Abstract

Based on imprinting theories, we explored how CEOs’ academic experience impacts corporate high-quality development. Using data from Chinese listed companies between 2010 and 2019 and the least squares method, we discovered that CEOs’ academic experience increased corporate high-quality development by increasing corporate value creation and sharing. According to discretionary managerial theory, we further explored the boundaries of CEOs’ academic experience that affects corporate high-quality development. CEOs’ academic experience in corporate high-quality development is more significant when CEOs have power within the enterprise and when the product market is competitive and market-oriented. The results held when Heckman’s, the double-difference method, and the placebo test were used to address the endogeneity problem. Our findings contribute to the literature on the imprinting theory and corporate high-quality development and provide a basis for deciding how governments can promote corporate high-quality development from a corporate micro-decision perspective.

Plain language summary

This study explores how the Academic Experiences of CEOs affect the High-Quality Development in Chinese Listed Companies.

Keywords

Emerging economies’ economic development level has rapidly increased in the past three decades (Arena et al., 2018; J. Li & Lin, 2019). However, rapid economic development creates negative effects such as environmental pollution and low-quality products (Azadi et al., 2011; J. Li & Lin, 2019). With slowing economic growth, emerging economies struggle to reduce environmental pollution and change their economic development model (Wei et al., 2023). Therefore, the Chinese Government has

The high-quality development of an enterprise is the concentration of its competitiveness and potential for sustainable development (Atta Mills et al., 2021). Currently, there is no uniform standard for calculating high-quality development of enterprises. Many scholars use the sustained growth of total factor productivity (TFP) of enterprises to measure the high-quality development of enterprises. Total Factor Productivity (TFP) measures the level of productivity improvement of a firm based on given factor inputs (D. Shi et al., 2019). However, regarding economic development, stakeholders’ requirements for high-quality corporate development are not limited to improving productivity; enterprises are expected to shoulder additional social responsibilities, consider the public interest, and achieve socially harmonious development. Some scholars have argued that high-quality corporate development is closely related to competitiveness, growth, and corporate social responsibility (CSR; S. J. Huang et al., 2018).

Therefore, high-quality corporate development is essential for fostering competitive advantage and social responsibility. A growing body of research has demonstrated that the variability in corporate strategies is primarily attributed to CEOs’ personal lives and professional experiences. For example, the CEO’s academic experience positively influences investment and financing decisions and socially responsible investment (Cao & Guo, 2020; Ying & Han, 2021; X. L. Zhang et al., 2019). However, studies have not examined when and how CEOs’ academic experience affects high-quality corporate development. This study aims to fill that research gap.

China’s transition market provides an ideal environment for testing our framework because, firstly, the Chinese government has proposed a strategy for high-quality economic and corporate development as the foundation for high-quality economic development. Our research provides a timely examination of this topic. Secondly, since China acceded to the WTO, Chinese-listed companies have recruited many professors and researchers working in universities or research institutes as CEOs. As of 2020, 15.8% of listed companies in China had CEOs with academic experience, indicating that academic CEOs have become essential among listed company executives in China. Thirdly, although China is undergoing a complex economic transition, Confucian culture strongly influences social development. Scholars shaped by Confucian culture are social elites and moral role models. Scholars exhibit more robust creative ideas and moral values than individuals in other professions, which motivates them to seek the collective good for the entire social group. Therefore, in the Chinese business environment, we observe many differences in the relationship between academically experienced CEOs and high corporate quality.

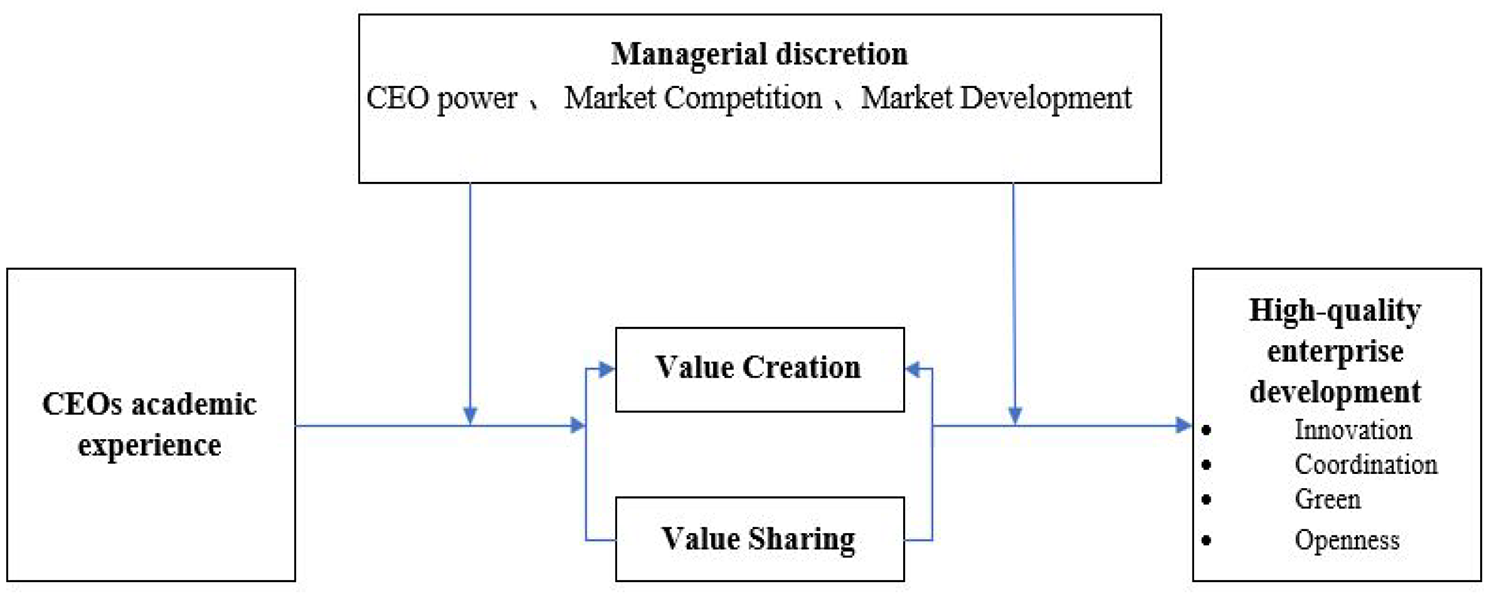

Accordingly, this study proposed a theoretical framework. Specifically, it explored how CEOs’ academic experience affects corporate high-quality development. Imprinting theory suggests that academic experience sensitizes CEOs and gives them a cognitive “competence imprint” of excellence. The imprinting theory posits that academic experiences render CEOs more sensitive and endow them with exceptional cognitive “capability imprints” and “moral imprints,” which facilitate superior value realization and the goal of socially shared development outcomes for enterprises. Our study uses data from 3,325 listed companies in China and compares the level of quality corporate development of CEOs with and without academic experience. Subsequently, it explores the mechanism whereby the former influences the latter. According to managers’ discretion theory, the impact of a CEO’s academic experience on corporate decision-making behavior is influenced by the discretionary power possessed by CEOs. CEO power, competition in the external market, and regional marketization differences are essential factors affecting CEOs’ decision-making ability. This study reveals that the CEO’s academic experience significantly affects corporate high-quality development when a CEO has more power. This impact is more significant in enterprises with higher degrees of marketization. Therefore, the enterprise exploits the CEO’s academic experience in fierce product market competition scenarios and ensures high-quality development.

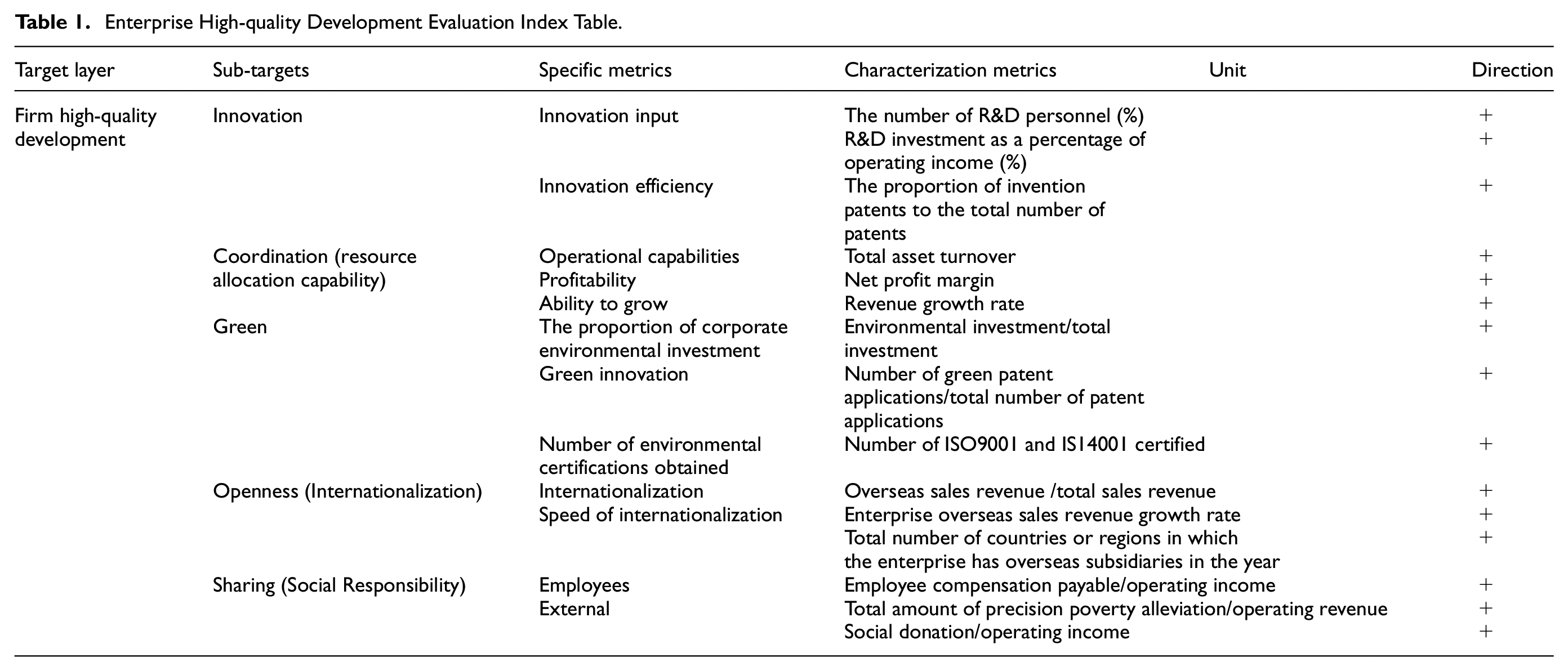

Our study makes the following contributions: First and foremost, it contributes to the literature on the determinants of high-quality development of firms, with a particular stream of research specific to China. Previous studies have focused on external factors’ impact on companies’ high-quality development (T. Guo & Sun, 2021; Hu & Tu, 2022; Wu & Cheng, 2021; Yan et al., 2023; G. Zhang & Meng, 2020). By demonstrating how CEOs’ academic experience affects high-quality corporate development, we expand the literature about the dynamics of high-quality business development and explain the differences in the high degree of quality development among firms. Secondly, We enrich the leadership literature by introducing ideas from imprinting theory. Existing research has used imprinting theory to explore the impact of CEO academic experience on CSR fulfillment (Y. B. Guo et al., 2022), financialization (Du & Zhou, 2019), cash holding levels (Jiang et al., 2019), and stock price collapse (He & Han, 2021). Our findings suggest that the imprinting effect of the academic experience is intrinsic and present in the complex decision-making processes of executives; we provide evidence for the application of imprinting theory to managerial decision-making. In addition, our study is significantly different from the effect of a CEO’s academic background on corporate strategy. The CEO’s academic experience has a sustained and far-reaching impact on his cognitive structure, managerial competence, and value shaping. This will affect his risk appetite and decision-making differences to a certain extent and ultimately be reflected in the firm’s behavioral decision-making. The CEO’s educational background (e.g., obtaining a master’s degree or a doctorate) is the executive’s ability to embodiment. At the same time, a CEO’s academic experience shapes their traits by their personal experiences. Studies such as (Bernile et al., 2017) and (Benmelech & Frydman, 2015) illustrate the impact of executives’ competencies and experiences on executives’ decision-making styles and the differential impact on firm decisions. In contrast to the previous use of TFP as an indicator of high-quality development of enterprises, the present study constructs an indicator system based on the Chinese government’s concept of “innovation, coordination, green, openness, and sharing” using the entropy weighting method—a technique for order preference by similarity to an ideal solution (TOPSIS)—to calculate the score of corporate high-quality development indicators. This index measurement method measures production capacity and input to serve society. Therefore, this measure is more comprehensive than TFP and can better measure quality development.

Literature Review and Research Hypotheses

Literature Review

Factors Influencing Corporate High-Quality Development

Prior research has found that macroeconomic and microfilm characteristics significantly impact firms’ high quality. Some studies have elucidated environmental regulation (H. Liu et al., 2020), financial environment (B. Shi & Tang, 2019), government audit (Dong & Zhang, 2021), media (G. Zhang & Meng, 2020), and the Internet (X. Liu & Hui, 2021) Digital technology innovation (B. Huang et al., 2023) as macroeconomic characteristics affecting corporate high-quality development. Micro-firm characteristics include the social capital owned by corporate managers (Lin & Long, 2021), internal controls (G. S. Zhang & Meng, 2020), innovative behavior (Z. Chen & Liu, 2019), and employee relations within the enterprise (L. Li, 2021).

CEO Academic Experience in China

Since 1978, China has implemented a timely policy of internal reform and external opening. After 30 years of tremendous innovation, a reform policy, and opening up to the outside world, China has achieved outstanding success in the global arena. Privatization of state-owned enterprises is the most crucial policy for economic reform. Implementing this policy has led many enterprising people, for example, university professors, to leave the non-business sector and enter private enterprises or start their own companies. This phenomenon of starting a new career in the private sector is called “literati going to sea” (especially for those who work for the government and government-affiliated institutions such as universities). Some university researchers have entered the corporate sector as senior managers, while others have set up their own companies. In our sample, approximately 15% of the CEOs of public companies had academic experience. In some European countries, only a few CEOs who have earned PhDs have had independent research experience. In contrast, this study focuses on CEOs who have engaged in full-time scientific research at a significant stage of their lives.

Impact of CEO’s Academic Experience

Corporate governance is a classic issue in the field of business management. The quality of corporate governance is closely related to the firm’s value (El-Deeb et al., 2022; Khatib & Nour, 2021). Managerial characteristics are internal factors that affect corporate governance. Existing studies have examined managers’ age (Jenter & Lewellen, 2015), gender (Gul et al., 2011), educational background (Bernile et al., 2017), and personal experiences such as military experience (Benmelech & Frydman, 2015) and the Great Depression experience (Bernile et al., 2017), all of which significantly impact firms’ decision-making. Current scholars have found that managers’ academic experiences are essential in shaping firms’ differentiated decision-making behavior.

Existing research adopts the perspectives of higher-order theory and imprinting theory to examine individuals’ academic experiences. Higher-order theory posits that senior executives’ demographic characteristics and personal experiences influence their cognitive patterns and values, leading to individualized decision-making styles. Higher-order theory elucidates the possible mechanisms through which individuals impact organizations. However, the most significant theoretical gap in higher-order theory is that, while it emphasizes the importance of the top management team, it overlooks the social mediators that may translate individual awareness into concrete actions and, consequently, influence organizational outcomes (Whitler et al., 2021) As a complement to higher-order theory, the imprinting theory emphasizes the impact of external environments on individuals and points out that such environmental influences require specific carriers. These ecological influences leave identifiable imprints on individuals, guiding their behavior and affecting their decision-making processes.

Existing research has found that Academic experience equips corporate senior management with a more cautious and objective mindset, instilling a sense of professionalism and rationality (Francis et al., 2015). Furthermore, long-term academic experience fosters a stronger sense of ethics and self-discipline among executives, discouraging corporate tax avoidance and high on-the-job spending (Francis et al., 2015; Zhou et al., 2017). It also enhances corporate environmental performance (Xu & Zhang, 2023) and the quality of food safety information disclosure (Bi et al., 2024).

The long-term, complex, and creative traits cultivated during academic research at universities, research institutions, or associations significantly shape executives’ mindset, behavior, dedication, and ethical discipline, forming their “competence imprints” and “moral perception imprints.” These imprints contribute positively to the high-quality development of enterprises.

Main Hypotheses

In the context of global sustainability concerns, high-quality corporate development necessitates a greater emphasis on the sustainability of society, environment, and economy, achieving a virtuous cycle between economic returns and social responsibilities. Value creation forms the foundation of high-quality corporate development. By producing competitive products and services, firms can achieve stable profitability and sustained economic growth (Hou et al., 2024). high-quality corporate development benefits the firm’s long-term development and positively impacts the entire economic system. Firms should not only focus on the interests of shareholders but also consider the rights of other stakeholders, including employees, customers, suppliers, and the general public (Lu et al., 2024). Through reasonable value-sharing mechanisms, firms can meet the reasonable expectations of different stakeholders, foster harmonious stakeholder relationships, and enhance the firm’s social reputation and public recognition.

In summary, value creation and value sharing are indispensable elements for high-quality corporate development, as they generate economic benefits while meeting the reasonable expectations of stakeholders. Inspired by this, this paper proposes hypotheses on how CEOs’ academic backgrounds influence their value-creation capabilities and the firm’s value-sharing level. Subsequently, based on the managerial discretion theory, this paper explores the boundary conditions affecting the relationship between a CEO’s academic background and high-quality corporate development. The theoretical framework is illustrated in Figure 1.

The theoretical framework of the study.

Value-Creation and Corporate High-Quality Development

According to imprinting theory, CEOs’ cognitive level and values are influenced by their academic experience. The theory states that individuals must meet three conditions to be imprinted: first, individuals experience periods of sensitization during their growth; second, the sensitization period significantly impacts the individual; and third, the imprint formed by the individual does not disappear even if the environment changes. The key sensitization influences on individuals includes their academic experiences. Scholars have argued that individuals maintain their beliefs and the ways of thinking they endorse during their academic experiences, even at an early stage of their careers. CEOs with academic backgrounds often possess a trait known as the “capability imprint,” which refers to the unique skills and knowledge backgrounds acquired in academic or scientific settings. This “capability imprint” makes them more sensitive to cutting-edge scientific knowledge and advanced management expertise.

The value creation ability of a company stems from its unique innovation capability, integration of internal and external resources, and consistent focus on a specific industry. CEOs’ academic experience facilitates their executive team’s ability to grasp market needs quickly and effectively deal with the various complex issues arising from the investment and financing process. Scholars-turned-CEOs can help enterprises develop core competitiveness, establish a competitive advantage, and strengthen their value-creation capabilities. Competitiveness theory suggests that enterprise competitiveness stems from the unique ability to innovate, integrate internal and external resources, and continue to focus on cultivating a specific industry. Regarding innovation ability, the innate interest of academically experienced CEOs makes them significantly more focused on innovation than the average CEO (Zhou et al., 2017). The professional knowledge and network resources of scholarly CEOs can help firms better attack the difficulties encountered when innovating and obtain critical information needed for innovation (Yuan et al., 2020). From the resource integration perspective, the academic experience of scholarly CEOs equips them with the ability to integrate resources. The academic activity explores a specific research object and identifies essential laws in a complex phenomenon. Resource integration analyzes and finds the essential law of development considering enterprises’ various complex resources and development goals. Scholars conduct in-depth research about a field to gain a regular understanding. It is taboo for academic research to change the object of research constantly. CEOs with academic experience have achieved specific research results and been recognized by the academic community. Academic CEOs choose to continue operations in a specific industry rather than diversify. Therefore, they understand the concept of continuing to focus on a specific field to obtain results. Thus, academic CEOs’ brand of competence accounts for their ability to innovate, integrate resources, and focus closely on industrial development. This helps companies form their unique core competencies and transform them into competitive advantages, optimizing their value-creation ability.

Value- Sharing and Corporate High-Quality Development

Value sharing aims to allow enterprises and the public to share in the fruits of corporate development. Through their academic experiences, CEOs contribute to enhancing the level of value sharing within their companies. The moral imprint that academic experience imparts on CEOs fosters a heightened sense of social responsibility and philosophical thought among senior executives, driving them to recognize the significance of corporate social performance and public recognition (Bi et al., 2024). Executives with academic research backgrounds actively strive to strengthen their moral awareness and increase their moral responsibility, reflecting societal recognition and the need to maintain personal reputation. Corporate communication with the public deepens stakeholders’ understanding of business operations and secures their support. Gaining stakeholder support is essential for value sharing and achieving legitimacy. Legitimacy theory posits that obtaining external support can facilitate smoother business operations within a company. Zhou et al. (2017) noted that “rigorous academic training cultivates rational thinking, making CEOs more cautious in decision-making; thus, the quality of corporate information disclosed to the outside world is higher.”Wen et al. (2019) also observed that “CEOs with academic experience possess a higher level of ethical standards and are more disciplined.” This rational, cautious thinking and a high degree of self-discipline create a robust self-monitoring mechanism that suppresses agency costs between management and shareholders. Consequently, companies led by CEOs with more academic experience exhibit greater information transparency (Ying & Man, 2021). This enhances stakeholder and public trust, enabling enterprises to garner more external support and ultimately fostering coordinated development. Enterprises are committed to assuming social responsibilities. Teaching, research, and service to society are the primary objectives of academic experiences, emphasizing dedication. Therefore, CEOs with academic backgrounds possess a higher moral sensibility and ethical imprint than the general populace, prompting them to proactively engage in socially relevant projects and give back to society. Consequently, the academic experiences of CEOs profoundly influence the realization of value sharing within their companies.

H1: CEOs with academic experience can increase the high-quality development of enterprises.

Manager’s Discretion

Managerial discretion is the basis for dealing with uncertainties from within the organization, company goals, and uncertainty with the external institutional environment, as well as the individual’s ability to execute and the ability of individuals to implement and realize their own will (Finkelstein & Hambrick, 1990). The CEOs’ autonomy is vital in strategy formulation, selection, and change (X. Zhang et al., 2020). We analyze the regulatory effect of a CEO’s academic experience on high-quality development from three perspectives: CEOs’ power, product market competition, and marketization.

CEOs’ Power

When a CEO obtains more power, they are granted more discretion and can have more autonomy over the enterprise’s decision-making, thus affecting high-quality development. First, “ powerful CEOs have several material, human, and information resources at their disposal inside and outside the enterprise” (Can et al., 2019). “This allows CEOs with academic experience to invest significant resources in innovation, providing the material basis for effective resource integration in the business” (Zhou et al., 2017, p. 154). When CEOs with academic experience have greater power, they can unilaterally veto proposals that are overly focused on the short-term benefit of the company to the board. When making decisions, they focus their resources on critical industries conducive to the company’s long-term benefits. The CEO’s power enables enterprises to concentrate their superior resources on deep plowing within critical industries, which is conducive to improving core competitiveness. Second, powerful CEOs select people who share their values and ethics to join the executive team, as the CEO’s proposals are more likely to be adopted. They may also choose people with a strong sense of ethics and social responsibility to join the board to receive more support for proposals related to social responsibility, thereby improving the level of CSR implementation and, thus, value sharing. Therefore, we propose Hypothesis 2:

H2: When the CEO has more power, the CEO’s academic experience has a more noticeable positive impact on the quality development of the company.

Market Competition

Fierce competition in the product market is an essential feature of the external environment that affects managers and the development of firms. When a company is in an industry where the product market is more competitive, its survival and development are more closely related to the CEO’s competence level (Hambrick, 2002). In a fiercely competitive market, the risk of failure highlighted by bankruptcy is high. To make the firm invincible in the face of fierce market competition, CEOs must maximize their full potential, strive to improve decision-making and optimize their development in a way consistent with their long-term development goal. To survive and achieve long-term development, enterprises must promote innovation, accelerate product upgradation, and improve corporate governance to enhance operational capabilities. CEOs with academic experience have strong systematic thinking abilities and are better at organizing enterprise development ideas. Much emphasis is placed on the role of academia in innovation, and every scholar regards innovation as a critical indicator for judging academic achievement (Benmelech & Frydman, 2015). The experience accumulated in academia and innovation enables CEOs to understand the nature and characteristics of innovation better; thus, they can provide targeted guidance during innovation, making it more possible to achieve successful innovation. Simultaneously, under fierce product market competition, enterprises survive and develop by enhancing their competitive advantage and increasing investment in social responsibility, thus improving their social reputation. CEOs with academic experience help enterprises obtain capital market recognition to reduce financing costs when the capital market transmits high-quality information. CEOs with academic experience will lead their companies to take on more social responsibility based on the need for corporate survival and development and their moral values. Industries with less competitive product markets are usually monopolistic. Most monopolistic enterprise developments depend on the CEO’s ability concerning market position and policy advantages. Thus, CEOs lack the motivation to launch subjective initiatives to improve the firm high-quality development. Therefore, we propose the following hypothesis:

H3: When the product market competition faced by enterprises is more intense, CEOs with academic experience have a greater impact on high-quality development.

Market Development

A good financing environment, rich talent supply market, flexible and effective market mechanism, fair and transparent legal environment, and appropriate policy support are necessary external conditions for promoting high-quality development. “China’s vast territory, different natural endowments in different places, and the various national policies since the reform and opening-up have caused the current imbalance in its regional economic development” (Long et al., 2023). The marketization process significantly reflects the differences in local policies, resource endowments, and legal environments. Therefore, marketization may significantly affect the relationship between CEOs’ academic experience and high-quality development. Generally, in areas with relatively high market penetration, the ability to allocate market resources is relatively strong, the financial market is developed, the supply of talent market is sufficient, and the mechanism used to protect intellectual property is perfect. CEOs’ academic experience allows enterprises to invest resources toward innovation (Francis et al., 2015). Simultaneously, in areas with high marketization, the media has a strong willingness and ability to monitor whether enterprises have faithfully fulfilled their duties to protect stakeholder interests; thus, CSR is higher (Fan et al., 2011). However, resource allocation and the financial environment are relatively backward in areas with low marketization, the awareness of the protection of Intellectual Property Rights is relatively poor, and companies lack resources and motivation to innovate. In such areas, the number of enterprises is small, the resources for development are scarce, local governments and firms have a closer relationship, and companies lack the motivation to fulfill their social responsibilities. Therefore, enterprises lack the conditions for high-quality development. On this basis, we propose the following hypothesis:

H4: When a firm is in a region with greater marketization, CEOs with academic experience have a greater influence on its high-quality development.

Research Design

Sample Selection and Data

The present study samples A-share companies listed on the Shanghai and Shenzhen stock exchanges between 2010 and 2019, excluding financial and insurance corporations, bankrupt entities, and firms with incomplete data. Listed enterprises hold significant importance in China’s drive toward high-quality development, as innovation and corporate social responsibility are intimately linked to firm scale. For example, research has underscored that larger firms generally necessitate diverse resources for innovation endeavors (Hoskisson et al., 2014). Consequently, firm size is widely acknowledged as a pivotal determinant in pursuing high-quality development. Since most prominent corporations in China are publicly traded on the Shanghai and Shenzhen markets, these listed companies were selected as the focal sample for our investigation.

The temporal scope of 2010 to 2019 was judiciously selected as comprehensive data regarding the academic backgrounds of senior executives was not readily accessible prior to 2010. The initial dataset encompasses all A-share companies listed on the Shenzhen and Shanghai stock exchanges, with data procured from the China Stock Market & Accounting Research (CSMAR) database. Notably, this database offers insights into whether executives possess academic experience but needs to specify the duration or nature of such experiences.

Throughout the data collection process, we identified potential biases stemming from selecting a specific time frame and excluding certain company categories. For instance, opting for an earlier period might constrain the temporal breadth of the dataset. Moreover, the limitations inherent in the CSMAR database, mainly the scant detailed information concerning executives’ academic experiences, could introduce uncertainty.

To counteract these biases, we meticulously processed continuous data during the data cleaning phase, trimming values at the 1st and 99th percentiles to excise extreme outliers. This meticulous approach yielded a refined sample consisting of 26,142 valid observations. All data were rigorously processed using Stata16, employing multiple testing methodologies to ensure the robustness and reliability of our findings.

Variable Definition and Model Setting

Measuring CEOs’ Academic Experience

The key independent variable, CEOs’ academic experience (ACADEMY), is an indicator variable that equals one if the CEO has academic experience and 0 otherwise. Academic experience includes teaching, conducting research at a university, or working in a professional non-profit research institution. Given the research hypothesis, the coefficient of ACADEMY is predicted to be positive and significant.

Measuring High-Quality Firm Development

“The indicators of high-quality development have been studied to construct different index systems and use the principal component analysis method to extract factors for analysis” (Dong & Zhang, 2021, pp. 5–8). “The TFP has been identified as an alternative indicator for measuring high-quality development” (B. Shi & Tang, 2019, pp. 85–86). The disadvantage of the principal component analysis method is that the expert score has a certain degree of subjectivity. Additionally, regarding application conditions, the correlation between the indicators must be high.

“The technique for Order Preference by Similarity to an Ideal Solution (TOPSIS) ranks the evaluation objects by measuring the best and worst solutions among the priority solutions. It calculates the distance between each object and the best and worst solutions, respectively, and obtains the relative proximity of each object to the best solution. The entropy-TOPSIS method is a combination of the entropy and TOPSIS methods. The entropy method uses the inherent information of the evaluation index to determine the utility value of the index, avoiding the bias caused by subjective factors to a certain extent” (B. Shi & Tang, 2019, pp. 85–86). Therefore, the weight value of the index is more reliable than the subjective weighting methods, such as the Delphi method and hierarchical analysis.

Firm TFP is primarily measured with value creation, ignoring the output of enterprise value sharing. Following prior studies (S. J. Huang et al., 2018; Yu et al., 2012), this study refers to “the five major concepts of the 19th National Congress of the Communist Party of China on high-quality economic development—‘innovation, coordination, green, openness, and sharing’—combined with the actual enterprise structure to measure the indicator system of high-quality development” (Yu et al., 2012, pp. 30–32). The study uses the TOPSIS method to calculate the high-quality development score of each enterprise. Table 1 presents the evaluation index system.

Enterprise High-quality Development Evaluation Index Table.

Control Variables

We include several control variables in our model that have been shown to influence the quality of an enterprise’s growth: firm size (Size), the natural logarithm of the firm’s total assets; gearing (Lev), total liabilities divided by total assets; firm establishment (Age), the natural logarithm of the firm’s time on the market; equity concentration (Top1), the percentage of shares held by the top shareholder; board size (Boardsize), the logarithm of the total number of board members; the percentage of independent directors on the board (Indep); executive ownership (Gm-holding), the number of shares held by executives as a percentage of total shares (i.e., the proportion of independent directors in the board of directors); and executive shareholding (Gm-holding), the proportion of shares held by executives to the total number of shares. We also control for factors related to the CEO’s characteristics: CEO’s age (CEOage), the logarithm of the CEO’s age; gender (gender), one if the CEO is female and 0 if male; and CEO’s compensation (CEOsalary), the logarithm of CEO’s compensation.

Empirical Model

The study uses the following model to test the effects of CEOs’ academic experience on high-quality firm development.

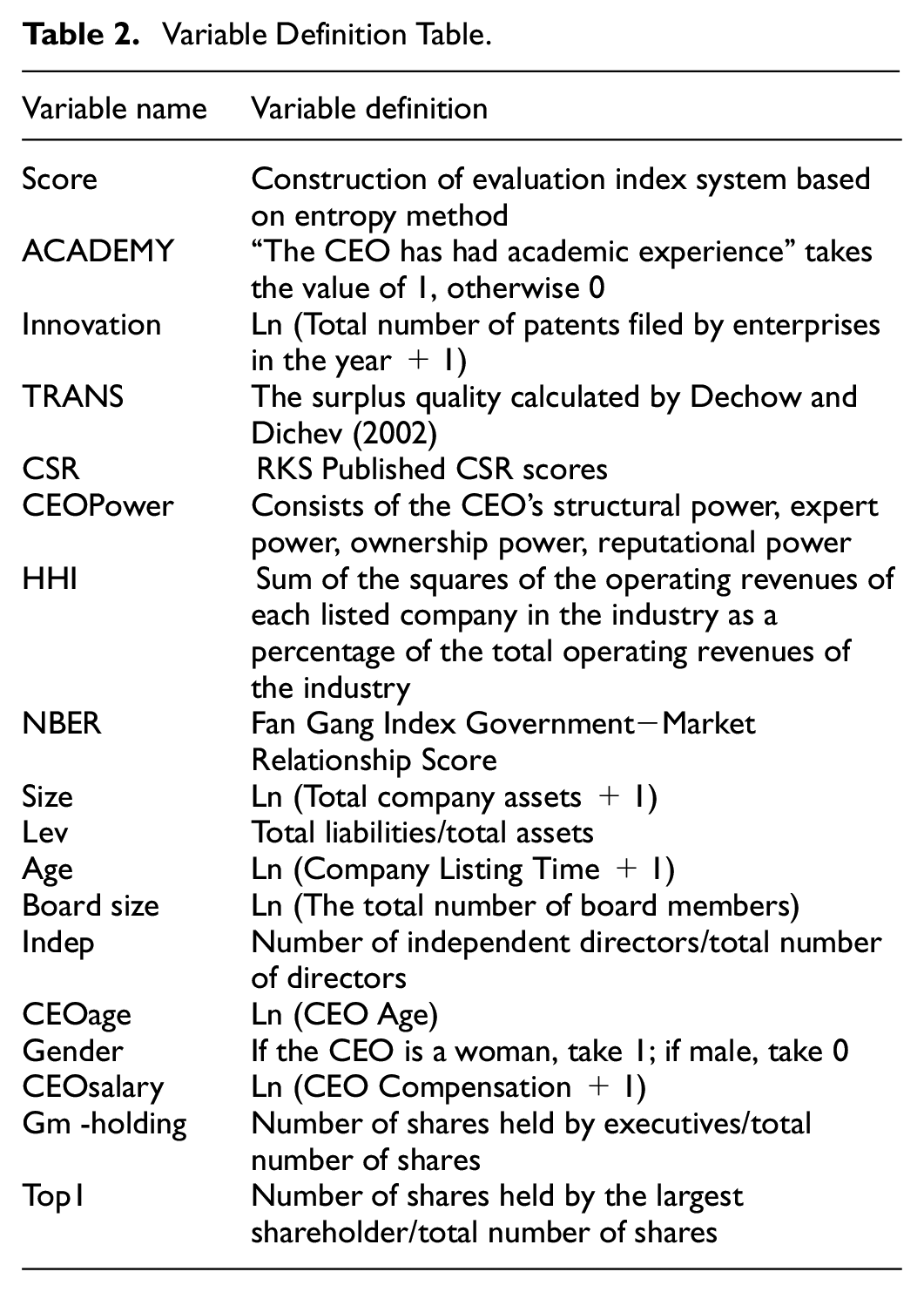

In Model (1), Scorei,t represents the high-quality development score of firm i in year t. The higher the score, the higher the firm’s high-quality development level. ACADEMYi,t is 1 if the CEO of firm i has academic experience in year t, and 0 otherwise. Controli,t represents the control variables. Year is the year dummy variable, and Industry is the industry dummy variable. The control variables are presented in Table 2.

Variable Definition Table.

Results

Descriptive Statistics

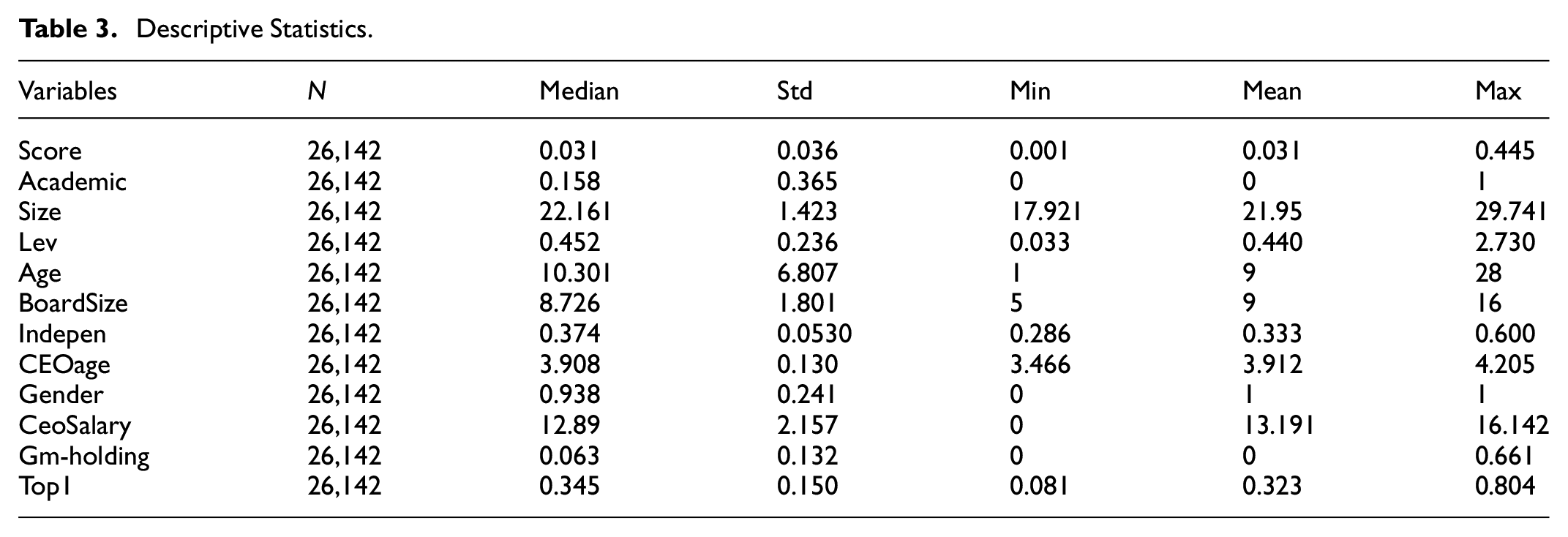

Descriptive results for the main variables are presented in Table 3. The statistical results show that the mean value of high-quality development of China’s listed companies is 0.031, which is relatively low; the maximum value is 0.543, and the standard deviation is 0.036, indicating that the difference in high-quality development among enterprises is relatively significant. Currently, the % of CEOs with academic experience in China’s listed companies is 16.2%. This shows the relevance of studying the relationship between CEOs with academic expertise and high-quality corporate development. Table 4 reports the results of the univariate tests. After grouping the sample by CEOs with or without academic experience, the sample size of CEOs with academic experience was 4,415, and that of CEOs without academic experience was 22,871. The mean value of the former group has a significantly higher-quality firm development score of 0.036 with a median value of 0.017 compared with the mean value of 0.031 of the latter group, with a median of 0.013. This indicates that the high-quality development scores of CEOs with academic experience are higher than those of CEOs without academic experience. The values of these variables were reasonably distributed with some degree of variation, consistent with previous Chinese studies (Ma et al., 2019).

Descriptive Statistics.

Univariate Test.

***, **, * Denote significance levels at 1%, 5%, and 10%, respectively.

Main Hypothesis

Table 5 reports the regression results of the primary test. Column (1) shows the regression coefficient of 0.003 for the CEO’s academic experience as an explanatory variable without the inclusion of control variables and after controlling for industry and year-fixed effects, with the level of high-quality corporate development (Score) as the explanatory variable, which is significantly positive at the 1% level. Column (2) shows that after adding the control variables and controlling for industry and year-fixed effects, CEOs’ academic experience regression coefficient is significantly positive at 1% for high-quality development (Score) as an explanatory variable. The coefficients of the control variables were very similar to those found in previous studies. For example, large and profitable firms score higher for high-quality development. This indicates that CEOs’ academic experience promotes high-quality development; thus, H1 is confirmed.

Association Between a CEO’s Academic Experience and a Firm’s High-quality Development.

Note.***, **, * Denote significance levels at 1%, 5%, and 10%, respectively.

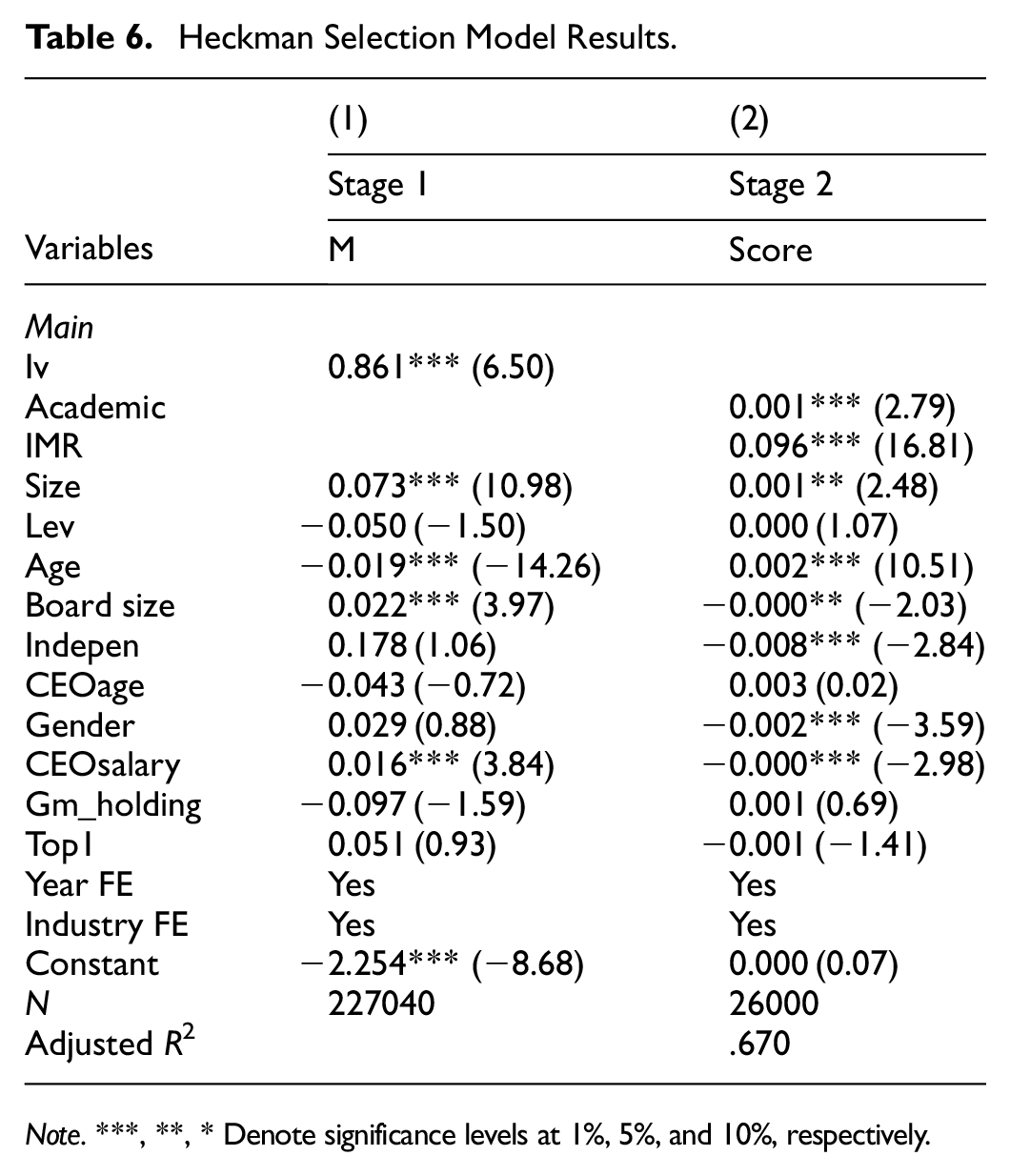

Heckman Selection Model

This study may have a self-selection problem because most companies where CEOs with academic experience choose to work are at a high-quality level of development. We employ a Heckman two-stage approach to mitigate this endogeneity problem. First, the number of higher-education institutions in the province where the listed company is incorporated is a more appropriate instrumental variable (Ying & Man, 2021). As the number of higher-education institutions in a company’s province of incorporation increases, the company gains opportunities to communicate with higher-education institutions, and the company is more likely to select managers with academic experience. However, no study has found that the number of higher-education institutions in the province where the firm is registered affects business development quality. Instrumental variables were added to the first regression stage using the probit equation. The inverse Mills ratio (IMR) calculated in the first stage was then added to the regression equation in the second stage. Columns (1) and (2) of Table 6 show that the regression coefficient for the instrumental variable in the first stage is 0.861, which is significantly positive at the 1% level. In the second stage, with the addition of IMR, the regression coefficient for ACADEMIC is 0.001, which is significantly positive at the 1% level. The coefficient for IMR is also significantly positive, indicating the presence of self-selection in the sample. However, this also suggests that the positive relationship between the CEO’s academic experience and high-quality firm development is robust to the sample after controlling for endogeneity issues.

Heckman Selection Model Results.

Note.***, **, * Denote significance levels at 1%, 5%, and 10%, respectively.

Propensity Score Matching (PSM) + Differences-in-Differences (DID)

To further mitigate the effects of endogeneity problems, such as reciprocal causality and omitted variables, on the regression results, this study uses a double difference model employing the CEO change event for testing. Therefore, Model (2) is developed to test this.

First, the company where the change in executive resulted in a CEO with academic experience was set as the treatment group, treat = 1. The CEO’s academic experience before and after the change was defined as treat = 0. The test interval was set to 1 year before and after the CEO change for 3 years. If the time of consecutive CEOs’ changes is less than 4 years, only the sample of the first change is retained. Model (2) focuses on the coefficient β3 of Post×Treat, which, if positive, indicates that the change in CEOs’ academic experience promotes high-quality development. However, a significant difference may exist in firm characteristics between CEOs with and without academic experience. Therefore, to reduce the problem of sample selection bias resulting from firm characteristics, propensity score matching (PSM) is performed on the sample before the double difference test is conducted to eliminate the endogeneity problem created by the sample selection bias. This is done by dividing the sample into companies with CEOs with academic experience as the treatment group () and companies with CEOs without academic experience as the control group. Subsequently, the CEO with academic experience is regressed as a dummy variable on all control variables to calculate the propensity score for each firm and matched using a 1:3 with put-back, thereby eliminating the bias of the sample. Finally, a double difference test is performed on the matched sample, and the results in Column (2) of Table 7 show that the coefficient of treat ×Post is 0.001, significant at the 1% level. This indicates that the level of quality corporate development increases significantly when a CEO with no academic experience is replaced with one with academic experience. Additionally, in the sample regression after PSM, the results in Column (1) of Table 7 show that the regression coefficient of the CEO’s academic experience is 0.005, significant at the 1% level. This indicates that the positive relationship between a CEO’s academic experience and high-quality corporate development is robust after controlling for sample selection bias.

PSM + DID Test Results.

Note.***, **, * Denote significance levels at 1%, 5%, and 10%, respectively.

Placebo Test

The academic experience of CEOs promoting high-quality corporate development may be coincidental. Following prior studies, this study conducts a placebo test to verify this (Figure 2) . First, firms with academically experienced CEOs are randomly assigned to the listed enterprises in the sample, generating new explanatory variables. Subsequently, the new explanatory variables are re-regressed on the high-quality development of the firms, with the number of regressions controlled at 500. If the main factor affecting high-quality development is among secondary factors other than the CEO’s academic experience, the regression coefficient of the new explanatory variables should be significantly positive. However, if the main factor influencing the high-quality development of the company is the CEO’s academic experience, the regression coefficient of the new explanatory variable should be insignificant. The regression coefficient and density of the new explanatory variables show that the distribution of the t-values is normal, centered on 0; most t-values of the new explanatory variables are 0; the regression coefficient of the new explanatory variables is insignificant. This proves CEOs’ academic experience is more significant in promoting quality corporate development than other factors. This figure displays the distribution of regression coefficients from 500 placebo tests. The dashed line indicates the 95% confidence interval.

Placebo test coefficient T-value kernel density map.

Robustness Checks

Replace Dependent Variable

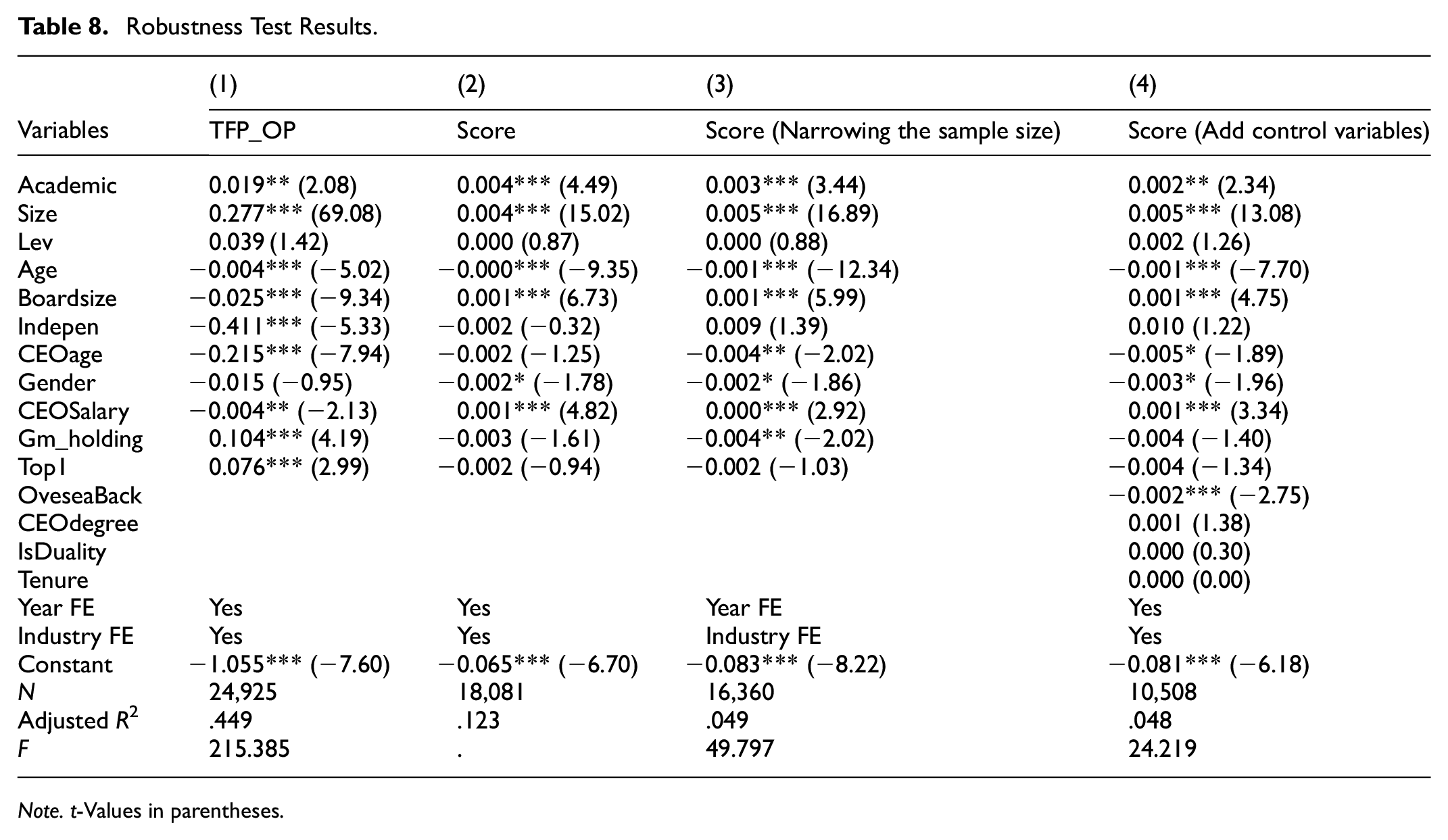

TFP is selected to measure high-quality development. The methods for calculating TFP are (Segarra-Ona et al., 2011; OP and LP), which are semi-parametric. The advantage of the OP method is that it corrects the bias of sample selection; therefore, this study uses the OP method for calculating the TFP of enterprises. Column (1) of Table 8 presents the regression results after replacing the explanatory variables. The results show that the regression coefficient of ACADEMIC is 0.019, significantly positive at the 5% level. This indicates that CEOs’ academic experience promotes high-quality development, and the regression results of the main effect are robust. ***, **, * Denote significance levels at 1%, 5%, and 10%, respectively.

Robustness Test Results.

Note. t-Values in parentheses.

Explanatory Variables Lagged by One Period

The impact of the CEO’s academic experience on the decision-making behavior and development of the firm does not occur in the current period; therefore, this study regresses the CEO’s academic experience lagged by one period on the level of high-quality development of the firm. Column (2) of Table 8 shows the results of its empirical test. The results show that the regression coefficient of ACADEMIC lagged by one period is 0.004, significantly positive at the 1% level. This indicates that the regression results of the main effect are robust.

Narrowing the Sample Size

Manufacturing enterprises account for a high proportion of the sample among the listed companies. The high-quality development of manufacturing companies is of immense significance in improving China’s overall corporate high-quality development. If CEOs’ academic experience significantly affects corporate high-quality development, this positive effect should exist in manufacturing enterprises. Column (3) of Table 8 shows the regression results after retaining the sample of manufacturing companies. The regression results show that ACADEMIC is 0.003, significantly positive at the 1% level. This indicates that the regression results of the main effect are robust.

Adding Control Variables

This study includes the factors influencing CEOs’ decision-making ability (CEOs’ overseas experience, CEOs’ academic experience, dual positions and one position, and CEOs’ tenure) in the regression equation for further testing to reduce the effect of omitted variables on the regression results. Column (4) of Table 8 shows the test results. After adding additional control variables, ACADEMIC is 0.002, significant at the 1% level. This indicates that the results of the main effects are robust after controlling for the effects of omitted variables.

Potential Mechanism Test

Value Creation

This study examines two potential mechanisms by which CEOs’ academic experience can impact high-quality corporate development: the ability of CEOs’ academic experience to help firms enhance their value creation capabilities and their level of value sharing. This study predicts that CEOs’ academic experience enhances corporate value creation. It uses the total number of patents filed by listed companies in the current year to measure the innovation ability of enterprises.

This study estimates the median number of patent applications in the year using the industry in which the enterprise is located. It classifies the enterprises for which the number of patent applications is less than the median number for the year. It uses the industry as a group with weak innovation ability and vice versa. Table 9 presents the results of the value creation mechanism test. Column (2) shows that in the group of firms with strong innovation capability, ACADEMIC is 0.003, significant at the 1% level. Correspondingly, the regression coefficient of CEOs’ academic experience on high-quality development is insignificant in the group with weak innovation capacity. This result is consistent with our expectations.

Potential Mechanism Test: Value Creation.

Note.***, **, * Denote significance levels at 1%, 5%, and 10%, respectively.

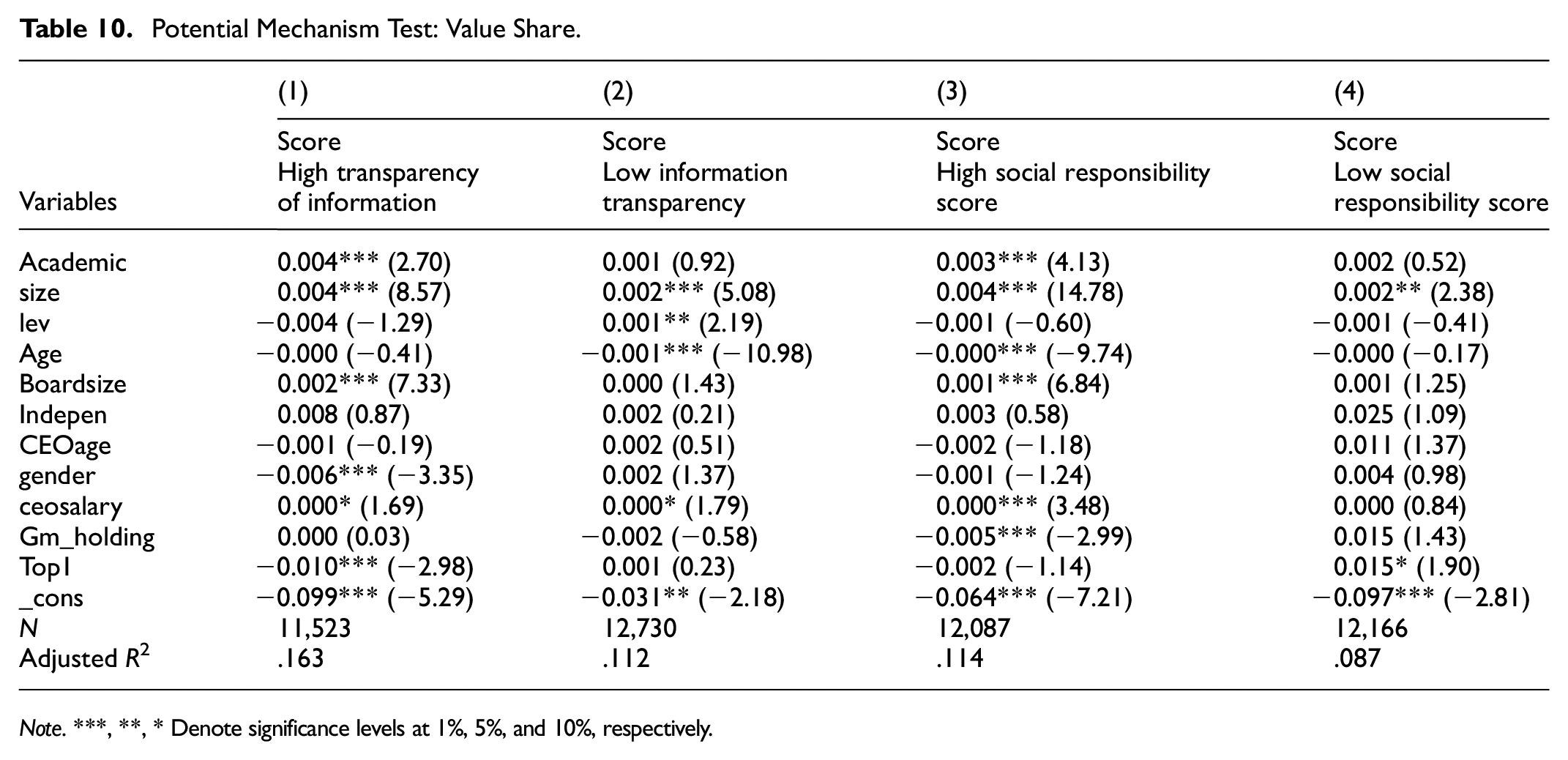

Value Sharing

Value sharing implies that firms make more transparent information available to the public and take additional social responsibility. This study predicts that the positive impact of CEOs’ academic experience on high-quality corporate development is more pronounced when information transparency is high, and the firm takes on additional social responsibility. The study measures firms’ information transparency using the surplus quality calculated according to a previous model (C. Chen et al., 2018). The regression results show that in the group with high information transparency, the regression coefficient of CEOs’ academic experience on high-quality corporate development is 0.04, significant at the 1% level. Following previous studies, this study uses the CSR score published by Rundling Global (RKS) to measure CSR (Quan et al., 2015). This score comprehensively evaluates the fulfillment of social responsibility reflected in CSR reports as an index, and a higher score means a higher degree of fulfillment of social responsibility. This study estimates the median social responsibility score of enterprises by industry. It classifies them into high and low social responsibility score groups based on whether they are greater than the median social responsibility score of the industry. Column (4) of Table 10 reports the regression results of CEOs’ academic experience on high-quality corporate development. The results show that in the group with high CSR scores, ACADEMIC is 0.03, significant at the 1% level. In the group with low CSR scores, ACADEMIC is not significant. This result is consistent with the study’s predictions.

Potential Mechanism Test: Value Share.

Note.***, **, * Denote significance levels at 1%, 5%, and 10%, respectively.

Moderating Effects

CEOs’ Power

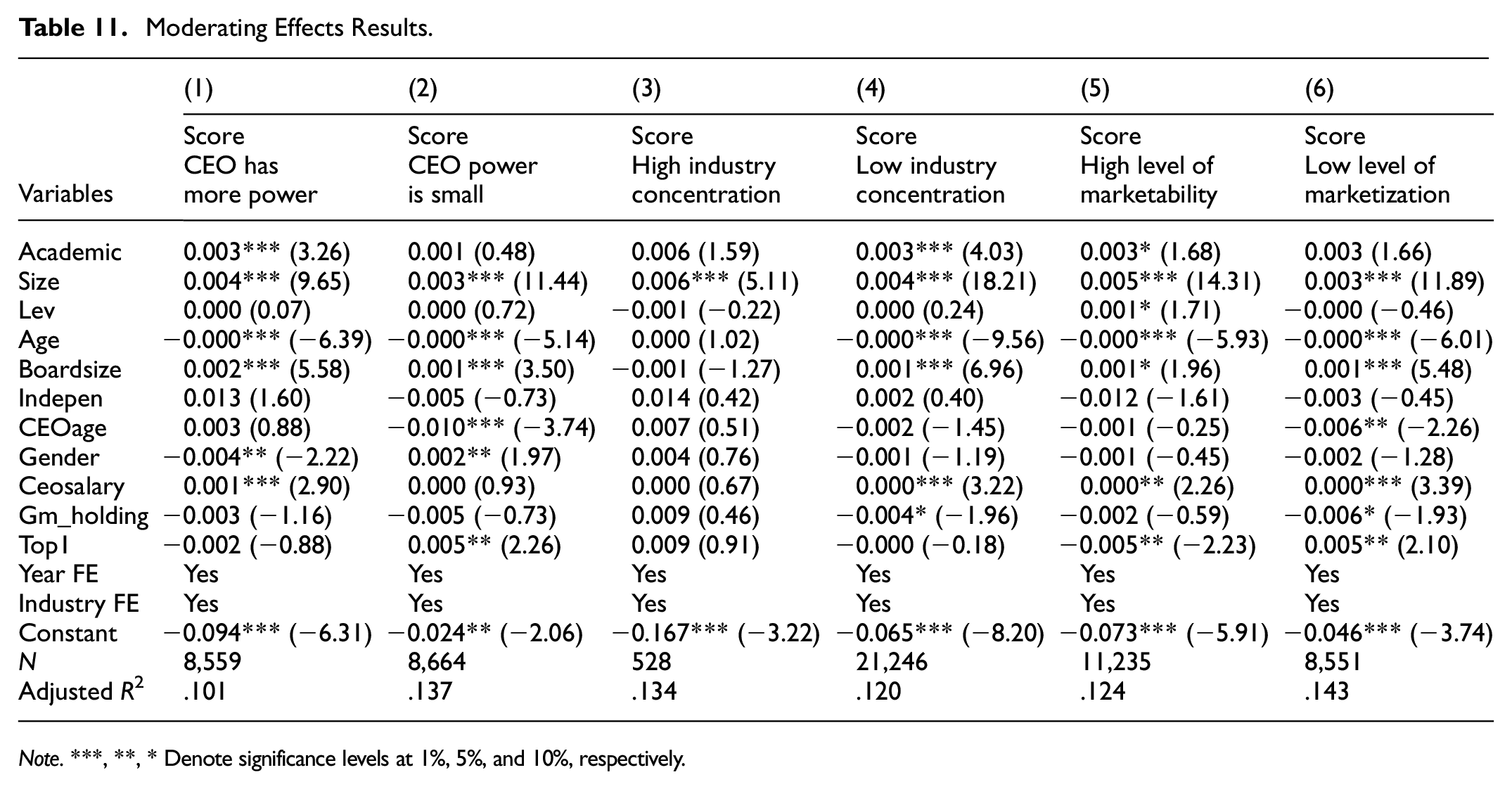

This study predicts that CEOs’ power positively moderates the relationship between CEOs’ academic experience and high-quality corporate development. Columns (1) and (2) of Table 10 show that ACADEMIC is 0.003, which is significant at the 1% level in firms with more excellent CEOs’ power. However, ACADEMIC is insignificant in firms in which CEOs have less power. These results confirm the inference that the more power the CEO has, the more significantly the academic experience of the CEO contributes to high-quality development. Thus, H2 is confirmed.

Industry Competition

Based on the previous analysis, this study predicts that industry competition positively moderates the role of CEOs’ academic experience and high-quality development. Columns (3) and (4) of Table 11 indicate that in industries with more competitive product markets, ACADEMIC is 0.003, significant at the 1% level, and not significant in industries with lower product market competition. These results confirm the moderating effect of product market competition between CEOs’ academic experience and high-quality corporate development; the positive impact of CEOs’ academic experience on high-quality corporate development is substantia in industries with a more competitive product market. Thus, H3 is confirmed.

Moderating Effects Results.

Note.***, **, * Denote significance levels at 1%, 5%, and 10%, respectively.

Marked Development

Based on the previous analysis, this study tested the moderating effect of marketization on CEOs’ academic experience in cases of high-quality development. Columns (5) and (6) of Table 11 show that ACADEMIC is 0.003 at the 1% level for firms in regions with a high level of marketization. ACADEMIC is insignificant for companies in areas with low marketization. These results confirm the moderating effect of marketization levels between CEOs’ academic experience and high-quality development; the positive effect of CEOs’ academic experience on high-quality development is stronger in regions with higher marketization levels. Thus, H4 is confirmed.

Discussion

Theoretical Implications

First, we extend the application of the imprinting theory by exploring how CEOs’ academic backgrounds influence corporate high-quality development. Previous research has primarily focused on the impact of a single imprint in individual experiences on managers, such as Y. B. Guo et al. (2022), which has confirmed the importance of academic experiences in shaping personal ethical norms and behavioral capabilities. However, existing literature must be more comprehensive in studying whether academic experiences simultaneously influence personal behavioral patterns and ethical norms. Our research fills this gap by finding that academic experiences strengthen personal ethical imprints and promote innovation capabilities and unconventional behavior patterns. This finding also resonates with the complex influence of CEOs’ academic experiences on decision-making, as proposed by Jiang and Xin (2024), providing a new perspective for a more comprehensive understanding of the multiple effects of academic experiences.

Moreover, our study indicates that although individuals may have obtained academic experiences before becoming CEOs, these experiences have deep-rooted imprint effects that continue to influence executive decision-making processes. This aligns with the findings of Z. Zhang et al. (2022), which suggest that CEOs’ academic backgrounds have a long-term impact on their strategic decisions and corporate behaviors. Therefore, our research not only deepens the understanding of how the individual experiences of executives influence corporate decision-making behaviors but also contributes to the literature on the impact of the academic experiences of executives on corporate high-quality development.

Second, our research further explores the economic consequences of CEOs’ academic experiences. Prior studies have often focused on analyzing the impact of CEOs’ academic experiences on specific decision-making behaviors of enterprises, such as innovation activities (Shen et al., 2020), initial public offerings (IPOs; B. Zhao et al., 2022), and green innovation (J. Zhao et al., 2022). These studies typically focus on how executives’ academic experiences affect a single decision-making behavior of enterprises, overlooking the impact of CEOs’ academic experiences on the overall decision-making capabilities of enterprises. The level of corporate high-quality development is a direct reflection of its comprehensive decision-making capabilities. This study confirms that CEOs’ academic experiences significantly impact corporate high-quality development, thus enriching the literature on how executives’ personal experiences affect corporate decision-making behaviors and deepening our understanding of this field.

Finally, our research contributes to the antecedent literature on high-quality corporate development. For example, scholars have studied the impact of macro factors such as government innovation subsidy policies (Yan et al., 2023), environmental regulation policies (T. Guo & Sun, 2021), and green credit policies (Hu & Tu, 2022), as well as micro factors such as internal controls of enterprises (G. Zhang & Meng, 2020) and the centrality of director networks (Wu & Cheng, 2021). However, these studies need to look into the critical role of managerial characteristics in corporate high-quality development. Our research shows that CEOs’ academic experiences significantly influence corporate high-quality development, providing a new perspective on the internal driving factors of corporate high-quality development. This finding broadens the scope of research on corporate high-quality development and points to new directions for future research.

Practical Implications

First, our findings confirm that the CEO’s academic experience affects high-quality corporate development. To achieve high-quality corporate development, reduce adverse environmental effects, and improve public health, companies should focus on core executives’ professional experience in shaping their decision-making abilities. This is because academic experience provides CEOs with strong systematic thinking abilities and inner discipline, which improves the company’s governance and comprehensive decision-making levels. Second, companies should provide a platform for people to display their talents, trust core management, and share power scientifically such that capable management exploits their abilities and becomes the driver of high-quality corporate development. This study also shows that companies perform better when CEOs with academic experience are given more power. At a government level, this study confirms the positive significance of CEOs’ academic experience in improving corporate governance to promote corporate value creation and sharing. The government should build a platform for communication between universities and enterprises and introduce more comprehensive supporting policies to encourage universities and research personnel to join or launch their enterprises. This can provide a talent guarantee for high-quality development. The government should play the role of “government with a purpose,” promote marketization in regions with poor economic development, allow the market to allocate resources, limit the government’s excessive intervention in the market economy, promote the transformation of enterprises from a passive waiting role to active participation in market competition, and create a favorable external environment for high-quality firm development.

Limitations and Future Research

Our study has the following limitations. Firstly, the constructed evaluation system of indicators for measuring high-quality development in enterprises may need to be more comprehensive to reflect the differences in high-quality development fully. In terms of assessment techniques, future advancements may involve leveraging more advanced data analytics methods, such as artificial intelligence and machine learning, to enhance the accuracy and reliability of the assessment system. In terms of evaluation dimensions, it is advisable to consider incorporating indicators from multiple dimensions, such as corporate strategy and operations, into the assessment system to gain a more comprehensive understanding of the high-quality development of enterprises. Secondly, we only examined the impact of CEOs’ academic experiences on companies’ high-quality development. This study did not explore the influence of the academic experience of other key executive positions, such as the Chief Financial Officer and Chief Operating Officer, on high-quality development. To fill this gap, future research could explore the impact of the academic backgrounds of other key executive positions, such as chief financial officers (CFOs) and chief operating officers (COOs), on high-quality development. This exploration could involve examining how their experience in the academic field affects various aspects of organizational performance, efficiency, financial strategy, and risk management. By including these perspectives, the research could provide a more comprehensive understanding of executives’ academic backgrounds and role in driving high-quality growth in organizations. Thirdly, this research focused only on Chinese listed companies and should have considered the specific circumstances of other emerging economies. Future research should focus on continuously improving the methods for measuring high-quality development in companies. Future research needs to broaden its scope to consider the specific circumstances of other emerging economies. This may involve a comparative analysis of companies in different countries or regions to understand their similarities and differences in achieving high-quality development. Additionally, legal, cultural, and policy environments in different countries or regions should be considered for their impact on corporate development. Through such research, a more comprehensive understanding of the pathways and critical factors for achieving high-quality development in different contexts can be attained.

Conclusion

We find that corporate CEOs’ academic experience positively impacts the high-quality development of firms. To confirm the robustness of the results, this study conducted a series of tests, such as replacing high-quality indicators, reducing the sample size, and adding control variables. The results of all these tests indicate that the main findings are robust. To mitigate the endogeneity problem in this study, we constructed a DID model based on the exogenous CEO change event to control for the endogeneity’s effect, and the findings remain valid. Within the firm, the impact of the CEO’s academic experience on high-quality firm development is greater when the CEO has more power. Regarding the external environment, the level of marketization has a positive moderating effect on the relationship between the two. The utility of the CEO’s academic experience in promoting high-quality corporate development is greater when the firm faces a more competitive product market.

Footnotes

Author Contributions

JZ: Conceptualization, Methodology, Software Writing, Reviewing, and Editing

Funding

The author disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Our research study was supported by the National Natural Science Foundation of China under Grant No. 72103144 and the Humanities and Social Sciences Foundation of the Ministry of Education of China under Grant No. 24XJJC790001.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data supporting the results of this study are available upon request from the corresponding author (Q.G.).