Abstract

China has not established a regulatory framework for the disclosure of negative information related to ESG. As a result, firms face a dilemma when confronted with ESG-related adverse events: withholding disclosure risks reputational damage upon exposure, while disclosing may invite legitimacy concerns. To address this dilemma, a study is conducted using A-share listed firms that disclose ESG-related negative information between 2020 and 2021. By setting an event window spanning ten trading days before and after the announcement of negative events, the research reveals that disclosing ESG negative information leads to significant short-term negative market effects. Although the adverse market impact is less pronounced when firms voluntarily disclose negative ESG information compared to when it is disclosed passively, this does not suffice to encourage proactive disclosure. Further regression analysis is conducted to examine the long-term value effect of disclosing ESG negative information, showing that the level of disclosure significantly enhances the long-term value of the firm. The stark contrast between the two effects suggests that, first, ESG is fundamentally a concept rooted in sustainable development, and the long-term value effect of disclosing negative information aligns with this principle. Second, ESG is a practice, and negative information is an objective reality within such practice. Choosing to disclose ESG negative information appropriately reflects a positive attitude, proving beneficial in the long run. Therefore, it is recommended that government regulatory bodies establish a mandatory framework for ESG negative information disclosure and incorporate such disclosures into the ESG rating system.

Introduction

Since China set its “carbon peak and carbon neutrality” goals, the demand for ESG information has surged. According to the “China Listed Firms ESG Development Report,” the proportion of firms independently publishing ESG-related reports increased from 26.97% of A-share listed firms in 2020 to 31.34% in 2021, indicating a significant upward trend. However, only 5.62% of listed firms are highly willing to disclose negative ESG information and improvement plans Wang et al. (2022). Most firms, mindful of market competition and brand image, exhibit a rather low willingness to disclose negative information (D. S. Yang and Cong, 2024). Disclosing negative information is a challenging issue.

Globally, the disclosure of ESG information has gradually shifted from voluntary to mandatory, whereas in China, there are currently no explicit regulations regarding compulsory ESG information disclosure. In May 2024, under the guidance of the China Securities Regulatory Commission, the Shanghai, Shenzhen, and Beijing share exchanges jointly issued and implemented the “Guidelines for Sustainable Development Reports of Listed Firms,” explicitly requiring sample firms of the SSE 180 Index, STAR 50 Index, SZSE 100 Index, ChiNext Index, and firms dually listed domestically and abroad to publish sustainability reports, while encouraging other listed firms to disclose such reports voluntarily. Evidently, China presently mandates only some firms to disclose ESG-related information. Even if China achieves a mandatory ESG disclosure framework in the future, the disclosure of negative information remains more challenging than that of positive information, necessitating theoretical and practical breakthroughs to address the complexities of ESG negative information disclosure.

Theoretical contributions of this study include a measurement method for the level of ESG negative information disclosure provided. While signaling theory, legitimacy theory, and stakeholder theory traditionally underpin ESG disclosures, they are more suited to explaining the motivations behind positive information disclosure and less effective in supporting the motives behind negative information disclosure. This study attempts to employ impression management theory to underpin hypotheses regarding the proactive versus passive and long-term versus short-term value effects of ESG negative information disclosure.

The practical contributions of this study involve examining the market effects of proactive versus passive disclosure during negative ESG events. This study offers valuable insights for firms in selecting appropriate ESG negative information disclosure strategies. Finally, when listed firms publish annual ESG reports that include both positive and negative information, it reflects the balance of the ESG report. Whether the disclosure of negative ESG information affects a firm’s long-term value is an intriguing topic. This study, by analyzing the impact of negative ESG information on long-term corporate value, incorporates ownership nature industry heterogeneity and examines the role of internal control in internal supervision. This provides empirical evidence on how negative ESG information can further influence a firm’s long-term value.

Literature Review

Research on Related Motivation

The existing studies on the motivations behind the disclosure of environmental, corporate governance, and social responsibility information primarily focus on positive information, such as self-interested motives (Zheng & Wang, 2021), ownership concentration (Naser et al., 2006), board independence (Lavin & Montecinos-Pearce, 2021), disclosure costs (Yue et al., 1997), financing needs (Cheng et al., 2014), and managerial social reputation (Z. Zhang & Chen, 2018). Self-interested motives include growth needs, reputation needs, and resource needs, etc. (J. W. Liu et al., 2025). The self-interested impression management greenwashing behavior adopted by enterprises in heavy polluting industries reduces the quality of environmental information disclosure (Zheng & Wang, 2021), enterprises with financing needs have higher greenwashing inclination (R. B. Huang et al., 2019), the implementation of compensation incentives by enterprises tend to encourage “greenwashing,” whereas equity incentives may curb such behavior and enhance ESG reporting quality (Wei & Gao, 2025). On the contrary, research indicates that firms, driven by internal financing motivations, reputation maintenance incentives, and external stakeholder pressures, are more likely to adhere to the constraints of social trust, thereby mitigating ESG overstatement (Y. C. Wang & Zhou, 2025), research also finds that investor-listed company ESG information interaction can curb corporate greenwashing by enhancing information transparency, reducing managerial myopia, and increasing reputational pressure (Zhao et al., 2025). From an external perspective, media attention and institutional factors have a significant impact on the quality of information disclosure (X. Chen & Zhang, 2022; Wu et al., 2015; Zhai et al., 2022; Zhou, 2024), however, the implementation of the policy has not led to enterprises disclosing all the information they should, but merely served as a tool for legitimacy management (Q. B. Chen, 2023), furthermore, Lee and Liang (2024) find that carbon regulation initiatives have a significant impact on corporate ESG performance, especially in the real estate sector. Their study further supports the importance of ESG disclosure for corporate sustainability and provides empirical evidence for understanding the variations in corporate ESG performance under different policy contexts. In addition, institutional investors’ shareholding will intensify the strategic disclosure of ESG information by enterprises (Z. F. Wang et al., 2025). The more frequently real earnings management occurs, the lower the willingness of enterprises to disclose ESG sustainability (T. L. Liu et al., 2023). The more frequently real earnings management occurs, the lower the willingness of enterprises to disclose ESG sustainability (T. L. Liu et al., 2023). In contrast, research specifically addressing the motivations for disclosing negative ESG information is limited. Some studies suggest that firms conceal negative information mainly to alleviate financing constraints (P. Huang & Li, 2020), reduce future share price crash risks (Tian & Wang, 2017), maintain a good reputation (Yu et al., 2021), and achieve short-term maximum benefits (Healy & Palepu, 2001).

Research on Related Economic Consequences

In the realm of economic consequence research, the majority of studies fail to make a clear distinction between positive and negative information. Instead, they investigate economic consequences solely from the holistic perspective of ESG information disclosure. For example, ESG information disclosure has been shown to enhance corporate value (J. F. Chen & Zhang, 2024; Kim, 2024), it is conducive to reducing financing costs (Lavin & Montecinos-Pearce, 2022; Y. Q. Wang & Xie, 2022), ESG information disclosure can reduce the risk of stock price crashes (Xi and Wang, 2022), and high-quality ESG information disclosure contributes to improving stock returns (H. Zhang, 2023). Moreover, ESG information disclosure exerts a notable promotional effect on the total factor productivity of enterprises (Sheng et al., 2024), and it significantly impacts ROE (Al-ahdal et al., 2023). Regarding the research on the economic consequences of negative information, if stakeholders perceive that firm activities negatively impact the ecological environment and society, which do not align with social norms and values, the disclosure of negative information may significantly damage the firm’s image and reputation, jeopardizing its legitimacy (Deegan, 2002; Lin et al., 2016). The results reveal that two-sided messages with the disclosure of highly relevant negative CSR information lead to negative effects in comparison to one-sided messages with only positive information, consequently, brands should exercise caution in communicating highly relevant negative CSR aspects (Müller et al., 2023). However, some studies hold contrary views. For instance, voluntary disclosure of negative information does not adversely affect investors’ decisions (Reimsbach & Hahn, 2015). Voluntary disclosure of environmental penalties can mitigate negative impacts on share market returns (Ding et al., 2020), the disclosure of negative information enables consumers to gain a deeper understanding of corporate information, thereby facilitating their intention to engage in word-of-mouth recommendations (B. R. Yang et al., 2024). Specifically, the higher the frequency of proactive information disclosure and the proportion of negative information disclosed, the more prominently the risk of stock price crashes is reduced (H. Q. Chen et al., 2024). The positive explanation of negative information during disclosure can lead investors to rate a firm’s social responsibility performance more favorably Zhang, He & Han (2016).

The studies above mainly unfold from the perspective of ESG information disclosure, the studies lack a direct focus on the economic consequences of disclosing negative ESG information. Given the mixed conclusions in related research and the significant obstacle posed by the fear of disclosure risks when negative ESG events occur, it is essential to move beyond the current paradigm that assumes positive information brings economic, environmental, and social benefits. Since negative events in firm operations have a high probability of occurrence, it is more advantageous to actively and fairly disclose such information rather than conceal it. This necessitates empirical evidence on the economic consequences of disclosing negative ESG information and how to enhance the balance of ESG reports. Consequently, the paper undertakes an in-depth empirical analysis to probe into the impacts of ESG negative disclosure on the short-term and long-term market values of enterprises.

Theoretical Analysis and Research Hypothesis

When listed firms encounter negative ESG events, they often amplify the anticipated consequences of disclosing negative information, fostering a stereotype that such disclosure inevitably brings adverse effects. As a result, they may unconsciously avoid negative information in their sustainability reports. Grewal et al. (2019) find that insufficient regulatory oversight and inadequate information disclosure can lead to adverse market effects. Furthermore, Gupta and Goldar (2005) discovery that poor environmental conduct by listed firms is penalized by the share market. Zhu (2011), using A-share listed firms that committed violations from 2008 to 2010 and their matched counterparts as the research sample, finds that the share prices of violators exhibit a significant negative reaction around the announcement date. K. Chen et al. (2020), studying environmental violations in the A-share market from 2010 to 2018, reveal that on the day of environmental information disclosure, the market imposes punitive reactions against the firm. However, by the second day after disclosure, the punitive impact has substantially weakened, and the negative influence is short-lived.

Given these findings, which suggest that negative information disclosure generates adverse market effects, this study posits that negative ESG information is more comprehensive and likely to cause a drop in share prices in the short term. Therefore, the research hypothesis is proposed:

However, there are significant differences in terms of disclosure timing and attitude. Delayed disclosure following exposure by regulatory authorities or the media constitutes passive disclosure, reflecting a negative attitude. This gives investors the impression of dishonesty, thereby undermining their confidence. The monthly environmental violation information disclosed by South Korea’s Ministry of Environment is significantly correlated with share valuations, with all listed firms appearing on the list experiencing noticeable declines in market value (Dasgupta, 2006). Negative ESG information reported through media channels significantly impacts share valuations (Wong & Zhang, 2022). Capelle-Blancard and Petit (2019) find that, based on a sample of 100 listed firms from 2002 to 2010, those facing negative ESG news see an average market value decline of 0.1%. If a firm fails to disclose negative information proactively and is instead exposed by a third party, it significantly negatively impacts investor decision-making (Reimsbach & Hahn, 2015).

Compared to passive disclosure of negative information, proactive disclosure – occurring prior to reports from regulatory authorities or the media – may be interpreted as a signal of trustworthiness, with the potential to mitigate the adverse impact of negative information (Toffel & Short, 2011). However, the subsequent direct research on proactive information disclosure remains scarce.

The studies above indicate that the market effects of passive disclosure of negative information differ from those of proactive disclosure. If a listed firm adopts a passive impression management strategy by concealing ESG-related negative information, it may maintain share price stability in the short term. However, given the trend toward increasing transparency, it faces the risk of exposure by the media and regulatory authorities, potentially causing greater harm to the firm’s interests. Conversely, opting for a proactive impression management strategy and voluntarily disclosing negative information reflects a commitment to social responsibility. If the firm also actively communicates and implements corrective measures, it further enhances its social image. Therefore, the following hypothesis is proposed:

Enhancing the disclosure of water resource emissions to communicate the state of water resources contributes to increasing corporate value (R. Huang, 2023). ESG performance can significantly and positively influence firm value (B. Wang & Yang, 2022; Wang et al., 2022). However, there are uncertainties. For instance, ESG practices may initially reduce firm value, but over the long term, they have a positive lagging effect on firm value (Yi et al., 2022). The relationship between ESG information disclosure and firm value may follow a “U” shape (R. Wang, 2022). ESG information disclosure should encompass both positive and negative aspects. In research on how ESG information disclosure enhances firm value, negative information has yet to be considered. The uncertainty in research findings on ESG information disclosure may include the impact of negative ESG information, which has not been studied. Related research indicates that the more a listed firm tends to conceal significant internal control deficiencies, the higher its cost of equity and debt capital and the lower its firm value (Zhang et al., 2016). There is a negative relation between firm carbon emissions and equity market value, while carbon management disclosure is positively related to equity market value (Saka & Oshika, 2014). The enhancement of firm value through carbon information disclosure is not immediate but is realized over time (X. Liu et al., 2021).

Some of these studies have touched upon the issue of disclosing negative information. The occurrence of negative information, such as resource consumption, is often objective. From the perspective of its impact on long-term firm value, a proactive impression management strategy transforms investors’ attitudes from short-term negative reactions to long-term positive assessments. Thus, the following hypothesis is proposed:

A sound and robust internal control system enhances the reliability of environmental information disclosure reports (Cohen & Simnett, 2015). Internal control has a positive impact on the market value (Gal & Akisik, 2020). However, some studies suggest that internal control is either unrelated (Beneish et al., 2008) or even negatively related to firm value (Engel et al., 2007). From the perspective of risk management and control, low levels of internal control increase corporate risk. In contrast, high-quality internal control can incentivize, constrain, and regulate managerial behavior through a series of institutional arrangements (Beneish et al., 2008), thus being beneficial for enhancing firm value. As an internal organizational arrangement, the primary goals of internal control are to improve firm performance and value, enhance the quality of financial reporting, and reduce the likelihood of violations. Therefore, internal control should play a moderating role in the relationship between negative ESG information disclosure and firm value. The hypothesis is proposed as follows:

Research Design

The Impact of ESG Negative Information Disclosure on Short-Term Firm Value

Sample Selection and Data Sources

The sample comprises listed firms on the Shanghai and Shenzhen A-shares that independently released ESG-related reports between 2020 and 2021. These reports, broadly defined, include ESG reports, social responsibility reports, and sustainability reports. The sample selection process is as follows.

First, this study obtains announcements. This study visits the official Giant Tide Information website, selects the period from January 1, 2020, to December 31, 2021, and uses keywords such as “administrative penalty,”“accident,”“incident,”“punishment,”“recall,”“pollution,”“sanction,”“warning letter,”“administrative supervision,”“notification,” and “cancellation.” This study identifies the list of sample firm security codes and uses Python to gather and download relevant announcements of negative events disclosed by A-share listed firms.

Second, this study filters the announcements that are obtained. This study excludes announcements unrelated to negative events in ESG. This study removes announcements with titles containing words like “progress,”“last five years,”“rectification status,”“reminder announcement,”“supplementary announcement,”“handling results,” and “update,” as these indicate the event has already occurred and been disclosed to avoid duplicate records. This study searches for titles containing the keyword “pre-notification.” If a listed firm receives a pre-notification of a penalty from a regulatory body before the official penalty, consider the “pre-notification” as the event disclosure point since its content is similar to the formal announcement. This study retains the pre-notification announcement and excludes subsequent formal penalty announcements. This preliminary screening based on the definition of ESG negative events yields 200 ESG negative event disclosure announcements.

Third, this study performs further screening. This study excludes announcements of significant events during the event period that may affect empirical analysis, such as share buybacks, stake increases, profit distributions, and donations that might significantly impact share prices. Announcements involving two ESG negative events within the event window are excluded, as multiple disclosures by the same firm during the event period could concurrently impact share performance, potentially leading to inaccurate results, resulting in a final sample of 176 ESG negative events. Firms in the financial sector, as well as ST/*ST firms, have been removed.

After these steps, this study obtains 112 qualified sample firms involving 140 ESG negative event disclosure announcements. The required daily individual share return rates, daily market return rates, and other financial data are sourced from the CSMAR database and the CNRDS database.

Selection of Research Methods

For the analysis of short-term value, most studies employ the event study method, while some opt for the difference-in-differences (DID) method. However, DID is primarily used to assess the effects of policy implementation, focusing on the impact before and after the enactment of a policy. In contrast, the event study method is mainly utilized to evaluate the effect of a specific event on a firm’s share price. In terms of research focus, DID emphasizes the average effect before and after an event, whereas the event study method centers on analyzing the impact at specific points in time. Both methods facilitate the evaluation of effects surrounding an event.

However, beyond comparing share price changes before and after an event, this study also seeks to analyze the duration of the event’s impact by examining fluctuations in share prices around the event date. Moreover, compared to DID, the event study method is better equipped to address heterogeneity in temporal treatment effects. Given the differing timing of negative event disclosures across firms in the sample, most studies tend to favor the event study method for analyzing share market changes before and after specific events. To gain a more detailed understanding of the fluctuations in share prices on each announcement day before and after ESG negative events, this study adopts the event study method.

Event Study Procedure

The most direct market effect of the actions of listed firms is the fluctuation in their share prices. According to the efficient market hypothesis, if share prices fully reflect all available information, the market can be deemed efficient. Although the development of the Chinese securities market developed relatively late, it has progressed rapidly, achieving the standards of a weak-form efficient market. In such a market, various types of information about a firm are quickly reflected in its share price, causing fluctuations. Based on this, this study explores the impact of disclosing ESG negative information on the short-term value of firms by measuring share price changes – specifically by calculating abnormal returns and conducting significance tests. The specific steps are as follows.

First, this study determines the event date, event window, and estimation window. Generally, the announcement day of a firm’s ESG negative event is taken as the event disclosure date. However, some announcements are released on Saturdays, Sundays, or public holidays, which are outside the share trading period and thus unsuitable for event studies. Therefore, this study sets the nearest trading day after the announcement day as the event disclosure date if the announcement falls on a weekend or holiday, noted as t = 0. The event window is defined as the ten trading days before and after the ESG negative event announcement, noted as t = [−10, 10]. The estimation window is defined as the 110 to 11 trading days before the ESG negative event announcement, noted as t = [−110, −11].

Second, this study establishes the estimation model. This study employs the market model to estimate the expected normal returns. The formula is as follows:

In the formula:

Third, this study calculates the excess return, representing the short-term value of the firm. The formula for actual returns is as follows:

In Formula 2,

The excess return is the difference between the actual return and the expected normal return, expressed as:

In Formula 3,

In Formula 4, the average excess return (AAR t ) on day t is calculated as the mean excess return of N shares on day t during the event period.

The cumulative excess return

The cumulative average excess return

Fourth, this study tests significance. After calculating the AAR and CAAR values within the event window of [−10, 10], it is necessary to employ statistical methods to test the significance of these calculations and verify whether AAR and CAAR are significantly different from zero. If the test results indicate a significant difference from zero, it signifies a strong short-term market effect resulting from the disclosure of negative ESG events by listed firms. Otherwise, the short-term market effect is not significant. This study employs a one-sample T-test to validate hypothesis H1 and an independent samples T-test to validate hypothesis H2.

One-Sample T-Test

To examine the impact of ESG negative information disclosure on share prices, this study employs the one-sample T-test method to test the average abnormal return (AAR) and cumulative average abnormal return (CAAR) of the sample data, specifically to determine whether there is a significant difference between the sample mean, and the population mean, thereby verifying the significance of the results. If AAR and CAAR show statistical significance during the event period, it indicates that the disclosure of ESG negative information exerts a significant market effect on share prices. First, the significance of the average abnormal return (AAR) is tested. The null hypothesis H0: AAR

t

= 0. The alternative hypothesis H1: AAR

t

≠ 0. A t-statistic is constructed, where

Next, the significance of CAAR is tested. The null hypothesis H0: CAAR

t

= 0. The alternative hypothesis H1: CAAR

t

≠ 0. A t-statistic is constructed, where

Independent-Sample T-Test

The independent samples T-test analyzes whether there is a significant difference by comparing the means of two samples, specifically examining whether the AAR and CAAR values of two independent samples differ significantly. In this study, a pairwise comparison is conducted between the proactive disclosure and passive disclosure samples of ESG negative information to determine if there are significant differences in AAR and CAAR values across different groups. If significant differences are observed, it indicates that proactive disclosure and passive disclosure of ESG negative information have markedly different impacts on share prices, leading to divergent returns for listed firms, thus validating hypothesis H2. If no significant differences are found, it suggests that the impact of proactive versus passive ESG negative information disclosure on share prices is not substantially distinct.

The Impact of ESG Negative Information Disclosure on Firm Long-Term Value

Sample Selection and Data Sources

Taking A-share listed firms that published ESG reports, social responsibility reports, and sustainability reports in 2020 to 2021 as samples, Python is employed to extract negative ESG textual information. After excluding samples that do not disclose negative ESG information, 607 sample firms are obtained, involving 897 observations. Among these, 381 negative ESG text samples are extracted in 2020 and 516 in 2021. The samples are then processed as follows: (a) excluding 317 firms with incomplete data for 2020 to 2021; (b) excluding 41 listed firms in the financial and insurance industries; (c) excluding one firm listed after 2020.

After the above screening, 248 sample firms and 496 observations are finally obtained. To eliminate the influence of outliers, continuous variables are subjected to a 1% level winsorize bilateral truncation. The relevant financial data are sourced from the CSMAR Database using Stata 17.0 software.

Definition and Measurement of Variables

The dependent variable is firm value, representing the firm’s long-term market effect. Firm value is measured using Tobin’s Q, introduced by a Harvard University financial economist in 1969, and represents the ratio of a firm’s market value to the current replacement cost of its capital. Tobin’s Q is significantly influenced by share prices, which serve as aggregators of information, sensitively reflecting the impact of information disclosure on firm value while being less susceptible to short-term investor decisions. Tobin’s Q represents a firm’s development potential and growth capacity, offering an effective fit for both market and financial data. By incorporating the capitalized value of diversified business returns, it accurately reflects the true value of a firm. Additionally, Tobin’s Q has the advantages of readily available data and relative ease of calculation. Considering previous scholarly research and the advantages of Tobin’s Q in representing corporate value, this study utilizes Tobin’s Q to represent firm value.

The explanatory variable is the level of ESG negative information disclosure. Currently, there is no standardized measure for ESG negative information disclosure, necessitating the creation of corresponding indicators to quantify this level. The tone of information disclosure can convey the underlying content of the text provided by listed firms (Loughran & McDonald, 2011). Therefore, this study measures the level of ESG negative information disclosure from the perspective of textual tone analysis. In existing tone quantification research, most studies calculate textual tone based on the number of positive and negative sentiment words as well as the total word count (J. Liu et al., 2022; Lu & Lin, 2022).

To further express the emotional intensity of negative information tone, this study adopts the approach used by Zuo (2022), which incorporates negation words and degree words into sentiment analysis, employing Python techniques to perform quantitative analysis of textual tone. The general steps are as follows. First, select texts containing ESG information, such as social responsibility reports, sustainability reports, and ESG reports. Next, construct an ESG sentiment lexicon, a degree word lexicon, and a negation word lexicon, and use Python to extract ESG negative text. Finally, measure the level of ESG negative information disclosure.

A higher score for the degree of textual tone indicates either a larger volume of ESG negative information disclosure or a more intense tone, suggesting that the firm provides a more comprehensive account of the negative events, thereby achieving a higher level of ESG negative information disclosure. The calculation formula is as follows:

In Equation 11, m represents the number of negative ESG text sentences for the sample firm, S_S is the sentiment score of the negative sentences, and ESG_(i,t) denotes the absolute value of the total sentiment score of negative ESG text sentences for the i-th sample firm in the t-th year. A larger ESG_(i,t) value indicates a stronger emotional expression and a more comprehensive disclosure of negative ESG information in the report.

Based on the sentiment tone analysis results, this study categorizes sentiment analysis scores into five levels, as shown in Equation 12. A score of 0 to 30 indicates a low level of ESG negative information disclosure, 30 to 60 indicates a relatively low level, 60 to 90 represents a medium level, 90 to 120 signifies a relatively high level, and a score of 120 or above indicates a high level of ESG negative information disclosure. The five levels of ESG negative information disclosure for listed firms –“low,”“relatively low,”“medium,”“relatively high,” and “high”– are assigned values of 1, 2, 3, 4, and 5, respectively.

The moderating variable is the level of internal control, measured using the Dibo Internal Control Index of Shenzhen, divided by 1,000. The control variables selected include firm size (size), debt-paying ability (lev), growth potential (growth), profitability (roa), ownership concentration (top1), and years listed (age). Additionally, year (year) and industry (industry) dummy variables are included to account for year and industry fixed effects.

The definitions of the relevant variables are shown in Table 1.

Variable Names and Definitions.

Model Specification

Based on the research above hypotheses and variable design, Model 1 and Model 2 are established, wherein Model 1 is employed to test Hypothesis H3, and Model 2 is utilized to test Hypothesis H4. The models are specified as follows:

Empirical Results and Analysis

Impact of Negative ESG Information Disclosure on Short-term Firm Value

Full Sample Empirical Analysis

The average abnormal returns and T-values for the full sample within [−10, 10] trading days are presented in Table 2.

Average Excess Returns and t-Values for the Full Sample Over the Trading Days of [−10, 10].

, and *** indicate significance at p < .05, and p < .01, respectively.

As shown in Table 2, the average abnormal return on the announcement day of negative ESG events for listed firms is significant at the 1% level. During the event period, the average abnormal return reaches its minimum at −1.563%, indicating that the disclosure of negative ESG events has a significant negative short-term impact on the firm’s share price. On the first trading day following the announcement, the average abnormal return is −0.433%, significant at the 5% level, suggesting a continued negative impact from the disclosure of negative ESG events. The average abnormal return shows little fluctuation from 10 trading days before the announcement to the day of the announcement and gradually returns to normal levels from the second to the 10th trading day after the announcement. The changes in cumulative average abnormal returns (CAAR) within each sub-window and their significance tests are presented in Table 3.

Cumulative Average Excess Return Profile and t-Value Within Each Sub-Window.

, **, and *** indicate significance at p < .1, p < .05, and p < .01, respectively.

Table 3 shows that the CAAR value in the sub-window [−5, −1] before the announcement date is significant at the 10% level, while other sub-windows are not significant. The CAAR values in the sub-windows [−1, 1], [−3, 3], and [−5, 5] around the announcement date are significant at the 1% level, and the CAAR value in the [−10, 10] window is significant at the 5% level. However, the CAAR values in the sub-windows after the announcement date do not pass the significance test. This indicates that the negative effect of ESG information disclosure arises before the announcement date, with the most substantial negative impact occurring on the announcement day.

In summary, Tables 2 and 3 conclude that the disclosure of negative ESG information brings about a significant negative market effect, thus verifying Hypothesis H1.

Grouped Sample Empirical Analysis

According to Hypothesis H2, the negative ESG disclosure events are categorized into voluntary and involuntary disclosures. To discern whether a listed firm’s disclosure of negative ESG events is voluntary or involuntary, one must compare the actual disclosure times of the regulatory agencies, media reports, and the firm’s disclosures. Financial news data for listed firms was downloaded from the CNRDS database, which includes news data from 20 authoritative media outlets. By obtaining the negative news content via the URLs of negative news, one can determine the timing of the firm’s ESG negative event disclosures and compare it with the media’s publication of the same events. If the media’s publication time precedes the firm’s disclosure, it indicates that the firm’s disclosure is involuntary.

Furthermore, if a firm does not disclose negative ESG events beforehand but only does so after receiving penalty decisions and regulatory measures from relevant authorities, it also constitutes involuntary disclosure. Through this analysis, the samples are divided into voluntary and involuntary negative ESG information disclosures. After screening, 34 events of voluntary disclosure and 106 events of involuntary disclosure are obtained. The average values of AR and CAR for the grouped samples and their respective T-tests are shown in Tables 4 and 5.

T-Test of AR Means for Grouped Samples.

, and *** indicate significance at p < .05, and p < .01, respectively.

Subgroup Sample CAR Means T-Tests.

, **, and *** indicate significance at p < .1, p < .05, and p < .01, respectively.

Table 4 shows that the AAR for voluntary disclosure is not significant 1 day before and after the announcement date. In contrast, the AAR for involuntary disclosure on the announcement day is −1.861%, significant at the 1% level, and the AAR on the first trading day following the announcement is −0.463%, significant at the 5% level. This indicates that involuntary disclosure of negative ESG information has a significant impact on share prices on the announcement day and the following trading day, whereas voluntary disclosure does not significantly affect share prices. Although voluntary disclosure of negative ESG information results in a negative market effect, it is smaller compared to involuntary disclosure.

Table 5 shows that within the sub-window [−1, 1], the CAAR for voluntary disclosure is −1.587%, significant at the 5% level, while other sub-windows do not show significance. The CAAR value for the sub-window [−10, 10] is 0.484%, indicating that voluntary disclosure of negative ESG information only negatively impacts share prices within the trading day before and after the event. In contrast, the CAAR for involuntary disclosure is significant in the sub-windows [−5, −1], [−1, 1], [−3, 3], [−5, 5], [−10, 10], and [1, 2]. This demonstrates that prior to involuntary disclosure, negative ESG events already have a significant adverse effect on the share market, with this impact lasting longer than that of voluntary disclosure.

Overall, the negative market effect of voluntary ESG negative information disclosure is relatively minor, whereas the negative market effect of involuntary ESG negative information disclosure is more substantial and enduring. These empirical results confirm Hypothesis H2.

Impact of Negative ESG Information Disclosure on Long-term Firm Value

Descriptive Statistical Analysis

Table 6 presents the descriptive statistics of the main variables.

Results of Descriptive Statistics.

As shown in Table 6, the maximum value of Tobin’s Q is 9.631, the minimum value is 0.8, and the standard deviation is 1.428, indicating substantial differences in firm value among different firms. The level of negative ESG information disclosure (QUAL_ESG) has a maximum value of 5, a minimum value of 1, and an average value of 1.528, suggesting that the level of negative ESG information disclosure among listed firms is relatively low, with a standard deviation of 0.869, indicating minimal variation in disclosure levels among different firms. The level of internal control (IC) has a maximum value of 0.883, a minimum value of 0.303, and a standard deviation of 0.09, indicating that the internal control levels among different listed firms do not vary significantly.

Analysis of Regression Results

Table 7 presents the regression results for Model 1 and Model 2.

Regression Results.

, **, *** denote significance at the 10%, 5%, and 1% levels respectively, with t-values provided in parentheses.

As shown in Table 7, the level of ESG negative information disclosure is significantly related to firm value at the 5% level, with a correlation coefficient of 0.136. This indicates that the enhancement of ESG negative information disclosure significantly promotes the increase in firm value, thus validating hypothesis H3. The reason is that improving the level of ESG negative information disclosure increases firm transparency, alleviating issues of information asymmetry both internally and externally. Moreover, the tone of ESG negative information in the disclosed texts of listed firms reflects the importance attached to negative events, thereby better indicating the adequacy of ESG negative information disclosure.

Although ESG negative information may have short-term adverse effects, in the long run, it greatly promotes the enhancement of firm value. This is because investors are not purely rational. Some may irrationally sell their shares upon the disclosure of negative information by listed firms. However, once investors return to rational thinking, the candid disclosure by the firms boosts investor confidence, thereby exerting a positive market effect on the capital market.

The moderating effect of internal control does not pass the significance test, possibly because internal control cannot influence the external environment, and internal control itself has certain limitations. Hence, it cannot provide a “guarantee” for improving the quality of ESG negative information disclosure, thereby affecting its moderating role in the relationship between ESG negative information disclosure and long-term corporate value.

Robustness Test

The sustainability of a firm is a crucial determinant of its value. This study conducts empirical analysis by replacing firm value with the growth rate of operating income (Value) and the natural logarithm of market capitalization (Lnmkt). Table 8 displays the robustness regression results after substituting the dependent variable. From the first column, it is evident that the quality of ESG negative information disclosure is significantly and positively related to firm value at the 5% level. The second column shows a significant positive relation at the 10% level. Both relations demonstrate significance. The robustness regression results are consistent with the primary regression results, confirming the robustness of this study’s conclusions.

Regression Results With Substituted Dependent Variables.

, **, *** denote significance at the 10%, 5%, and 1% levels respectively, with t-values provided in parentheses.

The factors influencing firm value are multifaceted. The model (1) may not encompass all relevant factors, potentially leading to omitted variable bias, which can induce endogeneity in the regression results. Therefore, this study adopts the approach of Yuan et al. (2022), utilizing instrumental variables to conduct a two-stage regression on Model (1) to control for endogeneity issues. Instrumental variables must possess identifiability, exclusivity, and relevance. First, this study selects the average quality of ESG negative information disclosure of other firms within the same industry (AINDUSTRY) as the first instrumental variable. There is a degree of relation between the quality of ESG negative information disclosure among firms in the same industry. There is no evidence suggesting that the ESG negative information disclosure quality of other firms within the same industry affects the target firm’s value. Second, this study selects the tenure of executives (TIME) as the second instrumental variable. Studies indicate a relationship between executive tenure and the disclosure of negative information (Ali & Zhang, 2015; Xu, 2017). However, no research has shown a significant relationship between executive tenure and firm value.

Table 9 presents the endogeneity test results. The relevance test result, “minimum eigenvalue statistic,” is 40.281, which is greater than the 10% critical value, indicating that this study rejects the hypothesis of weak instruments. The exogeneity test result shows a p-value much greater than .1, indicating that the instrumental variables meet the exogeneity condition. As shown in the second column of Table 9, after controlling for endogeneity, the quality of negative ESG information disclosure remains significantly and positively related to firm value. Therefore, the study results are robust.

Endogeneity Test Regression Results.

, **, *** denote significance at the 10%, 5%, and 1% levels respectively, with t-values provided in parentheses.

Heterogeneity Analysis

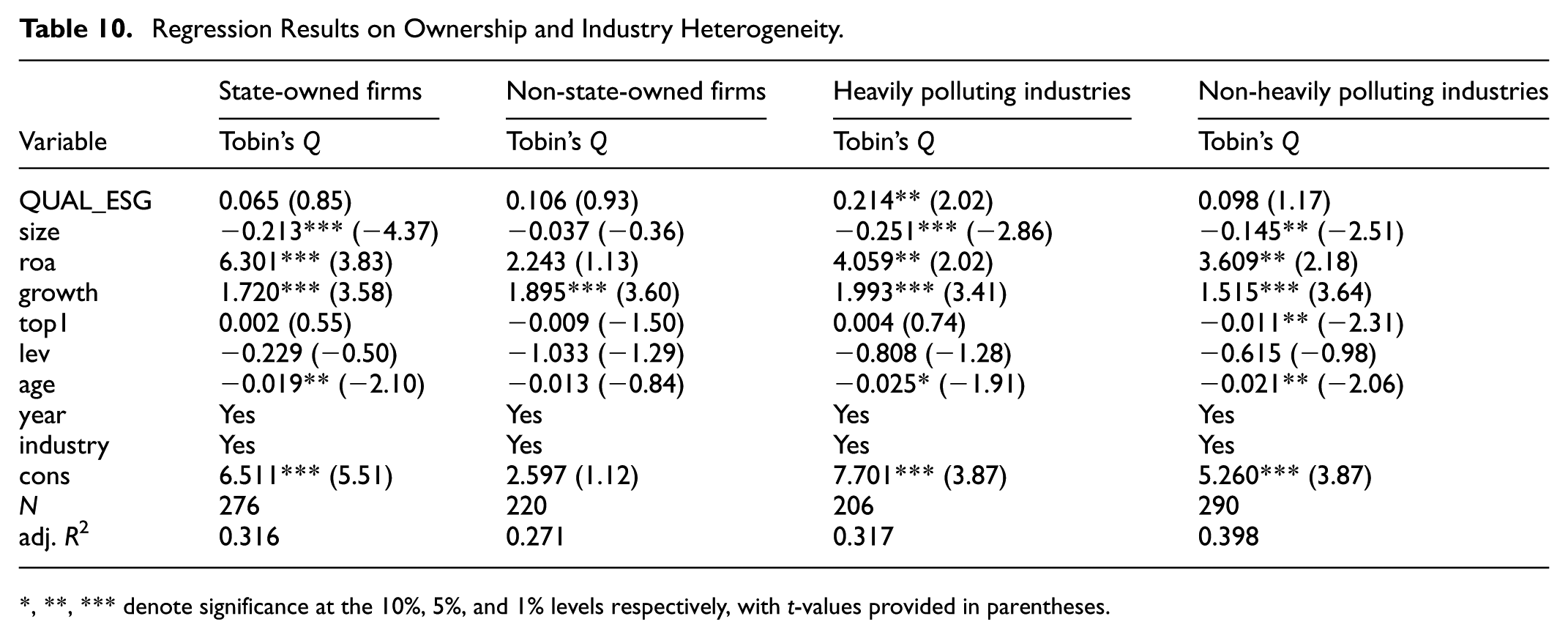

Compared to private firms, state-owned firms are more strongly influenced by political factors. Particularly, the chairpersons and CEOs of state-owned firms are appointed by the organization department, leading to a greater focus on political reputation than on operational performance. However, Table 10 indicates that the impact of ESG negative information disclosure on firm value does not significantly differ between state-owned and private firms. This suggests that political reputation is also a concern for private entrepreneurs, as many of them hold positions as deputies to the National People’s Congress or members of the Chinese People’s Political Consultative Conference and thus have considerable political connections. Table 10 also reports the relationship between ESG negative information disclosure and firm value in heavily polluting versus non-heavily polluting industries. The higher attention received by heavily polluting firms is a normal reaction under the anchoring effect and aligns with expectations.

Regression Results on Ownership and Industry Heterogeneity.

, **, *** denote significance at the 10%, 5%, and 1% levels respectively, with t-values provided in parentheses.

Conclusions and Implications

Research Conclusions

Stakeholders have shown an increasing interest in ESG information disclosure, prompting extensive theoretical discussions that affirm the value effect of such disclosures. However, these studies often overlook the significance of negative information in sustainability reports. This study focuses on A-share listed firms that released ESG negative information from 2020 to 2021, employing event study methodology to analyze the impact of ESG negative information disclosure on short-term firm value. The findings are as follows.

First, the disclosure of ESG negative information by listed firms leads to a temporary negative market effect, with a noticeable decline in average abnormal returns starting five trading days before the announcement, dropping below zero. The most significant decline occurs on the announcement day, with average abnormal returns exceeding zero and gradually returning to normal levels by the third trading day post-announcement.

Second, both proactive and reactive disclosures of ESG negative information negatively impact the share market. Proactive disclosure results in a smaller negative market effect, while reactive disclosure leads to a more substantial negative market impact.

Third, the negative market effect of proactive ESG negative information disclosure is short-lived, mainly concentrated on the announcement day and the trading day before and after the announcement. In contrast, reactive disclosure causes a negative market effect starting five trading days before the announcement, which persists until the third trading day after the announcement, thus lasting longer.

Fourth, regression analysis on the long-term market impact of ESG negative information disclosure reveals a positive relation between the level of ESG negative information disclosure and firm value. When examining the pathway of this positive relation, the internal control variable is introduced, but no moderating effect of internal control is found. Heterogeneity analysis indicated that firm integrity significantly constrains ESG negative information disclosure.

The stark contrast between the short-term and long-term value effects of ESG negative information disclosure offers valuable insights for enhancing investor information.

Research Implications

Based on the conclusions above, the following insights are offered to standardize ESG disclosures.

First, an examination of the collected texts reveals overlapping and redundant titles such as “ESG Report and Social Responsibility Report” and “Social Responsibility Report and Sustainability Report,” indicating non-standard disclosure practices. Thus, report titles should be standardized, and the overlap of various reports should be avoided.

Second, a shift in perspective is essential. Given the objective existence of negative ESG information and its potential long-term positive value effects, proactive disclosure and the implementation of corrective measures should be advocated rather than concealment. This requires media promotion and the establishment of policies for disclosing negative ESG information to gradually change societal perceptions, particularly those of market investors, and mitigate abnormal share price fluctuations caused by firms’“reporting concerns.”

Third, in terms of disclosure content and methods, it is advisable to draw on the experiences of developed regions internationally and establish basic standards for ESG information disclosure, gradually moving toward a “comply or explain” semi-mandatory stage. Firms should be required to issue separate ESG reports simultaneously with their annual reports.

Fourth, regarding market regulation, a combined assessment of negative and positive information indicators can effectively evaluate a firm’s ESG performance. Emphasizing a balanced ESG rating, market rating pressures compel firms to proactively disclose negative ESG information, thereby improving the current state of negative information disclosure. Additionally, leveraging the roles of government regulatory agencies and the media is crucial. Regular assessments and public disclosures of negative events and their handling by government regulators, along with timely reporting of negative ESG news by major media outlets, contribute to effective market regulation. Reassessing and supervising major media is also necessary.

Research Limitations and Prospects

First, in studying the short-term market effects of ESG negative information disclosure, while major factors potentially impacting share prices during the event period are excluded when screening the sample data, share price fluctuations are influenced by multiple factors, making it challenging to eliminate all influencing variables.

Second, in the heterogeneity analysis, the influence of the political reputation of executives in state-owned firms, who integrate administrative and capital power, on ESG negative information disclosure requires further in-depth investigation.

Third, as the ESG concept becomes increasingly entrenched, China is transitioning from a semi-voluntary, semi-mandatory disclosure stage to a fully mandatory disclosure stage. The economic consequences of ESG negative information disclosure within this evolving institutional context warrant further exploration in future research.

Footnotes

Ethical Considerations

Not applicable. This study did not involve human participants or collect any personal data; all data were obtained from publicly available sources and expert-rated documents.

Consent to Participate

Not applicable. No human subjects were recruited or interviewed for this research.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data supporting this study’s findings are available from the corresponding author upon reasonable request.