Abstract

Over the past few decades, financial institutions have been considerably influenced by swift technological advancements. Therefore, it is critical to understand employees’ reactions and adoption of cutting-edge technologies in order to build up their morale, efficiency and work quality. Furthermore, there is slow technology adoption and learning in Pakistani financial institutions owing to a lack of infrastructure, lack of trust, improper knowledge, security, and quality of services offered by financial institutions. Thus, this study intentions to empirically examine the effects of personality dimensions (optimism, innovativeness, discomfort, and insecurity) of TRI (Technology Readiness Index) on the cognitive dimensions of TAM (Technology Acceptance Model) for online readiness, as well as to investigate this relationship with the moderating role of individual beliefs (subjective norms and self-efficacy) in financial institutions of Pakistan. In this study, a self-administered questionnaire was utilized to acquire 351 valid responses from the employees of financial institutions in Pakistan. The model was tested employing the collected data with the help of the Partial Least Structural Equation Modeling (PLS-SEM) technique applied through SmartPLS 3.3.2 software. The findings reveal that both technology readiness and technology acceptance are cardinal in shaping employees’ behavioral intentions toward the internet banking system. Furthermore, the results posit that individual beliefs significantly concatenate TRI and TAM into TRAM. This study suggests that integrating TRI with TAM in relationship with moderating roles of subjective norms and self-efficacy would give countenance to the employees of financial institutions in adopting avant-garde technology to boost their efficiency and work quality.

Keywords

Introduction

The technological revolution has played a pivotal role in facilitating not only the service providers but also their employees and customers (Parasuraman & Colby, 2015). Information and communications technology (ICT) has also brought advanced revolutionary changes within financial institutions to take advantage of developed as well as developing countries (Ahmad et al., 2019; Patel & Patel, 2018). The progress of the internet in the banking domain reinforces multiple e-commerce applications and delivery channels to transform into an online platform for transactions (Biranvand & Hakkak, 2014). The rapid shift from traditional to electronic banking prompts financial institutions to utilize resources in adopting the latest technologies for efficient business processes, innovative operations, and convenient customer services to create a competitive advantage (Saleem & Rashid, 2011). Inferentially, technology appears to be a novel partner of workers; therefore, enabling role and harmony with digital fluency is essential for employees to perform tasks efficiently (Larivière et al., 2017). Organizations have introduced various computer applications and information systems, thereby attaining users’ considerable attention (Marangunić & Granić, 2015). Hence, technology adoption is a major focusing area for researchers to avoid rejection of system adoption and enhance technology usage (Chuttur, 2009).

Pakistan embraced e-banking in the late 1990s. These initiatives have been taken to gain advantages from technology and attempt e-readiness within the country (Shakil Ahmad & Rashid, 2012). Technological development has enhanced service delivery channels and made the banking industry highly competitive, even in diversified environments. Kundi and Shah (2009) stated that with insufficient infrastructure and a low rate of technology adoption, the e-banking system had not been fully operationalized in Pakistan. The lack of infrastructure and accessible technology created various problems in adopting e-banking services and shook customers’ trust. The fact revealed that although a heavy investment of resources and provision of IT-related products and services, a low rate of technology adoption is still reported in Pakistan. Pakistan has an internet usage rate of 35.9%, compared with neighboring Muslim countries such as the UAE, leading with 95%, followed by an 89.6% rate in Malaysia, 84.1% in Iran, and finally, 73.7% in Indonesia (Kapios, 2022). Major causes of deficiency of e-readiness are demonstrated as insufficient infrastructure, lack of trust, improper knowledge, security, and quality of services offered by financial institutions in Pakistan (Ahmad et al., 2019; Kundi & Shah, 2009). Afshan et al. (2018) also observed that the lack of infrastructure and accessible technology had created various problems in adopting e-banking services, thereby wobbling the trust of customers. Moreover, a gap exists concerning the behavior of technology adoption in financial institutions in Pakistan (Ahmad et al., 2019). The failure to implement IT applications has been a high cost born by organizations; hence the major problem created by the underutilization of ITs is the low acceptance and adoption rate in organizations (Al-Gahtani, 2016). Therefore, Parasuraman and Colby (2015) recommended that analyzing the causes and correlations of TR is one promising area of research in this context. Specifically, an individual behavioral perspective can better explain the acceptance and adoption of new technologies. Thus, previous research has pointed out that subjective norms are the social influence in adopting a specific technology, which would act as a moderating effect on technology adoption decisions (Lee et al., 2011). Similarly, self-efficacy has the capacity to act as a moderator with reference to the adoption of new technologies (Jaradat & Faqih, 2014). All these facts have encouraged us to identify the potential influencing factors for technology adoption, particularly in the financial sector of Pakistan.

Thus, this study aims to empirically examine the effects of personality dimensions (optimism, innovativeness, discomfort, and insecurity) of TRI (Technology Readiness Index) on the cognitive dimensions of TAM (Technology Acceptance Model) for online readiness, as well as to investigate this relationship with the moderating role of individual beliefs (subjective norms and self-efficacy) in financial institutions of Pakistan. Lin et al. (2007) originally suggested the technology readiness and acceptance model (TRAM) to understand individuals’ adoption behavior of new technologies and integrate technology readiness (TR) into the technology acceptance model (TAM) (Chiu & Cho, 2020). Technology readiness and acceptance models expand the horizon of academia and permit deep insights in practice where information systems instigate an incremental role (Godoe & Johansen, 2012). Frameworks like TR and TAM are helpful for a superior understanding of technology adoption, and the investigation of relevant variables needs more comprehensive research (Chiu & Cho, 2020). Therefore, the combined concept of TR with TAM can assist in diminishing the gap between personality traits and technology acceptance of employees in organizations (Chiu & Cho, 2020). TRAM is the focus of this study, and is concerned with the personality traits of an individual to accept the technology.

However, investigating the causes and correlates of TR is one promising research direction and the inclusion of constructs in scholarly investigations, such as moderators (Parasuraman & Colby, 2015). In this frame of reference, prior research on information systems has considered that subjective norms are a social impact on the decision of innovative adoption (Lee et al., 2011). Similarly, a notable knowledge gap pertaining to self-efficacy has been observed in the context of the adoption of new technologies (Hayashi et al., 2020; Jaradat & Faqih, 2014). Furthermore, there is little empirical information to comprehend the phenomena of newly adopted technology among Pakistani financial institution staff. (Othman et al., 2019; Shakil Ahmad & Rashid, 2012; Sharif Abbasi et al., 2011). Thus, there is a lack of clear evidence in the available literature about the relationship between workers’ readiness and acceptance of new technologies under the effect of subjective norms and self-efficacy in Pakistan’s financial industry.

Against this backdrop, the current study has been designed to empirically examine the role of subjective norms and self-efficacy on the relationship between TRIs personality trait dimensions and the cognitive dimensions of TAM. Thus, the study’s overarching goal is to investigate the convergence or divergence of TAM and its application across diverse situations in order to propose an object-oriented framework that would confirm the application of technology acceptance behavior of employees in Pakistan. This work adds to the body of knowledge about TRAM with respect to financial institutions with moderating effects of subjective norms and self-efficacy. It is expected that managers and employees would take it positively and adopt new technology, provided it is beneficial because technology readiness and acceptance are important in increasing employee’s behavioral intention toward online systems. Moreover, persons can be hired with high self-efficacy and receptibility to subjective norms.

Literature Review and Hypotheses Development

Technology Acceptance Model (TAM)

The use of technology is critical to the performance of financial organizations such as banks since new technology has shown to be beneficial in a variety of ways. The use of cutting-edge technology in financing procedures enhances efficiency, saves costs, improves accuracy, improves customer service, allows for simple communication, and fosters strong collaboration with stakeholders (Rawwash et al., 2020). The desire of bank workers and consumers to utilize new technology is dependent on electronic banking; however, this intention is influenced by technology users’ perceptions and features. Our research looks at how perceived usefulness, ease of use, and behavioral control, affect bank employees’ intention to use technology. Many authors have already provided opposing viewpoints on the relationship between perceived usefulness, ease of use, and banking personnel’s intention to accept technology. The paper offers its thoughts in light of these arguments.

Originating from the Theory of Reasoned Action (TRA) (Azjen & Fishbein, 1980), the Technology Acceptance Model (TAM) was introduced by Davis (1989). TAM assesses the acceptance of a newly introduced technology, and is also considered the persuasive, essential, parsimonious and widely cited model (Sunny et al., 2019; Veiga et al., 2001). His explorative studies resulted in the identification of two beliefs: the perceptions of usefulness (PU) and perceived ease of use (PEOU). These two constructs are influential on the user’s behavior of acceptance or rejection of technologies. Perceived usefulness (PU) is the extent to which people think utilizing a certain technology will help them perform their jobs better, whereas perceived ease of use (PEOU) is the extent to which a particular technology is simple to use (Davis, 1989). Numerous studies have confirmed that simplicity, understandability and broad applicability are the major strengths of TAM (e.g., Nyoro et al., 2015). Therefore, it is the most prevailing concept that has the potential to advocate human behavior to accept or reject information systems (Burton-Jones & Hubona, 2006; Sternad & Bobek, 2013).

Several studies experimented with TAM, and supported its application, validation, and replication (Ahmed et al., 2018). On the other hand, Chuttur (2009) argued that despite too many citations of TAM, mixed opinions had been found pertaining to the practical effects and theoretical assumptions of TAM. The findings of Chuttur (2009), pointing out some deficiencies in TAM, have suggested more adequate and rigorous research in different contexts. Accordingly, TAM has been modified and extended in various studies for the sake of improvement. TAM is considered a more reliable and economic model to predict the factors influencing technology acceptance. That is why it has been extensively used for investigating the dominant factors representing technology acceptance behavior, eventually leading to technology use (Abdullah et al., 2016; Sternad & Bobek, 2013). The continuous progress of the technological field and rapid growth and multiplicity of users encourage recent streams of research to elevate the understanding and upgrade the potential of TAM (Marangunić & Granić, 2015). In short, the reason for selecting TAM as a major component of this research is because of its application, replication, validation, and empirical reinforcement in various domains (Alalwan et al., 2016; Lee, 2010; Schaupp et al., 2010).

Technology Readiness (TR)

In financial institutions, the application of technology is fully appreciated by the management, but there is a deficiency in supporting technology infrastructure (technology readiness) (Kamaludin & Purba, 2015). Technology readiness, comprising negative and positive beliefs toward technology, originated from the concept of personal innovativeness of Parasuraman. Parasuraman (2000) proposed that optimism, innovativeness, discomfort, and insecurity were the four facets of individuals’ personalities to evaluate the propensity regarding new technologies. Although, these beliefs depict different personality directions, in combination, they measure the overall tendency to embrace modern technologies. Colby and Parasuraman (2001) implemented these indicators in the consumer market to evaluate target group readiness for new technology. They discerned the application through the concept of Techno-Ready Marketing (TRM).

The application of TRM classifies consumers based on their inclination toward technology in the field of marketing. These four independent personality indicators were elaborated as positive and negative aspects of personality to utilize technologies to complete goals in professional and personal lives (Colby & Parasuraman, 2001). According to Lin et al. (2016), optimism and innovativeness represent individuals’ motivation, while discomfort and insecurity denote inhibition. So, the psychological state of these conflicting factors creates a specific attitude toward adopting technology. According to Parasuraman (2000), a high score of a person on motivators leads to increased readiness, whereas a high score on inhibitors contributes to low technology readiness. Therefore, optimism and innovativeness are perceived as the drivers of “use of technology” in a beneficial manner. Consequently, result-oriented and productive individuals are more prone to readiness. In contrast, discomfort and insecurity are referred to as inhibitors of “use of technology.” People high on these two measures are perceived as pathetic and overwhelmed by technology. These four dimensions of personality traits transpire differently due to individuals’ diverse thoughts and feelings relating to technology, and sometimes these traits contradict and modulate each other (Parasuraman & Colby, 2015).

Combined Concept of TR and TAM

In this subsection, it has been explained how constructs of TRI have been incorporated into the technology acceptance model at an individual level. The technology readiness index is a comparatively modern measurement procedure to be tied with the TAM model for technology adoption. Since the year 2000, researchers have taken into account these two research paradigms to determine the effects on technology adoption and acceptance (Ahmed et al., 2018; Erdoğmuş & Esen, 2011; Godoe & Johansen, 2012; Hung & Cheng, 2013; Jin, 2013; Kuo et al., 2013; Lin & Chang, 2011; Lin et al., 2007; Stock & Gross, 2016; Walczuch et al., 2007). The combination of TRI has also been studied with the Theory of Planned Behavior (TPB) (predecessor of TAM), and found a strong influence of TPB’s constructs pertaining to technology adoption (e.g., Chen & Li, 2010). Other studies merged determinants of TRI and TAM to explore the role of educational data mining (EDM) utilization among university undergraduate students (e.g., Wook et al., 2017). Hence, numerous types of research have been carried out to study a unified model of the two paradigms (TRI and TAM) to investigate the link between the cognitive components of technology acceptance and the personality trait dimension of technology readiness (Chen & Lin, 2018; Godoe & Johansen, 2012; Lin et al., 2007; Martens et al., 2017; Panday, 2018; Panday & Rachmat, 2019; Shin & Lee, 2014).

Taking into account a review of the literature on the combination of technology readiness and acceptance, the following hypotheses have been proposed:

H1a: There is a positive relationship between optimism and perceived usefulness.

H1b: There is a positive relationship between optimism and perceived ease of use.

H2a: There is a positive relationship between innovativeness and perceived usefulness.

H2b: There is a positive relationship between innovativeness and perceived ease of use.

H3a: There is a negative relationship between discomfort and perceived usefulness.

H3b: There is a negative relationship between discomfort and perceived ease of use.

H4a: There is a negative relationship between insecurity and perceived usefulness.

H4b: There is a negative relationship between insecurity and perceived ease of use.

Subjective Norms and Technology Acceptance

Subjective norms were defined by Ajzen (1991) as a perception of social influences or pressures to indulge in a desirable behavior. According to Sun and Zhang (2006), compliance, internalization and identification contribute as the three mechanisms to exert influence on the direct relationship between perceived usefulness (PU) and perceived ease of use (PEOU). Among these, internalization and identification modify an individual’s beliefs, such as PU and PEOU. Subjective norms (SN) explain and predict the behavioral intention and actual actions of people (Chi et al., 2012). Schepers and Wetzels (2007) stated that the usage, extension and replication of TAM were proposed by many researchers, but some aspects remain unclear, for example, the inconclusive and mixed role of subjective norms. Similarly, their finding indicates that subjective norms have a larger and significant moderating influence on PU, PEOU and behavioral intention. Likewise, Svendsen et al. (2013) investigated the relationship between personality dimensions and subjective norms along with TAM constructs, and found that the constructs SN, PU, and PEOU played a significant role in technology acceptance.

A number of studies have revealed the significance of subjective norms or group pressure in users’ technology acceptance, especially in the deployment of moderating effect on the opinion of new technology adoption in obligatory positions (Lee et al., 2011; Svendsen et al., 2013). The subjective norms were the commonly used variable as an external factor of TAM and were significantly influenced by its determinants PU and PEOU (Swidi et al., 2014). Conclusively, subjective norms have a strong moderating effect on attitude and behavioral control (Abdullah et al., 2016; Mahmood & Sahar, 2017.

Extant studies in the literature provided insufficient explanations pertaining to technology readiness and technology acceptance in the context of employees of the financial sector. The existing literature on technology acceptance is extensively reviewed and analyzed, but the influence of subjective norms and self-efficacy have not been studied in this framework. Therefore, we put forward the following hypotheses:

H5: Subjective Norms moderate the effect of optimism on perceived usefulness.

H6: Subjective Norms moderate the effect of innovativeness on perceived usefulness.

H7: Subjective Norms moderate the effect of discomfort on perceived usefulness.

H8: Subjective Norms moderate the effect of insecurity on perceived usefulness.

Self-Efficacy and Technology Acceptance

Bandura (1982) articulated that self-efficacy manifests judgment of persons’ own capability to accomplish a specific task. There are two sources of self-efficacy: experience and someone’s own performance. Moreover, persons with low self-efficacy are considered pessimistic with little self-esteem to attain goals (Hayashi et al., 2020). According to earlier research, self-efficacy is a critical factor in the acceptance and usefulness of new technology and has a positive association with many of the major factors that make up the technology acceptance model (Al-Gahtani, 2016; Park et al., 2012).

Park et al. (2012) investigated the effect of different external variables on behavioral intention in the context of mobile learning. They discovered that employing m-learning, subjective norms and self-efficacy had both direct and indirect impacts on behavioral intention. Later, Park et al. (2014) further argued that high and low levels of self-efficacy in one application might be different from the other because of the specific context. Moreover, they derived many constructs in the domain of self-efficacy, like the internet, computer, and mobile-related self-efficacies. Park et al. (2014) also emphasized to search for additional actors like self-efficacy and anxiety to investigate their impact on the usage of technology among employees in business organizations. Similarly, Jaradat and Faqih (2014) expressed that self-efficacy posits a favorable influence on the intention of consumers’ adoption of m-payment because a strong sense of self-efficacy enhances adoption, while low levels control the process of consumers’ m-payment adoption. They came to the conclusion that PU is positively and more strongly influenced by self-efficacy, and this results in real technology usage.

To put forth and investigate a conceptual model that bridges the gap by empirically investigating some crucial elements like Subjective norm and Self-efficacy that affect the relationship between the cognitive dimensions of TAM, specifically Perceived usefulness, and the personality trait dimensions of TRI.

Although, the moderating effect of self-efficacy has been reported in various studies in different domains, still, there is a great need to investigate the role of self-efficacy in different technological frameworks (Hayashi et al., 2020; Simosi, 2012). In view of these arguments, we propose,

H9: Self-efficacy moderates the effect of optimism on perceived usefulness.

H10: Self-efficacy moderates the effect of innovativeness on perceived usefulness.

H11: Self-efficacy moderates the effect of discomfort on perceived usefulness.

H12: Self-efficacy moderates the effect of insecurity on perceived usefulness.

Likewise, Ahmad et al. (2019) suggested that perceived usefulness and intention to adopt the innovative technology are both positively correlated with perceived usefulness. They further emphasized that perceived ease of use is a determining factor in the adoption and critical assessments. Past studies also propose that perceived usefulness and ease of use are the important constituents of attitude in the technology acceptance model (Sharif Abbasi et al., 2011; Sternad & Bobek, 2013). In the same vein, Abdullah et al. (2016), and Biranvand and Hakkak (2014) empirically affect not only the intention but also the attitude of using the technology. Thus, based on the literature, we put forward the following hypotheses:

H13a: Perceived Ease of Use is positively related to Perceived Usefulness.

H13b: Perceived Ease of Use is positively related to Behavioral Intention to Use.

H14: Perceived Usefulness is positively related to Behavioral Intention to Use.

Parasuraman and Colby (2015) argued that examining the sources and correlates of TR and including construct in academic inquiries, such as as a moderator, are two potentially rewarding study avenues. Prior research on IS has considered that subjective norm is the social influence related to adopting a particular technology. It would have a moderating impact on the decision of innovative adoption (Lee et al., 2011). A notable knowledge gap was observed in the current literature pertaining to self-efficacy because of the limited moderating role in the adoption of new technologies (Jaradat & Faqih, 2014). Hence, there is no direct evidence in the existing literature on the relationship between employees’ readiness toward new technology under the influence of subjective norms and self-efficacy within the banking domain in Pakistan. Thus, a study is needed to investigate the relationship between employees’ technology readiness and technology acceptance in the financial industry.

Based upon the preceding hypotheses, the four dimensions of TRIs (optimism, innovativeness, discomfort and insecurity) have been used as predictors of the general belief of employees pertaining to the perceived usefulness and perceived ease of use. It further incorporates prominent components that potentially influence the adoption of advanced technologies, the first is subjective norms (perceived social influences), and the second is self-efficacy (judgment of own capability to accomplish tasks), as shown in Figure 1.

Theoretical model with hypothesized paths.

Methodology

Sample and Procedure

Based on quantitative analysis, the current research design is causal by nature. The financial sector is highly identical due to strict standard operating procedures. Therefore, there is a small room, such as the adoption of the latest technology, where each corporation can individualize its performance. Thus, it is argued that the present study would be better suited to this sector. Hence, the population of study in this investigation comprises the employees of five Pakistani financial institutions, including Jubilee Life Insurance company limited, AKD Securities Limited, National Bank of Pakistan (NBP), and Muslim Commercial Bank (MCB), and Habib Bank Limited (HBL) of Pakistan. As of March 31, 2021, Jubilee Life Insurance company has percentage assets of 93%, AKD securities limited has percentage assets of 56%, NBP has percentage assets of 93%, MCB bank has percentage assets of 92%, Habib Bank has percentage assets of 93%. Since the chosen organizations are representative of the financial sector of Pakistan due to diversity in sub-sectors, the limited organizational variations due to their cultures, conditions and ecosystems would reflect the behavior of the overall population of the selected sector, hence increasing the generalizability of the results (David, 2013).

Past studies suggest the appropriateness of data collected by means of survey questionnaires about the espousal of technology (e.g., Al-Gahtani, 2016; Godoe & Johansen, 2012; Walczuch et al., 2007; Wook et al., 2017). Therefore, the data were collected with the help of convenient sampling through a questionnaire from the employees of the forenamed financial institutions located in Lahore, Karachi, and Islamabad. Due to COVID-19, the authors sought formal permission and appointment from the corresponding officials before collecting the data following the pandemic SoPs. The data were collected from December 2020 to February 2021. The offline data collection method was chosen to increase the response rate. The ethical protocols of the Helsinki Declaration were followed. Informed consent was obtained from respondents, allowing them to quit the response in case they felt uneasy about providing the information.

The responses to the components were measured using a seven-point Likert scale, ranging from 1 (strongly disagree) to 7 (strongly agree), in line with other researchers’ work on technology (e.g., Al-Gahtani, 2016; Godoe & Johansen, 2012; Kuo et al., 2013). The employees were given a total of 700 self-administered questionnaires. After cleaning data, finally, usable questionnaires received 351, representing an effective response of 50.14%, which is adequate (Babbie, 2013).

Profile of the Respondents.

A small population variance was found among the respondents because different financial companies like AKD Securities Limited, HBL, MCB, NBP, and Jubilee Life were different; more specifically, NBP belongs to the public sector and four other insurance companies are from the private sector. The respondents were 16% and 84% from public and private institutions, respectively. In detail, 12.3% of employees were from AKD Securities Limited, 21.9% from HBL, 24.2% from MCB, 16% from NBP, and 25.6% from Jubilee Life. The majority of the participants (76.1%) were male, and the age profile of the participants working in financial institutions showed that a large number of participants were between 25 and 34 years—46.2%, and 35 and 44 years—25.9% years. According to marital status, 63.5% were married and the remaining 36.5% of the respondents were single. With reference to education level, 3.7% of respondents had MPhil, 44.7% Master’s, 42.5% Bachelor’s degrees, whereas 9.1% had less than graduation education. This distribution of respondents illustrates that the majority of survey participants were young graduates with master’s degrees employed in the private sector of financial institutions.

Measures

The instrument was extracted from past studies, and reviewed by the experts for local context, as displayed in the appendix. The indicators were operationalized using different items from past studies, and references to construct operationalization have been provided (see Appendix). The questionnaire used in the present research comprises two sections, one has six questions concerning the demographic profile of respondents and the second has 40 questions to get responses to all the constructs. The indicators of technology readiness adopted from Parasuraman and Colby (2015) had 16 items with a reliability of 0.87. Similarly, 15 items scale for the technology acceptance model was adopted from Davis (1989) and Venkatesh and Davis (1996). The reported reliability value is 0.91. Likewise, four items scale of subjective norms was adopted from Venkatesh and Bala (2008). Its reported Cronbach alpha value is .775. Finally, the five items scale of self-efficacy was adopted from Venkatesh et al. (2003). Its stated Cronbach alpha value is .806.

Data Analysis and Results

Descriptive Statistics

The developed model is analyzed through the Partial Least Square Structural Equation Model (PLS-SEM) (Ringle et al., 2015). The PLS-SEM is utilized to evaluate the measurement and structural models in this study. The structural model refers to the link between the latent constructs themselves, whereas the measurement model (outer model) deals with the relationship between the constructs and their indicators (Hair et al., 2021). The fact that PLS-SEM allows contemporaneous analysis for both measurement and structural model, which leads to more accurate estimations, was the reason for its adoption in this investigation (Barclay et al., 1995).

Measurement Model Assessment

The results generated from the measurement model assessment represent the robustness of the constructs demonstrated by reliability, convergent, and discriminant validities measured through different indicators described below.

Convergent Validities

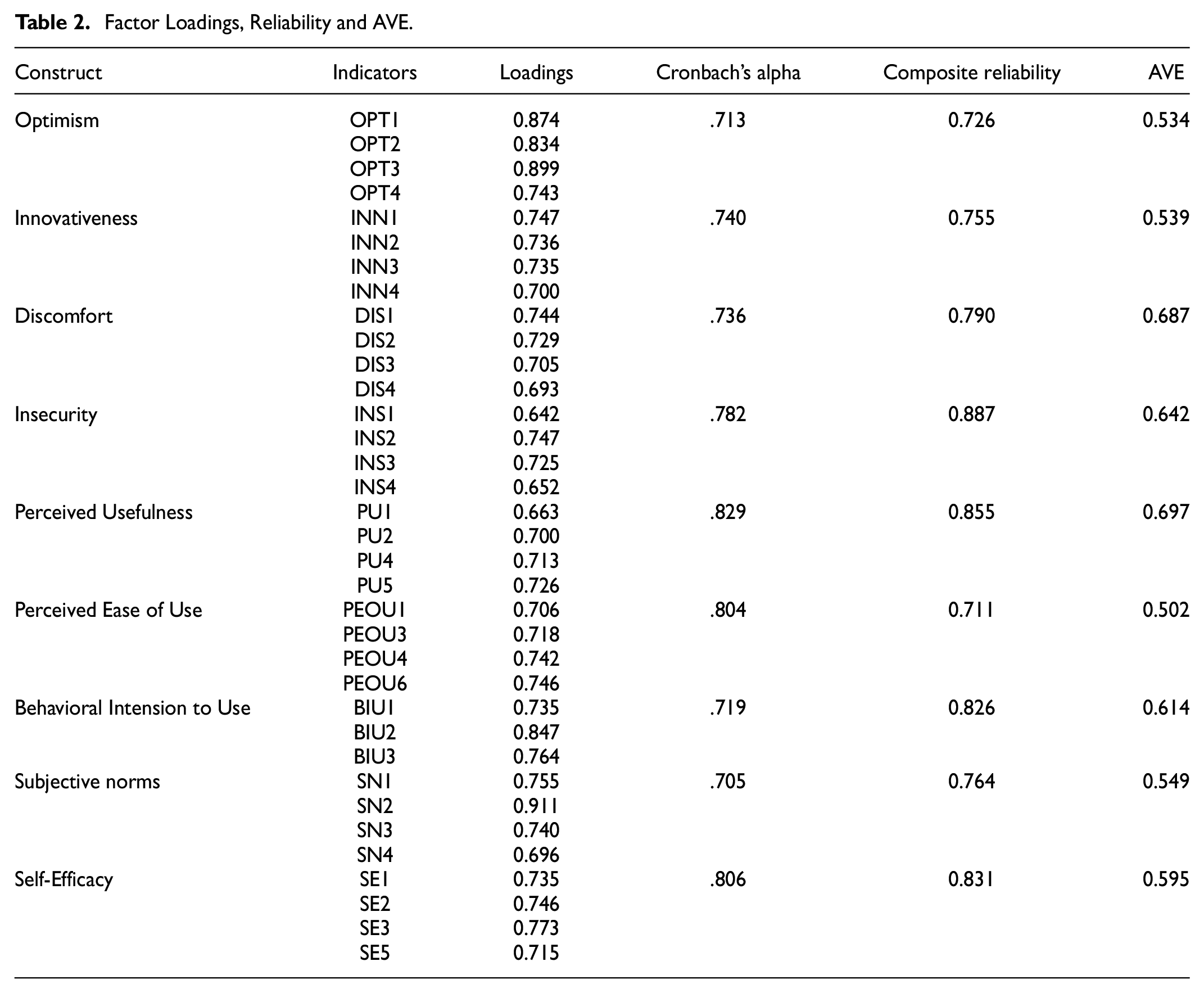

When assessing convergent validity, a variety of factors must be taken into account. These performance metrics include the average variance extracted (AVE), composite reliability, and the factor loading of the individual measures. The literature suggests that Hair et al. (2021), In order to be accepted, the factor loadings and composite reliability values must be equal to or more than 0.7, and the AVE values must be greater than 0.5. The convergent validity findings are shown in Table 2. The loadings for the measurement items were found to be greater than the recommended value in this research. Additionally, it was demonstrated that the AVE, Cronbach’s alpha, and composite reliability (CR) values were all greater than the required thresholds. The convergent validity is therefore confirmed.

Factor Loadings, Reliability and AVE.

Discriminant Validities

Discriminant validity refers to the degree to which one concept varies from all other constructs in the study model (Chin, 1998a, 1998b). Three factors should be considered for determining discriminant validity: the Fornell-Larcker criterion (i.e., the square root of AVE), cross-loadings, and the Heterotrait-Monotrait ratio of correlations (HTMT). Table 3 presents the HTMT based on the multitrait-multimethod matrix. Since the calculated values of HTMT are less than the recommended values of 0.85, it establishes discriminant validity (Kline, 2011).

HTMT Criterion for Discriminant Validity.

Additionally, the current study satisfies the Fornell-Larcker criterion for discriminant validity, which states that each construct’s square root of AVE (diagonal value) in the correlation matrix must be greater than the correlation of latent constructs, as shown in Table 4.

Correlation Matrix and Discriminant Validity.

Note. The bold values in the diagonal denote the square roots of AVE.

The correlational results reported in Table 4 show that optimism and innovativeness dimensions of personality traits exhibit a positive relationship, whereas discomfort and insecurity depict a negative association with PU and PEOU. Furthermore, subjective norms and self-efficacy have positive relationships with the perceptions of usefulness and ease of use—the core beliefs of technology acceptance. Moreover, innovativeness shows a positive association with self-efficacy and subjective norms. Similarly, optimism demonstrates a positive relationship with subjective norms. Finally, insecurity and discomfort narrate a negative association with the influencing factors of self-efficacy and subjective norms. These initial findings prompted us to perform further analyses.

Furthermore, the diagonal of Table 4 also represents the square roots of AVE to inspect the discriminant validity as per Fornell and Larcker’s (1981) criterion to be discussed in the subsequent section. Construct validity is established through convergent and discriminant validities. The convergent validity, which shows the mutual closeness of measures of a construct, is demonstrated through indicator reliability and AVE values. There were 40 items in the questionnaire, but 5 had to eliminate due to poor loadings, less than the benchmark of 0.6 (Gefen & Straub, 1997). Hence, the final set of 35 indicators with loadings ranging from 0.642 to 0.899 was retained for further analysis. Furthermore, the average variance extracted (AVE) scores are higher than the threshold of 0.5 (Hair et al., 2010). Therefore, the constructs show convergent validity, and meet the necessary condition of uni-dimensionality.

On the other hand, the discriminant validity of a construct is established if its measures are statistically distinct from other items. The discriminant validity has been proven since the diagonal values in Table 4, which reflect the square roots of AVE, are greater than the correlations with other constructs (Fornell & Larcker, 1981).

Structural Model Assessment

After the validity of constructs and the reliability of indicators have been established, the hypothesized relationships between constructs are assessed by the structural model, as shown in Figure 2.

Structural equation model.

In SmartPLS, bootstrap-based tests indicate the overall model fit and show coherence with a factor model it represents as confirmatory factor analysis (CFA) (Henseler et al., 2016). The values of SRMR and R2 delineate the model significance and fit measures (Henseler et al., 2016). According to Hu and Bentler (1999), a value of SRMR less than 0.08 indicates a healthy and good fit model. Wetzels et al. (2009) propose the threshold for R2 > 20%.

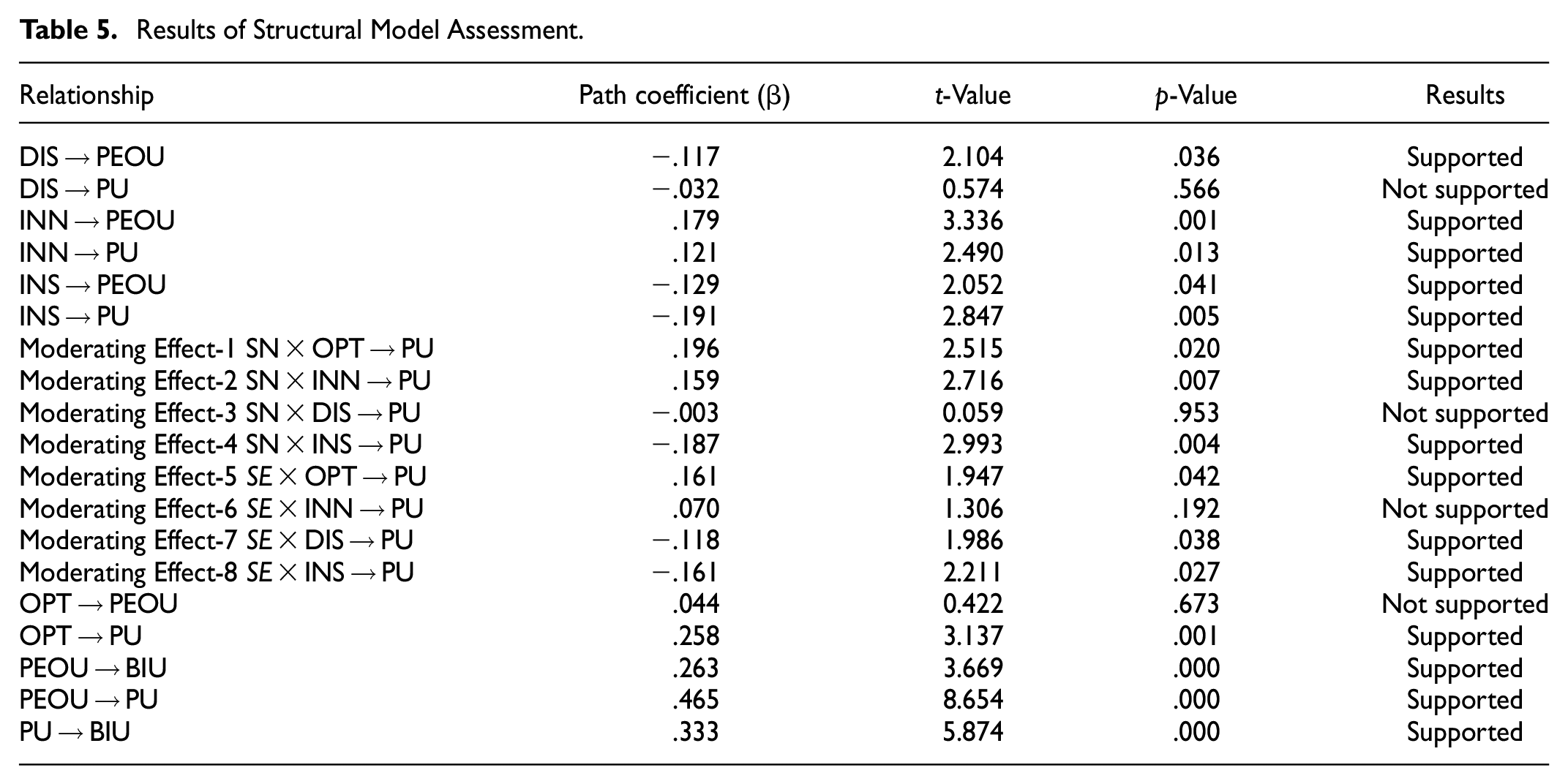

Our results show the value of SRMR = 0.072, p < .05, which indicates that the model is a good fit. Moreover, the explanatory powers of the three dependent constructs are satisfactory: PU (R2 = 38.2%), PEOU (R2 = 47.9%), and BIU (R2 = 36.3%). The path coefficient (β) implies that β units would change in the response variable by a one-unit change in the predictor. When the two-tailed test is applied, the value of t > 1.96 at a significance level of α = .05 is the criterion to accept or reject a hypothesis along a specific path (Chin, 1998a; Hair et al., 2014). In the context of the current study, the analysis of the results, including path coefficient (β), t-value, and p-value, has revealed that 15 hypotheses were supported, as shown in Table 5. Among the insignificant effects are: the effect of optimism on perceived ease of use (OPT → PEOU = 0.044, t = 0.422, p = .673), the effect of discomfort on PU (DIS → PU = −0.032, t = 0.574, p = .566). Similarly, subjective norms did not significantly moderate the negative effect of DIS on PU (SN × DIS → PU = −0.003, t = 0.059, p = .953), which was not expected. Finally, the moderating influence of self-efficacy was not confirmed in the relationship between innovativeness and perceived usefulness (SE × INN → PU = 0.070, t = 1.306, p = .192), which was not expected. Thus, H1b, H3a, H7, and H10 have been rejected.

Results of Structural Model Assessment.

Discussion

The findings illustrate how financial institutions are concerned about the relative advanced technology adoption benefits that result in lower costs and greater returns. This cutting-edge technology has encouraged the financial sector to provide a number of value-added financial services to maintain and draw in new customers. Therefore, banks must remove identified barriers that jeopardize consumers’ usage and continuity intentions in addition to choosing to maximize their competitive advantage by expanding their service domains and reducing their overheads. However, this strategy has not yet strengthened their expectations. The current study elaborates on various factors, including personality traits, self-efficacy, and subjective norms, that positively affect employee attitudes about technology adoption and usage intention.

Technology users with particular individual traits might prefer user-friendly new gadgets. Optimism and innovativeness dimensions of the personality trait of TRI exhibit a positive relationship, whereas, discomfort and insecurity depict a negative association with PU and PEOU of the TAM model. Previous research on TR and TAM supports the strong positive relationships between PEOU and PU (e.g., Godoe & Johansen, 2012; Kuo et al., 2013; Lin & Chang, 2011; Walczuch et al., 2007; Wook et al., 2017). Furthermore, subjective norms and self-efficacy have positive relationships with the perceptions of usefulness and ease of use—the core beliefs of technology acceptance. Previous studies stated that self-efficacy (SE) showed a strong positive relationship with PU and PEOU (Abdullah et al., 2016; Al-Gahtani, 2016; Park et al., 2012). Moreover, innovativeness shows a positive association with self-efficacy and subjective norms. Optimism demonstrates a negative relationship with self-efficacy, while positive with subjective norms. Finally, insecurity and discomfort narrate a negative association with the influencing factors of self-efficacy and subjective norms.

The PLS-SEM results exhibit that optimism attained a relatively strong positive influence on the core belief of technology acceptance PU (β = .258 and t = 3.137, p < .05). The strength of relation (β = .258) is positive and significance at α = 5% with correspondence to t-value = 3.137 (t > 1.96). All these findings support hypothesis H1a. Thus, optimism is a significantly strong predictor of the perceived usefulness of adopting new technology. These findings could enlarge the spectrum of technology readiness regarding individuals’ beliefs, as described by Walczuch et al. (2007), Erdoğmuş and Esen (2011), Hung and Cheng (2013), and Kuo et al. (2013). More specifically, optimistic employees have positive and open thoughts toward online banking systems because they are prone to achieving benefits and feeling confident by using the online banking system. In contrast to Erdoğmuş and Esen (2011), Godoe and Johansen (2012), and Jin (2013), this study is not successful in confirming the effect of optimism on perceived ease of use. The results demonstrated that perceived ease of use is not significantly predicted by optimism (β = .044 and t = 4.236, p > .05). The findings are not supported, so H1b is rejected. This is because the optimistic employees’ belief in the banking culture of Pakistan does not directly translate to utilizing new technology and system regardless of how easy the system is.

Similarly, the findings showed that perceived usefulness is significantly positively influenced by innovativeness (β = .121 and t = 2.490, p < .05) and perceived ease of use (β = 0179, t = 3.336, p < .05). Therefore, both hypotheses, H2a and H2b, are supported. Previous research (Erdoğmuş & Esen, 2011; Hung & Cheng, 2013; Jin, 2013; Kuo et al., 2013; Walczuch et al., 2007; Wook et al., 2017) provide strong evidence from empirical investigations that innovativeness is a significant determinant of perceived usefulness and perceived ease of use. The possible reason may be that employees of financial institutions understand this phenomenon and that early adoption of advanced technology is the key to success and a need of the hour. They might have thought to be the first mover, and well aware of the significance and benefits of the latest interventions in Pakistani financial institutions.

On the other hand, the findings failed to confirm the effect of discomfort on perceived usefulness (β = −.032 and t = 0.574, p = .566). The value of estimates of this path coefficient (β = −.032) verifies the negative association and direction which is in accordance with the hypothesis, but it is not statistically significant (p < .05). Therefore, the results do not support H3a. Previous studies have also reported an insignificant relationship between discomfort and perceived usefulness (Erdoğmuş & Esen, 2011; Godoe & Johansen, 2012; Hung & Cheng, 2013; Kuo et al., 2013). The employees’ high rating on discomfort felt overwhelmed by the usage of new applications and systems because of the complexity in the financial sector. In contrast, the findings demonstrated a negative association between discomfort and perceived ease of use (β = −.117 and t = 2.104, p < .05). Therefore, H3b is fully supported. The significant relationship between discomfort and perceived ease of use was also delineated by previous studies such as Lin and Chang (2011), Kuo et al. (2013), and Wook et al. (2017). Employees with minor discomfort discern easy and comfortable accomplishing tasks timely and accurately with the system because extended working hours encourage them to avoid misperceptions about e-banking.

Likewise, the findings confirmed that insecurity has a significant negative association with perceived usefulness (β = −.191 and t = 2.847, p < .05), and perceived ease of use (β = −.129 and t = 2.052, p < .05). These results highly support both hypotheses H4a and H4b. These have also been reported by an empirical investigation by other researchers (Jin, 2013; Kuo et al., 2013; Lin & Chang, 2011; Walczuch et al., 2007; Wook et al., 2017). Employees do not bother and get confused pertaining to system security and trust. The major perceived reason was autocorrected and insured automated software that displays the details of customers before any transaction. Secondly, long-term familiarity with IT overcomes insecurity regarding IT arena through training and experience with the online banking system.

It is expected that perceived ease of use (PEOU) significantly predicts the perceived usefulness of internet banking system adoption. The results disclosed that perceived ease of use has a strong positive significant relationship with PU (β = .465 and t = 8.654, p < .05). This relationship exhibited conformity with past studies by Hung and Cheng (2013), Kuo et al. (2013), and Wook et al. (2017). The core belief of perceived ease of use also has a positive effect on behavioral intention to use (BIU) (β = .263 and t = 3.669, p < .05). The results support both hypotheses H13a and H13b, which are in congruence with the previous findings (Wook et al., 2017). On comparative grounds, perceived usefulness has a stronger effect on the behavioral intention to use e-banking adoption than PEOU. The results (β = .333 and t = 5.874, p < .05) denote that behavioral intention to use is positively influenced by perceived usefulness. Therefore, hypothesis H14 is fully supported in this study. The findings are similar to the previous studies (Lin & Chang, 2011; Wook et al., 2017).

Now, referring to the moderating effects of subjective norms (SN) between TRI and PU, the results indicate that SN positively moderates the effect of OPT on PU (SN × OPT → PU = 0.196, t = 2.515 and p < .05), indicating that the positive direct effect of OPT on PU would further enhance in social influence contexts. Thus, H5 is fully supported. The positive interaction of SN on the effect of OPT on PU could be interpreted such that optimistic employees seem to be more open and positive toward the usefulness of the online banking system, for social influence in technology adoption would offer great benefits and convenience to their performance. In a similar context, SN positively moderates the effect of INN on PU (SN × INN → PU = 0.156, t = 2.716 and p < .05), thereby supporting H6. This could be explained such that the higher the level of social influence of employees, the stronger the effect of innovativeness on perceived usefulness, as reported among Pakistani employees. As a matter of fact, in banking culture, most employees provide assistance and consultation about new banking software and updates, so they influence each other in the sense of support and competition toward early adoption. Similarly, internet banking enables their personality traits to work at home or with friends compelled to adopt, at least with an early majority. The third moderating result reveals that subjective norms could not significantly moderate the negative influence of discomfort (DIS) on perceived usefulness (SN × DIS → PU = −0.003, t = 0.059 and p < .05). Hence, H7 was not supported. It means that it is less likely that the effect of discomfort on the system’s perceived usefulness attenuates with increasing social influence. The employees rating high on discomfort felt overwhelmed using new applications and systems. But because of the complexity, work-life imbalance, and pathetic working conditions, subjective norms make no prominent impact on utilizing the system comfortably. Finally, our study confirmed that the negative effect of insecurity on PU was significant when moderated by SN (SN × INS → PU = −0.187, t = 2.993 and p < .05). Thus, H8 is supported. In summary, subjective norms (SN) have significantly moderated the three paths of the four relationships identified in TR and TAM, as shown in Figure 1. Hence external influence plays a prominent role in employees’ readiness and adoption. Banking employees’ security concerns can be reduced by training and experience, so social influence is instrumental in operating the software and systems effectively.

In a similar fashion, taking up the moderating effects of self-efficacy (SE), it has been observed that SE positively moderates the effect of OPT on PU (SE × OPT → PU = 0.161, t = 1.947 and p < .05), thus giving countenance to H9. Self-efficacy, an intrinsic motivational factor, has also significantly shored up the relationship between optimism and PU. Hence, employees’ judgment of their capabilities plays a significant role in being comfortable and motivated with the e-banking system. Our findings further indicate self-efficacy did not significantly moderate the relationship between innovativeness and perceived usefulness (SE × INN → PU = 0.070, t = 1.306 and p < .05). Hence, H10 was not supported. However, even in this setting, it is less likely that the effect of innovativeness on the system perceived usefulness will diminish with the influence of moderating factor self-efficacy. Probably, employees may feel enthusiastic about their gained experience from the newest features of the technology, but they achieve this when they overcome their fears by pushing themselves with the growing use of the system and exploring its features more and more to reduce difficulties. Further to this line, the results reveal that a high level of self-efficacy will attenuate the negative direct effect of discomfort on perceived usefulness. That is, supporting H11, SE positively moderates the effect of DIS on PU (SE × DIS → PU = −0.118, t = 1.986 and p < .05). In other words, discomfort and self-efficacy have a moderating effect on perceived usefulness among employees in technology adoption. Finally, SE moderates the negative association of INS with PU (SE × INS → PU = −0.161, t = 2.211 and p < .05). Hence, H12 was endorsed. Thus, self-efficacy, an intrinsic motivational factor, has significantly moderated the relationships of optimism, discomfort, and insecurity of TRI with PU TAM. In a nutshell, the employees’ judgment of their capabilities can play a significant role in motivating them to use the online banking system.

Theoretical and Practical Implications

The outcomes of this research imply theoretical and practical repercussions. The integrated model of TAM and TRI provides strong support for system usage and user satisfaction with internet technology among the employees of financial institutions. Since technology readiness is person-specific while TAM’s constructs (usefulness and ease of use) are system-specific, the TRAM (Technology Readiness and Acceptance Model) blends system features with individual factors. It significantly increases the applicability and explanatory capability of earlier models in the context of organizations. Additionally, TRAM can clarify why people with high technology readiness index do not always embrace new technologies because the perception of ease of use and usefulness also play a crucial role in the mechanism of technology acceptance behavior. It is pertinent to mention here that the other extensions to TAM, for example, UTAUT, deals with user intentions to accept technology based on subjective norms, and UTAUT2 mainly includes extrinsic factors, whereas TRAM, which is the focus of this study, is concerned with the personality traits of an individual to accept the technology. Moreover, the two core beliefs, subjective norms and self-efficacy, contribute as a coping strategy to strengthen bonding between a person’s readiness for technology with the perceived ease of use and usefulness of the technology itself.

The findings revealed that conceding both technology readiness and technology acceptance are important in increasing employees’ behavioral intention toward online systems. Three out of four personality traits of TR that are optimism, innovativeness, and insecurity, have been empirically identified as antecedents of perceived usefulness, whereas, optimism, discomfort and insecurity have been identified as key elements of perceived ease of use, eventually influencing employees’ intentions toward new technology usage. The results also confirm the relationships between perceived usefulness, and perceived ease of use in adopting new technology. In addition, subjective norms and self-efficacy have remarkably concatenated technology readiness with acceptance and adoption in recuperating the underutilization of advanced technologies among employees.

This study contributed to the literature on TRAM with moderating effect of subjective norms and self-efficacy. It shows that managers and employees take it positively and adopt new technology, provided it benefits them. On parallel grounds, a number of studies on IT have also revealed the significance of subjective norms or group pressure in users’ technology acceptance, especially in the deployment of moderating effect on the opinion of new technology adoption, especially in obligatory position (Lee et al., 2011; Svendsen et al., 2013). Bandura (1982) stated that self-efficacy manifested judgment of persons’ own capability to accomplish a specific task. Persons with low self-efficacy were considered pessimistic and had little self-esteem to attain goals; their experience and own performance represented two sources of self-efficacy. Previous studies stated that self-efficacy played an important role in the acceptance and usability of new technology, and showed a strong positive relationship with key determinants of the technology acceptance model (reviewed by Al-Gahtani, 2016; Park et al., 2012). However, this study has specifically contributed to understanding the catalytic role of individual beliefs in transforming technology readiness to technology acceptance. This study suggests that integrating TRI with TAM in relationship with moderating roles of subjective norms and self-efficacy would give countenance to the employees of financial institutions in adopting avant-garde technology to boost their efficiency and work quality.

Conclusions

By incorporating subjective norms and self-efficacy as individual beliefs, this study performed an empirical inquiry in financial institutions to determine the state of employees’ technology readiness and technology acceptance model into one improved research model. The moderator variables provide a more comprehensive framework for a better understanding of the technology acceptance phenomenon than academic literature.

The findings revealed that conceding both technology readiness and technology acceptance are important in increasing employees’ behavioral intention toward online systems in financial institutions. Three out of four personality traits of TR, optimism, innovativeness, and insecurity, have been empirically identified as antecedents of perceived usefulness. On the other hand, optimism, discomfort and insecurity were identified as key determinants of perceived ease of use, eventually influencing employees’ intentions toward new technology usage. The results also confirmed the relationships between two core individual beliefs of subjective norms and self-efficacy conducive to the acceptance and adoption of underutilized cutting-edge technologies among employees, specifically in financial institutions. The moderating effect of the subjective norms significantly moderates the relationships of optimism, innovativeness, and insecurity of TRI with the perceived usefulness of TAM. Similarly, self-efficacy also significantly moderates these relationships. This study contributed to the literature on TRAM by moderating the effect of subjective norms and self-efficacy. It shows that managers and employees of banks and insurance companies positively adopt new technology, provided it is beneficial for them. This study suggests that integrating TRI with TAM in relationship with moderating roles of subjective norms and self-efficacy would give countenance to the employees of financial institutions in adopting avant-garde technology to boost their efficiency and work quality.

The study concentrated on the employees’ intention and adoption of new technology, yet, it did not examine the consequences (post-adoption behavior) of using such technology on the employees’ satisfaction and loyalty. Therefore, these aspects could be a valuable direction to examine in future research.

Limitations and Future Research

Although, the research contributes substantially, this study is not without limitations. First, due to the cross-sectional nature of the study, it is prone to common method bias with a single instrument of a questionnaire. Therefore, further validation is required to assimilate findings. Second, the study concentrated on the employees’ intention and adoption of new technology, yet, it did not examine the consequences (post-adoption behavior) of using such technology on the employees’ satisfaction and loyalty. Therefore, these aspects could be a valuable direction to examine in future research.

Furthermore, the generalizability of the results is limited due to the single-country setting. In order to enlarge the landscape of applicability of the findings, future studies should be carried out in other regions across industries. Similarly, data of the current study were collected using convenience sampling of Pakistani employees working in financial institutions. However, this could have a negative effect on the generalizability of the results. Consequently, it would be worthwhile for future studies to use different sampling techniques (e.g., random sampling) to capture more generalizability of the Pakistani banking employees.

Besides, the results of the current study have been extracted using a quantitative modus operandi. Nevertheless, applying a qualitative approach would provide a deeper picture regarding the diverse aspects that could form the Pakistani employees’ perception and behavior toward e-technologies. Finally, this study only focused on the employees’ perspective but did not look at this problem from the customers’ perspective. Therefore, future studies should look at this challenge from customers’ perspectives in order to provide a full picture by clarifying all the facets related to the successful implementation and adoption of technology from both sides.

Footnotes

Appendix Questionnaire

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Ethics Statement

Ethical review and approval were not required for this study on human participants because the opinion was gathered and analyzed anonymously. Moreover, the results do not discuss exclusive opinion of a certain respondent.