Abstract

This study is anchored to assimilate the body of knowledge on herd behavior in financial markets to understand the evolution of the subject, focal concepts, and core areas researched in the past, as well as present the agenda for future research. The data involved carefully selecting 214 research articles published from 1994 to 2023 in journals indexed in the Web of Science (WoS) database using the Preferred Reporting Items for Systematic Reviews and Meta-Analyses (PRISMA) framework. The paper examines the evolution and growth of the subject. It performs thematic review of the top 100 most influential articles to identify six focal concepts and areas discussed in the past. The findings are synthesized into three primary themes to develop a comprehensive intellectual structure for the future. The results reveal that most studies examine equity market herding in developed countries. Additionally, theoretical and empirical studies are disconnected, resulting in a partial understanding of the determinants of herd behavior. Further, there is a dominance of empirical-based studies that are inadequate in explaining the complex herd behavior. This study makes significant academic contributions through thematic review by identifying the research gaps and developing a structured framework for future research agenda complemented with the proposed methodological approach that can be used as a reference for forthcoming research.

Introduction

Behavioral finance suggests that investor psychology and irrational behavior impact investment decisions. Consequently, the influence of sentiment, emotions, and behavior has come to the forefront of deciphering market movements (Bharti & Kumar, 2020; Statman, 2017) and asset valuations (Hirshleifer, 2015), especially in the aftermath of the sub-prime crisis, Eurozone crisis, and the pandemic of COVID-19 (Kizys et al., 2021). The research argues that understanding investor behavior is the route to explaining the market anomalies of asset bubbles and crashes (Broman, 2022).

Investors, being humans, are influenced by the crowd, exhibiting a mimicking behavior and resulting in coordinated correlated trades. This pattern of following the consensus unthinkingly, sometimes even overlooking private information, is called herding behavior (Zheng et al., 2021). Although studied in the context of zoology and sociology, the research on herding within finance is still unfolding and embryonic.

Herd behavior results in over-enthusiasm and market exuberance that has implications on the trends, movements, and eventually asset risk premiums (Luo & Schinckus, 2015). Extreme herd behavior creates asset bubbles that ultimately crash, making markets volatile and causing contagions into related asset classes or interconnected markets. The impact of herd behavior has also been acknowledged by governments and practitioners globally (Kizys et al., 2021). Implementations of surveillance systems, short sale bans, and strict disclosure policies to enhance transparency have been a few regulatory initiatives to mitigate the destabilizing effects of herding behavior, especially during extreme return periods and crises (OECD, 2020). A case in point is the government’s response to COVID-19, which engulfed the stock markets with anxiety and fear. The period witnessed prompt regulatory response in terms of financial stimulus packages, grants, and social schemes to mitigate the impact of herding on financial markets.

With the multiple financial market crises since the watershed event of the 2008 global financial crisis (GFC), the subject of herding has made its appearance in the context of multiple asset categories, attracting academic attention (Loang & Ahmad, 2023; Mnif et al., 2020; Philippas et al., 2013; Yang & Yang, 2014). The phenomenon has been studied explicitly in the context of equities (Wanidwaranan & Padungsaksawasdi, 2022), currencies (Sibande et al., 2023), bonds (Cai et al., 2019), commodities (A. Kumar et al., 2021), cryptocurrencies (Bouri et al., 2019), real estate investment funds (REITs’; Philippas et al., 2013), and mutual funds (Aghamolla & Hashimoto, 2020). The research has also focused on the subject through the lens of fundamental or non-fundamental factors to herd (Galariotis et al., 2015). Further, the financial literature contains multiple methodological frameworks to identify herding in financial markets, including statistical and experimental research designs.

The current study adopts the well-established systematic literature review (SLR) methodology (Tranfield et al., 2003). The SLR critically analyzes the context of past studies to identify the focal areas and recent developments on the topic for knowledge synthesis, facilitates the raising of new research questions associated with gaps, and frames the future research agenda. We supplement the SLR with thematic review of the selected studies and consolidate them into three primary themes: (a) research methodological approaches to measure herd behavior, (b) theoretical research context and disassociation with empirical-based literature, and (c) herding in portfolio asset allocation decisions. The paper identifies research problems and associated gaps for evolving the scope of the subject.

This paper is organized into five sections. The present section introduces the topic, followed by the second section, which details the theoretical background. The following section explains the SLR methodology and data, including article curation and coding. We then present an analysis and discuss the publication trends, descriptive statistics, and emerging themes highlighting the future research agenda. The last section is the conclusion with limitations.

Theoretical Background

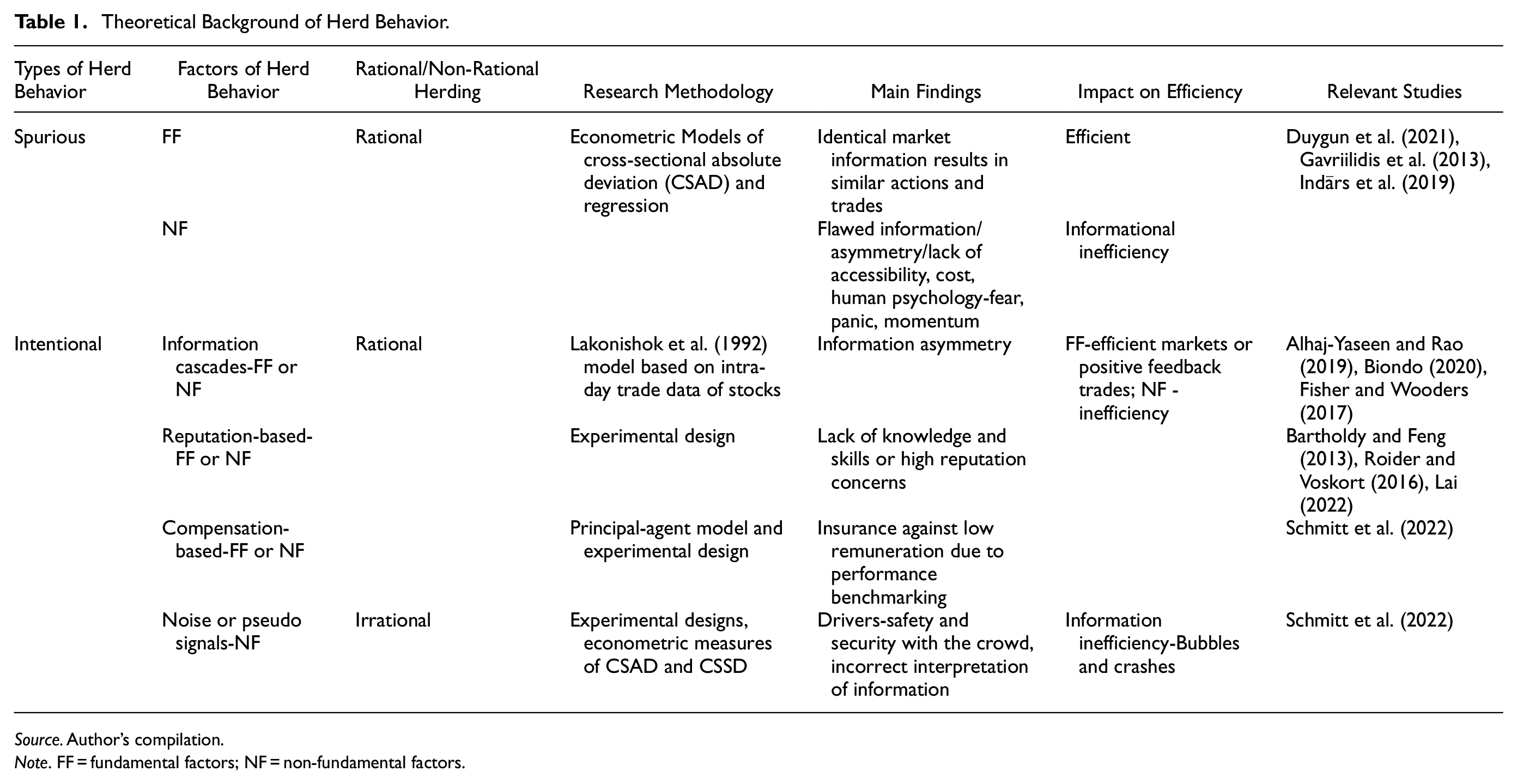

The assumptions of investor rationality and efficient markets have been criticized on account of market frictions and anomalies (Bikhchandani & Sharma, 2000). The debate on the legitimacy of standard finance theories has brought forward the discipline of behavioral finance, which is underpinned by behavioral decision-making theory, which describes the influence of beliefs and values on investment decisions (Davidson, 2010). The popular prospect theory of decision-making under uncertainty by Kahneman and Tversky (2012) highlights that investors are affected by biases and resort to heuristics that influence investment decisions. Markets suffer from “noise trading,” and asset prices diverge from fundamentals, creating opportunities for informational inefficiencies (Cipriani et al., 2022). Given a choice between private information and crowd action, investors incline toward the latter and converge to herd (Galariotis et al., 2016) classified herding as intentional, where investors willingly suppress private information and herd in the direction of the crowd with the expectation of a payoff causing informational blockage and inefficiency.

In contrast, spurious herd behavior explains that homogeneous responses in the market result from receiving similar information sets, providing standard signals and efficient outcomes (Wanidwaranan & Padungsaksawasdi, 2022). Style investing, preference for home stocks, or sector preference in investing are examples of spurious herding (Broman, 2022). Another view of herding is rational and non-rational, where rational herding results from information externalities, payoff externalities, or principal-agent models. The informational externalities explain investors gain more information from the actions of others rather than private information, resulting in informational cascades (Cipriani et al., 2022). The payoff externalities suggest that the expected gains to acquire new stock information depend on other traders’ assessments.

In contrast, principal-agent models explain unskilled portfolio managers being evaluated on a relative basis herd to safeguard reputation or maximize compensation. On the other hand, irrational herd behavior results from unquestioningly imitating the crowd due to fear, anxiety, lack of skill or knowledge to interpret information, or comfort and security with the majority (Altaf & Jan, 2023). Table 1 presents the integration of theory with empirical studies on herd behavior for better comprehension.

Theoretical Background of Herd Behavior.

Source. Author’s compilation.

Note. FF = fundamental factors; NF = non-fundamental factors.

Although the scholarly work on herd behavior is prolific, specific key research questions remain unaddressed. First, how has the intellectual structure on herd behavior evolved with respect to the key ideas? This elaboration is pertinent to understanding what is known and unknown in the literature to identify the future research scope. Previous studies on herd behavior have concentrated on developed financial markets, while research on frontier and emerging economies was inadequate. Also, the findings are largely inconsistent and mixed as a majority of the studies conclude herd behavior is preceded by periods of stress, while the other studies are indeterminate if the reverse relationship is also significant (Gavrilakis & Floros, 2023; Loang & Ahmad, 2023; Pochea et al., 2017; Vidal-Tomás & Alfarano, 2020). Second, how can the literature be expanded by evolving new research methodologies? Understanding this is necessary to explore the multifaceted herd phenomenon and connect the empirical studies and theory. The empirical studies focus on the evidence of herd behavior and intensity, and the theory seeks to address the underlying investor motivations for the herd without highlighting the relation between individual and group herding intensity (Alfarano et al., 2008; Bharti & Kumar, 2022b; Pochea et al., 2017; Yousaf & Ali, 2020). As a result, there is a loose association between empirical statistical data-driven models and theoretical frameworks leading to crippled policy response. Third, how can herd behavior be used profitably in devising investment and asset allocation strategies? The question is relevant due to the shortage of studies on the topic as the pivot of research remains concentrated on herding in equity markets (Barber et al., 2009) with inadequate exploration in other asset classes- bonds (Li & Zou, 2008), cryptocurrency (da Gama Silva et al., 2019; Haykir & Yagli, 2022; Omane-Adjepong et al., 2021) necessary to achieve the diversification benefits. Four, studies have examined herding in the context of the aggregate market, overlooking the micro level of sectoral herd behavior (Padungsaksawasdi, 2020; Yao et al., 2014). The understanding is imperative as investors and market participants seek multiple investment tools for profits, risk management, and hedging. To seek answers to the above-raised questions, we consolidate the academic work on the topical subject of herd behavior and provide an update on the most recent studies to build intellectual territory.

This paper brings together a collective structured insight into the research on herd behavior in financial markets and significantly contributes to the literature in four aspects. First, to the best of our knowledge, a comprehensive and synthesized review of the three decades of academic expertise based on herding in financial markets has not been performed in the past. Although bibliometric analysis studies are available, our study is the first SLR with a thematic review of herding. Furthermore, our period includes the publications till 2023 comprising the research during COVID-19. The findings augment the knowledge pool by synthesizing the impact of influential events and exogenous determinants on herding. Second, our selection and analysis criteria for review follow the PRISMA 2020 framework (Preferred Reporting Items for Systematic Reviews and Meta-Analyses) and overcome the researcher bias (Page et al., 2021), in contrast to the narrative literature reviews done previously. The PRISMA 2020 framework for article curation and analysis is objective and provides an unbiased understanding of the subject. Third, we perform a thematic review of the top 100 most cited articles on the topic to objectively identify the themes and sub-themes from the leading publications with the highest impact and expand the knowledge landscape by specifying the dimensions under which research on herding is concentrated. Fourth, our study objectively identifies the research gaps associated with problems. It proposes a research agenda for the future with the proposed research methodology that can serve as a reference for the future.

SLR Data Curation and Methodology

SLR Methodology

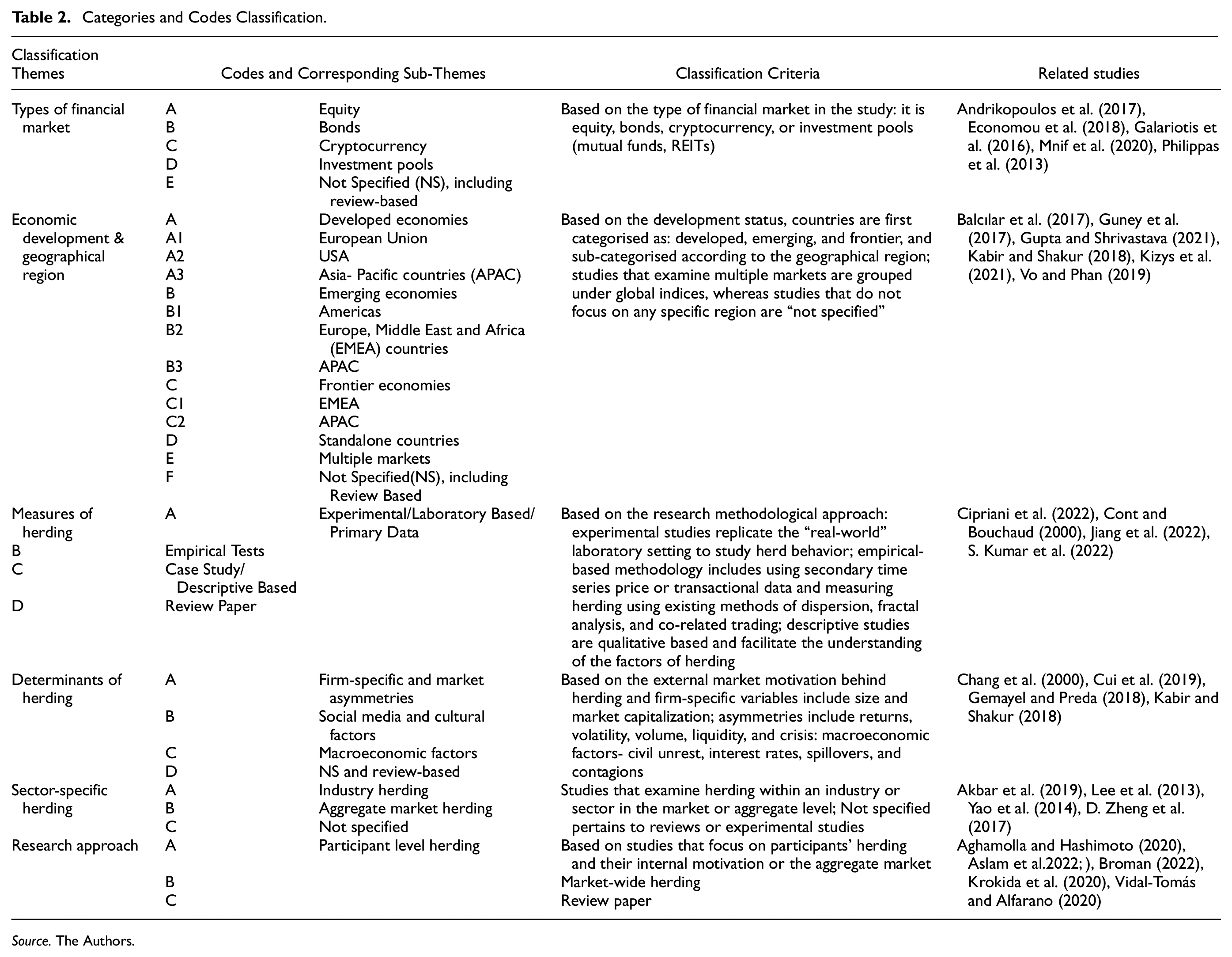

SLR is a standard method to systematically retrieve and consolidate past publications in a transparent, unbiased, and replicable method (Tranfield et al., 2003). SLR facilitates a clear and comprehensive synthesis and is well-suited to incorporate findings from multiple studies in a replicable structure (Valcanover et al., 2020). We established the database to extract the related studies and analyze the articles to identify the key concepts, code, and group them into six descriptive categories—types of the financial market, economic development and geographical region, measures of herding, determinants of herding, sector-specific herding, and research approach. Next, the thematic review of the papers is performed to develop new insights that fit into the primary aim of this study.

Articles Curation

This study uses the updated PRISMA 2020 technique (Page et al., 2021) and carries out the “identification” of the relevant articles on the database of the Web of Science (WoS). WoS includes more than 34,000 multidisciplinary journals on behavioral finance and is extensively used by the research community (Birkle et al., 2020). A single WoS database is used to maintain the quality and consistency of the articles. Further, WoS covers highly influential peer-reviewed journals manually curated and selected based on scholarly criteria, focussing on social science, arts, and humanities—the disciplines relevant to the current paper. Moreover, the database ensures that article retrieval is uniformly structured, especially required in SLR, to make the search results reproducible and reportable.

We followed a funnel approach to search the articles where the preliminary search was performed using the keywords that appeared in the papers downloaded, utilizing the snowballing method. The first set of keywords were “herding behavior,” “information cascades,” and “financial markets.” Thereafter, the BOOLEAN criteria was used to find the relevant articles (Huang et al., 2015). The search string included in the title search (TS) query as (“Herd” OR “Herd* Behaviou*” OR “Info* Cascad*” OR OR) AND (“Financial* Market*” OR “Capital* Market” OR “Investor Rational*” “Return Dispersion*” “Positive Feedback Trad*” OR “Financial Crisis”) to search for title, abstract and keywords of articles published during 1994 to 2023. The asterisk (*) ensures the inclusion of all relevant studies and prevents the removal of pertinent articles. We initially retrieved 419 articles. Next, the articles in English, in the subject areas of economics, business finance, and management, were selected, returning 239 articles. These were manually validated based on abstracts, keywords, and areas of study by a committee of academic subject experts. Only journal articles are included in this study. Excluding conference proceedings, editorials, commentary, books, or publications specific to government-owned entities (document type) returned 227 articles. This exclusion ensures that the selection is uniform and includes only quality publications (Bellucci et al., 2022). Through manual screening, duplicate articles and inaccessible papers were excluded. Efforts were made to retrieve the paid articles freely by accessing the university website and authors’ self-archived versions. We retrieved the final sample of 214 articles. Figure 1 shows the PRISMA flow chart for article search.

PRISMA 2020 flow chart for article selection.

Categorization and Coding Criteria of Articles

We adopt the method of Donthu et al. (2021) and S. Kumar et al. (2022) and select the top 100 articles from the 214 studies. The top 100 papers were categorized and coded under the six themes from 1 to 6 and their respective sub-themes (A to F; Table 2 using the MAXQDA software). Selecting the top 100 papers based on average citations per year eliminates researcher bias. It ensures that the selection is based on the relative impact on the academic community. The themes were:

Types of Financial Market

Economic Development and Geographical Region

Measures of Herding

Determinants of Herding

Sector Specific Herding

Research Approach

Categories and Codes Classification.

Source. The Authors.

The first theme (1) of the type of financial market highlights the article’s focus in the context of the kind of asset market. It is divided into five sub-themes (A to E)—equity (A), bond (B), cryptocurrency(C), investment pools(D), or review-based (E), including experimental designs. The second theme (2) relates to the economic development status of the sample market and its geographical region based on the MSCI 2023 market classification. The sub-themes are coded A to F for developed markets (A-A1-European Union, A2-US, A3-Asia-Pacific), emerging markets (B- B1- Americas, B2- Europe, Middle East and Africa, B3- Asia Pacific), frontier markets (C- C1- Europe, Middle East and Africa, C2-Asia-Pacific), standalone markets (D), multiple markets (E), and not specified (F) such as review- based articles or experimental studies. The third theme (3) refers to the measure of herding. It classifies the studies based on the research methodology adopted to identify the research objective of the study for a deeper understanding of the context of analysis and highlighting the gaps in the literature. Here, the sub-themes are coded from A to D as experimental/laboratory-based/primary data studies (A), empirical studies (B), case study/descriptive based (C), and review papers (D). The fourth theme (4) explains the external factors and determinants motivating herd behavior with A to D codes- firm-specific and market asymmetries (A), social media and cultural factors (B), macroeconomic factors (C), and review-based or not specified articles(D). The fifth theme (5) codes the studies based on their coverage- the perspective of industry herding (A), aggregate market herding (B), or not specified (C- review-based articles). Next, the sixth theme of the research approach (6) classifies the sample articles based on the data of the study and coded as the micro level of participant herding (A), aggregate market-wide herding (B), or review-based papers (C). The research approach is vital as it has implications for the research methodology of the article.

The following steps have been performed to conduct the thematic review after selecting the source database:

An investigative exploratory study was performed using the search terms and keywords identified using the snowballing method to accurately retrieve the main keywords that aligned with the research questions, followed by carefully selecting the final set of research articles.

The selected studies were analyzed based on the publication trend to understand the growing scholarly interest in the subject and justify the motivation of the current paper.

The top 100 most cited papers (average citation per year) were selected and classified, coded based on six primary themes using the MAXQDA software to understand and appreciate the dimensions and orientation of the past studies.

The content of selected articles was examined and summarized to develop a structural framework of research questions, associated gaps, the scope of future studies, and the potential research approach.

Analysis of Results and Discussion

Publication and Citation Results

The increase in the publications on herd behavior in financial markets in the past two decades, as illustrated in Figure 2, is evidence of scholarly interest. A dominant number of studies published pre-2008 have explored herding in the context of rational decision-making among market participants such as analysts, managers, and institutional investors (Ahmed et al., 1997; Nofsinger & Sias, 1999). However, 2008 was a turning point in academic literature, and there was a noticeable jump in the number of articles published. This period coincided with the GFC, and investor anxiety, fear, and negative sentiment flushed the market. Past empirical studies have analyzed herding during periods of crisis, with GFC 2008 being the most researched structural break. However, other significant market upheavals of the 21st century- the launch of cryptocurrencies, the Eurozone crisis, the oil price crash of 2014, and the COVID-19 crisis, the Russia-Ukraine war, have been inadequately researched. Popular review-based studies highlighting open and unresearched issues on the subject are Bikhchandani and Sharma (2000), Devenow and Welch (1996), Hirshleifer and Hong Teoh (2003), and Spyrou (2013). Nonetheless, the available review articles are narrative and dated. As a result, there is a need to present an objective, updated synthesis of the literature.

Year-wise publications and citations.

Descriptive Results of the Studies

We analyze the descriptive statistics in Table 3 of the top 100 papers selected based on average citations per year. The number denotes the articles under each classification theme (1 –6) and further according to the sub-theme as per the codes assigned (A to F). N/A is “not applicable” and applies to studies not examined for the specified codes.

Descriptive Statistics of the Top 100 Papers.

Source. The Author.

Note. The table presents the number of articles among the top 100 cited articles that study herding in the context of the key themes and sub-themes as per the codes in Table 2. The numbers in bold denote the total number of studies in each sub-theme.

Types of Financial Market

The results demonstrate predominant research on equity markets (84 articles; Pochea et al., 2017), while studies on other asset classes are- five on cryptocurrencies (Haykir & Yagli, 2022), three (6.6%) analyzing investment pools like mutual funds and REITs (A. Kumar et al., 2021; Philippas et al., 2013), and two on bond markets (Cai et al., 2019). This pattern clearly shows a noticeable scarcity of academic progress in the context of other types of capital markets- bonds, cryptocurrencies, and derivatives, that demand attention. Herd behavior largely depends on the kind of instrument, its issuance and availability, the associated risks, trading facilities, depth of the market, frequency of trading, and sociological factors, including the impact of social media (Cai et al., 2019; Enoksen et al., 2020). Understanding the phenomenon in other related capital markets is pertinent due to its implications on contagion and spillovers in the interconnected environment. Further, the World Economic Forum (2022) finds that new-age instruments like cryptocurrencies are no longer fringe elements necessitating the knowledge of investor behavior for managing abrupt speculative trades and volatility.

Economic Development and Geographical Region

The majority of the studies concentrate on developed markets (45 studies; Lu et al., 2017; Mnif et al., 2019), followed by emerging markets (27 studies; Gupta & Shrivastava, 2021; Yang & Yang, 2014). Only four studies examine frontier markets (Bui et al., 2018). Among the developed markets, half of the studies focus on the US, followed by European nations (17) and the APAC countries of Hong Kong, Japan, and Australia (5). Among the emerging markets, studies concentrate on the APAC region of China, Taiwan, South Korea, and Malaysia (16 articles; Chen et al., 2021), followed by the EMEA of the Gulf markets (eight; Loang & Ahmad, 2023). Most studies on frontier markets examine Vietnam and Pakistan and a panel of African nations (four articles; Guney et al., 2017) and provide indeterminate conclusions. The structure and information disclosure environment in frontier and emerging markets are different viz-a viz developed countries (Indārs et al., 2019; Schmitt et al., 2022). We argue for more research in the context of emerging and frontier markets as they present dichotomy -opportunity in terms of untapped massive capital flows and huge investor base on the one hand, and risks of opaque information and reporting environment, high cost of information acquisition, and loose regulatory policies that affect the fundamental research process and the stock price adjustments. This understanding will enrich the literature and enable suitable policy actions.

Measures of Herding

This theme examines the research method approach used in the selected studies. Measurement of herd behavior is based on the data type and analysis unit (Demirer et al., 2010). The results highlight inadequate primary data-based studies, including laboratory experiments (3% studies), case studies, and descriptive-based approaches (9%; Harras & Sornette, 2011). However, the dominant research method is empirically driven based on secondary data sources and statistical methodologies (77%; Ukpong et al., 2021; Wanidwaranan & Padungsaksawasdi, 2022). The literature uses market asymmetries to influence herd behavior and applies statistical tests and regression on the time series data (da Gama Silva et al., 2019; Loang & Ahmad, 2023). Other statistical methods are sentiment analysis, fractals, and correlated trading patterns (Balcılar et al., 2017; Mnif et al., 2020). The review-based studies are only 6% of the top 100 articles and comprise narrative reviews (Spyrou, 2013) exposed to researcher bias or bibliometric reviews (Choijil et al., 2022) that examine the number of publications without academic viewpoint and expertise. The inadequacy of primary data-based and qualitative research designs needs attention to investigate the behavioral pattern of herding involving the human aspect. For better comprehension, case studies and experimental designs are recommended.

Determinants of Herding

Research is consistent with the assumption that market asymmetries aggravate anxiety, resulting in “group-thinking” and herd (Yousaf & Ali, 2020). Most studies examine external market movements- heterogeneous returns, trading volumes, volatility, liquidity, and periods of crisis as external drivers of the herd (Arsi et al., 2022). The past literature has examined herding during the Asian financial crisis (Chiang & Zheng, 2010), the Eurozone crisis (Mobarek et al., 2014), and the subprime crisis (Andrikopoulos et al., 2017) and COVID-19 (Bharti & Kumar, 2022b; Espinosa-Méndez & Arias, 2021). Christie and Huang (1995) pioneered the idea that market stress periods correlate with herd behavior. Chang et al. (2000) concluded herding in emerging markets of Taiwan and South Korea even during normal periods. According to Pochea et al. (2017), asymmetries capture investor sentiment, enthusiasm, and fear and are predictors of herding. The second sub-theme explores herding due to the frenzy from social media platforms and culture that consolidate the crowd perception (da Gama Silva et al., 2019; Veldkamp, 2006). The reach and impression of social media opinions on the retail and uninformed investors make them converge to the vox populi (Gupta & Shrivastava, 2021). Cryptocurrency valuations and growth are a case in point (Bharti & Kumar, 2022a, 2022b; Enoksen et al., 2020). The third sub-theme identifies herding on account of fundamental and macroeconomic factors such as civil unrest (Espinosa-Méndez, 2022), spillovers, contagions (Kabir & Shakur, 2018), and macroeconomic news-oil price shocks, sanction announcements (Indārs et al., 2019). However, the literature is indeterminant because of the limitations of the econometric methods and multiple methodologies of estimating the external drivers, consequently causing a disconnect between the theory and empirical understanding. It is appropriate to explore the interdisciplinary topic of “herding” from multiple dimensions to connect the drivers of herd behavior to the magnitude of herding.

Sector Specific Herding

This category classifies the studies from the perspective of the empirical orientation and examines aggregate market herd behavior or industry-specific herding. Zheng et al. (2017) conclude investors have a proclivity toward specific sectors and industries based on industry familiarity, past performance, style or investing, and herd around “hot” sectors and away from “cold” sectors (Gavriilidis et al., 2013). As each industry has a different sensitivity to market asymmetries, the sector return and constituent stock returns converge, resulting in herding behavior. Only 12% of the studies explore sector-specific herd behavior. Cakan and Balagyozyan (2016) empirically conclude herding in the Turkish banking and financial services stocks. Zheng et al. (2017) studied a panel of nine Asian countries and inferred intense herd activity in the technology and financial stocks during bull markets or low trading volumes. Similar results are given by Lee et al. (2013) for China. However, most studies examine herd behavior for the complete market (77%). Understanding herding within sectors is pertinent because of the implications on portfolio management services. Further, as momentum and herd behavior are closely connected, winner industries outperform the loser industries, affecting market efficiency and price movements.

Research Approach

Based on the research approach used in the empirical studies, herding can be estimated using micro-level data on the participant activity (37%; Spelta et al., 2021) for specific types of market participants -analysts (Clement et al., 2011), mutual funds (Deng et al., 2018), portfolio managers (Lu et al., 2017), and institutional investors (Cai et al., 2019). This approach is based on propriety data to explore herd behavior in the market and seek internal motivations for market agents to herd -spurious or intentional and rational or non-rational choice (Dang & Lin, 2016; Indārs et al., 2019; Jiang et al., 2022). However, the inadequacy of accessing proprietary-level data due to confidentiality is a limitation. The dominant research approach (57 studies) is driven by secondary price data and statistical techniques that provide indirect evidence of herding instead of its measurement (Bharti & Kumar, 2022b; Mnif et al., 2020; Yousaf & Ali, 2020). Nonetheless, the approaches falter in addressing the fundamental question of “how much herd behavior is attributable to investor irrationality?” The inconsistency in distinguishing between spurious and intentional herd behavior suggests the need to devise appropriate methodological approaches to augment the research.

Keyword Map

The keyword map illustrated in Figure 3, which identifies frequently used keywords and establishes a network of interrelated terms, is prepared using the VOSviewer. The size of the word corresponds to the frequency of its occurrence in the text. We have limited the minimum frequency of appearance to six times to visualize the most relevant words. The most frequently used words are “herding,” “behavior,” “stock market,” “information,” “financial markets,” and “performance.” The red cluster highlights “herding” has been studied in the context of “emerging equity markets” during “crisis” using the “cross-sectional” measures based on “stock returns,” market “liquidity,” and “prices” (Christie & Huang, 1995). The blue cluster includes studies on “financial markets,” “information cascades,” “market efficiency,” “uncertainty,” and “performance” (Tiniç et al., 2020). The related literature establishes the connection between informational cascades in financial markets and the impact on efficiency through asset prices and contrarian investment styles. Publications in the green cluster are dominated by “models” of “herd behavior,” “investments,” “contagions,” “cascades,” “speculations,” and “bubbles.” These studies examine the association of herding with contagions, speculation, and bubbles that impact market dynamics and investments (Yousaf & Ali, 2020). The yellow cluster comprises publications establishing the association between “volatility,” “herd behavior,” “risk,” “momentum,” and “sentiment.” These studies develop connections of herding with sentiment and momentum strategies (Yu et al., 2022). The intellectual structure facilitates a thorough understanding of past themes and identifies new research areas. Future studies can explore new models and methodological approaches, the impact of other behavioral biases like overconfidence on herd activity, and framing profitable investment and portfolio strategies by exploiting the herd phenomenon.

Keyword map.

Thematic Review

The thematic review of the studies is performed to identify the emerging key areas. We recognize, outline, and consolidate the significant focus areas in the literature to determine the research gaps and propose new research avenues.

Research Methodological Approaches to Measure Herd Behavior

Herding is a behavioral bias and abstract in description. Consequently, its measurement in absolute terms is difficult. The SLR reveals the following research methodological approaches:

Empirical methods—most studies use quantitative or qualitative surveys or experimental research designs to identify herd behavior using primary data, including case studies, questionnaires, interviews, or secondary market or trade transactions. Herd behavior due to internal and external factors affects different categories of market participants more than others. Empirical-based studies help analyze the impact of these factors on herd behavior, albeit with mixed conclusions. One reason is the data quality, while the second is the lack of qualitative-based research designs like experiments. The most common statistical techniques include regressions, analysis of variance (ANOVA), sentiment analysis, and fractals. We suggest developing theory-based measures of herd behavior using more suitable experimental research designs where the factors or predictors of herding are visible. As experimental designs ensure higher validity, they are more appropriate (Rizvi & Arshad, 2016).

Reviews-based or conceptual methods—previous studies use narrative or bibliometric techniques to analyze the subject. Bikhchandani and Sharma (2000) examine the leading causes of herd behavior, its measurement, and its application on stock markets. The bibliometric review paper by Choijil et al. (2022) is evaluates the evolution and identify the focal areas for the future. However, SLR-based studies are far and limited. Reviewing the related research with a focus on the existing methodologies, research designs, factors, motivations, drivers of herding, and its impact is pertinent. The critical, objective, and comprehensive review of the topic will enrich the body of knowledge.

Theoretical Research Context and Disassociation with Empirical-Based Literature

The theoretical framework on herding enlists that internal factors influence herding that is either spurious or intentional or rational or non-rational (Fang et al., 2017; Indārs et al., 2019; Peter Chung & Thomas Kim, 2017). Spurious herding occurs when the agents are exposed to similar information sets and make homogeneous decisions. In contrast, intentional herd behavior is a conscious decision to follow others and overlook private information. These factors result from rational decision-making to achieve reputational gains, maximize compensation, or imitate the predecessor, making markets inefficient (Duygun et al., 2021). Based on correlated trades, the empirical literature identifies that external market factors and asymmetries trigger herding. However, the studies fall short of classifying the motivation behind convergence, resulting in the oversimplification of the analysis (Tóth et al., 2015). Empirical-based studies are insufficient to provide deeper insight into a complex phenomenon’s underpinnings. Subsequently, the theory and evidence of herding are disconnected. We suggest integrating the two strands to separate non-rational from rational herd behavior through a primary research approach, experiments, and laboratory tests to include variables/predictors of investor behavior- personality traits, gender, and sociodemographic factors. Furthermore, these can be adopted as moderators to establish the relationship between market asymmetries and herding phenomenon.

Herding in Portfolio Asset Allocation Decisions

The agency theory postulates that the principal-agent relationship drives herd behavior (Drehmann et al., 2005). Active portfolio managers are entrusted with managing client portfolios with the objective of return maximization. However, their attributes and preferences influence asset allocations, resulting in a conflict of interest and impacting portfolio performance (Krichene & El-Aroui, 2018). Stock picking favored by peers, market dynamics, fund styles, and inclination toward hot sectors are critical in shapeing the manager’s behavior and herd tendency (Lai, 2022). Broman (2022) analyzes the exchange-traded funds (ETFs) and concludes that less sophisticated institutions follow style investing and herd, making markets inefficient. Qin and Bai (2014) find that highly investible stocks show higher momentum intensity, which is not always explained by fundamental factors. As the sizeable literature discusses participant herding and its motivations, the application in portfolio management for profit-making is still unaddressed.

Furthermore, companies in the same sector are exposed to similar types of business risks. As a result, strong corporate governance and reporting structures are the differentiating factors. Examining herding in sectors by including the measure for corporate governance in stocks can shed light on the investment rationale of managers, an area yet to be researched. Moreover, studies do not examine financial market integration, which can result in cross-border herding and provide more scope for diversification. This understanding is relevant as the new-age investor rethinks the traditional investment styles amid the emergence of social media, fintech and digital platforms that shape opinions.

Future Research Avenues

The in-depth analysis of articles has revealed unaddressed research gaps, thereby raising new research questions and paving the way for future studies. First, the most prominent issue in the literature is the measurement of herd behavior. Existing methods are inadequate in directly computing the strength of herding and are insufficient in differentiating between spurious and intentional herd behavior. Additionally, studies examine individual herding using stock-level aggregate data instead of personal traits, which results in aberrant findings. Second, few studies have examined emerging and frontier markets, especially in the context of institutional herding. The research is mainly silent on herding in other asset classes- commodities, bonds, and cryptocurrencies. Third, little is known about the impact of herding on asset prices, market efficiency, and risk premiums. Moreover, it is unclear how investors and market participants can use the informational content in herding measures to predict market movements. Table 4 tabulates the future research avenues and the proposed research methodologies to achieve them.

Future Research Agenda and Proposed Methodological Approach

Source. The Authors.

Limitations and Conclusion

The literature on herd behavior witnessed an upsurge after the 2008 GFC to seek answers to market bubbles and crashes. However, studies on the subject have recently gained momentum in light of the recent global events of the COVID-19 pandemic and the geopolitical issue of the Russia-Ukraine war. This article is based on the SLR of the research published on herd behavior in financial markets during three decades from 1994 to 2023. The PRISMA framework extracted the final corpus of 214 publications from the journals indexed in the WoS database. The primary objective of this research was to assimilate the knowledge on herding in financial markets and examine the overarching themes and concepts explored in the past to develop future research agendas. We classified the studies into six primary categories: type of financial markets, nature of market and geographical region, measures of herding, determinants of herding, sector-specific herding, and research approach. Our results highlighted maximum studies on equity markets in developed countries with limited research on other asset classes, sectors, or emerging and frontier markets. Further, most studies used secondary data and empirical research designs with less research on qualitative and primary data-based research. Past studies have developed an oversimplified model by directly associating the market asymmetries or motivations behind herd behavior with the phenomenon, with no reference to the moderating role of personality or individual traits.

The thematic review of the top 100 papers selected based on average citations per year facilitated the unification of the studies into three primary themes to understand the emerging research areas—research methodological approaches to measure herd behavior, theoretical research context, and disassociation with empirical- based literature, and herding in portfolio asset allocation decisions. Overall, this study identified the pressing research problems and gaps that need to be addressed before setting the scope of future studies.

This study makes significant threefold contributions to the literature. First, this paper provides a ready reference of the most recent and expansive tri-decadal studies on the subject to identify the focus areas in the past research for a thorough understanding. Second, our thematic discussion provides a detailed analysis of the approaches and methodologies on herd behavior that will help future academicians design more appropriate methods. Third, the critical evaluation of the top articles facilitates the consolidation of the studies and develops an intellectual structure for deeper insight by outlining the core themes and sub-themes of interest that can widen the scope of studies on herd behavior.

Although this study is comprehensive, it is not free from limitations. First, sourcing articles from a single WoS database eliminates other quality and relevant publications and scholarly work from other platforms. However, using a single multidisciplinary database promises quality peer-reviewed journals consistent with scholarly contributions. Second, our criteria for keyword selection is based on subject expert validation and is open to subjectivity. Third, thematic review is subject to the limitations of the interpretative power of authors; however, this is an inherent drawback of SLRs’. We overcame this limitation through regular and frequent discussions to increase the reliability of the analysis. Therefore, this study serves as a holistic guide for future scholarly work on herd behavior.

Supplemental Material

sj-docx-1-sgo-10.1177_21582440251319995 – Supplemental material for Thematic Review and Discussion of Research on Herd Behavior in Capital Markets: Highlighting the Gaps and Proposing Future Research Avenues

Supplemental material, sj-docx-1-sgo-10.1177_21582440251319995 for Thematic Review and Discussion of Research on Herd Behavior in Capital Markets: Highlighting the Gaps and Proposing Future Research Avenues by Bharti, Nupur Soti and Ashish Kumar in SAGE Open

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The Article Processing Charge (APC) of this article is anticipated from the employer (To be disclosed later to maintain anonymity). The authors are grateful for the same.

Ethical Considerations

There are no human or animal participants in this article, and informed consent is not required.

Consent to Participate

Not applicable.

Consent for Publication

Not applicable.

Data Availability

All data analyzed during this study are included in this published article and its supplementary information file.

Supplemental Material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.