Abstract

In an era where the digital economy is burgeoning, understanding its impact on industrial structure is crucial. This study develops a multi-sector endogenous growth model, combined with non-homothetic CES consumption preferences, to analyze how the digital economy influences the upgrading of China’s industrial structure. Based on a supply-demand coupling framework, this model examines the impact of key factors such as technological accumulation, digital empowerment, consumption scale expansion, and the alleviation of financing constraints. Empirical test supports the theoretical predictions, and reveals the following key findings: (1) The development of the digital economy significantly promotes industrial structure upgrading by expanding the consumption scale. However, as demand in the service sector becomes more rigid, the positive impact of the digital economy on upgrading begins to decelerate. (2) Through technological empowerment, the digital economy boosts industrial R&D success rates, widening the technological gap among sectors and accelerating industrial upgrading. (3) The effect of alleviating financing constraints on industrial structure upgrading is less pronounced, as the digital economy does not exhibit sector-specific bias in addressing these constraints. These findings highlight the importance of leveraging digital technologies not only for consumption expansion but also for enhancing technological capacity.

Keywords

Introduction

High-quality economic development has become imperative against the backdrop of China’s “triple-overlap” challenge—growth deceleration, painful structural adjustment, and the lagged effects of earlier stimulus measures. Since March 2022, a more complex international landscape and the uncertain trajectory of COVID-19 have amplified headwinds for China’s economy, highlighting an urgent, practical need for new engines of growth. Yet, with the waning of demographic dividends and the diminishing returns from rapid industrialization, traditional drivers alone no longer suffice: new engines of structural advancement must be identified, moving beyond traditional `big push' models (Murphy et al., 1989). Against this backdrop, rapid industrial-structure adjustment and digital transformation—aimed at unlocking latent productivity—are essential to sustain China’s growth momentum and to navigate the middle-income trap (Zhu et al., 2021).

China offers a paradigmatic laboratory for examining this phenomenon. It couples the world’s largest user base in the digital economy with a proactive, state-led digitalization strategy, while still grappling with the shift from a manufacturing-based system to a more advanced, service-oriented economy—an ideal setting for study. The 14th Five-Year Plan and the Vision 2035 blueprint position the digital economy as a strategic fulcrum for China’s modernization. Rooted in the 1990s notion of “network intelligence” (Kewsuwun, 2020), the digital economy was formally defined at the 2016 Hangzhou G20 Summit as an economic paradigm that treats digital knowledge and information as principal inputs, relies on modern networks as foundational platforms, and uses efficient ICT application to catalyze productivity gains and structural optimization (Pan et al., 2022). Since the 13th Five-Year Plan launched the digital-economy strategy, China has rapidly expanded digital infrastructure. State Council data indicate that core digital-economy sectors accounted for roughly 7.8% of GDP in 2020. After March 2022, even as total retail sales of consumer goods fell 11.1% year-on-year, e-commerce and online retail grew by 5.2%, highlighting the digital economy’s resilience and its central role in high-quality development. This unique practical context enables unprecedented, data-rich observation of how the digital economy shapes industrial upgrading.

Despite widespread recognition of the digital economy’s structural impact, three critical gaps persist in the literature. First, studies tend to isolate single drivers—such as technology, consumption, or financing—without examining their interdependent roles in upgrading pathways. Second, the moderating influence of demand-side rigidities, particularly the rising inelasticity of service consumption, remains underexplored. Third, prevailing models often rely on static or homothetic preference specifications, overlooking endogenous feedback loops between digital penetration, sectoral asymmetries, and household behavior.

To address these gaps, this study first develops a multisector Schumpeterian endogenous-growth model augmented with non-homothetic constant substitution elasticity (CES) consumption preferences, following Comin et al. (2021), embedding the digital economy within a coupled supply–demand framework. Second, the effects of the digital economy on structural upgrading are decomposed into four sub-channels—relative technological accumulation, digital empowerment, consumption-scale expansion, and financing-constraint relief—and formally deriving the corresponding mediators to enhance analytical rigor. Third, by employing theoretical deduction to identify total consumption, relative technology gaps, and sectoral financing metrics as mediating variables, we minimize ad hoc specification and bolster empirical reliability.

This study offers three tightly integrated contributions. First, we advance theory by developing a supply–demand coupling model—built on a multisector Schumpeterian endogenous-growth framework with non-homothetic CES preferences—that uniquely captures (i) diminishing returns as service-sector demand becomes inelastic and (ii) endogenous technological divergence amplified by digital bias. Second, using China as a paradigmatic laboratory, we show empirically that the slowdown in digital-driven structural upgrading stems not from undifferentiated financing constraints but from widening technological gaps triggered by service-demand rigidities. Third, we distill these insights into a focused policy roadmap for emerging economies, arguing that sustained upgrading requires targeted digital-capacity building in services rather than blanket financing measures, thereby ensuring high-quality structural transformation even as demand elasticities evolve.

The remainder of this study is organized as follows. Section “Literature review” reviews relevant literature and identifies research gaps. Sections “Theoretical Model” and “Empirical Test” present our theoretical model and empirical test. Section “Conclusions and Implications” discusses the policy implications of our results and concludes with directions for future research.

Literature Review

Digital Economy and Industrial Structure Upgrading

The digital economy has emerged as a potent catalyst for industrial structure upgrading in developing contexts, operating through multiple, intertwined channels and delivering both economic and environmental gains. At the city and regional levels, the digital economy directly promotes sectoral shifts—especially in resource-based and resource-exhausted cities—by fostering innovation, with the effect strongest where firms are closer to provincial capitals (Li et al., 2024). This process then mediates wider benefits: for example, structural upgrading is the principal mechanism through which the digital economy significantly raises household consumption—particularly in rural and western areas—thereby narrowing regional consumption gaps in a non-linear manner as upgrading deepens (Guo et al., 2023; Wang & Li, 2024). Similarly, by streamlining factor markets and adjusting industrial compositions, the digital economy accelerates technology transfer, although the magnitude of this effect varies with institutional distance, geographic proximity, and technological classification (Cai et al., 2024).

Beyond consumption and technology diffusion, the digital economy also underpins sustainable development. It not only directly fosters low-carbon growth but does so chiefly through structural upgrading, establishing a clear “digital economy → industrial structure upgrading → low-carbon development” pathway (Tan et al., 2024; Hao et al., 2023). At the provincial level, the digital economy exhibits a positive, non-linear relationship with total factor productivity—acting as an innovation driver with more pronounced effects in eastern China (Pan et al., 2022; Luo et al., 2023). Within industries, digital adoption raises green total factor productivity, with threshold effects such that firms more deeply embedded in global value chains reap larger green-productivity gains (Liao et al., 2021). Moreover, the interplay between market institutions and the digital economy shapes industrial transformation: high degrees of marketization amplify the positive impact of the digital economy—especially in developed regions—via mediators such as industry–finance integration, technological innovation, and consumption upgrading (Bi et al., 2025). Finally, the spatial agglomeration of digital activities fosters inclusive green growth through channels including energy-use reduction, pollution control, economic expansion, human-capital accumulation, and technological progress—though the effectiveness of supportive policies can differ markedly between local and neighboring jurisdictions (Ren et al., 2022).

Collectively, this body of work places industrial structure upgrading at the heart of the digital economy’s contributions to enhanced consumption, innovation, productivity, technology transfer, market transformation, and both low-carbon and inclusive green growth—while underscoring significant regional heterogeneity, non-linear effects, and the importance of complementary factors such as market integration, global value chain positioning, and supportive policy frameworks.

Mechanisms Linking Digital Economy to Industrial Structural Upgrading

Optimizing economic structure is a primary goal of the digital economy, and this influence unfolds through three concentric levels. At the macro scale, the digital economy strengthens the real economy and creates an enabling environment for structural change. The interdependence of balanced macroeconomic growth (“Kaldor fact”) and major shifts in industrial composition (“Kuznets fact”) has been well documented (Tan et al., 2024), and each wave of general-purpose technology has driven structural evolution (Hao, Wang, et al., 2023). As a quintessential general-purpose technology, the digital economy—characterized by openness, collaboration, sharing, and connectivity—permeates production processes, enhances cross-departmental factor coordination, and reallocates traditional resources to accelerate upgrading (Zhu et al., 2021). Yet rapid digitalization in finance may yield only short-term gains for high-tech industries; lasting impacts emerge once digital services are thoroughly integrated with the physical sector (T. Zhao et al., 2022; Zhao & Weng, 2024). Moreover, by lowering intertemporal consumption barriers and easing liquidity constraints, digital platforms unlock suppressed household spending—addressing China’s persistent consumption shortfall and catalyzing high-quality growth (Leong et al., 2022).

At the meso level, the digital economy reshapes relative prices and thus drives factor reallocation. Differences in sectoral productivity—captured by the “Baumol effect” (Baumol, 1967)—translate into shifts in relative output prices, influencing demand for labor and capital (Ngai & Pissarides, 2007). Subsequent work (Acemoglu & Guerrieri, 2008; Caselli & Coleman, 2001; Alvarez-Cuadrado et al., 2017) emphasizes how variations in factor intensities and substitution elasticities further alter relative costs. By embedding intelligent and personalized digital solutions into production, operations, and sales, the digital economy enhances management efficiency, fosters rapid innovation diffusion, and leverages ubiquitous connectivity for cross-sector data sharing (Zhu et al., 2021). It also modifies factor substitutability—empowering labor and capital—and reduces search and transmission costs for financial resources, thereby facilitating capital deepening, lowering production costs in capital-intensive industries, and ultimately prompting structural shifts (Meng & Wang, 2023).

At the micro level, enterprises drive structural transformation through digital-enabled innovation. New structural economics highlights that upgrading depends on improved factor endowments (Gollin et al., 2002); digital finance addresses “difficult and expensive financing,” providing efficient R&D backing (Yin et al., 2019). Meanwhile, digital technologies cut information-collection, coordination, and time-transmission costs, expanding firms’ innovation frontiers (Abi Saad et al., 2024) and complementing other production technologies to bolster R&D capabilities (Heo & Lee, 2019). Connectivity and sharing further stimulate innovation spillovers, as upstream and downstream firms exchange information and jointly optimize technology configurations (Szalavetz, 2019).

Despite substantial empirical evidence demonstrating the digital economy’s role in driving structural upgrading, scholarly discourse remains skewed toward descriptive paradigm analyses, leaving theoretical foundations underdeveloped. In particular, there is a pronounced gap in frameworks that jointly encompass both supply- and demand-side drivers of structural change. On the supply side, variations in sectoral production technologies—embodied in the “Baumol effect”—explain how relative price shifts redirect factor allocation. On the demand side, changes in consumption patterns—captured by Engel’s law—illustrate how evolving household preferences reallocate resources across sectors (Herrendorf et al., 2013). Yet prevailing empirical models typically employ absolute measures of technological advancement or aggregate demand changes, which obscure the relative interplay between these two classical forces and prevent a coherent reconciliation of the “Kaldor fact” (the co-evolution of balanced growth and structural transformation) with the “Kuznets fact” (the timing and magnitude of industrial shifts). Addressing this duality within a unified analytical framework is essential for a deeper understanding of how the digital economy reshapes industrial structure.

Theoretical Model

Multisector Growth Model with Non-Homothetic Preferences

The “Baumol effect” and “Engel’s law” are widely recognized as pivotal factors influencing changes in industrial structures, with scholars developing various theoretical models to demonstrate this from both supply and demand perspectives. While these models adeptly uncover the fundamental reasons behind shifts in industrial structure, they often struggle to reconcile the “Kaldor facts” with the “Kuznets facts.” From the demand-side perspective, which emphasizes Engel’s law, the “Kaldor fact” is typically contingent on stringent conditions, such as those outlined in the model by Kongsamut et al. (2001). A critical condition for realizing the “Kaldor fact” involves a specific proportional relationship between the utility functions of residents and the technological parameters of industrial production. Conversely, from the supply-side perspective that highlights the “Baumol effect,” balanced economic growth is achievable only in an asymptotic sense. In response to these challenges, several targeted models have been proposed. For instance, Boppart (2014) introduced a Price-Independent Generalized Linear Independent utility function in the demand-side model to mitigate boundary constraints. Additionally, scholars like Ngai & Pissarides (2007), Acemoglu and Guerrieri (2008), and Alvarez-Cuadrado et al. (2017) have developed multi-sector growth models. However, these models still exhibit limitations: demand-side models tend to focus solely on the impact of household income disparities on industrial structure changes, overlooking the influence of consumption preferences; multi-sector growth models treat technological progress as exogenous and suggest that equilibrium growth is only feasible when multiple sectors converge to a neoclassical growth framework. To address these shortcomings, this article integrates Schumpeter’s endogenous growth theory into a multisector growth model to facilitate conditions for endogenous technological progress and balanced economic growth, adopting the methodology of T. Zhao et al. (2022). Additionally, non-homothetic CES consumption preferences are incorporated to capture the effects of consumption biases on industrial structure changes. The specific model settings are as follows.

Final Goods Production Sector

Assuming there are

where

Assuming that labor is free to move across sectors, the labor factor endowment constraint can be expressed as:

where

Intermediate Goods Production Sector

It is assumed that the market for intermediate goods is perfectly competitive, and intermediate goods manufacturers use the final products as the input factor for R&D to produce inputs for the sectoral final goods with one-to-one technology. However, there is uncertainty as to whether the R&D will be successful, and the probability of success is represented by

Furthermore, based on the setting of Aghion et al. (2015), this study assumes that the success rate of technology R&D

where

Household Consumption Sector

Assuming that representative families have invariant intertemporal substitution preferences, their consumption utility function is (Kongsamut et al., 2001):

where

where

Due to the assumption that the final products of each sector can be directly consumed, the resource constraint in the economic system is:

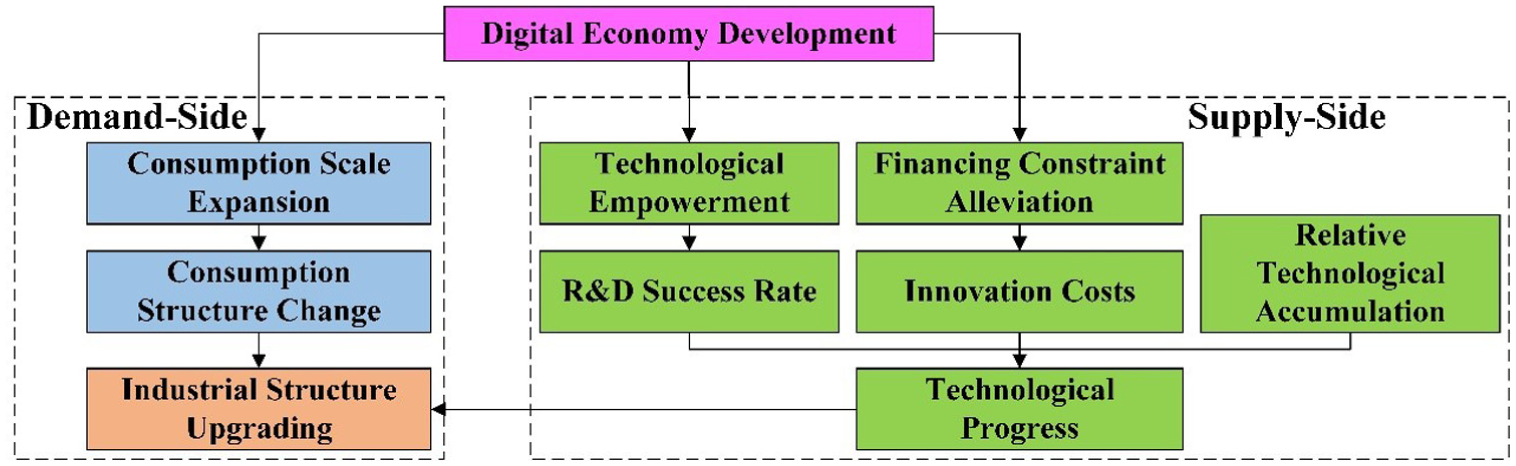

The supply–demand coupling framework between the digital economy and industrial structure upgrading is depicted in Figure 1.

Conceptual framework.

General Equilibrium Analysis

Optimal Production Behavior of Final Goods Production

Under the condition of a perfectly competitive market, the production sector

Taking the optimal first-order partial derivative of Equation (9), the following labor demand function and intermediate product demand function can be obtained, respectively:

Optimal Decision Behavior of Intermediate Goods Production

The intermediate product manufacturer chooses the optimal sector’s final product investment to achieve maximum profit, namely:

Substituting the intermediate product demand function, that is, Equation (11), into Equation (12) and taking the optimal first-order condition, the optimal intermediate product output of the middleman can be obtained as:

Substituting the optimal intermediate production into the intermediary profit function and the industrial production function to obtain the optimal intermediary profit and industrial final product production, respectively:

Furthermore, perfect competition in the labor factor market determines that the marginal product value of labor factors in various industries is equal. By substituting the optimal intermediate output into the labor demand function to obtain:

Rewriting the above equations, we can obtain:

Equation (17) indicates that the relative price of a sector is the reciprocal of its relative technological level in a perfectly competitive labor market. The higher the level of production technology, the lower the price of the final product.

Optimal R&D Behavior of Intermediate Goods Production

Due to the monopolistic production of intermediate goods by intermediaries, they can obtain monopolistic profits from the research and development of the latest intermediate goods. However, once production technology is surpassed, old intermediate products will be replaced by new intermediate products, causing monopolistic profits to evaporate. In this situation, the intermediary has no choice but to invest more in research and development and constantly update production technologies, resulting in the “creative destruction” of production technologies. If the technology is successfully developed, the intermediary will earn R&D benefits

Therefore, this study assumes that the innovation cost of intermediaries is

Combining Equations (8) and (14), and solving Equation (18) to optimize the first-order conditions can determine the optimal probability of successful research and development:

From Equation (19), the success rate of innovation for intermediate product manufacturers is influenced by the empowering effect of digital technology

Optimal Consumption Behavior of Representative Household

Representative households achieve maximum household utility by determining the optimal consumption quantity

where

Rewriting Equation (21), we can obtain:

Equation (22) indicates that the relative price of the final product is determined by the proportion of sector output contribution

Decomposition of Factors Affecting Industrial Structure Upgrading

The significant transformation of industrial structure is a prominent and typical fact that occurs in the process of economic development. Existing literature mainly used the sectoral output ratio, sectoral labor allocation ratio, or sectoral consumption structure to measure it. Although different measurement indicators have different meanings, this study conducts industrial structure research under the coupling framework of supply and demand sides, which makes the above measurement indicators have good consistency in measuring industrial structure. Therefore, the following propositions are derived:

Integrating Equation (15) with Equation (17), and Equation (23) can be further rewritten as:

The supply and demand relationship can be obtained from the clearing conditions of the industrial final product market as follows:

Substituting Equation (15) into Equation (25), from which Equation (23) can be rewritten as:

Thus, Proposition 1 obtains certification.

Furthermore, by combining Equations (4), (10), (11), (19), (22), (23), and (26), the economic structure can ultimately be decomposed into the following forms:

The first item on the left side of Equation (27) represents the proportion of industrial output contribution, which is a constant and has no significant impact on changes in industrial structure; the second item is the ratio of historical industrial production technology, which can be regarded as the cumulative effect of technology. In the scenario where the final product of the sector can be replaced, that is

The fourth item on the left side of Equation (27) represents the technological empowerment effect of the digital economy. By taking the logarithm of Equation (27) and taking the derivative over time, combined with Equation (4), we can obtain:

To promote the upgrading of industrial structure through the digital economy, the growth rate of the output value of the tertiary sector must be higher than that of the output value of the secondary sector.

The left side of Equation (29) represents the supportive effect of digital technology on enterprise technology R&D. This study defines it as the relative technological expansion effect of the digital economy, and the right side represents the relative financing constraint release effect of the digital economy. The greater the empowering effect of digital technology

Model Assumptions and Practical Relevance

The analytical tractability of our theoretical model derives from four simplifying assumptions, each of which carries implications for real-world application and suggests directions for refinement.

First, we assume sectoral homogeneity, meaning all firms within a given sector follow identical production and digital-adoption functions. While this reduces model complexity, it abstracts from the considerable variation in technology absorption and organizational capacity observed across enterprises—particularly between leading firms and smaller incumbents. As a result, policy prescriptions based on this assumption may overstate the impact of universal digital interventions and understate the need for firm-specific support measures.

Second, the model presumes perfect labor mobility, so that workers can reallocate instantly between manufacturing, services, and other sectors. This reflects recent relaxations in China’s hukou restrictions, which have materially eased geographic mobility, but it neglects the persistent skill mismatches and retraining frictions that slow workforce transitions in practice. Consequently, projections of structural upgrading may be overly optimistic if they fail to account for the time and resources required to reskill displaced workers.

Third, digital empowerment (δ) is treated as an exogenous, uniform input across sectors. Empirically, we proxy δ with a province-level composite index (Section “Endogeneity Test”), yet this aggregation masks substantial within-province heterogeneity in digital readiness—between urban and rural areas, and among firms of different sizes. Policymakers should therefore interpret estimated δ-effects as indicative of broad regional trends rather than precise firm-level elasticities.

Fourth, our consumption module adopts a non-homothetic CES specification in which service-sector demand becomes increasingly inelastic once per-capita income exceeds a threshold (ξ). This rigidity aligns with National Bureau of Statistics data showing service-expenditure elasticity declining from 1.2 in 2011 to 0.8 in 2022. Nonetheless, exogenous shocks—such as the COVID-19 pandemic or sudden regulatory changes—can temporarily reverse these elasticities, highlighting the need for dynamic extensions.

Together, these assumptions enable a clear equilibrium characterization of how the digital economy, consumption patterns, and financing interact to drive structural change. At the same time, they counsel caution in microtargeted policy design. Future research could enrich the framework by incorporating firm-level digital-maturity scores—drawn, for example, from platform data or proprietary surveys—to capture heterogeneity in technology adoption and refine policy calibrations accordingly.

Empirical Test

Model Setting

Based on the theoretical analysis, we further examine the empirical relationship between the development of the digital economy and the upgrading of the industrial structure. Let

where

Next, we discuss the selection of variables in the model. Although many scholars believe that the upgrading of the industrial structure is a comprehensive improvement involving multiple dimensions such as the overall upgrading of the industrial structure, the high-end advancement, and the rationalization of the industrial structure, to maintain consistency with the theoretical derivation, this study approximates the upgrading of the industrial structure using the high-end advancement of the industrial structure, that is, the ratio of the value of the tertiary sector to the value of the secondary sector. The core explanatory variable in this study is the development of the digital economy. Although there is no consensus on the measurement of the digital economy, we assess the digital economy development level from four critical dimensions, that is, per capita express delivery volume, number of broadband access ports, mobile phone penetration rate, and the digital inclusive finance index, following Hao, Wang, et al. (2023) and Ma et al. (2023). This study uses Z-score for data standardization treatment, and based on this, uses time-series global principal component analysis to select principal components whose cumulative variance contribution rate reaches 80% to refine the indicators of the digital economy and calculate the comprehensive development level of the digital economy. The digital inclusive finance index in China comes from the Digital Finance Research Center of Peking University, and the other data comes from the “China Urban Statistical Yearbook.” The specific calculation results of the digital economy development index are presented in Figure 2. As shown in the figure, the digital economy index of China’s 31 provinces experienced substantial growth during the period from 2011 to 2022.

Digital economy development of provinces in China between 2011 and 2022.

Variable Selection and Data Sources

This study selects foreign direct investment (FDI), per capita GDP (PGDP), human capital (HC), and unemployment rate (UE) as control variables. According to the theoretical model, the mediating variables selected in this study include total consumption (TC), relative technological expansion (RTE), and relative financing constraint (RFC). The foreign direct investment is measured by the actual amount of foreign capital used by each city, human capital is measured by the per capita government education expenditure, and the unemployment rate is measured by the number of unemployed people at the end of the year, divided by the total population at the end of the year. The total consumption is measured by the total retail sales of consumer goods in each city, the relative technological expansion effect is represented by the ratio of per capita output value of the tertiary sector to the secondary sector, and the relative financing constraint release effect is represented by the ratio of the SA index (Hadlock & Pierce, 2010) of the tertiary sector to the secondary sector. The financing constraint release effect is calculated based on the SA index classified by province and sector of Chinese listed companies.

Data on financing variables are from the Peking University Digital Finance Index, and the remaining variables are from “China City Statistical Yearbook” and the “China Population and Employment Statistical Yearbook.” The financing constraint release effect is calculated based on the SA index classified by province and sector of Chinese listed companies. The study takes 288 Chinese cities from 2011 to 2019 as the research sample, and the descriptive statistics of the relevant variables are shown in Table 1.

Descriptive Statistics of Variables.

Benchmark Regression Results

Table 2 presents the regression results of the benchmark model. Models (1) to (4) employ various combinations of time and city-fixed effects to examine the direct impact of the digital economy on the upgrading of the industrial structure. The findings indicate a significant positive effect of the digital economy’s development on industrial structure upgrading, with estimated coefficients of 0.345, 0.303, 0.151, and 0.033, significant at the 5% level or better. This evidence supports the preliminary conclusion that the digital economy’s advancement in Chinese cities positively influences industrial structure upgrading.

Benchmark Regression Results.

and ** denote significance at the 1% and 5% levels, respectively.

Regarding control variables, all except for FDI positively influence industrial structure upgrading. The estimated effect of the unemployment rate (UE) on industrial structure is statistically insignificant. A plausible mechanism lies in the nature of labor reallocation during economic downturns: as UE rises, laid-off workers tend to enter the tertiary sector, where market entry barriers are relatively low (e.g., low-end services and the informal gig economy). This reconfiguration reflects the forced absorption of idle labor into low-value-added service activities rather than productivity-enhancing upgrading. Consequently, the influx of non-specialized labor contributes little to sectoral value added and does not effectively promote genuine industrial upgrading.

By contrast, FDI has a negative and statistically significant effect on industrial structure, indicating that FDI not only fails to enhance China’s industrial structure but also exerts a restraining influence. This finding aligns with the “pollution haven” hypothesis: particularly in earlier stages of development, foreign capital is skewed toward secondary-sector activities—such as manufacturing and energy-intensive industries—where environmental regulations are less stringent. An increase in the share of such FDI reinforces the secondary sector’s weight relative to the tertiary sector, thereby inhibiting the overall upgrading process.

Drawing from China’s unique institutional landscape, we controlled for: (1) provincial industrial policies (count of digital initiatives in government work reports), which may artificially accelerate digitization; (2) environmental regulations (SO2 removal rates), addressing “pollution haven” effects that skew sectoral composition; (3) labor mobility (migrant population shares), capturing workforce reallocation independent of digital forces; (4) infrastructure quality (road density), which co-evolves with digital networks; (5) trade openness (export-import/GDP), accounting for global market shocks; and (6) urbanization rates, controlling for structural transition momentum. Crucially, we tested interaction effects between these confounders and digital development—finding, for instance, that stringent environmental regulations significantly attenuate digital upgrading (β_interaction = −0.12, p < .01), suggesting policy trade-offs between ecological goals and structural transformation. These controls were embedded within a coefficient stability framework (Oster, 2019), with sensitivity analyses confirming results remain robust unless unobservable factors exert 3.2× stronger influence than observed factors—a highly improbable scenario given our exhaustive covariate set.

Robustness Test

This study identified two concerns regarding the benchmark regression results. The first pertains to the potential lag effect of the digital economy’s development on the industrial structure. To investigate this, we re-evaluated the regression using data from the digital economy that lagged by one period in our benchmark model, as presented in Model (5) of Table 3. The findings indicate that the influence of the digital economy on industrial restructuring remains robust, regardless of whether the data is lagged.

Robustness Test Results.

and ** denote significance at the 1% and 5% levels, respectively.

The second concern pertains to the measurement of the digital economy. Although the concept was defined during the G20 Leaders’ Hangzhou Summit in September 2016, academia has yet to agree on a standardized measurement for the digital economy. This lack of consensus stems from two main issues: the variety of indicators used to measure the digital economy and the different models applied to gauge its development. As a result, the use of differing indicators and methodologies leads to multiple outcomes for the digital economy development index, raising concerns about “selective bias” due to “result-oriented choice bias” in robustness tests that employ indicator substitution. To address this challenge, this study employs the “Broadband China” initiative as a case study to implement a multi-time-point DID method for robustness testing. This approach not only circumvents the selection issues related to the measurement indicators and methodologies of the digital economy but also capitalizes on the critical role of network infrastructure development in the digital economy’s growth. The “Broadband China” policy, an expansionist initiative aimed at enhancing the scale, speed, and coverage of broadband services, provides an excellent quasi-natural experiment for our research. It allows for the verification of exogenous policy impacts and helps mitigate the endogeneity concerns within our model. The specific model setting is outlined as follows:

In Equation (31), the dummy variable

Endogeneity Test

The issue of endogeneity, particularly reverse causality, is a critical factor affecting the robustness of our model results. While the digital economy can influence the upgrading of industrial structures, the converse is also true—upgraded industrial structures can impact the digital economy. For instance, as industrial structures evolve, residential consumption patterns shift towards higher quality demands, thereby accelerating the need for new infrastructure and laying a stronger foundation for the digital economy’s growth. To address the endogeneity between these variables, this study utilizes two instrumental variables for analysis.

(1) IV-Geo: Spherical distance to Hangzhou (Alibaba HQ) × Provincial digital finance index mean, capturing exogenous proximity-driven digitization. This variable is chosen because it correlates with the digital economy’s development, yet it is ostensibly unrelated to the evolution of industrial structures, thus satisfying the requirements for an instrumental variable’s relevance and exclusion. In this study, we enhance the temporal relevance of this instrumental variable by combining the spherical distance from each city to Hangzhou with the average development index of inclusive finance.

(2) IV-Hist: Post offices per capita (1984) × Provincial digital finance index mean, reflecting pre-digital path dependency. This choice is predicated on the assumption that the digital economy largely depends on “online” communication, and areas with a higher number of post offices may be more predisposed to developing “online” communication habits, thereby facilitating the adoption and growth of digital technologies.

First-stage Cragg-Donald F-statistic (21.03) exceeds Stock-Yogo critical values, rejecting weak IV concerns. The Oster sensitivity analysis shows β becomes zero only if δunobs > 3.2 × δobs.

To temporally adjust this variable, we interact the number of post offices per million people in 1984 with the average development index of inclusive finance. The specific results are presented in Table 4. The results from the heteroscedasticity weak instrumental variable test indicate that the chosen instrumental variables are effective. Moreover, the estimation results confirm the robustness of the findings.

Endogeneity Test Results.

and ** denote significance at the 1% and 5% levels, respectively.

Mechanism Test

According to theoretical deduction, the primary factors influencing the upgrading of industrial structure include the consumption scale effect, relative technological expansion effect, and relative financing constraint release effect, all driven by the development of the digital economy. To empirically validate the pathways through which the digital economy impacts industrial structure upgrading, this study will employ the Hayes mediation effect test method. We will construct the following mediation effect test model:

where

Mediation Effect Test Results.

, **, and * denote significance levels of 1%, 5%, and 10%, respectively.

According to Columns (1) to (6) of Table 5, the digital economy promotes industrial structure upgrading primarily by expanding the consumption scale and by empowering industrial technology R&D, consistent with theoretical expectations.

The consumption-scale effect (TC) operates through demand expansion: the digital economy—for example, via e-commerce platforms and fintech applications such as Alipay—lowers transaction costs, improves payment convenience, and broadens the variety of goods and services, thereby unlocking latent consumption demand. This expansion in aggregate demand alters relative demand elasticities across sectors and raises the output value of the tertiary sector, which typically exhibits higher income elasticity (e.g., tourism, entertainment, premium services), thus shifting the structure toward services. However, the effect attenuates over time as certain digital services (e.g., mobile data and basic online communication) become necessities for most of the population, transitioning from discretionary to essential expenditures with lower income elasticity.

The digital-empowerment effect (RTE) arises because digital technologies (e.g., big data, AI, cloud computing) are more readily applicable and have diffused more rapidly in services than in manufacturing. In practice, finance uses these tools for risk assessment, logistics for route optimization, and entertainment for content recommendation, all of which raise productivity and R&D success rates in the tertiary sector more quickly than in the secondary sector. Consequently, the relative technological gap widens in favor of services, fostering upgrading by making the tertiary sector more technologically advanced and efficient.

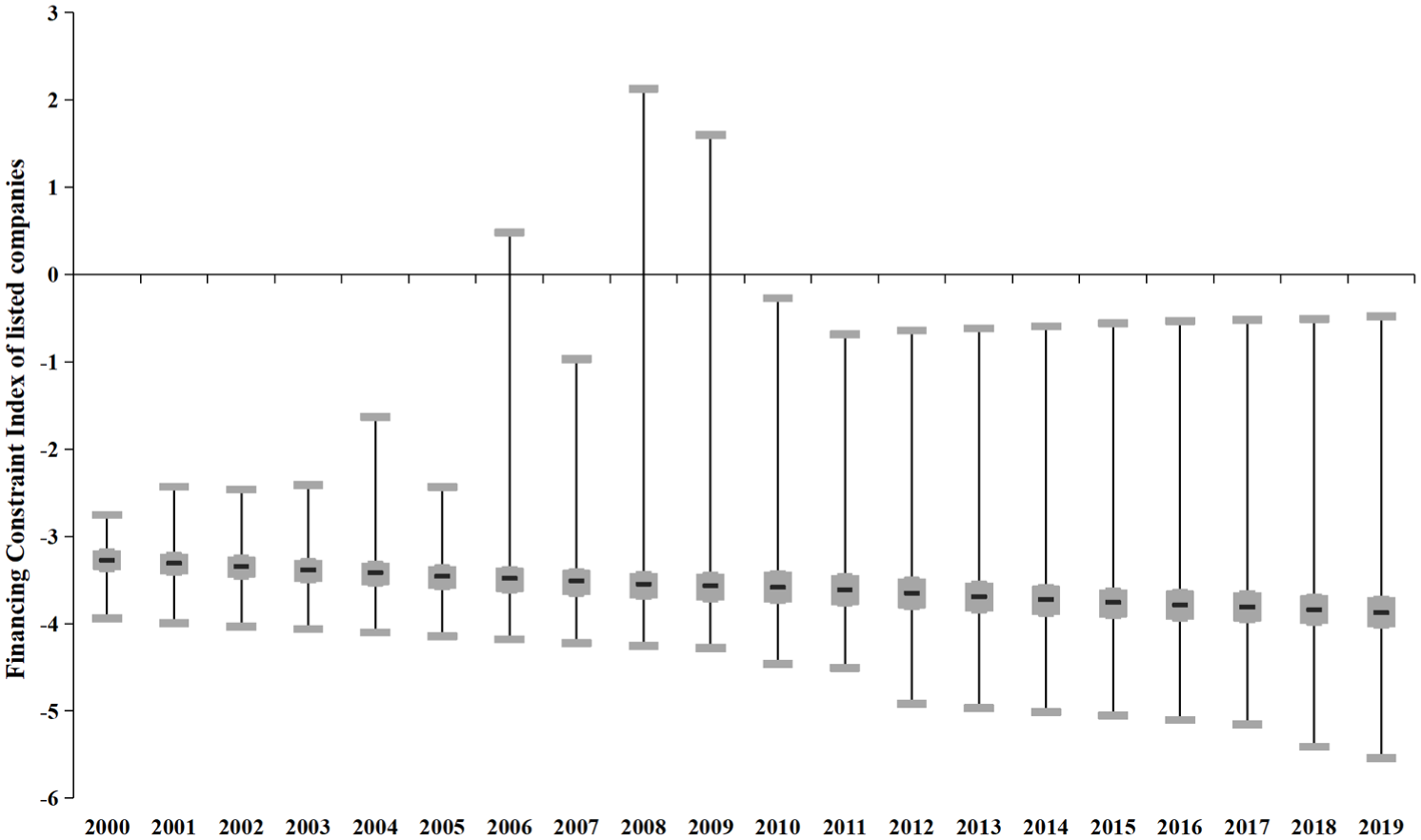

The financing-relief effect (RFC) is not statistically significant as a channel for industrial structure upgrading. One explanation is data selectivity bias (e.g., sample composition or measurement limitations). More importantly, digital finance (e.g., Ant Group’s microloans) alleviates absolute financing constraints for SMEs broadly rather than privileging the service sector; because the development of digital financial infrastructure (e.g., online banking, digital credit scoring) benefits manufacturing and services relatively evenly, it does not generate a meaningful relative advantage for services that would reallocate activity away from manufacturing. Consistent with this interpretation, Figure 3 shows a steady decline in absolute financing constraints for both sectors but no persistent trend in the relative constraint, which fluctuates around 1.

Relative financing constraints index of listed companies.

From the perspective of contribution, the effect driven by consumption scale and digital empowerment contributes 21.5% and 35.1%, respectively, to industrial structure upgrading. The impact of the consumption scale effect is less pronounced than that of the digital empowerment effect. This is primarily due to the higher current elasticity of consumption demand in the tertiary sector compared to the secondary sector. However, in the digital economy era, with the increasing rigidity of demand in service industries (such as communication, which has become a necessity for most residents), the disparity in the elasticity of consumption demand across industries narrows. Consequently, the influence of expanding consumption scale on industrial structure upgrading diminishes.

Surprisingly, the effect of the digital economy on industrial structure upgrading through the release of relative financing constraints is not significant. This outcome prompts two explanations: First, data selectivity bias may contribute to this finding. For evaluating the impact of relative financing constraint release effects, the study utilizes the SA index calculated from the data of listed companies as a measure. However, listed companies typically have stronger financing capabilities than general enterprises, and this data does not fully capture the effect of digital economy-driven financing constraint relief on enterprises, particularly small and medium-sized enterprises, leading to insignificant results. Second, these findings do not imply that the digital economy fails to alleviate corporate financing constraints. Figure 3 clearly shows that with the development of the digital economy, the absolute financing difficulty faced by listed companies in both the secondary and tertiary industries has decreased annually. Nevertheless, from a relative standpoint, the financing difficulty between the tertiary and secondary industries remains approximately constant, with no significant fluctuations observed alongside the development of the digital economy. This suggests that while the digital economy aids in easing financing constraints for enterprises, it does not induce a sector-specific bias, and therefore, its impact on upgrading the industrial structure remains limited.

Conclusions and Implications

Conclusions

This study develops a unified framework—integrating multisector Schumpeterian endogenous growth theory with non-homothetic CES consumption preferences under a supply–demand coupling approach—to examine how digital economy development drives China’s industrial structure upgrading. The model aligns three structural indicators (industrial output ratios, labor allocation, and consumption patterns) and isolates three core mechanisms—consumption-scale expansion, digital-empowerment, and financing-constraint relief—through which the digital economy influences structural change. We then empirically validate these channels using panel data, fixed-effects regressions, and mediation-effect analysis. Our key findings are threefold:

(1) Consumption-scale effect. Digital economy development significantly advances structural upgrading by enlarging aggregate consumption. However, as service-sector demand becomes more inelastic, this positive effect gradually decelerates.

(2) Digital-empowerment effect. By enhancing industrial R&D success rates, digital technologies widen relative technological gaps and thereby accelerate the shift toward higher value-added activities.

(3) Financing-relief effect. Although the digital economy uniformly eases financing constraints across sectors, the absence of sectoral bias limits this channel’s potency in driving structural transformation.

Taken together, these results confirm that the digital economy plays a positive and significant role in promoting industrial upgrading—but that its marginal benefits may wane over time. As digital technologies converge and service-demand elasticities solidify, the distinctive uplift in the tertiary sector may diminish, risking a structural swing back toward secondary industry.

Policy Implications

Building on our theoretical model and empirical results, we propose a three-tier policy framework—targeting service-sector digitization, digital industrialization, and sector-specific financing—to sustain and amplify the digital economy’s upgrading effects. This framework follows directly from our core findings on consumption rigidity, technological empowerment, and the absence of sectoral bias in financing.

First, to counteract demand rigidity and sustain consumption-driven upgrading, governments should implement policies that simultaneously reduce adoption barriers and build digital capacity in the service sector. Based on our finding that the consumption-scale effect decelerates as service demand becomes inelastic, the policy objective must shift from merely stimulating demand to enhancing the quality and productivity of service provision. For example, a “Cloud Voucher” program that reimburses small and medium-sized enterprises (SMEs) in logistics, retail, and personal services for up to 30% of qualified cloud-service fees can rapidly spur digitization and operational efficiency. The effectiveness of such financial incentives can be maximized by integrating the subsidy application platform with the national digital identity system (e.g., China’s OneID), which enables automated applicant verification and real-time API monitoring to detect and prevent misuse, potentially reducing administrative costs by roughly 40%. Crucially, these financial incentives must be coupled with standardized digital-skills training and certification programs to ensure that firms and employees not only acquire new tools but also possess the capabilities to deploy them effectively, thereby maximizing productivity gains and sustaining the value proposition of services.

Second, to deepen the technology-driven upgrading effect, fiscal incentives must be precisely aligned with R&D risk profiles and delivered with minimal bureaucratic delay. Our results show that digital empowerment, by widening the inter-sectoral technology gap, is the most potent driver of structural change, and a graded tax-credit scheme can amplify this channel. Such a scheme could offer a baseline 120% deduction for eligible R&D expenses, escalating to a 150% deduction for high-risk, high-reward foundational research and applied innovations in critical fields such as healthcare AI, advanced logistics algorithms, and clean-energy technologies. To address delayed disbursement that often undermines innovation policy, the application and verification process can be streamlined through technology by embedding smart-contract logic on a permissioned blockchain; once predefined R&D milestones are objectively confirmed by independent validators or verified data feeds, tax credits or grants are released instantly to the enterprise. This design reduces administrative lag, enhances transparency, and provides timely cash flow to innovators.

Third, to address the finding that uniform financing relief does not create relative advantages, policy must move beyond blanket easing to a dynamic, data-driven credit infrastructure that channels resources to the most productive firms while correcting market biases. The development of digital financial infrastructure has benefited manufacturing and services relatively equally, thus failing to push structural change, and a comprehensive credit-assessment platform can help overcome this limitation. Building on pilots such as Shenzhen’s Gov-Bank-Chain, policymakers can link traditionally siloed data—customs declarations, tax filings, social-insurance payments, and utility transaction records—on a secure, privacy-preserving blockchain, and apply machine-learning risk analytics to generate more accurate, real-time credit scores for SMEs, cutting loan-approval times to under 72 hr and lowering default rates by over 20%. However, because market forces alone may not direct sufficient capital to underserved segments, complementary measures are needed; regulators should consider mandating “digital inclusion quotas,” requiring financial institutions to allocate a minimum proportion (e.g., 30%) of their SME loan portfolios to firms in the service sector and to those operating in less-developed central and western regions, thereby actively countering inherent market biases.

Finally, robust coordination and monitoring are essential for these measures to deliver sustained, high-quality structural upgrading. A unified digital portal for subsidies, tax credits, and loan applications should be established to minimize fragmentation and simplify compliance for businesses, and real-time performance dashboards tracking economic, environmental, and social metrics—such as sectoral productivity growth, patent filings, green TFP, and SME survival rates—should be deployed. This infrastructure enables policymakers to assess impacts continuously, to recalibrate incentives swiftly based on empirical evidence, and to ensure that public resources effectively drive the intended industrial transformation.

Generalizability and Boundary Conditions

The empirical insights from China’s digital transformation offer valuable yet context-bound pathways for industrial upgrading. The channels through which the digital economy drives industrial upgrading—namely, service-sector demand rigidity and technology-enabled R&D acceleration—are theoretically applicable across late-industrializing economies. In practice, however, their operational effectiveness depends on three interrelated boundary conditions.

First, infrastructure readiness underpins all digital economy strategies. Our results assume 5G coverage exceeding 60% and cloud-computing adoption above 40%—thresholds that enable the consumption-scale effects observed in China’s urban centers. In economies where 5G penetration remains below 25% (e.g., Vietnam, India), limited bandwidth constrains service-digitization returns and dampens upgrading momentum.

Second, institutional capacity shapes how quickly and evenly digital investments translate into structural change. China’s state-capitalist model deployed a $180 billion 5G rollout and leveraged platform–SME ecosystems (e.g., Alibaba) to synchronize supply- and demand-side innovations. By contrast, democracies with fragmented governance (e.g., Brazil, Indonesia)—where digital-policy coordination indices fall below 0.4—exhibit 30–50% weaker technology-empowerment effects, according to counterfactual simulations using World Bank GovTech metrics.

Third, labor-market flexibility and upskilling determine whether digital expansion generates inclusive employment. China’s high adult upskilling rate (> 70%) and substantial informal-sector absorption (>35% of jobs) facilitated a smooth transition from manufacturing to services. In contexts with rigid labor regulations (e.g., South Africa) or acute digital skill gaps (e.g., Mexico’s 48% competency shortfall), there is a risk of “jobless upgrading,” where output growth in tertiary activities does not translate into commensurate employment gains.

To adapt these insights, we recommend a phased approach: begin with cost-efficient infrastructure catch-up (e.g., edge-computing microgrids as in India’s Digital Village initiative), then pursue institutional hybridization (blending public broadband expansion with private API governance, as in Vietnam’s SME-digitization partnership with Meta), and finally embed digital apprenticeships into industrial policy (following Indonesia’s SMESCO Academy model). Mechanistic validity appears to hold once per-capita GDP exceeds $7,500 (e.g., Thailand’s Bangkok–Central Corridor) and research expenditure surpasses 1.5% of GDP, underscoring the need for context-specific calibration rather than direct transplantation.

These findings do not extend to advanced economies (e.g., Germany’s Industry 4.0) or to fragile states (e.g., Nigeria’s limited grid access), whose structural conditions lie outside this framework. Future studies should empirically test these boundary conditions in middle-income hubs such as Mexico’s manufacturing corridors and Poland’s service clusters. Policymakers in these contexts must also refine industrial-financing mechanisms—particularly for SMEs—so that the digital economy remains a sustained catalyst for high-quality structural transformation.

Limitations and Future Research

This study is subject to three main limitations that should frame the interpretation of our findings and guide subsequent investigations. First, our use of the SA index to proxy financing constraints relies on data from publicly listed firms, thereby omitting most (over 95%) of China’s non-listed SMEs. As a result, we may underestimate how the digital economy relieves credit frictions for grassroots entrepreneurs, especially in service sectors dominated by micro-entities. Future work should incorporate alternative data sources—such as Ant Group’s microloan records—to construct real-time, firm-level financing-constraint indices that capture the experience of unregistered SMEs.

Second, the non-homothetic CES framework we adopt assumes a constant elasticity of service-sector demand, which precludes abrupt shifts in consumption patterns induced by exogenous shocks. The COVID-19 lockdowns of 2020–2022, for example, transformed education and healthcare from discretionary to essential services, violating the model’s steady-state elasticity. To address this, researchers could embed state-dependent elasticity functions or stochastic shock absorbers into the preference specification, thereby allowing consumption parameters to recalibrate dynamically in response to crises or policy interventions.

Third, our analysis excludes the informal gig economy—platform-based freelancers and micro-entrepreneurs account for roughly 32% of China’s tertiary employment, yet operate outside conventional industry classifications. Ignoring this segment risks overlooking the disruptive potential of the digital economy in labor-intensive service niches. Subsequent studies should leverage platform-scraped big data (e.g., Meituan order records, Kuaishou livestream metrics) to quantify informal-sector value creation and better integrate it into structural-change models.

By pursuing these methodological pivots—(1) integrating digital-payment and microloan datasets for comprehensive financing measures, (2) allowing elasticities to vary with state conditions, and (3) mapping informal activity with granular platform data—future research can enhance empirical precision and bridge formal economic modeling with the on-the-ground realities of digital transformation. Such extensions will be especially valuable in emerging economies, where institutional voids and rapid technology adoption amplify both the challenges and opportunities of structural upgrading.

Footnotes

Author Contributions

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: We appreciate the financial support from the Major Project of Philosophy and Social Sciences Research in Jiangsu Province's Universities (No. 2025SJZD054), the National Natural Science Foundation of China (Nos. 72564014, 72064005), Guangxi Bagui Youth Talent Training Program, Guangxi Philosophy and Social Science Planning Research Project (No. 22BGL003), Natural Science Foundation of Guangxi Province (No. 2020GXNSFAA159041), and GUAT Special Research Project on the Strategic Development of Distinctive Interdisciplinary Fields (No. TS2024311). We also appreciate the constructive criticism provided by the anonymous referees.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The datasets generated during and analyzed during the current study are available from the corresponding author upon reasonable request.

Declaration of Generative AI and AI-Assisted Technologies in the Writing Process

During the preparation of this work, the authors used OpenAI’s ChatGPT service to improve language and readability. After using this service, the authors reviewed and edited the content as needed and took full responsibility for the content of the publication.