Abstract

The international division of labor has entered the era of the global value chain (GVC) due to the continuous influence of the scientific and technological revolution. At the same time, sustainable development has taken center stage in the evolution of international trade, and the export spell is an important indicator to measure the sustainable development of export trade. Based on the China customs data, the Chinese industrial enterprises database and the Chinese input-output table from 2000 to 2012, this paper uses the survival analysis method to estimate the enterprises’ export spells and calculate their positions in the GVC through upstreamness. It then investigates the impact of export spells on the position changes of the GVC enterprises. According to the paper, export enterprises near the bottom of the GVC are more vulnerable to extinction. And the duration of enterprises’ export spells has a U-shaped relationship with their positions in the GVC, which means that enterprises will continue to move downstream of the GVC as duration increases, but positions will shift upstream if duration reaches the inflection point. The mechanism test shows that the quality of export products is an important channel through which the duration of enterprises’ export spells influences their GVC positions.

Introduction

Over the last century, the world has experienced profound changes. The occurrence of global events such as Sino-American trade tensions and the COVID-19 epidemic has impeded the global industrial chain and supply chain circulation, increasing transaction costs. It also decreased transaction efficiency and impacted the international economic and trade order. Under these conditions, the difficulty for enterprises’ export spells is also increasing. At the appropriate time, the Chinese government proposed a new development pattern with domestic circulation as its mainstay, and both domestic and international circulations mutually reinforce each other. It is a more open domestic and international “dual circulation” as opposed to a closed domestic circulation. The Chinese government stated at the G20 Extraordinary Summit on COVID-19 that “all countries should strengthen international macroeconomic policy coordination and maintain the stability of the global industrial chain together.” Enterprises are the micro-foundation of the global industrial chain, which clarifies that in the era of the GVC, the response to changes in the international economic and trade pattern is to elevate the status of Chinese enterprises and establish a high-quality international circulation.

In accordance with the international division of labor model of the GVC, countries contribute with their own distinct advantages. Each enterprise imports intermediate inputs and is responsible for a part of the production process. It is no longer responsible for the whole production chain. To better participate in international circulation, it is necessary to seize a high position in the GVC in order to attain an irreplaceable role and avoid being squeezed out during the reconfiguration of the global economy. With the help of low labor costs and resource endowments, Chinese enterprises have achieved massive growth in foreign trade by integrating themselves into the GVC. In stark contrast to the rapid growth of Chinese goods trade, a significant portion of Chinese enterprises’ export trade is concentrated in labor-intensive industries or low-end manufacturing links with low value-added, resulting in an extended period of rising trade figures without corresponding trade gains.

In such an uncertain environment, the viability of enterprises is of utmost importance. As the microscopic main body for achieving Chinese trade expansion, enterprises are the driving force for ascending to the middle and upper levels of the GVC. The ability of enterprises’ export spells reflects their international competitiveness. Export spells can save enterprises a portion of costs, resulting in higher profits and the ability to create and maintain jobs (H. Chen et al., 2018). It will also make it easier to get into new markets, but the reality is that the duration of Chinese enterprises’ export spells is comparatively short (Y. Chen et al., 2014). Academics generally hold two distinct perspectives regarding the effect of export spells on enterprises’ participation in the GVC: one is “low-end locking,” while the other is high-quality and stable progress. On the one hand, enterprises that continue to export may acquire the requisite knowledge and skills through “learning by exporting” and thereby move up the GVC. On the other hand, the enterprises’ export spells may also be the result of the “comparative advantage trap,” which leads Chinese enterprises to fall into the “low-end locking” in the global division of labor. Therefore, in order to develop a high-quality international circulation, it is important to explore the capability of enterprises’ export spells based on the perspective of the GVC.

Compared to previous research, this paper makes the following contributions. First, it investigates the relationship between enterprises’ export spells and their positions in the GVC for the first time, and it investigates the mechanism by which export spells affect enterprises’ ascent up in the GVC. Second, most of the current research on the positions of the GVC focuses on the national and industrial levels, whereas this paper measures them from the enterprise level and investigates how to realize the ascent of enterprises’ positions in the GVC from a micro perspective. Third, most of the recent studies have not considered the impact of recent changes in the international economic and trade environment. For this reason, we analyze how Chinese enterprises can develop their export trade and improve their positions in the GVC by considering the current international economic and trade patterns such as counter-globalization, increasing uncertainty, and global industrial chain reconstruction. It offers novel strategies for Chinese enterprises to escape the “low-end locking” trap of the GVC and expand their trade in domestic and international circulations. The remainder of this paper is structured as follows, firstly, a review of the relevant literature on firms’ export spells and global value chains, and the research hypotheses of this paper based on this literature; secondly, the setting of the econometric model, the measurement of the indicators and the description of the data sources; Thirdly, the empirical research session, which contains the baseline regression, the robustness test, the treatment of the endogeneity problem, the test of heterogeneity, and the test of the mechanism; Finally, the countermeasure suggestions based on the research content of this paper.

Literature Review and Research Hypothesis

In the past two decades, the emergence of the GVC has altered the pattern of international trade. The active participation of Chinese enterprises in the GVC has been a primary driver of Chinese economic growth. Numerous studies have demonstrated that exporting enterprises are typically more productive and have stronger R&D innovation capabilities than non-exporting enterprises (Love & Roper, 2015). Enterprises incorporated into the GVC will increase exports, promote technological innovation, and boost productivity (Lyu et al., 2017; Xi & He, 2015; Zhang & Zheng, 2017) and realizing export upgrading (Ndubuisi & Owusu, 2021). One reason behind these benefits is that enterprises learn by exporting, which promotes innovation and improves productivity (Wagner, 2012). However, the “learning by exporting” effect may not manifest in the short-term exports of enterprises. Therefore, it is necessary to explore the enterprises’ export spells.

In terms of the literature related to firms’ survivability and export spells. For enterprises to increase their exports and strengthen their positions in the GVC, it is crucial that they possess the necessary skills. Similar to the level of enterprise productivity and technological innovation, the export viability of enterprises reflects the enterprises’ capacities and international competitiveness. In recent years, the issue of enterprises’ export spells has been a hot topic in international economics. Regarding the measurement of enterprises’ export spells, the majority of the literature uses the duration of export spells as a proxy variable for duration of enterprises’ exports (Y. Chen et al., 2012; Wei & Li, 2013; Zhou et al., 2013), Their results of measuring the firms’ export spells show the following characteristics: first, the average time of the duration of Chinese firms’ exports is relatively short, less than 2 years on average; second, the differences in the firms’ own capabilities will lead to significant differences in the duration of enterprises’ exports, and third, there are significant differences in the survival rates of exports of enterprises in different industries, regions, and the nature of ownership. Therefore, Chinese enterprises still need to further improve their own sustained export capability.

From the perspective of enterprises participating in the GVC, since different positions of enterprises in the GVC will result in different values (Kogut, 1985), many researchers have examined the dynamic changes of enterprises embedded in the GVC. Tang and Zhang (2018) calculated the positions of Chinese enterprises in the GVC from 2000 to 2008 and found slight rises. The processing trade, state-owned, and eastern enterprises all played a significant role in the ascent. In addition, Tang and Zhang stated that Chinese enterprises should continue to improve their positions in the GVC. Hu et al. (2018) observed whether enterprises move to industries with high-upstreamness and found that enterprises in high supply chain positions were more likely to shift to low-upstreamness industries. Ma et al. (2017) incorporated trade methods of processing with supplied materials and with imported materials into the theoretical model to examine the relationship between financing constraints and the climbing of the GVC. They demonstrated that enterprises with small financing constraints are more likely to move up in the GVC. Therefore, how to enhance the positions of enterprises embedded in the GVC and increase the added value of enterprise trade is a pressing issue that Chinese export enterprises must address immediately.

To explore how a firm’s sustained exporting affects the firm’s GVC position, it is necessary to understand what are the influencing factors that affect the firm’s sustained exporting and the firm’s GVC position. Macro factors including the minimum wage, the cultural distance between the country of origin and the country of destination, the geographical distance, the exchange rate, and others influence the enterprises’ export spells (Du & Wang, 2015; Liu & Qi, 2019; Pan, 2018; Yue, 2023; R. Zhao et al., 2016). At the micro-enterprise level, factors like initial trade volume, number of export destinations, enterprise scale, enterprise productivity, exported product types, innovation level and time since establishment all have substantial effects on the duration of export spells (Y. Chen et al., 2012; Reddy & Sasidharan, 2023). On the one hand, export spells can save a great deal of costs for exporting enterprises. Albornoz et al. (2016) noted that the probability of survival for enterprises entering the export market would increase with the ratio of sunk costs and fixed costs. It also increased with enterprises’ export experience because the export experience would reduce enterprises’ fixed costs and sunk costs, and the impact on the fixed costs is greater than the impact on the sunk costs. On the other hand, enterprises can improve their productivity and technological innovation through technological spillovers and the “learning by exporting” effect (C. Zhao & Wen, 2016). Martuscelli and Varela (2018) argued that production efficiency was the real reason for increasing the survival rate of enterprises. Export product diversification and export destination concentration could increase the survival rate, indicating that the role of information networks significantly impacted the export survival rate.

Product quality has garnered growing scholarly attention in recent years as one of the many aspects that determine enterprises’ export performance and embedded positions in the GVC. Enterprises with greater productivity have a larger market share, are more inclined to export, and generate products of a higher quality. Hallak and Sivadasan (2009) note that productivity is not the only determinant of enterprises’ export participation when there is a quality threshold for exported products; high productivity enterprises whose product quality falls below the quality threshold will not be able to enter export markets successfully. However, the relevance of export product quality in enterprises’ export spells and embedded positions in the GVC remain obscure.

Furthermore, the “productivity paradox” of Chinese export enterprises necessitates special consideration. An important reason for local Chinese enterprises to participate in the GVC is that a large number of processing trade enterprises engage in “export-induced import” (Zhang & Zheng, 2017), which indicates that Chinese enterprises have the “capture” effect of embedded in the low end of the GVC. Therefore, the dynamic change of Chinese enterprises’ embedded positions in the GVC is likely to show a “U” or “inverted U shape.” Numerous studies have proved a nonlinear relationship between enterprises’ behaviors and their embedded positions in the GVC. For example, Lyu et al. (2017) found that enterprises embedded in the GVC can improve their productivity, and there is an “inverted U-shaped” relationship between enterprises’ productivity and embedded positions in the GVC. Y. Wang et al. (2014) found that Chinese enterprises embedded in the GVC can further promote technological progress. But there is a dampening effect, which means that the positions of enterprises embedded in the GVC also have an “inverted U-shaped” trend with technological progress. The research of H. Wang et al. (2015) also pointed out that the positions of Chinese enterprises embedded in the GVC generally show an “inverted U-shaped” trend. All these studies reveal that the performance of enterprises embedded in the GVC varies in the short and long term.

Based on the above discussion, this paper proposes the basic hypothesis: firms’ continuous exporting will improve their GVC position. In addition, the quality of exported products may serve as an important mechanism for firms’ sustained exporting to affect their GVC position.

Model Setting, Variable Selection, and Data Processing

Model Setting

The following model is constructed to examine the relationship between the duration of export spells and the positions of enterprises in the GVC:

Where

Variable Measurements

GVC Embedded Position

The object of this paper is the enterprise-level GVC embedded position. We measure the distance between industry and final demand based on the practice of Fally (2012) and Antràs et al. (2012) by employing the upstreamness value. The upstreamness value indicates the position of a specific industry in the GVC, and a higher upstreamness means that the industry has a greater distance from the final product consumption.

The industry upstreamness index can be calculated using the standard input-output table. This metric is the weighted average of the quantities of industry i at each stage from the input to final demand. Consequently, the greater this index, the more upstream an industry is in the production chain. Following this method, we construct an upstreamness index for the industry using the Chinese input-output table. Then we map this metric to the product data imported and exported by Chinese enterprises to characterize each enterprise’s position in the GVC, that is, the upstreamness of enterprises. Following is the equation for calculating the industry upstreamness value

where

We refer to the method of Chor et al. (2014) and use industry upstreamness values to infer the embedded position of each Chinese enterprise in the GVC. Specifically, referring to the method of Lyu et al. (2020) and combining it with Chinese customs data, we match HS product codes with Chinese input-output table industry categories in order to calculate the product upstreamness. Then the export value (

where

Duration of Export Spells

In this paper, the duration of export spells is employed to illustrate the capacity of enterprises’ export spells. According to Y. Chen et al. (2012), Békés and Muraközy (2012), and Kostevc and Zajc (2020), the duration of export spells is the time from entering a destination country to exiting that country (without an interval), that is, the number of years that an enterprise f exported to the destination j. There are two important considerations in data processing: First, there is the issue of data censorship. Since the time range for data selection is 2000 to 2012, it is hard to determine the export status of enterprises beyond the observation period. We cannot identify the actual start time of exporting enterprise-destination in 2000 due to a problem with data left censoring. Similarly, because of the data right censoring, we are unable to identify the end time of enterprise-destination in 2012.

Referring to the practice of Y. Chen et al. (2012), we delete the enterprise-destination that had export behaviors in 2000, so the longest duration is 12 years. And the survival analysis method for defining outcome variables can address the problem of data right censoring. Second, there is an issue of multiple durations, in which enterprises may export to a particular destination country for a period of time, then exit and later re-enter it. According to Besedeš and Prusa (2006), the presence of multiple durations has no impact on the distributional characteristics of the duration of export spells. Moreover, multiple durations can be considered as independent of one another. For example, during the period 2000 to 2012, firm A exported in 2000, 2001, 2002, 2006, 2007, 2008, and 2009, then it will have two export spells of 3 and 4 years respectively. To better depict the “cumulative effect” of the duration, it is expressed by the actual duration of export spells of the enterprise-destination country by referring to the practice of X. Chen and Shen (2015). There may be a nonlinear relationship between the duration of enterprises’ export spells and enterprises’ upstreamness; therefore, the squared term of actual duration of export spells of the enterprise-destination is incorporated in the model.

Measurement of Control Variables

This paper chooses control variables at the enterprise, industry, and macroeconomic levels. At the enterprise level, the control variables consist of total factor productivity, enterprise capital intensity, enterprise scale, and enterprise age. The measurement of total factor productivity adheres to the methodology of Lu and Lian (2012), which use the GMM method to estimate the total factor productivity growth rate of industrial enterprises in China from 2000 to 2012. The enterprise capital intensity is represented by the logarithm of net value of fixed assets, whereas the enterprise scale is represented by the logarithm of the number of employees. The age of an enterprise is calculated by the difference between the current year plus one and the year of opening, and then taking the logarithm. At the industry level, the Herfindahl index is chosen as a proxy variable for industry aggregation, with the following formula:

Data Processing and Descriptive Statistics

Data Sources and Processing

To test the hypotheses of this paper, a panel dataset of Chinese industrial firms from 2000 to 2012 is constructed. The data sources used in this paper are mainly from: the Chinese Industrial Enterprise Database, Chinese Customs Database, and the Chinese Input-Output Table, which are all from 2000 to 2012. Except for GDP per capita statistics from the China Statistical Yearbook, all other control variable data is calculated using the China Industrial Enterprise Database. This paper deletes samples with zero values for gross industrial production value, industrial added value, fixed assets, employees, and other data, following the methodology of Nie et al. (2012).

First, the upstreamness of each industry is calculated through the input-output table. Since the research object is the enterprises upstreamness and the industry classification in the input-output table corresponds to the HS code, we may connect the input-output table and the customs data according to this correspondence. And then we can calculate the upstreamness at the product level based on the proportion of each enterprise’s product exports to the total exports of the industry in which the enterprise is located. Lastly, enterprises upstreamness is determined by summing. Secondly, referring to the method described by Upward et al. (2013), we integrate the Chinese customs data and the industrial enterprise data based on the enterprise name. The successfully integrated samples include the export data at the enterprise level. When there is an export amount from the enterprise to the destination country, it is marked as the existence of export behavior. Then, we compute the duration of export spells of the enterprise-destination country, which is utilized to express the export spells capacity. We delete the enterprise-destination countries exported in 2000 to address the left-censored problem and set the outcome variable to solve the right-censored problem. Multiple durations that are independent of one another do not affect the distribution characteristics of the duration of export spells. In addition, keeping data for multiple durations can yield richer sample information and reflect the dynamic changes of enterprises in the GVC.

Duration of Export Spells Estimation

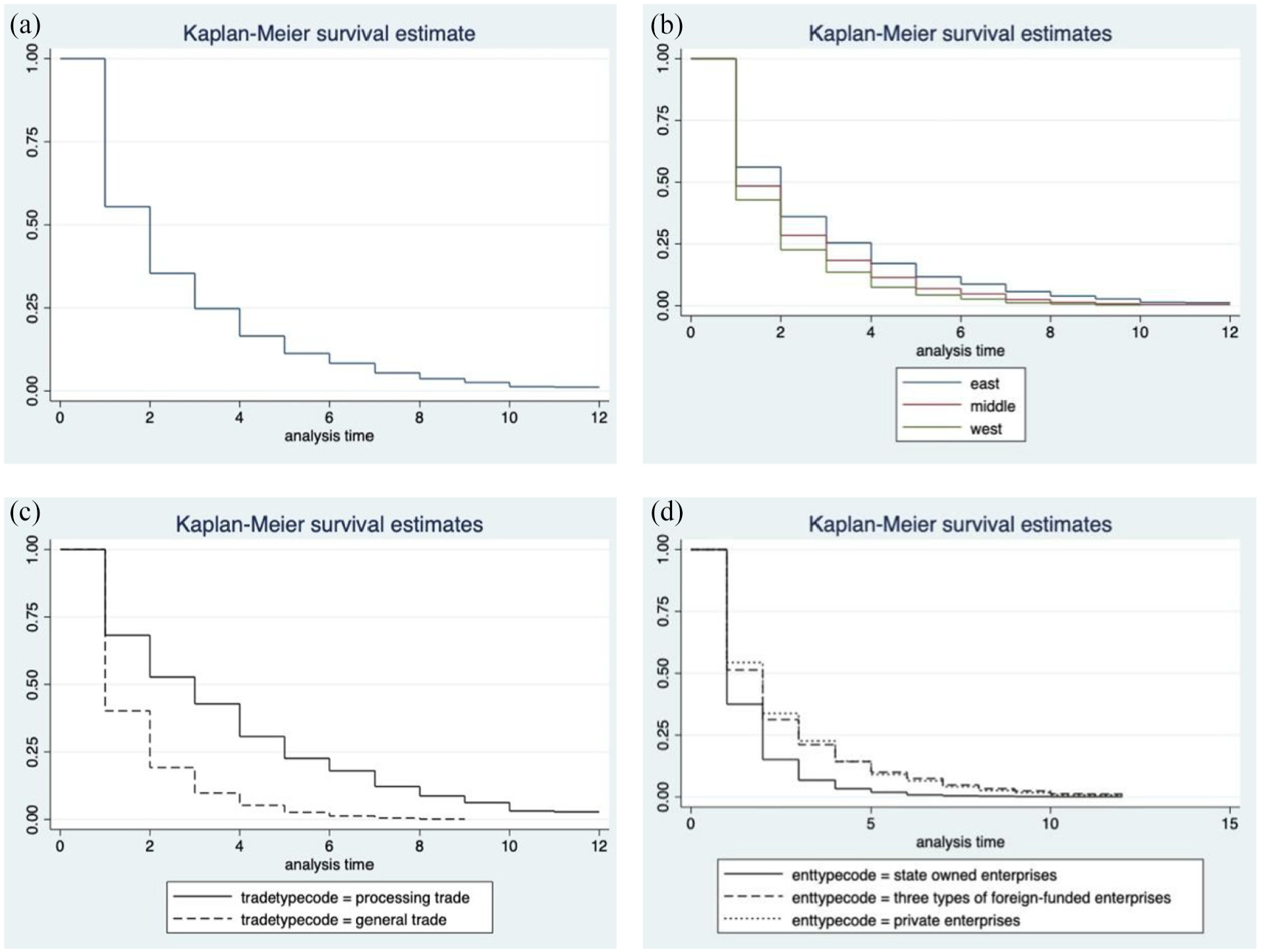

Based on the above approaches and sorted data, this paper measures the duration of enterprise export spells from several perspectives. As shown in Figure 1a, the duration of export spells of the full sample is determined. With an average export length of 1.84 years, the Chinese export survival curve demonstrates a decreasing tendency. In the initial year, there is a significant export risk for enterprises, but the survival rate gradually climbs and stabilizes as time passes.

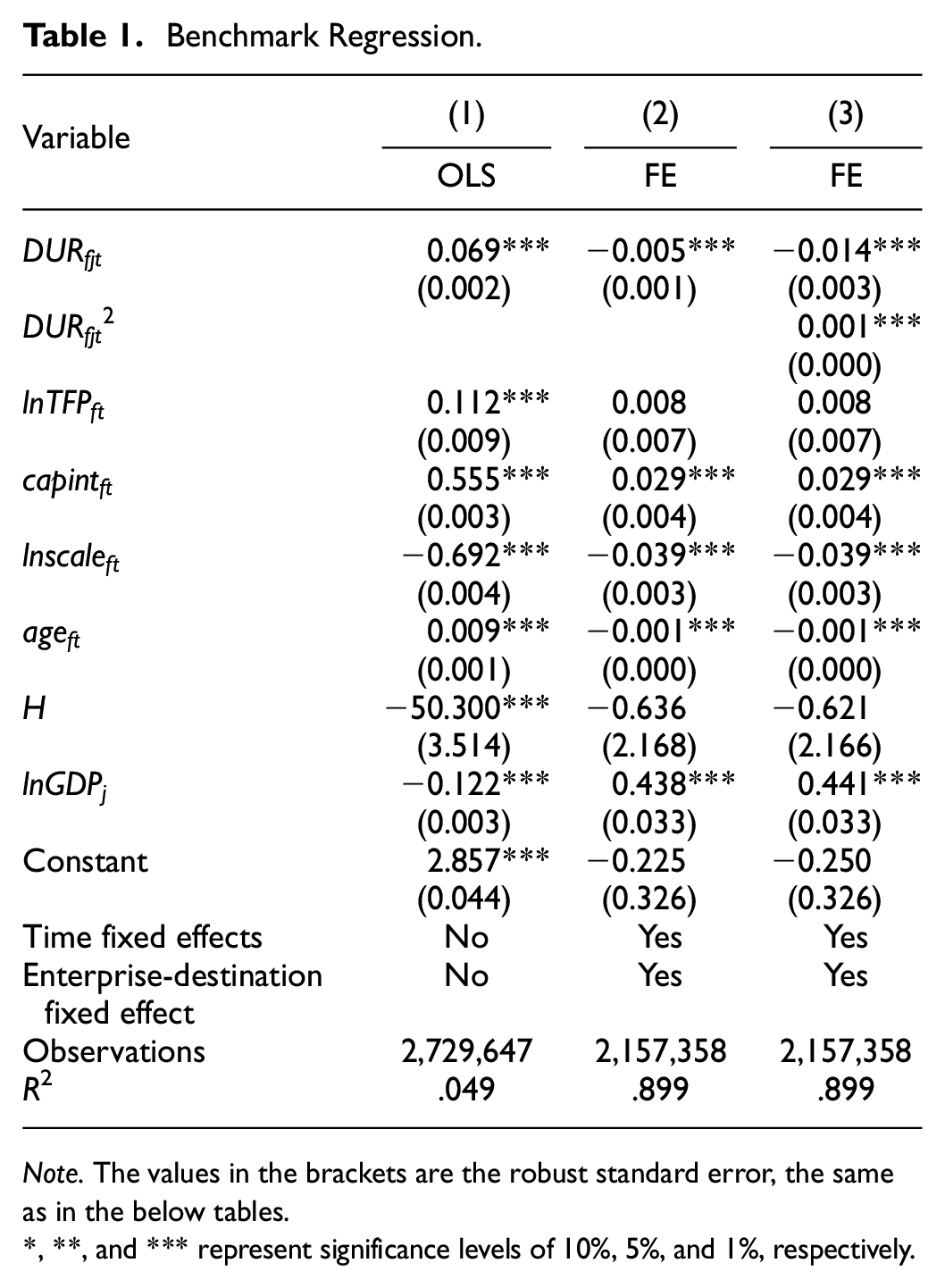

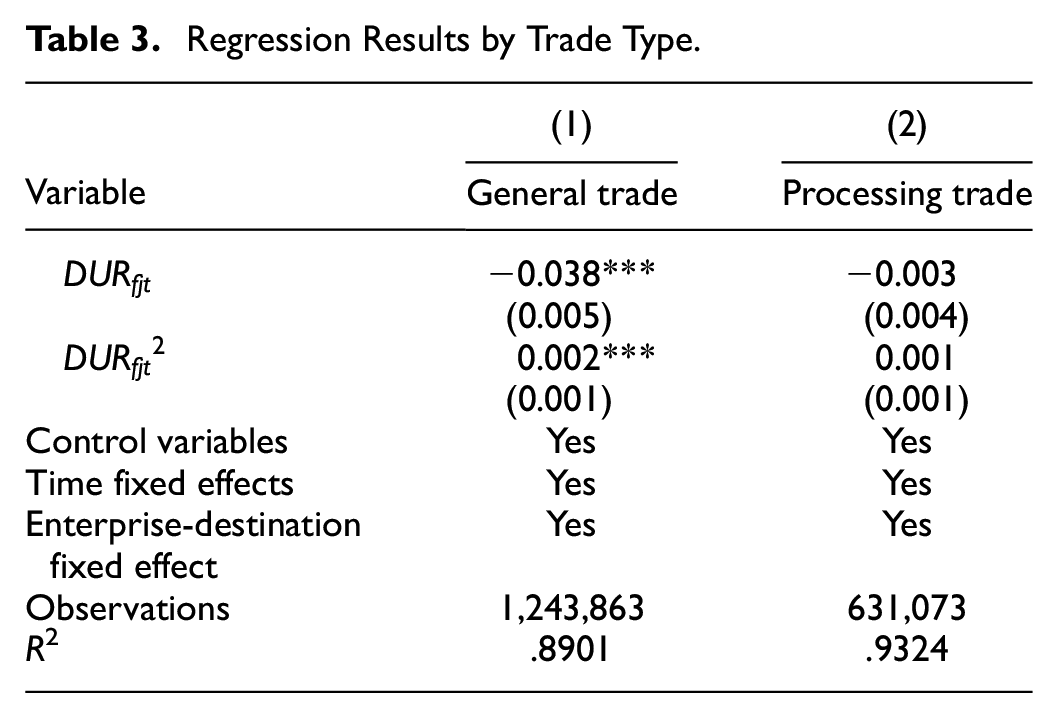

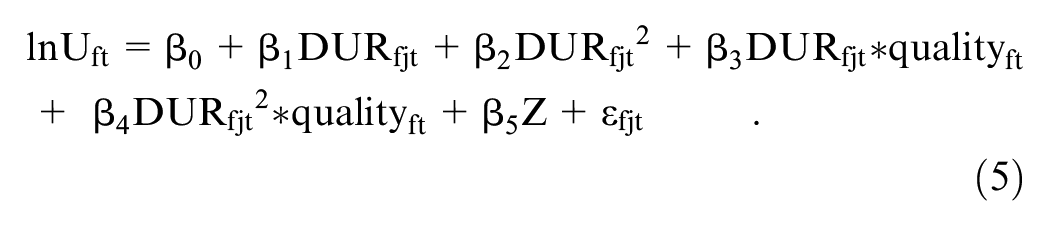

Export survival curve of Chinese enterprises: (a) full sample, (b) by region, (c) by trade type, and (d) by ownership.

To determine whether there are disparities in the export survival rates among different enterprise types, we calculated the duration of enterprises’ export spells in different regions, trade types, and ownership structures. The outcomes are depicted in Figure 1b to d.

China’s exports are mainly concentrated in the eastern region, and a calculation reveals obvious regional disparities in the duration of export spells for Chinese enterprises. The average export survival time of enterprises in the eastern region is 1.85, which is greater than the central and western regions’ 1.71 and 1.73, respectively. As shown in Figure 1b, the export survival curve of eastern enterprises is significantly higher than those of the central and western regions. In terms of export performance, the eastern region has always outperformed other regions due to the influence of factors such as economic development level and geographical location. In addition, as the forefront of China’s reform and opening-up, the eastern region has relatively complete relevant policies, infrastructure construction, and the ability to develop external markets. As a result of these benefits, the eastern enterprises typically have a higher export survival rate.

As depicted in Figure 1c, there is no statistically significant difference between the duration of export spells of enterprises engaged in different trade types. The export survival curve of processing trade enterprises is slightly higher than that of general trade enterprises due to the lower financial burden and export risk. This also demonstrates that embedded in the GVC via processing trade effectively lengthens the export duration of enterprises’ export spells.

As shown in Figure 1d, there are significant differences in the duration of export spells between enterprises with different ownership structures. The probability of export survival is significantly greater for three types of foreign-funded enterprises (i.e., Sino-foreign joint ventures, cooperative enterprises, and exclusively foreign-owned enterprises) and private enterprises than for state-owned enterprises. Among them, the export survival rate of three types of foreign funded enterprises is marginally lower than that of private enterprises. This may be due to the fact that China began to relax foreign capital controls in 2001 and abolished the requirement that foreign-funded enterprises must export the majority of their output. However, three types of foreign-funded enterprises have more connections with foreign markets due to the presence of foreign capital, so their export survival rate is higher than that of state-owned companies.

According to the results of the preceding analysis, the duration of export spells of the majority of Chinese enterprises is not particularly long. In the context of domestic and international dual circulations and the reconstruction of the GVC, the obstruction of the industrial chain circulation will result in a further decrease in the duration of enterprises’ export spells. For enterprises that originally planned to export, existing from the export market means that a large amount of costs cannot be recovered.

Measurement Results and Analysis

Benchmark Regression Results

On the basis of the model developed in this paper, regressions were performed on the full sample, and the results are presented in Table 1: column (1) displays the mixed regression results. The coefficient of the explanatory variable duration of enterprise export spells is significantly positive, but the results of the mixed regression are inaccurate due to individual effects. Column (2) contains the relevant control variables (total factor productivity, enterprise capital intensity, enterprise scale, enterprise age, Herfindahl index, and GDP per capita in the destination country), the year fixed effects, enterprise fixed effects, and enterprise-destination fixed effects. The results show that the coefficient of the duration of enterprise export spells is significantly negative, indicating that an increase in the duration of export spells of an enterprise is associated with a decline in its upstreamness. In order to confirm the possibility of a nonlinear relationship between the duration of export spells and upstreamness, the squared term of the variable

Benchmark Regression.

Note. The values in the brackets are the robust standard error, the same as in the below tables.

, **, and *** represent significance levels of 10%, 5%, and 1%, respectively.

By analyzing the relevant control variables, we can also conclude, in line with the findings of Ju and Yu (2015), that export enterprises with high upstreamness also have high capital intensity. Enterprise scale and upstreamness are negatively correlated, because we use the number of employees to represent enterprise scale, and labor-intensive industries are predominantly concentrated in downstream positions in the GVC. Enterprise age has a significant negative effect on the upstreamness, but the value is close to zero.

Heterogeneity Test

Having calculated the duration of enterprises’ export spells by region, trade type, and ownership, it has been determined that the duration of export spells varies across enterprise types. On this basis, we continue to investigate whether the duration of export spells of various enterprise types has different effects on their positions in the GVC. Consequently, on the basis of model (1), we made estimations according to enterprises’ region, trade type, and ownership.

Due to China’s vast territory and uneven regional development, enterprises in the east, middle, and west have varying durations of export spells and export upstreamness. As the frontier of opening-up, the eastern region is influenced by its geographical advantage and historical development level, has more frequent import and export activities, and will have greater influence in the process of participating the GVC. Therefore, we divided samples into three subsamples based on their regional locations: eastern, central, and western. Table 2 reveals that an increase in the duration of enterprises’ export spells in the western region will increase their upstreamness, whereas the results in the eastern and central regions remain unchanged, with the upstreamness of enterprises in the central region being more significantly impacted by the duration of export spells. Export spells cause enterprises in different geographic regions to diverge to both ends of the GVC, indicating that Chinese enterprises do not move upstream or downstream in a single approach within the context of embedded GVC. Faced with the reconstruction of international economics and trade, China can achieve greater economic domestic circulation by connecting upstream and downstream, but only if it continues to opening-up and achieves high-quality international circulation.

Regression Results by Region.

On the basis of the benchmark regression, we continue to discuss the extent to which the export upstreamness of different enterprise trade types is influenced by the duration of export spells. The results are presented in Table 3, which reveals a negative impact on the export survival of enterprises of various trade types. The impact on enterprises engaged in general trade is more evident, whereas the impact on enterprises engaged in processing trade is close to 0, which is statistically unsignificant.

Regression Results by Trade Type.

The results are shown in Table 4. The effects of the duration of export spells on the export upstreamness are essentially identical for all three enterprise ownership types. Except for state-owned enterprises, all exhibit a negative correlation at the 1% significance level. This suggests that the bias caused by “internal differences” in the sample has less of an effect on the overall regression and that the results are robust. Probably due to the unique nature of state-owned enterprises, export spells are not a significant method for them to move up the GVC. There is a large proportion of three types of foreign-funded enterprises that belong to the important sectors of multinational corporations in order to achieve global vertical specialization of labor. And since the majority of sectors where foreign investors entered China in the early days are processing and assembly sectors, export spells may cause these enterprises to enter a “low-end locking” dilemma, resulting in a greater absolute value for the duration of export spells coefficient in column (2).

Regression Results by Ownership.

Robustness Test

Endogeneity Problem

In this paper, what we want to investigate is the impact of enterprises’ export spells on their export upstreamness. Since both the duration of export spells and export upstreamness are enterprise-level variables, we employ the two-stage least squares method (2SLS) to address the mutual causality endogeneity issue. Referring to Mao and Xu’s (2018) practices, we apply the first order difference to the basic model’s key explanatory variable, that is, we select the duration of enterprises’ export spells lagged by one period as the instrumental variable for regression. As shown in columns (1) and (2) of Table 6, the coefficients are significantly greater and remain significant after the endogeneity problem has been resolved.

Index Replacement

The key explanatory variable used in this study is the duration of export spells of the enterprise-destination country. Since the total number of years of actual exports is greater than the number of years of continual export during the period 2000 to 2012, we use the cumulative duration of export spells of the enterprise-destination country in the robustness test. The column of Table 6 (3) displays the results, which indicate that the sign and significance level of the regression coefficient of the key explanatory variable do not differ fundamentally from the benchmark regression. It further verifies the robustness of the results.

Excluding Trade Intermediaries

Due to the fact that import and export intermediaries are primarily engaged in import and export trade agencies, the presence of trade intermediary enterprises may have some influence on the research outcomes. Examining the positions of trade intermediary enterprises in the GVC is meaningless because they do not have production behaviors. Based on this consideration, we adopt the method of Ahn et al. (2011) for dealing with trade intermediary enterprises. In the customs trade database, enterprises whose names contain “import and export,”“economic and trade,”“trade,”“technology and trade,”“foreign economic,” and other words are classified as trade intermediary enterprises to be tested and excluded. The results are displayed in column (4) of Table 5, and the coefficient and sign of the key explanatory variable do not change fundamentally and remain significant, indicating that the conclusions are robust.

Robustness Test Results,

Source. Authors.

Adding Control Variables

To continue exporting, enterprises must ensure sufficient capital. The greater the financing constraints, the greater the enterprises’ financial pressure, which can be detrimental to export spells and affects the enterprises’ positions in the GVC. For robustness, we include financing constraints in the benchmark regression model. The ratio of interest expenses to fixed assets is used to calculate enterprises’ financing constraints (

Discussion of the Non-Linear Relationship

In the preceding discussion, we determined that there is a nonlinear relationship between the duration of export spells and the upstreamness. When the duration reaches the inflection point, it will demonstrate that enterprises move upstream in the GVC. The inflection point is reached when the duration of export spells reaches 7 years, according to the coefficient of the benchmark regression in Table 1. To test this hypothesis, we omit enterprise-destination samples with export spell durations less than 7 years, leaving a sample of 38,687 enterprise-destinations for econometric analysis based on model (1). Table 6 displays the results, which support the positive stimulus relationship between the duration of export spells and enterprise upstreamness at 5% significance level, indicating that the enterprise-destination group only experiences an increase in global value volume when the duration of export spells exceeds 7 years. In light of the current restructuring of the international economic and trade structure, enterprises should focus more on export spells. Only when enterprises surpass the export threshold will they be motivated to seize new opportunities to ascend upstream in the GVC.

Duration of Export Spells ≥7 Years Enterprise—Destination.

Source. Authors.

Mechanism Analysis

The previous benchmark regression demonstrates that the relationship between the duration of enterprises’ export spells and upstreamness is “U-shaped.” In this paper, we will use the mediation model to further investigate the influence mechanism from the perspective of the enterprise export product quality. Using the method of X. Chen et al. (2019), the quality of the enterprise’s export products is used as the explained variable to determine whether the quality of the enterprise’s export products has a “U-shaped” relationship with the duration of enterprises’ export spells. Then, the interaction term of product quality and the duration of export spells, and the interaction term of product quality and the square of the duration of export spells, are introduced into the basic model. The equations for regression are constructed as follows:

where the subscripts f, j, and t denote the enterprise, export destination country, and time, respectively.

As shown in Table 7, column (1) is calculated according to equation (4). The coefficients of the duration of export spells and its squared term are negative and positive, respectively, indicating that the impact of the duration of export spells on the quality of export products is “U-shaped,” which decreases first and then increases later, reflecting the relationship between the duration of export spells and upstreamness of enterprises. Assuming that the duration of export spells inhibits enterprises from moving upstream in the GVC through upgrading export product quality, the coefficient of the interaction term between the duration of export spells and export product quality should be positive. According to column (2) of Table 7, the coefficient of the interaction term between the duration of export spells and export product quality is significantly positive, indicating that higher export product quality can mitigate the negative effect of the duration of export spells on upstreamness, that is, the above hypothesis is true. Column (3) displays the estimation results after adding the export product quality based on column (1). The coefficient is significantly positive, indicating that export product quality is a factor that drives the enterprises to move upstream in the GVC. The absolute value of the duration of export spells coefficient is 0.018, which is less than 0.023 in Table 3, indicating that the quality of export products has mitigated a portion of the detrimental effect of export spells on the upstreamness of enterprises. Comparing columns (2) and (3) of Table 7, the absolute value of the coefficient of the duration of enterprises’ export spells decreases after the addition of enterprise export product quality, indicating the existence of the mediation effect, that is, the increase in the duration of enterprises’ export spells inhibits the quality of enterprise export products, thereby influencing the upstreamness movement of enterprises in the GVC.

Mechanism Test.

Source. Authors.

Based on the preceding discussion, this paper argues that there may be an “export low-end locking” inhibitory mechanism in the impact of the duration of export spells on the positional change of enterprises embedded in the GVC. An increase in the duration of export spells can increase the export experience of enterprises in the destination country, but this experience gained from export spells can lead to “active inertia” and cause enterprises to fall into the “comparative advantage trap.” Under the GVC environment, developing countries are more likely to be confined to the lower end of the GVC for an extended period of time; consequently, in the context of global economic and trade environment fluctuations, these enterprises are more likely to lose their competitiveness and be squeezed out of the GVC. Developed countries hold the key technologies and core resources, while China participates in the GVC primarily due to its cheap labor and resource advantages. Long-term, as the duration of export spells of Chinese enterprises increases, they are more likely to use existing production resources to continue to maintain their competitive export advantage while ignoring enterprises’ transformation and upgrading. The increase in the duration of enterprises’ export spells exposes them more frequently to verticalized professional division of labor. Developed countries use core technology to suppress, and it is difficult for Chinese enterprises to create knowledge and enhance competitiveness. Consequently, Chinese enterprises lose their core competitiveness and are restricted to the low end of value creation.

On the other hand, the duration of export spells may facilitate the “learning by exporting” effect. Through export spells, enterprises can obtain specific data, consumer preferences, and distribution channels in particular export markets. Compared with the initial phase of entering the target market, the longer the export continues, the more fixed costs can be shared, and the profits of export enterprises will also increase with the export spells (X. Chen & Liu, 2015). Therefore, enterprises face fewer financing constraints, and those with fewer financing restrictions are located at the top of the GVC. Therefore, an increase in the duration of enterprises’ export spells results in the accumulation of profits and the relaxation of financing constraints, which will increase the enterprise’s investment in R&D and be advantageous for their ascent of the GVC.

Conclusion and Suggestions for Countermeasures

From the perspective of the GVC, this paper examines the effect of enterprises’ export spells on their participation in the international circulation, using enterprise-destination as the basic research object and survival analysis to describe the duration of export spells and export risks of Chinese enterprises. Different enterprise characteristics are analyzed separately, which reveals that there are substantial differences in the survival time of enterprises with different ownership and in different regions. Using the upstreamness of enterprises as an indicator of their positions in the GVC, it is evident that the duration of enterprises’ export spells and the upstreamness of enterprises exhibit a “U-shaped” relationship that first decreases and then rises. In the preceding discussion, it is determined that when the duration of export spells exceeds 6 years, it will cross the inflection point of the “U-shape”; that is, as the duration of export spells increases to a certain degree, it will be advantageous for enterprises to move up the GVC, whereas a shorter duration will only cause enterprises to slide down the GVC. Through the intermediary effect test, this paper determined that the quality of enterprise export products is a significant channel for enterprises to influence their positions in the GVC via export spells.

The international economic and trade pattern are undergoing adjustment and reconstruction, and the GVC faces the possibility of rupture. How can Chinese enterprises establish strategic objectives to attain a high-quality “dual circulation” pattern? In light of this paper’s findings, we propose the following recommendations:

First, export spells are conducive to enterprises’ export cost reduction. In the context of trade liberalization, enterprises can sign multiple short-term export contracts to find the optimal export solution; however, the cost advantage brought about by export spells is not readily apparent. In the context of the reconstruction of the global industrial chain, countries pay more attention to domestic demand and are more inclined to promote trade development through regional economic integration measures. Stable and lasting trade relationships can save more costs in such a situation. As previously stated, there is a “U-shaped” relationship between the duration of enterprises’ export spells and their upstreamness. After calculations, it has been determined that the average duration of export spells of Chinese enterprises is less than 2 years. Seventy-five percent of enterprises’ duration of export spells is less than 3 years, which is still a brief period. It has not yet reached the “inverted U” inflection point (6 years). To move up the GVC, enterprises should continue to extend their duration of export spells and gain experience in specific export markets through the “learning by exporting” effect.

Second, enterprises with longer durations of export spells have already had more stable positions in the GVC, at which time they should focus on production efficiency and R&D investment. In the context of international economic and trade pattern restructuring, the first to be squeezed out of the GVC and industrial chain are enterprises in the low end with low value-added, which lack international competitiveness and are highly substitutable. Excessive duration of export spells may trap enterprises downstream in the GVC. In general, the innovation value and profitability of downstream products of the GVC are lower. Therefore, enterprises with longer duration of export spells should shift their focus to R&D and improve enterprise productivity to transform and upgrade to higher positions in the GVC, rather than simply increasing export scale and the duration of export spells.

Third, against the backdrop of increased global unpredictability, the domestic and international dual circulations development pattern has presented Chinese enterprises with enormous challenges and opportunities. To effectively meet the current challenges, we must insist on the opening-up policy, maintain the stability of the global supply chain, and bring new momentum to the global economy’s stability. When enterprises pursue a transformation and an upgrade in the GVC, they should simultaneously devote themselves to extending the duration of export spells and enhancing the quality of export products.

It should be noted that this paper still has certain limitations and shortcomings: first, the available data cannot be up-to-date because of the inconsistent time span and inconsistent statistical caliber of the many databases; second, the object of the study is the industrial firms in China, which fails to observe the changes of the firms in other industries; and third, although this paper has tried to carry out as much as possible to conduct the robustness test and the test of heterogeneity, there may be a certain amount of research error due to the limitations of the methodology of the empirical research. Therefore, the updating of research data, the experimentation of research methods and the expansion of more research objects are the main directions for future research.

Footnotes

Acknowledgements

This research was funded by the national social science fund of China, Grant Number 19CJY019.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study was supported by The National Social Science Fund of China “Study on the Mechanism Path and Countermeasures of Labor Market Flexibility to Promote Common Wealth in China (23BJL067).

Data Availability Statement

The datasets are available from the corresponding author on reasonable request.