The gap between actual performance and expected levels typically leads to a preference for firms to deviate from industry-standard strategies (Ali et al., 2024). However, when SOEs face performance difficulties, the government provides timely financial assistance and tax incentives (Kong et al., 2023). Non-SOEs often have a long-term business philosophy. To ensure that business objectives can be achieved and external resource support can be sought to gain a competitive advantage in the domestic market, decision-makers are more willing to engage in differentiated strategies, especially when the actual performance of the enterprise falls below the set target (Arregle et al., 2024). Therefore, the nature of property rights among non-SOEs strengthens the need to increase strategic heterogeneity to gain a competitive advantage under performance expectation gaps.

Furthermore, when performance gaps continue to worsen and threaten enterprise survival, non-SOEs strengthen the negative impact of performance below the aspiration level on strategic deviance. This is due mainly to the following reasons: On the one hand, facing bankruptcy indicates that enterprises have severely inadequate resources and that their institutional legitimacy is questioned by stakeholders. Strategic heterogeneity requires a large amount of human, material, and financial resources, which not only cannot reverse the survival threat but can also lead to more serious difficulties (He et al., 2017). At this time, non-SOEs show greater strategic convergence in strategic behavior; on the other hand, SOEs often have natural links with the government, resulting in significant advantages in resource endowments (Liu et al., 2022). Additionally, managers of SOEs are often directly appointed by the government and lack professional knowledge of enterprise management. Once enterprises invest in strategic change, they will not easily make change.

Research Design

Sample and Data Selection

In this article, all companies listed on the Shanghai and Shenzhen A-share markets from 2005 to 2019 are selected as the basic sample. To ensure the rationality of sample selection, the data were processed according to the following principles: (1) removing financial listed companies; (2) removing ST, *ST, and PT enterprise samples; (3) removing enterprise samples with asset-liability ratios exceeding 100%; and (4) removing enterprises in industries with fewer than five enterprises according to the three-digit code classification. In addition, to avoid the impact of outliers on the empirical test results, the main continuous variables were trimmed at the 1% level. The sample data are all from the CSMAR database.

Measurement of the Variables

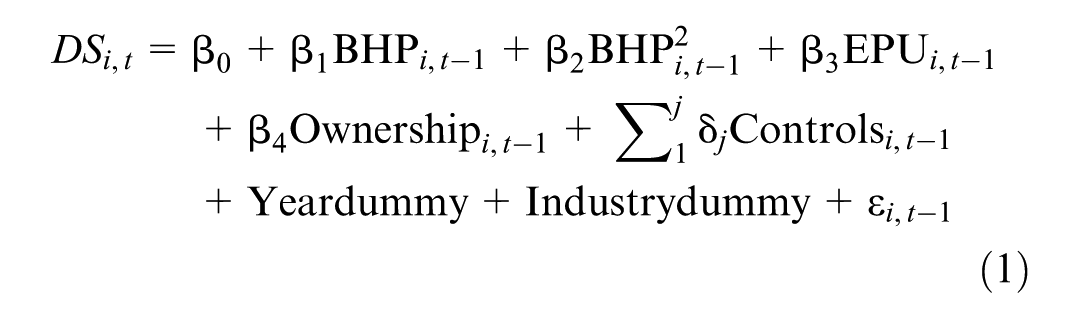

Strategic Deviance (DS). This indicator reflects the degree to which a company’s strategy deviates from the mainstream trends in the industry. Drawing on the practices of Tang et al. (2011), this article selects six-dimensional indicators, including R&D investment, market investment, capital intensity, corporate financial leverage, the degree of fixed asset renewal, and management expenses, to measure strategic deviance. The average value of the above six-dimensional data is calculated to measure the company’s strategic deviance in the average year, denoted as DS. The larger the DS value is, the greater the degree to which the company’s strategy deviates from the conventional industry model.

Performance below aspiration level (BHP). This is measured by the difference between actual performance and expected levels. That is, Pi,t − 1 − HAi,t − 1. Where Pi,t − 1 refers to the actual performance of the company, measured by return on equity (ROE), and HAi,t − 1 refers to the weighted combination of the company’s actual performance in period t − 2 (weighted at .6) and expected performance in period t − 2 (weighted at .4). Therefore, the performance expectation gap (Pi,t − 1 − HAi,t − 1) represents the difference between actual performance (Pi,t − 1) and expected targets (HAi,t − 1). Furthermore, multiplying I1 by the performance expectation gap variable (Pi,t − 1 − HAi,t − 1) results in a truncated performance expectation gap variable: if the gap is below expectations (Pi,t − 1 − HAi,t − 1 < 0), it is labeled “performance below the aspiration level” (BHP); if the gap is above expectations (1 − I1) (Pi,t − 1 − HAi,t − 1) > 0, it is labeled “performance above the aspiration level” (AHP). For easier analysis and understanding, this paper takes the absolute value of performance below the aspiration level. The larger this absolute value is, the lower the actual performance is compared to the expected levels.

Economic policy uncertainty (EPU). This is measured using the economic policy uncertainty index constructed by Baker et al. (2016). Since this article’s sample data are annual, we adopt the arithmetic mean method to convert monthly data into annual data.

Property nature (ownership). Referencing the practices of Zhou (2013), this article categorizes the samples into state-owned enterprises and nonstate-owned enterprises on the basis of the nature of their actual controllers. When the actual controller of a company is an individual, family, or foreign-funded company, this paper considers such companies as nonstate-owned enterprises and assigns ownership a value of 1; otherwise, it is 0.

In addition, other factors that may affect a company’s strategic deviance, including enterprise age (Age), enterprise size (Size), the leverage ratio (Debt), management shareholding (Cshr), the separation rate of the rights and obligations of shareholders (Sep), the equity multiplier (Em), the cash ratio (Cash), and performance expectation surplus (AHP), are selected as control variables. Moreover, this article also controls for factors such as year dummies (Yeardummy) and industry dummies (Industrydummy).

The meanings and measurement methods of the major variables are summarized in Table 1.

Variable Definitions.

Regression Model

Given that the strategic deviance of enterprises is often determined by performance feedback in the previous period, the explanatory variables are lagged by one period. Additionally, to avoid a series of problems such as heteroscedasticity, time series correlation, and cross-sectional correlation that may exist in nonbalanced panel data, the Driscoll and Kraay (1998) method is used to estimate the panel data model.

On the basis of research Hypothesis 1 of this article, which posits an inverted U-shaped relationship between performance below the aspiration level and the enterprise’s strategic deviance, regression Equation 1 is established.

To test the moderating effects of economic policy uncertainty and the nature of property rights, based on Equation 1, we add the interaction terms of economic policy uncertainty, the nature of property rights, performance below the aspiration level and its squared value to establish Equations 2 and 3 as follows:

Results

Descriptive Statistics and Correlation Analysis

As shown in Table 2, the mean of strategic deviance (DS) is .6094, and the standard deviation is .3217, with a range from .1849 to 1.8505, indicating that the overall distribution is reasonable and that there are significant differences in the strategic deviance of different enterprises at the industry level. The mean performance below the aspiration level (BHP) is .0448, and the standard deviation is .1374, indicating that the average gap between actual performance and historical expectations is .0448. The mean economic policy uncertainty (EPU) is 1.5458, and the standard deviation is .8747. The mean property rights nature (Ownership) is .5053, and the standard deviation is .5000.

Descriptive Statistics of the Variables.

Table 3 presents the correlation analysis of the main variables. The results indicate that the correlation coefficient between performance below the aspiration level (BHP) and strategic deviance (DS) is positive. Economic policy uncertainty (EPU) and the nature of property rights (Ownership) are positively correlated with strategic deviance (DS), but the relationships between these variables still need to be further explored through regression analysis. Additionally, the correlation coefficients between the main explanatory variables are all less than .5, indicating that there is no serious multicollinearity problem.

Correlation Analysis.

To provide a clear overview of the basic composition of the sample used, Table 4 presents the distribution of key characteristics of the sample firms involved in the main variables.

Firm Characteristics Distribution.

Results of the Main Effects

The Hausman test results reveal that the fixed effect is better than the random effect; thus, this article uses the fixed effect model for estimation. Table 5 presents the test results of the relationship between performance below the aspiration level and strategic deviance. Among them, Model 1 is the benchmark model containing control variables and moderating variables; Models 2 and 3 are the test models that add performance below the aspiration level and its squared term, respectively.

Regression Results.

Note. Standard errors in parentheses.

p < .10. **p < .05. ***p < .01.

The results of Model 2 show that the regression coefficient of performance below the aspiration level does not pass the significance test, indicating that the linear relationship between performance below the aspiration level and strategic deviance does not hold. Next, this article tests whether the quadratic curve relationship holds according to the three criteria proposed by Lind and Mehlum (2010).

First, in Model 3, the coefficient of performance below the aspiration level is .1584, which is significant at the 1% level, and the coefficient of the squared term of the performance expectation gap is −.1687, which is also significant at the 1% level. In addition, after the interaction term of the moderating variables in Model 6 is added, both the independent variables and their squared terms are still significantly positive and significantly negative, indicating that the results are robust. The F-test rejects the null hypothesis that both the coefficients of performance below the aspiration level and its squared term are zero at the 1% level. Compared with Model 2, Model 3 has significantly increased explained variance (△R2 = .0012, p < .01); second, when the value of the performance below the aspiration level is at the left end of its range, β1 + 2β2 × BHPlow is .1584. When the value of the performance below the aspiration level is at the right end of its range, β1 + 2β2 × BHPhigh is −.2403. The signs of the sample boundary slope are opposite and are significant at the 1% level; third, the inflection point (.4693) of the curve falls within the range of the performance expectation gap. Therefore, Hypothesis 1 is validated, and there is an inverted U-shaped relationship between performance below the aspiration level and strategic deviance.

Results of Mediating Effects

Models 4 and 5 in Table 5 consider the moderating effects of economic policy uncertainty and the nature of property rights on the relationship between performance below the aspiration level and strategic deviance. The results of Model 4 show that the interaction between performance below the aspiration level and economic policy uncertainty is significantly negative (β = −.1490, p < .01) and that the interaction between squared performance below the aspiration level and economic policy uncertainty is significantly positive (β = .0987, p < .01), which is the opposite of the coefficient of squared performance below the aspiration level (−.3203). This finding indicates that in the gap range where the expected reference point is dominant, economic policy uncertainty weakens the positive relationship between performance below the aspiration level and strategic deviance, whereas in the gap range where the survival reference point is dominant, economic policy uncertainty suppresses the negative relationship between performance below the aspiration level and strategic deviance; this result is still robust in Model 6.

The results of Model 5 show that the interaction between performance below the aspiration level and the nature of property rights is significantly positive (β = .1994, p < .1), and the interaction between squared performance below the aspiration level and the nature of property rights is significantly negative (β = −.1662, p < .1), indicating that compared with state-owned enterprises, nonstate-owned enterprises weaken the inverted U-shaped relationship between performance below the aspiration level and strategic deviance; this result is still robust in Model 6.

Robustness Test

This study conducts robustness tests by altering the measurement method of the expectation level. In this article, we borrow the research of Chen (2008) to measure the expectation level, which is calculated according to the formula Ai,t − 1 = (1 − α1)Pi, t − 2 + α1Ai, t − 2, where α1 represents the weight, which is between 0 and 1. We start from 0 and increase by 0.1 each time to assign weights. In the previous section we reported the test results of α1 = .4. Here, we report the test results when α1 = .6. As shown in Table 6, neither the main effect nor the moderating effect significantly changed, which is consistent with the results in Table 5.

Robustness Test.

Note. Standard errors in parentheses.

p < .10. **p < .05. ***p < .01.

Conclusions

On the basis of strategic balance theory and enterprise behavior theory, this study takes A-share listed companies on the Shanghai and Shenzhen stock exchanges from 2005 to 2019 as samples and empirically examines the nonlinear impact of the performance expectation gap on the degree of enterprise strategic difference and its boundary of influence. The research findings are as follows: First, there is a significant inverted U-shaped relationship between the gap in performance expectations and the degree of strategic divergence. This finding indicates that as the performance gap widens, the strategic choices of enterprises shift from initial strategic convergence to strategic divergence and eventually return to strategic convergence in the face of survival crises. Second, the uncertainty of economic policies weakens the abovementioned inverted U-shaped relationship, indicating that in a highly uncertain environment, the management’s tendency to attribute all problems to the external environment will suppress their motivation to make extreme strategic adjustments. Third, compared with that of nonstate-owned enterprises, the inverted U-shaped relationship of state-owned enterprises is weaker, which highlights the differences in resource endowment and risk-bearing willingness brought about by the nature of property rights.

This study makes several theoretical contributions. First, integrating the behavioral theory of the firm with strategic balance theory provides a more comprehensive theoretical framework for understanding strategic choices under performance feedback (Kahneman et al., 1979). The inverted U-shaped relationship between performance shortfall and strategic deviation bridges the gap between two seemingly contradictory theoretical perspectives: “change driven by adversity” and “threat-rigidity” (Greve, 2003). The results indicate that these theories are not mutually exclusive; rather, they explain the dominant behavioral logic of firms at different stages of performance shortfall—guided by expectation reference points versus survival reference points—thereby advancing the understanding of performance feedback theory. Second, by introducing economic policy uncertainty and ownership as key boundary conditions, this research deepens the understanding of the contextual complexity underlying the relationship between performance shortfalls and strategic deviation. It was found that economic policy uncertainty attenuates the inverted U-shaped relationship, providing empirical evidence from a transitional economy for self-enhancing attribution bias (Blagoeva et al., 2020). Moreover, the moderating effect of ownership nature confirms the important role of institutional logic and the resource-based view in strategic decision-making, suggesting that firms’ strategic choices are not only driven by internal performance feedback but also profoundly shaped by external institutional environments and internal resource endowments.

Furthermore, the conclusions of this study hold significant practical value for enterprise managers facing performance pressure. First, managers should abandon the simplistic linear thinking that “when performance declines, change is necessary” or “when performance declines, stability must be sought.” The key lies in accurately diagnosing the gap range that the enterprise is in. In the middle of the gap, one should have the courage to empower innovation and seek strategic breakthroughs. On the verge of a survival crisis, the strategic focus should be shifted to maintaining legitimacy, preserving strength, and avoiding high-risk bets. Second, in the face of economic policy uncertainties, the senior management team should be vigilant against the collective tendency of “external attribution,” and avoid attributing all problems to the environment and missing the window of opportunity for internal change. A more sensitive environmental scanning mechanism should be established to be adept at identifying and capturing new opportunities from fluctuations. Third, managers of nonstate-owned enterprises should recognize the advantages of their strategic flexibility, but they also need to maintain a high degree of awareness toward the risk of bankruptcy. Managers of state-owned enterprises should avoid the inertia caused by “soft budget constraints.” They should proactively utilize their inherent resource and legitimacy advantages to make forward-looking strategic plans instead of passively waiting for rescue.

While this study offers contributions to the existing body of literature, it is subject to certain limitations, which simultaneously highlight potential avenues for future scholarly inquiry. First, concerning the sample and measurement approach, this investigation is grounded in data from A-share listed companies on the Shanghai and Shenzhen stock exchanges. Although the findings provide meaningful insights for transitional economies, the extent to which these conclusions can be generalized to non-listed firms or enterprises operating within different institutional frameworks remains an open question. Future research could enhance the external validity of these findings by conducting comparative analyses across diverse national contexts and varied forms of corporate ownership. Second, with regard to the exploration of underlying mechanisms, the interpretation of the identified inverted U-shaped relationship and its boundary conditions relies predominantly on perspectives of attributional tendencies and resource constraints. However, this study does not directly examine potential mediating mechanisms, such as the psychological cognition of top management teams or the allocation of organizational attention. To better unpack the “black box” of how performance shortfalls influence strategic choices, subsequent studies may consider incorporating experimental designs or survey-based data to further elucidate the internal psychological and decision-making processes involved.

Footnotes

Ethical Considerations

The authors declare that this research complies with all relevant ethical guidelines and does not involve human subjects, animal experimentation, or other activities requiring ethical review.

Author Contributions

Conceptualization: Q.H.; Methodology: T.Z.; Software: Q.H.; Validation: Q.H.; Formal analysis: T.Z.; Investigation: T.Z.; Resources: L.X.; Data curation, T.Z..; Writing—original draft preparation: Q.H.; Writing—review and editing: T.Z.; Visualization: Q.H.; Supervision: L.X.; Project administration: T.Z. All authors have read and agreed to the published version of the manuscript.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the National Natural Science Foundation of China (Grant Number: 72471074); Excellent Scientific Research and Innovation Team Construction Project of Anhui Business and Technology College (Grant Number: 2025KYTD06); Key Project of Humanities and Social Sciences Research in Anhui Universities (Grant Number: SK2021A1081).

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data will be made available on request.