Abstract

Enhancing the employment structure and alleviating the degree of labor-capital mismatch promotes domestic demand growth, economic restructuring, and long-term stability, resulting in high-quality economic development. In light of this, this paper investigates the impact and influence of inclusive finance on employment structure and labor mismatch. In response to an empirical study using data from 271 cities, the growth of inclusive finance has a considerable positive influence on both employment structure and labor factor mismatch. On this premise, the mechanism test discovers that industrial advanced adjustment, rationalization adjustment, and industrial adjustment intensity play diverse intermediary roles; The labor resource mismatch index can be lowered and the employment structure can be improved using industrial advanced adjustment, while the pursuit of the degree of industrial coordination is not always conducive to the realization of the effective allocation of the employment structure, and the intensity of industrial adjustment is too high, even though it significantly promotes the upgrading of the employment structure, it also exacerbates labor mismatch.. The heterogeneity test then reveals that the effects of inclusive finance on labor factor mismatch and employment structure varied depending on city size and geographic variations.

Plain language summary

This study explores how inclusive finance affects employment structure and the mismatch between labor and capital, which is key to driving domestic demand, economic transformation, and long-term economic stability. Using data from 271 cities in China, the research finds that the growth of inclusive finance has a significant positive impact on improving employment structure and reducing labor-capital mismatch. The study also shows that changes in industries—specifically upgrading, rationalizing, and intensifying—play different roles in this process. Industrial upgrading can reduce labor mismatches and improve employment structure, while excessive industrial coordination may not always lead to better job distribution. Furthermore, overly intense industrial changes can help upgrade the job structure but might worsen the labor mismatch. Lastly, the study reveals that the effects of inclusive finance on employment and labor mismatch differ based on city size and geographic location.

Introduction

Improving the employment structure and enhancing employment quality are fundamental livelihood issues that remain a top priority in the comprehensive development of a modern socialist country. However, China continues to face significant challenges in the employment sector, including structural unemployment and labor mismatch, which are exacerbated by economic pressures, technological advances, and emerging employment patterns. These issues severely hinder the quality of economic development (Cai & Wang, 2010). Therefore, optimizing the employment structure and improving employment quality through effective policy measures have become pressing concerns that require urgent attention.

In contrast to traditional finance, which places emphasis on the overall volume and scope of financial services, inclusive finance places emphasis on the expansion of financial services. It does this by assisting small, medium, and micro enterprises, as well as disadvantaged groups, in obtaining financial services at a reasonable cost, significantly widening the financial services’ income boundary, and enabling the financial system to support more employment processes (Peng et al., 2022). Since the Chinese government issued the Plan for Promoting Inclusive Financial Development (2016–2020) in 2015, a series of policies aimed at advancing inclusive finance have been introduced. As illustrated in Figure 1, “employment assistance” has consistently been a central focus of these initiatives. The policy emphasis has evolved in the following ways: (1) The focus has shifted from “targeting key groups” to “implementing employment priority policies and providing dedicated funds,” clarifying the shift from identifying groups in need to actively implementing support measures. (2) Inclusive finance has consistently prioritized the “small and medium-sized vulnerable” groups, with a particular focus on those facing employment difficulties. (3) The objective of “promoting employment” has expanded beyond increasing “quantity” to improving “quality.” This includes leveraging the labor absorption capacity of the service sector and channeling financial support to small and micro enterprises in key areas such as technological innovation, specialized industries, advanced manufacturing, foreign trade, and industrial upgrading, all of which contribute to employment stability and sustainable economic growth.

China’s policies related to inclusive finance and employment from 2015 to 2023.

Against this theoretical and practical backdrop, this paper seeks to answer two key questions: First, can inclusive finance drive a “qualitative” transformation in the employment structure? Second, if so, what are the underlying mechanisms? To address these questions, the paper examines the impact of inclusive finance on both the employment structure and labor allocation, exploring how industrial adjustment—both in terms of direction and intensity—mediates this relationship. Additionally, the paper investigates the heterogeneity of inclusive finance’s effects on employment structure and labor allocation efficiency, considering geographic location and city size without relying on regional characteristics.

This paper makes several key contributions to the existing literature. First, in the context of achieving high-quality, full employment, the role of economic and financial leadership in shaping employment has garnered significant attention from both theoretical and practical perspectives. While much of the existing research focuses on how inclusive finance increases overall employment and employment rates, this study shifts the focus to the upgrading of the employment structure and the dynamics of the labor market, examining whether inclusive finance can bring about a “qualitative” transformation in employment. Second, the paper demonstrates that industrial restructuring plays a crucial role in improving the employment structure and reducing labor mismatches through inclusive finance. By considering both the direction and intensity of industrial restructuring, this study enriches the theoretical understanding of how inclusive finance can support employment, offering a more comprehensive approach to the relationship between financial inclusion and labor market outcomes.

The structure of the remainder of this paper is organized as follows: the second part presents a review of the literature and related theoretical analysis; the third part outlines the measurement of relevant indicators and the construction of the empirical model; the fourth part provides the empirical analysis of the impact of financial inclusion on employment structure and labor mismatch, including benchmark regression results, tests for endogeneity and robustness, mechanism analysis, and heterogeneity analysis; and the fifth part offers policy recommendations based on the research findings.

Literature Review and Mechanism Analysis

Studies Related to Inclusive Finance

Scholars have extensively studied the concept and indicators of financial inclusion. When inclusive finance was formally introduced in 2005, it was explicitly defined as targeting micro and small enterprises, farmers, and low-income urban populations. In the following year, the United Nations’Blue Book on Inclusive Finance recognized that inclusive finance was increasingly playing a key role in addressing the issue of economic imbalance across nations. In 2013, the Decision of the Central Committee of the Communist Party of China on a Number of Important Issues Concerning the Comprehensive Deepening of Reforms emphasized the development of inclusive finance as a strategic priority. Since then, China has actively embraced the concept, with key policy documents like the Plan for Promoting Inclusive Financial Development (2016-2020) establishing a clear framework for national implementation and promoting broader access to financial services.

The definition of financial inclusion has evolved over time, with its indicators expanding beyond the initial eight proposed by Beck et al. (2007)—including the availability of financial institutions and ATMs—to encompass additional dimensions such as geographic coverage, affordability, and service accessibility (Arora, 2010; Gupte et al., 2012; Sarma & Pais, 2011). Over the years, the concept of financial inclusion has increasingly incorporated Chinese characteristics and local context, adapting to the country’s unique development needs.

Inclusive finance, due to its unique connotations and strategic positioning, has played a significant role in alleviating the financial constraints of “small, medium, micro, and vulnerable” groups, while also enhancing their capacity for risk resilience. It has contributed to key objectives such as increasing farmers’ incomes and reducing poverty (Chao et al., 2021; W.-B. Li et al., 2024; Peng et al., 2022). At the macro level, inclusive finance supports the high-quality development of the real economy (Dabla-Norris et al., 2015), reduces poverty (L. Li, 2018), improves banking stability (Ahamed & Mallick, 2019), and addresses energy poverty, thereby contributing to the achievement of the Sustainable Development Goals (Dash & Mohanta, 2024; Dong et al., 2022; Jahanger et al., 2024). At the micro level, inclusive finance helps reduce financing constraints for private enterprises, improves the corporate financing environment, and fosters innovation (Ali et al., 2023; Charfeddine & Zaouali, 2022; Lee et al., 2020). In this regard, inclusive finance plays a crucial role in addressing the imbalance in economic development, supporting both macroeconomic stability and microeconomic growth.

Inclusive Finance and Employment

Many academics have investigated and tested the effect of inclusive finance in boosting employment since it is crucial for advancing development, stabilizing employment, and safeguarding people’s livelihoods. Enhancing inclusive finance’s impact on employment has two main effects: first, it directly increases job availability by increasing financial scale and penetration (Brixiová et al., 2020; Chun et al., 2019; Song et al., 2024); second, it indirectly creates jobs by easing the financing burden on private enterprises, small and medium-sized businesses, and microenterprises, which in turn addresses the labor shortage (Ajide, 2020; Bruhn & Love, 2014). Research has been done to provide in-depth explanations of the connections between inclusive finance and employment rates and total employment, but the literature reviews on the connections between inclusive finance and labor allocation and employment structure are more pertinent to this research.

The first is the improving effect of financial inclusion on the structure of employment. The dual economy’s labor-intensive industry development is no longer able to satisfy the demands of economic transformation, and the financial and technological service sectors are experiencing a rise in labor demand as a result of the promotion of inclusive finance. Through the expansion of financial services coverage and the creation of jobs through enterprise development, inclusive finance in my nation has recently lowered the bar for businesses, particularly small and micro businesses, to enter the financial market and obtain financial services. This has had a substantial impact on the employment structure. According to Lin et al. (2019), China’s small, medium, and micro enterprises are primarily dispersed throughout the secondary and secondary industries, but the development of inclusive finance can enhance labor transfer in the primary industry due to the decline in income elasticity and “diminishing returns” of investment in the primary industry. In the third industry, inclusive finance encourages labor mobility across industries while also easing the financial challenges faced by small, medium, and micro businesses. Simultaneously, the use of digital components has led inclusive finance to propose stricter guidelines for the work structure. J. Hu and Lu (2024) found that digital inclusive finance leads to a higher demand for both high-skilled and low-skilled labor, while reducing the demand for middle-skilled labor, resulting in a polarization of the labor employment structure. Yang and Geng (2022) further refined this by identifying that the three dimensions of digital financial inclusion—depth, breadth, and digitization—positively impact the optimization of employment structure. Additionally, Tang et al. (2024) demonstrated that digital inclusive finance broadens the scope of financial inclusion and effectively stimulates employment growth in the urban private sector, which is positively correlated with shifts in industrial structure. Indeed, the job structure will unavoidably change in tandem with the development of financial services and technological advancements. In its member nations, the OECD projects that in the next 20 years, the percentage of occupations susceptible to automation technology will rise to 57%. In certain emerging nations, this percentage even surpasses 70%, and in China, it could reach up to 77%. Technology will automatically pick the necessary skilled workforce, Acemoglu (2002) pointed out, lowering the labor supply with strong substitutability and resulting in the phenomena of “employment polarization.” The current broad coverage of financial services encourages labor mobility across many industries, therefore industry-specific employment structures will also be modified correspondingly. What impact does inclusive finance have on the employment structure, then? Additional confirmation is required.

The second is the impact of financial inclusion on labor allocation efficiency. Structural contradictions in employment still exist in China’s labor market, and the mismatch between human resource supply and job demand, as well as the mismatch of resources in the labor market, continue to be the main problems of the “employment difficulty.” Labor mismatch in the employment market further contributes to unequal wage growth (Handel, 2003), the coexistence of unemployment and job vacancies (Shimer, 2007), and low labor productivity (McGowan & Andrews, 2015).. In the past, educational mismatch was thought to be the primary cause of labor market distortion because of issues like the unequal distribution of educational resources and the limitations of the household registration system. Though the educational distortion has lessened due to the progress of education reform, the labor force distortion still persists. Mateos-Romero and Salinas-Jiménez (2018) thinks that the “skill mismatch” issue is mostly to blame for the labor force’s present low level of job satisfaction. Ang et al. (2024) and Yan and Zhang (2024) found that the development of fintech and the agglomeration of financial institutions play a significant role in promoting the efficiency of labor allocation by reducing information asymmetry, alleviating the agency problem, and substituting low-skilled labor. According to Sun et al. (2022), digital inclusive finance takes into account the awkward position that small and medium-sized businesses occupy in the financial system. Digital finance will fully utilize the “labor pool” effect to address the issue of financial resources not being allocated in a timely manner to small and medium-sized businesses with high labor intensity and low capital intensity. This will allow labor to be dispatched flexibly in areas with redundant and insufficient allocation, making the labor market more efficient and mitigating mismatch issues. It is evident that financial services marketing has successfully reduced labor market inefficiencies.

Based on the aforementioned theoretical analysis, we can conclude that adjusting the industrial structure is crucial for improving the employment structure by encouraging labor transfer between industries or by mitigating the labor mismatch problem in the labor market. The industrial structure is impacted by the expansion and deepening of financial services, but whether this is a good thing or a bad thing depends on the circumstances. According to several academics, upgrading the industrial structure is facilitated by appropriate financial supplies and effective financial services (Aghion et al., 2005; Sasidharan et al., 2015). C. Wen et al. (2024) found that digital inclusive finance can optimize industrial structure, upgrade agriculture’s internal structure, and promote rural income growth, thereby reducing the income gap between urban and rural areas. Wen-jin et al. (2021) extended this conclusion by identifying a nonlinear relationship between the development of digital inclusive finance and industrial structure upgrading. Specifically, the breadth of digital inclusive finance coverage has a significant long-term positive impact on industrial upgrading, while both the depth and the level of digitization also contribute in a nonlinear manner. The optimization and upgrading of the industrial structure as well as the transformation of the economic development mode can be facilitated by increasing the availability and coverage of financial services, as noted by Xie et al. (2017) and Wang and Zhao (2019). These studies emphasize that changing the financial development mode is the fundamental component of altering the industrial structure. According to some academics, financial development may not always have a positive impact, and that excessive financialization of the economy hinders manufacturing firms’ ability to innovate, change, and advance. Second, the path of industrial adjustment affects how inclusive finance affects the industrial structure. Depending on the circumstances, it may also encourage advanced adjustment and industrial rationalization. According to M. Xu and Zhang (2015), industrial rationalization and adjustment are the driving forces in the near term, but advanced adjustment is primarily responsible for their long-term effects. F. Li et al. (2022) argue that digital inclusive finance positively impacts both industrial optimization and rationalization. Digital inclusive finance drives industrial transformation through factors such as residents’ income and technological innovation, which, in turn, influence industrial structure advancement and rationalization. Lastly, the adjustment of industrial structure is a process of “creative destruction.” On one hand, optimizing the industrial structure accelerates economic growth and spurs the development of new industries, leading to job creation. On the other hand, the significant changes accompanying industrial restructuring can lead to large-scale job destruction (Zhu & Xiong, 2009). Therefore, it is essential to consider both the direction and intensity of industrial structure adjustment when assessing its effects on employment and economic transformation.

In addition, changes in industrial structure lead to corresponding adjustments in employment structure from the demand side, and significantly influence the effectiveness of financial inclusion in reducing poverty and promoting employment. Therefore, understanding the dynamics of industrial structure is crucial for comprehending regional employment changes, economic performance, and industrial development (Drucker, 2015). Several scholars have examined the employment growth driven by industrial changes within specific sectors. For instance, Schettkat and Yocarini (2006) identified three key factors driving employment growth in the service sector: inter-industry productivity differences, inter-industry labor division (outsourcing), and changes in final demand. Lim and Lee (2019) emphasized the role of competitive markets in driving employment, further distinguishing between product and process innovations. They concluded that product innovations act as a catalyst for employment, while process innovations tend to have a negative impact on employment, particularly in more monopolistic markets. Scherer (1967) found a positive correlation between the employment of scientists and engineers and industry concentration. Additionally, Bathelt (1991) observed that employment in key technology industries is highly concentrated within large firms and specific sectors.

As financial structures and the efficiency of financial operations improve, a higher index of advanced industrialization makes it easier for financial inclusion to reduce financial poverty, increase employment, and enhance employment quality (Yue & Zou, 2021). Given these insights, What part then does industrial restructuring play in providing inclusive finance to address issues related to employment? Does the direction and strength of the adjustment cause a difference in this case? The mechanism of action between the three is seen in Figure 2, which illustrates the theoretical and practical significance of testing its actual effect in this procedure.

Mechanism of industrial restructuring and inclusive finance’s impact on jobs.

The analysis presented above will direct our attention to the following research questions: First, how does inclusive finance affect the structure of employment? Does it make the phenomenon of labor mismatch less severe? Secondly, what are the pathways via which inclusive finance operates? What functions do industrial adjustment intensity, rationalization, and advanced adjustment each have?

Research Design

Empirical Modeling

In order to identify the relationship between financial inclusion and urban employment structure and labor capital mismatch, the following fixed effects model is constructed:

In the upper formula, the bid i and t respectively represent cities and years, respectively. is explained by the variables to indicate the employment structure, and

Furthermore, industrial advanced adjustment, industrial rationalization adjustment, and industrial adjustment intensity are introduced, respectively, and combined with the model proposed by Baron and Kenny (1986) and the method proposed by Z. Wen et al. (2004), the model is set up as shown in Equations 3 and 4 in order to analyze the influence mechanism of industrial adjustment on employment institutions and labor mismatch index:

Among them, M

it

represents the possible influence mechanism, which are industrial advanced adjustment, industrial rationalization adjustment, and industrial adjustment intensity; Y

it

is the employment structure LS and the labor mismatch index Abstaul, γ and θ represent the estimated parameters,

Selection of Variables and Indicators

Explained Variable

Here is the method of drawing (Qi et al., 2020) to use the ratio of the number of employment (LS) of the tertiary industry and the number of employment in the secondary industry, and use (Bai & Liu, 2018) to use the annual average employment in various regions The number of people and regional GDP construct a labor mismatch index. This index reflects the mismatch of the total labor force of the region through the degree of distortion of factor prices. Due to the different labor configuration of each region, there will be a distribution of 0 as the dividing line. In order to make the regression coefficients consistent, the absolute value of the index is treated to get as an explanatory variable, the larger the value, the more serious the resource mismatch. When the return coefficient

Core Explanatory Variables

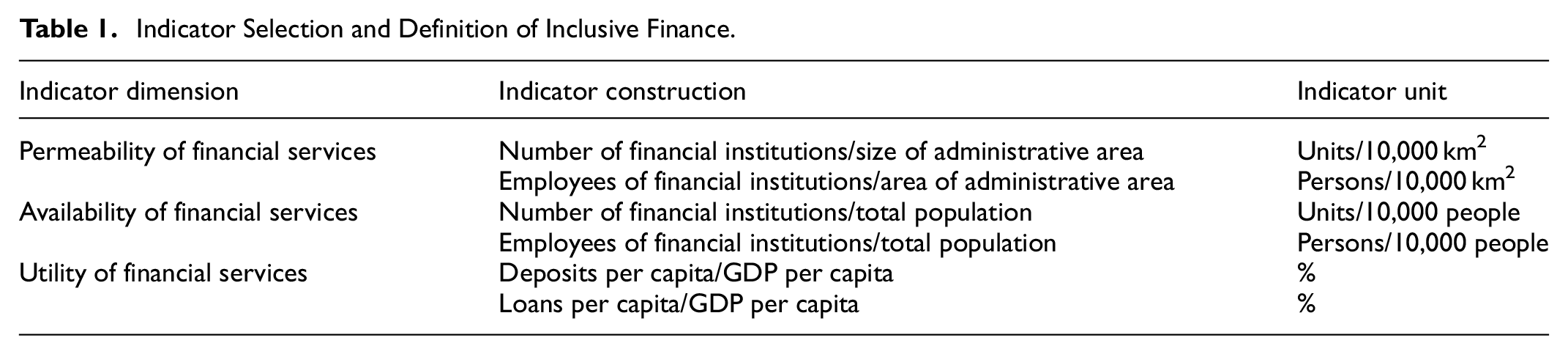

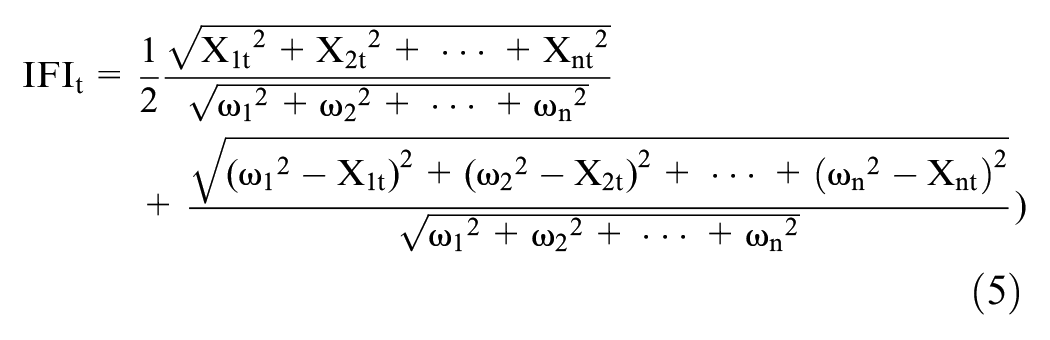

Consistent with many scholars, select indicators of the three dimensions of the permeability, acquisition and effectiveness of financial services, and build the regional inclusive financial development index (IFI). Specifically, draw on the data processing ideas of Sarma and Pais (2011), and use the mutant coefficient method and the Euclidean Distance Method to build an inclusive financial development index, as shown in Formula 5 and Table 1.

Indicator Selection and Definition of Inclusive Finance.

Dimensionless standardization, weighting, and synthesis of the inclusive finance index were done for the collected data, and the formula for measuring the inclusive finance index was constructed as follows:

The value of IFI is between [0, 1], and the closer the value is, the higher the level of inclusive financial development, and the lower the other. In the inspection of stability, using the Principle Component Analysis to synthesize the inclusive financial index. Weighted six sub -indicators to get a single indicator, that is, the inclusive financial index ZIFI.

Intermediate Variable

Here, the impact of various industrial adjustment directions on the improvement of employment by inclusive finance and the effect of industrial adjustment intensity on this process are tested using industrial seniorization adjustment (HIS), rationalization adjustment (TL), and industrial adjustment intensity (TSTR) as mediating variables, respectively. According to You and Zhang (2022), the ratio of the value added of the tertiary industry to the value added of the secondary industry represents the industrial advanced adjustment, which represents the optimization and upgrading of the industrial structure, primarily the process of development from lower to higher level. The TL index, on the other hand, is used to express industrial rationalization adjustment, which focuses on the variation in the quality of inter-industry coupling. This indicates the degree of effective resource utilization and the ability for industries to coordinate; the closer the TL value is to 0, the more the industrial structure tends to be in equilibrium and rational. Additionally, based on the methodology of Zhu and Xiong (2009), the change in the employed population’s proportion in industry subcategories is used to measure the intensity of industrial adjustment (TSTR). This indicator is used to analyze the magnitude of the intensity of industrial change; the higher the indicator, the greater the intensity of industrial adjustment. The effect of industrial adjustment on job creation may be counteracted if it is carried out too intensely.

Control Variables

Referring to the practice of the previous literature, all the control variables are defined here as follows: (1) the average wage of employees (Wage), (2) the disposable income of urban residents (Udi), and (3) the number of international Internet users (Net), and all the above indexes are logarithmized, and with the increase of the average wage of employees and the disposable income of urban residents, people’s consumption and investment capacity increases, which means that more people have the ability to participate in economic activities, which promotes the development and expansion of enterprises, which in turn leads to an increase in employment opportunities. At the same time higher penetration of the international internet reduces business information asymmetry, making it easier for entrepreneurs and small and micro enterprises to access financing opportunities in order to conduct business and create jobs. (4) The level of foreign investment (Foreign), expressed as the ratio of the actual amount of foreign capital used to the gross domestic product (GDP); (5) the degree of openness to the outside world (Open), expressed as the ratio of the total amount of foreign investment to the gross domestic product (GDP); and (6) the level of investment in fixed assets (Invest), expressed as the ratio of the total amount of investment in fixed assets to the gross domestic product (GDP). Foreign investment is usually accompanied by expansion and growth of enterprises, increasing the scale of production and services and leading to a demand for more labor. It also facilitates the expansion of the market size, promotes overall economic growth, provides development opportunities for various industries and expands the job market.

Sample Selection and Data Sources

The prefecture-level cities were chosen as study samples for the article between 2011 and 2021. We removed the data from four municipalities and a portion of the aberrant values from Beijing, Tianjin, Chongqing, and Shanghai in order to guarantee the data’s unity and regression effect. Treatments for division and ratio are carried out in turn. Following the foregoing, it is concluded that 271 prefecture-level cities constitute the research object. Statistics from the State Administration of Finance Supervision are used to calculate the number of inclusive financial indicators, which is equivalent to the number of financial institutions in China. The province Statistical Yearbook, China Financial Yearbook and China Statistical Yearbook are the primary sources of further data. A portion of the wind database income and the China Regional Finance Run report query are missing.

Empirical Results and Analysis

Benchmark Regression Results

The findings of the regressions between the labor capital mismatch index and inclusive finance and regional employment structure are presented in Table 2. Specifically, the regression results after taking the control variables into account are shown in columns (2) and (4). According to column (1), inclusive finance has a marginal effect on employment structure of 0.501, which is significant at the 5% level. This suggests that inclusive financial development facilitates the upgrading of regional employment structures and that inclusive finance significantly encourages the transfer of labor from secondary industry employment to the tertiary sector. The expansion of financial services aids in adjusting the employed population and encourages the creation of a more flexible and adaptive employment structure, whether it is through fostering entrepreneurship or aiding in the growth of the service sector. This aligns with the findings of Jiang and Fan (2022) and K. Zhang and Pang (2023), who demonstrated that digital inclusive finance significantly fosters entrepreneurial activity, thereby driving the optimization of employment structures. Yang and Geng (2022) further highlighted the role of digital inclusive finance, concluding that financial development facilitates employment structure optimization by reducing financing costs and promoting structural adjustments in the labor market.

Benchmark Regression Results.

Note. t-statistics in parentheses.

p < .01. **p < .05. *p < .1.

Columns (3) and (4) of Table 2 show the effects of financial inclusion on the regional labor-capital mismatch index. It is found that the estimated coefficients of inclusive finance are −0.355 and −0.325, respectively, and that they pass the 1% significance test. This indicates that as the financial inclusion index rises, regional labor mismatch is alleviated, leading to qualitative improvements in employment structures. Labor allocation efficiency has long been a critical issue in China’s job market. Previous studies, such as those by Bowlus and Sicular (2003) and Wang et al. (2007), revealed that while rural China has undergone substantial market-oriented reforms and witnessed growth in non-farm employment, labor demand and supply remain mismatched, partly due to the underdevelopment of the land market, insufficient education, and historical institutional constraints. The development of inclusive finance can effectively enhance rural human capital through innovations that improve skill distribution, thereby increasing labor allocation efficiency (Jaimovich, 2011).

A comparison of the four columns highlights that the expansion of financial services provides the labor force with more employment choices, encouraging workers to pursue jobs better aligned with their skills. This alleviates issues such as regional “employment redundancy” and underemployment, thereby mitigating structural unemployment and promoting a more efficient labor market.

Mechanism of Action Tests

Based on the earlier theoretical research, inclusive finance could encourage industrial restructuring to improve the employment structure and reduce labor capital mismatch. However, does industrial adjustment intensity impact the process, and does advanced or rationalized adjustment play a significant role in this regard? To identify the true mechanism via which inclusive finance enhances employment, we will put the aforementioned three processes to the test.

In the beginning, we examine how industrial restructuring affects employment structure. Table 3 displays the estimation results. The effects of industrial advanced adjustment are shown in columns (1) through (3). It is clear that all of the inclusive finance (IFI) results are significantly positive, supporting the validity of the full-sample estimation’s conclusion regarding inclusive finance and the optimization and upgrading of the employment structure. The overall impact of inclusive finance development on employment structure is 0.504, as indicated by the coefficient of inclusive finance in column (1) of 0.504. The coefficients of inclusive finance and industrial advancedization adjustment are 0.377 and 0.283, respectively, after the mediating variable of industrial advancedization adjustment (HIS) is added in column (3). These results are significant at the 1% level, indicating that the employment structure and industrial advancedization adjustment do in fact mediate the relationship between inclusive finance and the latter. The growth of inclusive finance can considerably aid in the advanced adjustment of industrial structure, as shown by column (2)’s inclusive finance coefficient of 0.451, which is substantial at the 1% level. This suggests that financial inclusion primarily provides financial support by directing limited resources to sectors with higher productivity and output growth, thereby driving the optimization and transformation of traditional industries (L. Xu & Tan, 2020). X. Zhang et al. (2019) further expanded the analysis of financial development, examining its impact on the structural upgrading of the manufacturing industry across three dimensions: financial scale, financial efficiency, and financial agglomeration. Their findings reveal that financial efficiency is positively correlated with manufacturing structural upgrading, while financial scale and financial agglomeration are negatively correlated. The optimization and upgrading of industrial structure, in turn, entails the emergence of new technologies and business models. This transformation generates a rising demand for highly skilled personnel, particularly in high-end manufacturing, information technology, and modern service industries (Ma et al., 2023). Consequently, the labor market has shifted toward high-skill, knowledge-intensive positions, fostering a significant improvement in the employment structure aligned with the demands of an evolving economy. Subsequent computations reveal that the employment structure through industrial advancedization has an indirect effect of inclusive finance of 0.128 (0.451 × 0.283), which accounts for 25.4% of the whole effect (0.128/0.504), and a direct effect that accounts for 74.8% of the entire effect (0.377/0.504). It is evident that the process of developing inclusive finance advances both the modernization and optimization of the employment structure as well as the advanced degree of industrial structure.

Mechanism Test I: Impact of Industrial Restructuring on Employment Structure.

Note. t-Statistics in parentheses.

p < .01. **p < .05. *p < .1.

The effect of industrial rationalization and adjustment (TL) is examined in Table 3’s columns (4) and (5). The regression coefficient of inclusive finance on the TL index in column (4) is 0.156, meaning that the index of industrial rationalization decreases by 0.156. In a similar vein, it is possible to calculate the indirect effect of inclusive finance on the employment structure through the adjustment of industrial rationalization, which is 0.063 (0.156 × 0.404), accounting for 86.5% (0.436/0.504) of the total effect. The dynamic development of resource allocation efficiency and coordination capacity among industries, which is reflected in the optimal allocation of production components among industries, is, in our opinion, the essence of the rationalization of industrial structure. The majority of factors of production transferred to the service industry are deployed in the consumptive service industry at the low end of the value chain, which is essentially a degradation of resource allocation. While inclusive finance eases the financing constraints of SMEs, guides innovation and entrepreneurship of SMEs, and promotes the inter-industry transfer of labor factors, the upgrading of the manufacturing industry has not yet been completed, and the development of the productive service industry endogenous to the high-end manufacturing industry is insufficient (Aduda & Kalunda, 2012). There are drawbacks to the industrial structure’s rationalization. Simultaneously, the index of industrial structure rationalization does not directly encourage the migration of laborers to the tertiary sector; instead, it places greater emphasis on the equitable distribution of production factors across various industries than on the growth of employment within individual industries (L. Hu et al., 2023). This indicates a restraint on the optimization and modernization of the employment structure.

The analysis of the intensity of industrial adjustment is presented in Table 3’s columns (6) and (7). The regression coefficient of inclusive finance on the intensity of industrial adjustment in column (6) is 0.421, significant at the 5% level, suggesting that the growth of inclusive finance leads to changes in the industrial structure. The calculations show that the indirect effect of inclusive finance on the employment structure through the intensity of industrial adjustment is 0.027 (0.421 × 0.065), which accounts for 5.43% (0.027/0.504) of the total effect, while the direct effect accounts for 91.5% (0.461/0.504) of the total effect. The impact effect of industrial advanced restructuring outweighs the intensity of industrial restructuring in terms of promoting the upgrading of the employment structure, as can be shown by comparing the regression coefficients in columns (3) and (7). However, a higher intensity of industrial adjustment does not necessarily translate into improved employment quality. The division of labor resulting from the same industrial policies may yield entirely different outcomes across regions (Massey, 1983). To gain deeper insights into these dynamics, the efficiency of labor allocation will be examined in subsequent analyses.

We test models (3) and (4) once more by substituting the labor mismatch index for the explanatory variable, as indicated in Table 4. After adding the adjustment of industrial advancement in column (3), the coefficient of inclusive finance is −0.307 and the coefficient of the adjustment of industrial advancement is −0.038, which is significant at the 5% level. This means that inclusive finance has an indirect effect of −0.017 (−0.038) on the labor mismatch index through industrial advancement. The coefficient of inclusive finance in column (1) is −0.325, meaning that the total effect of inclusive finance development on the labor mismatch index is −0.325. The direct effect accounts for 94.46% of the total effect (−0.307/−0.325), while the Mismatch Index yields an indirect effect of −0.017 (−0.038 × 0.451), which contributes for 5.27% of the total effect (−0.017/−0.325). A comparison of column (3) in Table 3 with column (3) in Table 4 shows that the advanced adjustment of industrial structure not only facilitates the upgrading of the employment structure but also significantly reduces the labor-capital mismatch index, thereby enhancing the efficiency of labor resource allocation. As Shi (2021) observed, the evolution of industrial structure is closely tied to the allocation of production factors across industries. Given that labor is one of the most critical production factors, its distribution among industries may directly influence the optimization of industrial structure. Thus, the optimization and upgrading of industrial structure are inherently synchronized with changes in the efficiency of labor allocation.

Mechanism Test II: The Impact of Industrial Restructuring on Labor Mismatch.

Note. t-Statistics in parentheses.

p < .01. **p < .05.

The indirect effect of inclusive finance on the labor mismatch index through the adjustment of industrial rationalization is −0.024 (−0.153 × 0.156), which accounts for 7.34% of the total effect (−0.024/−0.325), while the direct effect accounts for 92.62% of the total effect (−0.301/−0.325), as per the regression results in columns (4) and (5). The phenomena of labor distortion cannot be effectively mitigated by an increase in the industrial rationalization index; on the contrary, it may even make labor mismatch worse. Kang and Guo (2023) argue that resource mismatches directly reduce total factor productivity and exacerbate the irrationalization of industrial structure, which in turn further diminishes total factor productivity. This irrationality often manifests as an uneven distribution of labor across industries, resulting in labor mismatches. When the data from Table 3’s columns (4) and (5) are combined, it becomes clear that the adjustment of industrial rationalization is not a means of promoting inclusive finance-driven employment upgrading or lowering labor mismatch.

Lastly, examining the results in columns (6) and (7) of Table 4, it is evident that inclusive finance has an indirect impact of 0.0088 (0.421 × 0.021) on the labor mismatch index through the intensity of industrial adjustment. Comparing this with the total effect of −0.325, it becomes clear that a greater intensity of industrial adjustment, paradoxically, contributes to a mismatch in labor factors, hindering the effective allocation of labor resources. Furthermore, comparing column (7) of Table 3 reveals that while industrial adjustment intensity may bring some improvements to the employment structure, it also leads to labor capital distortion, thereby reducing the ability to allocate labor efficiently. Ma et al. (2023) argue from the perspective of capital bias in industrial adjustment, noting that during industrial restructuring, capital tends to flow preferentially into high-tech and high value-added industries, which have a higher demand for skilled labor. This creates a mismatch, as low-skilled labor cannot meet the demand of these sectors. Hornstein et al. (2005) further contend that technological changes have profoundly impacted both productivity and the labor market. This transition, from manufacturing to services, has not necessarily resulted in efficient resource allocation. Specifically, the efficiency of inter-industry labor transfer from traditional to new industries remains low, while some service sectors, particularly low-end consumer services, fail to adequately absorb the displaced labor force. This leads to labor concentration in low-value-added sectors and degrades overall resource allocation.

Robustness Check

After confirming in the previous section that inclusive financial development can facilitate the upgrading and optimization of employment structures and mitigate labor-cap mismatch, we attempted a series of robustness tests to see if there was still a potential bias issue even after adjusting for rich regional characteristic variables.

First, the financial inclusion index is constructed using a consistent method, with the benchmark model employing the approach outlined by Sarma and Pais (2011) to measure the financial inclusion index for each region. In the robustness test, the methodology of Tram et al. (2023) will be applied, utilizing principal component analysis to synthesize the financial inclusion index (ZIFI).

Second, the analysis explores whether the employment improvement effect of financial inclusion varies when different information sets are used. Specifically, we test whether excluding the impact of the COVID-19 pandemic in 2020 and 2021 on the global economy alters the results. Additionally, urban characteristic variables, such as per capita road area and per capita green space at year-end, are incorporated into the model. The test results are displayed in Table 5, where the regression coefficients of inclusive finance pass the significance test, confirming the previously mentioned fundamental conclusions.

Robustness Test I: Substitution Variables, Samples and Indicators.

Note. t-Statistics in parentheses.

p < .01. **p < .05.

Lastly, the instrumental variable method and the difference-in-differences (DID) model are employed to test for endogeneity. Columns (1) through (3) of Table 6 display the test findings for the one-period lagged inclusive finance index that was chosen as the instrumental variable. It is observed that both the labor mismatch index and the employment structure’s regression coefficients pass the test at the 1% level. This demonstrates that inclusive finance does considerably enhance the employment structure and job market after resolving any potential endogenous issues, supporting the validity of the previous regression results. Additionally, as a “quasi-natural experiment,” the Chinese government formally introduced the strategy of “developing inclusive finance” in the 2013 Decision of the CPC Central Committee on Several Major Issues Concerning Comprehensively Deepening Reforms. This decision marked a new phase in the development of inclusive finance in China, with the core objective of providing more convenient, efficient, and low-cost financial services to a broader range of social groups, particularly small and micro-enterprises, farmers, low-income individuals, and other underserved populations. This policy has played a crucial role in shaping the subsequent growth of inclusive finance in China. To account for this policy shift, the difference-in-differences model is specified as shown in Equation 6.

Robustness Test II: Endogenous Discussion.

Note. t-Statistics in parentheses.

p < .001.

Given that the conference took place at the end of 2013, Equation 6, which measures the construction of inclusive finance, gives 2014 to 2021 a value of 1 and 2011 to 2013 a value of 0. The other variables’ definitions and measurements align with the preceding section. The double difference model-based regression findings are shown in Table 6’s columns (4) and (5). The regression coefficient of labor factor distortion is −0.434, which is similarly statistically negative at the 1% level, while the predicted coefficient of employment structure has a positive sign and passes the significance test. This suggests that the labor factor distortion in the employment structure and the labor market has improved since the Third Plenary Session of the 18th Central Committee explicitly recommended the development of inclusive finance, so confirming the prior conclusion once more. In addition, it demonstrates that endogeneity problems have no impact on the benchmark regression’s outcomes.

Heterogeneity Analysis

Given this, the article will next examine the geographic location and city size of the two dimensions of the relationship in order to analyze the heterogeneity of the relationship. Previous analyses of the inclusive finance and employment structure, as well as the inclusive finance and labor capital mismatch index, focused more on the overall level and neglected to address whether the relationship between the two will show a differentiated pattern in different regions and between different categories.

First, consider the geographic differences across regions. Variations in geography and resource endowments have contributed to imbalances in economic development across China. Compared to the western region, the eastern and central regions exhibit higher levels of financial development, more complete industrial structures, and greater employment opportunities, which in turn attract high-quality talent. This suggests that the development of inclusive finance is more likely to improve employment outcomes through industrial restructuring in these regions. Building on the approach of C. Zhang et al. (2024), the urban sample is divided into eastern, central, and western regions. The regression results in Table 7 reveal that the employment structure has significantly improved in the eastern and central regions. In contrast, the development of inclusive finance does not appear to promote the upgrading of the employment structure in the western region. Additionally, the expansion of financial services effectively alleviates labor mismatch between regions. Specifically, the regression coefficient for inclusive finance in the eastern region is −0.053, indicating a negative correlation with the labor mismatch index, though this result is not statistically significant.

Heterogeneity Test I: Differences in Geographical Location.

Note. t-Statistics in parentheses.

p < .01. **p < .05. *p < .1.

Furthermore, the impact of inclusive financing will be impacted by variations in urban scale. The Notice on Adjusting the Division of Urban Scale published by the Chinese government categorizes cities into five categories: super cities (with a resident population of 10 million or more), megacities (with a resident population of 5–10 million), large cities (with a resident population of 1–5 million), medium cities (with a resident population of 0.5–1 million), and small cities (with a resident population of less than 500,000), considering the small sample size of small and medium-sized cities, megacities, mega-cities, and other cities are distinguished here, and the test results are shown in Table 8. inclusive finance has a significantly stronger effect on improving employment in supercities than in other regions, however, it also causes a labor-capital mismatch in the region, and compared with supercities, inclusive finance has a more significant effect on improving labor allocation efficiency in other cities. Megacities, characterized by vast labor markets, highly developed economic systems, numerous enterprises, and diverse industries, provide an environment where inclusive finance can rapidly reach a large number of small and micro-enterprises and individuals, offering essential financial support to drive employment structure upgrading. In contrast, the labor markets of small and medium-sized cities are relatively simple, dominated by labor-intensive industries. As a result, inclusive finance has a more substantial impact on enhancing labor allocation efficiency in these regions, particularly in rural areas.

Heterogeneity Test II: Differences in City Size.

Note. t-Statistics in parentheses.

p < .01. **p < .05. *p < .1.

Discussion

Employment has always been a major national concern, and achieving high-quality economic development and creating a new economic development pattern depend on finding strategies to encourage high-quality job creation and overcome labor factor barriers. In particular, this study examines the role of industrial restructuring in these processes. This article focuses on and explores the relationship between the growth of inclusive finance and the urban employment structure and the efficiency of labor allocation in the employment market. The findings indicate that:

First The development of inclusive finance not only significantly reduces labor mismatch but also positively influences the employment structure. Second, An analysis of various adjustments to the industrial structure reveals that high-level industrial restructuring is the most effective way to modernize the employment structure and improve the efficiency of labor allocation. However, the extent of industrial adjustments must be carefully managed; while such adjustments enhance the employment structure, they can also exacerbate mismatches in labor factors.

Furthermore, heterogeneity analysis revealed that the efficiency of labor allocation is even more pronounced in the center and western regions and cities and that the employment structure of inclusive finance has a more noticeable improvement effect in the east, central regions, and super cities. Geographical location and the size of the urban population have an impact on how inclusive finance affects labor configuration and employment structure.

The study’s findings are used in this article’s policy proposals for creating a more comprehensive and tolerant financial development framework, as well as some steps to address employment-related concerns. First, enhance strategic planning and expand the scope of financial services. Fully leverage the positive role of inclusive finance in driving improvements in the labor market by continuously refining employment-focused provisions within inclusive finance policies. By directing labor mobility through targeted financial support, these measures can effectively enhance labor allocation efficiency within the job market. Second, inclusive finance should be further promoted to foster the growth of small and medium-sized enterprises (SMEs) by enhancing financing efficiency, maximizing the availability of finance, and supporting scientific and technological innovation to help SMEs transition into high-value-added and high-technology industries, which will ultimately result in the upgrading of employment. Additionally, regional governments should consider the diverse impacts of industrial adjustment on employment and implement targeted industrial policies tailored to local employment conditions, avoiding uniform approaches that disregard regional differences.

The third is to enhance the ties between regions and focus on coordinated development. Regions should actively collaborate with neighboring areas to extend the reach of inclusive finance, thereby enhancing employment opportunities and facilitating broader industrial optimization and workforce advancement. Due to China’s large geographical expanse, the development of financial services varies significantly across regions. Economically and financially advanced areas tend to benefit disproportionately, attracting resources from less developed regions and exacerbating disparities. To address this, economically stronger cities should act as hubs to support the development of surrounding areas, fostering balanced progress and promoting equitable, high-quality employment growth nationwide.

Footnotes

Ethical Considerations

This research does not involve human participants or animals.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: We gratefully acknowledge the financial support provided by the National Natural Science Foundation of China (grant No. 72163021) and Jiangxi Provincial Social Sciences “Key Project of the 14th Five-Year Plan”(grant No. 21YJ01). In addition, we would like to express our sincere gratitude to the experts who generously shared their insights and suggestions.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data will be made available on request.