Abstract

Based on structural equation modeling, the impact of changes in organizational framework on firm performance and the intervention function of operational efficiency are scrutinized. The study selects a sample of Chinese listed manufacturing firms and constructs a mediation model containing organizational structure change, operational efficiency and firm performance. The results find that (1) organizational change has a significant positive impact on firm performance through management process optimization and resource integration; (2) operational efficiency partially mediates the impact of organizational change on firm performance from the dimensions of cost control and asset efficiency; and (3) the main findings still hold under multiple robustness tests. The study concludes that firms should actively promote organizational change and that operational efficiency is a leverage point for firms to continuously optimize their performance.

Introduction

With the rapid development of global economic integration and technological advances, the uncertainty and complexity of the environment in which businesses operate has increased significantly. According to the World Economic Forum, more than 70% of enterprises around the world have undergone significant changes in the past decade to cope with the rapidly changing market and technological environment (Cameron & Green, 2020). In China, with the transformation and upgrading of the manufacturing industry, companies are facing more intense competition at home and abroad. According to China’s Ministry of Industry and Information Technology (MIIT), the value added of China’s manufacturing industry will account for 27.1% of GDP in 2023, but the average profit margin of enterprises will be only 6.5%, which is much lower than that of developed countries. Based on this, how to build an efficient and agile organizational structure to further improve corporate performance has become a key issue for Chinese enterprises (Errida & Lotfi, 2021).

Organizational change is an important tool to improve the competitiveness of enterprises. Studies have shown that structural change can significantly improve productivity and other efficiency indicators (George et al., 2019). But there is a lack of research on the specific impact of structural change on core business performance. Existing studies in China are less likely to explore the long-term impact of organizational structural change on firm profitability and the mediating role played by operational efficiency. In addition, the specific mechanism of operational efficiency in the relationship between structural change and performance has not been thoroughly validated (Hanelt et al., 2021). This study aims to fill this research gap by exploring the impact of organizational structural change on the performance of Chinese manufacturing firms and the path of its transmission through operational efficiency (Keller & Schaninger, 2019).

The main questions of this study are stated as follows: does organizational change significantly improve the profitability of Chinese manufacturing firms? What role does operational efficiency play in this process? These questions are important for understanding how Chinese firms enhance their competitiveness through organizational change (Kotter, 2021). Based on this, this study sets the following research objectives:

to explore the direct impact of organizational change on the performance of Chinese manufacturing firms: to verify through empirical analysis whether organizational change can directly improve firms’ profitability.

to analyze the mediating role of operational efficiency: to explore the mediating mechanism of operational efficiency between organizational structure change and firm performance, and to verify its indirect impact on profitability.

assess the robustness of the research results: adopt various methods and data processing tools to ensure the reliability and generalizability of the research results.

In order to achieve the above objectives, this study constructs structural equation modeling (SCM) and empirically analyzes it using panel data of listed manufacturing firms in China (Laumer et al., 2019). Through this process, we are not only able to verify the direct impact of organizational change on firm performance, but also reveal the mediating role of operational efficiency in it, providing valuable references for corporate decision makers (Supriharyanti & Sukoco, 2022).

Rationale and Research Hypothesis

The Impact of Organizational Change on Firm Performance

Organizational structure change, as an important part of enterprise change, is committed to improving the operational efficiency and competitiveness of enterprises (Tipu, 2022). Resource base theory suggests that an enterprise's competitive advantage comes from its unique configuration of resources and capabilities. Reasonable organizational change can enhance the core competitiveness of an enterprise by optimizing resource allocation and improving operational efficiency. Specifically, the simplification of management levels and the optimization of decision-making processes can accelerate the speed of information communication and problem solving, reduce the communication barriers between levels, and improve the efficiency of decision-making (Vakola, 2019). Mokogwu (2024) research shows that flat management makes decision-making closer to the actual situation on the front line and improves the speed of response. Daspit (2013) by adjusting the departmental setup and functional division. By adjusting departmental settings and dividing functions, Casey (2021) further clarifies responsibilities and authority, and reduces duplication of functions and conflicts among departments, which helps to improve the efficiency of collaboration among departments and avoid redundancy and inefficient operations.

Improving operational efficiency can have a positive impact in many ways. By optimizing management processes and integrating resources, enterprises can effectively reduce operating costs and thus expand profitability (Verhoef et al., 2021). Flat organizational structure enables enterprises to respond faster to changes in market demand and improve market competitiveness. Flat structure strengthens communication between upper and lower levels, employees have a greater sense of ownership, cross-departmental collaboration is more efficient, and teamwork efficiency is improved. However, some scholars have pointed out that organizational structure change may bring short-term negative impacts (e.g., role confusion and decreased sense of belonging), increase coordination costs in the short term, and affect employees' work attitudes and performance. In addition, changes in organizational structure do not directly affect firm performance, and their effects are moderated by a variety of conditional factors, such as change strategies, entrepreneurship, and employee attributes (Warner & Wäger, 2019).

Based on the above analysis, this paper proposes Hypothesis 1: Under the condition of controlling relevant variables, rational organizational structure change significantly and positively affects firm performance (Katsaros et al., 2020). As the change directly optimizes resource allocation and improves operational efficiency indirectly enhances the profitability of the firm.

Organizational Change, Operational Efficiency, and Firm Performance

Appropriate organizational restructuring can simplify administrative procedures, optimize business processes, reduce coordination costs and increase the labor efficiency of departments and employees. Its specific manifestations include flattening management levels, simplifying the decision-making chain, speeding up the response to problems, reducing the time lag in information transmission, and improving decision-making efficiency. Modular organizational structure divides departmental functions by business processes and concentrates specialized capabilities to improve operational efficiency. Decentralization of departmental boundaries amplifies the cooperation and association between different departments, improves the effectiveness of knowledge and asset allocation, and significantly enhances the operational efficiency of the organization. Firms reduce operational expenditures to allocate additional resources for production and operations, thus improving the overall efficiency of the firm.

Operational efficiency plays an important mediating role in the process of organizational restructuring. Firms increase profitability by reducing operating expenses, which directly improves the profitability of the firm. Enhancing the synergy of internal processes improves the overall operational efficiency of the firm. Modular management combinations optimize internal synergies to improve output efficiency, and firms seize external market opportunities to further expand production capacity and capture market share to achieve scale effects and greater profitable growth. However, the improvement of operational efficiency may also be limited by a number of factors. When the corporate culture is not aligned with the goals of the change, employees may be resistant to the change, resulting in a limited magnitude of operational efficiency improvement. The highly dynamic market environment allows competitors to quickly emulate the change model, affecting the sustainability of operational efficiency.

Based on the above analysis, this paper proposes Hypothesis 2: Operational efficiency plays a mediating role in examining the impact of organizational change on overall firm performance. By introducing operational efficiency as a mediating variable, this study not only verifies the direct impact of organizational change on firm performance, but also reveals the internal mechanism behind it.

Research Gaps and Unique Contributions

Although existing research has explored the impact of organizational structural change on operational efficiency, studies lack insights into the specific path of its impact on core business performance (e.g., profitability). In addition, the mediating role of operational efficiency between structural change and performance has not been fully validated. By introducing operational efficiency as a mediating variable, this study fills this research gap and provides a new perspective for understanding the impact of organizational structural change on firm performance. The unique contribution of this study is to extend the endogenous mechanism and reveal the endogenous mechanism of the impact of organizational structure change on firm performance by introducing operational efficiency as a mediating variable. Empirical analysis is used to verify the direct impact of organizational change on corporate performance and the mediating role of operational efficiency, providing solid empirical support for the theory. And on this basis, this study provides specific recommendations for corporate decision makers to help them better focus on the improvement of operational efficiency when implementing organizational structure change, so as to optimize corporate performance.

Research Design

SCM Model

To facilitate a more comprehensive study of the impact of organizational restructuring on firm performance, this investigation constructed an enhanced conceptual framework aimed at elucidating the mechanisms by which improved operational efficiency affects intervention outcomes (Agbemava et al., 2024). The framework is illustrated in Figure 1. In this research framework model, the initial focus of the study was to test the direct effect of the explanatory variable, OSC, on the response variable, EP, in order to verify whether Hypothesis 1 was valid. After testing the direct path of action of OSC on EP, this study introduces the mediating variable OE and evaluates the effect of OSC on OE and the subsequent effect of OE on EP, with the aim of evaluating the moderating role of the mediating effect in the process of OSC's influence on EP, thus testing Hypothesis 2. In the causal chain of the model, OSC acts as the independent variable, and its changes will first affect the mediating variable OE, and then further affect EP via the moderating role of OE (Cham et al., 2024). This mediating effect model, by examining the total effect of OSC on EP and its decomposed direct and indirect effects (mediated by OE), can provide a deeper understanding of how and through what paths organizational structural change ultimately affects the firms’ operating performance (Cham et al., 2024).

SCM mediated effects model.

Based on the model inference, the measurement model and the structural model are set up using the SCM method commonly used in structural equation modeling. The measurement model determines the measurement properties of each potential variable by identifying the measurement indicators of the variables and the internal consistency between them (Ting et al., 2024). In this study, three measures of OSC, OE, and EP were selected, and correlation analysis and Cronbach’s alpha coefficient were used to examine the correlation between the measures and between the measurement variables (Rivera, 2024). Structural modeling describes the causal relationships between variables and tests the research hypotheses. Path coefficients a, b, and c’ were set to indicate the effect of OSC on OE, the effect of OE on EP, and the direct effect of OSC on EP, respectively. The model was estimated to obtain parameter estimates and subsequently checked for the combined adequacy of the model and the significance of the parameters.

Measurement modeling:

Structural modeling:

This study will test the above SCM model using software such LISREL to examine the relationship between organizational change and firm performance and to test whether the mediating role of operational efficiency holds.

Variable Selection and Measurement

Explanatory Variables

The explanatory variable of this study is organizational structural change (OSC). Organizational structural change refers to the enhancement and reorganization of organizational structures and management procedures by firms in order to improve organizational coordination and operational efficiency. This study examines two main types of organizational structural change: flat reform refers to the establishment of a flat organizational form by firms reducing the number of management levels and expanding the span of individual managers. Modular transformation refers to the division of business modules according to business processes and value chains, where each module is highly autonomous but works in close collaboration with other modules, and both types of changes have the core objective of improving the efficiency of decision-making and operations.

In order to comprehensively reflect the effect of organizational structure change, this study selected the following three measurement indicators from the dimensions of management process and organizational form:

OSC1: Number of management levels. Reflects the length of the management chain of the enterprise. Fewer levels indicate a higher degree of flattening. This indicator was chosen because one of the core objectives of flattening reforms is to reduce the number of management levels in order to improve decision-making efficiency and responsiveness.

OSC2: Degree of decision-making authorization. Reflects the autonomous decision-making authority of junior and middle managers. A higher degree of empowerment indicates a higher degree of flattening. This indicator was chosen because delegation of decision-making is an important feature of flattening reforms and enhances organizational flexibility and innovation.

OSC3: Number of departments. Reflects the number of functional departments in the enterprise. A lower number indicates a higher degree of modularization and integration. This indicator was chosen because modular retrofitting aims to improve operational efficiency and resource utilization by reducing redundant departments.

Explained Variables

The explanatory variable in this study is enterprise performance (EP). Enterprise performance is an important indicator for evaluating the operation and value creation of an enterprise, and can reflect the operational status of an enterprise from multiple dimensions (Bustami et al., 2024). Given that both organizational changes and improvements in operational efficiency can have a positive impact on cost control and profit growth, this study chooses to focus on financial indicators that reflect corporate profitability to measure corporate performance. The corporate profitability indicator is a key measure for evaluating the economic benefits and shareholder returns obtained by an enterprise, which intuitively reflects the profitability of an enterprise in its main business, and can show the effect of the contribution of organizational structure changes to the performance of an enterprise (Gunsayan & Guhao, 2021).

Based on the financial report indicators of listed companies, this study selects the following three specific measures to examine corporate performance:

EP1: Operating profit growth rate. Reflects the growth rate of profits drawn from the main business income of the enterprise.This indicator was chosen because operating profit directly reflects the profitability of a company’s core business and is one of the most important indicators of corporate performance.

EP2: Net profit growth rate. Reflects the rate of growth of after-tax profits ultimately achieved by the enterprise. This indicator is chosen because net profit is the ultimate expression of the enterprise's operating results, which can fully reflect the profitability and operating efficiency of the enterprise.

EP3: Return on net assets. Reflects the ratio of profits made by the enterprise to capital invested, and is an important profitability indicator.This indicator was chosen because return on net worth measures the efficiency of a firm’s use of capital and is a key indicator for investors to assess the performance of a firm.

Based on the above three specific measures, a comprehensive index can be constructed to examine the performance of the enterprise, which can be called “Comprehensive Performance Index (

Assuming that the operating profit growth rate, net profit growth rate, and return on net assets are denoted by

Where,

The choice of weights should be rationally assigned based on the importance of each indicator to enterprise performance and the actual situation. For example, if the net profit growth rate is considered to have the most important impact on enterprise performance, it can be given a higher weight, while a lower weight is assigned to other indicators.

The higher the result of the calculation of the Composite Performance Index

Mediating Variables

The mediating variable is the operational efficiency (OE) of the firm. OE indicates the effectiveness of an enterprise's internal management and business operations, and is an important indicator of an enterprise's operational status. The core objective of organizational change is to improve the efficiency of the firm in all aspects of management and operations by adjusting and optimizing the organizational structure and business processes (Al Doghan & Sundram, 2023). If the change in organizational arrangements succeeds in improving the operational efficiency of the institution, then this improved efficiency will have a favorable impact on the institution's revenue and execution. Thus, operational efficiency plays an intermediate moderating role in the process of organizational change affecting firm performance (Homayoun et al., 2024).

Referring to the established literature, this study selects the following three indicators to measure the operational efficiency of the firm mainly from the dimensions of cost control and output efficiency:

OE1: Selling Expense Ratio. Reflects the efficiency of the sales side of the business, with lower levels indicating less consumption of resources in the sales process (Tripathi, 2024).This indicator was chosen because the cost of goods sold ratio can reflect the efficiency of resource utilization in the sales activities of the company and is one of the important indicators of operational efficiency.

OE2: Overhead Expense Ratio. Reflects the efficiency of the management side, the lower it is, the less costly it is to manage the operation process. This indicator was chosen because the management expense ratio reflects the ability of companies to control costs in their management activities and is one of the most important indicators of operational efficiency.

OE3: Asset turnover speed. Reflects the efficiency of the asset’s end-of-use, with higher levels indicating a higher value of output generated by the asset. This indicator was chosen because the speed of asset turnover reflects the efficiency of the utilization of the firm’s assets and is one of the key indicators of operational efficiency.

Control Variables

To improve the accuracy of model inference, this study also introduces some control variables to reduce the influence of confounding effects.

Firm-level variables:

(1) Enterprise size. Expressed as the natural logarithm of total assets, it reflects the absolute size of the firm, and large firms are more prone to organizational change due to resource advantages. Also firm size affects performance. This indicator was chosen because firm size may affect the effectiveness of implementing organizational change and firm performance.

(2) Age of the enterprise. Expressed in terms of the number of years the enterprise has been in existence, the longer the enterprise has been in existence, the more stable the organizational structure and culture, and the more difficult it is to change. This indicator was chosen because the age of the firm may affect the stability of the organizational structure and the difficulty of change.

(3) Industry. Industry dummy variables are set to distinguish the industry sectors to which the sample firms belong, and there are differences in the operation mode and performance level of different industries due to differences in technological characteristics and market environments. This indicator was chosen because there are significant differences in the mode of operation and level of performance across industries.

Market-level variables:

(1) Market growth rate. Expressed in terms of the market growth rate of the main industry in which the enterprise is located, a fast-growing market provides more opportunities for the enterprise and mitigates the risk of change. This indicator was chosen because market growth rates may affect the growth opportunities and risks of change for firms.

(2) Industry concentration. Expressed as the sum of the market share of the top 4 enterprises in the industry to which the enterprise belongs, enterprises in industries with a high degree of competition face greater pressure to change. This indicator was chosen because industrial concentration may affect the competitive pressures and incentives to change of firms.

Data Sources and Processing

This study selects a sample of listed companies in China’s manufacturing industry, which are representative and leading companies in their respective industries with publicly disclosed and relatively reliable performance data. Manufacturing companies also pay more attention to and rely on the improvement of organizational efficiency. In this study, 2010 to 2020 is chosen as the designated study period, and the chosen time period includes longer durations, thus allowing for the examination of dynamic effects and ensuring the real-time nature of the data. The data used for the explanatory and control variables were obtained from the annual reports of Hong Kong and A-share listed companies. On the contrary, the data for dependent and intermediate variables were obtained from the financial statements of listed companies, ensuring accuracy, consistency and comparability of the data.

For missing values, this study used list wise deletion to remove samples with large areas of missing values to ensure the completeness of the sample. To improve the robustness of regression estimation, all continuous variables were processed (percentile method) to reduce the effect of 5% of very large and very small values. After data processing, based on the SCM model requirements, this study constructs two types of samples: (1) Longitudinal samples. Dozens of enterprises in a certain industry are selected, and panel data of different years are used for time series analysis; (2) Horizontal sample. Select representative enterprises in different industries, single year or less year data, for horizontal comparison, these two types of samples contain both dynamic changes and industry-wide representation, providing a solid empirical basis for subsequent model testing and inference.

Empirical Results and Analysis

Descriptive Statistics of Variables

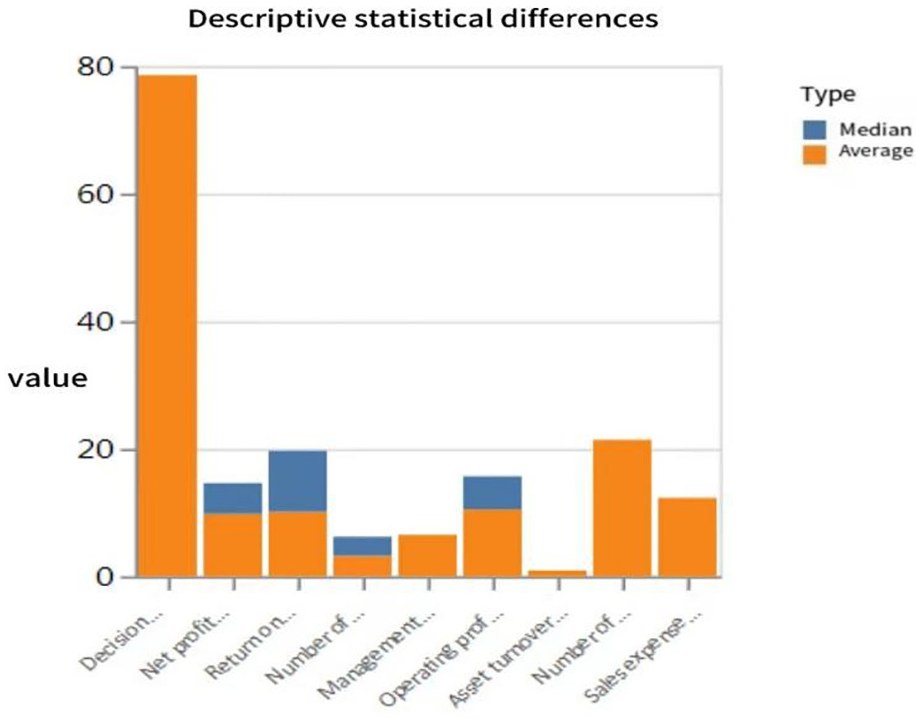

As can be seen from Table 1, the three measures of the explanatory variable organizational structure change are relatively close to each other, indicating that the sample enterprises have pushed to carry out more consistent structural change measures. Specifically, the mean value of the number of management levels is 3.2, and the median is 3, indicating that most of the enterprises are controlled at 3 to 4 levels, with a flatter structure (Adna & Sukoco, 2020); the mean value of the degree of decision-making authorization reaches 78.6%, suggesting that the middle and lower-level and middle-level managers have stronger autonomous decision-making power; and the mean value of the number of departments is 21.4, suggesting that the enterprises have made full use of modularization and business units to rationalize the internal organization. All these indicators show that the sample enterprises have carried out more adequate flat reforms and modular restructuring.

Descriptive Statistics of Variables.

As can be seen from Figure 2, The higher mean and median of the three indicators of the explanatory variable firm performance indicate that the sample firms have better overall operating efficiency and a certain level of profitability (Bartels & Weiss, 2019). For example, the return on net assets is close to 10%, which is at a higher position in the industry. The large standard deviation of operating profit and net profit says that there is a certain difference in performance between enterprises, and control variables need to be introduced to distinguish their effects.

Differences in descriptive statistics.

The values of the three measures of operational efficiency for the intermediary variable are relatively stable, saying that companies are relatively close to each other in terms of overhead control and asset operational efficiency, and that operational efficiency is more synchronized overall (Chebbi et al., 2020). Lower selling expense ratios and management expense ratios also indicate a higher level of cost control during operations.

In summary, the descriptive statistics of the variables lay the foundation for the model analysis. The high degree of organizational structure change and more stable operational efficiency provide ideal conditions for testing the impact of change on corporate profitability indicators. The subsequent model will deeply test the influence path of organizational structure change on enterprise performance.

Variable Correlation Analysis

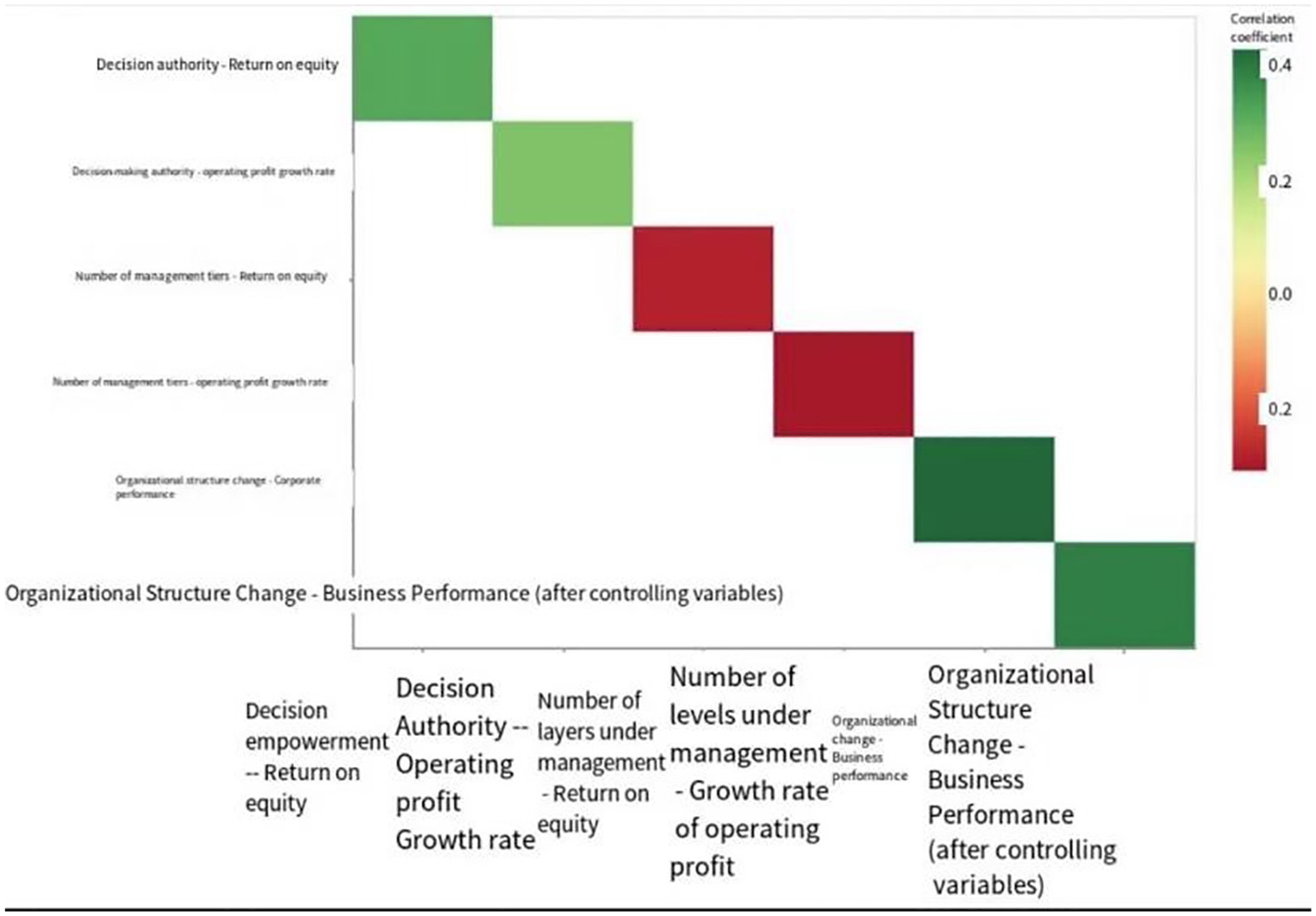

On the whole (as shown in Table 2), the correlation coefficient between organizational structure change and corporate performance reaches 0.428 (p < .01), indicating that there is a significant moderate positive correlation between these two variables, verifying the positive effect of pushing for structural change on enhancing corporate profitability (Chen & Kim, 2023). Specifically for each measure, the reduction in the number of management levels is significantly and positively correlated with both operating profit and return on net assets; the decentralization of decision-making is also significantly and positively correlated with these two performance indicators. This suggests that the flattening of the organizational structure and the delegation of authority at the grassroots level can indeed promote the improvement of corporate profitability.

Variable Correlation Analysis.

After the introduction of control variables (as shown in Figure 3), the partial correlation coefficient between organizational change and firm performance remains significant and slightly increases, from .428 to .392.This suggests that the positive effect of change on performance is robust and is not a mixed effect due to other factors such as size or industry differences. Organizational change does enhance firms’ profitability by improving internal management and resource allocation. This provides strong evidence to support the setting of the hypotheses of this study. It is also noted that although the correlation between performance indicators and structural change is more pronounced, the correlation coefficients range between 0.26 and 0.42, which is a medium strength level, which on the one hand suggests that change can indeed affect performance, but the path of the effect may be characterized by a more complex underlying mechanism.

Heat map of the correlation matrix.

SCM Model Test

A Test of the Direct Impact of Organizational Change on Firm Performance

Table 3 shows the direct impact test of the structural equation model used in the survey on the effect of organizational change on firm performance. The overall model fit is good,

Direct Effect of Organizational Change on Firm Performance.

After controlling for other variables, the path coefficient of the effect of organizational change on firm performance, c’, is still significantly positive and has a magnitude of 0.389 (Guo & Xu, 2021). This implies that, other things being equal, a 1 standard deviation increase in the degree of organizational change is expected to directly bring about a 0.389 standard deviation increase in the firm's performance indicators. The higher path coefficients and significance at the 1% level demonstrate that change can create a strong positive push on corporate profitability. Hypothesis 1 holds under the model test. This finding is contrary to the traditional view that changes in organizational structure can not only improve the effectiveness of business operations, but can also directly affect the ultimate performance of the firm. Initiatives such as flattening, modularization and process re-engineering create higher profitability for firms by improving the effectiveness of organizational operations. This validates the principle that change simplifies management and improves efficiency. Companies should focus on improving and enhancing the profitability of the company through organizational restructuring.

Tests for the Mediating Role of Operational Efficiency

Table 4 reports the mediation effect test of operational efficiency in the study. The paths of organizational change on operational efficiency and firm performance are both significantly positive (Hoa & Anh, 2024); while the coefficient of change on performance decreases from 0.389 to 0.213 after the addition of the mediator variable, proving that operational efficiency plays a partial mediating role. The mediating effect accounts for 55% of the total effect, exceeding the 20% criterion for determining mediating efficacy. The direct effect of change on firm performance remains significant and it can be argued that the implementation of restructuring has the potential to directly improve firm profitability by streamlining operations, reducing expenditures and enhancing resource allocation. This validates Hypothesis 1. On the other hand, change-optimized operational efficiency can also contribute to firms' achievement of higher sales scales and asset efficiency, which in turn improves profitability, which validates the mediating path Hypothesis 2 (as shown in Figure 4).

Mediation Effect Test for Operational Efficiency.

Path diagram of the impact of organizational change on firm performance.

The robustness examination of Sobel’s test and Bootstrap method also provides further evidence that the partial mediating effect of operational efficiency in structural change for firm profitability is solid. This suggests that the mechanism by which organizational structural change can indirectly affect firm performance by improving operational efficiency is statistically valid. Specifically, firms can reduce management levels, optimize departmental settings, and increase grassroots authority by adjusting internal organizational relationships, taking initiatives such as flattening, modularization, and business process re-engineering to improve effectiveness in all aspects of management and business operations, reduce management operating costs and operating expenses, and enhance asset use efficiency and output levels. These improvements in operational efficiency can aggregate the synergies of cost control and synergy, and together drive the overall profitability and core performance indicators of the enterprise to improve. Multiple robustness tests in this study also confirm that this mediating mechanism of operational efficiency in the path of structural change affecting performance is reliable and is not affected by the definition or measurement of specific variables. This provides a decision basis for company management to focus on operational efficiency when promoting organizational change.

Robustness Tests

As can be seen from Table 5 in this study, the model was subjected to various rigorous tests to assess the reliability of the findings. Alternative indicators such as number of management levels and degree of flattening were used to refit the model and the result was that the positive effect of organizational change on firm performance remained significant (Weber et al., 2022). This indicates that the main findings are not affected by the definition and measurement of particular variables. The study then compares the difference in effects in samples with high and low growth periods (as shown in Figure 5). The findings suggest that the effect of change on performance is particularly pronounced during the accelerated expansion phase of the industry in which the firm operates. This may be due to the fact that the high-growth environment provides room for firms to make organizational adjustments and also allows the positive effects of structural change to be fully amplified. This study deals with outliers in the regression model, for example, using percentile and Venn Diagnostics. The main findings remain robust. This suggests that the findings obtained are less susceptible to extreme data or exogenous variables.

Summary of Robustness Tests.

Robustness comparison of model path coefficients.

Prerequisites for Statistical Tests

In conducting the above statistical tests, the study ensured that the following prerequisites were met to ensure reliability and validity of the results:

Normality test: the normality of the variables was tested through the Shapiro-Wilk test. The results showed that the variables conformed to normal distribution, ensuring the validity of the statistical tests.

Linear relationship test: the linear relationship between the variables was verified through scatter plot and correlation analysis. The scatterplot showed that there was a clear linear trend between the variables, and the results of correlation analysis supported this conclusion.

Multicollinearity test: the variance inflation factor (VIF) test was used to ensure that there is no serious problem of multicollinearity among the explanatory variables. the VIF values were all less than 5, indicating that the multicollinearity is within the acceptable range.

Sample size adequacy test: the sample size of this study is 300 listed companies, which meets the sample size requirements of structural equation modeling and mediation effect analysis and ensures the stability and reliability of the model.

Independence test: the independence between the sample data is verified by Durbin-Watson test. the DW value is close to 2, indicating that there is no significant autocorrelation problem between the sample data.

Interpretation and Comparison of Research Findings

Interpretation of the Mechanism by Which Organizational Change Directly Affects Enterprise Performance

Organizational structure change can directly have a positive impact on enterprise performance, and its intrinsic mechanism is to enhance the operational capacity and competitive strength of enterprises through optimizing resource allocation, streamlining management processes, improving decision-making efficiency, enhancing operational capacity and stimulating employee motivation and other aspects (Verhoef et al., 2021). Specifically, by reducing organizational layers, flat management makes information transmission more rapid and accurate, avoids delays and distortions caused by layer-by-layer transmission, and helps enterprises deploy resources more efficiently, reduce resource wastage, and improve the efficiency of resource use. Alnoor (2020) point out that flat management can significantly improve the resource allocation efficiency of enterprises and the information flow speed. Flat and modular management simplifies internal approval and decision-making processes, reduces communication costs between management levels, improves the timeliness and accuracy of decision-making, and enables enterprises to respond faster and seize market opportunities in a timely manner in the face of market changes. Huang & Li (2022) similarly found that simplifying management processes can effectively improve the decision-making efficiency and market responsiveness of enterprises. Increased decision authorization gives more autonomy to grassroots teams, making decisions closer to frontline realities and improving execution efficiency and innovation. This argument is confirmed by Pengyu Chen, SangKyum Kim that an increase in decision authorization significantly enhances an organization’s innovation and execution efficiency. In addition, modular organizational structure optimizes departmental functions according to business processes and product lines, concentrates professional resources, clarifies division of labor and collaboration, facilitates synergistic effects, improves the efficiency of production operations and supply chain management of enterprises (Ouedraogo et al., 2024), and shortens the whole process time from design to delivery of products.Jones and Kim show that modular organizational structure can significantly enhance the operational efficiency and market competitiveness. The above change measures effectively integrate internal resources, cut redundancy and inefficiency, improve resource use efficiency, and optimize the whole process operation of product development, marketing and supply chain, making the operation and control of the enterprise more efficient, flexible and faster. The above change measures have enhanced the overall competitiveness of the enterprise and won a larger market share and profit margin for the enterprise, which is directly reflected in the improvement of core performance indicators such as revenue and profitability. This argument is also supported by empirical studies by Fan Gao, & Bo Weng, who found that organizational change can significantly improve the financial performance of firms.

Deeper Explanation of the Mediating Role of Operational Efficiency

Operational efficiency plays a partly mediating role in the process of organizational structure change affecting enterprise performance, and its intrinsic path is that the change contributes to the increase of enterprise profit level by improving the operational efficiency of each link. Flattening and modularization of the organizational structure optimizes the internal management and decision-making processes and cuts down on redundant and inefficient links, thus reducing the operating cost expenditures of multiple functions such as marketing, production and management, and leading to an increase in the operational efficiency of the firm in terms of the selling expense ratio and the administrative expense ratio. This argument is similar to the findings of Magno (2024) and Bohmer (2019) that organizational change can significantly reduce a firm’s operating costs and improve overall effectiveness. A clear division of labor and efficient cross-departmental collaboration after the change is conducive to improving the efficiency of production operations and supply chain operation, shortening the time of the whole process from product design to delivery, and improving the efficiency of the use of corporate assets and the speed of turn around. Kamble (2020) and Shah (2020) research confirms that the division of labor and synergistic collaboration after the structural change can significantly improve the production efficiency and the effectiveness of the supply chain management. Flat management gives greater autonomy and decision-making power to the grassroots, stimulates employee ownership, enhances labor efficiency and output quality, and further improves overall operational efficiency. In summary, the improvement of operational efficiency is reflected in the improvement of profitability indicators such as corporate profitability and return on net assets, which becomes an important mediating path for organizational change to affect corporate performance. This finding not only validates the original purpose of the change, which is to “reduce costs and increase efficiency” in order to improve profitability, but also provides key leverage for firms to optimize their performance on a sustained basis.

Comparison of Differences Between the Findings of This Study and Previous Studies

The findings of this study on the relationship between organizational restructuring, operational efficiency and firm performance are significantly different and innovative from previous studies. The traditional view is that organizational restructuring mainly affects the internal operational efficiency of firms, while the impact on the final financial performance is insignificant. However, this study finds that rational organizational change not only optimizes management processes and integrates resources to improve operational efficiency, but also directly positively affects core performance indicators such as operating profit margin and net profit margin. This finding challenges the traditional notion that structural change only affects intermediate processes and cannot be reflected in profit performance, and expands the path of change on corporate value creation. Although the studies of Laamanen (2019) and Guenther (2023) also focus on the impact of organizational change on operational efficiency, they do not explore its direct effect on financial performance. The findings of this study fill the aforementioned research gap.

Established studies have focused more on the direct impact of operational efficiency on firm performance, but less on the mechanism of its role in the relationship between structural change and performance. This study not only verifies the partial mediating effect of operational efficiency in the relationship between the two, but also further analyzes the specific path of this mediating effect, i.e., how the change promotes profit growth by improving the operational efficiency of each segment. Although the studies of Burnes (2020) have addressed the impact of operational efficiency on firm performance, they have limited exploration of the mediating mechanism. This study enriches the endogenous theory of the mediating path of operational efficiency by analyzing this mediating mechanism in detail, providing a new perspective for firms to formulate organizational optimization and performance management strategies. The rigorous robustness test ensures the reliability of the conclusions and innovations found in this study, which further enhances the credibility of the study and provides a valuable addition to existing theories and practices.

Theoretical and Practical Implications of This Study’s Findings

This study’s finding that organizational change directly affects firm performance and that operational efficiency plays a partly mediating role in it, makes an important extension and addition to existing theories.

Based on the analysis of theoretical significance, this study challenges the traditional view that organizational change only affects the internal process but cannot be reflected in the final performance, reveals the path of structural adjustment that directly contributes to profitability, and enriches the theoretical perspective of the relationship between change and corporate value creation. By analyzing the mediating mechanism of operational efficiency in the relationship between organizational change and firm performance, this study unravels the logic behind this “black box” and enriches the endogenous theory of the mediating effect. In addition, the innovative findings of this study not only fill the research gaps in the related fields, but also provide new evidence support for the application of organizational theory in explaining the process of corporate value creation and further improve the related theoretical system.

Based on the analysis from the perspective of practical significance, the results of this study are of great revelation and guiding significance to the organizational management practice and performance management decision-making of enterprises. The study directly verifies that appropriate organizational changes are conducive to improving corporate profitability, which provides strong evidence for companies to implement structural innovations such as flattening and modularization, and lays the basis for companies to assess the benefits of change. The study emphasizes that operational efficiency is an important lever of corporate performance and reveals ways to improve operational efficiency, providing directional guidance for the company to continuously optimize cost control and efficiency improvement in all segments. The mediating role of operational efficiency between change and performance is found, suggesting that companies should pay simultaneous attention to the optimization of operational efficiency when formulating restructuring and performance management strategies as an important part of achieving change objectives and performance improvement. Based on the above theoretical and practical contributions, this study provides a scientific basis for corporate management to help them define clearer goals and paths when promoting organizational change, so as to achieve higher corporate performance.

Conclusions and Recommendations

Conclusions

By constructing a structural equation model, this study empirically analyzes the path and internal mechanism of organizational structure change on enterprise performance, and draws the following main conclusions: First, reasonable changes in organizational structure have a direct contributing effect on enhancing the profitability of enterprises. Adjustment measures such as flat management and modular transformation significantly improve the core performance indicators such as operating profit margin, net profit margin, and return on net assets by optimizing resource allocation, simplifying decision-making process, and improving execution efficiency. This finding breaks through the traditional viewpoint and confirms that structural change not only affects the internal operation of enterprises, but also directly creates economic value and wins more profit growth space for enterprises, which expands the influence of structural optimization on the path of enterprise value creation from the theoretical level (Collins et al., 2022). Second, operational efficiency plays a partly intermediary role in the process of organizational change for enterprise performance improvement. Structural adjustment reduces operating cost expenditures and enhances the efficiency of asset utilization and output quality by improving the operational efficiency of sales, management, asset use and other aspects, which in turn promotes the overall improvement of performance indicators such as profitability. The mediating effect of operational efficiency validates the desired goal of pursuing “cost reduction and efficiency enhancement” in order to improve profitability, and enriches the application of operational efficiency as an operating lever in promoting performance management. Third, the main findings of this study have been subjected to rigorous robustness tests, such as multiple substitution variables, different business environments, and outlier control, and the results are still statistically and economically significant, indicating that the conclusions have good reliability and applicability, and laying a strong theoretical foundation for enterprises to formulate organizational optimization and performance management strategies.

Recommendations

Based on the above findings, this paper proposes the following recommendations that are important insights for organizational management practices and performance management decisions in enterprises.

First, enterprises should vigorously promote the optimization of organizational structure changes to break through the rigid management pattern. This study confirms that measures such as flattening and modularization adjustment can directly promote the improvement of corporate profit level, which provides strong support for companies to implement similar changes. Specifically, at the management level, the company should proceed to compress layers, decentralize power, clean up redundant positions, and build a flat and efficient operation system (By et al., 2020); at the business level, the departmental settings should be adjusted around the product line or core processes to form an organizational form in which each professional module works closely together. At the same time, management process optimization and resource integration is the top priority of the change, the company needs to re-engineer the internal control and resource allocation model as a whole, to fully tap the potential of quality and efficiency.

Secondly, organizational change needs to be gradual and risk-averse. Change involves fundamental adjustments to the operation of the company and the rights and interests of its personnel, and is prone to cause organizational turmoil and cultural conflict. Therefore, the company needs to scientifically assess the gap between its own status quo and its goals, benchmark advanced practices to formulate a phased roadmap for change, and strictly control the magnitude of adjustment to prevent excessive impact (Kotter, 2021). At the same time, it is necessary to track the effect of feedback in a timely manner, and take measures to mitigate potential risks and warnings. During the change period, the company should also increase staff training to eliminate the sense of discomfort and motivate the grassroots managers and technical staff to participate actively in order to form a wide range of recognition and support for the change.

Third, continuously optimize operational efficiency and leverage performance. Research shows that operational efficiency is an important leverage point for corporate profit level and a key intermediary link that affects the effect of organizational change. Therefore, the Company should incorporate the assessment of operational efficiency into normalized management, establish a performance assessment system covering all departments, business lines and production links, implement refined management, and continue to tap into the space for cost savings and asset utilization enhancement. At the same time, it is necessary to closely link the operational efficiency indicators with the internal business units and individual remuneration performance, forming a top-down.

Limitations of the Study and Future Research Directions

Despite the useful theoretical and practical contributions of this study, there are still some limitations. First, the sample of this study is mainly from a particular region and industry and may not be fully representative of other regions or industries. The culture of different regions and the characteristics of specific industries may have different impacts on the effects of organizational change, so future research can expand the sample to cover more regions and industries to enhance the generalizability of the findings. Second, this study mainly focuses on financial performance indicators and does not explore in depth the effects of organizational structure change on non-financial performance (e.g., employee satisfaction, customer satisfaction, etc.). Future research can combine qualitative and quantitative methods to comprehensively assess the multidimensional effects of organizational change, thus providing more comprehensive management recommendations for enterprises. In addition, this study assumes that organizational change is a linear process, but non-linear or complex characteristics may exist in actual change. Future research can explore the dynamic mechanisms and stage-by-stage effects of the change process in order to analyze the whole process of change and its continuous effects on performance in a more detailed way.

The existence of research limitations in this paper provides a direction for future research, and through further exploration and refinement, the relationship between organizational change and corporate performance can be more comprehensively understood, providing richer references for corporate management and theoretical research.

Footnotes

Ethical Considerations

The authors declare that the research was conducted in the absence of any animal and human studies.

Consent for Publication

Consent to publish by all authors.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data will be made available on request.