Abstract

With the development of the global economy, there is growing attention to mobile payment. However, the attention on mobile payment was mainly focused on developed context, while research in developing context is still at an early stage. In recent years, mobile payments have decisive influence on the financial transactions of consumers all over the world. This research seeks to look into the predictors affecting the adoption of mobile payments through the extended Technology Acceptance Model (TAM) which incorporates perceived quality, self-efficacy, and trust as additional predictors. Survey questionnaires were spread and 371 valid feedbacks were received from consumers in Malaysia who have experience using mobile payment. Structural equation modeling was utilized via the SmartPLS for processing data analysis. The results showed that the behavioral intention of Malaysian consumers was significantly predicted by perceived usefulness, perceived ease of use, and perceived quality, while the behavioral intention was found to positively influence the use behavior of mobile payment. In addition, trust was confirmed to significantly moderate the relationship between behavioral intention and use behavior. However, the moderating effect of self-efficacy was not ascertained. The results served as a reference for FinTech service companies to develop mobile payment platforms in the future and contribute to the technology marketing scholarship.

Introduction

Human daily life has been significantly and decisively influenced by the emergence and advancement of information technology (Nur & Panggabean, 2021). The continuous development of mobile devices, like smartphone, mobile phones, has contributed to the growth of the global mobile payment market (Wei et al., 2021; Zhong & Chen, 2023). In comparison with traditional payment methods, mobile payments have relative advantages. For instance, users who engaged in the usage of mobile payment applications are enabled to complete their payments with the advantage of wireless and communication technologies at any time and anywhere regardless of the restrictions of time and location (Zhong & Chen, 2023). In recent years, there is a growing number of consumers have demonstrated a tremendous acceptance behavior of electronic transactions (Shankar & Datta, 2018; Shao et al., 2019). According to Handarkho (2023), the likelihood that the existing method of payment to be replaced by mobile payment in near future is signified by the trend that numerous mobile application users have applied such a reliable and comfortable platform for their banking and financial purposes.

Mobile payment is the symbol of technical evolution and innovativeness, and it is referred to as financial activities through mobile devices (Al-Saedi et al., 2020; Shao et al., 2019). As highlighted by Migliore et al. (2022), mobile payment is considered as all transactions that are completed by consumers through mobile-based applications. By using mobile payment platforms, financial transactions can be facilitated easily (Al-Saedi et al., 2020). For instance, consumers are allowed to conduct various transactional activities such as distance payments, bill payments, and online transfers, to name a few (Lin et al., 2020). Thus, mobile payment provides users with a convenient and efficient method for the transaction (Lei et al., 2022).

In the context of Malaysia, as reported by Star Online in 2022, there is a growing level of mobile payment adoption among Malaysians due to the Covid-19 pandemic, the dominant payment tools among the majority of Malaysians were QR payments, Mobile wallets, and contactless cards. To encourage Malaysians to use mobile payment, the relevant policies were highlighted by the government through the launch of the 10-year financial sector blueprint 2011 to 2020 by the Bank Negara to promote mobile payment adoption (Ibrahim et al., 2019; Yong et al., 2021). Up to 2022, 55% of Malaysian consumers claimed their adoption of digital payment without using cash, which showed an increase of 13% over last year. However, Ismail (2021) mentioned that the continuity of mobile payments usage in Malaysia is still low and unsatisfying. More so, mobile-based payment methods adoption and use are rather slow in both developed and emerging countries (Talwar et al., 2020). As there were negative feelings, precautions that the users perceived toward mobile payments that have affected their behavior intention (Yong et al., 2018).

Due to that, numerous pieces of literature analyzing the predictors that determine the acceptance of technologies (R. Al-Maroof et al., 2021; Hwang et al., 2021; Kaye et al., 2021; Rabaa’i, 2023; Saprikis & Avlogiaris, 2023). The majority of the research on financial technology acceptance has been carried out in developed countries (Humbani & Wiese, 2019). However, few studies discuss the acceptance of mobile payment concentrating on the context of developing countries (Alhassan et al., 2020). Therefore, there is a demand for growing intention on the use of information technologies such as mobile payment in developing countries (Giao et al., 2020; She et al., 2022). According to Farouk et al. (2023) and Renganathan (2023), Malaysia is a developing and upper-middle-income economy. Hence, the current research was conducted to investigate the determinants affecting consumers’ intention and actual use of mobile payment in the Malaysian context.

Other than that, prior literature showed that the users’ behavioral intention was not a unique determinant that leads to users’ behavior (Mensah et al., 2020) and suggested other factors between behavioral intention and use behavior (Lai et al., 2022). Furthermore, Rehman et al. (2019) indicated that the relationship between behavioral intention and use behavior can potentially change with the intervention of external constructs, showing that there is a need to adopt a moderator between behavioral intention and use behavior. In addition, self-efficacy was studied as a predictive factor of users’ behavioral intention and use behavior towards the technology (Hijazi et al., 2023; Pan, 2020; Zhao & Zhao, 2021), whether the self-efficacy influences both behavioral intention and use behavior towards the mobile payment as moderator was still unwell known. Thus, this research attempts to include trust and self-efficacy as moderators between users’ behavioral intention and use behavior towards mobile payment.

The technology acceptance model (TAM) has been mostly used by researchers for investigating the behavioral intention of mobile payments use (Chen et al., 2019), however, the majority of past research focused on technology acceptance factors such as perceived usefulness and perceived ease of use. However, the other influential factors like quality/ reliability to use mobile payments were less explored (Kar, 2021; Tian et al., 2023). Consequently, this research carried out an extended model to incorporate perceived quality, which has been confirmed by prior studies as antecedents towards behavioral intention to use mobile payment (Tang et al., 2021).

Thus, the current study seeks to examine the predictors, namely perceived usefulness, perceived ease of use, and perceived quality on behavior intention and use behavior of mobile payment. In addition, two moderating factors, self-efficacy, and trust were incorporated to intervene the association between behavioral intention and use behavior toward using mobile payment.

The study contributed theoretically and practically. Theoretically, this study analyzed the TAM framework in mobile payment’s context. It extended the original TAM model with incorporation of the perceived quality as a predictor (Tian et al., 2023) and tested trust (She et al., 2022) and self-efficacy (Hijazi et al., 2023; Pan, 2020) as the moderating variable between intention and use behavior. From a practical perspective, it provides insights to policymakers and the Fintech industry in understanding users’ perceptions and behaviors. It will help Fintech companies to strengthen the marketing strategy for improving users’ capabilities, confidence, and access to digital financial technologies, which are crucial for Malaysians to achieve a cashless society in the year 2025 (N. H. Hashim et al., 2023).

Literature Review

Technology Acceptance Model

A variety of payment technologies were investigated by the researchers including internet banking (Raza & Hanif, 2013; Raza et al., 2015, 2020; Sharif & Raza, 2017); mobile banking (Raza et al., 2017, 2019); and mobile payment (Ali et al., 2024). In the current study, the Technology Acceptance Model (TAM), proposed by Davis (1989) for depicting the users’ behavior to adopt information technology, was applied to analyze the acceptance of mobile payment applications among Malaysian consumers. As the most well-known theoretical model (Jawad et al., 2022), TAM has been applied as a theoretical principle in different contexts, such as social media (Alismaiel et al., 2022), food delivery applications (Su et al., 2022), artificial intelligence-based technologies (Na et al., 2022). TAM explicates that perceived usefulness and perceived ease of use, as two dominant predictors, for anticipating the adoption of technology. Perceived usefulness is considered as the extent to which an individual perceives that using certain technology would affect job performance (Davis, 1989), while perceived ease-of-use is defined as the extent to which a person perceives that the utilization of a specific technology requires less effort from users (Davis, 1989). In the study, the research model applied constructs contained in the TAM model and incorporated other influential predictors that are proposed to impact users’ behavioral intention and use behavior of mobile payment.

Hypothesis Development

Perceived Usefulness and Behavioral Intention

Perceived usefulness (PU) refers “to the extent to which individuals perceive that the use of a certain technology would enhance their job performance” (Davis, 1989). PU is an influential determinant of users’ intention to accept a system (R. A. S. Al-Maroof & Al-Emran, 2018). Numerous past research revealed that there is a positive relationship between PU and the behavioral intention of consumers to adopt mobile payments platforms (Andavara et al., 2021; Al-Qudah et al., 2024; Liébana-Cabanillas et al., 2021; N. Singh et al., 2020). Generally, when consumers observe the usefulness of their transactions in mobile payment platforms, this will drive them to accept mobile payment platforms (Tsai et al., 2022). For instance, once consumers believe that the utilization of the mobile payment system can enhance their efficiency and reduce the effort in the process of their transaction, they tend to use it for payment purposes (Daragmeh et al., 2021). As mentioned by the statement above, this research postulates that:

Perceived Ease-of-Use and Behavioral Intention

Perceived ease-of-use (PEOU) is another predictor that anticipates the intention of users to use technology. Perceived ease-of-use is referred to as the extent to which an individual perceives that utilizing a technology requires less effort (Davis, 1989). Defined by J. Kim and Kim (2022), PEOU is considered as the extent of comfort perceived by users in the process of using mobile payment services. Furthermore, found by previous researchers, there is a positive association between PEOU and the behavioral intention of users to use technology such as mobile payment platforms (Hajazi et al., 2021; Sleiman et al., 2021; Tarigan et al., 2022). Based on past research, we hypothesized that:

Perceived Quality and Behavioral Intention

Solin and Curry (2023) defined perceived quality as the idiosyncratic judgment of consumers based on intrinsic and extrinsic cues towards the quality of a product. Liébana-Cabanillas et al. (2019) discussed service quality as the evaluation of perceived quality according to the differences between expectations and outcomes. As for this research, perceived quality is referred as the outcome of the experience utilizing mobile payment platforms. Basurra and Bamansoor’s (2021) study about extending TAM with external determinants including information quality to predict students’ use of mobile learning, the researchers reported a great positive effect of information quality on behavioral intention. Besides, Ryu and Ko (2020) found that information quality positively contributes to the behavioral intention of users to continually use financial technology. This has supported the notion of Tang et al. (2021) that service quality as a predictive factor has an influential impact and it affected the users’ intention to use WeChat. Based on the above discussion, the hypothesis was proposed:

Behavioral Intention and Use Behavior

Fishbein and Ajzen (1975) highlighted that behavioral intention is the extent to which the users’ willingness to use the technology. Prior empirical studies have confirmed behavioral intention as an influential predictor that directly impacts actual use. For example, Venkatesh et al. (2003) indicated that behavioral intention has a significant effect on the use of the system. Besides, Esawe (2022) found a positive impact of behavioral intention on the use behavior for utilizing mobile wallets. Patil et al. (2020) assessed the association between behavioral intention and the actual use of mobile payments and demonstrated that behavioral intention drives the actual usage of users. Nevertheless, there are several studies focused on related technologies towards the relationship between behavioral intention and actual use, less research carried out investigating such a relationship for mobile payment acceptance (Patil et al., 2020). Therefore, this research examined the mobile payment system and leads to the following hypothesis:

Moderating Effect of Self-Efficacy

As considered by Venkatesh and Bala (2008), self-efficacy refers to the level of confidence of a person performing a certain task or work using certain technology. Self-efficacy is the individuals’ belief in forming and deciding the necessary actions for accomplishing expected performance (Bandura, 1997). For Instance, Doanh and Bernat (2019) confirmed that self-efficacy leads to a higher behavioral intention. Besides, Al-Saedi et al. (2020) pointed out that self-efficacy is a pivotal influential construct in determining the users’ behavioral intention in the research. Additionally, the result of Le (2022) noted that self-efficacy is related to the behavioral intention of users to use mobile QR code payments. Moreover, in a study of Boonsiritomachai and Pitchayadejanant (2019), self-efficacy was found to positively influence the behavioral intention of mobile payment. Based on past research carried out by researchers, the hypothesis below was proposed:

Moderating Effect of Trust

Gefen (2000) defined trust as the intention of users to look forward to expected results performed by technology and their personal belief that the systems will fulfill their responsibility. Compared with traditional payment methods, trust in mobile payment systems can bolster users’ intention to use them for the transaction (Marinković et al., 2020). Zhu et al. (2017) found that trust is the most influential factor that determines the user’s behavioral intention to use mobile payment. In addition, numerous research also revealed the positive impact of trust on the behavioral intention of users to use mobile payment (Al-Saedi et al., 2020; Sharma et al., 2019; Widyanto et al 2020). Wu et al. (2021) showed that trust has a direct and significant effect on the behavioral intention of users to adopt mobile payment. Also, trust in service providers and trust in applications were proven to positively impact users’ behavioral intention to use mobile payment (Rahman et al., 2022). This research is supported by S. Singh et al. (2021) that there is a significant relationship between trust and behavioral intention among financial technology users. In another similar research on consumers’ online shopping purchasing behavior, Rehman et al. (2019) provided empirical evidence of the significant moderating effect of trust on consumers’ purchase intention and purchase behavior towards online shopping. Consequently, the discussion above leads to a research hypothesis below:

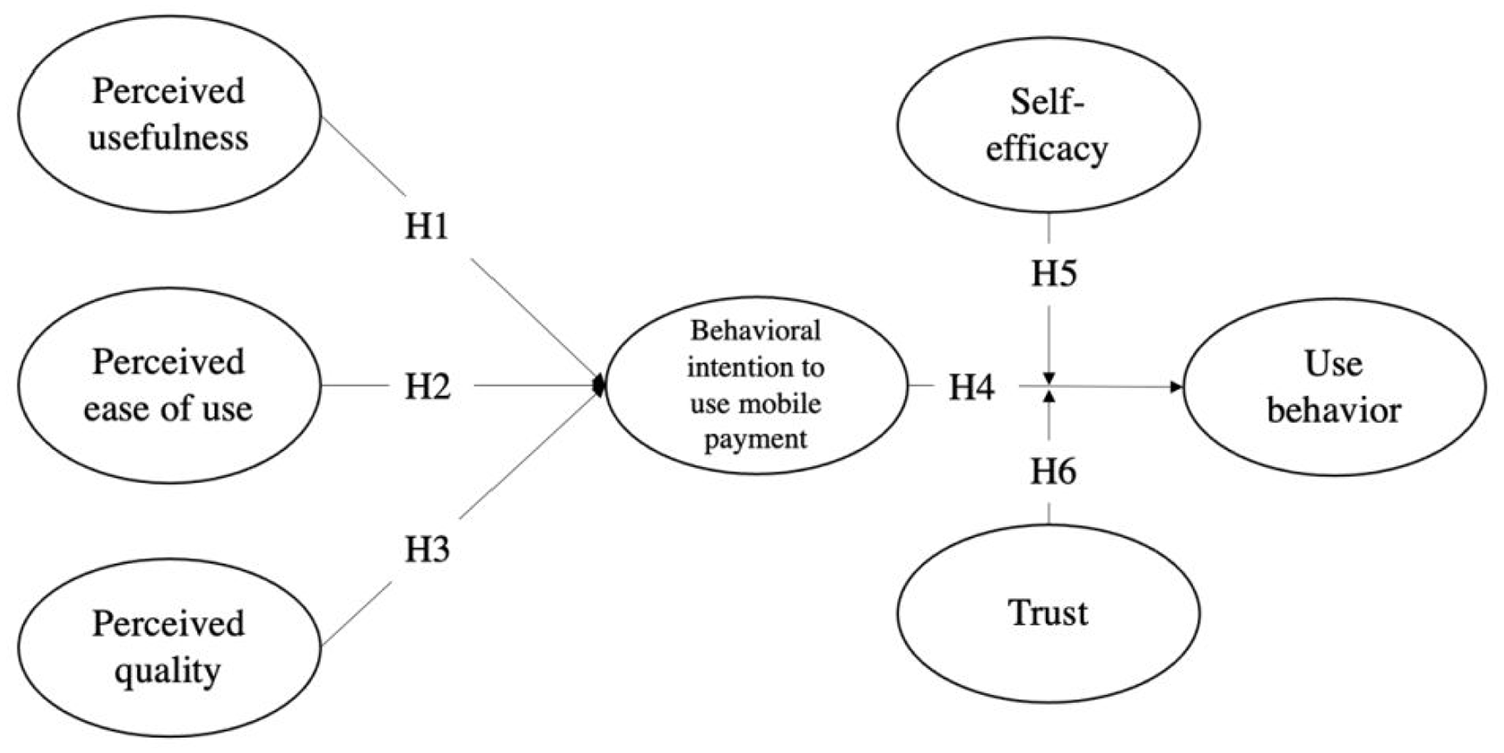

Drawing on the above-discussed evidence, a conceptual model of this study was shown in Figure 1 below, of which self-efficacy and trust were the moderators, and the rest was the antecedents influencing the consumers’ acceptance of mobile payment applications.

A proposed research model.

Methodology

Research Design

This research adopted a quantitative survey method to acquire feedback from mobile payment users. According to Apuke (2017), quantitative research is seen as a systematic investigation of a phenomenon by gathering the quantifiable data and the use of mathematical, statistical, or algorithmic techniques. As for the survey method in this research, it is an appropriate method for the current study and effectively enables the researcher to measure the attitudes and perceptions of participants (Babbie, 2020). Also, this research engaged population consists of Malaysian consumers, therefore, samples were chosen to meet certain criteria. For instance, the respondents must have experience in using mobile payment applications. Based on a survey method, the researcher distributed cross-sectional online questionnaires to qualified respondents.

Sampling Procedure

The sample for this study was the Malaysian consumers with experience in using mobile payment applications. Purposeful sampling was applied for obtaining feedback from respondents as the research focuses on mobile payment users in Malaysia. This is because respondents in the age group between 25 and 39 years old are more likely to use mobile phones for payments (Linge et al., 2023; Nandru et al., 2023; Widayani et al., 2022). As indicated by Tongco (2007), purposive sampling is a non-probability sampling technique which depends on the judgment of the researchers. Therefore, this research selects respondents who are mobile payment users because they have experience in using mobile payment.

Furthermore, to know the sample size for the current study, researchers used a-priori sample size technique (Memon et al., 2020) via the power analysis as it is a prominent analysis in most social sciences research (Hair et al., 2017), and the sample size via the G*Power 3.1.9.2 software indicated that the minimum sample size for the current study is 138 (effect size: 0.15; power: 0.95; number of predictors: 5). However, researchers managed to get 371 valid responses, thus it is sufficient for statistical analysis.

Measurements

The questionnaire for this research contains demographics and seven variables in the conceptual model. Section A: demographic information of respondents, Section B: perceived usefulness, Section C: perceived ease of use, Section D: perceived quality, Section E: behavioral intention, Section F: self-efficacy, Section G: trust, and Section H: use behavior.

Demographic questions for obtaining information about respondents consist of gender, age, race, and educational level. Besides, a screening question (Do you use mobile payment services?) was embedded in demographic questions as the respondents should have experience utilizing mobile payment services to filter the valid responses. The five-point Likert-type scale was applied for items, where 1 indicates strongly disagree, 2 indicates disagree, 3 indicates neutral, 4 indicates agree, and 5 indicates strongly agree were used. The 6 items for perceived usefulness were adapted from (Davis, 1989; de Luna et al., 2019; C. Kim et al., 2010; Wang & Dai, 2020), and perceived ease of use was measured by 5 items respectively from (Davis, 1989; Wang & Dai, 2020). As for perceived quality, it comprised 4 items adapted from Yang et al. (2021), and 4 items were adapted from C. Kim et al. (2010) for behavioral intention. Self-efficacy was measured through 3 items, modified from the study of Shankar and Datta (2018) as well as the 4 items for the trust were also adapted from Shankar and Datta (2018). Lastly, the 3 items for use behavior were adapted from Sivathanu (2018). The details of the measurement constructed can refer to Appendix 1.

Data Collection Procedures

The data were collected through an online survey. The online survey questionnaires were designed in Google form and distributed to respondents through the social media applications such as Facebook, WhatsApp, and WeChat were applied for spreading questionnaires to the mobile payment users. The researchers ensure the confidentiality and anonymity of the respondents’ information. The online survey was collected from May 2022 to June 2022. As mentioned earlier, researchers also included screening questions to ensure the respondents are actual users of mobile payment. Thus, 371 valid responses were collected after the filtering process.

Statistical Analysis and Its Significance

Data obtained from a participant were analyzed by adopting structural equation modeling (SEM) as a statistical tool with IBM SPSS 25 and SmartPLS 4, this is because PLS-SEM is regarded as a platform that is appropriate for examining complex research models with a greater number of latent variables. As for the present research, the research model consists of 29 latent variables, which can be somehow complex.

Most significantly, the current study implied testing the theoretical framework based on the perspective of prediction which justifies the use of PLS-SEM (Hair et al., 2019). This has further supported the notion of Ridgon (2016), that the prediction analysis is timely in research as it provides new observations within and outside of the sample.

Common Method Variance

To test the common method variance (CMV), a full collinearity assessment produced a variance inflation factor (VIF) value that should be less than five as suggested by Kock (2015) (see Table 1) Hence, it can be concluded that the CMV is not an issue in the current study.

Full Collinearity Assessment.

Results

The demographic characteristics of the respondents is demonstrated in Table 2. Among 371 participants, the result showed a higher proportion of female participants compared with male participants, with 143 (38.5%) male users and 228 (61.5%) female users. In terms of ethnicity distribution of respondents, more than half of them (62.5%) are Chinese while the rest of the respondents are Malay (28.6%) and Indian (8.9%). As for the age classifications of participants, respondents aged 35 to 39 years old represent 32.6% of the study. Based on the education background group, most of the participants (39.9%) have reached a diploma level, whereas a small proportion (6.2%) of respondents have a doctoral degree.

Demographic Characteristics of the Respondents (n = 371).

Measurement Model Assessment

The confirmatory factor analysis (CFA) was carried out to validate the measurement model by applying structural equation modeling (SEM). The reliability test of constructs, PU, PEOU, PQ, BI, SE, TRUST, and UB were gauged by referring to Cronbach Alpha and item loading. The Cronbach Alpha and item loading for measuring reliability should be higher than .7 to be considered acceptable (Hair et al., 2010). Table 3 presents the statistical result for the reliability test. In Table 3, the loadings and Cronbach Alpha of seven variables are all above .7. Therefore, the reliability result of this research is acceptable.

Convergent Validity.

Note. CR = composite reliability; AVE = average variance extracted.

As for the validity test, convergent validity and discriminant validity were developed for assessing the validity of constructs. In testing the convergent validity, based on Hair et al. (2013), the value of composite reliability (CR) is required to be higher than 0.7 while the value of Average Variance Extracted (AVE) should be higher than 0.5. The statistical outcome was shown in Table 3, indicating that the value of CR of all constructs is higher than the threshold of 0.7 and the AVE values for all constructs are above the threshold of 0.5. Hence, the convergent validity of constructs is ascertained.

Besides, the HTMT result was listed in Table 4. According to Kline (2015), the HTMT value between constructs should not exceed 0.85. As demonstrated in Table 4, all HTMT values are below 0.85, which showed that the discriminant validity was confirmed.

HTMT Ratio.

Structural Model

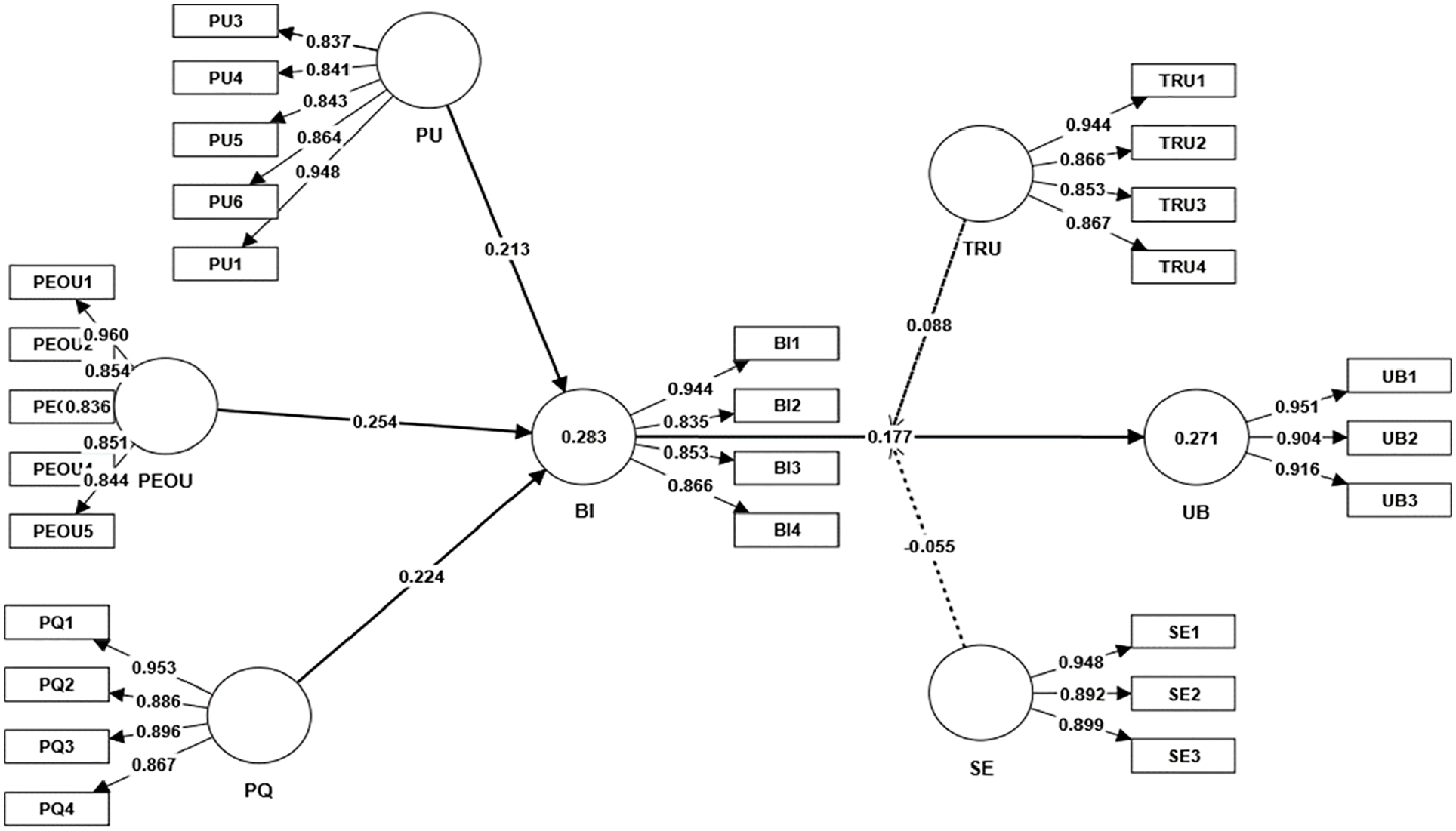

A structural equation modeling was developed to test the mobile payment use predicted by PU, PEOU, PQ, BI, SE, and TRUST. The hypothesized relationships were tested by using bootstrapping with 5,000 resamples on SmartPLS (Andrews & Buchinsky, 2002). The SEM result was shown in Table 5. The H1 hypothesized that Perceived usefulness positively impacts consumers’ behavioral intention to use mobile payments (β = .213, t = 4.103, p = .000). Thus, H1 is accepted. The H2 postulated that Perceived ease-of-use positively impacts Malaysian consumers’ behavioral intention to use mobile payments and the H2 was confirmed (β = .254, t = 5.183, p = .000). H3 proposed that perceived quality positively impacts Malaysian consumers’ behavioral intention to use mobile payments and the result of H3 was valid (β = .213, t = 4.103, p = .000). Lastly, the H4 proposed that behavioral intention positively impacts consumers’ use behavior of mobile payments. Based on the outcome of the research, this speculation was supported, with (β = .177, t = 3.632, p = .000) (Table 6).

Outcome Summary of Hypotheses Testing.

Note. 1-tailed test. PU = perceived usefulness; PEOU = perceived ease of use; PQ = perceived quality; BI = behavioral intention; UB = use behavior; ULCI = upper level confidence interval, LLCI = lower level confidence interval.

p < .01.

VIF and f2 Values.

Moderation Testing

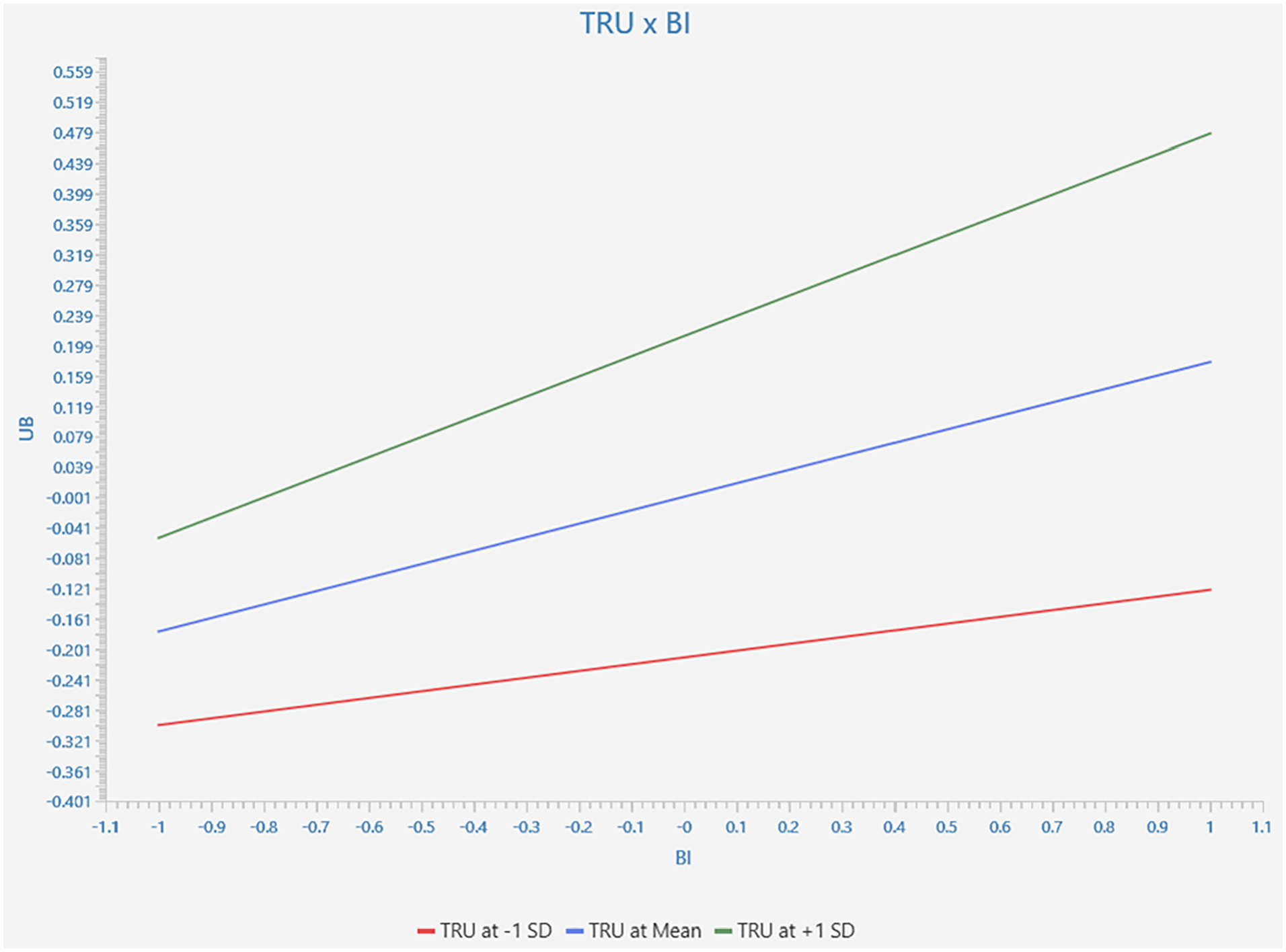

Self-efficacy and trust were introduced as moderating constructs in this research, to seek whether self-efficacy and trust moderates the association between consumers’ intention and their use behavior towards mobile payments, The outcome was listed in Table 7, indicating that trust, as the moderator, was found a significant moderating effect on behavioral intention and use behavior (β = .088; t = 1.821; p < .05; LLCI = 0.010, ULCL = 0.171). Therefore, the H6 was supported, and trust was decided as a significant moderator in the present study. However, the present study failed to reveal the significant effect of self-efficacy, with (β = −.055; t = 1.117; p ≥ .05; LLCI = −0.131, ULCL = 0.030). Based on the above-mentioned statement, H5 was rejected.

The Outcome of Moderation Testing.

Note. 1-tailed test. SE = self-efficacy; BI = behavior intention; UB = use behavior; ULCI = upper level confidence interval; LLCI = lower level confidence interval; S = supported; NS = not supported.

p < .05

Figure 2 presents the relationship between behavioral intention and consumers’ use behavior is significantly improved, when trust is high, but not for self-efficacy. Figure 2 presented the simple slope analysis, indicating that the association between behavioral intention and use behavior is moderated by trust and the relationship is strengthened when trust is high (Figure 3).

Simple slope analysis of the trust (moderator) on behavioral intention and use behavior.

Structural model.

PLS-Predict

PLS-SEM was developed as a “causal-predictive” technique to address the apparent dichotomy between explanation and prediction (Shmueli et al., 2019). To be helpful for future studies, variables can be replaced as the study continues to evolve, and the researchers hope to assess out-of-sample prediction ability by retaining the sample (Hair, 2020). To make this analysis in PLS-SEM easier, Shmueli et al. (2016) presented the PLS-predict approach, this holdout-sample-based procedure produces case-level predictions on an item or constructs level.

Since their resulting Q2 predict values are above zero (see Table 8), the Q2 predict evaluation indicates that both behavioral intention (BI) and use behavior (UB) have sufficient predictive relevance effects in the model. PLSpredict was applied to explore the model’s predictive relevance for out-of-sample prediction. Hence, the findings can be summarized as follows: (1) behavioral intention has a moderate predictive power, and (2) use behavior has a weak predictive power (see Table 8).

PLS-Predict.

Discussion

Perceived usefulness was proved as the prominent determinant of behavioral intention towards the adoption of mobile payments. This indicates that consumers intend to utilize mobile payment platforms once they believe that the services provided by mobile payment systems enable them to benefit from the services. This outcome was in line with numerous past studies (N. Singh & Sinha, 2020, Alwi, 2021; To & Trinh, 2021), especially in the mobile wallet adoption. This highlighted that the usage of mobile payments should help consumers with their transactions in financial activities, providing them a convenient and efficient experience in their process of payment. In that, the consumers’ likelihood of accepting the mobile payment applications can be strengthened.

Additionally, perceived ease-of-use was also confirmed to contribute to the intention of consumers toward mobile payments. This implies that consumers are more willing to accept and use mobile payment applications when they believe mobile payment is free of effort. Such a result was initially carried out by Davis (1989) who describes that the extent to which users perceive the use of technology requires less effort leads to the users’ adoption. This outcome supports past research (Effendy et al., 2021; Jesuthasan & Umakanth, 2021; Vărzaru et al., 2021) on the acceptance of mobile commerce and e-wallet. Of importance, the development of user-friendly mobile payment applications should be considered by their developers, ensuring the usage in conducting payments is understandable.

In terms of perceived quality, it was proven a significant factor affecting behavioral intention for adopting mobile payments. It was further reflected that consumers are willing to adopt mobile payment systems for the transaction if they believe in the quality of the system such as security. This finding corroborates with previous literature of (Tang et al., 2021; Liébana-Cabanillas et al., 2019) who discovered a significant association between perceived quality and users’ intention and continuance intention of mobile payments. To promote acceptance of consumers’ mobile payments in Malaysia, the quality of the system should be promised.

The findings pointed out that behavioral intention, as a factor, positively impacts users’ actual behavior to use mobile payments. This means consumers’ higher level of behavioral intention will promote the use behavior using mobile payments. The behavior of consumers using mobile payment is driven by their willingness. Based on the research of Sukaris et al. (2021), the behavioral intention was also confirmed as a positive predictor of the use behavior. It can be concluded that the behavioral intention to use mobile payments is considered as their interest towards mobile payment systems and predicts the use behavior of Malaysian consumers.

Trust, the final determinant moderating behavioral intention and use behavior of mobile payment was shown significantly. For instance, N. A. A. N. Hashim et al. (2020) have noted the significant effect of trust on the usage of mobile payment. While Shao et al. (2019) found trust performs a significant impact on the actual use of mobile payment in China. W. H. Wong and Mo (2019) also exhibited that the perceived trust of users towards the mobile payment as a payment platform would likely lead to consumer intention. The association between Malaysian consumers’ behavioral intention and use behavior toward using mobile payment is high when the level of trust is high.

However, the findings of the study showed that self-efficacy has no moderating effect. Thus, it contradicted the findings of Lew et al. (2020). The possible explanation of the different findings might be due to the respondents of the current study who aged 35 years old and above, comprised more than half of the respondents, thus, it is revealed that the respondents think they do not have much capacity to act necessary to use the mobile payments as they might be a late learner as according to the age factor. This is aligned with the notion of numerous past studies (Uthman Alo et al., 2021; C. Y. Wong & Mohamed 2020) that mobile payments are still emerging or at the infancy stage in the Malaysian context.

Conclusion

The purpose of this study is to investigate the antecedents affecting the consumers’ use of mobile payment. TAM was adopted and extended as the theoretical lens in the research to discuss the adoption of mobile payment. The research model consists of five exogenous variables (perceived usefulness, perceived ease-of-use, perceived quality, self-efficacy, and trust) and two endogenous variables (behavioral intention and use behavior). Based on the research model, the structural equation modeling (SEM) found that perceived usefulness, perceived ease-of-use, and perceived quality positively predict behavioral intention and use behavior towards mobile payments. Furthermore, trust strengthens the relationship between behavioral intention and use behavior.

Academic Implications

Firstly, this research provides some contributions to understanding the effect of predictors and their influence on the adoption of mobile payment in Malaysian. Theoretically, the research extends TAM by incorporating other predictors (perceived quality, self-efficacy, and trust). Through structural equation modeling, the empirical results suggested that all relationships are valid except the impact of self-efficacy, indicating that the proposed research model is sufficient in examining the consumers’ adoption intention in the context of mobile payment.

Besides, the research has tested and noted the significant moderating effect. Trust found moderates the association between behavioral intention and use behavior, this is considered to contribute to research with the new moderating relationship. Although past studies indicated the determinants and associations with the use of mobile payments, limited studies have investigated the moderating effect of trust on the relationship between behavioral intention and use behavior. Thus, the research may extend the overview toward the adoption of mobile payments generally.

Managerial/Practical Implication

Practically, the proposed factors and research model carried out are crucial in supporting the advancement of relevant mobile payment platforms. Therefore, the implications can also be referred to by service developers for advocating for consumers to accept the technology.

Firstly, the research findings would promote the understanding of mobile payment platform developers towards significant factors (perceived usefulness, perceived ease-of-use, perceived quality, trust) predicting the consumers’ intention to adopt the technology. In specific, the developers of mobile payment platforms also should develop innovative strategies, making consumers believe that the platform is useful and user-friendly.

As perceived quality is considered significant in the present study, the service developers could consider this information in focusing on the information and system quality of the platforms in the future to achieve financial innovation, thus, the consumers’ trust in mobile payment platforms can be further enhanced, and they will be more willing to adopt mobile payments platforms in comparison to traditional payment platforms. Lastly, the service providers of mobile payment also should build trust with users by improving the reliability of customer services of mobile payment platforms.

Limitations and Future Research Suggestions

The current research determines the predictors influencing the mobile payments acceptance. However, there are some existing limitations in the research. Firstly, the research focuses on the use of mobile payments, but the study neither investigates any specific type of mobile payment platform. Additional studies could select the specific type of mobile payment and examine their acceptance among consumers.

Moreover, the research was conducted among domestic respondents in Malaysia, yet the perception of consumers towards mobile payments differs from other consumers of different locations. Therefore, the respondents from different countries and their perceptions of mobile payment acceptance are still undiscovered. Future research could be conducted in different groups of nationality regarding the adoption intention and behavior.

Lastly, the study adopted a non-probability, purposive sampling, for acquiring data among Malaysian consumers as researchers were not able to identify the sampling frame (entire population of the mobile payment users in Malaysia). Future studies could select different age groups by employing probability sampling to better understand mobile payment adoption.

In addition, this research applies quantitative research design and survey methods for determining mobile payment adoption. Future researchers are recommended to use a qualitative or mixed approach, applying interviews and focus groups for a deeper understanding of this phenomenon.

Finally, this research adopted perceived quality—a quality factor that affecting users’ behavioral intention to use mobile payment. Future researchers can categorize quality factors into information quality and system quality and discuss their role in the technology adoption and contribute to the technology marketing scholarship.

Footnotes

Appendix 1

| Constructs | Code | Items |

|---|---|---|

| Perceived usefulness | PU1 | Using m-payment would enable me to pay more quickly. |

| PU2 | Using m-payment makes it easier for me to conduct transactions. | |

| PU3 | Using m-payment would be advantageous. | |

| PU4 | I would find m-payment a useful tool for paying. | |

| PU5 | I believe that m-payment system improves my decisions (providing flexibility, speed, etc.) | |

| PU6 | M-payment is usable in many stores. | |

| Perceived ease-of-use | PEOU1 | I believe that when I use m-payment, the process will be clear and understandable. |

| PEOU2 | I believe that it is easy for me to become skillful at using m-payment. | |

| PEOU3 | I believe that m-payment is easy to use. | |

| PEOU4 | It is easy to download m-payment application. | |

| PEOU5 | It is easy to receive transaction details from m-payment. | |

| Perceived quality | PQ1 | It’s easy and convenient to make payments using m-payment applications. |

| PQ2 | The m-payment application responds quickly. | |

| PQ3 | The visual design of the m-payment application looks great. | |

| PQ4 | The m-payment application can help me complete payment quickly. | |

| Behavioral intention | BI1 | I intend to pay for purchases using m-payment. |

| BI2 | Assuming that I have access to m-payment, I intend to use it. | |

| BI3 | During the next six (6) months I intend to pay for purchases using m-payment. | |

| BI4 | 1 year from now I intend to pay for purchases using m-payment. | |

| Self-efficacy | SE1 | I feel confident using m-payment to perform transactions. |

| SE2 | I feel confident using my mobile phone to access online transaction services. | |

| SE3 | I feel confident using my mobile phone for m-payment. | |

| Trust | TRU1 | I believe that legal frameworks for m-payment provision are sufficiently robust to protect consumers. |

| TRU2 | I believe that m-payment service provider has sufficient expertise and resources to provide the services. | |

| TRU3 | I believe that m-payment service provider act ethically when managing my personal data. | |

| TRU4 | I believe that m-payment service provider act honestly in dealing with consumers. | |

| Use behavior | UB1 | I pay for purchases using m-payment systems. |

| UB2 | I use m-payment systems for transferring money to my family, friends and/or other contacts. | |

| UB3 | I use m-payment systems when doing online shopping. |

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors would like to thank Multimedia University for providing financial support to publish the article.

Data Availability Statement

The datasets generated are available from the first author upon reasonable request.