Abstract

This study aims to increase the knowledge on relations between corporate social responsibility (CSR), employee commitment, and firm performance in Serbia. The theoretical part of the article analyzes the relations between CSR and firm performances, as well as CSR and employee commitment, based on available world-wide research results. The empirical part of the article presents the research results for large companies in Serbia, regarding the relations between CSR and firm performance, CSR and employee commitment, and the mediating role of employee commitment on the relationship between CSR and firm performances. The sample consists of 53 large companies, each with more than 250 employees. The database was compiled between October 2019 and March 2020 using self-developed questionnaires. PLS-SEM analysis was implemented to uncover the relationship that exists between the variables. The authors determined that there was no direct effect of CSR on firm performances, but positive, statistically significant effects on employee commitment. Although the direct effect is missing, employee commitment has a positive mediation effect on CSR-firm performance link. The concluding part of the article outlines the theoretical and practical implications, acknowledges research limitations, and offers future research directions.

Introduction

Corporate social responsibility (CSR) is a business concept that emerged in the first part of the 20th century and has been actively developing ever since. According to Moura-Leite and Padgett (2011), CSR was established in the 1950s, when the primary focus of CSR was on the responsibilities of businesses toward society, while today CSR is considered an important strategic factor (p. 528). CSR is balancing between three related areas of business, that is, economy, society, and environment (Aleksić et al., 2020; Berber et al., 2019). CSR includes the elements of a circular economy (Vukadinović & Ješić, 2019), which is seen as a sustainable concept for development of the economy. According to I. Ali et al. (2010), organizations use CSR to “strengthen their relationships with different stakeholders including customers, investors, government, suppliers, and employees. These strengthened relationships ensure corporations the minimum conflicts with stakeholders and the maximum loyalty from all stakeholders” (R. Ali et al., 2010, p. 2796). The stakeholder approach of CSR is used as a starting point in defining the research aim of this article.

This is a concept that needs to create value in terms of environmental preservation, social development and well-being, and economic results, so there are numerous research works dealing with CSR and its relations to firm performances (Balabanis et al., 1998; Farooq et al., 2019; Mackey et al., 2007; McWilliams & Siegel, 2000; Mishra & Suar, 2010; Saeidi et al., 2015; Saha et al., 2020; Q. Zhu, Yin et al., 2014). In the majority of earlier research, the authors found mediating roles of different factors related to the internal and external business environment rather than direct positive relations between CSR and firm financial performance. Among the various factors identified as mediating the CSR-performance link are competitiveness, firm reputation, satisfaction of customers (Saeidi et al., 2015), organizational trust (Wang et al., 2014), leadership and management (Malik et al., 2020; Wu et al., 2015; Y. Zhu, Sun, et al., 2014), innovation (Anser et al., 2018), and so on. Most of the reference research works concluded that these factors had a positive mediation effect on the CSR—performance link, in terms of strengthening the relationship. This is vital, given that companies will “fail to convince stakeholders that they are serious about CSR unless they can demonstrate that their policies consistently achieve the desired social, environmental, and ethical outcomes” (Collier & Esteban, 2007, p. 19).

Employee behavior was one of the factors often identified as having a mediating role on the CSR—performance link (Gao & He, 2017; Lee et al., 2013; Turker, 2009a). Collier and Esteban (2007, pp. 19–20) stated that because it was the employees of a firm who carried the main burden of responsibility for implementing CSR on a daily level, the achievement of organizational CSR outcomes largely depended on employee willingness to collaborate. On the one hand, it is assumed that CSR will increase the employees’ positive work behavior, such as employee commitment (I. Ali et al., 2010; Collier & Esteban, 2007; De Silva & Lokuwaduge, 2019; Turker, 2009a), organizational citizenship behavior (Farid et al., 2019; Gao & He, 2017; Oo et al., 2018), loyalty (Kim et al., 2018; Q. Zhu, Yin, et al., 2014), and engagement (Duthler & Dhanesh, 2018; Rupp et al., 2018; Singh, 2019). Some organizations promoted CSR as a “way to attract a large number of qualified employees, and a previous research work suggested that firms with better CSR were more attractive for new employees” (Wong & Gao, 2014, p. 501), where CSR was seen as an important predictor of employer brand (Ognjanović, 2020). On the other hand, it is expected that motivated, committed, and engaged employees will contribute to the increase of the business results of an organization. Therefore, it is important to explore the relations between CSR and employee commitment, between CSR and firm performances, and mutual relations between all three constructs.

Based on the statements above, the authors defined the main goal of the research. The article investigates the relationship between CSR and firm performance of organizations, and examines what the role of employee commitment in this relation is. The study is motivated by the fact that although there is considerable research on CSR-firm performance link, the influence of employees, and their commitment on this relation has so far been disregarded (De Silva & Lokuwaduge, 2019). The methodology of this research is obtained desk research of the available literature accompanied by field research and data analysis in Smart PLS software. The PLS-SEM analysis has been used to explore the proposed relations. The research was conducted on the territory of the Autonomous Province of Vojvodina, Republic of Serbia, in the period from October 2019 to March 2020, in business organizations with more than 250 employees. It must be emphasized that this research is the first of its kind conducted within the Republic of Serbia.

The article has three main parts. The first part presents the main theoretical foundations on CSR, employee commitment, and the relations between CSR, employee commitment, and firm performances. In the second part, the authors introduce the methodology and the results of the research on the relationship between CSR and firm performance and the mediation through employee commitment. The final part contains the conclusions, the theoretical and managerial implications, and limitations of the presented research.

Theoretical Background and Hypothesis Development

There are various theoretical approaches toward understanding CSR. One of them sets out from the fact that companies seek to integrate social and environmental requirements in their business activities, considering the needs of different stakeholders on a voluntary basis, not exclusively fulfilling obligations defined by law (Ćulafić, 2015). The very concept of CSR has been modified and reevaluated over the years, and many companies are facing demands for radical changes in the domain of their approach to society and the environment. There is an expressed need to integrate the CSR into companies’ business strategies.

A different approach to CSR starts from the assumption that it is based on the needs of adapting to the environment, achieving economic and political goals, social integration, and all this with the realization of business sustainability.

Thus, it is possible to distinguish four groups of theories of CSR, as listed below (Garriga & Melé, 2004):

The first group, known as instrumental theory, sets out from the assumption that the justification of any social activity lies exclusively in the function of making a profit. Namely, the starting point of this theory is the notion that companies exist with the aim of creating wealth, this being their only social responsibility, therefore, this approach solely considers the economic aspect of the interaction between enterprise and society.

The second group, termed political theory, emphasizes the social power of companies, the focus is on accepting and fulfilling social duties and rights.

The integrative theory states that the survival, growth, and development as well as success of business depend on the society, which is why it is necessary to integrate all social requirements into the business activities of a company.

The fourth group is called ethical theory. Its starting point is emphasizing the importance of the relationship between the company and the whole society from the aspect of respecting ethical values and dictates the need for the existence of CSR (Garriga & Melé, 2004).

In the group of instrumental theories of CSR, the theory that deserves special attention is the theory of shareholders, as it is based on highlighting the motives of the existence of companies that are reflected in the realization of profit and revenue growth. Their responsibility is directed exclusively toward the owners of capital, that is, shareholders, so the supporters of this theory claim that companies are responsible only in terms of increasing profits in compliance with legal obligations, and that all additional responsibilities in terms of social goals are only a burden for them (Castelo Branco & Lima Rodriques, 2007). The theory of shareholders has met with numerous criticisms, pointing out that its main drawback is the exclusivity in the effort to make a profit, excluding the interests of other stakeholders. Therefore, the approach where shareholders are given an advantage over other stakeholders faced with a large number of criticisms. The criticism of the shareholder theory has triggered the emergency of new theories, like agency and stakeholder theory, and the pyramid model of CSR.

The agency theory is the original answer to the criticized theory of shareholders. This theory is based on the conflict of interests that exists between the shareholders and managers of the company, striving to overcome them, that is, to achieve a balance between them (Panda & Leepsa, 2017). The greatest difference lies in the risk-taking approach, where managers are willing to take much less risk than shareholders because shareholders can always diversify their assets into other forms of financial assets, while managers face the risk of company failure and job loss.

This is followed by the emergence of the theory of stakeholders, which is the complete opposite to the originally presented theory of shareholders. Followers of this theory underline the company’s responsibility to all stakeholders, that is, all people, individuals, and legal entities as well as organizations and groups affected by the company’s activities. The main goal of developing this theory is to overcome significant differences in terms of wealth of social groups, further, to develop the concept of CSR, create conditions for maintaining business profitability, all the while protecting the interests of all stakeholders within and outside the company. This theory represents the very root of the concept of socially responsible business, after which numerous models and theories in this area appear (Banks et al., 2016; Heath & Norman, 2004). The strategies and financial performance of an organization are affected by different stakeholders like shareholders, management, employees, local community, financial institutions, consumers, suppliers, and so on. CSR is “composed of multiple stakeholder-related activities, including employee relations, diversity management, corporate governance, environmental protection, community development, consumer relations” (Yoon & Chung, 2018, p. 89).

Further development has led to the theory of sustainable development which implies a long-term perspective and approach to preserving the environment and society as a whole, in other words, it implies the realization of development in the present that has no negative effects on the development of future generations.

The pyramid model of CSR builds on the theory of shareholders and lists four basic layers of corporate responsibility, introduced in the form of a pyramid. These are the economic, legal, ethical, and the philanthropic layer. The base of the pyramid represents the economic aspect, stressing the greatest responsibility toward shareholders and making a profit. The second layer is the legal aspect, it implies respect for rules and regulations, followed by the ethical layer, encompassing responsibility toward all stakeholders. The final layer is the philanthropic aspect which implies a contribution to the entire social community (Carroll, 2016; Claydon, 2011).

The triple bottom theory incorporates the mutual harmonization and business synergy of profit, people and the planet (environment), with the basic goal of making a profit as an economic achievement, yet promoting that the activities be harmonized both in the social and environmental sense, caring for and respecting the needs of the people and their environment. This theory is based on the realization of profits, that is, the interests of shareholders, the care for the whole society within the company and outside, including all employees, consumers, customers, creditors, suppliers, competition, and government, as well as protection of the planet, the environmental aspect of business (Claydon, 2011).

The management theory shows yet another stance, it has arisen in response to the agency problem, and sets out from the assumption that managers are no longer agents but managers and that the necessary balance is achieved by aligning the goals of managers with those of all stakeholders in such a way that managers strive to achieve adequate results of the company while also satisfying all actors involved (Heath & Norman, 2004).

In the present research, the authors opted for the stakeholder approach, since this theory implies that all stakeholders that can be affected by the organizations’ activities should, in fact, be taken into account. This is also the approach that is commonly used in various studies around the world (Farmaki, 2019; Rettab et al., 2009; Saeidi et al., 2015; Taghian et al., 2015; Turker, 2009b; Yoon & Chung, 2018). The stakeholder approach enables a “better understanding of how different stakeholder focused CSR practices influence the performances of a firm” (Yoon & Chung, 2018, p. 90).

CSR and Firm Performances

CSR is developing as a business concept. There are numerous definitions of CSR, including the most basic and well-known one by Carroll (1979, pp. 499–500), in which he stated that “CSR embodies the economic, legal, ethical, and discretionary categories of business performance in a simultaneous way.” Today CSR is widely portrayed as a concept that “allows the balance between economic, social and environmental goals” (Berber et al., 2019, p. 2). CSR provides different benefits to the company, but also to the community in which company operates (R. Ali et al., 2020; Čelić, 2019; Cho et al., 2019). Dahlsrud (2008) stated that socially responsible business concerns the responsibility of the organization and the undertaking of the measures within the organization, which exceed its legal obligations and economic goals. These broader responsibilities encompass a range of issues but are usually summarized as social and environmental concerns—social relations extend to society as a whole, and not just to social issues.

CSR is reflected in the “adoption and realization of discretionary business practice and investments that provide support to the community to improve its well-being and environmental protection” (Sekulić & Pavlović, 2018, p. 61).

A key question concerning CSR is its relation to organizational performances, namely, there are diverging views regarding the importance of CSR for business. One of the approaches is that CSR needs to be understood as part of the business strategy, while the other one sees CSR as a waste of money, having a negative influence on business. This second point of view is rooted in Friedman’s agency theory that “supports the idea that the use of corporate resources for non-commercial activities harms the value for all stakeholders” (Berber et al., 2018, p. 148). According to him, “the social responsibility of business is to increase its profits” (Friedman, 2007). Since these two points of view are starkly different, many authors explored this question and the majority of the empirical findings confirmed a positive relation between CSR and firm results (productivity, profitability, return on investment, firm value, return on equity, return on assets, etc.) (Cho et al., 2019; Farooq et al., 2019; Mackey et al., 2007; Rettab et al., 2009; Saha et al., 2020; Q. Zhu, Yin et al., 2014), although there were also some results indicating negative or neutral relationships (Bocquet et al., 2017; Crisóstomo et al., 2011; Kao et al., 2018). Therefore, the question of what the effects of CSR onto organizational performances are, has yet to be answered unequivocally.

Furthermore, CSR is often investigated as a construct composed of different dimensions. The most prominent dimensions derived from the previous research are as follows:

“economic, legal, ethical, and philanthropic” (Carroll, 1979; Grubor et al., 2020; Lee et al., 2013);

stakeholder approach—“customers, employees, shareholders (investors), environment, market, community, etc.” (Fatma et al., 2014; Rettab et al., 2009; Turker, 2009b);

internal and external CSR—“the internal CSR activities include the respect for human rights, employee health and safety, work-life balance, employee training, equal opportunity, and diversity, while the external CSR activities relate to environmental and social practices that help to strengthen the firm’s legitimacy and reputation among its external stakeholders, and include volunteerism, cause-related marketing, corporate philanthropy as well as environmental and wildlife protection” (Hameed et al., 2016, p. 2).

Orlitzky et al. (2003) investigated different approaches for studying the relationship between CSR and organizational performance. The three large groups of measures of organizational performances are as follows:

“market-based (investor returns), these reflect the notion that shareholders are a primary stakeholder group whose satisfaction determines the company’s fate. The bidding and asking processes of stock-market participants, who rely on their perceptions of past, current, and future stock returns and risk, determine a firm’s stock price and thus market value;

accounting-based (accounting returns), such as return on assets (ROA), return on equity (ROE), or earnings per share (EPS), capture a firm’s internal efficiency in some way. Accounting returns are subject to managers’ discretionary allocations of funds to different projects and policy choices, and thus reflect internal decision-making capabilities and managerial performance rather than external market responses to organizational (non-market) actions;

perceptual (survey) measures ask survey respondents to provide subjective estimates of, for instance, the firm’s “soundness of financial position,” “wise use of corporate assets,” or “financial goal achievement relative to competitors” (pp. 407–408).

The authors relied on survey measures in this research, by creating “organizational performance” as a multidimensional variable that encompasses: (a) financial performance (profits, return on assets, return on equity, and return on investment) and (b) market performance (market share, sales). Further details about these variables can be found in the “Method” section of this article.

As a complex concept, CSR is related to firm performance. In the majority of the examined research, some indirect relations have been identified between these two constructs. “CSR can be positively related to financial performance because it may increase the sales, the reputation of a firm, enhance customer loyalty, raise employee morale, productivity, and stimulate innovation” (Ağan et al., 2016, p. 1874). Rettab et al. (2009) expanded the scope of observation of CSR’s relationship to organizational performance, and they added employee commitment, financial performance, and corporate reputation into their research. On the example of Dubai, Rettab et al. (2009) revealed a positive relationship between CSR, as a composite variable composed of several dimensions of CSR and firm financial performance, employee commitment, and corporate reputation. Similar to the aforementioned research, Saeidi et al. (2015) broadened the scope of observation of CSR-organizational performance relationships and introduced competitive advantage into the analysis. According to their research on 205 companies in Iran, the CSR variable, which consists of an economic, environmental, discretionary, and ethical component, has a positive effect on the organization’s (financial) performance, with the link being mediated by the company’s reputation and competitive advantage: The positive impact of CSR on business performance is the result of the positive effect that CSR has on competitive advantage, reputation, and customer satisfaction. CSR plays a vital role in indirectly enhancing firm performances through improving reputation and competitive advantage while improving the levels of customer satisfaction, too.

On a sample of 191 companies in Korea, Cho et al. (2019) explored the relationship between CSR and profitability and firm value (financial performance). The results in this case also confirmed that CSR performance had a positive correlation with the company’s profitability and the company’s value. CSR dimensions in the form of stability, fairness, contribution to social service, consumer satisfaction, environmental protection, employee satisfaction, and contribution to economic development were put in relation to financial performance. In the correlation between social responsibility and profitability (ROA) scores, only the social contribution has a positive relationship. Examining the correlation between CSR and growth rate, only the items of stability and social contribution have a statistically significant positive association. In terms of corporate value, stability and social contribution show a statistically significant positive correlation. (Cho et al., 2019, pp. 19–20)

Using data for 113 U.S. firms in the software industry between 2000 and 2005, Kim et al. (2018) found that socially responsible activities improve a firm’s financial performance when the firm’s level of competitive action is high, while socially irresponsible activities also improved its financial enterprise performance when the level of competitive actions were low. Competitive actions refer to externally directed, specific and perceived competitive moves to enhance a firm’s competitive position (new product launches, marketing, and capacity expansion, as a reflection of aggressive pursuit of new ways to satisfy desires of customers). (Kim et al., 2018, pp. 1099–1100)

Blasi et al. (2018) found that CSR in general increases stock returns and reduces financial risk. They analyzed the relationship between the firms’ CSR activities and their economic performances on a sample of 988 US-based companies from nine different sectors (basic materials, consumer goods, consumer services, financials, health care, industrial, oil & gas, technology, and utilities). (Blasi et al., 2018, p. 218)

Having in mind the previously presented research results, the present authors state that implementing CSR practices has a positive impact on firm performance because such organizations perform business practices that are more ethical and responsible toward their internal and external stakeholders, and on that basis, they create a more positive firm image and thereby ensure a better position on the market. Such companies can have better relationships with their suppliers, customers, public entities, local and state government, employees, and shareholders, thus, as a result, those companies can experience higher profitability, productivity, environmental efficiency, and other firm performances. Based on the afore-mentioned, the first research hypothesis is as follows:

CSR and Employee Commitment

According to the above-mentioned CSR constructs, a key dimension is related to employees, found in almost all approaches to CSR dimensions. The human potentials and human resource management (HRM) are seen as one of the most important business elements that are related to organizational success (Bogićević-Milikić, 2019; Meier et al., 2021). CSR toward employees encompasses different activities within HRM, such as “communication and information flow, fair and adequate training and development, empowerment of employees, looking after the health and well-being of employees, balance of working and family life and concern for the safety of the workplace” (Grubor et al., 2020, p. 5). Skilled and motivated employees are essential for gaining desired business goals, especially in the new economy, which is related to the information technology, artificial intelligence, and new generations (Y and Z generation of people). Employees’ ideas, creativity, intelligence, skills, knowledge, and psychological efforts will contribute to success in modern business. Training and development are related to “the permanent acquisition of new knowledge and skills, as a necessary basis for the development and survival of the society” (Slavković & Slavković, 2019, p. 116).

Commitment is defined as “a force that binds an individual to a course of action that is relevant to a particular target” (Meyer & Herscovitch, 2001, p. 301). Commitment can also be described as a component of motivation (Meyer et al., 2004), thus it “refers to identification with organizational goals, willingness to exert effort on behalf of the organization, and interest in remaining with the organization” (Whitener, 2001, p. 518). “Commitment binds an individual to an organization and thereby reduces the likelihood of turnover. The three main forms of employees’ commitment are affective commitment, normative commitment and continuance commitment” (Meyer et al., 2004, p. 993).

Affective commitment is related to emotional attachment to, identification with, and involvement in the organization. Continuance commitment means the perceived costs associated with an employee leaving the organization. Normative commitment reflects a perceived obligation of an employee to remain in the organization. (Meyer et al., 2002, p. 21) The benefits to organizations of having a strongly committed workforce are that employees who are committed to an organization are less likely to leave and more likely to attend regularly, perform effectively, and be good organizational citizens. Commitments to other work-relevant foci, such as occupations, supervisors, work teams, and customers have also been linked to retention and other indices of effective performance of benefit to employers. (Meyer & Maltin, 2010, p. 323)

According to Đorđević et al. (2019), employee commitment is influenced by organizational justice, and employees who perceive that their organizations to be rather fair, will also be more committed and increasingly motivated to achieve more for their companies.

Research results revealed that a company’s social responsibility activities were important to its employees and tended to have a positive impact on employee commitment (Backhaus et al., 2002; Tian & Robertson, 2019; Turker, 2009a). The authors Backhaus et al. (2002) found that CSR dimensions related to environmental protection and natural environment, local community and respect for the diversity of people had the greatest positive impact on the employer’s attractiveness, viewed from the perspective of job seekers and employees. Turker (2009a) proved on a sample of 269 workers in Turkey that social responsibility dimensions positively influenced employee commitment to the organization. CSR dimensions related to employees and clients were significant predictors of the organizational commitment. According to Tian and Robertson (2019), perceived CSR can impact employees’ organizational commitment. Hofman and Newman (2014) explored the relationship between employees’ perceptions of CSR and their organizational commitment on a sample of 280 employees from five export-oriented manufacturing firms in China. They found that employee perceptions of CSR practices towards internal stakeholders have positive relations to employees’ organizational commitment. Conversely, employee perceptions of CSR practices towards external stakeholders had a nonsignificant or only marginally significant impact on organizational commitment. Besides, the collectivism and masculinity orientations of employees, as cultural dimensions were found to moderate the relationship between CSR and employee commitment.

In addition, CSR can promote organizational identification which will, in turn, enhance organizational commitment (De Silva & Lokuwaduge, 2019).

Based on the afore-mentioned, the implementation of CSR in an organization can influence and lead to better reputation and image, that will be understood not only by external stakeholder, but also by employee that will be able to associate themselves with organizations. If an organization acts as socially responsible, its employees can be proud of such an organization. They will see those types of practices as responsible, especially those related to employees in terms of career progression, equal pay and incentive pay, indiscriminatory behavior of managers, good communication, and positive climate. Employees can be more attached to the company, and therefore, they can be more committed. The second proposed research hypothesis is as follows:

The relationship between CSR and firm performance has been extensively researched in the past. Although it has been investigated in different sectors, industries, and even countries, there are still no unambiguous indicators of such a relationship. Positive, negative, and even neutral relations were identified, what is more, most studies found this relation to be mediated (Anser et al., 2018; Galbreath & Shum, 2012; Malik et al., 2020; Wang et al., 2014; Wu et al., 2015; Y. Zhu, Sun, et al., 2014) or moderated (Bai & Chang, 2015; Jia, 2020; Lee & Kim, 2017). As the authors stated in the Introduction of this article, employee behavior is one of the factors that has a mediating role in the link between CSR and performance (Collier & Esteban, 2007; Gao & He, 2017; Lee et al., 2013; Turker, 2009a). CSR can be seen as a driving force for an increase in employees’ positive work behavior, such as employee commitment (I. Ali et al., 2010; De Silva & Lokuwaduge, 2019; Farooq et al., 2014; Turker, 2009a). Ivanović-Đukić et al. (2018) stated that the positive influence of employees on organizational performances depended on their attitudes and behaviors. Regarding employee commitment, the results of the study conducted in Pakistan, on a sample of 371 professionals working in different sectors, proved that “there were significantly positive relationships between CSR actions and employee organizational commitment, CSR and organizational performance and employee commitment and organizational performance” (I. Ali et al., 2010). Stawiski et al. (2010) stated that the organizational commitment and productivity would be higher if the employees experience CSR actions. Choi and Yu (2014) found that “organizational commitment was an indirect mediator of CSR and performance, through organizational citizenship behavior” (OCB). The effects of CSR on organizational commitment were greater than on OCB, which means that commitment has important role of on CSR-OCB link, and on that basis, firm performances. Chun et al. (2013) investigated the mentioned relationship on a sample of 3,821 employees and financial results from 130 Korean companies. The results of their study showed that collective organizational commitment and interpersonal OCB mediated the link between corporate ethics (as a wider concept than CSR) and firm financial performance.

Drawing on findings of these previous studies, the present authors find that employees who perceive that their employers are implementing socially responsible practices in numerous areas of business (HRM, relationships with external stakeholders, and shareholders) will be more committed to the organization and perform better, thus, on that basis, this will positively influence organizational performance in terms of productivity, profitability, among others. Therefore, CSR should affect organizational performances through the mediation of employee commitment. The third research hypothesis is as follows:

Method

As mentioned before, for the purpose of this study, the authors conducted a field research on the territory of the Autonomous Province of Vojvodina, Republic of Serbia in the period from October 2019 until the end of March 2020. The following section of the article offers details on the applied questionnaire, variables, and the model.

Questionnaire and Variables

The questionnaire used in the research is based on the findings of various earlier studies (Rettab et al., 2009; Saeidi et al., 2015; Turker, 2009a).

The questionnaire was composed of closed questions and respondents were asked to select their answers from given sets of alternatives. The questionnaire consisted of three parts: the first part was related to the organizational details, the second part contained questions on CSR, while the third part was related to organizational outcomes and employee behavior (Grubor et al., 2020).

Corporate social responsibility was measured through 26 questions, on a Likert-type scale (1 = not at all to 5 = to a great extent). A CSR variable was developed as a formative construct, from six factors (dimensions) of CSR: responsibility to the environment (four questions, presented as Envi1, Envi2, Envi3, and Envi4), employees (five questions, termed HRM1, HRM2, HRM3, HRM4, and HRM5), community (four questions, referred to as Comm1, Comm2, Comm3, and Comm4), investors (four questions, given as Invest1, Invest2, Invest3, and Invest4), suppliers (five questions, presented as Supp1, Supp2, Supp3, Supp4, and Supp5), and customers (four questions, referred to as Cust1, Cust2, Cust3, and Cust4). The questions were chosen from research of Rettab et al. (2009) and Turker (2009a). These two studies were deemed suitable for the development of the present approach in Serbia, given that both studies were conducted in developing countries, too, namely in Dubai and Turkey. This section gives some samples of the questions from the questionnaire. Questions regarding employees’ responsibility dimension included these examples: “Do you treat all employees fairly and respectfully, regardless of gender or ethnicity?,” “Do you provide all employees with pay according to their workload?,” “Do you support all employees who want to continue their education and develop their careers?,” and so on. In the case of responsibility to customers, respondents were asked to answer on the following questions: “Do you provide all clients with high-quality service?,” “Do you provide all customers with the information they need to make purchasing decisions?,” “Do you respect all customer complaints about the company’s products and services?,” “Do you customize products or services to maximize customer satisfaction?”

Firm performances (Fin Perf) were measured through six usually observed indicators, market share (Fin1), profit rate (Fin2), return on investment (ROI)(Fin3), return on assets (ROA)(Fin4), return on equity (ROE)(Fin5), and growth in sales volume (Fin6) (Rettab et al., 2009; Saeidi et al., 2015). These measures were based on the research of Saeidi et al. (2015) who found that firm performances, especially financial ones, can be drawn from a balanced scorecard approach. The respondents had to compare their performances with those of their main competitors, using statements, such as, “In relation to your competitors, evaluate your business results over the past year,” on a scale from 1 to 5, with the meanings 1 = weak or the least within this branch, 2 = below average, 3 = average or equal to the competition, 4 = above average, and 5 = superior. The reasons for using subjective questions to assess firm performance instead of accounting measures are the twofold. On the one hand, according to Santos and Brito (2012), “this approach allows the control of different economic activities in the sample when comparing the firm to the industry’s average, and it minimizes the sector influence on the data sets.” On the other hand, as Vij and Bedi (2016) suggested, the implementation of subjective measures of firm performances is particularly useful in research situations where it is very difficult to access the actual data of organizations due to the “reluctance of the managers to share sensitive data or because of poor reporting by the firms” (p. 612).

Employee commitment was measured through three questions, on a 5-point Likert-type scale, from 1 = strongly disagree to 5 = strongly agree. The questions are chosen from the study pf Jaworski and Kohli (1993) and Rettab et al. (2009): “Our employees often go beyond their responsibilities to secure the benefit and well-being of the organization” (presented as EC1), “The bonds between our organization and our employees are very strong” (given as EC2), and “Our employees are very committed to our organizations” (referred to as EC3).

Sample and Data Collection

The sample used for this study consists of 53 large companies that operate on the territory of AP Vojvodina, in the Republic of Serbia, with more than 250 employees (large organizations), mostly from the processing industry (35,8% of the sample), that are in private ownership, with 66% national companies and 34% foreign subsidiaries. (Grubor et al., 2020)

The average number of employees in the selected companies is 773. There are a total of 151 large organizations in the AP Vojvodina, the northern province of the Republic of Serbia, according to the data from Statistical Office of the Republic of Serbia (Popović, 2019). A total of 151 questionnaires were sent out, with 59 responses collected until the deadline. Six responses out of the 59 had many missing answers, so they were disregarded in terms of further analysis. The final sample consists of 53 valid responses (n = 53). This means that the sample makes up 35.33% of the population.

Data collection was performed by using an on-line questionnaire, created in Google forms. As the questionnaire was created for the managerial staff, the respondents were managers in a senior position, who had the access to the necessary data. Most of the respondents belong to either the top management board (43.4%) or middle management level (43.4%), while only 13.2% were respondents were from the line managerial level. The managers were asked to rate their organizations according to the questions on CSR, commitment, and firm performances. The single respondent methodology was implemented; only one questionnaire was collected per organization, as a representative of the entire company. “It is expected that the level of professionalism and internal regulations of the analyzed organizations will not allow respondents (who stated that they have managerial responsibilities) to give false answers” (Berber et al., 2020, p. 993).

Data Analysis

To investigate the proposed relations, PLS-SEM analysis has been performed using the statistical software Smart PLS. The software was applied to estimate the measurement and structural model parameters and to generate the accompanying bootstrap estimates.

The first part of the analysis referred to the measurement of the reflective constructs in the model. Seeing as all constructs employee commitment and financial performances are reflective, Grubor et al. (2018) and Hair et al. (2019) suggest measures for analyzing reflective constructs: “individual indicator reliability, internal consistency reliability, convergent validity, and discriminant validity.” CSR is a formative indicator, second-order construct. In the process of testing mediating effects, “the mediating testing method was used to test both total and indirect effect and the statistical significance of the mediating variable” (Hsu et al., 2020, p. 6). Apart from these, the bootstrap method was applied to estimate the statistical significance of total effects, direct and indirect effects.

Results

Testing the Questionnaire

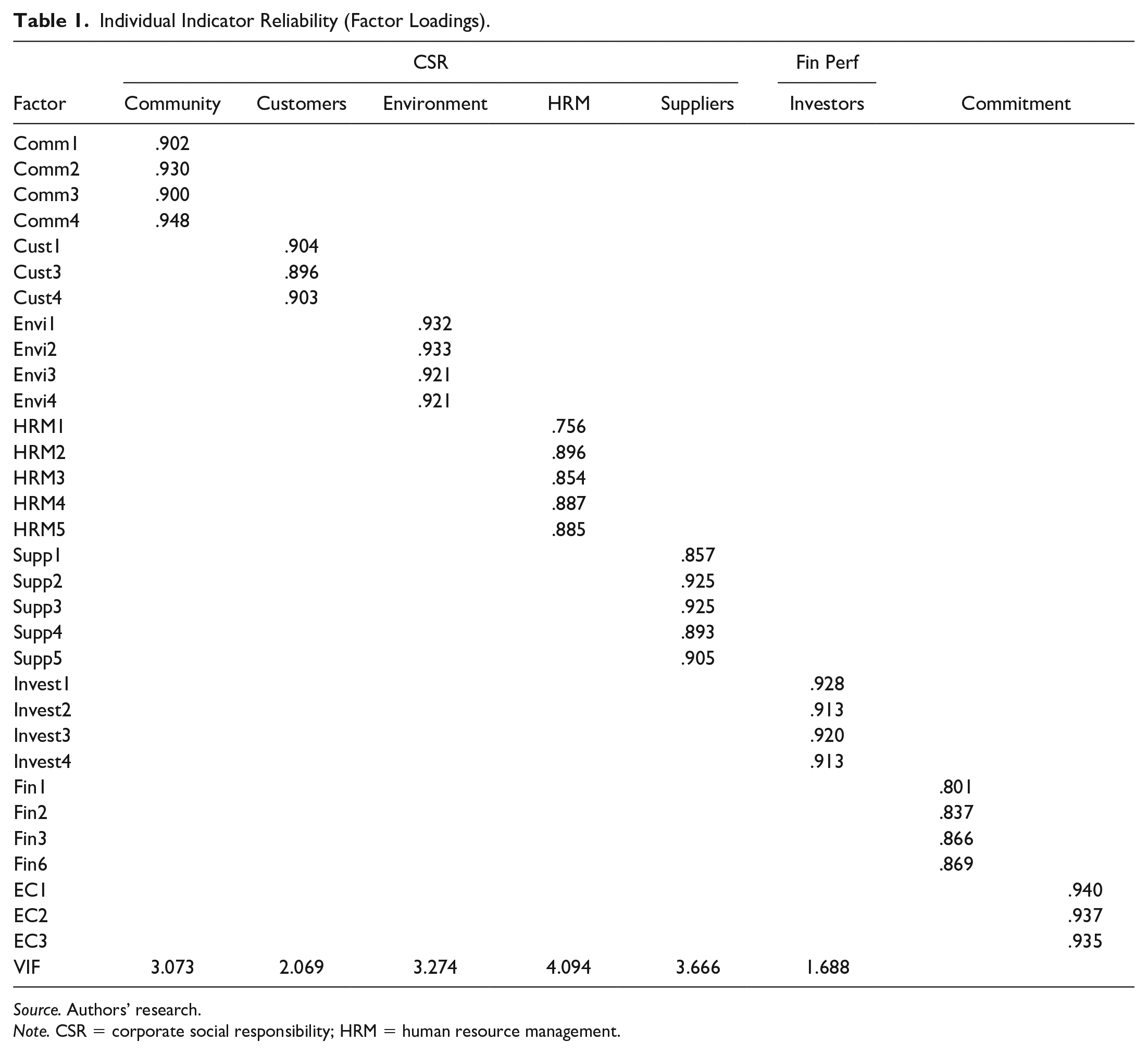

Table 1 outlines factor loadings. Since some variables did not surpassed loadings of .708, they were leaved out from the analysis (in this case those were variables Cust2, Fin4, and Fin5). In the final step, all factors had loadings higher than .708 and they are used in the following analysis (Hair et al., 2019).

Individual Indicator Reliability (Factor Loadings).

Source. Authors’ research.

Note. CSR = corporate social responsibility; HRM = human resource management.

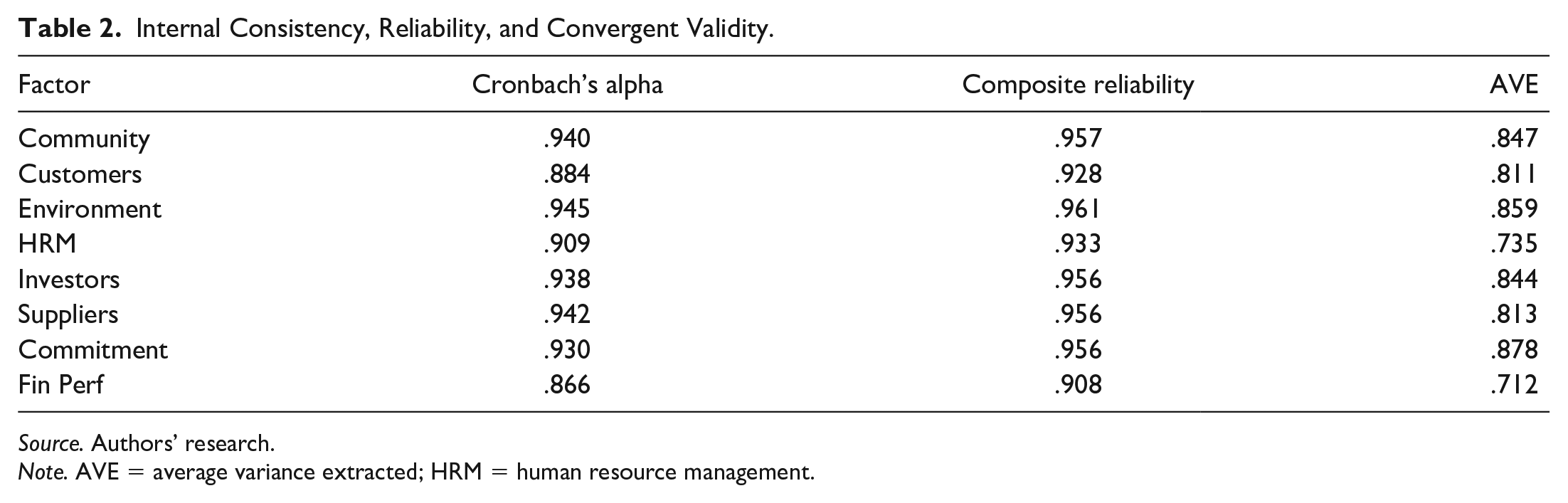

Internal consistency reliability and convergent validity are measured by composite reliability, Cronbach’s alpha, and average variance extracted (AVE). According to the data from Table 2, internal consistency and convergent validity are satisfied for all three reflective constructs because Cronbach’s alpha and composite reliability are having values above .70, while AVE is ≥ .50.

Internal Consistency, Reliability, and Convergent Validity.

Source. Authors’ research.

Note. AVE = average variance extracted; HRM = human resource management.

From the data in Table 3, the Fornell–Larcker criterion was performed to investigate discriminant validity. Each construct’s square root of AVE is higher than its correlations with other constructs which confirms discriminant validity.

Discriminant Validity Assessment: Fornell–Larcker Criterion.

Source. Authors’ research.

Note. HRM = human resource management.

The multicollinearity analysis revealed that not all variance inflator factors (VIF) surpassed the value of 5, most of them were around the value of 3, which indicated that there were no collinearity issues (Hair et al., 2019). Common method bias (CMB) was also detected through a full collinearity assessment approach (VIF indicators in Table 1, the last row). Moreover, the Harman’s single factor score (Podsakoff et al., 2012) showed that the total variance for a single factor was less than 50% (it was 48%), which means that common method bias did not affect the data in this research.

When assessing the formative model it is necessary to investigate convergent validity (redundancy analysis), collinearity diagnosis (VIF), statistical significance of weights, and relevance of indicators with a significant weight. Regarding the CSR formative construct, VIFs presented in Table 1 showed that there was no multicollinearity in the model, since all of them were around 5 or less. All indicators had statistical significance (p < .05), and all indicators showed loading higher than .50.

Testing the Model

The second part of the testing was to investigate the relations between CSR, employee commitment, and firm performances. The data in Table 4 and Figure 1 present the PLS-SEM coefficients and significance level, and the coefficient of determination of the model. The R2 value is .600 for employee commitment and .313 for firm performances, which means that the independent variable explains 60% of the variance in employee commitment and 31.3% of the variance in the firm performances. Coefficients of the relationships between the formative construct (CSR), independent, and reflective constructs, dependent (firm performances), and mediator (employee commitment) demonstrated different values in the model. According to data presented in Table 4, there are statistically significant direct positive relationships between CSR and employee commitment (B = .774, t = 11.488, p < .01), and between employee commitment and firm performances (B = .483, t = 2.117, p < .05). Based on the results, H2 is confirmed and based on the sample of Serbian companies, CSR is positively related to employee commitment. Further, employee commitment is positively related to firm performance. However, in the case of the relation between CSR and firm performance, there is no statistically significant relation (B = .147, t = 0.626, p > .05). Therefore, the first hypothesis H1 is not confirmed. Effects size (F2) revealed the remaining variance of R2 in the dependent variable. The recommended values for R2 are “0.02, 0.15, and 0.35 with small, medium, and large effects” (Hair et al., 2012; Khan et al., 2020). In the case of the model, there was only one value that showed very small effects, and that was the F2 for CSR-financial performance link (F2 = .013).

Mean, Standard Deviation, T-Statistics, and P-Values.

Source. Authors’ research.

Note. CSR = corporate social responsibility.

Path coefficient estimates.

As for the effects of commitment on the link between CSR and firm performances, a positive mediated relationship was found, where CSR had a positive influence on firm performance through employee commitment (B = .339, t = 2.023, p < .05). Based on the results, the third hypothesis H3 is confirmed (Table 5).

Verification of the Relationship Between Variables in the Structural Model.

Source. Authors’ research.

Note. CSR = corporate social responsibility.

*p < 0.05.

Discussion

The results of this research echoed similar results in previous studies. In this current sample, the authors did not determine direct positive statistically significant relations between CSR and firm performances of companies, measured by ROA, ROI, ROE, market share, sales increase, and productivity. Although it was expected that the relationship would be positively significant, as proposed by the first hypothesis in this sense, this was not the case, therefore H1 was not confirmed. These results did not show negative, but an insignificant positive relationship. The reasons why CSR does not have a direct positive effect on performances were investigated by Rettab et al. (2009), who found that “the institutional environment in developing economies were usually driven by policies that promote high economic growth and international competitiveness, that, if not properly managed, may lead to social inequality, poor labor practices, and enormous environmental damage” (p. 374). Moreover, usually there are no well-established regulatory mechanisms that will monitor and enforce regulations regarding environmental protection, consumers’ rights, employees’ well-being, fair business practices among investors, and so on. This is of key importance for Serbia, a developing country that went through a considerable development trajectory from socialism and planned economy, through the 1990s, to market economy, capitalism, and democracy after 2000. In the case of Serbia, the starting pattern of capitalism was explained as “wild capitalism, characterized by “informality, clientelism, corruption, personal political networking and gangsterism sit side-by-side with more “normal” capitalism characterized by legality, and “western” codes and norms of behavior” (Upchurch & Marinkovic, 2011, p. 330). This kind of capitalism existed during the process of transition in Serbia, after 2000” (Berber et al., 2020, p. 974). The fight for business success and profit exceeded the other parts of the business (employees’ needs, consumer rights, environmental protection, and the fulfillment of obligations toward suppliers, investors, and the state, regularly). On the other hand, nowadays Serbian companies are developing their CSR activities to a greater extent. An increasing number of them participate in different areas of CSR, mostly in environmental protection programs, sponsorship to the local community, professional development of young people, and others. Further, the employees’ position is improving, as most companies now recognize the problem of workforce shortages and the need to have professional and committed employees in each position. For example, in the latest empirical research on CSR and business performances in Serbia, Ivanović-Đukić and Lepojević (2015) found that there were differences between the most efficient, average, and below-average efficient companies at the level of CSR and underlined that significant differences exist in certain CSR segments.

The best condition was found in areas related to responsibility to business partners, suppliers and consumers, global environmental concerns, also health and safety at work, but the most problematic areas were still the adaptation to change, human resource management, management of environmental impacts and also natural resources and local communities.

A potential explanation for this relationship lies in the notion that the negative effect of CSR on firm performance “may unintentionally capture the initial cycle of CSR with its significant short-term cost while the positive effect of CSR on firm performance captures the longer-term benefits” (Kao et al., 2018, p. 174). If companies in Serbia start to invest more in socially responsible practices (for example, in incentive pay, career development and employees training, environmental protection, fair cooperation with foreign suppliers and customers, etc.), they will experience higher costs, that can have a negative influence on firm financial performance in the short-run (annual results), or this relationship will not be strong.

Given that no direct effects of CSR were found on firm performances, the authors explored another relation, between CSR and employee commitment, and then the mediation of employee commitment on CSR-firm performance link. It was determined that there were positive statistically significant relations between CSR and employee commitment. This means that a more developed level of CSR practices in companies leads to greater employee commitment. In this way the authors confirmed their second hypothesis (H2). This is a very important finding, in accordance with previous research (Backhaus et al., 2002; Hofman & Newman, 2014; Tian & Robertson, 2019; Turker, 2009a). CSR will have a positive impact on the commitment of employees that will become more identified with organization, increase their efforts on the job, and stay in the organization for a longer period of time. Committed employees will show a lower level of turnover intentions, higher productivity, better relations with co-workers, customers, and managers, and on that basis, they could be the factor of the business success of the whole organization. Regarding this relation between CSR and commitment, companies should deeply investigate the HRM activities that are recognized as socially responsible, like action programs to improve the participation of marginalized groups in the workforce, flexible working time, job rotation, profit sharing, employee share ownership, communication, information flow, better-defined training needs, empowerment of employees, looking after the health and safety of the workplace and well-being of employees, like the balance of working and family life. (Berber et al., 2014)

Such CSR activities can improve employees’ commitment, their performances, and on that basis, the total organizational performances.

Concerning the last hypothesis (H3) on the mediating role of employee commitment on CSR-firm performance link, the authors found that employee commitment mediated this relationship, and has positive, statistically significant effect. According to the results of the analysis, employee commitment positively enhances the relation between CSR and firm performance. CSR will increase employee commitment, and, through employee commitment, it will have a positive effect on firm performance. The present findings are in the line with the previous research that dealt with the mediating role of commitment on CSR and performance relation (I. Ali et al., 2010; Choi & Yu, 2014; Chun et al., 2013; Stawiski et al., 2010). Responsible business practices of companies result in increased employee commitment, and such committed employees have a positive effect on overall business performances.

Conclusion

In this study, the authors set out to show how CSR is related to organizational performances in organizations from a developing country. This relationship was investigated in previous research in the world, with quite specific results. Some research results pointed to positive, but also negative, direct or indirect relationship. We have used employee commitment as a mediator in this relationship, since the literature suggested that commitment is one of the most important employees’ attitudes that enhance employee performances and positive work behavior. To increase the uniqueness of our study, we used a specially designed questionnaire, based on previous successful research, applying single respondent methodology, where only one questionnaire was filled in each organization taken into consideration. The respondents were managers on higher level in a company. The main findings of the study are that there are no direct positive statistically significant relations between CSR and firm-level performances of companies, measured by ROA, ROI, ROE, market share, sales increase, and productivity, while this relationship is mediated through employee commitment. Also, we found that CSR is positively related to employee commitment. This means that implementation of CSR activities and practices is positively related to commitment of employees, which leads to proactive work behavior and better work results. The authors confirmed second and third hypotheses, while the first one was not confirmed. These results are in the line with some previous research, especially those that were implemented in developing countries, like Serbia is. Possible explanation of the non-significant relationship between CSR and firm performances is the thought that CSR activities are seen as a cost for a company, and in short-term they cannot produce profit. It is important to emphasize the long-term benefits that CST can bring to the company, like stringer brand, improved image, satisfied employees and consumers, local community, and so on.

Theoretical and Practical Implications of the Study

The results of the research presented in this article entail certain theoretical and practical implications. The most important theoretical implication of the article lies in the increased understanding of the effects of the employee commitment on the relationship between organizations’ socially responsible initiatives and overall firm performances. The study enriches the literature on CSR by providing the data of the role of employee commitment on CSR-performance relationship. The authors did not find direct, but indirect (mediated by employee commitment) positive relation between CSR and performances. An additional theoretical implication is connected to the questionnaire designed for Serbia that was developed from earlier versions that were implemented in Western developed and South-East developing countries (Rettab et al., 2009; Saeidi et al., 2015). Serbia, as a country of Central and Eastern Europe, differs in its institutional, cultural, and economic system from other regions, but these factors did not change the results and the reliability of the tests. Apart from the characteristics of institutional and economic systems, it is important to bear in mind the organizational factors when exploring these relations. Therefore, this research can be a starting point for future analysis of mediating or moderating organizational effects on CSR-performance link.

The practical implication of the research lies in the empirical evidence of the positive influence of CSR initiatives on employees’ behavior, and through commitment, on firm performance. Companies should develop and implement specific CSR activities because it has been proven that responsible and ethical business practices which take into account large group of stakeholders, and a wider business, social and natural environment, will bring greater benefits for the companies because their employees perceive their firm as a responsible, fair and good place of work, and on that basis, management can increase their motivation and commitment, and performances. When employees are influenced by companies CSR practices, they will experience higher organizational commitment, and consequently, the higher productivity. Having in mind the importance that employee commitment had on CSR-performance link, employees’ well-being programs, development possibilities, and other employee-friendly practices need to be tied in with CSR policies and implemented inside business and HR strategy. These kinds of employee-friendly practices will make a base for increasing employee commitment, and on that basis, to enhance positive work behavior, that will lead to better business performances. Also, CSR has to be seen as an investment that should be treated as a strategic decision to undertake, that needs costs, but that can enhance business results in medium or long-term.

Limitations of the Study

Though the authors found statistically significant relations and mediating effects, they acknowledge certain limitations of this research. The first and most important research limitation is the relatively small sample. The main reason why such a small sample was used lies in the fact that this was the first research of its kind in Serbia and that the main idea of the researchers was to investigate large companies because the explored practices are more prevalent in large companies (concerning relationship to shareholders and investors). However, the overall number of such large companies in Serbia is no more than 540 in total. Of course, future research will aim at the inclusion of SMEs, and the investigation of CSR in such companies, and the analysis of the differences in CSR approach between large and SME companies. A further limitation is the single respondent methodology used for data gathering (Gerhart et al., 2000). “This could be the source of measurement errors, but it is expected that the level of professionalism and internal regulations of the organizations will not allow respondents (who stated that they have managerial responsibilities in organizations) to make false statements” (Berber et al., 2020, p. 993). Finally, the authors did not explore partial mediation effects of different CSR dimensions on employee commitment and firm performances. This may also reveal relations between specific CSR activities regarding employees, customers, investors, community, and suppliers, and the environment. Therefore, it may serve as the subject of future research.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors received financial support for the research from the Provincial Secretariat for Higher Education and Scientific Research of Autonomous Province of Vojvodina, Republic of Serbia during the project “Effects of corporate social responsibility in the field of human resources management on the performance and sustainability of organizations” (number: 142-451-2482/2019-03).