Abstract

This study conducted in-depth analysis using a random effects panel data analysis method, utilizing a comprehensive dataset of financial companies listed on the Shanghai and Shenzhen stock exchanges from 2001 to 2022 to investigate the impact of financial technology on the performance and risk of Chinese financial institutions. Based on data from financial companies listed on the Shanghai and Shenzhen stock exchanges between 2001 and 2022, the study found that while financial technology had no significant effect on return on assets (ROA), it significantly improved the liquidity ratio (LR). This finding suggests that although the advantages of financial technology in enhancing operational efficiency and risk management do not directly translate into immediate profitability, they do lead to significant improvements in liquidity management. The study underscores the crucial role of financial technology in the evolution of the financial sector and emphasizes the necessity of establishing a balanced regulatory framework, enhancing education, and promoting deep integration between financial technology and traditional financial services. Through robustness checks, this study ensures the reliability of its findings.

Introduction

The financial services landscape in China has been undergoing a transformative evolution, largely attributed to the advent of Financial Technology (FinTech). Originating as a disruptive force globally in the wake of the 2008 financial crisis, FinTech has become a central pillar in China’s financial ecosystem (Arner et al., 2015; Lee & Shin, 2018). Initially confined to startups offering specialized services such as mobile payments and peer-to-peer lending, FinTech’s scope in China has exponentially expanded to include a wide array of applications, from blockchain and artificial intelligence to data analytics and cybersecurity (Guo & Liang, 2016; Varma et al., 2022).

Several factors have catalyzed the meteoric rise of FinTech in China. The ubiquity of smartphones and the proliferation of high-speed internet have democratized access to financial services, thereby reducing the dependency on traditional financial institution infrastructure (Claessens et al., 2018). This technological democratization has been particularly appealing to China’s burgeoning middle class, a demographic inherently comfortable with digital technology and often skeptical of traditional financial institutions (Demirguc-Kunt et al., 2018). Furthermore, regulatory frameworks in China have been relatively flexible, fostering an environment conducive to FinTech innovation and competition (Zetzsche et al., 2017).

The implications of FinTech on the performance of financial institution in China are multifaceted and nuanced. On one hand, FinTech has introduced operational efficiencies through automation, thereby reducing costs and enhancing profitability (Dwivedi et al., 2021; Torre Olmo et al., 2021). Moreover, the utilization of advanced algorithms and machine learning has enabled banks to offer personalized services, augmenting customer satisfaction and engendering brand loyalty (Almulla & Aljughaiman, 2021). On the other hand, the emergence of FinTech platforms specializing in niche services has intensified competition, compelling traditional banks to innovate or risk becoming obsolete (Claessens et al., 2018).

However, the integration of FinTech into China’s financial institution is not without its challenges. The digitalization of financial services has escalated cybersecurity risks, including data breaches and fraudulent activities (Arner et al., 2015; Varma et al., 2022). Regulatory challenges also abound, particularly concerning data protection, financial stability, and consumer protection (Zetzsche et al., 2017). The rapid pace of technological advancements necessitates continual system updates, adding to operational costs and complexities (Lee & Shin, 2018).

FinTech serves a dual role as both an enabler of innovation and a disruptor of traditional banking models in China (Lee & Shin, 2018). While it has facilitated the provision of more efficient and customer-centric services, it has also led to market fragmentation and new forms of collaboration and competition (Claessens et al., 2018). Furthermore, FinTech has the potential to advance financial inclusion but also poses risks if not regulated properly, as highlighted by the World Bank (2018).

The FinTech revolution has engendered a complex interplay of opportunities and challenges for the financial institutions in China. While it has acted as a catalyst for operational and strategic innovation, it has concurrently introduced a new risk paradigm that necessitates meticulous management and regulatory oversight. Despite the burgeoning literature on this subject, there exists a research gap in empirically investigating the nuanced impact of FinTech on both the performance and risk profiles of financial institutions in China. This thesis aims to fill this gap by providing a comprehensive empirical analysis from China on the impact of FinTech on financial institution performance and associated risk factors.

The marginal contribution of this study lies in three key areas. Firstly, it provides a micro-level quantitative analysis of FinTech’s impact on financial institutions, contrasting with the predominantly qualitative or macroeconomic-level research found in prior studies. Secondly, the study introduces an innovative approach to measure FinTech development by analyzing the frequency of related keywords in financial reports, offering a systematic and novel way to assess FinTech adoption. Lastly, it highlights important theoretical and policy implications, revealing FinTech’s positive effect on liquidity management and its complex impact on profitability. These contributions collectively enhance our understanding of FinTech’s role in shaping financial institution performance and risk management.

Literature Review and Hypotheses Development

Literature Review

In the contemporary economic landscape, traditional financial institutions play a central role in providing essential financial services and supporting economic development. However, with the rapid advancement of financial technology (FinTech), these institutions face unprecedented challenges and opportunities. The emergence of FinTech has not only reshaped service delivery methods and improved operational efficiency but also introduced new competitors, altering market dynamics (Vučinić, 2020; Xie, 2023). This transformation has profound implications for the profitability and risk management of traditional financial institutions, prompting them to reevaluate their business models and strategies.

In existing literature, there has been extensive research on factors influencing the profitability and risk of financial institutions. From macro and micro perspectives, these factors can be broadly categorized as follows:

From a macro perspective, the profitability of traditional financial institutions is influenced by various macroeconomic factors, including economic growth rate, interest rate environment, inflation rate, and policy and regulatory environment (Climent-Serrano & Pavía, 2015; McKillop et al., 2020; Yao et al., 2018). Firstly, the economic growth rate directly affects the demand for loans and investment returns of financial institutions. During periods of economic expansion, increased financing needs of businesses and individuals stimulate loan growth and improve asset quality, thereby enhancing the profitability of financial institutions (Nasreen et al., 2020). Secondly, the interest rate environment significantly impacts the Net Interest Margin (NIM) of financial institutions (Brei et al., 2020). Rising interest rates typically imply higher borrowing costs but also offer higher returns on deposits and loans. Financial institutions need to adeptly manage interest rate risk to maintain profitability stability. Inflation rate is also a key factor, affecting both the purchasing power of currency and the possibility of interest rate adjustments (Ozili & Ndah, 2021). In a high inflation environment, financial institutions may face risks of cost escalation and deteriorating asset quality, but may also leverage increasing loan rates to boost income. Finally, changes in policy and regulatory environments directly influence the operational modes and profit opportunities of financial institutions (Cui et al., 2020). For example, stringent regulatory policies may increase compliance costs for financial institutions, while loose monetary policies may promote loan growth and asset price appreciation.

In the globalized financial system, macroeconomic factors have a significant impact on the risk management of traditional financial institutions. These macroeconomic influences primarily include volatility in global financial markets, changes in macroeconomic policies, and international trade and political events (Nahar et al., 2020). Firstly, increased volatility in global financial markets enhances market risk (Widarjono, 2020), affecting the portfolio value and foreign exchange exposure of financial institutions. Significant fluctuations in asset prices, especially in stock and bond markets, may result in substantial unrealized losses, impacting institutions’ capital adequacy and liquidity positions. Secondly, macroeconomic policies, including adjustments in monetary and fiscal policies (Al-Busaidi & Al-Muharrami, 2021), directly influence the operating environment of financial institutions. For instance, central bank interest rate decisions directly affect borrowing costs and investment returns of financial institutions, while changes in fiscal policies may affect economic growth expectations and market confidence, thereby influencing the business prospects of financial institutions. Furthermore, international trade policies and geopolitical events are also significant macro-level risk sources (Abbass et al., 2022). These events may increase market uncertainty, affecting cross-border financial flows and exchange rate fluctuations, thereby introducing additional risks to financial institutions’ cross-border operations. For example, trade wars may lead to economic slowdown in certain markets, affecting external revenue sources and asset quality of financial institutions.

The profitability of traditional financial institutions is not only influenced by macroeconomic factors but also closely depends on a series of micro-level factors such as asset quality, business models and innovation, and cost control. Firstly, asset quality is one of the key indicators for measuring the profitability of financial institutions (Murad et al., 2021). A high-quality asset portfolio can reduce credit losses and enhance the returns on loans and investments. The increase in non-performing loan ratio not only directly erodes profits but also adds additional provisioning costs, putting pressure on the profitability of financial institutions. Secondly, business models and innovation play a decisive role in the profitability of financial institutions (Iheanachor et al., 2021). In today’s rapid development of financial technology, institutions that can leverage new technologies to develop innovative financial products and services, such as providing personalized customer service through digital platforms, often attract more customers, broaden revenue sources, and enhance market competitiveness. Conversely, institutions lacking innovation capabilities may lag behind in competition and lose market share. Cost control is another key factor influencing the profitability of financial institutions (Dong et al., 2020). Effective cost management strategies, including technological automation, optimization of branch networks, and human resource management, can significantly reduce operating costs and improve efficiency. Especially in the current environment of increasingly popular financial technology, reducing costs through technological innovation has become an important way to enhance profitability.

At the micro level, traditional financial institutions face risks primarily stemming from technological risks and security threats, compliance and legal risks, as well as challenges in business transformation. Firstly, technological risks and security threats are increasingly prominent in the digital era (Osmani et al., 2020). With the digitization of financial services, data breaches, cyberattacks, system failures, among others, have become significant risks that financial institutions cannot afford to overlook. These technological risks may not only lead to direct economic losses but also damage the institution’s reputation and customer trust. Secondly, compliance and legal risks also pose significant challenges to financial institutions (Jan et al., 2021). The regulatory environment of financial markets continues to evolve, especially in areas involving the application of financial technology, with new laws and regulations constantly being introduced. Financial institutions need to continuously update their compliance strategies to adapt to these changes; otherwise, they may face risks of fines, business restrictions, or even license revocation. Finally, as financial technology integrates and business models innovate, traditional financial institutions also face numerous challenges in business transformation (Abdulquadri et al., 2021). This includes issues such as technology integration, matching employee skills, and market acceptance of new business models. The uncertainties and potential business interruptions during the transformation period may have short-term impacts on the stability and profitability of institutions.

The rapid development of financial technology, particularly “ABCD” technologies—Artificial Intelligence (AI), Blockchain, Cloud Computing, and Big Data—has profoundly impacted traditional financial institutions. These technologies have played important roles in enhancing the profitability and risk management of financial institutions while also bringing new challenges.

Financial technology has improved the operational efficiency and customer service quality of financial institutions through “ABCD” technologies. AI and Big Data enable financial institutions to accurately identify customer needs and provide personalized services, thereby increasing customer satisfaction, loyalty, and cross-selling opportunities (Mhlanga, 2020). Blockchain technology reduces transaction costs and time, improves the efficiency of fund utilization, and opens up new revenue channels (Kabra et al., 2020). Cloud computing provides flexible computing resources for financial institutions, reducing IT investment and operational costs, enabling institutions to respond to market changes more quickly and seize profit opportunities (Lăzăroiu et al., 2023). However, the application of financial technology may also disrupt traditional business models, affecting existing revenue sources of financial institutions (Fung et al., 2020; Sampat et al., 2024). Particularly, the low-cost, high-efficiency services provided by financial technology innovation companies may attract customers away from traditional financial institutions, thereby affecting their profitability. Additionally, the initial large-scale investment in new technologies may increase cost pressures and impact short-term profitability.

In terms of risk management, AI and Big Data provide powerful tools for financial institutions to achieve more accurate risk assessment and prediction, effectively reducing credit and market risks (Hasan et al., 2020; Königstorfer & Thalmann, 2020). Blockchain technology enhances transaction security and transparency by providing tamper-proof records, helping to reduce operational risks (Patel et al., 2020). The flexibility of cloud computing also supports risk data analysis and disaster recovery, enhancing the overall risk resilience of financial institutions (Stewart, 2022). At the same time, reliance on advanced technology also introduces new risks (Li et al., 2020). For example, data security and privacy become major concerns for cloud computing and big data applications; the opacity of AI decision-making processes may increase compliance risks; the decentralized nature of blockchain technology, while enhancing security, may pose challenges in repair and accountability once issues arise.

After conducting a comprehensive review of existing literature, this study found that most research focuses on qualitatively or macroscopically exploring the impact of financial technology on financial institutions, while there is a relative lack of literature that quantitatively analyzes this impact through empirical research. These studies often emphasize theoretical analysis and case studies, lacking quantitative assessment and empirical verification of the impact of financial technology. Additionally, existing literature also lacks in quantifying the level of development of financial technology, failing to provide a unified and accurate measurement standard, which limits the in-depth understanding of the relationship between financial technology progress and financial institution performance. This study aims to fill these research gaps. By using microdata from listed financial companies, this study not only explores in depth the specific effects of financial technology development on financial institutions but also develops a quantitative measurement method for the level of financial technology development. This method combines the performance of financial technology in different dimensions, providing a new perspective for the comprehensive evaluation of financial technology.

Types of FinTech and Their Impact

FinTech, representing the intersection of finance and technology, encompasses a wide range of innovations that have the potential to reshape the financial landscape. Drawing on the work of Allen et al. (2021), which provides a comprehensive review of FinTech innovations and their policy implications, this study identifies several key types of FinTech and discusses their potential impacts:

Blockchain and Distributed Ledger Technologies: Blockchain technology offers transparency and security through decentralized ledgers, reducing transaction costs and increasing trust in financial transactions. This transparency reduces intermediary costs and enhances operational efficiency, which ultimately can lead to increased profitability for financial institutions.

AI-Based Credit Scoring and Alternative Data: Artificial intelligence and machine learning are revolutionizing credit risk assessment by incorporating alternative data sources, such as social media activity and transaction histories. AI-based credit scoring provides a more precise evaluation of borrowers, leading to reduced default rates and optimized loan portfolios, which contribute positively to financial institutions’ profitability.

Robo-Advising and Quantitative Investment Strategies: Robo-advisors utilize algorithms to provide automated, cost-effective financial advice, enabling financial institutions to reach a broader client base with lower service costs. This contributes to greater financial inclusion and increases profitability through operational efficiencies and cost savings. Robo-advising also helps customers receive more consistent advice, enhancing their investment experience and satisfaction.

Cybersecurity and Fraud Detection: FinTech innovations in identity verification, fraud detection, and anti-money laundering (AML) are improving the security of financial transactions. By reducing fraud and improving compliance with regulatory standards, financial institutions can minimize financial losses and operational risks, thereby enhancing both stability and profitability.

Theories

In order to establish a solid theoretical foundation for understanding the impact of FinTech on financial institutions, this study draws upon three key theories: the theory of financial intermediation, Technological Innovation Theory, and Risk Management Theory. These theories offer different perspectives on how FinTech can influence financial performance and risk management. By integrating insights from each of these theoretical frameworks, the study provides a comprehensive explanation of the mechanisms through which FinTech affects financial institutions. Below is a detailed discussion of each theory and its relevance to the research.

The theory of financial intermediation explains how financial institutions act as intermediaries between savers and borrowers, thereby improving the efficiency of financial markets. According to this theory, financial institutions help reduce transaction costs and information asymmetry by pooling resources from savers and allocating them to borrowers with productive investment opportunities. The theory suggests that financial institutions enhance the allocation of resources in the economy, leading to higher economic growth and development. Allen and Santomero (1997) expanded this theory by emphasizing the role of financial intermediaries in mitigating information problems and reducing risks associated with lending. In the context of FinTech, the theory can be used to explain how technological advancements might further improve the efficiency of financial intermediation by providing better information, lowering transaction costs, and increasing the accessibility of financial services.

Technological Innovation Theory, introduced by Schumpeter in 1934, argues that technological advancements are the primary drivers of economic growth and development. The theory emphasizes that innovations, especially those related to technology, can lead to the creation of new products, services, and processes that improve productivity and efficiency (Ziemnowicz, 2020). In financial services, technological innovations such as blockchain, artificial intelligence, and mobile payment systems can significantly enhance the quality and efficiency of services. This theory supports the idea that the adoption of FinTech could lead to improved financial performance for institutions by reducing costs, expanding market reach, and enabling new revenue models. It provides a theoretical foundation for understanding how technological change can disrupt traditional financial practices and create opportunities for growth.

Risk Management Theory focuses on the identification, assessment, and mitigation of risks within financial institutions. It posits that effective risk management practices are essential for maintaining financial stability and protecting against losses. Merton and Perold (2008) contributed to the theory by discussing how financial innovations and risk management tools can help institutions manage risks more effectively. In the context of FinTech, Risk Management Theory suggests that technologies such as big data analytics, artificial intelligence, and real-time monitoring systems can enhance the ability of financial institutions to predict and manage risks. By improving the precision of risk assessments and the speed of responses to potential threats, FinTech can play a crucial role in reducing systemic risk and enhancing the overall stability of the financial system.

Hypotheses

To better understand the impact of FinTech on financial institutions, it is crucial to establish clear research hypotheses grounded in theoretical analysis and prior empirical findings. The hypotheses developed in this study are based on three key theories: the theory of financial intermediation, Technological Innovation Theory, and Risk Management Theory. These theories collectively help explain the mechanisms through which FinTech may influence financial performance and risk management. By building on these foundational insights, the hypotheses provide a structured approach for examining FinTech’s influence on financial institutions’ profitability and liquidity.

Based on the above theories, the study proposes two main hypotheses:

Hypothesis 1 (H1): The application of FinTech has a significant positive impact on the profitability (ROA) of financial institutions. The theoretical rationale is that FinTech can enhance profitability by improving operational efficiency and broadening revenue streams.

Hypothesis 2 (H2): The application of FinTech significantly improves the liquidity management capability (LR) of financial institutions, thereby reducing liquidity risk. This is supported by Risk Management Theory, which suggests that advanced technological tools can enhance the efficiency of fund flows.

Methodology and Models

Data Sources

The study utilizes data from listed financial companies on the Shanghai and Shenzhen stock exchanges from 2001 to 2022 as the initial research sample. The data underwent the following treatments: firstly, financial enterprises were retained; secondly, samples labeled with “ST” and those delisted during the period were excluded; thirdly, companies conducting IPOs within the observation period were excluded; fourthly, to mitigate the impact of outliers, this study trims all continuous variables at the micro level at the 1% and 99% levels. The original data were sourced from the China Stock Market & Accounting Research (CSMAR) Database, while relevant corporate annual report data were obtained from the official websites of the Shenzhen Stock Exchange and the Shanghai Stock Exchange.

After data cleaning and organization, this study ultimately employed panel data consisting of 57 Chinese listed financial enterprises from 2001 to 2022 as the research subjects.

Explained Variables

This study selected two dependent variables to assess the impact of financial technology on financial institutions, namely profitability and risk management capabilities. For the profitability indicator, this study chose Return on Assets (ROA). ROA serves as a crucial metric for measuring the profitability of financial institutions, reflecting their efficiency in managing assets and generating profits (Siniţîn & Socol, 2020). Compared to other profitability indicators such as net profit margin or Return on Equity (ROE), ROA provides a more neutral measurement standard as it considers the scale and efficiency of company assets rather than just the utilization of shareholder equity. This renders ROA a more comprehensive and impartial indicator for assessing the profitability of financial institutions, particularly suitable for comparative studies across institutions or time periods. Therefore, selecting ROA as a measure to evaluate the impact of financial technology on the profitability of financial institutions can more accurately reflect the overall impact of financial technology on their profitability.

For the risk management indicator, this study chose the liquidity ratio as a key metric to assess the risk management capabilities of financial institutions (Ahamed, 2021). Among numerous risk measurement indicators, one reason for selecting the liquidity ratio is its relatively good quantifiability and ease of measurement in available data. Liquidity risk is one of the primary risks faced by financial institutions, affecting their short-term solvency and the flexible utilization of funds. Selecting the liquidity ratio as an indicator for risk management can effectively reflect financial institutions’ ability to cope with fund shortages and market fluctuations. Furthermore, compared to other risk indicators such as credit risk and market risk, the liquidity risk measurement indicator is more intuitive and feasible in existing data, which is crucial for the operationality and accuracy of empirical research. By analyzing the liquidity ratio, this study can offer deep insights into the impact on financial institutions’ risk management capabilities, particularly in the current rapid development of financial technology, and how financial institutions address challenges and risks by enhancing liquidity management.

Core Explanatory Variable

The core explanatory variable in this study is the level of financial technology development. The core explanatory variable in this study is the level of financial technology development, represented by the natural logarithm of the frequency of financial technology-related terms, denoted as “LnFT.” Specifically, “LnFT” is calculated based on the frequency of keywords related to financial technology—such as Artificial Intelligence (AI), Blockchain, Cloud Computing, and Big Data—extracted from the annual reports of listed financial institutions. This frequency is logarithmically transformed to correct for skewness, which is typical in count data. The keywords were identified based on relevant academic discussions, and the data was collected using Python to extract and count these terms from the annual reports, excluding terms that were not directly related to financial technology. These four key technologies have profound impacts on the operational models and performance of Chinese financial institutions. These technologies not only promote the improvement of profitability of financial institutions but also have important impacts on liquidity management, thereby affecting the Return on Assets (ROA) and Liquidity Ratio (LR) of institutions.

Financial technology significantly influences the ROA of Chinese financial institutions. While the application of these technologies promotes profitability in various aspects, it also brings negative impacts, exerting pressure on the ROA of financial institutions. Artificial Intelligence and Big Data, through efficient data processing and analytical capabilities, help financial institutions improve the accuracy of loan decisions, reduce default rates, thereby increasing asset returns. Additionally, the application of these technologies enhances customer service and personalization of products, increases customer stickiness, and positively impacts the increase of non-interest income of financial institutions. The application of Blockchain technology reduces transaction costs, improves the efficiency of fund circulation, especially in cross-border payments and supply chain finance fields, and opens up new revenue channels. Cloud computing provides scalable computing resources for financial institutions, reducing investment and maintenance costs of IT infrastructure, enabling institutions to respond to market changes more flexibly, which is conducive to improving ROA.

However, the application of financial technology also negatively affects the ROA of financial institutions. Firstly, the high cost of technological investment. Although technological investment can improve efficiency and profitability in the long run, the massive investment in technology research and application in the short term will significantly increase the cost burden of financial institutions, compress profit margins, and negatively impact ROA. Secondly, rapid technological updates lead to asset depreciation. With the rapid development of financial technology, financial institutions must continuously update technological equipment and software to maintain competitiveness, which may lead to rapid depreciation of existing technological assets, increase depreciation and amortization costs, further affecting ROA. Additionally, technological risks cannot be ignored. The application of financial technology, especially Blockchain and cloud computing, increases the dependence of financial institutions on technology. Once technical failures or data security incidents occur, they will not only cause direct economic losses but also damage customer trust, affect institutional reputation, and indirectly have negative impacts on ROA. Lastly, intensified market competition. Financial technology reduces market entry barriers, attracting more non-traditional financial competitors, such as technology companies and financial technology startups, to enter the financial services field. These newcomers often have stronger technological advantages and lower operating costs, intensifying market competition, squeezing the market share and profit margins of traditional financial institutions, and negatively impacting ROA.

The application of financial technology also has a positive impact on liquidity management of financial institutions. Big Data technology enables financial institutions to more accurately predict market trends and customer behavior, optimize fund allocation, and improve fund utilization efficiency. Through accurate liquidity demand forecasting, financial institutions can reasonably arrange short-term and long-term funds, maintain a high liquidity ratio, and reduce liquidity risks. The flexibility and scalability of cloud computing provide financial institutions with the ability to respond to emergencies, such as rapidly increasing computing resources when funds are needed, processing a large number of transactions, and ensuring stable liquidity. Additionally, financial services on cloud platforms can achieve more efficient fund circulation and management, which is conducive to improving liquidity ratios. The application of Blockchain technology in improving payment and settlement efficiency reduces transaction settlement time, accelerates fund liquidity, and is of great significance to improving the liquidity management capabilities of financial institutions. Through Blockchain technology, financial institutions can achieve real-time clearing of funds, improve fund utilization, and improve liquidity ratios.

Currently, research on the level of financial technology development in China is mostly qualitative analysis. Some scholars use the Digital Financial Index of Peking University as a measure of the level of financial technology development, but this index can only reflect the level of financial technology development in regions from a macro perspective. In comparison, measuring the level of financial technology development from the micro perspective of enterprises requires exploring a new method. This study refers to the method used by Han et al. (2017), who paired and selected keywords, and statistically counted the cumulative number of corresponding industrial policy documents in each province and city as a characterization index of industrial policy intensity. This study measures the level of enterprise financial technology development by the frequency of corresponding keywords in annual reports disclosed by listed companies, serving as a proxy indicator for enterprise financial technology development level. From a technical perspective of variable design implementation, this study collected and organized annual reports of all A-share listed financial industry companies on the Shanghai Stock Exchange and Shenzhen Stock Exchange using Python crawler functionality, and extracted all text content using the Java PDFbox library, using this as a data pool for subsequent keyword filtering. In determining financial technology feature words, this study, based on academic discussions, identified Artificial Intelligence (AI), Blockchain, Cloud Computing, Big Data, and related content as keywords. Finally, based on Python, this study searched, matched, and counted word frequencies based on feature words in annual report texts of listed companies, then classified and collected word frequencies of key technology directions, and finally formed the total word frequency, thereby constructing an indicator system for enterprise digital transformation. Since this type of data has typical right-skewed characteristics, this study logarithmically processed it to obtain an overall indicator depicting enterprise digital transformation.

Control Variables

When assessing the impact of financial technology on the Return on Assets (ROA) and liquidity ratio of financial institutions, considering the significant influence of financial condition and operational efficiency of financial institutions on their profitability and risk management capabilities, this study selected the leverage ratio (LEV), cash flow ratio (Cashflow), accounts receivable ratio (REC), and inventory ratio (INV) as control variables. The following elaborates on the potential impacts of these control variables on ROA and liquidity ratio:

The leverage ratio (LEV) measures the proportion of total liabilities to total assets of financial institutions, reflecting the institution’s financial leverage level (Barth & Miller, 2018). A higher leverage ratio implies a higher debt burden, which may lead financial institutions to sacrifice investment and operational flexibility to repay debts, thereby affecting their ROA. Additionally, higher debt levels may reduce the institution’s liquidity ratio because it implies the institution needs to retain more liquid assets to meet debt repayment demands, thus reducing funds available for other investments or operational activities.

The cash flow ratio (Cashflow) reflects the ability of financial institutions to generate cash flow from day-to-day operational activities (Elahi et al., 2021). A higher cash flow ratio usually indicates stronger cash inflows, which contribute to improving ROA as it indicates the institution can effectively generate profits from its core business. Furthermore, stronger cash flow also helps improve the liquidity ratio because it means the institution has enough cash to meet short-term financial obligations, reducing liquidity risk.

The accounts receivable ratio (REC) reflects the proportion of accounts receivable to total assets of financial institutions and serves as an indicator of the leniency of the institution’s credit policy and customer payment ability (Frankel et al., 2020). A higher accounts receivable ratio may have a negative impact on ROA because an increase in accounts receivable may reduce the efficiency of fund utilization and delay income realization. Additionally, a higher accounts receivable ratio may also increase liquidity risk because it may lead to increased uncertainty in cash inflows, affecting the institution’s liquidity management.

The inventory ratio (INV) reflects the proportion of inventory to total assets of financial institutions. For financial institutions involved in physical commodity trading, a higher inventory ratio may reduce ROA because excess inventory may lead to idle funds, reducing the return on assets (Chen et al., 2020). Furthermore, higher inventory levels may also pressure the liquidity ratio because excess inventory may take longer to convert into cash, affecting the institution’s short-term debt repayment ability.

These control variables have significant impacts on the ROA and liquidity ratio of financial institutions, so considering these variables is crucial when analyzing the impact of financial technology on the profitability and risk management capabilities of financial institutions. Table 1 shows the definitions of all variables.

Variable Definitions.

Models

To ensure the appropriate model selection between fixed and random effects, the Hausman test was conducted for both models used in this study—profitability (ROA) and liquidity management (LR). The Hausman test is instrumental in identifying whether the unobserved heterogeneity in the panel data is correlated with the explanatory variables.

Profitability Model (ROA): The Hausman test produced a p-value greater than .05, indicating that the random effects model is suitable for this analysis. This suggests that the unique errors are not correlated with the independent variables, and hence the random effects model provides efficient and unbiased estimates.

Liquidity Management Model (LR): For the liquidity management model, the Hausman test also indicated that the random effects model was appropriate, supporting the initial model choice.

These results justify the use of the random effects model for both analyses, confirming that the unique characteristics of the financial institutions do not systematically influence the key variables under study. Therefore, the empirical approach used in this research maintains its validity, and the chosen model effectively captures the impact of financial technology on financial institutions’ performance.

In this study, random effects models were chosen to examine the impact of financial technology on the Return on Assets (ROA) and liquidity ratio of Chinese financial institutions, as well as the relationship between control variables (leverage ratio LEV, cash flow ratio Cashflow, accounts receivable ratio REC, inventory ratio INV) and these key indicators. The selection of random effects models is primarily based on several considerations:

Random effects models are suitable for addressing the issue of unobservable heterogeneity in panel data. There are many unique characteristics among financial institutions that are difficult to directly measure, such as management quality, corporate culture, or strategic direction, which may remain stable over time but vary across different institutions. By allowing for the presence of these unobserved effects, random effects models can more accurately estimate the actual impact of explanatory variables on the dependent variables.

Random effects models provide a highly flexible analytical approach for panel data that contain both time-series data (data that varies over time) and cross-sectional data (data from different entities). Given that our study involves data from multiple financial institutions across multiple time periods, random effects models allow us to effectively utilize this complex data structure, thereby conducting a more comprehensive analysis of the various dimensions of the impact of financial technology on financial institutions.

Random effects models can balance the influences of time-series and cross-sectional data when analyzing panel data, which is particularly important for the purposes of this study. This type of model can help us understand the impact of financial technology on different financial institutions (cross-sectional dimension) and across different time periods (time-series dimension), thus providing a more comprehensive and in-depth insight.

Adopting random effects models can enhance the accuracy of empirical analysis. By considering the unobservable heterogeneity within financial institutions, these models reduce biases caused by omitted variables, resulting in more accurate estimates of the explanatory variables. This is crucial for accurately assessing the impact of financial technology and control variables on ROA and liquidity ratios.

Due to their ability to address unobservable heterogeneity in panel data, flexibility in handling complex data structures, balancing of time-series and cross-sectional data influences, and improvement in the accuracy of empirical analysis, random effects models are an ideal choice for analyzing the impact of financial technology on financial institutions in this study. The adoption of this methodological approach facilitates a deeper understanding of the effects of financial technology on profitability and risk management capabilities across different financial institutions and time periods.

The following two equations represent the regression equations used in this study, where ROA and LR denote the return on assets and liquidity ratio, respectively, representing the two dependent variables of this research. α and γ are the intercept terms in the two regression equations. ε and ε’ represent the error terms in the two regression equations. β and θ represent the coefficients of the variables in the two regression equations.

Data Analysis and Results

In this study, descriptive statistical analysis was conducted on key financial indicators of financial institutions to assess the impact of financial technology on their profitability and liquidity management. Table 2 shows the content of descriptive statistics for each variable. The average Return on Assets (ROA) was found to be 0.0257, with a standard deviation of 0.0659, indicating variability in the profitability of financial institutions. The lowest ROA recorded was −0.3830, while the highest was 0.4494, reflecting a wide range from losses to high profits. The average Liquidity Ratio (LR) was 3.0144, but with a high standard deviation of 6.1614, and a maximum value surging to 40.8447, implying significant differences in liquidity management capability among financial institutions. The natural logarithm of FinTech’s frequency (LnFT) had an average value of 0.6490, with a standard deviation of 1.0423, revealing differences in the application frequency of financial technology across various financial institutions. The average Leverage Ratio (LEV) was 0.6476, reflecting the prevalent level of institution leverage, with a relatively large standard deviation of 0.2660 indicating diversity in debt strategies. The average Cash Flow Ratio (Cashflow) was 0.0165, with a fluctuation range from −0.4162 to 0.4208, indicating instability in the cash flow situation of financial institutions. Analysis of the proportion of accounts receivable (REC) and inventory (INV) further revealed differences in operational capital management among financial institutions, with average REC and INV ratios of 0.0235 and 0.0348, respectively, and standard deviations of 0.0427 and 0.1016, indicating significant differences in efficiency in credit management and inventory control. These descriptive statistical results provide foundational data for exploring in-depth how financial technology affects the profitability and liquidity of financial institutions, highlighting the extensive differences among financial institutions in these key financial indicators and laying the groundwork for subsequent analysis.

The Descriptive Statistics for Each Variable.

Table 3 presents the analysis results regarding profitability. In this study, two models were employed to investigate the impact of financial technology on the profitability (ROA) of Chinese financial institutions, while considering multiple financial control variables. In Model 1, the coefficient of the natural logarithm of financial technology frequency on profitability (represented by ROA) was −0.069, with a standard error of 0.0043, indicating that the influence of financial technology was not statistically significant in this model. Similarly, in Model 2, despite introducing control variables, the coefficient of the core explanatory variable LnFT remained insignificant. The results suggest that the direct impact of financial technology is statistically insignificant, implying that its effect on the profitability of financial institutions may be more pronounced through indirect pathways or that its positive and negative effects may offset each other.

The Data Analysis Results on the Factors Affecting Profitability in Financial Institutions.

Note. The coefficients are standardized coefficients. The numbers in parentheses represent the standard deviation of the variable.

Significance at the 5% level. ***Significance at the 1% level.

However, the model with control variables revealed several key financial indicators significantly affecting ROA: an increase in Leverage Ratio (LEV) significantly decreased ROA, with a coefficient of −0.413, indicating that high debt levels may increase financial pressure on financial institutions, thereby weakening their profitability. Specifically, a 1 standard deviation increase in LEV is associated with a 0.1099 decrease in ROA, relative to its average value. The positive coefficient of Cash Flow Ratio (Cashflow) at 0.213 underscores the importance of robust cash flow in enhancing profitability, indicating that effective cash flow management can strengthen the financial stability of financial institutions. A 1 standard deviation increase in Cashflow is associated with an 0.02234 increase in ROA. The negative coefficients of Receivables Ratio (REC) and Inventory Ratio (INV) at −0.088 and −0.240, respectively, reveal that higher levels of receivables and inventory may impair the efficient utilization of assets and profitability. Specifically, a 1 standard deviation increase in REC is associated with a 0.0038 decrease in ROA, and a 1 standard deviation increase in INV is associated with a 0.0244 decrease in ROA, relative to their average values.

These findings emphasize that, in addition to financial technology, traditional financial management practices still play a crucial role in enhancing the profitability of financial institutions, particularly the strategic choices in asset-liability management, cash flow control, and receivables and inventory management are crucial for maintaining and enhancing the profitability of financial institutions.

Table 4 presents the data analysis results on the influencing factors of liquidity risk in financial institutions. This study conducts an in-depth analysis of the impact of financial technology on the liquidity ratio of financial institutions, while examining the role of key financial control variables. In the preliminary analysis (Model 3), the effect of financial technology on the liquidity ratio is not significant, with a coefficient of 0.054 and a standard error of 0.3554, suggesting no direct statistical correlation between the application of financial technology and the liquidity management capability of financial institutions when other financial variables are not considered. This may reflect the complexity and indirectness of the impact of financial technology, or it could be because the benefits of financial technology take time to accumulate and manifest in liquidity indicators.

The Data Analysis Results on the Influencing Factors of Liquidity Risk in Financial Institutions.

Note. The coefficients are standardized coefficients. The numbers in parentheses represent the standard deviation of the variable.

Significance at the 10% level. **Significance at the 5% level. ***Significance at the 1% level.

Further analysis (Model 4) introduces leverage ratio (LEV), cash flow ratio (Cashflow), receivables ratio (REC), and inventory ratio (INV) as control variables. In this more complex model, the application of financial technology significantly enhances the liquidity ratio, with a coefficient of 0.025, significant at the 1% level, emphasizing that financial technology effectively reduces liquidity risk and enhances liquidity by improving the operational efficiency and fund management capability of financial institutions. Specifically, a 1 standard deviation increase in financial technology (LnFT) is associated with a 0.0261 increase in the liquidity ratio, relative to its average value.

Furthermore, the significant negative coefficient of leverage ratio (−0.508) indicates that high debt levels exert pressure on the liquidity of financial institutions. A 1 standard deviation increase in LEV is associated with a 0.1351 decrease in liquidity, relative to its average value. The negative coefficient of cash flow ratio (−0.368) suggests that excessive cash inflows may indicate funds being used for non-liquid investments by financial institutions. A 1 standard deviation increase in Cashflow is associated with a 0.0385 decrease in liquidity, relative to its average value. The negative coefficient of receivables ratio (−0.181) demonstrates that high receivables may delay cash inflows, adversely affecting liquidity. A 1 standard deviation increase in REC is associated with a 0.0077 decrease in liquidity, relative to its average value. Conversely, the positive coefficient of inventory ratio (0.144) reveals that in certain circumstances, higher inventory levels may have a positive impact on liquidity due to anticipated sales growth. A 1 standard deviation increase in INV is associated with a 0.0146 increase in liquidity, relative to its average value.

These series of analysis results not only reveal the positive role of financial technology in enhancing the liquidity management capability of financial institutions but also underscore the importance of traditional financial indicators in liquidity risk management. The comparison between Model 3 and Model 4 demonstrates the variation in the relationship between financial technology and financial institution liquidity under different model settings, providing important economic insights for financial institutions to optimize financial management while adopting financial technology.

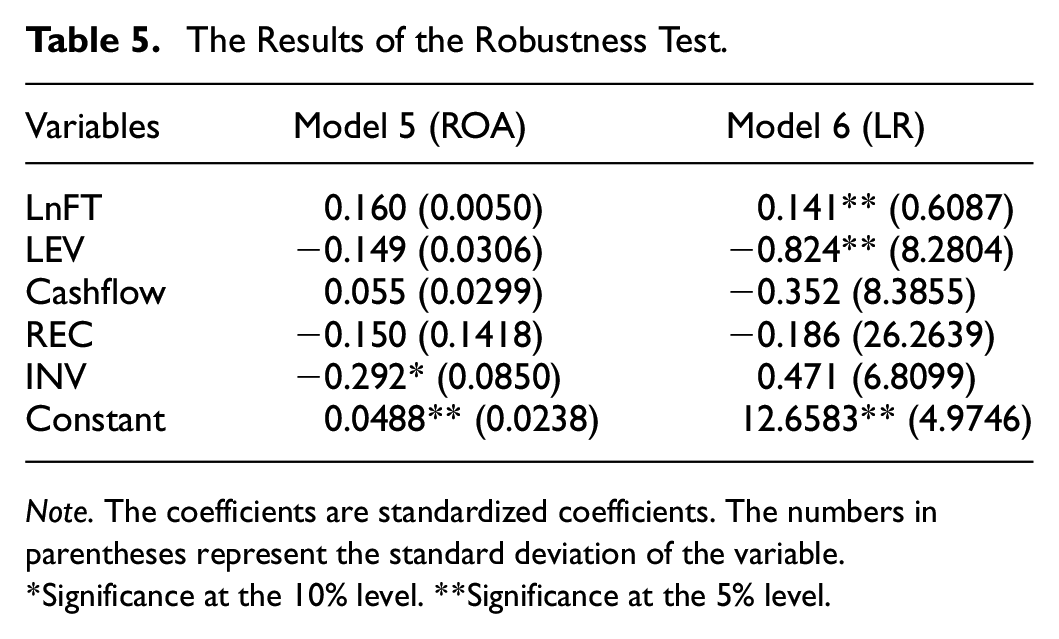

Table 5 shows the results of the robustness test using the fixed effects models. This study deepens the understanding of the impact of financial technology on the profitability and liquidity ratios of financial institutions by conducting robustness tests using fixed effects models, ensuring the reliability and generalizability of the research findings. The implementation of robustness tests significantly enhances the accuracy and transparency of the research, allowing for the effective control of unobservable individual heterogeneity and reducing potential omitted variable bias. The introduction of fixed effects models is particularly suitable for the panel data used in this study, leveraging the temporal variation in the data to reveal differences in the impact of financial technology across different times and financial institutions. The choice of this method not only strengthens confidence in the universality of the research findings but also enhances the reliability of causal inference by more precisely controlling for individual inherent characteristics. Therefore, the robustness tests of fixed effects models not only confirm the positive role of financial technology in enhancing liquidity management and profitability of financial institutions but also provide important methodological reference for exploring complex economic phenomena, ensuring a solid foundation and broad applicability of the research conclusions.

The Results of the Robustness Test.

Note. The coefficients are standardized coefficients. The numbers in parentheses represent the standard deviation of the variable.

Significance at the 10% level. **Significance at the 5% level.

The robustness test results reveal that in Model 5, the impact of financial technology on ROA is not significant, consistent with the initial random effects model analysis. This suggests that the direct connection between financial technology and the profitability of financial institutions may not be apparent or may involve indirect mechanisms. Furthermore, other financial indicators such as leverage ratio, cash flow ratio, accounts receivable ratio, and inventory ratio also show insignificant effects on ROA in the fixed effects model, further emphasizing the complexity of the impact of internal characteristics and external environmental changes on profitability.

Analysis in Model 6 highlights the significant positive impact of financial technology on enhancing liquidity management, with a coefficient of 0.141, significant at the 5% level. Specifically, a 1 standard deviation increase in financial technology (LnFT) is associated with a 0.1470 increase in the liquidity ratio, relative to its average value. This finding reinforces the crucial role of financial technology in optimizing the liquidity of financial institutions, particularly under the fixed effects model, where its positive impact becomes more pronounced, underscoring its key role in improving operational efficiency and fund management capability. Meanwhile, the negative impact of leverage ratio on liquidity ratio is significant, with a coefficient of −0.824. A 1 standard deviation increase in LEV is associated with a 0.2192 decrease in liquidity, relative to its average value, confirming that high levels of leverage may exacerbate the liquidity risk of financial institutions. The insignificant effects of other financial indicators in Model 6 once again emphasize the complex interactions among different financial management indicators.

Through the robustness test of the fixed effects model, this study enhances the reliability and depth of research on the impact of financial technology on the profitability and liquidity ratios of financial institutions. These analyses not only confirm the positive role of financial technology in enhancing liquidity management of financial institutions but also, through comparison and validation, reveal the complexity and multidimensionality of the impact of financial indicators on institutional performance. The application of the fixed effects model provides a meticulous consideration of inherent characteristics and temporal variations in financial institutions, offering solid empirical support for understanding the relationship between financial technology and institutional performance, thereby deepening our understanding of the role of financial technology in the modern financial domain.

Discussion and Conclusion

This study delves into the impact of financial technology development on the profitability (ROA) and liquidity ratio (LR) of Chinese financial institutions, utilizing various analytical models and conducting robustness tests. Firstly, it is found that the development of financial technology does not significantly affect the ROA of financial institutions. This could be because the benefits of financial technology are difficult to directly translate into profit enhancement for financial institutions in the short term, or because the positive and negative effects of financial technology offset each other in terms of profitability. Additionally, the impact of financial technology may be realized more through indirect pathways, such as indirectly influencing profitability by improving service quality and customer satisfaction, which are challenging to capture in the current analytical models.

However, the impact of financial technology on the liquidity ratio of financial institutions is significant and positive, especially in the robustness test of the fixed effects model, where the development of financial technology significantly improves the liquidity ratio. This underscores the positive role of financial technology in optimizing fund management, enhancing operational efficiency, and reducing liquidity risk for financial institutions. By promoting information flow, streamlining transaction processes, and improving the efficiency of fund utilization, financial technology effectively enhances the liquidity management capability of financial institutions. This finding suggests that although financial technology may not directly impact the short-term profitability of financial institutions, it plays an essential role in enhancing long-term stability and risk management for financial institutions.

Overall, the development of financial technology is crucial for financial institutions, especially against the backdrop of rapid development and increasing competition in the financial industry. While the direct positive impact of financial technology on profitability has not statistically manifested, its significant positive impact on the liquidity ratio reveals the valuable role of financial technology in enhancing risk management capabilities and institutional resilience. Therefore, financial institutions should actively embrace financial technology, leveraging its tools and services to optimize operational processes and risk management strategies, thereby maintaining a competitive edge and promoting long-term sustainable development. The findings of this study offer valuable insights into how financial institutions can effectively utilize financial technology and provide solid empirical support for a deeper understanding of the relationship between financial technology and institutional performance.

Given the current limitations on the direct impact of financial technology (fintech) development on the profitability of financial institutions, the following three policy recommendations are crucial for guiding the development of fintech and financial institutions:

Enhance the regulatory framework for fintech, balancing innovation and risk: Policymakers should pay attention to the dual effects of fintech development and balance the relationship between encouraging innovation and preventing risks through an enhanced regulatory framework. Regulatory authorities need to formulate forward-looking and flexible regulatory policies that not only promote the healthy development of fintech but also ensure the stability of financial markets and the protection of consumer interests. Clearly defining compliance requirements and risk management frameworks for fintech companies in regulatory policies can help financial institutions better utilize fintech for risk control and business innovation.

Strengthen fintech education and talent cultivation: In the current situation where fintech may not directly significantly enhance the profitability of financial institutions, enhancing the understanding and application capabilities of practitioners in fintech becomes particularly important. Governments and financial institutions should increase investment in fintech education and training, including establishing fintech-related courses at higher education institutions and providing on-the-job training for financial institution employees, to cultivate talent with knowledge and skills in fintech. This will help financial institutions more effectively utilize fintech to optimize business processes, improve service efficiency, and indirectly enhance profitability.

Promote deep integration of fintech with traditional financial services: Policymakers should encourage cooperation between financial institutions and technology companies to promote the deep integration of fintech with traditional financial services. By promoting the adoption of advanced fintech solutions by financial institutions, such as big data analysis, cloud computing, and artificial intelligence, financial institutions can optimize risk management, customer service, and internal operations, indirectly enhancing their profitability. At the same time, policy support for technological innovation and business model innovation by financial institutions can improve the quality and efficiency of financial services, thereby gaining a competitive advantage.

By implementing the above policy recommendations, strong support can be provided for the sustainable development of fintech and financial institutions. Even in the current stage of fintech development where direct significant enhancement of financial institutions’ profitability may not be evident, these measures will create conditions for financial institutions to optimize operations, improve service capabilities, and enhance risk management capabilities through indirect means, thus supporting the long-term development and profitability improvement of financial institutions.

Footnotes

Ethical Considerations

There are no human participants in this article and informed consent is not required.

Author Contributions

Conceptualization, W.W. and D.X.; methodology, W.W.; software, W.W.; validation, W.W., D.X. and Y.L.; formal analysis, W.W.; investigation, W.W.; resources, W.W.; data curation, W.W.; writing—original draft preparation, W.W.; writing—review and editing, W.W.; visualization, W.W.; supervision, W.W.; project administration, D.X. and Y.L. All authors have read and agreed to the published version of the manuscript.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data can be applied by sending email to the correspondence author.