Abstract

This study examines the impact of financial innovation on economic growth in Vietnam, using panel data analysis during 2010 to 2020 in both the whole country level and regional level. Financial innovation measurements include financial institutions innovation and financial markets innovation which are constructed based on two core sectors of the financial system. For the whole country level, the results from the difference-GMM method indicate that financial institutions innovation positively impacts economic growth in Vietnam. Meanwhile, the negative influence of financial markets innovation on economic growth is pointed out in the study. For six regions of Vietnam, the similar results as the country in five regions are documented except the Central Highlands region which shows that financial institutions innovation non-significantly influences its regional growth. Findings from this research elicit significant policies that recognize financial innovation as a crucial driver to boost economic growth in Vietnam and foster economic regions.

Plain language summary

Background of the research: In the context of transition countries, the paucity of research on the linkage between financial innovation and economic growth contrasts sharply with the abundant studies in developed or developing countries. In the case of a transitional country - Vietnam, this topic has been left open. Also, a large cohort of literatures tend to focus on group countries or individual countries using national aggregated data while the effects of financial innovation on economic growth at the disaggregated level are interesting. Aims and purpose of the research: To examine the effect of financial innovation on economic growth in a transition country, using Vietnam as a case study in both the whole country level and regional level. Financial innovation in this research is captured comprehensively via two core sectors of the financial system including financial institutions innovation in financial markets innovation. Methods and research design: This paper labors a panel data of 63 provinces in Vietnam over the period of 2010-2020 to examine the effect of financial innovation on economic growth in the whole country level and also divides 63 provinces into 6 regions to estimate this nexus in the regional level. Difference-GMM method is used to analyse empirical results and system-GMM technique is labored to test the robustness. Results and importance: This study documents that increasing financial institutions innovation could enhance economic growth in Vietnam while financial markets innovation might mitigate it. In six regions, similar results as the whole country in 5 regions are presented except the Central Highlands region which shows non-significant results of the effect of financial institutions innovation on its regional growth. Findings from this research elicit significant policies for laboring financial innovation as an impulse to boost economic growth in Vietnam and foster economic regions.

Keywords

Introduction

The importance of financial innovation as a vital driver for the economy of each country has been broadly recognized. Financial innovation shows positive influence on economic growth through enhancing capital accumulation, facilitating financial transactions, mitigating cost and risk (Naeem et al., 2023; Oyadeyi, 2024). In addition, by creating equity and credit resources through instruments and diversifying investment portfolios, financial innovation can generate more national capital resources and enhance economic growth (Agarwal & Zhang, 2020; Luong et al., 2024). However, the negative impact of financial innovation on countries’ economic growth is also addressed. Financial innovation can increase complexity due to new but insufficient financial products which results in a bubble in the financial system and accelerates the vulnerability and fragility of markets. This will probably lead to a financial crisis and reduce economic growth (Allen, 2012; Bernier & Plouffe, 2019). Consequently, the relation between financial innovation and economic growth remains ambiguous as well as possibly showing different linkages in specific countries.

In the scope of transition economies, the paucity of research on financial innovation-growth linkage contrasts sharply with the abundant studies in advanced and emerging countries. Meanwhile, transition countries’ specific characteristics in terms of geography, politics, and economic system offer noteworthy and unique experiments in conducting research. Transition countries are located in important geopolitical areas in Europe and Asia (IMF, 2000) and these countries experienced the process of political transformation related to changing governments’ regime (Ishiyama, 1995). In terms of economical perspective, transition countries changed their economic system from government-based to market-based economies that provide favorable conditions for the engagement of the private sector in economic activities (Beck & Laeven, 2006).

As a transition country, Vietnam experienced a period of reforming the economic system. Considered as the main driver for economic development, the financial system of Vietnam has strong transformative steps in order to function business activities. With the background of a mono-tier banking system with bank credits limited to channel capital for state enterprises, the financial system of Vietnam now is having the engagement of a variety of forms of financial institutions such as commercial banks, finance companies, credit funds, insurance companies, venture capital companies in order to enrich the investment and facilitate the activities of the national private sector (Anwar & Nguyen, 2009; Leung, 2009). Besides, Vietnam has improved the characteristics of weak legal and policy infrastructures to develop the stock and bond markets which approach the global financial system standards (Leung, 2009; Ministry of Finance, 2023). Therefore, it is essential to examine whether economic growth in Vietnam is impacted by innovation in the financial system.

Regarding empirical research on the influence of financial innovation on economic growth, there exists a large cohort of literatures tend to focus on group countries (Luong et al., 2024; Domeher et al., 2022; Naeem et al., 2023) or individual countries using national aggregated data (Nazir et al., 2021; Oyadeyi, 2024; Satia & Okle, 2020). Meanwhile, focusing on this linkage at a disaggregated level are interesting. Since provinces in a country are more homogeneous in socio-economic characteristics, governance capacity and the background of the financial system, employing provincial data to observe the impact of financial innovation on national economic growth and regional growth is more relevant. Also, in the case of a transition country - Vietnam, this topic has been left open and that would be pioneer research which assesses whether financial innovation affects the economic growth in Vietnam using data from provincial units. In addition, after the country’s reunification in 1975, Vietnam has consistently adopted the socialist development model throughout the provinces and regions system in the whole country from the North to the South. However, each region has its own socio-economic characteristics and there still exists the disparity in the economic development among regions.

Therefore, the study will fulfill the limitations of previous research and contribute to current literature in three main points. By examining the case of a transition country as Vietnam, this paper plays a role in analysing the impact of financial innovation on national economic growth in Vietnam at the whole country level using the provincial data. Besides, we extend to observe how financial innovation affects regional growth in different regions in Vietnam. Additionally, this research captures financial innovation in two core aspects consisting of financial institutions innovation and financial markets innovation. Accordingly, this study has the objective of investigating the impact of financial innovation on economic growth in Vietnam at the whole country level and regional level using panel data analysis of 63 provinces during 2010 to 2020. By utilizing the difference-GMM method, the study documented major findings that financial institutions innovation positively impacts economic growth in Vietnam while there exists the negative influence of financial markets innovation. Regarding the regional level, similar results are found in five regions apart from the Central Highlands. This evidence reveals impactful policies that prioritize innovation in the financial system to stimulate Vietnam’s economic growth.

Following this introduction, the remainder of this study is structured in four sections. The conceptual framework, theoretical and empirical literature in the field is presented in section 2. Section 3 mentions data and methodology, section 4 shows empirical results and discussion, and followed by the conclusions in section 5.

Literature Review

Financial innovation has been observed as a phenomenon which plays an essential role in financial development and economic development (Frame and White, 2012; Goetzmann & Rouwenhorst, 2005; Tufano, 2003). Conceptually, the financial innovation and economic growth linkage in previous literature is interpreted in both positive and negative channels. On strand of the literature shows positive effects of financial institutions innovation which can increase economic growth through lowering financial transactions’ cost and facilitating it to be more convenient. That not only functions business activities but also fosters the mobilizing saving and generating wider access to credit resources in order to reach a higher economic growth (Agarwal & Zhang, 2020; Carbó Valverde et al., 2007). Additionally, financial innovation in other institutions such as insurance companies, venture capital, mutual funds can offer a variety of hedging from risk and investment choices to diversify portfolios (Apergis & Poufinas, 2020). Also, the advent of various new types of equity and debt securities presents financial innovations in financial markets that enrich the capital market and make financial markets more complete (Tufano, 2003). Hence, activities in the economy reach a higher value of produced outcome, enhancing economic growth. Another strand of research pointed out detrimental influences of financial markets innovation on economic growth. Securitization loans and subprime securitization are considered financial markets innovation which lowered lending standards and the effort on monitoring loans (Beck et al., 2016). That leads to financial markets’ volatility and complexity, possibly resulting in financial crises and affecting activities in other sectors, decreasing economic growth (Gennaioli et al.,2012; Henderson & Pearson, 2011).

Theoretically, Chou (2007) based on the Solow growth theory (Solow, 1956) to demonstrate that financial innovation positively links to economic growth. By generating an extension form of Cobb-Douglas production function, financial innovation connects the saving-investment linkage. The theoretical connection showed how financial innovation channels its impact on economic growth is clarified through observing the capital flow in a paradigm economy including four agents: households, financial innovators, financial intermediaries and firms. Chou (2007) solved the utility and profit maximization functions of each agent at the equilibrium and proved that financial innovation channels its positive impact on economic growth through increasing capital per worker and output per worker that implies continuous increase in financial innovation would boost economic growth at a higher stage.

Empirically, a large cohort of previous literature is mainly analysed on panel data of countries classified as developed and developing. In particular, Bernier and Plouffe (2019) demonstrated that financial innovation positively affects economic growth in 23 OECD advanced economies. Similarly, Naeem et al. (2023) documented this link in 46 high-income nations. These findings are also supported in research of Laeven et al. (2015) and Beck et al. (2016). For developing countries, Domeher et al. (2022) reveals the positive linkage in 26 SSA countries. This paper interprets that financial innovation could reduce cost and risk for financial institutions that enhance financial development and economic growth. This positive relation is also documented in Asian countries (Nazir et al., 2021). In addition, Luong et al. (2024) captured financial innovation in a broad concept and supported the positive influence of financial institutions innovation on economic growth while financial markets innovation documents negative impacts. However, the paper analysed a sample of transition countries and neglected investigating the case study of an individual country.

The majority of research observed a group country while the study in an individual case study is scarce. In Bangladesh, Qamruzzaman and Jianguo (2017) investigates this effect using time series data from 1980 to 2016. By using ARDL bound tests, the research documented positive effects of financial innovation on Bangladesh’s economic growth in Bangladesh at both short run and long run. Nazir et al. (2021) conducted research for China, India and Pakistan during 1970 to 2016 and indicated that there are positive impacts of financial innovation on economic growth in China, India and Pakistan. In Africa, some studies are found in lower-middle-income countries. Adu-Asare Idun and Aboagye (2014) investigates the link of financial innovation and economic growth in Ghana during 1990 to 2009. The results of ARDL bound tests show that financial innovation has a positive effect on economic growth in Ghana in the short run but it will be negative in the long run. Similarly, positive impacts of financial innovation are also demonstrated in research on Zimbabwe (Bara & Mudzingiri, 2016) and Camerron (Satia & Okle, 2020).

Besides, empirical works which focus on national economic growth in the level of each region or province are extremely scarce. Carbó Valverde et al. (2007) observed this link in 17 regions of Spain from 1986 to 2001 and found that financial innovation drives positive influences on gross products of each region, investment and the growth of gross savings. Wang et al. (2022) examined this effect in China from 2011 to 2019 using data provincial data and demonstrated the important role of financial innovation in accelerating regional growth in 31 provinces.

Accordingly, there are quite limited empirical studies observing the impact of financial innovation on national economic growth utilizing provincial units’ data in an individual country and limited in Vietnam for a transition country. Also, previous studies only focus on financial innovation in some aspects such as bank credit, the broad money (M1) to narrow money (M2) ratio. Therefore, this study aims at analyzing the impact of financial innovation on Vietnam’s economic growth at the country level and regional level employing data from provincial units and observing financial innovation in a broader concept of the financial system’s structure.

Methodology

Data and Variables Measurement

This paper labors a panel data of 63 provinces in Vietnam over the period of 2010 to 2020. The list of these provinces is mentioned in the Appendix. Following the categorizing of the Government’s Resolution No.138/NQ-CP, this study divided 63 provinces into six socio-economic zones or six regions in Vietnam including the Northern midlands and mountainous region, the Red river delta region, the North central and Coastal, the Central Highlands, the Southeast region and the Mekong Delta region.

The study utilizes the real Gross Provincial Product per capita (GPP per capita) to measure economic growth in Vietnam and this variable serves as a widely adopted measurement in previous research on economic growth (Bara & Mudzingiri, 2016; Bernier & Plouffe, 2019; Qamruzzaman & Jianguo, 2017). For financial innovation measurement, previous studies used proxy variables such as M2/M1, banking sector credit, and private credit to GDP (Beck et al., 2016; Bernier & Plouffe, 2019; Laeven et al., 2015) which only capture general aspects and do not present specific innovation characteristics whether financial innovation comes from banking or capital market sector. Therefore, this research will address this limitation by capturing core sectors of the financial system perspective encompassing financial institutions innovation and financial markets innovation (see Table 1). For financial institutions innovation, ATMs and POS terminals present services, process, technology innovation which functions financial transactions, mitigating costs, increasing liquidity and generating credit and equity resources. Financial markets innovation is measured by stock and securities participation which presents the adoption of new products or instruments into society. We collected these data from three main sources including Censuses of the General Statistics Office of Vietnam, Provincial Statistical Yearbook, and annual statistics of The State Bank of Vietnam in provincial branches.

Data Description.

Source. Authors.

For control variable, based on the framework of Barro and Sala-i-Martin (2003), we added four macroeconomic factors as control variables consisting of inflation rate, labor force, foreign direct investment and urban population. These variables are selected depending on the availability of data sources in provincial units.

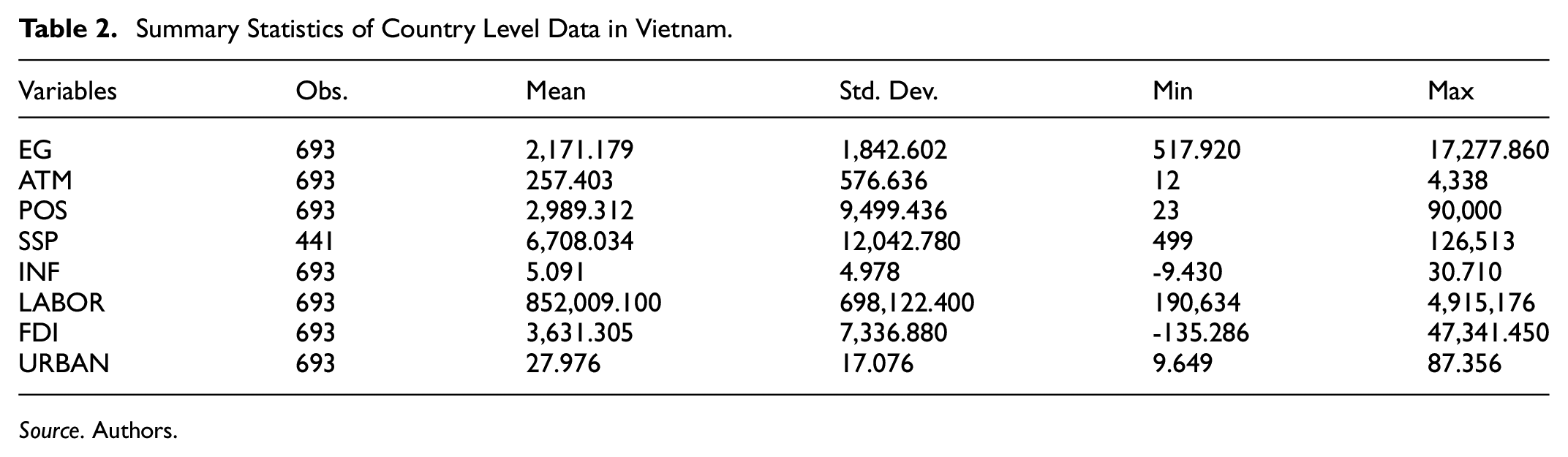

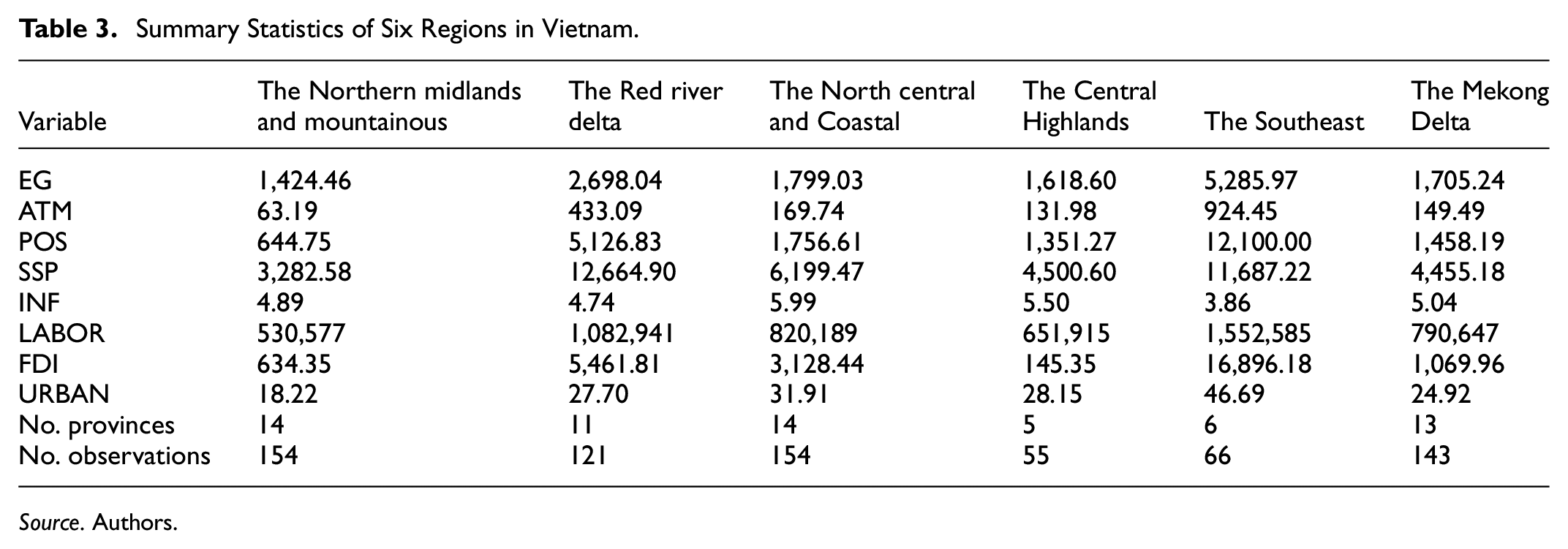

Table 1 describes the data description and Tables 2 and 3 exhibit the summary statistics of variables in the whole country and provincial level respectively.

Summary Statistics of Country Level Data in Vietnam.

Source. Authors.

Summary Statistics of Six Regions in Vietnam.

Source. Authors.

From the summary statistics in Tables 2 and 3, it shows different level of financial innovation and economic structure according to different regions. For the Northern midlands and mountainous region, this region is considered as the poorest region with the lowest average GPP per capita and financial innovation level compared to other regions. This is due to the region’s geographic structure that is mainly a mountainous and hilly area. For the Red river delta region, this is considered as the center in terms of the political and cultural of the country, with having Hanoi as the capital. The average GPP per capita and financial innovation level, this region is considered as the second-highest compared to other regions. For the North Central and coastal region connected to the North-South trade corridors and international trading and this region has the medium level in GPP per capita and financial innovations level compared to other regions. The Central Highlands region located in the border intersection of other ASEAN and its terrain is mainly dangerous mountains that reduce potential opportunities for economic development. As the second-poorest region, GPP per capita and financial innovations level in this region are the second-lowest level compared to other regions. The Southeast region located on national and international traffic routes with many gateways by land, railway, river, sea and air. As the financial center of the country, the Southeast region has the highest level of GPP per capita and financial innovations compared to other regions. The Mekong Delta region is located along the Southern economic corridor and this region is the country’s leading center for rice production, farming, fishing and seafood processing. The level of GPP per capita and financial innovations in this region are ranked as the medium level compared to other regions.

Empirical Model

This research constructs the empirical model as follows:

where: i is each province (1, …, 63); t denotes the period of time period (1, …, 11);

Regarding control variable, is inflation rate,

This study applies the difference-Generalized-Method-of Moments (GMM) techniques to estimate the empirical results in order to control endogenous problems in regressions. We tested the panel unit root and the results confirm the stationary property of all variables. We also use the system-GMM estimation for the robustness tests, confirming consistent results compared to the difference-GMM. These methods are appropriate for dynamic panel estimations, providing robust and consistent empirical results (Arellano & Bond, 1991; Arellano & Bover, 1995; Roodman, 2009).

Empirical Results

Financial Innovation and Economic Growth in Vietnam

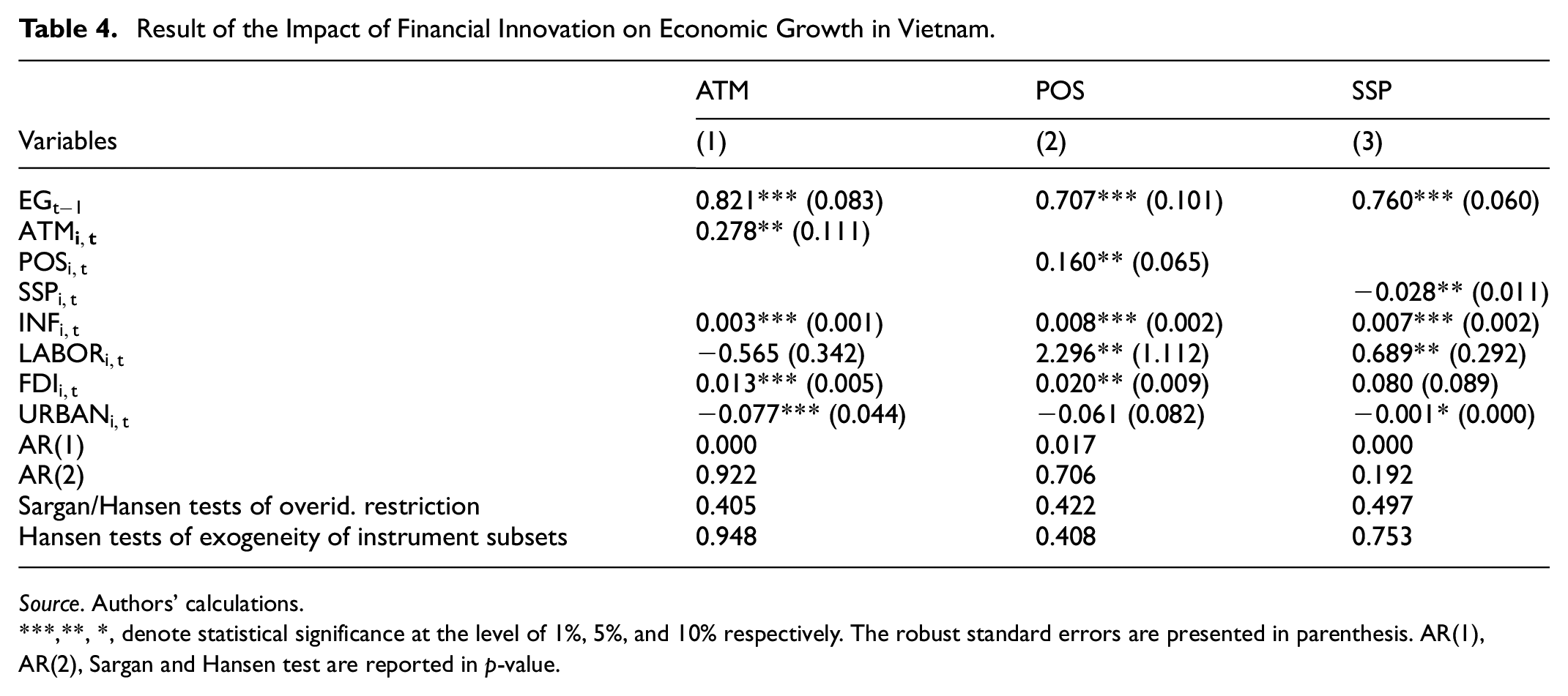

Table 4 below presents the results of financial innovation indicators. Column (1), (2), and (3) show the impact of financial innovation measured by ATMs usage numbers (ATM), POS terminals numbers (POS) and stock and securities participation (SSP), respectively.

Result of the Impact of Financial Innovation on Economic Growth in Vietnam.

Source. Authors’ calculations.

,**, *, denote statistical significance at the level of 1%, 5%, and 10% respectively. The robust standard errors are presented in parenthesis. AR(1), AR(2), Sargan and Hansen test are reported in p-value.

Column (1) and (2) show that financial institutions innovation have positive influences on economic growth in Vietnam and the findings are statistically significant and consistent with the expectation (Bara et al., 2016; Satia & Okle, 2020). An increase in the number of ATMs can serve customers basic services and this can facilitate banking services especially in rural areas with difficult financial access and increase more financial transfer which encourages economic growth in the country (Ogbuji et al., 2012). Besides, the operation of ATMs could help to process financial transactions conveniently. Also, more technology innovation via ATMs which combine more banking functions into machines and communicating with users by screen-touch and face-to-face teller would encourage using banking systems more convenience and thus supporting more business activities and individuals’ demand and accelerating economic growth. This positive effect of ATMs on Vietnam’s economic growth is consistent with Kazakhstan - a transition economy in the Commonwealth of Independent States (Kireyeva et al., 2021) and Botswana as a developing country (Motsatsi, 2016).

For the effect of POS terminals numbers (POS), this indicator presents a significant positive impact on economic growth in Vietnam, as a higher number of POS terminals will result in greater economic growth. Hasan et al. (2013) stated that the introduction and expansion of POS terminals improve payment processes by offering payment methods for users such as debit cards, credit cards and QR-code that reduces cash in transactions and increases capital flow, encouraging consumption and increasing economic growth in European countries, hence these channels might be applied to explain for case study of developing countries as Vietnam. A wider network of POS terminals also provides more convenience to supervise sale activities, facilitating business activities effectively. Generally, this financial innovation functions in cost-reducing and liquidity-enhancing that can increase economic growth (Umar et al., 2021) and the finding in this study is similar to other countries such as Nigeria and Botswana which have relatively higher level of Fintech and financial innovation compared to Vietnam (Anifowose & Ekperiware, 2022; Motsatsi, 2016).

The impact of financial markets innovation on national economic growth is presented in column (3). The result shows that financial markets innovation measured by stock and securities participation (SSP) negatively affects economic growth in Vietnam. Though stock and bond markets can encourage economic growth (Bencivenga & Smith, 1991; Levine, 1991; Levine & Zervos, 1996; Thumrongvit et al., 2013), it also depends on the capacity of the financial markets in each country. The stock and bond markets in Vietnam were established in 2000 and 2009 respectively under a background of a low-income economy. Hence, the financial markets of Vietnam are considered as an underdeveloped market in which the stock market has a significant number of speculative trading while bond markets are less efficient. Moreover, financial markets in Vietnam do not have a robust legal system as well as financial markets’ infrastructure. In these situations, more new financial innovation in the financial market could generate complexity and fragility and distort investments, simulating higher system risks and this can possibly have negative impacts on national economic growth. These findings are also documented in previous studies (Beck et al., 2016; Qamruzzaman & Jianguo, 2018; Satia & Okle, 2020).

Table 4 also indicates variables’ results including the lagged of gross provincial product (

The result of autocorrelation test including AR(1) and AR(2) and the Hansen test present equations have no autocorrelation and instruments used in the model are appropriate. That demonstrated the results measured by the first difference-GMM are sufficiently estimated.

Financial Innovation and Economic Growth in Different Regions in Vietnam

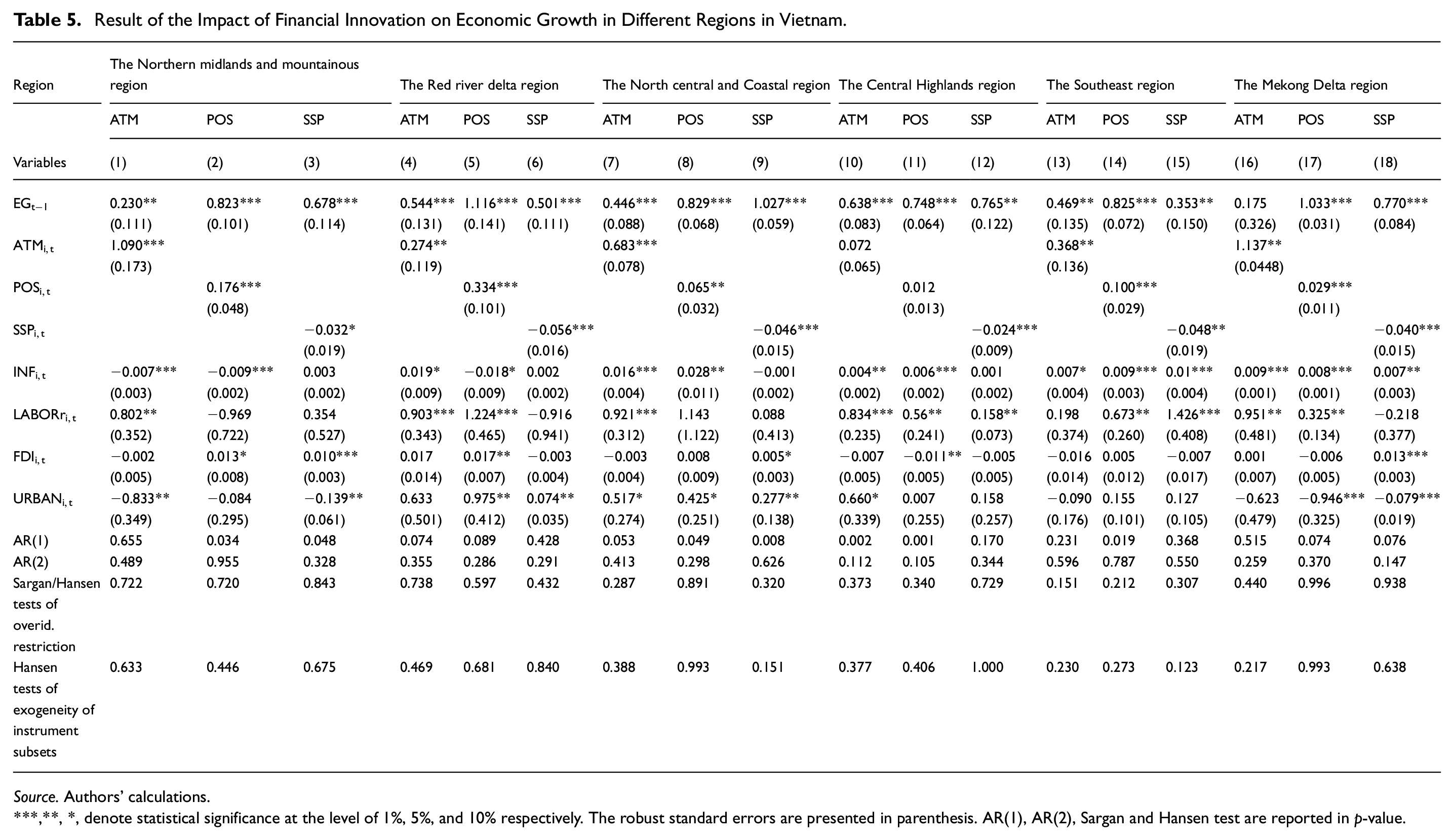

Table 5 shows the impacts of financial innovation on regional economic growth of six regions including the Northern midlands and mountainous, the Red river delta, the North central and Coastal, the Central Highlands, the Southeast and the Mekong Delta.

Result of the Impact of Financial Innovation on Economic Growth in Different Regions in Vietnam.

Source. Authors’ calculations.

,**, *, denote statistical significance at the level of 1%, 5%, and 10% respectively. The robust standard errors are presented in parenthesis. AR(1), AR(2), Sargan and Hansen test are reported in p-value.

For the impact of financial institutions innovation, almost 5 regions show similar findings with the whole country level that financial innovation positively affects regional growth. The Northern midlands and mountainous region is classified as the poorest region in economic development and the lowest in the level of ATMs and POS terminals. Positive impacts of financial institutions innovation shown in column (1) and (2) presents by enhancing more ATMs and POS terminals in the area that has low access and innovation can help to improve accessing the financial services and products of this region. Thereby, households and businesses can have credit funding for their activities and thus increase the average GPP per capita of the Northern midlands and mountainous region. Regarding the Red river delta region, positive effects of financial institutions innovation (ATMs and POS) on regional growth shown in column (4) and (5) are documented. This region is the second highest in the level of financial innovation among six regions thus promoting a higher number of ATMs and POS terminals can facilitate business activities and function in credit-generating and capital-generating, producing more output and increasing economic growth in the region. The result in column (7) and (8) highlights the statistically significant positive linkage between financial institutions innovation on regional economic growth in the North central and Coastal region. This region is at the medium level of economic development and financial innovation. Therefore, a higher number of ATMs and POS terminals also results in positive effects of financial institutions innovation on regional growth. Similarly, financial institutions innovation in the Southeast region presents positive impacts on regional growth shown in column (13) and (14). As a financial center of the country, this region shows the highest level of GPP per capita and financial innovation. Hence, adopting a greater number of ATMs and POS terminals still facilitates the working of business and creating a variety of credit resources for regional development, resulting in high positive effects on economic growth. For the Mekong Delta region, results in column (16) and (17) show similar positive signs and statistically significant indicators presenting financial innovation in financial institutions. This region presents the medium level of financial innovation, a higher number of ATMs and POS terminals facilitate business activities, causing a large amount of credit capital has been invested in developing agriculture, promoting production and expanding industries which can increase regional growth (SBV, 2023). Different from the above regions, the Central Highlands region documented no statistical significance of the number of ATMs in column (10) and POS terminals in column (11). The probable explanation is that this region is classified as the second lowest in GPP per capita and financial innovation, the lowest FDI among six regions (see Table 3) together with other difficulties in geography and socio-economic. Besides, low level of technology infrastructure and limited number of business units that hinder adopting financial innovation in terms of technology, such as ATMs and POS terminals. Also, this region has the highest level of ethnic minorities which accounts for 40% of the region’s population and this society mainly does agriculture and this reduces demand for using financial innovation, causing non-significant effects on regional growth.

Regarding financial innovation in financial markets, Table 5 presents the negative effect on regional growth of all six regions in Vietnam, consistent to the whole country level. The negative impact of the Northern midlands and mountainous region shown in column (3) probably is due to the weak background of financial markets in this region including low information technology and high ethnic minorities population who are mainly doing agriculture and low education level (T. A. Nguyen et al., 2021). These conditions limit them to access information of financial markets and limit the operation of stock and securities markets which require educated participants (T. A. N. Nguyen, 2022). Therefore, low information trading can lead to noise trading and volatility in financial markets, negatively affecting regional growth. For the Red river delta region though this region shows highest level of stock and securities participation (see Table 3) and the operation of Hanoi Stock Exchange (HNX) in the region reaches about 30% GDP of the country in 2020 (Ministry of Finance, 2021), however, as an underdeveloped markets, the financial markets in Vietnam still have limitations related to legal and infrastructure systems which have not created a robust background when adopting financial innovations in financial markets, resulting volatility in the HNX and negative impacts on regional growth ( see column (6)) (Beck et al., 2016; Gennaioli et al., 2012). Similar to the whole country level, financial markets innovation in the North central and Coastal and the Central Highlands region still shows a negative effect due to weak background in terms of regulation as well as regions’ financial infrastructure shown in column (9) and (12). Considering the Southeast region, this region has the operation of Ho Chi Minh City Stock Exchange (HOSE) reached about 67.59% of the country’s GDP in 2020 (Ministry of Finance, 2021). However, with the background of an underdeveloped country, financial markets generally face fragility, high short-term trading and high volatility in HOSE when applying complex financial markets innovation showing detrimental influence on regional economic growth (see column (15)). For the Mekong Delta region, because this region has received international project funding which creates a volatility of portfolio investments and due to shortage regulations and legal system of the underdeveloped financial markets background in the country thus simulating negative impacts of financial markets innovation on regional growth shown in column (18).

Table 5 presents significant effects of control variables on regional growth in almost all regression. Generally, inflation, labor force and foreign direct investment positively affect regional economic growth while the negative impact of urban population on regional growth is documented. Besides, AR(1), AR(2) and tests of exogeneity of instruments in all regressions provide evidence supporting the proper specification and estimation.

Conclusion

This research examines the impact of financial innovation on economic growth in Vietnam at the whole country level and regional level from 2010 to 2020 using provincial data. This study employs three indicators to measure financial institutions innovation and financial markets innovation including ATMs usage numbers, POS terminals numbers and stock and securities participation. By using the difference-GMM technique, empirical results provide evidence that financial innovation in financial institutions showing by an increase in ATMs and POS terminals numbers positively affect economic growth in Vietnam at the whole country level, as expected and in line with previous studies. A higher number of these indicators can enhance economic growth in Vietnam through mitigating transaction costs, facilitating financial transactions, increasing the liquidity of capital, and encouraging business activities. The study pointed out the negative influence on national economic growth of financial markets innovation. The background of financial markets in Vietnam is underdeveloped thus adopting more financial markets innovation could result in complexity, speculative trading, and higher fragility that probably lead to crisis, reducing economic outcomes and lowering economic growth.

In the regional level, the positive impact of financial institutions innovation on regional growth is found in five regions, except the Central Highlands region. The Central Highlands region presents no significant effect of financial innovation in terms of technology such as ATMs and POS terminals. This is due to its regional characteristics such as less development in infrastructure, a high proportion of ethnic minorities, low labor force, and lowest FDI and that limits the impact. Financial markets innovation of all six regions shows negative effects on regional growth, similar to the result of the whole country.

The results of this study suggest significant concerns for issuing policies in Vietnam and each region. The study documents positive influences of financial institutions innovation including ATMs and POS terminals. Based on that, these innovations should be considered as motivators in issuing policies to enhance economic growth in Vietnam. As second most developed regions, implementing policies encouraging adopting more ATMs and POS terminals in the Red river delta and the Southeast regions could provide a huge number of credit sources and facilitate business activities of individuals, firms, especially for high skill labor force and urbanization, contributing to enhancing regional growth. Besides, increasing more ATMs and POS terminals in the North central and Coastal region and the Mekong Delta region not only service financial transactions demand of locality but also endow more credit capital for maritime economy, tourism, rice production, and farming in these regions, spurring higher regional growth. In the North midlands and mountainous region, policies aimed to invest in general telecommunications, internet and technology infrastructure in rural areas to facilitate the operation of financial innovations should be more conducted. For the Central Highlands region, it’s necessary to increase investing in technology infrastructure and installing more ATMs, POS terminals as well as promote the benefit from using ATMs and POS terminals to rural households, ethnic minorities and businesses which help to improve the popularity of these innovations to locality, encouraging its impact on the regional economy.

Also, the study raises important concern for policy makers regarding economic growth in Vietnam and six regions negatively impacts of financial markets innovation. Because the scale of financial markets in Vietnam is relatively small and underdeveloped, policy makers should consider sufficient aspects carefully when issuing new policies or adopting new financial innovations to fit with the circumstances. Also, policy makers should construct robust regulation, legal systems and financial infrastructure. That would reduce the uncertainty and encourage capital flow into financial markets. Furthermore, operating two stock exchanges with different regulations under an undeveloped background could generate complexity when adopting financial innovation. Hence, policy makers could merge HNX and HOSE in order to unify the regulations as well as issuing appropriate management policies in financial markets.

Although this study contributes to enrich knowledge of this effect in Vietnam and regions, we still face limitations. The study measures financial institutions innovation by ATMs and POS terminals numbers and can not capture other types of financial innovation such as mobile banking and internet banking and products of other financial institutions. Therefore, further studies should examine these types of financial innovation and can expand to Fintech products as well. Besides, future works can develop to examine whether financial innovation is associated with economic growth in specific industries such as agriculture, manufacturing, or tourism.

Footnotes

Appendix

The list of 63 provinces includes An Giang, Ba Ria – Vung Tau, Bac Lieu, Bac Giang, Bac Kan, Bac Ninh, Ben Tre, Binh Duong, Binh Dinh, Binh Phuoc, Binh Thuan, Ca Mau, Cao Bang, Can Tho, Da Nang, Dak Lak, Dak Nong, Dien Bien, Dong Nai, Dong Thap, Gia Lai, Ha Giang, Ha Nam, Hanoi, Ha Tinh, Hai Duong, Hai Phong, Hau Giang, Hoa Binh, Hung Yen, Khanh Hoa, Kien Giang, Kon Tum, Lai Chau, Lang Son, Lao Cai, Lam Dong, Long An, Nam Dinh, Nghe An, Ninh Binh, Ninh Thuan, Phu Tho, Phu Yen, Quang Binh, Quang Nam, Quang Ngai, Quang Ninh, Quang Tri, Soc Trang, Son La, Tay Ninh, Thai Binh, Thai Nguyen, Thanh Hoa, Ho Chi Minh City, Thua Thien Hue, Tien Giang, Tra Vinh, Tuyen Quang, Vinh Long, Vinh Phuc, Yen Bai.

Acknowledgements

The author Thi Thuy Huong Luong would like to greatly thank Mr. Minh Quang (GSO) and Mr. Le Quang Nam (SBV) for their kindly help to access data sources in Vietnam. This research is funded by University of Finance – Marketing

Ethical Considerations

This study does not involve animals or humans.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research is funded by University of Finance – Marketing

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.