Abstract

This study focuses on the admission criteria of a bachelor of accountancy (BAcc) degree program as one of many factors influencing students’ success in graduating in the regulated time frames. The present study used constructivist learning and student engagement theories as connected lenses to explore the effect of admission criteria on first-year-level students’ academic performance. The research findings emanate from a mixed methods methodology using logistic regression, one of the choice models in the International Business Machines (IBM) Statistical Package for Social Scientists (SPSS), and semi-structured interviews. A sample of 43 was randomly selected from the list of 91 students with NSC-level accounting to match the number of 43 students who did not do NSC-level accounting offered in South African high schools. This gave the researchers a study sample 86, which reduced 81 following incomplete data submission by five students. The study’s findings suggest a sensitive understanding of students’ engagement with program materials and admission criteria. The admission criteria embraces prior high school knowledge reflected in the NSC-level admission points score (APS) and NSC-level mathematics. In addition, student dedication is a dimension of student engagement that we explored. The value of the study is a contribution to the reconsideration of student engagement alongside program admission requirements, leading to the integration of constructivist learning and student engagement theories. Prior studies have not integrated constructivist learning and student engagement theories into their research design. We recommend the continued use of the NSC-level APS score and mathematics in the admission requirements of the BAcc learning and development programs. We also recommend using teaching and learning activities that bring out student dedication. More research should be done on all aspects of student engagement premised on graduating students.

Introduction

Proponents of constructivist learning theory (CLT) contend that experience is the major component of students’ success in their studies (Papaioannou et al., 2022). Flowing from CLT tenets is the advocacy for prior knowledge, which plays an important factor in the students’ successful completion of their professional certification assessments. Coetzee et al. (2018) demonstrated that learners without pre-enrolment accounting consult course facilitators to highlight the pressure associated with teaching and learning in accountancy at the higher education institution (HEI). Many studies have been conducted on first-year learners without an accounting background and their success rates. Research findings support the notion that learners with accounting awareness from the National Senior Certificate (NSC) level performed much better than students with no prior knowledge of accounting from the NSC level in their first-year introductory accounting (Papageorgiou, 2022; Papageorgiou & Carpenter, 2019; Rossouw & Brink, 2021). Other studies show that NSC-level accounting does not matter in the student’s success in accountancy training at an HEI. Bergin (1983) and Al-rashed (2001) are among the researchers who have established that the NSC-level accounting lacked explanatory power on the first-year academic performance at an HEI.

The present paper revisits the debate on admission criteria. The reasons for revisiting the debate on admission criteria are (i) admission requirements concerning National Senior Certificate (NSC) accounting as a high school subject for students applying for the “Bachelor of Accountancy (BAcc)” degree to become a Chartered Accountant (CA) vary among the higher education institutions (HIEs) in South Africa; (ii) the Chartered Accountant Competency Framework 2025 (CA2025) has changed the focus of topics taught and examined in the professional certification syllabus at a time when the 2008 NSC examination requirements have not; and (iii) evaluating BAcc degree admission criteria serving as contributing determinant academic success in South African (SA) studies. Scholarly research at the international level fails to show the SA BAcc degree admission requirements not to be determinants of academic success.

The present study builds on the work of Papageorgiou and Carpenter (2019), Ayaya (1997), and Al-rashed (2001) but applies the probabilistic model (logistic regression) instead of correlation analysis. The current exploration expands on the prior research by examining a context in which the Chartered Accountant competency framework (CA2025) will require revisiting admission requirements into the HEI’s BAcc degree programs. The study context has learners’ demographics that are at variance with what has been used in other studies. The study tests the influence of pre-admission requirements on academic performance outcomes witnessed in the first-level training under the Bachelor of Accountancy (BAcc) degree program. In addition, it explores the role played by students’ dedication to learning.

The rest of the write-up is organized to cover the study context, problem statement, and research propositions. The literature review results and brief highlights of the CA2025 competency framework implications to the admission criteria alongside the implicit tenets of the constructivism learning and student engagement theories follow the research propositions section. Research methods and analytical framework are discussed to feed into the results and discussions. The present article ends with a section on conclusions and practical implications.

The Study Context and Site

The prior studies referenced from SA were based on data samples drawn from historically advantaged HEIs offering three-year accountancy programs. The University of Limpopo (UL) BAcc degree program is a four-year learning and development program provided by a traditionally disadvantaged HEI in the country. The UL’s BAcc program was accredited after 2012. Most UL’s School of Accountancy (SoA) BAcc students are drawn from rural schools in the Limpopo Province. The evidence of challenges experienced by the students is shown in the number of appeals for readmission under the general rules of the University (Tables 1–6). The university’s general rules stipulate, among others, matters regarding the minimum and maximum study duration. The students who filed appeals with the school administration sought mercy from the school under the university’s general rules needed to go through the appeal process and be accorded mercy to complete their degrees. Therefore, we proceed with the exploratory journey on the premise that the admission criteria excluding prior NSC-level accounting knowledge facilitate students’ progression from the first-year level of study to subsequent years of study. Failing first-year level financial accounting gives students limited course registration options in the second year of BAcc degree studies.

First and Second-Year Progression Rates.

Source. Researchers’ analysis of the 2022 Examination Commission report of the Faculty of Law and Management.

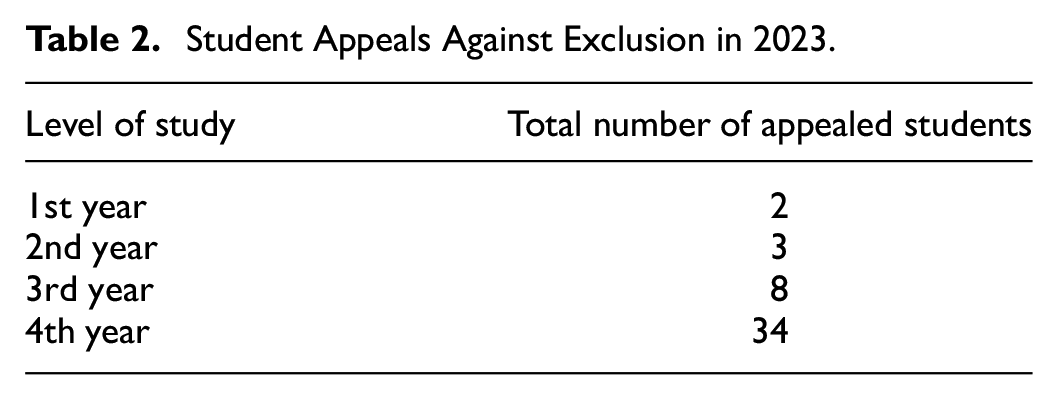

Student Appeals Against Exclusion in 2023.

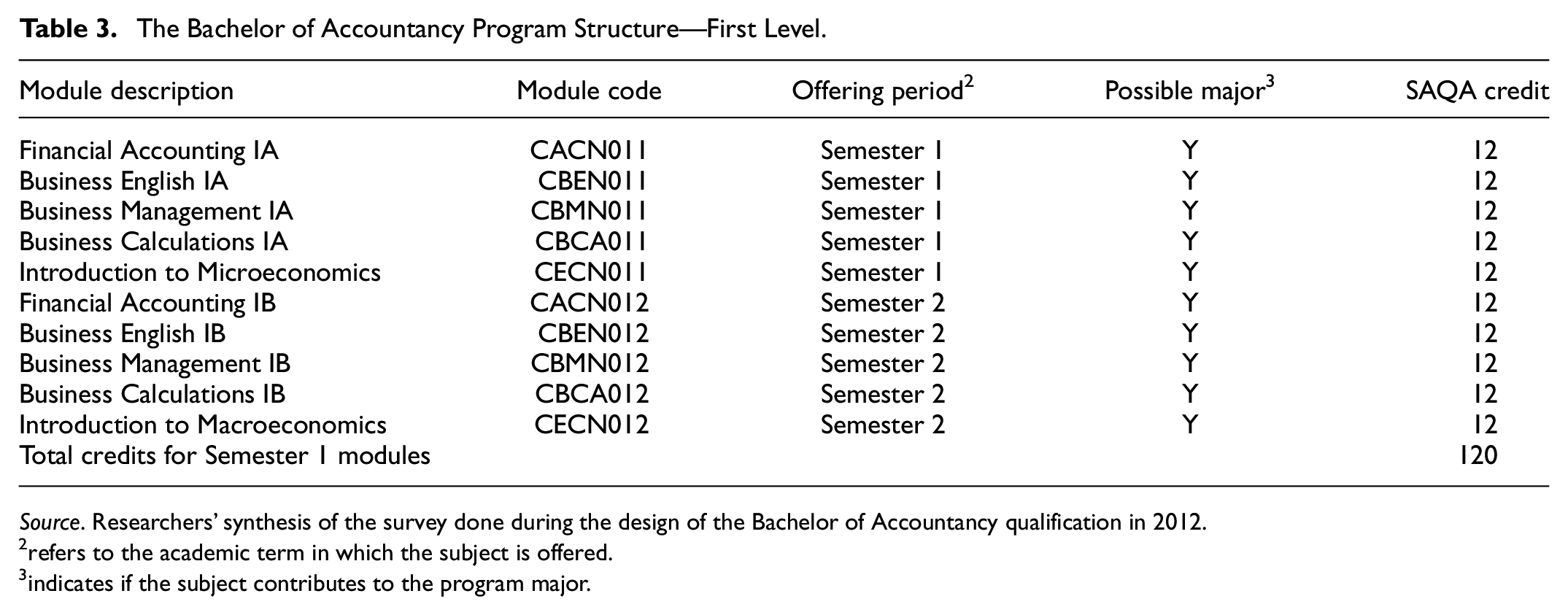

The Bachelor of Accountancy Program Structure—First Level.

Source. Researchers’ synthesis of the survey done during the design of the Bachelor of Accountancy qualification in 2012.

refers to the academic term in which the subject is offered.

indicates if the subject contributes to the program major.

The Bachelor of Accountancy Program Structure—Second Level.

Source. Researchers’ synthesis of the survey done during the design of the Bachelor of Accountancy qualification in 2012.

2refers to the academic term in which the subject is offered.

3indicates if the subject contributes to the program major.

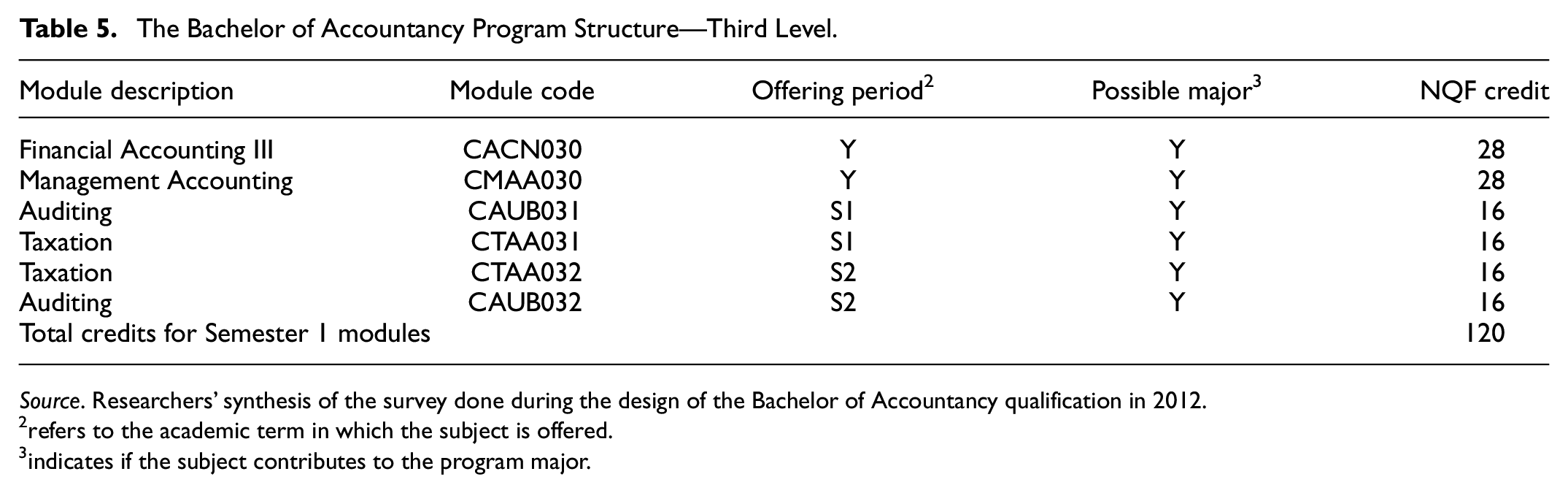

The Bachelor of Accountancy Program Structure—Third Level.

Source. Researchers’ synthesis of the survey done during the design of the Bachelor of Accountancy qualification in 2012.

2refers to the academic term in which the subject is offered.

3indicates if the subject contributes to the program major.

The Bachelor of Accountancy Program Structure—Fourth Level.

Source. Researchers’ synthesis of the survey done during the design of the Bachelor of Accountancy qualification in 2012.

refers to the academic term in which the subject is offered.

indicates if the subject contributes to the program major.

The UL’s SoA admits students with low admission points scores (APS) of 30 or better and mathematics with a pass level of 4 (50%–59%) compared to historically advantaged universities that admit students with APS scores of 34 or better and require mathematics pass levels of 6 (60%–70%) in the NSC examinations. The differences in the admission criteria make a case for a four-year BAcc degree program at the UL’s SoA.

The UL is a former “black only” university during the pre-1994 days of apartheid. It, therefore, mainly attracts students from rural and marginalized communities due to its rural setting in a town that is growing. The Department of Basic Education scored general education in the province among the country’s poorest-performing provinces. Most students arrive at the university from high school in the catchment area with a minimum basic university enrollment pass.

Williams et al. (2022) discovered two substantial findings. First, scholars who got 70% (level 6) or above in NSC accounting completed their accounting degree in record time. Furthermore, scholars who got 70% (level 7) below for maths and did not have an accounting background from secondary school could not complete their accounting degree in record time. The question worth asking is: to what extent do the admission criteria contribute to the less than satisfactory progression rates in the UL SoA BAcc program? How does student engagement contribute to ensuring BAcc first-year-level students’ academic success?

The quality of completion of an accounting degree is the prerequisite to the professional accounting initial tests of competence. The unsatisfactory progress depicted in Tables 1 and 2 calls for action and a revisit of the admission criteria, among other interventions. There is support from a South African study that revealed that academics perceived the lack of prior secondary school accounting knowledge as a hindrance to students completing an accounting module in the first year (Williams et al., 2022). Consequently, failing first-year level financial accounting courses automatically causes the students not to complete their accounting degree in 4 years, the stipulated minimum duration. Completing the first degree in accountancy is a requirement for the enrolment for a post-graduate accountancy diploma, a prerequisite to writing the initial tests of competence in the professional certification journey.

The first-year level requires students to cover topics in financial accounting, economics, business calculations, business English language (communication skills) and business management. The program designers envisaged the first-year level to offer a foundation to the chartered accountancy learning and development areas (management accounting, corporate finance, taxation, auditing, business strategy, financial reporting). Tables 3 to 6 summarize the program architecture. The program architecture shows that the Bachelor of Accountancy program prepares students for a professional accountancy certification offered by IFAC-affiliated professional bodies. In the contact-based setup, student mentors and tutors assist first-year students in working through the teaching and learning materials, contributing to assessments.

The professional certification requirements tended to respond to the labor market’s times and demands. Student progression is a critical factor in measuring the effectiveness of the admission criteria in addition to teaching and learning delivery modalities. The program design refers to the national qualifications framework (NQF) stipulating learning outcomes at different levels. The NQF is administered by the South African Qualifications Authority (SAQA).

Problem Statement

The majority of the University of Limpopo (UL) School of Accountancy (SoA) Bachelor of Accountancy (CA stream) students are experiencing challenges in completing their degree in the minimum given time of 4 years. Table 2 provides the number of students who filed appeals for registration renewal to complete the qualification. Table 3 shows the pass rate levels that depict less than satisfactory progress rates. The state of affairs depicted in Tables 3 and 4 shows signs of academic wastage that require interventions starting with a review of the admission criteria and examining how students engage with the subject matter in the BAcc degree program. Other interventions could be learning and teaching delivery that enlist student engagement. The prior studies on the topic have been case studies whose context is bound to differ from that of the UL SOA’s BAcc degree program. The results from a case study cannot be generalized (Hancock et al., 2021), and only theoretical generalizations can be made (Piekkari & Welch, 2018). In addition, as one moves out of SA higher education institutions, studies provide conflicting results regarding pre-enrolment attributes and the role played by prior accounting knowledge (Ayaya, 1996; Keef, 1988)

Some students have been affected by general university rules (G:26—Renewal of registration; G:25—Admission to a subsequent module; G:10—Duration of study, etc.), where they need to go through the appeal process to complete their degrees (SoA, 2022). The review of the 2022 results of the BAcc degree, first-year and second-year level students’ performance was found to be less than satisfactory. The review of 2022 showed a gloomy picture when the fourth-year results showed a pass rate of 44%, and 34 students were affected by the university’s general rules (Table 4). The statistics in Tables 1 and 2 above show instances of academic wastage. Over the years, students have needed help to complete the four-year degree in the required 4 years. The admission numbers in the first year are at least 150 students each year.

Nevertheless, those who complete the qualification in the required 4 years represent 60% of those admitted students. As a feeder program to the PGDA, the BAcc qualification has contributed 30 to 50 students (representing 16% of the BAcc graduates) since the inception of the post-graduate diploma in accountancy (PGDA) in the UL in 2018. The PGDA is a higher education qualification that precedes the administration of initial tests of competence for candidates seeking to undertake a professional certification in accounting and financial management with the South African Institute of Accountants (SAICA)

The Study Aims and Scope

This study is an initial attempt to explore research toward revising the admission criteria for the BAcc degree program. We explore how NSC students’ academic success in mathematics, English, APS and accounting influence first-year-level academic performance at a higher education institution. The exploration starts with first-entering students’ year-end academic performance as a response variable analyzed in logistic regression. Exploration is done from constructivist learning and student engagement theories so that we recognize the roles played by prior learning and student dedication as essential elements in teaching and learning. Bada and Olusegun (2015) and Stewart (2021) have argued that students construct new knowledge and its meaning from their prior learning experiences. The study does not consider teaching and learning interventions (study times, teaching approach, availability of books, etc.) that could influence academic success at the first-year level. However, we considered the student’s dedication complementary to a learner’s previous experiences. The study contributes to the joint use of the constructivist and student engagement theories in teaching and learning.

Research Questions and Hypotheses

The study endeavors to get answers to the following questions: What is the academic performance predictive value of the admission criteria? The following hypotheses were examined:

NSC-level accounting scores do not enhance the likelihood of a student succeeding in the first year of the BAcc program.

NSC-level mathematics scores enhance the likelihood of a student succeeding in the first year of the BAcc program.

NSC-level English language score enhances the likelihood of a student succeeding in the first year of the BAcc program.

Student dedication to studies does not overshadow the importance of pre-admission enrolment requirements of the BAcc degree program.

The four hypotheses are clarified further and linked to the results of the literature review.

Objectives and Significance

The research sought to consider and report on the admission criteria and student engagement as determinants of first-year academic success in the BAcc degree program. The significance of the study is that it establishes enrollment factors that can guide grade 11 learners to select NSC-level subject areas relevant to studies in accountancy at the University of Limpopo.

Significant research has been done to establish the impact of pre-enrolment attributes on academic success at the higher education level (Ayaya, 1997, 1999, Brook & Roberts, 2021). The findings are mixed. For example, Brook and Roberts (2021) established that mathematics results for first-entering students impact their ability to excel at the HEI accounting courses. Ayaya (1996) discovered that the Cambridge Overseas School Certificate significantly contributes to the overall student’s academic performance at the university. Ayaya’s (1997) study shows that mathematics and the English language contributed to academic success among accounting students. In addition, the context of the studies was different. Ayaya (1996, 1997) was based on a program in the National University of Lesotho degree offering. Previous research in this area considered a number of factors influencing academic performance, such as prior academic achievement, gender, marital status, age, language and quantitative analytical abilities. The mixed results could be credited to differences in the higher education institutions considered (Ayaya, 1999), the subjects analyzed, and the research methods adopted (Brook & Roberts, 2021). According to Ayaya (1999), the high school requirements are aligned with the Cambridge Certificate of Education. The methods applied used multiple regression and correlation analysis. In the present study, we employ logistic regression, one of the probabilistic models that have matured since the work of Amemiya (1981).

To this end, the study proposes to:

Provide recommendations to revise the admission requirements of the BAcc degree program.

Guide students seeking admission to the Bacc degree program.

Provide a foundation for future research to develop measures that mitigate academic waste.

This study will improve the understanding of the admission criteria, given the CA2025 imperatives. The admission criteria were implemented before the South African Institute of Chartered Accountants adopted CA2025. The content and examination approach for CA2025 has changed, and pre-admission requirements must be changed to reflect the changing times. CA2025 implementation is in full gear, and a review of the BAcc’s students’ performance, given admission requirements, is overdue. The BAcc degree courses have attracted exemptions from professional accountancy certification bodies (ACCA, CIMA). The SAICA and other professional accountancy certification organizations will also be interested in the results of this study due to their links with the SA’s HIEs.

Literature Review

Lack of Prior Accounting Knowledge Limits Academic Success at the First-Year Level of Accounting

Papageorgiou and Carpenter’s (2019) study examined whether accounting background contributed to students’ academic progress in the accounting offered at the HEIs. The study established a significant positive connection between students’ academic performances in the first-year accounting course and the NSC Accounting scores. The findings are consistent with the research results reported in the research of Rowlands (1988), Ayaya (1997), and Uyar and Güngörmüş (2011). Another survey by Matarirano et al. (2020) studied the influence that admission scores from the NSC assessments had on the achievements of first-entering scholars enrolled for the Accountancy qualification at Walter Sisulu University (WSU). This leads to the following testable hypothesis:

NSC-level accounting has not made a significant contribution to the success of the BAcc degree program.

The testable hypothesis is premised on the fact that studies reviewed in this regard focused on accounting subjects whose content emphasizes accounting procedures that have been automated in most accounting packages.

More recently, Jansen et al. (2022) investigated the reasons, outlooks, and awareness of first-entering accounting learners enrolled for an accounting degree at the University of the Western Cape (UWC). Their study contributed to considering the first-entering knowledge of students learning at historically underprivileged universities in South Africa. The research revealed that students’ reasons, outlooks, and awareness for higher education influence first-entering students’ success in their higher education learning. Jansen et al. (2022) findings contend that students’ time obligations remained associated with that intended by their HEI and were influenced by a combination of inside and outside considerations. Jansen et al. (2022) show the importance of other factors in constructing meaning in higher education teaching and learning. We can argue that those other factors include student engagement. Consequently, we developed a testable hypothesis:

Student engagement significantly contributes to academic success in the BAcc degree program.

NSC-level English language proficiency significantly contributes to student academic success in the BAcc degree program.

The accounting discipline at the HIEs is now more conceptual (Figure 1). It emphasizes pillars of financial accounting that include ethical conduct in reporting, communication, critical thinking, and financial reporting problems (Weygandt et al., 2018). First-year level accounting is among other subjects such as business English language, business management, and introduction economics (Table 3). Excelling in these other subjects is as important as excelling in the first-year level of accounting. The findings of the review studies emphasizing academic success in first-year level university accounting require a revisit.

Constructivist learning theory and CA2025 competency framework implementation.

Joynt’s (2022) study intended to provide an impenetrable explanation of a bridging course of accounting offered to first-entering scholars before they can enroll for a major in accounting degree. The focus was on transitional challenges the first entering students may have. The bridging module is intended to ameliorate the effects of the absence of an accounting background. Moreover, the study appraises the efficacy of the bridging module through econometric systems. According to Joynt (2022), the bridging module in accounting allows lecturers to guarantee that scholars are intellectually well-organized. The thinking in the discussion of the findings resonates well with the design of a four-year BAcc degree at the University of Limpopo. Joynt’s (2022) findings agree with the findings reported in the Ayaya (1997) study, which established a strong link between bridging courses and academic success at the National University of Lesotho.

Rossouw and Brink (2021) sought to examine the success rate of those scholars studying for accounting degrees with no NSC-level accounting. Their study results were to develop or change the framework for South African universities’ first-entering scholars’ admission requirements for a Bachelor of Accountancy for those students with no NSC-level accounting. Through structured questionnaires, a quantitative study technique was used to answer the study’s research questions. Rossouw and Brink’s (2021) findings show that 81% of students could complete their qualifications but not in the minimum stipulated time. The findings are informative and suggest that NSC-level accounting is unnecessary for a student to earn a degree in accountancy within the stipulated time. On the face of it, the results are consistent with the results and inferences in the Keef (1988) study. We argue that the NSC-level accounting is unnecessary when considering the teaching and learning approach that brings out students’ dedication to studying the subject matter as a language of business.

Williams et al. (2022) examined two groups of scholars registered for Bachelor of Accountancy with and without NSC-level accounting scores during 2017–2019 at the University of Western Cape. Williams et al. (2022) noted two substantial findings. Firstly, scholars who got 70% above in the NSC-level accounting completed their accounting degree in the required minimum duration. Furthermore, scholars who got 70% below for maths and did not have high NSC-level scores could not complete their accounting degree in record time. Once again, the conclusions pointed to the need for admission criteria to consider NSC-level mathematics and NSC-level accounting. The literature review results led the research to consider the following as testable hypothesis:

NSC-level mathematics is a significant contribution to the academic success in the BAcc degree program.

CA2025 Competency Framework and the Constructivist Learning Theory

The reviewed results focused on the three-year BCom (Accountancy) qualifications. The studies inadequately used the theoretical lenses of CLT. In addition, the methods employed relied on descriptive statistics and correlation analysis. The present study employs logistic regression analysis to respond to the likelihood of student success after enrolling in the BAcc degree program at the UL SoA. The response variable considers performance in the first-year level courses and not just performance accounting. Prior studies relied on samples drawn from graduates outside the CA2025 competency framework of the South African Institute of Chartered Accountants (SAICA).

CA2025 competency framework sets out what professional competence newly qualified CAs should demonstrate. CA2025 competency framework articulates the competencies an entry-level accountant should exhibit after completing the academic program at an HEI institution, a training program with an approved training site, a professional program and the two professional assessments. The framework recognized the evolving roles of a chartered accountant. In particular, the CA2025 competency framework emphasizes digital competencies, business acumen, ethical conduct in business and profession, critical thinking, and futuristic orientation in decision-making. Technical skills in management accounting, financial reporting, audit, corporate governance, and taxation continue to be offered, but with more emphasis on the pervasive skills. The NSC-level accounting curriculum was adopted for high schools in 2008 (Department of Basic Education, 2018). We submit that the changes accompanying adopting the CA2025 competency framework have yet to be anticipated in teaching and learning at the NSC level.

Consequently, to continue to expect the contents of NSC-level accounting to be significant in academic success should be re-examined. In addition, we conceptualize the first-year level accounting to respect the pillars depicted in Figure 1. Figure 1 illustrates how the prior knowledge and experience connect to envisaged teaching and learning in one of the first-year level learning areas (Financial Accounting). Student engagement is linked to the learning and teaching environment offered by the School of Accountancy at the study site and through virtual teaching platforms.

The CA2025 competency framework advocates for balance and integration between technical and non-technical competencies, which requires the present study to consider the academic performance that considers subject areas offered to first-entering students. The explanatory variables consider the NSC admission score, mathematics, exposure to NSC-level accounting, NSC-level admission points score and NSC-level English Language. The admission points score (APS) from the NSC-level subjects constitutes a measure of prior knowledge, which must interface with the knowledge and skills envisaged under the CA2025 competency framework. In addition, student dedication to learning digital skills, business acumen, problem-solving, etc., requires consideration when debating academic success under the BAcc degree program.

Student Engagement as a Contributor to Academic Success

The present studies have recognized the role CLT plays in academic success. However, the researcher contends that student engagement theory (SET) has much to offer, and learners must achieve academic success. The published literature has contributed to constructivist learning and student engagement theories as if they did not function jointly to explain the phenomenon of student academic success. Student engagement is an intricate, multidimensional construct that has attained great interest in higher education institutions (Kassab et al., 2023). The conceptualization of student engagement is a valuable step in developing the tools for its measurement when understanding academic success. The discussions on teaching and learning styles impinge on student engagement (Halif et al., 2020). Kassab et al. (2023) have proposed a framework for student engagement and contend that student engagement constitutes the student investment of time and energy in learning and teaching activities beyond lecture attendance.

Those in the health professions consider student engagement to carry the cognitive, affective, behavioral, agentic, and socio-cultural dimensions (Kassab et al., 2023). Human resource specialists have considered student engagement to have dedication, absorption, and vigor dimensions (Schaufeli & Bakker, 2010). This is what leads to the Utrecht Work Engagement Scale (UWES). In the current study, we do not seek to explore all perspectives of student engagement in the published literature. The present study recognizes student engagement dimensions as an ingredient that complements tenets of the constructivist learning theory to explain the phenomenon of academic success. The rationale for selective consideration of student engagement dimensions is informed by the HEIs’ general rule requiring students to attend at least 75% of teaching and learning activities offered in academic terms. The general is commonly called the “Due Performance (DP)” rule. Given the tenants of the SET, the researchers argue that the DP rule should be complemented by submissions of formative assessments based on assignments, concept tests and class activities.

From the above, the researchers considered the student engagement dimension related to dedication (complying with the DP rule, submission of assignments, concept tests and class activities). Student engagement, as a phrase, emerged in the discussions with selected BAcc degree students regarding success in the first-year level courses in the BAcc degree program. The researchers worked from the self-report survey and considered the submission of class tasks and interviews before assigning a classification value to student dedication, an aspect of student engagement. The researchers elected not to consider absorption and vigor associated with SET. The engagement dimension of dedication was measured by self-report surveys ranging from one (lowest) to seven (highest). The instrument was developed and tested using 20 students who were later excluded from the sample.

Data and Methods

Methodology

The study relied on mixed methods sequenced to collect evidence on the application of student engagement and constructivist learning theories. The quantitative part of the study relied on the use of logistic regression modelling, in which academic success is seen to be probabilistically influenced by the predictor variables. In addition, interviews were held with the informants to develop messages on the BAcc admission criteria and student engagement’s role in the student’s academic success in the BAcc degree program. The interview results are triangulated to the logistic regression results to achieve dependability.

Population and Sampling

The study population in the present exploratory analysis comprises BAcc students for the 2023 academic year. The population was 192 students, of whom 43 did not present NSC accounting scores on their certificates, and 38 were repeating the course (were not registered for the four courses offered in the first year). This left a population of 111 students with NSC-level accounting, of which 20 were used to test the research instruments on student engagement. This left the researchers with first-entering students with an NSC accounting. Forty-three students on the list of 91 confirmed having done NSC-level accounting. This compelled the researchers to randomly select 43 students from the list of 48 who did not hold NSC-level accounting. This sifting gave the researchers a study sample of 86, which was reduced to 81 following incomplete data submission by five students. The sample size of greater than 30 allowed for conclusions to be drawn.

Data Sources and Generation Instrument

Data sources entail secondary data on student academic scores in the university records. The University’s Principal Administrative Officers (The school of accountancy offices) keep the student score. Access to student NSC scores was facilitated through applications to the relevant offices and after necessary ethical clearance. Necessary disclosures were made to the relevant students, and they were called for their consent to participate in the interviews, the results of which are not highlighted in the present paper. The school of accountancy’s databank was used to collect data in Microsoft Excel indicating the students’ academic performance for the final examination, if students had NSC-level accounting, and the grades earned in the NSC-level accounting.

The student dedication aspect of the study relied on a tool that the researchers developed and tested before it was used to collect data. The tool was developed and tested with 20 students who did not form part of the study. The data was analyzed using IBM’s Statistical Package for Social Scientists (IBM SPSS Statistics Version 29). The SPSS generated descriptive statistics, too. The researchers also administered a semi-structured questionnaire to understand how the students without NSC-level accounting managed to progress through the program.

The Choice Models and the Study’s Analytical Framework

At the end of the academic year, the student passes the required courses in the program. Students can register for second-year courses except for accounting courses if they are yet to pass first-year-level accounting. The selection of the academic success variable was informed by the university’s reliance on academic-level performance to guide decisions on student progression. The researchers selected predictor variables based on their inclusion in the admission criteria. As pointed out earlier, student engagement in the DP rule requires students to participate in 75% of teaching and learning activities in an academic term. Soon after adopting and registering for the BAcc degree qualification, the UL made an informed choice to promote the admission requirements. The decision to progressively implement the admission requirements was based on the need for quality and success rates to ensure graduate progress to the post-graduate diploma in accountancy. The school’s teaching and learning philosophy did not change.

The logistic regression model was used to approximate the connection in which the likelihood of excelling depends on the predictor variables whose selection was informed by the CLT and SET. TA students succeeding in year one’s subject offerings is defined by ACC_P1 (Table 7). The logistic regression technique is used in this study because the conventional least square technique is unsuitable when the dependent factor is discrete (Hosmer & Lemeshow, 2013; Schober & Vetter, 2021; Wiersema & Bowen, 2009). The ACC-P1, our response variable, is dichotomous. Therefore, data analysis and relationship estimation are done in the environment of a probabilistic option model. In this study, the response factor is the probability that a student is disposed to succeed, given certain NSC-level scores or performance. The other variables affecting performance, considering student dedication, were covered in the second phase.

Explanatory and Criterion Variables and Their Coding.

Source. Researchers’ conceptualization of the study variables.

We measured the dedication dimension (Table 7) by five items that refer to obtaining a sense of significance from one’s studies, feeling enthusiastic and proud about one’s learning activities, and feeling inspired and challenged by it. The students were to rate the five items on a scale of 1 to 7. The five items, as adapted from the work of Schaufeli and Bakker (2010), were:

I find the first-level lecturers’ assignments complete with meaning and purpose.

My lectures and learning tasks assigned by first-level lecturers inspire me.

I am proud of the degree work that I do at the University of Limpopo

To me, my studies leading to the BAcc degree are challenging

I can continue studying for long periods to understand the subject matter in the bachelor of accountancy degree.

Those who obtain high scores on dedication strongly identify with the workload embedded in the BAcc degree program because they encountered it as profound, exciting, and demanding. Besides, they usually feel enthusiastic and proud about their academic work. Those who score low do not identify with their work because they do not experience it as meaningful, inspiring, or challenging; moreover, they feel neither enthusiastic nor proud about it. Lack of dedication should lead to unsatisfactory academic achievement.

The researchers explored alternate specifications of probabilistic choice models: linear probability, multiple linear regression, probit, and logistic techniques. The use of multiple regression requires the use of student raw scores without coding. These three statistical choice models are available on most computer-based statistical packages and can analyze binary choice cases such as adopting or not adopting newly introduced technology or practices. Of the three probabilistic models, logistic and probit are favored over the linear probability technique when numerical modelling is based on a sample of data (Ayaya & Scott, 2015). Given the situation, the linear choice equation cannot be accurate when the standard errors of the coefficient approximation are unfaithfully represented.

The literature supports the dependability of the logistic regression results. Schober and Vetter (2021) have noted that the error term does not mirror a normal distribution curve shape. Therefore, conventional significance tests are unsuitable if alternative hypotheses have to be declined or allowed. Thus, Chen and Tsurumi (2010) have advised using probit and logistic regression techniques as suitable methods to ensure heteroscedasticity of the error term and restrict the predicted values of the response variables in the limits of 0 and 1. Williams and Jorgensen (2023) have determined that neither logistic nor probit modelling has merits over the other when selecting amongst binary choice models.

Shah et al. (2020) compare, based on shared data sets and assumptions, the least squares technique and logistic regression. The results of both analyses were very similar and produced identical decisions. The researchers’ decision to prefer logistic regression over probit was informed by convenience and corroborating findings of Shah et al. (2020) and Williams and Jorgensen (2023). However, logistic regression generated more precise estimates of response variable possibilities as measured by the mean of squared differences between the observed and anticipated probabilities, leading to the conclusion that logistic regression was performed well over the ordinary least squares approach to forecasting the likelihood of an attribute and should be the model of choice for use in instances where the dependent variable is coded in binary form.

Results and Discussion

Model Fitting Results from Logistic Regression

After obtaining logit model fitting results (Table 9), the researchers examined the issue concerning “how do we gauge if the model fits data well?” The IBM SPSS statistics version 29 software contains procedures and statistics researchers counted on to respond to the question. The procedures fall into two groups. One procedure assesses predictive power. For instance, R 2, model categorization findings, and goodness-of-fit criteria. The second procedure gauges whether the generated equation needs to be more sophisticated to acceptably portray connections in the assembled data. After showing the limitations of other approaches, Schober and Vetter (2021) argue for measures proposed by Das (2021). Therefore, the researchers created the goodness of fit tests and ran directed tests where the equation may have stopped to pass all of them.

Findings depicting the regression coefficient approximations and all-inclusive categorization attained by the logit equation are presented in Tables 9 to 11. The coefficient estimates in Table 9 summarize the impacts of each predictor variable in the analytical framework guiding the investigation. The Wald measure equates to the share of the regression parameter to the standard error squared. Where the p-value of the Wald measure is ≤.05, we inferred that the parameter estimates for predictor variables are helpful in the model. However, the NSC-level English and NSC-level accounting are insignificant, given a computed significance value of .761 and .205, respectively. The direction of the estimated relationship of the predictor variables in the logit model results with academic success was negative. This was inconsistent with the researchers’ a priori anticipation that language skills help learners command an understanding of the subject matter offered in the first-year courses. The two explanatory variables contribute less than 100% to the odds of academic success (ACC-P1 = 2).

The omnibus test results (Table 7) is a likelihood-ratio chi-square test of the model fitting results with five explanatory variables against the model with the intercept only. The p-value of less than 5% denotes that the model of five variables outperforms the null model. The p-values represent the probability of obtaining this chi-square statistic of 11.272 if the explanatory variables do not affect academic performance (ACC-P1). We compared the p-value to a critical value of .05 to determine whether the whole model was statistically significant. In this case, the model is quantitatively substantial because the computed p-value is less than .05.

The ordered logit coefficient in Table 8 shows that for a one-unit increase in the explanatory variable, the log-odds of academic success is expected to change by its respective regression coefficient in the ordered log-odds scale while holding other predictor variables constant in the model fitting results. The positive coefficients in Table 8 make success more likely in the presence of NSC-level APS, NSC-level mathematics and student dedication. The negative coefficients make academic success less likely. The coefficients for NSC mathematics and NSC APS scores are significant at .049 and .029, respectively. These significant predictors have a positive impact on academic success. A one-unit increase in the mathematics pass level contributes 127% to the odds of academic success. The NSC-level APS one-unit change increases academic performance by more than 1 unit increase. In other words, if we increase NSC-level APS, the odds of academic success (Y = 1) against academic failure (Y = 0) will increase by 232%, resulting in academic success (Y = 1) being more likely than it was before the increase. The significance of NSC-level APS is consistent with the fact that NSC-level APS is a composite of NSC scores in six subject areas, including NSC-level accounting, NSC-level mathematics and NSC-level English language.

Omnibus Tests of the Model Coefficient.

Source. Researchers’ derivation from data coding and analysis results.

Coefficients in Table 9 having p-values less than .05 are statistically significant. Explanatory variables with p-values higher than .05 are dedication score, NSC-level English, and NSC-level Accounting. We accept the null hypothesis for these explanatory variables that the impact is not significantly different from zero. Explanatory variables with p-values lower than .05 are NSC-level APS and NSC-level mathematics. We, therefore, rejected the null hypothesis and stated that the logistic coefficient is significantly different from zero.

Modelling Fitting Results with First Academic Performance.

Source. Researchers’ derivation from data coding and analysis results.

Consequently, the two explanatory have a considerable influence on academic performance. The odds of academic success are 127% in the case of NSC-level mathematics and 232% in the case of NSC-level APS. The CLT proponents’ position is held concerning NSC-mathematics and NSC-APS. The non-significance of NSC-level accounting is contrary to research results reported in the studies of Rowlands (1988), Ayaya (1997), and Uyar and Güngörmüş (2011), who found accounting knowledge of first-entering students to be a significant factor in academic success.

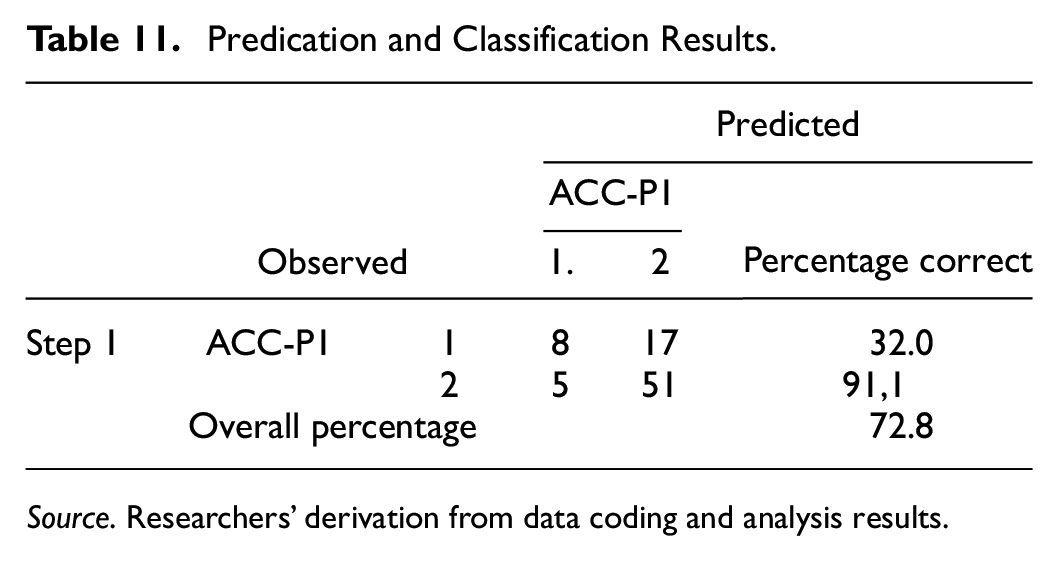

Tables 10 and 11 present the overall percentage of correct classification when the model has the intercept only (Table 10) and when explanatory variables are introduced. The overall percentage (Table 11) gives the overall percentage of cases correctly predicted by the full model fitting results of five explanatory variables. The rate increased from 69.1% for the model with the intercept only to 72.8% for the full model fitting results of five explanatory variables. Given the five explanatory variables, Table 11 gives the percentage of cases for which the academic performance (dependent variable) was correctly predicted.

The magnitude of the exponential coefficient (β) specifies a factor by which the likelihood is altered when the relevant predictor variable is moved by a single unit (Mood, 2010; Shah et al., 2020). The regression parameter constitutes the forecasted change in the predictor variable’s log-odds ratio of ACC-P1’s per unit change. The odds of a student achieving success is the ratio of the probability that a student would achieve academic success to the probability that a student would not have achieved academic success (ACC-P1 = 1), given the explanatory variable. Although insignificant, the regression coefficient of student dedication is positive. A change from 1 for student dedication would increase the odds by 30%.

The inclusive categorization results (73%) and the share of changes in the response variable projected by the fitted model (R 2) facilitate measuring how ably the generated model can predict the first level of academic success. The two statistics must lead us to respond to how sound the model suits the analyzed data. As a result, Table 12 depicts the Hosmer–Lemeshow (HL) test statistic for goodness-of-fit results, which aided in establishing whether the generated equation sufficiently depicts the underlying data. Although incorporated in most statistical packages, Nattino et al. (2020) have noted that the HL test statistic misses the reliability criterion whenever the sample size varies. Consequently, the inferences drawn based on the HL statistic had to be complemented by the inclusive grouping results (Tables 10 and 11). Mood (2010) contends that the HL test poses problems attributable to the number of categories generated from the experiment data.

Predication and Classification Results.

Source. Researchers’ derivation from data coding and analysis results.

Predication and Classification Results.

Source. Researchers’ derivation from data coding and analysis results.

Contingency Table for Hosmer and Lemeshow test.

Source. Researchers’ derivation from data coding and analysis results.

Results from Interviews with the Students

The researchers posed three questions to students who did not hold NSC-level accounting scores. This was a follow-up phase to confirm the irrelevance of NSC-level accounting for the academic success of BAcc degree enrollees and the insignificance of student dedication. One of the questions required the students to indicate if there was merit to include NSC-level accounting scores. One informant observed that:

NSC-level accounting should not be part of the university admission criteria. This is because first-year BAcc degree subjects are not equivalent to NSC subjects. The NSC-level accounting scores are already part of the NSC-level APS. A determined and persevering student who has not done NSC-level accounting can also master and be able to progress academically.

The second interview question sought to determine how students who did not hold grades in the NSC-level accounting department managed to cope. One informant pointed out that:

What worked for me during the academic year was the study packs I received from course facilitators and YouTube videos. I also researched topics I did not understand to understand what they were really about. Furthermore, asking questions in class and consulting after class also helped me.

Interview data showed the irrelevance of NSC-level accounting. Various resources, including those supplied by the course facilitators in the form of study packs and back-to-back assignments, could help students without NSC-level accounting catch up on the basics offered in the BAcc degree program. Classmates are also a resource first-year students can use to stay on course. The observations made by the informants confirm the conclusions drawn by Jansen et al. (2022). Findings maintain that students’ time obligations remained associated with that intended by their HEI, and they can be influenced by a combination of inside and outside considerations, as one informant observed:

Dedicated scholars can learn subjects offered to first-entering students in the BAcc degree programme. The subject matter comes as a language that requires more practice on the part of the students.

The observations were consistent with findings showing dedication as a positive contributor to academic success (Table 8). The significant NSC-level mathematics and NSC-level APS are compatible with Ayaya’s (1996) and Williams et al. (2022) findings. Numeracy levels and overall high school scores positively contribute to the likelihood of succeeding in training at a higher education institution.

Conclusions and Recommendations

This study focused on explaining first-year level performance (ACC-P1) to the exclusion of overall progress to subsequent years of study by the BAcc degree program students. Year II. The NSC-APS and NSC-Mathematics proved to be significant actors in the academic success of BAcc degree enrollees. The hypothesis regarding the significance of these variables was confirmed. The NSC-English language and NSC-level accounting failed to be significant. The two variables cannot be wished away from the admission criteria. We note that the contribution to the NSC-APS is already significant based on the field findings. Both NSC-level accounting and NSC-English language scores contribute to the calculated NSC-APS. Because the correct classification is under 75%, we conclude that there are variables that explain the academic success of the BAcc degree program. These other variables are not captured in the NSC-level APS or NSC-level mathematics.

From the results of the analysis and testing of hypotheses, we conclude that:

NSC-level accounting scores do not enhance the likelihood of a student succeeding in the first year of the BAcc degree program except through an enhanced NSC-APS.

NSC-level mathematics scores enhance a student’s likelihood of succeeding in the first year of the BAcc program.

NSC-level English language score does not enhance the likelihood of a student succeeding in the first year of the BAcc program except through its contribution to the NSC-level APS. If it does, then it does so through its contribution to improved NSC-level APS scores.

Student dedication to studies does not overshadow the importance of pre-admission enrolment requirements of the BAcc degree program. However, it plays a positive role in academic success.

The researchers have made initial attempts to contribute to revising the BAcc degree program admission criteria as a predictor of success in the first year. This study sought to provide answers to the following research questions:

What is the predictive value of the NSC-level mathematics results on subsequent ACC-P1?

To what extent do the NSC’s APS scores and NSC-level English impact ACC-P1?

How do the constructive learning and student engagement theories contribute to possibly revising the BAcc degree program admission criteria?

Given the answers to the above questions, the researchers recommend that:

The admission criteria for the BAcc degree program continue to emphasize APS score, NSC-mathematics, and NSC-English language.

The design of the offering during the first year of training in the BAcc degree programs should enlist enrollees’ dedication to working through the subject whose content is not directly linked to the NSC-level training.

More research should be done on student engagement and other factors impacting student performance in the program.

The due performance requirements in the university’s general rules are linked to student engagement when learning the program’s subject matter. The measurement of this due performance should go beyond class attendance to recognize the submission of formative assessments during the teaching period.

This study established a mix of NSC-level APS and NSC-level mathematics to influence academic success. The study considered student dedication but did not investigate student absorption, teaching and learning styles, or demographic factors. Studies reviewed have shown that maturity is a factor in academic success at the university level. The findings from the interviews with informants show that the architecture of CA2025, when factored in the first-year courses, makes the relationship between NSC-level accounting less direct with students’ academic performance in the BAcc degree program. Although insignificant in the logistic model fitting results, the student dedication variable showed a positive relationship confirmed in semi-structured interviews with the informants.

Given the final observation, the students are advised to manage aspects influencing their mathematical and language abilities at the university. The six subjects contributing to the NSC-level APS include English and Mathematics. These are aspects that guided NSC-level mathematics being significant. Students have already been exposed to business calculations (quantitative business methods) and the English language of business. These courses should continue at a much-enhanced level. We cannot rule out the role played by teaching and learning styles that enlist student dedication as an aspect of student engagement. The overall NSC-level APS should continue to be emphasized in the admission requirements. After entry, other factors guide students’ success. Some of these factors include using multiple sources of information to conquer the fear of the discipline.

Limitations of the Study and Direction for Future Research

Further research will be necessary to consider the overall progression to Year II and the completion of studies in 4 years instead of the maximum 7 years as response variables. Guiding students of accountancy to success has been a challenge. The pre-enrolment requirements that respect high school grades recognize the contribution of the CLT. Student engagement with the subject matter in the learning and development program has not been adequately integrated into applying the constructivist learning theory to matters of academic success in HEIs. The present study has initially attempted to integrate the two schools of thought. However, not all dimensions of student engagement were analyzed. The university’s general rules refer to due performance from students before they can write summative assessments. The measurement of this due performance goes beyond class attendance to recognize the submission of formative assessments during the teaching period. Therefore, the due performance requirements in the university’s general rules are linked to student engagement when learning the program’s subject matter. Therefore, conceptualizing student engagement in higher education is an area of future research. Kassab et al. (2023) have recognized both psychological and behavioral perspectives of student engagement. The performance requirements in the HEIs’ general rules are geared towards the behavioral perspective of student engagement. The present study did not address student engagement’s socio-cultural, absorption, and vigor dimensions and should be the focus of future studies.

Footnotes

Acknowledgements

I am grateful to the School of Accountancy and the students who gave us valuable data access.

Author Contributions

The authors’ substantive contribution(s) to the current journal article are shown below. Onesmus Ayaya: Conceptualization and design, Literature review, including theoretical framework, Data generation, Data analysis and interpretation, Manuscript writing, Critical revision of the manuscript, Overall responsibility. Michael Kgorompe Moswatsi: Literature review, including theoretical framework, Manuscript writing, Obtaining funding.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

Coded data used in the logistic results is available on request.