Abstract

This study aims to investigate the short-run and long-term impact of oil prices on the market returns of the Next Eleven (N11) economies in the presence of the moderating role of economic policy uncertainty on this relationship. This study uses monthly data on oil prices, economic policy uncertainty, and equity markets index from the period January 2005 to December 2022. Both ARDL and NARDL models are employed to examine the linear and asymmetric co-integration between oil prices and N11 market returns. The results of the ARDL model indicate that there is a statistically significant and positive correlation between oil prices and the equity market of Vietnam, but only in the long term. The selected countries demonstrate a more noticeable short-term connection as a result of the significant influence of oil prices on stock market returns. The NARDL technique reveals that oil prices have an asymmetric impact on the market returns of Pakistan, Bangladesh, Indonesia, Turkey, Vietnam, South Korea, and Mexico. In the short term, economic policy uncertainty has a moderating effect on the relationship between oil prices and the stock markets of Pakistan, South Korea, Mexico, Nigeria, and Egypt. This study is insightful for investors as by considering the uncertainty impact, they can restructure their portfolios and reallocate the risk accordingly. Investors should implement a flexible asset allocation strategy that adapts to fluctuations in the macroeconomic environment. Further, the practical implication of the research assists regulators in the fair price discovery through disclosure. Risk professionals should closely monitor the evolving global landscape since it will have an impact on the assets they manage.

Plain language summary

The current research investigates the impact of the asymmetry link between oil prices and the stock returns of the Next 11 countries that have sustainable economic development potential in the future. Within the dynamics of the current study, the moderating effect of EPU has been examined on the link between oil prices and N11 equity markets.

Introduction

Stock markets often serve as indicators of economic performance, as they are highly responsive to sudden shocks and changes in economic policies (Tiwari et al., 2025). Several theoretical frameworks have been used to analyze how changes in macroeconomic conditions affect stock returns such as the efficient market hypothesis proposed by Fama (1970) and the arbitrage pricing theory introduced by Ross (1976). Several recent studies have investigated the impact of oil prices on stock returns, but their conclusions have been inconclusive (Nakhli et al., 2025; Peiró, 2016). The discussion on the changes in oil prices and the returns of emerging markets within the framework of arbitrage pricing theory has persisted since the 1980s. The idea was expanded upon in the context of symmetric and non-linear backgrounds by Hashmi and Chang (2023). Therefore, it is essential to investigate the influence of uncertainty in this relationship to determine its effect on stock returns. The existing literature predominantly concentrates on investigating the unequal influence of oil prices on the stock markets of developed economies, with few studies undertaken on frontier and emerging countries (Castro & Jiménez-Rodríguez, 2024; Hashmi & Chang, 2023). Prior research also illustrates that the risk and propensity for returns in industrialized states differ from those in emerging nations (Dai & Tang, 2024). Examination of the asymmetric relationship between oil prices and market returns of N11 economies in the presence of the moderating role of economic policy uncertainty on this relationship has not been performed holistically. Goldman Sachs in 2005 coined the term N11 (Next 11) for a group of emerging economies that have high potential for growth and economic development following the BRICS nations (Shafiq et al., 2023). The N11 countries represent some of the fastest-growing economies in the world. They have large, young populations (Pakistan, Bangladesh, Nigeria) and are undergoing rapid industrialization (Vietnam, South Korea) and urbanization (Mexico, Turkey). Exploring the N11 countries is substantial for uncovering economic growth, diverse development models, trade and investment opportunities, socio-cultural diversity, challenges, and risks (Gupta & Bhatia, 2022). Understanding their economic trajectories can provide insights into investment opportunities. Secondly, their geopolitical roles make them important for understanding global economic dynamics. Thirdly, these exhibit a wide range of economic, political, and social systems so studying them provides valuable insight about diverse economic policies. Finally, as the N11 countries grow, they are likely to play a more significant role in shaping global economic and political systems in the future. Their growth, challenges, and opportunities make them essential subjects for researchers, policymakers, and businesses aiming to navigate the complexities across countries. Therefore, it is imperative to conduct a study on emerging economies, namely N11 countries that possess the potential to have sustained economic development potential in the future. The Next 11 countries comprise Pakistan, Bangladesh, Indonesia, Vietnam, South Korea, Iran, Mexico, Turkey, Philippines, Nigeria, and Egypt.

The current study investigates the moderating role of Economic Policy Uncertainty (EPU) on the equity markets of N11 countries, specifically with oil prices, given their significant global interdependence. Due to the impact of technology and globalization on financial markets, the level of uncertainty has substantially increased. The current state of the global financial markets is characterized by a high degree of complexity, which in turn leads to an increased level of uncertainty. The global economy faces dynamic difficulties, including the escalation of oil costs (Lee et al., 2024). As a result, the existing lack of certainty hampers the rate at which the economy expands, leading to a decrease in cash flows and a decline in stock prices. Policy uncertainty has a significant impact on specific economic outcomes, as evidenced by previous economic downturns (Olasehinde-Williams, 2024). An increased uncertainty increases investors' risk perceptions, which would entail an increased demand for a higher risk premium, affecting macroeconomic variables market prices, and future returns (Shen et al., 2025). If there is high uncertainty, perhaps the market participants become more sensitive to macroeconomic news. When EPU is high, investors may either overreact or underreact to macroeconomic news depending on how the uncertainty interacts with their interpretation of the news. High EPU can lead to increased risk premiums, reduced confidence in the predictive power of current economic data, and a shift in focus from fundamentals to policy outcomes. As a result, the usual effects of oil prices on market returns are either amplified or diminished, depending on the nature of the uncertainty. Therefore, it is essential to examine the moderating role of economic policy uncertainty in this study. The first objective of the study is to investigate the long-run relationship between macroeconomic variables and equity markets while the second objective is to determine the asymmetric response of equity markets to positive and negative changes in macroeconomic variables.

This study can be advantageous for policymakers, financial market participants, executive management, and asset managers. Additionally, this research will assist regulators in achieving equitable price determination through disclosure. Due to the presence of market inefficiencies, investors are motivated to employ innovative techniques and their extensive investment knowledge to make predictions using previous data to exploit these inefficiencies for their benefit. Politicians and government agencies need to understand that economic policy uncertainty surrounding fluctuations in oil prices can significantly harm investor confidence and asset prices. To address any misunderstanding surrounding the government’s position on economic problems, government agencies should provide transparent communication with elected representatives. This has the potential to decrease market volatility and enhance the value of financial assets by facilitating more accurate predictions of specific government initiatives. This study is valuable for determining the influence of economic policy uncertainty on the stock market and, more especially, the financial strategies of enterprises, considering events. Oil prices are significantly impacted by global economic policy uncertainties due to their significant global interdependence. Asset managers and investors with broad investment mandates and perspectives should be equally concerned about the asymmetric effects of oil price volatility.

Literature Review

The conventional asset pricing models proposed by Sharpe (1964), Lintner (1965), and Mossin (1966) provide that returns can be explained with the help of market premium only. However, the same was challenged by Ross (1976) who proposed the arbitrage pricing theory depicting that asset returns are influenced by “n” many factors, and such variations are reflected in the stock prices. Arbitrage Pricing Theory (APT) is an extension of (CAPM) that only incorporates the market premium as a single factor. They also provide a footing for a linear relationship between an expected return of an asset and the macroeconomic factors that substantially impact the asset’s risk (Chen et al., 1986). The APT presents an alternative multi-factor pricing model for securities, for analysts and investors to utilize, based on a market’s relationship between a financial asset’s expected return and its risks. Similarly, the discounted cash flow model or the present value model (PVM) also concludes that stock returns are significantly influenced by the behavior of macroeconomic variables (Humpe & Macmillan, 2009). Macroeconomic variables that substantially impact the future cash flows of a firm also impact the stock prices as the stock prices are cumulative discounted values of the firm’s future cash flows (Nautiyal & Kandpal, 2025). The present value of a firm is derived from using a risk-adjusted discount rate to discount the expected future cash flows and then using the discount rate to obtain value (Campbell & Shiller, 1988; Gordon, 1959). Bali and Cakici (2008) assert that market price dynamics can be impacted by any macroeconomic factor that can potentially change future cash flows or discount rates.

Theoretically, equity value is contingent on macroeconomic conditions and aggregates discounted predicted future cash flows at various investment horizons (Kwon, 2025). It can be determined that shocks to the oil price either affect expected future cash flows because an increase in production costs causes adverse shifts in the demand for commodities and services in oil prices leading to inflationary pressures, which causes stock prices to plummet (Dokas et al., 2023). However, studies reveal that counterintuitively shocks to oil prices induced by global economic growth may raise stock prices across the economic spectrum (Olasehinde-Williams, 2024). The current body of literature also demonstrated that if a supply shock drives up oil prices, stock prices may be negatively impacted by investors’ fear of unpredictability in oil production in the future (Pata et al., 2024). Hence, it is imperative to understand that different perspectives prevail on how shocks to oil prices impact stock market returns. Using a quantile regression approach, the study examined the impact of economic policy uncertainty on the volatility of the equity markets in the G7 and BRIC countries (Yuan et al., 2022). The empirical findings indicate that in the presence of economic policy uncertainty, the stock returns of the various economies portray heterogeneous asymmetry and tail reliance. de Oliveira et al. (2020) use a multivariate NARDL model to examine the influence of the uncertainty index on sustainability across different countries. Another study compared the performance of 24 emerging stock markets with industrialized stock markets and investigated how the pandemic has affected stock returns (Maghdid et al., 2024). The results of the study demonstrate that equity markets of developed economies tend to offer better opportunities for hedging compared to investments in financial markets in developing equity markets.

Arouri and Rault (2012) employed a Granger causality test to show that fluctuations in the price of oil were significantly correlated with movements in European stock markets. Pan et al. (2016) examined weekly future price data from February 2000 to August 2015 and concluded statistically significant asymmetric oil-stock connections. The correlation between commodities prices and stock market performance was studied using the DCC GARCH model (Nakhli et al., 2025). The results demonstrated an impartially significant and volatile relationship. Using co-integration, the findings depicted a correlation between the price of crude oil and the Indian stock market index (Sharma & Shrivastava, 2024). Many other studies Kumar et al. (2023); Dutta et al. (2019) and Benkraiem et al. (2018) also observed strong correlations between oil and stock prices.

Several economic determinants and business finance management policies are negatively influenced by economic policy uncertainty, according to the current literature (Al-Thaqeb & Algharabali, 2019; Xu et al. 2021). However, recent research in the literature has shown that the impacts of the EPU index on many elements and policies are not uniform. The problem with EPU’s asymmetrical impact is that it adds complexity by making its effects less predictable and may depend on other variables or the positioning of marketplaces (Lee et al., 2024). A sizable increase in uncertainty has a detrimental effect on economic activity, and the economy may take considerable time to recover, whereas a substantial decrease in uncertainty has no direct effect on economic activity (Zhong et al., 2025). Moreover, moderate shifts in either direction have negligible if any impact on economic activity (Xu et al., 2021). Using quantile regression, the study examined the effects of geopolitical and economic policy uncertainty on the Asian emergent stock market (Kannadhasan & Das, 2020). The findings show that geopolitical uncertainty only impacts lower quantiles, and EPU has a negative effect on stock returns. Iyke and Maheepala (2022) examined how COVID-19 affects the unpredictability of economic policies in Asian economies. The empirical findings demonstrate that COVID-19 has a positive effect on China’s and Korea’s economic policy uncertainty. Further, it was discovered that during the crisis, stock returns were more unpredictable. Additionally, numerous studies demonstrate how various uncertainty indices affect volatility and stock market returns (Carnahan & Saiegh 2025; Ghani & Ghani 2024; Phan et al., 2021; Zhao & Park 2024). The overall results indicate a greater degree of dependency and a more significant effect of economic policy uncertainty on the economy.

Research Methodology

Data Specification

This study uses monthly data on oil prices, economic policy uncertainty, and equity markets index from the period January 2005 to December 2022. The data on equity market returns for this study is sourced from the KSE-100 index for Pakistan, DSEX Composite for Bangladesh, JKSE Composite for Indonesia, KOSPI Composite for South Korea, EGX-30 index for Egypt, BIST-100 for Turkey, VN-30 index for Vietnam, PSEI Composite for the Philippines, NSE-30 index for Nigeria, and S&P for Mexico. However, Iran has been excluded from the sample due to economic and fiscal sanctions that it is exposed to. The oil price change is measured through Brent and the impact of economic policy uncertainty is captured using a monthly index of global economic policy uncertainty. The primary sources of data are the World Bank database and Yahoo Finance.

Model Specification

Both ARDL and non-linear ARDL models are employed in this research to examine hidden co-integration. The linear ARDL approach has been empirically tested in the first phase of this study to analyze the impact of oil prices on the market returns of N11 countries with the presence of a moderating role of EPU. The ARDL model is flexible as it can handle a mix of stationary and non-stationary variables, but the key point is that none of the variables should be I(2) or higher. ARDL model does not restrict its use if all variables are I(0) or I(1) (Pesaran et al., 2001). In the second phase of this study, the Nonlinear ARDL model is used to analyze the asymmetric impact of oil price variables on the market returns. NARDL helps to avoid spurious regression risks when variables are stationary or co-integrated and it further allows to inclusion of only specific lags, which makes it preferable to which VAR includes lags of all variables. Another justification for employing the non-linear ARDL model is that stock prices respond more rapidly to negative news in contrast to positive news. The NARDL model captures asymmetric cointegration in the long run and short run and it does not necessarily examine the nonlinear integration of individual series. Hence, employing both of these approaches is crucial to identify whether the research findings change when the NARDL model has been considered.

The representation of the ARDL equation is as follows:

The short-run relationship is explored by using ECM as mentioned below:

Where:

L with each variable shows that all variables are in the natural logarithm, t indicates time, i indicates lag order and µ indicates relevant error terms.

I indicate stock index.

Summation signs indicate error correction dynamics where the variables are employed with first difference.

OP indicates oil prices in $.

EPU indicates global economic policy uncertainty.

ΔI = Change in stock index.

ΔOP = Change in oil prices in $.

ΔEPU = Change in economic policy uncertainty.

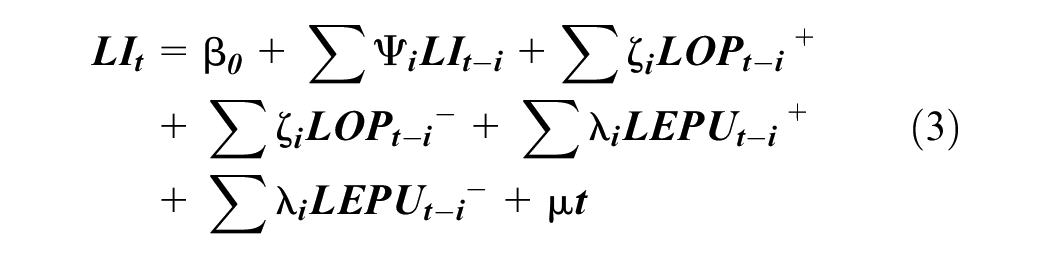

The asymmetric relationship between oil prices and equity market returns both in the long-term and short-run is presented below:

The role of moderator between oil prices and equity market returns both in the long-term and short-run is presented below:

Results and Discussion

Unit Root Analysis

Table 1 depicts the unit root test results of N11 countries to identify the order of integration for the variables under study. The reporting of data is portrayed in log form for coefficients’ smoothing. The Phillip-Perron testing is employed at a level as well as at 1st difference with the constant assumption for unit root testing. The findings reveal that all of the time series are non-stationary at a level that turns out to be stationary at 1st difference. ARDL model does not restrict its use if all variables are I(0)or I(1) (Pesaran et al., 1999, 2001). As variables are I(1), so there were two choices, either to use regression analysis on stationary series or cointegration analysis on non-stationary series. Regression analysis does not capture long-run co-movement whereas Cointegration analysis by Johanson and Jusilius (1991) approach does not capture asymmetric relationships.

Unit Root Analysis N11 Equity Markets.

Diagnostic Testing

The results shown in Table 2 report diagnostic testing information of N11 equity markets and report no autocorrelation issue. Further, the Ramsey test reveals that no problem with model specification is present. Mostly, normal distribution is not observed in the time series data. As times-series data encompass combinations of multiple integration orders; thus, heteroscedasticity presence does not affect estimates and it can be detected naturally (Shrestha & Chowdhury, 2005).

Diagnostic Test N11 Equity Markets.

ARDL Bounds Test

Table 3 depicts the information about the results of the ARDL bounds test of N11. The reported results of the bounds test indicate that variables are either I(0) or I(1) because the presence of any I(2) variables will violate the ARDL model making the computed F-stat invalid (Pesaran et al., 2001). Table 3 reveals both lower and upper limits for a 95% level of confidence interval as our model is based on such a confidence interval. In the case of Pakistan, Indonesia, Nigeria, and the Philippines, the long-term relationship is inconclusive or cannot be identified because the F-stat value of these four countries is higher than the lower bound of 2.32 but lower than the upper bound of 3.5. On the other hand, the F-stat value of Bangladesh, Turkey, Vietnam, South Korea, Mexico, and Egypt is more than the 3.5 upper bound concluding the existence of long-term co-integration in the variables. NARDL’s bounds testing for cointegration is robust to linear non-stationarity (variables being I(0)/I(1)), so standard tests are often sufficient for initial analysis (Shin et al., 2014).

ARDL Bounds Test N11 Equity Markets.

ARDL Model

Table 4 shows the short-term dynamic relationship between the oil prices and the equity returns of N11 stock markets. ECM (−1) demonstrates the speed of adjustment of one period from a long-term disequilibrium. The error correction model shows the magnitude to which the elimination of exogenous shock and correction of the short-term imbalance has occurred in the long run. Rationally, the value of ECM must be negative and significant. Hence, in the case of N11 countries, the same can be observed in the results of ECM except for Pakistan and the Philippines which have negative and statistically insignificant values indicating no adjustment in rectification of disequilibrium in the long run. However, the coefficients of the ECM term of the rest of the countries are significant and negative indicating a prompt adjustment from the disequilibrium route. As far as Bangladesh is concerned, the ECT coefficient indicates that 7% of price disequilibrium is rectified from its last month’s disequilibrium route. Likewise, from the previous period, a 10% adjustment in the stock prices of the Indonesian stock market has occurred to recover from price disequilibrium. Similarly, results of the ECT coefficient of Turkey, Vietnam, South Korea, Mexico, Nigeria, and Egypt show quick adjustment of stock prices towards the equilibrium path in the current month. The ECM depicts that oil prices have a statistically significant impact on the equity returns of Pakistan, Bangladesh, Indonesia, Turkey, Vietnam, South Korea, and Mexico in the short term.

ARDL Error Correction Model for Short Run Relationship N11 Equity Markets.

1% significance level, **5% significance level.

Table 5 shows that oil prices have a statistically significant and positive relationship with the equity market of Vietnam only in the long run. However, oil prices hold an insignificant impact on the remaining N11 equity markets. It demonstrates that the following equity markets follow independent walk in the long-term and their stock prices cannot be predicted by analyzing the behavior of change in oil prices.

ARDL Model for Long Run Relationship N11 Equity Markets.

1% significance level, **5% significance level.

Moderating Role of EPU on the Link Between OP and N11 Equity Markets

Table 6 shows the short-term dynamic relationship between the oil prices and the equity returns of N11 in the presence of the moderating role of economic policy uncertainty. There exists a negative and significant relationship at first lag between oil prices and the stock returns of the KSE-100 index that reverses into lag 2 with a significant effect on the returns of stock. The coefficient of interaction term is also positive and significant showing the EPU has magnified the relationship between OP and equity returns. Conversely, in the case of South Korea, Mexico, Nigeria, and Egypt, oil prices have positive and significant effects but the coefficient of interaction term is negative and significant showing the EPU weakens the relationship between OP and equity returns translating the opposite effect. Contrarily, in the case of Bangladesh, Indonesia, Turkey, Vietnam, and the Philippines the results of the interaction term are insignificant which means EPU does not play a moderating role between oil prices and returns of equity in the short run.

Moderating Role of EPU on the Short Run Link Between OP and N11 Equity Markets.

1% significance level, **5% significance level.

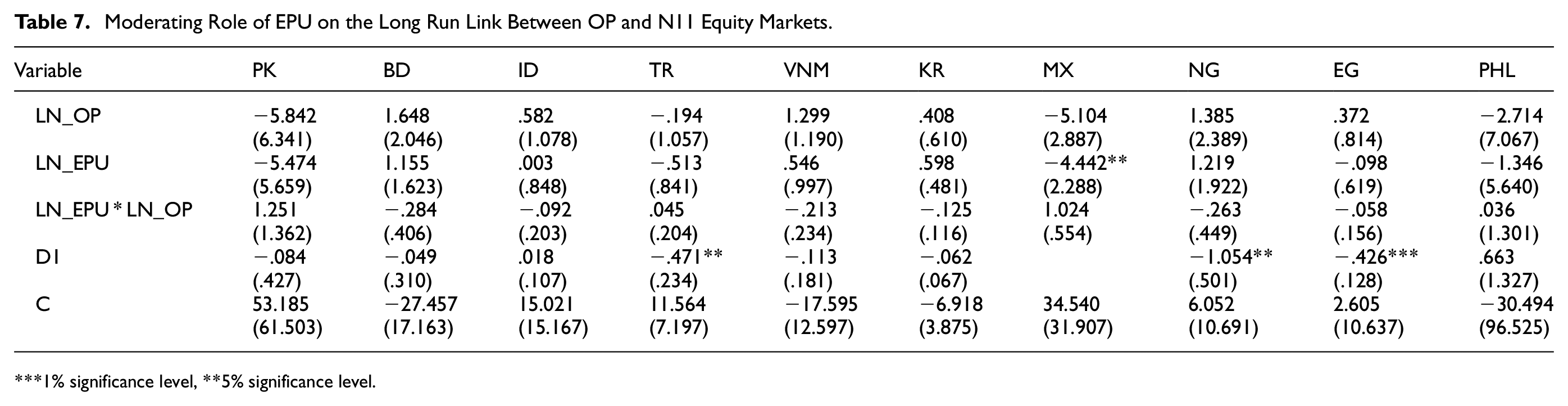

Table 7 shows that EPU does not have any statistically significant influence on the relationship between oil prices and stock returns of the N11 equity markets in the long run. It reveals that the N11 equity markets depict independent behavior in the long-term and their stock prices are not influenced by increases or decreases in economic uncertainty along with subsequent fluctuations in the oil prices.

Moderating Role of EPU on the Long Run Link Between OP and N11 Equity Markets.

1% significance level, **5% significance level.

NARDL Representation N11 Equity Markets

Asymmetric Impact of OP on N11 Equity Returns

Table 8 shows the short-run asymmetric impacts of oil prices and EPU on the stock returns of N11 countries. The coefficient reflecting the positive shock in the OP is statistically insignificant and positive showing no impact of a 1% upturn in oil prices on the stock returns of the KSE index in the short term. However, the coefficient revealing a negative shift in the oil prices is also negative and significant and a similar effect remains persistent on the stock returns even after 2 periods. The coefficient associated with the positive shock in the OP is negative and statistically significant after 2 lags indicating a .23% decline in the stock returns due to a 1% increase in the oil prices. However, a negative shock in the OP is associated with the negative trend in the stock returns as the coefficient is also negative and significant after 3 months.

Asymmetric Impact of OP on N11 Equity Returns in Short Run.

1% significance level, **5% significance level.

Also, the coefficient associated with the positive shock in the OP is statistically insignificant and positive showing no impact of the increase in oil prices on the stock returns of the equity market of Indonesia in the short term. Similar results can be seen in the case of Turkey, South Korea, Mexico, and Egypt in which an increase in OP creates no influence on the stock returns in the short-run. The decrease in oil prices has a significant and negative impact and will reduce the equity returns of the Indonesian stock market by .13% and by .18% in the Turkish equity market. In Vietnam, the coefficient reflecting the positive shock in the OP is positive and statistically significant indicating a .09% increase in the stock returns due to a 1% increase in the oil prices. The decrease in oil prices has a significant and negative impact on the stock returns causing a .27% decline in the current month which is then reversed in the subsequent month. The decrease in oil prices has a significant and positive impact on the stock returns causing a .07% increase in the stock returns of the KOSPI index. Hence, it is demonstrated that stock returns of N11 equity markets have an asymmetric relationship with the oil prices in the short-run and these results are aligned with the findings of(Chang & Rajput, 2018).

Table 9 shows the long-run asymmetric impacts of oil prices on the N11 equity markets. In Pakistan, Indonesia, Turkey, South Korea, Mexico, Nigeria, Egypt, and the Philippines, both coefficients representing positive and negative shocks in the oil prices are insignificant. It means no asymmetric relationship is present amid variables in the long run and the impact on equity markets of such countries is inconclusive in the long-term. In Bangladesh, the coefficient linked to positive shocks in oil prices is insignificant and negative, while the coefficient depicting negative change in OP is positive and significant. Hence, it can be demonstrated that in Bangladesh, a non-linear association exists among variables in the long run. In Vietnam, both coefficients representing positive and negative shocks in the oil prices are significant and positive. Thus, this unequal magnitude reveals the presence of a long-term asymmetric relationship amid variables of interest in Vietnam.

Asymmetric Impact of OP on N11 Equity Markets in Long Run.

1% significance level, **5% significance Level.

Discussion

Considering the estimation findings presented in the above section, the ECM depicts that oil prices have a statistically significant impact on the equity returns of Pakistan, Bangladesh, Indonesia, Turkey, Vietnam, South Korea, and Mexico in the short term. Other than Vietnam, the N11 equity markets have not been significantly impacted by fluctuations in oil prices in the long run. It demonstrates that the following equity markets have independent long-term trends, and it is impossible to predict their stock prices by analyzing the behavior of changes in oil prices. In the short run, EPU has the opposite effect by weakening the relationship between OP and equity returns in South Korea, Mexico, Nigeria, and Egypt. Based on the behavioral finance perspective, economic policy uncertainty can change investor decision-making dynamics, affecting market reactions. Depending on how much of the uncertainty has already been factored into the equity market, investors and other stakeholders may either overreact or underreact during periods of economic uncertainty. When new information becomes available in the financial markets, many investors opt for a “wait and see” approach rather than panic decision-making and instead wait for stability. Consequently, the link between EPU and stock markets weakens, leading to a diminishing effect of oil prices on stock returns. Long-term relationships between oil prices and stock returns of the N11 equity markets have not been statistically significantly influenced by EPU. It demonstrates that movements in oil prices that adhere to changes in economic uncertainty have no impact on stock prices. The findings of our study are consistent with the results of (Xu et al., 2021). In the NARDL model, each variable has a positive and negative sign, indicating that it has been decomposed into both positive and negative shocks. The asymmetric effect of these variables on stock returns is demonstrated by these negative and positive change variables. The findings of the NARDL model depict that stock returns of N11 equity markets have an asymmetric relationship with the oil prices in the short run and these results are aligned with the findings of (Dutta et al., 2019) and (Kumar et al., 2023). However, in the long run, both the positive and negative coefficients indicating oil price shocks are insignificant in Pakistan, Indonesia, Turkey, South Korea, Mexico, Nigeria, Egypt, and the Philippines. It indicates that there is no long-term asymmetry link among the variables and that the long-term effects on the equity markets of these countries are inconclusive.

Conclusion

Most of these previous studies focus on studying the asymmetric impact of oil prices on the equity markets of developed economies, with few studies conducted on the equity markets of frontier and emerging economies. It was crucial to research N11 countries that have sustainable economic development potential in the future. The current research serves the purpose of exploring the asymmetric impact of oil prices on the equity returns of N11 stock markets both in the short run and long run. It also investigates the moderating role of Economic Policy Uncertainty (EPU) on the equity markets of N11 countries, specifically with oil prices, given their significant global interdependence. This study uses monthly data on oil prices, economic policy uncertainty, and equity markets index from January 2005 to December 2022. Both ARDL and non-linear ARDL models are employed in this research to examine hidden co-integration.

Findings from the linear ARDL model depict that only in Vietnam’s equity market, do oil prices hold a significant positive impact in the long run. However, oil prices have a statistically significant impact on the equity returns of Pakistan, Bangladesh, Indonesia, Turkey, South Korea, and Mexico in the short run. Furthermore, the moderating role of economic policy uncertainty on the relationship between oil prices and equity returns of N11 stock markets is insignificant in the long run revealing that stock prices are not influenced by an increase or decrease in economic uncertainty along with subsequent fluctuations in the oil prices. However, in the short run, this effect is magnified in the case of Pakistan but weakened in the equity markets of South Korea, Mexico, Nigeria, and Egypt. The results of the NARDL model indicate that there is no asymmetric impact of oil prices on the stock returns of KSE, JSE, BIST, KOSPI, S&P, EGX-30, and PSEI in the short term. The asymmetric relationship between N11 stock markets and oil prices is inconclusive in the long term excluding Vietnam.

This study holds major implications for various stakeholders of the N11 equity markets, such as investors and portfolio managers. It provides valuable insights for investors since it allows them to strategically rebuild their portfolios and distribute risk in response to the impact of uncertainty. Furthermore, market participants and portfolio managers must recognize and adapt to changes in economic policy uncertainty (EPU) since it can significantly impact stock returns in both the short and long term. Therefore, they should carefully monitor the shifts in economic policy uncertainty and adjust their portfolios accordingly.

Direction for Future Research

The asymmetric association indicates that extensive research in this particular domain needs to be conducted as the selected N11 countries report an asymmetric impact of oil prices on stock markets. Further, more indicators should be incorporated to generalize the results. Lastly, a comparative analysis needs to be conducted for frontier and developed economies to analyze the behavior of macroeconomic indicators on the stock markets of such countries.

Footnotes

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data will be available upon request.