Abstract

This study introduces the concept of earnings purity, a novel construct in corporate finance, and investigates its impact on M&A premiums in China. Based on a multi-dimensional fixed-effects panel regression model, we find that higher earnings purity significantly increases M&A premiums by enhancing target firm valuation. To evaluate the rationality of using earnings purity as a basis for premium decisions, we analyze the opposing effects of information-sharing and information-exclusion, and then assess their relative strength by identifying a cubic S-shaped relationship between earnings purity and negotiation time. This pattern reveals a dynamic shift in the dominance of the two effects across different purity levels: information-sharing prevails at both low and high levels, while information-exclusion tends to dominate at moderate levels. It indicates that whether earnings purity serves as a primary basis for premium decisions depends on the capital market’s current earnings state. Heterogeneity analyses further show that the effect of earnings purity is more pronounced under adverse institutional conditions, for smaller targets, and in cross-border or inter-industry deals. These findings offer new empirical evidence on the role of earnings purity in M&A pricing and enhance our understanding of how earnings-based fundamentals contribute to the rationality of premium decision-making.

Introduction

Financial fundamentals and earning capacity of the target firm play important roles in shaping the valuation and long-term outcomes of M&A transactions. If the target lacks genuine profitability or exhibits weak financial fundamentals, the acquisition may fail to generate expected synergies, impose sustained financial burdens on the acquirer, and weaken its long-term strategic competitiveness. Despite the practical importance of this issue, the academic literatures offer limited theoretical frameworks to assess the intrinsic quality of target firms’ earnings, they primarily focus on earnings management or disclosure-based distortions in perspective of information theory. This study shifts attention to the underlying financial capacity of the target itself, examining the structural and sustainable components of earnings that reflect the firm’s intrinsic profitability and long-term value. Building on this perspective, we introduce the concept of earnings purity—the “gold content” of earnings—which captures not only a firm’s current operational earnings, but also its growth potential, earnings stability, and cash conversion capacity. This concept introduces a novel analytical framework that views earnings as a fundamental, value-linked attribute of the firm, providing a new insight into acquisition premiums based on intrinsic financial substance rather than externally observable reporting indicators.

Compared to related studies, earnings purity emphasizes the fundamental, sustainable profitability and directly signals a firm’s economic strength and future value potential, independent of managerial manipulation or accounting adjustment. Firstly, earnings quality, as discussed in the management literature (e.g., DD model), focuses on the reliability and authenticity of reported earnings, assessing the extent to which earnings represent the true economic performance or the degree of managerial manipulation (Raman et al., 2013). Secondly, Earnings management, grounded in accounting theory (e.g., the Modified Jones Model), involves deliberate adjustment of earnings to alter financial reporting outcomes, often distorting the true financial picture and increasing information asymmetry (Mughal et al., 2021; Perafán-Peña et al., 2022). Thus, earnings purity differentiates itself by offering an economic perspective that emphasizes the inherent value of a firm’s earnings, independent of manipulation or adjustment. This study examines the role of earnings purity in the Chinese M&A market, aiming to provide clearer insights into asset pricing and improve decision-making for acquirers.

We develop a theoretical model to examine how target firms’ earnings purity influences acquisition premium decisions, under both perfect and imperfect information scenarios. We also focus on evaluating the decision-making rationale behind using earnings purity as a pricing basis. To this end, we analyze the dual mechanisms of information-sharing and information-exclusion, and assess their dynamic interplay through a nonlinear relationship between earnings purity and negotiation time. Finally, we perform heterogeneity analyses across institutional environments, firm sizes, and deal types (e.g., cross-border and inter-industry transactions) to explore the contextual conditions under which earnings purity functions as a more informative and effective basis for premium determination.

This study contributes to the academic discourse in several ways. First, it enriches academic decisions in corporate finance by introducing a novel concept—earnings purity. Unlike the majority of literatures which centers on the authenticity and completeness of earnings disclosure (Bazrafshan et al., 2023; Mughal et al., 2021; Perafán-Peña et al., 2022; Raman et al., 2013; L. Wang, 2019), this study examines earnings purity as an indicator of operational efficiency and long-term sustainability. By integrating this concept into the analysis of mergers and acquisitions (M&As), it makes up for the deficiency of existing literatures and highlights the practical and theoretical importance of assessing earnings beyond traditional metrics.

Second, this study extends prior research by developing a theoretical model to analyze the relationship between a target firm’s earnings purity and M&A premiums in China, drawing upon foundational works in the field (McNichols & Stubben, 2015; Polachek & Yoon, 1987). By integrating the acquirer market value model with utility function theory, our model offers novel insights into how earnings purity affects the acquisition premiums. This nuanced approach elucidates the complex dynamics of M&A pricing, providing robust theoretical support for decision-making in mergers and acquisitions.

Finally, in the analysis of decision-making rationality, this study examines the information-sharing and information-exclusion effects associated with earnings purity, and identifies their relative strength by analyzing the dynamic nonlinear relationship between earnings purity and negotiation time. The findings show that for firms with either low or high levels of earnings purity, improvements in earnings purity help mitigate information asymmetry and shorten negotiation time, indicating a dominant information-sharing effect. In contrast, for firms at intermediate purity levels, moderate improvements may trigger incentives for earnings manipulation and prolong negotiations, reflecting the rise of information-exclusion effects. These insights refine our understanding of the informational value of earnings purity in pricing decisions and offer theoretical guidance for acquirers seeking to assess when and how earnings purity can serve as a reliable basis for premium determination across varying institutional contexts.

The rest of the paper is organized as follows: Section 2 outlines the theoretical framework and research hypotheses. Section 3 describes the data and empirical methodology. Section 4 presents the empirical results. Section 5 offers further discussion, and Section 6 concludes the study.

Theoretical Connotation, Literature Review and Hypothesis Development

Theoretical Connotation of Earnings Purity

Earnings purity, in corporate finance, refers to the “gold content” of a firm’s profitability, reflecting its genuine ability to generate sustainable profits without relying on irregular or non-operational revenue sources. This concept emphasizes two attributes–profitability and sustainability. Building on this definition, we develop an earnings purity index based on two dimensions: revenue generation and risk management.

Firstly, revenue generation may be evaluated along two perspectives: static and dynamic. The static evaluation focuses on the absolute level of earnings within a financial year, often assessed through net profit, operating income, and gross profit metrics (Delis et al., 2023; Ren et al., 2024). These indicators provide a snapshot of the company’s operational outcomes and profitability. However, this perspective alone does not capture the long-term value or sustainable profitability of the company. On the other hand, the dynamic state evaluates the sustained growth rate of earnings over consecutive financial periods. This metric considers the trends in profitability, offering insights into the future profit prospects and the management’s effectiveness in implementing long-term strategic goals (Zhou et al., 2024). The combination of above two approaches enables a more comprehensive assessment of a company’s financial health and its potential for continuous growth.

Secondly, a similar classification can also be used to assess a company’s risk management. The dynamic aspect is predominantly analyzed through the volatility of earnings over consecutive financial years, providing insights into the inherent uncertainty and potential risks of business operations (Edmonds et al., 2015; Tsafack et al., 2023). High earnings volatility typically indicates greater operational and financial risks, which could stem from diverse factors such as changes in market demand, fluctuations in raw material prices, and exchange rate variations. Besides, the static aspect is evaluated by the ability of earnings to generate cash flow within a specific financial period. This metric assesses whether a firm can sustainably produce cash through its regular operational activities, which is crucial for repaying debts, paying dividends, and funding capital expenditures (C. W. Wang et al., 2023; X. Wang et al., 2024). The consistency of cash flow serves as a crucial indicator of a company’s financial health. Insufficient cash flow stability can precipitate liquidity crises when the firm faces tight financial conditions.

In conclusion, we employ a multifaceted approach to measure earnings purity, including operational earnings, earnings sustainability, earnings volatility, and the ability to generate cash from earnings. This framework juxtaposes revenue generation and risk management, with the first two dimensions emphasizing revenue aspects, and the latter two focusing on the risk profile of firm’s earnings.

Literature Review of Earnings Purity and Acquisition Premium

Earnings purity, as proposed in this study, is a novel concept that captures the fundamental quality of a firm’s earnings by integrating multiple financial dimensions. It provides a holistic perspective on the firm’s operational conditions, offering theoretical value in understanding the core drivers of firm performance and practical relevance for facilitating more informed and strategic acquisition decisions. However, existing literature has not yet to examine the role of this fundamental quality in determining acquisition premiums; instead, most studies focus on the authenticity or completeness of earnings information and on operating characteristics.

The first examines the authenticity of financial reporting by the target firm, investigating whether earnings manipulation leads to valuation overestimation. They link earnings management by target firms to acquisition premiums, suggesting that managerial intervention in financial reporting can significantly affect acquirers’ valuation judgments (Campa & Hajbaba, 2016; Franck & Cedric, 2023; Perafán-Peña et al., 2022). These studies predominantly focus on the distorting effects of informational misrepresentation on pricing decisions, while largely overlooking the role of the target’s underlying operating capacity in premium determination. The second line of research investigates whether the operational characteristics of the target—such as firm size and growth potential—justify higher premiums. Although some studies have examined the relationship between operational capability and acquisition premiums, they tend to focus on fragmented dimensions, such as industry cycles, firm size, R&D intensity, or financial distress (Ahmed & Bebenroth, 2023; Alexandridis et al., 2013; Bugeja, 2015; Mataigne et al., 2021; Wnuczak & Osiichuk, 2024), rather than offering a systematic assessment of the target firm’s overall earnings capacity.

In fact, the target firm’s earning capacity is essential for achieving post-merger synergies and ensuring effective integration. A lack of systematic assessment of this capacity may impair the acquirer’s ability to make informed pricing decisions and to evaluate long-term deal outcomes. To address this limitation, this study introduces the concept of earnings purity—a composite measure capturing the strength of a firm’s earnings across four dimensions: operational earnings, earnings sustainability, earnings volatility, and the ability to generate cash from earnings. This framework provides a more structured basis for identifying fundamental financial drivers of acquisition premium decisions.

Hypothesis Development of Target Firm’s Earnings Purity and Acquisition Premium

We build upon the acquirer market value model (McNichols & Stubben, 2015) and establish a utility function to evaluate the impact of target firm earnings purity on acquisition premiums:

Where AcqMAValue represents the acquirer’s value enhancement, IVT is the target firm’s inherent value, Synergy is the synergistic effect, and Price is the transaction price.

In line with Polachek and Yoon (1987), the constraint condition is

Where HighPrice represents the maximum price an acquirer is willing to pay, based on the target’s assessed value. λ denotes the bargaining power between the target and acquirer, with a higher λ indicating stronger bargaining power for the target, affecting the transaction price.

We incorporate earnings purity into this model. During due diligence, the acquirer evaluates the target firm. This evaluation primarily hinges on the present value of the expected earnings, which is intimately linked to the earnings purity of the target firm. Therefore, variables directly influencing the assessment value function as derivatives of the target’s earnings purity. Consequently, Equations 1 and 2 are reformulated to explicitly account for this relationship, enhancing the precision of the valuation model used during mergers and acquisitions.

Where Ω EP is actual earnings purity the target firm. Ω EPexp , on the other hand, denotes the expected earnings purity of the target, as conjectured by the acquirer.

In accordance with Equations 3 and 4, the target inherent value (IVT) and synergy effect (Synergy) are directly linked to the target’s earnings purity (Ω EP ). This linkage underscores the role of earnings purity as internal information crucial for both the target and the merged entities. Conversely, the Price and HighPrice are influenced by the expected earnings purity (Ω EPexp ), as these valuations are determined prior to the transaction and are based on external perceptions held by the acquiring firm. The variable λ, ranging from 0 to 1, is an exogenous factor representing the relative bargaining power in the negotiation. A λ of 0 indicates that the price is solely influenced by the target’s inherent value (IVT), with the acquirer capturing all surplus value. Conversely, a λ of 1 suggests that the Price equates to the highest amount that the acquirer is prepared to offer, and the target retains all surplus value.

Continuing our analysis, we aim to determine the conditions for maximizing utility as outlined in Equations 3 and 4, under two specific scenarios: perfect and imperfect information situations.

Scenario 1: A Perfect Information Situation

In a scenario of perfect information, the acquirer has complete knowledge of the target firm’s earnings purity, such that the expected earnings purity aligns precisely with the actual earnings purity, denoted as Ω EPexp = Ω EP . Consequently, Equation 3 simplifies to

The first derivative of Equation 5 is

According to the conditions for utility maximization, the right side of Equation 6 should equal zero, as demonstrated in Equation 7.

In Equation 7, the impact of target’s earnings purity on highest price is determined by two primary factors: the influence of earnings purity on target’s inherent value, and its effect on merger synergy.

Theoretically, a target’s earnings purity may positively affect its inherent value and merger synergy. On one hand, earnings purity, often considered the “gold content” of operating revenue, is strongly associated with the target firm’s future earnings and inherent value. A higher earnings purity suggests a robust financial health and predictable revenue streams, which enhance the perceived intrinsic value of the target.

On the other hand, earnings purity positively influences synergies in operations, management, and finance. Operationally, acquiring a target with high earnings purity enhances the merged firm’s output and operational capabilities. Managerially, synergy is reflected in the improved performance of management teams, higher earnings purity often correlates with top-tier management practices, leading to increased profitability and efficiency. Financially, a superior earnings purity strengthens the merged firm’s cash flow and profitability, enhancing its borrowing capacity and reducing capital costs. This, in turn, attracts greater financial support from banks and financial institutions, bolstering the financial synergies of post-merger.

Consequently, the relationship between the target’s earnings purity and both the synergy ratio and highest price should be positive, implying that Equation 7 yields a value above zero. According to the following transaction price function,

There is a positive correlation between the transaction price and the target’s earnings purity. This suggests that, under controlled conditions, the M&A premium is positively associated with the target’s earnings purity. This relationship suggests that acquirers appreciate the robustness and sustainability of the operational activities signified by earnings purity.

Scenario 2: An Imperfect Information Situation

In an imperfect information scenario, the acquirer lacks full access to the target firm’s earnings information, leading to a disparity between expected and actual earnings purity, denoted as Ω EP ≠ Ω EPexp . Consequently, the Price function is maintained as described in Equation 4. The first derivative of Equation 3 then becomes

According to the conditions for utility maximization,

In Equation 10, the influence of target’s earnings purity on acquirer’s highest price is primarily determined by two factors: one is the impact of earnings purity on target’s inherent value and merger synergy, another is the correlation between target firm’s earnings purity and the expected earnings purity. Research supports the notion that a firm’s actual earnings can positively affect its expected earnings (Z. Li et al., 2024, Shams & Gunasekarage, 2016). For instance, Egging-Bratseth and Siddiqui (2023) demonstrate that superior profitability reduces firm risk and lead to higher expected profits. It indicates that target firm’s earnings purity positively influences the expected earnings purity. Therefore, both the ratio of Ω EPexp to Ω EP and the HighPrice to Ω EPexp are positive. Consequently, even in markets with imperfect information, the M&A premium is still positively correlated with the target firm’s earnings purity. Accordingly,

Materials and Methods

Data and Sample

This study constructs its sample based on the SDC Platinum Mergers & Acquisitions database, a widely used data source in international M&A research that provides comprehensive, standardized, and transaction-level information with high consistency and cross-study comparability (Arslan & Simsir, 2016). We focus on M&A transactions initiated by Chinese firms between 2007 and 2019. The sample period is selected for two primary reasons. First, following the implementation of the revised Company Law and Enterprise Income Tax Law in 2006, China’s M&A activity began to exhibit increasing institutionalization and regulatory standardization. Second, the onset of the COVID-19 pandemic in 2020 introduced substantial exogenous shocks that may distort the relationship between financial fundamentals and M&A behavior. Therefore, the sample is restricted to transactions completed before 2020.

To ensure the validity and comparability of financial indicators, the sample is further refined based on the following criteria: (1) We retain only transactions in which the target firm has a debt-to-asset ratio below 100% and the deal value is greater than zero. (2) Following the approach of Karolyi and Taboada (2015), we exclude transactions involving privatizations, leveraged buyouts, spin-offs, recapitalizations, equity swaps, self-tenders, and self-issuances. These deals often involve special institutional arrangements or strategic restructuring purposes, and the financial condition of the target firm may not reflect its normal operating performance. (3) We exclude all observations with missing values for key financial variables. After applying these filters, the final sample consists of 2132 M&A transactions initiated by Chinese firms during the 2007 to 2019 period.

Table 1 presents the distribution of our sample by industry and year. Most of the targets come from manufacturing sector, aligning with the broader distribution of industries within China. In line with Lan and Guo (2022), Tang et al. (2022) and Yang et al. (2022), we observe a rapid increase in M&A activities starting in 2014, with a peak in 2015. These trends affirm that our sample selection criteria are both random and reliable, ensuring a representative dataset for analysis.

Sample Distribution by Industry and Year.

M&A Premium

The M&A premium serves as the dependent variable in this study. Existing literature primarily adopts two approaches to measure acquisition premiums: the market value method and the book value method. The former is more applicable to transactions involving publicly listed targets in well-developed capital markets (Kaufman, 1988; Laamanen, 2007; L. Li & Tong, 2018), while the latter is more suitable for measuring premiums in emerging capital markets, negotiated transfers, and deals involving either unlisted or listed targets (Guo & Chen, 2025). Considering that China’s capital market is subject to factors such as local government intervention, resource scarcity, and irrational investor behavior, which may distort market-based pricing, this study adopts the book value approach to calculate the acquisition premium, denoted as Premium. The market-based measure is used later for robustness checks. Specifically, Premium is calculated as follows:

Earnings Purity

Prior studies often rely on isolated proxies such as R&D expenditure, asset size, or product life cycle (Alexandridis et al., 2013; Mataigne et al., 2021; Wnuczak & Osiichuk, 2024), which only indirectly capture certain aspects of a firm’s performance. These fragmented measures lack a unified theoretical logic and fail to systematically reflect a target’s fundamental earnings capacity. In contrast, this study proposes a composite framework—earnings purity—that integrates four interrelated dimensions: operational earnings, earnings sustainability, earnings volatility, and the ability to generate cash from earnings. This approach provides a more structured and conceptually grounded measure for evaluating the financial substance behind acquisition premiums. Specifically, operational earnings reflect profitability, measured by the gross profit margin (Liu et al., 2019). Earnings sustainability is crucial for a firm’s ongoing competitiveness and operational continuity, assessed through the sales growth rate. Earnings volatility, which can influence traditional asset pricing outcomes and firm valuation (Ang et al., 2006; Jiang et al., 2005), is captured by the inverse of earnings standard deviation over the past 3 years, that is, 1/σ(Salest-1,Salest-2,Salest-3). Lastly, the ability to generate cash from earnings, a key indicator of earnings liquidity, is measured by the ratio of net operating cash flow to sales. This dimension highlights the liquidity aspect of earnings, underscoring its importance for the firm’s future viability and investment capacity.

We utilized the four indicators—operational earnings, earnings sustainability, earnings volatility, and the ability to generate cash from earnings—in the year prior to the announcement. To compute the target’s earnings purity (i.e., EP), we standardized and weighted these indicators using the Z-score method, effectively quantifying each dimension’s impact on the overall earnings purity.

Control Variables

To mitigate omitted variable bias and improve the explanatory power and robustness of the regression results, this study includes a series of control variables that capture transaction characteristics, firm attributes, and ownership structure. Definitions of all variables are provided in Table 2. At the target firm level, we control for firm size (TSize), leverage ratio (TLev), return on assets (TROA), state ownership (TGov), and high-tech industry classification (THiTec) to account for the impact of firm fundamentals on acquisition premiums. At the transaction level, we control for whether the deal is a horizontal merger (Hor), a cross-border acquisition (Cross), whether the deal is friendly (Att), involves a related party (Relex), includes an earnout clause (Earnout), or involves a financial advisor hired by the acquirer (AAdv). These variables help address potential valuation biases arising from differences in acquisition motives and information asymmetry. In addition, we control for acquirer-level characteristics, including whether the acquirer is a state-owned enterprise (AGov), a publicly listed company (APub), operates in a high-tech industry (AHiTec), or is headquartered in one of the four first-tier cities including Beijing, Shanghai, Guangzhou and Shenzhen (ACity). These variables capture heterogeneity in acquirers’ access to resources, market expectations, and institutional environments.

Control Variable Definitions.

Model

We analyze the influence of target firms’ earnings purity on M&A premiums employing a three-way fixed effects model. This method controls for unobserved heterogeneity across acquirer and target industries, as well as over time, ensuring the robustness of our findings to industry-specific factors and temporal variations.

In Equation 12, i represents the transaction and t denotes the year of merger announcement. To account for factors that might explain the target’s earnings purity and the acquisition premium, we control for several characteristics of the target firm, such as firm size, leverage, sales growth, return on assets, and ownership structure. We lag the control variables by 1 year to mitigate potential endogeneity issues. Additionally, characteristics of the acquirer’s firm and specifics of merger itself are also controlled for. This model is clustered at the acquirer’s industry level, and we winsorize the continuous variables at the 1% and 99% thresholds to reduce the influence of outliers.

Summary Statistics

Table 3 presents the descriptive statistics for all variables. The mean Premium stands at 6.566, while the maximum reaches 212.462, suggesting a generally high and highly variable M&A premium across the sample. Conversely, the mean, minimum, and maximum values for earnings purity are 0.000, −9.068, and 12.206, respectively. This highlights a relatively low level of earnings purity among target firms.

Descriptive Statistics of the Variables.

The apparent paradox between high premiums and low earnings purity can be attributed to two potential explanations: first, acquirers may not sufficiently prioritize the earnings purity of target firms, second, the current earnings purity of target firms may inherently be low. This discrepancy underscores the importance of analyzing the “gold content” of target earnings and elucidating the dynamics between the intrinsic quality of a target’s earnings and the premiums acquirers are willing to pay during mergers and acquisitions.

Control variables such as TSize, TLev, and TROA are also summarized in Table 3. The mean value for TSize is 7.981, positioned centrally between the maximum and minimum values, suggesting that medium-sized enterprises are more frequently targeted for acquisitions compared to very large or very small companies. From the perspective of financial risk, the average TLev is below 50%, and approximately 75% of sample firms have a leverage ratio lower than 60%. This suggests that most targets maintain a relatively conservative capital structure, which may be an important consideration for acquirers when making M&A decisions. In terms of profitability, the mean TROA is slightly higher than the median, indicating a mildly right-skewed distribution. Overall, the distribution of TROA is concentrated, with the vast majority of observations falling within the narrow range of [0.014, 0.058] and remaining in positive territory. This reflects that the target firms in the sample generally exhibit sound profitability, with earnings performance clustered at a moderately high level.

Additionally, the analysis of Pearson’s correlations among variables indicates that the absolute value of correlation coefficients is less than 0.5 for all pairs, confirming that multicollinearity does not pose a problem in our model. This allows for reliable interpretations of the impacts of independent variables on the dependent variable without interference from excessive inter-correlations among explanatory variables.

Results

Causal Relationship Between Target’s Earnings Purity and Acquisition Premium

Baseline Results

Table 4 provides the empirical results for the relationship between earnings purity and acquisition premium across four columns, with each successive column incorporating additional control variables related to the target firm, transaction characteristics, and acquirer firm. The results consistently indicate a positive impact of the target firm’s earnings purity on the acquisition premium, supporting our initial hypothesis. This positive relationship suggests that higher earnings purity is valued by acquirers, potentially leading to higher premiums during mergers and acquisitions. This pattern remains robust even as we adjust for various firm and transaction-specific factors, underscoring the significant role that earnings purity plays in the valuation process during M&A activities.

Relationship Between Target Earnings Purity and M&A.

Note. Clustering of robust standard errors is shown in parentheses. The coefficients marked with ***, **, and * are significant at the 1%, 5%, and 10% levels, respectively. Similarly hereinafter.

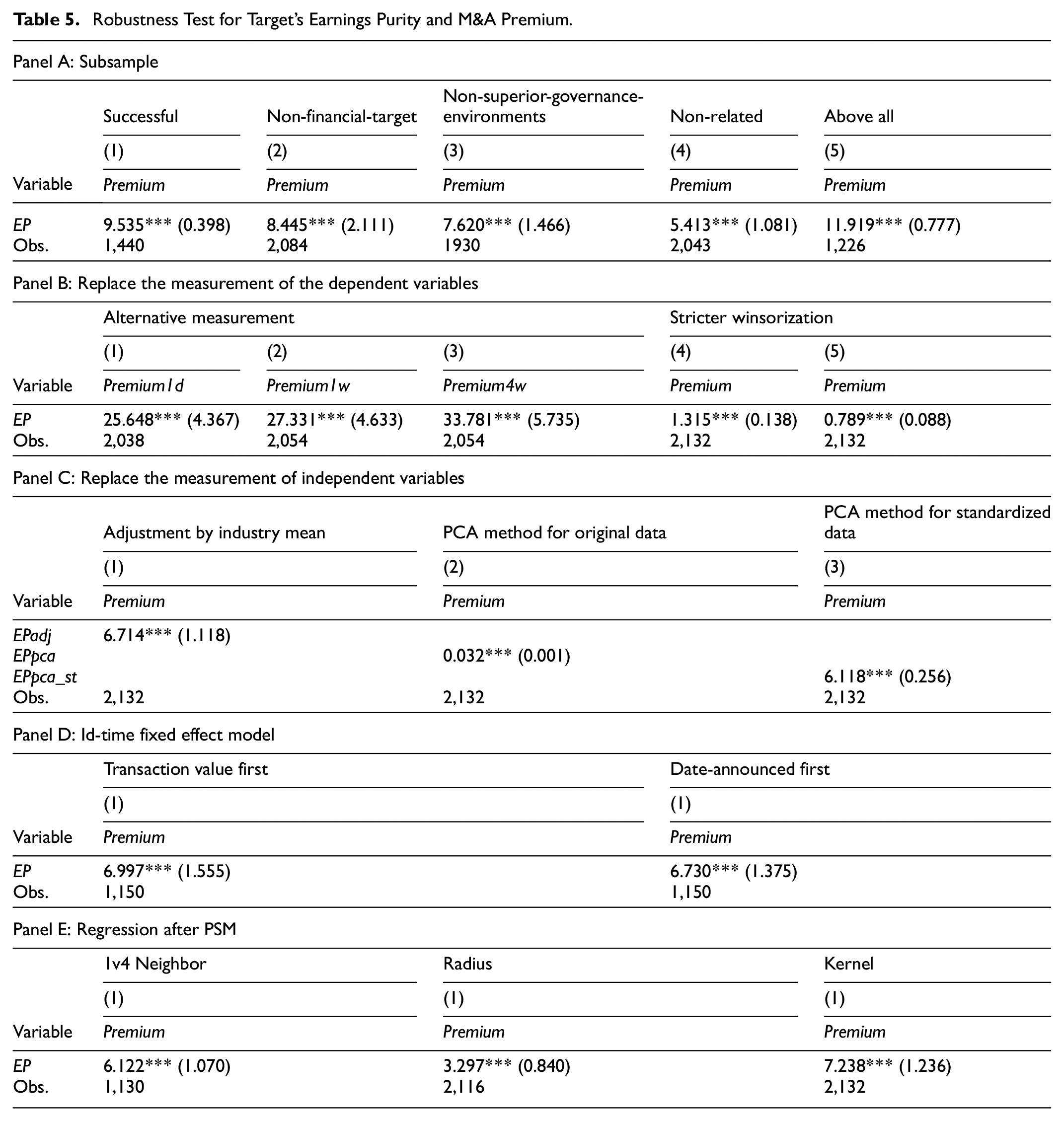

Robustness Check

For robustness, we conducted several regression analyses including the use of sub-samples, alternative measures for dependent and independent variables, a firm-time fixed effects model, regressions after propensity score matching (PSM), and instrumental variable (IV) approach. This comprehensive approach ensures that our findings are not sensitive to methodological variations and provides confidence in the stability of our results.

First, we conducted subsample analyses under several conditions. (1) We included only successful transactions to eliminate any biases from deals that failed to reach a premium agreement. (2) Transactions involving financial target firms were excluded due to their distinct characteristics from non-financial firms. (3) We excluded observations from regions with superior governance environments, as these could artificially inflate the perceived effects of earnings purity on premiums due to regional advantages. (4) Related mergers were excluded to prevent potential biases from transactions where parties have existing trade or management relationships. (5) We further re-examine the impact of target firms’ earnings purity on acquisition premiums by jointly considering the above four scenarios. Implementing these conditions ensures that our findings remain consistent across different scenarios, as evidenced by the unaltered baseline results shown in Table 5, Panel A.

Robustness Test for Target’s Earnings Purity and M&A Premium.

Second, we handle the dependent variable in two ways. (1) We employ alternative measurements of the premium. In line with existing literature (Gomes & Marsat, 2018; Jory et al., 2016; L. Li et al., 2018), we define the premium as the transaction price per share deflated by the target firm’s stock price 1 day, 1 week, or 4 weeks prior to the announcement, denoted as Premium1d, Premium1w, and Premium4w respectively. (2) We apply stricter winsorization to the dependent variable at the 2% and 98%, and 3% and 97% levels. Results in Panel B of Table 5 indicate that using these alternative approaches to handling the dependent variable does not alter the empirical conclusions.

Third, to address potential variability in earnings purity across sectors and over time, we implement three methods to refine our independent variable. (1) We adjust the earnings purity index by sector and year, referred to as EPadj. (2) We utilize principal component analysis (PCA) to compute the earnings purity index of the target firm, labeled EPpca. (3) We first standardize the four component indicators and then also apply PCA method to derive a weighted composite index, denoted as EPpca_st. The findings, presented in Table 5, Panel C, align with our main empirical results, confirming the robustness of our approach.

Forth, we adopt a firm-time fixed effects model to enhance our analysis. The primary model utilizes industry and time fixed effects, which may overlook variables invariant across different firms, potentially leading to endogeneity issues. The firm-time fixed effects model addresses this by considering both firm-specific characteristics and temporal factors. For firms engaged in multiple transactions within a single year, we employ two approaches for data arrangement: (1) retaining the transaction with the highest value, and (2) preserving the earliest transaction. The results, detailed in Table 5, Panel D, confirm that our baseline findings are robust even when switching to this empirical model configuration.

Finally, we employ Propensity Score Matching (PSM) to address potential sample selection biases inherent in ordinary least squares regression. Initially, we categorize the target firm’s earnings purity into treatment and control groups, with the former comprising transactions where the earnings purity (EP) index is above the median, and the latter where it is below. We then implement several matching techniques, including 1v4 nearest neighbor, 0.02 radius, and kernel matching, to align the treatment and control groups accurately. Subsequently, we conduct regressions on these matched samples. As depicted in Panel E of Table 5, the regression outcomes corroborate our main empirical findings.

Lagging explanatory variables in our model helps mitigate endogeneity issues due to reverse causality, but other concerns about endogeneity may persist. To address this, we utilize the instrumental variable (IV) approach and two-stage least squares (2SLS) method. To implement this, we identified comparable companies for each target, selecting those from the same industry and year as the target firm. We then calculated the average earnings purity of these comparable companies to serve as the instrumental variable, denoted as IV.

Building on economic reasoning, the instrumental variable (IV) is related to the target firm’s earnings purity (EP), but not directly to the acquisition premium (Premium). On one hand, companies often benchmark against industry leaders, implying that the earnings purity of these leaders could positively influence the earnings purity of the target firm. This is because firms strive to emulate the successful practices and financial health of leading companies within their industry. On the other hand, the relationship between IV and Premium is indirect. IV represents a measure of earnings purity comparable to that of the target firm, derived from industry peers, while Premium specifically refers to the acquisition premium paid for the target firm. Hence, while IV influences EP by reflecting industry norms and benchmarks, it does not directly affect the transactional valuation aspect captured by Premium.

Table 6 displays the results using the instrumental variable (IV) approach. The first-stage regression demonstrates a positive and significant correlation between IV and EP, aligning with our expectation. The F-statistic exceeds 10, confirming the strength of the IV and indicating no issues with weak instrumentality. In the second-stage regression, the coefficient of EP on Premium is significantly positive and approximately five times larger than the baseline results. This substantial increase suggests that, when endogeneity concerns are addressed, the impact of earnings purity on premiums is more pronounced. These findings emphasize the importance of including earnings purity in acquisition premium decisions and confirm the significant influence of the target firm’s earnings purity on determining acquisition premiums.

Endogeneity Test for Target’s Earnings Purity and M&A Premium.

Mechanism Test

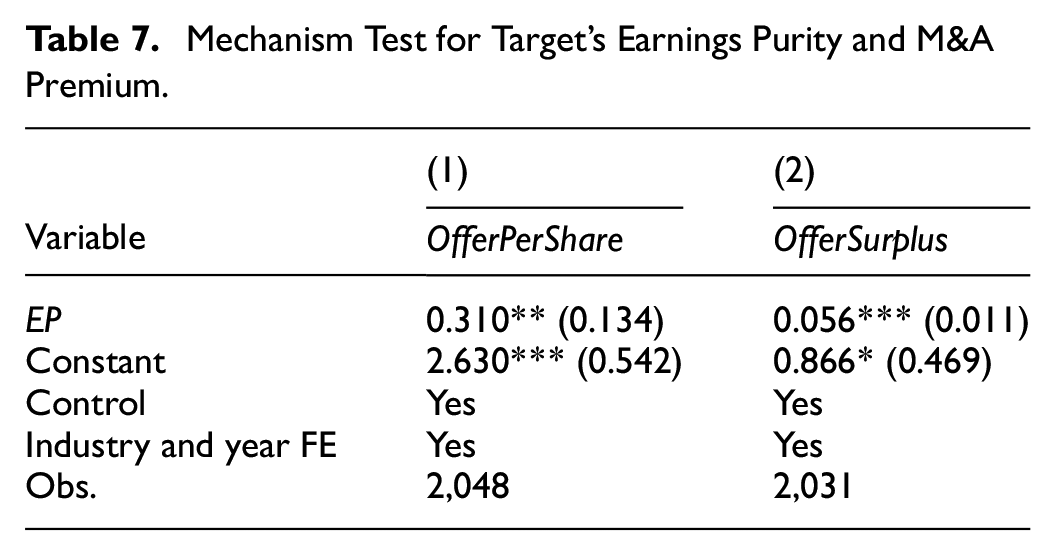

Theoretically, acquisition premiums reflect the acquirer’s willingness to pay above a benchmark value, which is typically shaped by their assessment of the target firm’s intrinsic worth. A higher perceived valuation of the target may lead to a higher offer price, and consequently, a higher acquisition premium. Therefore, valuation plays a critical intermediary role in the pricing logic of M&A transactions. To empirically test whether target firm valuation serves as a mechanism through which earnings purity affects acquisition premiums, we examine whether earnings purity has a significant impact on the acquirer’s valuation of the target. If earnings purity can explain variation in valuation-related measures, it supports the theoretical proposition that valuation mediates the relationship between earnings purity and acquisition premium. If no such relationship is found, then the validity of this mechanism is called into question.

We construct two regression models using valuation-related indicators as dependent variables: (1) OfferPerShare, defined as the acquirer’s offered price per share, reflects the absolute valuation placed on the target, (2) OfferSurplus, measured as the difference between the offer price per share and the target’s stock price 1 day before the M&A announcement, captures the valuation uplift relative to market expectations. As shown in Table 7, earnings purity (EP) has a significantly positive effect on both measures. These results confirm that higher earnings purity leads to higher valuation assessments by the acquirer, thereby validating valuation as a key mechanism linking earnings purity to acquisition premium decisions.

Mechanism Test for Target’s Earnings Purity and M&A Premium.

Rationality of Premium Decisions Based on Earnings Purity

We investigate whether earnings purity can serve as a reliable informational basis for premium decisions by analyzing its two competing effects: information sharing and information exclusion. Under the information-sharing effect, higher earnings purity promotes greater transparency and reduces information asymmetry between the acquirer and the target. Prior research suggests that managers are more inclined to disclose favorable information while concealing unfavorable news (Kothari et al., 2009). For target firms, higher earnings purity constitutes favorable news. Accordingly, target firms with greater “gold content” in earnings are more likely to provide forthcoming and transparent disclosure, facilitating more informed decision-making by acquirers. In contrast, the information-exclusion effect posits that greater earnings purity may also incentivize downward earnings management. Jones (1991) and Brushwood et al. (2022) show that when actual earnings exceed expectations, firms often suppress or defer recognition to retain future flexibility or avoid heightened scrutiny. This behavior can increase information asymmetry and obscure firm value, potentially distorting pricing decisions (McNichols & Stubben, 2015; Varaiya, 1988).

Therefore, while earnings purity has the potential to support well-informed premium setting through its transparency-enhancing function, it may also undermine decision reliability when used strategically to restrict information. The interplay of these two opposing mechanisms determines the effectiveness of earnings purity as a decision signal in M&A pricing. To empirically assess this, we proceed in two steps. First, we test whether both the information-sharing and information-exclusion effects are statistically significant. If only one mechanism is present, the role of earnings purity in premium determination can be directly inferred. However, if both effects coexist, further analysis is needed to assess their relative strength and to identify the conditions under which earnings purity serves as a valid basis for pricing decisions.

Tests for Information-Sharing and Information-Exclusion Effects

In terms of the effect of information sharing, targets with high earnings purity are more inclined to disclose or share such superior earnings, thereby reducing information asymmetry between parties (Raman et al., 2013). To measure the target firm’s level of information disclosure, we utilize two metrics: the bid-ask spread (Cheng et al., 2016; Lee & Chung, 2013), and stock price synchronicity (Martin & Shalev, 2017), denoted respectively as Spread and Synch. As demonstrated in Table 8, Panel A, there is a significant impact of target earnings purity on information disclosure. Specifically, enhanced earnings purity in the target firm correlates with narrower bid-ask spreads and reduced stock price synchronicity, indicating an increase in the degree of information disclosure or sharing. This, in turn, reduces the asymmetry between the acquirer and the target, thereby leading to a more reasonable acquisition premium (Fulghieri et al., 2014; Jory et al., 2016).

Information Effect of Earnings Purity.

Drawing on the information exclusion effect, improved earnings purity in the target may heighten incentives to manage earnings downward (Brushwood et al., 2022), suggesting that the target might obscure actual earnings while maintaining access to exclusive information. To assess the target’s earnings management, we employ following models: the MDD models (Dechow & Dichev, 2002; Marquardt & Zur, 2015), and the modified Jones model (Jones, 1991; L. Wang, 2019), denoted as MDD and MJones, respectively. As demonstrated in Panel B of Table 8, there is a positive correlation between target earnings purity and earnings management, as shown in columns (1) to (2), supporting the theoretical analysis of the information exclusion effect associated with earnings purity. Further analysis on the direction of such earnings management reveals that, target earnings purity significantly influences downward earnings management, as observed in column (5) and (6), but exerts a negligible effect on upward earnings management, as shown in column (3) and (4). This observation aligns with our theoretical expectations.

Consequently, both the information sharing and information exclusion effects are validated. Next, we proceed to analyze which effect predominates in order to assess the rationality of premium decisions based on earnings purity.

Relative Strength of Information-Sharing and Information-Exclusion

To assess the relative strength of the information-sharing and information-exclusion effects, we focus on negotiation time, defined as the duration between the M&A announcement date and the effective date. This variable is widely regarded as an indicator of the degree of information asymmetry between the acquirer and the target (Jurich & Walker, 2022). Longer negotiation periods suggest greater information asymmetry or a stronger information-exclusion effect, requiring more time for the acquirer to assess and access the target’s private information. In contrast, a shorter negotiation period reflects greater transparency or a dominant information-sharing effect, indicating lower asymmetry and more efficient communication.

Table 9 presents the regression results. Columns (1) to (3) incorporate the linear, quadratic, and cubic terms of earnings purity—denoted as EP, EPsquare, and EPcube, respectively. The significance of the higher-order terms indicates that the relationship between earnings purity and negotiation time is neither linear nor monotonic, but rather follows a non-linear “S-shaped” pattern. This pattern reflects a dynamic shift in the dominance of information mechanisms across different levels of earnings purity. Specifically, at lower levels, increases in earnings purity enhance transparency and reduce information asymmetry, resulting in shorter negotiation times—indicating a dominant information-sharing effect. At moderate levels, however, greater ambiguity or signaling complexity may prolong negotiations, reflecting the rise of the information-exclusion effect. As earnings purity continues to increase, negotiation time declines again, suggesting that once transparency is sufficiently high, the information-sharing effect regains dominance.

Test for Target’s Earnings Purity and Negotiation Time.

Note. Nego represents negotiation time, measured as a natural logarithm of the difference between effective date and announcement date.

To refine our interpretation of the mechanism, we examine the relationship between earnings purity and negotiation time specifically within the sample range observed in this study, as depicted by the empirical interval highlighted in Figure 1. The gray curve represents the estimated cubic relationship between earnings purity and negotiation time, while the black segment highlights the actual sample range, with earnings purity values concentrated between −9.07 and 12.21.

Cubic relationship between earnings purity and negotiation time.

The sample mean falls to the left of the first turning point in the curve (approximately EP = 1.98), within the downward-sloping segment of the curve. This indicates that, for most observations, increases in earnings purity are associated with shorter negotiation times. In other words, target firms in China’s M&A market generally exhibit relatively low levels of earnings purity, and acquirers face substantial information asymmetry when making decisions. Under these conditions, prioritizing targets with stronger and more transparent earning fundamentals can improve negotiation efficiency and support more informed and disciplined acquisition decisions. This result further confirms that the information-sharing effect is dominant in the current context, lending support to the validity and practicality of using earnings purity as a basis for premium determination.

Heterogeneity Test

Table 10 presents the results of the heterogeneity analysis. Columns (1) and (2) examine cross-industry and cross-regional mergers and acquisitions. The significantly positive interaction terms suggest that in these contexts acquirers are more likely to rely on earnings purity as a decision signal when setting acquisition premiums. Cross-border and cross-industry transactions often involve greater institutional, operational, and cognitive differences between the acquirer and the target, leading to higher information asymmetry. Under such conditions, observable and structural indicators such as earnings purity become particularly useful for acquirers in reducing uncertainty and guiding premium decisions.

Heterogeneity Test.

Note. In column 1, the variable of nonHor corresponds with the control variable Hor. In column 2, diffplace is a dummy variable that equals 1 if the acquirer and target are located in the same city, and 0 otherwise. In column 3, TSizetoInd is the ratio of TSize to its industry and year average. In column 4, the definition of ACity is provided in Table 2.

Columns (3) and (4) examine heterogeneity based on the target firm’s relative size and the institutional environment in which the acquirer operates. The negative interaction terms indicate that when targets are larger or when acquirers face stronger external monitoring and better regulatory systems, reliance on earnings purity as a pricing basis diminishes. In these contexts, acquirers tend to have better access to firm-specific information and perform more comprehensive due diligence, thereby reducing the need to rely on simplified financial proxies such as earnings purity in pricing decisions.

Discussion

Comparison With Prior Research

Compared with existing literature, this study is the first to introduce the concept of earnings purity and examine its influence on acquisition premium, extending the theoretical understanding of how firms’ internal earning capacity and information signaling jointly shape M&A pricing decisions.

Prior studies have primarily focused on the authenticity of financial disclosures and their impact on acquisition premiums (Bazrafshan et al., 2023; Mughal et al., 2021; Perafán-Peña et al., 2022; Raman et al., 2013; L. Wang, 2019), often measured through proxies such as accrual-based earnings management, real earnings management, or disclosure manipulation. In contrast, the earnings purity framework proposed in this paper emphasizes a more structural assessment of the firm’s underlying earning capacity. It evaluates earnings performance across four dimensions: operational earnings, earnings sustainability, earnings volatility, and the ability to generate cash from earnings. This multidimensional framework provides a foundation for assessing firms’ sustainable earning power and long-term value potential.

Moreover, through a combination of theoretical modeling and empirical analysis, this study finds that earnings purity positively affects acquisition premiums via the valuation channel. This finding aligns with prior evidence on the role of target fundamentals in premium determination. For example, Laamanen (2007) argue that higher R&D investment improves the firm’s earning potential and thus increases its acquisition value, while Ahmed and Bebenroth (2023) emphasize the importance of industry growth prospects in shaping acquisition pricing. Our results further reveal that, in the Chinese M&A market, the overall earnings purity of target firms remains relatively low, exposing acquirers to significant information asymmetry. In this context, using earnings purity as a selection criterion—favoring targets with stronger, more transparent earning capacity—can improve negotiation efficiency and enhance the overall rationality of the transaction. This finding not only offers novel theoretical insights into the pricing logic of China’s M&A market, but also provides a valuable analytical framework for future research on corporate valuation under information asymmetry.

Generalizability and External Validity

Although our findings provide strong evidence of the impact of earnings purity on acquisition premiums, the analysis is based primarily on the Chinese market. Given the unique institutional characteristics of China’s M&A environment—including the regulatory structure, capital market maturity, and financial disclosure practices—the generalizability of the results requires further discussion.

First, our heterogeneity analysis shows that the impact of earnings purity is negatively moderated by the quality of the institutional environment. This suggests that earnings purity may play different roles in M&A pricing across countries. In developed markets with stronger institutions and higher transparency, acquirers may face less information asymmetry and can obtain richer data through alternative channels, potentially reducing the marginal value of earnings purity. In contrast, in emerging or weakly regulated markets, earnings purity may become a critical indicator for acquirers in evaluating the intrinsic value of the target firm, exerting a stronger influence on premium decisions.

Second, the cubic relationship between earnings purity and negotiation time reveals a nonlinear mechanism that further illustrates the contextual role of earnings purity. Specifically, (1) In well-developed markets where target firms are more transparent, the information-sharing effect tends to dominate. Acquirers can quickly access reliable financial and operational information, improving negotiation efficiency. (2) In less developed markets with lower earnings purity, improvements in purity help mitigate information asymmetry and reduce due diligence costs, enhancing the efficiency and validity of acquisition decisions. (3) In countries where firms are clustered around moderate levels of earnings purity, incremental improvements may instead lead to increased managerial discretion and strategic signaling, thereby triggering more earnings manipulation and lengthening negotiation time. In such contexts, regulators should promote higher disclosure standards and improve earnings transparency to help firms escape the “earnings purity trap” and reduce risks associated with information exclusion.

Reproducibility of Results

This study provides a detailed account of the data sources, empirical design, and construction of the earnings purity index, ensuring transparency and replicability. We specify the data collection process, variable definitions, sample selection criteria, and the step-by-step construction and weighting method of the composite index. These methodological disclosures enable other researchers to reproduce our empirical results using the same publicly available data within the proposed framework.

In addition, the dataset used in this study—sourced from the SDC Platinum M&A database—offers high accessibility and traceability. The database provides detailed, standardized transaction-level information, including rich target-level firm attributes that are often unavailable in other commercial datasets. This enhances the transparency of empirical analysis and enables future researchers to conduct comparable studies based on the same foundational data. Given its extensive coverage and granularity, the SDC database holds significant potential for further research on target firm characteristics, valuation dynamics, and M&A behavior across diverse contexts.

In sum, the reproducibility of this research is well assured. Scholars may use our methodology to further examine the role of earnings purity in M&A valuation or extend the analysis to other capital markets. Through its transparent data procedures and well-defined empirical design, this study contributes a replicable and scalable framework for future academic and practical applications.

Conclusions

Existing literature has largely overlooked the “gold content” of earnings. This study introduces a novel concept—earnings purity—and investigates its impact on M&A premiums. The main conclusions are as follows: (1) Target firm’s earnings purity significantly influences acquisition premiums through valuation channel. This finding enriches the literature by shifting the focus from earnings disclosure credibility to the intrinsic structural quality of earnings as a core determinant of valuation in M&A transactions. (2) This study identifies two opposing effects induced by earnings purity: the information-sharing effect and the information-exclusion effect. By analyzing the cubic relationship between earnings purity and negotiation time, we uncover a dynamic evolution of these effects across different levels of earnings purity. Specifically, when earnings purity is at relatively low or high levels, the information-sharing effect dominates, reducing information asymmetry and improving negotiation efficiency. However, at moderate levels, the information-exclusion effect intensifies, potentially triggering managerial manipulation and prolonging negotiation, thus complicating pricing judgments. This result advances theoretical understanding of information mechanisms in M&A by revealing a non-linear relationship between financial fundamentals and negotiation dynamics, highlighting the conditional nature of informational efficiency. (3) Heterogeneity test show that the impact of earnings purity on acquisition premiums is significantly amplified in specific contexts, such as cross-industry M&As, cross-regional transactions, cases involving smaller target firms, and deals in weak institutional environments. This insight underscores the contextual dependence of earnings-based valuation logic and offers a framework for understanding when and where earnings purity plays a more critical role in premium setting.

Based on the above findings, the following policy recommendations are proposed: (1) Promote improvements in earnings purity at the firm level. Governments and regulatory bodies should encourage enterprises to improve financial transparency and standardize disclosure practices, especially regarding earnings quality. This can be achieved through stronger oversight of financial reporting and the promotion of robust financial management standards. (2) Strengthen the acquirer’s evaluation of earnings purity. Acquirers should incorporate earnings purity as a key indicator in their valuation models—particularly in complex transactions such as cross-industry or cross-regional M&As. Enhancing financial due diligence and establishing stronger information-sharing mechanisms can help reduce valuation bias and support more rational pricing decisions. (3) Increase market awareness of earnings purity. Firms and investors should recognize earnings purity as a critical metric for assessing long-term competitiveness and sustainable profitability. Improvements in earnings purity not only help attract investment but also provide a more stable foundation for long-term value creation.

While this study offers new insights into the relationship between earnings purity and acquisition premiums, several limitations remain. First, the empirical analysis is based on Chinese M&A transactions, therefore, the applicability of the findings to other institutional contexts warrants further empirical investigation. Future research could extend the sample to include cross-country comparisons, particularly between developed and emerging markets, to explore contextual differences in the role of earnings purity. Second, this study focuses primarily on pre-acquisition pricing decisions. Future studies may investigate the role of earnings purity in post-merger integration, especially in shaping synergy realization and long-term performance outcomes. Third, future work could incorporate other financial and non-financial indicators to construct a more comprehensive valuation model, thereby refining the theoretical framework linking earnings purity to M&A decision-making.

Footnotes

Funding

This study is supported by Shanghai Fintech Research Institution of Shanghai Lixin University of Accounting and Finance (2025-JK04) and Nanhu Scholars Program for Young Scholars of Xinyang Normal University.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

All data will be provided by the authors upon request.