Abstract

This study delves into the correlation existing between the managerial prowess of CEOs and the performance of sustainability initiatives, drawing insights from the upper echelon theory. Through a comprehensive triple-down analysis, we ascertain whether an augmentation in managerial capabilities expedites the adoption of practices promoting environmental, social and economic sustainability (recognized as the pillars of sustainability). Furthermore, the research delves into the impact of CEOs’ career horizons on the relationship between CEO’s managerial ability and sustainability performance. Employing a panel data methodology on a dataset encompassing Chinese publicly listed companies spanning the years 2010 to 2019, our findings reveal a positive influence of CEOs’ managerial competence on the overall sustainability endeavors of these firms. These outcomes maintain their robustness even after subjecting them to various alternative empirical examinations. The conclusions drawn from these findings substantiate the interconnection between managerial skill and sustainability performance, underscoring the discrete impacts on each facet of the sustainability pillars. The identification of the potential for fostering sustainability practices through the skillful dissemination of management skills stands as a pivotal inference with significant implications for practitioners in the field.

Plain language summary

There are a lot of factors which influence the manager’s decisions and strategy. The study is critical because it investigates the most important requisite of the organization’s leader, “the ability of the CEO.” Moreover, it establishes the stance on how the ability impacts the sustainability practices of the organization. While digging deep, this study presents the triple-down analysis of sustainability performance, that is, three pillars of sustainability, namely social sustainability, economic sustainability, and environmental sustainability. This is the first study that has (1) researched the relation of CEO’s managerial ability with sustainability in developing economy, (2) has classified sustainability into its main pillars and studied each one with CEO’s ability. Using panel data methodology on Chinese listed firms from 2010 to 2019, we report that CEO’s managerial ability impacts the overall sustainability practices of the firms positively. Moreover, we find that social sustainability and economic sustainability also increases with the increase of the CEO’s managerial ability of the firm. We could not reach any significant relationship of environmental sustainability with managerial ability. Our results remain robust after utilizing various methodologies and definitions. Our findings confirm the upper echelon theory’s insights that illustrate that the firm’s top leadership characteristics influence firm-level decisions.

Introduction

The drive for increased corporate accountability, particularly regarding sustainability, originates from industrialization, resource depletion, ecological degradation, and exploitative labor practices. Diverse stakeholders fuel this demand. The United Nations’ serious concern about global environmental challenges is evident in its formulation of sustainable development goals (Griggs et al., 2013). These SDGs center on social, environmental, and economic dimensions, redefined to emphasize development addressing current needs while safeguarding the Earth’s life-support systems for present and future generations. Contemporary accountability underscores a focus on a firm’s triple bottom line performance (Hussain et al., 2018), necessitating balanced attention to environmental, social and economic aspects of sustainability. Proposing indicators structuring sustainability assessments to reveal significant economic, environmental, and social impacts, the Global Reporting Initiative (GRI) emerges as a key player (Morhardt et al., 2002). Attaining equilibrium among these sustainability pillars requires a comprehensive understanding of the interplay between society, industry, and the environment, extending to the implications of present decisions for future generations. As such, an enhanced awareness of intricate concerns tied to sustainable development is vital.

Historically, the primary determinants of sustainability have been identified as institutional factors and organizational characteristics in prior research endeavors (Yuan et al., 2019). Nonetheless, there is a perceptible shift in current trends, with recent investigations turning their attention toward the pivotal role of the Chief Executive Officer (CEO) in matters of accountability (Lewis et al., 2014). Within this framework, scholars have endeavored to establish connections between sustainability and various attributes associated with CEOs. Education, age, experience, gender, power dynamics, media exposure, individual personality traits, and life stage, collectively influence aspects such as personality, political ideology, religiosity, and leadership style (García-Sánchez et al., 2020).

The current study delves into the relationship between the Managerial Ability of CEOs (MACEO) and the sustainability performance (SusPerf). Furthermore, this study delves into the examination of how a CEO’s restricted career trajectory within a company influences sustainability performance and its foundational elements. Previous research findings indicate a significant correlation between the CEO’s career horizon and the strategic choices made by the corporation, subsequently influencing the outcomes of the organization (Hambrick, 2007). Despite an extensive body of literature addressing sustainability performance and managerial ability independently, there exists a pressing need to establish a connection between these two aspects. A more comprehensive exploration of the interplay between the managerial competence of CEOs and the dimensions of sustainability is imperative for a holistic comprehension. While previous efforts to uncover this connection have been constrained, recent undertakings by García-Sánchez et al. (2020) and Yuan et al. (2019) have aimed to clarify the correlation between the managerial prowess of CEOs and their influence on Corporate Social Responsibility (CSR) or sustainability achievements. Nonetheless, these investigations have not extensively explored the complexities of sustainability nor utilized a comprehensive triple-down analytical framework. In contradistinction, our empirical contribution entails a meticulous exploration of all three sustainability dimensions within this specific interrelation.

Additionally, the prior research failed to explore the relationship between managerial competence and sustainability within developing economies such as China. This present study addresses and rectifies this research gap. This research uncovers a multitude of dimensions within the connection between management ability and sustainability by meticulously evaluating distinct elements of sustainability. In doing so, the research presents an all-encompassing perspective on sustainability, stressing the importance of skilled business management in upholding responsibilities in fiscal, social, and ecological spheres. By adding to the literature on the relationship between leadership skills and sustainability, this study lends credence to claims concerning the interdependence and relative importance of different aspects of sustainability (Lozano, 2008). Our study also demonstrates the influence of CEO career horizon on sustainability performance, complementing prior literature on the connection between CEO career horizons and financial performance (Krause & Semadeni, 2014; Matta & Beamish, 2008; McClelland et al., 2012). Notably, our research demonstrates that organizations’ strategic choices concerning non-financial performance, especially those pertaining to sustainability practices, are impacted by quantitative aspects of CEOs, such as their age.Furhermore, there is no study exist which has study the moderating role of CEO’s career horizon in the relationship of CEO’s managerial ability and sustainability performance.

Since the existing research does not fully account for the effect of the CEO’s managerial skill on all three dimensions of business sustainability, our investigation is particularly thorough. The Sustainability Performance (SP) reporting system developed by the Global Reporting Initiative (GRI) will help us get there. Guidelines for Sustainable Reporting (Hussain et al., 2018), businesses are required to divulge both favorable and unfavorable outcomes across all dimensions of sustainability, assuming an equal significance of each for the sake of long-term progress. Through the utilization of this framework, our study unveils numerous dimensions within the interconnection between management and sustainability by methodically quantifying distinct elements of sustainability in isolation (Lozano, 2008).

Numerous theoretical frameworks have been put forth by scholars to delineate sustainability. Among these are the resource dependence theory (Fodio & Oba, 2012), the resource-based view (Amran et al., 2014), the stewardship theory (Sharif & Rashid, 2014), and the neo-institutional theory (Ntim & Soobaroyen, 2013). However, each of these theories individually falls short of providing a comprehensive explanation of the link (Hussain et al., 2018), and no singular hypothesis can satisfactorily capture the intricate connections (Walls et al., 2012).

Theoretically, our research makes a distinctive contribution to various paradigms within the realms of management, governance, and society. Our primary hypothesis stems from the upper-echelon theory, which posits that a manager’s attributes significantly influence a firm’s decision-making processes. Furthermore, in order to establish the connection between managerial competence and sustainability, our study incorporates insights from agency theory. It is essential to comprehend the roles that various corporate governance mechanisms play as intermediaries in bridging the gap between management and sustainability. Furthermore, our study draws upon stakeholder theory (Freeman, 1884) to underscore the multifaceted nature of sustainability. This is the first study which has linked the literature streams along with empirical evidences of three intereting phenomenons namely sustainadbility performance of the firms, CEO’s managerial ability and CEO’s career horizon.

In addition, our findings hold potential to guide forthcoming research endeavors. Given that projected influences often focus on a single dimension of sustainability (be it social or environmental), there exists a need to evaluate sustainability performance within the context of the triple bottom line, encompassing economic, social, and environmental considerations.

Literature Review and Hypothesis Development

The literature has identified various factors influencing Sustainability Performance (SP), encompassing elements at the organizational, individual, societal, and institutional levels. A recent trend in research involves examining the behavioral drivers of Strategic Performance (SP) exhibited by senior leaders. This strategy is founded on the understanding that CEOs play a pivotal role in shaping the direction of an organization (Hambrick & Mason, 1984). CEOs are responsible for coordinating firm-level outcomes to satisfy the interests of all stakeholders (Godos-Díez et al., 2011; McWilliams et al., 2006). This is why sustainability is regarded as a strategic imperative (Aguinis & Glavas, 2012). Within the literature, there are several CEO characteristics that affect shareholder returns, including personal values. (Hemingway & Maclagan, 2004), conceit ((Petrenko et al., 2016), career horizon (Oh et al., 2016), hubris (Tang et al., 2015), personal rewards (Fabrizi et al., 2014), and political ideology (Chin et al., 2013).

The Upper Echelon theory firmly supports the relationship between CEO Managerial Ability (MACEO) and Sustainability Performance (SusPerf). This theoretical framework posits that CEOs’ attributes and competencies wield substantial influence over their firms’ strategic decision-making and overall performance (Hambrick & Mason, 1984). MACEO is intricately linked to an enhanced comprehension of a firm’s operations and the factors driving its performance (Cui et al., 2019; García-Sánchez & Martínez-Ferrero, 2019). This heightened ability facilitates the more effective utilization of organizational resources (P. R. Demerjian et al., 2013), enabling the assessment of novel business opportunities and adept management of uncertainty (Yuan et al., 2019). MACEO also enables a comprehensive understanding of environmental cues and the formulation of responsive strategies (Tang et al., 2015), fostering the adoption of innovative approaches (Y. Chen et al., 2015), and informed risk-taking (Yung & Chen, 2018).

In a similar vein, Porter (1992) recommends that managers should give more weight to long-term performance goals than short-term ones, such as R&D, advertising, and employee training. A manager’s replacement is frequently the result of subpar performance (Denis & Denis, 1995; Hermalin & Weisbach, 2012), which may make it difficult to find new employment (Kaplan & Reishus, 1990). Considering the correlation between management turnover and performance sensitivity (Weisbach, 1988), it is conceivable that firms boasting higher managerial prowess exhibit more adept sustainability practices. According to Di Giuli and Kostovetsky (2014) and Falck and Heblich (2007) corporate Social Responsibility (CSR) requires a long-term investment with erratic, postponed rewards. CEOs’ investment decisions in CSR are likely to be influenced by concerns about their careers. CEOs with elevated competence levels are prone to possess brighter future career prospects, thereby experiencing fewer career-related worries (Cui et al., 2019). Consequently, they can disregard the pressure to invest in ventures that yield swift and dependable returns. Moreover, their adeptness in navigating uncertainties allows capable CEOs to tackle the ambiguity associated with CSR investments with less trepidation. The ability of CEOs to have an impact on their companies’ CSR initiatives becomes crucial given that CSR strategies are by their very nature complex and long-term (Yuan et al., 2019). Since they are less pressured to prove their ability to the job market, competent leaders are more likely to support CSR activities despite the uncertainties and long-term effects (Rajgopal et al., 2006). According to earlier research (García-Sánchez & Martínez-Ferrero, 2019; Yuan et al., 2019), a CEO’s managerial skills are positively correlated with both CSR investments and performance.

Conventionally, the realm of social sustainability has largely fallen under the purview of governments, yet businesses are progressively emerging as substantial contributors. Socially sustainable activities encompass actions that enhance relationships with various stakeholders, including employees, customers, suppliers, and local community members. At the core of the concept of social sustainability is the system’s capacity to uphold an acceptable level of social well-being. Consequently, an organization attains social sustainability when its endeavors facilitate the prospects of future generations to cultivate thriving communities. Pertinent matters within the realm of social sustainability encompass issues like child labor, ethical trade, and supply chain management. Despite being outlawed in the majority of nations, child labor is nonetheless common. Trading that is honest and legitimate is referred to as ethical trading. On the other hand, Bribery, anti-competitive practices, corruption, inflated pricing, unethical marketing, and the abuse of market dominance are all examples of unethical business practices. With many organizations, especially multinational ones, sporting intricate and far-reaching supply chains, the demand for corporate responsibility extends beyond their own activities to include those of their suppliers. Firms that fail to optimize the utilization of their resources are more prone to veer away from social sustainability. As successful resource management and acute market awareness pave the way to sustainable competitive advantage for every business (Holcomb et al., 2009). Enterprises led by CEOs possessing exceptional managerial prowess are adept at harnessing their firm’s resources to the fullest extent (P. Demerjian et al., 2012; P. R. Demerjian et al., 2013). Consequently, these companies are less likely to engage in practices contrary to social sustainability (Yuan et al., 2019), as their resource optimization skills obviate the need for such approaches.

Environmental sustainability encompasses the conscious decision-making and proactive measures taken to safeguard the natural world, particularly with regard to its role in sustaining human life. The imperative of environmental sustainability is multifaceted, grounded in both humanistic considerations and practical necessities. From a human-centric viewpoint, the reliance of human survival on the environment underscores the need to confront the challenges posed by it. Environmental issues such as climate change, waste management, and pollution further accentuate the importance of sustainability efforts. The argument for sustainability extends intergenerationally, emphasizing the ethical obligation of the current generation to ensure a sustainable future for subsequent ones. Those advocating for nature’s intrinsic value emphasize its preservation as a fundamental principle. Although the strength of each of these justifications may differ, taken as a whole, they provide a strong case for environmental sustainability. CEOs with low managerial skills frequently choose making short-term investment decisions and steer clear of projects with higher levels of risk due to their predisposition for risk aversion (Graham et al., 2005). These CEOs, possessing lesser proficiency, tend to favor low-risk ventures, quick talent transfers, and short-term investments (Narayanan, 1985). Considering all of these variables, our hypothesis states that CEOs endowed with exceptional managerial ability show an unwavering commitment to engage in environmental preservation.

An organization’s impact on local, national, and global economies is part of the economic sustainability metric. By making the most of what they have, businesses may ensure their continued viability and success throughout time in this dimension. The overarching objective is to promote the sustained utilization of these resources for the long term. Both the long-term viability of enterprises and the stability of the financial system are included in economic sustainability. The practice of transparency, openness, and sincerity in reporting a corporation’s operations and strategic directions is among the most crucial components of economic sustainability. When a company is open with its stakeholders, those outside the company can gage the risks the company faces. CEOs with great managerial skills show extensive knowledge of their company’s operations, which improves their judgment and precision. This, in turn, enhances the quality of reporting and fosters transparency (P. R. Demerjian et al., 2013).

According to our argument, CEOs with greater levels of competency are more likely to invest in corporate social responsibility (CSR). Additionally, capable CEOs are more likely to choose excellent CSR programs that promote sustainability in the environmental, social, and economic spheres (García-Sánchez & Martínez-Ferrero, 2019; Tang et al., 2015).

H1: CEO’s managerial ability and sustainability performance are positively linked.

H1.1: There is a positive correlation between a CEO’s managerial competence and the social sustainability performance of the organization.

H1.2: The CEO’s managerial ability is positively associated with the environmental sustainability performance of the organization.

H1.3: The CEO’s managerial ability is positively connected to the economic sustainability performance of the organization.

Prior studies have shown that senior managers’ career spans tend to shorten as they get older, which reduces the long-term benefits for businesses (Davidson et al., 2007; Oh et al., 2016). Psychologists argue that managers change with time, which impacts their decision-making styles (Chatterjee & Hambrick, 2006; Ortiz-de-Mandojana et al., 2019). Amongst these factors, CEOs age has emerged as a crucial determinant in corporate decision-making. Notably, Gray et al. (1997) have observed a correlation between CEOs’ decision-making processes and their time horizons, with older CEOs exhibiting comparatively shorter horizons. Several factors substantiate our proposition. In comparison to their older counterparts, younger CEOs tend to grasp new concepts more swiftly due to the apparent decline in certain cognitive abilities with age (Sannino et al., 2020). As executives age, they often become more entrenched, displaying inflexibility and resistance to change (McClelland et al., 2012). These older leaders predominantly draw upon their previously well-honed organizational and strategic problem-solving strategies (McClelland et al., 2010). In contrast, many younger CEOs possess a contemporary understanding of recent global shifts. Unlike their older counterparts, young CEOs demonstrate a greater proclivity for embracing strategic shifts and aligning organizational operations with contemporary demands. Such executives are more inclined to adopt audacious decisions to pursue their objectives (Bertrand & Schoar, 2003). The career goals and decision-making inclinations of CEOs are influenced by their age as well. For example, previous studies have shown that when CEOs get older, their career perspectives tend to shorten, which results in a decreased emphasis on research and development (R&D) activities and a more cautious approach to investments (Barker & Mueller, 2002; Cazier, 2011; E-Vahdati & Binesh, 2022).

According to research by Serfling (2014), CEOs’ career perspectives tend to shorten as they get older, which increases their propensity for cautious investing choices. In line with this, senior CEOs have been found to have a more conservative approach to making financial decisions (Bertrand & Schoar, 2003).

The body of prior literature also emphasizes the appearance of agency problems when CEOs get closer to retirement age (Davidson et al., 2007), sometimes known as the “career horizon problem.” According to Matta and Beamish (2008), CEOs with shorter remaining tenures may have a propensity to shun making important investment decisions. Additionally, it has been noted that elder CEOs place more focus on short-term gains than long-term results (Davidson et al., 2007). The impact of a CEO’s measurable characteristics, such as age, on a firm’s strategic performance has been consistently shown in earlier research. These studies have covered topics like foreign market entry (Herrmann & Datta, 2002), anti-takeover measures (Buchholtz & Ribbens, 1994), and corporate social responsibility (CSR) initiatives (Oh et al., 2016). Younger CEOs are more likely to improve a company’s sustainability and environmental performance, according to Shahab et al. (2020). Similar to this, Yuan et al. (2019) found that the proxy for career horizon acts as a negative moderator in the positive link between CEO competencies and CSR performance, particularly as CEOs approach retirement. The influence of CEOs’ ages on the decision-making process to improve sustainability performance is not well understood, despite the vast research on the subject.

In substantiating the preceding discourse, we posit the ensuing arguments: Firstly, aging CEOs tend to exhibit an inclination toward a more entrenched and rigid cognitive framework owing to the efficacy of their prior strategic management approaches. This predisposition translates into a resistance toward adopting novel management styles, fostering inflexibility, and a proclivity for maintaining the status quo (McClelland et al., 2010). Secondly, it is interesting to observe that among Chinese listed companies, the ideas of corporate ethics and sustainability are still in their infancy. As a result, elder CEOs are less motivated to demonstrate sustainability performance, which requires a major time and resource commitment.

This reluctance is underscored by the potential compromise it poses to immediate profitability (Herda et al., 2014; Simnett et al., 2009).

Summing up, keeping insights from agency theory, able CEOs having short career horizon, will try to invest more on short term projects to earn the fame as successful CEO. On the contrary, able CEOs having long horizon will invest more toward long term projects including sustainability issues.

Building upon the aforementioned rationale, we put forth the subsequent hypothesis:

H2: CEO’s short career horizon negatively moderates the relationship between CEO’s managerial ability and sustainability performance.

H2.1: CEO’s short career horizon negatively moderates the relationship between CEO’s managerial ability and social sustainability performance.

H2.2: CEO’s short career horizon negatively moderates the relationship between CEO’s managerial ability and environmental sustainability performance.

H2.3: CEO’s short career horizon negatively moderates the relationship between CEO’s managerial ability and economic sustainability performance.

Research Methodology

Data Description

The “China Stock Market and Accounting Research” database supplied financial and governance data for all 4,132 A-shares that were listed on the Shanghai and Shenzhen exchanges between 2010 and 2019. The selection of 2010 as the starting point for data collection is supported by the initiation of China’s Thousand Talents Plan near the end of 2008. This initiative aimed to attract CEOs based on their proven managerial capabilities (Yuan et al., 2019). For the acquisition of sustainability assessments, the HEXUN website served as the source for the HEXUN-RKS ratings applicable to the entirety of A-share Chinese listed corporations. These HEXUN-RKS ratings encompass annual evaluations of Chinese firms across a spectrum of social, environmental, and economic indicators, ultimately aggregating into an all-encompassing CSR score. It is imperative to note that this database exclusively comprises Chinese enterprises that undertake the publication of sustainability reports, hence rendering it an extensively utilized resource within Chinese research undertakings (Lau et al., 2016; Shahab et al., 2020). To ensure methodological rigor, financial institutions were excluded from the dataset, with continuous variables subjected to an arrangement wherein the 1% tail was isolated to mitigate potential concerns related to outliers. Additionally, firms marked by a sequence of three consecutive years with missing values were excised from the dataset. The resulting dataset consists of a panel of 3,052 imbalanced firms, totaling 20,651 firm-year observations. From a low of 1,373 observations in 2010 to a high of 2,649 observations in 2018.

Variables Design

Dependent Variable

The dependent variable under scrutiny pertains to the assessment provided by independent rating agencies, exemplified by the “HEXUN-RKS” framework. This evaluation encompasses the enduring sustainability performance of entities, encompassing their comprehensive engagement in sustainable, social, environmental, and economic pursuits, as discerned through their involvement in Corporate Social Responsibility (CSR)-related endeavors over specific fiscal periods. The relevant values for this variable appear as continuous metrics taken from the HEXUN database, with a scalar spectrum ranging from 0 to 100 marking the greatest attainable rating score.

Independent Variable

Managerial Ability

Academics employ a diverse set of variables to assess managerial competency, which includes factors such as the company’s size (Rosen, 1990), historical stock performance (Fee & Hadlock, 2003), and media evaluations. However, given that these variables are presumed to gage managerial aptitude to an extent of typical representation and may possess limited robustness in terms of their testing efficacy, their reliability remains somewhat constrained (P. R. Demerjian et al., 2013).

Our research derives the construct for measuring CEO’s Managerial Ability (MACEO) from the work of P. Demerjian et al. (2020). The underlying concept is that this metric serves as an indicator of a CEO’s proficiency in efficiently converting business resources into revenue, particularly when juxtaposed with industry competitors. Managers are often regarded as having a higher level of ability when they can enhance the output obtained from a specific set of inputs. The challenge in quantifying managerial skill lies in its inherent non-measurability, necessitating its inference from observable outcomes stemming from resource allocation decisions. In a quest to enhance the precision of management skill assessment, P. Demerjian et al. (2020) employ a two-step approach. The initial step involves employing Data Envelopment Analysis (DEA) to compute firm efficiency on a year- and industry-specific basis. This method requires the specification of both input and result variables. The authors include seven input variables: cost of products sold, selling, general, and administrative expenditures, property, plant, and equipment, operating lease, R&D cost, goodwill, and other intangibles. Gross revenue is the measure of success. They start by utilizing DEA to resolve the following optimization issue:

The efficiency metric in the DEA model, as mentioned earlier, can range from zero to one. The total efficiency, representing the overall efficiency of the business, was divided into contributions from both management and the entire firm. This division was made because both management and the entire firm play roles in the overall efficiency of the business. Based on this distribution, six distinct factors were identified to impact whether managerial assistance is facilitated or hindered. Subsequently, in the next regression study, the aim was to establish the relationship between these company variables and the overall firm efficiency. Factors such as business size, market share, positive cash flow, and business age were considered as elements that promote managerial contributions. Additionally, the investigation accounted for complex multi-segment and multinational operations, two variables known to impede efficient managerial engagement.

They calculate the Tobit regression as follows:

In Model 2, the residual is used to measure managerial expertise. In a study (P. Demerjian et al., 2012), this metric was utilized to construct decile rankings of managerial proficiency, referred to as CEOMA in the context of this research. These rankings were developed while taking into account both the year and industry, enhancing comparability across various time periods and industries and reducing the impact of outliers.

CEO Career Horizon

Age affects CEOs’ career horizons (Cazier, 2011; Oh et al., 2016a);, which can be interpreted as a psychological element in professional performance over retirement (Davidson et al., 2007; Matta & Beamish, 2008). If the retiring CEO is 63 or older, HorizonCEO is equal to 1.

Control Variables

Several control variables associated with the company, the board, and the chief executive officer have been included to prevent skewed results. This study uses variables like Return on Asset (RetonAssets) ratio, Tobin’s Q (TobQ), Debt to Asset Ratio (DebtoAssets), and Size (log of total assets) as control measures, which is in line with the methodology of García-Sánchez and Martínez-Ferrero (2019). The potential relationships between sustainability performance (SusPerf) and firm performance, growth prospects, financial stability, and firm size are addressed by these variables.

For CEO-related controls, Incorporating the variables DualityCEO (which indicates whether the CEO also serves as chairman) and GenderCEO (which indicates whether the CEO is male). In addition, factors related to corporate governance are taken into account, such as SizeBoard (measured as the total number of directors), IndBoard (measured as the percentage of independent directors to total directors), and Board meeting (MeetBoard). Further, defination of the variables are available in the Appendix 1.

Following the methodology of Yuan et al. (2019), this study also incorporates the Herfindahl–Hirschman Index (HHI) to account for market competition. Furthermore, firmAge (firm age) is included. HHI reflects market competition through the summation of squared market shares of all firms within the same industry, as assessed at the fiscal year’s end. Net operating assets (NOA) and Altman’s z-score (ZScore) are two examples of financial flexibility metrics that can be adjusted for both sector and time effects econometric model. We used the following model to examine the relationships between SP (sustainability performance), SP_Social (social sustainability), SP_Env (environmental sustainability), and SP_Eco (economic sustainability), as well as CEOMA (CEO’S MANAGERIAL ABILITY).

Firm and time are represented by subscripts i and t. Z is the collection of control variable vectors.

Descriptive Statistics

Table 1 provides a comprehensive overview of descriptive statistics. In Chinese companies, the SusPerf scores range from 0 to 73, with an estimated average score of approximately 23. The average MACEO score varies between −0.314 and 0.391. Another characteristic of Chinese businesses is that their typical Board of Directors (BoD) comprises eight to nine members, and they conduct an average of nine meetings per year. Additionally, the descriptive statistics for the control variables align with those observed in previous research projects (McGuinness et al., 2017).

Descriptive Statistics.

Note. The descriptive statistics for each variable included in the basic model are shown in Table 1. Appendix 1 has a definition of each variable.

Results and Discussions

Impact of Managerial Ability on Sustainability Performance

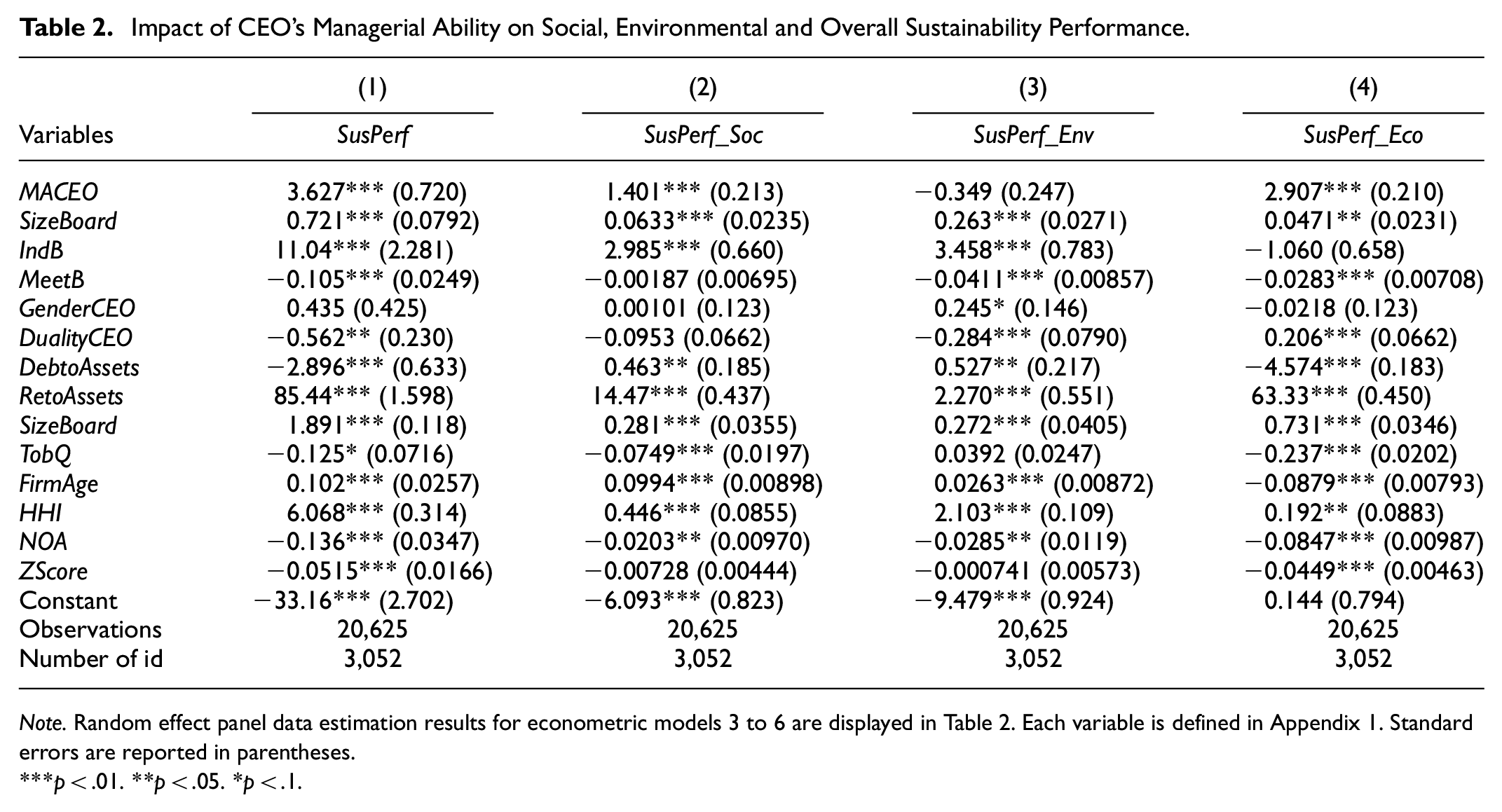

Models 3 to 6 are estimated using the random effect model method within a panel data framework, and the results are tabulated in Table 2. Following the Hausman specification test, a random effect regression model is used to examine the impact of CEOMA factors on SP, focusing on the SusPerf_Social, SusPerf_Env, and SusPerf_Eco dimensions.

Impact of CEO’s Managerial Ability on Social, Environmental and Overall Sustainability Performance.

Note. Random effect panel data estimation results for econometric models 3 to 6 are displayed in Table 2. Each variable is defined in Appendix 1. Standard errors are reported in parentheses.

p < .01. **p < .05. *p < .1.

The second column of Table 2 demonstrates the ramifications of CEOs’ managerial prowess on the holistic spectrum of sustainability performance. The coefficient, standing at 3.267 and achieving a significance level of 1%, signifies a positive relationship. This result demonstrates that better managerial competence contributes to enhanced performance in the realm of sustainability. Our research lends credence to H1, the hypothesis that links the CEO’s managing abilities and performance in the area of sustainability favorably. This result is consistent with both our expectations and earlier research studies, such as those carried out by García-Sánchez et al. (2020), García-Sánchez and Martínez-Ferrero (2019), and Yuan et al. (2019).

The antecedent literature has already underscored the pivotal role of elevated managerial proficiency for firms by highlighting its significance as a determinant of firm financial performance (Baik et al., 2011; Bertrand & Schoar, 2003; P. R. Demerjian et al., 2013). Our study contributes by revealing that managerial ability is equally pivotal for non-financial performance aspects, specifically in the context of Corporate Social Responsibility (CSR) for firms. Our findings emphasize that augmenting managerial ability corresponds to an increase in socially responsible practices while concurrently curbing behaviors that might be regarded as socially, environmentally, and economically irresponsible.

In this study, one way to gage a company’s commitment to social responsibility is to look at how it measures up in terms of social sustainability performance in areas like labor, human rights, social impact, and product stewardship. Table 2, column 3 displays the results of the study concerned with social sustainability. Based on the findings of our random effect model, we find that SusPerf_Social is positively related to the CEO’s managerial ability (MACEO). At the 1% level of significance, a coefficient of 1.401 suggests that increased management competence positively affects performance in the social dimension of sustainability has a favorable impact on the social component of sustainability performance.

The ensuing dimension scrutinized is environmental sustainability (SusPerf_Env), reflecting a firm’s commitment to environmentally responsible practices. The ensuing section, situated in Table 2 (column 4), expounds upon the results regarding the nexus between MACEO and SusPerf_Env. Our random effect model outcomes reveal an unexpected and statistically insignificant negative relationship between MACEO and SusPerf_Env. This incongruity with our initial hypotheses and Hypothesis H1.2 prompts a reconsideration of sustainability strategies. While these findings diverge from theoretical expectations, they are substantiated by real-world dynamics. In the aftermath of the commencement of the Thousand Talents Program, Chinese firms displayed remarkable performance in terms of growth and market prowess, yet environmental impact management proved to be a challenge. Notably, China’s standing as the world’s largest carbon dioxide emitter and its hosting of several of the world’s most polluted cities underscores the complexity of achieving environmental sustainability goals despite the government’s concerted efforts (Shahab et al., 2020).

Finally, exploring the economic side of sustainability entails improving local, national, and international economies by implementing transparency and accountability in entrepreneurial endeavors. In Table 2 (column 5), the panel data estimates for economic sustainability are described in more detail. The results of the random effect model show a significant and favorable association between SusPerf_Eco and the CEO’s managerial abilities (MACEO; Coefficient: 2.907, p = .01). According to this finding, Chinese businesses are adopting more sustainable economic practises as their managerial skills improve.

Moderating Impact of CEO’s Career Horizon

Table 3 presents the results of our examination into the impact of CEO Horizon (HorizonCEO) on the relationship between CEO’s managerial ability (MACEO) and sustainability performance (SusPerf). Models 7 to 10 employed panel data estimation through the random effect model approach. We assessed SusPerf, SusPerf_Social, SusPerf_Env, and SusPerf_Eco for their responsiveness to MACEO while incorporating the variations in the HorizonCEO) by employing a random effect regression model guided by the Hausman specification test. The results emanating from these models unveil a statistically significant negative correlation between MACEO and SUSPerf due to moderating impact of HorizonCEO. Evidently, a negative association exists between HorizonCEO and SusPerf, indicating that firms led by abler but older CEOs tend to engage in fewer sustainability practices due to the constraints posed by their relatively shorter career horizons in comparison to their younger counterparts. In other words, the sustainability performance is more pronounced among firms led by younger CEOs when contrasted with those helmed by their elder counterparts.

Impact of CEO Horizon on Social, Environmental and Overall Sustainability Performance.

Note. Estimation outcomes for econometric models 3 to 6 are shown in Table 2 below using random effect panel data. Each variable’s definition is provided in Appendix 1. Standard errors are reported in parentheses.

p < .01. **p < .05. *p < .1.

This assertion is grounded in the observation that social sustainability practices are still in the nascent stages within the context of Chinese listed firms. As such, business ethics in this domain are undergoing developmental evolution. Furthermore, the pursuit of sustainability practices may introduce a level of risk to current profit margins, which could be a disincentive for older CEOs. Additionally, Older CEOs are more likely to follow conventional management practises, frequently doing so because past policy decisions have been successful. This is especially true as they get closer to retirement. According to Strike et al. (2015) and Hussain (2023), this propensity may even lead to an intentional avoidance of Corporate Social Responsibility (CSR) assurance.

The findings of Yuan et al. (2019) similarly support the negative correlation between CEO age and CSR performance, particularly in the presence of higher block-holder ownership. These findings corroborate our second hypothesis, which stipulates that firms led by older CEOs are prone to providing lesser assurance for their CSR reports. Moreover, these results are consistent with the top-down view and other (L. Chen & Tsang, 2017; Cline & Yore, 2016; Lewis et al., 2014), providing support for the study’s subsequent hypotheses.

Robustness Tests

Sensitivity Analysis and Endogeneity Tests

Additionally, Table 4 in the Supplement offers additional insight into the sensitivity analyses and endogeneity tests that were conducted to reinforce the reliability of our primary findings. Initially, we scrutinized the connection between CEO management competence and future sustainability performance (from Models 3 to 6) by concentrating solely on the dependent variables for the forthcoming period (t + 1). This analysis was conducted to detect any potential issues related to spurious causation in our regression models.

Robustness Tests for Reverse Causality and Endogeneity.

Note. Results from the system GMM estimation are shown in panel 2, while results from the random panel data estimation are shown in panel 1. All of the regression variables’ test statistics and standard errors (between brackets) are asymptotically invulnerable to heteroscedasticity. Appendix 1 contains definitions for all variables used in the paper.

p < .01. **p < .05. *p < .1.

Upon thorough examination of our random effect panel data evaluation, our primary conclusions receive further affirmation. The outcomes of our supplementary regression analysis align consistently with those of our initial regression investigation. In Table 4, panel 1 (models 1–4), it is evident that CEOMA exhibits a positive and substantial association with Sustainability, Social Sustainability, and Economic Sustainability in the subsequent year. However, when focusing on environmental sustainability, the CEOMA coefficient bears a negative sign and lacks statistical significance.

In consonance with prior research methodologies, we adopted measures to address concerns regarding endogeneity, simultaneity, and the potential effects of firm-specific heterogeneity within our primary regression analyses (Khan et al., 2017, 2018, 2021). In our pursuit of refining the robustness of our results, we turned to the utilization of the System Generalized Method of Moments (sysGMM) technique. The outcomes of this re-estimation are presented in Panel B of Table 4. Notably, the parallelism between these supplementary findings and our primary results underscores the steadfastness of our observations. This alignment underscores the resilience of our outcomes against any potential biases stemming from spurious correlations engendered by heterogeneity or endogeneity.

In summation, the collective insights derived from our sensitivity analysis, endogeneity assessment, and sample selection examination contribute to the validation of the tenacity of our primary findings, even when scrutinized in light of potential statistical intricacies.

Alternative Definitions of Managerial Ability

The performance of a company is sometimes used as a proxy for the efficacy of its chief executive officer (CEO; e.g., Bertrand & Schoar, 2003; Murphy & Zábojník, 2004). To make our research more robust and offer a fresh viewpoint on CEO skill, we propose using industry-adjusted Return on Assets (IndAdjROA) as an alternative metric for gaging CEO competence. To further ensure the accuracy of our findings, we use this supplementary statistic into the re-estimation of Models (3–6).

IndAdjROA is computationally derived by juxtaposing income before extraordinary items scaled by the average total assets, subsequently subtracting the average industry Return on Assets (ROA) within the same industry and period for each firm-year. The comprehensive outcomes of the panel data estimations are explicated in Table 5. Upon scrutiny, it is evident that the coefficients corresponding to the industry-adjusted ROA exhibit statistical significance and positive directionality, with the exception of the coefficient associated with IndAdjROA pertaining to SusPerf_Env sustainability. Although the latter coefficient manifests a positive sign, it does not attain statistical significance. The coherence between these supplementary findings and our earlier results lends credence to the reliability of our previous deductions, reinforcing the premise that CEO managerial ability exerts a positive influence on sustainability practices across all its dimensions.

Robustness Tests: Alternative Definition of Managerial Ability.

Conclusions and Policy Implementations

This study serves as a pivotal juncture where two pivotal domains converge: the managerial competence of CEOs and the corporate sustainability performance. The investigation assumes paramount importance as it delves into a fundamental attribute of organizational leadership, namely the CEO’s ability, and elucidates its profound ramifications on the sustainability practices exhibited by the organization. Consequently, the study embarks on a comprehensive exploration, scrutinizing the intricate nexus between CEO managerial ability and the multifaceted dimensions of sustainability performance, which encompasses social sustainability, economic sustainability, and environmental sustainability. Moreover, the study explores the moderating role of short horizon of CEO on the relationship between managerial ability and sustainability performance.

By virtue of its depth and scope, this study unveils several novel contributions. Foremost, it emerges as a pioneering inquiry by delving into the interplay between CEO managerial ability and sustainability within the context of a developing economy. Furthermore, it constitutes the inaugural endeavor to dissect sustainability into its distinct pillars and examine the nexus of each with the CEO’s managerial ability. Through the use of a robust panel data approach covering Chinese listed enterprises from 2010 to 2019, this study provides empirical support for the central argument that the CEO’s managerial skill exerts a beneficial influence over the full spectrum of sustainability practises adopted by these organizations. Additionally, when the CEO’s management skills improve, the company’s social and economic sustainability follow similar upward trajectories.

Nevertheless, it is notable that the study does not unearth a significant association between environmental sustainability and managerial ability. The robustness of our results is substantiated through the application of diverse methodologies and definitions, assuring the veracity of our findings. In consonance with the insights of the upper echelon theory, which postulates the profound impact of top leadership traits on organizational decisions, our findings corroborate this perspective. Furthermore, the study brings to light a pertinent observation, namely that the limited tenure of CEOs curtails the extent of sustainability performance. This assertion serves as an additional layer of insight within the context of CEO dynamics and their bearing on sustainability pursuits.

This study’s outcomes have substantial implications in terms of policy and regulatory considerations. One pivotal inference from our findings pertains to the imperative for Chinese listed firms to enhance the capabilities and expertise of their upper management, particularly CEOs, to ensure the efficacious implementation of sustainable policies. In this context, the Thousand Talents Plan emerges as a viable avenue for bolstering this endeavor. Evidently, the Thousand Talents Plan has exerted a notable influence on China’s contemporary trajectory, fostering the active participation of Chinese professionals within organizations and significantly contributing to the origination of strategic policies.

Chinese participation in the 2016 Paris Climate Agreement shows its commitment to environmental and climatic issues, which strengthens such efforts. Our research also shows how important it is for Chinese businesses to have competent CEOs who can build relationships with their employees and keep them committed to developing sustainable practises. These findings not only buttress the ongoing process of standard-setting but also hold relevance for the comprehensive revision of all fundamental facets of sustainability within the ambit of the new Global Reporting Initiative (GRI) framework. By amplifying the nexus between CEOs’ managerial ability and the multifaceted domain of sustainability, this research provides a scholarly underpinning to the ongoing discourse on fostering responsible and enduring corporate practices within the Chinese business landscape.

The implications of our study extend significantly to practical and societal domains, particularly for policymakers vested in advancing Corporate Social Responsibility (CSR) agendas. The findings underscore the necessity for policymakers to factor in managers’ career apprehensions when formulating strategies to incentivize managerial investment in CSR initiatives. A prudent approach involves integrating managers’ proficiencies within the ambit of sustainability considerations, consequently warranting a nuanced appraisal of managerial capabilities. Such an endeavor entails redefining managerial ability as follows: “managerial ability denotes the extent to which a firm effectively deploys its resources to yield social, environmental, and economic outcomes.” This paradigm shift ensures that managers’ competencies are directed not solely toward financial performance but also extend to encompass sustainable performance domains of commensurate significance.

Moreover, our findings have direct relevance to enterprises prioritizing sustainability as a strategic imperative. A recommended stratagem for fostering sustainable performance involves devising incentive frameworks that incentivize CEOs for sustained accomplishments over the long term. Significantly, a cardinal implication lies in the imperative to instill within firms a comprehensive ethos of sustainability practice, encompassing the triad of social, environmental, and economic dimensions. The scholarly discourse illuminated in this study resonates with the broader corporate landscape, advocating for an integrative and holistic approach to sustainability that aligns with the current trajectory of responsible business practices.

In conclusion, although this work has made major contributions and produced useful results, it does have certain limits that should be explored in future studies. The lack of attention to the CEO’s educational background, financial competence, and Communist Party ties, all of which have a noticeable impact on managerial ability in the Chinese setting, is a major shortcoming. A promising trajectory for future inquiry involves incorporating an expanded CEO personality index that encompasses both observable and cognitive traits, thereby enriching the measurement of managerial ability. Secondly, the current study confines its examination to CEOs in top management roles, warranting an extension of the investigation to encompass other directors and members of the senior management team. Such an extension holds the potential to yield more comprehensive insights into the collective traits and capacities of the entire leadership cohort. Furthermore, the study’s emphasis on a massive sample gathered from the Chinese landscape hints at an interesting line of inquiry for the future. a look at how these new markets stack up against the more established ones in the United States. Such cross-regional comparisons have the potential to unveil divergent results owing to variations in sustainability concerns and levels of managerial aptitude across geographical boundaries. Despite the enhanced reliability and accuracy of our core measure of CEO ability in comparison to antecedent studies, there remains the possibility that this measure might inadvertently encapsulate certain uncontrolled features pertaining to firms’ operational, investment, and financing environments. Future inquiries could consequently center on refining the precision of assessments pertaining to managerial prowess, thereby contributing to a more nuanced understanding of this critical facet.

Footnotes

Appendix

Definition of the Variables.

| Variable name | Description |

|---|---|

| Sustainability performance | The corresponding values for this variable manifest as continuous metrics extracted from the HEXUN database, characterized by a scalar spectrum that ranges from 0 denoting the lowest rating score to 100 signifying the highest attainable rating score. |

| CEO managerial ability | A CEO’s proficiency in efficiently converting business resources into revenue. Measured by through the work of P. Demerjian et al. (2020). |

| Retiring CEO | Equals to 1 if CEO’s age is equal to or more than 63 years. |

| Return on asset (ROA) ratio | Total revenue divided by total assets |

| Tobin’s Q | Market value of the equity divided by book value of total assets |

| Debt to assets ratio | Total long term debt divided by total assets |

| Size | Log of total assets |

| Duality | 1 if CEO is also chairman |

| CEO gender | 1 if CEO is a male |

| Board size | Total number of directors in the board |

| Board independence | Ratio of independent directors to total assets |

| Board meetings | Number of board meetings in a year |

| Herfindahl-Hirschman index | The market shares of individual firms within a specific market or industry |

| Firm age | Years since the inception of the firm |

| Z-score | A financial metric used to assess the financial health and likelihood of bankruptcy of a company |

Acknowledgements

We would like to acknowledge Dr. Zahid Hussain and Prof. Chunhui Huo for their invaluable suggestions during the concept and design phases of this research project. We also extend our gratitude to the anonymous reviewers for their insightful comments and suggestions, which greatly improved the quality of the manuscript. Additionally, we thank the editor for their guidance and support throughout the publication process.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

We this study is based on secondary dataset. All the financial data are available on CSMAR, and CSR data extract from Bloomberg Huxin database.