Abstract

Since the introduction of SSE 50ETF options in 2015, China’s options market has steadily developed, significantly augmenting participation in the nation’s financial market. The futures market, by offering a diversity of trading strategies, has augmented the capacity of financial services to cater to the real economy and has enriched the toolbox for risk management. This paper investigates the impact of the introduction of aluminum options on the volatility of the corresponding futures market, by examining the daily closing prices of the principal continuous contract of aluminum futures. By incorporating dummy variables into the model, the study evaluates the significance and polarity of the dummy variable coefficients to assess the effect of the aluminum options introduction on futures market volatility. A comparative analysis of coefficients within the TGARCH model prior to and following the emergence of aluminum options is undertaken to explore the asymmetry in the underlying futures market post-options launch. The findings indicate that the listing of aluminum options elevates the volatility of the aluminum futures market. Simultaneously, the informational asymmetry within the aluminum futures market appears to have enhanced.

Introduction

In recent years, the options market has become increasingly pivotal within the global financial landscape, with the burgeoning aluminum options market being particularly notable. As a significant financial instrument, aluminum options offer market participants opportunities to hedge risks, engage in arbitrage, and diversify their investment and financing avenues (Alsubaie et al., 2022; Hou et al., 2023). As a novel financial derivative, options can be combined with other financial instruments to devise various investment strategies. They aid investors in diversifying risks and enhance the financial market’s resilience against systemic risks, thereby bolstering the overall stability and robustness of the financial system. Therefore, it is crucial to strengthen research on the options market to further refine our nation’s capital market (Mo et al., 2022).

However, it remains a topic of academic and industry focus whether option market activities influence the market of the underlying asset, particularly its market volatility (Kocaarslan et al., 2020; Shibata et al., 2017). The volatility of the underlying asset price serves as avital indicator of market risk and is a key factor in option pricing. ln theory, options market activities may affect the volatility of their corresponding underlying asset markets. Economic theory posits that options trading can impact the futures market in numerous ways, thereby influencing futures contract prices and the volatility of futures markets (Yahya et al., 2023). For instance, options trading can enhance financial market liquidity, attracting more traders to derivatives markets. Concurrently, it could augment market transparency, supplying more information, and improving the price discovery mechanism (Rahman, 2022; Maghyereh & Abdoh, 2020). This helps traders gain a more comprehensive understanding of market conditions. However, the direction and magnitude of this effect can be influenced by a multitude of factors, including market depth, liquidity, and various macroeconomic factors. Therefore, empirical research is indispensable to investigate the real-world implications of this impact (Tian et al., 2022a).

The research hypotheses of this paper are as follows:

The motivation for this study is to explore the impact of aluminum options listing on volatility and information asymmetry in the aluminum futures market. Aluminum, as a crucial industrial raw material, significantly influences the global economy due to its price volatility. Options, as an emerging financial instrument, have the potential to alter market dynamics. However, there is a scarcity of research on the impact of aluminum options on the aluminum futures market. By empirically analyzing the specific effects of aluminum options listing on the futures market, this paper aims to provide valuable insights for market participants and policymakers, thereby promoting more effective market regulation and more robust investment decisions.

Despite numerous studies examining the interplay between options and futures markets, there is a comparative dearth of research focusing on the influence of the aluminum options market on the volatility of aluminum futures markets (Borgards et al., 2021). Aluminum, as a vital industrial raw material, exerts a substantial influence on the global economy due to its price volatility. Hence, investigating the impact of aluminum options on the volatility of the aluminum futures market holds considerable theoretical and practical significance. In undertaking empirical research on the effects of aluminum options on the underlying futures market volatility, key scientific issues that need to be addressed include:

First, as both options and futures are financial derivatives, they share a close relationship. In theory, the presence and activity in the options market exert influence on its corresponding futures market. For instance, substantial buying or selling of options may affect the prices and volatility in the futures market. Second, information from the options market can be utilized to predict volatility in the futures market. Volatility, being one of the most critical variables in financial markets, bears significant implications for risk management and investment decisions. Third, the behaviors of traders in both the options and futures markets significantly influence market volatility. Trader behavior is shaped by several factors, including their risk appetite, information-acquisition capacity, and trading strategies.

The aim of this paper is to conduct an empirical examination of the effect of aluminum options on the volatility of the aluminum futures market. By scrutinizing the trading data in the aluminum options market, we aim to uncover the relationship between options market activity and futures market volatility. This understanding could furnish valuable insights for market regulation and investment decision-making. Focusing on aluminum options, this study endeavors to address three pivotal scientific questions pertinent to this task. We utilize the daily closing price of the continuous aluminum futures contract from December 10, 2017, to May 10, 2023, as the data for investigating the specific impact of aluminum option listing on futures market volatility. During the research process, we employ the Eviews 10.0 software to perform an empirical analysis of the return series, selecting the GARCH model as the primary research instrument. We incorporate dummy variables into the model and assess the significance and directional values of these dummy variable coefficients to gauge the effect of aluminum options listing on futures market volatility. Simultaneously, we compare the coefficients of the TGARCH model pre- and post-listing of aluminum options to analyze asymmetrical shifts in the futures market following the introduction of options. Our findings reveal that the listing of aluminum options escalates the volatility of the aluminum futures market and ameliorates the information asymmetry effect within the futures market. Finally, drawing on our empirical findings, we propose several recommendations for the development of our derivatives market from the perspectives of various participants.

The main findings of this study are as follows:

(1) The listing of aluminum options significantly increases the volatility of the aluminum futures market. Analysis using GARCH and TGARCH models demonstrates that the introduction of aluminum options leads to a substantial increase in market volatility, indicating that options market activities have a significant impact on price fluctuations in the futures market.

(2) The listing of aluminum options reduces information asymmetry in the market. The model analysis reveals that the introduction of aluminum options decreases the effect of information asymmetry. The options market provides more price information and transparency, enhancing the price discovery mechanism and promoting fairer information dissemination and price formation.

(3) There is an asymmetry in the volatility response after the listing of options. TGARCH model results indicate a significant asymmetry in the volatility response of the aluminum futures market to positive and negative information shocks. Specifically, the impact of negative news on market volatility is greater than that of positive news. This effect is mitigated after the listing of options, suggesting that improved market transparency reduces the excessive influence of negative information on market volatility to some extent.

Related Work

Research on the Aluminum Market Futures and Commodity Futures

Aluminum, a critical industrial raw material, experiences price volatility influenced not only by supply and demand but also by various factors such as international markets, policy changes, and inventory levels. Unlike financial or other commodity options, the aluminum options market involves numerous actual producing and consuming companies whose hedging needs and trading behaviors can uniquely impact futures market volatility. Additionally, the relatively nascent development stage of the aluminum options market means that its liquidity and maturity have not yet reached the levels seen in other options markets, potentially leading to greater volatility. These distinctive characteristics of aluminum options warrant thorough research and analysis to better understand their impact on the futures market.

In a review of related studies, prior research has explored the impact of financial options, energy options, and options on various metals on the volatility of corresponding futures markets. For instance, Mahajan et al. (2022a) found that the introduction of crude oil options significantly influences market volatility, with effects varying across different time scales. Similarly, Tian et al. (2022b) demonstrated that while options trading enhances market liquidity in the natural gas futures market, its impact on volatility depends on the market’s maturity. Studies on metal futures markets, such as those focusing on gold and silver options, typically indicate that the introduction of options improves market liquidity and the price discovery function, though the effects on volatility are complex. In contrast, aluminum options, as derivatives on a key industrial raw material, have a distinct market participant structure and supply-demand dynamics, resulting in a unique influence on futures market volatility. By systematically analyzing aluminum options, this study further deepens the understanding of the impact mechanisms within metal options markets and provides new empirical evidence in this domain.

Research on the Impact of Financial Option Listing on the Corresponding Spot Market

Currently, numerous scholarly studies focus on the impact of financial option listing on the corresponding spot market. Options are financial derivatives that provide market participants with additional tools for investment, hedging and risk management (Chen et al., 2022; Zhang et al., 2022). Therefore, the listing of options may attract more investors to the market, thus increasing the depth of the market. The existence of an options market may help to better discover future prices, this is because option prices are an expectation of future prices which is formed by the consensus of market participants. Therefore, the listing of options may improve the price discovery function of the spot market. Options trading can lead to greater spot price volatility because option traders may hedge their option positions by buying and selling spot. Therefore, the listing of options may increase the volatility of the spot market. When conducting such studies, quantitative methods are needed to assess the specific impact of options listing on the spot market, such as conducting event studies and constructing financial models. Bae et al. (2004) show that while futures trading in Korea improves spot price volatility and market efficiency, volatility spillovers are also present in stocks that do not trade futures. They further consider the potential impact of changes in the daily limit prices used by the Korea Stock Exchange during the test period on our empirical findings. Detemple and Jorion (1990) study the impact of option launches on the underlying stock. In addition to the price increases and volatility decreases that occur at the time of the new option launch, the following new empirical results are obtained and interpreted: the market value around the launch date of the new option increases, and the value of the industry index excluding the option stock increases. Anderegg et al. (2022) provides a theoretical modeling and empirical study of the feedback effect of hedging on foreign exchange spot market volatility. They study aggregate option market makers and aggregate option market takers, reflecting the total open positions of all option traders in the market. Rastogi and Athaley (2019) study the problem of integrating volatility in three markets, spot, futures and options, in order to provide a reference for hedging purposes and the formulation of derivatives policy.

Research on the Impact of Volatility in Futures Markets

Volatility in futures markets is an important research topic, mainly because of the implications this volatility has for investors, the economy, and macroeconomic policy (Sayed & Auret, 2023). This effect can be either positive or negative. Volatility in the futures market may also affect futures prices and thus the real economy (Lee et al., 2022; Rastogi & Athaley, 2019). Volatility in futures markets can affect the real economy. For example, if futures prices are volatile, they may have an impact on the production and sales of related industries (Mahajan et al., 2022b; Wei et al., 2023). At the same time, the volatility of the futures market may also affect the macro economy, such as influencing monetary policy and fiscal policy. In order to study the volatility of futures market more effectively, researchers may use various quantitative models, such as GARCH model, ARCH model, etc., to quantify the volatility of the market and explore its impact on various factors. At the same time, they may also perform regression analysis using historical data to predict future market volatility. Mallikarjunappa and Afsal (2008) constructed a GARCH model to study volatility changes in the spot market before and after the listing of relevant futures and options derivatives, using the S&P CNX Nifty index as a benchmark. The study indicated that the listing of derivatives had no significant impact on the movement of spot market volatility. Using an exponential GARCH model, Zhang et al. (2023) introduce a dummy in the variance equation to capture the change in volatility after the introduction of bitcoin futures. We find that spot return volatility decreases in the short run after its introduction, but increases in the long run.

In addition, researchers may also explore the relationship between the volatility of futures markets and other economic indicators, such as economic growth, inflation, etc., to further understand the impact of the volatility of futures markets on the economy. Li et al. (2022) studied the impact of COVID-19 on the spillover effect of time-frequency volatility in the international crude oil market and the major energy futures market in China. The findings suggest that policymakers and investors should be cautious about the differential impact of the pandemic at multiple scales. Sun et al. (2023) combined the TVP-VAR method and DY spillover index to study for the first time the information spillover relationship between the major global crude oil futures markets and the crude oil spot market before and after the launch of Chinese crude oil futures. We find that Chinese COF mainly plays the role of net receiver of information in the world COF/COS market, and its influence and price discovery function in the international market need to be improved.

Despite the theoretical elucidation of the influence mechanism of option listing on the spot market within numerous scholarly articles, it is evident that the research focus primarily lies on financial and energy options, with studies on metal options being relatively scarce. Theoretically, the introduction of aluminum options would affect the volatility of aluminum futures and spot market prices. However, due to the recent listing of aluminum options in China, research findings concerning them are markedly limited. As of yet, there exists no scholarly literature investigating the potential impact of introducing aluminum options on the aluminum futures market, nor the nature of such an impact. Thus, this paper endeavors to address this corresponding research gap.

This paper systematically examines the impact of introducing aluminum options on the volatility of the aluminum futures market, addressing a gap in the study of metal options markets. Utilizing GARCH and TGARCH models, the paper not only demonstrates an increase in market volatility following the listing of aluminum options but also offers new empirical evidence by exploring the mechanisms underlying the reduction of market information asymmetry. Additionally, the paper emphasizes the significance of the asymmetric effect, thoroughly discussing its role and impact in related studies and highlighting the greater influence of negative news on market volatility compared to positive news. These findings provide valuable theoretical support and empirical insights for future research and market practice.

Mathematical Modeling

GARCH Model Construction

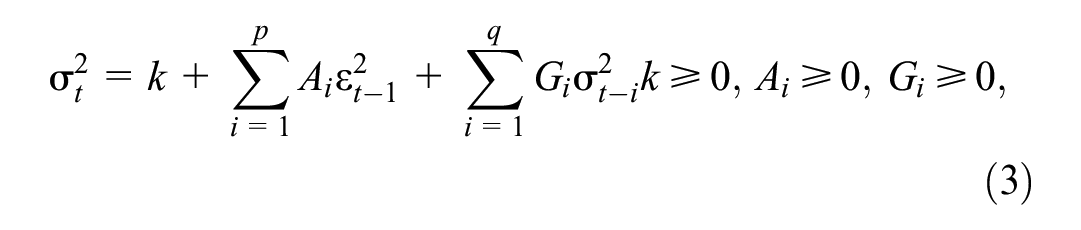

The GARCH model, widely utilized for financial time series analysis, effectively explores the volatility of time series, offering a robust basis for static short-term predictions. Financial time series frequently exhibit heteroscedasticity, a challenge which cannot be sufficiently addressed by constructing solely an ARMA (p, q) model. This issue arises due to the residual heteroscedasticity caused by extreme phenomena or evident external interventions in financial time series. To address the ARCH effect, we employ the generalized ARCH model, the GARCH model, to mitigate the impact of heteroscedasticity. Here is its representation:

where

If the residual error displays an ARCH effect post-modeling, the use of the ARCH model for further estimation necessitates the determination of additional parameters. The GARCH model effectively ameliorates this limitation. In studying the impact of aluminum option listing on the volatility of the underlying futures market, we fine-tuned the GARCH model. For this purpose, we introduced factor descriptions of dummy variables where DF = 0 signifies the period before option listing and DF = 1 indicates the period after option listing. The conditional variance of the enhanced GARCH model is represented as follows:

We used the numerical value and statistical test of

Table 1 presents the goodness of fit table for the GARCH model, comparing the AIC, SC, and HQC values calculated by each model to select the one with minimum accuracy as the final GARCH model. GARCH (1,1), demonstrated by Table 1, shows the best fitting effect, and it is prevalently applied in financial time series analysis. Therefore, we selected GARCH (1,1) to investigate the influence of aluminum options on the amplitude of futures market changes.

Comparison Table of the Goodness of fit of GARCH Models for Each Order of Aluminum Futures Yield.

The mean value equation obtained by GARCH is

and the variance equation is

TGARCH Model Construction

This generalized autoregressive conditional heteroscedasticity model of threshold is designed to capture volatility clustering and leverage effects in financial time series, distinguishing volatility based on a threshold value. Positive and negative information shocks have distinct impacts on volatility. In financial scenarios, “bad news” (negative yields) typically incites greater volatility than “good news” (positive yields).

In practical applications, good and bad news exert dissimilar effects on financial markets. The GARCH model, however, cannot portray this market asymmetry. Building on the previous GARCH (1,1) model, we constructed the TGARCH (1,1) model, simultaneously introducing the fictitious variable DF to examine the effect of aluminum options on the volatility asymmetry of the aluminum futures market. The TGARCH model, developed by incorporating asymmetric effect terms into the GARCH model, is expressed as follows:

where

where

To estimate TGARCH model parameters, we employ the Maximum Likelihood Estimation (MLE) method, a popular parameter estimation technique. The essence of MLE is to select the set of parameters that maximize the likelihood of observing the sampled data. The likelihood function for the TGARCH model for each period t is as follows:

where

The mean equation derived from the TGARCH model is given as

and the variance equation as

Time-varying Ggranger Causality Analysis and Wavelet Coherence Analysis

Time-varying Ggranger Causality Analysis

Granger causality is a method of causality analysis based on time-series forecasting (Ozcelebi & Izgi, 2023; Troster et al., 2018). While standard Granger causality analysis assumes that the causal relationship between time series remains constant throughout the sample period, time-varying Granger causality analysis allows this causal relationship to vary over time.

Suppose we have two time series

where

For time-varying Granger causality analysis, the above equation can be extended by introducing time-varying coefficients in the model

Here,

Wavelet Coherence Analysis

Wavelet coherence analysis (WCA) is used to detect the local resonance of two time series at different time scales, that is, the correlation in different time frequency ranges (Patel et al., 2023). It is an analytical tool that combines the time and frequency domains and is particularly suitable for analyzing non-stationary time series.

For two time series

where

Empirical Analysis and Conclusion

Data Source and Processing

The empirical study presented here uses data from China’s derivatives market to evaluate the influence of aluminum options on the volatility of its underlying futures market, the aluminum futures market. To ensure the consistency of our trading data, we selected the closing price of the primary continuous contract of aluminum futures on the Shanghai Futures Exchange. We excluded non-trading days to form a continuous time series that would provide a more accurate and systematic evaluation of the impact of the aluminum option listing on the entire aluminum futures market. The sample space consisted of the daily closing price of the main continuous contract of aluminum futures from December 10, 2017, to May 10, 2023, totaling 1,313 data points. The data were sourced from the Choice Financial Database, and we used Eviews10.0 software to construct the empirical model.

In order to meet the modeling conditions of GARCH and TGARCH models, the original sample data of the daily closing price of the main continuous contract of aluminum futures should be logarithmically operated. The daily rate of return of aluminum futures is obtained through the processing of formula 6, and the GARCH model is established. The serial expression of daily returns of continuous contracts is shown in formula:

where

We processed the daily yield series of the main continuous contract of aluminum futures after logarithmic transformation using Eviews 10.0 software, as depicted in Figure 1. As observed, the volatility of the daily return rate of aluminum futures exhibits a strong clustering effect.

Aluminum futures full sample daily return series.

For a clearer understanding of the data, we processed the return rate series of the complete sample (2017.12.10–2023.5.10) into a histogram, as illustrated in Figure 2. Figure 2 demonstrates that the mean daily return rate of the primary continuous contract of aluminum futures in the entire sample is 0.019099, which exceeds zero, suggesting a positive rate of return. The skewness of the series stands at −0.753219, and its kurtosis is 7.379377, significantly higher than the normal distribution kurtosis value of 3. This suggests that the daily return series of aluminum futures does not follow a standard normal distribution and exhibits a leptokurtic nature. Furthermore, Figure 2 highlights a Jarque-Bera (J-B) statistic value of 1172.507 for the daily return rate of aluminum futures, a substantially large figure with a corresponding P-value of 0. This implies that, with a 1% level of confidence, the daily return series for the complete sample of aluminum futures does not adhere to a standard normal distribution.

Full sample yield series histogram of aluminum futures.

ADF Stationarity Test

The stationarity of financial time series is a prerequisite for empirical analysis. If the data is not stationary, it requires processing until stationarity is achieved before proceeding with subsequent analyses. The Augmented Dickey-Fuller (ADF) test was employed to ascertain the sequence’s stationarity, with the results displayed in Table 2. According to Table 2’s unit root test results, the P-value of the daily yield data for aluminum futures remains 0 across confidence levels of 1%, 5%, and 10%. This indicates that the daily return rate series rejects the null hypothesis and lacks a unit root, affirming its stationarity. As such, this data is suitable for subsequent empirical research, allowing for the construction of a mean model for the yield series of the primary continuous contract of aluminum futures.

Aluminum Futures Main Continuous Contract Daily Yield Unit Root Test.

Aluminum Futures Conditional Mean Model Test

The selection of an appropriate mean model can be determined by examining the autocorrelation and partial autocorrelation plots of the aluminum futures yield series, as depicted in Figure 3.

Aluminum futures daily yield series ACF and PACF chart.

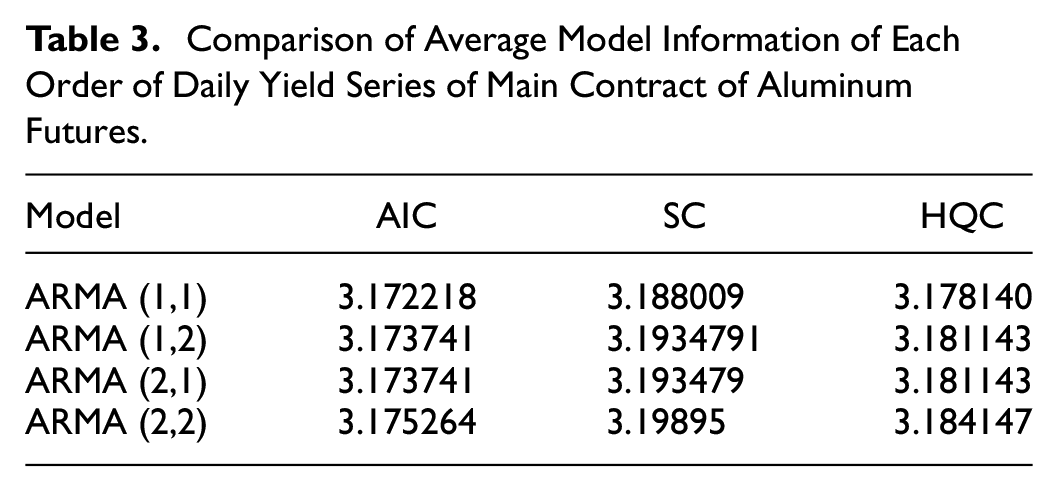

A striking similarity between the autocorrelation and partial autocorrelation plots of the daily yield series from the main contract of aluminum futures indicates an absence of conspicuous trailing and truncation phenomena, thus negating the applicability of AR or MA models. In light of the multifactorial influences on financial time series data, an ARMA model is chosen as the mean model. Typically, the highest order of each component in the ARMA model is set to 2, allowing a low-order ARMA model to effectively capture the characteristics of the time series. By comparing the fitted AIC, SC, and HQC values of models with varying orders, the optimal ARMA model is identified in accordance with the principle of minimum value. Table 3 displays AIC, SC, and HQC information corresponding to ARMA (1,1), ARMA (1,2), ARMA (2,1), and ARMA (2,2). Guided by the minimum principle of AIC, SC, and HQC, ARMA (1,1) is chosen as the mean value equation. Following model selection, the fit of the ARMA (1,1) model is assessed through a Q statistic autocorrelation test applied to the fitting residual sequence with a lag of 10 orders, as illustrated in Figure 4.

Comparison of Average Model Information of Each Order of Daily Yield Series of Main Contract of Aluminum Futures.

Q test of residual auto-correlation of daily yield series of main contract of aluminum futures.

The Q test, typically utilized to ascertain the presence of autocorrelation in the residual sequence, indicates near-zero autocorrelation and partial autocorrelation values for each lag order, based on Figure 4. With the probability values of Q statistics exceeding 0.05 at the 5% significance level, the null hypothesis is accepted, suggesting an absence of autocorrelation in the residual series and affirming the fit of the ARMA (1,1) model.

Finally, an ARCH effect test is performed. Finally, an ARCH effect test is performed in Table 4. The test’s null hypothesis posits no ARCH effect, while the alternative hypothesis posits an ARCH effect in the sequence. If the corresponding P-value exceeds the chosen confidence level, the null hypothesis is accepted, indicating no ARCH effect in the sequence. Test results are presented in Table 3, which shows the ARCH effect test performed on the fitted residual sequences. At a 5% confidence level, corresponding P-values were all less than .05, thereby rejecting the null hypothesis and confirming the presence of an ARCH effect in the sequences.

ARCH Heteroskedasticity Test Results.

Evaluating the GARCH Model Results of Aluminum Futures

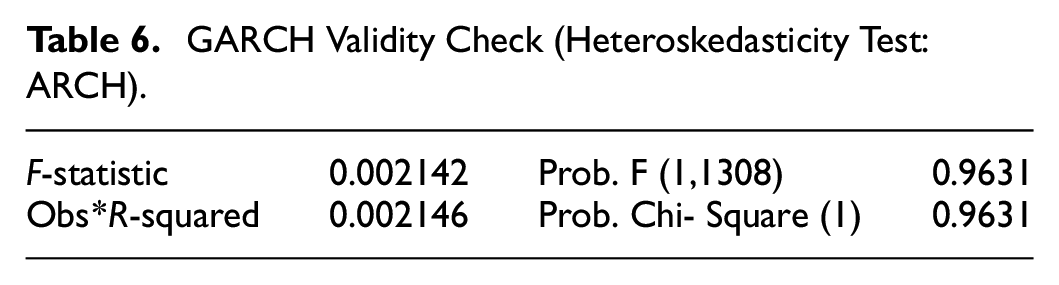

Table 5 presents the empirical outcomes of applying the GARCH (1,1) model to the daily return series of the full sample of main contracts of aluminum futures. To evaluate the model’s efficacy, the residual sequence from the GARCH (1,1) model undergoes an ARCH-LM detection test to confirm the elimination of any ARCH effect. These results are detailed in Table 6. An ARCH-LM test on the residual sequence reveals P-values of 0.9631 for both the F statistic and the LM statistic, exceeding the 5% threshold, thus negating any statistical significance. These findings demonstrate an absence of autoregressive conditional heteroskedasticity in the ARCH-LM test results of the GARCH (1,1) model’s corresponding residual sequence, verifying the effectiveness of the previously constructed GARCH (1,1) model.

GARCH Fitting Results of the Whole Sample.

Note.

GARCH Validity Check (Heteroskedasticity Test: ARCH).

The ARCH coefficient

Empirical Analysis of the TGARCH Model Results for Aluminum Futures

Table 7 displays the test results of the TGARCH model applied to the daily return series of the primary continuous contracts of aluminum futures. According to the model fitting outcomes, the coefficient

The Regression Result Statistics of the Daily Return Series TGARCH (1,1) Model of the Main Continuous Contract of Aluminum Futures.

To authenticate the model’s effectiveness, an ARCH-LM test is conducted on the residual sequence of the TGARCH (1,1) model. As Table 8 illustrates, the P-values for both the F and LM statistics are greater than 5%, suggesting a lack of statistical significance. These results confirm the absence of autoregressive conditional heteroscedasticity in the residual sequence of the TGARCH (1,1) model, thereby validating the model’s reliability.

GARCH Validity Check Heteroskedasticity Test: ARCH.

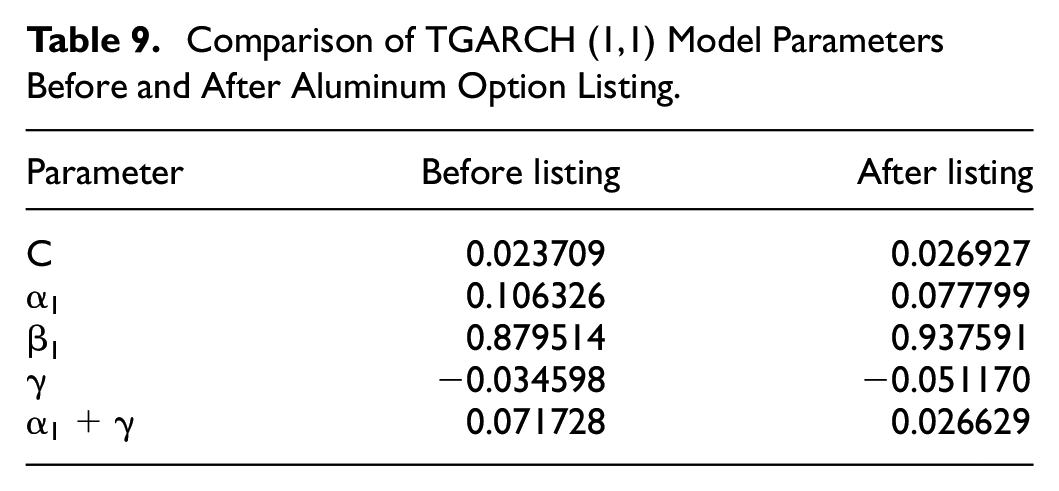

Table 9 discloses that all the calculated parameters have passed the significance test at the 5% confidence level. As

Comparison of TGARCH (1,1) Model Parameters Before and After Aluminum Option Listing.

Empirical Analysis of Time-varying Granger Causality Analysis and Wavelet Coherence Analysis

In the Granger causality test, we used lags of up to 2 periods. The Granger causality test results show the following p-values for the lags 1 and 2 can be seen in Figure 5. These p-values are above the conventional significance level (e.g., 0.05), suggesting that there is no strong evidence to reject the null hypothesis that “time” (converted to a numerical format) does not Granger-cause “Closing price.” In other words, based on this analysis, it appears that time (as numerically represented by ordinal dates) does not have a significant causal effect on the closing price of aluminum futures.

Graph of the results of the Granger causality test.

We have completed the wavelet coherence analysis and generated a graph showing the coherence between the closing price and its two lags. Figure 6 shows the magnitude of the coherence at different frequencies, with darker colors indicating higher coherence. As can be seen in Figure 6, at certain points in time and frequencies, the closing price and its lagged term show higher coherence. This means that there is a certain degree of synchronized movement between the two at these particular frequencies and time periods. The chart shows the coherence between the closing price and its two lags at different frequencies (scales) and points in time.

Wavelet coherence analysis between closing price and uts 2-period lagged series.

Research Results, Policy Implications, and Conclusions

Research Results

This study leverages the daily closing prices of the primary aluminum futures contract between December 10, 2017, and May 10, 2023, for an empirical investigation on the influence of aluminum options’ introduction on the volatility of the aluminum futures market. Initially, we employ a GARCH (1, 1) model using the daily return rate of the principal aluminum futures contract and study the effect on market volatility by analyzing the model fit results. Next, we construct a TGARCH model to examine the asymmetrical effect within the aluminum futures market. Our key findings are twofold: the listing of aluminum options has escalated the volatility of the target futures market and mitigated its asymmetry.

The GARCH model construction revealed that the dummy variable coefficient is greater than 0, implying an increased magnitude and frequency of changes in the aluminum futures market following the aluminum options listing. Moreover, the

The launch of aluminum options has lessened the aluminum futures market’s information asymmetry. The model analysis suggests a reduction in both the positive and negative news effects on the aluminum futures market’s volatility after the introduction of aluminum options. Additionally, the parameter of information shock’s asymmetrical effect in the aluminum futures market has declined following the aluminum options listing, signifying a decrease in information asymmetry in the aluminum futures market due to enhanced market transparency and openness, fostering fair information dissemination and price formation.

Policy Implications

In this subsection, we discuss the policy implications of this study and offer specific recommendations and countermeasures. First, the study’s findings indicate that the introduction of aluminum options significantly increases market volatility. Therefore, policymakers should strengthen regulation of the options market to ensure stability. Specific recommendations include implementing stricter trading rules to curb excessive speculative behavior and enhancing market transparency. Second, the reduction in information asymmetry due to the listing of aluminum options suggests that policymakers should encourage financial innovation and expand the variety of financial instruments available to improve market efficiency and information flow. Additionally, government and regulatory bodies should focus on investor education to enhance the professional knowledge and risk management capabilities of market participants, ensuring they can effectively use options for investment and hedging purposes. By adopting these policies and countermeasures, the development of the aluminum options market can be better supported, contributing to the overall health and stability of the financial market.

Options tools are increasingly utilized by investors, and risk management concepts are progressively strengthened and executed. Nevertheless, this study reveals that the introduction of aluminum options has exacerbated the aluminum futures market’s volatility instead of reducing it. Through the TGARCH model results, we observe information asymmetry in China’s aluminum futures market, causing a leverage effect. This indirectly reflects the Chinese derivative market’s immaturity and the lack of investor professionalism. This, in turn, leads to several irrational trading behaviors, thus preventing options’ full functionality. Consequently, to expedite the derivative market’s comprehensive development, to maximize the role of options in risk management, and to equip investors with more effective risk management tools.

In conclusion, futures traders can benefit from the insights of this research and related policy implications, with regards to risk management awareness, options trading proficiency, attentiveness to market fluctuations, improvement in information asymmetry, and engagement in the advancement of the options market. Considering risk management, given that the introduction of aluminum options has augmented the volatility of the aluminum futures market, industry professionals must heighten their focus on risk management. Concerning options trading expertise, options, being intricate financial derivatives, necessitate a high degree of professional skills and risk discernment for traders. Industry professionals should consistently enhance their aptitude for options trading and risk management, thoroughly comprehend the properties and trading strategies of options, to effectively navigate market risks. In monitoring market dynamics, the impact of options listing on the futures market is subject to change, influenced by various factors like market conditions and policy amendments. Hence, industry professionals must keep abreast of the latest trends in the options and futures market, and adjust their trading strategies accordingly. Regarding participation in the expansion of the options market, the growth of the aluminum options market presents new investment avenues. Industry professionals should actively involve themselves and contribute to the expansion of the options market, attaining greater investment returns through the amplification of trading volumes and diversification of trading strategies.

Experimental Conclusions

The empirical analysis using GARCH and TGARCH models in this study reveals that the introduction of aluminum options significantly increases the volatility of the aluminum futures market while reducing information asymmetry. Compared to existing studies, such as Hou et al. (2023), who identified economic development as a significant factor influencing aluminum futures price volatility; Mo et al. (2022), who demonstrated that major risk events transmit to the aluminum futures market, affecting its volatility; and Yahya et al. (2023), who explored the volatility transmission effect from the metal market to solar stocks, this study presents a unique contribution. Specifically, it provides the first systematic analysis of the specific impact of aluminum options on the aluminum futures market, uncovering a sustained increase in market volatility and a reduction in information asymmetry following the listing of options. These findings offer new empirical evidence and theoretical support for further research on the aluminum futures and derivatives market.

We thoroughly discuss the acceptance or rejection of the research hypotheses. First, Hypothesis 1 suggests that the introduction of aluminum options will significantly increase the volatility of the aluminum futures market. Empirical analysis using GARCH and TGARCH models confirms this hypothesis, demonstrating that the introduction of aluminum options does indeed increase both the magnitude and frequency of market volatility. This effect may be attributed to the influx of market participants and trading activities brought about by options trading, which enhances market liquidity and the price discovery function. Secondly, Hypothesis 2 posits that the introduction of aluminum options will reduce information asymmetry in the aluminum futures market. The study’s results support this hypothesis as well, showing that the introduction of aluminum options enhances market transparency, improves the efficiency of information transfer, and reduces information asymmetry. This is likely because the options market provides additional price information and trading opportunities, enabling market participants to more accurately assess and reflect market conditions. By discussing these two hypotheses, we gain a deeper understanding of the significant impact that aluminum options have on the futures market.

The findings of this paper share both similarities and differences with studies on other commodity and financial instrument markets. For instance, research on the gold options market indicates that while the introduction of options generally enhances market liquidity and price discovery, it has a complex impact on market volatility—often increasing it in the short term but potentially decreasing it over the long term (Bae et al., 2004). In contrast, this paper reveals that aluminum options have consistently heightened market volatility since their introduction. In the stock options market, the introduction of options typically improves price discovery efficiency for the underlying stock and reduces information asymmetry, but it can also lead to a short-term increase in volatility (Detemple & Jorion, 1990), which aligns with the findings of this study. Additionally, in energy options markets, such as crude oil options, the introduction of options has been shown to significantly influence market volatility and price discovery mechanisms (Sun et al., 2023). These comparisons underscore common effects of option introduction on market volatility and information asymmetry across various commodity and financial markets, while also highlighting the distinct characteristics of the aluminum market.

Discussions

This study examines the impact of listing aluminum options on the volatility and information asymmetry of the aluminum futures market through empirical analysis. The results indicate that the introduction of aluminum options significantly increases both the magnitude and frequency of volatility in the aluminum futures market, highlighting the direct influence of active options trading on futures market dynamics. This finding aligns with economic theory, which posits that options market activity can affect the volatility of the underlying asset market in multiple ways. However, the associated increase in market volatility underscores the need for caution when utilizing options for risk management and investment strategies. Moreover, the study finds that the introduction of aluminum options reduces market information asymmetry, enhances market transparency, and improves the efficiency of information transmission. The TGARCH model results reveal an asymmetric market response to positive and negative news, indicating a leverage effect in the market’s reaction to information shocks. The introduction of aluminum options appears to mitigate this asymmetry, contributing to greater market stability.

Futures traders should prioritize risk management strategies, especially following the listing of aluminum options, as increased market volatility presents higher trading risks. To navigate the uncertainties associated with market volatility, traders should employ more sophisticated and diversified risk management tools and strategies. Given the complexity of options trading, it is essential for traders to possess advanced professional knowledge and strong risk assessment capabilities. Market participants should continuously refine their trading skills and deepen their understanding of the nature, functions, and strategies of options to effectively manage risks in a volatile market environment. The impact of options listing on the futures market is influenced by various factors, including market conditions and policy changes. Therefore, traders must stay informed about the latest market developments and promptly adjust their trading strategies to respond to market shifts and policy adjustments. The development of the aluminum options market also presents new investment opportunities. By actively participating in and promoting the growth of this market, traders can enhance its depth and breadth, increase trading volumes, diversify strategies, and potentially achieve higher investment returns.

This study offers new empirical evidence and research perspectives on the impact of metal options, particularly aluminum options, on futures markets. The findings enhance our understanding of how options markets influence underlying asset markets and establish a strong foundation for future research. By empirically analyzing and validating the economic theory that options market activities can affect the volatility of underlying asset markets, especially within metal futures markets, the study supports the hypothesis that options trading increases market liquidity and transparency. Using GARCH and TGARCH models, the study demonstrates their applicability in analyzing volatility and information asymmetry in financial markets, providing valuable references for future research. These models can aid researchers in better understanding and predicting market volatility, thereby informing decisions made by policymakers and market participants. The findings indicate that the introduction of options markets helps mitigate information asymmetry in the underlying market, enhancing market transparency and the efficiency of information transfer. This insight offers a theoretical basis for further research on market transparency and information transfer mechanisms, contributing to the development of more effective market regulatory policies.

The data sample for this study encompasses the aluminum futures market from December 10, 2017, to May 10, 2023. This relatively short timeframe may not fully capture the long-term effects of the options market’s development. Additionally, the macroeconomic and market conditions during the sample period may be unique, potentially limiting the broader applicability of the findings. The study is confined to analyzing the aluminum futures and options markets in China, without considering similar markets in other countries or regions. Differences in institutional environments, market structures, and participant behaviors across markets may limit the global relevance of the study’s conclusions. Moreover, the study primarily focuses on the impact of options listing on futures market volatility, without accounting for other factors that could influence volatility, such as macroeconomic variables, policy changes, and global market linkages. These omissions may affect the accuracy and reliability of the study’s results to some extent.

Future research could extend the data sample over a longer time span to thoroughly assess the long-term impact of the options market’s development. This approach would allow for the capture of additional market variations and cyclical patterns, thereby enhancing the reliability and broader applicability of the study’s findings. A cross-market comparative study is also recommended to analyze the effects of options markets across different countries and regions on their respective underlying asset markets. By comparing institutional environments, market structures, and participant behaviors across various markets, researchers could gain a more comprehensive understanding of the mechanisms by which options markets influence futures markets. Additionally, future research could incorporate a broader range of influencing factors, such as macroeconomic indicators, policy changes, and market sentiment, to develop a more complex and comprehensive model. This would enable a more accurate assessment of the options market’s impact on futures market volatility and uncover additional potential mechanisms of influence. Further exploration of changes in market microstructure, including market depth, liquidity, and transaction costs, could provide deeper insights into the volatility dynamics of both futures and options markets. Detailed microdata analysis could reveal more intricate aspects of market behavior and mechanisms, offering a stronger foundation for policy formulation and market management.

Conclusions and Prospect

This research provides an in-depth empirical analysis of the influence that aluminum options exert on the volatility of the corresponding futures market. By selecting aluminum options as a focal case study, we meticulously analyzed the daily closing prices of the principal continuous contracts for aluminum futures spanning from December 10, 2017, to May 10, 2023. The analysis was conducted using the advanced statistical software Eviews 10.0 and employed the GARCH model suite, a robust toolset designed to scrutinize return series data. To specifically assess the impact of aluminum options listing on futures market volatility, we incorporated dummy variables into our models, allowing for a more precise evaluation of this relationship. The findings from our analysis indicate that the listing of aluminum options significantly increases volatility within the aluminum futures market. Concurrently, it appears to improve the asymmetrical information effect, suggesting that the introduction of options can also play a role in enhancing market transparency.

The empirical examination of how aluminum options affect the futures market is of paramount importance, particularly for those involved in the design of future options products and the formulation of regulatory frameworks. Our study’s conclusions provide valuable insights that can guide policymakers in making informed decisions to regulate and stabilize the market. Additionally, we hope that this research will serve as a foundational reference for future academic studies, offering a springboard for further exploration in this area.

Moreover, this study contributes critical insights into the broader understanding of how the options market influences the volatility of associated futures markets. Despite the valuable findings presented here, this area of research warrants further investigation. Comparative studies that examine the impacts of various types of futures options are particularly needed, as they could shed light on the unique dynamics at play across different markets. Furthermore, a deeper exploration into other influencing factors, such as macroeconomic conditions, policy shifts, and global market trends, is necessary to build a more comprehensive understanding of the subject.

As the Chinese options market continues to expand and evolve, its influence on the futures market is likely to become increasingly significant. This anticipated growth underscores the importance of vigilant monitoring by investors and regulatory bodies. Understanding the development of the options market and its implications will be crucial for managing associated risks and ensuring market stability. Therefore, we strongly encourage stakeholders to stay informed about the progress of the options market, as doing so will enable them to better navigate and respond to the complexities of an ever-changing financial landscape.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study is supported by Program for the Philosophy and Social Sciences Research of Higher Learning Institutions of Shanxi, Research on “Insurance + futures” serving Shanxi agricultural development, Grant Number: 2020W320

Ethic statement

Not applicable.

Data Availability Statement

Data will be made available on request.