Abstract

This study uses the Shanghai-Hong Kong Stock Connect as a quasi-natural experiment to explore how capital market liberalization affects green innovation in China’s A-share listed firms. The findings show that the Stock Connect stimulates independent but not cooperative green innovation. This effect is driven by active investor governance and, to a lesser extent, the threat of investor exit, with the former having a more substantial positive influence. The impact is more pronounced in firms located in regions with more robust legal systems and better corporate governance. Capital market liberalization boosts firms’ motivation and capacity for green innovation, providing valuable insights for policymaking and the continued development of liberalized capital markets.

Keywords

Introduction

Environmental issues in China are increasingly affecting both economic development and public health. However, green investments often do not generate immediate returns, which reduces corporate motivation for innovation in this area (Manso, 2011). As a result, many companies take a reactive approach to environmental challenges, focusing on compliance instead of proactive solutions (Saunila et al., 2018). According to the International Energy Agency (IEA), China consumed 4 billion tons of oil-equivalent energy in 2023, surpassing the 2.27 billion tons of oil-equivalent energy in the United States. As a result, China has become the world’s largest energy consumer. Moreover, according to the 2024 Global Environmental Performance Index (EPI) report jointly released by Yale University and other research institutions, China’s EPI score was only 35.4, ranking 156th among 180 countries. In response, China has introduced various policies since 1979, including green credit and environmental permits, to encourage low-carbon, eco-friendly enterprises.

Green innovation, which focuses on resource conservation and pollution reduction, is a complex but potentially high-reward investment for companies (Mrkajic et al., 2019; Yang et al., 2022). Those who engage in green innovation are often seen as promising by governments, investors, and the media. A pivotal moment in China’s financial history was the Shanghai-Hong Kong Stock Connect launch on November 17, 2014, allowing institutional and individual investors from mainland China and Hong Kong to trade each other’s stocks. This initiative provides a unique opportunity to study how capital market liberalization affects corporate green innovation.

Capital market liberalization primarily involves removing restrictions on capital flows, enabling foreign investors to enter and engage in market transactions. Previous research has mainly focused on how liberalization lowers financing costs and stimulates investment (Dow & Gorton, 1997; Mitton, 2006; Wang et al., 2009). However, few studies have examined how capital market liberalization specifically influences green innovation from the perspective of foreign investors. Two mechanisms are commonly discussed: active governance, where investors influence corporate decisions directly through their voice, and the threat of exit, where investors use the risk of selling their shares to push for better corporate behavior (Admati & Pfleiderer, 2009; Wang et al., 2009; Xu et al., 2020).

While the role of corporate governance is critical, it remains unclear whether foreign investors affect green innovation more through the threat of exit or through active governance. Our research extends existing studies by using a difference-in-differences approach to explore the impact of the Shanghai-Hong Kong Stock Connect on corporate green innovation, focusing on the role of legal frameworks and corporate characteristics.

The paper is structured as follows: first, we review the relevant literature on green innovation and the effects of capital market liberalization on governance. We then present our hypotheses and explain the data, sample, and methods used for analysis. Finally, we discuss the results and provide conclusions.

Literature Review

Influential Factors of Corporate Green Innovation

Green innovation refers to corporate advancements in technologies and processes to conserve resources, reduce energy consumption, and minimize environmental pollution (Saunila et al., 2018). Engaging in green innovation enhances resource efficiency throughout the product lifecycle (Chen et al., 2018) and ensures compliance with environmental regulations, thus avoiding governmental penalties (Chang, 2011). Furthermore, firms involved in green innovation often enjoy enhanced long-term reputations. Current research on the determinants of green innovation primarily examines external institutional environments and corporate characteristics. Scholars have investigated how environmental regulations, management tools, and organizational changes influence green innovation (Horbach, 2008; Laffont & Tirole, 1996; Wagner, 2007).

There has been extensive discussion in existing research on stimulating green innovation. At the micro level, knowledge stock, talent reserves, strategic positioning, and board governance influence corporate green innovation decisions (Horbach, 2008; Laffont & Tirole, 1996; Wagner, 2007). Meanwhile, at the macro level, favorable market environments, institutional contexts, and financial support are recognized as positively impacting green innovation (Yalabik & Fairchild, 2011). Generally, environmental regulatory policies directly impact green innovation (Lin et al., 2024; Zhao et al., 2024). For instance, F. Liu et al. (2024) reveal a significant positive correlation between Green Factory Identification and corporate green innovation, confirming the effectiveness of green industrial policies in driving innovation.

Beyond environmental regulatory policies, some scholars have also highlighted the stimulating effects of green fiscal and financial policies, such as carbon market shocks (He & Dai, 2024) and ESG ratings (Peng & Kong, 2024), on green innovation. Recent studies indicate that capital market liberalization promotes corporate green innovation (Sha et al., 2022), yet the specific mechanisms through which this occurs remain unclear. Herein, we employ the Shanghai-Hong Kong Stock Connect as a natural experiment to explore how capital market liberalization influences corporate green innovation.

Theoretical Framework

Corporate governance theory identifies two mechanisms through which external investors exert influence. Firstly, through active governance, investors with substantial shareholdings can influence corporate decision-making by participating in voting processes and proposing changes (Ferreira & Laux, 2007; Hartzell & Starks, 2003; Kim & Verrecchia, 1994). Secondly, the exit threat mechanism involves investors impacting stock prices through market transactions, indirectly influencing corporate decisions (Baker et al., 2003; Foucault & Frésard, 2012; Loureiro & Taboada, 2015). Previous literature suggests that external investors enhance managerial oversight and reduce information asymmetry, thereby improving investment efficiency (Bekaert & Harvey, 2000; Henry, 2000). Capital market liberalization is also known to lower capital costs by sharing risks (Bae et al., 2012), improve production efficiency by mitigating agency problems (Bekaert et al., 2000; Larrain & Stumpner, 2017), and optimize internal governance structures (Doidge et al., 2004).

Moreover, the exit threat mechanism posits that external investors’ trading activities enhance the informativeness and efficiency of stock prices, thereby influencing corporate decision-making (Bond et al., 2012; Edmans, 2014). For instance, selling or short-selling stocks based on informed assessments can impact stock prices, affecting managerial decision-making by altering risk profiles and potential dismissal risks. Thus, our theoretical framework proposes that foreign investors influence corporate green innovation under capital market liberalization through the governance effect and the exit threat mechanism. These mechanisms interact to shape corporate behavior and facilitate or hinder advancements in green innovation.

Hypotheses Development

Before implementing the Shanghai-Hong Kong Stock Connect trading mechanism, foreign investors, including those from Hong Kong, could not directly invest in the Chinese A-share market except through channels such as Qualified Foreign Institutional Investors (QFII). Companies listed on the Shanghai Stock Exchange and other A-share markets were relatively closed. After the implementation of the Shanghai-Hong Kong Stock Connect, Hong Kong investors could directly invest in eligible Shanghai Stock Connect stocks. This mechanism significantly reduced investment restrictions for foreign investors compared to previous capital market opening policies, facilitating cross-border capital flows and market transactions. Existing studies have found that firms often prioritize compliance under regulatory pressure to maintain organizational legitimacy (Ramanathan et al., 2017). Hong Kong investors generally possess more extensive investment experience, team capabilities, and professional expertise than mainland investors (Grinblatt & Keloharju, 2000), enabling them to identify and engage with local companies effectively. Research by Albuquerque et al. (2009) indicates that investors in developed capital markets tend to stay at the forefront of technological advancements and leverage information advantages through market transactions to improve market efficiency.

The information feedback mechanism of the stock price is critical for the capital market to influence the real economy. Since implementing the Shanghai-Hong Kong Stock Connect, foreign investors have utilized their information advantages to identify undervalued companies and correct overpricing through market transactions. The launch has contributed to aligning corporate valuations with market realities, reducing mispricing, and enhancing the informational content of stock prices (Li et al., 2004). Shanghai-Hong Kong Stock Connect companies are motivated to actively undertake environmental responsibilities, including green innovation, to enhance public perception and reputational value. As a critical component of corporate social responsibility (CSR), green innovation is an essential metric for external investors to evaluate a company’s operational status and technological potential (Dyck et al., 2019). The Shanghai-Hong Kong Stock Connect has significantly increased the propensity of target company management to pursue green innovation, thereby enhancing the attractiveness of their stocks to foreign investors. Simultaneously, under the Connects trading framework, management has improved the quality of disclosures related to CSR and green innovation (Yoon, 2019). Enhanced disclosure quality attracts foreign investors, facilitates their use of relative information advantages to access incremental insights, and reflects these in stock prices through trading.

Previous studies suggest that the design of the Shanghai-Hong Kong Stock Connects operational mechanism discourages foreign investors from exercising governance through “voting with their hands” and instead encourages “exit threat” as a governance approach (Baker et al., 2003; Edmans, 2009). However, as most companies in the Stock Connect are manufacturing firms, data from the MSCI 2024 ESG ratings reveal that the overall ESG ratings of Chinese-listed companies remain relatively low (refer to https://www.msci.com/zh/esg-ratings). There is a significant gap in the current state of green innovation between listed companies in China and developed countries like the US. The mandatory disclosure requirements of the Hong Kong Stock Exchange have driven sustainability information disclosure among Chinese A-share listed companies (C. Liu et al., 2021). Consequently, these ESG disclosure regulations have greatly enhanced ESG disclosure in China. Companies have instead sought to address shortcomings to attract investors, emphasizing green innovation and social responsibility to differentiate themselves from competing manufacturing firms. This trend has significantly encouraged foreign investors to engage in governance through “voting with their hands,” thereby promoting improvements in corporate green innovation. Minority shareholders express their concerns through social media platforms, exercising direct governance mechanisms. These forums, primarily comprising discussions among shareholders about corporate developments, significantly influence managerial decisions. Discontent expressed in these online communities can impact daily operations and prospects, compelling management to respond. The high information density and wide dissemination of social media amplify the governance role of minority shareholders, fostering effective oversight and optimizing investment efficiency. Based on these insights, we propose the following hypotheses:

Data and Methodology

Data and Sample Selection

The initial sample of Shanghai-Hong Kong Stock Connect (SHSC) target companies includes constituent stocks of the SSE 180 Index, SSE 380 Index, and 568 eligible A-share companies listed on the Shanghai Stock Exchange (SSE) with dual “A+H” shares. This study also adjusts the list of SHSC target companies based on changes following the program’s implementation on November 17, 2014, such as removals and newly added entries. Non-SHSC target companies include those not incorporated into the SHSC program from the SSE and all listed companies on the Shenzhen Stock Exchange.

Green patents, which focus on energy conservation, emission reduction, and pollution control technologies, provide a more direct and measurable indicator of a firm’s output in green innovation. These patents are not only quantifiable but also hold substantial practical value. Additionally, considering the time lag between the initiation of innovation activities by listed companies and the eventual filing of green innovation patent applications, we use the number of green innovation patent applications in the subsequent period as the dependent variable. Based on the availability of data about green innovation and considering the time lag between innovation investment and patent application, we have selected Shanghai and Shenzhen A-share listed firms from 2011 to 2017 as our initial sample. The dependent variable, green innovation, is measured using green patent data collected from the China Research Data Service Platform (CNRDS) from 2012 to 2017. We classify patents in the International Patent Classification Green Inventory of the World Intellectual Property Organization (WIPO) as green (Amore & Bennedsen, 2016).

Following Berkowitz et al. (2015), the data on independent variables includes firm size, financial leverage, fixed asset ratio, ownership structure, board independence, firm growth, and the proportion of independent directors is sourced from the CSMAR database. To better capture the impact of the Shanghai-Hong Kong Stock Connect, launched in 2014, on corporate green innovation, we use observations from 3 years before and after its implementation for empirical analysis. After excluding missing data and outliers, we applied winsorization to the main variables at the upper and lower 1% thresholds. In previous research on listed companies, it is common practice to apply Winsorization to key continuous variables at the 1% tails to eliminate the interference of outliers. The threshold for this adjustment is determined by the need to preserve the maximum amount of sample data while removing the influence of extreme values. In this study, for the sake of rigor, we plotted and observed scatter diagrams of the main continuous variables and confirmed that there was no need to increase the tail-trimming ratio. Therefore, we maintained the standard approach used in previous literature of applying winsorization to key continuous variables at the 1% thresholds. This process resulted in a final dataset comprising 4,658 firm-year observations from 1,862 companies.

Variables and Estimation Models

We take the launch of Shanghai-Hong Kong Stock Connect as a quasi-natural experiment and set up the following empirical models to verify the research hypotheses. The difference-in-differences (DID) model is well-suited for analyzing causal effects in natural experiments. By focusing on changes in the treatment and control groups before and after the intervention, the DID model minimizes the influence of external factors (e.g., macroeconomic changes) on the outcome, leading to more accurate policy effect estimation. First, following the previous literature (Berkowitz et al., 2015), we establish model (1) to examine the impact of the launch of the Shanghai-Hong Kong Stock Connect on corporate green innovation.

where Green represents the total amount of corporate green innovation, the value of Post is 1 in and after 2014, and the value is 0 before 2014. Specifically, the value of Connect is 1 if the firm is the subject stock of Shanghai Stock Connect and equals 0 otherwise. Since the model controls for firm fixed effects and year fixed effects, the coefficient of interaction term Connect × Post is the statistic indicator of difference-in-difference, and the coefficient β1 is expected to be positive, indicating that the Shanghai-Hong Kong Stock Connect can promote the improvement of corporate green innovation.

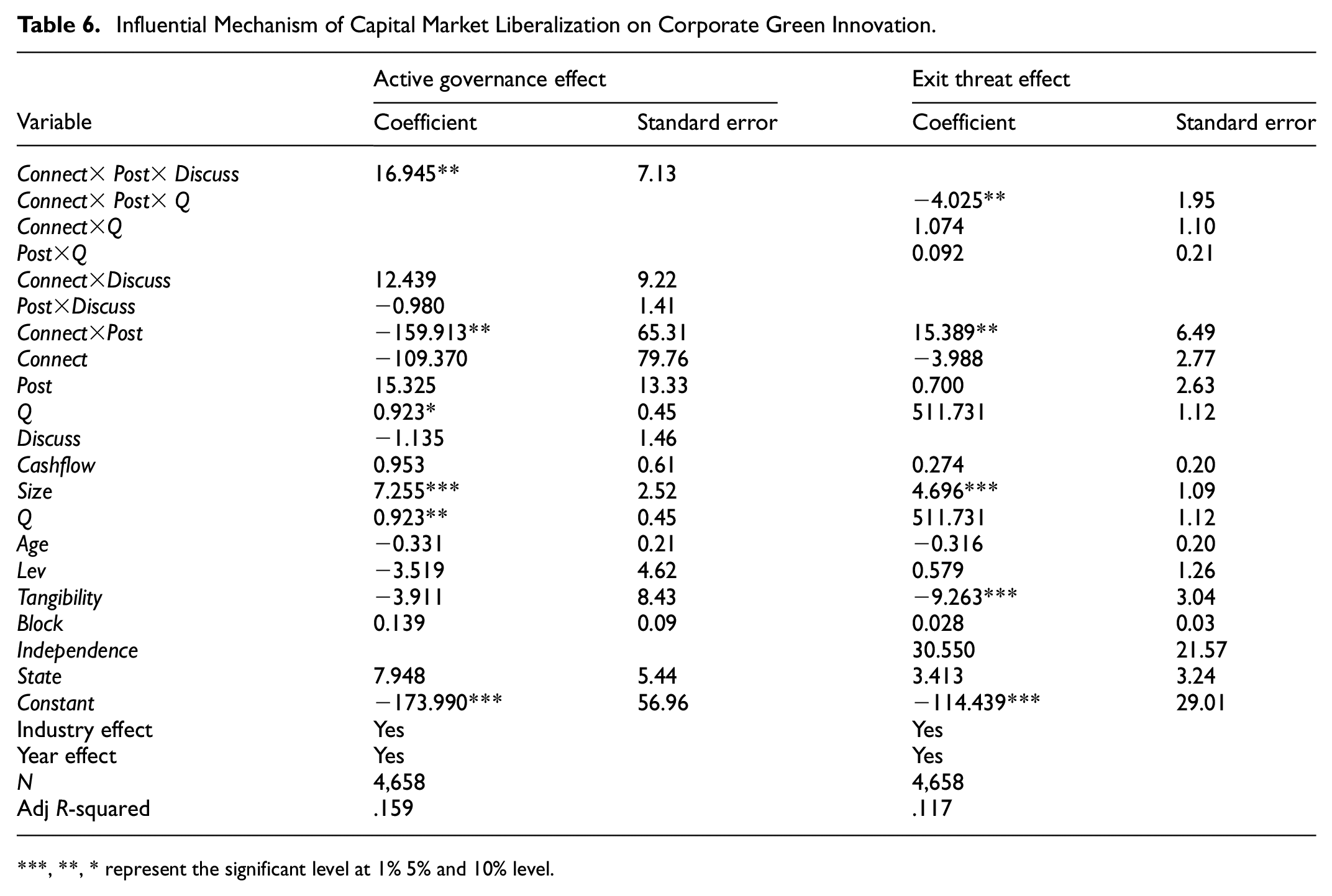

Second, we follow Foucault and Frésard (2012) and establish model (2) to test whether and how the implementation of the Shanghai-Hong Kong Stock Connect affects corporate green innovation through investor governance.

Where Discuss represents the number of posts in the official forum of listed firms, the coefficient of Connect × Post × Discuss reflects the sensitivity of corporate green innovation on active governance of corporate investors after the implementation of Shanghai-Hong Kong Stock Connect. The coefficient β1 is expected to be positive, indicating that the active governance of investors after implementing the Shanghai-Hong Kong Stock Connect can promote corporate green innovation.

Third, we establish model (3) to test whether and how the Shanghai-Hong Kong Stock Connect implementation affects corporate green innovation through an exit threat mechanism.

The coefficient of Connect × Post × Q reflects the sensitivity of corporate innovation on the stock price of the target firms after the implementation of Shanghai-Hong Kong Stock Connect. The coefficient β1 is expected to be negative, indicating that the exit threat of investors after implementing the Shanghai-Hong Kong Stock Connect inhibits corporate green innovation.

Variable Definition

Dependent variable (Green): green innovation. Green patents, which focus on energy conservation, emission reduction, and pollution control technologies, provide a more direct and measurable indicator of a firm’s output in green innovation. These patents are not only quantifiable but also hold substantial practical value. Therefore, we classify patents in the International Patent Classification Green Inventory of the World Intellectual Property Organization as green innovation (Amore & Bennedsen, 2016). The patent application information of listed firms is obtained from the innovation patent database in the CNRDS database. Green innovation is measured by the number of green patents among all patents applied by the firms in that year. In the regression analysis, the variables affecting corporate financing constraints are controlled, including firm size, financial leverage, fixed asset ratio, ownership, independence of directors, firm growth, and the concentration of powers. We also control for industry and year-fixed effects. The specific variable definitions are shown in Table 1.

Variable Definition.

Source. Compiled by the author.

Empirical Results

Descriptive Statistics

As shown in Table 2, the average number of corporate green innovations is 4.483, the maximum value of corporate green innovation is 1,381, and the standard deviation is 38.414, indicating that Chinese listed firms have profound polarization in environmental protection and the pursuit of green innovation has not become an expected behavior. At the same time, the mean value of firm size is 22.272, and the standard deviation is 1.544, indicating a significant difference in the scale of enterprises in terms of financial leverage, profitability, operational cash flow, and firm value.

Descriptive Statistics.

Source. Compiled by the author.

The total sample includes 4,658 firm-year observations, of which 3,806 firm-year observations are in the treatment group and 852 firm-year control group. Table 3 describes the industrial characteristics of corporate green innovation. Among these, 66.6% of these observations in the controls belong to the manufacturing industries, 2,504 observations belong to the manufacturing industry, and 142 observations belong to the financial industry. The average value of green innovations in the control group is 1.9; the industry distribution of the samples in the treatment group is relatively scattered, with 395 manufacturing observations accounting for 43.6%. Second, the samples of information transmission, software, and information technology services accounted for about 9% of the sample, and the average number of green innovations is 16.1. It is proved from the above descriptive statistics that there are significant differences in green innovation between the treatment group and the control group.

Industrial Characteristic Description of Corporate Green Innovation.

Source. Compiled by the author.

We divide the sample into Shanghai-Hong Kong Stock Connect (SHSC) target companies and non-SHSC target companies and calculate the average number of green innovation patent applications for both groups from 2011 to 2016 to plot a time trend graph. The solid line represents SHSC target companies, while the dashed line represents non-SHSC target companies (as shown in Figure 1). Both groups exhibited the same growth trend for green innovation patents before implementing the SHSC policy. However, 1 year after the policy’s implementation, the number of green innovation patents that non-SHSC target companies applied maintained its original growth trend. In stark contrast, SHSC target companies showed a significant change in the growth rate of green innovation patent applications, leading to an expanding gap between the two groups over time. This preliminary evidence suggests that the SHSC policy has promoted the growth of green innovation patent applications among SHSC target companies.

The time trend of corporate green innovation.

Correlation Analysis

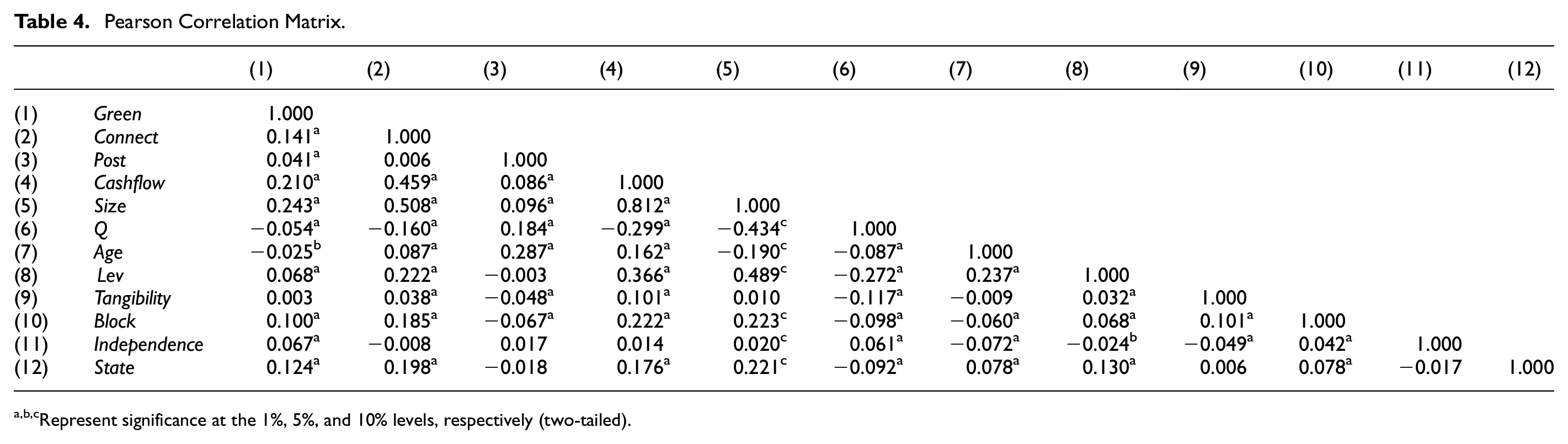

Before the regression analysis, we conducted a correlation analysis on the main variables in the regression model, and the correlation between the variables was preliminarily verified. As shown in Table 4, the correlation coefficient between Connect and Green is .141, and the correlation coefficient between Cashflow and Green is .210. Generally, the correlation coefficient between the variables is less than 0.5, showing no collinearity problem between the variables in the regression model.

Pearson Correlation Matrix.

Represent significance at the 1%, 5%, and 10% levels, respectively (two-tailed).

Empirical Results

To examine how the Shanghai-Hong Kong Stock Connect affects the green innovation of target companies, Table 5 reports the estimated results of the model (1). First, from the overall impact of the Shanghai-Hong Kong Stock Connect on the corporate green innovation in Column 1 of Table 5, the coefficient of Connect × Post in the total sample is 13.924, which is significant at the 1% level, indicating that the implementation of Shanghai-Hong Kong Stock Connect has improved the overall level of green innovation of the target firms of Shanghai-Hong Kong Stock Connect compared with non-Shanghai-Hong Kong Stock Connect firm (can also be seen in Figure 2). Next, we separate the green innovation into independent innovation and cooperative innovation and examine them separately. For the impact of the Shanghai-Hong Kong Stock Connect on the independent innovation of enterprises (See Column 2), the coefficient of Connect × Post in the total sample is 9.518, which is significant at a 5% level, indicating that the implementation of the Shanghai-Hong Kong Stock Connect has improved the green independent innovation level of the enterprises in the treatment group (the firms that are subject to Shanghai-Hong Kong Stock Connect) compared to those in the control group (the firms not subject to Shanghai-Hong Kong Stock Connect). Regarding the impact of the Shanghai-Hong Kong Stock Connect on corporate cooperation innovation (See Column 3), the coefficient of Connect × Post in the total sample is 4.407, which is significant at the 10% level. It shows that implementing the Shanghai-Hong Kong Stock Connect has improved the green cooperation innovation of firms in the treatment group (the firms subject to the Shanghai-Hong Kong Stock Connect) compared with those in the control group (those not subject to the Shanghai-Hong Kong Stock Connect). More importantly, implementing the Shanghai-Hong Kong Stock Connect promotes corporate green innovation in the treatment group, which is mainly reflected in improving the corporate innovation capabilities of green independent innovation.

The Impact of Capital Market Liberalization on Corporate Green Innovation.

, **, * represent the significant level at 1% 5% and 10% level.

Corporate green innovation in SHSC target companies and non-SHSC target companies.

Furthermore, to investigate the influential mechanism of the Shanghai-Hong Kong Stock Connect on the green innovation of target companies, we examine the two potential mechanisms: the investor governance effect and the stock price feedback effect. Table 6 reports the empirical results of model (2) and model (3). First, from the perspective of the investor governance mechanism of the Shanghai-Hong Kong Stock Connect, the coefficient of Connect×Post×Discuss is 16.945, which is significant at the 5% level. The results show that the Shanghai-Hong Kong Stock Connect can improve the active governance of investors through social media and thus promote green innovation. Second, from the exit threat mechanism from the Shanghai-Hong Kong Stock Connect, the coefficient of Connect×Post×Q in the total sample is −4.025, which is significant at the 5% level. The results show that the exit threat mechanism of the Shanghai-Hong Kong Stock Connect will bring about short-sighted managerial behavior and inhibit the green innovation output of firms. In general, capital market liberalization can significantly promote corporate green innovation. Compared with the negative impact of the exit threat mechanism, the positive effect of the investor governance mechanism from the capital market liberalization is dominant.

Influential Mechanism of Capital Market Liberalization on Corporate Green Innovation.

, **, * represent the significant level at 1% 5% and 10% level.

Robustness Check

A critical assumption in estimating the difference-in-difference model is that the treatment group and the control group have a parallel trend (Parallel Trend) before the policy change; that is, there is no treatment effect. Parallel trends test establishes a baseline for comparison, validates the difference-in-difference estimation, and strengthens the reliability of the findings. We take the implementation of the Shanghai-Hong Kong Stock Connect as an external policy shock to study its impact on corporate green innovation, which needs to satisfy the assumption of a balanced trend. We use the following two methods to examine. First, the Shanghai-Hong Kong Stock Connect was implemented in 2014, and we retained the samples before 2014 to test the difference in the green innovation level between the treatment group and the control group. As shown in column (1) of Table 7, the coefficient of Connect has not reached a significant level, indicating that before the implementation of the Shanghai-Hong Kong Stock Connect, there was no significant difference among the pilot firms on corporate green innovation between pilot companies and non-pilot firms. The results indicate that the treatment and control groups had e parallel trends before implementing the Shanghai-Hong Kong Stock Connect, which satisfies the parallel trend assumption. Second, we set different dummy variables in other years. Respectively, we set Pre1 before the implementation of Shanghai-Hong Kong Stock Connect as 1, then set Post0 in the implement year as 1, and set Post1 as the year after the implement year. We add Pre1, Post0, and Post1 into the model, respectively, and examine the difference in the level of green innovation between pilot and non-pilot companies in different periods. Column (3) of Table 7 shows no significant difference between the two groups before the Shanghai-Hong Kong Stock Connect implementation.

Robustness Test-Parallel Trend Assumption.

, **, * represent the significant level at 1% 5% and 10% level.

In comparison, there is a substantial difference between the two groups in the second year after the implementation of the Shanghai-Hong Kong Stock Connect. There is a lag in the effect of the Shanghai-Hong Kong Stock Connect. Thus, the parallel trend assumption is satisfied and supports the estimation validity of the difference in the difference method.

The placebo test is used to assess false positives, validate causal inference, and improve confidence in results in the robustness check of the difference-in-difference. To further examine that the impact of capital market liberalization on corporate green innovation is not due to other unobservable factors, a placebo test is conducted by changing implementation time. Suppose the Shanghai-Hong Kong Stock Connect was implemented in 2011. In that case, there will be differences in green innovation between the treatment and control groups since 2011, and the Connect × Post term can only be satisfied. Suppose the basic conclusion of our study is due to some unobservable inherent differences between firms in the control group and treatment group. In that case, the new implementation year will also lead to the same result. However, from Table 8, it can be found that the coefficients of Connect × Post × Discuss and Connect × Post × Q did not reach a significant level, indicating that the previous results are not due to some unobservable inherent differences between the firms in the treatment group and the control group.

Robustness Test-Placebo Test.

, **, * represent the significant level at 1% 5% and 10% level.

Considering that the investment distribution plan for 2014 was decided in 2015, we add back the observations in 2014 and consider 2014 as the year in which the policy was implemented, and the main empirical results in Table 9 remain.

Robustness Test-Added 2014 Sample.

, **, * represent the significant level at 1% 5% and 10% level.

A Tobit model is often employed in robustness checks to correct OLS bias and estimate causal relationships with truncation or zero inflation. In addition to the above robustness tests, since the number of corporate cooperative innovations cannot be negative, a Tobit model is applied for parameter estimation based on previous studies to avoid sample estimation bias and discontinuity (Simar & Wilson, 2007). The empirical results presented in Table 10 are consistent with the earlier results.

Robustness Test-Change Empirical Model.

, **, * represent the significant level at 1% 5% and 10% level.

Further Analysis

The Impact of the Regional Legal Environment

The regional legal environment plays a crucial role in implementing and enforcing policies, exhibiting significant disparities across different regions in China (Fan et al., 2001; Luo & Zhang, 2016). Areas with a robust legal framework typically exhibit effective execution of environmental laws and regulations. In contrast, regions with weaker legal systems often face challenges in environmental governance, leading to more pronounced environmental issues. Consequently, the effectiveness of the Shanghai-Hong Kong Stock Connect system in ecological governance varies significantly based on the local legal environment. Specifically, the environmental governance impact of the Shanghai-Hong Kong Stock Connect is more substantial in regions with a better legal environment compared to those with poorer legal frameworks.

To empirically test this hypothesis, we categorized our sample into two groups based on the regional legal environment rankings from the China Marketization Index released in 2016. A value of 1 denotes listed firms in provinces with a favorable legal environment, while 0 represents firms in regions with less favorable legal conditions. The results, presented in Table 11, indicate that implementing the Shanghai-Hong Kong Stock Connect significantly enhances corporate green innovation in areas with a relatively robust legal environment. Conversely, in areas with weaker legal environments, the effect of the Shanghai-Hong Kong Stock Connect on promoting corporate green innovation is not statistically significant. These findings underscore that the Shanghai-Hong Kong Stock Connect has a more significant marginal effect on environmental governance in regions with more robust legal frameworks. Our results provide empirical evidence that the regional legal environment significantly moderates the impact of the Shanghai-Hong Kong Stock Connect on corporate green innovation. Firms in regions with better legal governance structures benefit more from the Stock Connects initiatives to enhance environmental practices. This highlights the importance of local legal environment in shaping the outcomes of capital market policies on corporate behavior and environmental performance.

The Impact of Regional Legal Environment.

, **, * represent the significant level at 1% 5% and 10% level.

The Influence of Corporate Governance Characteristics

The decision-making process regarding corporate green innovation is influenced by external legal environments and the firm’s internal governance characteristics. Managers often prioritize short-term economic performance over environmental investments. However, green innovation is crucial for the long-term sustainable development of firms and can enhance their reputational standing. We measure agency costs using the ratio of independent directors and examine the impact of the Shanghai-Hong Kong Stock Connect on green innovation across firms with varying agency costs. Table 12 illustrates that in the higher agency cost group, the coefficient of Connect × Post is 5.998, indicating insignificance.

The Impact of Corporate Governance Characteristics.

, **, * represent the significant level at 1% 5% and 10% level.

Conversely, in the lower agency cost group, the promotion effect of the Shanghai-Hong Kong Stock Connect on corporate green innovation is significant, with a coefficient of Connect × Post at 14.235, significant at the 5% level. These results suggest that implementing the Shanghai-Hong Kong Stock Connect promotes corporate green innovation more significantly in firms with lower agency costs than those with higher agency costs. In summary, our findings highlight that while external legal environments play a crucial role, internal governance characteristics (particularly agency costs) significantly shape the responsiveness of firms to initiatives like the Shanghai-Hong Kong Stock Connect in promoting green innovation. Firms with lower agency costs demonstrate a more pronounced positive response, emphasizing the importance of effective internal governance structures in fostering sustainable practices and innovation.

Conclusion and Discussion

We examine the impact of capital market liberalization on corporate green innovation using data from Chinese A-share listed firms between 2011 and 2017, with the implementation of the Shanghai-Hong Kong Stock Connect in 2014 as a natural experiment. Our findings show that the Stock Connect has significantly boosted independent Green rather than cooperative innovation. We also explore the mechanisms behind this effect, focusing on investor governance and the exit threat. Our results suggest that investor governance’s positive impact outweighs the exit threat’s negative impact. Additionally, this effect is more substantial for firms in regions with better legal protection and lower agency costs.

Our study contributes to the literature in several ways. First, it expands on governance theory by exploring the interplay between investors’ active governance and “exit threat.” Previous studies have focused on foreign investors’ informational advantages in developed markets (Baker et al., 2003; Edmans, 2009; Foucault & Frésard, 2012; Loureiro & Taboada, 2015). Our research highlights how foreign investors, with their resources and expertise, can provide valuable information and influence corporate green innovation. Unlike the previous conclusion that capital liberalization like Shanghai Hongkong Connect will hinder the active governance mechanism and encourage the exit threat mechanism (Edmans, 2009), we find that although stock price feedback mechanisms may hinder green innovation, the benefits of investor governance mechanisms prevail under capital market liberalization. There is a significant gap in the current state of green innovation between listed companies in China and developed countries like the US. Companies have instead sought to address shortcomings to attract investors, emphasizing green innovation and social responsibility to differentiate themselves from competing manufacturing firms. This trend has significantly encouraged foreign investors to engage in governance through “voting with their hands,” thereby promoting improvements in corporate green innovation. These findings provide solid and practical evidence on the tradeoff of listed companies in emerging countries regarding investor preference and institutional differences.

Second, we add to the understanding of green innovation by examining market-driven governance rather than relying solely on regulatory pressures (Horbach, 2008; Laffont & Tirole, 1996). Our study shows that green innovation is driven by environmental regulations and investors’ willingness to tolerate short-term performance fluctuations. As a quasi-natural experiment, the Shanghai-Hong Kong Stock Connect demonstrates that market liberalization promotes independent green innovation, particularly in firms with solid legal protection and internal governance. Unlike traditional investments, green innovation involves long cycles, high risks, and complex decisions (Hall, 2002; Holmstrom, 1989). The Shanghai-Hong Kong Stock Connect is especially effective in promoting green innovation in firms with solid legal protection and internal governance.

Based on these findings, we offer several policy recommendations that could apply beyond China, particularly in emerging markets with varying legal systems. First, governments should continue to deepen capital market liberalization. Allowing foreign investors to participate can enhance market efficiency, improve information accessibility, and strengthen corporate governance. In emerging markets, gradual liberalization can reduce market volatility risks and promote sustainable growth. Second, firms should prioritize strengthening their corporate governance and environmental initiatives. While green innovation may not yield immediate returns, it improves resource efficiency and long-term sustainability. Foreign investors can help mitigate agency problems and promote better environmental governance, especially in emerging economies with developing governance practices. Finally, governments should incentivize firms to invest in green technologies, encouraging the transition from resource-intensive to technology-driven models, which will align with global standards and enhance long-term competitiveness in emerging markets.

The study has some limitations. First, future research could focus on patent quality as a measure of green innovation, distinguishing between high and low-quality patents. This would allow a deeper exploration of how liberalization influences the quality of green innovation. Second, the relationship between corporate green innovation and environmental investments remains unexplored. Future studies could examine whether these investments complement or substitute each other and how firms balance them under different internal and external conditions.

Footnotes

Ethical Considerations

This article does not contain any studies with human participants performed by any of the authors.

Author Contributions

Yinglin Wan; Conceptualization, Methodology, Supervision, Writing—original draft, Writing—review & editing. Jiulu Jia; Resources, Writing—original draft, Visualization. Jiacheng Fu; Conceptualization, Methodology, Validation, Formal analysis.

pervision, Writing—original draft, Writing—review & editing.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was funded by Humanities and Social Sciences Fund of Ministry of Education of China, grant number NO. 23YJC630168.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data that support the findings of this study are available from the corresponding author upon request.