Abstract

In recent years, there has been significant interest in economic policy uncertainty and its economic consequences. Fluctuations in economic policies can introduce instability into business operations, resulting in elevated credit default risks. It is important to investigate whether Chinese commercial banks take economic policy uncertainty into account and adopt a more diversified loan structure to mitigate the risks associated with policy changes. In this study, we investigate the impact of economic policy uncertainty on loan concentration within a sample of Chinese commercial banks from 2007 to 2020. Using a panel dataset of 311 banks, we employ fixed-effects regression models and conduct robustness checks with instrumental variables and dynamic panel regressions to address endogeneity concerns. Our findings reveal a significant negative correlation between economic policy uncertainty and the loan concentration of banks. These results hold strong even when subjected to rigorous testing for endogeneity using instrumental variables and dynamic panel regressions. Furthermore, we also find that the negative impact of economic policy uncertainty on loan concentration is more pronounced in regional banks, small-sized banks, and banks with lower market shares. Moreover, the mechanism analysis demonstrates that operational risk serves as a vital channel through which economic policy uncertainty affects loan concentration. By shedding light on how macroeconomic policies impact the financial behavior of commercial banks, we provide new empirical evidence and valuable insights into the dynamics of bank loan structures. In light of our findings, we propose policy recommendations to ensure economic policy stability, encourage the diversification of loan portfolios, expand the regulatory scope on loan concentration, and foster improvements in the regulatory system.

Plain language summary

In recent years, there has been a lot of interest in how uncertain economic policies affect the economy. When economic policies change frequently, it can make it hard for businesses to plan ahead, which increases the risk of them not being able to repay their loans. We want to find out if Chinese banks consider this uncertainty when deciding how to spread out their loans to different industries, which can help them manage these risks better. In this study, we looked at how economic policy uncertainty affected the concentration of loans in Chinese banks from 2007 to 2020. We found that when economic policy uncertainty was high, banks tended to spread out their loans more instead of concentrating them in just a few industries. We used different statistical tests to make sure our findings were accurate. We also found that this effect was stronger for smaller banks, banks in certain regions, and banks with lower market shares. Additionally, we found that the way economic policy uncertainty affects loan concentration is through increasing operational risks for banks. Our study provides new evidence on how economic policies influence the decisions of banks and how they manage their loans. Based on our findings, we suggest policies to make economic policies more stable, encourage banks to diversify their loan portfolios, regulate loan concentration better, and improve the overall regulatory system.

Introduction

Within China’s prevailing financial system, dominated by indirect financing, commercial banks assume an indispensable role. Acting as a crucial intermediary between macroeconomic policies and firms, commercial banks serve as a linchpin for any macroeconomic strategies, necessitating corresponding credit policies. The provision of a stable and dependable credit supply by banks holds immense practical significance in alleviating the financing constraints faced by firms. This support, in turn, fosters the development of the real economy, upholds financial stability, and propels the transformation and advancement of China’s manufacturing sector.

However, while banks facilitate economic development, they also face elevated risks, particularly from shifts in macroeconomic policies. When viewed from a direct impact perspective, the implementation of new economic policies requires banks to collaborate with corresponding credit policies. For instance, the state may leverage credit expansion to bolster high-tech industries. On an indirect level, alterations in economic policy are funneled through the credit policies of commercial banks, thereby impacting tangible economic entities. These entities, in turn, are shaped by business activities, with the ultimate outcomes feeding back into the banking sector. Consequently, economic policy and its inherent uncertainties emerge as a risk factor that banks inevitably factor into their operational considerations.

Economic policy uncertainty poses a significant challenge for both real enterprises and the financial system. According to Baker et al. (2016), the global economic policy uncertainty index has risen by 108% since the onset of the 2008 economic crisis and is far more volatile than historical levels. Notably, the level of economic policy uncertainty reached its highest point in 20 years on two occasions: November 2018, when the second batch of U.S. tariff lists from the U.S.-China trade war took effect, and November 2020, when the COVID-19 pandemic broke out. Phan et al. (2021) found that economic policy uncertainty negatively impacts financial stability. Al-Thaqeb et al. (2022) found that economic policy uncertainty negatively impacts individuals, businesses, governments, and economies both locally and internationally. Cui, Wang et al. (2023) showed that economic policy uncertainty is significantly and negatively associated with corporate green innovation. So how would banks respond to economic policy uncertainty? Most studies have found that under the influence of economic policy uncertainty, banks will downsize credit and reduce market-oriented credit investment (Ng et al., 2020).

However, the existing literature on loan structure holds two contrasting views. One suggests that diversified loan structures mitigate risk by reducing the impact of customers’ individual risks on the bank (Boyd & Prescott, 1986; Diamond, 1984), while the other argues that concentrated loan structures allow banks to accumulate industry expertise and better manage credit risks (P. G. Berger et al., 2017; Liberti et al., 2017).

Given these contrasting views and the growing importance of economic policy uncertainty, it is critical to understand how economic policy uncertainty impacts loan structures of banks. Specifically, will banks choose a more concentrated or diversified loan structure in response to economic policy uncertainty? Addressing this question is essential for both theoretical understanding and practical policy-making, as it sheds light on how banks manage credit risk in volatile economic environments.

To gain a deeper understanding of the above issue, we set forth several research objectives. First, we explore how economic policy uncertainty changes the loan structure of banks. Second, we examine whether the impact of economic policy uncertainty on banks’ loan concentration varies based on factors such as the business scope, bank size, and market shar. Finally, we investigate the mechanisms through which economic policy uncertainty impacts loan concentration. We used a sample of Chinese commercial banks from 2007 to 2020 for the study. Our findings reveal that economic policy uncertainty significantly reduces the loan concentration of commercial banks. This implies that in a market environment with a high level of economic policy uncertainty, banks will actively choose a more diversified loan structure to cope with the risk of economic policy changes and reduce their dependence on major customers. Importantly, our results remain robust even when considering alternative measures of loan concentration and excluding extraordinary years. To address potential endogeneity concerns, we employ instrumental variables regressions and dynamic panel models, which consistently support our main regression results. Furthermore, our study uncovers that operational risk serves as a critical channel through which economic policy uncertainty influences the loan structure. We also find that the negative impact of economic policy uncertainty on loan concentration is more pronounced in regional banks, small-sized banks, and banks with lower market shares. Consequently, economic policy uncertainty exerts a more pronounced negative impact on the loan concentration of these banks.

Compared to existing literature, we make several contributions. First, while previous studies have mainly focused on the impact of economic policy uncertainty on the financial behavior of listed companies (Gulen & Ion, 2016), less attention has been paid to commercial banks. However, policy makers can directly affect the scale and channels of bank loan allocation through monetary and industrial policies, which in turn regulate the financing behavior of listed companies. The financial behavior of listed companies will ultimately be fed back to the commercial banks, which will have a further impact on the commercial banks. Our study provides an incremental contribution to the understanding of how economic policy uncertainty affects bank finance.

Second, most of the existing literature has focused on the impact of economic policy uncertainty on loan sizes (Ng et al., 2020). By examining the impact of economic policy uncertainty on the loan structure of commercial banks, our study has certain theoretical significance for loan structure adjustment under the environment of economic policy uncertainty.

Third, the existing literature is cognitively divided on the economic meaning of loan concentration. The traditional view perceives loan concentration as a risk factor (e.g., Bebczuk & Galindo, 2008; Boyd & Prescott, 1986; Diamond, 1984; Rossi et al., 2009), suggesting that banks should adopt a more diversified loan structure. However, some scholars argue that higher loan concentration enables banks to leverage industry expertise for better credit management (e.g., P. G. Berger et al., 2017; Liberti et al., 2017; Loutskina & Strahan, 2011). It remains uncertain what will firms choose to do to cope with the risk of economic policy changes. The analysis of this issue provides a new explanation for understanding the economic meaning of loan concentration.

Fourth, loan concentration has been a key supervisory component of China’s regulatory authorities. Since 2003, the China Banking Regulatory Commission (CBRC) has issued a series of policy documents to restrict the loan concentration of commercial banks. Are these policies effective and has the reduction of loan concentration reduced bank risk? Has the restriction on loan concentration also led to an increase in the cost of information collection for banks? Whether commercial banks also take the initiative to reduce loan concentration to mitigate credit risk are a series of questions that require attention. Out study contributes to the understanding of the economic implications of loan concentration in an environment of economic policy uncertainty and promotes the improvement of bank regulatory policies.

Literature Review

Economic Consequences of Economic Policy Uncertainty

Economic policy uncertainty refers to the uncertainty caused by the government’s failure to specify the direction and intensity of economic policy expectations, policy implementation, and changes in policy stance (Gulen & Ion, 2016; Le & Zak, 2006). It has been found that economic policy uncertainty tends to cause macroeconomic fluctuations, resulting in changes in the industry outlook as well as the market information environment (Bernanke & Kuttner, 2005), and exacerbating information asymmetry between managers and stakeholders (Nagar et al., 2019). Uddin et al. (2020) argued that increased economic policy uncertainty should be treated as a risk factor due to its negative impacts on market and economy. Alola and Uzuner (2020) provided evidence that economic policy uncertainty can also influence housing market pricing. Therefore, in a market environment with a high degree of economic policy uncertainty, the investment, financing, and operational behavior of companies tend to face relatively high risks.

Most of the existing literature has focused on the impact of economic policy uncertainty on the investment and financing behavior of listed companies. For example, in terms of investment, Gulen and Ion (2016) found that economic policy uncertainty makes firms face more uncertainty when investing in the future. Gao et al. (2024) reported a negative relationship between economic policy uncertainty and foreign direct investment inflows. Gupta et al. (2024) concluded that economic policy uncertainty increases investment-cash flow sensitivity. Kurniawan et al. (2024) argued that economic policy uncertainty negatively affects investment activity and financial reporting quality. Therefore, in a market environment with higher economic policy uncertainty, firms’ investment activities will decline. In terms of financing, it has been found that economic policy uncertainty leads to higher financing costs (Demerjian, 2017; Kim, 2019), so firms tend to reduce credit financing and respond through equity financing or endogenous financing (Hanlon et al., 2017). This helps reduce their reliance to bank loan resources and mitigate the risk of economic policy changes. Farooq et al. (2024) showed that firms in countries with higher economic policy uncertainty face more financing constraints than those in countries with lower economic policy uncertainty. Asimakopoulos et al. (2024) found that economic policy uncertainty is negatively associated with leverage. They also found that higher economic policy uncertainty levels force firms to increase their speed of adjustment due to tighter financing requirements.

Some scholars have also focused on the impact of economic policy uncertainty on the financial behavior of commercial banks. It is found that in the case where economic policy uncertainty negatively affects the experience behavior of firms and leads to a rise in the expected credit default risk, banks will take various measures to control credit risk. Demerjian (2017) found that in a market environment with high economic policy uncertainty, banks will impose stricter restrictions on loan issuance and set more stringent loan contracts. Ng et al. (2020) discovered that in order to cope with the risk of economic policy changes, banks make more loan provisions to cope with potential credit losses. Danisman and Tarazi (2024) revealed that bank stability decreases as economic policy uncertainty rises. Syed (2024) found that economic policy uncertainty negatively impacts banking stability. The existing literature focuses on the impact of economic policy uncertainty on the size of loan allocation. How will economic policy uncertainty affect the loan structure of banks? Will banks respond to economic policy uncertainty by constructing a diversified loan allocation system? This is the main concern of our study, and also the difference between our study and the existing literature.

Economic Meaning of Bank Loan Concentration

Loan concentration refers to the over-concentrated allocation of bank loan resources in certain areas (Tabak et al., 2011). Regarding the economic meaning of loan concentration, scholars hold two different views. The traditional view argues that loan concentration is a risk factor and therefore commercial banks should hold a more diversified loan structure to reduce risk. For example, Diamond (1984), Boyd and Prescott (1986) found that diversified loan helps to reduce the impact of individual customer risk on banks, thus realizing the cost of loan regulation and mitigating credit risk. Cui, Li et al. (2023) found that a more concentrated customer base reduces suppliers’ credit risk. In practice, loan concentration has been an important factor of banking crises over the past three decades (Bebczuk & Galindo, 2008; Rossi et al., 2009).

China’s policy authorities also regard loan concentration as a risk factor and have issued a series of policies and regulations on bank loan concentration. In 2003, the China Banking Regulatory Commission (CBRC) issued the Guides on Commercial Banks Management of Risks Involved in Credit Extension to Group Clients, which set a limit on the credit granted by commercial banks to a single group customer, ensuring it does not exceed 15% of the bank’s net capital. In 2005, the CBRC further stipulated that banks’ credit limits should be as follows: “the top ten customers should not be higher than 50%, the largest single customer should not be higher than 10%, and the largest single group customer should not be higher than 15%.” In 2018, the CBRC issued the Measures for the Management of Large Exposures of Commercial Banks to provide stricter control over the risk of loan concentration. In 2020, the China Insurance Regulatory Commission (CIRC) issued the Notice on the Establishment of the Management System of Real Estate Loan Concentration of Banking Financial Institutions, which regulated the upper limit of real estate loans for commercial banks as well as the upper limit of personal housing loans. It can be seen that loan concentration is an important regulatory indicator within China’s financial system.

On the other hand, some scholars have interpreted the economic meaning of loan concentration from the perspective of industry expertise. This viewpoint argues that when bank loans are overly concentrated in certain fields, banks are able to collect more information and accumulate industry-specific knowledge. It helps to reduce the information asymmetry between banks and industry customers, identify credit risks in a timely manner, and control the risks within an acceptable range (e.g., Acharya, 2006; Tabak et al., 2011; Winton, 1999). In the case of diversified bank loan concentration, it is more difficult for banks to collect information about their customers, which is not conducive to the management of credit risk. Beck et al. (2022) found that both individual and systemic bank risk decrease with specialization. Therefore, in the case of diversified credit, commercial banks will spend more time and energy on customer tracking and management, collecting customer information, and accumulating customer and industry experience (A. N. Berger et al., 2005; Liberti & Mian, 2008). It will also result in in associated costs and fees.

Economic Policy Uncertainty and Bank Loan Concentration

Some researches described above suggests that increased economic policy uncertainty can lead to macroeconomic volatility, increased information asymmetry, and greater risks for firms and banks. To manage and mitigate the increased credit risk and uncertainty associated with economic policy uncertainty, banks may adopt a more diversified loan allocation strategy.

On the other side, an alternative perspective argues that loan concentration in specific industries allows banks to accumulate specialized knowledge and reduce information asymmetry. In that situation, banks are likely to choose a more centralized loan structure in response to increased economic policy uncertainty.

Given the presence of economic policy uncertainty, our research question arises: Will banks choose a more concentrated or diversified loan structure in response to increased economic policy uncertainty?

Theoretical Analysis and Research Hypotheses

Research on economic policy uncertainty started earlier by Pindyck (1982) and Abel (1983), who explored the theoretical research of the impact of uncertainty on firms’ optimal investment decisions. Their analytical framework is based on the real option mechanism, which argues that in the face of uncertainty, a firm’s investment decision-making is equivalent to holding a call option. According to the real options theory, an increase in market uncertainty enhances the value of this option, leading firms’ investment decision-makers to adopt a wait-and-see approach.

Hassett and Metcalf (1999) extended this classical real options framework by incorporating economic policy uncertainty, thereby examining its effects on investment. This expansion broadened the applicability of the theoretical framework based on the real options mechanism.

With advancements in measuring economic policy uncertainty, many empirical studies have emerged alongside earlier theoretical research. These studies have widely explored the economic effects of economic policy uncertainty at the empirical level. When faced with the shock of economic policy uncertainty, banks may choose between diversification or centralization in their loan structure decisions. Among them, a diversified loan policy can bring the following substantial benefits to banks. First, portfolio theory shows that maintaining a diversified portfolio or source of income can effectively reduce the bank’s overall risk-taking (Markowitz, 1952). It also helps to mitigate the negative impact of individual customer risk on the bank and maintain the bank’s operational stability (Dhaliwal et al., 2016; Srivastava et al., 1998). Especially in a market environment with a high degree of economic policy uncertainty, where it is impossible to anticipate which industries will be affected by changes in economic policy in the future, the diversification of bank loan can achieve risk hedging and effective control potential risks and losses. Second, the diversification of bank loans also means the reduction of its customer concentration, so the bank can get more bargaining power (Emerson, 1962; Heide & John, 1988). It is crucial for banks to control credit risks and decrease costs.

On the other hand, maintaining a diversified loan structure for banks also entails certain costs and expenses, which come from the following sources. First, maintaining a low level of loan concentration means that banks may deal with more new customers from different industries and geographies. This leads to a rise in the level of information asymmetry between them, as banks lack knowledge of their industry background, geographic characteristics, and the firm’s operations (Acharya, 2006; Tabak et al., 2011; Winton, 1999). Second, information asymmetry between banks and new customers may lead to more time and cost for managing customer relationships, such as visiting and researching the customer’s industry and geography to understand the customer’s industry background and business environment. Conducting interviews and surveys with customers to understand their actual operating conditions in order to accurately assess their actual operating ability and solvency. Tracking records of customers in different industries, geographies and backgrounds, and collecting customer information on a regular basis (Beck et al., 2022; Liberti et al., 2017; Loutskina & Strahan, 2011). These efforts are undertaken to minimize information asymmetry with customers and maintain control over credit risk. The more decentralized the loan structure and the lower the concentration of customers, the higher the cost that firms have to pay to reduce the information asymmetry with customers.

Whether banks choose a more centralized or diversified loan structure depends on their trade-off between costs and benefits. Economic policy uncertainty has an important impact on the “benefit-cost” structure of banks. From the perspective of benefits, higher economic policy uncertainty implies an increase in expected risks. Maintaining a more diversified loan structure can help banks avoid more losses and avoid unnecessary risk-taking, thus bringing more benefits to banks. At the same time, banks’ core profitability mechanism is to realize the risk hedging situation to obtain a certain return. Therefore, in a market environment characterized by high economic policy uncertainty, banks are incentivized to maintain a diversified loan structure. From a cost perspective, increased economic policy uncertainty signifies a changing market environment with uncertain future prospects. Consequently, there is an increase in information asymmetry between banks and companies, as the banks’ prior market perceptions may not align with the reality. To address this, banks need to engage in more market tracking and research activities to reassess their overall risk perception. Regardless of whether a bank maintains a centralized or diversified loan structure, it must undertake information-seeking activities. However, the cost of maintaining a diversified loan structure is relatively lower compared to a centralized structure.

Based on this analysis, we conclude that economic policy uncertainty leads to greater relative benefits and lower costs for banks to maintain a diversified loan structure. We anticipate that banks will establish more diversified loan structures in environments with higher levels of economic policy uncertainty. As a result, we propose the following hypothesis:

Hypothesis 1 (H1): Holding other conditions constant, the higher the economic policy uncertainty, the lower the concentration of bank loans.

Method

Data Sources

To investigate the influence of economic policy uncertainty on the concentration of bank loans in Chinese commercial banks, we collected the financial data of 311 urban commercial banks within China from 2007 to 2020. We excluded observations with missing data to ensure data integrity. To mitigate the influence of outliers, we applied winsorization at the 1% and 99% levels to all continuous variables. Furthermore, we standardized all variables in the regression model to facilitate the comparison of each regression coefficient.

The economic policy uncertainty index (EPU) used in our study is based on the Chinese economic policy uncertainty index developed by Baker et al. (2016). Industry level bank loan distribution data is manually collected from annual financial report of Chinese commercial banks. Bank financial variables are sourced from CSMAR Database, Chinese Research Data Services Platform (CNRDS) and ORBIS Bank Focus database. In cases where data was missing, we made efforts to maximize the utilization of the Wind Database and annual reports from banks to fill in these gaps.

The availability of data is a significant constraint in the research of Chinese commercial banks. To maximize the sample size and mitigate the negative impact of sample bias on the conclusions of our study, efforts are made from the following aspects:

First, we obtain data from multiple sources to ensure the authenticity and reliability of our data. Currently, the two main databases that include data on Chinese commercial banks are ORBIS Bank Focus and CSMAR. ORBIS Bank Focus is a global banking database that includes financial data from banks in most countries, including Chinese commercial banks; CSMAR includes financial data of listed companies in China, including Chinese commercial banks. Although both databases cover Chinese commercial banks to some extent, there are still some missing values. Therefore, we combine data from both databases to expand our sample size as much as possible.

Second, after merging the data on Chinese commercial banks from the two databases, we identify some other issues related to sample bias: (1) there are missing values for some control variables. For example, while both ORBIS Bank Focus and CSMAR include data on the company size of Bank A, neither provides information on the bank’s ownership structure or board size; (2) there are discrepancies in the financial indicators of the same bank between the two databases, which may be due to data entry errors. These issues can introduce sample bias. To address these problems, we collect annual financial reports of banks from sources such as the Cninfo website and banks’ official websites. We extracted the necessary financial indicators from these reports and replaced missing or potentially erroneous data to ensure accuracy.

Last, even after the above steps, we find that some banks’ financial data still contained missing values. Therefore, we employ interpolation methods to fill in these missing values. For example, if Bank B’s total asset turnover rate (TA) for 2013 is missing, we replace the missing value with the average of the total asset turnover rates for 2012 and 2014. If a financial indicator is missing for several consecutive years, we fill in the missing values with the mean of that indicator within the sample. After processing the missing values in this way, we obtain financial data for 311 Chinese commercial banks from 2007 to 2020, resulting in a total of 2,039 bank-year observations. Statistical analysis shows that the assets of these banks account for 90% of the total assets of Chinese commercial banking system, and the descriptive statistics also reflect that the distribution of various financial indicators aligns with the overall economic patterns of the Chinese banking industry. Therefore, although some sample bias remains, it does not constitute a significant impact on the overall conclusions of our study.

Empirical Model

We develop an OLS regression model (1) to investigate the relationship between economic policy uncertainty and bank loan concentration. In order to mitigate the impact of individual bank-specific factors on bank loan concentration that remain constant over time, we incorporate individual bank fixed effects in the regression model. As discussed in Section “Theoretical Analysis and Research Hypotheses,” we hypothesize that commercial banks will construct a more diversified loan structure when facing high level economic policy uncertainty, so that we predict the coefficient of EPU (β1) will be significantly negative. The specific variable definitions and predicted sign are presented in Section “Variables Description” and Table 1.

Definitions of the Main Variables.

Variables Description

Dependent Variable: Bank Loan Concentration

Our main explanatory variable LC_HHI is derived from supply chain theory. In supply chain research, HHI method (Herfindahl Index) are widely used in measuring the customer concentration by using sales volume data of each customer (Patatoukas, 2012; Cen et al., 2017; Leung et al., 2021). Customer concentration HHI index is calculated as equation (2): (1) Obtain sale volume of each customer (Xi) and total sale volume (X) for a certain time period; (2) Divide Xi by X to obtain the sale proportion from each customer; (3) Customer Concentration (CC) is calculated by the sum of squares of Xi/X. The range of CC is from 0 to 1. The higher the value of CC, the higher the customer concentration. In banking industry, customers are companies that receive loans from banks. The calculation methods for customer concentration are also applicable for calculating loan concentration. Therefore, we migrate the methods that used in supply chain research to calculate customer concentration to banking research and using this method to measure loan concentration.

In line with the researchers conducted by Tabak et al. (2011), P. G. Berger et al. (2017), and Bhuyan et al. (2022), We employed equation (3) to calculate Herfindahl-Hirschman Index (HHI) as a measurement of loan concentration. In this equation, IndLoan i,j,t represents the amount of loans invested by bank i in industry j during year t , while IndLoan i,t represents the total amount of loans invested by bank i across all industries in year t. The resulting LC_HHI i,t serves as an indicator of the concentration of bank loans among industries for that specific year, reflecting the potential risk associated with the loan structure of banks. A higher value of LC_HHI i,t indicates a more concentrated loan structure within the bank, implying a greater credit risk. Conversely, a lower value of LC_HHI i,t indicates a more diversified loan structure, effectively dispersing the credit risk:

Independent Variables: Economic Policy Uncertainty

We adopted the economic policy uncertainty index (EPU) constructed by Baker et al. (2016) as a measurement to capture economic policy uncertainty. Since EPU is monthly data, to match with the bank’s annual data, we transformed it into annual data by calculating the arithmetic mean across the months. We also divided the resulting annual economic policy uncertainty index by 100. In addition, we used alternative methods to measure economic policy uncertainty and conducted robustness tests.

Control Variables

To account for factors that might have an impact on economic policy uncertainty and bank loan origination, we have incorporated bank fundamental variables, bank risk variables, bank operation variables, and macroeconomic level variables in our analysis. The detail definitions of all the variables are presented as follows.

We first include bank fundamental variables into consideration, such as Bank Scale (Size), Equity to Debt Ratio (ETD), and Deposit to Loan Ratio (DLR). These variables reflect a bank’s capacity to extend loans to customers. Second, the Capital Adequacy Ratio (CAR), Loan Loss Provision (LLP), and Non-Performing Loan (NPL) reflect a bank’s resilience to risks. Third, we incorporate Asset Turnover (AT) and Return of Asset (ROA) in the model (1) to account for the profitability of the banks. Last, we incorporate macroeconomic variables into the empirical model, including the Growth Rate of Regional Gross Domestic Product (GGDP), Macroeconomic Sentiment Index (MACROPI), Enterprise Prosperity Index (FIRMPI), and Banking Prosperity Index (BANKPI), to account for macroeconomic conditions.

Data Analysis and Results

Descriptive Statistics

Panel A of Table 2 presents descriptive statistics for variables of the full sample. LC_HHI has a mean value of 0.1625, ranging from a minimum of 0.0265 to a maximum of 0.5918. These figures demonstrate substantial variations in loan structures among different banks.

Descriptive Statistics.

Panel B of Table 2 provides the descriptive statistics categorized by the nature of the banks. Chinese banks can be divided into four categories: state-owned banks, urban commercial banks, rural banks, and other banks. As shown in the Panel B of Table 2, national banks exhibit a larger scale compared to other banks, with state-owned banks outperforming their counterparts by achieving higher ROA. Urban commercial banks demonstrate superior risk management capabilities, evidenced by their lower levels of non-performing loans. Above findings confirm the fulfillment of the fundamental premise for the empirical analysis. Additionally, tests for multicollinearity indicate that the variance inflation factor (VIF) of the main variables remains below 5, signifying the absence of significant multicollinearity issues in the constructed empirical model.

Univariate Analysis

In Table 3, we categorize the sample into two groups based on the mean value of economic policy uncertainty (EPU) and perform univariate tests to compare the mean and median differences of LC_HHI between these groups. The results of Table 3 reveal that In the group with a higher EPU, the mean and median of LC_HHI are both lower, and the differences between the two groups are significant at 1% level. The findings above imply that in the presence of elevated economic policy uncertainty, there is a decrease in the concentration of bank loans, leading to a more diverse loan structure.

Univariate Analysis.

indicates significance at the .01 level or better.

Baseline Result

In Table 4, we perform an empirical analysis to examine the relationship between economic policy uncertainty (EPU) and bank loan concentration (LC_HHI). In column (1), we incorporate only the independent variable EPU in the regression equation. In columns (2) to (6), we progressively incorporate additional control variables, such as basic financial indicators of banks, bank risk indicators, bank operating indicators, bank governance indicators, and macroeconomic indicators, respectively. The regression results of Table 4 indicate that EPU is associated with a more diversified loan structure.

Impact of Economic Policy Uncertainty on Bank Loan Concentration.

Note. Column (1) include bank fixed effect. Column (2) include bank fundamental variables. Column (3) include bank credit risk variables. Column (4) include bank operation variables. Column (5) include bank governance variables. Column (6) include macroeconomic variables. T-statistics are adjusted by bank level cluster-robust standard errors, and are reported in parentheses. **, and *** denote statistical significance at the 5%, and 1% levels, respectively.

Robustness

Replacement of Core Variables Measurements

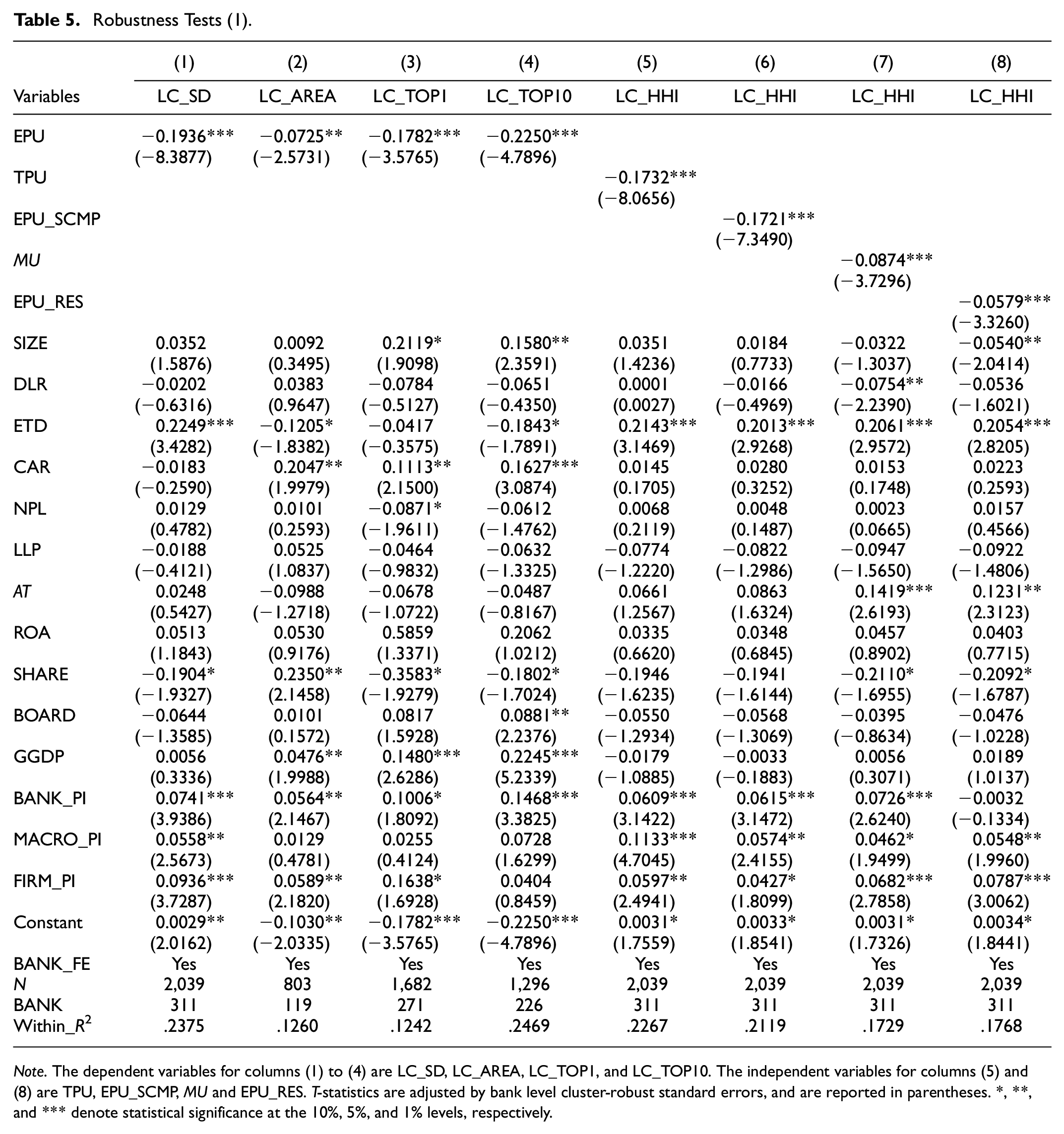

Table 5 presents the replacement of measures for core variable. In columns (1) to (4), the dependent variable LC_HHI is replaced as dispersion degree of loan share by industry (LC_SD), regional loan concentration (LC_AREA), share of loans to the top customer (LC_TOP1) and top 10 customer (LC_TOP10). In columns (5) to (8), the indepndent variable EPU is replaced with trade policy uncertainty index (TPU), China economic policy uncertainty index (EPU_SCMP), conditional variance of GDP growth rate for each province in China to estimate EPU by GARCH (1, 1) model and EPU that exclude macroeconomic factors (EPU_RES). Across all these columns, we find that EPU to be significantly negative with LC_HHI.

Robustness Tests (1).

Note. The dependent variables for columns (1) to (4) are LC_SD, LC_AREA, LC_TOP1, and LC_TOP10. The independent variables for columns (5) and (8) are TPU, EPU_SCMP, MU and EPU_RES. T-statistics are adjusted by bank level cluster-robust standard errors, and are reported in parentheses. *, **, and *** denote statistical significance at the 10%, 5%, and 1% levels, respectively.

Other Robustness Tests

In Table 6, we perform some other tests to validate our main finding. In columns (1) and (2), we employe the method of Nguyen and Phan (2017) to control annual year fixed effect. In column (3), we exclude 2019 and 2020, which were impacted by the COVID-19 pandemic and the US-China trade war. In column (4), we exclude the period of high economic growth prior to 2009. In column (5), we exclude the years 2008 and 2015, which witnessed significant fluctuations in the macroeconomy. In column (6), we restrict the sample period from 2012 to 2020 to exclude the promulgation of the Measures for Capital Management of Commercial Banks by Chinese policy department. Across all these columns, our main findings keep robust.

Robustness Tests (2).

Note. In column (1), we randomly exclude a time dummy variable and incorporate the remaining time dummy variables in the regression model. In column (2), we include annual year level cluster-robust standard errors to control for year fixed effect. In column (3), we exclude the year of COVID-19 and US-China trade war (2019 and 2020). In column (4), we exclude the year before 2009. In column (5), we exclude the year of 2008 and 2015. In column (6), we exclude the year before 2012. T-statistics are adjusted by bank level cluster-robust standard errors, and are reported in parentheses. *, **, and *** denote statistical significance at the 10%, 5%, and 1% levels, respectively.

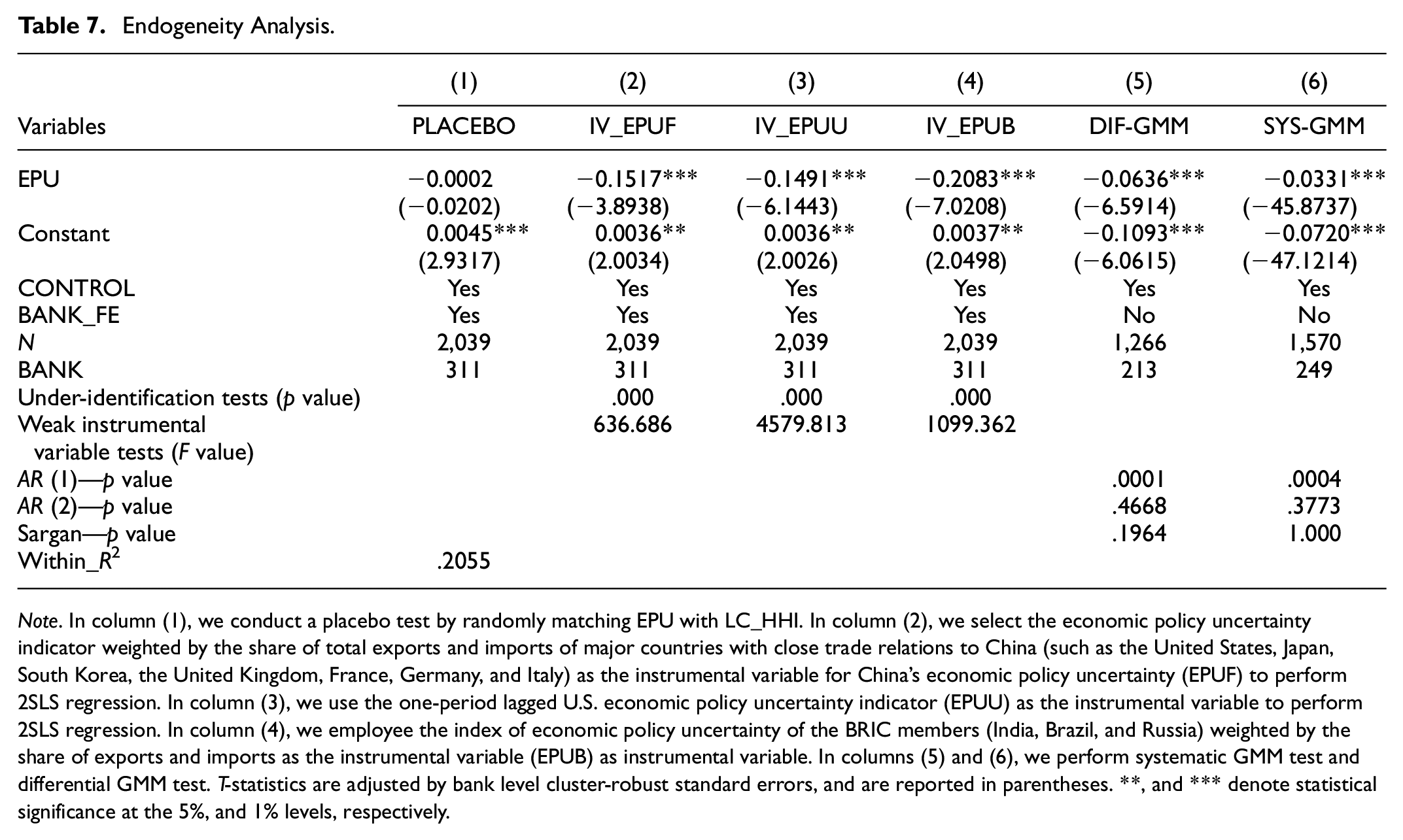

Endogeneity Analysis

In Table 7, we address the issue of endogeneity through following approaches. In column (1), we perform a placebo test by randomly pairing the independent and dependent variables. In columns (2) to (4), we employ the instrumental variables approach to control potential endogeneity problem. In columns (5) and (6), we addressed the endogeneity issue by using the system GMM model and the difference GMM model. The above results show that after controlling for the endogeneity issue, the relationship between economic policy uncertainty and loan concentration remains significant.

Endogeneity Analysis.

Note. In column (1), we conduct a placebo test by randomly matching EPU with LC_HHI. In column (2), we select the economic policy uncertainty indicator weighted by the share of total exports and imports of major countries with close trade relations to China (such as the United States, Japan, South Korea, the United Kingdom, France, Germany, and Italy) as the instrumental variable for China’s economic policy uncertainty (EPUF) to perform 2SLS regression. In column (3), we use the one-period lagged U.S. economic policy uncertainty indicator (EPUU) as the instrumental variable to perform 2SLS regression. In column (4), we employee the index of economic policy uncertainty of the BRIC members (India, Brazil, and Russia) weighted by the share of exports and imports as the instrumental variable (EPUB) as instrumental variable. In columns (5) and (6), we perform systematic GMM test and differential GMM test. T-statistics are adjusted by bank level cluster-robust standard errors, and are reported in parentheses. **, and *** denote statistical significance at the 5%, and 1% levels, respectively.

Heterogeneity Analysis

In Table 8, we conduct a series of heterogeneity analyses. In columns (1) and (2), we divide the sample into national banks and regional banks. In columns (3) and (4), we divide the sample into large-scale banks and small-scale banks based on the median bank asset. In columns (5) and (6), we divide the sample into large-market share group and small-market share group based on the median of market share. the regression results of Table 8 reveal that the relationship between EPU and LC_HHI are more pronounced for regional banks, small-scale banks and small-market share banks. This can be attributed to the fact that these banks with weaker risk-absorbing capacity (Karadima & Louri, 2020) tend to adopt more aggressive loan strategies facing environment of high economic policy uncertainty.

Heterogeneity Analysis.

Note. Columns (1) and (2) present the regression results of national banks and regional banks. Columns (3) and (4) present the regression results of large-scale banks and small-scale banks. Columns (5) and (6) present the regression results of large-market share banks and small-market share banks. T-statistics are adjusted by bank level cluster-robust standard errors, and are reported in parentheses. *, **, and *** denote statistical significance at the 10%, 5%, and 1% levels, respectively.

Mechanism Analysis

In Table 9, we investigate the mechanism through which economic policy uncertainty (EPU) impacts loan concentration (LC_HHI). First, we measure bank risk by using two indicators: Risk_ROA (standard deviation of seasonal return of asset) and RISK_PRO (standard deviation of seasonal income margin). Then, we use a three-step mediation effect model to test the mechanism. Across these columns, we find that EPU increases the volatility ROA and income margin, which in turn leads banks to adopt a more diversified loan structure. The results show that operational risk is the critical mechanism through which economic policy uncertainty affects loan concentration.

Mechanism Analysis.

Note. Columns (1) to (3) present the results of how EPU affect RISK_ROA, and how RISK_ROA affect the loan structure of the banks. Columns (4) to (6) present the results of how EPU affect RISK_PRO, and how RISK_PRO affect the loan structure of the banks. T-statistics are adjusted by bank level cluster-robust standard errors, and are reported in parentheses. *, **, and *** denote statistical significance at the 10%, 5%, and 1% levels, respectively.

Further Analysis

Further Decomposition of Loan Concentration

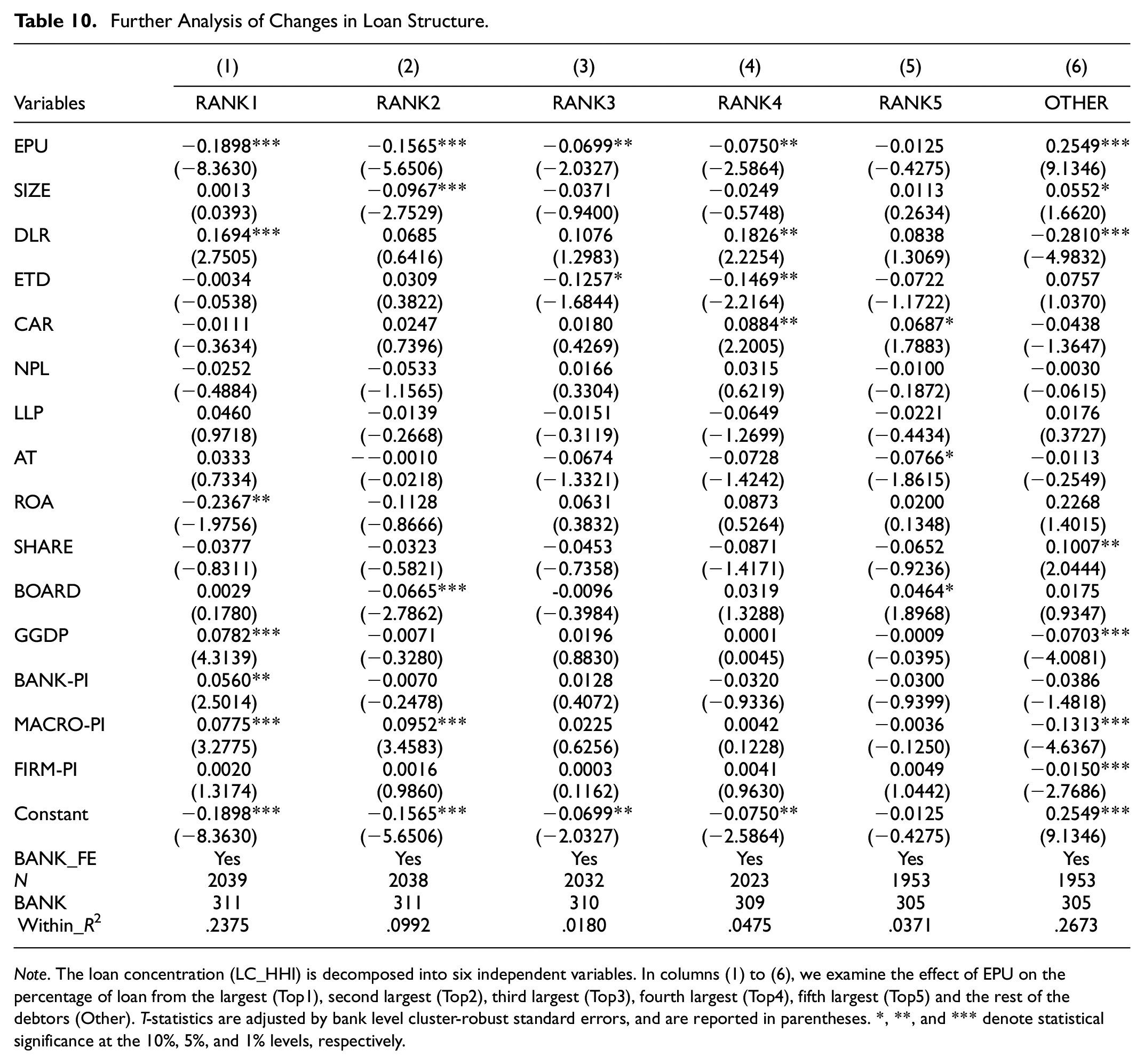

In Table 10, we examined how banks’ loans are distributed across various categories in facing of EPU. RANK1 to RANK5 represent the industries ranked from first to fifth in terms of loan share, OTHER represents industries outside the top five. The regression results of Table 10 reveal that due to the impact of economic policy uncertainty, banks reduced the loan share to their top four clients and increased loans to other clients, which is consistent with our main finding that banks adopted a strategy of diversifying loan concentration to mitigate the risks associated with economic policy uncertainty.

Further Analysis of Changes in Loan Structure.

Note. The loan concentration (LC_HHI) is decomposed into six independent variables. In columns (1) to (6), we examine the effect of EPU on the percentage of loan from the largest (Top1), second largest (Top2), third largest (Top3), fourth largest (Top4), fifth largest (Top5) and the rest of the debtors (Other). T-statistics are adjusted by bank level cluster-robust standard errors, and are reported in parentheses. *, **, and *** denote statistical significance at the 10%, 5%, and 1% levels, respectively.

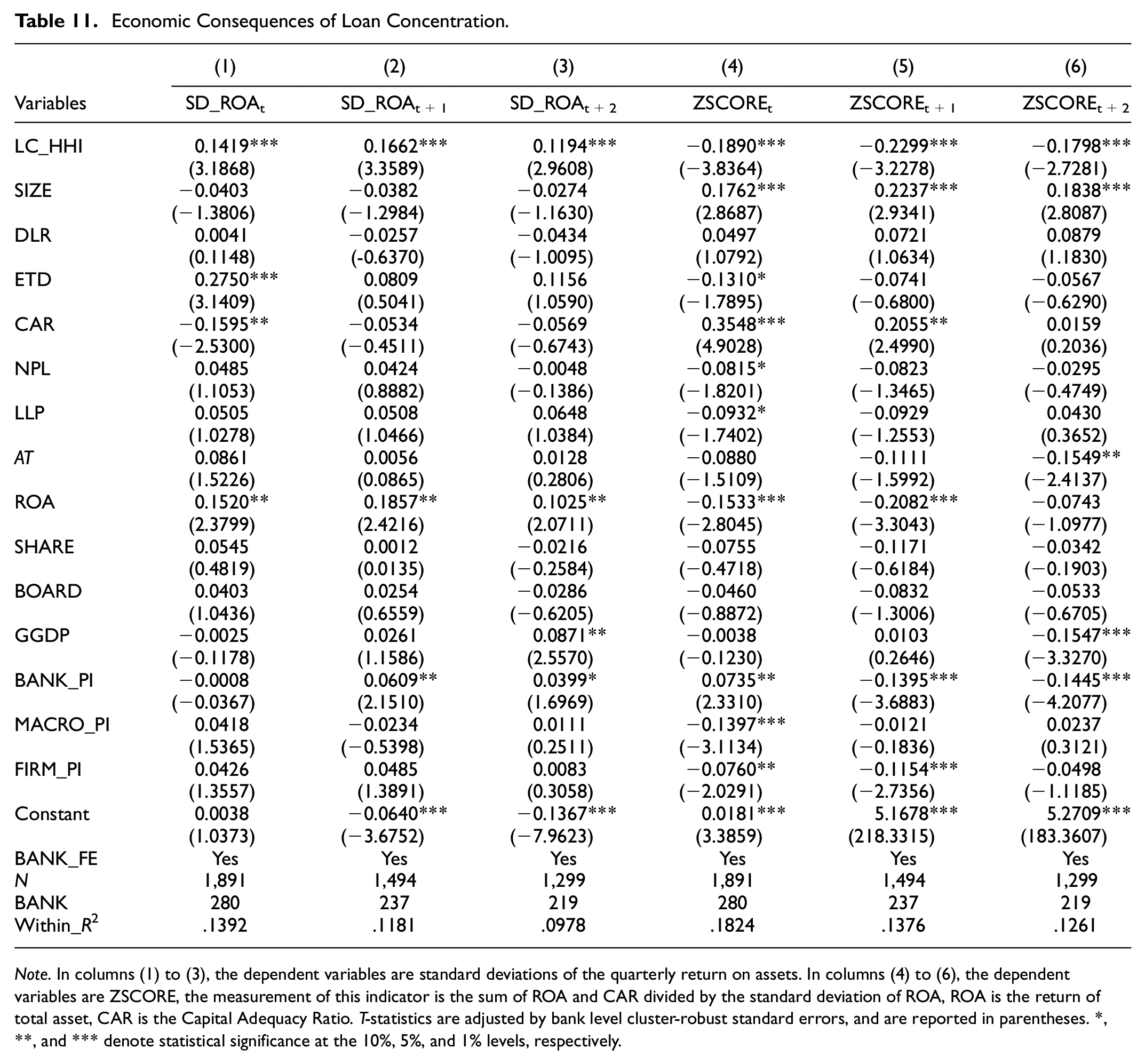

Loan Restructuring and Loan Risk Mitigation

We have observed that an increase in economic policy uncertainty prompts banks to adopt a more diversified structural strategy. Does the adoption of a diversified structural strategy result in a reduction in the operational risk faced by banks and an increase in operational stability? In columns (1) to (3), we use standard deviation of banks’ returns to capture the operation risk of commercial banks, and find that reduction in loan concentration has led to a decrease in the volatility of bank ROA in the subsequent 3 years. In columns (4) to (6), w use Z-score to measure the bankruptcy risk of banks, and find that reduction in loan concentration has led to a decrease of solvency risk in the subsequent 3 years. Overall, the regression results in Table 11 further validate the correctness of the main findings of our research.

Economic Consequences of Loan Concentration.

Note. In columns (1) to (3), the dependent variables are standard deviations of the quarterly return on assets. In columns (4) to (6), the dependent variables are ZSCORE, the measurement of this indicator is the sum of ROA and CAR divided by the standard deviation of ROA, ROA is the return of total asset, CAR is the Capital Adequacy Ratio. T-statistics are adjusted by bank level cluster-robust standard errors, and are reported in parentheses. *, **, and *** denote statistical significance at the 10%, 5%, and 1% levels, respectively.

Cross-Country Analysis

In order to validate the generalizability of the research conclusions in different countries and regions, we collected data from commercial banks in major countries between 2007 and 2020. A total of 7,087 commercial banks were included, with 99,162 observations. Specifically, the data included 11,690 observations from UK banks, 9,170 observations from French banks, 26,802 observations from German banks, 8,106 observations from Italian banks, 26,894 observations from Japanese banks, 3,402 observations from South Korean banks, and 13,818 observations from Russian banks. Based on this multinational sample, we re-examined the relationship between economic policy uncertainty and loan concentration. As shown in the regression results in Table 12, the relationship between economic policy uncertainty (EPU) and loan concentration (LC_HHI) remains significantly negative, indicating that the research conclusions are robust across different countries and regions.

Cross-Country Analysis.

Note. The sample are collected from other country banking system, including Great Britain, France, Germany, Italy, Russia, Japan, and Korea. The dependent variables for all columns are LC_HHI, independent variables are EPU for every country. In column (1), we control for bank fixed effect and year fixed effect. In column (2), we added control variables based on column (1). In column (3), we control for country fixed effect and year fixed effect. In column (4) we added control variables based on column (3). ***, ** indicates significance at the .01, .05 level or better, respectively.

Discussion

Conclusion

In recent years, both the domestic and international economic environments have become increasingly complex due to the occurrence unpredictable events. Examples of these events include the U.S.-China Trade War, the COVID-19 pandemic, and the Russia-Ukraine conflict. These events have had multidimensional impacts on China’s economic development, presenting significant challenges in formulating and implementing economic policies. As a result, economic policy uncertainties have had a growing influence on both the real economy and the financial system (Gulen & Ion, 2016; Nagar et al., 2019; Ng et al., 2020). Within Chinese indirect financing-based financial system, banks play a crucial role in connecting macroeconomic policies with enterprise behavior (Jiang et al., 2019). Consequently, they are directly and significantly affected by economic policy uncertainties (P. G. Berger et al., 2017; Ng et al., 2020). Our focus on addressing the following question: What measures will banks undertake to manage the impact of economic policy uncertainty when credit risk gradually increases due to these uncertainties? To answer this question, we empirically examine the relationship between economic policy uncertainty and loan concentration of Chinese commercial banks. The specific findings of our study are as follows: (1) We observe a significant negative relationship between economic policy uncertainty and bank loan concentration. As economic policy uncertainty increases, bank loan concentration decreases. This finding suggests that reducing loan concentration is a crucial measure for banks to manage the risks associated with economic policy changes. Even after conducting several robustness tests and considering endogeneity issues, the findings remain consistent, which is consistent with prior literature that banks will take measures to address the risks posed by economic policy uncertainty (P. G. Berger et al., 2017; Ng et al., 2020). (2) Through heterogeneity analysis, we find that the impact of economic policy uncertainty is more pronounced for banks with weaker risk resilience, such as regional banks, small-sized banks, and banks with low market share. (3) The mechanism analysis demonstrates that the business risk faced by enterprises is an important mechanism through which economic policy uncertainty affects the loan structure of banks, which is consistent with classical theory that high loan concentration can lead to excessive risk-taking (Tabak et al., 2011; Dhaliwal et al., 2016; Liberti et al., 2017). (4) Further analysis of the economic consequences of bank loan concentration reveals that reducing bank loan concentration effectively mitigates bank business risk and improves overall bank business stability.

Potential Impact of Exogenous Factors

Our study reveals that in a market environment with high economic policy uncertainty, Chinese commercial banks adjust their loan structures towards diversification to manage risk. The research conclusion also has certain reference value for understanding the current global economic situation. Today, China is the largest industrial nation in the world, often referred to as the “world’s factory.” At the same time, China maintains complex and extensive trade relations with other countries around the world, playing a crucial role in global economic activities. Therefore, external factors such as international policies and global economic events significantly impact the relationship between China’s economic policy uncertainty and the concentration of bank loans. Meanwhile, the relationship between China’s economic policy uncertainty and loan concentration also has a significant impact on the stable and prosperous development of the global economy.

From the perspective of influencing factors, international policies and economic events have a complex and far-reaching impact on China’s economic policy uncertainty. Chinese policy makers incorporate factors such as international trade policies, global economic conditions, international monetary policies, geopolitical risks, and recommendations from international organizations into their decision-making models when formulating economic policies. The presence of these factors compels the Chinese government to continuously adjust its economic policies to respond to international situations and risks, which in turn increases the level of domestic economic policy uncertainty. For example, recent U.S. presidential elections have demonstrated that different political parties in the U.S. hold varying trade and China policies. Consequently, the Chinese government needs to develop different economic and industrial policies to address different election outcomes, thus exacerbating domestic economic policy uncertainty. Especially during trade wars, when there is uncertainty about which industries will be subjected to trade sanctions and which are expected to face higher bad debt losses, maintaining a lower loan concentration is an important measure to mitigate the risks associated with changes in economic policies.

From the perspective of economic consequences, the relationship between economic policy uncertainty and loan concentration also has significant implications for the sustainable development of the global economy. As an engine of the world economy, Chinese enterprises, on one hand, need to import industrial raw materials such as oil and iron ore from around the world, and on the other hand, Chinese-produced industrial goods are sold globally. Similar to continental European countries like Germany, France, and Russia, China’s financial system is centered around its banking system, with most enterprises obtaining necessary funding for production and operations through bank loans. Therefore, when economic policy uncertainty leads to a reduction in loan concentration, it affects enterprises’ procurement, production, and sales activities. At a macro level, this translates into fluctuations in national-level raw material imports and industrial goods sales due to changes in loan scales, which in turn has indirect effects on upstream raw material exporting countries and downstream industrial goods purchasing countries. Overall, studying the causal relationship between economic policy uncertainty and loan concentration is of significant reference value for understanding the current international economic situation.

Policy Recommendations

These findings have significant policy implications: First, economic policy uncertainty has a substantial impact on banks’ loan structural strategies. Increased economic policy uncertainty raises the potential credit default risk for banks and reduces the stability of their operations. Especially against the backdrop of an increasingly turbulent international situation and the intensifying U.S.-China trade war, the risks of economic policy changes have intensified, and commercial banks are facing more severe crises. Therefore, commercial banks need to maintain a more reasonable loan structure, strengthen their ability to cope with external uncertainties. Considering the heterogeneity of the impact of economic policy uncertainty on banks’ liquidity creation, banks need to actively seek a differentiated and specialized development path based on their own characteristics such as scale and scope of operations, gradually gaining unique competitive advantages and room for sustainable development, in order to better serve the development of the real economy.

Second, adjusting the loan structure proactively based on economic policy uncertainty is feasible for commercial banks. This study finds that banks adjusting their credit structure based on economic policy uncertainty effectively reduces bankruptcy risk and enhances operational stability. Therefore, credit structure adjustments under economic policy uncertainty have a positive effect on the sustainable development of banking system. From the perspective of financial system risk prevention and improving financial security capabilities, this paper suggests that regulatory agencies should incorporate economic policy uncertainty into decision-making models to strengthen banks’ expectations management, and formulate policies based on a comprehensive analysis of China’s economic policy uncertainty and its impact on the real economy and financial institutions’ responses. This approach should consider the effects of economic policy uncertainty on credit structure and bank risk-taking, thereby improving bank risk supervision.

Third, Strengthen the banking system’s ability to identify and assess economic policy uncertainty, and guide the efficient allocation of credit resources. This study finds that the impact of economic policy uncertainty on bank loan concentration is heterogeneous. State-owned banks, large banks, and those with a significant market share are better able to mitigate the risks of economic policy changes by diversifying their loan portfolios. This phenomenon implies that banking regulators may lack necessary preparedness and requirements regarding economic policy uncertainty in China. In the presence of severe economic policy uncertainty, non-state-owned, smaller, and banks with a lower market share are more likely to suffer liquidity crises, potentially triggering major financial events that threaten national security. Therefore, it is urgent for regulatory agencies to develop detailed contingency plans for economic policy uncertainty. On one hand, they should guide banks in establishing differentiated risk control measures based on their characteristics. On the other hand, they should coordinate with other monetary and fiscal measures to enhance banks’ capacity to handle uncertainty, ensure liquidity, and improve credit allocation efficiency.

Footnotes

Acknowledgements

We thank the associate editor and the reviewers for their useful feedback that improved this paper.

Author Contributions

Chenxi Wang: Software, Resources, Methodology, Investigation, Data curation, Conceptualization, Funding acquisition. Ran Duan: Writing-original draft, Visualization, Supervision, Software, Methodology, Investigation.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Shantou University Research Start-up Fund Project “Governance Structure Changes and Internal Control Deficiency Standards Formulation: Mechanisms and Economic Consequences.” Project Number: STF22014. Scientific Research Project of Higher Education Institutions of Department of Education of Guizhou Province “Research on Enterprise Digital Transformation and Internal Control.” Project Number: (2022) No. 122.

Ethical Considerations

Our study examines the impact of uncertainty on bank loan restructuring, which uses financial data of banks, without involving humans or animals.

Consent Details

Our study examines the impact of uncertainty on bank loan restructuring, which uses financial data of banks, without involving humans or animals.

Data Availability Statement and Fig Share References

The data will be made available on request from the corresponding author.