Abstract

This article undertakes an empirical investigation on how firm board characteristics relate with corporate social responsibility disclosure (CSRD) in the banking industry of developing economies with a particular interest in Nigeria. The study focuses on a sample of 11 out of the 13 Nigerian listed national commercial banks which provide similar services and are subject to the same regulations and disclosure requirements by the Central Bank of Nigeria (CBN) from 2007 to 2018. Multiple regression analysis was employed on panel data obtained from the banks’ audited financial statements. The findings show that board with large number of persons, low proportion of persons operating outside the bank operations, and higher percentage of feminine directors on the board support higher level of corporate social responsibility (CSR). The results of large number of persons on board and better proportion of feminine administrators support the resource dependency theory and agency theory which offer the broad theoretical underpinnings for this study. The low percentage of nonexecutive administrators negates stand of bank regulators. This implies that banks with an oversized board size, gender diversity, and less board independence are seemingly favorably disposed to improve on CSR.

Keywords

Introduction

Social responsibility (SR) in the business parlance is the commitment of business to behave ethically toward society. Ethical behavior means the exhibition of honesty and fairness in relating with all the stakeholders in the business. Corporate social responsibility (CSR) is one in which the corporate entity builds into its strategic arrangement of social values that enable it to behave responsibly toward the society. The claim is rife that any business that relates ethically with its stakeholders operates a strategy that benefits the company, as well as society. Again, if CSR is seen as a solution to agency problem, good governance should appreciate it and be used to appreciate the value of the firm in the marketplace, but if it is seen as an agency problem, good governance should diminish the value of CSR. Corporate social responsibility disclosure (CSRD) is the dissemination of information on what the firm has done or doing for the sake of the welfare and interest of the society. It can be in the area of philanthropy, environment conservation, and diversity in labor practices, human rights, and selfless services. Good handling of CSR can improve the sustainability of a business through the attraction of increasing sales via positive media presentation, appeal of buyers, low labor turnover and retention of employees with good talent, good community relations, easy access to capital, reduced operational costs, and big ticket transactions with improved financial performance and business growth. On the contrary, corporate governance (CG) is the system of rules, practices, and processes by which companies are governed or by which the rights and responsibilities in a firm are distributed among the stakeholders. The aim of CG is to manage the balance in the use of resources in business between economic goals and social goals of individuals and society. The indices of good CG include operation of rule of law, independence, accountability, fairness (moral integrity), responsiveness, transparency, participatory and consensus-oriented, and effective and efficient use of resources. One of the channels of delivering CG is the board of directors (BOD) who represent the shareholders.

Principle 2.3 of the Nigerian code of CG for banks demands that certain factors should be considered in constituting the BOD of public companies. The theory stresses expertise, abilities, experience, executive management, nonexecutive management, and independent professional nonexecutive managers. This requires that the board’s makeup will be well balanced and that certain number of board members should be persons not in the employment of the company (called nonexecutive directors [NEDs]). Also, the number of persons who constitute the board (known as board size) should be large enough to reflect the resources required to run the company smoothly. However, no issue of gender was mentioned in the code. The expectation has been that if the board is well structured with balanced membership, the issue of accommodating the interest of all the stakeholders especially the society in the corporate objectives of the business will be taken care of. Such board structure will also encourage the managers to pilot the affairs of the business in making profit and responsibly interacting ethically with all the stakeholders even to the extent of establishing corporate attitudes that will advance social causes. As public companies especially banks are expected to observe the principles of the code with respect to board composition or structure, there are some studies that investigated how such structure influences the level of CSR undertaken by companies but they are mostly conducted on data from developed and developing economies. Orazalin (2019) and Habbash (2016) investigate the effects of board characteristics on CSRDs in the context of the banking sector of Kazakhstan, an emerging economy of Central Asian region, and Saudi Arabia, an Arab country, respectively. Within the context of a developing country, Coffie et al. (2018) study effect of board size on CSRD. Nguyen et al. (2015) investigate the relationship between board gender diversity and firm financial performance in the context of a transitional economy Vietnam characterized by an underdeveloped CG system and confirm an impactful positive relationship between the two. Chen and Keefe (2018), Ali et al. (2017), Lu et al. (2015), Mamun and Ahmed (2017), Peraita (2017), Ben-Amar and Mcilkenny (2015), and Wang and Oliver (2009) researched on developed economies. Other studies conducted mostly on developed economies are shown in the “Literature Review” section. Very few studies have analyzed the effect of board structure on the CSRD in African countries with different regulations and socioeconomic settings compared with other continents. Locally, the empirical evidence on the association between CG mechanisms with respect to board structure and CSRD in the context of Nigerian banking system is limited. This empirical study aims to provide much-needed evidence in this area from Nigeria—one of the largest populous oil-rich emerging economies in Africa with specific interest on the banking system. To the best of the researchers’ knowledge, this study is the most recent and unique in that it attempts to contribute to the understanding of banking-sector-level determinants of CSR and fill the gap in the literature. The findings of the study could be of interest to policy makers and stakeholders in determining the relevance of board composition in the boardroom.

For clarity purpose, this article is divided into five major sections. The “Introduction” section handles the background information of the study. In the “Literature Review” section, we have the review of previous studies in the area of study. This is followed by the description of materials and methods for the study in the “Materials and Methods” section. The “Results and Discussion” section contains the results and discussion, while the article is concluded in the “Conclusion” section.

Literature Review

Garcia et al. (2020) investigated and analyzed the determinants of voluntary disclosure of corporate social performance (CSP) through a literature review of articles in EBSCO, ISI, and JSTOR databases published from 1987 to 2015, to discover the theoretical perspectives and the variables used in measuring the determinants of CSP disclosure (the independent variables). They confirmed that there was no single explanation for what determined CSP disclosure, and the theories that support a relationship between CSP disclosure and its determinants are legitimacy, institutional, stakeholder, agency, and voluntary disclosure. According to Wonsuk and Abebe (2016), the resource dependence and stakeholder theories suggest that the extent to which firms build relationship with certain stakeholders is closely tied to the personal and social background of board members. This in turn influences the allocation of resources to corporate philanthropy. Therefore, organizations with good board structure are considered to be stronger corporate leaders, more financially and environmentally conscious relative to companies with weak board composition. This indicates that a close correlation may occur between board characteristics and company CSR. Banks in Nigeria bear their social duty in fields such as eradicating severe hunger and malnutrition, fostering education, supporting gender equity, empowering women, reducing infant mortality, improving maternal safety, ensuring environmental sustainability, jobs, and upgrading vocational skills, social entrepreneurship ventures, contribution to federal, state, or local government relief funds for socioeconomic development among others but mostly makes their contributions in terms of donations and charitable gifts to the societies of their interest. According to the banks leadership structure, before such donations and charitable gifts are carried out, the policy-making cadre of the bank management which is the BOD must consider its worthiness. Therefore, this study becomes imperative to find out the influence of board characteristics on the CSRD in the annual financial statements of the banks.

Theoretical Framework

Theoretically, no single theory can predict the association of board structure and CSR, but agency theory (Habbash, 2016; Nguyen et al., 2015), stakeholder theory and resource dependency theory (Nguyen et al., 2015), and legitimacy theory (Khan et al., 2013) have been used to provide insight implying the possibility that board structure may affect CSR. Thus, investigating board structure–CSR nexus is an empirical issue. From the perspectives of Fama and Jensen (1983) and Jensen and Meckling (1976), agency theory preaches that the BOD reduces principal–agent conflicts through its monitoring actions which will consequently affect firm performance. Adams and Ferreira (2009) show that in gender-diverse boards, female directors have better attendance records to meetings with better monitoring capacity in a sample of U.S. firms. This means that gender diversity in the boardroom can also secure improved monitoring and projects a responsible board which may ultimately appreciate the value of CSR. This is because the potential influence of board gender diversity on CSR is based on the level of firm financial performance and the firm can improve financial performance by including more female directors to provide stricter monitoring and directing actions on the management (Gul et al., 2011). On the contrary, Adams and Ferreira (2009) argue that board gender diversity can work against the firm performance of well-governed firms because of unnecessary, excessive monitoring.

The heavy push toward protection of only the interest of shareholders without having on board the interest of other interest groups has been fingered as one of the major causes of incessant corporate collapses in the world. Stakeholder theory emphasizes that the welfare of all legitimate parties that ensure the needed resources for meeting the ultimate objectives of a business are constantly flowing to the desired direction should also be taken care of, of which society is among. CG institutes the ways an entity is run to hold the balance between the organization goals and the goals of all the interest groups, including the society at large. According to Freeman et al. (2004), if any business wants to have effective performance, it should pay attention to all relationships that can affect or be affected by the achievement of the firm’s purpose. Society at large is a major stakeholder in every business. One of the means through which the corporate entities can take care of the interest of the society is by maximizing the wealth of the society via CSR. Thus, it is assumed that the size of BOD should be made up of persons who support this idea of CSR to legitimize the performance of the business with consequent impact on CSR.

Resource dependency theory opines that the BOD provides resources to the firm from various dimensions or diversity in terms of gender, experience, qualification, expertise, capital, executive directors (EDs) and NEDs, and so on. This serves as a mechanism to form links with the external environment that can help the management in the achievement of organizational goals (Wang & Oliver, 2009). On this note, it has been argued that firms with high composition of more diverse boards in terms of EDs/NEDs and male/female directors, assembled due to their wider expertise and knowledge, in appropriate board size can network better with the external environment and improve reputation through CSR (Haniffa & Cooke, 2002; Haniffa & Hudaib, 2006; Hillman & Dalziel, 2003; Liu et al., 2014; Nicholson & Kiel, 2007; Pfeffer & Salancik, 2003). Hillman et al. (2002), as cited by Nguyen et al. (2015), argued that diversifying the BOD by adding more women would help companies to gain legitimacy as gender equality becomes increasingly one of the widely accepted social norms.

Based on the extant literature, this study is anchored on the agency theory and resource dependency theory. It is assumed that formation of boards that tows the lines of these theories will provide BOD with appropriate board size, sufficient independence, and gender diversity essential for firm performance and consequently CSR. Although the two theories suggest association of board structure and CSR, the nature of the association remains unclear. This makes the study imperative to answer the following empirical questions. What level of association exists between board size and CSR? To what extent does board independence influence CSR? How does board gender diversity affect CSR?

Empirical Review and Hypotheses Development

Prior empirical studies on this topic, mostly conducted on data from developed and developing economies, provide equivocal results.

Board size and CSR

From the resource dependency theoretical perspective, the quest to have a number of certain personalities who have the wherewithal to move a business positively forward may attract large number of people to become members of BOD of the business. This is confirmed by the empirical studies of Al-Qahtani and Elgharbawy (2020), Mohd-Said et al. (2018), and Shamsul et al. (2011), which record that board size is determined by a variety of factors that include industry type, firm size, and the complexity of the firm’s business. Huse (1990) studied BODs in small enterprises in Norway and found that board composition depends on company size and ownership structure, and varies with industry. However, a broad board structure dominated by numerous administrators who have little resources and inability to track the activities of management and offer valuable guidance on important business choices provides incentives for executive management to tow the line of selfish aggrandizement to the detriment of other stakeholders (Ahn et al., 2010). According to Jizi et al. (2013, p. 604), considering group dynamics, smaller boards are often expected to be more effective at monitoring and controlling management than larger boards. Due to their limited size, they are expected to benefit from more efficient communication and coordination, as well as higher levels of commitment and accountability of individual board members.

Also, they emphasized that the demerits of small boards include over-burdening of each member with excess workload, which might limit the monitoring ability of the board, and working with a less diversified range of expertise, which can affect the quality of the advice and monitoring such board can offer. At times, chief executive officers (CEOs) deliberately build these larger boards to distribute influence and dilute the weight of powers of some board members on the executives. Yoshikawa and Phan (2003) suggest that small board of seven or eight persons should be more organized and more efficient, where teamwork, collaboration, and decision making are smoother, and devoid of CEO domination and control. Some empirical studies suggest that board size, as one of the internal CG mechanisms used to protect and promote shareholders’ and other stakeholders’ interests, is positively related to CSRD (Al Fadli, 2020; Htay et al., 2012; Jizi et al., 2013; Kiliç et al., 2015; Majumder et al., 2017; Ozordi et al., 2018; Said et al., 2009; Zeeshan et al., 2018). Within the context of 33 listed firms of a developing country from 2008 to 2013, Coffie et al. (2018) found that board size has a positive relationship with CSRD. Thus, larger boards promote the level of CSRD. On the contrary, larger boards were found to react negatively to CSR (Zou et al., 2014). Lakhal (2005) reveals that board size is irrelevant. Orazalin (2019) reveals that board size has no impact on the level of CSRDs. In this study, based on the resource dependency theoretical concept, we expect banks as financial institutions under strict regulations from varied regulators, to distribute board functions to persons with diversified range of expertise in a manner that will bring out effective monitoring and guidance of the management toward maximizing the welfare of the stakeholders especially the society. Thus, we predict the following hypothesis:

Board independence and CSR

For successful supervision of management of public companies, the structure of boards is quite relevant. To infuse effective monitoring and guidance of the management toward maximizing the welfare of the shareholders and other stakeholders, the agency theory and stakeholder theory, respectively, propose a higher proportion of independent directors on the board to track any self-interested behavior by management, reduce service expenses, and incorporate fresh knowledge innovations from different aspects, transparency, and objectivity in managing public firms. The EDs who hold advanced talents, experience, and useful awareness of the business practices and everyday operations of the companies (Cho & Kim, 2003) help to run the company. The power of the board resides in its freedom, and as such its success in fostering CSR rests with the board independence. Independent board seems to be more objective in their analysis of the company’s management and behavior (Huse, 1990). They are also seen by some researchers (Adawi & Rwegasira, 2011; Ibrahim & Angelidis, 1995; Michelon & Parbonetti, 2012) to be more willing to take on social responsibilities and honor obligations that will meet stakeholder interests. Lim et al. (2007) posit that having more of nonexecutive independent directors over EDs enhances good corporate citizenship and reduces information asymmetry between shareholders and managers. Also, Rouf (2011) reported that more of autonomous directors enhance mutual transparency. Htay et al. (2012) and Jouiroua and Chenguel (2014) reported that the level of CSR reacts directly with percentage of outside directors over inside directors in Malaysian banks and in Tunis companies. Jizi et al. (2013) state that banks with independent boards are expected to display a greater focus on long-term sustainability and engagement in CSR and CSR reporting because their welfare is not tied to the apron string of the CEO’s goodwill. They posit that independent directors are more favorably disposed toward investment in CSR activities to enhance the perception of the social status of the firm in the eyes of the society. Some empirical studies indicate that board independence as an internal CG mechanism used to protect shareholder interests is positively related to CSRD (Abdul & Mustafa, 2016; Al Fadli et al., 2020; Bravo et al., 2015; Jizi et al., 2013; Muttakin & Subramaniam, 2015; Said et al., 2009). Khan et al. (2013) examined how board independence influences organizational CSRDs in the annual reports of Bangladeshi companies and found that board independence has positive significant impacts on CSRDs. Thus, more independent BODs promote both shareholders’ and other stakeholders’ interests. This suggests that independent directors are likely to support the disclosure of CSR activities to reduce information asymmetry between insiders and outsiders. However, Shamsul et al. (2011) and Majumder et al. (2017) record that board independence has insignificant positive association with CSRD, while Mohd-Said et al. (2018) register no association between the two constructs. Orazalin (2019) reveals that board independence has no impact on the level of CSRDs. Habbash (2016) examined the influence of board independence on CSRD practices in an emerging Arab country, Saudi Arabia, for the period 2007–2011, and found it a negative determinant of CSR. Coffie et al. (2018) reveal that increasing the number of NEDs may not necessarily improve the level of CSRD. Based on the current literature, we predict the following hypothesis:

Board gender diversity and CSR

In this era of calls for gender equality, many countries (e.g., Denmark, Finland, France, Iceland, Norway, Spain, and Sweden) have enacted laws on compulsory quotas for female representation on boards of public firms to promote women’s involvement in key human endeavors (Agyemang et al., 2017; Ford & Pande, 2011; Velte, 2019). As a result, women are now actively involved in business and other key economic fields. Richardson (2013) and Agyemang et al. (2017) stated that, in the United States, women constitute 16.9% of board members at Fortune 500 in 2013, less than one fifth of the firms had at least 25% women directors, and 10% of the firms had no women in their BOD. Davies (2011) reveals that women in boardrooms worldwide constitute 3.6% in the urban Asia-Pacific, 23% in Sweden and the Philippines, and 9.6% in the United Kingdom. The issue of association of women in the board and the influence on CSR became a topic of debate (Babcock, 2012; Grosser & Moon, 2005; Kate, 2009; Setó-Pamis, 2015; Soares et al., 2011; Testa, 2012). Some scholars claim that the inclusion of women members in the board has raised the degree of welfare (Firer & Mitchell Williams, 2003), raised the board’s commitment to the problem of CSR as women have high social awareness (Chapple & Moon, 2005), strengthened the credibility of the organization by CSR and charitable corporate donations (Charbel et al., 2017), and encouraged further participation among board members (Ozordi et al., 2018) and ethical behavior (Burgess & Tharenou, 2002). Some other empirical studies give credence to the gender-based argument that having more female on the board enhances CSRD (Abdul & Mustafa, 2016; Abdulsamad et al., 2017; Al-Qahtani & Elgharbawy, 2020; Atif et al., 2020; Ayman & Hong-Xing, 2019; Bravo et al., 2015; Kiliç et al., 2015; Lu et al., 2015; Mohd-Said et al., 2018; Ozordi et al., 2018; Wonsuk & Abebe, 2016; Zeeshan et al., 2018). These suggest that the representation of women on the board improves board flexibility, offers distinctive consistency of behavior from a particular point of view, enables constructive dialogue in the boardroom, and mitigates expropriation possibilities. From the perspective of agency theory, the presence of female directors in the boardroom can improve monitoring capacity of the board and attention to CSR, but excessive monitoring on the management can cause problems in already well-governed firms. Bear et al. (2010) found positive influence of female representation on the board on CSR. The findings of Abdulsamad et al. (2017) indicate that boards with gender diversity are better regulators, but mandating gender quotas in the boardroom could hurt well-governed companies with inefficient additional surveillance. However, Majumder et al. (2017) found insignificant positive association of board gender diversity with CSR. Orazalin (2019) reveals that board gender diversity has a positive influence on CSR reporting. The issue here is: Can the board of businesses with female representation influence the degree of investment in CSR? Based on the mixed evidence discussed above, we predict the following hypothesis:

Materials and Methods

Materials

The study seeks to investigate the impact of board characteristics on CSR reported in annual reports of Nigerian listed national commercial banks. It focuses on listed commercial banks from 2007 to 2018, which provide similar services and are subject to the same regulations and disclosure requirements by the Central Bank of Nigeria (CBN). We excluded regional banks, banks other than commercial banks, banks without up to date release of annual reports as at the commencement of the study from our considerations. This leaves us with a population of 13 banks from which a sample of 11 banks was selected. The sample, which constitutes 85% of the population, is made up of banks that reported on CSR consistently from 2007 to 2018 in their annual reports. The analysis does not include banks for which there is incomplete data. Sampling technique was purely judgmental based on disclosure of CSR data in the annual reports. This left us with 132 observations from 2007 to 2018. Given that the bank consolidation that started in July 2004 in Nigeria ended on December 31, 2005, a year gap was given to allow the banks to consolidate on the effects of such exercise—the reason behind the study’s sample period 2007–2018. The 2018 is the last year with complete data on the sample banks. The CSR data were collected from the banks’ 2007–2018 annual reports. The proxy for CSR is the amount of expenditure on donations and charitable gifts to the society in general by the banks. In line with previous researches, reported quantitative figures on CSR in the banks’ CBN-approved fully audited annual reports were used, as such annual reports command wide readership among shareholders, stakeholders, financial analysts, and credit rating agencies, and the CSR information provided in the annual reports has great reliability.

The data on board characteristics (structure) were also collected from the banks’ annual reports approved by CBN. The board characteristics are the independent variables which are the factors hypothesized to have influence on CSR. They are board size, board independence, and board gender diversity. In line with the extant literature, board size refers to the number of directors on the corporate board (Abdulsamad et al., 2017; Kiliç et al., 2015; Mohd-Said et al., 2018). Board independence was determined as the percentage of the number of NEDs on the BOD relative to the total number of directors on the board (Mohd-Said et al., 2018; Shamsul et al., 2011). Board gender diversity refers to the number of female directors on the BOD (Ayman & Hong-Xing, 2019; Kiliç et al., 2015; Mohd-Said et al., 2018). In this study, gender diversity is determined as a percentage of the number of female directors on the BOD relative to the board size.

Control Variables

To avoid model under specification, we control for additional variables, which might also affect the level of CSR. In line with Schiehll et al. (2011), the control variables included in the model are leverage, profit after tax, and total revenue of the banks. The presumption in this study is that debt in a company’s financial structure affects negatively on the level of CSR the company can engage. Jizi et al. (2013, p. 607) state that firm leverage should be controlled for because the need of managers of highly leveraged firms to generate and retain cash to service the debt might reduce their ability to fund CSR. Again, while some empirical research found no indication of a relationship between leverage and CSR disclosure but Barnea and Rubin (2010) indicate a negative relationship between leverage and CSR disclosure.

Leverage of the bank is determined by dividing the sum of current and long-term liabilities by the total assets. Profit after tax is an accounting measure which shows how effectively and efficiently management used equity to enhance profit available to the residual owners. It is important to control banks’ financial performance because if the banks are financially doing well, they will have more resources which they can be used to engage more investment in CSR. Total revenue (REV) is measured by gross earnings of each bank and taking the natural log of it before it was used in the regression model. Firm size is likely to influence the amount of CSR, because large firms are more exposed to the influence of many powerful stakeholder groups and so tend to spend more on CSR to take care of the interest groups (Barnea & Rubin, 2010; Branco & Rodrigues, 2006; Jizi et al., 2013). Thus, larger banks as measured by gross earnings are likely to invest more on CSR to improve the confidence of stakeholders. One way of increasing their goodwill is to make the public know about their activities through CSR.

Model Specification

To test the hypotheses, the economic model used by Khan et al. (2013) and Majumder et al. (2017) is adopted (Equation 1):

where CSR represents corporate social responsibility amount, β0, the fixed intercept element; BDI, board independence; BDS, board size; BGD, board gender diversity; LEV, leverage; PAT, profit after tax; and e, error term.

Regression method was applied on panel data to establish the influence of board independence, board size, and board gender diversity on CSR of the banks. The Hausman test favors the use of fixed effects.

Results and Discussion

Descriptive Statistics

Table 1 reveals that the amount of CSR of the listed banks for the 12-year period ranged from N774,000 to N3,065,000,000 and with average values of N324,754,800 and the standard deviation of N483,742,500. The board independence averaged at 63.84% with a standard deviation of 11.19% as the minimum and the maximum are 46.15% and 91.67%, respectively. That is, the average of 63.84% of board members of listed banks were outside directors with minimum of 46.15% and the maximum of 91.67%. The average board size is 14.05 (14 members) with a standard deviation of 2.8 and ranging between seven and 20 members. Female presence on board shows a mean of 15.11% with a likely deviation of 11.49% and ranging between 0% and 40%. The mean number of outside directors is 9 while the inside directors is 5, which constitute 64.29% outside directors and 35.71% inside directors. This conforms to the suggestion that outside directors should be greater to ensure board independence.

Descriptive Statistics.

Source. Authors’ computations using E-View Version 9.0.

FD = female directors.

Correlation Matrix

Table 2 reveals that the explanatory variables board independence, board gender diversity, and leverage exhibit negative association with CSR. The negative correlations imply that the level of CSR reduces as they increase, and vice versa. The positive correlations between board size (BDS), profit after tax (PAT), and revenue (REV) simply mean that CSR increases as they increase, and vice versa. The number of EDs shows a positive correlation with CSR. That is, as the number of EDs increases, CSR increases. This may indicate sign of expropriation of the shareholders by the management in Nigerian listed banks. In line with Atif et al. (2020), it is argued, this is being moderated by the female representation on the board and independent NEDs as both have negative correlation with the CSR.

Correlation Matrix.

Source. Authors’ computations using E-View Version 9.0.

FD = female directors.

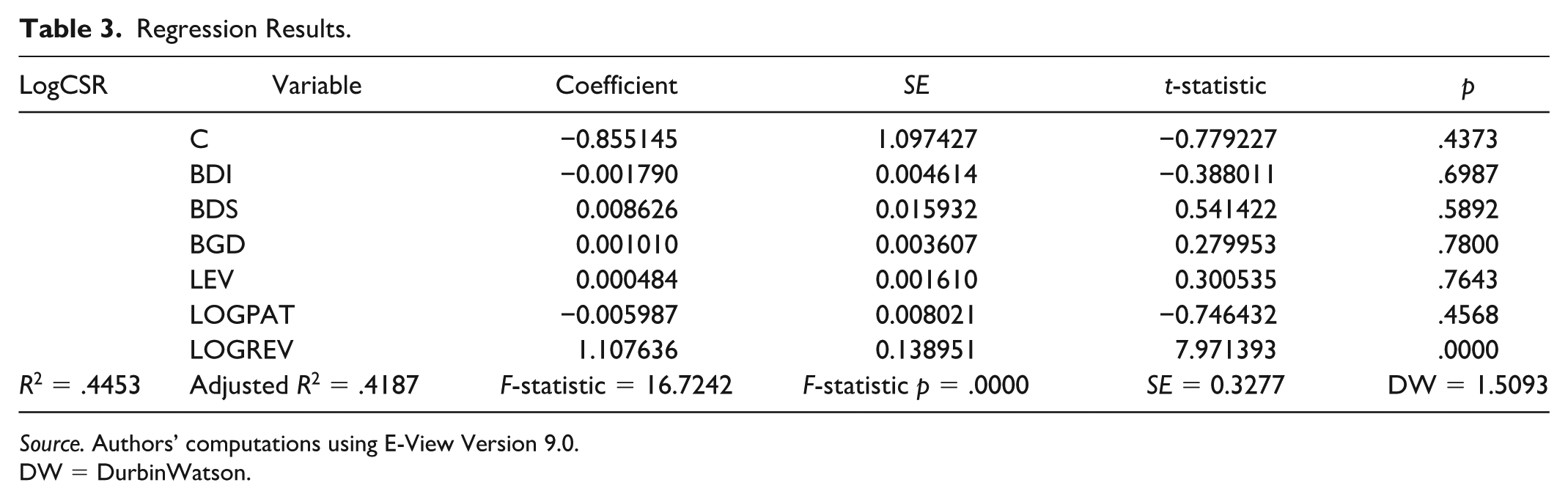

Regression Results

The regression results generate this resultant equation: LogCSR = −0.855145 − 0.001790 BDI + 0.008626 BDS + 0.001010 BGD +0.000484 LEV − 0.005987 LogPAT + 1.107636 LogREV.

While board size (BDS) and board gender diversity (BGD) displayed direct influence on CSR, board independence (BDI) showed negative influence. This implies that banks with less board independence, a big-size board, as well as gender diversity invest more on CSR. The variables considered in the model account for 44.53% of change in the CSR (coefficient of determination, R2 = .4453).

Test of Hypotheses

From Table 3, it is observed that board size has positive (0.008626) and insignificant (p = .5892) association with CSR, thereby rejecting the null hypothesis, and established that board size positively relates to CSRD in the Nigerian banking sector from 2007 to 2018. These results answer the empirical question: What level of association exists between board size and CSR?

Regression Results.

Source. Authors’ computations using E-View Version 9.0.

DW = DurbinWatson.

From Table 3, it is observed that board independence has negative (–0.001790) and insignificant (p = .6987) association with CSR, thereby confirming the null hypothesis, and established that board independence negatively relates to CSRD in the Nigerian banking sector from 2007 to 2018. These results answer the empirical question: To what extent does board independence influence CSR?

From Table 3, it is observed that board gender diversity has positive (0.001010) and insignificant (p = .7800) association with CSR, thereby rejecting the null hypothesis, and established that board gender diversity positively relates to CSRD in the Nigerian banking sector from 2007 to 2018. These results answer the empirical question: How does board gender diversity affect CSR?

The insignificant positive influence of board size (BDS) on CSR concurred with the empirical findings of some previous studies (Al Fadli, 2020; Htay et al., 2012; Jizi et al., 2013; Kiliç et al., 2015; Majumder et al., 2017; Ozordi et al., 2018; Said et al., 2009; Zeeshan et al., 2018), though contrary to the findings of Zou et al. (2014) who prefer smaller board size. Thus, larger boards weakly promote the level of CSRD in the Nigerian banking sector. This finding suggests the rejection of the first hypothesis and establishes the fact that the banks require large board size to influence the decision on the amount of CSR. The finding affirms that there is a weak positive relationship between board size and level of CSR. Theoretically, the study supports the view of the resource dependency theoretical perspective which states that the quest to have a number of certain resources/personalities who have the wherewithal to move a business positively forward may attract large number of people to become members of BOD of the business.

The insignificant negative effect of board independence (BDI) on CSR aligns with the empirical findings of the studies by Shamsul et al. (2011) and Majumder et al. (2017) in terms of the strength of the relationship as they recorded insignificant but positive association, and disaligns in both magnitude and strength with the findings of Said et al. (2009), Jizi et al. (2013), Bravo et al. (2015), Muttakin and Subramaniam (2015), Abdul and Mustafa (2016), and Al Fadli et al. (2020), which recorded various degrees of significant positive association between board independence and CSR. This suggests that more independent BODs are likely to decrease the level of CSR in the Nigerian banking sector. The negative relationship of CSR and BDI implies that as BDI increases, the level of CSR decreases, and vice versa. Theoretically, the study supports the agency theory perspective, which posits that if CSR is seen as a solution to agency problem, good governance should appreciate it and be used to appreciate the value of the firm in the marketplace, but if it is seen as an agency problem, good governance should diminish the value of CSR.

The finding of insignificant positive relationship between board gender diversity (BGD) and the amount spent on CSR concurs with the findings of Orazalin (2019), Abdulsamad et al. (2017), Majumder et al. (2017), and Bear et al. (2010) who found insignificant positive association between board gender diversity and CSR. This suggests that the banks require substantial female representation on the board to drive positively CSR activities. The finding implies that increasing the number of women on the board increases the degree of CSR. From the perspective of agency theory, the presence of female directors in the boardroom can improve monitoring capacity of the board and attention to CSR.

Surprisingly, high leverage (LEV) attracts high CSR, but this may be based majorly on the amount of deposits being mobilized by the banks. Thus, the higher the customers’ deposits, the higher will be the amount dispensed on CSR. In a banking business environment where banks do public relations (PR) to officers manning the finance positions in big organizations to collect huge deposits from them, such PR may be part of the CSR. The PAT has insignificant negative association with CSR. It is most likely that the banks do increase and used CSR to lure more deposits into their coffers during the period of tight monetary control or scarcity of funds in the economy coupled with low profit available to the owners of the banks. Hence, low PAT gingers the banks to engage more of CSR to get to the minds of people for profitable transactions. Firm size as measured by gross earnings of the banks has significant positive relationship with CSR, implying that bigger banks are likely to invest more on CSR.

Conclusion

This study provides evidence that the two of the internal CG mechanisms, namely, the size of board (BDS) and the gender diversity (BGD), which are presumed to promote both the shareholders’ and other stakeholders’ interests positively support more investment on CSR while the independence of the board aligns with the agency theory which kicks against CSR based on the assumption that managers should not be trusted to do a good job on CSR without implanting their selfish interests into the process which will negatively affect the bottom line of the banks. Therefore, size, gender diversity, and independence of board have influence in determining the level of CSR disclosed by the listed banks. It is therefore concluded that banks with large board size constituted with persons from different expertise with capacity to mobilize resources from various dimensions will optimize resource allocation and utilization toward CSR; hence, such large board size should be encouraging in the banking industry. This is food for thought for bank policy makers. As female participation in the top echelon of decision-making process in banks makes banks more socially responsible, there is need to adopt policies that will support giving quota for female representation on the board. Extant literature established that board independence releases effective monitoring and control of managerial actions toward protection of the rights and interests of the stakeholders which include CSR, but it is clear that a different theory is created from the findings of this study. Existence of more independent directors generates more independence for the board, but in this study the results show that the more the board’s independence, the less the investment in CSR. This indicates a sign of expropriation of the shareholders as more the proportion of inside directors, the more is the amount of CSR, which may confirm the fear expressed in agency theory by the principal for not supporting CSR and calling it a waste pipe. For the 12-year period, the banks spent 16.06% of their total revenue (gross earnings) and 1.99% of their profit after tax on CSR (Appendix B).

Based on these findings, the study recommends a reasonable board size that ensures assemblage of adequate resource persons to mobilize the resources of the bank and enhance the level of CSRs. A quota for female representation on the BOD is advocated in every bank board to ensure diversity in decision-making process and socially responsible banks. As board independence has negative relationship with CSR, it suggests that the presence of independent directors on the board discourages the banks to invest more on CSR as one of the legitimation strategies to manage the expectations of stakeholder groups. This study provides motivation for regulators and companies to continue to improve board gender diversity. The study supports evidence from prior studies, conducted in the developed countries, that legitimacy theory is also applicable in the banks of Nigeria, which is a developing country. Attempts should be made in further studies to find out why the impact of board independence on CSR differs from generally acclaimed effect. This study contributes to the existing literature on governance and CSR reporting, specifically in the Sub-Saharan Africa, as well as the potential of future studies in developing countries using a legitimacy theory as the basis for their investigations and motivation. The main limitation of the study is investigating only few variables of board structure and leaving out other variables such as cultural diversity and age diversity. Future studies could include more variables which may yield results that are more significant. Again, the use of donations and gifts to charity by the banks as a proxy for CSR may be challenged, but that remains the only objective measure of CSR for now, as CSR is a new concept in Nigeria business landscape but gradually metamorphosing. This study focused only on the banking sector in Nigeria. It is suggested that future studies should consider the implications of board structure on CSR and on other sectors such as manufacturing. This would help to understand the behavior in other sectors to promote aggregate benefit in the economy.

Footnotes

Appendix

Percentage of CSR Amount to Total Revenue, Total Assets, and Net Profit.

| Indices | CSR: Total revenue | CSR: Total assets | CSR: Profit after tax |

|---|---|---|---|

| Mean | 0.160556 | 1.606736 | 0.019931 |

| Median | 0.140000 | 0.895000 | 0.020000 |

| Maximum | 0.800000 | 31.37000 | 0.120000 |

| Minimum | 0.000000 | 5.760000 | 0.000000 |

| SD | 0.133646 | 3.559648 | 0.017916 |

| Observations | 144 | 144 | 144 |

Source. Authors’ Computation (2020) using data collected from the annual financial statements of the subject-banks from 2007–2019.

Note. CSR = corporate social responsibility; CSR: Total revenue = amount of CSR relative to gross earnings of the banks obtained by dividing amount of CSR by gross earnings; CSR: Total assets = amount of CSR relative to total assets; CSR: Profit after tax = amount of CSR relative to profit after tax.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.