Abstract

The impact of financial inclusion on health have largely remained underexplored in the existing literature, particularly in the ASEAN nations. This study is conducted to examine this impact using a sample of 14,815 observations collected from (i) the Gallup World Poll and the (ii) the World Bank Global Findex databases. Various estimation techniques, including (i)Lewbel’s (2012) IV estimations, and mediation analysis are utilized in this study. The empirical results indicate that financial inclusion positively affects health outcome, proxied by the Personal Health Index. Our mediation analysis confirms that income, education, food, and housing security emerge as key mediating channels through which financial inclusion improves health. The positive impact from financial inclusion on health outcome remains robust after accounting for a between-country variation using multilevel modeling and addressing potential endogeneity using Lewbel’s instrumental variable estimation. A country-specific analysis confirms that financial inclusion significantly improves health outcome in five ASEAN countries, including Singapore, Thailand, Indonesia, the Philippines, and Myanmar.

Plain Language Summary

This study examines the impact of financial inclusion on health by making essential financial products and services (e.g. bank accounts, credit, and insurance) accessible to all individuals and businesses, especially those in low-income or underserved communities in the ASEAN countries. We find that extending financial inclusion will support and improve health and this positive effect is more pronounced for women than men. This positive effect is also observed via various mechanisms including income, education, food and housing security in the ASEAN countries. These important findings call for the ASEAN governments to formulate and implement policies targeting extending providing essential financial products and services to the underserved communities in the nations.

Introduction

Health is considered one of the most important aspects of human well-being and a prerequisite to economic and social development. By definition, health is a state of complete physical, mental and social well-being and not merely the absence of disease or infirmity (World Health Organization, 2025). Achieving good health is fundamental among all countries around the globe and is one of the Sustainable Development Goals, particularly SDG-3 (UNICEF, 2025). According to the World Health Organization (2021), non-communicable diseases killed at least 43 million people globally. With non-communicable diseases being the cause of 70% of deaths globally, people in older age groups and in low- and middle-income countries experience more deaths and bear the heaviest health burden. Over half the world’s population lacks access to essential health services. Two billion people face severe financial hardship when paying out-of-pocket for the services and products they need (World Health Organization, 2023). Even though the globe has seen an increase in the number of people who are able to obtain selected health services, such as immunization and family planning, as well as antiretroviral treatment for HIV and insecticide-treated bed nets to prevent malaria, the progress is considered uneven (World Health Organization, 2025). In Southern Asia and Eastern Asia regions, various families still lack financial protection for healthcare services. The inequality in financial access to healthcare services remains a critical issue among low and lower-middle-income countries, with 74% of mothers and children of the wealthiest fifth of households receiving at least six of seven basic maternal and child health interventions. This rate is only 17% for the poorest fifth of households in low and lower- middle income countries. Deloitte reports that health inequities account for approximately $320 billion in annual healthcare spending, signaling an unsustainable crisis for the industry (Deloitte, 2022). Thus, there is a rising need to counter health issues in Southeast Asian nations.

Simultaneously, the Association of Southeast Asian Nations, or ASEAN, experiences a significant rise as a dynamic economic hub. In 2023, the combined GDP of ASEAN Member States was USD 3.8 trillion. The region also plays a crucial role in global trade by being the third-largest trader globally, with $3.6 trillion (ASEAN, 2024). From 2011 to 2019, Myanmar experienced an average 6% rate of economic growth annually, with a significant reduction in poverty (World Bank, 2025). Cambodia is among the fastest growing countries, with a real GDP growth rate of 6.1% in 2024 along with a GDP per capita growth rate of 6.34%. Furthermore, ASEAN’s demographic power of a combined population exceeding 650 million crucially contributes to economic growth of the region (World Bank, 2025). In 2023, there were 67 million households in ASEAN that are part of the “consuming class” who made significant discretionary purchases. This number is projected to double to 125 million households, turning ASEAN into a dynamic consumer market in 2025. According to the World Economic Forum, ASEAN’s top priority is to leverage its demographic strength, promote digital transformation and enhance human welfare to achieve its full potential. In this context, financial inclusion, defined as the accessibility to affordable and adequate financial services that can help them build wealth, including savings, credit, loans, equity, and insurance, is a catalyst for achieving 7 of the 17 Sustainable Development Goals (SDGs; World Bank, 2025). Thus, there is a need for financial inclusion in Southeast Asia countries, shown through the Strategic Action Plans (SAPs) of the ASEAN Financial Integration 2016 to 2025, which includes policy actions, targets and milestones to promote financial inclusion in the region. In line with the common goal of ASEAN, an important question has emerged: Does financial inclusion matter to health in the ASEAN countries?

Prior research has extensively examined the diverse impacts of financial inclusion on enhancing human capital and demographic aspects, including reducing poverty (Churchill & Marisetty, 2020; Koomson et al., 2024), promoting education and employment (Célerier & Matray, 2019; Wang et al., 2024), and financial distress (Yue et al., 2022). Similarly, financial inclusion highlights its role in improving numerous banking and economic aspects, namely risk reduction (Yang & Masron, 2024); bank entry, deposits and lending (Fonseca & Matray, 2024); tourism demand (Gopalan & Khalid, 2024); and economic growth (Liu et al., 2021). The literature also examines the influence of financial inclusion on the environment, such as reducing pollution (Shahbaz et al., 2022), mitigating ecological footprint (Qing et al., 2024), and increasing energy efficiency (Khan et al., 2024). However, few studies have examined the relationship between health benefits and financial inclusion, particularly in Southeast Asia countries.

This study makes three contributions to the existing literature on financial inclusion and health. First, this study examines the effect of financial inclusion on health in the ASEAN countries, which has received limited attention in previous research. Interestingly, by conducting country-specific analyses, our results imply that the effect of financial inclusion on health is influenced by country-specific contexts. Second, we investigate the heterogeneous impact of financial inclusion on health outcomes by gender that remains underexplored in the existing literature. Our findings reveal that while financial inclusion benefits both men and women, the health benefits of financial inclusion are more pronounced for women compared to men. Third, we identify income, education, food security, and housing security as key mediating channels through which financial inclusion enhances health, contributing to a deeper understanding of the mechanisms underlying this relationship.

Following this introduction, the remainder of the article is structured as follows. Section “Literature Review and Hypothesis Development” reviews the relevant literature and develops research hypotheses. Section “Data and Methodology” details the data sources and model specifications. Section “Results” presents the empirical results and discussions. Finally, section “Concluding Remarks” concludes and discusses policy implications derived from our results.

Literature Review and Hypothesis Development

Impacts of Financial Inclusion

Enhanced financial inclusion is associated with better human capital and demographic aspects. Wang et al. (2024) consider that digital financial inclusion, through improving credit availability, social capital, and non-agricultural employment, is crucial in reducing multidimensional poverty in China's rural areas and central-western regions. Similarly, Churchill and Marisetty (2020) demonstrate that the relationship between financial inclusion and poverty reduction is robust among various proxies and measurements of poverty and financial inclusion. Regarding the influence of financial inclusion on other aspects of human capital, the positive effects of financial inclusion are larger on male and rural-located children. This effect is gained through improved living conditions, health, education levels, income, and asset accumulation (Célerier & Matray, 2019; Koomson et al., 2024) since families with accounts, indicating higher financial inclusion, are more likely to send their children in school, be literate, work, and have higher occupational income, business ownership, and real estate wealth (Stein & Yannelis, 2020) even in period of shocks (Abiona & Koppensteiner, 2022). Regardless of other benefits, financial inclusion is also associated with higher financial distress (Yue et al., 2022).

In addition, financial inclusion is associated with risk-reducing effects, meaning that financial inclusion is crucial in risk reduction and risk assessment accuracy (Yang & Masron, 2024). Furthermore, financial inclusion enhances not only bank entry, deposits and lending but also entrepreneurship, employment, and wage growth (Fonseca & Matray, 2024). This effect is stronger, especially in cities with insufficient number of commercial banks. Financial inclusion is associated with higher credit market participation (Yue et al., 2022). Similarly, digital inclusive finance services have a positive impact on mitigating the negative impacts of traditional inclusive loans. Using data from 85 emerging markets and developing economies around the globe, Gopalan and Khalid (2024) find that financial inclusion strongly promotes tourism demand, and that financial inclusion plays a significant role in raising tourism revenue for these countries. Utilizing data from 2011 to 2019 in China, Liu et al. (2021) show that digital financial inclusion has noteworthy effects on economic growth. Their analysis also finds that two important channels through which digital financial inclusion benefits economic growth are promoting small and medium-sized enterprise entrepreneurship and stimulating residents’ consumption.

Various studies find the positive effects of financial inclusion on ecological sustainability. For the G20 nations, inclusive finance demonstrates a notable mitigation effect on the ecological footprint (Qing et al., 2024). In upper-middle-income countries such as Malaysia, financial inclusion increases energy efficiency, and the impact is overall positive for each quantile (Khan et al., 2024). However, another strand of the literature finds no evidence to support the positive relationship between financial inclusion and environmental benefits. Le et al. (2020) argue that though financial inclusion appears to have led to higher emissions of carbon dioxide in the region, their empirical results imply that there are no policy synergies between financial inclusion and lower carbon dioxide emissions. Increased financial inclusion is found to reduce the collaborative reduction of pollutant and carbon emissions in different geographical locations with different levels of pollution (Shahbaz et al., 2022).

Few papers closely examine the relationship between financial inclusion and subjective health. Banerjee et al. (2023) finds that financial inclusion positively influences life expectancy and infant mortality rates, which are proxies for objective health. Similarly, Immurana et al. (2021) show that financial inclusion promotes life expectancy and reduces death rates. Another study by Heyert and Weill (2024) indicates that financial inclusion enhances individual happiness. The results from the study by Ajefu et al. (2020) show that financial inclusion positively impacts mental health. Our article fills in the gap by analyzing the influence of financial inclusion on health, thus capturing individuals’ self-perceptions of their overall health status and well-being.

A Theoretical Background

The social determinants of health hypothesis by the World Health Organization (2021) states that the conditions in which people are born, grow, work, live, and age, and the wider set of forces and systems also influence human health. This hypothesis serves as the theoretical foundation to explain and predict the relationship between financial inclusion and health. Financial inclusion increases the capital available for investments in education, stable food supply, housing, environment, and timely health services, allowing individuals to prioritize preventive care and maintain better health. Moreover, when individuals gain access to financial products and services (i.e., a higher level of financial inclusion), they can save money, secure loans to start businesses, and manage financial shocks like unexpected medical expenses or job loss. While financial inclusion predominantly offers positive effects on health, it is worth noting potential downsides, such as the risk of over-indebtedness. Access to credit, if mismanaged, can lead to excessive debt, increasing financial strain and potentially worsening mental health. For instance, Karlan and Zinman (2010) find that while expanding credit access improves food consumption, economic self-sufficiency, and certain aspects of mental well-being, it can also have adverse effects, particularly by increasing stress levels. However, these negative impacts can be minimized or offset through appropriate lending policies and consumer protection policies. Thus, we propose the following hypothesis:

The effects of financial inclusion on health may vary by gender, with women potentially experiencing greater benefits due to their unique socioeconomic roles and constraints. In many societies, women face disproportionate barriers to financial access, making them more likely to be excluded from formal financial systems. When women gain access to financial services, they not only improve their own economic status but also tend to direct resources toward family well-being. Behavioral economics suggests that women are more likely than men to spend on healthcare and education for their households (Duflo, 2012; Thomas, 1990, 1993). This spending pattern amplifies the health benefits of financial inclusion for women and their dependents, such as children. Additionally, financial inclusion can enhance women’s decision-making power within the household, a critical factor in contexts where gender norms limit their agency. For women, financial inclusion thus acts as a powerful tool to enhance both their economic and health capabilities. On these observations, we develop the following research hypothesis.

By providing access to credit and savings, financial inclusion enables individuals to enhance their knowledge and increase access to economic progress, which in turn boosts their income (Swamy, 2014). Higher-income levels directly improve health by increasing the ability to purchase health-related goods and services. For example, individuals with more financial resources can afford better nutrition, essential for preventing malnutrition and related illnesses, and access quality healthcare, including preventive measures and timely treatments (Dahl, 1996; Von Dem Knesebeck et al., 2016). Furthermore, increased income reduces chronic stress (Baird et al., 2013; Hall et al., 2022; Shields-Zeeman et al., 2021), which is known to harm both mental and physical health. Through this mechanism, financial inclusion translates economic gains into tangible health improvements.

Financial inclusion, such as student loans and savings, may support education financing, allowing individuals to overcome financial constraints, acquire higher levels of education (Li & Peng, 2023) and achieve higher attendance rates (Sakyi-Nyarko et al., 2022). Higher educational levels have been shown to enhance health literacy and promote better health-related decision-making. For instance, individuals with higher educational levels are associated with lower physical or mental disorders, particularly depression (Dear et al., 2002). Furthermore, better-educated people are less likely to smoke, less likely to be obese, less likely to be heavy drinkers, more likely to drive safely and live in a safe house, and more likely to use preventive care (Cutler & Lleras-Muney, 2010). Thus, financial inclusion contributes to an improved state of health through the channel of education.

Higher accessibility to financial services might enable individuals to ensure their capital, stabilize smooth consumptions, and invest in income-generating activities, thus improving food security. Studies have shown that financial inclusion, through enhancing entrepreneurship and equipping households with better financial status, positively influences food security (Koomson et al., 2023). Particularly, digital financial inclusion directly contributes to the level of coordinated development of food production ensuring supply (Liu & Ren, 2023). By mitigating food insecurity, financial inclusion might promote better health outcomes. Food insufficiency and the lack of nutrition, as a result of high food insecurity, could damage residents’ mental and physical health. Individuals from food-insufficient households have significantly higher odds of reporting poor/fair health, suffering from major depression and distress (Vozoris & Tarasuk, 2003), and experiencing compromised psychosocial functioning (Olson, 1999). Hunger also negatively impacts children’ mental and physical health (Weinreb et al., 2002). Therefore, improved financial inclusion might mitigate the negative impacts of food insecurity on human health.

Financial inclusion plays a pivotal role in reducing housing insecurity. Access to financial services enables individuals to secure stable housing through mechanisms such as mortgage financing, rental assistance, and the ability to accumulate savings for housing needs. For instance, federal funding increases sheltered homelessness (Lucas, 2017). Housing instability, characterized by frequent moves, overcrowding, or difficulty paying rent, has been associated with not having a usual source of care, postponing needed medical care, postponing medications (Kushel et al., 2006), higher prevalence of overweight/obesity, hypertension, diabetes, and cardiovascular disease (Gu et al., 2023). By facilitating financial stability, financial inclusion helps individuals maintain consistent and adequate housing, thereby reducing the health risks associated with housing insecurity. Moreover, stable housing provides a foundation for accessing healthcare services, maintaining employment, and supporting overall well-being.

Data and Methodology

Data

This study utilizes data collected from two distinct sources: the Gallup World Poll (GWP) and the World Bank Global Findex (WBGF) database. Specifically, we obtain data on health from GWP, using the Personal Health Index as a key measure. The control variables are also collected from GWP, including gender, age, marital status, employment status, and place of residence. Meanwhile, data on financial inclusion for individual is collected from WBGF. Below, we provide an overview of these two datasets and describe the procedure to merge these two datasets using the unique respondent identifiers.

The World Bank Global Findex Database (WBGF) was first conducted in 2011 and has been updated in subsequent waves in 2014, 2017, and 2021. It serves as a definitive source of global data on financial access, covering payments, savings, and borrowing behaviors. The 2021 edition, based on nationally representative surveys of approximately 128,000 adults across 123 economies, provides updated indicators on the access to and usage of both formal and informal financial services, as well as digital payments. The dataset also offers insights into the financial behaviors that foster financial resilience and highlights disparities in financial service access among women and low-income individuals. Notably, the WBGF survey is conducted by Gallup Inc., in parallel with the Gallup World Poll, meaning that these two datasets share the same respondents.

Each respondent has a unique identifier, allowing us to merge the two datasets. Since this study focuses on ASEAN countries, we attempt to merge all available waves of WBGF with GWP for these countries. However, we encounter two limitations. In 2011, the WBGF did not provide respondent identifiers in the publicly available dataset, preventing us from matching it with the 2011 GWP. In 2021, while respondent identifiers were included in WBGF, they did not match those in the 2021 GWP, making the merging process infeasible.

As a result, we can merge only the 2014 WBGF with the 2014 GWP and the 2017 WBGF with the 2017 GWP. Our final sample consists of 17,222 observations in 2014 and 2017, covering 8 ASEAN countries, namely Cambodia, Indonesia, Laos, Myanmar, the Philippines, Singapore, Thailand, and Vietnam.

Dependent Variable

The Personal Health Index is used as the dependent variable in this study, capturing individuals’ self-perceptions of their overall health status. The Personal Health Index focuses on subjective assessments, providing valuable insights into how individuals evaluate their own health and well-being. Self-reported health measures are widely used in health economics and public health research, as they strongly correlate with actual health outcomes, healthcare utilization, and labor outcomes (Blundell et al., 2023; Idler & Benyamini, 1997; Lorem et al., 2020). The Personal Health Index is constructed using survey responses from the Gallup World Poll (GWP), which collects self-reported health data from individuals across more than 150 countries. The index is based on a set of standardized questions that assess various dimensions of personal health, including physical health limitations, quality of rest, and emotional well-being. These questions allow researchers to quantify subjective health experiences and compare them across populations and time periods.

The Personal Health Index specifically incorporates responses to key survey items that assess different aspects of well-being. The first component is physical limitations, which are measured by asking respondents whether they have health problems that prevent them from performing daily activities and whether they experienced significant physical pain during the previous day. The second component is rest and recovery, assessed by asking respondents whether they felt well-rested the previous day. The third component is emotional well-being, measured by asking respondents whether they experienced feelings of worry or sadness during the previous day. This structure ensures a comprehensive evaluation of health by capturing physical, restorative, and emotional dimensions.

Independent Variables

The key independent variable in this study is financial inclusion. We construct the financial inclusion index using data from the WBGF, applying principal component analysis (PCA) to capture key dimensions of financial access and usage. Specifically, the financial inclusion index encompasses five key dimensions. The first is bank account ownership and usage, measured by asking whether the respondent has an account. If the respondent has an account, we further assess usage by asking whether they made any deposits into the account in the past year and whether they withdrew money from it during the same period. The second dimension is debit card ownership and usage, measured by asking whether the respondent has a debit card and, if so, whether they used it in the past year. Similarly, the third dimension, credit card ownership and usage, follows the same approach. The fourth dimension is formal savings, assessed by asking whether the respondent saved money at a formal financial institution in the past year. The fifth dimension, formal borrowing, is measured using a similar approach. These five dimensions are largely in line with the measurement of financial inclusion in previous studies (Grohmann et al., 2018; Nguyen et al., 2023). Finally, we apply PCA to these measures to construct the financial inclusion index, ensuring a comprehensive and statistically robust representation of financial inclusion.

We have conducted various analyses to assess the appropriateness of the financial inclusion index. The Bartlett test of sphericity strongly rejects the null hypothesis that the variables used to construct the index are not intercorrelated at the 1% significance level. The Kaiser–Meyer–Olkin (KMO) measure of sampling adequacy is .8400, well above the threshold of .5. Similarly, Cronbach’s alpha is .8664, exceeding the threshold of .7. Overall, these statistics confirm the appropriateness of the financial inclusion index.

Furthermore, following previous studies (Elgar et al., 2021; Lesner, 2025; Macchia & Oswald, 2021; Nazar et al., 2025), we control for respondents’ socioeconomic and demographic characteristics to mitigate the risk of confounding bias. These control variables include gender, age, marital status, employment status, and place of residence, all of which are collected from the GWP. Overall, these control variables are selected based on previous empirical studies.

Model Specifications

We estimate Equation 1 as specified below.

where i indicates the respondent.

For the baseline result, the ordinary least squares (OLS) estimation is used to estimate Equation 1. However, as our data exhibit a hierarchical structure, with respondents nested in countries, there are two levels in our data: (i) individual level and (ii) country level. Although we already control for country-fixed effects to mitigate the potential confounding bias arising from different characteristics of each ASEAN country, some may argue this is not sufficient. As such, we adopt multilevel modeling as a robustness check in this study.

Multilevel Modeling

Multilevel modeling, also referred to as hierarchical linear modeling, is a statistical technique specifically designed to analyze data with a nested or hierarchical structure, such as individuals clustered within countries (Gelman & Hill, 2007; Raudenbush & Bryk, 2002). This approach explicitly accounts for the hierarchical nature of the data by modeling both within-group (individual-level) and between-group (country-level) variations. In our study, respondents are nested within countries, suggesting that observations within the same country may be correlated due to shared economic development and institutions. Multilevel modeling addresses this by incorporating random effects at the country level, allowing the intercept to vary across countries.

One primary advantage of multilevel modeling is its ability to handle the correlation among observations within the same cluster. Ignoring this clustering, as might occur in a standard OLS regression, can lead to underestimated standard errors, thereby inflating the risk of Type I errors and producing misleading statistical inferences (Snijders & Bosker, 2012). By contrast, multilevel modeling adjusts for this within-country correlation, yielding more accurate standard errors and more reliable hypothesis tests. In comparison, while the inclusion of country-fixed effects in our baseline OLS model controls for time-invariant country-specific characteristics—such as institutional or geographic factors—it assumes that the error terms are independent across individuals. This assumption is likely violated in hierarchical data, where unobserved country-level factors may influence all individuals within a given country similarly. Country-fixed effects mitigate confounding due to these unobserved factors but do not explicitly model the dependency within clusters or allow for variation in the relationship of interest across countries. Another advantage of multilevel modelling is that it allows us to incorporate country-level variables such as economic development, infrastructure, institutional quality and financial development, which may both affect financial inclusion and personal health. Thus, multilevel modeling operates more effectively than country-fixed effects alone in this context because it accounts for the hierarchical structure of the data, corrects for within-country correlation, and provides a richer understanding of both average and country-specific effects. This robustness check enhances the validity of our findings by ensuring that our estimates are not biased due to the nested nature of the data.

Lewbel’s (2012) IV Estimation

We employ Lewbel’s (2012) IV estimation to check whether potential endogeneity issues are severe in our model as a further robustness analysis. This method is a powerful tool for assessing the robustness of models when strong and reliable instruments are lacking. Consequently, Lewbel’s (2012) method has been widely utilized in economics research in recent years (see, e.g., Cheng et al., 2025; Garg et al., 2025; Gozgor et al., 2025; Howard et al., 2025; Kamguia et al., 2025; Nguyen et al., 2025; Opoku et al., 2025; Yu et al., 2025). Specifically, Lewbel’s (2012) method is an econometric technique designed to address endogeneity in regression models when traditional external instrumental variables (IVs) are unavailable or difficult to justify. Endogeneity may arise in our analysis due reverse causality—for example, if healthier individuals are more likely to seek financial inclusion, rather than financial inclusion solely improving health. Such issues could bias our OLS estimates, undermining the causal interpretation of the relationship between financial inclusion and personal health.

In conventional IV approaches, identification relies on excluded instruments that are correlated with the endogenous regressor (financial inclusion) but uncorrelated with the error term. However, finding valid instruments that satisfy these conditions is often challenging, particularly in studies of financial inclusion and health across multiple countries. Lewbel’s (2012) method offers an alternative by constructing internal instruments from the existing variables in the model, leveraging heteroskedasticity in the data. The approach assumes that the error terms exhibit heteroskedasticity and that this heteroskedasticity is correlated with the endogenous regressor. Under these conditions, Lewbel’s (2012) method generates instruments based on the higher moments of the data (e.g., interactions between centered variables and their residuals), which are then used in a two-stage least squares (2SLS) framework to obtain consistent estimates. We empirically test these conditions in the results section. We show that they are satisfied, confirming the suitability of Lewbel’s (2012) method in our case

The benefits of Lewbel’s (2012) method are manifold. First, it eliminates the need for external instruments, which may be unavailable or theoretically contentious in our context. Second, it provides a practical solution for testing the robustness of our baseline OLS results to endogeneity, enhancing the credibility of our findings. By applying Lewbel’s (2012) method, we can assess whether such bias is present and obtain estimates that are robust to this concern.

Results

The Descriptive Statistics

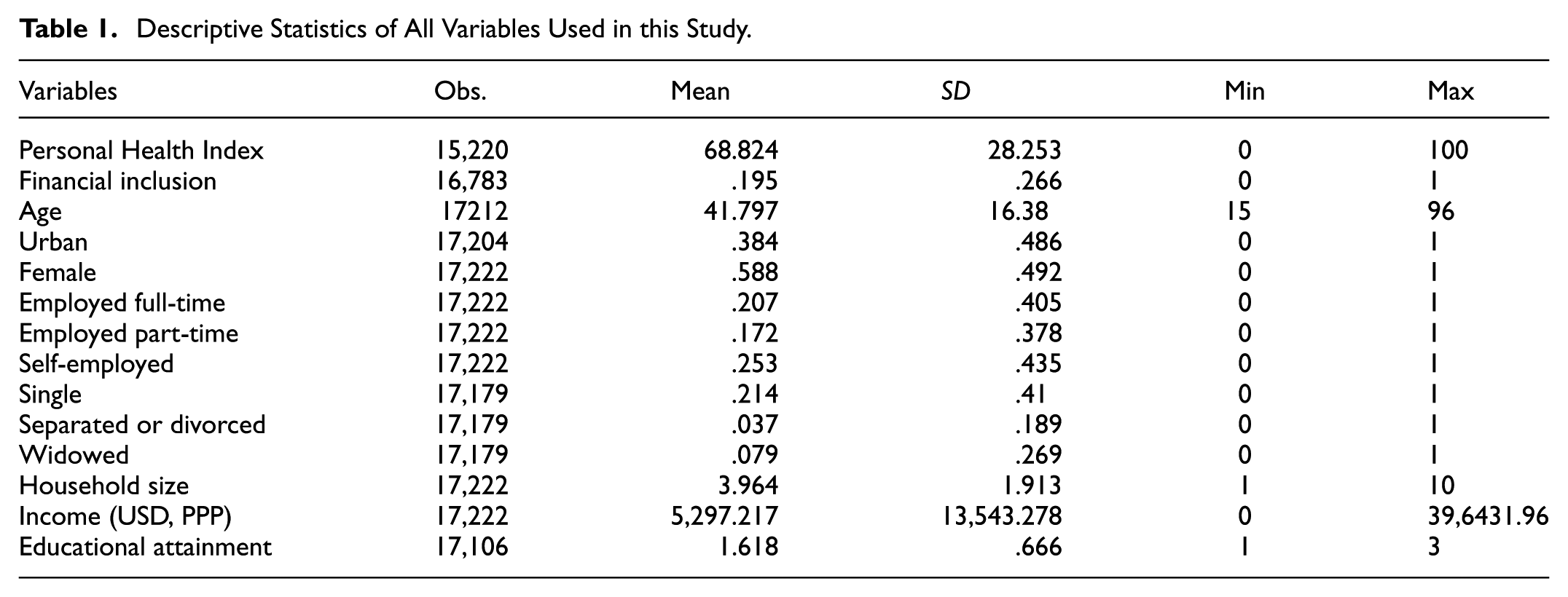

Table 1 presents the descriptive statistics for the variables used in this study. The Personal Health Index, our primary outcome variable, ranges from 0 to 100, with a mean of 68.824 and a standard deviation of 28.253. This suggests a moderate average level of personal health, with substantial variation across individuals. The financial inclusion index, which ranges from 0 to 1, has a mean of .195 with a standard deviation of .266, implying that on average, individuals in the sample exhibit relatively low levels of financial inclusion and there are significant disparities in financial inclusion among the ASEAN countries.

Descriptive Statistics of All Variables Used in this Study.

Figure 1 illustrates financial inclusion trends across eight Southeast Asian countries between 2014 and 2017. Singapore exhibits the highest financial inclusion level, increasing from .5709 in 2014 to .6607 in 2017. Meanwhile, Cambodia shows a decline in financial inclusion, dropping from .0592 to .0511. A similar downward trend is observed in Myanmar (.0593–.0564), the Philippines (.1315–.1113), and Malaysia (.3695–.0953). In contrast, Indonesia and Vietnam experienced modest increases in financial inclusion, from .1540 to .1679 and .1091 to .1273, respectively. Thailand’s financial inclusion level remained nearly unchanged, at .2897 in 2014 and .2888 in 2017.

Financial inclusion in 2014 and 2017.

Figure 2 presents the Personal Health Index across the same countries during the same period. Health outcomes exhibit mixed trends. Singapore, Vietnam, and the Philippines maintain relatively high levels of health, with relatively small fluctuations, while Thailand and Myanmar experience substantial declines. Thailand’s Personal Health Index falls from 76.08 in 2014 to 68.22 in 2017, and Myanmar’s index drops significantly from 73.14 to 64.35. Indonesia also sees a decline, from 77.76 to 73.7, while Cambodia reports a slight improvement, from 53.6 to 55.59.

Personal Health Index in 2014 and 2017.

These findings highlight different trends in financial inclusion and health outcome across ASEAN countries. While some countries demonstrate improvements in financial inclusion, others have stagnated. Similarly, while health indicators have improved in some countries, several nations have witnessed declining health outcomes.

The Basis Results—The Effect of Financial Inclusion on Health Outcomes in the ASEAN Countries

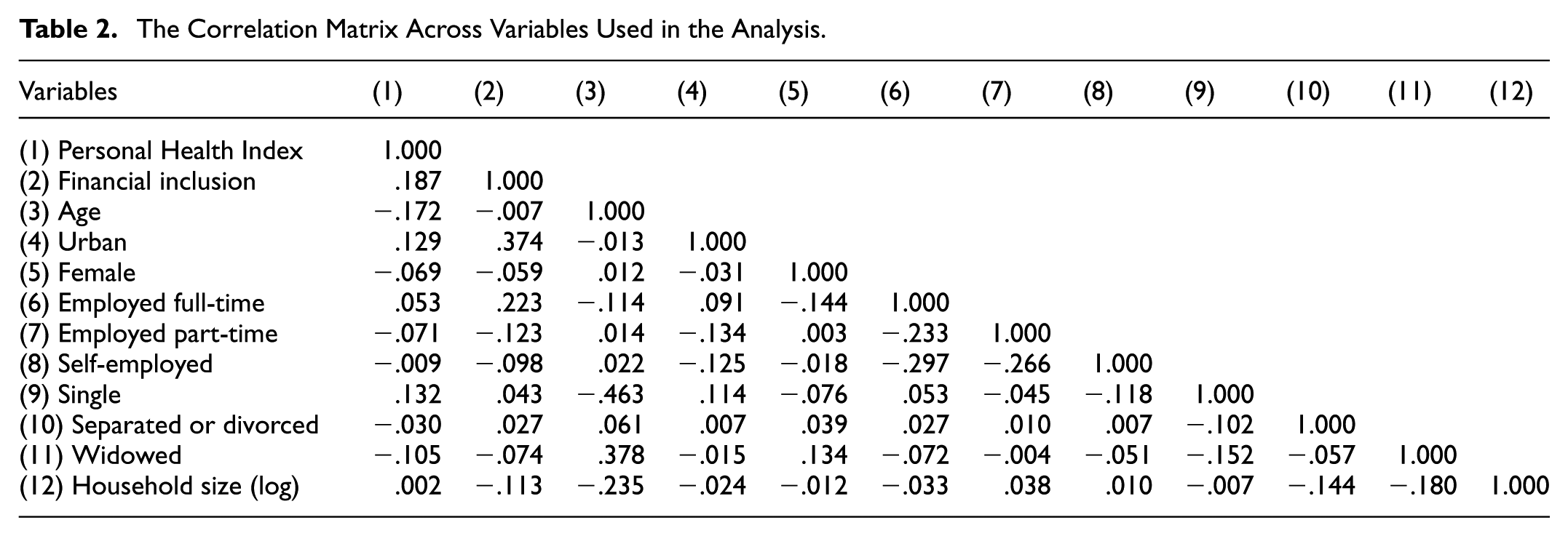

First, we assess whether multicollinearity poses a significant issue in our model by examining the pairwise correlation matrix and variance inflation factor (VIF) analysis, reported in Tables 2 and 3, respectively. The correlation matrix (Table 2) shows that no pair of variables exhibits an excessively high correlation level. Similarly, the mean VIF score remains well below the conventional threshold of 5 (Table 3). Therefore, multicollinearity is not a critical concern in our model.

The Correlation Matrix Across Variables Used in the Analysis.

The Variance Inflation Factor (VIF).

Next, we estimate the impact of financial inclusion on health using OLS estimation. To mitigate potential confounding bias, we control for individual characteristics. The results, presented in Table 4, indicate that financial inclusion has a statistically significant and positive effect on health (Column 1). Specifically, a one-standard-deviation increase in financial inclusion corresponds to a 4.667-point (=.266 × 17.545) increase in the Personal Health Index.

Empirical Results of the Impact of Financial Inclusion on Health Using the OLS Estimations.

Note. Robust standard errors are in parentheses.

p < .01. **p < .05. *p < .1.

In Column 2, we introduce time-fixed effects to account for time-varying factors that may simultaneously affect financial inclusion and health across ASEAN countries. The effect of financial inclusion remains positive and significant, reinforcing the robustness of our findings. In Column 3, we further include country-fixed effects to control for time-invariant factors such as geographic characteristics and cultural differences, which could otherwise bias our estimates. While financial inclusion continues to exhibit a statistically significant and positive impact on health, the effect size decreases. A one-standard-deviation increase in financial inclusion now corresponds to a 2.586-point (=.266 × 9.723) increase in the Personal Health Index. Overall, our findings provide strong evidence that financial inclusion has a positive and significant impact on health outcomes in ASEAN countries.

The Gender-Based Analysis: Men Versus Women

Understanding whether and how the relationship between financial inclusion and health outcomes varies by gender is both a critical and intellectually compelling endeavor. Males and females often confront distinct health challenges, exhibit differing health-related behaviors, and face unequal access to resources, all of which may shape the impact of financial inclusion on their well-being. For instance, women in many contexts, including the ASEAN region, encounter systemic barriers to healthcare access, such as socio-cultural restrictions, limited economic autonomy, and disproportionate caregiving responsibilities, that heighten their vulnerability to poor health outcomes (World Health Organization, 2019). Financial inclusion, by providing access to savings, credit, and insurance, may disproportionately benefit women by empowering them to overcome these barriers, secure healthcare services, and invest in preventive care. Men, who typically enjoy greater financial and healthcare access, may experience less pronounced incremental health gains from financial inclusion.

Additionally, gender differences in financial decision-making is also another motivation for moderation analysis. Evidence suggests that women are more inclined to allocate financial resources toward family health and well-being, including expenditures on nutrition and medical care for dependents (Duflo, 2012; Thomas, 1990, 1993). This behavior implies that financial inclusion may provide a multiplier effect on health outcomes for women, extending benefits beyond themselves to their households. In contrast, men may prioritize income-generating activities or personal consumption, potentially weakening the direct link between financial inclusion and their own health. These behavioral disparities, combined with persistent gender gaps in financial access evidenced by women’s lower-level financial inclusion (Klapper et al., 2022) underscore the need to examine whether financial inclusion serves as a lever for reducing gender-based health inequities.

We divide the sample into male and female to investigate the impact of financial health on females and males’ health separately. The results are reported in Table 5. Financial inclusion significantly and positively influences the health of both males (Column 1) and females (Column 2). The impact of financial inclusion on females’ health is larger than that of male. Similarly, when using full sample, and add the moderating term Financial inclusion * Female into the model, the moderating term is positive and significant. This means that financial inclusion is more beneficial to females’ health than males.

Moderation Analysis.

Note. Robust standard errors are in parentheses.

p < .01. **p < .05. *p < .1.

To explore these gender differences, we divide the sample into male and female subgroups and estimate the effect of financial inclusion on health outcomes separately for each. The results, presented in Table 5, demonstrate that financial inclusion exerts a significant and positive influence on the health of both males (Column 1) and females (Column 2). Notably, the magnitude of this effect is substantially larger for females than for males. The coefficient on financial inclusion in the female subsample exceeds that in the male subsample, indicating that women experience greater health improvements from enhanced financial access.

To robustly confirm this differential impact, we employ a second approach using the full sample and incorporate an interaction term, Financial inclusion * Female, into the regression model. The results reveal that this moderating term is both positive and statistically significant, reinforcing the finding that financial inclusion yields a stronger beneficial effect on women’s health compared to men’s. This consistency across subgroup and interaction analyses enhances confidence in the robustness of our conclusions. These results support hypothesis 2, which is that the effect of financial inclusion on women’s health is greater than its effect on men’s health.

These findings align with the theoretical expectations articulated above. The larger effect of financial inclusion on women’s health likely reflects their greater baseline vulnerability to financial exclusion and healthcare access constraints, as well as their tendency to channel financial resources into health-enhancing activities. For men, while financial inclusion remains beneficial, its relatively smaller impact may stem from their pre-existing advantages in resource access, which diminish the marginal health gains derived from additional financial tools.

The implications of these results are twofold. Theoretically, they underscore gender as a pivotal moderator in the nexus between financial inclusion and health, highlighting the necessity of disaggregating data by gender in future studies of socioeconomic determinants of well-being. Practically, they suggest that financial inclusion initiatives may deliver outsized health dividends when targeted toward women, particularly in regions where gender disparities in financial and healthcare access remain entrenched. Policymakers could leverage these insights to design interventions, such as women-focused financial literacy programs or subsidized health insurance schemes, that maximize health equity gains.

Robustness Checks

To assess the robustness of our results to potential biases, we employ two approaches: multilevel modeling and Lewbel’s (2012) instrumental variable (IV) estimation. The rationale for using these methods has been discussed in section “Model Specifications.”

First, we present the results from multilevel modeling in Table 6. Even after accounting for between-country variation, financial inclusion continues to exhibit a positive and significant effect on health (Column 1). To further validate the robustness of our findings, we incorporate macro-level variables that could simultaneously influence both financial inclusion and health. Specifically, we include GDP per capita (in logarithmic form) to control for economic growth, internet penetration and electricity access as proxies for infrastructure, the rule of law index as a proxy for institutional quality, and the IMF’s financial development index to account for financial sector development. After incorporating these controls into the model, the results remain largely unchanged (Columns 2–6), further confirming the robustness of our findings.

Multilevel Modelling.

Note. Robust standard errors are in parentheses.

p < .01. **p < .05. *p < .1.

Next, we examine whether endogeneity poses a serious concern that could bias our results by employing Lewbel’s (2012) IV estimation. This method exploits the presence of heteroscedasticity in the model to generate valid instrumental variables internally, eliminating the need for external instruments. The Breusch–Pagan/Cook–Weisberg test confirms the existence of heteroscedasticity, validating the appropriateness of Lewbel’s (2012) approach. The results, reported in Table 7, indicate that financial inclusion provides a positive and significant effect on health. The F-test statistic far exceeds the conventional threshold of 10, suggesting that our instruments are strong. Additionally, the Hansen J-test is not statistically significant, implying that our instruments satisfy the exogeneity condition. Overall, these tests suggest that Lewbel’s (2012) IV estimates are reliable.

Lewbel-IV Estimations.

Note. Robust standard errors are in parentheses.

, **, and * are statistically significant at 1, 5, and 10 percent.

A one-standard-deviation increase in financial inclusion leads to a 2.623-point increase in the Personal Health Index (.266 × 9.859), a result closely aligned with the estimate obtained from OLS estimation (Column 3 of Table 4). Moreover, the Durbin–Wu–Hausman endogeneity test is not statistically significant, failing to reject the null hypothesis of no endogeneity in our model. This further reinforces the reliability and robustness of our findings.

Country-Specific Analysis

As a further analysis, we divide the full sample by country to examine whether the effect of financial inclusion on health varies across ASEAN nations. There are several reasons why this effect may differ between countries. First, differences in financial development play a crucial role. Countries with well-developed financial systems, such as Singapore, may experience a stronger link between financial inclusion and health, as individuals have better access to formal financial services, including health insurance and emergency savings. In contrast, in countries with less developed banking systems, such as Laos and Cambodia (which are also classified as the least developed countries among all ASEAN nations by the United Nations), financial services and consumer protection policies may be limited, reducing the potential health benefits of financial inclusion. Second, income levels and education levels vary widely within ASEAN. Higher-income countries typically exhibit higher financial literacy, allowing individuals to use financial services more effectively for healthcare expenses and risk management. In lower-income countries, even if individuals have access to financial services, their ability to leverage them for health-related expenditures may be constrained by limited disposable income (Table 8).

OLS Estimations—Single Countries.

Note. Robust standard errors are in parentheses.

p < .01. **p < .05. *p < .1.

The results, presented in Table 9, confirm these variations. Financial inclusion has a positive and statistically significant effect on health in six countries: Singapore, Thailand, Indonesia, Myanmar, and the Philippines. Among them, Singapore exhibits the largest impact, followed by the Philippines and Indonesia, which rank second and third, respectively. In contrast, the effect of financial inclusion on health is positive but statistically insignificant in Cambodia, Laos and Vietnam suggesting that financial inclusion may have a negligible impact on health outcomes in these countries.

Mediation Analysis—Condition 1.

Note. Robust standard errors are in parentheses.

p < .01. **p < .05. *p < .1.

These results align with the earlier discussion: countries with lower levels of financial development, weaker consumer protection frameworks, and lower financial literacy tend to derive fewer health benefits from financial inclusion. The dominant prevalence of informal financial transactions and the low level of financial development in these economies may limit the role of formal financial services in improving health outcomes, facilitating better healthcare access, investment in preventive health, and implementing risk mitigation strategies.

The observed null effect of financial inclusion on health outcomes in Vietnam may stem from several factors. First, the absence of 2017 data for Vietnam's Personal Health Index hinders a comprehensive analysis of temporal trends, limiting our ability to assess recent changes in health outcomes. Second, Vietnam’s Personal Health Index was already relatively high at 73.86 in 2014, suggesting limited room for significant improvement. This effect could diminish the observable impact of increased financial inclusion on health. Moreover, the prevalence of informal credit systems in Vietnam plays a crucial role. Despite economic reforms, informal finance remains widespread, with studies indicating that a substantial portion of Vietnamese households continue to rely on informal lending sources. For instance, Barslund and Tarp (2008) indicate that informal loans accounted for about one-third of all loans, highlighting the enduring significance of informal finance mechanisms. Additionally, Lainez (2014) indicates that many borrowers perceive informal credit as an economic necessity rather than a detrimental practice, underscoring its deep-rooted presence in Vietnamese society. A similar pattern is observed among firms. Archer et al. (2020) show that fully constrained firms are more engaged in informal credit markets compared to unconstrained and partially constrained firms. This is evident in their higher likelihood of accessing informal credit and securing larger loan amounts. This reliance on informal credit may reduce the perceived necessity and utilization of formal financial services, thereby attenuating the potential health benefits associated with formal financial inclusion initiatives.

Mediation Analysis: What Drives the Positive Effects of Financial Inclusion on Health Outcomes in the ASEAN Countries?

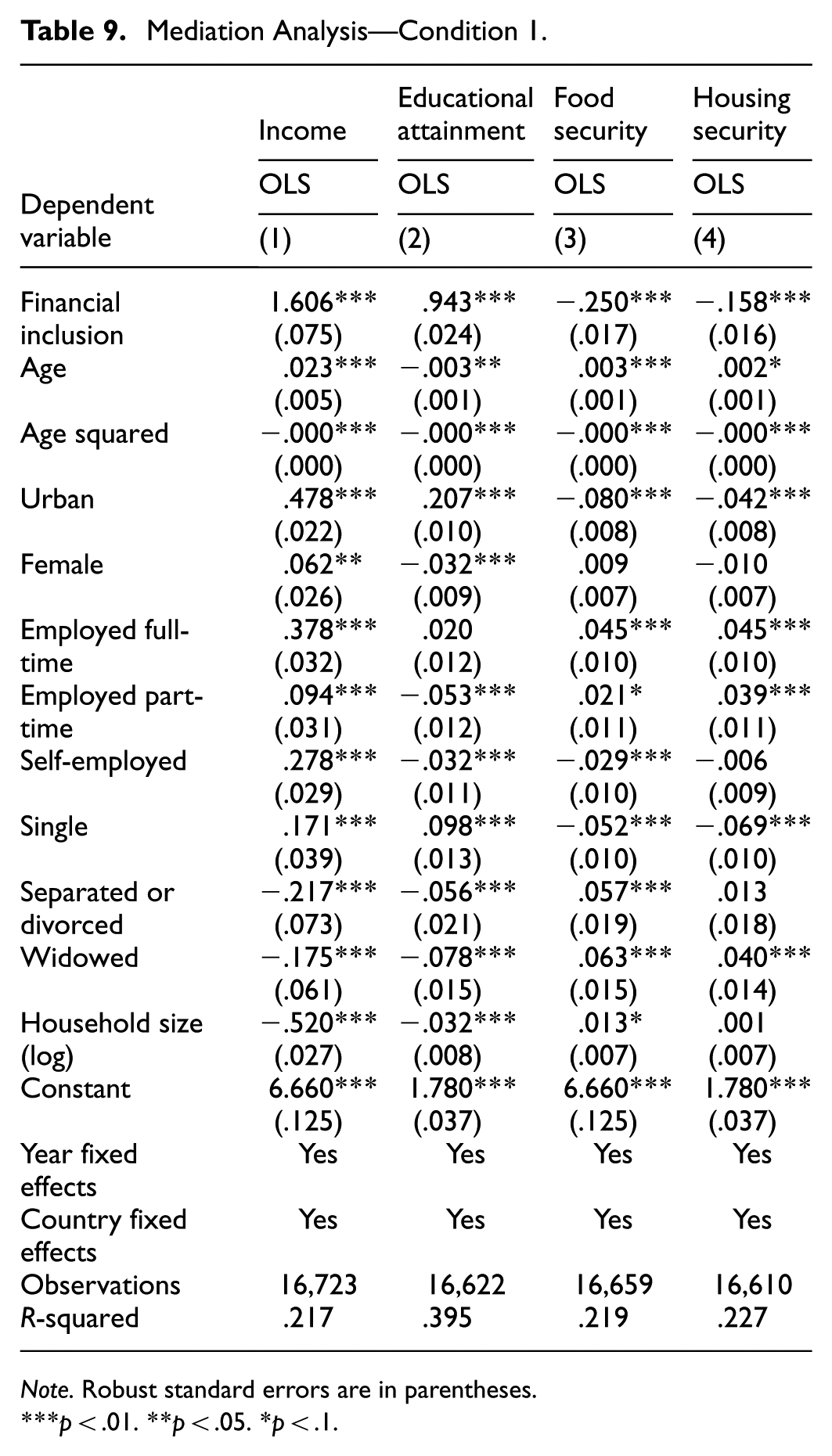

As discussed in the previous section “Impacts of Financial Inclusion,” financial inclusion has a positive and significant effect on health. In this section, we investigate the potential mechanisms through which financial inclusion influences health outcomes. We identify four key mediating channels: income, educational attainment, food insecurity, and housing insecurity. Each of these potential channels on the effect of financial inclusion on health outcomes is discussed in turn below.

Access to financial products and services enables individuals to increase their income by facilitating entrepreneurship, investment, and savings, which in turn can improve their ability to afford healthcare services. Similarly, financial inclusion may support education financing, allowing individuals to acquire higher levels of education, which has been shown to enhance health literacy and promote better health-related decision-making. Inclusive finance might also enhance food purchasing ability, thus improving individuals’ health. Finally, financial inclusion could mitigate the negative impacts of living in inadequate shelter or housing, which in turn may positively influence health.

To empirically test whether income, educational attainment, food insecurity, and housing insecurity mediate the relationship between financial inclusion and health, we follow the procedure outlined in Barkat et al. (2023). This procedure requires two conditions to be met for a variable to be considered a valid mediator. First, financial inclusion must be positively associated with the mediating variables (i.e., income, educational attainment, food insecurity, and housing insecurity). Second, when the mediating variables are included in the model, the effect size of financial inclusion on health must decrease, indicating that part of the effect is transmitted through these mediators. We proxy income using household income per capita in USD (adjusted for purchasing power parity), which is collected from the GWP. Educational attainment is measured as a categorical variable with three levels: 1 if the respondent has completed primary education or less, 2 if they have completed secondary education, and 3 if they have completed tertiary education or higher, which are also collected from the GWP. Food insecurity is measured as a dummy variable equal to 1 if, in the past 12 months, the respondent did not have enough money to buy food needed by themselves or their family, and 0 otherwise. Housing insecurity is measured as a dummy variable equal to 1 if, in the past 12 months, the respondent did not have enough money to provide adequate shelter or housing for themselves or their family, and 0 otherwise.

Table 9 presents the results for the first condition. We find that financial inclusion is positively and significantly associated with both income and educational attainment while negatively and significantly associated with food insecurity and housing insecurity, satisfying the first requirement for mediation.

Table 10 presents the results examining the second condition. When income is included in the model, the effect size of financial inclusion on health decreases from 9.723 to 7.397 (Columns 1–2). When educational attainment is included, the effect size further decreases to 5.451 (Column 4). Similarly, the effect size of financial inclusion on health respectively decreases to 6.228 (Column 6) and 8.055 (Column 8) when food insecurity and housing insecurity are added into the model. These reductions indicate that income, educational attainment, food insecurity, and housing insecurity serve as potential mediators, confirming that financial inclusion improves health outcomes partly by increasing income, enhancing educational attainment, and mitigating the adverse impact of food insecurity and housing insecurity.

Mediation Analysis—Condition 2.

Note. Robust standard errors are in parentheses.

, **, and * are statistically significant at 1, 5, and 10 percent.

As an additional robustness check, we employ structural equation modeling (SEM) to formally estimate the indirect effects of income, education, food insecurity, and housing insecurity in the relationship between financial inclusion and health. The results, presented in Table 11, show that all direct and indirect effects remain positive and statistically significant, reinforcing our previous findings. Overall, our analysis provides strong evidence that income, educational attainment, food insecurity, and housing insecurity are four key pathways through which financial inclusion enhances health outcomes, which is consistent with hypothesis 3a, 3b, 3c, and 3d.

Structural Equation Modelling (SEM).

Note. Robust standard errors are in parentheses.

, **, and * are statistically significant at 1, 5, and 10 percent.

Concluding Remarks

Motivated by growing interest in the health benefits of financial inclusion, this study investigates the impact of financial inclusion on health outcomes across eight ASEAN countries. A sample of 14,815 observations has been collected from two distinct sources: the Gallup World Poll (GWP) and the World Bank Global Findex (WBGF) databases. We start with the ordinary least squares (OLS) estimation to examine the effect of financial inclusion on health outcome among the ASEAN countries. Our data exhibit a hierarchical structure, with respondents nested in countries, there are two levels in our data: (i) individual level and (ii) country level. As such, we adopt multilevel modeling as a robustness check in this study although we already control for country-fixed effects to mitigate the potential confounding bias arising from different characteristics of each ASEAN country. Mediation analysis has also been utilized to identify the potential mechanisms to which financial inclusion affects health outcome across the ASEAN countries.

Our analysis yields several important findings. First, financial inclusion significantly enhances health outcomes, as measured by the Personal Health Index. After controlling for individual characteristics, country- and time-fixed effects, a one-standard-deviation increase in financial inclusion (.266) is associated with a 2.586-point increase in the Personal Health Index. This finding remains robust across multiple estimation strategies, including multilevel modeling and Lewbel’s (2012) instrumental variable approach, which addresses potential unobserved heterogeneity and endogeneity. Second, the health benefits of financial inclusion are notably stronger for women than for men. Subgroup and interaction analyses consistently demonstrate that financial inclusion exerts a larger positive effect on female health, likely due to women’s greater vulnerability to financial exclusion and healthcare access barriers, coupled with their tendency to allocate financial resources toward family well-being. This finding suggests that financial inclusion could play a pivotal role in narrowing gender-based health disparities in the ASEAN region.

Third, the effect of financial inclusion on health varies across countries. Significant positive impacts are observed in Singapore, Thailand, Indonesia, Myanmar, and the Philippines, with Singapore exhibiting the largest effect, while the relationship is statistically insignificant in Cambodia. These disparities likely reflect differences in financial development, consumer protection frameworks, and reliance on informal financial systems, which may dilute the health benefits of formal financial inclusion in less developed markets. Finally, our mediation analysis identifies income, educational attainment, food insecurity and housing insecurity as key channels through which financial inclusion improves health. Financial inclusion boosts both income and education as well as mitigating negative effects of food and housing insecurity, which in turn enhance individuals’ health. This underscores the interconnectedness of financial access, economic empowerment, and human capital in driving health outcomes.

This study enriches the literature on the socioeconomic determinants of health by providing robust evidence from the ASEAN region, a diverse and underexplored context. It establishes financial inclusion as a significant driver of health outcomes, with relevance for women, and highlights the importance of country-specific and gender-specific analyses in understanding this relationship. The identification of income, education, food insecurity, and housing insecurity as mediating mechanisms further advances our understanding of how financial access translates into well-being.

Our findings offer several actionable policy recommendations for ASEAN policymakers aiming to improve public health. First, governments should prioritize expanding access to formal financial services, particularly in rural and underserved areas where financial inclusion remains low. Initiatives such as mobile banking, agent networks, and incentives for financial institutions to serve low-income populations could bridge this gap, especially in countries like Cambodia and Laos, where financial inclusion lags. Second, given the outsized health benefits for women, policymakers should implement gender-specific financial inclusion programs. Women-focused financial inclusion initiatives could empower them to overcome systemic barriers to healthcare and economic autonomy, thereby reducing gender health inequities. Third, the heterogeneity across ASEAN countries underscores the need for tailored policy approaches. In financially advanced economies like Singapore, expanding digital financial services could further enhance health outcomes. In contrast, in less developed markets such as Cambodia, foundational efforts to build trust in formal financial systems and reduce reliance on informal credit are essential first steps. In countries where financial inclusion has a limited impact on health, simply implementing policies to expand access to financial services may not be sufficient to improve population health. Instead, these countries must create an enabling environment for financial inclusion to be effective. For example, strengthening consumer protection frameworks and promoting financial education can be crucial initiatives. Ensuring that financial services are safe, transparent, and accessible—particularly for populations with low financial literacy—can maximize the health benefits of financial inclusion.

It is important to note that the above recommendations should be considered in conjunction with differences on various socio-economic aspects among the ASEAN countries, including institutional and systemic differences—such as variation in financial market development, the persistence of informal credit systems, or disparities in health infrastructure. For example, the development of financial markets varies significantly among ASEAN members due to significant differences in economic growth and development, regulatory frameworks, and financial liberalization. ASEAN countries are different significantly regarding income per capita. For example, Brunei and Singapore are advanced countries with a very high income per capita whereas Cambodia and Laos are at the very low end of the income-per-capita ladder. Vietnam is on the rise with the aim to be a high-income country by 2045. Singapore appears to have a liberalized and open financial markets, while others, such as Malaysia, Thailand and Vietnam have put effort to catch up. Market structure is also very different between the ASEAN countries. In particular, a report by the Organization for Economic Co-operation and Development (OECD, 2025) indicate that the credit-based and the market-based financing to GDP in Singapore are 120% and 93% (relative to the country’s GDP). These figures are 130% and 8%, respectively, for Cambodia. These differences highlight significant difference and the main concerns for firms in Cambodia to look for financing to support their performance and growth.

This study suffers various limitations. Data availability is a key limitation in this current study. Extending the data periods when they become available in the future is desirable. In addition, measuring health outcome can also be considered from different perspectives such as physical health and/or mental health. These issues should be considered in future studies to enhance the robustness and relevance of key important findings from this study.

Footnotes

Acknowledgements

We are indebted to the reviewer who highlighted an important point that helped clarify the varying impacts of financial inclusion on mental health across the countries in our sample.

Ethical Considerations

This article does not contain any studies with human or animal participants.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study is funded by the Ministry of Education and Training of Vietnam under Grant B2025-MBS-04.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.